introduction to ifrs 3 & consolidation - ibr-ire.be · ias 28 investments in associates ias 27...

TRANSCRIPT

Introduction to IFRS 3 & Consolidation

Introduction to IFRS 3 & ConsolidationPage 2

Content

►

Consolidation►

IFRS 3 in a nutshell

►

Business Combination vs Asset Acquisition►

Defining a business

Introduction to IFRS 3 & ConsolidationPage 3

Where do we come from?

1 January 2005 1 July 2009

Be GAAP

IAS 27 + SIC 12

IAS 27 revised

ED 10

?

Control-based approach

Consolidation

g}} ERNST & YOUNG Qu"lity fn E,~ryt"jng We 00

Introduction to IFRS 3 & ConsolidationPage 5

Consolidation in IFRS An Overview

►

IAS 27 Consolidated and Separate Financial Statements►

IAS 28 Investments in Associates

►

IAS 31 Interests in Joint Ventures►

SIC-12 Consolidation -

Special Purpose Entities

Introduction to IFRS 3 & ConsolidationPage 6

IFRS - Consolidation Scope

►

IFRS requires each investment to be screened using the following decision tree:

CONTROL

JOINTCONTROL

SIGNIFICANT INFLUENCE

IAS 39

Fullconsolidation

Equity or Proportionateconsolidation

Equity consolidation

yes

yes

yes

no

no

no

Introduction to IFRS 3 & ConsolidationPage 7

IAS 27 Consolidated Financial Statements Main features

►

All subsidiaries must be consolidated in the parent financial statements. ►

Limited exemption to avoid preparing consolidated financial statements

►

Uniform accounting policies must be used in the group►

Non-controlling interests must be presented separately within equity

►

In separate financial statements, investments in subsidiaries must be accounted at cost or in accordance with IAS 39►

Not applicable in Belgium

Introduction to IFRS 3 & ConsolidationPage 8

IAS 27 Consolidated Financial Statements Exemption from presentation

►

The parent is itself a subsidiary►

The ultimate parent of the parent produces consolidated financial statements that comply with IFRS and are available for public use

►

The parent is not a listed public company or is not in the process of being one.

►

Complies with 7th directive of the European Council

Introduction to IFRS 3 & ConsolidationPage 9

IAS 27 Consolidated Financial Statements Exemption from presentation

►

Intermediate Holding Company

P

S1 S2

D1 D2

40%

100%

60%

100%

P: IFRS financial statement preparerS2: In listing process

Hence:

IFRS requirement to prepare IFRS

financial statements

NO EXEMPTION !!

Introduction to IFRS 3 & ConsolidationPage 10

IAS 27 Consolidated Financial Statements Concept of control

►

Control is the power to govern the financial and operating policies of an entity so as to obtain benefits from its activities.

►

Presumed to exist when the parent owns more than half the voting power of an entity

►

The parent also has control, even if it owns less than half of the voting rights, if it has power ►

over more than half of these rights, because of an agreement with other investors

►

to govern the financial and operating policies of the subsidiary under a statute or an agreement

►

to appoint or remove a majority of the directors►

to cast a majority of the votes at directors' meetings

Guidance on application can be found in US GAAP: EITF 96-16

Introduction to IFRS 3 & ConsolidationPage 11

IAS 27 Consolidated Financial Statements an example from Alliance Pharma Plc (2009)

32. JointVenture

Nam~

l!n'r-"9 l.! d

Princ ip;o l Act ivity

Distr ib ul i"" 01 p h~rmac~L1 ~~ I prodCO:h

CO'"'"'t ')' oI l ncorp or~t i on

8 rilis h Virgi n 5i<>nd,

" Ow n~

Th~ Group con,idcred the ~~,tcnc~ 0/ ,u bst~rI "" part ici pat in g r ':l ht , he ld by l h~ mno rily , ha reholder which pr"" i'" l"'t , ha reholder wil h ~ ","0 ri ght ""cr th~ '':l nil ica nt l i", ncia l and opcrat ng po l ~ ',. 0/ Un':l r"l Lt d ~ n d detNmned tha t. ~,~ r<"Sult 01 H ... "" r ':l ht , . l h~ Group does rol h""", cont ro l """,r l h~ l i", ncia l and opcrat in g po l ~ io, 0/ Un':l r"l Lt d. <J.'pito I"" Gro up ·.1'(1" ow ne",hi p n te "" l

:JJ ERNST & YOUNC Qo<,o,;". .. C"'?''"''s ~ 00

Introduction to IFRS 3 & ConsolidationPage 12

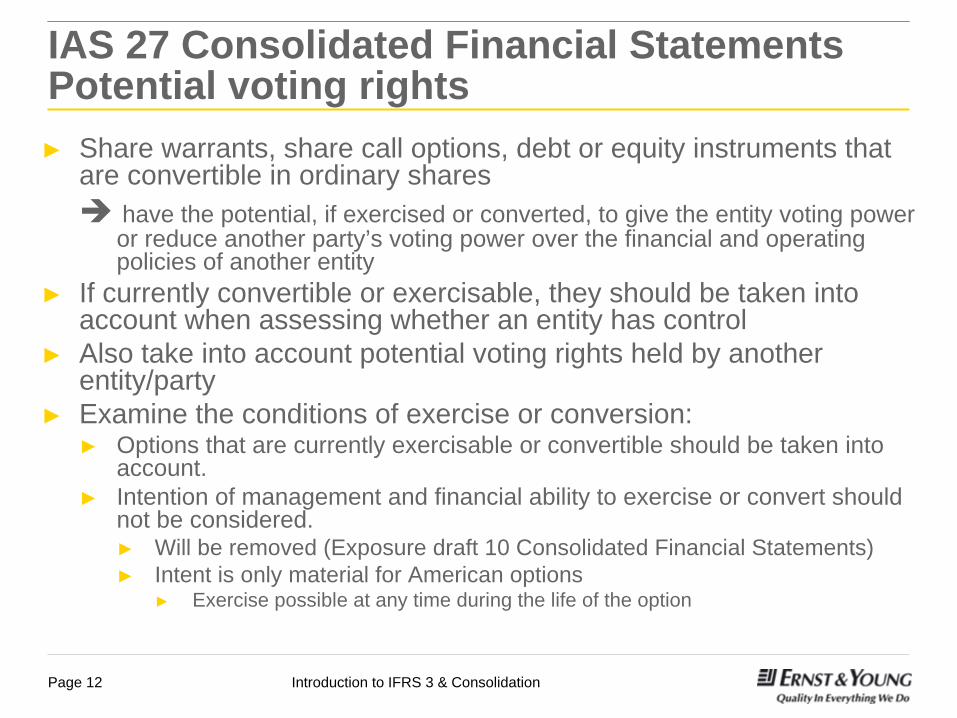

IAS 27 Consolidated Financial Statements Potential voting rights►

Share warrants, share call options, debt or equity instruments that are convertible in ordinary shares

have the potential, if exercised or converted, to give the entity voting power or reduce another party’s voting power over the financial and operating policies of another entity

►

If currently convertible or exercisable, they should be taken into account when assessing whether an entity has control

►

Also take into account potential voting rights held by another entity/party

►

Examine the conditions of exercise or conversion:►

Options that are currently exercisable or convertible should be taken into account.

►

Intention of management and financial ability to exercise or convert should not be considered.►

Will be removed (Exposure draft 10 Consolidated Financial Statements)►

Intent is only material for American options►

Exercise possible at any time during the life of the option

Introduction to IFRS 3 & ConsolidationPage 13

IAS 27 Consolidated Financial Statements Potential voting rights►

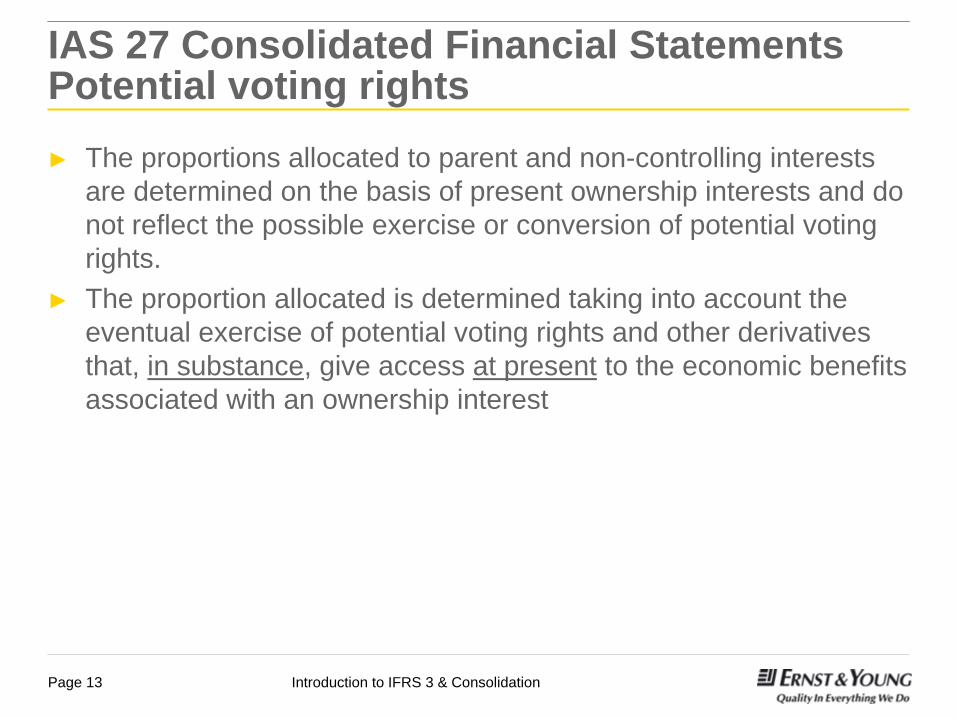

The proportions allocated to parent and non-controlling interests are determined on the basis of present ownership interests and do not reflect the possible exercise or conversion of potential voting rights.

