interest rate risk management in krishna grameena...

TRANSCRIPT

xxi

CHAPTER-IV

INTEREST RATE RISK MANAGEMENT IN KRISHNA GRAMEENA BANK

CHAPTER-IV

INTEREST RATE RISK MANAGEMENT IN KRISHNA GRAMEENA BANK

4.1 Introduction

Interest Rate Risk denotes the changes in interest income and

consequent possibility of loss due to changes in the rate of interest. “The

management of interest risk is fundamental to sound practice. If poorly

managed, a bank can experience earnings, liquidity and ultimately capital

adequacy problems. Traditionally, bankers and bank regulators have

focused on the impact on earnings from changes in interest rates. A change

in interest rates affects not only earnings but also the market values of all

fixed rate instruments. Whether these changes manifest themselves

immediately in earnings depends on accounting rules. It merely because,

such changes may be buried in historic cost accounting does not mean that

they do not matter”1.

“Deregulation of interest rates has exposed the banks to the adverse

impact of interest rate risk. Interest rate risk is the risk where unexpected

change in the market interest may impact on the Net Interest Income (NII)

and Net Interest Margin (NIM). Any mismatches in the cash flows (fixed

assets or liabilities) or re-pricing dates (floating assets or liabilities), expose

bank’s Net Interest Income or Net Interest Margin to variations. The

earnings of assets and cost of liabilities are closely related to market interest

rate volatility. Interest rate risk may take the form of gap or mismatch risk,

basis risk, embedded option risk, yield risk, price risk”2.

The interest rate risk can thus be viewed from two different but

complimentary perspectives. One perspective is the traditional accounting

perspective which focuses on the sensitivity of earnings to rate movements.

The other is the economic perspective which focuses on the sensitivity of

99

the market values of all financial instruments, whether they are assets,

liabilities or off-balance sheet contracts. The economic perspective focuses

on the market values of the bank’s capital accounts which is often referred

to as the market value of portfolio equity. The sensitivity of the market

value of portfolio equity to changes in interest rate is a good,

complimentary indicator of the level of interest rate risk inherent in an

institution’s current position and a leading indicator of future earnings

trends.

4.2 Sources of interest Rate Risk3

The following are the various sources and dimensions of interest rate

risk in bank.

1. Repricing Risk

As financial intermediaries banks encounter interest rate risk in

several ways. The primary and most often discussed form of Interest Rate

Risks arise from timing differences in maturity (for fixed rate) and re-

pricing (for floating rate) of bank assets, liabilities and off-balance sheet

positions. While such re-pricing mismatches are fundamental to the

business of banking. They can expose a bank’s income and underlying

economic value to unanticipated fluctuation as interest rates vary.

2. Yield Curve Risk

Re-pricing mismatches can also expose a bank to changes in the

slope and shape on the yield curve. As the economy moves through

business cycles the Yield Curve changes rather more frequently. The Yield

Curve Risk arises when unanticipated shifts of the Yield Curve have

adverse effects on a bank’s income or underlying economic value. For

instance, the underlying economic value of a long position in ten year

government bonds hedged by a short position in five year government

100

bonds could decline sharply if the Yield Curve steepens, even if the position

is hedged against parallel movements in the Yield Curve.

3. Rate Level Risk

This refers to the possibility of changes in the level of interest rate.

The general change in the level of interest rates is a key factor in the choice

of fixed/floating mix, maturity and hedging decisions. During a given

period the interest rate levels are to be restructured either due to the market

conditions or due to regulatory intervention. In the long run, rate level risks

affect decisions regarding the type and the mix of assets/ liabilities to be

maintained and their maturing period. The Reserve Bank of India has been

lowering the statutory Cash Reserve Ratio (CRR) for banks in a phased

manner from 12 per cent since the year 1996 onwards. The decrease in CRR

increases the liquidity of banks which further results in lowering the

PLR/interest rates. For all new deposits the revised interest rates will be

applicable which will result in low marginal cost of funds.

4. Basis Risk

Another important source of interest rate risk commonly referred to

as basis risk which arises from imperfect correlation in the adjustment of

the rates earned and paid on different instruments with otherwise similar

repricing characteristics. Even when assets and liabilities are properly

matched in terms of repricing risk the banks are often exposed to Basis

Risk. When interest rates change these differences can give rise to

unexpected changes in the cash flows and earning Spreads between assets,

liabilities and off-balance sheet instruments of similar maturities or

repricing frequencies.

5. Embedded Option Risk

An additional and increasingly important source of Interest Rate Risk

arises from the options embedded in many bank assets, liabilities and off-

101

balance sheet (OBS) portfolios. Big changes in the level of interest

encourage premature withdrawal of deposits on the liability side or

prepayment of loans on the asset side and it creates a mismatch and gives

rise to repricing risk. When funds are raised by the issue of bonds/securities

it may include call/put options and these two options are exposed to a risk

when the interest rates fluctuate. Bonds with put and call option may be

redeemed before their original maturity as the holder will like to exercise

put option in an increasing interest rate scenario while the issuer will

exercise call option if interest rates have fallen.

6. Volatility Risk

In deciding on the mix of the assets and liabilities the short-term

fluctuations in the pricing policies are to be considered in addition to the

long run implication of the interest rate changes. In a highly volatile market,

the risk will acquire serious proportions as the impact will be felt on the

cash flows and profits. The volatility witnessed in the Indian call money

market in 1994 explains the presence and the impact of the volatility Risk.

While some banks defaulted in maintenance of CRR, many banks borrowed

funds at high rates which had substantially reduced their profits.

4.3 Effects of Interest Rate Risk

Changes in interest rates can have adverse effects both on a bank’s

earnings and its economic values. Such effects of interest rate risk in bank

are shown below.

4.3.1 Earnings Perspective

This is the traditional approach to Interest Rate Risk assessment

taken by many banks. In the earning perspective the focus of analysis is the

impact of changes in interest rates on accrual or reported earning. As

reduced earning or outright losses can threaten the financial stability of an

institution by undermining its capital adequacy and by reducing market

102

confidence. Such earnings perspective focuses attention on net interest

income (i.e., the difference between total interest income and total interest

expense). However, as banks have expended increasingly into activities that

generate fee-based and other non-interest income a broader focus on overall

net income incorporating both interest and non-interest income and

expenses has become more common. The non-interest income arising from

many activities such as, loan servicing and various asset securitizations

programmes can be highly sensitive to market interest rates.

4.3.2 Economic Value Perspectives

Variation in market interest rates can also affect the economic value

of a bank’s assets, liabilities and Off Balance Sheet positions. It will

ultimately impact the Market Value of Equity or the value of Net Worth of

the bank. Thus the sensitivity of a bank’s economic value to fluctuations in

interest rates is particularly important consideration of shareholders,

management and supervisors. The economic value of an instrument

represents an assessment of the present value of its expected net cash flows

discounted to reflect market rates. Since the Economic Value Perspective

considers the potential impact of interest rate changes on the present value

of all future cash flows, it provides a more comprehensive view of the

potential long term effects of changes in interest rates than is offered by the

Earning Perspective.

The Earnings and Economic Value Perspectives focus on how future

changes in interest rates may affect a bank’s financial performance. The

past interest rates may also have an impact on the future performance as

instruments that are not marked to market may already contain embedded

gains or losses due to past rate movements which may be reflected over

time in the bank’s earnings.

103

4.4 Interest Rate Risk Measurement in Bank

Banks should have Interest Rate Risk Measurement system that

capture all material sources of Interest Rate Risk and that assess the effect

of interest rate changes in ways that are consistent with the scope of their

activities. The assumptions underlying the system should be clearly

understood by risk managers and bank management. Mere identification of

the presence of the Interest Rate Risk will not suffice. A system that

quantifies the risk and manages the same should be put in place so that

timely action can be taken. Any delay or lag in the follow-up action may

lead to a change in the dimension of the risk i.e. lead to some other risks

like Credit Risk, Liquidity Risk etc. and make the situation uncontrollable.

Risk Measurement System should assess all material Interest Rate Risk

associated with a bank’s assets, liabilities and OBS positions utilize

generally accepted financial concepts and risk measurement techniques and

have well document assumptions and parameters.

4.5 Techniques of Measuring Interest Rate Risk in Bank

Following are the various techniques or methods of measuring

interest rate risk in banks commonly used.

4.5.1 Maturity Gap Method

The simplest techniques for measuring a bank’s Interest Rate Risk

exposure begin with a maturity / repricing schedule that distributes interest-

sensitive assets, liabilities and OBS positions into ‘time bands’ according to

their maturity (if fixed rate) or time remaining to their next repricing (if

floating rate). This technique which is referred to as Gap is the difference

between Rate Sensitive Assets (RSA) and Rate Sensitive Liabilities (RSL)

that mature or repriced during a particular period of time. The objective of

this method is to stabilize / improve the Net Interest Income in the short run

over discreet periods of time called the Gap periods.

