interest rate risk & investment strategy how to prepare for your next exam & the next rate...

TRANSCRIPT

Interest Rate Risk & Investment StrategyHow to Prepare For Your Next Exam & The Next Rate Environment

Presented by:Jeffrey F. Caughron, Associate PartnerAsset / Liability [email protected]

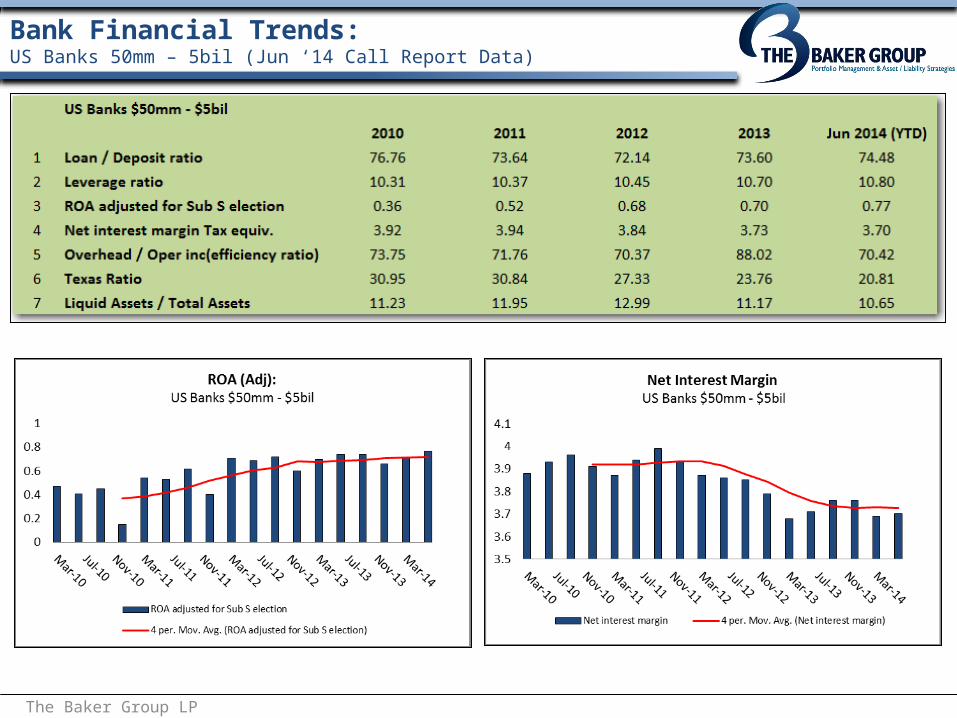

Bank Financial Trends:US Banks 50mm – 5bil (Jun ‘14 Call Report Data)