►

The proportion allocated is determined taking into account the eventual exercise of potential voting rights and other derivatives that, in substance, give access at present

to the economic benefits

associated with an ownership interest

Introduction to IFRS 3 & ConsolidationPage 14

IAS 27 Consolidated Financial Statements Potential voting rights – Example 1

►

Entity A sells one-half of its interest to Entity D►

Entity A buys call options from Entity D

►

exercisable at any time at a premium to the market price when issued ►

for the 40 % ownership interest and voting rights that were sold

►

Entity A could exercise options at any time►

power to continue to set the operating and financial policies of

Entity C►

Potential voting rights are considered (amongst others) in par 13 of IAS 27

►

Entity A controls entity C

A B

C

20 %80 %

Introduction to IFRS 3 & ConsolidationPage 15

IAS 27 Consolidated Financial Statements Potential voting rights – Example 2

►

Entity A also owns call options ►

Exercisable at any time►

Would give additional 20% of voting rights in D►

Would decrease interests of entity B and entity C in entity D to 20 % each

►

Potential voting rights,as well as the other factors described in paragraph 13 of IAS 27 and paragraphs 6 and 7 of IAS 28 are considered and it is determined that Entity A controls Entity D

A B

D

30%40 %

C

30 %

Introduction to IFRS 3 & ConsolidationPage 16

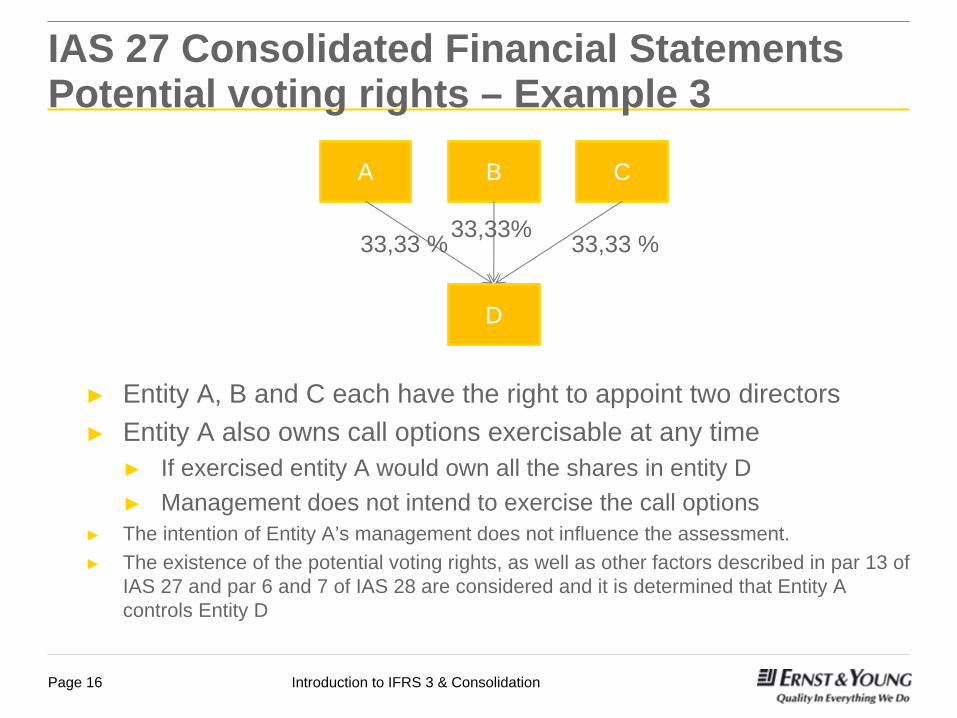

IAS 27 Consolidated Financial Statements Potential voting rights – Example 3

►

Entity A, B and C each have the right to appoint two directors►

Entity A also owns call options exercisable at any time►

If exercised entity A would own all the shares in entity D►

Management does not intend to exercise the call options►

The intention of Entity A’s management does not influence the assessment.►

The existence of the potential voting rights, as well as other factors described in par 13 of IAS 27 and par 6 and 7 of IAS 28 are considered and it is determined that Entity A controls Entity D

A B

D

33,33%33,33 %

C

33,33 %

Introduction to IFRS 3 & ConsolidationPage 17

►

IAS 27 does not

allow a subsidiary to be excluded from consolidation simply because►

It operates under severe long-term restrictions that impairs its ability to transfer funds to the parent (control must be lost for exclusion

to

occur)►

Its business activities are dissimilar from those of the other entities within the group.

►

The control is temporary►

The parent is a venture capital, mutual fund, or similar entity.

►

This differs from Belgian GAAP / Company Law

IAS 27 Consolidated Financial Statements Exemption to include a subsidiary

Introduction to IFRS 3 & ConsolidationPage 18

IAS 27 Consolidated Financial Statements Consolidation procedures►

Line-by-line combination of financial statements

►

Elimination of the parent’s investment in subsidiaries and its portion of their equity

►

Separate presentation of the non-controlling interest share in the profit or loss and in net assets.

►

Elimination in full of intra-group balances, transactions, income and expenses, and dividends

►

Elimination in full of unrealised profits and losses but intragroup losses may indicate impairment that requires recognition

►

Adjustments to align accounting policies

Introduction to IFRS 3 & ConsolidationPage 19

IAS 27 Consolidated Financial Statements Non-controlling interests (NCI)

►

Definition of a minority interest (MI): ►

Minority interest is that portion of the profit or loss and net assets of a subsidiary attributable to equity interests that are not owned, directly or indirectly through subsidiaries, by the parent

►

What is NCI?►

“Non-controlling interest (NCI) is the equity in a subsidiary not attributable directly or indirectly to a parent.”

►

Focus is on equity instruments not owned by the parent.

►

Choice of two methods of measurement:►

Fair value at the date of control –

full goodwill method►

Share of the value of the net assets of the acquiree –

the partial goodwill method

►

Choice for each acquisition –

not an accounting policy

►

Determining fair value of non-controlling interest►

Exchange price includes a control premium?

Introduction to IFRS 3 & ConsolidationPage 20

Definition of non-controlling interest (cont.)

►

Question:►

Is there a difference between MI and NCI?

►

Example:►

Parent owns 80% of a subsidiary►

At 1/1/2009 the net assets of the subsidiary are CU1,000

►

On 1/1/2009 the subsidiary writes a call option over its own shares and receives CU 50

►

Two approaches

to accounting for this transaction in the consolidated accounts:►

Increase of CU 40 in equity attributable to owners of the parent and an increase in non-controlling interest of CU 10

►

Increase in non-controlling interest of CU 50

Parent

Subsidiary

80%CU 800

NCI or MI20%

CU 200

Option holder

Options CU 50

CU1,000

Introduction to IFRS 3 & ConsolidationPage 21

Definition of non-controlling interest (cont.)

►

This has far reaching consequences if the entire payment for the options is treated as NCI:►

Options are currently not treated as MI►

The issuance of the following instruments by a wholly-owned subsidiary might give rise to non-controlling interests:►

convertible debt and other compound financial instruments►

warrants►

options over own shares►

options under share-based payment plans►

Considerable challenges in accounting for equity instruments that a party somewhat less than a present ownership interest in a consolidated subsidiary

Equity instruments as NCI

Introduction to IFRS 3 & ConsolidationPage 22

IAS 27 Consolidated Financial Statements Non-controlling interests

►

Attribution of losses►

Profit or loss and each component of other comprehensive income►

Attributed to owners of the parent►

Attributed to the non controlling interests

►

Even if this results in the non-controlling interests having a deficit balance

accounting for NCI's share of losses

Introduction to IFRS 3 & ConsolidationPage 23

IAS 27 Consolidated Financial Statements Change in ownership

►

Accounting for loss of control ►

Derecognition►

Assets and liabilities of former subsidiary►

Any non-controlling interest in former subsidiary►

Recognition ►

Fair value of any received consideration►

Any distribution of shares to owners in their capacity as owners►

Impact on profit or loss or retained earnings►

Any amounts in OCI that would be reclassified at disposal►

Recognition any resulting difference as a gain or loss attributable to the parent

