invest in arica 2014

DESCRIPTION

a list of tax advantages that promote inversion and development of the region.TRANSCRIPT

INVEST IN ARICA AND PARINACOTA

Cruz de Mayo (Cross of May), tangible evidenceof religious syncretism in the Andean world.

Pelican or Huajachein Fishermen Cove.

Cover:One of the earliest methods of trading in the zone represented in countless rock art icons.

Made by:CORDAP

Photography:Francisco Manríquez

INVEST IN ARICA AND PARINACOTA

CORPORACIÓN DE DESARROLLO DE ARICA Y PARINACOTA The Arica and Parinacota Development Corporation is non-profit institution, created by law N° 19.669 (Arica II law), with the main objective of encourage the progress of the provinces of Arica and Parinacota, to serve as an advisory association on public investment and policy decisions, and to evaluate the advance of enacted development measures. The corporation acts as a coordinating entity among private and public sectors and civil society.The committee is formed by the most representative enterprise unions and social associations of the region. Intendants, governors and mayors are also part of the corporation. Currently, the directory is presided over by Ms. Edward Gallardo Malebran, president of the Association of Industrial Workers of Arica.

GOBIERNO REGIONAL DE ARICA Y PARINACOTAMission:To maximize the long term growth potential of the economy, and to promote a better use of the productive resources of the country, in order to reach a sustainable economic growth that includes a better quality of life for every Chilean, especially from the most vulnerable sectors.Strategic objectives: To responsibly administrate fiscal policy, according to the macroeconomic context, in order to promote the long term growth potential, also contributing to the improvement of quality of life of Chilean people, especially from the most vulnerable sectors. To design and support legal initiatives, that allow maximizing the economic growth rates, according to the goals of the government.To focus in the opening of financial markets promoting the financial integration of the country with international markets.To coordinate organizations and entities that depend on the Treasury Department, to maximize its contribution to the economic growth of the country.

INVEST IN ARICA AND PARINACOTA

PROCHILEProChile is an institution dependant on the Ministry of Foreign Affairs, and its role is to promote the exportation of goods and services. In addition, it contributes stimulating the foreign investment in Chile and in Chilean tourism. ProChile has a network of 50 commercial offices all around the world and 15 regional offices across the country. Specialized work teams contribute to the positioning of Chilean attributes in the international markets, supporting the exporting companies with high quality information and diverse tools in their management abroad.

ZONA FRANCA DE IQUIQUE (ZOFRI)ZOFRI: THE BEST COMMERCIAL AND INDUSTRIAL PARTNER FOR AMERICA AND THE WORLD.The Free Trade Zone of Iquique (ZOFRI) was created in 1975, and since 1990 it has been administered by Zofri S.A. Within the context of its creation, these are the reasons of its establishment:- To promote development of the most distant zones of the country- To reinforce geopolitical sovereignty with the neighboring countries- To contribute the economical growth with entrepreneurs’ incentives, due to the high tariff rates back in those years

Currently, Zofri S.A is recognized as a logistics and commerce system of international excellence. Zofri’s connectivity with the Bioceanic Corridor translates into certain comparative advantages: 3,300 kilometers (about 2,000 miles) will connect Chile-Bolivia-Brazil; Puerto de Santos (Brazil) will connect with ports from Iquique and Arica. New markets in Bolivia, Brazil, Paraguay and Peru (86 million people). Access to the main urban centers: Santa Cruz, Campo Grande, Corumba and Cuiaba.Currently, Zofri possesses 4 business unities with global selling volumes (2012) bording US$4,411 million:- Wholesale Business Center, Iquique- Shopping Center, Iquique- Logistics Center, Iquique- Industrial Park, Arica

Presentation

Arica and Parinacota region is located in the northern frontier of the Chilean territory. It is a new region, with a regional independent government since 2008. It possesses cultural, economic and geopolitical characteristics that make this region different from others of the country.Due to its history and geographic location, for many years its development grew different from the national figures, despite their opportunities and resources. In a country economically and politically centralized as Chile, the region was not “visible” for the Central Zone.With the creation of the Arica and Parinacota region, the phenomenon started changing: the existence of a regional government and council, with its own public budget administration. Along with this, the creation of a new organized private sector, as an economic development axis, for the future of the region is being developed.

Law N°20,655 about distant zones of the country, dictated on February 1, 2013, established a list of tax advantages for a period of 12 years. These advantages promote inversion and development of the region.The Arica and Parinacota Development Corporation, along with ZOFRI S.A as a franchisee for the administration of the Industrial Free Trade Zone of Arica and the regional directive of PROCHILE have created a Regional Committee of Promotion of Investment, and its first task is to promote the potential advantages of the region, regarding its resources, and a beneficial tax legislation.This document is a synthesis of the potential advantages that the Regional Committee of Promotion of Investment has decided to foment.

Former Customs building, design by Gustave Eiffel, opened in 1874.

Morenada making their show in “With the Force of the Sun” Carnival.

11INVEST IN ARICA AND PARINACOTA

Index

Chapter I Potentialities and advantages of the region1.1 Territory and Location1.2 Air Connectivity1.3 Road Connectivity1.4 Railway Connectivity1.5 Maritime Connectivity1.6 Universities and Technical Training Institutes1.7 Hotel Accommodations and Casinos1.8 Industrial Zone of Arica1.9 Available Areas1.10 Regional Economy

Chapter II Investment opportunities in the region

2.1 Aquaculture2.2 Agriculture2.3 Chain of Activities2.4 Non-conventional Renewable Energies2.5 Logistics2.6 Mining Services2.7 Tourism

Chapter III Potentialities and tax advantages of the region

3.1 Tax Credit to Regional Investment3.2 Industrial Free Trade Zone 3.3 Workforce Hiring Bonuses3.4 Investment Bonuses: Priming Fund and Development of Distant Zones 3.5 Simplified Exportation System3.6 Exportation Centers3.7 Extension Free Trade Zone3.8 Special Taxes for Residents3.9 Registration Certificate

Chapter IV Benefit Requirements and Processing

4.1 Investment Tax Credit4.2 Arica Industrial Free Trade Zone4.3 Workforce Hiring Bonuses4.4 Investment Bonuses: Priming Fund and Development of Distant Zones4.5 Simplified Exporting System4.6 Exportation Centers

Chapter V Comparative Analysis of Results

5.1 Comparative table5.2 Practical Example 15.3 Practical example 25.4 Practical example 35.5 Practical example 4

Appendix 1Map of Arica and its Industrial Areas

appendix 2Law 20,655 report, establishing special incentives for the most distant zones of the country, regarding Arica and Parinacota re-gion. ByRaúl Castro Letelier, Lawyer.

Train Station Arica - La Paz, opened March 6, 1912.

CHAPTER I POTENTIALITIES AND ADVANTAGES OF THE REGION

1.1 TERRITORY AND LOCATION

Arica and Parinacota is the most northern region of Chile, it is the only region that has frontiers with two countries; at North it borders with Peru, at East with Bolivia and the south borders with Tarapaca. The region has a surface of 16,873.3 km2 and 213,595 inhab-itants, divided into two provinces: Arica and Parinacota.The province of Arica takes up the coastline and desert plateau, which is crossed by the fertile agricultural valley of Lluta, Azapa, Chaca and Camarones. The province is subdivided into counties, being Arica the capital of the region, gathering the 98,7% of the total popula-tion of the region.The province of Parinacota takes up the lower part of the mountain chain and the high Andean plateau. The lower part of the Andean mountain chain has agricultural and touris-tic potential, with colonial towns that support the maintenance of the churches that take part of “Ruta de las Misiones” (The Mission Route).The high Andean plateau is a virgin area at 4,000 meters above sea level, with unique landscapes and auquenido grazing pastures. It is subdivided into General Lagos and Putre counties.The whole region has a great potential development in agriculture, mining, logistics ser-vices, tourism and nonconventional energy. These sectors have been defined as the axis for regional development.

“The whole region has a great potential development in agriculture, mining, logistics services, tourism and nonconventional energy. These sectors have been defined as the axis for regional development.”

The large amount of cargo movement from neighboring cities indicated in the following map:

Sunset at Chinchorro Beach.

City Population Distance from Arica Orientation Route

15INVEST IN ARICA AND PARINACOTA

1.3 ROAD CONNECTIVITY

Arica has great road connectivity. By the eastern side of the city the 5 North Road (Pan-american Highway) connects the south American countries of the Pacific. To the north of Lluta river, from the Pan-anamerican highway the 11-CH is originated, and connects Arica with Bolivia.

Traffic is not an issue in Arica, giving the fact that it has four double road avenues that cross the city from north to south:• CapitánÁvalosAvenue• AlejandroAzolaAvenue• SantaMaríaAvenue• LuisBerettaPorcelAvenueFrom east to west there are three double road avenues:• RenatoRoccaAvenue• DiegoPortalesAvenue,thatcontinuestowardseastbytheAzapaRoad• 21deMayoextension/SenadorValenteRossiThe number of avenues with high vehicular capacity allows fast transportation from any point of the city.

Tacna Perú (1)Ilo Perú (2)Arequipa Perú (1)Alto Hospicio (3)Iquique ( 3)Antofagasta (3)Calama (3)El Alto, Bolivia (4)La Paz, Bolivia (4)Cochabamba, Bolivia (4)Santa Cruz, Bolivia (4)

298.04463.780

925.66794.254

183.997346.126138.109

1.283.349923.741695.226

1.811.390

56 kilometers209 kilometers405 kilometers300 kilometers 310 kilometers717 kilometers586 kilometers500 kilometers510 kilometers671 kilometers

1.177 kilometers

NorthNorthNorthSouthSouthSouthSouthEastEastEastEast

Pan-americanPan-americanPan-american5 North Road5 North Road5 North Road5 North Road

11 - CH11- CH11 - CH11 - CH

(1) population 2011(2) population 2007(3) population 2012(4) population 2009

1.2 AIR CONNECTIVITYThe city has an international airport, the “Chacalluta Airport”, located at 18.5 kilometers north of the city. The estimated travel time from the town to the airport is 20 minutes; this terminal registers 7 national flights each day destined to Santiago. Most of them are direct, although some stopover in Iquique and Antofagasta. Flights are carried out by two airlines: LAN and SKY AIRLINE.Arica is also connected abroad by air: SKY provides one daily flight to La Paz, Bolivia and two flights per week to Arequipa, Peru. On the other hand, LAN Peru offers three daily flights to Lima, Peru from Tacna airport, 40 kilometers away from Arica.