The Baker Group LP

Fed Funds & 10yr T-Note Yield:1998 - Today

The Baker Group LP

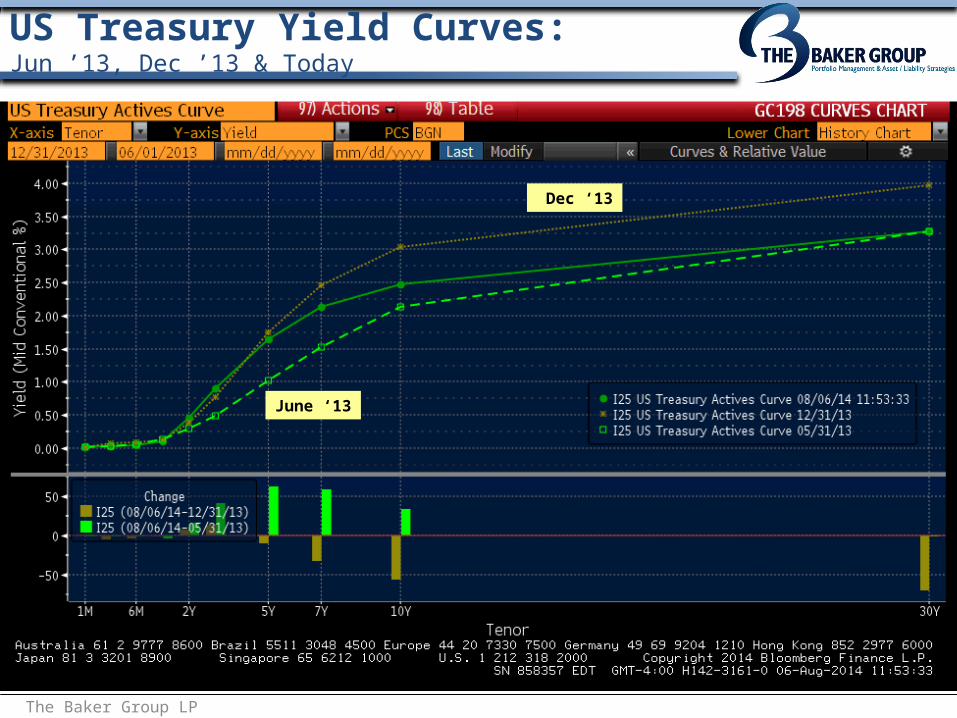

US Treasury Yield Curves:Jun ’13, Dec ’13 & Today

The Baker Group LP

June ‘13

Dec ‘13

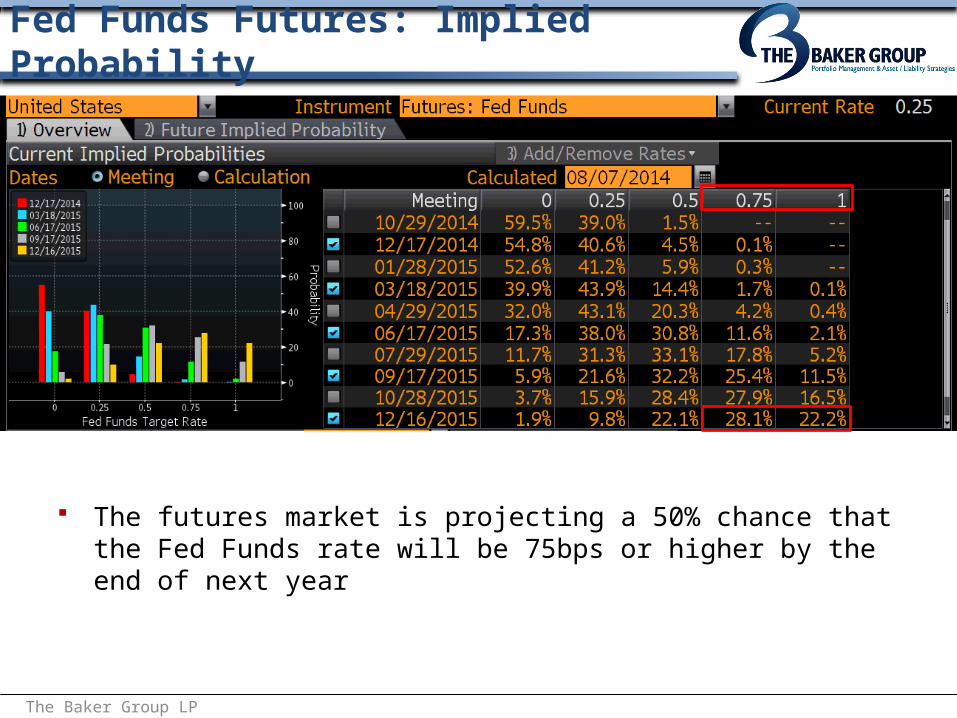

The futures market is projecting a 50% chance that the Fed Funds rate will be 75bps or higher by the end of next year

Fed Funds Futures: Implied Probability

The Baker Group LP

Adjusting for the TED spread, current projections indicate that the fed funds rate will only be around 2.50% even three years from now

Eurodollar Futures: 90-Day Contract

The Baker Group LP

FFIEC Advisory on Interest Rate RiskJanuary 2010

Board and Senior Management responsibilities– Board: understand IRR and be regularly informed about bank exposures…

Director Education.– Management: implement policies, procedures, controls and sufficiently

detailed reporting processes

IRR analysis should assess stress scenarios– Rate shifts of 400 basis points – 12 & 24 month horizon– EVE rate shock to measure longer horizon– Non-parallel yield curve shifts– Capture scenario cash flows and optionality

Model & Process Validation– Model must be validated (software integrity)– Reports should be Back-Tested (methodology & assumptions)– Review of Assumptions (assess and adjust when necessary)– Should be Institution Specific & Should be Stress Tested

Are Earnings & Capital sufficient to support IRR levels?

The Baker Group LP

“Proper measurement of IRR requires regularly assessing the reasonableness of assumptions that underlie an institution’s IRR exposure estimates.”

...FFIEC Advisory on Interest Rate Risk Management – January 2010

Assumptions should be “institution specific” Use regression analysis to determine Sensitivities (betas) Prepayments should be based on historical bank data NMD average life or decay analysis (open/close or balance)

Annual Back-Test and Assumptions Review To assess accuracy (reasonableness) of assumptions Adjustments should be made accordingly

Interest Rate Risk: Key Modeling Assumptions

The Baker Group LP

“Institutions should incorporate “stressed” assumptions for non-maturity deposits in IRR models”

Two Ways to Stress NMD Assumptions Ratchet up pricing betas

(shift sensitivities) and reduce time lags

Simulate a “migrations” of NMD balances into more rate sensitive funding (time deposits or wholesale funding)

Continuing “Hot Topic”: Non-Maturity DepositsMarch 2009 - Today

The Baker Group LP

Mar ’0954.58%

Mar ’1469.45%

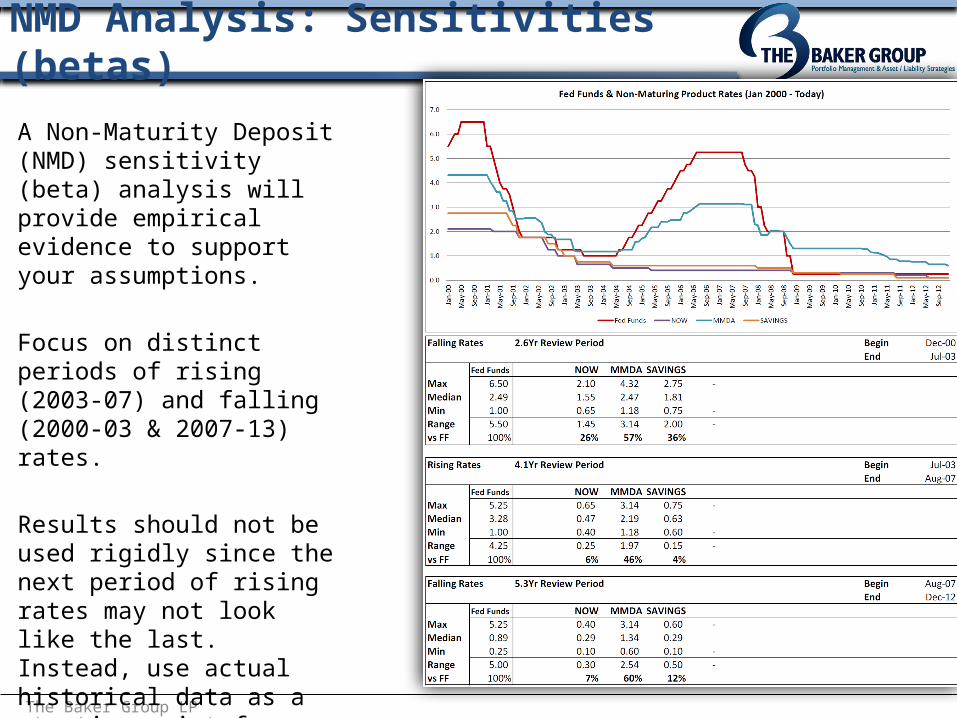

NMD Analysis: Sensitivities (betas)

The Baker Group LP

A Non-Maturity Deposit (NMD) sensitivity (beta) analysis will provide empirical evidence to support your assumptions.

Focus on distinct periods of rising (2003-07) and falling (2000-03 & 2007-13) rates.

Results should not be used rigidly since the next period of rising rates may not look like the last. Instead, use actual historical data as a starting point for determining appropriate sensitivities.