104

The first step in Gap Analysis is to bifurcate the entire asset and

liability portfolio into two distinct categories viz., rate sensitive assets and

rate sensitive liabilities.

All the RSAs and RSLs are grouped into maturity buckets based on

the maturity and the time until the first possible repricing due to change in

the difference between the Interest Rate Sensitive Assets (RSAs) and the

Interest Rate Sensitive Liabilities (RSL).

RSG = RSAs – RSLs

RSG = Rate Sensitive Gap based on maturity

RSAsGap Ratio =

RSLs The bank can use the Gap to maintain / improve its Net Interest

Income for changing interest rates, otherwise adopt a speculative strategy

wherein by altering the Gap effectively depending on the interest rate

forecast the Net Interest Income can be improved. During a selected Gap

period the RSG will be positive when the RSAs are more than the RSLs,

negative when the RSLs are in excess of the RSAs and zero when the RSAs

and RSLs are equal. In order to tackle the rising/falling interest rate

structures the Maturity Gap Method suggests various positions that the

treasurer can take i.e.

i. Maintain a positive Gap when the interest rates are rising.

ii. Maintain a negative Gap when the interest rates are on a decline.

iii. Maintain a zero Gap position for firms to ensure a complete

hedge against any movements in the future interest rates.

The objective of an Asset Liability Management policy will be to

maintain the Net Interest Margin within certain limits by managing the risks

and the bank should first decide the maximum and minimum levels for the

NIM. The success or failure of the Maturity Gap Method depends to a large

105

extent on the accuracy level of the forecasts made regarding the quantum

and the direction of the interest rate changes. The assumption in the Gap

method that the change in the interest rates is immediately affecting all the

RSAs and RSLs by the same quantum is not always true in reality. Another

limitation of the Gap method is that the treasurer may not have the

flexibility in managing the Gap so as to effectively produce the targeted

impact on the net interest income. Simultaneously this model ignores the

time value of money for the cash flows occurring during the Gap period

which is an important factor to be considered.

4.5.2 Rate Adjusted Gap

The Maturity Gap Approach assumes a uniform change in the

interest rates for all assets and liabilities but this may not be the case in

reality. The market perception towards a change in the interest rate may be

different from the actual rise/fall in interest rates. Similarly irrespective of

any amount of fluctuation in the interest rate of the bank the differential

interest rate remains constant because of certain regulations. In the Rate

Adjusted Gap techniques, all the rate sensitive assets and liabilities will be

adjusted by assigning weights based on the estimated change in the rate for

the different assets/liabilities for a given change in interest rates.

4.5.3 Duration Analysis

Duration Analysis concentrates on the price risk and the

reinvestment risk while managing the interest rate exposure. It studies the

effect of rate fluctuation on the market value of the assets and liabilities and

Net Interest Margin (NIM) with the help of duration. Frederick Macaulay

observes that it is possible to blend information contained in the size and

timing of all cash flows into one number called duration. Duration is the

weighted average of time taken (in years) to receive all cash flows, the

weights being the present values of the cash flows. The Rate Sensitive Gap

calculated in Duration Analysis is based on the duration and not the

106

maturity of the assets and liabilities. Duration Gap recognizes that Interest

Rate Risk arises when the timings of cash inflows and outflows differ even

if the assets and liabilities are categorized as rate insensitive as per the

conventional Gap technique. The Duration Gap (DGAP) is computed as the

difference between the composite duration of bank assets and marked down

composite duration of it liabilities.

DGAP = DA – K DL

Where in, DGAP = Duration Gap DA= Duration of Bank Assets KDL=composite Duration Liabilities Here DA is the summation of each asset’s duration weighted by its

share in total assets whereas DGAP is the duration of bank equity. The

impact on market value of equity due to interest rate movements can be

summarized as:

“A bank can immunize the market value of its equity by setting

DGAP = 0. In reality if a bank wants to perfectly hedge its equity value it

has to set its asset duration slightly less than its liability duration to

maintain positive equity.

No. Nature of

DGAP Change in Interest

Rate Change in Market Value of

Equity

1 DA = K DL Increase No Change

2 DA = K DL Decrease No Change

3 DA > K DL Increase Market Value Increases

4 DA > K DL Decrease Market Value Decreases

5 DA < K DL Increase Market Value Decreases

6 DA < K DL Decrease Market Value Increases

The DGAP measure is more scientific and realistic but more

sophisticated and complex in approach at the same time. A basic

107

precondition for the use of this tool as a hedge mechanism is that all the

assets and liabilities of banks have to be positioned as marked to the market.

But for many banks in India very low portions of their balance sheets are

marked to the market. Therefore, the DGAP tool has less applicability in the

Interest Rate Risk immunization of a bank’s balance sheet”.4

4.5.4 Simulation Techniques

Simulation techniques involve detailed assessment of the potential

effects of changes in interest rates on earnings and economic value by

simulating the future path of interest rates and their impact on cash flows. In

static simulations, the cash flows arising solely from the bank’s current on

and off balance sheet positions are assessed and in a dynamic simulation

approach, the simulation builds in more detailed assumptions about the

future course of interest rates and expected changes in the bank’s business

activity over that time many banks (especially those using complex

financial instruments or otherwise having complex risk profiles) employ

more sophisticated Interest Rate Risk measurement system than those based

on simple maturity repricing schedules.

4.5.5 Value-at-Risk Approach

Value-at-Risk methodology is a risk control method which

statistically predicts the maximum potential loss a bank’s portfolio could

experience over a specific holding period at a certain probability. Using this

method it is possible to measure the amount of risk for each produce with a

common yardstick. The Value-at-Risk methodology takes into

consideration the sensitivity of the current position’s marginal move in the

risk factors like interest rates, foreign exchange rates etc., the standard

deviation of the historical volatility of the risk factors and the correlation

between the risk factors. The VaR is used to estimate the volatility of Net

Interest Income (NII) and net portfolio with a desired level of confidence.

The Value-at-Risk concept has been recommended by the Basle Committee

108

as a standard measure of risk. The Basle Committee on banking supervision

has recommended that Value-at-Risk may be calculated as on 99 per cent

confidence interval basis.

The variety of the techniques range from calculation that rely simply

on maturity and re-pricing charts, duration Gap analysis, static simulations

based on current on balance sheet and off balance sheet positions, highly

sophisticated dynamic modeling techniques that incorporate assumptions

about the behaviour of the bank and its customers in response to changes in

the interest rate environment. All those methods vary in their ability to

capture the different forms of interest rate exposure. It is needless to

mention that the usefulness of each technique depends on the validity of the

underlying assumption and the accuracy of the basic methodologies used to

model Interest Rate Risk exposure.

4.6 RBI Guidelines with regards to Interest Rate Risk Management

in bank

The RBI issued guidelines in the year 1999 to tackle the problem of

short-term liquidity. As per the Prudential Norms set by the RBI every bank

has to ensure that the net outgo of funds during the coming 28 days should

not exceed 20 per cent of the total outflow of cash. The Reserve Bank has

also adopted Maturity Ladder for a comparative study of future cash

inflows and cash outflows and all banks have been directed to prepare

Liquidity Statements on the pattern of Maturity Ladder at quarterly intervals

starting from the June 1999. In constructing the Maturity Ladder, a bank has

to allocate each cash inflow or outflow to a given calendar date from a

starting point. A maturing asset will result in cash inflow while a maturing

liability will amounts to cash outflow.

For constructing the Maturity Ladder classification of available data

is necessary. For example a five-year deposit with only three months left to

109

maturity will be classified as cash outflow likely to take place in three

months time. Thus maturity profile could be used for measuring the future

cash flows of banks in different time buckets.

“The time buckets, given the Statutory Reserve Cycle of the days, have

been distributed as follows.