Disposal of a subsidiary

Reclassification of other comprehensive

Introduction to IFRS 3 & ConsolidationPage 24

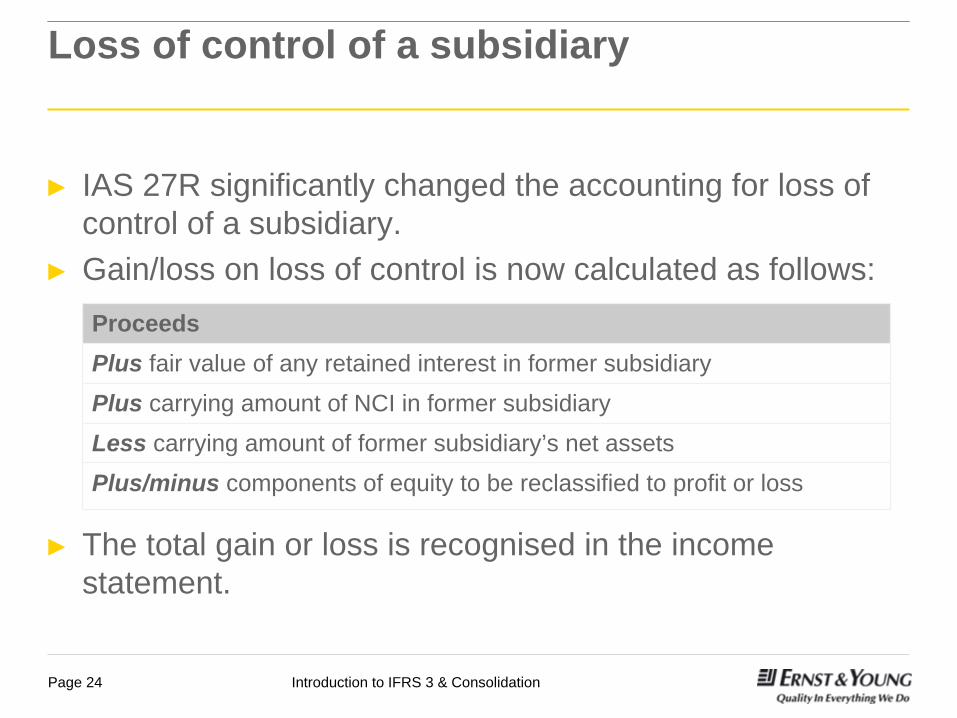

Loss of control of a subsidiary

►

IAS 27R significantly changed the accounting for loss of control of a subsidiary.

►

Gain/loss on loss of control is now calculated as follows:

►

The total gain or loss is recognised in the income statement.

ProceedsPlus fair value of any retained interest in former subsidiary

Plus carrying amount of NCI in former subsidiary

Less carrying amount of former subsidiary’s net assets

Plus/minus components of equity to be reclassified to profit or loss

Introduction to IFRS 3 & ConsolidationPage 25

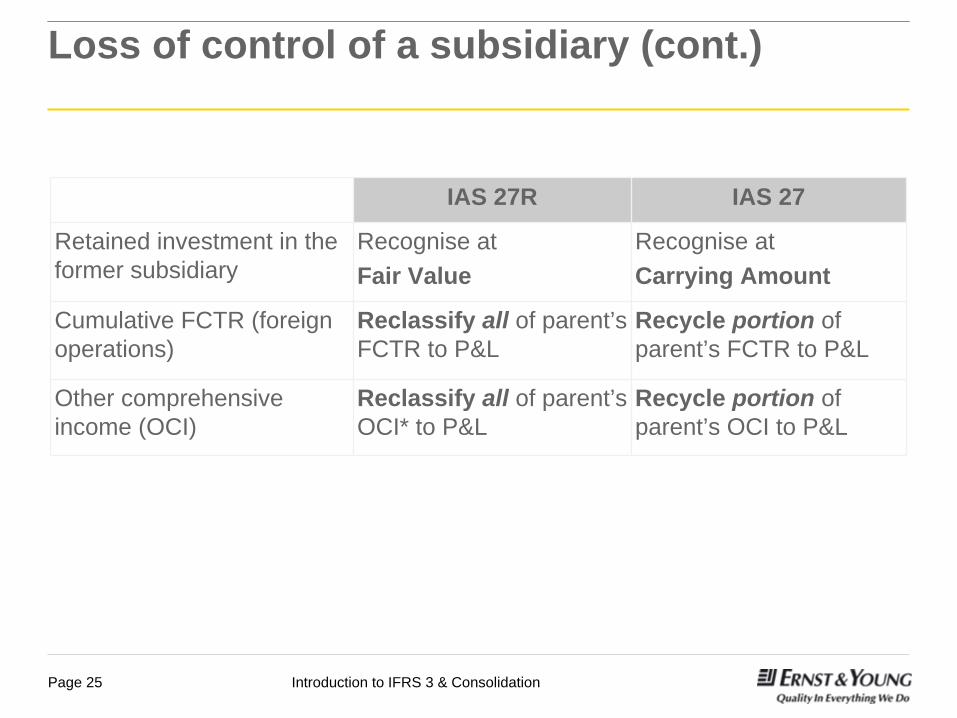

Loss of control of a subsidiary (cont.)

IAS 27R IAS 27

Retained investment in the former subsidiary

Recognise at Fair Value

Recognise at Carrying Amount

Cumulative FCTR (foreign operations)

Reclassify all of parent’s FCTR to P&L

Recycle portion of parent’s FCTR to P&L

Other comprehensive income (OCI)

Reclassify all of parent’s OCI* to P&L

Recycle portion of parent’s OCI to P&L

* Only if required to be recycled.

Introduction to IFRS 3 & ConsolidationPage 26

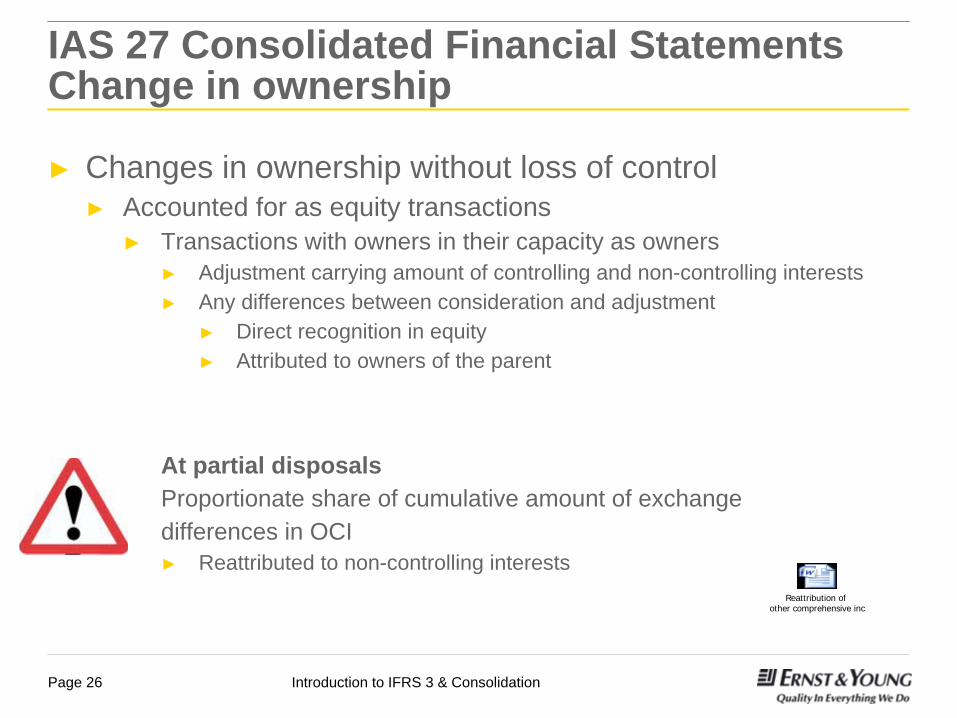

IAS 27 Consolidated Financial Statements Change in ownership

►

Changes in ownership without loss of control ►

Accounted for as equity transactions►

Transactions with owners in their capacity as owners►

Adjustment carrying amount of controlling and non-controlling interests►

Any differences between consideration and adjustment►

Direct recognition in equity►

Attributed to owners of the parent

At partial disposalsProportionate share of cumulative amount of exchangedifferences in OCI ►

Reattributed to non-controlling interestsReattribution of

other comprehensive inc

Introduction to IFRS 3 & ConsolidationPage 27

Step acquisitions

New Old

Calculation of goodwill

Remeasurement of net assets relating to pre- existing interests

Remeasurement of pre- existing interest to fair value

Measurement of identifiable net assets

One goodwill calculation at acquisition date

Not applicable

Recognise in profit or loss

Fair value at acquisition date

Fair value at acquisition date

Not applicable

Accounted for as a revaluation

Numerous goodwill calculations –

for each exchange transaction

Introduction to IFRS 3 & ConsolidationPage 28

Step acquisitions (cont.)

►

Pre-existing interests►

Obtaining control of an entity is a significant economic event►

Transfer any related available-for-sale (AFS) reserve to profit or loss

►

Determination of the fair value of pre-existing non- controlling equity investments

►

Based on current consideration transferred?►

Discounted as a “minority”

or “non-controlling”

interest?

Introduction to IFRS 3 & ConsolidationPage 29

IAS 28 Investments in Associates Key definitions►

An associate is an entity over which the investor has significant influence and which is neither a subsidiary nor a joint venture of the investor.

