intro to economics - markets

TRANSCRIPT

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 1/41

Markets

Dr. Katherine Sauer

A Citizen¶s Guide to Economics

ECO 1040

1

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 2/41

Overview

I. The Invisible Hand

II. Two Key Economic Assumptions

III. Prices and the MarketA. demand

B. supply

C. equilibrium

D. price controls

2

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 3/41

I. The Invisible Hand

Adam Smith (1723 ± 1790) is often referred to as the founder of

modern economics.

He was actually a Scottish philosopher of morality who got famous

for writing The Theory of Moral Sentiments (1759).- when confronted with moral decisions, people imagine

an ³impartial spectator´

- this spectator carefully considers the decision and advises

accordingly

- people decide using sympathy, not just selfishness

The concept of the ³invisible hand´ appeared in this book before

appearing his now more famous work, An Inquiry into the Nature

and Causes of the Wealth of Nations (1776).3

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 4/41

He also studied astronomy and liked the idea that even though

planets moved in their own orbit, there was a natural harmony with

the rest of the planets.

He thought that people could also move in different paths and yet

³harmonize´ with one another.

³ It is not from the benevolence of the butcher, the brewer, or the baker, that we expect our dinner, but from their regard to

their own interest.́ - from the Wealth of Nations

Smith doesn¶t say that people are motivated ONLY by self-interest.

He says that self-interest motivates more powerfully and consistently

than things like kindness or altruism.

4

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 5/41

He said that if each person seeks to promote their self-interest, then

society prospers.

³« he intends only his own gain, and he is in this, as in

many other cases, led by an invisible hand to promote an

end which was no part of his intention.´

Smith never took nor taught an economics course.

ECONOMICS DIDN¶T EXIST!!!!

Until the 19th century, academics considered economics a part of

philosophy.

5

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 6/41

II. Two Key Economic Assumptions

Assumption 1:Individuals act to make themselves as well off as possible.

- not limited to material well-being

Economists define the term utility to be the happiness or

satisfaction from an action.- different preferences

- different utility

Individuals will strive to maximize their utility.

Why did the chicken cross the road?

To maximize her utility.

6

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 7/41

Maximizing utility isn¶t simple.

- tradeoffs

- weigh benefits and costs (not just monetary)

- constraints

All actions have a tradeoff and an opportunity cost.

People don¶t always make well thought out decisions.

7

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 8/41

In-Class Activity: Think about your day today.

- What actions are you choosing to take today?

- What are the tradeoffs you are facing because of your actions?

- What are the constraints you are facing?

- Given the constraints and the tradeoffs that exist, are you

maximizing your utility today?

- What if you had forgotten that you have a big chemistryexam tomorrow, you haven¶t started studying yet and you

just remembered it now? How would you change your

actions to maximize your utility?

- Or perhaps your boss calls and asks you to come in to

work this evening? How would you change your actions to

maximize your utility?

8

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 9/41

Assumption 2:

Firms attempt to maximize profits.

revenue ± costs = profits

Firms take inputs (land, labor, capital) and combine them in a way

that adds value.

In a market economy, the firms decidewhat to produce

how to produce it

where to produce it

how much to produce

how much to charge

Why did the entrepreneur cross the road?

To make a profit.9

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 10/41

III. Prices and the Market

How does an economy face the task of allocating scarce resourcethat have alternative uses?

A market economy is coordinated by prices.

- Each economic actor (consumers, producers, landlords,

workers, retailers, «) makes transactions with otherson mutually agreeable terms.

[ you might not LIKE the terms, but the transaction

itself is voluntary ]

- Prices convey the terms.

Prices convey information and play a crucial role in determining

how resources get used.

10

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 11/41

An example:

In the past decade Americans have really taken a liking to sashimituna.

11

http://www.cheflorenagarcia.com/page/sesame-crusted-sashimi-tuna

So it is ordered more often at restaurants.

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 12/41

R estaurants begin placing larger orders with their wholesalers.

12

Tsukiji fish market ± Tokyo, Japanhttp://www.trekearth.com/gallery/Asia/Japan/Kanto/Tokyo/Ginza/photo317680.htm

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 13/41

In the language of economics we¶d say that the demand for tuna has

increased .

