introduction: the road ahead: fatca, igas and the crs · web view“following its passage by both...

TRANSCRIPT

GATCA: GLOBAL ACCOUNT TAX COMPLIANCE “ACTS”:

Prof. Haydon P. Perryman, CGMA

Version 3.44November 2, 2015

WITHHOLDING

DUE DILIGENCE(Remediation)

Pre-existingCustomers

DUE DILIGENCE(Onboarding)

New Customers

Certifications

This document was prepared as a courtesy and should not be regarded as an authoritative reference to the

US Internal Revenue Code, US IRS Notices, Income Tax Regulations, Inter Governmental Agreements on FATCA, the OECD’s Automatic Exchange of Information, the Common Reporting Standard Implementation Handbook, or HMRC Guidance Notes for the Automatic Exchange of Financial Account Information

This document is for general information purposes only, and should not be used as a substitute for consultation with professional advisors.

Babylon Pangea Ltd is not responsible for any errors or omissions, or for the results obtained from the use of this document. All information in this document is provided "as-is", with no guarantee of completeness, accuracy, timeliness or of the results obtained from the use of this information, and without warranty of any kind, express or implied.

Formatting copyright © 2015 Babylon Pangea Ltd. Introduction – The Road Ahead © 2015 Babylon Pangea Ltd. Pyramid Diagram © 2015 Babylon Pangea Ltd. Communication Style of the FATCA Project Manager and how this relates to Subject Matter Expertise © 2015 Babylon Pangea Ltd. Appendix 1: Accounts and Products excluded from FATCA © 2015 Babylon Pangea Ltd. Appendix 7: Mapping Countries for reporting purposes © 2015 Babylon Pangea Ltd.All rights reserved.

No claim to original Government or OECD works.Version 3.44

November 2, 2015.

Latest edition of Guide to GATCA1

SOLICITATIONThis content is for general information purposes only, and should not be used as a substitute for

consultation with professional advisors.

1 http://haydonperryman.com/supporting-documents/gatca/

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

CONTENTS.................................................................................................................................................................................. 3

INTRODUCTION: THE ROAD AHEAD: FATCA, IGAS AND THE CRS...........................................................................4

FATCA – COMMUNICATION STYLE OF THE PROJECT MANAGER AND HOW THIS RELATES TO SUBJECT MATTER EXPERTISE............................................................................................................................................. 8

FATCA, IGA & CRS REGULATORY MILESTONES AND DATES...................................................................................29

UK FATCA, CDOT AND DAC2/CRS REGULATORY MILESTONES AND DATES......................................................30

FOR FATCA, THE IGAS AND THE CRS; WHAT GETS REPORTED, WHEN AND HOW?........................................36

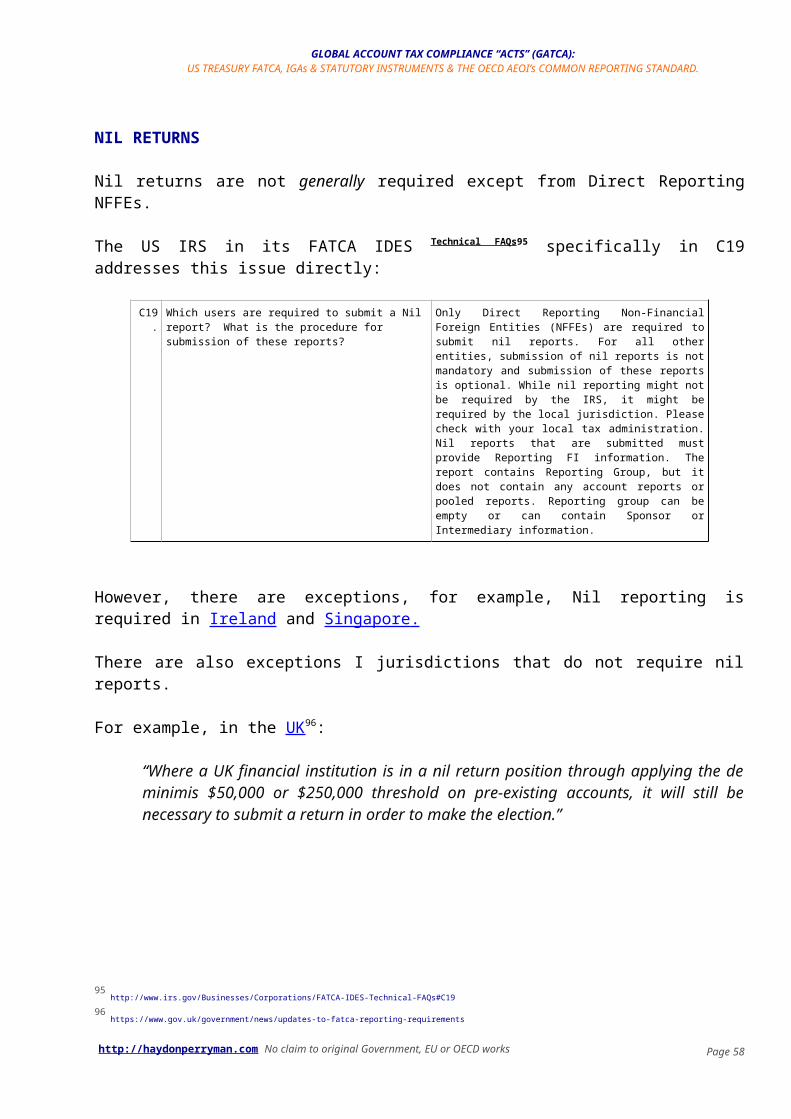

NIL RETURNS.......................................................................................................................................................................... 42XML SCHEMAS.................................................................................................................................................................................. 43WHAT GETS REPORTED:...................................................................................................................................................................44CONCLUSION:..................................................................................................................................................................................... 49

SIX THINGS YOU ARE NOT BEING TOLD ABOUT FATCA, THE IGAS AND THE CRS...........................................51

SELECTION CRITERIA FOR A CRS/FATCA ADVISER...................................................................................................52

FATCA POLICY........................................................................................................................................................................ 53

HYPERLINKS TO SUBSECTIONS OF THE US TREASURY FATCA TEXT..................................................................58

HOW TO LOOK UP ANY § OF FATCA IN SECONDS........................................................................................................61