More information:www.lan.com ywww.skyairline.cl

Index 2010 2011 2012

16 INVEST IN ARICA AND PARINACOTA

1.4 RAILWAY CONNECTIVITY

Arica is connected by railway with La Paz (Bolivia). The train has a cargo transportation capacityof240,000tons/year,and209kilometersofthewholetrackarelocatedintheChilean side. This train was built after the Peace Treaty of 1904 between Bolivia and Chile.

There is also a train that connects Arica and Tacna. This railway belongs to the Peruvian government and it is used only for passenger transportation, although it is less important compared to road transportation. It has great touristic potential, which could be accom-plished if low investment were carried out in it.

1.5 MARITIME CONNECTIVITY

The Arica and Parinacota region has a port located in the center of the city. The port has a transference capacity of 3,956,000 tons. and it is composed by 5 sites. It has a paved sur-face of 185,445 m2, and 27,048 km2 of them are built (storehouses and other buildings). The statistics of traffic are:

75% of the tonnage corresponds to cargo in movement from Bolivia, country that has a treaty (“peace and friendship treaty” between Bolivia and Chile) since 1904, which deter-mined the boundary between the two countries, and by which Chile accorded to facilitate the free traffic of goods by the Arica port. According to the agreement, the Bolivian cargo does not pay storage the first 365 days since it was unloaded. Also, Bolivia does not pay for the first 60 days of storage of a cargo that will be loaded.

More information: www.puertoarica.clwww.tpa.cl

Source: CORDAP using EPA data base.

“According to the agreement,the Bolivian cargo does not pay

storage the first 365 dayssince it was unloaded.

Also, Bolivia does not payfor the first 60 days of

storage of a cargothat will be loaded.”

Merchant ships

Gross tonnage

295

2.131.367

352

2.659.060

241

2.590.830

17INVEST IN ARICA AND PARINACOTA

1.6 UNIVERSITIES AND TECHNICAL TRAINING INSTITUTES

Arica has many universities and technical training institutes, which allow the existence of qualified personnel available and also offers the possibility of training for workers. The universities have continuation of studies and evening studies programs.

1.7 HOTEL ACCOMODATIONS AND CASINOS

Arica has 50 accommodation premises for tourists and people that visit the region for work and businesses. Among these, we find hotels, houses with vacancy for tourists and hostels. There are a total of 1,430 rooms and 2,918 available beds (Source: INE).Putre, capital of the province of Parinacota, located at 135 kilometers to the east of Arica by 11-CH road at 3,500 meters above sea level, has 3 hotels and some hostels.Also, the city has a casino that belongs to the local government, and there is a project to build a new hotel-casino complex, the “Arica City Center”.

More information: http://www.visitarica.cl

Institution Type website

Universidad de TarapacáUniversidad Arturo PratUniversidad Santo TomásUniversidad Tecnológica INACAPCFT Santo TomásCFT INACAPCFT PukaráCFT Tarapacá

Public UniversityPublic UniversityPrivate UniversityPrivate UniversityTechnical Training InstituteTechnical Training InstituteTechnical Training InstituteTechnical Training Institute

www.uta.clwww.unap.clwww.santotomas.clwww.inacap.clwww.santotomas.clwww.inacap.clwww.cftpukara.clwww.cfttarapaca.cl

Source: CORDAP on Ministry of

Education database.

18 INVEST IN ARICA AND PARINACOTA

1.8 INDUSTRIAL ZONE OF ARICA

The city planning scheme of 2009 shows 3 industrial zones in Arica:ZI1, INDUSTRIAL ZONE 1: industrial sector destined for fishing and complementary ac-tivities along with accommodation activity. It is located at the south coastal boarder 5 kilometers away from the city.ZI2, INDUSTRIAL ZONE 2: industrial sector located at the north of the Lluta River, 10 ki-lometers from the city. It is formed by Puerta de America and Zofri-Chacalluta and it is destined to harmless annoying industry, complementary activities and infrastructure of all kinds.ZI3, INDUSTRIAL ZONE 3: Industrial area destined for harmless industry, except for health, education, culture and recreation equipments. It is located at the north of the city, among Santa Maria Avenue at east, Alejandro Azola Avenue at west, Ecuator Avenue at south and Los Artesanos Avenue at north.Appendix 1 shows the map of Arica with the location of its industrial zones.

More information: http://www.dom.muniarica.cl/pag.php?id=28&tipo=html

1.9 AVAILABLE AREAS

The Ministry of National Assets possesses 24 available pieces of land, which will be put out to tender to the best offer during 2013, for real estate projects and urban equipment, for a total of 72.26 hectares in the new industrial park Pampa Chacalluta. Also, there are 21 pieces of land destined to industrial and nonconventional renewable energy projects, for a total of 18.28 hectares, which will be put out to tender in the same period of time.The Ministry of National Assets has recently announced the adaptation of a new surface of 352.2 hectares in the new industrial park Pampa Chacalluta, to the east of Chacalluta Park administered by Zofri S.A, located at industrial zone 2. The plots will be put out to tender and the referential price of one hectare goes between 950 and 2,500 UF ($21,750,003 and $57,236,850), $40,000 and $120,000 in American dollars.

More information: http://www.bienesnacionales.cl/wp-content/uploads/2012/12/librobienes.pdf

19INVEST IN ARICA AND PARINACOTA

1.10 REGIONAL ECONOMY

The Arica and Parinacota region possesses a thriving regional economy, that after several years of postponement, is currently showing positive figures, manifesting a great advance in the regional economy for the last couple of years, due to public investment of public policies and the development of neighboring matters, that have turned Arica into a region of services.

Law N°20,655 about distant zones: a recently promulgated law that will thrust private investment in the region, strengthening the growing tendency. The tax advantages of the regional investment, coming from this and other laws, are detailed on the second part of this document.

Sources: 1 Central Bank of Chile2 National Institute of Statistics,

3 Internal Revenue Services,4 Arica’s Local Port Company,

5 AFP superintendence,6 Regional Government of Arica and

Parinacota*FNDR: National Development Fund

(destined for investment administered by a regional council)

**PROPIR: Public Regional Investment Program (amount of money invested in

the region by the government).

Indicator Period Value

Regional GDP (1)INACER 2003 (2)Workforce (2)Employment (2)Unemployment (2)Companies in the region (3)Company-sales in the region (3)Port movement (4)Taxable salary average (5)FNDR * (6) PROPIR ** (6)

2011October-December 2012 October-December 2012 October-December 2012 October-December 2012 20112011 2012 June 201220132012

$ 595.709 millions137.282,62778,0235.6 %13,906UF 50,151,135.52,590,830 Ton.$ 521,966$ 30,000,000$ 258,071,959,000

Troupe of dancers at carnival “With the power of the sun”.

Flamingo or Andean flamingo in Lluta estuary.

22 INVEST IN ARICA AND PARINACOTA

Chapter II INVESTMENT OPORTUNITIES IN THE REGION

2.1 AQUACULTURE IN ARICA AND PARINACOTA REGION

DescriptionAquaculture consists on growing aquatic plants or breeding fish, crustaceans and mol-lusks as hydro biological resources on under control environments, with the goal of ob-taining an abundant production for local purchase and commercial purposes.

The Arica and Parinacota region has a large marine surface. Currently, 13 maritime con-cessions have been given or are being processed at the south of Arica. Nevertheless, this activity is new, but it opens opportunities to develop associations and strategic alliances.

Potential MarketsThe main export markets for aquaculture are Japan, USA and the EU besides national de-mand for marine products.

Opportunities•Newindustryintheregion,littleornocompetitionatall.•FastdevelopmentofthePacificorJapaneseoyster(Crassostreagigas),comparedto breeding in other regions of the country.•Mildclimate,absenceofroughwaterandstorms.

Related webpages (public entities, local information):•NationalServiceofFishingandAquaculturehttp://www.sernapesca.cl/•ChileanNationalCouncilforScienceandTechnologyhttp://www.conicyt.cl/

Miscellaneous relevant information•TheAricaandParinacotaDevelopmentCorporationpresentedtheproject“Breedingof the Northern Pacific oyster”. The experimental phase turned out with positive results, proving to be a possible and profitable initiative.•Therearemarineproductsprocessingplantswithexperienceregardingexportationto EU, USA, Japan and Australia, among others.•Therearealreadyassignedandavailableconcessionsintheregion.

23INVEST IN ARICA AND PARINACOTA

2.2 AGRICULTURE IN ARICA AND PARINACOTA REGION

DescriptionThe Arica and Parinacota region is characterized by having a privileged climate. The aver-age temperature is 15° C minimum and 25°C maximum in the winter, and 20° and 30° respectively in the summer. This climate advantage allows farm workers to carry out their activities through the whole year. Regional agriculture is characterized by high-tech levels using drip irrigation and greenhouses with anti-aphid nets, allowing a high production in the valleys of Azapa and Lluta.TheLlutaValleyisazoneoffarmingandagriculturalexploitation,speciallycorn,onionsand garlic. On the other hand, the main products grown in the Azapa valley are olives, tomatoes, peppers and green beans. Besides, many seed companies have settled in the area, such as Pioneer, Maraseed and Syngenta.There are projects that will sustain the agricultural development of the region, such as the culverting of the Azapa waterway and the water reservoirs of Livilcar and Chironta. Plus, 1,050 hectares were put out to tender in Pampa Concordia. These initiatives will allow the expansion of the agricultural surface to 9,975 hectares.The province of Parinacota has agricultural valleys in the lower zones of the Andean mountain range in Belen, Socoroma, Chapiquilla, Lupica, Saxamar and Ticnamar, among others, and they offer products such as oregano and quinoa; products of high interna-tional demand. It is important to mention, that in the agriculture of Parinacota, due to the altitude of the ground (2,500 meters above sea level), practically, there are no plagues, allowing the development of an organic agriculture.