The reason for the increase in demand is a change in people¶s

preferences for tuna.

What do you predict will happen to the price of tuna as it becomes

more popular?

Intuitively, we understand that the price of tuna will probably

rise.

We can build a simple but powerful economic model that

will predict this.

13

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 14/41

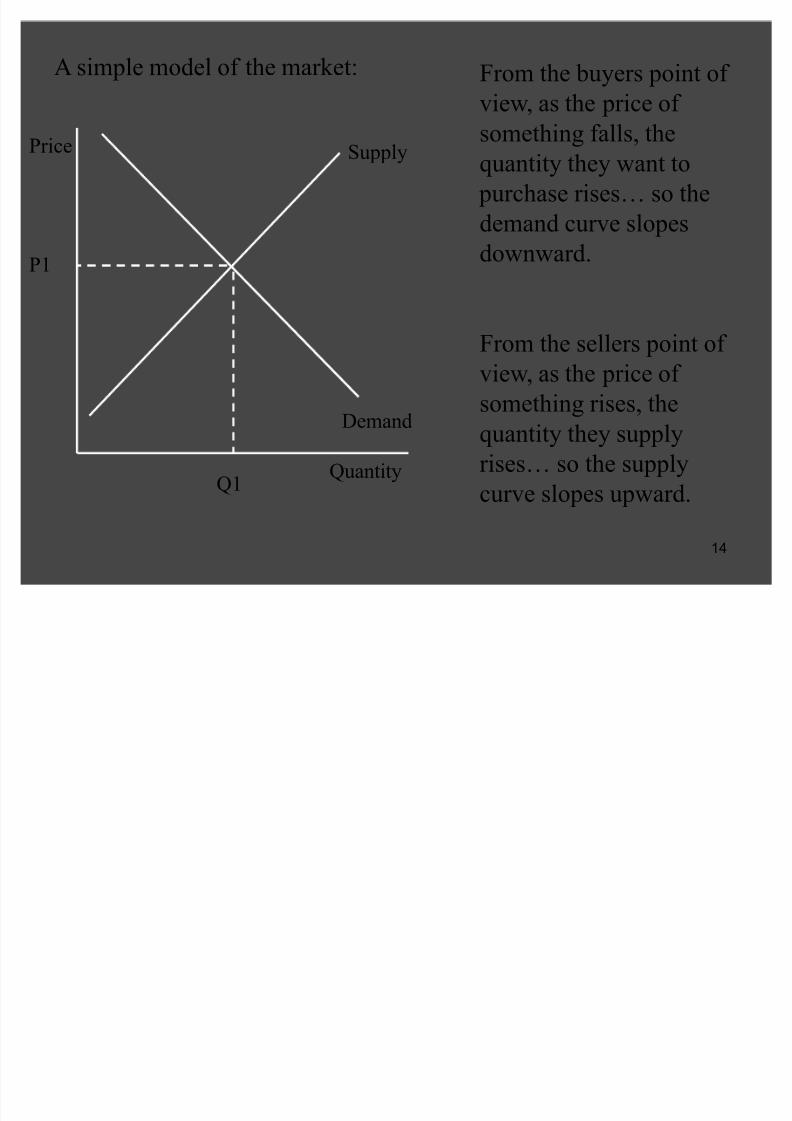

A simple model of the market:

14

Price

Quantity

Supply

Demand

From the buyers point of

view, as the price of

something falls, thequantity they want to

purchase rises« so the

demand curve slopes

downward.

From the sellers point of

view, as the price of

something rises, thequantity they supply

rises« so the supply

curve slopes upward.Q1

P1

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 15/41

1515

Price

Quantity

Supply

Old Demand

When the demand for

tuna increases, the

demand curve shifts tothe right.

The price rises.

The quantity also rises.

But how are there

³magically´ more fish

being caught?