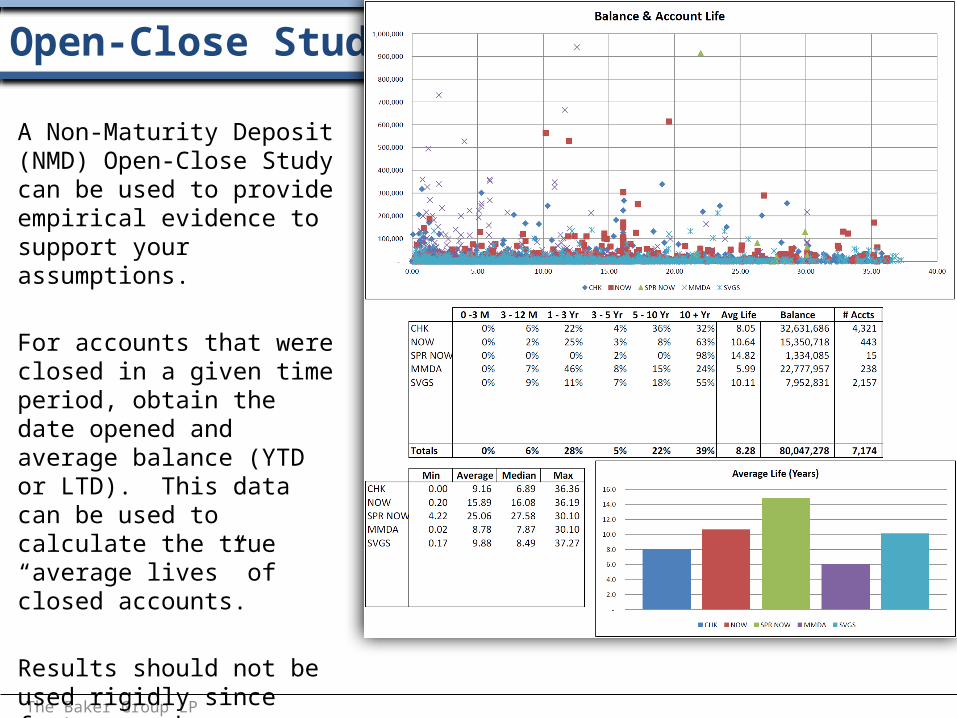

Open-Close Study

The Baker Group LP

A Non-Maturity Deposit (NMD) Open-Close Study can be used to provide empirical evidence to support your assumptions.

For accounts that were closed in a given time period, obtain the date opened and average balance (YTD or LTD). This data can be used to calculate the true “average lives” of closed accounts.

Results should not be used rigidly since factors such as demographics may cause deposits to behave differently in the future.

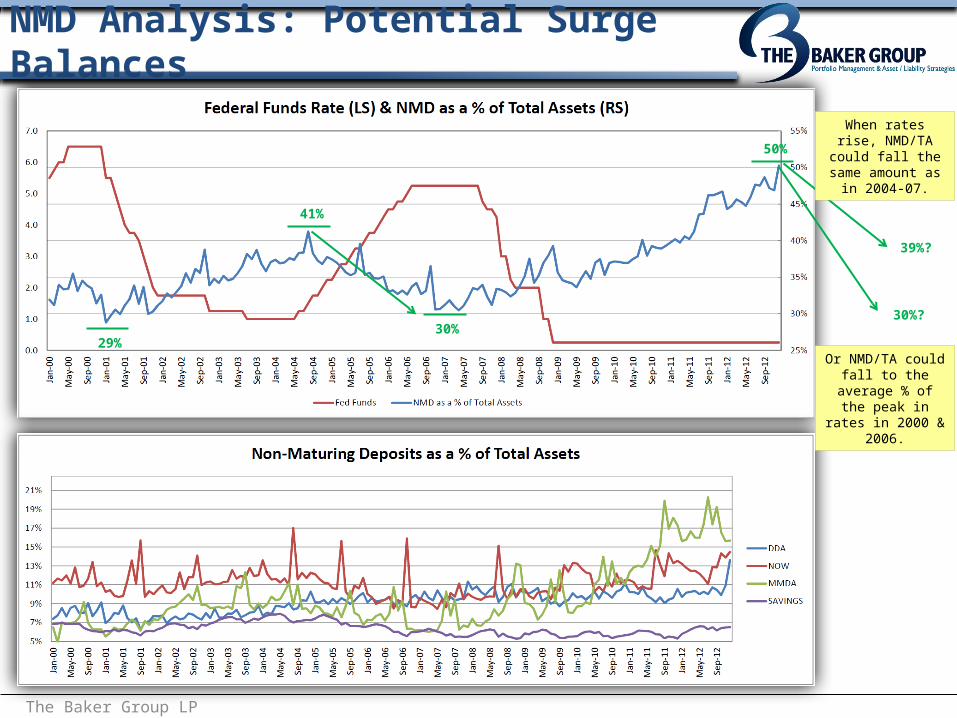

NMD Analysis: Potential Surge Balances

The Baker Group LP

29%30%

41%

50%

39%?

When rates rise, NMD/TA could fall

the same amount as in 2004-07.

Or NMD/TA could fall to the average % of the peak in rates

in 2000 & 2006.

30%?

