inv metals (tsx.inv) - goodmanschoolofmines.laurentian.ca · carolina las penas thesis i –...

TRANSCRIPT

INV Metals (TSX.INV)

Spencer McFarlane

Hari Muralidharan Ashar Subzwari Dalton Austin

FEBRUARY 7-9, 2019

Prepared By

▪ Projects: LomaLarga,TierrasColaradas,LasPenas,Carolina,LaRebuscada▪ Valuation: Wederivedoursharepricesingaweightedblendof80%NAVand

20%PrecedentsTransactions.▪ Ownership: Iamgold35.59%

TerryMacGibbon8.38% CandaceMacGibbon4.49%

• CSR:INVmaintainsastrongpresencewithinlocalcommunitiesthroughcommunityoutreachandeducation.

Executive Summary – INV Metals

CompanyHighlights ValuationMetrics

XXStockPerformance

Segmentation

RevenueProjectionsBasedonMetal % Gross(mm)(FY22e) Gold 86 $139 Silver 7 $11.3 Copper 7 $11.3

MarketCap $62.04 AvgTradingVolume 32.64kNetAssetValue $341M Revenue(FY22e) $162MP/NAV 0.14x EBITDA(FY22e) $104 MNAVPS NetFixedAssets $69MCash $7.34M TotalDebt $0

KeyValuationStatistics($mm)

HighLevelCorporateStrategy Targetpotentialjurisdictionswithqualityassets

Thoroughlyexploretheareaforpromisingdeposits

Developthetargetarea

Sellthedevelopmentforapremium,orgeneratecashflowsthroughproduction

*Asa%ofnetsales.

Thesis

M&APotential

Jurisdication

StrongBrass

1

2

3

INVmetalsjuniorgoldexplorationcompany. Wecametoablendedtargetpriceof$1.5/sharewhichisinlinewithanalystestimates.

Company Overview – Loma Larga

ResourceClassification

Tonnage(Mt)

Au(g/t)

ContainedAu(Moz)

Ag(g/t)

ContainedAg(Moz)

Cu(%)

ContainedCu(Mlb)

Grade(G/tAuEq)

ContainedGoldEquivalent(MozAuEq)

Proven+Probable

13.9 4.91 2.20 29.6 13.27 0.29 88.0 5.81 2.60

Measured+Indicated

19.8 4.25 2.71 27.8 17.7 0.25 109.5 5.01 3.2

Inferred 4.7 2.22 0.33 29.7 4.5 0.14 14.5 2.84 0.43

LifeofMine 12 Years AfterTaxIRR 24.7%

DevCapExEstimated $309.5 M SustainingCapital $72.7MProjectedRevenue $2.2B After-TaxCFEstimate $582M

Ramp-UpTonnes/Day 3,000 Tonnes/DayYr5+ 3,400Ramp-UpAnnualGEO 267,000 AnnualGEOYr5+ 206,000

• De-Risk:Nocommunitywaternearby.• Only80HectaresofDisturbance• Explorationpotentialonallsidesoftheproject.• PotentialPorphyry• Lotsofinformationfrombeingthere12years.

BeneficialQualities

KeyStatistics

LomaLargaisahigh-gradeGolddevelopmentassetwithshallowdepositsthatINVacquiredfromIAMGoldin2012.

Company Overview – Other Assets

INVtakesadvantageofEcuador’sunder-exploredminingindustrywithseveralkeyExplorationAssets.

TierrasColaradas• Indicatedhighgradegoldandsilvervaluesdetected

onthethreemainveinsontheproperty. • 484samplesrangeinvaluefrom0.005to240g/tof

gold,and<0.2–2,479.0g/tsilver.

LasPenas • Coversanareaof30,278hectars. • Approximately30kmnorthofLomaLarga. • Twohighgradeveins: LaCrestaVeinSystemrangingupto88g/tgoldGalletaVeinSystemrangingupto35.9g/tgold,3,507g/tsilver,and821ppmcopper.

Carolina• PotentialforPorphyry• 1kmawayfromSolGold‘sCascabelMine. • Samplingwascomprisedof147rockchipsamples.