Potential MarketThe main goal for the regional products is the national market. Arica supplies the Central Zone of the country during winter, when vegetables are scarce. Also, exportation of olives, onions and garlic is carried out to Brazil.

Opportunities•TosupplytheCentralZonedemandduringwinterseason•Highefficiencyagriculture•Investmentprojectsthatwillallowanimprovementinthewateruse.

“The Lluta Valley is a zone of farming and agricultural exploitation, specially corn,

onions and garlic. On the other hand, the main products grown in the Azapa valley

are olives, tomatoes, peppers and green beans.

Besides, many seed companies have settled in the area, such as Pioneer, Maraseed and

Syngenta.“

24 INVEST IN ARICA AND PARINACOTA

Related webpages (public entities, local information)•MinistryofAgriculturehttp://www.minagri.gob.cl/•AgricultureandLivestockDevelopmentInstitutehttp://www.indap.gob.cl/•AgriculturalandLivestockServicehttp://www.sag.gob.cl/

Miscellaneous relevant information• Recently,theprojectPampaConcordiahasbeenputouttotender,withtheaimofset-ting up 1,050 hectares to grow tomatoes, peppers and lettuce, among others.• ThehydricmanagementplanhasanestimatedinvestmentcostofUS$250milliondol-lars; 97% of the cost is destined for infrastructure. The priority is to increase the amount of available resources, implementing water reservoirs and the culverting of the Azapa waterway. Thus, the plan contemplates a size increase of the irrigated area, due to the treated water from the city, and to the water from the Concordia aquifer.

2.3 CHAIN OF ACTIVITIES IN ARICA AND PARINACOTA REGION

DescriptionThe concept applies to the connection of goods and services with other countries, which having a minimal transformation process in Chile, are subsequently exported to markets in which Chile has benefits. This initiative has become relevant in Asian markets, where tariffs are high, but Chile is exempted from paying due to the commercial agreements, which translates into an important competitive advantage.The project suggests that entrepreneurs from other countries, that we will denominate “partners”, take part along with the Arica and Parinacota region, in a process of productive complementation, in order to export to destination markets, where Chile has preferential access. This project grins up multiple advantages, such as an increase in the exportation volume and strengthening of the already existent commercial relations among entrepre-neurs. In conclusion, is not about selling products from one country to another, but a mat-ter of working together towards a common goal (source: chain of activities, DIRECON).

Potential marketThe main exportation markets are countries that possess commercial treaties or free trade agreements with Chile

“The project suggests thatentrepreneurs from other countries, that we will denominate “partners”, take part along

with the Arica and Parinacota region, in a process of productive complementation, in order to export to destination markets,

where Chile has preferential access. “

25INVEST IN ARICA AND PARINACOTA

2.4 NONCONVENTIONAL RENEWABLE ENERGY IN ARICA AND PARINACOTA REGION

DescriptionNonconventional renewable energy (NCRE) is obtained through inexhaustible natural sources, such as the sun, wind or the sea, being transformed into electricity.The Arica and Parinacota region has unique conditions, a high solar radiation of 3,000 KWH/m2/year,andavailablezonesfortheinstallationofPVpowerplants.Windpoweris another of the NCRE that can be developed due to the climate advantages of the zone. Nevertheless, it has not been carried out so far. The Chilean desert provides an advantage related to the altitude, causing the dry air not to expand the electromagnetic waves, al-lowingtheaccumulationofthemonaPVpowerpanel.Theaccumulationofthewavesishigher than in Mojave Desert.

Opportunities•GeographiclocationofArica•ProximitywithPeruvianandBolivianmarkets•Emergencylawsthatallowrawmaterialstoenterthecountrywithoutpayinganytaxes (Industrial Free Trade Zone).•Chile’sprestigeasanexportingcountry•Toexpandtheexportableoffer,basedontheadvantagesofferedbytheregion.

Related webpages (public entities, local information)•Customswww.aduana.cl•Zofriwww.zofri.cl•MinistryofInternationalAffairswww.direcon.gob.cl

Other relevant information •ThereareBoliviancompaniesthat importwoodandBolivianfurniture,whichareex-ported to different countries. •Anchovyfilletscompanies,KYCSeafoodsLtda.andAgropescaS.A.importrawmaterialssemi elaborated from Peru, and in Arica plants can anchovies to export them to the United States, Europe and Australia.

26 INVEST IN ARICA AND PARINACOTA

These initiatives contribute to an autonomous power supply system in the region, on a country highly dependent on foreign oil. It is a challenge for the government, that by the year 2020, 20% of the Chilean energy supply will be composed by renewable energies, thus, the construction of renewable energy plants is essential for the sustainable development of the country.The goal of the government is to promote the regional climate and geographic conditions, in order to launch it as the capital of the renewable energies in Chile.In the Arica and Parinacota region there are 25 land applications addressed to the Na-tional Assets Ministry, which manifests a clear interest, especially from private actors, to develop NCRE projects in the zone.

Potential MarketTo cover the energetic demand of the country, specially the one generated by the mining companies.

Opportunities•Unexploredmarket,fewcompetitors.•Highdemandforcleanenergies,byminingandindustrialcompanies.•Largeareasofflatsurface.•Plantshavesocialacceptance,duetotheirnon-contaminantcondition.

Related web pages (public entities, local information)•MinistryofNationalAssetswww.bienesnacionales.cl•MinistryofEnergywww.minenergia.cl•MinistryoftheEnvironmentwww.mma.gob.cl•NationalCommissionofEnergywww.cne.cl•CenterofRenewableEnergieswww.cer.gob.cl

Miscellaneous relevant information •TherearethreeprojectsthatalreadyreceivedRCA(environmentalqualificationresolu-tion). The first one is the multinational Sky Solar Chinese plant, with an investment of US$70 millions and 127 hectares, located 26 kilometers away from Arica, in El Aguila hill. With84,240PVpanels,itproduces18MW.ThesecondprojectcorrespondstoPampadoscruces,oftheSolventusCompany,thatwillinvestUS$82millions,with313,020PVpanelsand 30 MW of power. The third project is carried out by Mainstream Renewable Power companies,withaninvestmentofUS$180millions.TheideaistobuildaPVparkcalled“ElAguila”,with252,000PVpanelsand70MWofpower,locatedat1,800metersabovesealevel on a surface of almost 146 hectares.

27INVEST IN ARICA AND PARINACOTA

2.5 LOGISTICS SERVICE IN ARICA AND PARINACOTA

DescriptionThe region is characterized by having two frontiers, with Peru at the north and Bolivia at northeast. Also, it has proximity with the west center of Brazil and northeast of Argentina.Arica and Parinacota is located in a strategic zone. Because of its characteristics, it meets the logistics needs of markets that require port, transportation and storage services. The port of Arica is one of the main terminals of Chile, which has had an important growing because of the great volume of Bolivian cargoes. Chile leads the South American logistics efficiency ranking, which makes it even more interesting to invest in this initiative, considering the great development of mining indus-tries.

Potential market:It is strongly oriented towards international markets.

Opportunities•Topromoteexportationofservices.•Lackofspecializedindustriesinparticularcargoes.•Toincreaseregionalcompetition.

Related webpages (public entities, local information)•Arica’sportenterpriseswww.puertoarica.cl•Arica’sportterminalwww.tpa.cl

•Bytheendofthefirstsemesterof2013,ElAguilaplantwillbeginfunctioning.With2MW of power, the plant will be connected to SING trough a substation, property of E-CL, which will allow covering a 30% of the energetic requirements of the operations from El Aguila, which belongs to Quiborax S.A.

“Arica and Parinacota is locatedin a strategic zone. Because

of its characteristics, it meetsthe logistics needs of markets that require

port, transportationand storage services.“

28 INVEST IN ARICA AND PARINACOTA

Miscellaneous relevant informationA large increase in the cargo movement in the port of Arica has occurred during 2012, moving 2,590,830 tons. A 75% of this volume corresponds to Bolivian cargo, a 15% corre-sponds to Chilean cargo, a 4% to Peruvian cargo, and the rest belongs to other countries.The implementation of an Interoceanic Corridor that will connect de Mato Grosso zone in Brazil with Arica

29INVEST IN ARICA AND PARINACOTA

2.6 MINING INDUSTRY SERVICES

DescriptionMining industry is a very important foundation for the development of the region. Cur-rently, there are several mining projects on the run. Although, there are projects already starting to function, the mining companies (nationals and transnationals) show great in-terest due to the potential offered by the high zone of the Andean mountain chain. Thus, the establishment of mining industries in the region, especially in Parinacota and Cama-rones, is imminent.The establishment of the facilities will need support services for the development of the activity, such as assembly services, engineering, construction, logistics, transportation, feeding, metallurgy, etc. it is an interesting opportunity of service supply for the mining companies installed in the region or even, in adjacent regions, such as Tarapaca, Antofa-gasta and the south of Peru, due to the geographical advantages of the region.

Potential MarketThere is a potential market soon to be open by the service companies for mining indus-tries, due to the government policies that have turned mining into an axis of development for the region, besides the already existing market of Tarapaca, Antofagasta and the south of Peru.

Opportunities•Newmarket•Scarceofferofminingservicesintheregion•Previouspreparationforservicedemand

Related webpages (public entities, local information )•MinistryofMiningwww.minmineria.gob.cl•MinistryofNationalAssetswww.bienesnacionales.cl•MinistryofEnergywww.minenergia.cl•MinistryofEnvironmentwww.mma.gob.cl

Miscellaneous relevant information•QuiboraxS.A,aplantthatprocessesandextractsulexite,hasaproductionof100,000tons. of boric acid, and it is considered as the third biggest producer in the world.