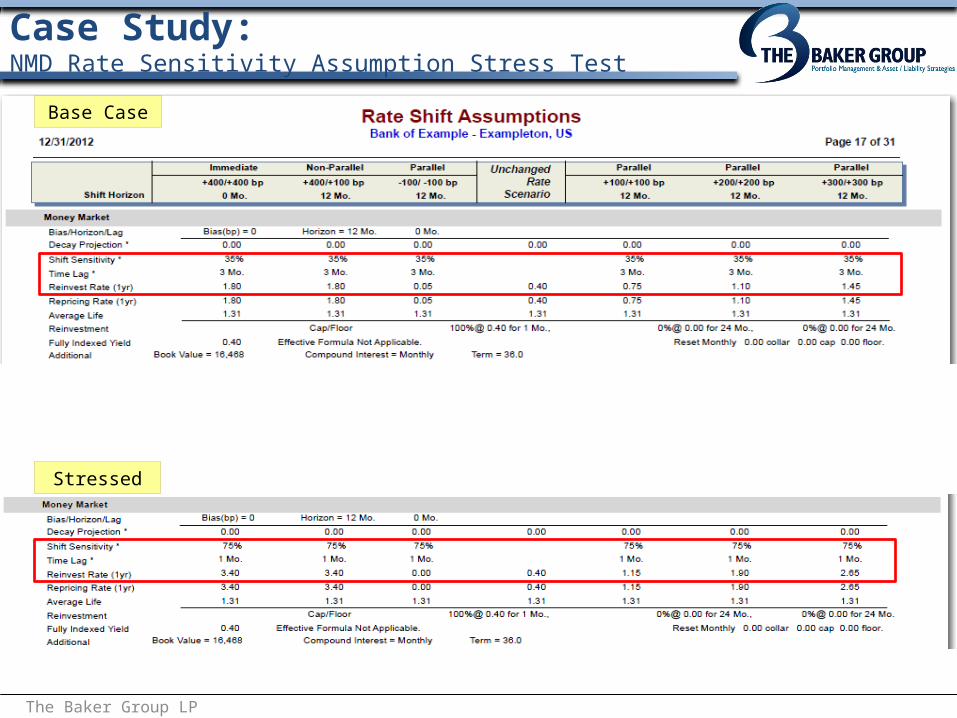

Case Study:NMD Rate Sensitivity Assumption Stress Test

The Baker Group LP

Base Case

Stressed

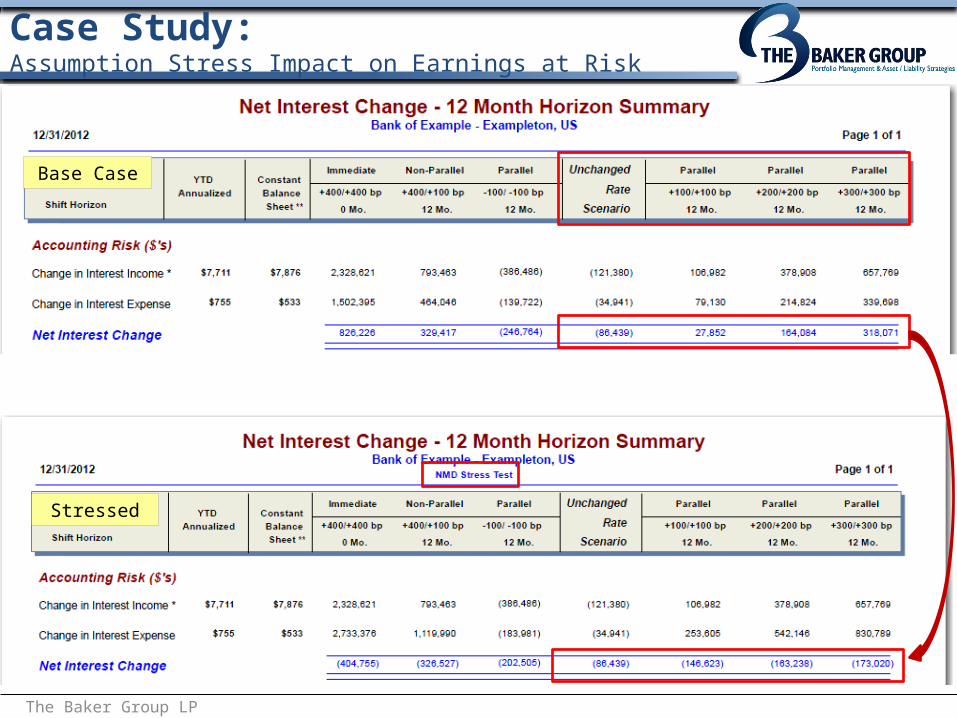

Case Study:Assumption Stress Impact on Earnings at Risk

The Baker Group LP

Base Case

Stressed

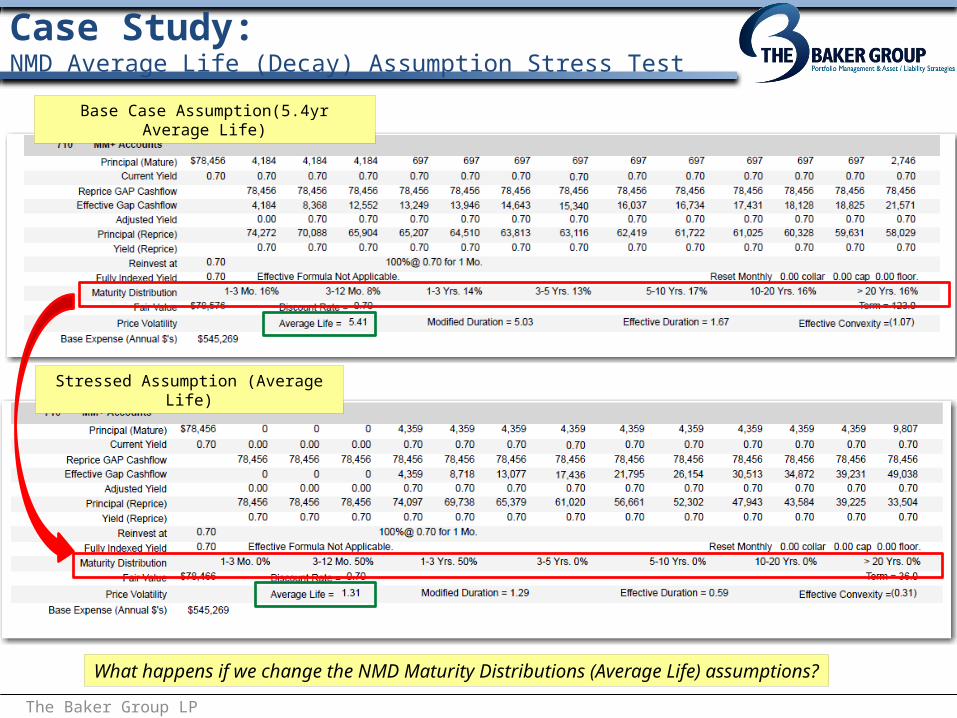

Case Study:NMD Average Life (Decay) Assumption Stress Test

The Baker Group LP

What happens if we change the NMD Maturity Distributions (Average Life) assumptions?

Base Case Assumption(5.4yr Average Life)

Stressed Assumption (Average Life)

Case Study:Assumption Stress Impact on Economic Value of Equity

The Baker Group LP

Base Case (5.4yr Avg Life)

Stressed (1.3yr Avg Life)

