intelligent buildings and the bid specification process...

TRANSCRIPT

Intelligent Buildings and the Bid Specification Process 2012

Intelligent Buildings and the Bid Specification Process 2012 Landmark Research Study

Executive Summary

Continental Automated Buildings Association (CABA)

1.1 Detailed Table of Contents, Background, Objectives and Executive Summary – Study PowerPoint Presentation 1.2 Detailed Executive Summary and Table of Contents – Final Written Report

www.CABA.org

Prepared by:

1.1

Intelligent Buildings and the Bid-Specification Process

Table of Contents

2

Background, Project Objectives and Methodology 4

Key Takeaways 7 State of the Industry 8 Major Participant Groups 9 Bid-Specification Methods 10 Challenges with the Present Methods 11 Process Optimization 12 Project Cases 13 Conclusions 14

Contact Information 15

Intelligent Buildings and the Bid-Specification Process

Table of Contents (continued)

3

Presentation - Table of Contents: Key Findings Key Takeaways

State of the Industry Major Participant Groups Present Delivery Process and Value Chain Procurement Process by Technology: Key Challenges Procurement Process by Market Type: Key Challenges Bid-Specification Methods Challenges with Present Methods Areas to be Addressed Anticipated Demand and Growth Areas Opportunity and Success Factors Process Optimization Changes to Project Approach Emerging Value Chain Project Cases Conclusions Contact Information

Intelligent Buildings and the Bid-Specification Process

Background

4

The Continental Automated Buildings Association (CABA) is an industry association dedicated to the advancement of intelligent homes and intelligent buildings technologies. CABA is an international association, with over 300 major private and public technology companies committed to research and development within the intelligent buildings and connected home sector. Association members are involved in the design, manufacture, installation and retailing of products for home and building automation. CABA is a leader in initiating and developing cross-industry collaborative research, under the CABA Research Program. In 2012, CABA’s Intelligent & Integrated Buildings Council (IIBC) commissioned the “Intelligent Buildings and the Bid-Specification Process” research study to greatly improve the understanding of the commercial bid and product specification process throughout the intelligent buildings industry value-chain and related decision-making process. The broad purpose of the study was to identify and understand the market imperfections and inconsistencies that exist in designing and implementing intelligent building projects, as well as making investment decisions on intelligent technologies. To this end, the research identified and assessed critical areas and importance factors to enable project sponsors to: further product/services market development; unify stakeholder decision-making processes; identify opportunities/needs for training and coaching to remove obstacles from the process; and to provide product demand information to parallel market segments and other business areas. Organizations that participated in CABA’s “Intelligent Buildings and the Bid-Specification Process” 2012 study included: Automated Logic Corporation, BACnet International, Cadillac Fairview Corporation, Diebold Incorporated, Distech Controls Inc., Honeywell International, Hydro One Networks Inc., Ingersoll Rand/Trane/Schlage, International Facility Management Association (IFMA), Johnson Controls Inc., Lenel Systems International, Ontario Power Authority, Overhead Door Corporation, Philips Research North America, Siemens Industry, Inc., Smardt Chiller Group Inc., Telecommunications Industry Association (TIA), United Technologies Corporation and Verizon. CABA commissioned Frost & Sullivan (www.frost.com), an independent market research and consulting firm, to conduct this 2012 landmark research study.

Intelligent Buildings and the Bid-Specification Process

Project Objectives

Key Research Objectives: The key objectives of this research are as follows:

• Evaluate the main aspects of the bid specification process • Understand how decisions are made in the process and the role of key influencers in

such decisions • Determine the optimal way of working with various stakeholders involved in the

process • Create the right customer and partner awareness approaches to achieve better

technology adoption • Understand common goals and objectives that can be established for various

participants to work cohesively for success • Understand the changing dynamics of the industry and the impact on intelligent

building solutions and services • Create the right business approach to respond to changing demand • Define opportunities and prospects for market participants

5

Intelligent Buildings and the Bid-Specification Process

Methodology

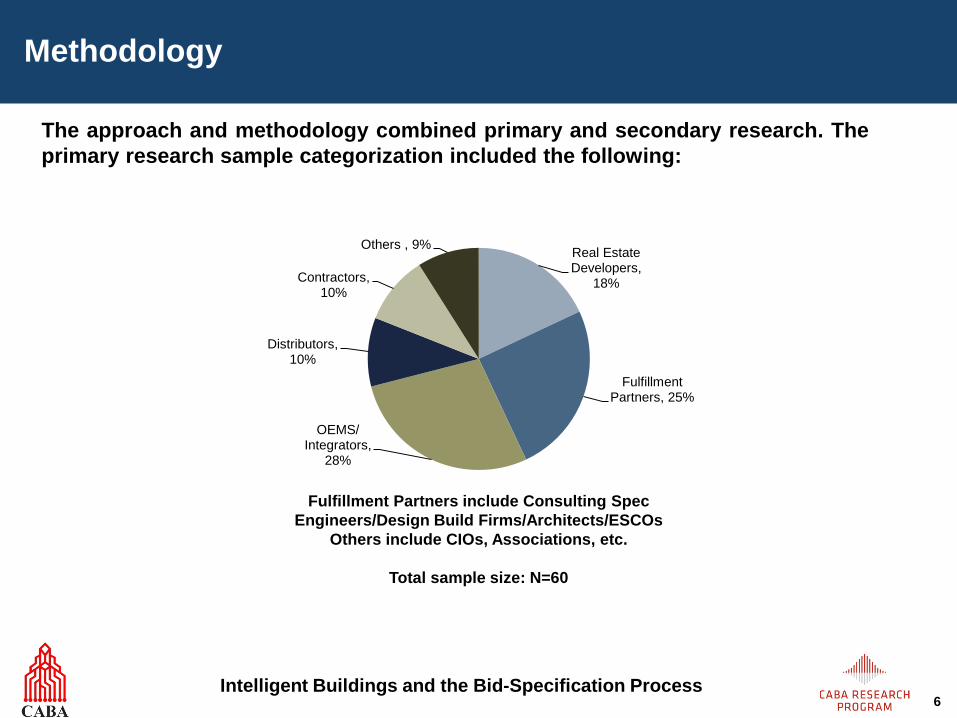

The approach and methodology combined primary and secondary research. The primary research sample categorization included the following:

Fulfillment Partners include Consulting Spec Engineers/Design Build Firms/Architects/ESCOs

Others include CIOs, Associations, etc.

Total sample size: N=60

Real Estate Developers,

18%

Fulfillment Partners, 25%

OEMS/ Integrators,

28%

Distributors, 10%

Contractors, 10%

Others , 9%

6

Intelligent Buildings and the Bid-Specification Process

Key Takeaways

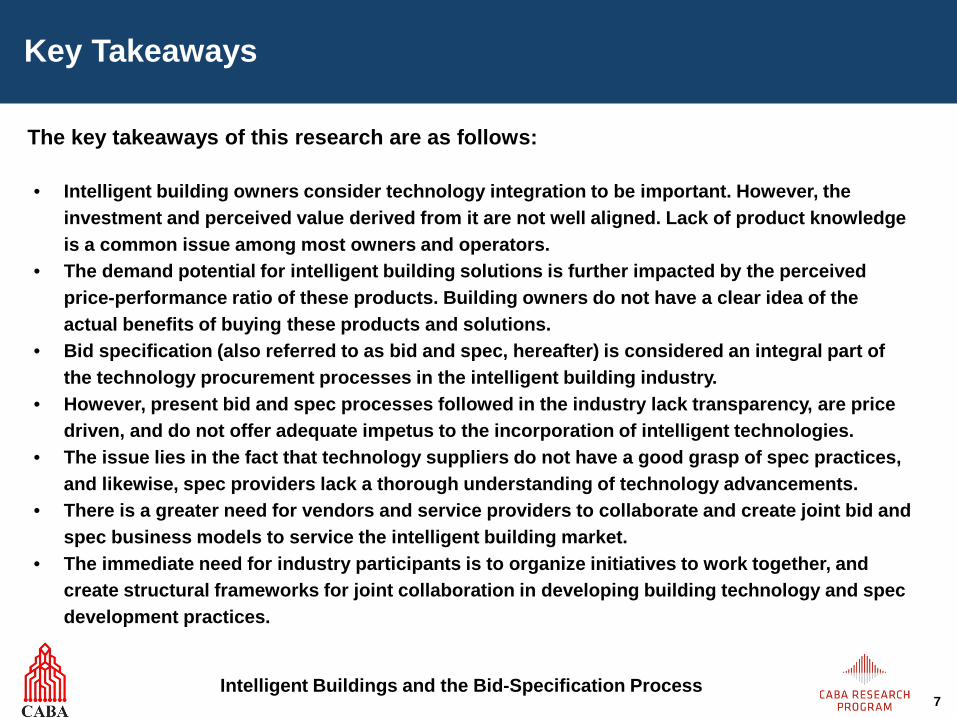

The key takeaways of this research are as follows: • Intelligent building owners consider technology integration to be important. However, the

investment and perceived value derived from it are not well aligned. Lack of product knowledge is a common issue among most owners and operators.