Q1

P1

New Demand

Q2

P2

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 16/41

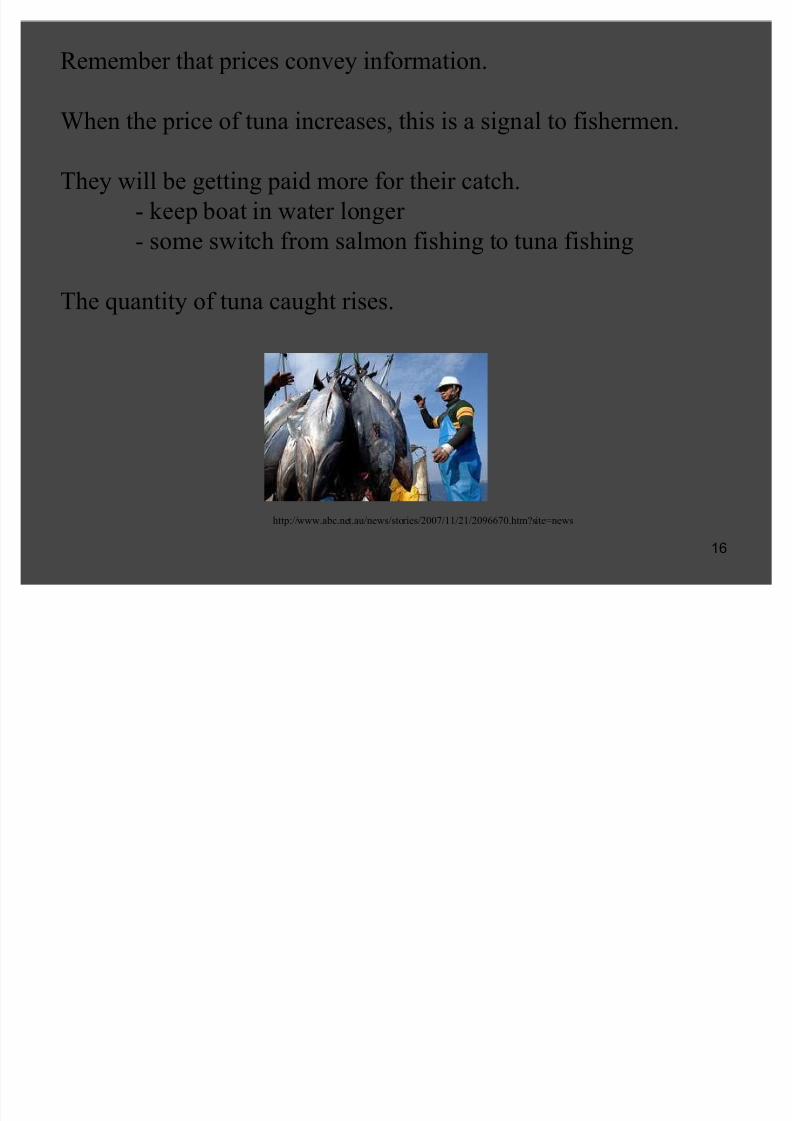

R emember that prices convey information.

When the price of tuna increases, this is a signal to fishermen.

They will be getting paid more for their catch.

- keep boat in water longer

- some switch from salmon fishing to tuna fishing

The quantity of tuna caught rises.

16

http://www.abc.net.au/news/stories/2007/11/21/2096670.htm?site=news

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 17/41

III. Demand, Supply, and the Market:

A. Demand

The Law of Demand says that there is an inverse relationship

between price and quantity demanded (ceteris paribus).- as price rises, the quantity demanded falls

- as price falls, the quantity demanded rises

This is why (in general) the demand curve slopes downward.

Demand represents consumers¶ willingness and ability to pay for a

good or service.

17

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 18/41

Demand will shift if there is a change in:

1. number of buyers

2. income

- For normal goods when income increases, demand shifts right.

- For inferior goods when income increases, demand shifts left.

3. preferences/ tastes

4. price of related goods

- When the price of a substitute rises, demand for its substitute

rises (shifts right).- When the price of a complement rises, demand for its

complement falls (shifts left).

5. expectations about the future18

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 19/41

B. Supply

The Law of Supply says that there is a positive relationship

between price and quantity supplied (ceteris paribus).