Coppervalueswithin34samplesgradedgreaterthan200ppm,including10greaterthan300ppm,and2greaterthan800ppm

LaRebuscada• LocatedinthecentralpartofEcuador,intheprovince

ofCotopaxi,thissiteis3,205hectares. • Atotalof148sampleswerecollectedwith25values

greaterthan1.0g/tgold.

Tierras Colaradas La Rebuscada

Carolina Las Penas

Thesis I – Potential for M&A INV metals is ripe for acquisition for their quickly approaching development, high quality grade, scalability and proven management team.

M&A Activity in Mining Industry

Loma Larga Is Ripe Acquisition

Trends and highlights

§ Deal value in 2018 was $53.4, representing a 90% increase from prior year. M&A activity was largely driven by 3 high profile deals ( Barrick acquires Randgold, Newmont acquires Gold Corp.

§ On average, deal size was $160.5 million, a 113% growth over 2017. Robust growth despite geopolitical headwinds, namely trade ware and GDP slowdown in China.

§ Despite this, M&A activity remained strong on the back of improving gold prices and companies taking advantage of low valuations.

§ Analysts see the small to mid –tier sector of the mining industry as the sweet spot.

156 170

131

207

168

143

171

211 207

142 157

128

$-

$5

$10

$15

$20

$25

$30

0

50

100

150

200

250

Disclosed deal value Deal volume

Quickly approaching development

1

High Quality Asset 2

• Pre feasibility study completed, and project ready for financing

• Construction commencing as soon as 2020, meaning investors receive ROI relatively soon.

Proven Management team 3

• High grade mineral resource estimates, quality assets with exploration upside

• Saleable concentrate to help with financing and avoid EPS dilution through large equity financing

• Establishing development in now mining friendly environment

• History of acquiring quality assets and sale of business at high control premium.

0.12x 0.14x 0.23x 0.24x

0.33x 0.34x

0.48x 0.57x 0.61x

0.70x

0.00x 0.10x 0.20x 0.30x 0.40x 0.50x 0.60x 0.70x 0.80x

Thesis I – Potential Acquirers IAMGOLD appears to be the most logical acquirer of INV based on financial feasibility, strategic alignment, and risk profile.

Potential Acquirers of INV and brief description

§ IAMGOLD currently owns 36% of the company based on most recent share ownership. Decided to divest initial investment in Ecuador in 2012 based on unfavourable industry dynamics at the time ( Sold Quimsacocha to INV).

§ IAMGOLD currently has cash and cash equivalents and short term investments of 744.5 million as of September 30th, 2018.

§ Company has well established exploration properties and land positions throughout Brazil, Chile and Argentina. Geographies that are similar to Eucador.

§ Strategy is to build on this base through existing operating mine expansions, optimization initiatives, development of new mines and the advancement of exploration properties.

§ Cash and Cash equivalents on hand are $120.7 million of available cash and 685 million in credit. Guidance for 2018 Capital injection indicates 192 million will be utilized for expansion.

YAMANA GOLD IAMGOLD

Financial Feasibility

Strategic Alignment

Robust Risk Profile

Thesis II – Operational Mines in Ecuador

CurrentlythereareafewmineswithinEcuadorbutwiththereforms,moreplayersarelookingtoenterthescene

CurrentMinesinEcuador ConcessionsinEcuador

EcuadorEndangered&MiningFeeds

Thesis II– Ecuador “Mining Law”

FavorablechangestominingregulationandtaxpolicyhascementedEcuador’spositioninasakeygeographyforjuniorandseniorproducers. EcuadorMiningLawRegulationTimeLine

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

2018

Unfavourablemininglaw KinrossabandonsFrutaDelNorte

MajoroverhaulofminingregulationsWindfalltax

DeeperDive

2008

2013

2013

2018

▪ April2008,sawtherevokingof80%ofminingconcessionsandtheadditionofthe70%windfalltax.

▪ June2013KinrossAbandonsFrutaDelNorteafterfailuretonegotiateterms(mainlyduetowindfall

tax).

▪ June2013,sawamajoroverhaulinregulationsnamelytougherenforcementonillegalmining,implementationofcategoriesofmines,andstandardizedcalculationforwindfalltax.