• The demand potential for intelligent building solutions is further impacted by the perceived price-performance ratio of these products. Building owners do not have a clear idea of the actual benefits of buying these products and solutions.

• Bid specification (also referred to as bid and spec, hereafter) is considered an integral part of the technology procurement processes in the intelligent building industry.

• However, present bid and spec processes followed in the industry lack transparency, are price driven, and do not offer adequate impetus to the incorporation of intelligent technologies.

• The issue lies in the fact that technology suppliers do not have a good grasp of spec practices, and likewise, spec providers lack a thorough understanding of technology advancements.

• There is a greater need for vendors and service providers to collaborate and create joint bid and spec business models to service the intelligent building market.

• The immediate need for industry participants is to organize initiatives to work together, and create structural frameworks for joint collaboration in developing building technology and spec development practices.

7

Intelligent Buildings and the Bid-Specification Process

State of the Industry

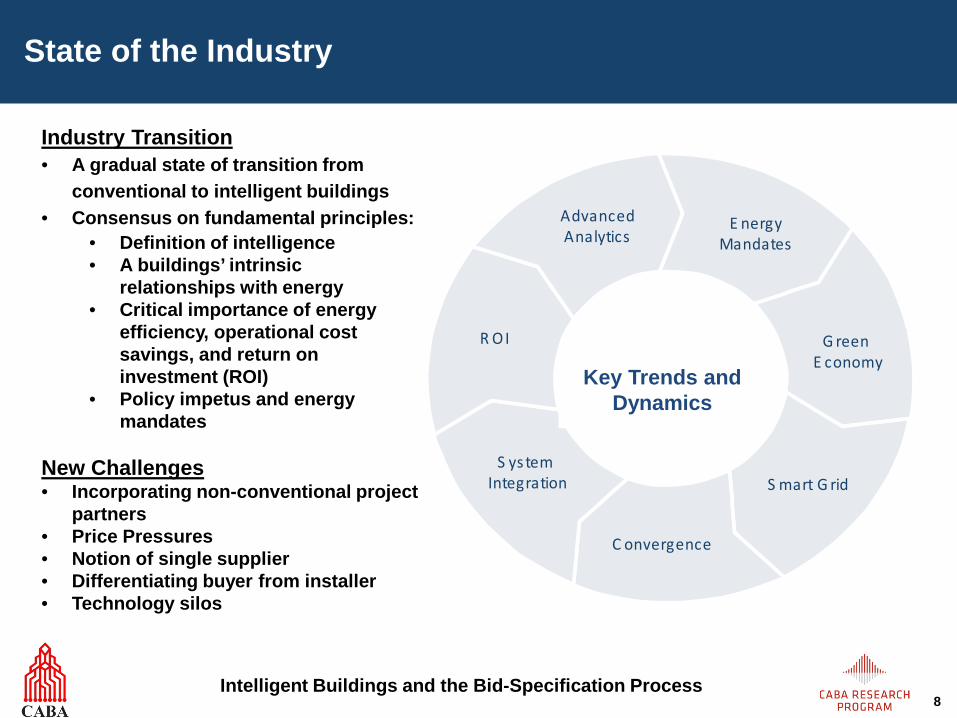

Industry Transition • A gradual state of transition from

conventional to intelligent buildings • Consensus on fundamental principles:

• Definition of intelligence • A buildings’ intrinsic

relationships with energy • Critical importance of energy

efficiency, operational cost savings, and return on investment (ROI)

• Policy impetus and energy mandates

New Challenges • Incorporating non-conventional project

partners • Price Pressures • Notion of single supplier • Differentiating buyer from installer • Technology silos

Meg atrends

S hift to IP F eature -R ich P roducts

Interoperability

C onvergence

Improved S torage

P rice/ P erformance

R O I

E nergy Mandates

G reen E conomy

S mart G rid

C onvergence

Advanced Analytics

R O I

S ys tem Integration

Meg atrends

S hift to IP F eature -R ich P roducts

Interoperability

C onvergence

Improved S torage

P rice/ P erformance

R O I

E nergy Mandates

G reen E conomy

S mart G rid

C onvergence

Advanced Analytics

R O I

S ys tem Integration

Key Trends and Dynamics

8

Intelligent Buildings and the Bid-Specification Process

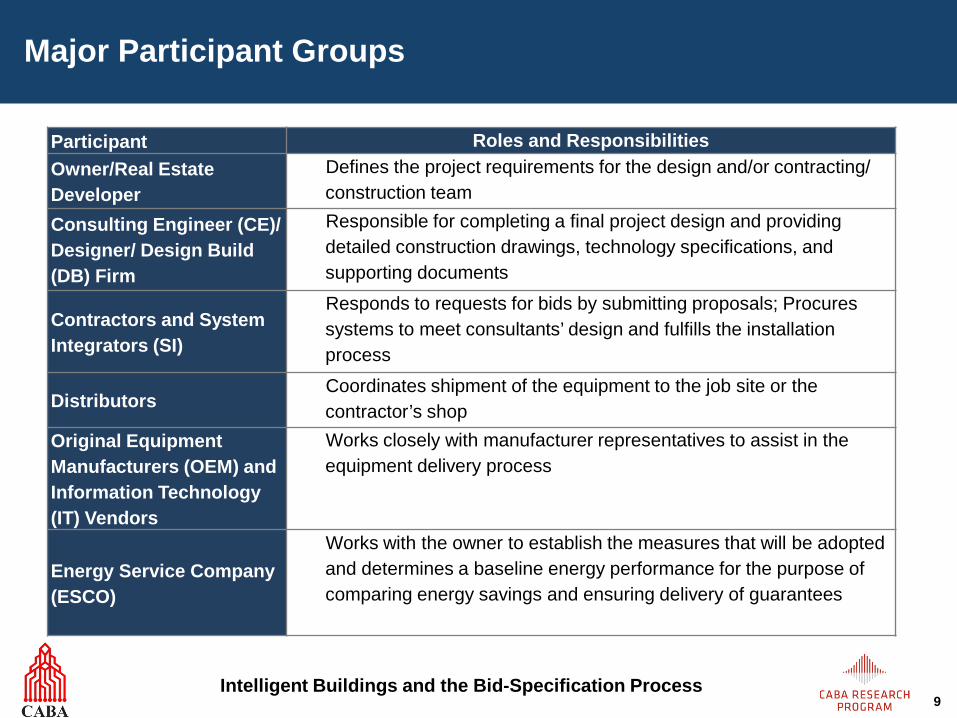

Major Participant Groups

Participant Roles and Responsibilities Owner/Real Estate Developer

Defines the project requirements for the design and/or contracting/ construction team

Consulting Engineer (CE)/ Designer/ Design Build (DB) Firm

Responsible for completing a final project design and providing detailed construction drawings, technology specifications, and supporting documents

Contractors and System Integrators (SI)

Responds to requests for bids by submitting proposals; Procures systems to meet consultants’ design and fulfills the installation process

Distributors Coordinates shipment of the equipment to the job site or the contractor’s shop

Original Equipment Manufacturers (OEM) and Information Technology (IT) Vendors

Works closely with manufacturer representatives to assist in the equipment delivery process

Energy Service Company (ESCO)

Works with the owner to establish the measures that will be adopted and determines a baseline energy performance for the purpose of comparing energy savings and ensuring delivery of guarantees

9

Intelligent Buildings and the Bid-Specification Process

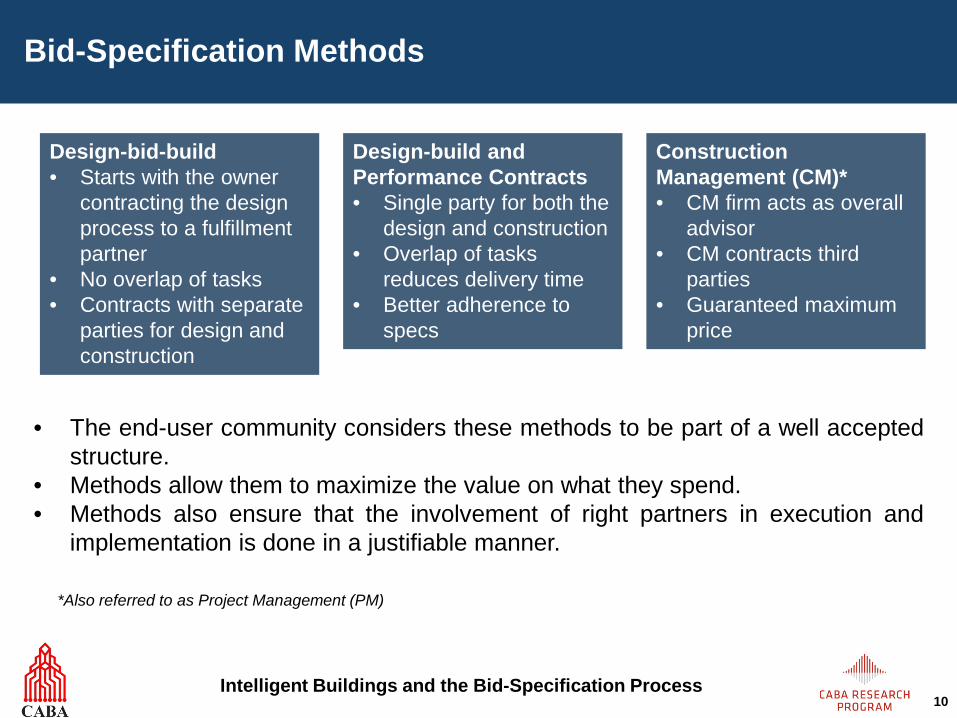

Bid-Specification Methods

Design-bid-build • Starts with the owner

contracting the design process to a fulfillment partner

• No overlap of tasks • Contracts with separate

parties for design and construction

Design-build and Performance Contracts • Single party for both the

design and construction • Overlap of tasks

reduces delivery time • Better adherence to

specs

Construction Management (CM)* • CM firm acts as overall

advisor • CM contracts third

parties • Guaranteed maximum

price

• The end-user community considers these methods to be part of a well accepted structure.