(i) 1 to 14 days

(ii) 15 to 28 days

(iii) 29 days and above up to 3 months

(iv) Over 3 months and up to 6 months

(v) Over 6 months and up to 1 year

(vi) Over 1 year and up to 3 years

(vii) Over 3 years and up to 5 years

(viii) Over 5 years”.5

Within each time bucket there could be mismatches depending on

cash inflows and outflows. While the mismatches up to one year would be

relevant since these provide early warning signals of impending liquidity

problems. The main focus should be on the short term mismatches viz. 1-14

days and 15-28 days. Banks are expected to monitor their cumulative

mismatches across all time buckets by establishing internal prudential limits

with the approval of the Board/Management Committee. The mismatches

(negative Gap) during 1-14 days and 15-28 days in normal course may not

exceed 20 per cent of the cash outflows in each time bucket. If a bank in

view of its current asset-liability profile and the consequential structural

mismatches needs higher tolerance level it could operate with higher limit

sanctioned by its Board/Management Committee giving specific reasons on

the need for such higher limit. The discretion to allow a higher level was

intended for a temporary period i.e. till 31 March, 2000. Indian banks with

large branch network can afford to have larger tolerance levels in

mismatches in the long term if their term deposit base is quite high. While

110

determining the tolerance level the banks may take into account all relevant

factors based on their asset-liability base, nature of business, future strategy

etc.

In case the negative Gap exceeds the prudential limit of 20 per cent

outflows (1-14 days and 15-28 days), the bank may show by way of

footnote as to how it proposes to finance the Gap to bring the mismatch

within the prescribed limits. The Gap can be financed from market

borrowings, bills Rediscounting, repay and deployment of foreign currency

resources after conversion into rupees etc.

In the context of poor MIS, slow pace of computerization in banks

and the absence of total deregulation, the Reserve Bank has decided to

implement the simplest method of traditional Gap Analysis as a suitable

method to measure the Interest Rate Risk. It is the intention of RBI to move

over to the modern techniques of Interest Rate Risk measurement like

Duration Gap Analysis, Simulation and Value at Risk over time when banks

acquire sufficient expertise and sophistication in acquiring and handling

MIS.

“The Gap or mismatch risk can be measured by calculating Gaps

over different time intervals. Gap Analysis measures mismatches between

rate sensitive liabilities and rate sensitive assets. An asset or liability is

normally classified as rate sensitive if,

(i) Within the time interval under consideration there is cash flow.

(ii) The interest rate resets/reprices contractually during the interval.

(iii) RBI changes the interest rates (interest rates on Savings Bank

Deposits, DRI Advances, Export Credit, Refinance, and CRR

balance etc.) in cases where interest rates are administered.

(iv) It is contractually pre-payable or withdrawable before the stated

maturities”6.

111

The Gap Report should be generated by grouping rate sensitive

liabilities, assets and off-balance sheet positions into time buckets according

to residual maturity or next repricing period whichever is earlier. For

determining rate sensitivity, all investments, advances, deposits,

borrowings, purchased funds etc. that mature / reprice within a specified

time frame are deemed interest rate sensitive. Any principle repayment of

loan including final principle payment and interim instalments are also rate

sensitive if the bank expects to receive it within the time horizon. Generally,

certain assets and liabilities that receive / pay rates with a reference rate are

repriced at pre-determined intervals and are rate sensitive at the time of

repricing. While the interest rates on term deposits are fixed during their

currency, the advances portfolio of the banking system is basically floating

and the interest rates on advances could be repriced any number of

occasions corresponding to the changes in PLR.

Each bank should set prudential limits on individual Gaps with the

approval of the Board/Management Committee. The prudential limits

should have a bearing on the total assets, earning assets or equity. The

banks may workout earnings at risk (EaR) or Net Interest Margin (NIM)

based on their views on interest rate movements and fixes a prudential level

with the approval of the Board/Management Committee.

4.7 Maturity Gap analysis Technique in Krishna Grameena Bank

There are various techniques of assessing interest rate risk

management in bank like Maturity Gap analysis technique, Rate adjusted

Gap, Duration Analysis, Simulation Technique, Value at Risk (VaR) and

Derivatives etc. The Maturity Gap analysis technique of asset liability

management is used to assess Interest Rate Risk in Krishna Grameena Bank

for the period of seven accounting years from 2005-06 to 2011-12 and also

efforts are made to study the effect of changes in interest rates on Net

112

Interest Income (NII) and on Net Interest Margin (NIM) and on Net Income

of Bank.

Gap analysis is a technique of asset-liability management that can be

used to assess interest rate risk or liquidity risk. It measures at a given date

the gaps between rate sensitive liabilities (RSL) and rate sensitive assets

(RSA) (including off-balance sheet positions) by grouping them into time

buckets according to residual maturity or next repricing period, whichever

is earlier. An asset or liability is treated as rate sensitive if

i) Within the time bucket under considerations, there is a cash flow;

ii) The interest rate resets/ re-prices contractually during the time

buckets;

iii) Administered rates are changed and

iv) It is contractually pre-payable or withdrawal allowed before

contracted maturities.

This gap is used as a measure of interest rate sensitivity. A bank

benefits from a positive gap i.e., RSA>RSL, if interest rate rises. Similarly,

a negative gap (RSA<RSL) is advantageous during the period of falling

interest rate. The interest rate risk is minimized if the gap is near zero.

4.8 Determination of Rate Sensitive Assets and Rate Sensitive

Liabilities

Rate sensitive assets and liabilities are arrived by grouping only

those assets and liabilities which come within the time bucket 1-14 days to

6 months-1 year. There should be constant resets and reprices of interest

rates during the time buckets. There should be contractual prepayment and

withdrawal. The total of assets and liabilities which satisfy the above

conditions are taken as rate sensitive assets and rate sensitive liabilities.

Thus the gap is given by

113

Gap = Rate Sensitive Assets- Rate Sensitive Liabilities

Rate Sensitive Asset Gap Ratio =

Rate Sensitive Liabilities

After the computation of rate sensitive assets and rate sensitive

liabilities uniform rate of interest has been assigned for rate sensitive assets

and fixed rate assets. This has been followed for rate sensitive liabilities and

fixed rate liabilities.

The interest rate for assets is to be calculated by using the following

formula,

Interest earned Interest rate for assets

= Total advances + Total investments + Total Foreign currency assets – Non-earning assets

x 100

The interest rate for assets has been arrived at by taking into account

total advances, total investments, total foreign currency assets and non

earning assets.

The interest rate for liabilities is to be calculated by using the

following formula:

Interest expended Interest rate for liabilities

= Total deposits + Total borrowings + Total foreign currency liabilities

x 100

The interest rate for liabilities has been arrived at by taking into

account the interest expended, total deposits, total borrowings and total

foreign currency liabilities.

4.9 Computation of mix

The portfolio mix for assets and liabilities have been computed. The

mix for rate sensitive assets, fixed rate assets, non earning assets, rate

114

sensitive liabilities, fixed rate liabilities and non interest bearing liabilities

have been calculated to suggest the appropriate mix for assets and

liabilities.

Volume of rate sensitive assets Mix of rate sensitive assets =

Total/ Average of assets x 100

Volume of fixed rate assetsMix of fixed rate assets =

Total/ Average of assets x 100

Volume of non-earning assets Mix of non-earning assets =

Total/ Average of assets x 100

Volume of rate sensitive liabilities Mix rate of sensitive liabilities =

Total/ Average of liabilities x 100

Volume of fixed rate liabilities Mix of fixed rate liabilities =

Total/ Average of liabilities x 100

Volume of non-interest bearing liabilities Mix of non-interest bearing

liabilities =

Total/ Average of assets

x100

4.10 Computation of performance measures

The Net Interest Income (NII), Net Interest Margin (NIM), Net

Income (NI) and gap are the measures used to gauge the performance of

Bank with relation to the asset liability management.

4.10.1 Net Interest Income

Net Interest Income = (Interest rate of RSA x Volume of RSA) +

(Interest rate of FRA x Volume of FRA) – (Interest rate of RSL x Volume

of RSL) – (Interest rate of FRL x Volume of FRL).

115

4.10.2 Net Interest Margin

“This ratio identifies core earning capacity of the bank and its

interest differential income as a percentage of average total assets. An

alternative calculation prescribes earning assets as the denominator based

on the presumption that the interest margin applies to earning assets

engaged in providing interest income. However, both non-earning assets

and non-interest bearing liabilities have a powerful impact on the net

interest margin. This is because non earning assets are a drag on income,

particularly if they are financed with interest bearing liabilities, while non

interest bearing deposits boost earnings, particularly if they are financing

high interest bearing assets. The Standard ratio prescribed by the World

Bank is 4.5%”.7

It can be calculated by using the following formula.

Net interest income Net Interest Margin =

Total performing assetsx 100

4.10.3 Net Income

Net Income is the difference between the net interest income and

provisions and contingencies. It can be calculated by using the following

formula.

Net Income = Net interest income – Provisions and contingencies

The various formulas suggested above are used for drawing

conclusions about the interest rate risk management in Krishna Grameena

Bank. The results are calculated for KGB by using all the three parameters

for seven years from 2005-06 to 2011-12.