▪ August2018sawthetotalremovalofwindfalltax,andcapitalgainstaxreductiononsharetransactionsfrom22%to8-10%.

Thesis II– Ecuador “Economics”

▪ Background:EcuadorandINVbothhaveavestedinterestinensuringthatthismineissuccessful,andshouldbetreatedasapartnership.

EcuadorisprimedtohaveaproductivepartnershipwithINVmetalsbasedontheoverrelianceontheoileconomyandmutualinterests.

Sources:TradingEconomics&CountryEconomy

CompanyProposaltoEcuador

EcuadorOilRents%ofGDP

GDPEcuador

EcuadorPublicDebt%ofGDP

WhatINVhastooffer WhattheEcuadorianGovernmentcanoffer JobCreation AccesstoQualityMiningsites TaxGeneration CreateValueforShareholders CommunitySupportSystems RiskDiversification

Thesis II– Macro Outlook

SupplyandDemand EquityMarkets

Debt-to-GDP

Supplyconstraints,Equitymarketsell-offs,Debt,andFinancialSafetyareallshort-termdriversforabullishGoldprice.

SafeHaven

• Debtasa%ofGDPthatisgreaterthen100%islikelytodecreasethevalueoftheUSD,andincreasesthevalueofgold.

• TheUSdebtleveliscurrentlyaround100%andprojectedtogrowat5%yoyassumingnorecession.Thisinitselfisnotsustainable,andwitharecessionthedebtlevelswillincreaseconsiderably.

• Estimatesoftotalglobaldebtare244trillion,whichisover318%ofglobalGDP.

PoliticalUncertaintyfromUK,EU,US,China Tradetensionswilllikelyhaveanimpacton: • Speculativeandmaterialpressuresoncommodityprices. • Actualdemandforcommodities. • Inflationarypressures. Recession • GSgivesa43%chanceofarecessioninthenext3years. • 75%ofJPM’sultrahighnetworthclientssaytheyexpectoneby2020. ReducedLiquidity • Adrivingfactorinthestrengthoftheequitymarketistheexcessliquidity

giventothemarketfromtheFED,whichallowsinvestorstotakemorerisks.

• Now,theFederalReserveisallowingUS$328Billionofbondstomature.

Wheneverthestockmarketdeclinessignificantly,oneofthefirstalternativeinvestmentsthatinvestorsconsidertransferringmoneyintoisgold.

• Supplychangesslowlyandisratherinelasticcomparedtodemand.Theconstraintbetweenwhat’savailableandwhat’sneededdrivestheprice.

• AccumulatingGold

inventoriesincreasescarcityanddriveuptheprice.

CandaceMacGibbon,CPACA–CEO/Director❑ Withover20yearsexperienceintheminingsector.❑ InstitutionalSalespersonRBCCapitalMarkets,2006-2008.Workedasaminingassociate

forBMOCM,2004-2006.❑ Hasbeenwiththecompanysince2008,andhasheldthetitlesof,VP,CFO,President,and

eventuallyCEOin2015.

BillShaver,P.Eng–COO❑ Mr.Shaverhasover40yearsofexpertiseinmineconstructionandoperations.Someofhis

careernotablesincludethefoundingofDynatec,workingastheCOOofFNXMining,andCEOofDMCMiningservices.

❑ Mr.ShaverservesasaConsultantofShaverEngineeringLimitedandminingcompaniesonaworldwidebasiswithemphasisonsafety,managementandtechnicalevaluationofoperatingminesandprojects.

SunnyLowe,CPA,CA–CFO❑ Hasalmost20yearsoffinanceexperiencespentmostlyintheminingsector.Has

developedskillsacrossdisciplinessuchasEnterpriseRiskManagement,GlobalTaxationandCompliance,andBusinessSystemsandControls.

❑ FromherexperiencesintheVPofFinanceroleatKinrossGoldCorp,andthroughotherpositions.

❑ MostrecentlyVPofFinanceatKinrossGoldCorporation.

Investment Thesis III – Management

Investment thesis III – Terry MacGibbon

TerryMacGibbon,amininghalloffamerthatincitesconfidenceinshareholderseverytimeheisinvolved. Attributes

Successfultrackrecord

AssetSelection ▪ All4companiesthatTerryhas

managedhavehadtransformativeassetsinopportunisticgeographies.