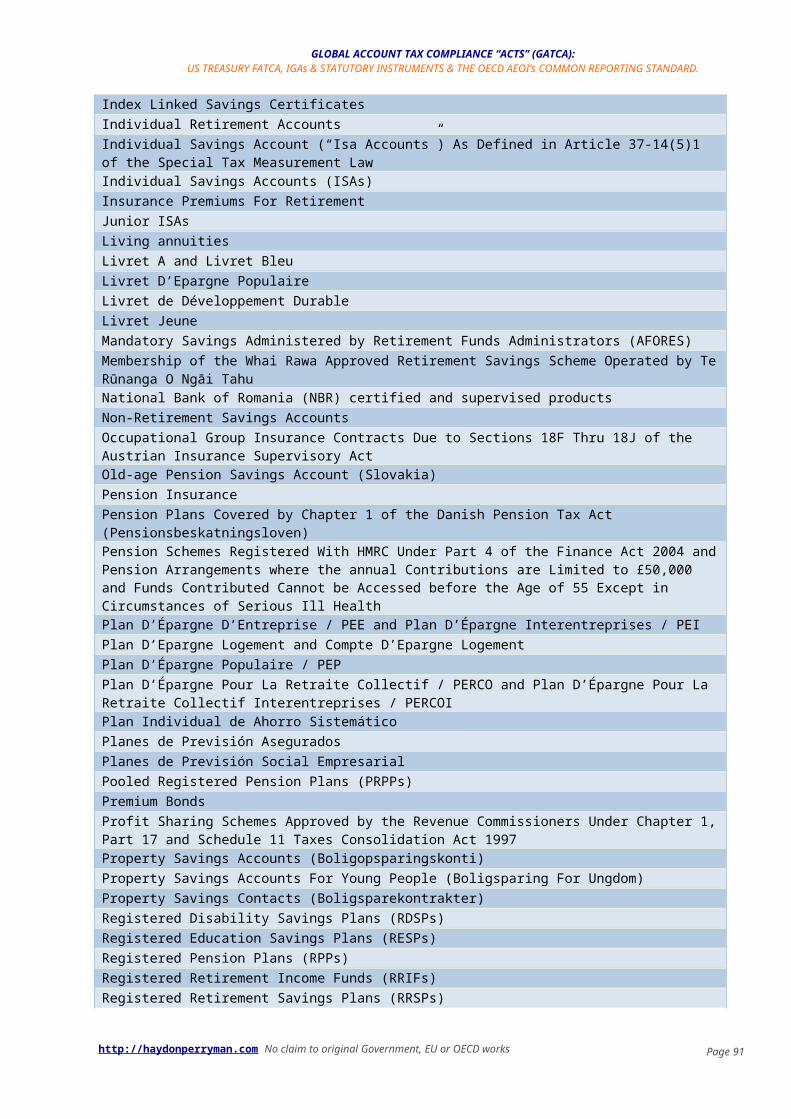

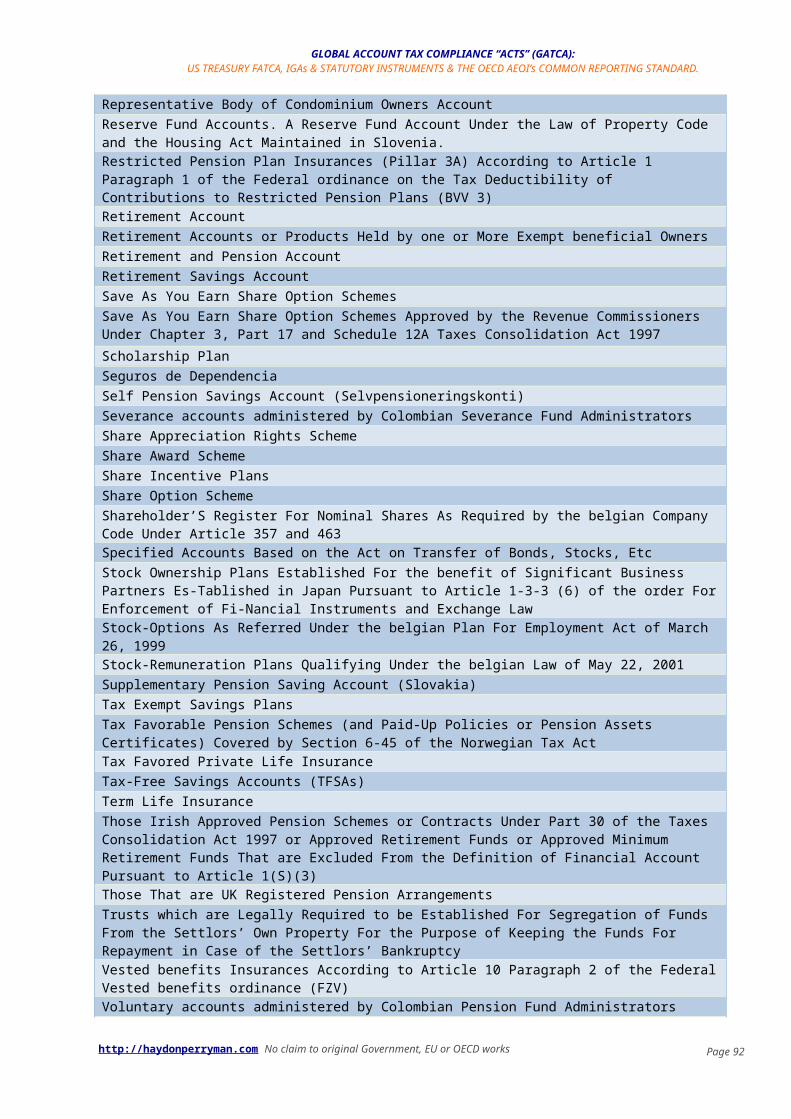

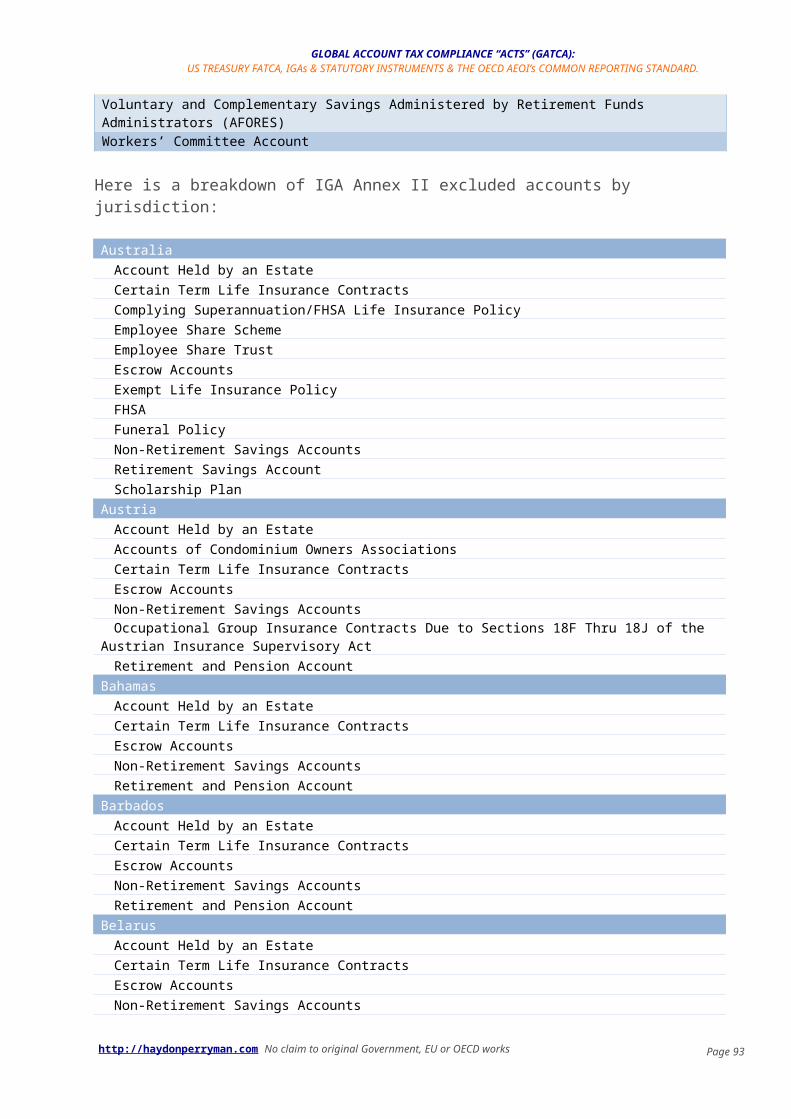

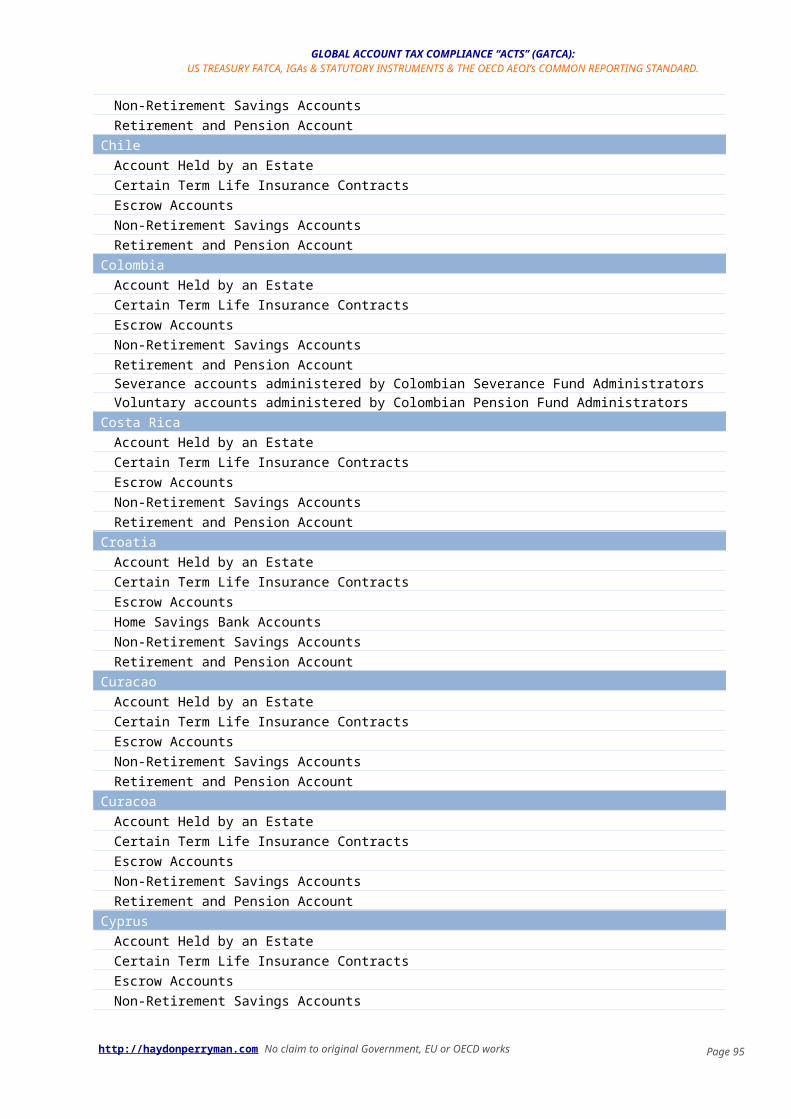

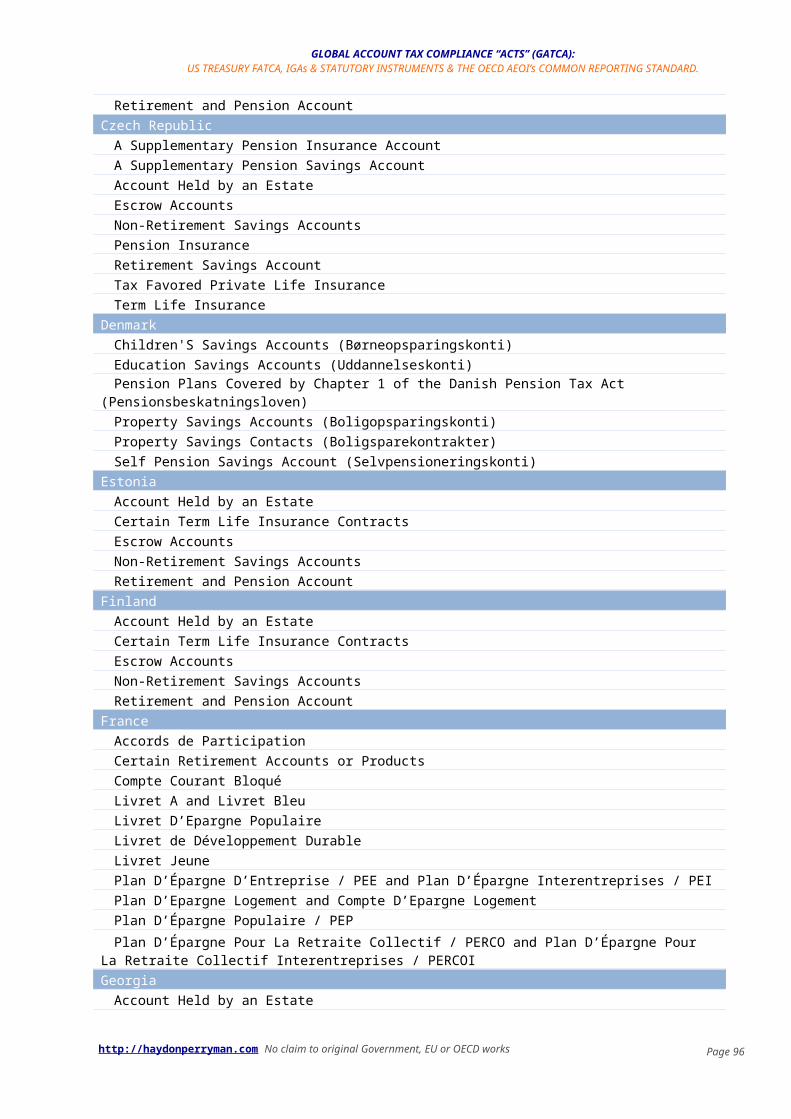

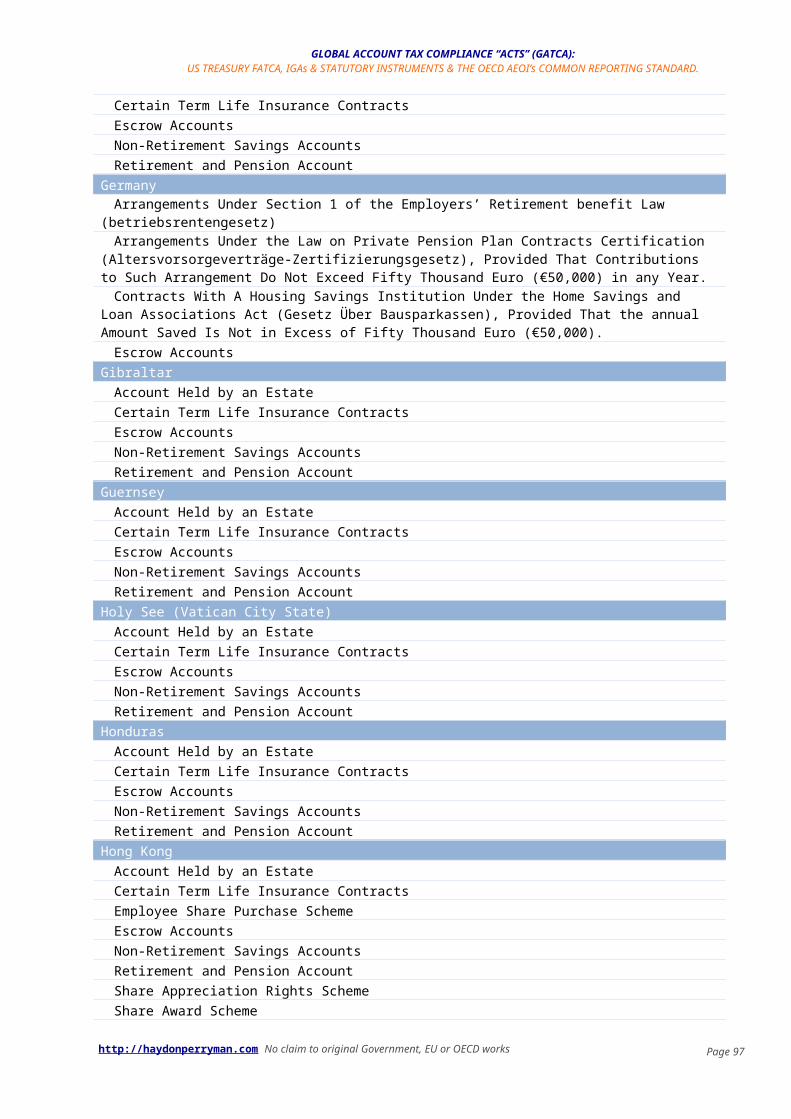

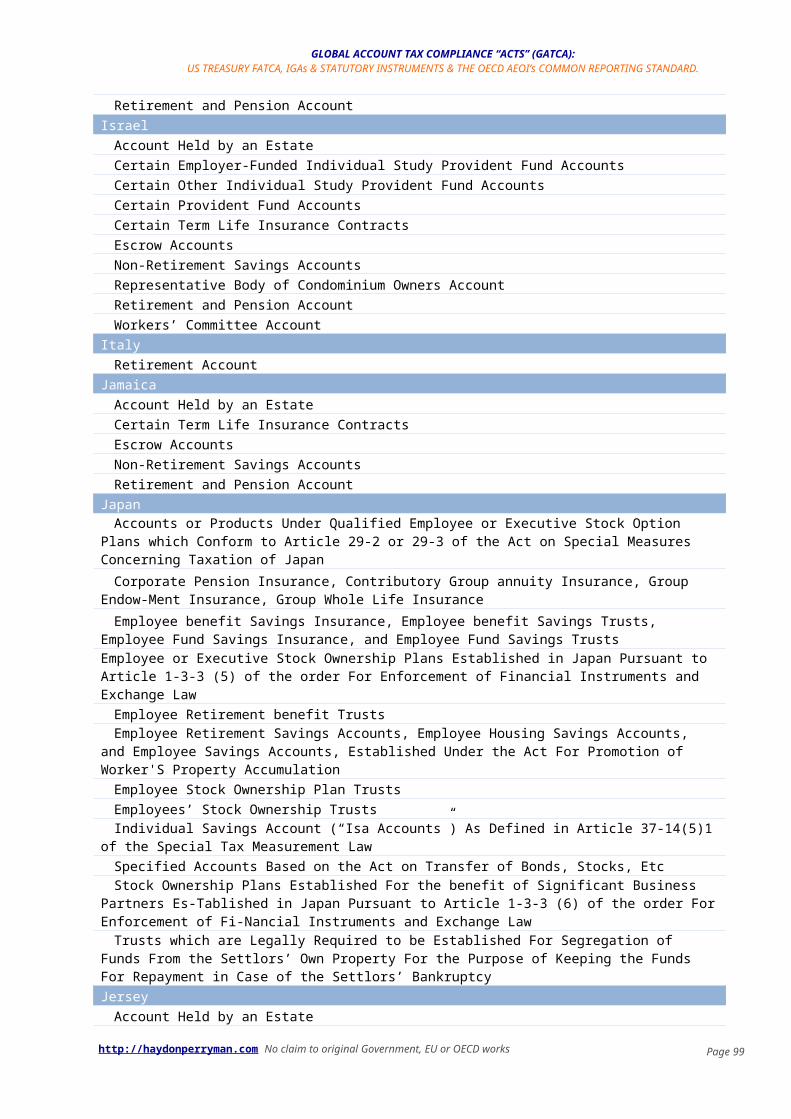

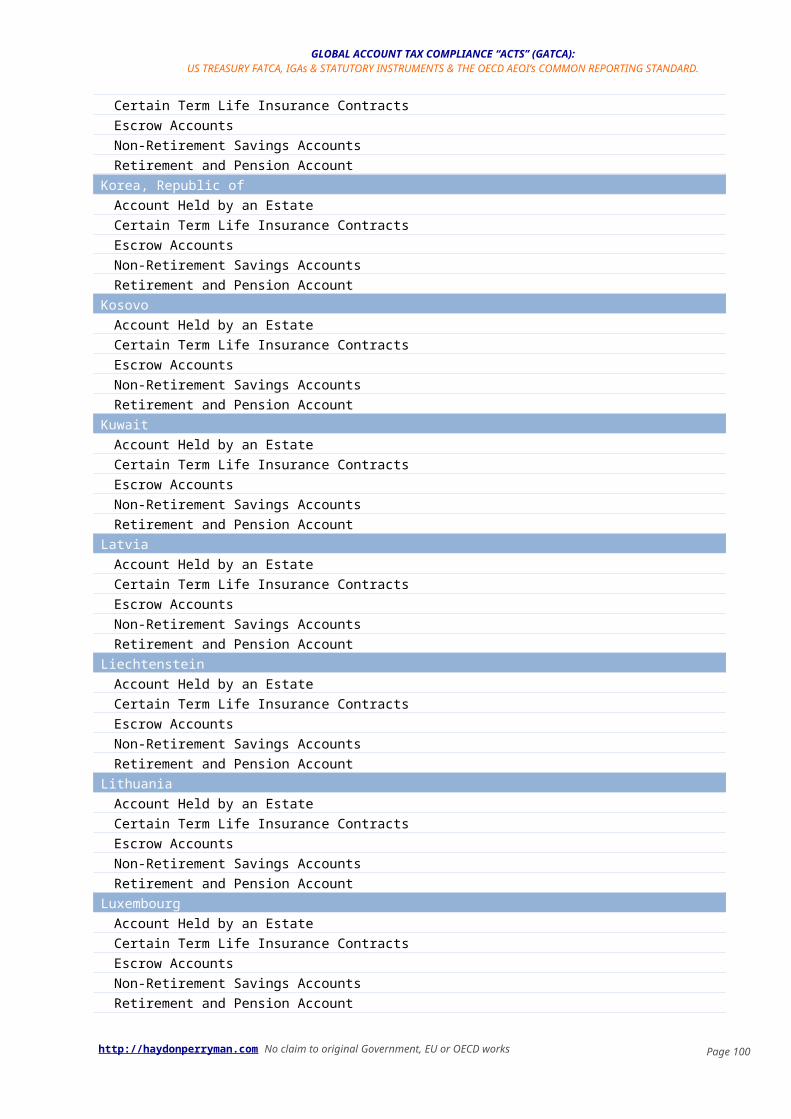

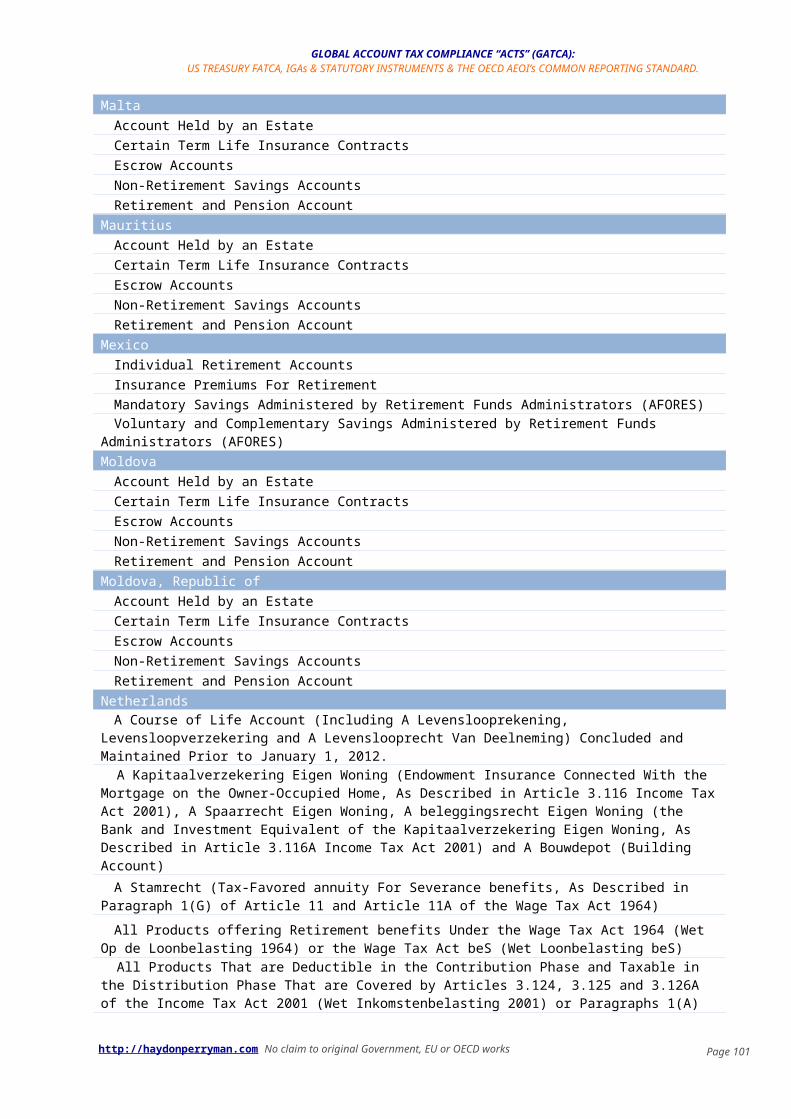

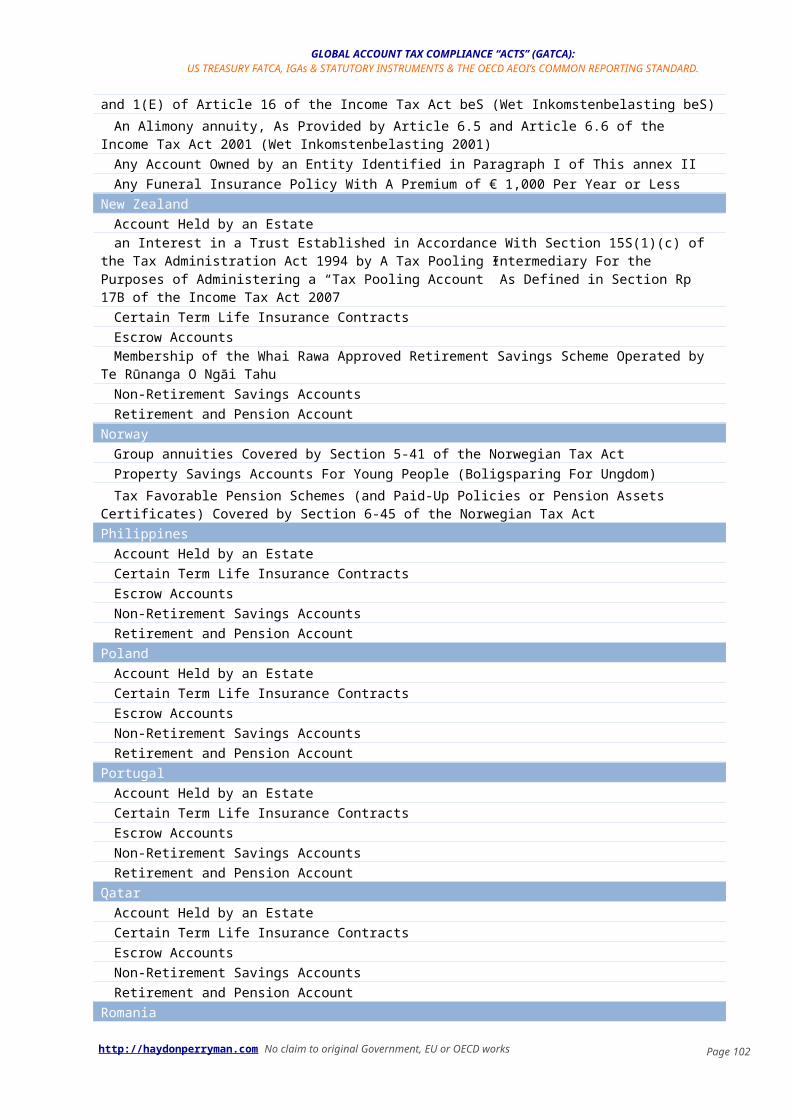

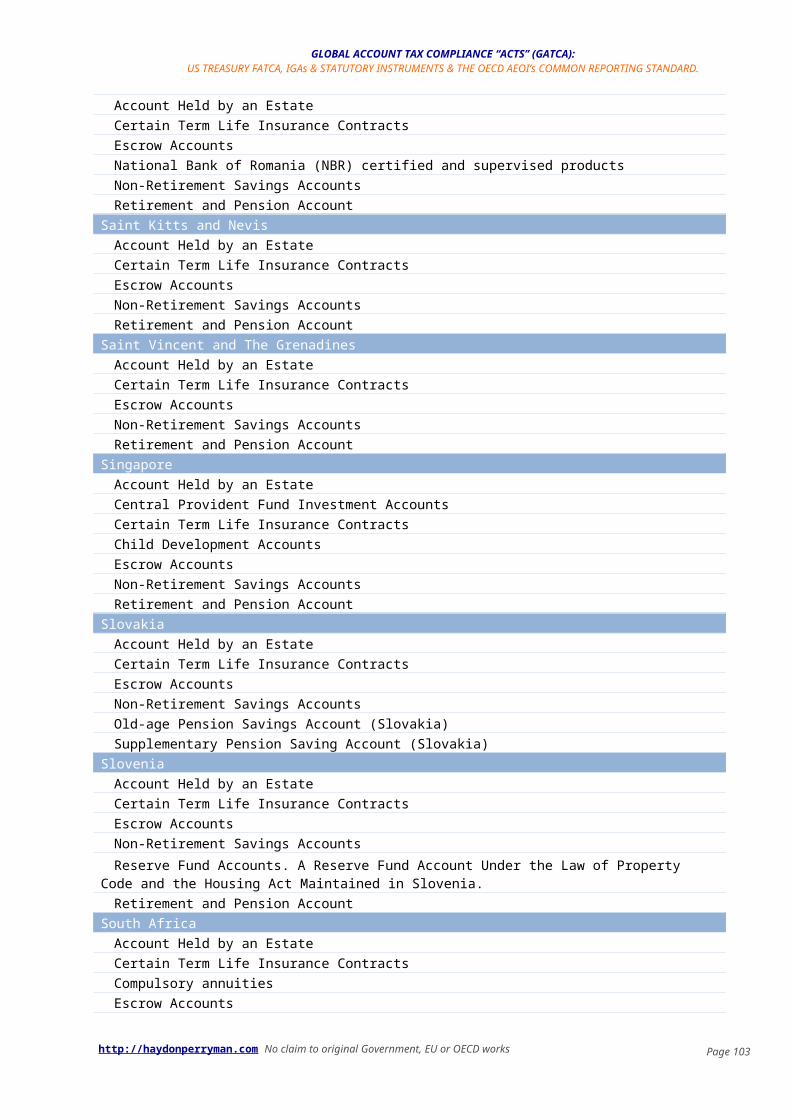

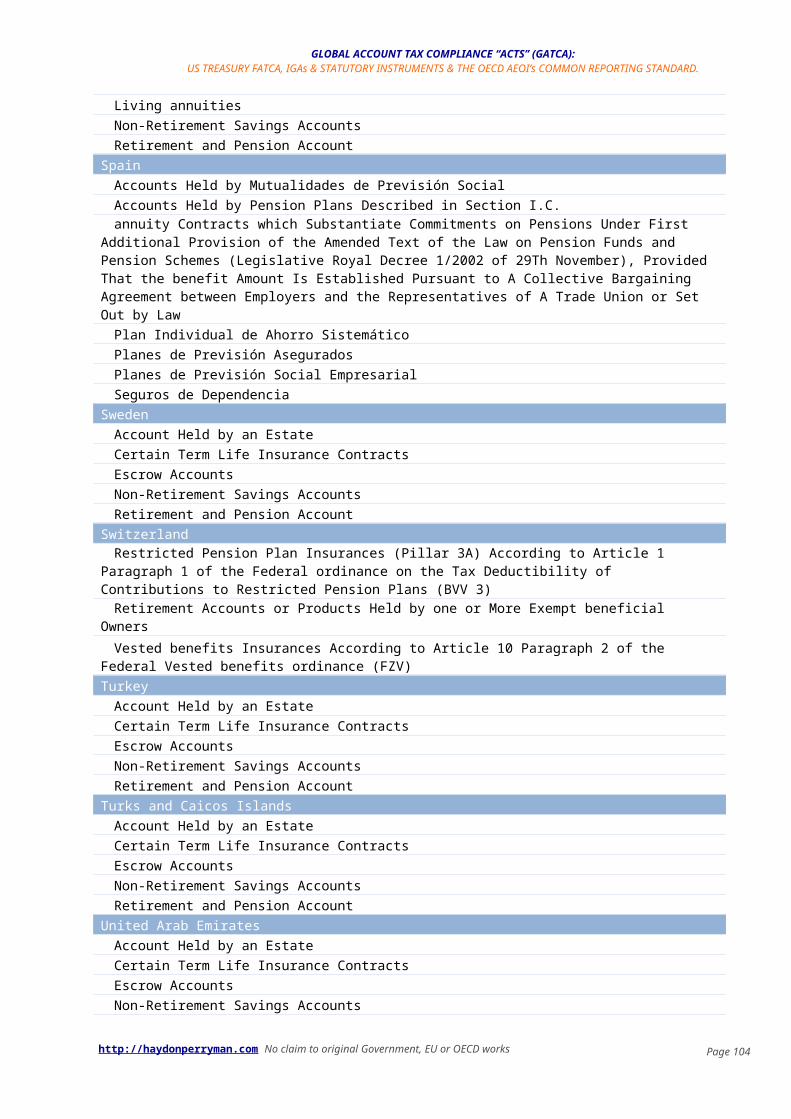

APPENDIX 1: FINANCIAL ACCOUNTS EXCLUDED, IN IGA JURISDICTIONS, FROM FATCA BY ANNEX II OF AN IGA (AS AT SEPTEMBER 10, 2015)................................................................................................................. 62

APPENDIX 2: CURING US INDICIA UNDER A UK IGA...................................................................................................79

APPENDIX 3: CURING INDICIA UNDER THE CRS..........................................................................................................83

APPENDIX 4: CLASSIFICATION OF LEGAL ENTITIES UNDER THE UK IGA...........................................................84

APPENDIX 5: RESPONSIBLE OFFICER ATTESTATIONS.............................................................................................87RESPONSIBLE OFFICER ATTESTATIONS (APPLICABLE TO NON-IGA AND IGA MODEL 2 JURISDICTIONS)......................87QUALIFIED CERTIFICATION............................................................................................................................................................. 88