• Methods allow them to maximize the value on what they spend. • Methods also ensure that the involvement of right partners in execution and

implementation is done in a justifiable manner.

*Also referred to as Project Management (PM)

10

Intelligent Buildings and the Bid-Specification Process

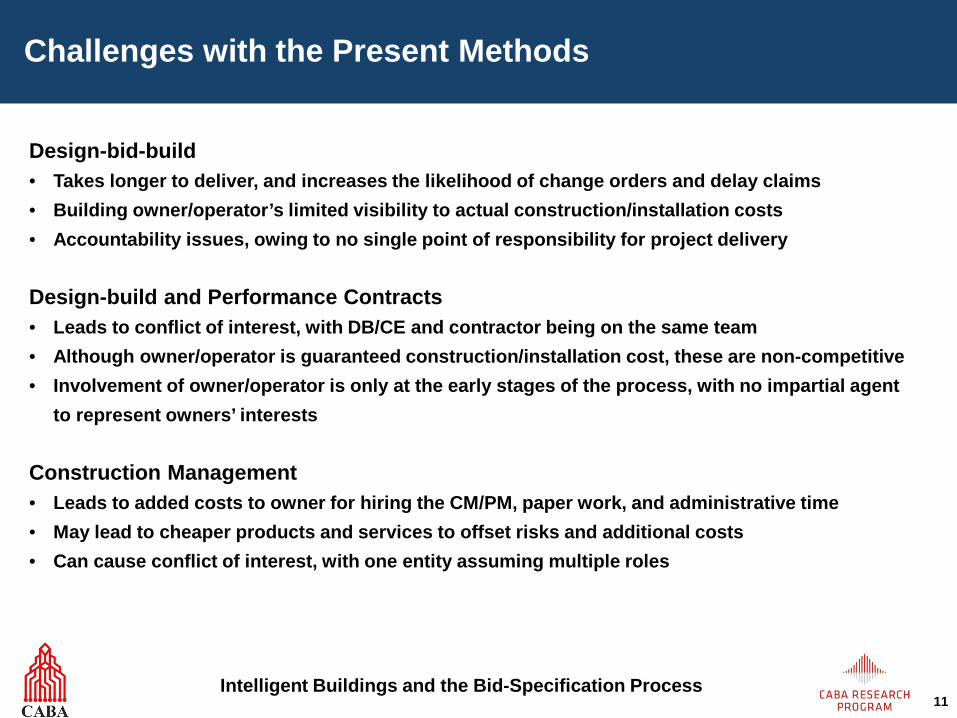

Challenges with the Present Methods

Design-bid-build • Takes longer to deliver, and increases the likelihood of change orders and delay claims • Building owner/operator’s limited visibility to actual construction/installation costs • Accountability issues, owing to no single point of responsibility for project delivery Design-build and Performance Contracts • Leads to conflict of interest, with DB/CE and contractor being on the same team • Although owner/operator is guaranteed construction/installation cost, these are non-competitive • Involvement of owner/operator is only at the early stages of the process, with no impartial agent

to represent owners’ interests Construction Management • Leads to added costs to owner for hiring the CM/PM, paper work, and administrative time • May lead to cheaper products and services to offset risks and additional costs • Can cause conflict of interest, with one entity assuming multiple roles

11

Intelligent Buildings and the Bid-Specification Process

Process Optimization

The following aspects need to be incorporated in the present bid and spec methods: • Opting for Objective Points Criteria - An objective evaluation criterion is required to ensure that product

and technology selection is based on some quantification of actual benefits to the project/building. • Role of Quality Surveyor/Advisor - Given the disconnect among various delivery partners in the bid spec

processes, there is a critical need for autonomous supervision to ensure that processes are followed transparently and the correct choices are made in selection of products, technology and services.

• Create Scope for New Vendors - Creating scope for the inclusion of these smaller players is necessary, as it allows the building owner to take advantage of new innovative technology – at pricing that may not be available from larger vendors.

• Avoid Cost Thresholds - Removing this component could potentially help optimize the process and allow for the inclusion of more vendors and suppliers into the selection process.

• Mandate a Feedback Loop - Including this as a prescriptive requirement into the contractual process can offer valuable insights into technology performance, cost-benefit evaluation and establish their importance in intelligent building projects.

• Integrated Value Chain and Delivery Approaches - This will prompt suppliers and service providers to collaborate and offer the most optimal solution, while capitalizing on collective bargaining capabilities to influence selection.

12

Intelligent Buildings and the Bid-Specification Process

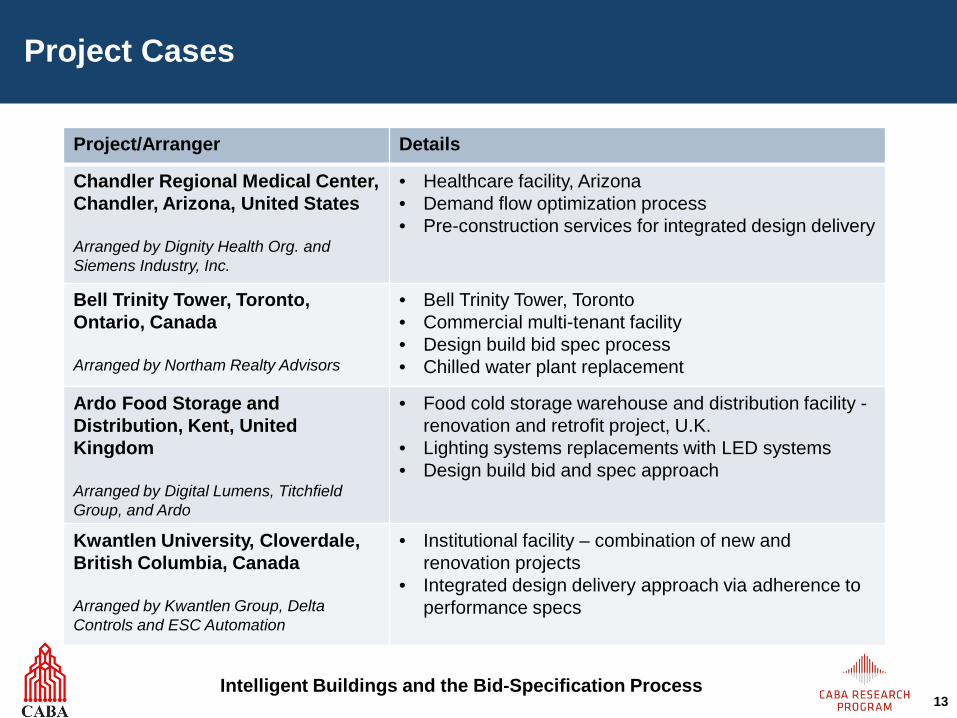

Project Cases

Project/Arranger Details

Chandler Regional Medical Center, Chandler, Arizona, United States Arranged by Dignity Health Org. and Siemens Industry, Inc.

• Healthcare facility, Arizona • Demand flow optimization process • Pre-construction services for integrated design delivery

Bell Trinity Tower, Toronto, Ontario, Canada Arranged by Northam Realty Advisors

• Bell Trinity Tower, Toronto • Commercial multi-tenant facility • Design build bid spec process • Chilled water plant replacement

Ardo Food Storage and Distribution, Kent, United Kingdom Arranged by Digital Lumens, Titchfield Group, and Ardo

• Food cold storage warehouse and distribution facility - renovation and retrofit project, U.K.