►

Significant influence is the power to participate in the financial and operating policy decisions of an investee, but is not control over these policies►

This is presumed to exist if the investor holds 20% or more of the voting power and presumed not to exist if it holds less than 20%. Either presumption is rebuttable

►

The existence and effect of potential voting rights currently exercisable or convertible have to be taken into consideration in assessing significant influence

Introduction to IFRS 3 & ConsolidationPage 30

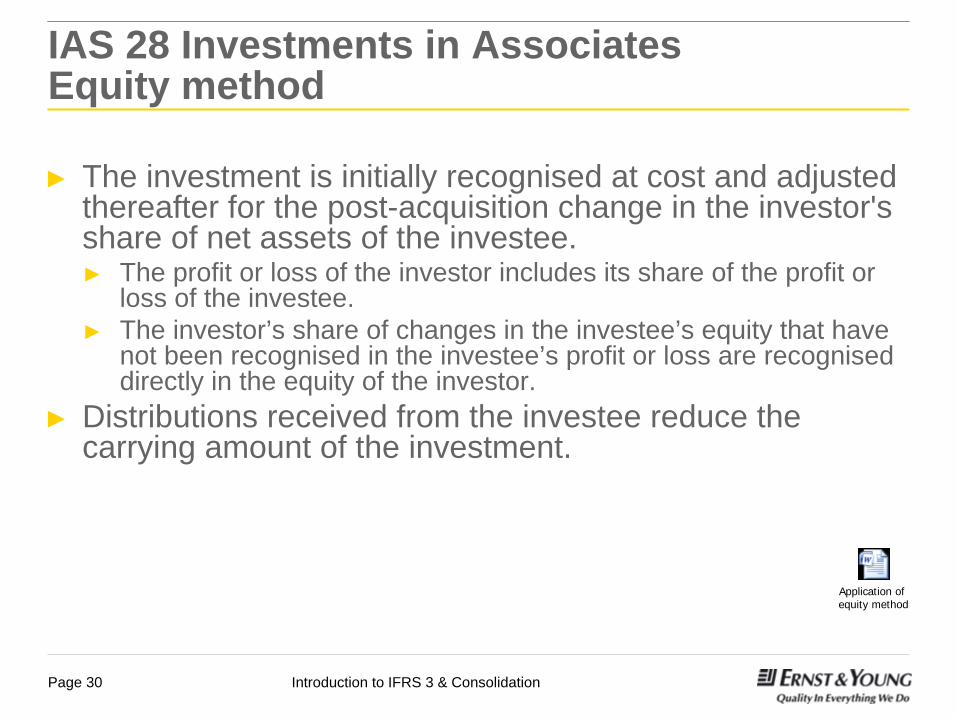

IAS 28 Investments in Associates Equity method

►

The investment is initially recognised at cost and adjusted thereafter for the post-acquisition change in the investor's share of net assets of the investee.►

The profit or loss of the investor includes its share of the profit or loss of the investee.

►

The investor’s share of changes in the investee’s equity that have not been recognised in the investee’s profit or loss are recognised directly in the equity of the investor.

►

Distributions received from the investee reduce the carrying amount of the investment.

Application of equity method

Introduction to IFRS 3 & ConsolidationPage 31

►

On acquisition of an associate, any difference between the cost of the investment and the investor’s share of the fair values of the associate’s net identifiable assets is treated as goodwill

►

Goodwill relating to an associate is included in the carrying amount of the investment, and the whole amount of the investment (rather than the goodwill) is tested for impairment

►

Any negative goodwill is taken directly to income

IAS 28 Investments in Associates Goodwill

Introduction to IFRS 3 & ConsolidationPage 32

►

IAS 28 prescribes the accounting treatment for investments in associates in separate financial statements (by reference to IAS 27)

►

IAS 28 requires an entity to consider the potential voting rights when assessing significant influence

►

IAS 28 does not require the equity method when an associate is acquired with a view to be disposed of (IFRS 5)

►

IAS 28 require to have uniform accounting policies in investor and associate’s financial statements

IAS 28 Investments in Associates Equity method

Introduction to IFRS 3 & ConsolidationPage 33

►

Profits or losses resulting from upstream and downstream transactions between the investor or its subsidiaries and its associate are recognised in the investor’s financial statements to the extent of unrelated investor’s interests in the associate

►

The investor’s share in the associate’s profits and losses resulting from these transactions is eliminated

IAS 28 Investments in Associates Transactions with Associates

Q&A Elimination of profits and losses re

Introduction to IFRS 3 & ConsolidationPage 34

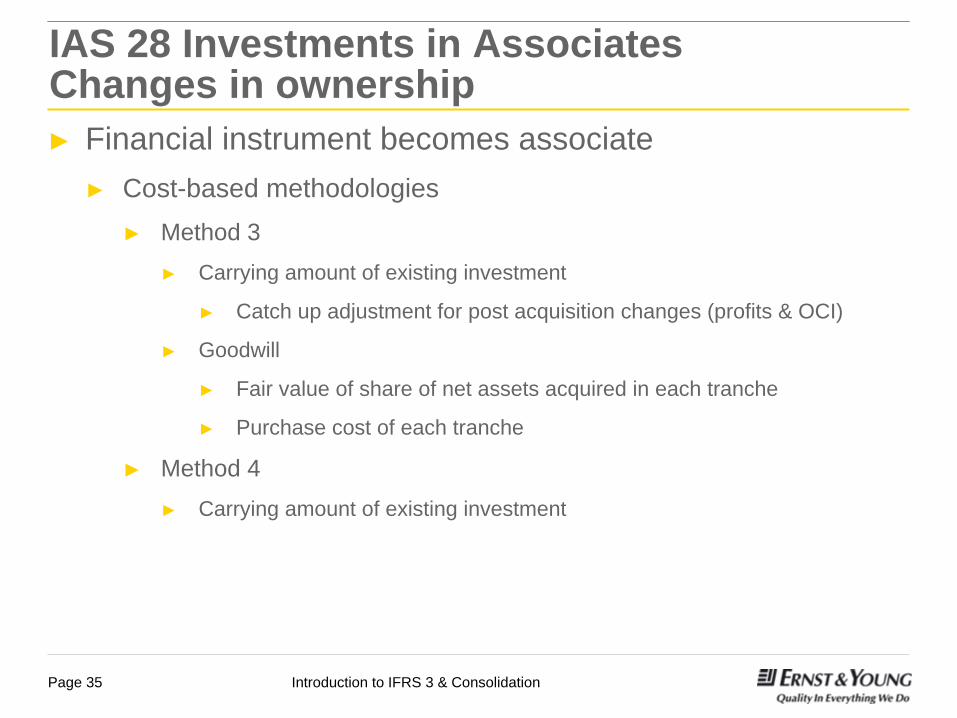

►

Financial instrument becomes associate►

Unclear guidance

►

Cost-based methodologies (based on IFRIC discussions)►

Method 1 (one goodwill calculation)►

Carrying amount = initial cost to purchase financial instrument

►

Goodwill = fair value of share of net assets –

carrying amount

►

Method 2 (separate goodwill calculation)►

Carrying amount = initial cost to purchase financial instrument

►

Goodwill

►

Fair value of share of net assets acquired in each tranche

►

Purchase cost of each tranche

IAS 28 Investments in Associates Changes in ownership

Introduction to IFRS 3 & ConsolidationPage 35

►

Financial instrument becomes associate►

Cost-based methodologies►

Method 3►

Carrying amount of existing investment

►

Catch up adjustment for post acquisition changes (profits & OCI)

►

Goodwill

►

Fair value of share of net assets acquired in each tranche

►

Purchase cost of each tranche

►

Method 4►

Carrying amount of existing investment

IAS 28 Investments in Associates Changes in ownership

Introduction to IFRS 3 & ConsolidationPage 36

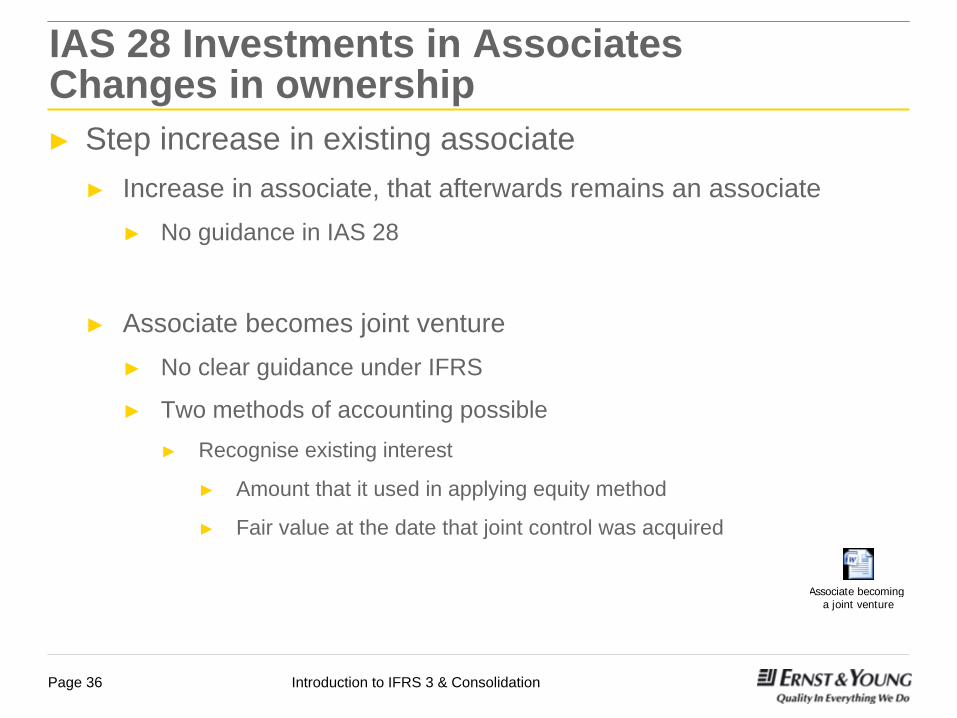

►

Step increase in existing associate►

Increase in associate, that afterwards remains an associate►

No guidance in IAS 28

►

Associate becomes joint venture►

No clear guidance under IFRS

►

Two methods of accounting possible►

Recognise existing interest

►

Amount that it used in applying equity method

►

Fair value at the date that joint control was acquired

IAS 28 Investments in Associates Changes in ownership

Associate becoming a joint venture

Introduction to IFRS 3 & ConsolidationPage 37

►

Associate becomes a subsidiary►

Previously held equity is re-measured at fair value at acquisition date►

Gain or loss recognised in profit or loss

►

Previously recognised changes in value of equity interest in OCI►

Reclassified to profit or loss

►

Fair value of previously held equity►

Part of business combination (in acquisition method)