- as price rises, the quantity supplied rises

- as price falls, the quantity supplied falls

This is why (in general) the supply curve slopes upward.

Supply represents producers¶ production costs.

19

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 20/41

Supply will shift if there is a change in:

1. number of sellers

2. price of inputs

- As input prices rise, supply shifts left.

- As input prices fall, supply shifts right.

3. production technology

- An advancement in technology will increase supply.

4. expectations about the future

20

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 21/41

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 22/41

2222

Price

Quantity

Supply

Demand

Q*

P*

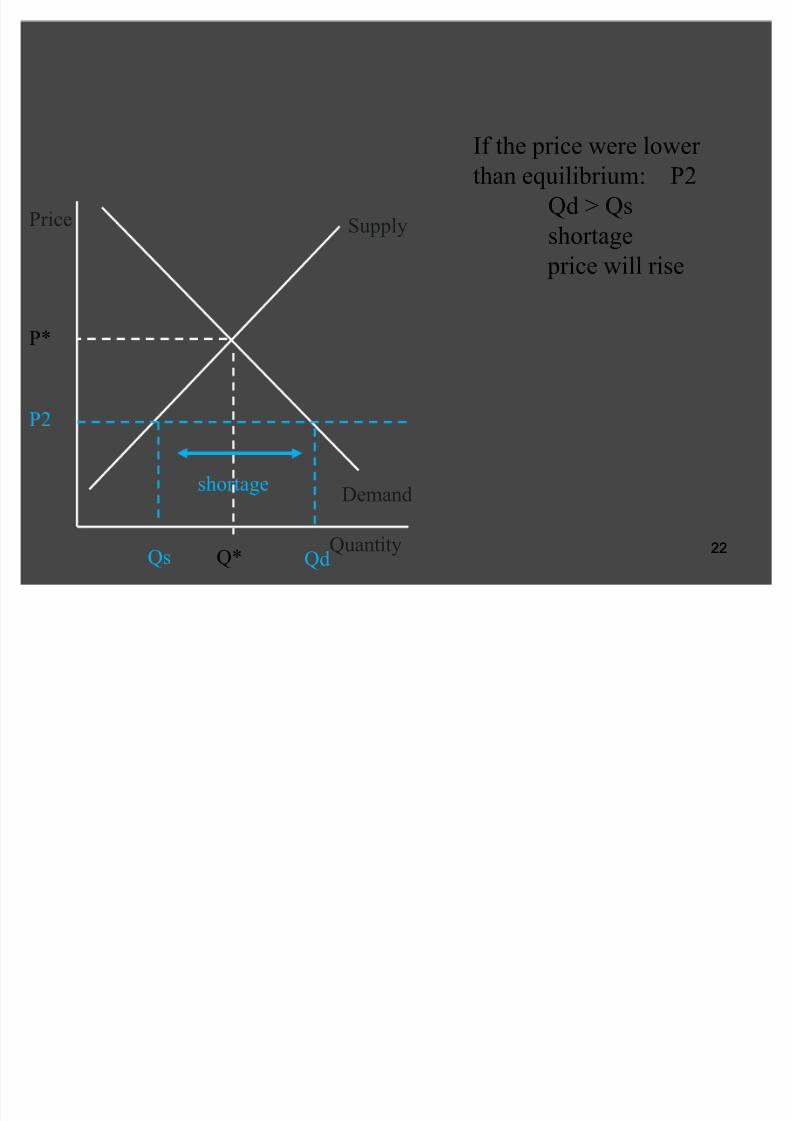

If the price were lower than equilibrium: P2

Qd > Qs

shortage

price will rise

P2

Qs Qd

shortage

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 23/41

2323

Price

Quantity

Supply

Demand

P*

Surpluses put downward

pressure on price.

Shortages put upward

pressure on price.

At P*

Qd = Qsno shortage

no surplus

price is stable

³equilibrium´ price

Qd=Qs

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 24/41

24

example:

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 25/41

25

The Market for Opium:

Price

Quantity

Supply

Demand

Q1

P1

Favorable weather

conditions resulted in a bumper crop of opium.

This would shift the

supply curve to the right.

The price of Opium falls

and the quantity rises.