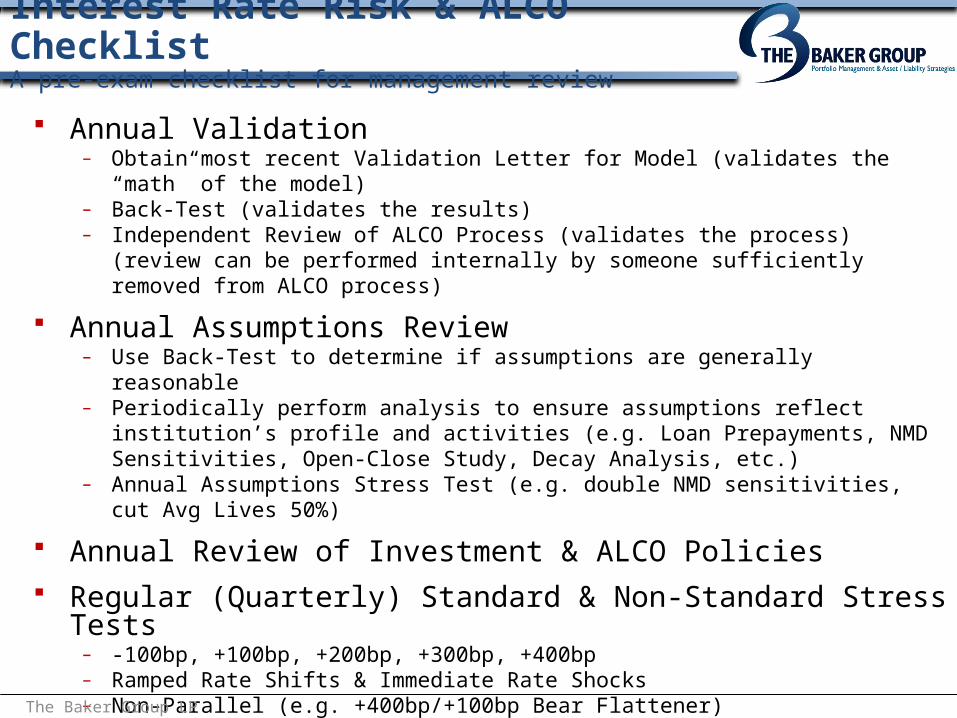

Interest Rate Risk & ALCO ChecklistA pre-exam checklist for management review

Annual Validation– Obtain most recent Validation Letter for Model (validates the “math” of the model)– Back-Test (validates the results)– Independent Review of ALCO Process (validates the process)

(review can be performed internally by someone sufficiently removed from ALCO process)

Annual Assumptions Review– Use Back-Test to determine if assumptions are generally reasonable– Periodically perform analysis to ensure assumptions reflect institution’s profile and activities (e.g.

Loan Prepayments, NMD Sensitivities, Open-Close Study, Decay Analysis, etc.)– Annual Assumptions Stress Test (e.g. double NMD sensitivities, cut Avg Lives 50%)

Annual Review of Investment & ALCO Policies Regular (Quarterly) Standard & Non-Standard Stress Tests

– -100bp, +100bp, +200bp, +300bp, +400bp– Ramped Rate Shifts & Immediate Rate Shocks– Non-Parallel (e.g. +400bp/+100bp Bear Flattener)– 12 & 24 Month Horizons– Earnings at Risk & Economic Value of Equity

The Baker Group LP

“For a number of FDIC-supervised institutions, the potential exists for material securities depreciation relative to capital in a rising interest rate environment.”

“Examiners will continue to consider the amount of unrealized losses in the investment portfolio and the degree to which institutions are exposed to the risks of realizing losses from the depreciated securities when qualitatively assessing capital adequacy and liquidity and assigning examination ratings.”

FDIC FIL on Market Risk

The Baker Group LP

10yr T-Note: Aug ’10 – Today

The Baker Group LP

The question most institutions should be asking themselves is how many bonds did we buy down here versus up here?

Avg Yield = 1.88%

Avg Yield = 2.70%

The Baker Group LP

Keep a keen eye on risk management reports… Are we okay with these numbers/levels when rates rise?

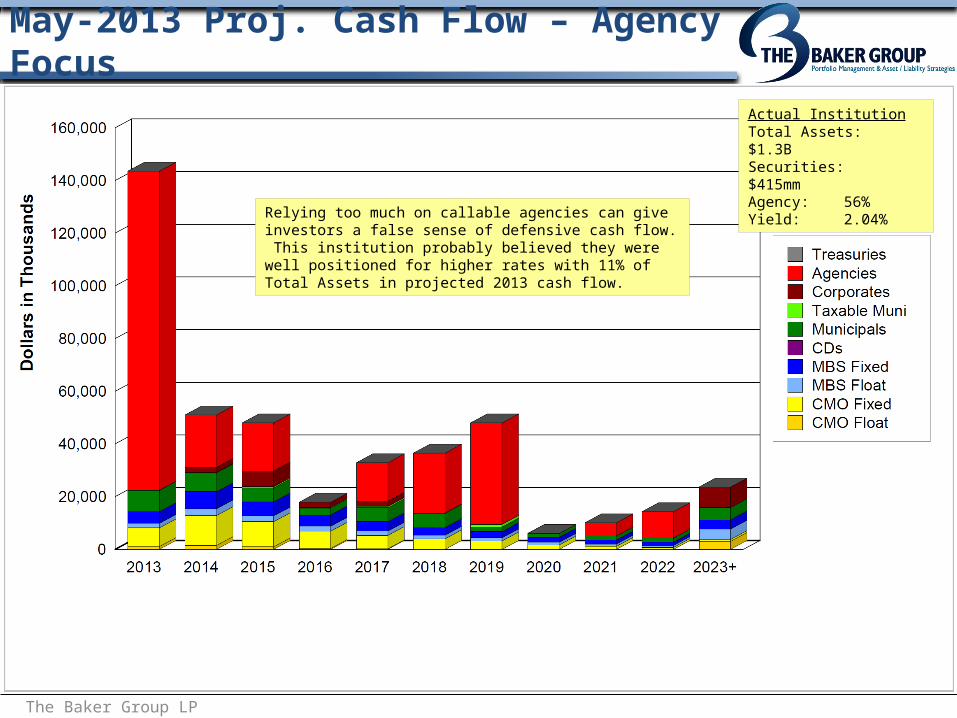

May-2013 Proj. Cash Flow – Agency Focus

The Baker Group LP

Relying too much on callable agencies can give investors a false sense of defensive cash flow. This institution probably believed they were well positioned for higher rates with 11% of Total Assets in projected 2013 cash flow.