• Lighting systems replacements with LED systems • Design build bid and spec approach

Kwantlen University, Cloverdale, British Columbia, Canada Arranged by Kwantlen Group, Delta Controls and ESC Automation

• Institutional facility – combination of new and renovation projects

• Integrated design delivery approach via adherence to performance specs

13

Intelligent Buildings and the Bid-Specification Process

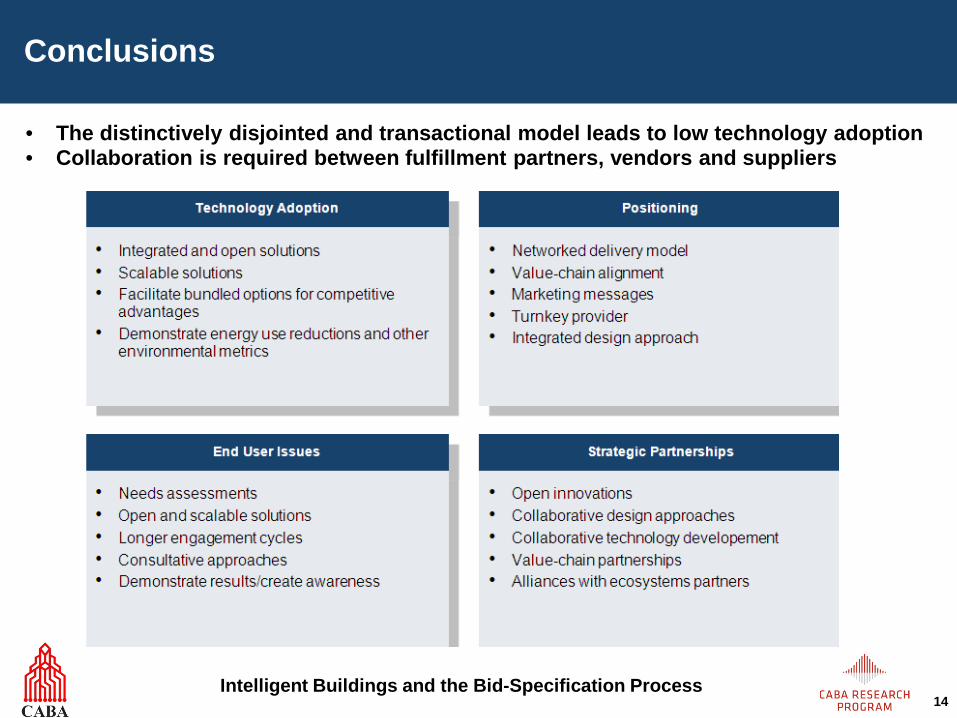

Conclusions

• The distinctively disjointed and transactional model leads to low technology adoption • Collaboration is required between fulfillment partners, vendors and suppliers

14

Intelligent Buildings and the Bid-Specification Process

Contact Information

15

Contact

John Hall CABA Research Director

Suite 210 1173 Cyrville Road

Ottawa, ON K1J 7S6

613.686.1814 ext. 227

Contact

George Grimes CABA Business Development Manager

Suite 210 1173 Cyrville Road

Ottawa, ON K1J 7S6

613.686.1814 ext. 226

CABA and the following CABA members funded this project:

Emerald Sponsors

Diamond Sponsors

Prepared by:

www.CABA.org

1.2

Intelligent Buildings and the Bid Specification Process

2

Disclaimer

Frost & Sullivan takes no responsibility for incorrect information supplied to us by industry participants or users. Qualitative and quantitative market information is based primarily on interviews and secondary sources referenced at the research phase and; therefore, is subject to fluctuations. The scope of this research does not include quantitative market sizing or projections.

Intelligent building and/or bid spec, cases, capabilities of products and technologies, and processes evaluated in the report are representative of the market, but not comprehensive, and inclusion in the study does not imply endorsement. Research evaluations are aligned with the agreed scope of work of this project and findings are subject to best-effort analysis and availability of information.

All directional statements about the expected future state of the industry are based on consensus-based industry dialogue with key stakeholders, anticipated trends, and best-effort understanding of the future course of the industry.

The views expressed in this report accurately reflect Frost & Sullivan’s views based on primary and secondary research with industry participants, industry experts, end users, standards bodies, industry organizations, and other related sources.

In addition to the above, Frost & Sullivan’s robust in-house research models and processes, along with the repository of Industry Research and Decision-support Databases, have been instrumental in the completion of this report.

The trends identified in this report are based on discussions with industry participants and Frost & Sullivan’s ongoing research in intelligent buildings, technology, services, and related markets. Conclusions drawn are anticipated only and do not imply prediction of events in the future. These conclusions are based on best judgment of exhibited trends, expected direction the industry may follow, and consideration of a host of industry drivers, restraints, and challenges, which represent the possibility for such trends to occur over a time frame. All supporting analyses and data, as permissible, within contractual time and budget, are provided to the best of ability.

Information provided in all segments is based on availability and the willingness of participants in sharing these within the scope, budget, and allocated time frame of the project, and reflects the views of industry participants.

While the document is believed to contain correct information, Frost & Sullivan does not make any warranty, expressed or implied, or assume any legal responsibility for the accuracy, completeness, or usefulness of the information, product, technology, solution, company name, or process discussed in the report, or claims that its use would not infringe any privately-owned rights.

References made to products, technology, solutions, trade names, vendors, or otherwise, do not necessarily constitute or imply its endorsement or recommendation.

No part of our analyst compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed in this service.

Frost & Sullivan consulting services are limited publications containing valuable market information provided to the Continental Automated Buildings Association (CABA) in response to an information

Intelligent Buildings and the Bid Specification Process

3

request. Our customers acknowledge, when ordering, that Frost & Sullivan consulting services are for customers’ internal use and not for general publication or disclosure to third parties.

No part of this consulting service may be given, lent, resold, or disclosed to non-customers without written permission of CABA. Furthermore, no part may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the permission of the above parties.

© 2012 Frost & Sullivan and CABA. All rights reserved. This document contains highly confidential information. No part of it may be circulated, quoted, copied, or otherwise reproduced without the written approval of CABA.

Intelligent Buildings and the Bid Specification Process

4

Study Background The Continental Automated Buildings Association (CABA) is an industry association dedicated to the advancement of intelligent homes and intelligent buildings technologies. CABA is an international trade association, with over 300 major private and public technology companies committed to research and development within the intelligent buildings and connected home sector. Association members are involved in the design, manufacture, installation and retailing of products for home and building automation. CABA is a leader in initiating and developing cross-industry collaborative research, under the CABA Research Program. In 2012, CABA’s Intelligent & Integrated Buildings Council (IIBC) commissioned the “Intelligent Buildings and the Bid-Specification Process” research study to greatly improve the understanding of the commercial bid and product specification process throughout the intelligent buildings industry value chain and related decision-making process. The broad purpose of the study was to identify and understand the market imperfections and inconsistencies that exist in designing and implementing intelligent buildings projects, as well as making investment decisions on intelligent technologies. To this end, the research identified and assessed critical areas and importance factors to enable project sponsors to: further product/services market development; unify stakeholder decision-making processes; identify opportunities/needs for training and coaching to remove obstacles from the process; and to provide product demand information to parallel market segments and other business areas. Organizations that participated in CABA’s “Intelligent Buildings and the Bid-Specification Process” 2012 study included: Automated Logic Corporation, BACnet International, Cadillac Fairview Corporation, Diebold Incorporated, Distech Controls Inc., Honeywell International, Hydro One Networks Inc., Ingersoll Rand/Trane/Schlage, International Facility Management Association (IFMA), Johnson Controls Inc., Lenel Systems International, Ontario Power Authority, Overhead Door Corporation, Philips, Siemens Industry, Inc., Smardt Chiller Group Inc., Telecommunications Industry Association (TIA), United Technologies Corporation and Verizon. CABA commissioned Frost & Sullivan (www.frost.com), an independent market research and consulting firm, to conduct this 2012 landmark research study.

Intelligent Buildings and the Bid Specification Process

5

1

Executive Overview

1.1 Project Background

The Continental Automated Buildings Association (CABA) is a not-for-profit industry association dedicated to the advancement of intelligent home and intelligent buildings technologies. The organization is supported by an international membership of more than 300 organizations involved in the design, manufacture, installation, and retailing of products relating to home automation and building automation. Public organizations, including utilities and government organizations, are also members.

The Intelligent & Integrated Buildings Council (IIBC), a core working committee of the Continental Automated Buildings Association (CABA), commissioned this research project titled “Intelligent Buildings and the Bid Specification Process1,” with the objective that it could assist in building the industry’s knowledge base and perspectives on the bid spec process adopted for executing and fulfilling technology adoption, service integration, retrofit projects, and other ongoing developmental plans in the building industry. Frost & Sullivan was commissioned by the Project Steering Committee, instituted for the specific purpose of funding and overseeing this collaborative research, to undertake the project on behalf of CABA.

1.1.1 Overview and Focus Areas

The heterogeneous and fragmented nature of the building technology industry and its associated service segments warrants that various stakeholders be involved in any given project delivery process. The ultimate decision on technology adoption is usually dependent on the influence of various service partners. Differences in operational methods of these partners leads to delay in implementation and often results in the selection of low-cost options that do not offer long-term benefits to the building owner.

Intelligent Buildings and the Bid Specification Process

6

Stringent budgets and quicker payback frequently become the sole criteria for selecting a particular set of technology solutions. Incorporation of intelligence is usually either postponed indefinitely or not considered at all. The present bid spec processes followed in the industry further add to the issue because contractors, system integrators, and consulting spec engineers exert varying degrees of influence on the end-user’s decision making process.