IAS 28 Investments in Associates Changes in ownership

Associate becomes subsidiary

Introduction to IFRS 3 & ConsolidationPage 38

►

Joint Venture –

a contractual arrangement whereby two or more parties undertake an economic activity that is subject to joint control

►

Joint control –

contractually agreed sharing of control over an economic activity when strategic financial and operating decisions of the activity require unanimous consent of the parties sharing control

IAS 31 Interests in Joint VenturesKey Definitions

Introduction to IFRS 3 & ConsolidationPage 39

IAS 31 Interests in Joint Ventures ScopeScope exemption for ►

Venturers’

interests in jointly controlled entities held by

venture capital organisations or mutual funds, unit trusts and similar entities including investment-linked insurance funds, when these investments are measured at fair value in accordance with IAS 39Such investments are classified as held for trading and measured at fair value in accordance with IAS 39, with changes in fair value recognised in profit or loss in the period of the change

►

Interest classified as held for sale under IFRS 5

Introduction to IFRS 3 & ConsolidationPage 40

IAS 31 Interests in Joint Ventures Forms of Joint Venture

►

IAS 31 identifies three types of joint ventures:►

Jointly controlled operations►

Jointly controlled assets►

Jointly controlled entities

►

Common characteristics: two or more venturers bound by a contractual arrangement and joint control

Introduction to IFRS 3 & ConsolidationPage 41

IAS 31 Interests in Joint Ventures Jointly Controlled Operations

►

This is where the venturers use their own assets and other resources, rather than setting up a separate entity or financial structure

►

IAS

31 requires a venturer to recognise:►

the assets that it controls and the liabilities that it incurs, and►

the expenses that it incurs and its share of the income that it earns from the sale of goods or services by the joint venture

Introduction to IFRS 3 & ConsolidationPage 42

IAS 31 Interests in Joint Ventures Jointly Controlled Operations

►

Example from financial statement of Xstrata Plc►

Notes to the financial statement►

6. Principal Accounting Policies

Loans to jointly controlled operations

Introduction to IFRS 3 & ConsolidationPage 43

IAS 31 Interests in Joint Ventures Jointly Controlled Assets

►

Joint control, and often joint ownership, of one or more assets (i.e., tenants in common)

►

IAS

31 requires a venturer to recognise:►

its share of the jointly controlled assets, classified according

to the nature of the assets

►

any liabilities which it has incurred individually►

its share of any liabilities incurred jointly with the other venturers►

any income from the sale or use of its share of the output of the joint venture, together with its share of any expenses incurred by the

joint

venture, and►

any expenses which it has incurred in respect of its interest in

the joint venture

►

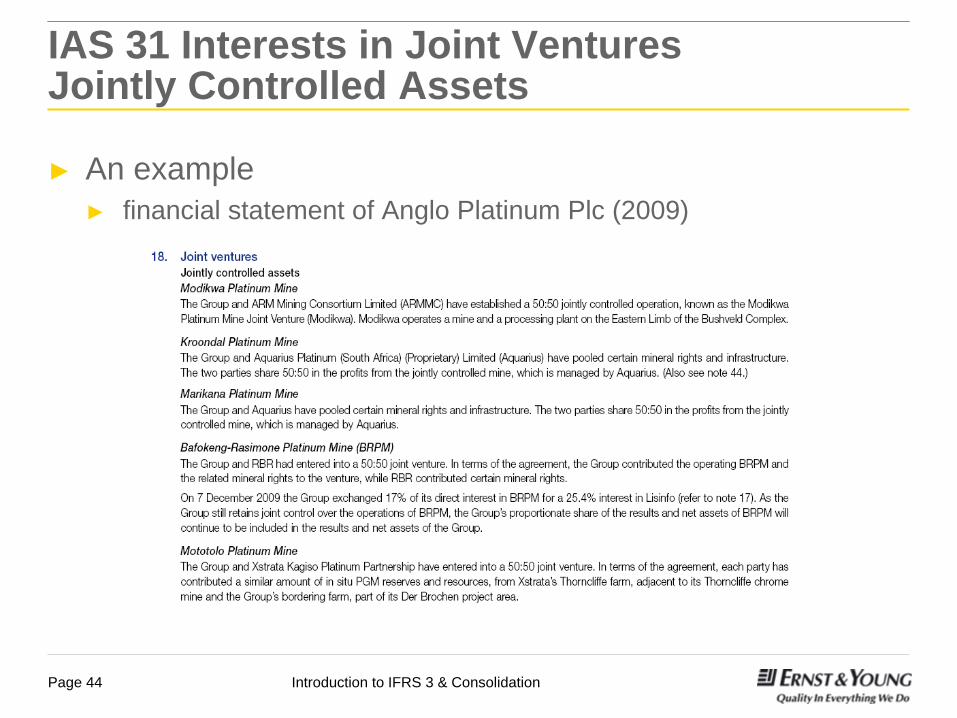

Ex p903 op slide Anglo Platinum Ltd

Introduction to IFRS 3 & ConsolidationPage 44

IAS 31 Interests in Joint Ventures Jointly Controlled Assets

►

An example►

financial statement of Anglo Platinum Plc (2009)

Introduction to IFRS 3 & ConsolidationPage 45

IAS 31 Interests in Joint Ventures Jointly Controlled Entities

►

Involves the establishment of a corporation, partnership or other entity in which each venturer has an interest

►

IAS 31 prescribes the use of one of two accounting treatments:►

proportionate consolidation►

This requires the venturer's share of each of the assets, liabilities, income and expenses of the jointly controlled entity to be included in the venturer's financial statements on a line-by-line basis

►

the equity method, as described in IAS 28

Introduction to IFRS 3 & ConsolidationPage 46

IAS 31 Interests in Joint Ventures Jointly Controlled Entities

►

Proportionate consolidation►

On the balance sheet of the venturer►

Its share of the assets that it controls jointly ►

Its share of the liabilities for which it is jointly responsible►

On the income statement of the venturer►

Its share of the income and expenses of the jointly controlled entity

►

Procedure for consolidation of subsidiaries (IAS 27) will generally be appropriate►

Elimination of investment in parent’s statement and parent’s share of equity in jointly controlled entity’s statement

►

Intragroup eliminations only for parent’s share of balances, transactions, income, expenses and dividends►

Other party’s share is not considered intragroup►

Consistent accounting policies

Introduction to IFRS 3 & ConsolidationPage 47

IAS 31 Interests in Joint Ventures Jointly Controlled Entities

►

Example from financial statement of Tui Travel Plc (2009)►

1 Accounting Policies►

C Basis of Consolidation

Introduction to IFRS 3 & ConsolidationPage 48

IAS 31 Interests in Joint Ventures Transactions Between Venturer and JV

►

Venturer contributes/sells asset to JV►

Venturer recognises that portion of gain or loss that is attributable to the interests of the other venturers

►

Venturer recognises full amount of any loss if transaction provides evidence of an impairment loss

►

Venturer purchases asset from JV►

Venturer shall not recognises its share of the profits of JV from the transaction until it resells the asset to a third party

►

Venturer recognises its share of loss if transaction provides evidence of an impairment loss

Introduction to IFRS 3 & ConsolidationPage 49

IAS 31 Interests in Joint Ventures Changes in ownership

►

Financial instrument becomes joint venture►

Unclear guidance in IAS 31►

For venturers applying equity method ►

Same method as “financial instrument becoming associate”►

Cost-based methodologies►

For venturers applying proportionate consolidation►

Several possibilities►

Fair value principles►

Cost-based approach►

Project on joint ventures may result in removal of this option

Introduction to IFRS 3 & ConsolidationPage 50

IAS 31 Interests in Joint Ventures Changes in ownership

►

Step increase in existing joint venture►

Not specifically addressed in IAS 31►

For venturers applying equity method►

Two methods►

Purchase price + directly attributable expenses added to carrying amount►

Restate investment to fair value through P&L every time

►

For venturers applying proportionate consolidation►

Method 1►

No remeasurement at fair value►

Any acquisition related costs are expensed►

Method 2►

Cost-based approach ►

Cost = purchase price + any directly attributable expenses►

Project on joint ventures may result in removal of this option

Introduction to IFRS 3 & ConsolidationPage 51

IAS 31 Interests in Joint Ventures Changes in ownership

►

Joint venture becomes a subsidiary►

IFRS 3 requires that for all previously held equity interests ►

Re-measurement at fair value►

Any difference with fair value is recognised in profit or loss►

Reclassification of any previously recognised amounts in OCI ►

This fair value amount will be included in acquisition method

IFRS 3 in a nutshell

g}} ERNST & YOUNG Qu"lity fn E,~ryt"jng We 00

Introduction to IFRS 3 & ConsolidationPage 53

Overview of IFRS 3 / IFRS 3Revised

►

IFRS 3 Revised: applies as from 1 July 2009►

Compared to current IFRS 3, the IFRS 3R will have an impact on ►

Goodwill recognised,►

P&L at the date of acquisition, and►

P&L in future periods

Introduction to IFRS 3 & ConsolidationPage 54

Overview of IFRS 3 / IFRS 3Revised

5Lmnary of cllanee GoodWill

OlJliln 10 me<I~1e _c:o.·u~ inlellSl ilits lair nlle ") Accou,.q llll tllqts in .nKUip inteitIU 01 1 !lIbsidiary (l!liI ~ nol ltSIIII i. bss