Actual InstitutionTotal Assets: $1.3BSecurities: $415mmAgency: 56%Yield: 2.04%

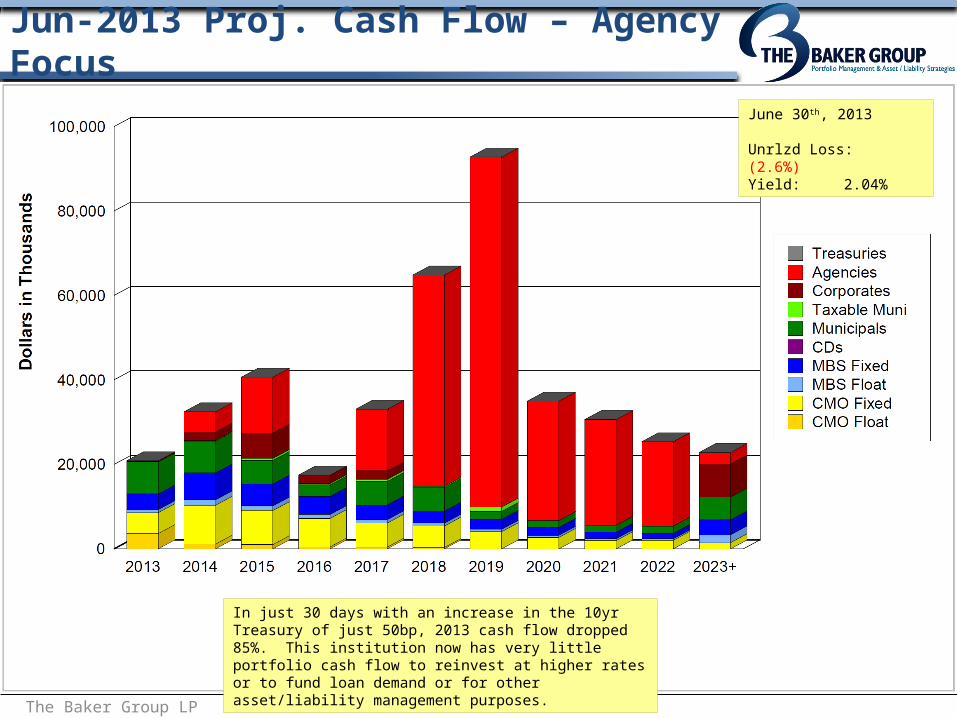

Jun-2013 Proj. Cash Flow – Agency Focus

The Baker Group LP

In just 30 days with an increase in the 10yr Treasury of just 50bp, 2013 cash flow dropped 85%. This institution now has very little portfolio cash flow to reinvest at higher rates or to fund loan demand or for other asset/liability management purposes.

June 30th, 2013

Unrlzd Loss: (2.6%)Yield: 2.04%

May-2013 Proj. Cash Flow – MBS Focus

The Baker Group LP

Actual InstitutionTotal Assets: $666mmSecurities: $142mmMBS/CMO: 80%Yield: 2.70%

This institution relies mainly on MBS/CMO cash flow to provide yield and stable reinvestment opportunities.

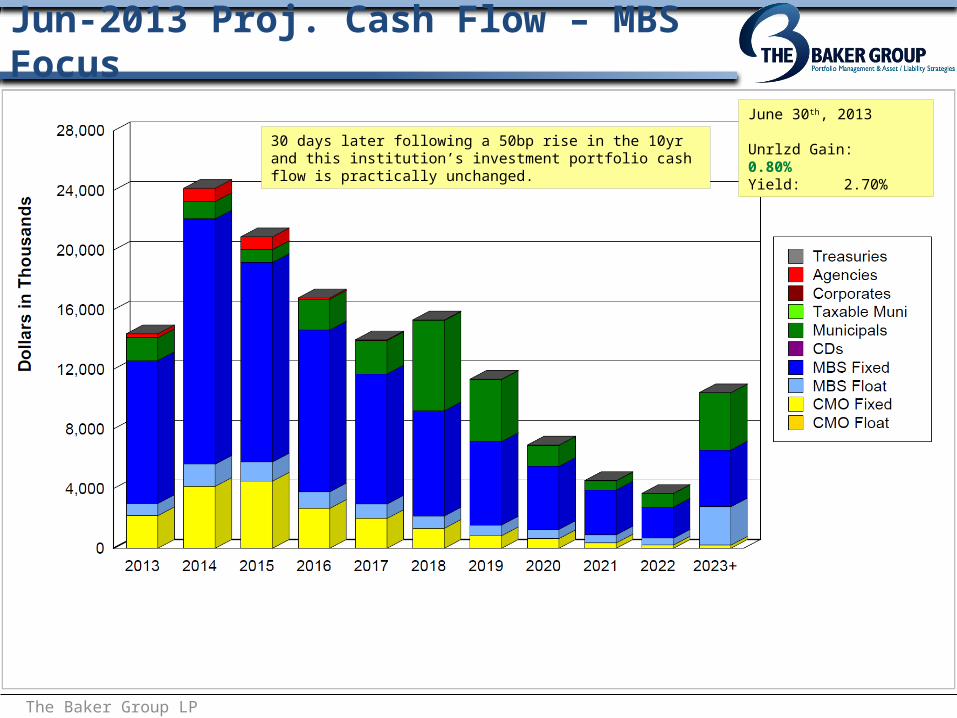

Jun-2013 Proj. Cash Flow – MBS Focus

The Baker Group LP

30 days later following a 50bp rise in the 10yr and this institution’s investment portfolio cash flow is practically unchanged.

June 30th, 2013

Unrlzd Gain: 0.80%Yield: 2.70%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1 2 3 4 5 6 7 8 9 10+