The bid spec process is characterized by vendors and service providers from established technology, product, and solution segments, as well as those offering smart and energy-efficient alternatives. These players operate in the market with a variety of service providers involved from prototype development to delivery. Given this position, there are challenges that the building technology industry players have to face, both internally and externally, to create a strong position for themselves in the market.

Therefore, the key focus areas agreed upon by the Project Steering Committee include the following:

• Current status of intelligent technology adoption • The optimal delivery ecosystem for success of bid spec projects • Level of awareness of various decision-makers • Process changes to be adopted • The opportunities for various industry participants

The content of this report encompasses the above focus areas.

1.2 Key Objectives of Project Sponsors

The key objectives of project sponsors are as follows:

• Evaluate the key aspects of bid spec processes • Understand how decisions are made in the process and the role of key influencers in

such decisions • Determine the most optimal way of working with various stakeholders involved in the

process • Create the right customer and partner awareness approaches to achieve better

technology adoption • Understand common goals and objectives that can be established for various

participants to work cohesively for success • Understand the changing dynamics of the industry and the impact on intelligent buildings

solutions and services • Create the right business approach to respond to changing demand • Define opportunities and prospects for market participants

Intelligent Buildings and the Bid Specification Process

7

1.3 Methodology and Research Design

Frost & Sullivan used a combination of primary and secondary research methodologies to compile the necessary information for this project. Information provided in all segments is based on availability and the willingness of participants in sharing these within the scope, budget, and allocated time frame of the project. The trends identified in this report are based on discussions with industry participants and Frost & Sullivan’s ongoing research in building technologies, energy, and related markets. The conclusions drawn are based on our best judgment of exhibited trends, the expected direction the industry may follow, and consideration of a host of industry drivers, restraints, and challenges that represent the possibility for such trends to occur over a specific time frame. All supporting analyses and data, as permissible within the contractual time and budget, are provided to the best of our ability.

Primary Research

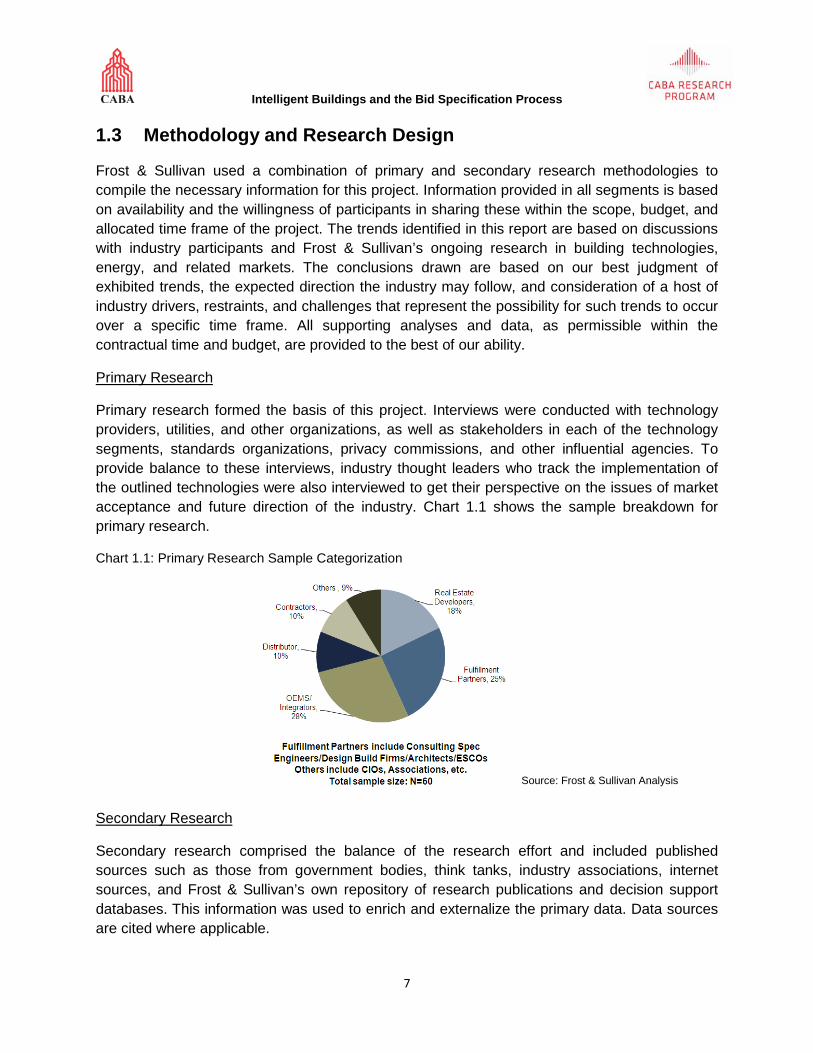

Primary research formed the basis of this project. Interviews were conducted with technology providers, utilities, and other organizations, as well as stakeholders in each of the technology segments, standards organizations, privacy commissions, and other influential agencies. To provide balance to these interviews, industry thought leaders who track the implementation of the outlined technologies were also interviewed to get their perspective on the issues of market acceptance and future direction of the industry. Chart 1.1 shows the sample breakdown for primary research.

Chart 1.1: Primary Research Sample Categorization

Secondary Research

Secondary research comprised the balance of the research effort and included published sources such as those from government bodies, think tanks, industry associations, internet sources, and Frost & Sullivan’s own repository of research publications and decision support databases. This information was used to enrich and externalize the primary data. Data sources are cited where applicable.

Source: Frost & Sullivan Analysis

Intelligent Buildings and the Bid Specification Process

8

1.4 Definitions

The definition of an “intelligent building” was coined through consensus-based deliberations as part of previous projects undertaken by CABA and Frost & Sullivan. As developed over the course of the following two projects: Convergence of Green and Intelligent Buildings2, and the Intelligent Buildings Roadmap 20113, an intelligent building is defined as a building that uses both technology and process to create an environment that is safe, healthy, and comfortable, and enables productivity and well-being for its occupants. An intelligent building provides timely, integrated system information for its owners so that they may make intelligent decisions regarding its operation and maintenance. An intelligent building has an implicit logic that effectively evolves with changing user requirements and technology, ensuring continued and improved intelligent operation, maintenance, and optimization. It exhibits key attributes of environmental sustainability to benefit present and future generations.

What can we expect of such a building?

• Improved interdependency between building systems and building users • A building that can detect the state it is in and make adjustments to itself • Provides a healthier and more comfortable environment • Improves long-term economic performance • Reduces energy and resource usage • Leverages renewable energy technologies • Improves indoor air quality and occupant satisfaction • Is easier to maintain and built to last • Advanced/enhanced capabilities to deal with "churn" (occupant turnover/evolving mission) Intelligent buildings transcend integration to achieve interaction in which the previously independent systems work collectively to optimize the buildings’ performance and constantly create an environment that is most conducive to the occupants’ goals. Additionally, fully interoperable systems in intelligent buildings tend to perform better, cost less to maintain, and leave a smaller environmental imprint than individual utilities and communication systems. Each building is unique in its mission and operational objectives and, therefore, must balance short- and long-term needs accordingly.

Intelligent buildings serve as a dynamic environment that responds to occupants’ changing needs and lifestyles. As technology advances, and as information and communication expectations become more sophisticated, networking solutions both converge and automate the technologies to improve responsiveness, efficiency, and performance. To achieve this, an intelligent building combines data, voice, and video with security, heating, ventilation and air conditioning (HVACR), lighting, building controls, and other electronic controls on a single IP network platform that facilitates user management, space utilization, energy conservation, comfort, and systems improvement.

Intelligent Buildings and the Bid Specification Process

9

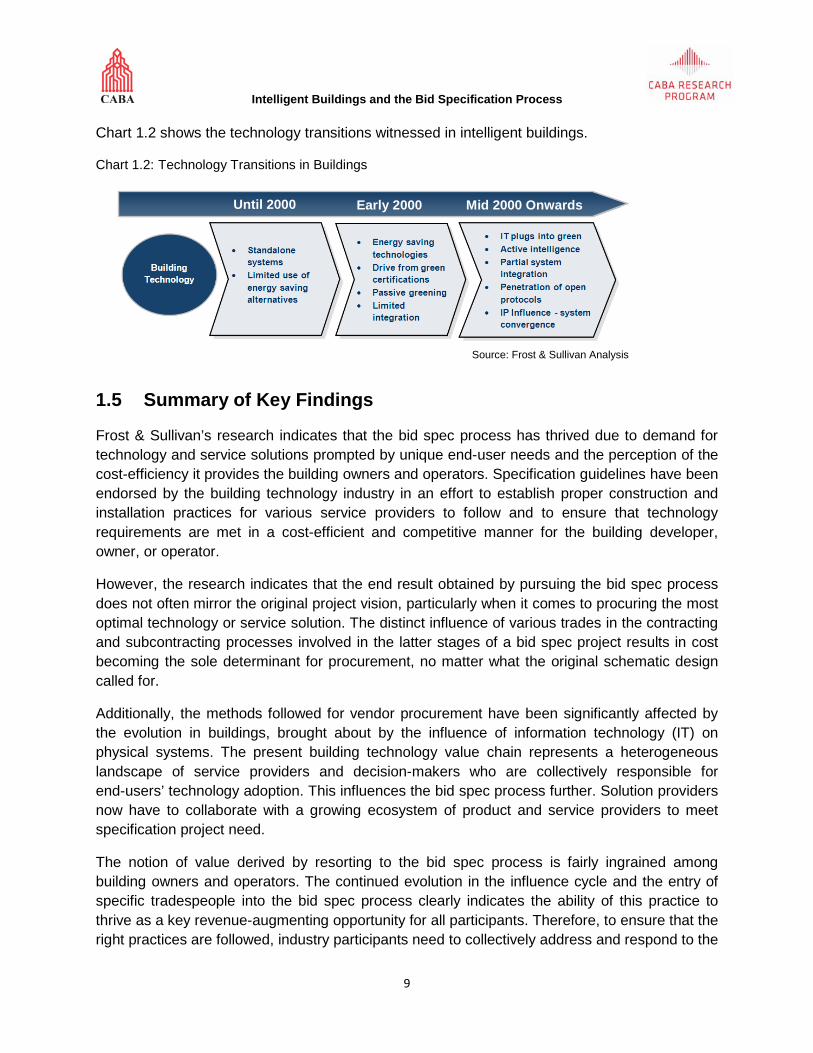

Chart 1.2 shows the technology transitions witnessed in intelligent buildings.