StrategicAcquisitions

SourceFinancing

CommunityCentered

▪ Historyofacquiringquality“noncore”propertiesintheSudburybasinfromINCOforthesuccessstorythatisFNX.

▪ Strongrelationshipswithfinancialsponsors,equityinvestorsandinvestmentbankstosecurefinancingforacquisitionsandoperations.

▪ Theabilitytopartnerwithcommunitymembersandestablishcommongroundtoavoidcommunityoutcryandprotest.

Morelosgoldproject-becamemidsizedgoldproducer,345kounces,fixedtensionswithresidentsonprojectsite,tailingspondwouldwashovervillage,relocated

villagersandbuiltabettervillageforthem.

FNXminingcompanymergedwithquadramininglimitedacquiredbyKGHMPOLSKA3billion–startedoutbyacquiring5minesinthefootwallofSudburythatwasnotattractiveforlargercompanies,butbyusinghistoricaldataandadvancedcomputersoftwareallowedthemtodiscoverore

relativelyquickly..

Tmacresources-turnedaroundhopebaygoldprojectafterNewmontfailedtomakeadevelopmentplan,acquiredthroughallstockdeal,completedasuccessfuldrillingathopebayandboostedmeasuredandindicatedby59%to4.4millionounces.Also

minimizedcoststo$785usdanounce.Didanipofor155millionandsecured

120millionindebtfromprivatelenders,miningipohasntbeendone

onthetsxsince2012

Invmetals-designedwithminimalenvironmentalimpact,10,000

tonesofmostlysilicausedtofillinthemineandrestwillbere

vegetated.

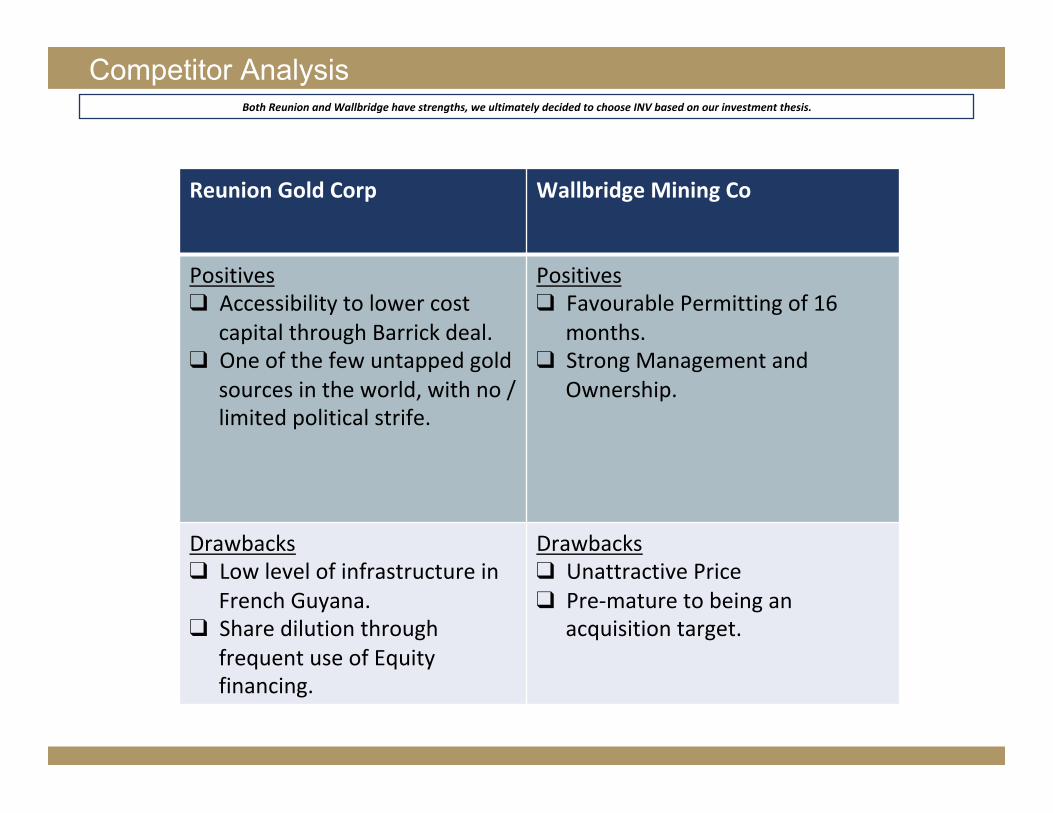

BothReunionandWallbridgehavestrengths,weultimatelydecidedtochooseINVbasedonourinvestmentthesis.