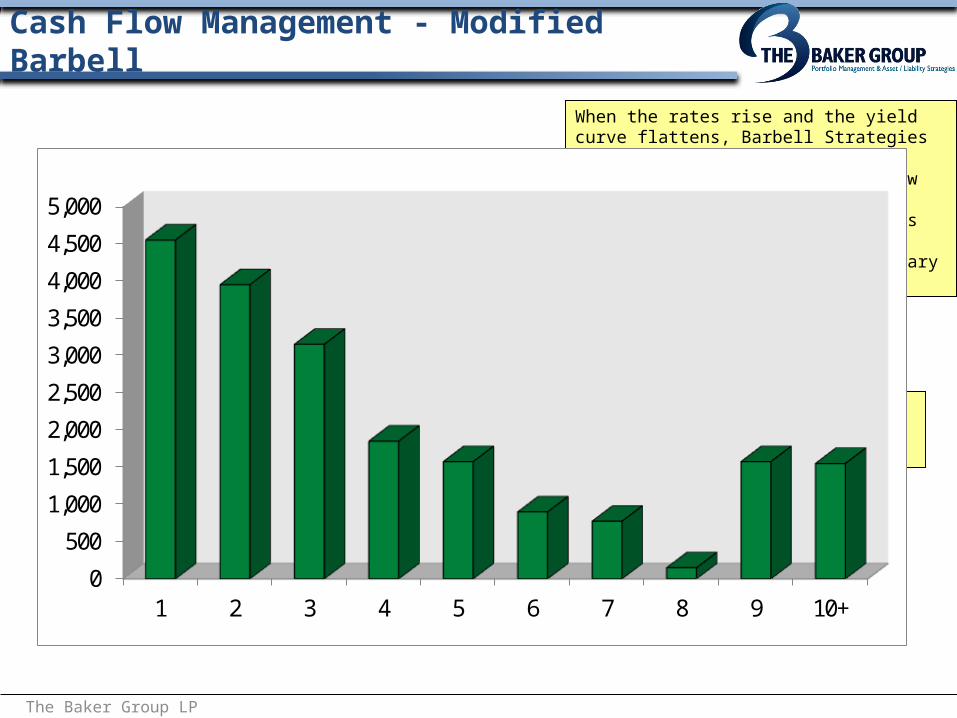

Cash Flow Management - Modified Barbell

The Baker Group LP

Descending Liquidity Ladder of Short Agencies and MBS/CMO Casfhlow

Barbell of Long Tax-Exempt Municipals

When the rates rise and the yield curve flattens, Barbell Strategies often outperform traditional Ladders. Short duration cashflow is defensive and provides reinvestment opportunities (loans or bonds) while longer duration bonds (munis) provide the necessary income.

Bond Sector Yield Spreads

The Baker Group LP

Muni

MBS

Agency

In the last year, spreads have tightened on all sectors. Spreads on MBS and Agencies are near pre-crisis levels (2006-07), while Municipal TE spreads remain elevated.

Comparative Yield Curves:AA BQ Muni, US Agency & US Treasury

The Baker Group LP

Muni net yields exceed treasuries and Agencies on maturities 10yrs and longer

Municipal Yield Curve History

The Baker Group LP

During the last tightening cycle in 2004-06, the longest municipals performed the best while short to intermediate munis depreciated the most. Today, long municipal yields (20yr) are near the levels of 2006-07 while short munis (1yr) remain at record lows. Although counterintuitive, long munis could outperform when “rates” rise.

Mortgage rates rose 130bps last year, but have now drifted 50bps lower.

The Refi Index is down over 75%... near a 6 year low, but prepays have increased modestly for the 4th month in a row.

Home sales and house prices rising again, but remain well below previous peaks. New home sales are at multi-decade lows when adjusted for population.

Base speeds (turnover/mobility) still around 7% CPR, about half of the rate during previous periods of rising rates – beware extension risk! Favor LLB, GNMA, 10-15yrs, higher coupons.

Fed purchases should steadily fall, ending in the fourth quarter. Securitized issuance (and originations) remain very light.

GSE reform moving through Congress but not expected to pass until after election with gradual implementation

MBS yield spreads are very tight… partly due to extremely low volatility Must continue to balance both prepayment and extension risk

MBS Outlook for 3Q14

The Baker Group LP

Supply Still Less Than ½ 2007 Levels

The Baker Group LP

MBA 30yr Fixed Rate: 2004 - Today

The Baker Group LP

From a low of 3.47% in Dec. 2012, mortgage rates jumped to 4.80% last summer and have now fallen back to 4.35.

MBA Refi Index: 2004 - Today

The Baker Group LP

Refinance applications are near the lowest level in six years

Refi Risk @ 4% Rate Less Than 2011

The Baker Group LP

In Dec 2011 when mortgage rates last fell through 4%, 95% of Agency MBS could refi and save 50bp or more.

Today, only 50% can refi and save 50bp.

Higher Coupons Reduce Depreciation Risk

The Baker Group LP

Px drop from May 1st to Sep 5th

15yr 2.0 = 7.5%15yr 2.5 = 5.8%15yr 3.0 = 3.8%15yr 3.5 = 2.7%15yr 4.0 = 1.9%15yr 4.5 = 1.5%

QE3 Announced

When yields rise, higher coupon MBS have historically seen much less price depreciation (and much less overall volatility) than lower coupons.

Taper Tantrum

The Baker Group LP

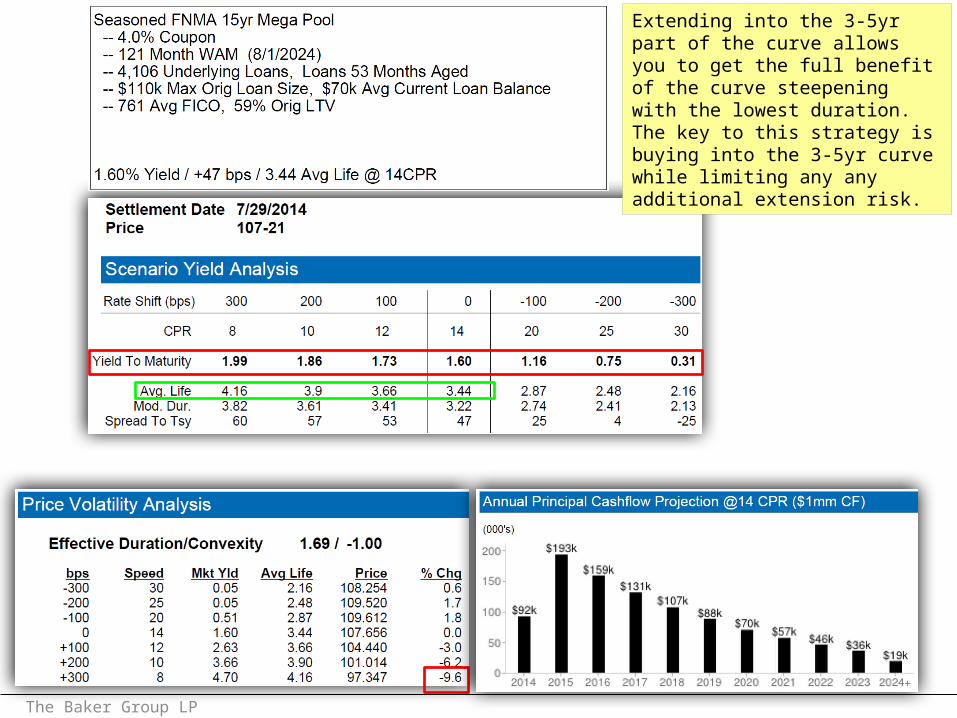

Extending into the 3-5yr part of the curve allows you to get the full benefit of the curve steepening with the lowest duration. The key to this strategy is buying into the 3-5yr curve while limiting any any additional extension risk.