“The establishment of thefacilities will need support services for the

development of the activity, such as as-sembly services, engineering, construction,

logistics, transportation, feeding, metal-lurgy, etc. “

30 INVEST IN ARICA AND PARINACOTA

•Celite, aplant thatprocessesandextractsdiatomorkieselghur,hasaproductionof28,000 metric tons. per year.•CanCan,aminingcompanythatbelongstotheAngelinigroup,announcedtheopeningof the mining site Choquelimpie, a project that includes an investment of US$600 million. Tailings will be treated in a plant located in the same sector of Putre.•TheexplotationofSalamanquejadepositisthefirstinitiativeofPampaCamaronesS.A,a Chilean company created in 2009, which belongs to Pampa Mater S.A (65.3%), Arrigoni MineríaSpA(26.7%)andtoSamsungC&TChileCopperSpA(8%),withaninitialinvestmentof US$30,000,000. The deposit expects a production with resources of 12,000,000 tons. of average grade copper.•TheprojectLosPumas,whichbelongstoHemisferioSurMiningCompany (MHS),ex-pects a manganese production of 220,000tons. per month. The project is currently under SEIA evaluation.•TheSouthernCooperCorporationisinthemiddleofanexploringprocessforitsCata-nave project.•ThecompanyMineraRioTintoisinthemiddleofanexploringprocessforitsMamutaproject in Camarones, and Palmani in Alto Lluta.

2.7 TOURISM IN ARICA AND PARINACOTA

DescriptionThe Arica and Parinacota region is located in the northern border of the country. Arica County is known as “the city of eternal spring”, because of its friendly weather and great beaches, which can be visited during whole year. The region has a strong Andean influ-ence, and because of this, there are many touristic attractions, for people who want to learn about regional culture. Arica shares a border with Peru and Bolivia, manifesting a multicultural distinctive hallmark.The region possesses great archaeological sites for tourism, such as Chinchorro culture with mummies from 10,000 years B.C and geoglyphs and petroglyphs in Arica and Lluta valleys. These valleys posses an incalculable beauty; the arid desert mixes with the green of the fertile valleys. In Parinacota, people can see the Andes mountain range, where there is also the Chungara lake, the highest in the world located at 4,517 meters above sea level, and diverse villages in the foot hills, such as Putre Socoroma, belen, Ticnamar, Codpa and villagesintheAndeanhighplateau,suchasParinacota,CaquenaandVisviri.Theirculturalheritage is incomparable.The main characteristics of Arica are its pleasant climate and the mild temperatures of the ocean, which allow practicing water sports, such as surfing and body boarding.Arica is located in a halfway point between Machu Pichu and San Pedro de Atacama, close

“The region possesses greatarchaeological sites for tourism,such as Chinchorro culture withmummies from 10,000 years B.C

and geoglyphs and petroglyphsin Arica and Lluta valleys.“

31INVEST IN ARICA AND PARINACOTA

to Tiwanaku as well, a renowned archaeological site strategically located as a resting city for travelers.

Potential MarketDue to the cultural heritage and privileged climate, the market aims to the tourism for foreign and national travelers.

Opportunities•Agrowinginterestoftouristsfortourismofspecialinterest.•Cruiseseason.•ProximitywithTacna,acommercialtouristicattractionlocatedatthesouthofPeru,65kilometers away from Arica.•GreatroadconnectivitywithPeru,Boliviaandtherestofthecountry.•Greatairconnectivitywiththerestofthecountry,BoliviaandPeru.There isalso,anindirect connection with Peru, through Tacna Airport.

Related web pages (public entities and local information)•NationalServiceofTourismwww.sernatur.cl•VisitAricawww.visitarica.cl

Miscellaneous relevant information•Sernaturcarriedout,alongwithArturoPratUniversity,aconservationprojectwitheco-touristic value for the green turtles that are located in the coastal borderline of Chinchorro beach, in Puntilla, which will become an important touristic attraction.•Thereisaprojectofrestorationfor30churchesintheAndeanfoothills.ThechurcheswerebuiltbetweenthecenturiesXVIIandXVIIIandtherestorationiscarriedoutbyFun-dacion Altiplano, and it is called “Ruta de las Misiones”. The idea is to generate a touristic route through the foot hill villages, visiting the pre-Columbian churches of the area.•TheAndeanCarnival“INTICH’AMAMPI”gathersover7,000dancerswhoduringthreedays dance through the streets of the city with colorful costumes.•Theinternationalchampionshipofsurfing,inthewavenamed“ElGringo”intheformerisland El Alacran gathers the most important exponents of the world.•ItisimportanttoremarkthegreattouristicdevelopmentofPutre,capitaloftheprovinceof Parinacota, where interesting touristic projects have been developed, being even com-pared to San Pedro de Atacama.

32 INVEST IN ARICA AND PARINACOTA

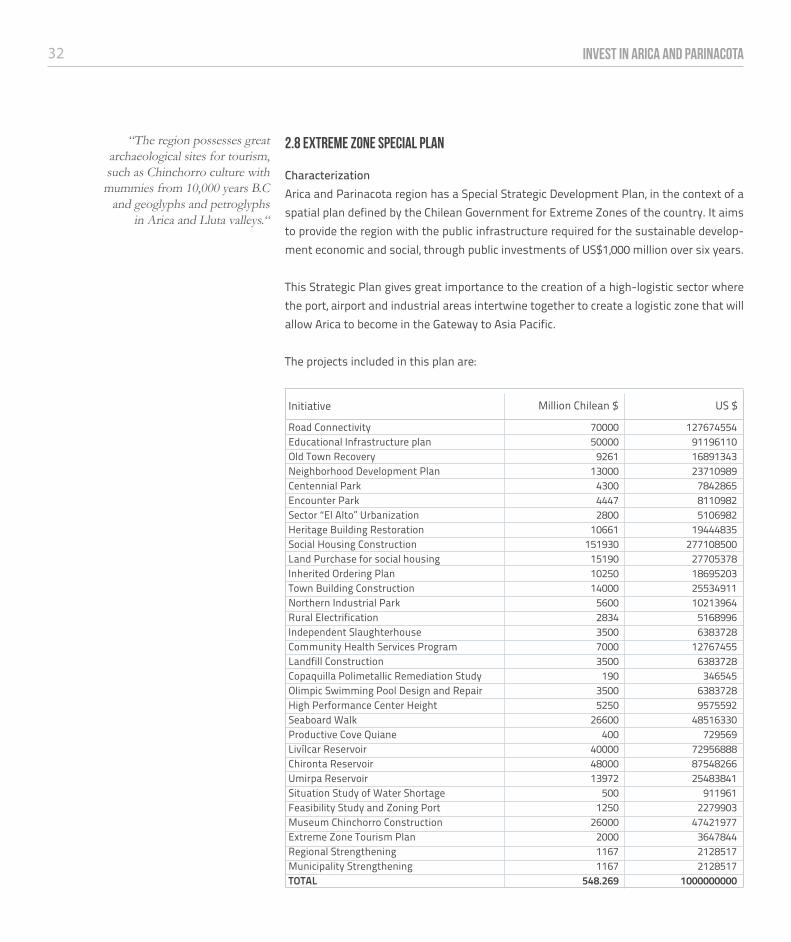

2.8 EXTREME ZONE SPECIAL PLAN

CharacterizationArica and Parinacota region has a Special Strategic Development Plan, in the context of a spatial plan defined by the Chilean Government for Extreme Zones of the country. It aims to provide the region with the public infrastructure required for the sustainable develop-ment economic and social, through public investments of US$1,000 million over six years.

This Strategic Plan gives great importance to the creation of a high-logistic sector where the port, airport and industrial areas intertwine together to create a logistic zone that will allow Arica to become in the Gateway to Asia Pacific.

The projects included in this plan are:

“The region possesses greatarchaeological sites for tourism,such as Chinchorro culture withmummies from 10,000 years B.C

and geoglyphs and petroglyphsin Arica and Lluta valleys.“

Initiative Million Chilean $ US $

Road ConnectivityEducational Infrastructure planOld Town RecoveryNeighborhood Development PlanCentennial ParkEncounter ParkSector “El Alto” UrbanizationHeritage Building RestorationSocial Housing ConstructionLand Purchase for social housingInherited Ordering PlanTown Building ConstructionNorthern Industrial ParkRural ElectrificationIndependent SlaughterhouseCommunity Health Services ProgramLandfill ConstructionCopaquilla Polimetallic Remediation StudyOlimpic Swimming Pool Design and RepairHigh Performance Center HeightSeaboard WalkProductive Cove QuianeLivílcar ReservoirChironta ReservoirUmirpa ReservoirSituation Study of Water ShortageFeasibility Study and Zoning PortMuseum Chinchorro ConstructionExtreme Zone Tourism PlanRegional Strengthening Municipality StrengtheningTOTAL

7000050000

926113000

430044472800

10661151930

151901025014000

56002834350070003500

19035005250

26600400

400004800013972

5001250

26000200011671167

548.269

127674554911961101689134323710989

784286581109825106982

19444835277108500

27705378186952032553491110213964

51689966383728

127674556383728

34654563837289575592

48516330729569

729568888754826625483841

9119612279903

47421977364784421285172128517

1000000000

33INVEST IN ARICA AND PARINACOTA

Potential MarketCover the needs that will be generated through the design, engineering study and imple-mentation of works that includes the Special Plan of Strategic Development.

Opportunities- Building and Engineering Companies- Architectures Companies- Specialized Companies on Consulting and Studies of Soil, etc.

Other InformationIt has been nominated a responsible manager for the successful achievement of this Stra-tegic Development Plan for Arica and Parinacota. He works for the Regional Government of Arica and Parinacota and he is a Mayor’s adviser about this matter and the person in charge of the coordination of different regional address involved in the design and execu-tion of the works.

Alpaca in the wetlands of Parinacota.

36 INVEST IN ARICA AND PARINACOTA

CHAPTER III POTENTIALITIES AND TAX ADVANTAGES OF THE REGION

3.1 TAX CREDIT TO REGIONAL INVESTMENT

The tax credit to regional investment is an incentive for the first category taxpayers that invest over 5000 UTM in Arica or Parinacota. The investment is destined for the production of goods or services. There is no upper limit for the investment; therefore, there is no limit for the tax credit.The benefit is automatic (does not require application) and it corresponds to a 30 or 40% of the investment. Arica investors have the right to a 30% of credit for the investment. The ones carried out in Parinacota generate a tax credit of 40%, same percentage than the investments carried out for tourism in Arica.When the amount of the credit is equal or higher than the average of the first category tax determined for the last three years, the compulsory monthly payment (PPM) could be completely suspended.It is important to remark that the profits defined by the law, correspond to the whole year profit of the company, whether they belong to activities carried out in the region or for the investment carried out outside it. This gives to the credit a particular recovery speed for national companies already established that also have activities in other regions of the country. The income tax that must be paid for the profits generated in the rest of the country will be paid by the tax credit obtained in the region, and devolution of the already paid PPM (monthly provisional payment) will be given.This benefit is in force for investments carried out before December 31, 2025, and the tax credit will be implemented until year 2045.