ReunionGoldCorp WallbridgeMiningCo

Positives❑ Accessibilitytolowercost

capitalthroughBarrickdeal.❑ Oneofthefewuntappedgold

sourcesintheworld,withno/limitedpoliticalstrife.

Positives❑ FavourablePermittingof16

months.❑ StrongManagementand

Ownership.

Drawbacks❑ Lowlevelofinfrastructurein

FrenchGuyana.❑ Sharedilutionthrough

frequentuseofEquityfinancing.

Drawbacks❑ UnattractivePrice❑ Pre-maturetobeingan

acquisitiontarget.

Competitor Analysis

Valuation – Net Asset Value

KeyAssumptions

NetAssetValuation

PlantInfrastructure ProjectedFiscalYearsEndingSeptember30th Scenarios 2020E 2021E Total BearCase (8,954) (15,800) (24,754) BaseCase (8,596) (15,168) (23,764) BullCase (7,163) (12,640) (19,803)

IndirectCosts ProjectedFiscalYearsEndingSeptember30th Scenarios 2020E 2021E Total BearCase (113,556) (23,450) (137,006) BaseCase (109,014) (22,512) (131,526) BullCase (90,845) (18,760) (109,605)

DevelopmentCapExAssumptions

Gold Price Development CapEx Discount Rate

Fair Value Per Share Base Case Bear Case Bull Case Bear Case Bull Case Bear Case Bull Case

PVofFreeCashFlowstoFirm(FCFF) $86,660 ($25,127) $198,448 $79,361 $115,858 $11,733 $202,947 EnterpriseValueoffirm 86,660 (25,127) 198,448 79,361 115,858 11,733 202,947-Debt - - - - - - -+CashandEquivalents 7,000 7,000 7,000 7,000 7,000 7,000 7,000NetDebt (7,000) (7,000) (7,000) (7,000) (7,000) (7,000) (7,000)EquityValueoffirm 93,660 (18,127) 205,448 86,361 122,858 18,733 209,947DilutedSharesoutstanding 93000 93000 93000 93000 93000 93000 93000