116

4.11 Calculation of Rate Sensitive Asset and Rate Sensitive Liability,

Gap, Net Interest Income, Net Interest Margin and Net Income

in Krishna Grameena Bank

Table-4.1: Residual Maturity pattern of assets and

liabilities for the year 2005-06

Rs. in Lakhs

Maturity patterns

Deposits Advances Investments BorrowingsForeign

currency assets

Foreign currency liability

1 to 180 days

19932.15 19135.92 -- 454.59 -- --

181 to 365 days

5537.58 10525.24 250.00 10656.78 -- --

1 to 3 years

12575.36 10976.35 436.35 1019.76 -- --

3 to 5 years

4625.92 7564.46 9617.67 788.85 -- --

Over 5 years

3612.54 5515.36 1457.49 6233.78 -- --

Source: Annual Report of KGB for the year 2005-06.

Table-4.2: Break up of assets and liabilities based on

Maturity Pattern for the year 2005-06

Items Volume (Rs. In lakhs)

Interest Rate Mix (%)

RSA 29911.16 9.67 38.93

FRA 35567.68 9.67 46.30

NEA 11340.25 -- 14.77

Total/ average 76819.09 6.44 100.00

RSL 36581.10 4.13 47.61

FRL 28856.21 4.13 37.56

NIBL 11381.78 -- 14.83

Total/ Average 76819.09 2.75 100.00

Figures computed from Annual Report of KGB for the year 2005-06

117

The above table 4.2 shows the break up of assets and liabilities in the

year 2005-06. The table suggests that the RSA and RSL, which are Rate

Sensitive Assets and Rate Sensitive Liabilities of balance sheet positions

have been classified according to the residual maturity. Here the entire

volume of Rate Sensitive Assets, Rate Sensitive Liabilities, Fixed Rate

Assets, Fixed Rate Liabilities, non-earning assets and non-interest bearing

liabilities has been calculated and the total amount comes around

Rs.76819.09 lakhs.

The interest rates for RSA, FRA, RSL and FRL shows that the total

average of interest rate for assets comes around 6.44 and the average of

interest rate for liabilities comes around 2.75. The mix for RSA, FRA,

NEA, RSL, FRL and NIBL has been computed. The mix for assets i.e.,

RSA comes around 38.93, for FRA it is 46.30, for NEA it is 14.77. The

mix for liabilities i.e., RSL comes around 47.61, for FRL it is 37.56 and for

NIBL it is 14.83 %. It has been confirmed from the table 4.3 which shows

that there is a negative gap i.e., RSA < RSL. This trend is advantageous

during the period of falling interest rates. The interest rate risk is

minimized if the gap is nearing to zero.

Table-4.3: Summary of Performance Measures for the year 2005-06

Rs. in Lakhs

Change in interest rate

Performance Measure Initial

Position 2% decrease

in interest rate

2% increase in interest

rate

GAP (RSA-RSL) -6669.94 -6669.94 -6669.94

Net interest income 3629.24 3762.64 3495.84

Net interest margin (%) 5.79 6.00 5.57

Net income 3078.55 3211.95 2945.154

Figures computed from Annual Report of KGB for the year 2005-06.

118

The above table shows summary of performance measures can be

arrived at by the calculation of net interest income, net interest margin

(NIM) and net income (NI). It can be inferred that during the year 2005-06

the gap is negative and it comes around Rs. 6669.94 lakhs. The interest

income is Rs 3629.24 Lakhs. The net interest margin is 5.79 % which is

more than the standard norm prescribed by the World Bank and the net

income comes around Rs 3078.55 lakhs. The above data is shown with the

help of figure 4.1.

Figure-4.1: Summary of Performance Measures for the year 2005-06

0

500

1000

1500

2000

2500

3000

3500

4000

Rs.

in L

akh

s

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

When interest rate negative shock of 2% was applied, it increased the

NII to Rs.3762.64 lakhs, NIM to 6%, and NI to Rs.3211.95 lakhs.

However, when interest rate positive shock of 2% was applied, it reduced

the NII to Rs.3495.84 lakhs, NIM to 5.57% and NI to Rs.2945.154 lakhs. It

is concluded that decrease of 2% in interest rate has increased the net

interest margin by 0.21% over the initial position. It is because of the

negative Gap.

119

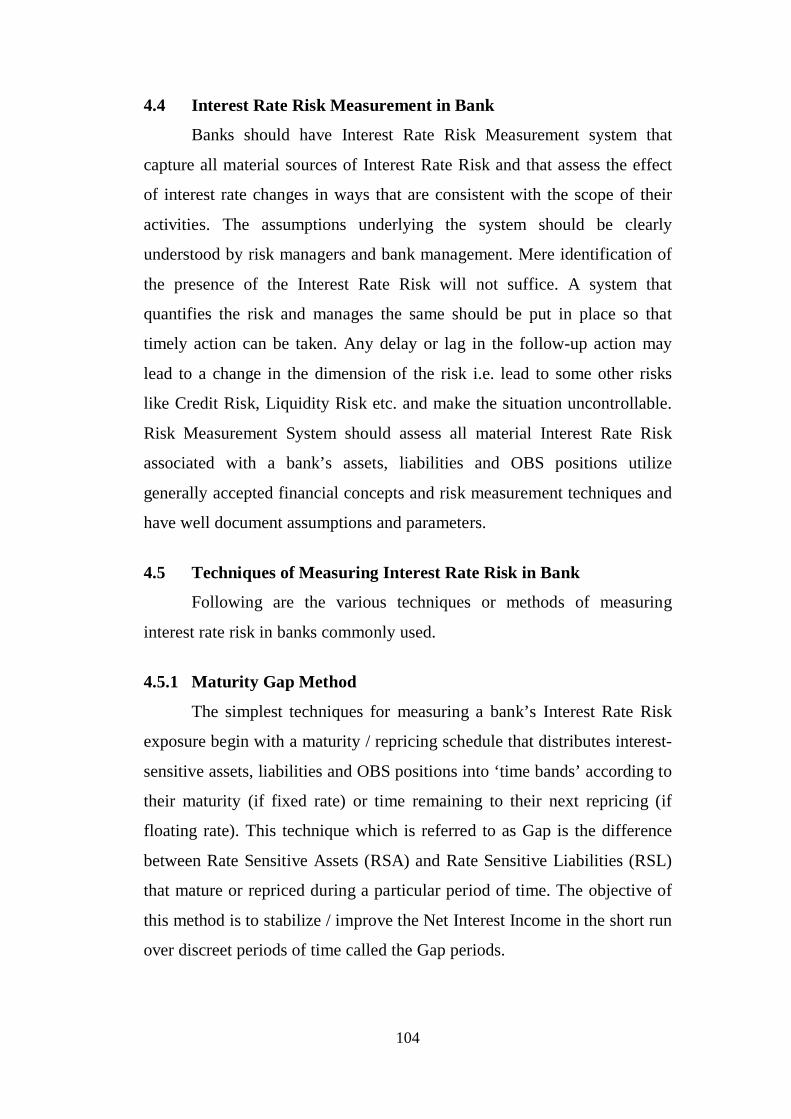

Table-4.4: Period-wise Residual Maturity of assets and

liabilities for the year 2005-06

Rs. in Lakhs

Items 1 to 180

days 181 to 365

days

Advances 19135.92 10525.24

Investments -- 250.00

Foreign currency assets -- --

Deposits 19932.15 5537.58

Borrowings 454.09 10656.78

Foreign currency liabilities -- --

GAP -1250.32 -5419.12 Source: Annual Report of KGB for the year 2005-06.

It is evident from the above table that the residual maturity of the rate

sensitive assets and rate sensitive liabilities from 1 day to 180 days and 181

days to 365 days for the year 2005-06. It is revealed that the time buckets

of 1-180 days, 181-365 days are vulnerable paving way to negative gaps of

high volume.