Supply 2

P2

Q2

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 26/41

26

The Market for Heroin:

Price

Quantity

Supply

Demand

Q1

P1

Opium is an input to

Heroin.

Since the price of Opium

fell, the supply of Heroin

will rise.

The supply curve for

Heroin shifts right.

The price of Heroin fallsand the quantity rises.

Supply 2

P2

Q2

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 27/41

D. Price Controls

What happens if prices aren¶t allowed to equate Supply and

Demand?

Ex: In the former Soviet Union, prices were set, raised, and

lowered by central planning. The government was responsible for

over 20 million prices.

The government decided to increase the price for moleskins.

- hunters increased their hunting of moles

- state purchases of moleskins increased

- the distribution centers were filled with pelts

- industry was unable to use all the pelts and they rotted

When a government tries to control all the prices, the result is a

surplus of some items and a shortage of others.

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 28/41

In the US (and many other market economies), the government

doesn¶t try to control ALL the prices, but does control some of

them.

There are 2 basic types of price controls:

price ceilings ± prevent the price from going ³too high´ price floors ± prevent the price from falling ³too low´

- making sure the price is ³fair´

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 29/41

29

Price

Quantity

Supply

Demand

Q*

P*

Pc

Qs Qd

shortage

Price ceiling

1. Price Ceilings are legally binding maximum prices.

To be effective, they must be placed below the equilibrium

price.

Price ceilings areimplemented in order to

help out buyers of a good

or service.

They cause shortages.

They often cause a

reduction in quality.

They sometimes lead to

black markets.

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 30/41

30

Ex: R ent control

Proponents of rent control often argue that rents need to becontrolled so that people who begin renting an apartment cannot

be forced to move out of the apartment as a result of increases in

rent (e.g. fixed income retirees).

R ent control is considered a big success politically.

In the short run, the shortage is small because the supply of

housing is fixed.

In the long run, the shortage grows larger.