Impliedpricepershare 1.01 (0.19) 2.21 0.93 1.32 0.20 2.26

GoldPriceAssumptions

DiscountRateAssumptions

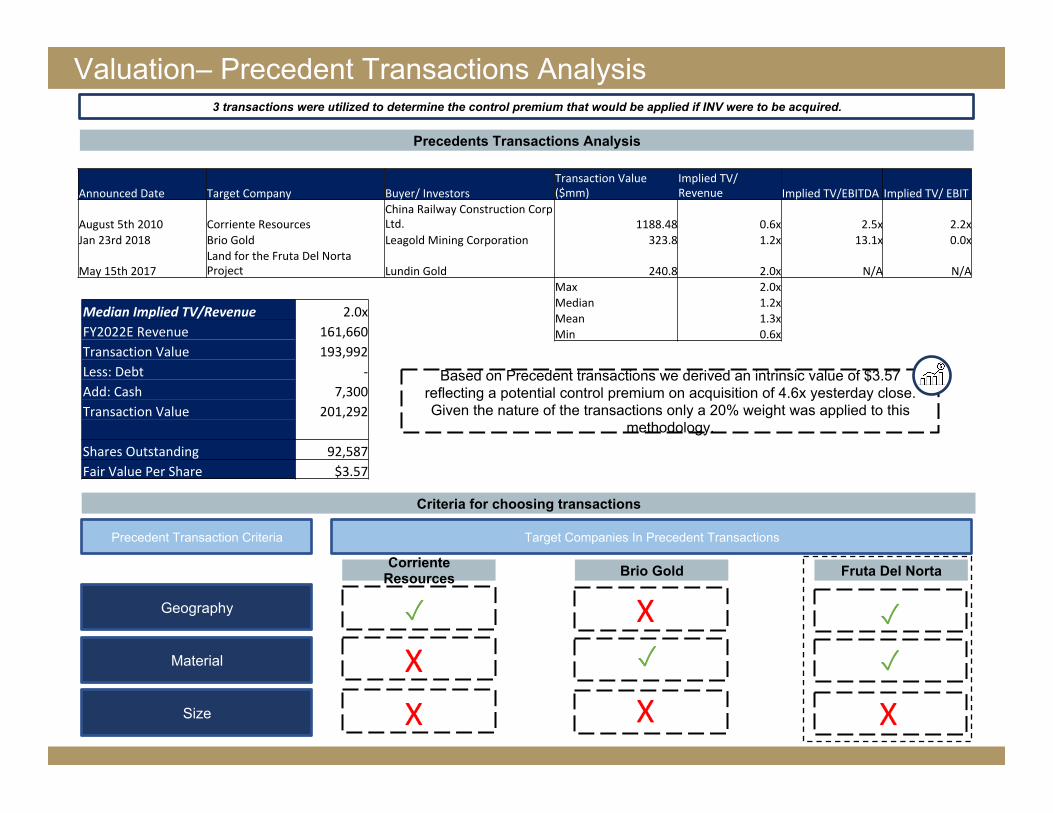

Valuation– Precedent Transactions Analysis 3 transactions were utilized to determine the control premium that would be applied if INV were to be acquired.

Precedents Transactions Analysis

AnnouncedDate TargetCompany Buyer/InvestorsTransactionValue($mm)

ImpliedTV/Revenue ImpliedTV/EBITDA ImpliedTV/EBIT

August5th2010 CorrienteResourcesChinaRailwayConstructionCorpLtd. 1188.48 0.6x 2.5x 2.2x

Jan23rd2018 BrioGold LeagoldMiningCorporation 323.8 1.2x 13.1x 0.0x

May15th2017LandfortheFrutaDelNortaProject LundinGold 240.8 2.0x N/A N/A

Max 2.0xMedian 1.2xMean 1.3xMin 0.6x

MedianImpliedTV/Revenue 2.0xFY2022ERevenue 161,660TransactionValue 193,992Less:Debt -Add:Cash 7,300TransactionValue 201,292 SharesOutstanding 92,587FairValuePerShare $3.57

Based on Precedent transactions we derived an intrinsic value of $3.57 reflecting a potential control premium on acquisition of 4.6x yesterday close. Given the nature of the transactions only a 20% weight was applied to this

methodology.

Criteria for choosing transactions

Precedent Transaction Criteria

Geography

Material

Size

Target Companies In Precedent Transactions

Corriente Resources Brio Gold Fruta Del Norta

Team – Thank You for listening!

HariMuralidharan AsharSubzwariDaltonAustin SpencerMcFarlane

Spencerisa3rdyearfinancestudentatRyersonUniversity.HehasinternshipexperienceintheMiningIndustryandSalesandTrading.HeisactivelyinvolvedwiththeRyersonInvestmentGroupwhereheservesasthePortfolioManagerfortheMetals&Miningsector.

Asharisa4thyearfinancestudentatRyersonUniversity.HeiscurrentlypursuingtheCFAdesignationandhasastronginterestininvestmentmanagement.Heisalsoactivelyinvolvedincasecompetitionsandstudentgroupwork.

Daltonisa1styearaccountingandfinancestudentatRyersonUniversity.HeisanactiveparticipantintheFinancialAdvisorSkillsTrainingprogram,amemberoftheRyersonCasePoolteam,andanAnalystfortheRyersonInvestmentGroupintheFinancialssector.

Hari is a fourth-year finance student at Ryerson University. He has internship experience as a Private Equity Analyst and as a Consultant. He is actively involved with the Ryerson Investment Group where he serves as the Portfolio Manager for the Technology, Telecom, and Media sector.