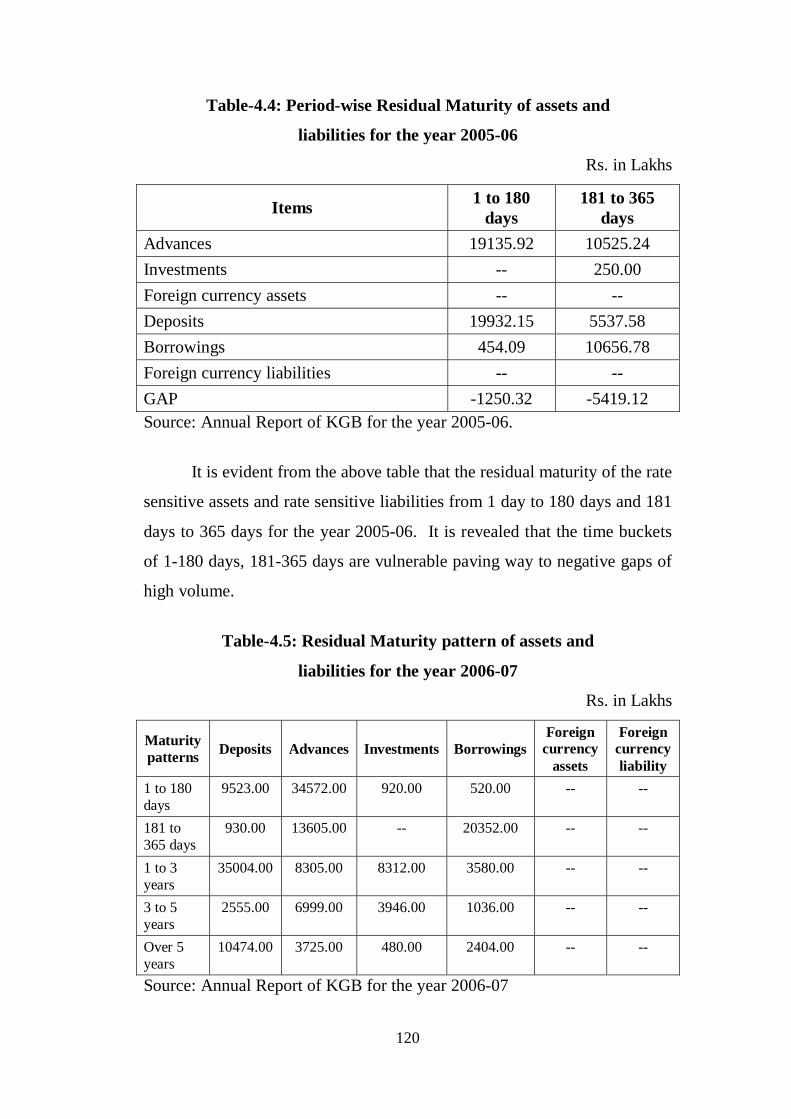

Table-4.5: Residual Maturity pattern of assets and

liabilities for the year 2006-07

Rs. in Lakhs

Maturity patterns

Deposits Advances Investments BorrowingsForeign

currency assets

Foreign currency liability

1 to 180 days

9523.00 34572.00 920.00 520.00 -- --

181 to 365 days

930.00 13605.00 -- 20352.00 -- --

1 to 3 years

35004.00 8305.00 8312.00 3580.00 -- --

3 to 5 years

2555.00 6999.00 3946.00 1036.00 -- --

Over 5 years

10474.00 3725.00 480.00 2404.00 -- --

Source: Annual Report of KGB for the year 2006-07

120

Table-4.6: Break up of assets and liabilities based on

residual maturity pattern for the year 2006-07

Items Volume (Rs. In lakhs)

Interest Rate Mix (%)

RSA 49097.00 9.81 48.91

FRA 31767.00 9.81 31.64

NEA 19516.77 -- 19.45

Total/ average 100380.77 6.54 100.00

RSL 31325.00 3.95 31.20

FRL 55053.00 3.95 54.84

NIBL 14002.77 -- 13.96

Total/ Average 100380.77 2.63 100.00

Source: Figures computed from Annual Report of KGB 2006-07

The above table shows the break-up of assets and liabilities in the

year 2006-07. It suggests that the RSA and RSL have been classified

according to the residual maturity. Here, the entire volume of rate sensitive

assets, rate sensitive liabilities, fixed rate assets, fixed rate liabilities have

been calculated and the total comes around Rs.100380.77 lakhs.

The interest rates for RSA, FRA, RSL and FRL have also been

computed. The total average of interest rates for assets comes around 6.54

and the average of interest rate for liabilities comes around 2.63.

The portfolio mix computation suggests that the asset mix i.e., RSA

comes around 49 and for FRA it is around 32, for NEA around 19.

Similarly, the liability mix i.e., RSL, comes around 31, for FRL around 55

and for NIBL comes around 14.

The table 4.7 shows that there is a positive gap i.e., RSA > RSL.

This trend is advantageous during the period of increasing interest rates.

121

Table-4.7: Summary of Performance Measures for the year 2006-07

Rs. in Lakhs

Change in interest rate

Performance Measure Initial

Position 2% decrease

in interest rate

2% increase in interest

rate

GAP (RSA-RSL) 17772 17772 17772

Net interest income 4520.82 4166.86 4877.74

Net interest margin (%) 5.81 5.36 6.27

Net income 3718.53 3364.57 4075.45

Figures computed from Annual Report of KGB for the year 2006-07.

The performance measures such as Net Interest Income (NII), Net

Interest Margin (NIM) and Net Income (NI) have been calculated. It can be

inferred that in the year 2006-07 the GAP i.e., RSA-RSL is positive and it

comes to Rs.17772 lakhs. The net interest income is Rs.4520.82. lakhs, the

net interest margin is 5.81 which is also more than the standard norm

prescribed by the World Bank and the net income comes to Rs.3718.53

lakhs.

The summary of performance measure for the year 2006-07 is also

shows with the help of figure 4.2.

When interest rate negative shock of 2% was applied, it reduced the

NII to Rs.4166.86 lakhs, NIM to 5.36% and NII to Rs.3364.57 lakhs,

whereas, when interest rate positive shock of 2% was applied, it increased

NII to Rs.4877.74, NIM to 6.27% and NI to Rs.4075.45 lakhs. When there

is a positive gap (i.e., RSA > RSL) this trend is more advantageous during

the period of increasing interest rates.

122

Figure-4.2: Summary of Performance Measures for the year 2006-07

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Rs.

in L

akhs

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

Table-4.8: Period wise Residual Maturity of assets and

liabilities for the year 2006-07

Rs. in Lakhs

Items 1 to 180

days 181 to 365

days

Advances 34572 13605

Investments 920 --

Foreign currency assets -- --

Deposits 9523 930

Borrowings 520 20352

Foreign currency liabilities -- --

GAP 25449 -7677 Source: Annual Report of KGB for the year 2006-07.

The above table shows the residual maturity of the rate sensitive

assets and rate sensitive liabilities from 1 to 180 days and 181 to 365 days

for the year 2006-07. It revealed that the time buckets of 181 days to 365

days are vulnerable paving way to negative gaps of high volume. The

negative gaps are due to the mismatch in the maturity pattern of assets and

liabilities.

123

Table-4.9: Residual Maturity pattern of assets and

liabilities for the year 2007-08

Rs. in Lakhs

Maturity patterns

Deposits Advances Investments BorrowingsForeign

currency assets

Foreign currency liability

1 to 180 days

1227.00 41824.00 253.00 5810.00 -- --

181 to 365 days

119.00 16459.00 -- 6238.00 -- --

1 to 3 years

4511.00 10046.00 10634.00 6118.00 -- --

3 to 5 years

329.00 8467.00 5049.00 7555.00 -- --

Over 5 years

691.14 4506.00 1538.00 5596.00 -- --

Source: Annual Report of KGB for the year 2007-08

Table-4.10: Break up of assets and liabilities based on

residual maturity pattern for the year 2007-08

Items Volume (R. in lakhs)

Interest Rate Mix (%)

RSA 58536 9.67 46.96

FRA 40240 9.67 32.28

NEA 25869.76 -- 20.76

Total/ average 124645.76 6.44 100.00

RSL 13394 4.35 10.74

FRL 93223 4.35 74.79

NIBL 18028.76 -- 14.47

Total/ Average 124645.76 2.90 100.00

Source: Figures computed from Annual Report of KGB for the year 2007-08

The above table reveals the break-up of assets and liabilities in the

year 2007-08. It shows that the RSA and RSL which are rate sensitive

124

assets and rate sensitive liabilities of balance sheet positions have been

classified according to the residual maturity. Here the entire volume of rate

sensitive assets, rate sensitive liabilities, fixed rate assets, fixed rate

liabilities, non-earning assets and non-interest bearing liabilities have been

calculated and the total comes to Rs.124645.76 lakhs.

The interest rates for RSA, FRA, RSL and FRL have also been

calculated. The average of interest rate for assets comes to 6.44 and the

average of interest rate for liabilities comes is 2.90.

The portfolio mix computation suggests that the asset mix i.e., RSA

comes around 47 and for FRA it is little over 32 %, for NEA around 21%.

Similarly the liability mix i.e., RSL, comes around 11%, for FRL comes

around 75 %and for NIBL 15%.

The following table shows that there is a positive gap i.e., RSA >

RSL. This trend is advantageous during the period of increasing interest

rates.