More information:http://www.sii.cl/contribuyentes/actividades_especiales/zonas_extremas.htm#aricahttp://www.leychile.cl/Navegar?idNorma=30787

1 UTM= US$ 70,47At September 30, 2014

Tax Credit Arica Act• Taxpayers are allowed to claim this be-nefit since January 1, 2012 until December 31, 2025 and the Credit recovery entitled can be made until 2045. • The credit rate for industrial projects or services is: 30% to Arica, 40% to Parinaco-ta and 40% to touristic projects, calculated on the new depreciable fixed assets net value. • Minimum investment 500 UTM• No contest.• Might be used to pay income tax 1st class. • The paid income tax generates the Tax Credit 1st Class that will reduce the Com-plementary or earnings distributions.

37INVEST IN ARICA AND PARINACOTA

3.2 INDUSTRIAL FREE TRADE ZONE

The manufacturing industrial companies installed in Arica enjoy the benefit of the prefer-ential tax regime established by law 1055 (1975), meaning, that they can be a part of the Free Trade Zone system of Arica. By definition, the industrial companies carry out activities in factories, plants or work-shops, destined to produce merchandise with a final product which is different than the raw materials, parts or pieces used in the manufacturing process. The preferential tax regime is also applicable to the companies that during their produc-tive process cause an irreversible transformation in foreign raw materials, parts or pieces used in the manufacturing process, that add value to the final product.Raw materials, pieces and parts that are imported to be incorporated into the final product areexemptedfrompayingsometaxes,fees,customburdensandVAT(value-addedtax).Also, the services required for the industrial process are exempted from paying value-added taxes, such as transportation, electric energy, water, etc, according to the law 20,655 for distant zones.The products elaborated by Free Trade Zone companies, are exempted from paying taxes, fees and custom burdens (including clearance fees) when transported to the rest of the country.The companies that are users of the Industrial Free Zone have the benefit that, when they buy raw material and necessary products for the industrial process in local business (Arica),theyarenotliabletopaytaxesontheseinputspurchase(VAT).

More information:http://www.sii.cl/pagina/jurisprudencia/legislacion/complementaria/dfl_341.htmhttp://www.sii.cl/pagina/jurisprudencia/legislacion/complementaria/dfl_341.htmhttp://www.zofri.cl/index.php/es/atractivos-para-la-inversion-.html

Industrial Free Zone • Purchases exempted of VAT and fee.• Purchases exepmted of VAT. • Utilities exempted of income tax 1st class.• Valid until December 31, 2030.

38 INVEST IN ARICA AND PARINACOTA

3.3 WORKFORCE HIRING BONUSES

Monthly bonuses handed over to the employers of Arica and Parinacota for workforce hir-ing and the payment of the consequent taxes.The bonuses correspond to a 17% of $182,000 ($30,940), a standard value which is adjusted every January 1st according to the CPI of the year.Workers that are partners or owners, and direct relatives are excluded from the benefit. The employers from these sectors are also excluded:The public sector, small and medium-scale copper and iron enterprises, companies in which the state of its enterprises receive a governmental fee of more than a 30%, mining companies that directly or indirectly hire more than 100 workers at the same time, bank-ing corporations, financial corporations, insurance companies, deductive fishing, pension funds administrators, private health insurance companies, currency exchange agencies, insurance brokerage firms, employers that receive bonuses according to the law n° 701, from 1974 (incentive for the development of forestation) and independent and profes-sional workers.This benefit is currently in force until December 31, 2025.

More information:http://www.sii.cl/pagina/jurisprudencia/adminis/2003/renta/ja509.htmhttp://www.tesoreria.cl/web/Contenido/Documentos/3770/guia_egresos.pdf

3.4 INVESTMENT BONUSES: PRIMING FUND AND DEVELOPMENT OF DISTANT ZONES

The bonuses are grant funds to promote the development of small and medium size busi-ness and services and investments carried out in: construction, machinery and equipment, special animals for reproduction, and transportation vehicles with capacity for more than 2,500 kilograms and passenger transportation vehicles for more than 14 passengers.The maximum allowable bonuses correspond to a 20% of the investment or 50,000 UF (indexation unit, 1 UF is equivalent to $22,800 or US$45), and as a requirement, the benefi-ciary annual sales cannot exceed 40,000 UF.This benefit has been extended until December 31, 2025.

More information:http://www.leychile.cl/Navegar?idNorma=3941http://www.corfo.cl/programas-y-concursos/programas/dfl-15-bonificacion-a-compra-de-bienes-de-capital-para-zonas-extremas

Workforce bonus DL.889• A 17% bonus on a taxable base of $182,000 given to workforce hiring, which equals $30,490 per worker• The benefit is effective from January 1st of 2012 until December 31, 2025.

Investment Bonus DFL/15• A 20% Investment/reinvestment bonus on depreciable fixed assets• Bonus rate of 20% of the new/first fixed assets value in the country• Applicant requirements: Maximum investment of 40,000 UF; sales must’s exceed 50,000 UF• Grant fund• The benefit is effective from 2012 to 2025

39INVEST IN ARICA AND PARINACOTA

3.5 SIMPLIFIED EXPORTING SYSTEM (also known as VAT refund for tourists)

When leaving the country, crossing the customs of Chacalluta, foreigners that bought products in licensed businesses (allowed to extend bills for foreign people), may recover theVATvalueintheofficeoftheTreasureDepartment,locatedinthecustom.Themini-mum purchase is 0.5 UTM (US$40). The tourist will be able to ask for a refund of US$2,000 dollars per day.This tool improves the commerce competition of licensed businesses in Arica, taking into account that Tacna also has a Free Trade regime (ZOTAC), and the rates of informal flow trade is very high.

More information:http://www.sii.cl/documentos/resoluciones/2009/reso67.htmhttp://www.sii.cl/documentos/circulares/2009/circu33.htm

3.6 EXPORTATION CENTERS

Exportation centers are considered within the incentive plan for the development of the region, pointed out by law 19,420 (2001). These centers are private areas located in the region, destined to collect national goods, and from other foreign and South American countries,freefrompayingVATandcustomfees.Goods are allowed to be exhibited, packed, unpacked, labeled, re-packed and then sent to different destinations: foreign lands, Zofri and Arica’s Free Trade Zone, free from taxes. The delivery to the Trade Free Zone has a 0.58% of the CIF value, and to the rest of the countryapaymentofcustomburdensandVATmustbecarriedout.Thecargomovementmust be a wholesale transaction, or whose value exceeds 15 UTM (US$1,200)

More information:http://www.chileatiende.cl/fichas/ver/19http://www.leychile.cl/Navegar?idNorma=30787

40 INVEST IN ARICA AND PARINACOTA

3.7 EXTENSION FREE TRADE ZONE

Iquique Free Zone, established by Decree with Law Force N° 341 in 1975, determined that everyoneofTarapacáRegion(whichthenincludedAricaandIquique),whethernaturalorlegalpersons(companies)canbuyforuseand/orconsumptiongoodsthataretosalewithintheprecinctsoftheFreeZone(ZOFRI),willbeextentoftheVAT(IVApayment).Theconcept of Extension Free Zone it’s defined by every territory that was in the Tarapaca Region,outsidethewalledcityofIquiqueZOFRI.WiththecreationofXVRegionofAricaandParinacota,October8th,2007,wassplitfromtheformerTarapacáRegionanditkeepfully the benefit of been Extension Free Zone.The companies’ benefits that are in Arica, by the fact of being located in Extension Free Zone, allows them to buy in the Commercial Free Zone, every kind of free merchandise oftheAggregateValueTax,theyalsocanaccesstobeCommercialFreeZoneusers, inthe form of Public Warehouse (without storage or market in Iquique), which leads to the realization of a hybrid business model (general regime and free trade zone regime), and can use both tax regimes.The costs associated to access to be users of the Commercial Free Zone or others inquiries can be address to the following emails: [email protected]/[email protected]

More information:http://www.leychile.cl/Navegar?idNorma=30787

3.8 SPECIAL TAXES FOR RESIDENTS

The residents of Arica and Parinacota enjoy a “regional bonus” consisting on a reduction of the tax base in which the calculation of the Income Tax and the Global Complementary Tax are applied, so it is not an income. The dependent workers with a contract according to the Labor Code and the independent workers that issue receipts for fees for their services, enjoy this reduction.The “regional bonus” is equivalent to the 40% of the income, with a maximum bonus equal to the local bonus that a public employee grade 1-A of the Unique Scale of Salaries on the public section receives, according to the D.L. N° 249 of 1974: the 56% of $546.953, ie, $306,294 monthly income untaxed.

More Information:http://www.leychile.cl/Navegar?idNorma=5904http://www.sii.cl/documentos/circulares/1976/circu10a.htm

41INVEST IN ARICA AND PARINACOTA

3.9 REGISTRATION CERTIFICATE

The Arica and Parinacota region has others benefits for the people of the region: the Ar-ticle 13 of the Municipal Income Act reduces a 50% of the annual vehicle appraised value fixed by the Internal Revenue Service (IRS), the registration certificate is calculated over this value.This benefit only applies to the particular cars, luxury rental cars, passenger or special ser-vices vehicles, station wagons, vans, ambulances, hearses, cars, trucks and motorcycles whose owners reside in the region.Appendix 2 includes a report on the extent of the Law for End Regions to the Arica and Parinacota Region, made by the attonery Mr. Raúl Castro Letelier

More Information:http://www.sii.cl/pagina/jurisprudencia/legislacion/complementaria/ley_3063a.htm

Reconstruction of churchesin the Andean foothills.