APPENDIX 6: EXAMPLES OF KEY DIFFERENCES BETWEEN OECD AEOI & US TREASURY FATCA...............89

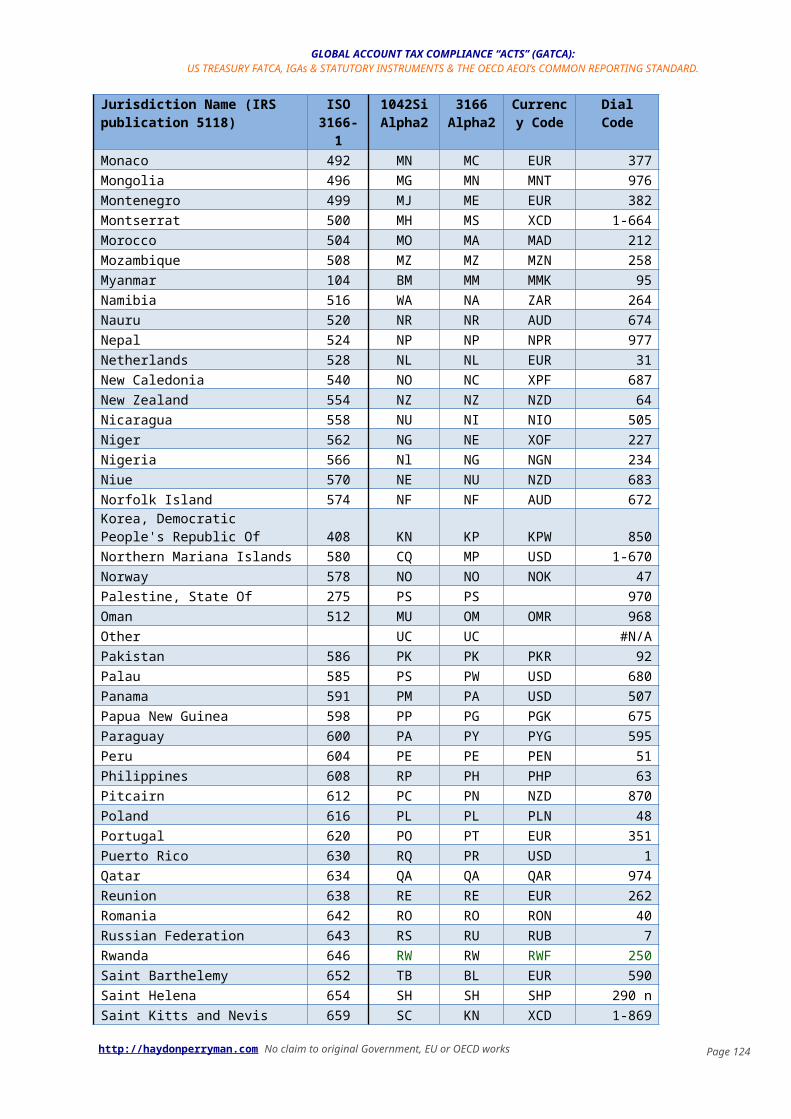

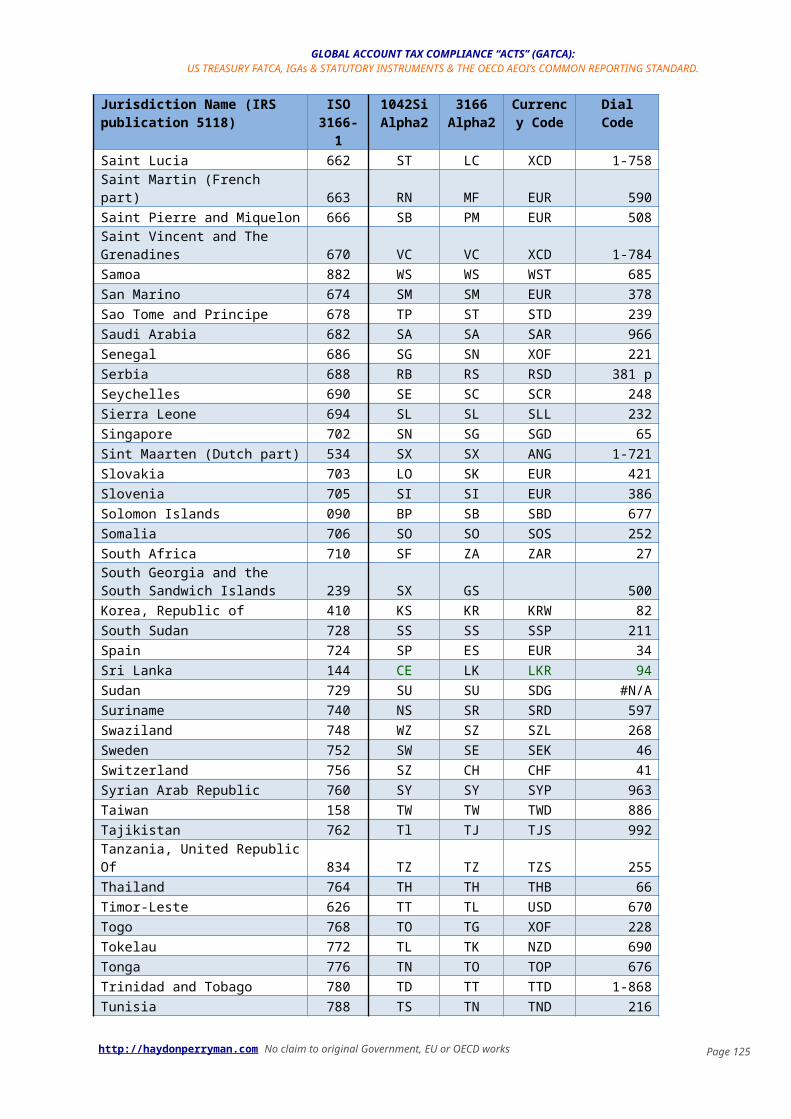

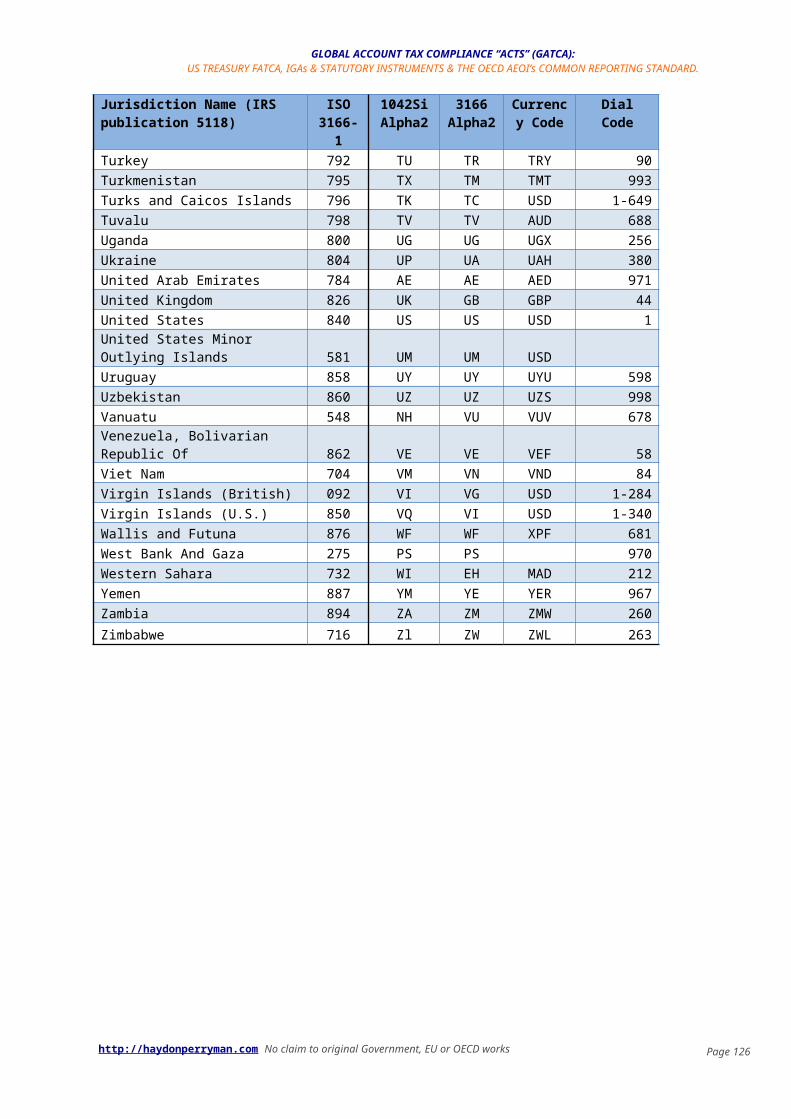

APPENDIX 7: MAPPING COUNTRIES AND CURRENCIES FOR REPORTING PURPOSES....................................90

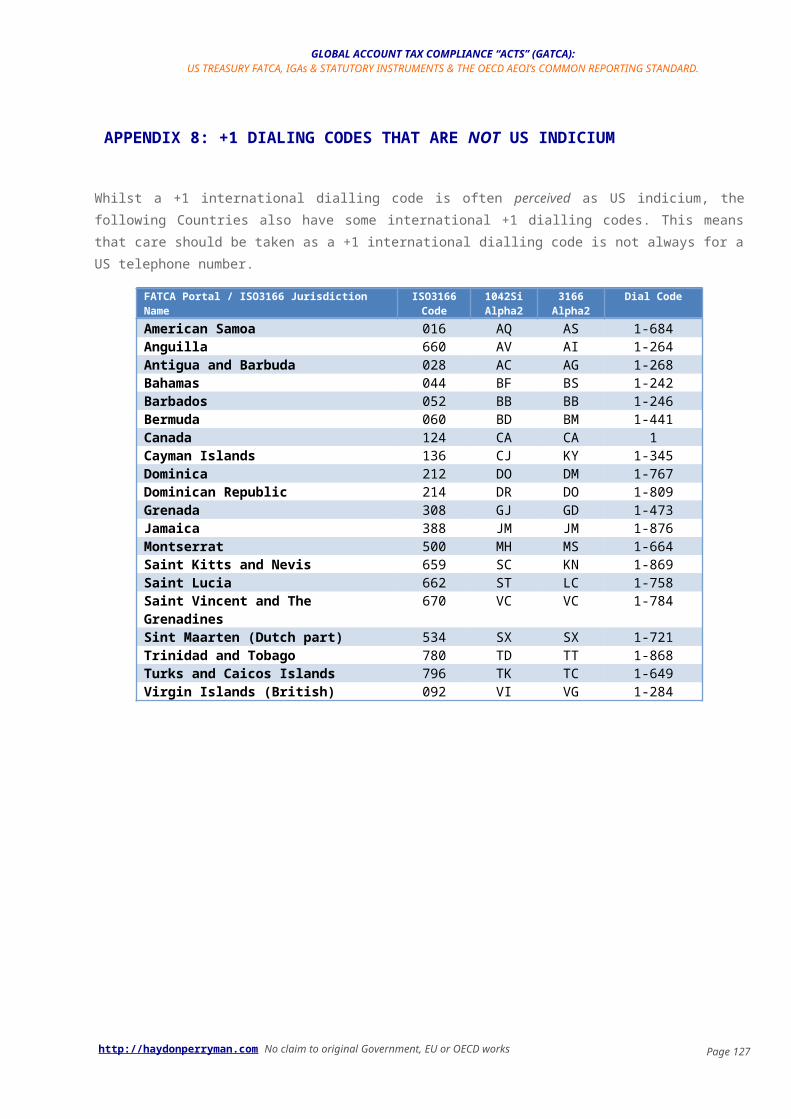

APPENDIX 8: +1 DIALING CODES THAT ARE NOT US INDICIUM............................................................................97

APPENDIX 9: SUPPORTING DOCUMENTS...................................................................................................................... 98

INTER GOVERNMENTAL AGREEMENTS..................................................103

APPENDIX 10: GIIN LIST..............................106

APPENDIX 11: FINES ISSUED BY US REGULATORS FOR ALLEGED FACILITATION OF TAX EVASION VIA OFFSHORE ACCOUNTS.................................121

APPENDIX 12: US COMPETENT AUTHORITY AGREEMENTS.........................126

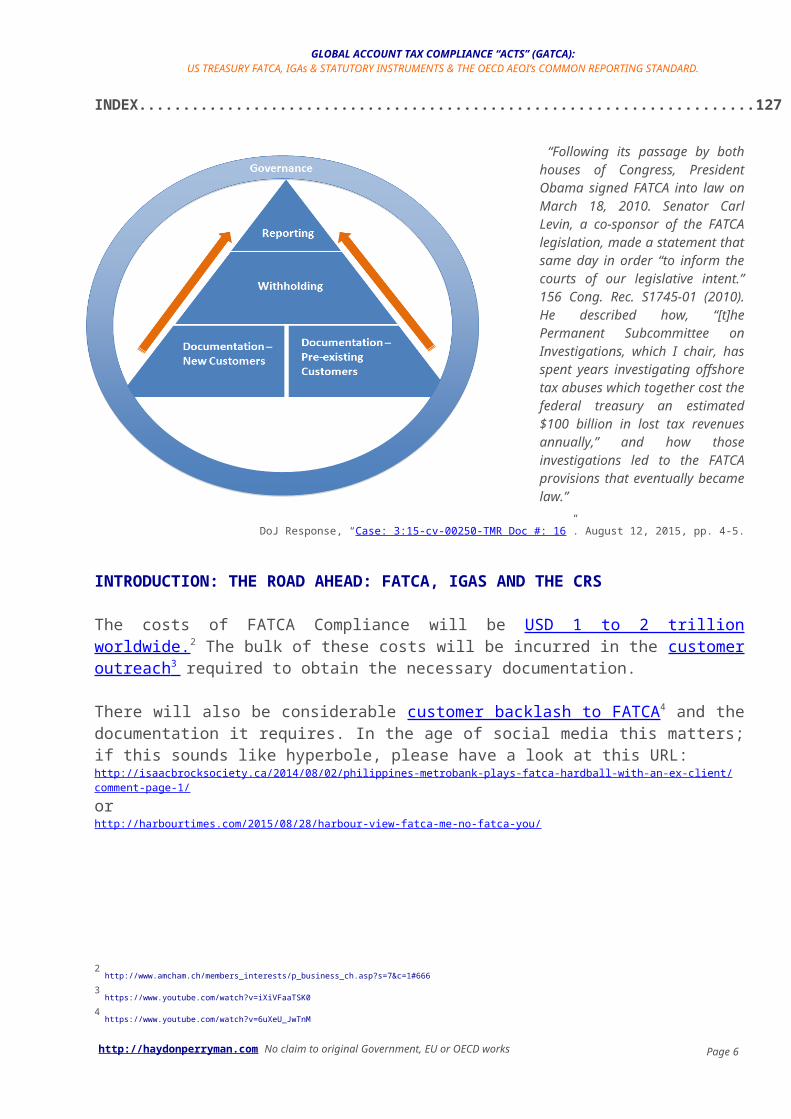

INDEX.................................................................127

“Following its passage by both houses of Congress, President

http://haydonperryman.com No claim to original Government, EU or OECD works Page 3

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

Obama signed FATCA into law on March 18, 2010. Senator Carl Levin, a co-sponsor of the FATCA legislation, made a statement that same day in order “to inform the courts of our legislative intent.” 156 Cong. Rec. S1745-01 (2010). He described how, “[t]he Permanent Subcommittee on Investigations, which I chair, has spent years investigating offshore tax abuses which together cost the federal treasury an estimated $100 billion in lost tax revenues annually,” and how those investigations led to the FATCA provisions that eventually became law.”

DoJ Response, “Case: 3:15-cv-00250-TMR Doc #: 16”. August 12, 2015, pp. 4-5.

INTRODUCTION: THE ROAD AHEAD: FATCA, IGAS AND THE CRS

The costs of FATCA Compliance will be USD 1 to 2 trillion worldwide.2 The bulk of these costs will be incurred in the customer outreach 3 required to obtain the necessary documentation.

There will also be considerable customer backlash to FATCA4 and the documentation it requires. In the age of social media this matters; if this sounds like hyperbole, please have a look at this URL:http://isaacbrocksociety.ca/2014/08/02/philippines-metrobank-plays-fatca-hardball-with-an-ex-client/comment-page-1/

orhttp://harbourtimes.com/2015/08/28/harbour-view-fatca-me-no-fatca-you/

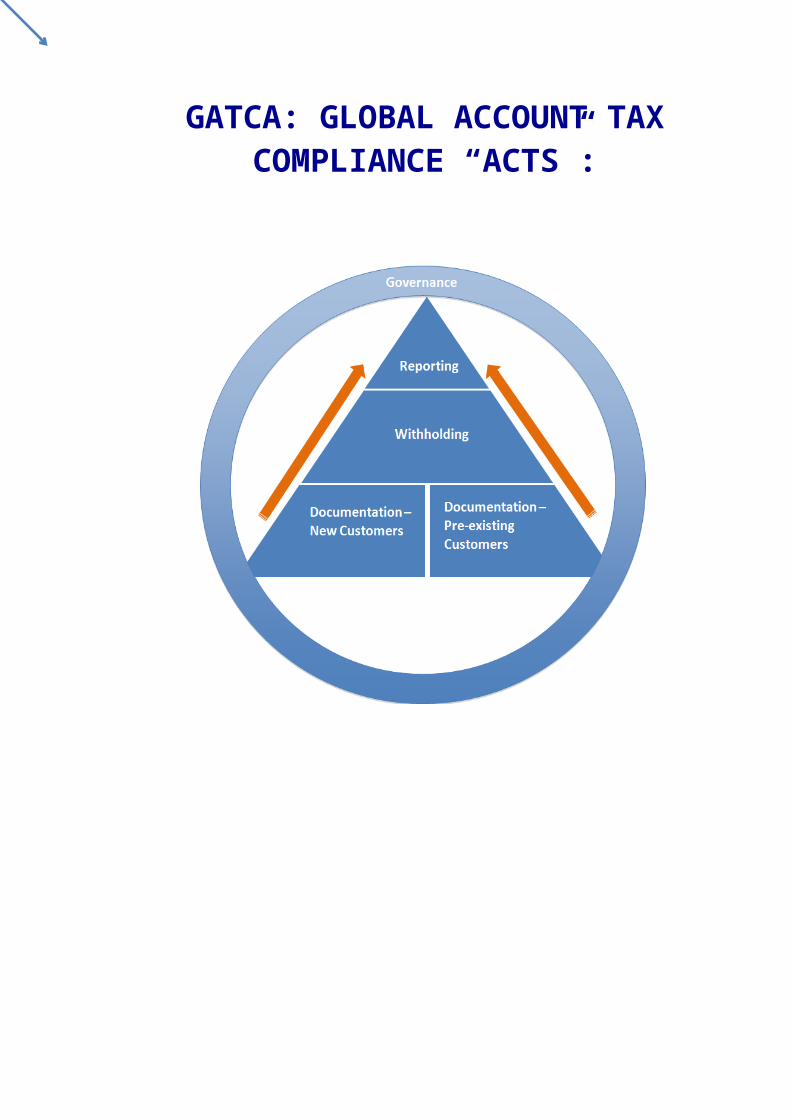

At a most basic level, FATCA 5 , the IGAs 6 and the CRS 7 are about making tax part of standard KYC/AML procedures 8 and then reporting, for tax purposes, to those Jurisdictions, in which the account holder has tax residence or citizenship.

FATCA has three pillars and, when conjoined, these support governance.

To put this another way, the diagram below illustrates the four key components of FATCA.

1. Governance. Attestations 9 to the IRS and personal liability imposed on the Responsible Officer 10 for the FATCA compliance of the Financial Institution he or she represents.

2 http://www.amcham.ch/members_interests/p_business_ch.asp?s=7&c=1#666

3 https://www.youtube.com/watch?v=iXiVFaaTSK0

4 https://www.youtube.com/watch?v=6uXeU_JwTnM

5 http://www.irs.gov/Businesses/Corporations/Foreign-Account-Tax-Compliance-Act-FATCA

6 http://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA-Archive.aspx

7 http://www.oecd.org/ctp/exchange-of-tax-information/automatic-exchange-financial-account-information-common-reporting-standard.pdf

8 http://haydonperryman.com/terms-and-definitions/amlkyc-procedures/

9 http://haydonperryman.com/supporting-documents/responsible-officer-attestations/

10 http://haydonperryman.com/terms-and-definitions/responsible-officer-ro/

http://haydonperryman.com No claim to original Government, EU or OECD works Page 4

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

2. Withholding 11 on Non-Participating FFIs 12 (NPFFIs) and Recalcitrant Account Holders (RAHs).

3. Reporting. Reporting US Accounts 13 individually, NPFFIs and RAHs in aggregate.

4. Documentation. Customer Due Diligence which, as matter of practicality, essentially makes tax part of standard KYC/AML procedures.

The diagram above makes the point that Documentation (or CDD) is foundational and that Reporting can be considered the capstone.

While FATCA was the catalyst for the OECD’s AEOI and whilst the Common Reporting Standard was based on the Model 1 IGAs; there are important differences between them.

(For the key differences between US Treasury FATCA and the OECD’s Automatic Exchange of Information’s Common Reporting Standard, see Appendix 6.)

However, Documentation (or CDD) and Reporting remain, which is to say that they are consistently present throughout the US Treasury version of FATCA, the IGAs, the Statutory Instruments that write the IGAs into domestic law and also in the OECD’s Automatic Exchange of Information.

The role of the Responsible Officer and related attestations that the RO has to provide are not mentioned in the IGAs, nor in the Common Reporting Standard (page Error: Referencesource not found).

Hence, there is no legal instrument to enforce a Responsible Officer to take on personal liability in an Inter Governmental Agreement Model 1 IGA Jurisdiction 14. However, the same can not be said of an IGA Model 2 Jurisdiction because FFIs in Model 2 Jurisdictions enter into a Foreign Financial Institution Agreement (FFI-A) (page Error: Reference source notfound) with the IRS. FFI-As include both the personal liability of the Responsible Officer and Attestations.