Table-4.11: Summary of Performance Measures for 2007-08

Rs. in Lakhs

Change in interest rate

Performance Measure Initial

Position 2% decrease

in interest rate

2% increase in interest

rate

GAP (RSA-RSL) 45142 45142 45142

Net interest income 4913.79 4010.96 5816.64

Net interest margin (%) 5.08 4.15 6.02

Net income 4091.31 3188.48 4994.16

Figures computed from Annual Report of KGB for the year 2007-08

125

The performance measures such as net interest income (NII), net

interest margin (NIM) and net income (NI) have been calculated. From the

above table it can be inferred that in the year 2007-08, the GAP i.e., RSA-

RSL is positive and it comes to Rs.45142 lakhs. The net interest income is

Rs.4913.79 lakhs, the net interest margin is 5.08 %. It is more than the

standard ratio fixed by the World Bank. The net income comes to

Rs.4091.31 Lakhs. The above data is shown with the help of figure 4.3.

Figure-4.3: Summary of Performance Measures for the year 2007-08

0

1000

2000

3000

4000

5000

6000

Rs.

in L

akhs

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

When interest rate negative shock of 2% was applied, it reduced, NII

to Rs.4010.96 lakhs, NIM to 4.15% and NI to Rs.3188.48 lakhs. However,

when interest rate positive shock of 2% was applied, it increased NII to

Rs.5816.64 lakhs, NIM to 6.02% and NI to Rs.4994.16 lakhs.

The above table clearly exhibits that the change in interest rate

affects on NII, NIM and NI. When the rate sensitive asset is more than the

rate sensitive liabilities this trend is more advantageous during the period of

increasing interest rates.

126

Table-4.12: Period wise Residual Maturity of assets and

liabilities for the year 2007-08

Rs. in Lakhs

Items 1 to 180

days 181 to 365

days

Advances 41824 16459

Investments 253 --

Foreign currency assets -- --

Deposits 1227 119

Borrowings 5810 6238

Foreign currency liabilities -- --

GAP 35040 10102 Source: Annual Report of KGB for the year 2007-08

The above table shows the residual maturity of the rate sensitive

assets and rate sensitive liabilities from 1 to 180 days and 181 to 365 days

for the year 2007-08 since there is a positive GAP of assets and liabilities

from 1 to 180 days and 181 to 365 days.

Table-4.13: Residual Maturity pattern of assets and

liabilities for the year 2008-09

Rs. in Lakhs

Maturity patterns Deposits Advances Investments Borrowings

Foreign currency

assets

Foreign currency liability

1 to 180 days

8044.00 49840.00 9565.00 4125.00 -- --

181 to 365 days

4146.00 17860.00 2461.00 3266.00 -- --

1 to 3 years

38681.00 9050.00 9050.00 3200.00 -- --

3 to 5 years

15091.00 7456.00 1999.00 450.00 -- --

Over 5 years

29792.00 11680.00 30233.00 -- -- --

Source: Annual Report of KGB for the year 2008-09

127

Table-4.14: Break up of assets and liabilities based on

residual maturity pattern for the year 2008-09

Items Volume (Rs. In lakhs)

Interest Rate Mix (%)

RSA 79726 9.43 51.62

FRA 39230 9.43 25.40

NEA 35483 -- 22.98

Total/ average 154439 6.28 100.00

RSL 19581 4.80 12.67

FRL 117447 4.80 76.04

NIBL 17411 -- 11.29

Total/ Average 154439 3.20 100.00 Source: Figures computed from Annual Report of KGB for the year 2008-09

The above table shows the break up of assets and liabilities in the

year 2008-09. The data reveals that the RSA and RSL which is rate

sensitive assets and rate sensitive liabilities of balance sheet positions have

been classified according to the residual maturity. Here the entire volume

of rate sensitive assets, rate sensitive liabilities, fixed rate assets, fixed rate

liabilities, non-earning assets and non-interest bearing liabilities have been

calculated and the total comes to Rs.154439 lakhs.

The interest rates for RSA, FRA, RSL and FRL have also been

computed. The average of interest rate for assets comes to 6.28 and the

average of interest rate for liabilities comes to 3.2.

The portfolio mix computation suggests that the asset mix i.e., RSA

comes around 52 and for FRA around 25, for NEA around 23. Similarly,

the liability mix i.e., RSL, comes around 13, for FRL 76 and for NIBL

comes around 11.

128

The following table shows that there is a positive gap i.e.,

RSA>RSL. This trend is advantageous during the period of increasing

interest rates.

Table-4.15: Summary of Performance Measures for 2008-09

Rs. in Lakhs

Change in interest rate

Performance Measure Initial

Position 2% decrease

in interest rate

2% increase in interest

rate

GAP (RSA-RSL) 60145 60145 60145

Net interest income 4640.20 3437.30 5843.10

Net interest margin (%) 3.98 2.95 5.01

Net income 4140.51 2937.61 5343.41

Figures computed from Annual Report of KGB for the year 2008-09.

The performance measures such as net interest income (NII), net

interest margin (NIM) and net income (NI) have been calculated. From the

above table it can be inferred that in the year 2008-09, the GAP i.e., RSA-

RSL is positive and it comes around Rs.60145 lakhs. The net interest

income is Rs.4640.20 lakhs, the net interest margin (NIM) is 3.98% which

is very low when compared to the standard ratio prescribed by World Bank

is 4.5% and the net income comes around Rs.4140.51 Lakhs.

When 2% decrease in interest rate was applied, it decreased NII to

Rs.3437.30, NIM to 2.95% and NI to Rs.2937.61 lakhs. On the other hand,

when 2% increase in interest rate was applied, it increased NII to

Rs.5843.10 lakhs, NIM to 5.015 and NI to Rs.5343.41 lakhs.

The above table reveals that the increase in interest rate is more

advantageous when there is a positive gap. The above data is shown with

the help of figure 4.4.

129

Figure-4.4: Summary of Performance Measures for the year 2008-09

0

1000

2000

3000

4000

5000

6000

Rs.

in

Lakh

s

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

Table-4.16: Period wise Residual Maturity of assets and

liabilities for the year 2008-09

Rs. in Lakhs

Items 1 to 14 days

15 to 28 days

29 days to 3

months

3 to 6 months

6 months

to 1 year

Advances -- -- -- 49840.36 17860.78

Investments -- -- -- 9565.88 2461.00

Foreign currency assets

-- -- -- -- --

Deposits -- -- -- 8044.59 4146.17

Borrowings -- -- -- 4125.00 3266.99

Foreign currency liabilities

-- -- -- -- --

GAP -- -- -- 47236.65 12908.71

Source: Annual Report of KGB for the year 2008-09.

130

Table-4.17: Residual Maturity pattern of assets and

liabilities for the year 2009-2010

Rs. in Lakhs

Maturity patterns

Deposits Advances Investments BorrowingsForeign

currency assets

Foreign currency liability

1 to 14 days

5600 11200 -- -- -- --

15 to 29 days

5500 11000 -- -- -- --

29 days to 3 months

6800 24000 -- -- -- --

3 to 6 months

15400 20000 -- 1500 -- --

6 months to 1 year

21000 19800 -- 5115 -- --

1 to 3 years

24000 12500 9666 2400 -- --

3 to 5 years

12500 10000 16836 1000 -- --

Over 5 years

18722 5803 2352 30119 -- --

Source: Annual Report of KGB for the year 2009-10.

The above table shows the residual maturity of the rate sensitive

assets and rate sensitive liabilities from 90 days-180 days to 181 days – 365

days for the year 2008-09. The difference between rate sensitive assets and

rate sensitive liabilities of 3 months to 6 months and 6 months to 1 year

shows the positive Gap.

The above table shows the break up of assets and liabilities in the

year 2009-10. The table suggests that the RSA and RSL which are rate

sensitive assets and rate sensitive liabilities of balance sheet positions have

131

been classified according to the residual maturity. Here, the entire volume

of rate sensitive assets, rate sensitive liabilities, fixed rate assets, fixed rate

liabilities, non-earning assets and non-interest bearing liabilities have been

calculated and the total comes to Rs.169102 Lakhs.

Table-4.18: Break up of assets and liabilities based on

residual maturity pattern for the year 2009-10

Items Volume (Rs. In lakhs)

Interest Rate Mix (%)

RSA 86000 9.36 50.85

FRA 57157 9.36 33.80

NEA 25855 -- 15.35

Total/ average 169102 6.24 100.00

RSL 60915 4.94 36.02

FRL 88741 4.94 52.47

NIBL 19446 -- 11.51

Total/ Average 169102 3.29 100.00

Source: Figures computed from Annual Report of KGB for 2009-10.