Chart 1.2: Technology Transitions in Buildings

1.5 Summary of Key Findings

Frost & Sullivan’s research indicates that the bid spec process has thrived due to demand for technology and service solutions prompted by unique end-user needs and the perception of the cost-efficiency it provides the building owners and operators. Specification guidelines have been endorsed by the building technology industry in an effort to establish proper construction and installation practices for various service providers to follow and to ensure that technology requirements are met in a cost-efficient and competitive manner for the building developer, owner, or operator.

However, the research indicates that the end result obtained by pursuing the bid spec process does not often mirror the original project vision, particularly when it comes to procuring the most optimal technology or service solution. The distinct influence of various trades in the contracting and subcontracting processes involved in the latter stages of a bid spec project results in cost becoming the sole determinant for procurement, no matter what the original schematic design called for.

Additionally, the methods followed for vendor procurement have been significantly affected by the evolution in buildings, brought about by the influence of information technology (IT) on physical systems. The present building technology value chain represents a heterogeneous landscape of service providers and decision-makers who are collectively responsible for end-users’ technology adoption. This influences the bid spec process further. Solution providers now have to collaborate with a growing ecosystem of product and service providers to meet specification project need.

The notion of value derived by resorting to the bid spec process is fairly ingrained among building owners and operators. The continued evolution in the influence cycle and the entry of specific tradespeople into the bid spec process clearly indicates the ability of this practice to thrive as a key revenue-augmenting opportunity for all participants. Therefore, to ensure that the right practices are followed, industry participants need to collectively address and respond to the

Source: Frost & Sullivan Analysis

Until 2000 Early 2000 Mid 2000 Onwards

Intelligent Buildings and the Bid Specification Process

10

fundamental challenges associated with the bid spec processes. The key findings of the research are summarized below under the following headings.

1.5.1 Current State of the Intelligent Buildings Industry

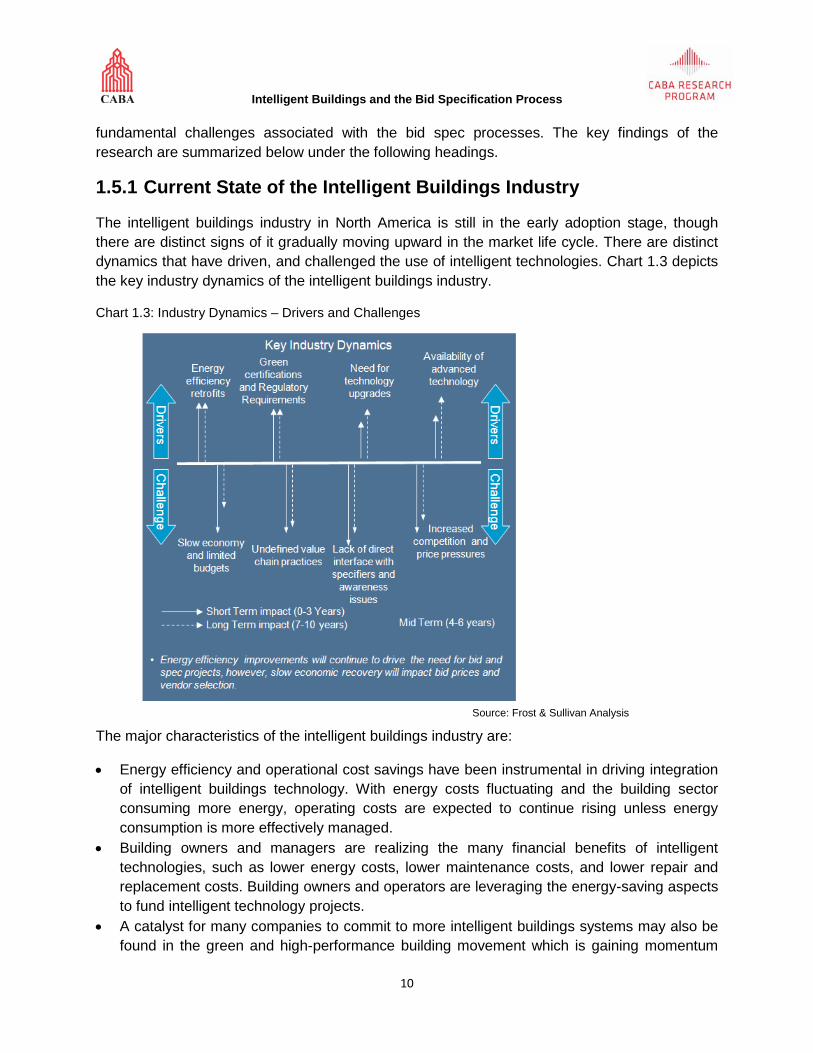

The intelligent buildings industry in North America is still in the early adoption stage, though there are distinct signs of it gradually moving upward in the market life cycle. There are distinct dynamics that have driven, and challenged the use of intelligent technologies. Chart 1.3 depicts the key industry dynamics of the intelligent buildings industry.

Chart 1.3: Industry Dynamics – Drivers and Challenges

The major characteristics of the intelligent buildings industry are:

• Energy efficiency and operational cost savings have been instrumental in driving integration of intelligent buildings technology. With energy costs fluctuating and the building sector consuming more energy, operating costs are expected to continue rising unless energy consumption is more effectively managed.

• Building owners and managers are realizing the many financial benefits of intelligent technologies, such as lower energy costs, lower maintenance costs, and lower repair and replacement costs. Building owners and operators are leveraging the energy-saving aspects to fund intelligent technology projects.

• A catalyst for many companies to commit to more intelligent buildings systems may also be found in the green and high-performance building movement which is gaining momentum

Source: Frost & Sullivan Analysis

Intelligent Buildings and the Bid Specification Process

11

daily. Building owners are investing in better building performance as a way to reduce energy costs.

• Additionally, there is pressure on building owners to provide detailed accountings of their greenhouse gas (GHG) emissions with taxation proposals or legislation (as in California) intended to either limit or tax emissions of carbon dioxide and other gases.

• Bid and spec has been integrated into procurement processes by building owners to maximize project efficiency, particularly when it comes to incorporating cost-prohibitive intelligent buildings solutions.

• A highly-fragmented delivery process and the presence of numerous stakeholders influencing the process create several hurdles in project execution. Schematic designs, adopted early on, often get revised on account of cheaper substitutes.

• A consensus-based approach to project delivery is needed, whereby various stakeholders can collaborate from the early conceptual stages of the project. This will ensure that all goals are met in an optimal manner and generate long return on investment (ROI) over the life cycle of a building.