Model 1 IGA FIs do not sign an FFI-A, so strictly speaking, there is no legal enabler to enforce personal liability on their Responsible Officer. Having said that, legal opinions do vary, and it is appropriate to obtain legal advice on this issue. Further, many FIs span multiple Jurisdictions, including Non IGA and IGA Model 2 Jurisdictions. As a Responsible Officer may have responsibility across each type of IGA, the possibility of personal liability not applying in IGA Model 1 Jurisdictions alone, may provide very little solace. It may also be, that as part of an FIs “FATCA Policy 15 ” the RO assumes Personal Liability, even for a Model 1 FI. It should be noted that this would be a Business Requirement, rather than a 11

https://www.whitehouse.gov/the_press_office/LEVELING-THE-PLAYING-FIELD-CURBING-TAX-HAVENS-AND-REMOVING-TAX-INCENTIVES-FOR-SHIFTING-JOBS-OVERSEAS/

The Administration conservatively estimates this package would raise $8.7 billion over 10 years by: Withholding Taxes From Accounts At Institutions That Don’t Share Information With The United States: This proposal requires foreign financial institutions that have

dealings with the United States to sign an agreement with the IRS to become a "Qualified Intermediary" and share as much information about their U.S. customers as U.S. financial institutions do, or else face the presumption that they may be facilitating tax evasion and have taxes withheld on payments to their customers. In addition, it would shut down loopholes that allow QIs to claim they are complying with the law even as they help wealthy U.S. citizens avoid paying their fair share of taxes.

Shifting the Burden of Proof and Increasing Penalties for Well-Off Individuals Who Seek to Abuse Tax Havens: In addition, the Obama Administration proposes tightening the reporting standards for overseas investments, increasing penalties and imposing negative presumptions on individuals who fail to report foreign accounts, and extending the statute of limitations for enforcement.

12 http://haydonperryman.com/terms-and-definitions/nonparticipating-ffi/

13 http://haydonperryman.com/terms-and-definitions/u-s-account/

14 http://www.tia.gov.ky/pdf/Responsible_Officer_Role_in_Cayman.pdf

15 https://www.youtube.com/watch?v=TGprVYpzEzA

http://haydonperryman.com No claim to original Government, EU or OECD works Page 5

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

Regulatory Requirement. (Regulatory requirements should be capable of being traced to a § of a regulation and Title V of the Hire Act does not apply outside of the US unless these provisions are agreed under a contract. That contract would be the FFI-A and Model 1 FIs do not enter into a FFI-A. This is the case regardless of the fact that a Responsible Officer must be identified16 in Q10 on Form 8957 17 – as part of the process of registering a Foreign Financial Institution on the IRS FATCA Portal. Registering on the IRS FATCA Portal is not the same as entering into a FFI-A).

The IGAs also, for the most part, remove withholding intra IGA Jurisdictions.

“If Model 1 partner countries comply with Article 2 as well as the “Time and Manner of Exchange of Information” agreed to in Article 3 and other rules, then their reporting FFIs “shall be treated as complying with, and not subject to withholding under, section 1471,” nor will they be required to withhold “with respect to an account held by a recalcitrant account holder” under § 1471.”

DoJ Response, “Case: 3:15-cv-00250-TMR Doc #: 16”. August 12, 2015, pp. 6-7.18

Withholding can only occur on NPFFIs and RAHs. The IGAs explicitly suspend withholding on RAHs. Further, the IGAs also state that a Financial Institution in an IGA Jurisdiction can only become “Non-Participating” after “significant non-compliance 19 ”. “Significant non-compliance” does vary by IGA, for example, Japan (IGA Model 2), has a path to resolution that lasts for a year. The UK has a path to resolution that lasts for 18 months. In any event, only when the time allowed for resolution has elapsed can an FFI in an Inter Governmental Agreement Jurisdiction be “Non-Participating”. Hence, in the near future, there should be no withholding, in and on, FFI intra-IGA Countries. (See the definition of a Participating FFI on page Error: Reference source not found.)

There are, however, exceptions: let us say that you are a Financial Institution in an Inter Governmental Agreement Jurisdiction and that you have an upstream arrangement with a US Withholding Agent (USWA). Let us also say that your FI has not yet registered on the IRS FATCA Portal and, hence, has no GIIN.

As of January 1, 2015, the USWA can no longer treat your FI as a participating FFI, notwithstanding the fact that your FI is based in an Inter Governmental Agreement Jurisdiction, unless the USWA has obtained and verified your GIIN.

Under this scenario, your upstream USWA will withhold on you.

The moral of the story is that, if you are a Financial Institution in an IGA Country, there are scenarios where you can be withheld upon, if you do not have a verifiable GIIN to make available.

16 http://www.irs.gov/Businesses/Corporations/Frequently-Asked-Questions-FAQs-FATCA--Compliance-Legal#General

17 http://www.irs.gov/pub/irs-pdf/f8957.pdf

18 http://isaacbrocksociety.ca/wp-content/uploads/2015/08/DOJ-response.pdf

19 http://haydonperryman.com/terms-and-definitions/nonparticipating-ffi/

http://haydonperryman.com No claim to original Government, EU or OECD works Page 6

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

It is fair to say that FATCA, in an IGA 20, will be a very different experience to FATCA in a Non IGA Jurisdiction. (IGA status of all Jurisdictions 21 .)

A New Era

Documentation (or CDD) and Reporting remain; indeed, they have been expanded to include 96 Jurisdictions 22 (and counting). FATCA tackled American Citizenship for tax purposes. The OECD’s AEOI tackles all and multiple tax residences in 94 Jurisdictions (and counting).

Hence, FATCA can be seen as the AEOI in microcosm, except that the AEOI has no withholding and, as yet, makes no mention of personal liability of a Responsible Officer or Attestations.

Interestingly, Singapore a Model 1 IGA jurisdiction, has opted to use IDES rather than host its in XML solution. Singapore is the first IGA Model 1 jurisdiction to opt to use IDES directly23. If other Model 1 IGA countries follow suit it may be that IDES could become the de facto FATCA reporting tool, which in turn, could lead to it coming the CRS reporting tool. Only time will tell.

Here is a selection of deadlines for US Treasury FATCA, the IGAs and the OECD AEOI’s Common Reporting Standard (CRS).

20 http://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA-Archive.aspx

21 http://haydonperryman.com/iga-aeoi-status-of-all-nations-by-iso-3166-code/

22 http://www.oecd.org/tax/transparency/AEOI-commitments.pdf

23 http://www.iras.gov.sg/irasHome/page.aspx?id=15664#FATCA_Test_Files

http://haydonperryman.com No claim to original Government, EU or OECD works Page 7

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

FATCA – COMMUNICATION STYLE OF THE PROJECT MANAGER AND HOW THIS RELATES TO SUBJECT MATTER EXPERTISE

This chapter will not be about ‘vanilla’ project management; there are many good publications on that subject. Instead this chapter will explain how, in practical terms, project management of FATCA differs from more generic projects and will offer practical advice, not so much about technical detail, but around the choice of communication style that the FATCA Project Manager ought to adopt and why that choice of communication style is peculiarly important for FATCA in particular.

This chapter will also go into some of the FATCA Project Management “do’s and don’ts” that I have observed in my:

five years of experience of managing FATCA programs24 and projects; sixteen years of experience of managing projects and programs in general (most of

these gained Post Qualification as an Accountant); as both a Prince2™ Practitioner and an MSP™ Practitioner and as a Qualified Mediator.

I am going to begin by explaining the fear that FATCA generates. Of course, most changes / projects induce fear of one sort or another; I am going to demonstrate that FATCA is extreme when in comes to generating fear.

The context of Fear that FATCA generates

For a list of Deferred Prosecutions, please see Appendix 11: Fines issued by US regulators for alleged facilitation of tax evasion via Offshore Accounts (on page 124).

Naturally, these fines are just the beginning. Many observe that currently these fines are on the Swiss Banks and that, perhaps, sooner rather than later, the attention of US regulation enforcers will turn to financial institutions outside of Switzerland.

Moreover, the damage done to these institutions goes beyond the fines themselves because they impact not only the bottom line immediately but also reputations and the damage to reputations can take years to overcome.

The IRS also recovers money via its Offshore Voluntary Disclosure Program25:

“The passage of FATCA coincided with the inception of the IRS’s Offshore Voluntary Disclosure Program (OVDP), which since 2009 has afforded U.S. taxpayers with previously undisclosed overseas assets[,] the opportunity to disclose them and pay reduced penalties. The IRS reported that by 2014, the OVDP had collected $6.5 billion through voluntary disclosures from 45,000 participants. “IRS Offshore Voluntary Disclosure Efforts Produce $6.5 Billion; 45,000 Taxpayers Participate,” available at

24 In my own Country that would be spelt programme, rather than, program

25 http://www.irs.gov/uac/2012-Offshore-Voluntary-Disclosure-Program

http://haydonperryman.com No claim to original Government, EU or OECD works Page 8

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

http://www.irs.gov/uac/Newsroom/IRS-Offshore-Voluntary-Disclosure-Efforts-Produce-$6.5-Billion;-45,000-Taxpayers-Participate

(last visited July 31, 2015).”

DoJ Response, “Case: 3:15-cv-00250-TMR Doc #: 16”. August 12, 2015, page 5

This is germane because, with the existence of an OVDP, the IRS in all likelihood knows precisely who has been facilitating tax evasion. This carries an implicit threat to those who were, or may have been “bad actors”, the message being “We know who you are, and we are coming to get you”.

Interestingly, none of these penalties required FATCA to be on the US Statute Books in order to be levied, which is to say that with or without Title V of the Hire Act aka FATCA, these penalties could have been levied. Nonetheless, the common perception is that FATCA and these fines are inexorably linked. The fear this inspires, rational or otherwise, can best be evidenced by the de facto widespread off-boarding of accounts held by Americans.

Nowhere in the regulation does FATCA require accounts held by Americans to be closed. Rather, the US regulation has a requirement for recalcitrant account holders i.e. those who do not provide documentation (regardless of US Citizenship for tax purposes or not) to be closed.

Given that the forthcoming CRS26 (Common Reporting Standard) covers 94 jurisdictions27, if the same logic were applied, account holders of an additional 94 jurisdictions could potentially have their accounts closed, simply because they are a tax resident of one of those 94 jurisdictions.

So why would established financial institutions close accounts of Americans if the regulation does not demand it?

Perhaps there are four reasons:

1. Groupthink. They see their peers in the industry are doing the same thing and follow unquestioningly.

2. Risk Mitigation – current business. Given the size of the fines and concomitant reputational damage, perhaps Financial Institutions simply offboard American accounts due to the fear of the US regulator applying fines to the FI.

3. Risk mitigation – previous business. Perhaps, as a result of OVDP, an FI perceives a likelihood of investigation and the FI closes all accounts to demonstrate contrition and “lessons learned” in order to mitigate any penalties.

4. Any combination of the three above.

In any event, this does demonstrate the fear of US regulatory authorities that FATCA creates and the counterintuitive ways in which this fear can manifest itself.

26 http://www.oecd.org/ctp/exchange-of-tax-information/implementation-handbook-standard-for-automatic-exchange-of-financial-information-in-tax-matters.pdf

27 http://www.oecd.org/ctp/exchange-of-tax-information/Status_of_convention.pdf

http://haydonperryman.com No claim to original Government, EU or OECD works Page 9

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

Senior Management will want to be in a position to evidence that they made every effort to comply. This will include taking the very best advice and evidencing “concrete” policies and procedures. That said, perhaps off-boarding Americans carte blanche is overzealous to say the least and, given that the CRS introduces a further 94 jurisdictions, is unsustainable. After all, if account holders from 95 tax jurisdictions (94 plus the USA) are off-boarded, would what is left still represent a viable customer base?

****

Closely associated regulations

Amongst those regulations closely associated with FATCA (Chapter 4 of the US Code) and the Local Statutory Instruments triggered by the FATCA IGAs28 (that have material differences to the US Treasury Regulations) are:

1. Chapter 3 of the US Tax Code 29 aka “Qualified Intermediary” or “1441 NRA regulations” – with which many Financial Institutions are not fully compliant. Non-Compliance with Chapter 3 also carries all the risks mentioned earlier in this chapter.

2. 871(m) 30 . Informally known in the industry as “Dividend Equivalents”, 871(m) was recently revised, and, perhaps because of the product mapping (to Financial Account Type) that FATCA necessitates is often associated with FATCA.

3. CDOT 31. Informally known as “UK FATCA”, CDOT looks for Brits among the UK’s three Crown Dependencies and seven overseas territories. It is worth pointing out that this regulation includes not only the UK but also the Cayman Islands. These are not small considerations. CDOT will eventually be superseded by the CRS but it is not yet clear whether this will be before 2017 Reporting. CDOT more closely mirrors the CRS because, firstly, there is no withholding and, secondly, a combination of unilateral and bilateral reporting. Indeed, some in the industry refer to CDOT as CRS in microcosm.

4. CRS. Of course, there is the CRS itself which is naturally of a volume of reporting far greater than FATCA itself by virtue of the 96 tax jurisdictions that are participating and the myriad of unilateral, bilateral and multilateral reporting arrangements between them.

These associated regulations carry with them their own “fear factor”: the fear of siloed 32 compliance that leads to complying with closely related regulations one-at-a-time when there may otherwise be synergies by combining compliance efforts.

The FATCA Project Manager

Hence, the FATCA Project Manager finds him or herself managing a hotspot of anxiety and is very rarely managing FATCA in isolation. Unless a tailored approach is adopted, their FATCA project may well consist principally of:

Fear, 28

http://www.treasury.gov/resource-center/tax-policy/treaties/Pages/FATCA-Archive.aspx29

https://www.law.cornell.edu/uscode/text/26/subtitle-A/chapter-330

https://www.law.cornell.edu/uscode/text/26/871#m31

https://www.gov.uk/government/publications/automatic-exchange-of-information-agreements-other-uk-agreements/automatic-exchange-of-information-agreements-other-uk-agreements

32 http://www.oxforddictionaries.com/definition/english/silo

http://haydonperryman.com No claim to original Government, EU or OECD works Page 10

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

Acrimony, Turbulence and Constant Adjustment.

While constant adjustment is a necessary feature of managing any FATCA Project fear, acrimony and turbulence can be mitigated against with a few simple steps, and I shall explain how.

Content. In the industry, there are many schools of thought about how much a Project Manager should know about the Subject Matter – not project management itself, but in this context, FATCA itself i.e. how much the project manager should know about:

1. The US Treasury FATCA regulationsa. FINAL FATCA Regulations [TD9610] 33 b. Temporary FATCA Regulation [TD9657] 34

c. Noticesd. Announcementse. Revenue Proceduresf. IRS website FAQsg. Official explanationsh. Publicationsi. Technical Specifications andj. Instructions

2. The IGAs3. The differences between the US Treasury Regulations, the IGAs and how

to navigate those differences4. The CRS5. Chapter 3 of the US Tax Code6. EU Council Directive 2014/107/EU35 (informally “DAC2”)7. 871(m)

Opinions vary. Sometimes those PMs who do not know much about the regulation are referred to as “Content-free”. This is by no means a compliment. However, on the “flip side” a PM who knows the regulation inside out can be perceived as Subject Matter Expert (SME).

Having a PM who is perceived as an SME carries its own risks:

1. Where FATCA expertise is in scarce supply, the PM can find him or herself in constant demand from parts of the FATCA program that are not under his or her remit. The consequences of this might be that the Project Management itself suffers and that the Project team are not given the necessary focus.

33 http://www.irs.gov/PUP/businesses/corporations/TD9610.pdf

34 http://www.irs.gov/pub/irs-utl/FATCA-Temporary-and-Final-Regs-under-chapter-4.pdf

35 http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014L0107&from=EN

http://haydonperryman.com No claim to original Government, EU or OECD works Page 11

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

2. SMEs are de facto not necessarily regarded as Project Managers. While a knowledge of the regulation must be helpful, knowledge of the regulation is not the same thing as leadership.