The interest rates for RSA, FRA, RSL and FRL have also been

computed. The average of interest rate for assets comes around 6.24 and

the average of interest rate for liabilities comes around 3.29.

The portfolio mix computation suggests that the assets mix i.e., RSA

comes around 51 and for FRA it is around 34, for NEA around 15.

Similarly, the liability mix i.e., RSL, comes around 36, for FRL around 52

and for NIBL comes around 12.

The table 4.19 confirmed that there is a positive GAP i.e.,

RSA>RSL. This trend is advantageous during the period of increasing

interest rates.

132

Table-4.19: Summary of Performance Measures for the year 2009-10

Rs. in Lakhs

Change in interest rate

Performance Measure Initial

Position 2% decrease

in interest rate

2% increase in interest

rate

GAP (RSA-RSL) 25085 25085 25085

Net interest income 6006.48 5506.46 6509.86

Net interest margin (%) 4.24 3.88 4.59

Net income 4637.34 4137.32 5140.72 Figures computed from Annual Report of KGB for the year 2009-10. The performance measures such as net interest income (NII), net

interest margin (NIM) and net income (NI) has been calculated. From the

above table it can be inferred that in the year 2009-10, the Gap is positive

and it comes to Rs. 25085 Lakhs. The net interest income is Rs.6006.48

lakhs, the interest margin is 4.24% and the net income comes to Rs.4637.34

lakhs. The standard ratio of NIM for the bank is 4.50% prescribed by the

World Bank. The calculated figure of NIM of KGB is less than the standard

norm given by the World Bank. The above data is shown with the help of

figure 4.5.

Figure-4.5: Summary of Performance Measures for the year 2009-10

0

1000

2000

3000

4000

5000

6000

7000

Rs.

in

Lakh

s

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

133

When 2% interest rate decreased, it reduced NII to Rs.5506.46 lakhs,

NIM to 3.88% and NI to Rs.4137.32 lakhs. However, when 2% increase in

the interest rate was applied it increased NII to Rs.6509.86 lakhs, NIM to

4.59% and NI to Rs.5140.72 lakhs. The above table suggests that in case of

positive Gap the bank is more advantageous during the period of increasing

interest rates.

Table-4.20: Period wise Residual Maturity of assets and

liabilities for the year 2009-10

Rs. in Lakhs

Items 1 to 14 days

15 to 28 days

29 days to 3

months

3 to 6 months

6 months

to 1 year

Advances 11200 11000 24000 20000 19800

Investments -- -- -- -- --

Foreign currency assets

-- -- -- -- --

Deposits 5500 5500 6800 15400 21000

Borrowings -- -- -- 1500 5115

Foreign currency liabilities

-- -- -- -- --

GAP 5700 5500 17200 3100 -6315

Source: Annual Report of KGB for the year 2009-10.

The table 4.20 shows the residual maturity of the rate sensitive assets

and rate sensitive liabilities of 1-14 days, 15-28 days, and 29 days -3

months, 3-6 months and 6 months – 1 year. It revealed that the time

buckets of 6 months-1 year is vulnerable paving way to negative GAP of

high volume.

134

Table-4.21: Residual Maturity pattern of assets and

liabilities for the year 2010-2011

Rs. in Lakhs

Maturity patterns Deposits Advances Investments Borrowings

Foreign currency

assets

Foreign currency liability

1 to 14 days

5900 11400 -- -- -- --

15 to 29 days

6200 11500 -- -- -- --

29 days to 3 months

8200 24300 -- -- -- --

3 to 6 months

20200 21100 -- -- -- --

6 months to 1 year

25100 20800 1197 600 -- --

1 to 3 years

28300 11400 2221 6000 -- --

3 to 5 years

15200 11100 15230 7500 -- --

Over 5 years

19588 7875 9480 20064 -- --

Source: Annual Report of KGB for the year 2010-11.

Table-4.22: Break up of assets and liabilities based on

residual maturity pattern for the year 2010-11

Items Volume (Rs.in lakhs)

Interest Rate Mix (%)

RSA 90297 11.00 49.40

FRA 57306 11.00 31.35

NEA 35163 -- 19.25

Total/ average 182766 7.33 100.00

RSL 66200 6.08 36.22

FRL 96652 6.08 52.88

NIBL 19914 -- 10.90

Total/ Average 182766 4.05 100.00 Source: Figures computed from Annual Report of KGB for 2010-11.

135

The table 4.22 shows the break up of assets and liabilities during the

year 2010-11. It shows that the RSA and RSL which are rate sensitive

assets and rate sensitive liabilities of balance sheet positions have been

classified according to the residual maturity. Here, the entire volume of rate

sensitive assets, rate sensitive liabilities, fixed rate assets, fixed rate

liabilities, non-earning assets and non-interest bearing liabilities have been

calculated and the total comes to Rs.182766 lakhs.

The interest rates for RSA, FRA, RSL and FRL have also been

computed. The average of interest rate for assets comes to 7.33 and the

average interest rate for liabilities comes around 4.00.

The portfolio mix computation suggests that the assets mix i.e., RSA

comes around 50% and for FRA comes around 31%, for NEA comes

around 19%. Similarly, the liability mix i.e., RSL comes around 36%, for

FRL is 53% and NIBL comes around 11%.

The following table shows that there is a positive Gap. This trend is

advantageous during the period of increasing interest rates.

Table-4.23: Summary of Performance Measures for 2010-11

Rs. in Lakhs

Change in interest rate

Performance Measure Initial Position 2% decrease in interest rate

2% increase in interest rate

GAP (RSA-RSL) 24097 24097 24097

Net interest income 6525.18 6043.24 7007.12

Net interest margin (%) 4.38 4.05 4.70

Net income 5385.61 4903.67 5867.55

Figures computed from Annual Report of KGB for the year 2010-11.

136

The performance measures such as net interest income (NII), net

interest margin (NIM) and net income (NI) has been computed. It can be

inferred that in the year 2010-11, the Gap is positive and it comes around

Rs.24097 lakhs. The net interest income is Rs.6525.18 lakhs, the net

interest margin (NIM) is 4.38 which is just below the standard norm fixed

by the World Bank (4.5%) and the net income comes to Rs.5385.61 lakhs.

The above data is shown with the help of figure 4.6.

Figure-4.6: Summary of Performance Measures for the year 2010-11

0

1000

2000

3000

4000

5000

6000

7000

8000

Rs.

in

Lakh

s

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

When 2% interest rate decreased, it reduced NII to Rs.6043.24 lakhs,

NIM to 4.05%, and NI to Rs.4903.67 lakhs, whereas when 2% increase in

interest rate was applied, it increased NII to Rs.7007.12 lakhs, NIM to

4.70% and NI to Rs.5867.55 lakhs. The change in interest rate ultimately

has effect on NII, NIM and NI. Due to the positive Gap the bank is more

advantageous during the period of increasing interest rates.

137

Table-4.24: Period wise Residual Maturity of assets and

liabilities for the year 2010-11

Rs. in Lakhs

Items 1 to 14 days

15 to 28 days

29 days to 3

months

3 to 6 months

6 months

to 1 year

Advances 11400 11500 24300 21100 20800

Investments -- -- -- -- 1197

Foreign currency assets

-- -- -- -- --

Deposits 5900 6200 8200 20200 25100

Borrowings -- -- -- -- 600

Foreign currency liabilities

-- -- -- -- --

GAP 5500 5300 16100 900 -3703

Source: Annual Report of KGB for the year 2010-11

The above table shows the residual maturity of the rate sensitive

assets and rate sensitive liabilities of 1-14 days, 15-28 days, and 29 days – 3

months, 3 – 6 months and 6 months – 1 year. It revealed that the time

bucket of 6 months to 1 year is vulnerable paving way to negative GAP of

high volume, this is due to mismatch between assets and liabilities.

138

Table-4.25: Residual Maturity pattern of assets and

liabilities for the year 2011-12

Rs. in Lakhs

Maturity patterns

Deposits Advances Investments BorrowingsForeign

currency assets

Foreign currency liability

1 to 14 days

6500 12900 -- -- -- --

15 to 29 days

7600 12600 -- -- -- --

29 days to 3 months

8800 24700 -- -- -- --

3 to 6 months

23100 21400 -- -- -- --

6 months to 1 year

27800 22300 1495 17300 -- --

1 to 3 years

29500 15400 2544 675 -- --

3 to 5 years

16900 11600 16366 1250 -- --

Over 5 years

19919 8574 9788 2069

Source: Annual Report of KGB for the year 2011-12.