The Baker Group LP

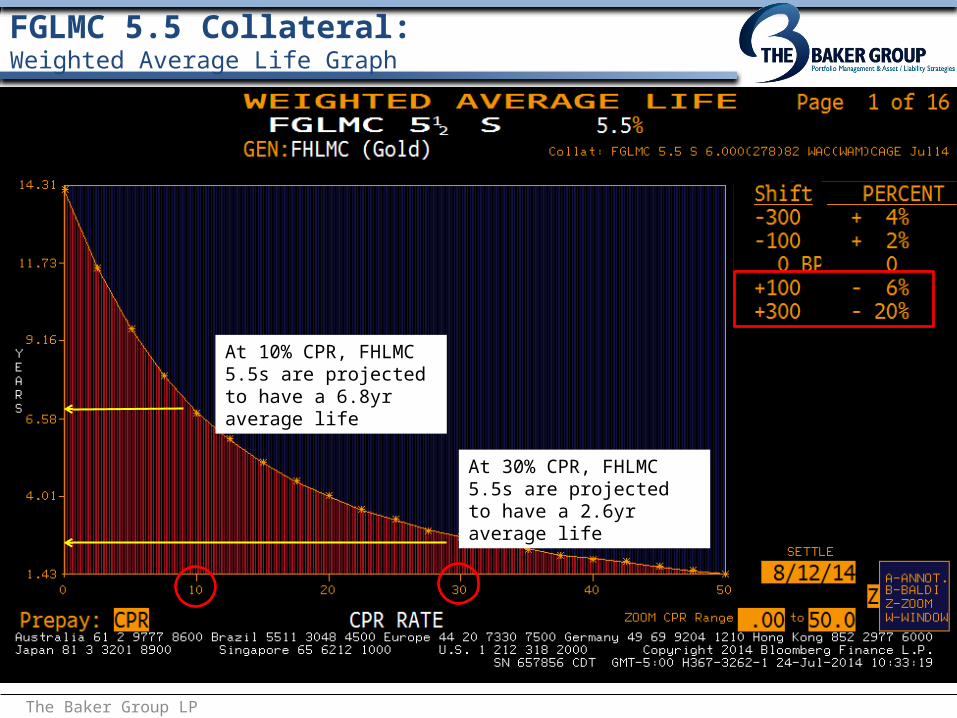

A good PAC CMO can allow us to buy into the 3-5yr part of the curve to pickup yield, minimize extension risk (PAC band) and lower “premium risk” (2.5% coupon off of 5.5% collateral) all while building a short defensive ladder of cashflow.

FGLMC 5.5 Collateral:Weighted Average Life Graph

The Baker Group LP

At 30% CPR, FHLMC 5.5s are projected to have a 2.6yr average life

At 10% CPR, FHLMC 5.5s are projected to have a 6.8yr average life

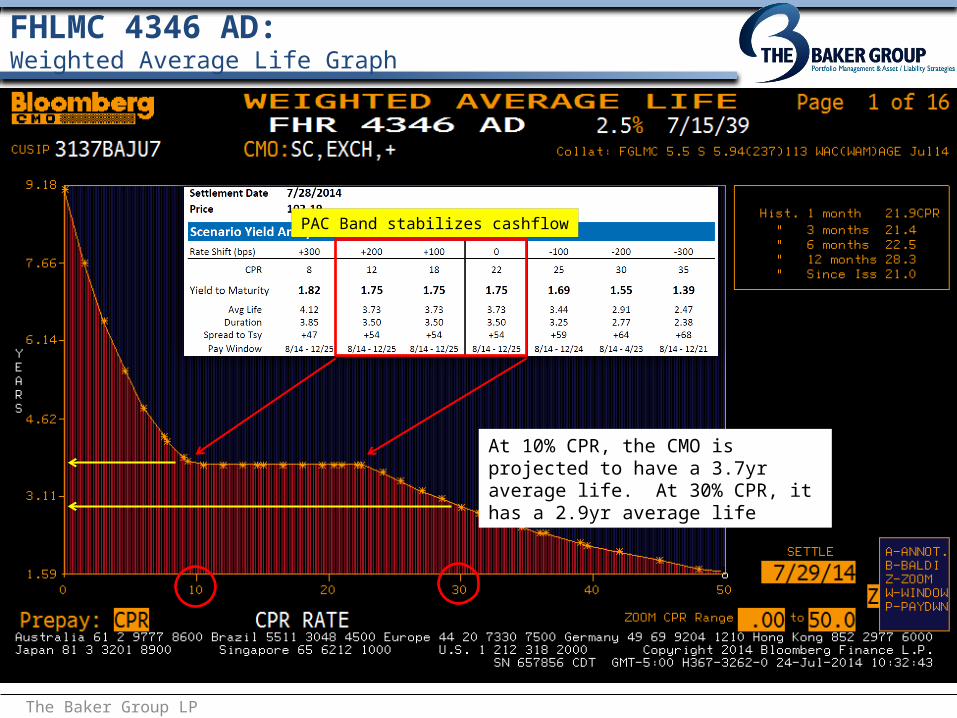

FHLMC 4346 AD:Weighted Average Life Graph

The Baker Group LP

At 10% CPR, the CMO is projected to have a 3.7yr average life. At 30% CPR, it has a 2.9yr average life

PAC Band stabilizes cashflow

Q3 Strategy Summary

Stay on Task with Strategy: Don’t Settle for Riskier Bonds Because Spreads are Tight

– Rise in rates is an opportunity, but only if you have the cashflow to take advantage– Loan yields haven’t moved up, so the bond portfolio often provides the best opportunity to

improve margin

Evaluate Balance Sheet and Portfolio Performance in the Wake of Last Summer’s “Taper Tantrum”

– Was I comfortable with my cash-flow extension?... price-volatility?... EVE?

Review Your ALCO Processes & Reporting Systems– Prepare for you next exam: stress tests, validation, NMD analysis, policies, review risk limits– Assess Depreciation risk relative to capital– NMD Analysis & Stress Testing is a continuing hot button for examiners

Reduce Cashflow Volatility & Fight Duration Extension– Collateral of MBS & Structure of CMOs… eliminate high volatility bonds, stabilize cash flows

Build a Diversified Barbell Of Stable Cash Flow– 1X Call Agy, Short CMOs, Defensive MBS, ARMs & Hybrid ARMs, Long Munis– MBS: focus on 10/15yr, higher coupons, low loan balance, NY/TX, Investor, GNMAs, ARMs

The Baker Group LP