3. The more the PM knows about the regulations, the more likely it is that they will want to contribute at the thought leadership level. Senior Management, at the thought leadership level, are typically supported by the Project Manager rather than challenged.

4. The stronger the perceived level of Subject Matter Expertise, the greater the risk that the PM is perceived as acting unilaterally and “doing FATCA to us”. It is necessary that those heavily impacted by the project have the perception of control.

5. The Project Manager is typically someone who coordinates to achieve an agreed path to success and, thus, is a facilitating coordinator rather than someone who sets the direction. Subject Matter Expertise may inadvertently cause the PM to lead where he or she should, instead, be looking others to agree on the direction. Having facilitated such a consensus, the PM would oversee the day-to-day management of activities consistent with that direction.

6. A person who claims two areas of expertise is often, rightly or wrongly, perceived as an expert in neither.

On the converse, a lack of expertise carries its own risk, principally that of building a runway in the wrong country i.e. achieving consensus in pursuing the entirely incorrect path. In the context of FATCA, this carries very real danger. For example, I have seen more than one Financial Institution build Withholding engines exclusively for FATCA, which cost tens of millions to build and are almost entirely unnecessary.

All agree, however, that a Project Manager, regardless of their knowledge of FATCA and related regulations, must have the core Change Management skills traditionally associated with a PM.

Further, all agree that FATCA expertise is required somewhere on the FATCA Program.

My recommendation is that FATCA expertise reside in at least two positions.I. At the Project Management level andII. At the Group Tax level

I believe that both are necessary. To explain why I will use the example of a live performance of Classical music. In this example, the Group Tax SME is the Composer, and the PM is the Conductor.

The role of the Group Tax SME

To explain further, the Group Tax SME composes a compilation of various compositions:

1. US Treasury FATCA2. IGA Models 1a & 1b3. IGA Model 24. Harmony on (1), (2) and (3). (Which as other chapters illustrate is no small

thing.)5. UK FATCA

http://haydonperryman.com No claim to original Government, EU or OECD works Page 12

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

6. CRS and DAC236

7. The differences between FATCA and the CRS and what that will mean for On-boarding, Remediation and Reporting

8. 871(m)9. Mapping Products to Financial Account Type and 871(m)10.Chapter 3.

How the FATCA PM and Group Tax SME complement each other

The Group Tax SME brings together this compilation in the form of two artefacts:

1. The FATCA Policy (see Chapter X) and2. The Rule Map

An explanation of the rule map will follow.

In such a way, the FATCA Policies and rules are seen, quite correctly, as coming from Group Tax.

The Project Manager’s role is simply to coordinate and conduct.

Further, the PM would “be doing FATCA to”, no one; rather, he or she is simply interpreting the Composers composition (albeit a compilation).

In practical terms, what this means is that the PM facilitates the transition of the FATCA Policy and Rule-map into:

1. Business Requirements2. Volume calculations i.e. define the size of the ask3. Scope. Following the lead set out in the FATCA Policy and Rule-map, the project

may (or may not) include US Tax Code Chapter 3 and 871m37 but may include:a. “US FATCA”. This includes:

i. US Chapter Four – for the US and Non IGA tax jurisdictionsii. Model 1 IGAs (both 1A & 1B)iii. Model 2 IGAs

b. CDOT aka UK FATCAc. CRS and DAC2

4. Reporting Relationships: i.e. which jurisdiction(s) a particular jurisdiction reports to for each regulation and a target operating model for the same

5. Detailed Project Plans (what need to be delivered, by when and by whom)6. Dependencies, Risks and Issues7. Roles and Responsibilities8. Shaping the correct teams and skill sets9. Target Operating Models10.Product-Based-Deliverables (this will be explained later in this chapter)

Naturally stakeholders and the PM can question the composition itself but importantly the question goes to the Group Tax SME rather than the PM.36

http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32014L0107&from=EN37

It may be that the approach for mapping Products to Financial Account Type (§1.1471-5(b)), for FATCA reporting processes has to be synchronized with any mapping for 871(m) compliance.

http://haydonperryman.com No claim to original Government, EU or OECD works Page 13

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

In my experience, challenges to the FATCA Policy and Rule-maps typically go to the PM so that he or she makes sure that they are opined upon on a timely basis but, importantly, the PM should not opine themselves.

In such a way, the PM retains their role as Conductor (facilitator) rather than Composer rather than both Conductor and Composer (judge, jury and executioner). The PM must be free to adopt a facilitative approach rather than an evaluative approach. 38

The more a PM is forced to adopt an evaluative approach, the greater the fear of FATCA within the organization i.e. the perception that FATCA is being done to us by a PM, who is playing the role of judge, jury and executioner.

Naturally, the corollary is the expertise in Group Tax.

Real examples that demonstrate the need for a content rich FATCA PM, a high calibre Group Tax FATCA SME and why the two roles are symbiotic

It is often underestimated how much FATCA Policies and Rule-maps need to be opined upon. What seems simple at 30,000 ft does not always seem simple when the ‘rubber meets the road’. Here are examples not only of where a Group Tax SME must opine but also of where experts are needed in both Group Tax and on the Project. The examples also demonstrate the calibre of expertise required of the Group Tax SME.:

1. Non-coterminous reporting periods. Whilst most jurisdictions report calendar years, South Africa and New Zealand do not. (South Africa reports the year to the end of February. New Zealand reports the year to the end of March.) Such issues typically are identified at the project level. However, they inevitably are resolved at the FATCA Policy (Group Tax SME) level. To illustrate, it may be that the FATCA Policy of the FI is to take a snapshot, for balance reporting purposes, at the end of Dec 31, each year. However, the policy may change to taking three snapshots: Dec 31, March 31 and the end of February.) This in turn will affect IT and the Target Operating Model.

2. “Sensitive jurisdictions”. Some jurisdictions such as Hong Kong, Mexico and Brazil may not allow customer data to be held at other locations. The FATCA Policy may be that all data is reported on so must be available in, say, London (in order to cover APAC and American time-zones as well as European time-zones). In this example, it may not be possible to report for these jurisdictions in line with FATCA Policy. Group Tax, as owners of the FATCA Policy, would be required to opine.

3. Can we assume that all Model 1 jurisdictions will have their own unique schema rather than adopt the US schema? Further, can we assume that they will not use “IDES”? Probably not: Singapore (an IGA Model 1 jurisdiction), for example, has elected to use the US XML schema and IDES. Other jurisdictions may follow. Also, XML schemas and their convergence may evolve into one standard in order to facilitate CRS compliance.

38 http://www.mediate.com/articles/zumeta.cfm

http://haydonperryman.com No claim to original Government, EU or OECD works Page 14

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

4. Can we assume an IGA Model 2 jurisdiction will always be an IGA Model 2 jurisdiction? No, the CRS is based on the Model 1 IGA. Hence, those Model 2 jurisdictions may seek to achieve efficiencies by migrating to a Model 1 IGA. Switzerland is an example of this scenario.

5. Atypical reporting jurisdictions. FATCA Policy may be that reporting is always conducted via Host Country Tax Authority Portals. However, Luxembourg, at the time of writing, had no such portal. Instead, either Fundsquare 39 or Sofie40 have to be used, neither of which is free. It may be that the Group Tax SME is aware of pre-existing relationships with either company for the purposes of other tax / regulatory reporting.

6. NP-FFI. The FATCA Policy may be that a customer can only have one FATCA Classification. However, in truth it may not be so simple. From a US point of view, ABC British Bank might be an NPFFI simply because it has not provided a GIIN. However, from a UK point of view, ABC British Bank is quite clearly an IGA Model 1 Reporting FFI. Should the FATCA Policy be amended? (An item for the Group TAX SME). If yes, what are the implications for IT? (An item for the PM) What if the de facto Target Operating Model only allowed for one FATCA Classification? Importantly, while the US part of the Bank would classify its client as an NP-FFI and withhold, parts of the Bank in IGA countries could not do the same because the path to becoming an NP-FFI in an IGA jurisdiction is altogether different. A true Group Tax FATCA SME will be aware of this.

The IGAs each state that a Financial Institution in an IGA Jurisdiction can only become “Non-Participating” after “significant non-compliance”. “Significant non-compliance” does vary by IGA. For example, Japan(IGA Model 2), has a path to resolution that lasts for a year. The UK has a path to resolution that lasts for 18 months. In any event, only when the time allowed for resolution has elapsed can an FFI in an Inter Governmental Agreement Jurisdiction be “Non-Participating”. Hence, shortly, there should be no withholding, on NP-FFIs from FIs in IGA jurisdictions.

The US Treasury definition of a Non Participating Foreign Financial Institution reads:

“The term non-participating FFI means an FFI other than a participating FFI, a deemed-compliant FFI, or an exempt beneficial owner.”

However, there is a variation on how the notion of Non Participating Foreign Financial Institution is applied. For example, here is a quote from the UK Inter Governmental Agreement. Article 4, Section 1:

“Notwithstanding the foregoing, a Reporting United Kingdom Financial Institution with respect to which the conditions of this paragraph are not

39 https://www.fundsquare.net/about

40 http://www.cetrel.lu/fr/home/financial-institutions/shared-service-solutions/sofie.html

http://haydonperryman.com No claim to original Government, EU or OECD works Page 15

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

satisfied shall not be subject to withholding under section 1471 of the U.S. Internal Revenue Code unless such Reporting United Kingdom Financial Institution is identified by the IRS as a Nonparticipating Financial Institution pursuant to subparagraph 2(b) of Article 5″

Under this particular Inter Governmental Agreement, in this particular Jurisdiction, in order to apply withholding, the US Internal Revenue Service has actually to identify the Reporting UK FI as Non-participating.

Further, 2(b) of Article 5, of the UK IGA41, reads:

Significant Non-compliance. a) A Competent Authority shall notify the Competent Authority of the other Party when the first-mentioned Competent Authority has determined that there is significant non-compliance with the obligations under this Agreement with respect to a Reporting Financial Institution in the other Jurisdiction. The Competent Authority of such other Party shall apply its domestic law (including applicable penalties) to address the significant non-compliance described in the notice. b) If, in the case of a Reporting United Kingdom Financial Institution, such enforcement actions do not resolve the non-compliance within a period of 18 months after notification of significant non-compliance is first provided, the United States shall treat the Reporting United Kingdom Financial Institution as a Non-participating Financial Institution. The IRS shall make available a list of all Reporting United Kingdom Financial Institutions and other Partner Jurisdiction Financial Institutions that are treated as Non-participating Financial Institutions pursuant to this paragraph.

7. “Other Income”. It may be observed that “Other Income” has a different definition in every jurisdiction. (The statement may or may not be true.) This ought to be raised as a Risk or Issue by the PM to the Group Tax SME rather than opined upon by the PM directly. The PM may well know what the solution should be, but I would argue that his or her role should be to facilitate rather than evaluate.

8. How is Other Income Reported?

9. On-boarding individuals without documentation.

41 http://www.treasury.gov/resource-center/tax-policy/treaties/Documents/FATCA-Agreement-UK-9-12-2012.pdf

http://haydonperryman.com No claim to original Government, EU or OECD works Page 16

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

While the IRS makes it clear that new individual accounts cannot be on-boarded without documentation:

http://www.irs.gov/Businesses/Corporations/Frequently-Asked-Questions-FAQs-FATCA--Compliance-Legal#GeneralQ10

If a Reporting Model 1 FFI or a Reporting Model 2 FFI that is applying the due diligence procedures in section III, paragraph B, of Annex I of the IGA cannot obtain a self-certification upon the opening of a New Individual Account, can the FFI open the account and treat it as a U.S. Reportable Account?

No. Pursuant to section III, paragraph B, of Annex I of the IGA, the FFI must obtain a self-certification at account opening. If the FFI cannot obtain a self-certification at account opening, it cannot open the account

SIFMA makes a counter argument:

http://www.sifma.org/issues/item.aspx?id= 8589953814 http://www.sifma.org/comment-letters/2015/sifma-submits-comments-to-treasury-department-regarding-fatca-faq-10-letter/

“It is our understanding that the guidance in FAQ 10 – – which refers to Model 1 IGAs – – is inconsistent with the published guidance of several IGA countries, including the United Kingdom and Canada. In particular, we understand that both the Government of the United Kingdom and the Canadian Government have taken the position that FIs (including USFIs) operating within the UK and Canada are not required to refuse to open or close a new individual account in the event they are not able to obtain a self-certification. Instead, under the UK and Canadian guidance, FIs are instructed to treat such accounts as reportable accounts.”

My experience is that this is precisely the kind of issue that gets addressed to the PM. This is a very good example of an issue that should be opined upon by a Group Tax SME rather than the PM.

The FATCA Policy may be that no account is on-boarded without documentation. However, as a matter of practicality the Policy may allow for, say, exceptions that are signed off by the appropriate authority. If that is the case, the Group TAX SME and the Project Manager would need to collaborate in order to ensure that such instances are picked up by the reporting team because undocumented accounts are reportable. Group Tax SMEs may not immediately identify this. However, it is precisely the sort of dependency that a content rich FATCA PM should immediately recognise.

Further collaboration would be required to ensure that the policy is consistent with closely associated regulations, for example, the CRS. The CRS does not allow onboarding without documentation.

http://haydonperryman.com No claim to original Government, EU or OECD works Page 17

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

The point here is that the PM should not evaluate but should facilitate. It is for Group Tax to opine. A PM should not railroad the onboarding team. However, it is appropriate for such a steer to come from Group Tax.

10.Mapping Products to Financial Account Types (for Reporting Purposes). An SME, who does not have a detailed understanding of FATCA but has come from a background of US Tax Code Chapter 3 compliance, may well determine what Products need to be mapped by first determining whether products are capable of receiving US income. While such an approach works for Chapter 3, it does not work for Chapter 4. There are many reasons for this, not least of which is that Non-US income is reportable under Chapter 4 but not Chapter 3. Also, the Project Manager ought to identify the potential to synergize any product mapping for FATCA purposes with 871(m). (871(m) is not part of Chapter Four.)

11.The accuracy of W8s. Even before FATCA’s inception, only 35% of W8s were fit for claiming treaty relief. (This is explained at length in Ross K McGill’s “US Withholding Tax”, 201342.) A Group Tax SME with Chapter Three experience will recognise that some W8s that are received from customers will need to be re-solicited. This is a point that might not be obvious to the PM and serves to illustrate that an SME is required from Group Tax. This point illustrates the need for Chapter Three experience. The former point explains why Chapter Three experience, on its own, is not sufficient.

12.Regional awareness of FATCA. I notice three distinct FATCA paradigms and they are split between regions (APAC, EMEA and the Americas). In the Americas, the paradigm is very much that of the US Tax Code and views IGAs as something of a side issue. In Europe, the paradigm is very much that of the IGAs: no withholding 43, no Responsible Officer44 and views the US Treasury Regulations as something of a side issue. Meanwhile, in the Middle East, Africa and APAC, awareness of FATCA

42 http://www.amazon.com/Withholding-Tax-Practical-Implications-Financial/dp/0230364616/ref=sr_1_1?s=books&ie=UTF8&qid=1441638119&sr=1-143 The IGAs also, for the most part, remove withholding intra IGA Jurisdictions.

“If Model 1 partner countries comply with Article 2 as well as the “Time and Manner of Exchange of Information” agreed to in Article 3 and other rules, then their reporting FFIs “shall be treated as complying with, and not subject to withholding under, section 1471,” nor will they be required to withhold “with respect to an account held by a recalcitrant account holder” under § 1471.”

DoJ Response, “Case: 3:15-cv-00250-TMR Doc #: 16”. August 12, 2015, pp. 6-7.

44 The role of the Responsible Officer and related attestations that the RO has to provide are not mentioned in the IGAs, nor in the Common Reporting Standard.