") ol contoI) as all t~ U3nSaCtio~

Cmti'fenI consióelililn IeCO(rised at I .. nlue at !he date 0I1IOII1isItiJ, dil V SIJJseqIJM: cllqes ttlll!r.lr, ~ in ~k IIfIoss

{xptnsiC IItqllisitkrlmsu u-=Wfed V

IlelSsm !he dJSSiftllion ol 11 Issets lIId tablilies ol tilt KQUft V

~I~II' w;wn lor It·KQUItd _ ol the KQUref Irld ~eli:stÎIC ltIa1ionships A Ol ~f betl"H11 tMlIOIIUi'er and iIXJi,"

Cmti'fenIlool.~s III'IIJ' lt!I«I Ilme Ihllile peSftl obItalions aisqlroll pUI MrIS V

~ise &aiRs or tosseslfom fJlelSl.Ji1 ioitial eq~ IIoIdire; i. slep acquisiliollS

" atfairnlll

Sfpam~ acc:od lor indtInIIiIies ItIate4 10 flab{lies ol lilt acqiMee V

ImpKlon

TfrTWcosl R&pa'ted results 10 Implement Volatll(y Eamf~s

>-

A

A

A

A

") A

' '''' V

Cllffelll '"

A

"

CwreRl ti.

"

:JJ ERNST & YOUNC Qo<.o';",'" C"'?''"''s ~ 00

Introduction to IFRS 3 & ConsolidationPage 55

IFRS 3R - Key Definitions

►

Definition of a business combination►

“A transaction in which an acquirer obtains control of one or more businesses.”

►

Definition of a business ►

"An integrated set of activities capable of beingcapable of being conducted and managed for the purpose of providing a return to investors"

►

"A business consists of inputs, and processes applied to those inputs, that have the ability to create outputs. Although businesses usually have outputs, outputs are not required for an integrated

set

to qualify as a business."

Introduction to IFRS 3 & ConsolidationPage 56

►

Acquiree must constitute a business►

Entities that do not constitute businesses –

not a business

combination►

A group of assets or net assets that do not constitute a business –

not a business combination

►

Allocate cost between the individual identifiable assets and liabilities based on their relative fair values at the date of purchase. No goodwill

►

Relative Fair value method

IFRS 3R - Key Definitions (ctd)

Introduction to IFRS 3 & ConsolidationPage 57

IFRS 3R - Scope Exclusions

►

Formation of a joint venture►

Business combinations involving entities under common control

►►

NewNew: no scope exclusion for mutual entities and combinations without consideration

The process

g}} ERNST & YOUNG Qu"lity fn E,~ryt"jng We 00

Introduction to IFRS 3 & ConsolidationPage 59

1.

Identifying the acquirer2.

Determining the acquisition date

3.

Measuring the consideration transferred4.

Identify assets acquired and liabilities assumed

5.

Measuring any NCI6.

Measuring goodwill

7.

Adjustments to Business Combination

IFRS 3 Application of the acquisition method

Introduction to IFRS 3 & ConsolidationPage 60

Business Combination: 1. Identifying the acquirer

Acquirer is the combining entity that obtains control –control is presumed if more than 50% of the voting rights are acquiredUse the guidance in IAS 27 to determine which entity obtained controlAcquisition date: the date on which the acquirer obtains control of the acquiree

Generally the date of legal transferAll pertinent facts and circumstances shall be considered in identifying the acquisiton date

Introduction to IFRS 3 & ConsolidationPage 61

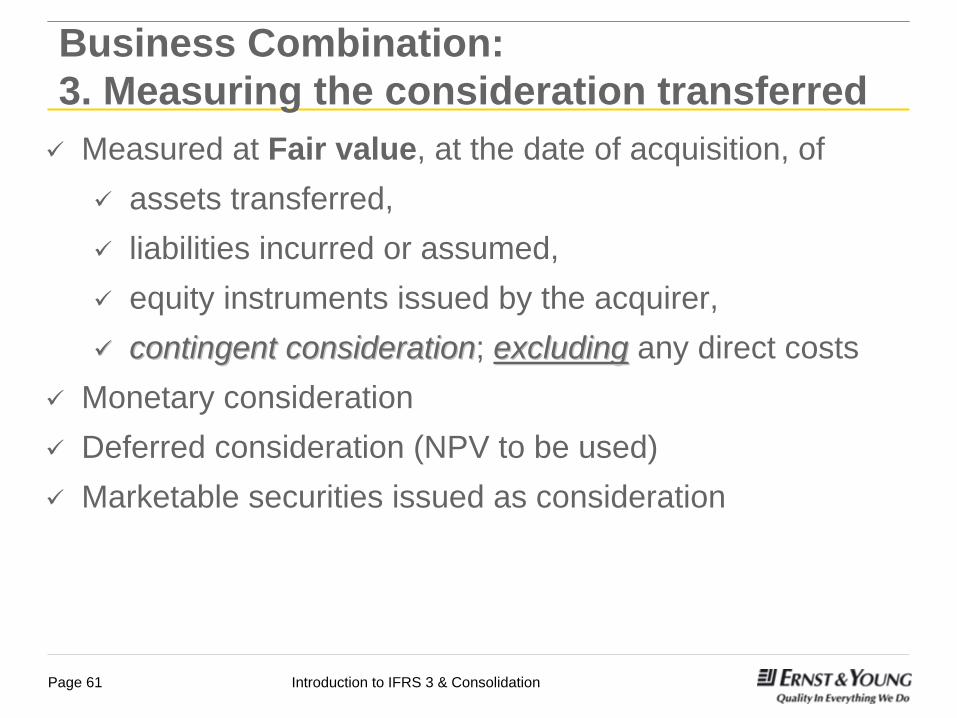

Business Combination: 3. Measuring the consideration transferred

Measured at Fair value, at the date of acquisition, of assets transferred, liabilities incurred or assumed, equity instruments issued by the acquirer, contingent considerationcontingent consideration; excludingexcluding any direct costs

Monetary considerationDeferred consideration (NPV to be used)Marketable securities issued as consideration

Introduction to IFRS 3 & ConsolidationPage 62

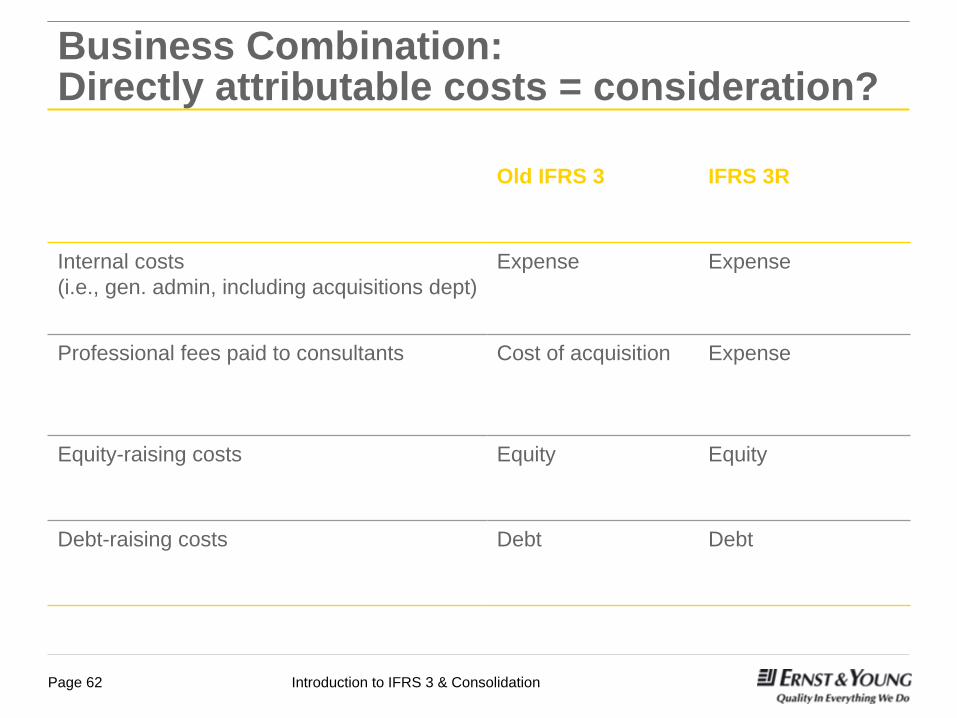

Old IFRS 3 IFRS 3R

Internal costs

(i.e., gen. admin, including acquisitions dept)Expense Expense

Professional fees paid to consultants Cost of acquisition Expense

Equity-raising costs Equity Equity

Debt-raising costs Debt Debt

Business Combination:Directly attributable costs = consideration?