44 INVEST IN ARICA AND PARINACOTA

CHAPTER IV BENEFITS REQUIREMENTS AND PROCESSING

4.1 INVESTMENT TAX CREDIT

Benefit Name INVESTMENT TAX CREDIT

Arica and Parinacota Internal Revenue Service Address: Arturo Prat N° 305, AricaPhone: 56-58-2587000www.sii.cl

• To have started operations.• To be a taxpayer affected by the First Class of the Tax Act Income. • To take full accounts.• The minimum investment is 500 UTM

The taxpayer must inform the credit to the IRS by affidavit attaching a technical detail of the investment which must specify at least:• Description of the taxpayer activities. • Description of the investment and the outreach. • Production or services capabilities today. • Production or services capabilities once the investment is done. • Financing of the investment.• Details of property to be acquired or built.• List of the bills that support the investment.• Total amount of the investment.• Gantt chart of the investment.

Notify the IRS of credit to be used in the respective Tax Year, on Form 22, Code 390. Applicable until 2045.

Tax Year 2025.

Institution

Requirements

Process

Bonus Payment

Time limit to invest

45INVEST IN ARICA AND PARINACOTA

4.2 ARICA INDUSTRIAL FREE TRADE ZONE

Benefit Name ARICA INDUSTRIAL FREE ZONE

Arica Industrial Free Zone Address: Chacalluta Industrial ParkPhone: 56-58-2585000www.zofri.comCustoms Regional DirectorateAddress: San Martin N° 141, 1st Floor, Alborada BuildingPhone: 56-58-2207100www.aduana.cl

•To be First Class taxpayer.• Perform an industrial process.

Make a presentation to the Arica Industrial Free Trade Zone with the following docu-ments in 4 copies:• Cover letter and document delivery to the Manager of Arica Industrial Free Zone.• Legal Representative Power (if applicable).• Representative ID photocopy.• Special Purpose Background Certificate.• Notarized affidavit.• Constitution deed.• Join to the Commercial Register.• Official Journal Publication. • Property deeds where will be the industrial processes with boundaries of the enclosure (sketch).• VAT number copy.• Last Year balance (if applicable).• User request. • Project Profile. Afterwards, it is sent to the Customs and once you receive the Resolution, must be sent to Intendancy for the issuance of the Resolution, proceeding to perform the Contract as Industrial User of the Arica Industrial Free Zone.

Indeterminate

Institution

Requirements

Process

Time limit

46 INVEST IN ARICA AND PARINACOTA

4.3 WORKFORCE HIRING BONUSES

Benefit Name WORKFORCE HIRING BONUSES

Arica and Parinacota Regional TreasuryAddress: Arturo Prat N° 305, AricaPhone: 56-58-2231150 58-2235590www.tesoreria.cl

• Pension quotes monthly paid.• Affidavit, declaring not been convicted in the past six months for anti-union practi-ces or violation to fundamental rights of the workers.

The process can be done in person at the Treasury Department or online through the website: Present Process:• Employer ID.• Bill of taxation of the month requested.• Deed of the Company (Corporations).• Bonus Application.• Affidavit.• Company VAT number.Online Process:• Must request the key on the Treasury website.• Go to Hiring Manpower Bonus.• Follow the instructions. The computer system feeds on information provided by the AFP and INP. The system processes the bonus applications online, giving immediate response to the request.

5 days after application is approved.

Annual

Institution

Requirements

Process

Bonus Payment

Time limit

47INVEST IN ARICA AND PARINACOTA

4.4 INVESTMENT BONUSES: PRIMING FUND AND DEVELOPMENT OF DISTANT ZONES

Benefit Name INVESTMENT BONUSES

Arica and Parinacota CORFOAddress: 7 de Junio N° 268, 7th floor, AricaPhone: 56-58-2351650www.corfo.cl

• Annual sales under 40.000 UF• Investment above 50.000 UF• Companies are excluded if the products are related to: • Copper and Iron Mines • Extractive Industrial Fishing • Public Sector

Rules and forms are available at CORFO’s website or can be withdrawn in Arica’s CORFO office, the application occurs here and the background application must be filed on CORFO’s offices, Arica Provincial Government and Parinacota Provincial Government before time limit. The documentation to be attached is:• Application of investment or reinvestment bonuses on Distant Zones• Start of operations photocopy.• ID and VAT number photocopy for natural persons.• Banking report if bank financing is required.• Social Deed and its amendments, Official Journal Publication, Commercial Registry, Notary authorized Devolution.• Validity Certificate.• Company and Legal Representative VAT number.• Latest Income Tax Return (Form 22).• Last 12 VAT returns (Form 29).• Last Tax Balance. • Project Profile to run must include at least: •Market Aspects •Technical Aspects •Organizational Aspects •Economic and Financial Aspects •Result of Project Status •Environmental Impact Considerations

From November 15 to December 31.

During the first quarter of next year

Institution

Requirements

Process

Time limit

Bonus Payment

48 INVEST IN ARICA AND PARINACOTA

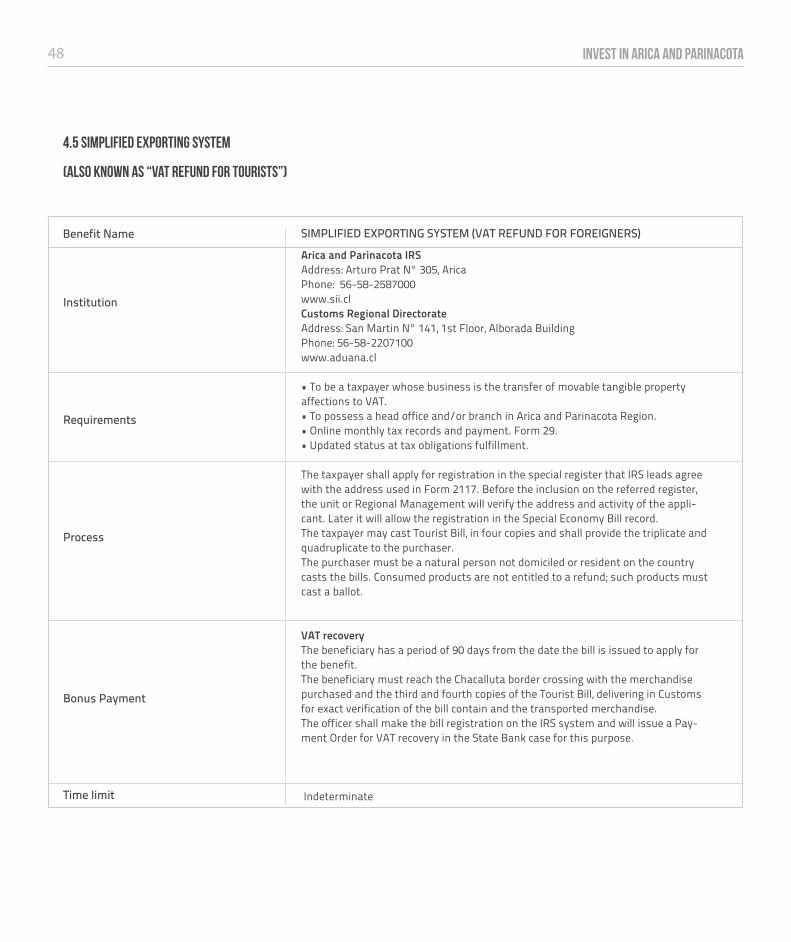

4.5 SIMPLIFIED EXPORTING SYSTEM

(ALSO KNOWN AS “VAT REFUND FOR TOURISTS”)

Benefit Name SIMPLIFIED EXPORTING SYSTEM (VAT REFUND FOR FOREIGNERS)

Arica and Parinacota IRS Address: Arturo Prat N° 305, AricaPhone: 56-58-2587000www.sii.clCustoms Regional DirectorateAddress: San Martin N° 141, 1st Floor, Alborada BuildingPhone: 56-58-2207100www.aduana.cl

• To be a taxpayer whose business is the transfer of movable tangible property affections to VAT.• To possess a head office and/or branch in Arica and Parinacota Region. • Online monthly tax records and payment. Form 29. • Updated status at tax obligations fulfillment.

The taxpayer shall apply for registration in the special register that IRS leads agree with the address used in Form 2117. Before the inclusion on the referred register, the unit or Regional Management will verify the address and activity of the appli-cant. Later it will allow the registration in the Special Economy Bill record.The taxpayer may cast Tourist Bill, in four copies and shall provide the triplicate and quadruplicate to the purchaser.The purchaser must be a natural person not domiciled or resident on the country casts the bills. Consumed products are not entitled to a refund; such products must cast a ballot.

VAT recoveryThe beneficiary has a period of 90 days from the date the bill is issued to apply for the benefit.The beneficiary must reach the Chacalluta border crossing with the merchandise purchased and the third and fourth copies of the Tourist Bill, delivering in Customs for exact verification of the bill contain and the transported merchandise.The officer shall make the bill registration on the IRS system and will issue a Pay-ment Order for VAT recovery in the State Bank case for this purpose.

Indeterminate

Institution

Requirements

Process

Bonus Payment

Time limit

49INVEST IN ARICA AND PARINACOTA

4.6 EXPORTATION CENTERS

Benefit Name EXPORTATION CENTERS

Finance Ministry

• Natural or Legal person.• Fulfill requirements specified in tender.

The Exporting Centers Administration will be put out to tender by the Treasury Department. The contracts relating to the Exporting Centers administration and operation will be established by Supreme Decree issued by Treasury

Indeterminate

Institution

Requirement

Process

Time limit

Arica’s San Marcos Church, built in France on the Gustavo Eiffel and Co. workshops, opened in July, 1876.

Typical Craft from Parinacota Province.

52 INVEST IN ARICA AND PARINACOTA

CHAPTER V – COMPARATIVE ANALYSIS OF RESULTS By Luis Araníbar, International Service Ltda.

5.1 COMPARATIVE TABLE: SUMARY ANALYSIS OF ARICA AND PARINACOTA REGION INCENTIVES

The following table summarizes the benefit analysis results of each business model, assumption considers US$1.000.000 investment, 40 workers labor, $ 400.000.000 annual gross sales and $ 40.000.000 annual profit, used in each posture:

ITEM/INCENTIVE TO ANALYZE

NOT APPLICABLETAX CREDITARICA ACTDFL-15 BONUS(OPTION)

MANPOWER BONUS

INDUSTRIALFREE ZONE

GENERAL SYSTEM COMPANY IN ARICA

INDUSTRIAL ZONECOMPANY IN ARICA

GENERAL SYSTEM COMPANY WITH HEAD OFFICE IN

SANTIAGO AND BRANCHIN ARICA FREE ZONE I

GENERAL SYSTEM COMPANY OUT OF

ARICA

$ 144.000.000 $ 144.000.000 $ 144.000.000

NOT APPLICABLE $ 96.000.000 $ 96.000.000 NOT APPLICABLE

NOT APPLICABLE $ 193.065.600 $ 193.065.600 $ 193.065.600

• Exempt from payment income tax.• Exempt from payment VAT.• Exempt from payment of fees. • Exempt from payment of MPP.• Subject to payment of tax law 18,211, equivalent to 0,58% of good CIF value.

Only to branch in Arica Free Zone: • Exempt from payment income tax.• Exempt from payment VAT.• Exempt from payment of fees. • Exempt from payment of MPP.• Subject to payment of tax law 18,211, equivalent to 0,58% of good CIF value.

NOT APPLICABLE NOT APPLICABLE

To any branch out of free zone, subject to:• Payment income tax of first class, which can be paid with Tax Credit of Arica Act, for both utilities, branch and head office.• Monthly Provisional Payments (MPP)• VAT

Subject to::• Payment income tax of first class, which can be paid with Tax Credit of Arica Act.• Monthly Provisional Payments (MPP)• VAT

Subject to:• Payment income tax of first class • Monthly Provisional Payments (MPP)• VAT

NOT APPLICABLEGENERAL SYSTEM

$ 01st YEAR INCENTIVES $ 22.851.200 $ 22.851.200 $ 100.000.000

$ 0INCENTIVESPROJECTION 2025

$ 337.065.600 $ 337.065.600 $ 337.065.600

$ 0INCENTIVE VS INVEST-MENT CONTRIBUTION

70,22% 70,22% 70,22%

53INVEST IN ARICA AND PARINACOTA

5.2 PRACTICAL EXAMPLE 1General System Company located out of Arica (In the rest of the country)

• Investment in new depreciable fixed assetsExchange rate CPL $480.- • Number of workers • Annual net sales• Utility

US $ 1.000.000$ 480.000.000 40$ 400.000.000$ 40.000.000

Records

• VAT taxpayer • Income Tax first class taxpayer

Rate 19%Rate 20%

Tax Area

• Debit sales tax (400.000.000 x 19%)• Income tax first class (40.000.000 x 20%)

$ 76.000.000 $ 8.000.000

Tax determination

• Tax Credit Arica Act • Investment Bonus DFL-15 • Manpower Bonus DL. 889 • Industrial Free Zone

NOT APPLICABLENOT APPLICABLENOT APPLICABLENOT APPLICABLE

INCENTIVES APLICATION

54 INVEST IN ARICA AND PARINACOTA

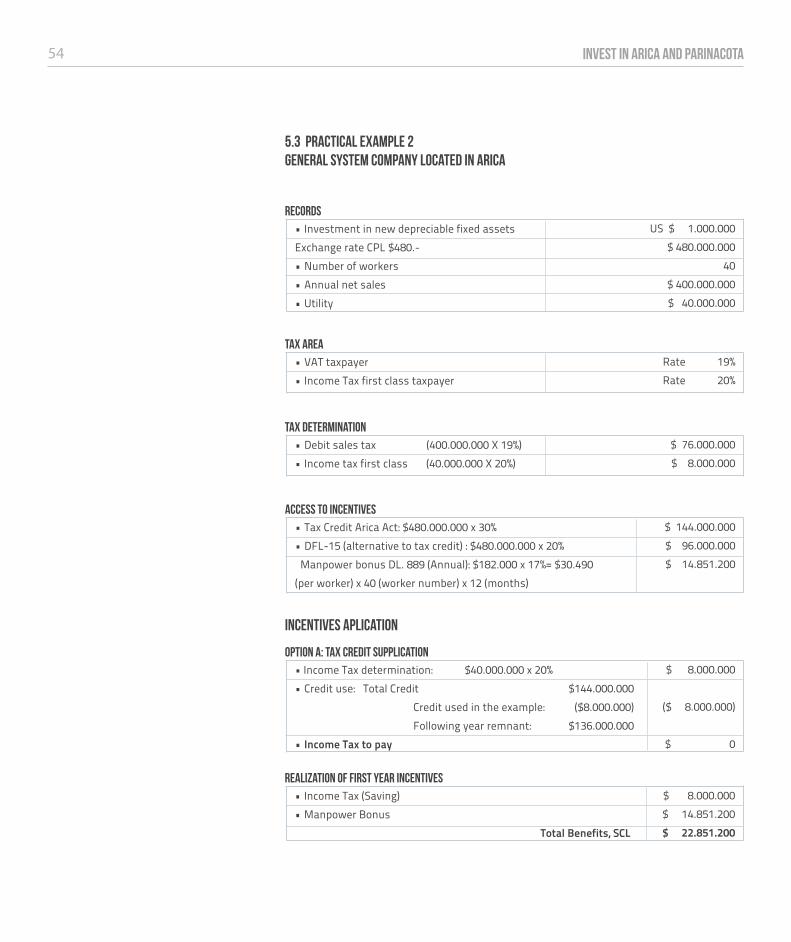

5.3 PRACTICAL EXAMPLE 2General System Company located in Arica

• Investment in new depreciable fixed assetsExchange rate CPL $480.- • Number of workers • Annual net sales • Utility

US $ 1.000.000$ 480.000.000 40$ 400.000.000$ 40.000.000

Records

• VAT taxpayer • Income Tax first class taxpayer

Rate 19% Rate 20%

Tax Area

• Debit sales tax (400.000.000 X 19%)• Income tax first class (40.000.000 X 20%)

$ 76.000.000 $ 8.000.000

Tax determination

• Tax Credit Arica Act: $480.000.000 x 30%• DFL-15 (alternative to tax credit) : $480.000.000 x 20% Manpower bonus DL. 889 (Annual): $182.000 x 17%= $30.490(per worker) x 40 (worker number) x 12 (months)

$ 144.000.000$ 96.000.000$ 14.851.200

Access to incentives

INCENTIVES APLICATION

• Income Tax determination: $40.000.000 x 20%• Credit use: Total Credit $144.000.000 Credit used in the example: ($8.000.000) Following year remnant: $136.000.000• Income Tax to pay

$ 8.000.000

($ 8.000.000)

$ 0

OPTION A: Tax Credit Supplication

• Income Tax (Saving)• Manpower Bonus

Total Benefits, SCL

$ 8.000.000$ 14.851.200 $ 22.851.200

Realization of First Year Incentives

55INVEST IN ARICA AND PARINACOTA

• Income Tax first class (Saving)• Manpower Bonus: 14.851.200 X 13

Total Benefits, SCL

Incentive vs. Investment Contribution: 70,22%

$ 144.000.000$ 193.065.600 $ 337.065.600

Incentives projection to 2025 (13YEARS)

• Investment in new depreciable fixed assets: • Calculation of DFL-15 Bonus: $480.000.000 x 20%

$ 480.000.000$ 96.000.000

OPTION B: DFL-15

Note: When the company gets the DFL-15 benefit by investments, the company earns only once a maximum amount equivalent to 20% of capital expenditures, which disables the company to get another benefit for its investments, such as tax credit of Arica Act. A company can apply to only one of the benefits of the area for any investment.

• Bonificación DFL-15• Bonificación a la mano de obra

Beneficios totales, en pesos

$ 96.000.000$ 14.851.200 $ 110.851.200

Realization of First Year Incentives

• DFL-15 Bonus• Manpower Bonus

Total Benefits, SCL

Incentive vs. Investment Contribution: 60,22%

$ 96.000.000$ 193.065.600 $ 289.065.600

Incentives projection to 2025 (13 YEARS)

56 INVEST IN ARICA AND PARINACOTA

5.4 PRACTICAL EXAMPLE 3Industrial Free Trade Zone Company in Arica

• Investment in new depreciable fixed assetsExchange rate CPL $480.- • Number of workers • Annual net sales • Utility

US $ 1.000.000$ 480.000.000 40$ 400.000.000$ 40.000.000

Records

• VAT taxpayer • Income Tax first class taxpayer

Rate 19%Rate 20%

Tax Area

• Debit sales tax • Income tax first class

Exempt Exempt

Tax determination

• Tax Credit Arica Act: $480.000.000 x 30%• DFL-15 (alternative to tax credit) : $480.000.000 x 20% Manpower Bonus DL. 889 (Annual): $182.000 x 17%= $30.490 (per worker) x 40 (worker number) x 12 (months)

$ 144.000.000$ 96.000.000$ 14.851.200

Access to incentives

INCENTIVES APPLICATION

• Income Tax determination: $40.000.000 x 20%• Credit use: Total Credit $ 144.000.000 Credit used in the example: ($ 8.000.000) Following year remnant: $136.000.000

Income Tax to pay

$ 8.000.000

($ 8.000.000)

$ 0

OPTION A: TAX CREDIT (Temporal disclaimer to the Income Tax exemption)

• Income Tax (Saving)• Manpower Bonus

Total Benefits, SCL

$ 8.000.000$ 14.851.200 $ 22.851.200

Realization of First Year Incentives

57INVEST IN ARICA AND PARINACOTA

• Income Tax first class (Saving)• Manpower Bonus: 14.851.200 X 13

Total Benefits, SCL

Incentive vs. Investment Contribution: 70,22%

$ 144.000.000$ 193.065.600 $ 337.065.600

Incentives projection to 2025 (13 years)

• Investment in new depreciable fixed assets: • Calculation of DFL-15 Bonus: $480.000.000 x 20%

$ 480.000.000$ 96.000.000

OPTION B: DFL-15

Note: When the company gets the DFL-15 benefit by investments, the company earns only once a maximum amount equivalent to 20% of capital expenditures, which disables the company to get another benefit for its investments, such as tax credit of Arica Act. A company can apply to only one of the benefits of the area for any investment.