139

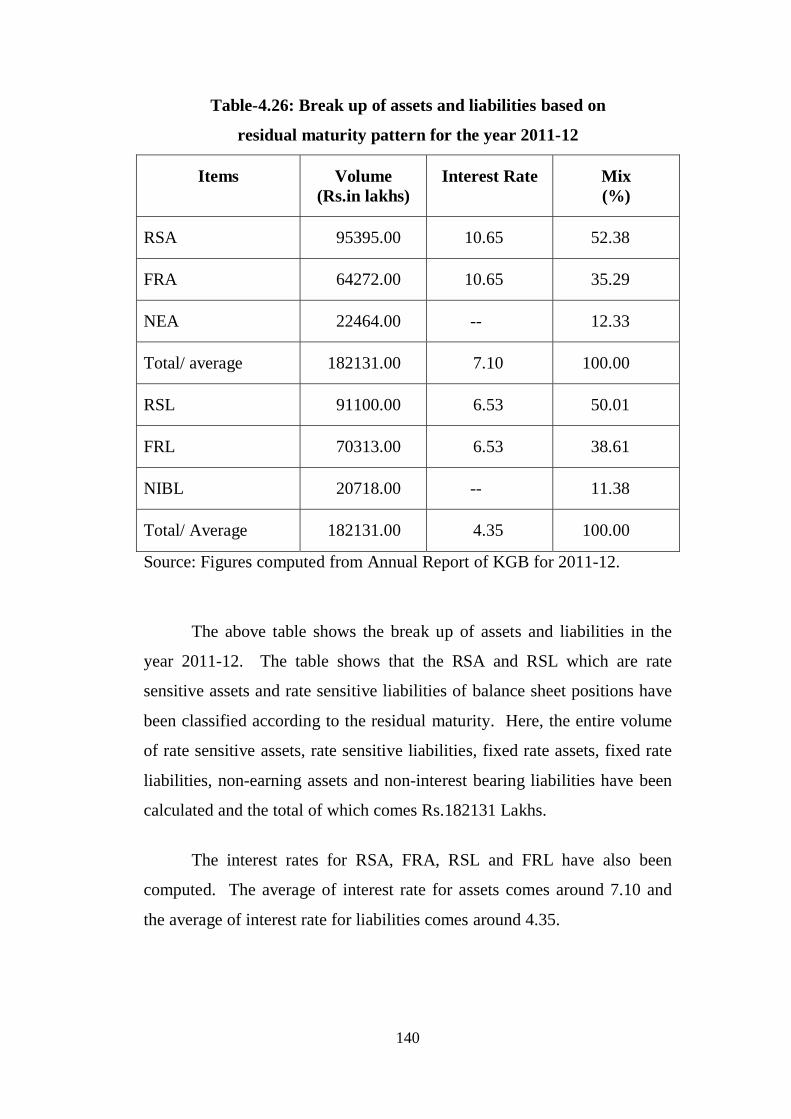

Table-4.26: Break up of assets and liabilities based on

residual maturity pattern for the year 2011-12

Items Volume (Rs.in lakhs)

Interest Rate Mix (%)

RSA 95395.00 10.65 52.38

FRA 64272.00 10.65 35.29

NEA 22464.00 -- 12.33

Total/ average 182131.00 7.10 100.00

RSL 91100.00 6.53 50.01

FRL 70313.00 6.53 38.61

NIBL 20718.00 -- 11.38

Total/ Average 182131.00 4.35 100.00

Source: Figures computed from Annual Report of KGB for 2011-12.

The above table shows the break up of assets and liabilities in the

year 2011-12. The table shows that the RSA and RSL which are rate

sensitive assets and rate sensitive liabilities of balance sheet positions have

been classified according to the residual maturity. Here, the entire volume

of rate sensitive assets, rate sensitive liabilities, fixed rate assets, fixed rate

liabilities, non-earning assets and non-interest bearing liabilities have been

calculated and the total of which comes Rs.182131 Lakhs.

The interest rates for RSA, FRA, RSL and FRL have also been

computed. The average of interest rate for assets comes around 7.10 and

the average of interest rate for liabilities comes around 4.35.

140

The portfolio mix computation suggests that the assets mix i.e., RSA

comes around 52 and for FRA it is around 35, for NEA around 13.

Similarly the liability mix i.e., RSL comes around 50, for FRL comes

around 39 and for NIBL comes around 11.

The following table shows that there is a positive Gap I.e.,

RSA>RSL. This trend is more advantageous during the period of

increasing interest rate.

Table-4.27: Summary of Performance Measures for 2011-12

Rs. in Lakhs

Change in interest rate

Performance Measure Initial

Position 2% decrease in interest

rate

2% increase in interest

rate

GAP (RSA-RSL) 4295 4295 4295

Net interest income 3382.25 3296.35 3468.15

Net interest margin (%) 2.14 2.09 2.20

Net income 2107.79 2021.89 2193.69

Figures computed from Annual Report of KGB for the year 2011-12.

The performance measures such as net interest income (NII), net

interest margin (NIM) and net income (NI) have been calculated. From the

above table it can be inferred that in the year 2011-12, the Gap is positive

and it comes to Rs.4295.00 lakhs. The net interest income is Rs.3382.25

lakhs, the net interest margin comes to 2.14% which is much lesser than the

standard ratio fixed by the World Bank and the net income comes to

Rs.2107.79 lakhs. The above data is shown with the help of figure 4.7.

141

Figure-4.7: Summary of Performance Measures for the year 2011-12

0

1000

2000

3000

4000

5000

6000

7000

8000R

s. in

Lak

hs

Net interest income Net income

Performance Measure

Initial Position 2% decrease in interest rate 2% increase in interest rate

When 2% interest rate decreased was applied, it decreased NII to

Rs.3296.35 lakhs, NIM to 2.09% and NI to Rs.2021.89 lakhs. However,

when 2% interest rate increased was applied, it increased NII to Rs.3468.15

lakhs, NIM to 2.20% and NI to Rs.2193.69 lakhs.

Changes of interest rate in bank will effect on NII, NIM and NI. In

case of positive GAP i.e., RSA>RSL, bank is more benefitted during the

period of increasing interest rate.

142

Table-4.28: Period wise Residual Maturity of assets and

liabilities for the year 2011-12

Rs. in Lakhs

Items 1 to 14 days

15 to 28 days

29 days to 3

months

3 to 6 months

6 months

to 1 year

Advances 12900 12600 24700 21400 22300

Investments -- -- -- -- 1495

Foreign currency assets

-- -- -- -- --

Deposits 6500 7600 8800 23100 27800

Borrowings -- -- -- -- 17300

Foreign currency liabilities

-- -- -- -- --

GAP 6400 5000 15900 -1700 -21305 Source: Annual Report of KGB for the year 2011-12.

The above table shows the residual maturity of the rate sensitive

assets and rate sensitive liabilities of 1-14 days, 15-28 days, and 29 days to

3 months, 3 – 6 months and 6 month – 1 year. It revealed that the time

bucket of 3 months to 6 months and 6 months to 1 year is vulnerable paving

way to negative GAP of high volume. It is needless to say that negative

gaps are due to mismatch in the maturity pattern of assets and liabilities.

It is evident from the above study that there are many techniques of

assessing interest rate risk which are in use but in the present study the

maturity gap analysis technique is used to assess the interest rate risk. The

bank is maintaining positive gap in almost all the years except during the

year 2005-06 wherein it was negative. It indicates that the bank is managing

effectively the composition of its assets and liabilities. The present decade

witnessed rising interest rates. The bank is taking full advantage of rising

interest rates by maintaining the positive gaps. It shows the efficiency of the

bank in managing the interest rate risk

143

144

REFERENCES:

1. Padhi A.K. “Programme on asset liability management” Bankers

Institute of Rural Development Lucknow , January 2010 p.38.

2. Bhattacharya K.M. “Risk Management in Indian Banks” Himalaya

Publishing House, Mumbai 2008.p.11.

3. Principles for the Management of Interest Rate Risk Basle

Committee on Banking Supervision, September 1997. Pp.6-7.

4. Timothy W. Kock and Scott Madonold “Managing Interest Rate

Risk” Thomson Asia Pte. Ltd., Singapur, 2003 pp.326-330.

5. Dhandapani Alagiri “Risk Management in Banks Current

Developments” ICFAI University Press Hyderabad, 2008 p.205.

6. Dr B. Charumathi “Asset Liability Management in Indian Banking

Industry- With Special Reference to Interest Rate Risk Management

in ICICI Bank” Proceedings of the World Congress on Engineering

Vol.11WCE London-UK, July 2008 pp.2-3.

7. Joshipura J.P. “measuring performance of banks using financial

ratio” The Indian Banker, Vol. lV No. 7, July 2009 pp.25-26.

****