Introduction to IFRS 3 & ConsolidationPage 63

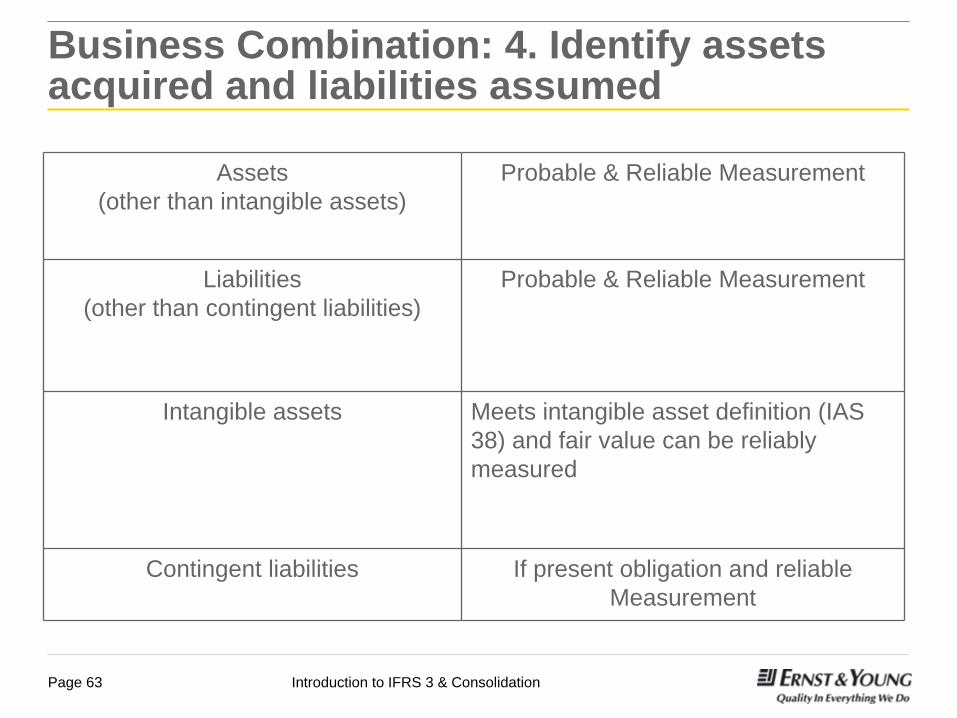

Business Combination: 4. Identify assets acquired and liabilities assumed

Assets (other than intangible assets)

Probable & Reliable Measurement

Liabilities (other than contingent liabilities)

Probable & Reliable Measurement

Intangible assets Meets intangible asset definition (IAS 38) and fair value can be reliably measured

Contingent liabilities If present obligation and reliable Measurement

Introduction to IFRS 3 & ConsolidationPage 64

-

General recognition of assets and liabilities whenit is probable that any associated future economic benefits willflow to or from the acquirer, andTheir fair value can be reliably measured

- Provisions for terminating or reducing the activitiesPresent obligation as a result of a past eventProbable outflow of resourcesReliable estimate

- Contractual obligations of the acquiree for which payment is triggered by a business combination

Business Combination: 4. Identify assets acquired and liabilities assumed

Introduction to IFRS 3 & ConsolidationPage 65

Easier recognition for intangible assets- Too often subsumed in goodwill, therefore

Probability of future economic benefits is always considered to be satisfied for intangible assets acquired in business combinationsDefinition of identifiability

contractual/legal rights or separability approachFair value of acquired intangible assets can normally be measured with sufficient reliabilityGroup of complementary intangible assets.

acquired IPR&D, customer lists, patents, copyrights, broadcasting license, trademark, …

Business Combination: 4. Identify assets acquired and liabilities assumed

More intangible assets !!!

Introduction to IFRS 3 & ConsolidationPage 66

Valuation of Intangible Assets

►

Market approaches►

Comparable market transactions

►

Usual market royalty rates

►

Cost approaches►

Indexed historical cost

►

Replacement cost

►

Income approaches►

Cash flows

►

Excess earnings►

Multi-period excess earnings method (MEEM)

►

Royalty rates►

Relief from royalty

The valuation approach selected will depend on the intangible’s nature/type.

Introduction to IFRS 3 & ConsolidationPage 67

Business Combination: 4. Identify assets acquired and liabilities assumed

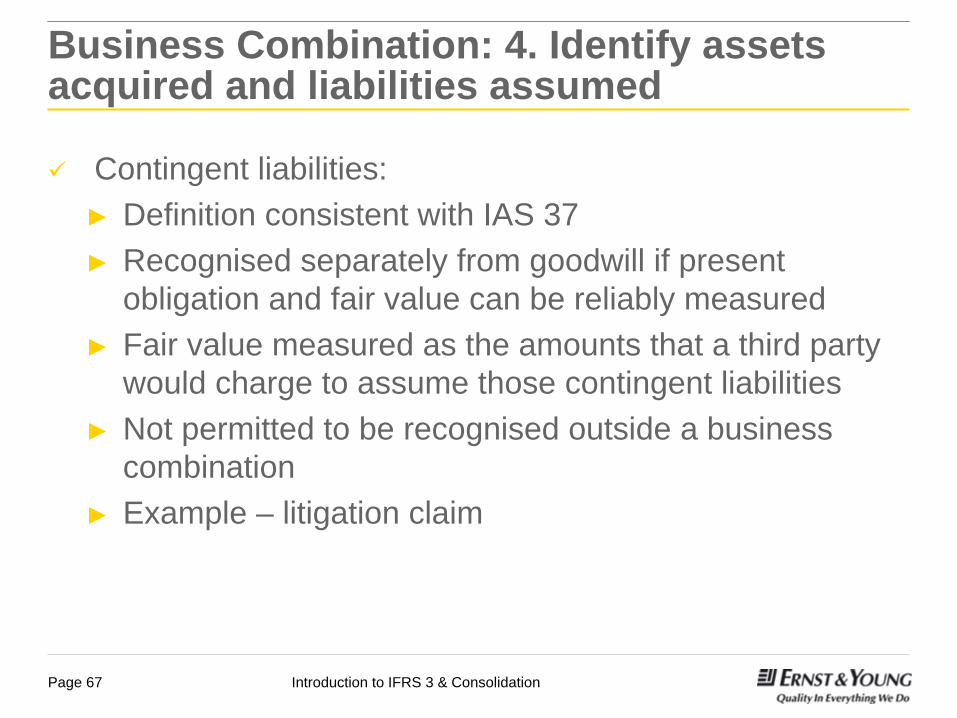

Contingent liabilities:►

Definition consistent with IAS 37

►

Recognised separately from goodwill if present obligation and fair value can be reliably measured

►

Fair value measured as the amounts that a third party would charge to assume those contingent liabilities

►

Not permitted to be recognised outside a business combination

►

Example –

litigation claim

Introduction to IFRS 3 & ConsolidationPage 68

Measurement of recognised assets and (contingent) liabilities at fair value except for Held For Sale (HFS) non current assets (fair value less costs to sell)Guidelines for determining fair value (IFRS 3 Appendix B41 & B45)Non-controlling interest => 2 methods for measurement

At their fair value at the date of controlat their proportion of the fair value of net identifiable assetsChoice on a transaction by transaction basis

Business Combination: 4. Identify assets acquired and liabilities assumed

Introduction to IFRS 3 & ConsolidationPage 69

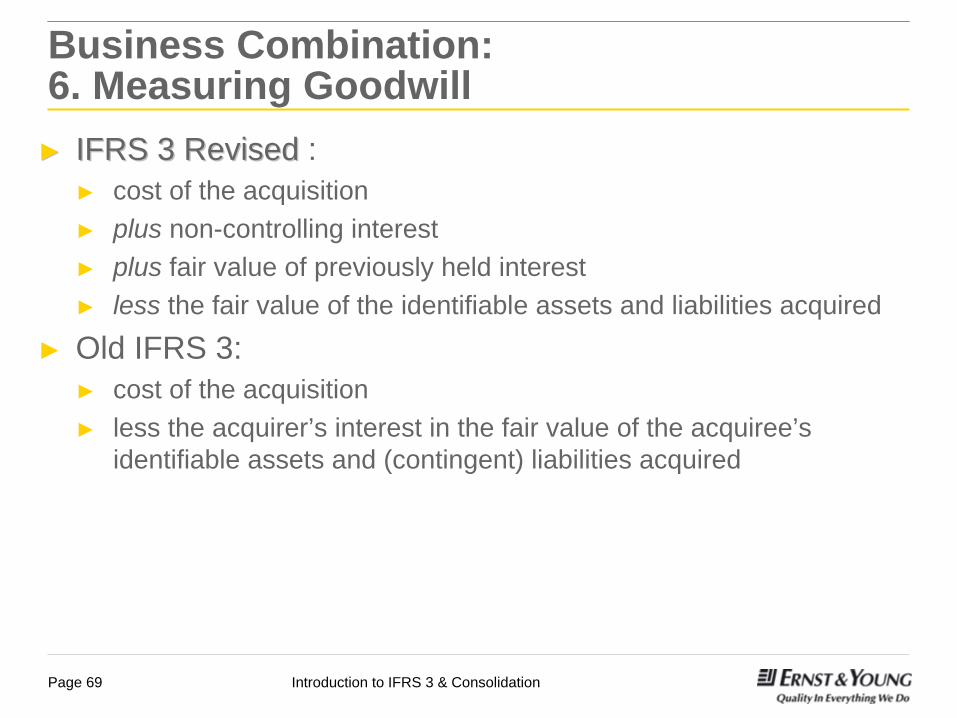

Business Combination: 6. Measuring Goodwill►►

IFRS 3 Revised IFRS 3 Revised : ►

cost of the acquisition ►

plus non-controlling interest ►

plus fair value of previously held interest ►

less the fair value of the identifiable assets and liabilities acquired

►

Old IFRS 3: ►

cost of the acquisition ►

less the acquirer’s interest in the fair value of the acquiree’s identifiable assets and (contingent) liabilities acquired

Introduction to IFRS 3 & ConsolidationPage 70

►

Carried at cost less any accumulated impairment losses►

Impairment test (at least) every year (No amortisation)

►

Reversal of impairment losses for goodwill is prohibited►

Allocation of goodwill to the CGUs that will benefit from the synergies of the acquisition

Business Combination: 6. Measuring Goodwill

Introduction to IFRS 3 & ConsolidationPage 71

Negative goodwill should be the reflection of-

Errors in recognising or measuring the fair value of either the cost of the acquisition or the acquiree’s identifiable assets or (contingent) liabilities

-

Bargain purchaseTherefore

-

Reassess the identification and measurement of the identifiable net assets acquired and of the cost of the combination

-

Recognise any remaining excess immediately in profit and loss as a gain

What if there is negative goodwill?

Introduction to IFRS 3 & ConsolidationPage 72

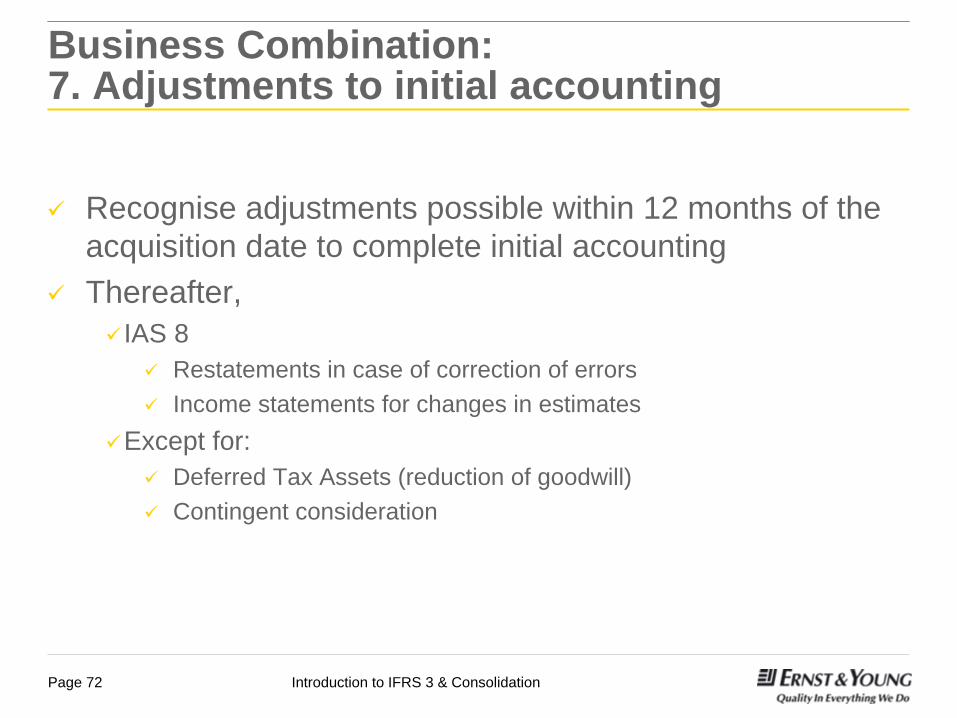

Business Combination: 7. Adjustments to initial accounting

Recognise adjustments possible within 12 months of the acquisition date to complete initial accountingThereafter,

IAS 8Restatements in case of correction of errorsIncome statements for changes in estimates

Except for:Deferred Tax Assets (reduction of goodwill)Contingent consideration

Business Combination vs. Asset Acquisition

g}} ERNST & YOUNG Qu"lity fn E,~ryt"jng We 00

Introduction to IFRS 3 & ConsolidationPage 74

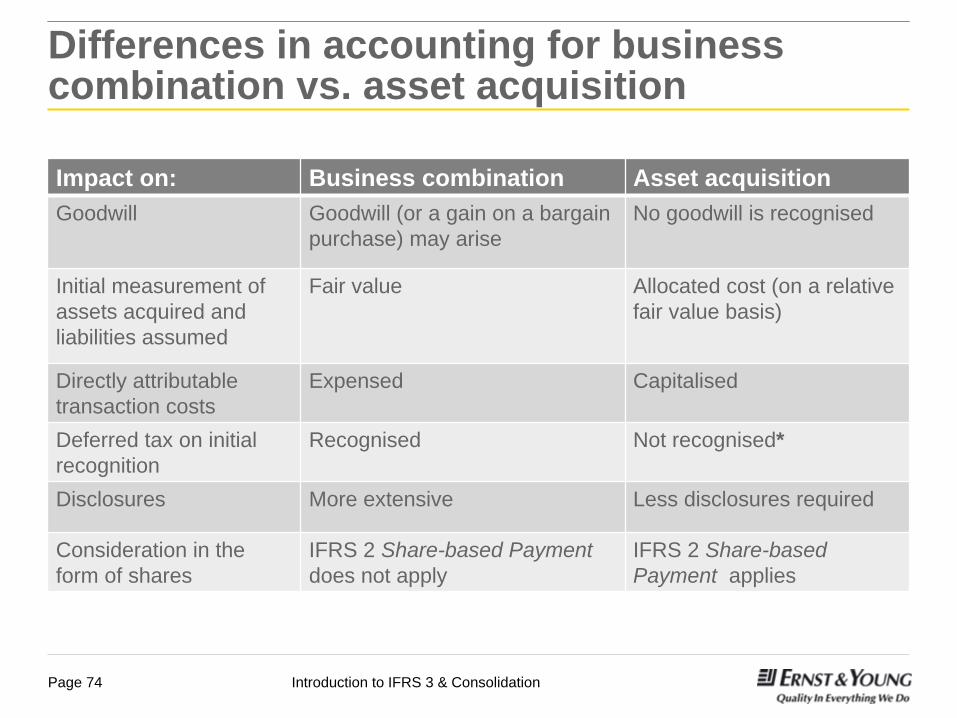

Differences in accounting for business combination vs. asset acquisition

Impact on: Business combination Asset acquisitionGoodwill Goodwill (or a gain on a bargain

purchase) may ariseNo goodwill is recognised

Initial measurement of assets acquired and liabilities assumed

Fair value Allocated cost (on a relative fair value basis)

Directly attributable transaction costs

Expensed Capitalised

Deferred tax on initial recognition

Recognised Not recognised*

Disclosures More extensive Less disclosures required

Consideration in the form of shares

IFRS 2 Share-based Payment does not apply

IFRS 2 Share-based Payment applies

*While this is generally the case, in some instances the initial recognition exception will not apply and a deferred tax balance will need to be recognised for any temporary difference.

Introduction to IFRS 3 & ConsolidationPage 75

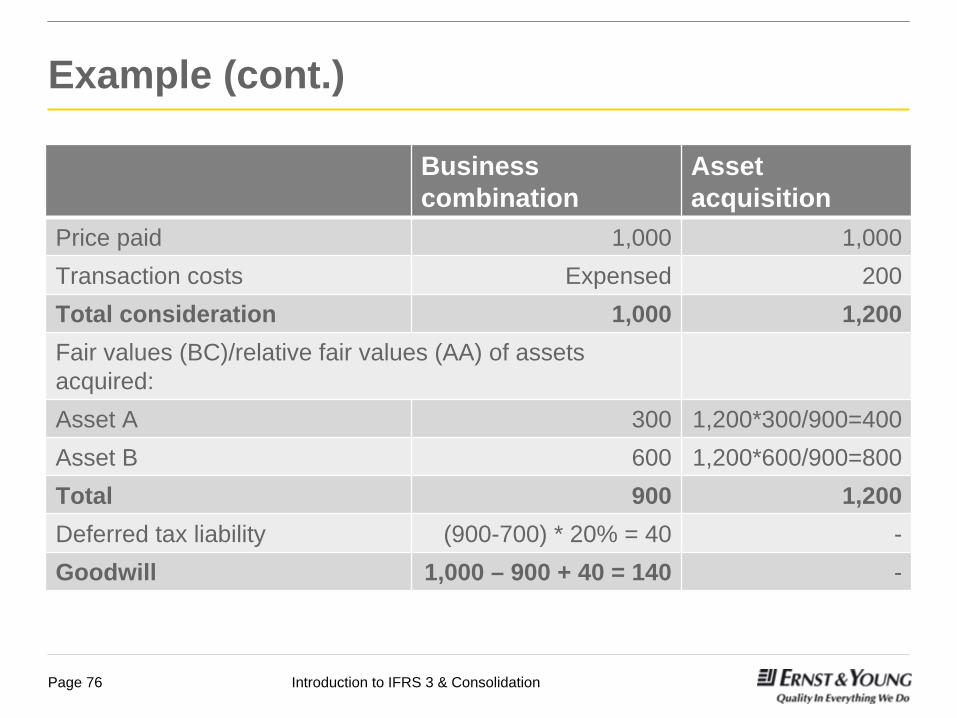

Example

►

Company P acquired 100% of the shares of Company S for 1,000, incurring transaction costs of 200.

►

S has no liabilities. The only assets of S are two buildings, A and B, the total book value of which is 700.

►

The tax base of the building is 700.►

The applicable income tax rate is 20%.

Introduction to IFRS 3 & ConsolidationPage 76

Example (cont.)

Business combination

Asset acquisition

Price paid 1,000 1,000Transaction costs Expensed 200Total consideration 1,000 1,200Fair values (BC)/relative fair values (AA) of assets acquired:Asset A 300 1,200*300/900=400Asset B 600 1,200*600/900=800Total 900 1,200Deferred tax liability (900-700) * 20% = 40 -Goodwill 1,000 – 900 + 40 = 140 -