8/8/2019 Intro to Economics - Markets

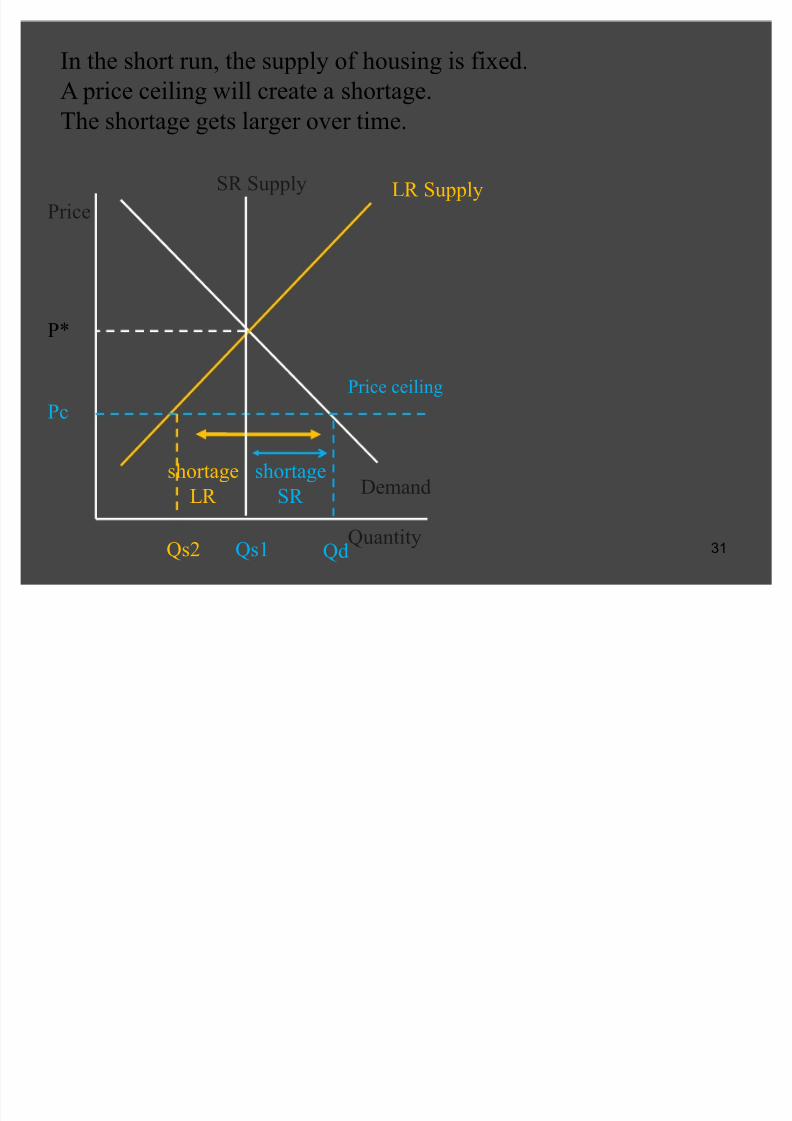

http://slidepdf.com/reader/full/intro-to-economics-markets 31/41

31

Price

Quantity

SR Supply

Demand

Qs1

P*

Pc

Qs2 Qd

shortage

SR

Price ceiling

In the short run, the supply of housing is fixed.

A price ceiling will create a shortage.

The shortage gets larger over time.

LR Supply

shortage

LR

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 32/41

32

New York City is a famous example.some results:

- low turnover of rent-controlled housing

- abandoned buildings (1,000s taken over by the

government and yet the city still has a homeless problem)

San Francisco (2001 study): 75% of rent controlled housing was

at least 50 years old.

Santa Monica 1979: building permits for apartments fell to onetenth of previous

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 33/41

33

Ex: Price controls on gasoline

Price

Quantity

Supply

Demand

Q*

P*

PcPrice ceiling

In the early 1970s, the Arab

Oil Embargo reduced the

supply of gasoline into theUS.

This caused the price of

gasoline to rise.

To reduce the effect, the US

government implemented

price controls (1973-74).

The price ceiling caused a

shortage of gasoline.

Supply 2

Q2

P2

Qs Qd

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 34/41

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 35/41

35

People waited in line for hours to fill up their tanks.

Waiting in line is a non-price rationing mechanism

(i.e. first come first served/allocated).

To prevent the long lines, California had the following policy tohelp ration the gas: Vehicle owners with a license plate number

ending in an odd (even) digit could only buy gas on odd

(even) dates of the month.

Are non-price rationing mechanisms more fair than the pricerationing mechanisms?

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 36/41

36

Important note: A shortage is not the same thing as scarcity.

Shortages are price phenomena.

Scarcity can exist without a shortage.Shortages can exist without scarcity.

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 37/41

37

Price

Quantity

Supply

Demand

Q*

P*

Pf

Qd Qs

surplus

Price floor

2. Price Floors are legally binding minimum prices.

To be effective, they must be placed above the equilibrium

price.

Price floors areimplemented in order to

help out sellers of a good

or service.

They cause surpluses.

They often lead to

additional government

actions.

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 38/41

38

Ex: agricultural goods

During the Great Depression there were price floors manyagricultural goods.

The higher price caused a surplus of food.

But hunger was a problem for many Americans.

1933 the US government bought 6 million hogs and destroyed

them.

Farmers poured milk into the sewers to keep prices up.

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 39/41

39

http://emsnews.wordpress.com/2009/10/16/crying-over-spilt-milk-in-world-trade/

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 40/41

40

Ex: the minimum wage

wage

Quantity of Labor

SLabor

DLabor

Q*

w*

wm

Qd Qs

Surplus

of people

wanting

to work

Minimum

wage

In the labor market, the

supply curve is the workers

wanting to work.

The demand curve is firms

hiring.

The market clearing wage isdeemed to be ³too low´ so a

minimum wage is

implemented.

What is the result?

8/8/2019 Intro to Economics - Markets

http://slidepdf.com/reader/full/intro-to-economics-markets 41/41

41

What do economists think about price controls?

Generally economists are not in favor of them.

Economists aren¶t totally against government intervention in the

market .

If governments intervene in the market, do it in a way where

prices still signal information.

ex: give a voucher or income transfer to the group youwant to help