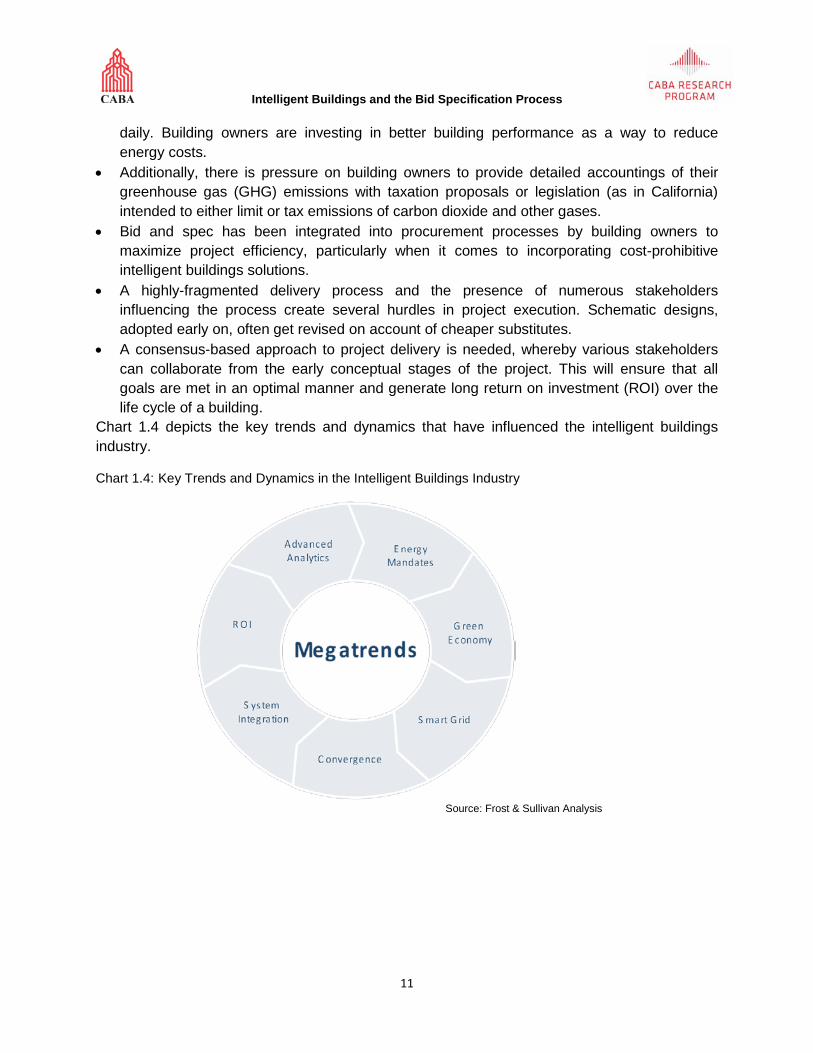

Chart 1.4 depicts the key trends and dynamics that have influenced the intelligent buildings industry.

Chart 1.4: Key Trends and Dynamics in the Intelligent Buildings Industry

Source: Frost & Sullivan Analysis

Intelligent Buildings and the Bid Specification Process

12

1.5.2 Review of Major Issues

The obvious disconnect among various value chain partners has led to bid spec processes being utilized sub-optimally, with little scope for incorporation of intelligent buildings solutions. However, as more strategic alliances are formed and stakeholder initiatives brought together, the acceptance and awareness of sophisticated bid and spec modules could increase favorably.

To respond to opportunities promptly, it is inevitable that most participants will have to form alliances to bundle solutions to position themselves competitively. Building owners’ needs evaluations are expected to be significant in determining the acceptability of various intelligent solutions offered and influencing the overall pace of market acceptance for products, services, and solutions.

In the immediate term, energy efficiency and reduction in operational expenses will continue to be the key drivers for adopting intelligent technologies. The ability to quantify energy savings and offering open and interoperable systems will be instrumental in keeping market demand sustained for these solutions. Bid spec processes will have to be remodeled to factor these needs.

Ultimately, changes in the delivery models and value chain alliances would need to be effected, as participants prepare to address the market potential for bid and spec in high growth vertical segments. Integrated approaches to solution delivery in bid spec are likely to be adopted to address this, where participants would work collaboratively. The industry expects intelligent buildings solutions to gain better commercial acceptance only in the longer time frame, once the key focus areas identified for the success of these solutions gradually get addressed through the strategic initiatives of industry participants.

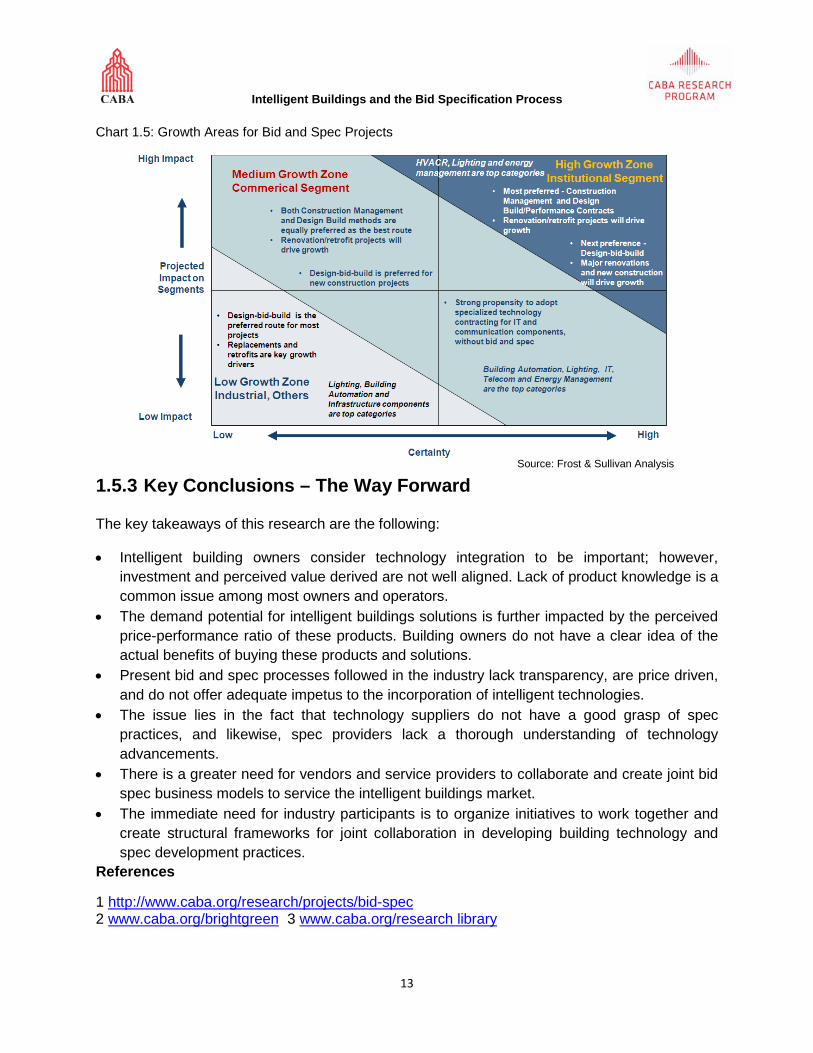

Chart 1.5 provides a snapshot of the growth opportunities present in the intelligent buildings industry for bid spec projects among the key vertical segments.

Intelligent Buildings and the Bid Specification Process

13

Chart 1.5: Growth Areas for Bid and Spec Projects

1.5.3 Key Conclusions – The Way Forward

The key takeaways of this research are the following:

• Intelligent building owners consider technology integration to be important; however, investment and perceived value derived are not well aligned. Lack of product knowledge is a common issue among most owners and operators.

• The demand potential for intelligent buildings solutions is further impacted by the perceived price-performance ratio of these products. Building owners do not have a clear idea of the actual benefits of buying these products and solutions.

• Present bid and spec processes followed in the industry lack transparency, are price driven, and do not offer adequate impetus to the incorporation of intelligent technologies.

• The issue lies in the fact that technology suppliers do not have a good grasp of spec practices, and likewise, spec providers lack a thorough understanding of technology advancements.

• There is a greater need for vendors and service providers to collaborate and create joint bid spec business models to service the intelligent buildings market.

• The immediate need for industry participants is to organize initiatives to work together and create structural frameworks for joint collaboration in developing building technology and spec development practices.

References

1 http://www.caba.org/research/projects/bid-spec 2 www.caba.org/brightgreen 3 www.caba.org/research library

Source: Frost & Sullivan Analysis

Intelligent Buildings and the Bid Specification Process

14

Table of Contents

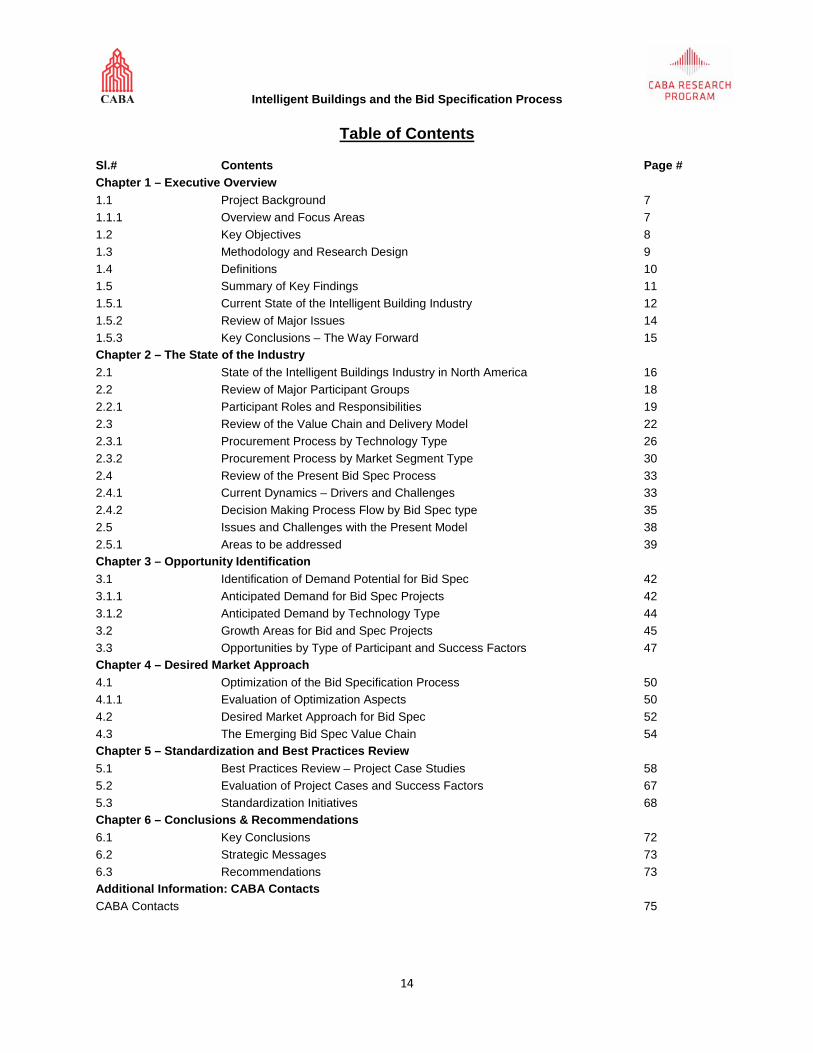

Sl.# Contents Page # Chapter 1 – Executive Overview 1.1 Project Background 7 1.1.1 Overview and Focus Areas 7 1.2 Key Objectives 8 1.3 Methodology and Research Design 9 1.4 Definitions 10 1.5 Summary of Key Findings 11 1.5.1 Current State of the Intelligent Building Industry 12 1.5.2 Review of Major Issues 14 1.5.3 Key Conclusions – The Way Forward 15 Chapter 2 – The State of the Industry 2.1 State of the Intelligent Buildings Industry in North America 16 2.2 Review of Major Participant Groups 18 2.2.1 Participant Roles and Responsibilities 19 2.3 Review of the Value Chain and Delivery Model 22 2.3.1 Procurement Process by Technology Type 26 2.3.2 Procurement Process by Market Segment Type 30 2.4 Review of the Present Bid Spec Process 33 2.4.1 Current Dynamics – Drivers and Challenges 33 2.4.2 Decision Making Process Flow by Bid Spec type 35 2.5 Issues and Challenges with the Present Model 38 2.5.1 Areas to be addressed 39 Chapter 3 – Opportunity Identification 3.1 Identification of Demand Potential for Bid Spec 42 3.1.1 Anticipated Demand for Bid Spec Projects 42 3.1.2 Anticipated Demand by Technology Type 44 3.2 Growth Areas for Bid and Spec Projects 45 3.3 Opportunities by Type of Participant and Success Factors 47 Chapter 4 – Desired Market Approach 4.1 Optimization of the Bid Specification Process 50 4.1.1 Evaluation of Optimization Aspects 50 4.2 Desired Market Approach for Bid Spec 52 4.3 The Emerging Bid Spec Value Chain 54 Chapter 5 – Standardization and Best Practices Review 5.1 Best Practices Review – Project Case Studies 58 5.2 Evaluation of Project Cases and Success Factors 67 5.3 Standardization Initiatives 68 Chapter 6 – Conclusions & Recommendations 6.1 Key Conclusions 72 6.2 Strategic Messages 73 6.3 Recommendations 73 Additional Information: CABA Contacts CABA Contacts 75

Intelligent Buildings and the Bid Specification Process

15

List of Charts and Other Exhibits

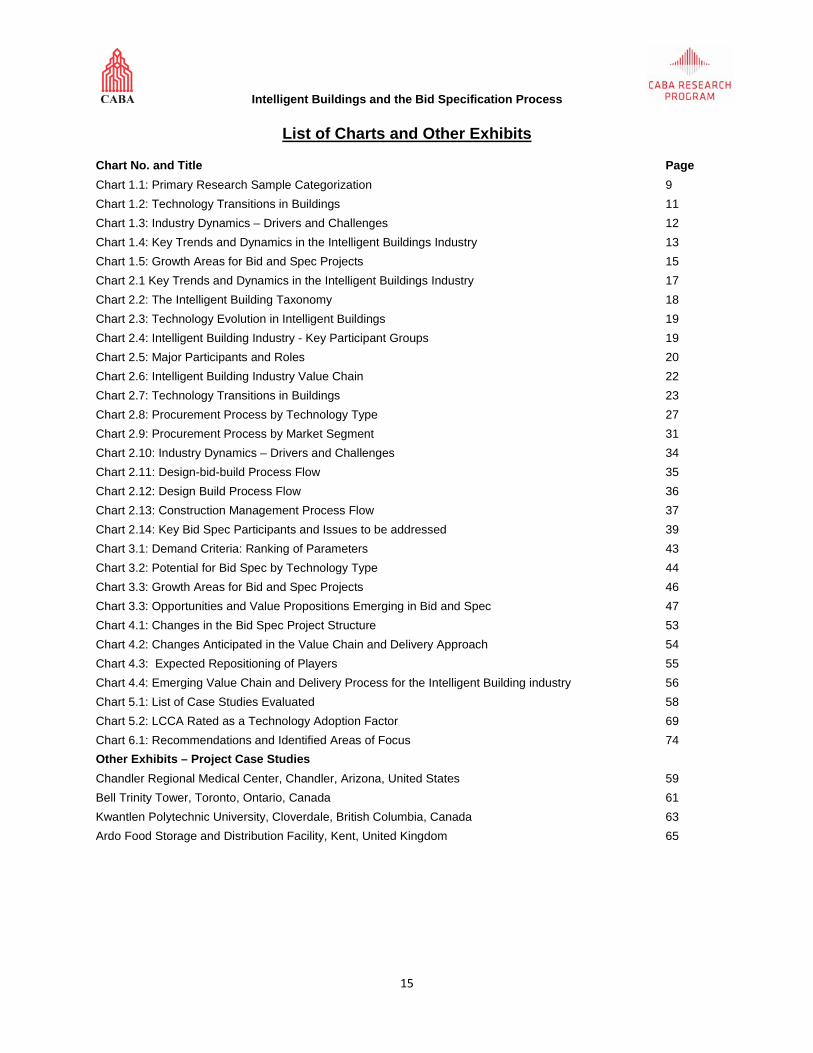

Chart No. and Title Page Chart 1.1: Primary Research Sample Categorization 9 Chart 1.2: Technology Transitions in Buildings 11 Chart 1.3: Industry Dynamics – Drivers and Challenges 12 Chart 1.4: Key Trends and Dynamics in the Intelligent Buildings Industry 13 Chart 1.5: Growth Areas for Bid and Spec Projects 15 Chart 2.1 Key Trends and Dynamics in the Intelligent Buildings Industry 17 Chart 2.2: The Intelligent Building Taxonomy 18 Chart 2.3: Technology Evolution in Intelligent Buildings 19 Chart 2.4: Intelligent Building Industry - Key Participant Groups 19 Chart 2.5: Major Participants and Roles 20 Chart 2.6: Intelligent Building Industry Value Chain 22 Chart 2.7: Technology Transitions in Buildings 23 Chart 2.8: Procurement Process by Technology Type 27 Chart 2.9: Procurement Process by Market Segment 31 Chart 2.10: Industry Dynamics – Drivers and Challenges 34 Chart 2.11: Design-bid-build Process Flow 35 Chart 2.12: Design Build Process Flow 36 Chart 2.13: Construction Management Process Flow 37 Chart 2.14: Key Bid Spec Participants and Issues to be addressed 39 Chart 3.1: Demand Criteria: Ranking of Parameters 43 Chart 3.2: Potential for Bid Spec by Technology Type 44 Chart 3.3: Growth Areas for Bid and Spec Projects 46 Chart 3.3: Opportunities and Value Propositions Emerging in Bid and Spec 47 Chart 4.1: Changes in the Bid Spec Project Structure 53 Chart 4.2: Changes Anticipated in the Value Chain and Delivery Approach 54 Chart 4.3: Expected Repositioning of Players 55 Chart 4.4: Emerging Value Chain and Delivery Process for the Intelligent Building industry 56 Chart 5.1: List of Case Studies Evaluated 58 Chart 5.2: LCCA Rated as a Technology Adoption Factor 69 Chart 6.1: Recommendations and Identified Areas of Focus 74 Other Exhibits – Project Case Studies Chandler Regional Medical Center, Chandler, Arizona, United States 59 Bell Trinity Tower, Toronto, Ontario, Canada 61 Kwantlen Polytechnic University, Cloverdale, British Columbia, Canada 63 Ardo Food Storage and Distribution Facility, Kent, United Kingdom 65

Intelligent Buildings and the Bid Specification Process

16

Additional Information: CABA Contacts

CABA Contacts

Summary findings are available via a PowerPoint version of this report. Please contact CABA for further information:

Contact

John Hall CABA Research Director 1173 Cyrville Road, Suite 210 Ottawa, ON, K1J 7S6 Phone: 613.686.1814 x 227 [email protected] George Grimes CABA Business Development Manager 1173 Cyrville Road, Suite 210 Ottawa, ON, K1J 7S6 Phone: 613.686.1814 x 226 [email protected]

To find additional CABA Landmark Research go to: http://www.CABA.org/estore.