Hence, there is no legal instrument to enforce a Responsible Officer to take on personal liability in an Inter Governmental Agreement Model 1 IGA Jurisdiction . However, the same cannot be said of an IGA Model 2 Jurisdiction because FFIs in Model 2 Jurisdictions enter into a Foreign Financial Institution Agreement (FFI-A) with the IRS. FFI-As include both the personal liability of the Responsible Officer (§1.1471-4) and Attestations.http://haydonperryman.com No claim to original Government, EU or OECD works Page 18

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

is, perhaps, still at its earliest stages. Evidence of this can be seen in the relatively low rate of GIIN registrations45 in APAC, Africa and the Middle East.

The role of bringing APAC, Africa and the Middle East up to speed ought to be aided by the Group Tax SME rather than left to the Project Manager. However, the Project Manager must assist, not least because they are best placed to explain the operational issues and mitigations.

Additionally, it may be that compliance with Chapter Three, for whatever reason (possibly awareness), is less strong in APAC and the Middle East. The Group Tax SME is best placed to explain any Chapter Three implications.

13.Training thought leaders and new FATCA team members. It may be that amongst Senior Management perceptions of FATCA have become entrenched. The Group Tax SME is best placed to dispel any myths and to train any new members of the FATCA Compliance Teams. In both cases, the PM would have a supporting role. Naturally, a PM ought not to be teaching Senior Managers about FATCA; that important role falls more naturally to Group Tax.

14.Making Changes to FATCA Policy and Rule-maps. Only Group Tax can make such changes. That said, they should be heavily supported by the PM. PM support should include:

Identifying exceptions where FATCA Policy may not be practical Handling any requests for dispensations to FATCA Policy Evidencing good faith46 attempts to comply with the FATCA

Policy and Rule-maps Managing any dependencies between FATCA Policy and Rule-

maps with other Projects. For example, Product Mapping to Financial Account Type47 and any synergies that may be possible with 871(m)48 compliance

Ensuring that the FATCA Policy and Rule-maps are re-base-lined every quarter. (If the Rule-map is not rebaselined there is a risk that the Project deliverables will address an obsolete understanding of the Regulations. Further, if the Rule-map is not regularly revised , there is a danger that its citations are incorrect.)

Configuration Management 49. Ensuring that all Project Deliverables that are based on the FATCA Policy and Rule-map are clearly and separately identified. For example, if, the FATCA Policy was that all Treasury Centres are always FFI, and if, say, the CBT, (Computer Based Training) that is mandatory for all staff reflects that all Treasury Centres are FFI, that, when the

45

http://apps.irs.gov/app/fatcaFfiList/flu.jsf46

In Notice 2014-33 the IRS declared 2014 and 2015 transitional years for FATCA. So long as companies can evidence good faith attempts to comply with FATCA it is unlikely that the IRS will make an example of them. Importantly “good faith” must be proved by having policies and procedures in place and evidencing that those policies and procedures were complied with.

47 http://www.law.cornell.edu/cfr/text/26/1.1471-5#b

48 http://www.law.cornell.edu/uscode/text/26/871#m

49 https://en.wikipedia.org/wiki/Configuration_management

http://haydonperryman.com No claim to original Government, EU or OECD works Page 19

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

FATCA Policy is revised, that the CBT is revised accordingly and to an appropriate timescale.

Ensuring that all Project Deliverables are clearly referenced to a particular section of the Rule-map. So that it is clear:

How each rule will be complied with, by when, how and by whom That each deliverable is mapped to a regulatory requirement, so

that, if and when a regulation or guidance changes, impacted project deliverables can be immediately be identified.

15.When is UK FATCA replaced by the CRS? In truth, at the time of writing nobody knows that answer to this. What is known is that it will, in time be superseded by the CRS. The question is, will this be before or after reporting on 2016, in 2017 has been completed? Guidance from HMRC is expected “any day now”. However, it appears that even amongst the exclusive population privileged to see a preview of this guidance, precisely when the CRS replaces CDOT is still to be determined. So what should be the planning assumptions? Again, the answer ought to come from Group Tax rather than the PM. Without such guidance, typically the PM will plan for the worst. To be fair, it is very difficult for Group Tax to issue such guidance because nobody knows. Hence, the de facto position appears to be, assume the worse i.e. assume FY 2016 is still reportable under CDOT (even though this means duplicative reporting of the same data.) Importantly, this is not a decision a PM should be expected to make unilaterally.

16.Regarding the CRS, how do we onboard for the CRS those jurisdictions that are not amongst the 94 jurisdictions who have committed to a deadline for information exchange? Here the Group Tax SME and the PM need to collaborate because whilst this is probably a Group Tax call, in order to make this call, Group Tax need to understand the impact on Onboarding Teams, IT, Target Operating Models and the general Business Benefits, Costs, Risks and Issues of various approaches. In all likelihood accounts on-boarded for account holders in any tax jurisdiction, MCAA members or not, will be the same, if only because no-one knows what further jurisdictions may yet sign up to the MCAA.

17.Excluded Accounts. Here the calibre of the Group Tax SME is telling. If the Group Tax SME does not have a detailed understanding of the IGAs, then they will, in all likelihood, be unaware of the excluded accounts that are listed in Annex II of each tax jurisdiction’s IGA. The lead on Excluded Accounts must come from Group Tax rather than the PM. However, mapping those Excluded Accounts to the Bank’s Products falls under of purview of the PM.

18.Which IGA to apply? Some FIs believe that the IGA to apply is the IGA of the jurisdiction of the bank that holds the account. Other FIs believe the IGA to apply is the IGA in which the account holder has tax residency. (In many cases the former and the latter are the same. However, not all FI agree on which IGA to apply where the former and the latter are not the same.) I, have my interpretation. However, what is most germane is that Group Tax opine and enshrine this into their FATCA Policy and Rule-maps. It is the PM’s job to shape the FATCA Policy and Rules-maps into Products and to deliver those Products to plan.

It is, however, worth pointing out the “Partner Jurisdiction Accounts” covered in the “Excluded Accounts” section of Annex II of the IGAs.

http://haydonperryman.com No claim to original Government, EU or OECD works Page 20

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

An account maintained in [a particular IGA jurisdiction] and excluded from the definition of Financial Account under an agreement between the United States and another Partner Jurisdiction to facilitate the implementation of FATCA, provided that such account is subject to the same requirements and oversight under the laws of such other Partner Jurisdiction as if such account were established in that Partner Jurisdiction and maintained by a Partner Jurisdiction Financial Institution in that Partner Jurisdiction.

19.Responsible Officer. While the IGA Model 1 and the CRS make no mention of the Responsible Officer; the Responsible Officer exists in the Treasury Regulations (§.1471-450) that the US and Non IGA jurisdictions must apply. This concept also exists in the FFI Agreement that FFIs in Model 2 jurisdictions must apply. This is a Group Tax call rather than a PM call. However, most FIs seem to agree that they want to apply the RO concept across all jurisdictions and apply it to not only FATCA but also to CDOT and the CRS. The adoption of the RO concept seems to be perceived as best practice. One variation is to differentiate between Responsible Officers in Model 1 IGA Countries by, instead, labelling those in IGA Model 1 jurisdictions “Responsible Executives”.

20.Balance Reporting. (End of Year Balance, Average Balances, Highest Balance.) Here is another example of ‘one size not fitting all’. Some IGA Countries opt for average balance reporting rather than end of year reporting. The FATCA Policy may be for end of year balances, converted into USD at the spot rate at the end of the year. However, as highlighted above, not all jurisdictions have coterminous financial years. Also, FATCA does allow reporting in local currency. This is an example of where the FATCA Policy will probably explicitly allow certain exceptions. This is a Group Tax call, but it may well be the PM who makes Group Tax aware of these exceptions and calls for a revised FATCA Policy.

21. Income Reporting. FATCA reporting for 2014, which was reported in 2015, included only balances as, under the regulations, only balances were reportable for FY 2014. However, as we report in 2016 on 2015, income is also reportable. A PM without an understanding of US Tax Code Chapter Three may be of the opinion that Income Reporting is new. However, a Group Tax SME whose knowledge includes Chapter Three will know that Income Reporting in the form of 104251 and 1042-S52 is far from new. What is new, however, is reporting Non-US income. Under this example, the PM and the Group Tax SME would need to collaborate amongst themselves and others to form an agreed view on how to map non-US income for FATCA reporting purposes.

22.Under UK FATCA and the CRS, are Active NFFEs, whose shares are not actively traded on a recognised exchange, reportable? The answer must come from Group Tax and become part of the FATCA Policy and Rule-map.

50 http://www.law.cornell.edu/cfr/text/26/1.1471-4

51 http://www.irs.gov/pub/irs-pdf/f1042.pdf

52 http://www.irs.gov/pub/irs-pdf/f1042s.pdf

http://haydonperryman.com No claim to original Government, EU or OECD works Page 21

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

23.What is the delta between CRS and FATCA and how should that delta be managed?

Known additional fields required for AEI/CRS:

i. Individuals: Place of birth. (However, the place of birth is not required to be reported unless the Reporting Financial Institution is otherwise required to obtain and report it under domestic law. Place of Birth, in this context, means Country of Birth and should, ideally be mapped to an ISO 3166 code53. However, mapping to an ISO 3166, in this context, is not a regulatory requirement.)

ii. Individuals and Entities: Tax Residences (Multiple), TIN or a valid reason a TIN is not provided. A TIN is not required

where:o a TIN is not issued by the relevant Reportable Jurisdiction

oro the domestic law of the relevant Reportable Jurisdiction

does not require the collection of the TIN issued by such Reportable Jurisdiction.

iii. Entities: Place of Incorporation Place of Organization AEI Status (AEI Status is not always going to be the same as

FATCA Status)

The US W8 series, in their current form, do not provide for CRS compliance:

The W8 BEN 54 does not capture the place of birth. In most IGA Countries, determining whether a Passive NFFE is

Reportable depends on identifying Controlling Persons55 (CP), rather than identifying US Beneficial Owners (USBO). The W8 series, for Passive NFFEs, identifies USBO, rather than CP.

CRS compliance requires, for entities, thiero Place of Incorporation, ando Place of Organization

The W8 series do not capture multiple tax residences

(Although not an issue directly pertaining to “US FATCA” or closely associated regulations, it would also be logical to include the LEI (Legal Entity Identifier) for Entities in order to facilitate compliance with some other regulations including Dodd-Frank and EMIR.)

53 http://data.okfn.org/data/core/country-list

54 http://www.irs.gov/pub/irs-pdf/fw8ben.pdf

55 http://www.henkjanvanderklis.nl/2013/09/fatca-means-business-how-to-recognize-a-controlling-person/

http://haydonperryman.com No claim to original Government, EU or OECD works Page 22

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

Navigating an approach to the delta between FATCA and the CRS should first begin with Group Tax agreeing what the deltas are and also whether alternatives to the W8s are acceptable and under what circumstances and in which tax jurisdictions.

* * * *

These examples may seem trivial, but they are real-life, everyday examples of issues that come to the FATCA PM, upon which he or she is often asked to opine by stakeholders of varying degrees of seniority and at considerable speed. Naturally, these should go to the Group Tax SME to opine upon.

These issues are too voluminous, time-consuming and counterintuitive for the PM to handle on an ad-hoc basis. Further, the PM needs the freedom to deliver on an agreed understanding of FATCA that has been shaped by Group Tax, rather than carry the burden of dispelling widely held beliefs.

Further, the PM needs to be afforded the time to ensure that those on the Project Team understand and accept what they are doing and how it fits into the broader picture of FATCA compliance. Project Team members need clear, agreed deliverables. In the complex world of FATCA, this takes time to achieve. Therefore, the same individual cannot, at, the same time, take on the additional roles and responsibilities that really ought to be undertaken by Group Tax.

Furthermore, the PM needs to be afforded the time and freedom to adopt a facilitative approach in order to build relationships outside his or her own Project Team. Success cannot be attained or sustained without building those relationships and building these relationships is not easily achieved if an evaluative approach is forced upon the PM.

The issue is not only one of time management but also one of management approach. The more the PM has to perform Group Tax responsibilities, the more that person is forced to take an evaluative approach rather than a facilitative approach. In the long run, the Project Manager must be free to adopt a facilitative approach. Hence, a FATCA PM is only as strong as their Group Tax SME counterpart.

This is all the truer given the climate of fear that FATCA generates.

Essentially project management is about three things:

1. Defining where we are, where we want to be and building and managing to, a plan to fill the gap

2. Risk and Issue Management3. Communicating with people in such a way the people are happy to follow

Without robust Group Tax SME support, the Project Manager’s ability to deliver those three things is handicapped because:

1. There is no agreement on where we need to be.2. The Risks and Issues are confused because there is no Group Tax owned and

up-to-date FATCA Policy and Rule-map that have been socialised and understood

http://haydonperryman.com No claim to original Government, EU or OECD works Page 23

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

3. The PM cannot take people with him or her if his or her style of communication is evaluative rather than facilitative as a result of having to educate stakeholders about what FATCA is and is not.

Supporting the Group Tax SME

Regarding the Group Tax SME, naturally their opinions on issues relating, say, to the examples above need to be made available quite rapidly to stop unnecessary uncertainty infecting the project. Therefore, the Group Tax SME needs to be afforded the time to respond to such questions on an ad-hoc basis. This is no small task: it requires a skilled, and therefore presumably expensive resource, to have enough space capacity to deal with impromptu questions as they are received. The Group Tax SME needs to be afforded the time to study and read in detail. Such a role also requires heavy support from Group Tax, the Project Sponsor and, of course, the Project Manager.

It is unlikely that many Group Tax SMEs have a depth of Change Management experience. However, the wave of regulatory change relating to tax matters looks set to continue into the foreseeable future. Hence, Group Tax will increasingly become high profile stakeholders and key contributors to Change Management.

A reiterative to shaping and reshaping FATCA Policy and Rule-maps

The nature of the FATCA Policy and Rule-maps are such that it will be necessary to rebaseline them once a quarter, or thereabouts.

I have seen Rule-maps that have not been revised since before the temporary regulations that were published in February 2014. This means that the rule map does not map to the sections of the regulations it cites. Worse, a great deal has happened in the world of UK FATCA and the CRS since February 2014 – none of this will have been reflected. This can quite literally lead to complying with an obsolete understanding of FATCA and associated regulations. This is not the ‘happy path’ should the bank later seek to rely on its rule-map as a “line in the sand” against which to evidence good faith attempts to comply with FATCA.

The FATCA Policy contains high-level policies and splits them out by: Governance and RO Attestations Withholding (if applicable) Reporting Documentation (Onboarding and Remediation)

The FATCA Policy Document is high level, but it will be explicit about exceptions.

Potential exceptions to FATCA Policy may be identified by the Project Manager and raised as Project Issues, together with associated details such as jurisdiction, division and product and explanation as to why an exception may be necessary or why the Policy may need to be revised.

When these Policies are first drafted they appear to be common sense. However, it is only when the Project is underway that exceptions are typically identified. Such exceptions include South Africa and New Zealand having non-coterminous reporting periods.

http://haydonperryman.com No claim to original Government, EU or OECD works Page 24

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

It is only when such potential exceptions are raised that it becomes clear that some FATCA policies may need to be adjusted because they are impractical in reality.

However, the FATCA Policy comes first so that there is an agreed view on what compliance looks like; then comes the rule map that breaks down the FATCA Policies perhaps by On-boarding, Remediation, Reporting, Withholding and Governance and perhaps splits these out by geographies and Business Divisions at a very detailed level.

Every one of these details carries a unique reference that relates to a Project-Based-Product Deliverable.

Often, it is only when you allocate such a deliverable to a named individual that local impediments become known and can be flagged.

Hence, such impediments, when flagged to the PM, can be identified as potential adjustments to the FATCA Policy and fed into a judicious process of FATCA Policy and Rule-map revision.

Equally, whenever Regulations or Guidance are revised, it will be necessary to update the FATCA Policy and Rule-maps and all the Project artefacts that are based on Rules/Policies that have changed.