• DFL-15 Bonus• Manpower Bonus: 14.851.200 X 13

Total Benefits, SCLIncentive vs. Investment Contribution: 60,22%

$ 96.000.000$ 193.065.600 $ 289.065.600

Incentives projection to 2025 (13 years)

Partner withdrawal (natural person)Increased overall gross income (factor 0,25)Taxable income for Global Complementary TaxTax or factor 0,32 Amount to reduceDeterminated taxReduction Income Tax first classReturn

$ 40.000.000 $ 10.000.000 $ 50.000.000 ($ 16.000.000)

$ 8.672.432,2 $ 7.327.567,8

$ 10.000.000 $ 2.672.432

Income Tax Credit first class in the on withdrawals or profit sharing

1 Increased overall gross income by First Class Tax: When appropriated apply the credit provided in Article 56, number 3 of de Income Tax Act, for quantities withdraw or distributed an amount equal to this will be added for the same overall gross income year and will be considered as a amount affected by the income tax 1st category to calculate this credit (final paragraph of Article 54, N° 1). Source: Manual de Consultas Tributarias Nº275.2 It is the taxable income factor found in the section between $43.422.480 and $57.896.640, according to the global complementary tax table for year 2013.

• DFL-15 Bonus• Manpower Bonus

Total Benefits, SCL

$ 96.000.000$ 14.851.200 $ 110.851.200

Realization of First Year Incentives

58 INVEST IN ARICA AND PARINACOTA

5.5 PRACTICAL EXAMPLE 4General System Company with Head Office in Santiagoand New Branch in Arica Industrial Free Zone

Records

Tax Area

• Tax Credit Arica Act: $480.000.000 x 30%• DFL-15 (alternative to tax credit): Manpower Bonus DL. 889 (Annual): $182.000 x 17%= $30.490(per worker) x 40 (worker number) x 12 (months)

$ 144.000.000NOT APPLICABLE 3

$ 14.851.200

Access to incentives (Arica Branch only)

• Net sales • Paid MPP (rate 2,5%) • Utility

$ 4.000.000.000$ 100.000.000$ 450.000.000

Head Office

• Investment in new depreciable fixed assets Exchange rate CPL $480.- • Number of workers • Annual net sales • Paid MPP (Accrued: $10.000.000)• Utility

US $ 1.000.000$ 480.000.000

40$ 400.000.000

-0-$ 40.000.000

Arica Branch

• VAT taxpayer • Income Tax first class taxpayer

Rate 19%Rate 20%

Head Office

• Debit sales tax • Income tax first class

ExemptExempt

Arica Branch

3 In the DFL-15 case, total sales exceed the maximum limit set by the competition ($1,141.842.500), there-fore, is off the bases for compete.

59INVEST IN ARICA AND PARINACOTA

• Income tax first class (Saving)• Manpower Bonus: 14.851.200 X 13

Total Benefits, SCL

Incentive vs. Investment Contribution: 70,22%

$ 144.000.000$ 193.065.600 $ 337.065.600

Incentives projection to 2025 (13 years)

• Income Tax determination: • Head office utility $450.000.000 x 20% = $90.000.000 • Arica branch utility $ 40.000.000 x 20% = $ 8.000.000 Total Income Tax $98.000.000• Credit use: Total credit $144.000.000 Credit used in the example: ($ 98.000.000) Following year remnant: $46.000.000• Income tax to pay• Paid MPP•Balanceinfavor(taxreturn)

$ 98.000.000

($ 98.000.000)

$ 0 $ 100.000.000$ 100.000.000

INCENTIVES APPLICATION

TAX CREDIT (Temporal disclaimer to the Income Tax exemption)

In this case, given the particular situation in which the benefits of the incentives in the area can be used in the overall results of the company:

Partner withdrawal in the year (natural person)Increased overall gross income (factor 0,25)Taxable income for Global Complementary TaxTax or factor 0,37 Amount to reduceDetermined taxReduction Income tax credit first classReturn

$ 50.000.000 $ 12.500.000 $ 62.500.000

($ 23.125.000) $ 11.567.266,2 $ 11.557.733,8

$ 12.500.000 $ 942.266

Income Tax Credit first class in the on withdrawals or profit

4 Increased overall gross income by First Class Tax: When appropriated apply the credit provided in Article 56, number 3 of de Income Tax Act, for quantities withdraw or distributed an amount equal to this will be added for the same overall gross income year and will be considered as a amount affected by the income tax 1st category to calculate this credit (final paragraph of Article 54, N° 1). Source: Manual de Consultas Tributarias Nº275.5 It is the taxable income factor found in the section between $57.896.640,1 and $72.370.800, according to the global complementary tax table for year 2013.

Candelabra cactus, grows naturally in the highlands,between 1700-3000 m, in extreme dryness.

Sunset in Fishermen Cove.

INVEST IN ARICA AND PARINACOTA 63

APPENDIX N° 1

ARICA AND INDUSTRIAL ZONES MAP

ZI2, INDUSTRIAL ZONE 2: Zofri ChacallutaGateway of America

ZI3, INDUSTRIAL ZONE 3: Industrial Neighborhood

ZI1, INDUSTRIAL ZONE 1: Industrial Fishing Sector

65INVEST IN ARICA AND PARINACOTA

APPENDIX N° 2

LAW N° 20,655 REPORT ESTABLISHING SPECIAL INCENTIVES FOR DISTANT AREAS ARICA AND PARINACOTA REGION

Raúl Castro LetelierAttorney

The law N° 20.655 establishing Special Incentives for Distant Areas in the country published in the Official Journal on February 1, 2013, amends various Acts related with Arica and Parinacota Region.For the purpose of facilitating the study of this Distant Zone Act, the Modifications to the Special Legislation are set bellow available to the Arica and Parinacota Region.

1.-ACT Nº19.853 THAT CREATES HIRING WORKFORCE BONUSES

The modifications which are introduced to this Act, in conjunction with Arica and Parinacota Region, are:

a) Benefit is established from January 1, 2012 through December 31, 2025;b) It extends the scope of taxable incomes from $147.000.- to $182.000.-, keeping the 17% percent, giving a total bonus of $30.940.- for each hired worker;c) Employers may use this Bonus for permanent or part-time workers; d) Such amount of $182.000.- will be adjusted on January 1st of each year according to changes in the CPI;e) To be eligible for bonus payment, the employers must submit an Affidavit, declaring not been convicted in the past six months for anti-union practices or violation to fundamental rights of the workers.- f) Treasurer, as Inspector Benefit, may require to the Employers delivery of the backgrounds it deems appropriate through any medium.

2.- DECREE LAW N° 3.529 ON ADDITIONAL STANDARDS OF FINANCIAL MANAGEMENT AND BUDGET IMPACT

By this 1980 Decree, a Promotion Fund and Development for Distant Regions was created, in order to subsidize the investments and productive reinvestments of small and medium investors, with the following characteristics:a) Bonuses that are granted under this fund will be 20% of each investment or reinvestment amount, during years 2012 to 2025 inclusive;b) This Fund may assign up to $2,500,000,000 annually, to Extreme Regions. This amount will be adjusted annually in the Budget Law under CPI changes; c) Resources distribution of this Fund shall be made by one or more Ministry of Finance Decrees; d) This Fund is regulated by the Ministry of Finance DFL N° 3 in 2001, which approved the Revised, Coordinated and Systemized Text of DFL N° 15 in 1981 of the same Ministry, which is also amended by the Act N° 20.655 on Extreme Zones in the following ways:

66 INVEST IN ARICA AND PARINACOTA

3.- LAW N° 19.420 THAT STABLISHES INCENTIVES FOR ECONOMIC DEVELOPMENT OF ARICA AND PARINACOTA PROVINCES.

In the Law N° 20.655 on Extreme Zones, the following modifications to the Incentives were introduced.

3.1 INVESTMENT TAX CREDIT:

The Articles 1 to 9 of the Law N° 19.420 (Arica Act I) regulate the Investment Tax Credit, entitled for taxpayers that declare the Tax First Class of Income Tax Act, on effective rents determined by Full Accounting, for the Investments made in Arica and Parinacota Provinces designed for production of assets and provision of services in this Provinces.-

This Credit is deducted from the First Class Tax that must be paid by taxpayers, from the commercial year of the asset acquisition or construction. Unused credit during the year must be deducted from the following year.- In the Law N° 20.655 on Extreme Zones were introduced the following modifications:

A) May Access this benefit those taxpayers whose investment projects exceed monthly 500 UTM. (Note: Before the Amendment were 2,000 UTM to Arica and 1,000 UTM to Parinacota) B) The taxpayers may be eligible for this benefit since January 1st of 2012 until December, 31 of 2025 and the Credit recovery due to them may be made until year 2045.(Note: Before the Amendment was until 2011 and 2034)C) The taxpayer who made investments under the Investment Credit Tax may suspend their MPP according to the following rules and by periods listed below:

1.- BENEFIT When the credit amount for the year, according to Affidavit and Information Duties that includes the number 3 and followings of this section, on the investments referred in this Act, equals or exceeds the average first class tax that has been determined during the last three tax years, the taxpayer is exempted from paying MPP. To calculate the average, the first class tax are deemed to zero, when the taxpayer has determinate a tax loss as result of the respective year. When the estimated credit is less than average first class tax stated in the preceding paragraph, the taxpayer may suspend the MPP up to an amount equal to 25% of total expenditures destined for investment referred to this law, the corresponding estimates for

d.1. Establishing new standards of evaluation in the Projects quality; d.2. Bonus applications will be received every year between November, 15 and December, 31, both dates inclusive; d.3. Bonus will be paid from the Budget of the following calendar year; d.4. Resolving Committee Constitution of Development Fund for Distant Areas is amended.

67INVEST IN ARICA AND PARINACOTA

commercial year.

In the previous cases, the estimated credit shall be the remaining credits under this law that can be charged to the following tax years. Besides, the deemed credit for the respective year, determined based on the appropriated credit rate according to the previous Article, applied to projected disbursements for the year, intended to the investments under this law, whether such credit is earned or not at the end of it.

To calculate the average indicated, the first class tax will be converted to UTM according to the prevailing value at the end of the commercial year that corresponds to the tax. The UTM number thus obtained, will be reconverted to SCL value that those have at the date of the affidavit submission referred in item 3 of this Article. artículo.