Product Based Project Deliverables & Planning

Project Based Planning is a well-established PM method. Therefore, I will not describe it here but, for those who wish to know a little more about it, a link is provided here:

https://en.wikipedia.org/wiki/Product-based_planning

The genesis of each FATCA Project Product is its description in the Rule-map.

Feel free to generate your own nomenclature. But whatever nomenclature you use56, a unique reference for a Rule/Product will probably look something like this.

20150901.FATC.000000.826.CDD.W8ONB.IB.AAAA

Date of Revision (YYYYMMDD), Regulation (FATC, AEOI, CDOT, 871M, CHP3) Policy Reference, ISO3166 Country Code, Concept (REP, CDD, GOV, WHG) Concept Reference Number (this example might be whether an alternative to

a W8 is acceptable) Division (e.g.,. IB = Investment Banking) Financial Product Reference (not to be mistaken for Project Product)

Hence, this example would be the FATCA Policy for Onboarding, in the UK, in the Investment Banking Division. In particular, this rule will tell me if an alternative to the W8 is acceptable. It will also tell me what part of the FATCA Policy this relates to and

56 This nomenclature could also be used to create an XBRL taxonomy so that information sharing between business divisions of large FIs is standardized.

http://haydonperryman.com No claim to original Government, EU or OECD works Page 25

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

when that policy was last revised. It will also tell me if that Policy includes this particular Financial Product.

Why go into such detail? So that rules can be “sliced by diced” so that one can query rules by, say, division or product, or country. Project artefacts can also be mapped to these codes so that it is known which rules they are designed to comply with. Further, projects artefacts can be mapped to the rule ID so that compliance with a rule can be evidenced by specific artefacts.

The beauty of this approach is that they can be grouped into logical clusters: say, financial products types, geographies or business units to suit the structure of the individual FI. They can be assigned an owner, and their delivery can be tracked. The same is true should ownership change due to the business restructuring and/or the FATCA Policy and Rule-maps changing.

Scope of the “FATCA” Project

In my opinion, the scope of the “FATCA” Project should include:

i. “US FATCA”, Model 1 IGAs Model 2 IGAs US Treasury Regulation (Chapter 4 of the US Tax Code)

ii. UK-CDOT, iii. CRS and DAC2

and out of scope should be:

i. Chapter 3, ii. and 871(m)

Of course, every project may be shaped differently, and there are valid reasons for having various other regulations in or out of the scope of Projects that, de facto, carry the FATCA moniker.

Conclusion

1. Recruit FATCA Subject Matter Expertise amongst both Project Managers and Group Tax. Both types of SME are required to sustain delivery.

2. Define the Scope (i.e. what FATCA related regulations are in or out of scope – and why).

3. Define compliance by use of a Rule-Map and Policy – split into Project-Deliverable Products.

4. Use Product Based Planning as an approach to breakdown deliverables into “bite sizes”. Group these Products according to the structure of the Business.

5. All Project Products (not to be confused with Financial Products) must be mapped to the Rule-map.

6. The Policy and Rule Map must be formally rebaselined every quarter.

http://haydonperryman.com No claim to original Government, EU or OECD works Page 26

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

7. Plan:I. Split Compliance by Regulation (possibly also by Division,

Jurisdiction/Region) – group into products using Product Based PlanningII. Start “right to left” i.e. begin with what has to be reported, to whom and by

when, for which regulation.

Key Points:

1. UK FATCA is superseded by AEI only after FY2016 reporting is complete.2. UK FATCA has two iterations of reporting. The first is for both 2014 and 2015, in this particular

context 2014 begins July 1.3. For the UK FATCA income is reportable for all of FY2016.4. US FATCA and AEI will continue to co-exist for the foreseeable future. The US has not signed up

to the AEI.5. AEI has two categories of jurisdictions Early Adopters and those other than Early Adopters. The

deadlines for those jurisdictions other than Early Adopters are one year after those for Early Adopters.

6. South Africa and New Zealand reporting periods are non-coterminous: South Africa's reporting period is to the end of February New Zealand's reporting period is to the end of March

III. Map Project-Deliverable-Products to every regulatory report requirement identified in II.

IV. Project Plan based on III. Milestone each Product or Group of Products.V. Schedule quarterly baselines of the FATCA Policy and Rule-map.VI. Schedule concomitant revisions to Project-Deliverable-Products as a result

of V.

8. Implement full change control over FATCA Policy and Rule-maps including why they changed, who changed them, who signed off on these changes and when these changes happened.

9. Map Financial Products to Financial Account Type – without this mapping it will not be possible to Report Income.

10.Evidencing good faith attempts to comply with FATCA and related regulations is every bit as important as compliance itself and, until 100% compliance is achieved, is probably your best line of defence against fines and concomitant reputational damage. Artefacts that can help evidence good faith attempts to comply will include:

FATCA Policy and changes, together with the associated rationale for the change.

Rule-maps and changes, together with the associated rationale for the change.

Mapping delivered Project Products to rules in the Rule-map Quality Assurance that Project Products are fit for purpose i.e.

meets compliance with the rule in the rule map that caused their inception.

“Vanilla” Project Documents including RAIDDS log Gantt Charts (and revisions) Progress/Highlight/Update Reports Minutes from Steering Committee Meetings

http://haydonperryman.com No claim to original Government, EU or OECD works Page 27

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

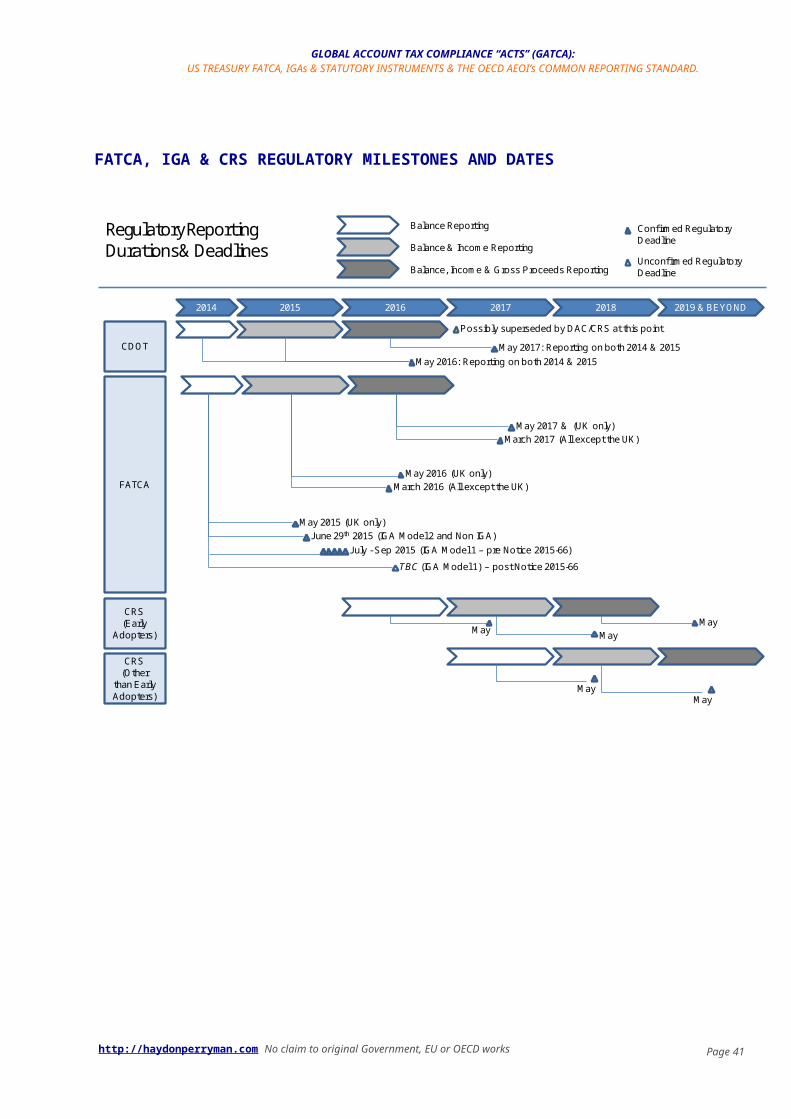

FATCA, IGA & CRS REGULATORY MILESTONES AND DATES

Conf irmed Regulatory Deadline

Unconf irmed Regulatory Deadline

2019 & BEYOND20182017201620152014

CDOT

FATCA

CRS(Early

Adopters)

CRS(Other

than Early Adopters)

2014

2014 Balance Reporting

Balance & Income Reporting

Balance, Income & Gross Proceeds Reporting

Possibly superseded by DAC/CRS at this point

May 2016: Reporting on both 2014 & 2015May 2017: Reporting on both 2014 & 2015

2014

May 2015 (UK only)June 29th 2015 (IGA Model 2 and Non IGA)

July - Sep 2015 (IGA Model 1 – pre Notice 2015-66)

TBC (IGA Model 1) – post Notice 2015-66

May 2016 (UK only)March 2016 (All except the UK)

May 2017 & (UK only)March 2017 (All except the UK)

Regulatory Reporting Durations & Deadlines

May MayMay

MayMay

http://haydonperryman.com No claim to original Government, EU or OECD works Page 28

GLOBAL ACCOUNT TAX COMPLIANCE “ACTS” (GATCA):US TREASURY FATCA, IGAs & STATUTORY INSTRUMENTS & THE OECD AEOI’s COMMON REPORTING STANDARD.

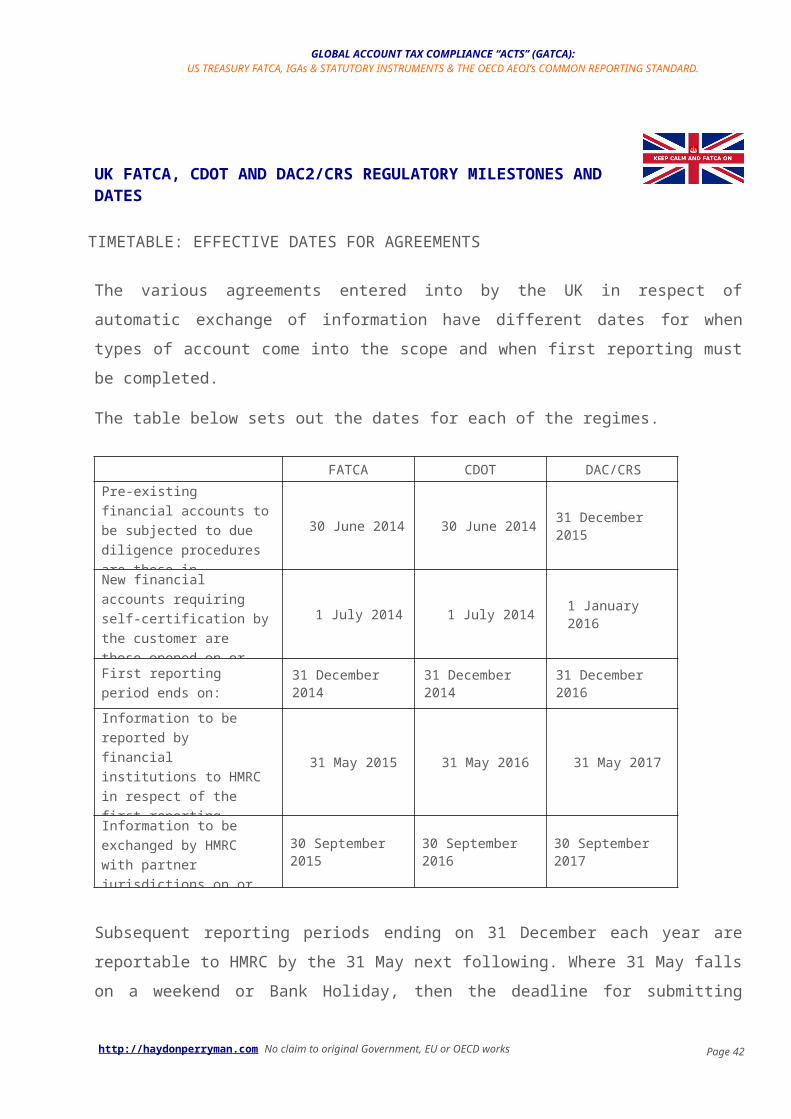

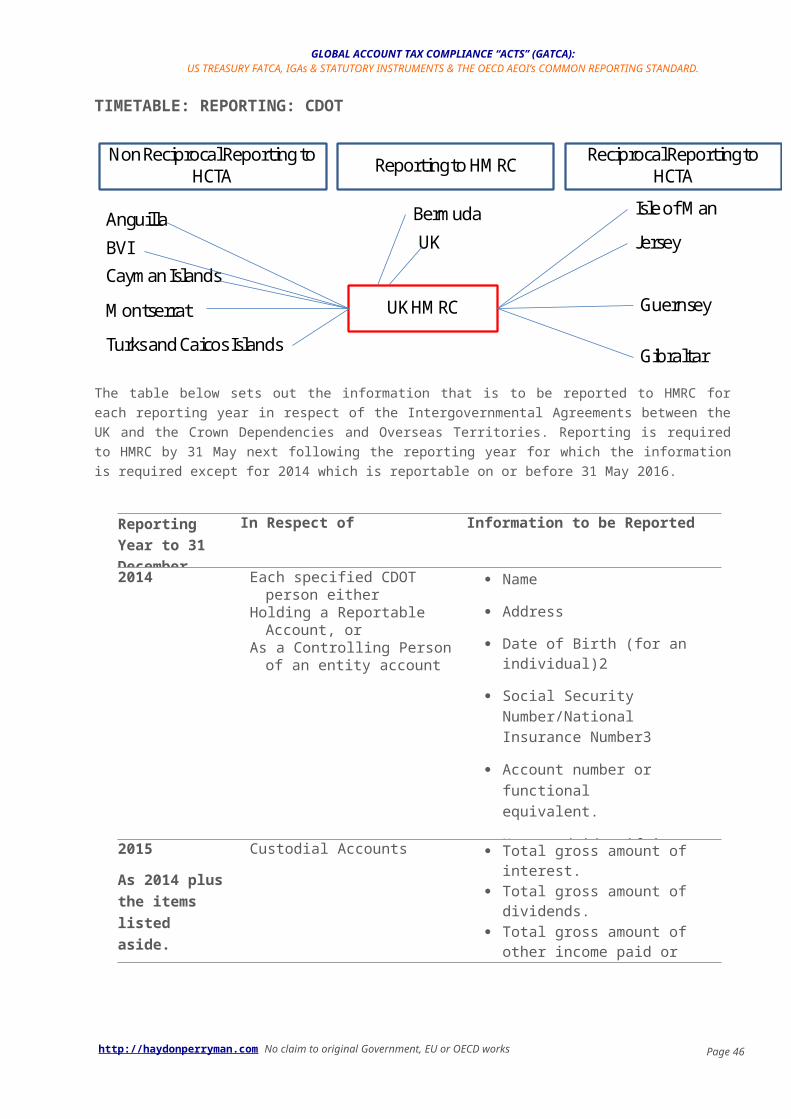

UK FATCA, CDOT AND DAC2/CRS REGULATORY MILESTONES AND DATES

TIMETABLE: EFFECTIVE DATES FOR AGREEMENTS

The various agreements entered into by the UK in respect of automatic exchange of information have different dates for when types of account come into the scope and when first reporting must be completed.

The table below sets out the dates for each of the regimes.

FATCA CDOT DAC/CRS

Pre-existing financial accounts to be subjected to due diligence procedures are those in existence as at:

30 June 2014 30 June 2014 31 December 2015

New financial accounts requiring self-certification by the customer are those opened on or after:

1 July 2014 1 July 2014 1 January 2016

First reporting period ends on: 31 December 2014 31 December 2014 31 December 2016

Information to be reported by financial institutions to HMRC in respect of the first reporting period on or before: