invest malaysia 2018 - maybank.com€¦ · market services for corporate ... • awarded best sme...

TRANSCRIPT

0www.maybank.com

Invest Malaysia 2018

Shangri-La Hotel, Kuala Lumpur

23-24 January 2018

Humanising Financial Services

1

Table of Contents

Maybank Overview: Strategy and Performance 2

Appendix:

1. Financial Performance 19

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

2

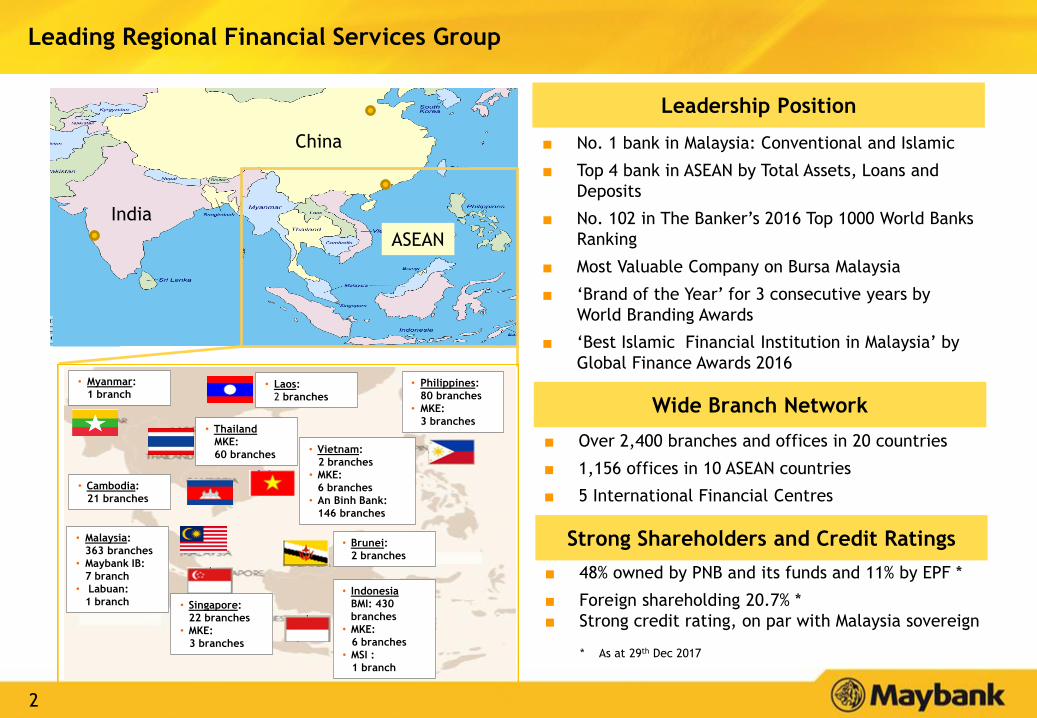

Leading Regional Financial Services Group

■ No. 1 bank in Malaysia: Conventional and Islamic

■ Top 4 bank in ASEAN by Total Assets, Loans and

Deposits

■ No. 102 in The Banker’s 2016 Top 1000 World Banks

Ranking

■ Most Valuable Company on Bursa Malaysia

■ ‘Brand of the Year’ for 3 consecutive years by

World Branding Awards

■ ‘Best Islamic Financial Institution in Malaysia’ by

Global Finance Awards 2016

■ Over 2,400 branches and offices in 20 countries

■ 1,156 offices in 10 ASEAN countries

■ 5 International Financial Centres

■ 48% owned by PNB and its funds and 11% by EPF *

■ Foreign shareholding 20.7% *

■ Strong credit rating, on par with Malaysia sovereign

Wide Branch Network

Leadership Position

Strong Shareholders and Credit Ratings

* As at 29th Dec 2017

China

India

ASEAN

• Myanmar:

1 branch• Laos:

2 branches

• Thailand

MKE:

60 branches

• Philippines:

80 branches

• MKE:

3 branches

• Cambodia:

21 branches

• Vietnam:

2 branches

• MKE:

6 branches

• An Binh Bank:

146 branches

• Malaysia:

363 branches

• Maybank IB:

7 branch

• Labuan:

1 branch • Singapore:

22 branches

• MKE:

3 branches

• Indonesia

BMI: 430

branches

• MKE:

6 branches

• MSI :

1 branch

• Brunei:

2 branches

3

Maybank Group’s Key Business Pillars

Group Community

Financial Services

Busi

ness

Pilla

rs

• Group CFS serves the Consumer,

Retail SME and Business Banking

(mid-sized corporates and SMEs)

segments of the Group.

• Together with the Private

Wealth desks, Group CFS

operates in 11 countries.

• 3 Centre of Excellences (CoEs)

established to drive key regional

businesses across our ASEAN

markets – Group Wealth

Management, Regional Retail

SME and Regional Cards.

• Group Insurance and Takaful

complements Maybank’s growth

internationally while leveraging

on Etiqa’s expertise in takaful

and bancassurance.

• Features a strong agency force

comprising over 10,000 agents,

28 branches, as well as a wide

bancassurance network through

Maybank branches, third-party

banks, co-operatives and

brokers.

• No. 1 digital insurance player in

Malaysia.

• Group Global Banking covers

Investment Banking (through

Maybank Kim Eng), Global

Markets, Corporate Banking,

Transaction Banking and Asset

Management.

• Covers investment and capital

market services for corporate

and institutional clients across

19 markets.

• Maybank Kim Eng (MKE) has

been in ASEAN for over 40 years

and is ASEAN’s largest brokerage

franchise which operates in 10

countries.

Desc

ripti

on

% o

f

9M

17

PBT

49.4% 6.9%43.7%

Group Insurance and

TakafulGroup Global Banking

Islamic Finance leverage model utilised to distribute Islamic products across the group, while

international business operations are embedded within each business pillar.

4

LARGE POPULATION

WITH YOUNG DEMOGRAPHICS

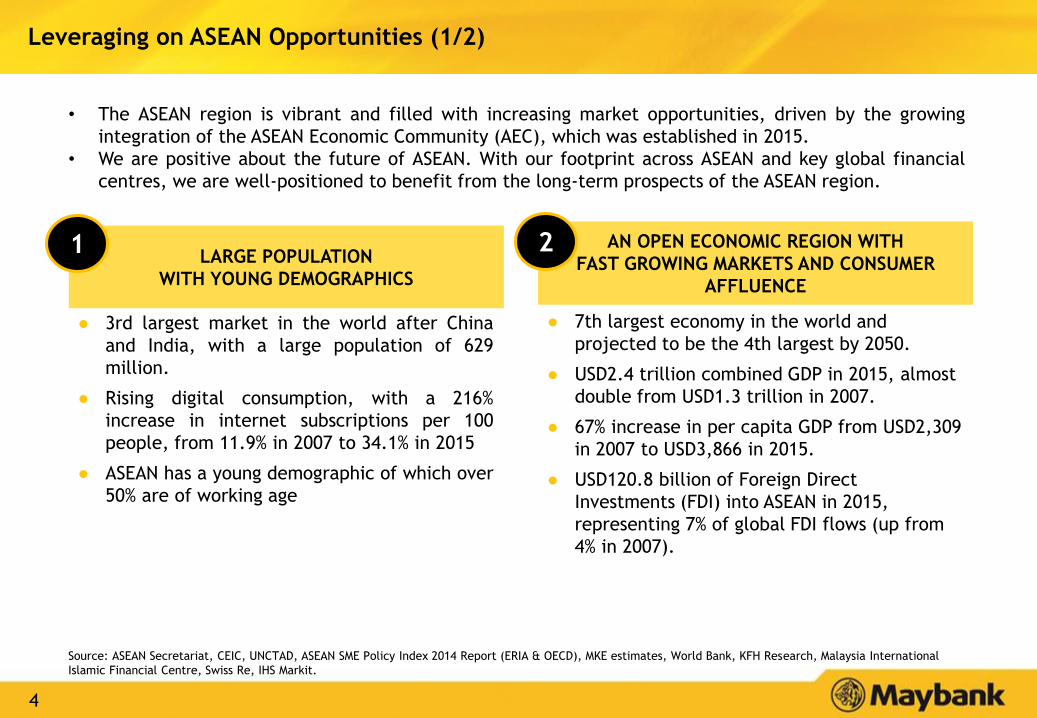

• The ASEAN region is vibrant and filled with increasing market opportunities, driven by the growing

integration of the ASEAN Economic Community (AEC), which was established in 2015.

• We are positive about the future of ASEAN. With our footprint across ASEAN and key global financial

centres, we are well-positioned to benefit from the long-term prospects of the ASEAN region.

● 7th largest economy in the world and

projected to be the 4th largest by 2050.

● USD2.4 trillion combined GDP in 2015, almost

double from USD1.3 trillion in 2007.

● 67% increase in per capita GDP from USD2,309

in 2007 to USD3,866 in 2015.

● USD120.8 billion of Foreign Direct

Investments (FDI) into ASEAN in 2015,

representing 7% of global FDI flows (up from

4% in 2007).

● 3rd largest market in the world after China

and India, with a large population of 629

million.

● Rising digital consumption, with a 216%

increase in internet subscriptions per 100

people, from 11.9% in 2007 to 34.1% in 2015

● ASEAN has a young demographic of which over

50% are of working age

AN OPEN ECONOMIC REGION WITH

FAST GROWING MARKETS AND CONSUMER

AFFLUENCE

Leveraging on ASEAN Opportunities (1/2)

Source: ASEAN Secretariat, CEIC, UNCTAD, ASEAN SME Policy Index 2014 Report (ERIA & OECD), MKE estimates, World Bank, KFH Research, Malaysia International

Islamic Financial Centre, Swiss Re, IHS Markit.

1 2

5

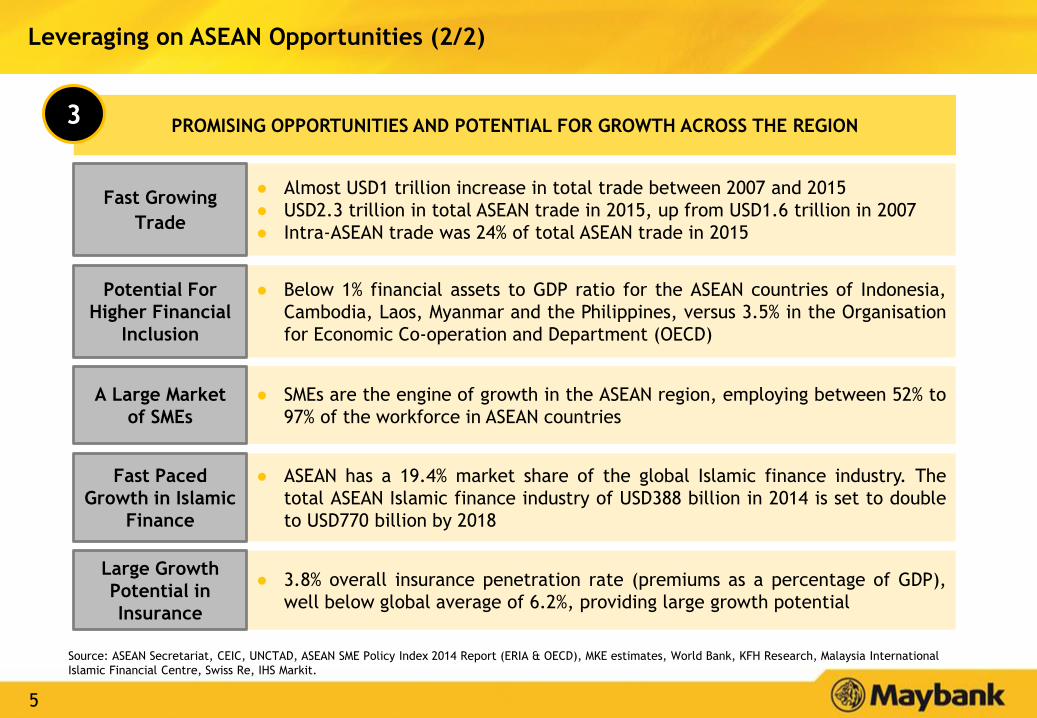

Leveraging on ASEAN Opportunities (2/2)

PROMISING OPPORTUNITIES AND POTENTIAL FOR GROWTH ACROSS THE REGION3

● Almost USD1 trillion increase in total trade between 2007 and 2015

● USD2.3 trillion in total ASEAN trade in 2015, up from USD1.6 trillion in 2007

● Intra-ASEAN trade was 24% of total ASEAN trade in 2015

Fast Growing

Trade

● Below 1% financial assets to GDP ratio for the ASEAN countries of Indonesia,

Cambodia, Laos, Myanmar and the Philippines, versus 3.5% in the Organisation

for Economic Co-operation and Department (OECD)

Potential For

Higher Financial

Inclusion

● SMEs are the engine of growth in the ASEAN region, employing between 52% to

97% of the workforce in ASEAN countries

A Large Market

of SMEs

● ASEAN has a 19.4% market share of the global Islamic finance industry. The

total ASEAN Islamic finance industry of USD388 billion in 2014 is set to double

to USD770 billion by 2018

Fast Paced

Growth in Islamic

Finance

● 3.8% overall insurance penetration rate (premiums as a percentage of GDP),

well below global average of 6.2%, providing large growth potential

Large Growth

Potential in

Insurance

Source: ASEAN Secretariat, CEIC, UNCTAD, ASEAN SME Policy Index 2014 Report (ERIA & OECD), MKE estimates, World Bank, KFH Research, Malaysia International

Islamic Financial Centre, Swiss Re, IHS Markit.

6

Maybank2020: Strategic Objectives (1/2)

The Top ASEAN Community Bank

The Leading ASEAN Wholesale Bank Linking Asia

The Leading ASEAN Insurer

The Global Leader In Islamic Finance

Digital Bank Of Choice

By leveraging on our regional presence, banking expertise and ASEAN growth opportunities

By leveraging on our ASEAN leadership capabilities to deliver client solutions across Asia

By enhancing synergies between Maybank’s regional banking footprint and Etiqa’s expertise

in takaful & bancassurance

By continuing to deliver innovative client-centric universal financial solutions, building on

our global leadership position

By putting our customers’ preferences first and transforming to deliver next-generation

customer experience on mobile and digital platforms

1

2

3

4

5

7

• Awarded Best Private Bank in Malaysia by Asian Private Banker for three consecutive years• Awarded Best SME Bank of the Year in Malaysia in 2017 by Alpha Southeast Asia• M2U ranked No.1 in the “Top 20 Local Brand Web Domains visited from Desktop Computers

in Malaysia” with over 3.6 million monthly unique visitors

Maybank2020: Strategic Objectives: Key FY2017 Achievements (2/2)

The Leading

ASEAN Wholesale

Bank Linking

Asia

2 • Maintained our lead as the ASEAN investment banking franchise by ranking • 1st in Bloomberg’s ASEAN Equity, Equity Linked & Rights and M&A tables• 2nd in ASEAN Local Currency Bonds and Global Sukuk tables

• Malaysian market share leader in corporate lending, trade finance and corporate deposits• MKE was awarded Best Investment Bank in Malaysia by Euromoney (3rd consecutive year)

The Leading

ASEAN Insurer

3 • Maintained No.1 online insurance position with >70% market share• Operational improvements such as most motor claims approval TAT under 30 minutes vs

industry benchmark of 3 days• Regional business expansion with bancassurance business growth into the Philippines and

75% acquisition stake in Indonesia’s PT Asuransi Asoka Mas

The Global

Leader In Islamic

Finance

4 • No.1 Global Sukuk Lead Manager on Bloomberg’s Global Sukuk League Table• No.1 Lead Manager on Bloomberg’s Ringgit Malaysia Sukuk League Table• Championed the Green Sukuk and Sustainable and Responsible Investment Sukuk market

development in Malaysia• Launched HouzKEY, a rent-to-own initiative in Malaysia

Digital Bank of

Choice

5 • Launched new Maybank2u app in Malaysia with improved user-friendliness, biometric features (Face & Voice ID) as security authentication and Secure2u function

• Launched various first–to-market digital initiatives: Maybank QRPay, Alipay-enabled merchant terminals in Malaysia and Maybank2u Pay (online merchant registration and payment via APIs)

The Top ASEAN

Community Bank

1

8

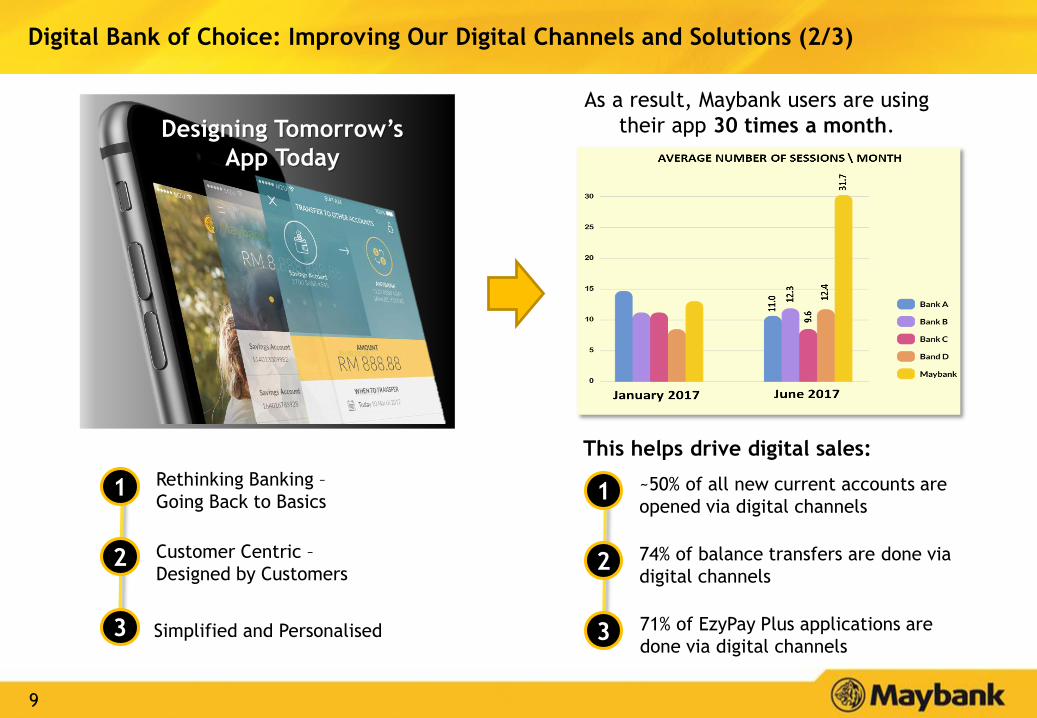

Digital Bank of Choice: Moving the Nation to a Cashless Society (1/3)

Maybank becomes the one-stop bank for all payment needs – both for the virtual

as well as the physical business world

9

Designing Tomorrow’s

App Today

Rethinking Banking –

Going Back to Basics

Customer Centric –

Designed by Customers

Simplified and Personalised

As a result, Maybank users are using

their app 30 times a month.

1

2

3

~50% of all new current accounts are

opened via digital channels

74% of balance transfers are done via

digital channels

71% of EzyPay Plus applications are

done via digital channels

1

2

3

This helps drive digital sales:

Digital Bank of Choice: Improving Our Digital Channels and Solutions (2/3)

10

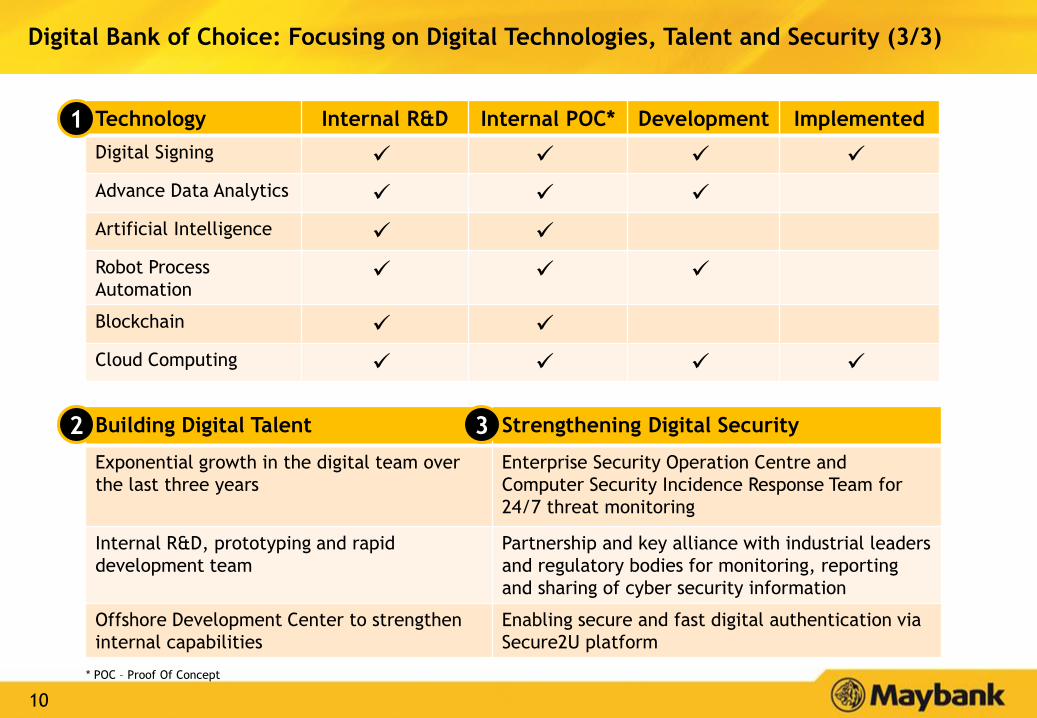

Digital Bank of Choice: Focusing on Digital Technologies, Talent and Security (3/3)

Building Digital Talent Strengthening Digital Security

Exponential growth in the digital team over

the last three years

Enterprise Security Operation Centre and

Computer Security Incidence Response Team for

24/7 threat monitoring

Internal R&D, prototyping and rapid

development team

Partnership and key alliance with industrial leaders

and regulatory bodies for monitoring, reporting

and sharing of cyber security information

Offshore Development Center to strengthen

internal capabilities

Enabling secure and fast digital authentication via

Secure2U platform

Technology Internal R&D Internal POC* Development Implemented

Digital Signing

Advance Data Analytics

Artificial Intelligence

Robot Process

Automation

Blockchain

Cloud Computing

1

2 3

* POC – Proof Of Concept

11

2.48 2.43

2.31 2.31 2.27

2.39

FY12 FY13 FY14 FY15 FY16 9M FY17

48.6 47.8

48.9 48.2

47.3

49.1

FY12 FY13 FY14 FY15 FY16 9M FY17

10.22 11.02 11.38 12.53

13.63 13.50

15.85 15.43 15.87 17.49

18.94 18.03

FY12 FY13 FY14 FY15 FY16 9M FY17

CET 1 TCR

16.0 15.1 13.8

12.2 10.6 10.3

FY12 FY13 FY14 FY15 FY16 9M FY17

Maybank’s Longer-Term Trends for Key Operating Ratios

Return on Equity (%) Net Interest Margin (%)

Total Capital Ratio &

CET 1 Ratio (%)

Cost to Income Ratio (%)

2017

guidance:

<50%

2017

guidance:

10% - 11%

2017

guidance:

5 bps to 10 bps

compression

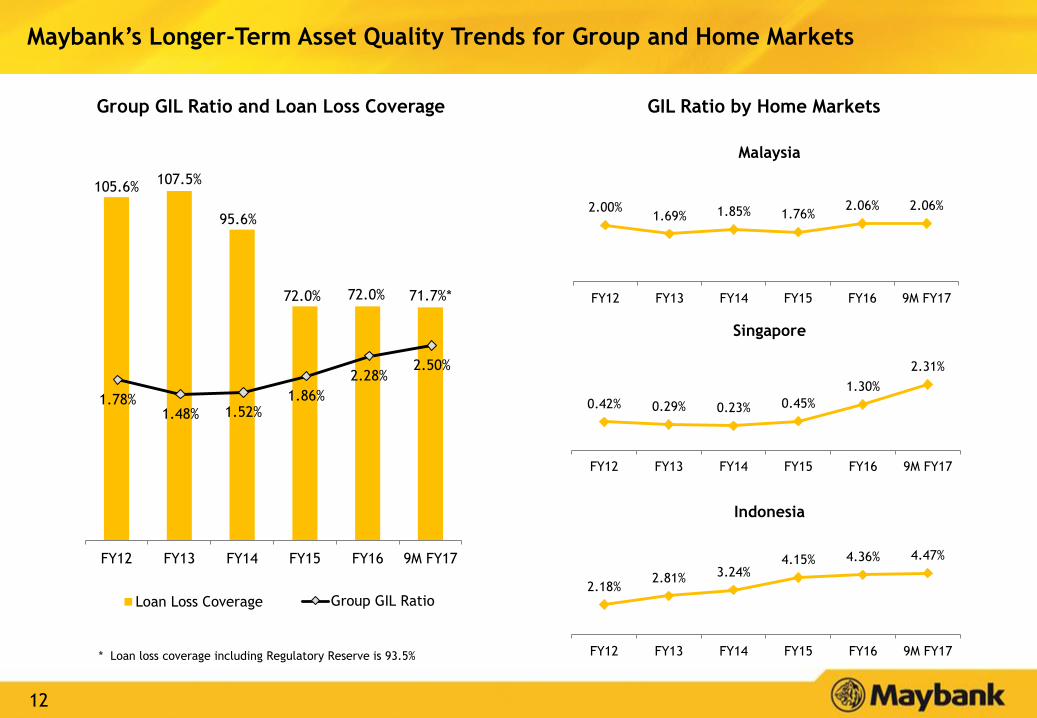

12

105.6%107.5%

95.6%

72.0% 72.0% 71.7%*

FY12 FY13 FY14 FY15 FY16 9M FY17

Loan Loss Coverage

Maybank’s Longer-Term Asset Quality Trends for Group and Home Markets

1.78%1.48% 1.52%

1.86%

2.28%2.50%

Group GIL Ratio

Group GIL Ratio and Loan Loss Coverage

* Loan loss coverage including Regulatory Reserve is 93.5%

GIL Ratio by Home Markets

2.00%1.69% 1.85% 1.76%

2.06% 2.06%

FY12 FY13 FY14 FY15 FY16 9M FY17

Malaysia

0.42% 0.29% 0.23% 0.45%

1.30%

2.31%

FY12 FY13 FY14 FY15 FY16 9M FY17

Singapore

2.18%2.81% 3.24%

4.15% 4.36% 4.47%

FY12 FY13 FY14 FY15 FY16 9M FY17

Indonesia

13

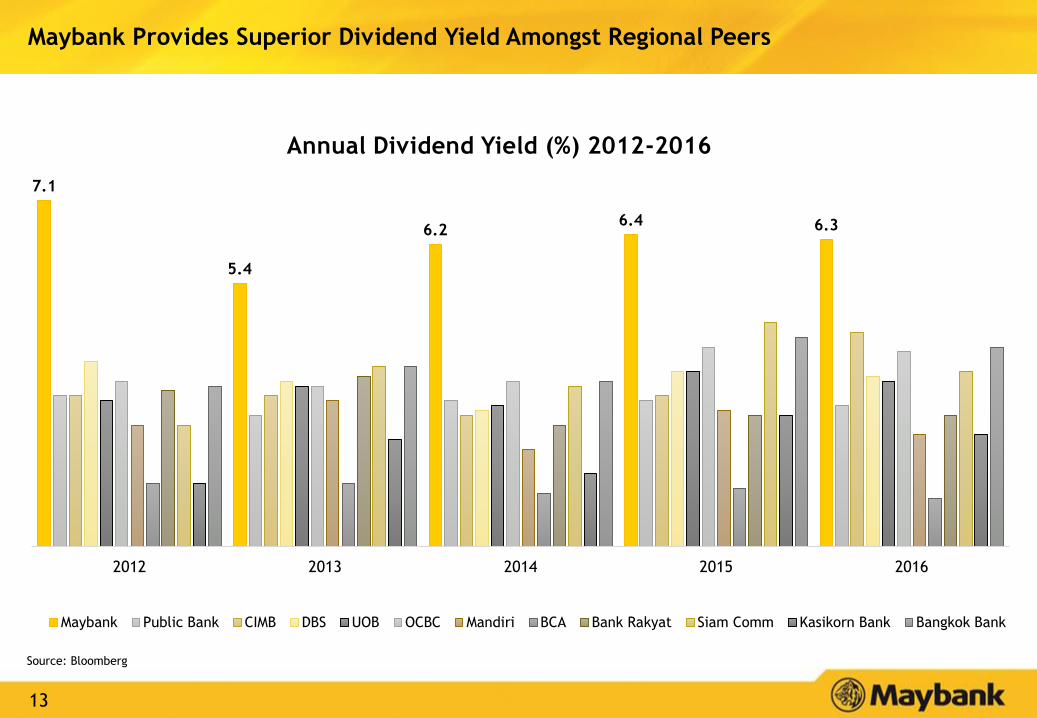

Maybank Provides Superior Dividend Yield Amongst Regional Peers

Source: Bloomberg

7.1

5.4

6.26.4 6.3

2012 2013 2014 2015 2016

Annual Dividend Yield (%) 2012-2016

Maybank Public Bank CIMB DBS UOB OCBC Mandiri BCA Bank Rakyat Siam Comm Kasikorn Bank Bangkok Bank

14

76.5% 74.9%79.9%

74.7% 71.9%78.5% 76.3% 78.1%

72.2%

11

2832

22.5 2424

20 23

44

32

36

33

3133 30

32

FY10 FY11 FP11 FY12 FY13 FY14 FY15 FY16 FY17

Final

Interim

54.0

82.6%*

52.0

* Reinvestment rate for the Dividend Reinvestment Plan

# The Net Dividend is 28.5 sen of which 15 sen is single-tier dividend.

85.9%*

85.7%*

88.2%*85.9%*

88.5%*91.1%*

86.1%*

88.6%*

85.74%*

55.060.0

36.0

65.0

53.557.0

84.0%*

Dividend Payout Ratio

Dividend (sen) and Payout Ratio (%)

87.5%*

83.7%*

83.5%*

89.06%*

#

Maybank Continues with High Dividend Payout; Above Policy Rate of 40%-60%

15

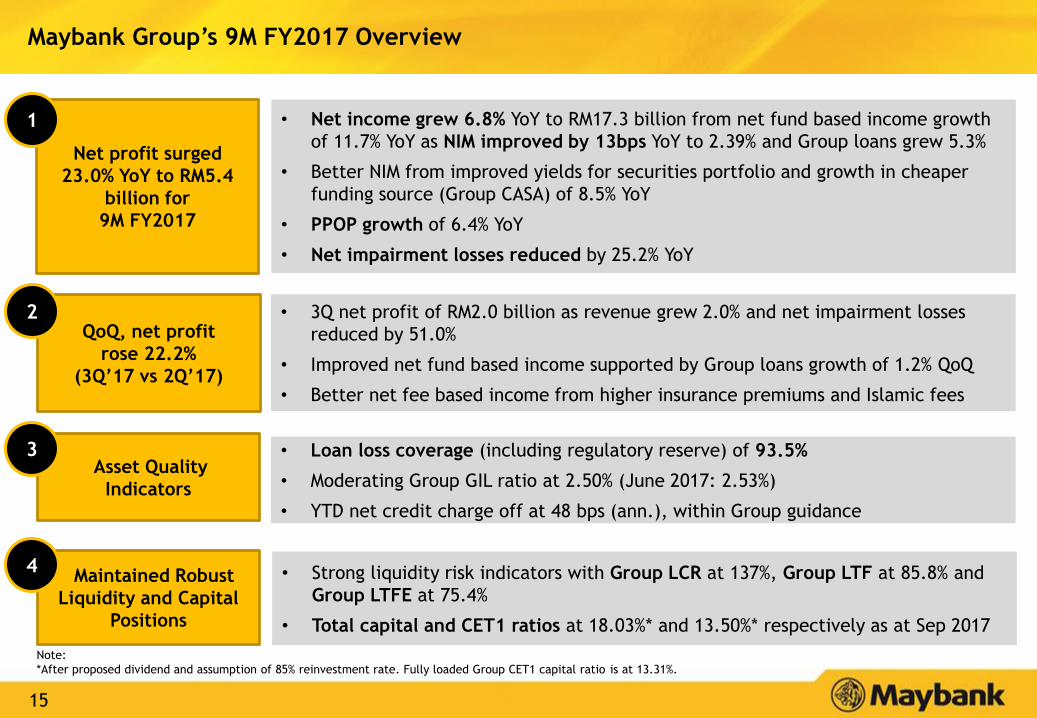

Net profit surged

23.0% YoY to RM5.4

billion for

9M FY2017

Maybank Group’s 9M FY2017 Overview

• Net income grew 6.8% YoY to RM17.3 billion from net fund based income growth

of 11.7% YoY as NIM improved by 13bps YoY to 2.39% and Group loans grew 5.3%

• Better NIM from improved yields for securities portfolio and growth in cheaper

funding source (Group CASA) of 8.5% YoY

• PPOP growth of 6.4% YoY

• Net impairment losses reduced by 25.2% YoY

1

• Loan loss coverage (including regulatory reserve) of 93.5%

• Moderating Group GIL ratio at 2.50% (June 2017: 2.53%)

• YTD net credit charge off at 48 bps (ann.), within Group guidance

Asset Quality

Indicators

• Strong liquidity risk indicators with Group LCR at 137%, Group LTF at 85.8% and

Group LTFE at 75.4%

• Total capital and CET1 ratios at 18.03%* and 13.50%* respectively as at Sep 2017

Maintained Robust

Liquidity and Capital

Positions

4

QoQ, net profit

rose 22.2%

(3Q’17 vs 2Q’17)

2 • 3Q net profit of RM2.0 billion as revenue grew 2.0% and net impairment losses

reduced by 51.0%

• Improved net fund based income supported by Group loans growth of 1.2% QoQ

• Better net fee based income from higher insurance premiums and Islamic fees

3

Note:

*After proposed dividend and assumption of 85% reinvestment rate. Fully loaded Group CET1 capital ratio is at 13.31%.

16

Full year Group loan growth of ~3%; loan growth for

Maybank Malaysia to be in line with industry growth

Managed cost growth to maintain CIR of < 50%

Maybank Performance Outlook for 2H 2017

5

Top line growth supported by effective NIM management1

3

Continued management of asset quality ahead of MFRS 9 adoption in 20186

Deposit growth to match loan growth; rising cost of funds trend 4

Maintaining full year ROE guidance of 10%-11%2

17

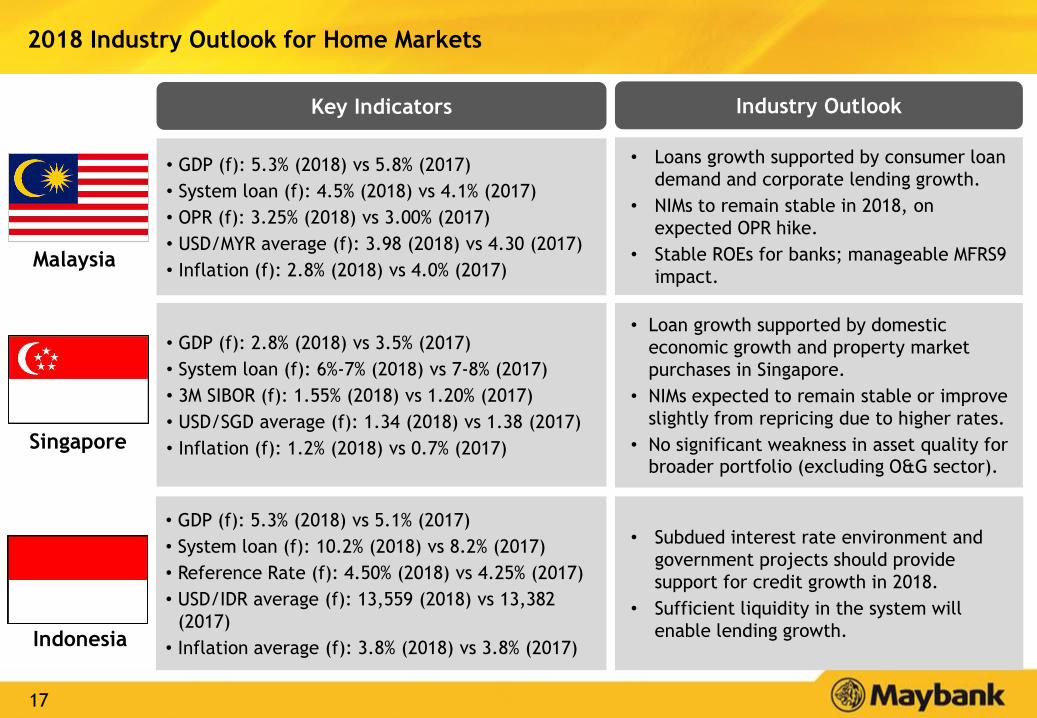

2018 Industry Outlook for Home Markets

Key Indicators Industry Outlook

Singapore

Malaysia

Indonesia

• GDP (f): 5.3% (2018) vs 5.8% (2017)

• System loan (f): 4.5% (2018) vs 4.1% (2017)

• OPR (f): 3.25% (2018) vs 3.00% (2017)

• USD/MYR average (f): 3.98 (2018) vs 4.30 (2017)

• Inflation (f): 2.8% (2018) vs 4.0% (2017)

• GDP (f): 2.8% (2018) vs 3.5% (2017)

• System loan (f): 6%-7% (2018) vs 7-8% (2017)

• 3M SIBOR (f): 1.55% (2018) vs 1.20% (2017)

• USD/SGD average (f): 1.34 (2018) vs 1.38 (2017)

• Inflation (f): 1.2% (2018) vs 0.7% (2017)

• GDP (f): 5.3% (2018) vs 5.1% (2017)

• System loan (f): 10.2% (2018) vs 8.2% (2017)

• Reference Rate (f): 4.50% (2018) vs 4.25% (2017)

• USD/IDR average (f): 13,559 (2018) vs 13,382

(2017)

• Inflation average (f): 3.8% (2018) vs 3.8% (2017)

• Subdued interest rate environment and

government projects should provide

support for credit growth in 2018.

• Sufficient liquidity in the system will

enable lending growth.

• Loan growth supported by domestic

economic growth and property market

purchases in Singapore.

• NIMs expected to remain stable or improve

slightly from repricing due to higher rates.

• No significant weakness in asset quality for broader portfolio (excluding O&G sector).

• Loans growth supported by consumer loan

demand and corporate lending growth.

• NIMs to remain stable in 2018, on

expected OPR hike.

• Stable ROEs for banks; manageable MFRS9

impact.

18

Table of Contents

Appendix:

1. Financial Performance 19

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

19

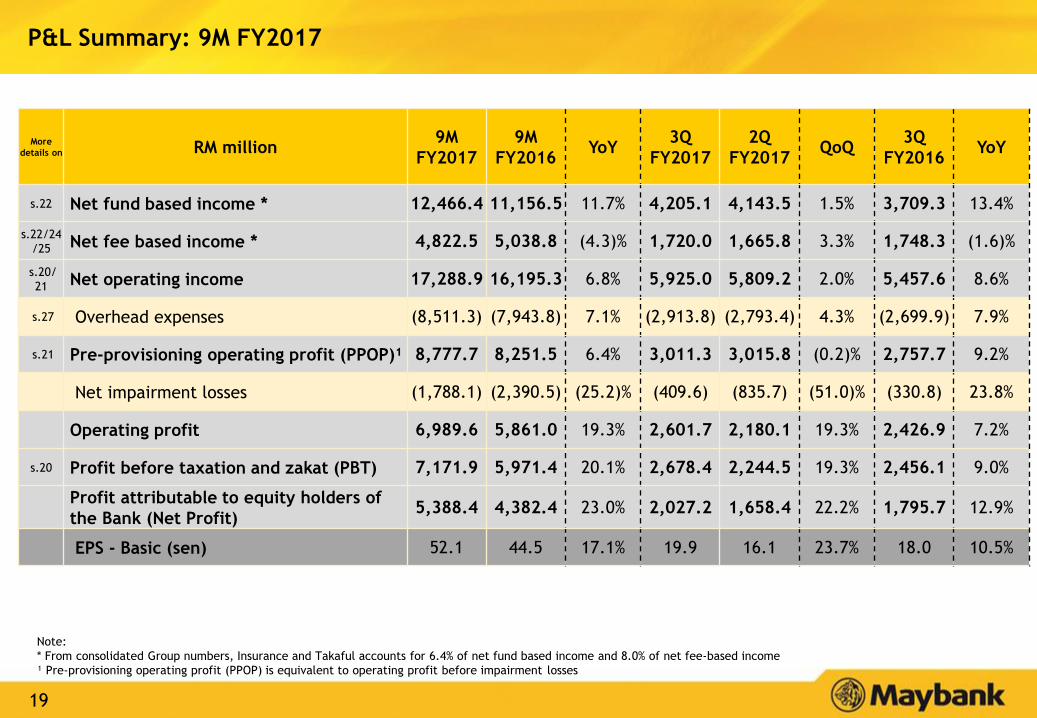

P&L Summary: 9M FY2017

More

details on RM million9M

FY2017

9M

FY2016YoY

3Q

FY2017

2Q

FY2017QoQ

3Q

FY2016YoY

s.22 Net fund based income * 12,466.4 11,156.5 11.7% 4,205.1 4,143.5 1.5% 3,709.3 13.4%

s.22/24

/25 Net fee based income * 4,822.5 5,038.8 (4.3)% 1,720.0 1,665.8 3.3% 1,748.3 (1.6)%

s.20/

21 Net operating income 17,288.9 16,195.3 6.8% 5,925.0 5,809.2 2.0% 5,457.6 8.6%

s.27 Overhead expenses (8,511.3) (7,943.8) 7.1% (2,913.8) (2,793.4) 4.3% (2,699.9) 7.9%

s.21 Pre-provisioning operating profit (PPOP)¹ 8,777.7 8,251.5 6.4% 3,011.3 3,015.8 (0.2)% 2,757.7 9.2%

Net impairment losses (1,788.1) (2,390.5) (25.2)% (409.6) (835.7) (51.0)% (330.8) 23.8%

Operating profit 6,989.6 5,861.0 19.3% 2,601.7 2,180.1 19.3% 2,426.9 7.2%

s.20 Profit before taxation and zakat (PBT) 7,171.9 5,971.4 20.1% 2,678.4 2,244.5 19.3% 2,456.1 9.0%

Profit attributable to equity holders of

the Bank (Net Profit)5,388.4 4,382.4 23.0% 2,027.2 1,658.4 22.2% 1,795.7 12.9%

EPS - Basic (sen) 52.1 44.5 17.1% 19.9 16.1 23.7% 18.0 10.5%

Note:

* From consolidated Group numbers, Insurance and Takaful accounts for 6.4% of net fund based income and 8.0% of net fee-based income

¹ Pre-provisioning operating profit (PPOP) is equivalent to operating profit before impairment losses

20

70.6%

9.6%

8.8%

11.0%

Malaysia Singapore Indonesia Others

58.7%18.5%

14.8%

8.0%

58.1%25.8%

8.1%8.0%

77.3%

10.2%

8.4%4.1%

61.4%16.2%

14.7%

7.7%

57.5%25.3%

8.3%

8.9%

International & Malaysia Portfolio Mix 9M FY2017

Overseas:

42.5%

9M FY2016

Net Operating Income Profit Before Tax

9M FY2017

Overseas:

38.6%

Overseas:

22.7%

Gross loans*

(Jan 16 – Sep 16)

Overseas:

41.9%

Overseas:

41.3%

Overseas:

29.4%

(Jan 17 – Sep 17)

RM5.97b RM461.2bRM16.20b

RM7.17b RM485.9bRM17.29b

Note:

* Including Islamic loans sold to Cagamas and excludes unwinding of interest

21

16,195

9,272

5,724

1,065 117 1,146

17,289

10,067

5,798

993 177

1,178

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

9M FY2016

9M FY2017

8,252

4,161 4,340

209 25 647

8,778

4,619 4,280

102 73 628

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

9M FY2016

9M FY2017

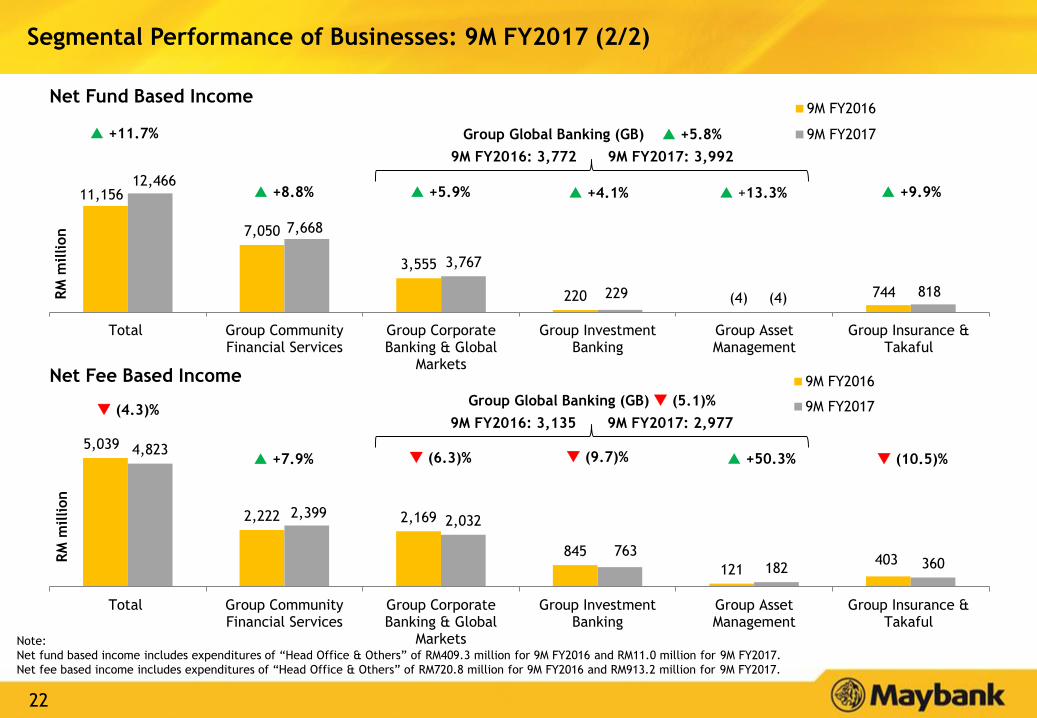

Segmental Performance of Businesses: 9M FY2017 (1/2)

Net Operating Income

RM

million

+6.8%

RM

million

PPOP

+8.6% +1.3% (6.8)% +2.8%

+6.4%

+11.0% (1.4)% (51.5)% +>100%

+51.5%

(2.9)%

Group Global Banking (GB) (2.6)%

Group Global Banking (GB) +0.9%

9M FY2016: 6,907 9M FY2017: 6,969

9M FY2016: 4,574 9M FY2017: 4,454

Note:

Net income & PPOP for group includes expenditures of “Head Office & Others” of RM1,130.0 million for 9M FY2016 and RM924.2 million for 9M FY2017.

22

11,156

7,050

3,555

220 (4) 744

12,466

7,668

3,767

229 (4) 818

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

9M FY2016

9M FY2017 +11.7%

Net Fund Based Income

5,039

2,222 2,169

845

121 403

4,823

2,399 2,032

763 182 360

Total Group CommunityFinancial Services

Group CorporateBanking & Global

Markets

Group InvestmentBanking

Group AssetManagement

Group Insurance &Takaful

9M FY2016

9M FY2017 (4.3)%

(9.7)% (10.5)%

Group Global Banking (GB) +5.8%

Net Fee Based Income

RM

million

RM

million

+4.1% +13.3%

+50.3%

+8.8% +5.9% +9.9%

9M FY2016: 3,772 9M FY2017: 3,992

Group Global Banking (GB) (5.1)%

9M FY2016: 3,135 9M FY2017: 2,977

Segmental Performance of Businesses: 9M FY2017 (2/2)

Note:

Net fund based income includes expenditures of “Head Office & Others” of RM409.3 million for 9M FY2016 and RM11.0 million for 9M FY2017.

Net fee based income includes expenditures of “Head Office & Others” of RM720.8 million for 9M FY2016 and RM913.2 million for 9M FY2017.

(6.3)% +7.9%

23

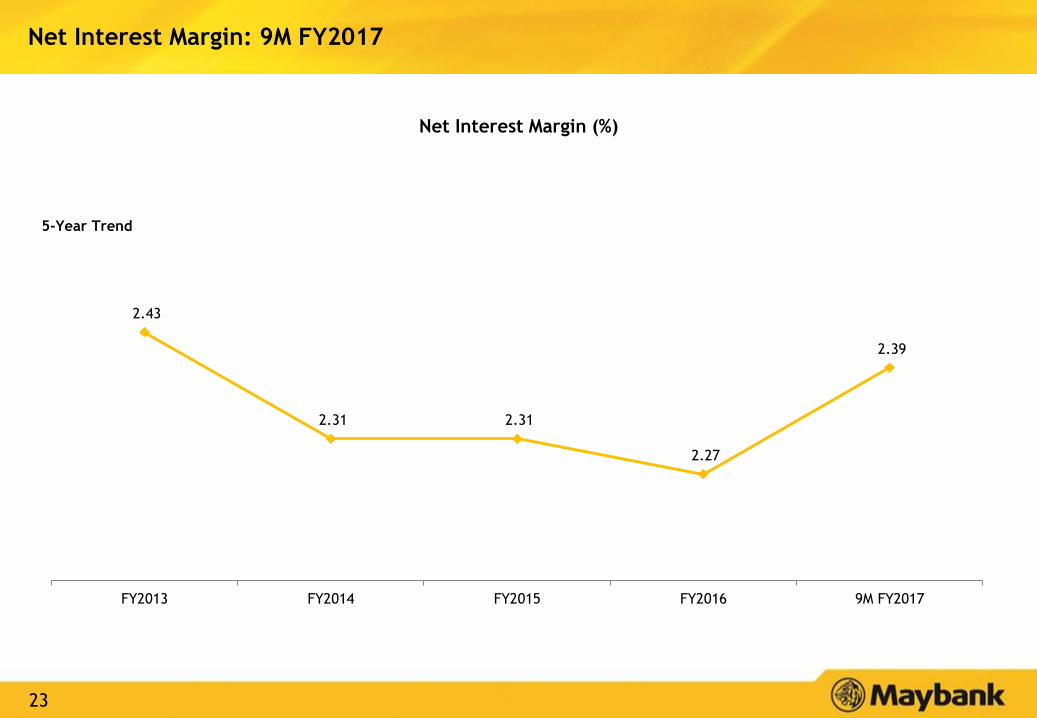

2.43

2.31 2.31

2.27

2.39

FY2013 FY2014 FY2015 FY2016 9M FY2017

Net Interest Margin: 9M FY2017

Net Interest Margin (%)

5-Year Trend

24

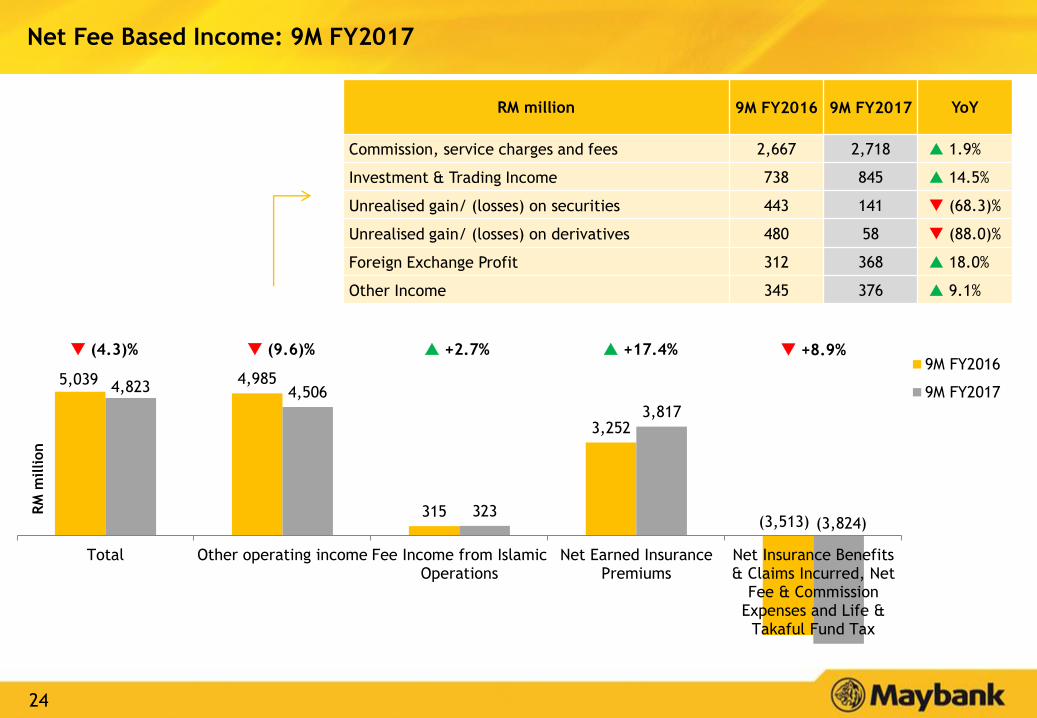

5,039 4,985

315

3,252

(3,513)

4,823 4,506

323

3,817

(3,824)

Total Other operating income Fee Income from IslamicOperations

Net Earned InsurancePremiums

Net Insurance Benefits& Claims Incurred, Net

Fee & CommissionExpenses and Life &

Takaful Fund Tax

9M FY2016

9M FY2017

RM

million

RM million 9M FY2016 9M FY2017 YoY

Commission, service charges and fees 2,667 2,718 1.9%

Investment & Trading Income 738 845 14.5%

Unrealised gain/ (losses) on securities 443 141 (68.3)%

Unrealised gain/ (losses) on derivatives 480 58 (88.0)%

Foreign Exchange Profit 312 368 18.0%

Other Income 345 376 9.1%

Net Fee Based Income: 9M FY2017

(4.3)% (9.6)% +2.7% +17.4% +8.9%

25

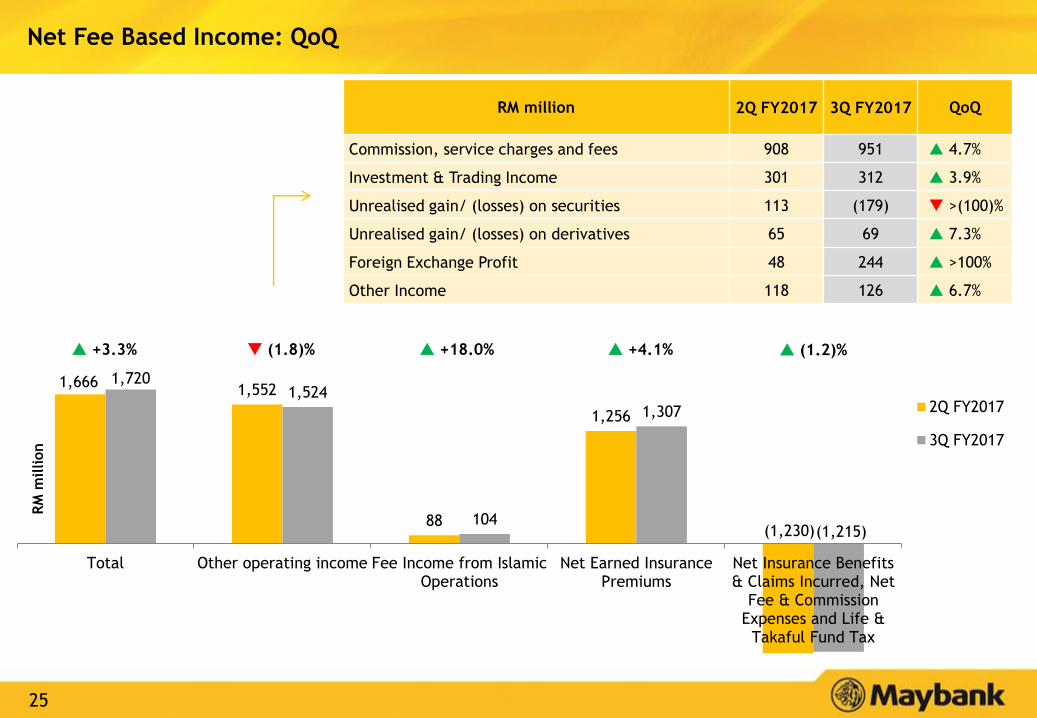

1,666 1,552

88

1,256

(1,230)

1,720 1,524

104

1,307

(1,215)

Total Other operating income Fee Income from IslamicOperations

Net Earned InsurancePremiums

Net Insurance Benefits& Claims Incurred, Net

Fee & CommissionExpenses and Life &

Takaful Fund Tax

2Q FY2017

3Q FY2017

RM

million

RM million 2Q FY2017 3Q FY2017 QoQ

Commission, service charges and fees 908 951 4.7%

Investment & Trading Income 301 312 3.9%

Unrealised gain/ (losses) on securities 113 (179) >(100)%

Unrealised gain/ (losses) on derivatives 65 69 7.3%

Foreign Exchange Profit 48 244 >100%

Other Income 118 126 6.7%

Net Fee Based Income: QoQ

+3.3% (1.8)% +18.0% +4.1% (1.2)%

26

Unaudited Income Statement for Insurance and Takaful Business

RM million9M

FY2017

9M

FY2016YoY

3Q

FY2017

2Q

FY2017QoQ

3Q

FY2016YoY

Net interest income 810.8 733.2 10.6% 260.6 299.1 (12.8)% 248.5 4.9%

Net earned premiums 3,817.1 3,251.6 17.4% 1,307.4 1,255.8 4.1% 1,018.4 28.4%

Other operating income 516.4 688.8 (25.0)% 84.4 172.3 (51.0)% 298.1 (71.7)%

Total operating income 5,144.4 4,673.5 10.1% 1,652.5 1,727.2 (4.3)% 1,565.0 5.6%

Net insurance benefits & claims

incurred, net fee & commission

expenses and life & takaful fund tax

(3,978.5) (3,648.0) 9.1% (1,289.2) (1,265.3) 1.9% (1,173.6) 9.9%

Net operating income 1,165.9 1,025.6 13.7% 363.2 461.9 (21.4)% 391.4 (7.2)%

Overhead expenses (542.5) (490.6) 10.6% (189.3) (186.8) 1.4% (162.2) 16.8%

PPOP 623.4 535.0 16.5% 173.9 275.1 (36.8)% 229.3 (24.2)%

Net impairment losses (35.5) (33.6) 5.7% (23.9) (9.8) >100% (0.2) >100%

Operating profit 587.9 501.4 17.3% 150.0 265.3 (43.5)% 229.0 (34.5)%

RM million9M

FY2017

9M

FY2016YoY

3Q

FY2017

2Q

FY2017QoQ

3Q

FY2016YoY

Net insurance benefits & claims

incurred, net fee & commission

expenses and life & takaful fund tax

(3,978.5) (3,648.0) 9.1% (1,289.2) (1,265.3) 1.9% (1,173.6) 9.9%

Less: intercompany elimination 154.6 135.4 14.2% 73.9 35.1 >100% 60.4 22.3%

Total net insurance benefits & claims

incurred, net fee & commission

expenses and life & takaful fund tax

(3,823.9) (3,512.6) 8.9% (1,215.3) (1,230.2) (1.2)% (1,113.1) 9.2%

Reconciliation of net insurance benefits & claims incurred, net fee & commission expenses and life & takaful fund tax

27

RM million9M

FY2017

9M

FY2016YoY

3Q

FY2017

2Q

FY2017QoQ

3Q

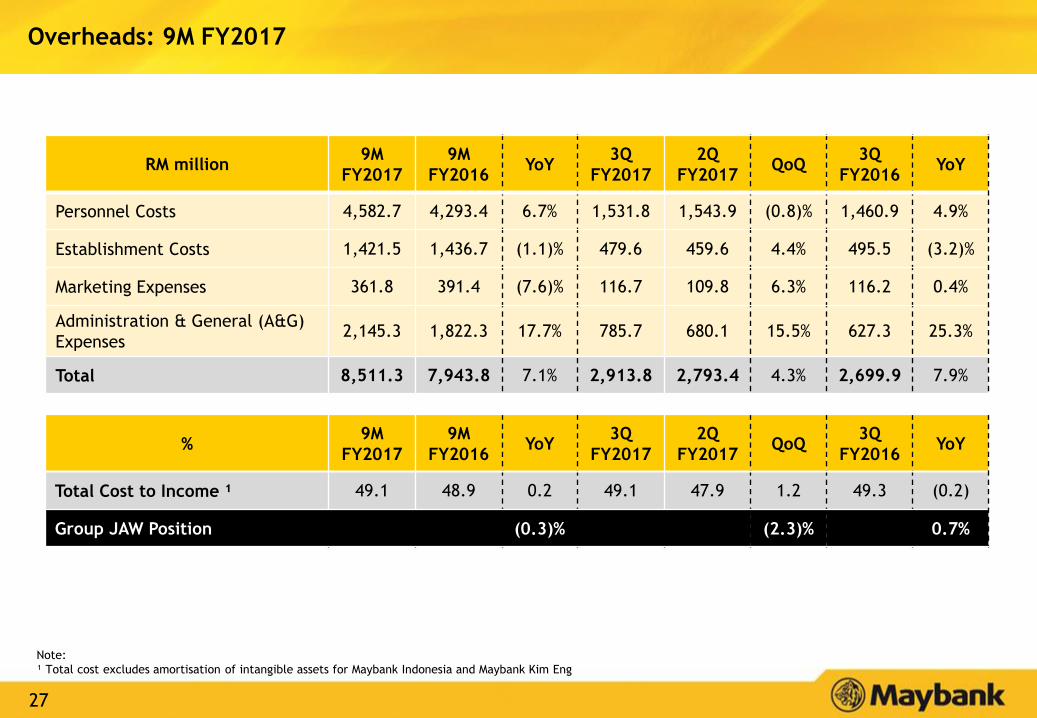

FY2016YoY

Personnel Costs 4,582.7 4,293.4 6.7% 1,531.8 1,543.9 (0.8)% 1,460.9 4.9%

Establishment Costs 1,421.5 1,436.7 (1.1)% 479.6 459.6 4.4% 495.5 (3.2)%

Marketing Expenses 361.8 391.4 (7.6)% 116.7 109.8 6.3% 116.2 0.4%

Administration & General (A&G)

Expenses 2,145.3 1,822.3 17.7% 785.7 680.1 15.5% 627.3 25.3%

Total 8,511.3 7,943.8 7.1% 2,913.8 2,793.4 4.3% 2,699.9 7.9%

%9M

FY2017

9M

FY2016YoY

3Q

FY2017

2Q

FY2017QoQ

3Q

FY2016YoY

Total Cost to Income ¹ 49.1 48.9 0.2 49.1 47.9 1.2 49.3 (0.2)

Group JAW Position (0.3)% (2.3)% 0.7%

Overheads: 9M FY2017

Note:

¹ Total cost excludes amortisation of intangible assets for Maybank Indonesia and Maybank Kim Eng

28

116.2 122.7

Sep 16 Sep 17

20.1 21.5

17.1 17.6

Sep 16 Sep 17

Community Financial Services Global Banking

95.8 94.5

22.4 30.2

Sep 16 Sep 17

+34.8%

44.245.2

Sep 16 Sep 17

190.6 199.8

72.2 79.1

Sep 16 Sep 17

461.2 485.9

Sep 16 Sep 17

Balance Sheet Management: 9M FY2017

261.5

37.4

118.5

RM

billion

SG

D b

illion

IDR

tri

llio

n

Gross Loans (YoY)

6.6% 4.6% 5.4% 5.3%

RM

billion

Group Malaysia Singapore Indonesia

39.1

278.7125.0

11.6 14.1

Sep 16 Sep 17

175.1190.1

Sep 16 Sep 17

5.6%

RM

billion

RM

billion

SG

D b

illion

IDR

tri

llio

n

CASA (YoY)

+4.8%

+9.4%

8.5% 21.7% 2.3%

+7.1%

+3.1%

(1.4)%

25.1% 31.9%40.3% 39.5%34.8% 36.8% 38.1% 37.8%CASA

Ratio:

Note: CASA ratio for Group and Malaysia includes investment accounts

Refer to pages 29-31 for detailed information on loans and deposits growth by country and products.

29

Group Gross Loans Growth: 30 September 2017

Note:

¹ Re-based loan growth figures are based on adjusted 31 December 2016 position in line with migration of client accounts, effective 1 January 2017

% of

Portfolio

30 Sep

2017

30 Jun

2017QoQ

31 Mar

2017

31 Dec

2016

YTD

Ann.

30 Sep

2016YoY

Group Gross Loans 485.9 480.1 1.2% 486.1 485.7 0.0% 461.2 5.3%

Malaysia (RM billion) 57% 278.7 273.8 1.8% 270.7 272.0 3.3% 261.5 6.6%

Community Financial Services 72% 199.8 197.1 1.3% 195.6 194.4 3.7% 190.6 4.8%

Community Financial Services ¹ 72% 199.8 197.1 1.3% 195.6 193.7 4.2% 190.6 4.8%

Global Banking 28% 79.1 78.0 1.4% 76.4 78.8 0.4% 72.2 9.4%

Global Banking ¹ 28% 79.1 78.0 1.4% 76.4 79.5 (0.7)% 72.2 9.4%

International (RM billion) 41% 199.8 199.0 0.4% 207.8 206.8 (4.6)% 192.6 3.7%

Singapore (SGD billion) 61% 39.1 38.5 1.6% 39.1 38.9 0.7% 37.4 4.6%

Community Financial Services 55% 21.5 21.1 2.2% 20.9 20.7 5.6% 20.1 7.1%

Global Banking 45% 17.6 17.2 2.2% 18.0 18.0 (3.3)% 17.1 3.1%

Indonesia (IDR trillion) 20% 125.0 123.1 1.6% 122.6 124.7 0.3% 118.5 5.4%

Community Financial Services 76% 94.5 93.5 1.0% 94.7 97.0 (3.5)% 95.8 (1.4)%

Global Banking 24% 30.2 29.3 3.3% 27.6 27.4 13.7% 22.4 34.8%

Other markets (RM billion) 19% 38.9 39.3 (1.1)% 43.3 44.6 (17.2)% 41.5 (6.3)%

Investment banking (RM billion) 2% 7.4 7.3 0.8% 7.6 6.9 9.2% 7.1 3.7%

30

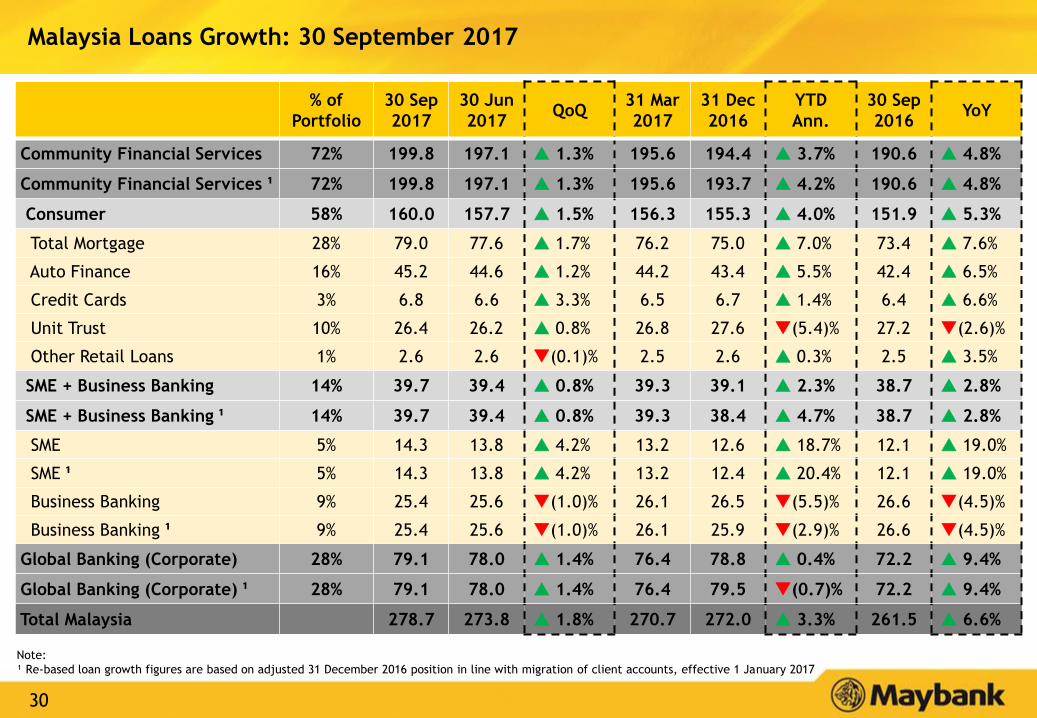

Malaysia Loans Growth: 30 September 2017

% of

Portfolio

30 Sep

2017

30 Jun

2017QoQ

31 Mar

2017

31 Dec

2016

YTD

Ann.

30 Sep

2016YoY

Community Financial Services 72% 199.8 197.1 1.3% 195.6 194.4 3.7% 190.6 4.8%

Community Financial Services ¹ 72% 199.8 197.1 1.3% 195.6 193.7 4.2% 190.6 4.8%

Consumer 58% 160.0 157.7 1.5% 156.3 155.3 4.0% 151.9 5.3%

Total Mortgage 28% 79.0 77.6 1.7% 76.2 75.0 7.0% 73.4 7.6%

Auto Finance 16% 45.2 44.6 1.2% 44.2 43.4 5.5% 42.4 6.5%

Credit Cards 3% 6.8 6.6 3.3% 6.5 6.7 1.4% 6.4 6.6%

Unit Trust 10% 26.4 26.2 0.8% 26.8 27.6 (5.4)% 27.2 (2.6)%

Other Retail Loans 1% 2.6 2.6 (0.1)% 2.5 2.6 0.3% 2.5 3.5%

SME + Business Banking 14% 39.7 39.4 0.8% 39.3 39.1 2.3% 38.7 2.8%

SME + Business Banking ¹ 14% 39.7 39.4 0.8% 39.3 38.4 4.7% 38.7 2.8%

SME 5% 14.3 13.8 4.2% 13.2 12.6 18.7% 12.1 19.0%

SME ¹ 5% 14.3 13.8 4.2% 13.2 12.4 20.4% 12.1 19.0%

Business Banking 9% 25.4 25.6 (1.0)% 26.1 26.5 (5.5)% 26.6 (4.5)%

Business Banking ¹ 9% 25.4 25.6 (1.0)% 26.1 25.9 (2.9)% 26.6 (4.5)%

Global Banking (Corporate) 28% 79.1 78.0 1.4% 76.4 78.8 0.4% 72.2 9.4%

Global Banking (Corporate) ¹ 28% 79.1 78.0 1.4% 76.4 79.5 (0.7)% 72.2 9.4%

Total Malaysia 278.7 273.8 1.8% 270.7 272.0 3.3% 261.5 6.6%

Note:

¹ Re-based loan growth figures are based on adjusted 31 December 2016 position in line with migration of client accounts, effective 1 January 2017

31

Group Deposits Growth: 30 September 2017

% of

Portfolio

30 Sep

2017

30 Jun

2017QoQ

31 Mar

2017

31 Dec

2016

YTD

Ann.

30 Sep

2016YoY

Group Gross Deposits 517.2 511.7 1.1% 508.1 517.1 0.0% 503.5 2.7%

Malaysia (RM billion) 60% 310.4 304.9 1.8% 301.8 300.9 4.2% 288.7 7.5%

Savings Deposits 13% 40.9 41.1 (0.5)% 41.2 38.8 7.3% 41.8 (2.2)%

Current Accounts 26% 81.8 82.1 (0.4)% 83.2 83.2 (2.2)% 74.3 10.0%

Fixed Deposits 53% 165.2 159.8 3.4% 159.5 163.5 1.4% 161.9 2.0%

Others 7% 22.5 21.9 2.6% 17.9 15.5 60.4% 10.6 >100%

International 40% 208.3 208.8 (0.2)% 208.2 217.7 (5.7)% 216.2 (3.7)%

Singapore (SGD billion) 66% 44.2 42.1 4.9% 42.3 44.5 (1.0)% 46.2 (4.4)%

Savings Deposits 15% 6.4 5.8 11.9% 5.8 5.7 16.9% 4.9 32.5%

Current Accounts 17% 7.6 7.6 0.6% 7.1 6.8 16.3% 6.7 13.8%

Fixed Deposits 68% 30.1 28.8 4.6% 29.4 32.0 (7.9)% 34.6 (13.1)%

Indonesia (IDR trillion) 18% 119.4 120.1 (0.6)% 118.0 119.3 0.1% 116.0 3.0%

Savings Deposits 21% 24.4 24.5 (0.3)% 24.8 25.6 (6.2)% 25.3 (3.6)%

Current Accounts 17% 20.8 20.2 2.6% 18.9 20.4 2.1% 18.8 10.2%

Fixed Deposits 62% 74.2 75.4 (1.6)% 74.3 73.3 1.7% 71.8 3.4%

Note:

Deposits figures are restated following a BNM circular dated 21 June 2017 which excludes structured deposits

32

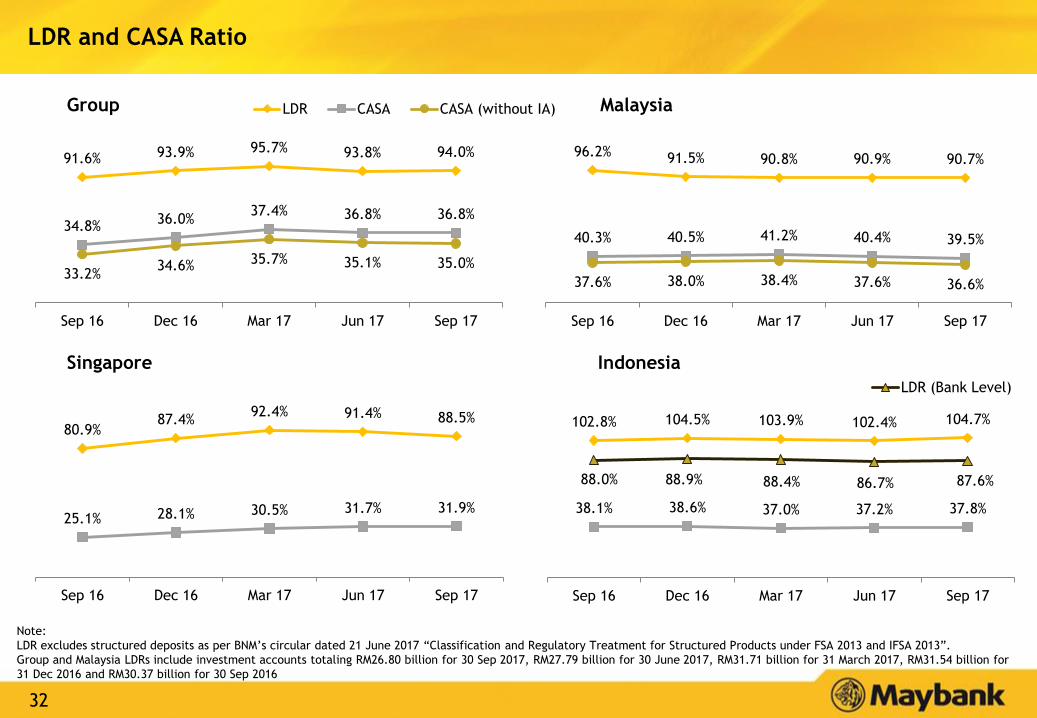

91.6% 93.9% 95.7% 93.8% 94.0%

34.8%36.0%

37.4% 36.8% 36.8%

33.2%34.6% 35.7% 35.1% 35.0%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

LDR CASA CASA (without IA)

96.2% 91.5% 90.8% 90.9% 90.7%

40.3% 40.5% 41.2% 40.4% 39.5%

37.6% 38.0% 38.4% 37.6% 36.6%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

LDR and CASA Ratio

Singapore Indonesia

Group Malaysia

102.8% 104.5% 103.9% 102.4% 104.7%

38.1% 38.6% 37.0% 37.2% 37.8%

88.0% 88.9% 88.4% 86.7% 87.6%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

LDR (Bank Level)

80.9%87.4%

92.4% 91.4% 88.5%

25.1% 28.1% 30.5% 31.7% 31.9%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

Note:

LDR excludes structured deposits as per BNM’s circular dated 21 June 2017 “Classification and Regulatory Treatment for Structured Products under FSA 2013 and IFSA 2013”.

Group and Malaysia LDRs include investment accounts totaling RM26.80 billion for 30 Sep 2017, RM27.79 billion for 30 June 2017, RM31.71 billion for 31 March 2017, RM31.54 billion for

31 Dec 2016 and RM30.37 billion for 30 Sep 2016

33

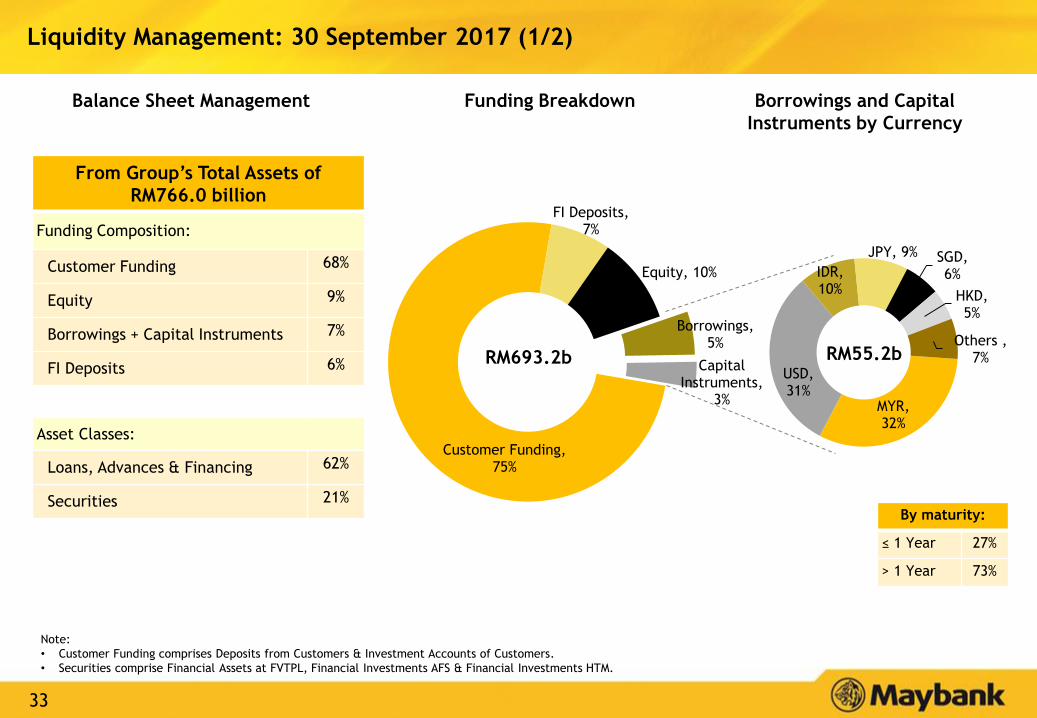

Borrowings, 5%

Capital Instruments,

3%

Customer Funding, 75%

FI Deposits, 7%

Equity, 10%

MYR, 32%

USD, 31%

IDR, 10%

JPY, 9% SGD, 6%

HKD, 5%

Others , 7%

Liquidity Management: 30 September 2017 (1/2)

Balance Sheet Management

RM693.2b RM55.2b

Funding Breakdown

Note:

• Customer Funding comprises Deposits from Customers & Investment Accounts of Customers.

• Securities comprise Financial Assets at FVTPL, Financial Investments AFS & Financial Investments HTM.

By maturity:

≤ 1 Year 27%

> 1 Year 73%

Borrowings and Capital

Instruments by Currency

From Group’s Total Assets of

RM766.0 billion

Funding Composition:

Customer Funding 68%

Equity 9%

Borrowings + Capital Instruments 7%

FI Deposits 6%

Asset Classes:

Loans, Advances & Financing 62%

Securities 21%

34

136.0%

151.9%

134.4%145.6%

137.0%

LCRMoving Towards More Reflective Liquidity Risk Indicators

Loan to

Deposits

Ratio

(LDR)

• Reflects simplistic assessment on deposits. It

ignores other funding instruments on the

balance sheet.

• Could be a contributor to the recurrence of

significant year-end spikes in the spread

between BNM’s OPR and 3-month KLIBOR.

• As financial institutions’ funding compositions

are more diversified today, traditional

indicators such as LDR are less relevant.

Loan to

Funding

Ratio

(LTF)

Loan to

Funding and

Equity Ratio

(LTFE)

Liquidity Management: 30 September 2017 (2/2)

𝐺𝑟𝑜𝑠𝑠 𝐿𝑜𝑎𝑛𝑠

𝐷𝑒𝑝𝑜𝑠𝑖𝑡𝑠 + 𝐵𝑜𝑟𝑟𝑜𝑤𝑖𝑛𝑔𝑠 + 𝑆𝑢𝑏𝑑𝑒𝑏𝑡

91.6%

93.9%

95.7%

93.8% 94.0%

83.2%

84.9%86.2%

85.5% 85.8%

73.7%75.1%

75.9%75.1% 75.4%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

LDR LTF LTFE

𝐺𝑟𝑜𝑠𝑠 𝐿𝑜𝑎𝑛𝑠

𝐷𝑒𝑝𝑜𝑠𝑖𝑡𝑠 + 𝐵𝑜𝑟𝑟𝑜𝑤𝑖𝑛𝑔𝑠 + 𝑆𝑢𝑏𝑑𝑒𝑏𝑡 +𝐸𝑞𝑢𝑖𝑡𝑦 (𝑖𝑛𝑐𝑙𝑢𝑑𝑒𝑠 𝑐𝑎𝑝𝑖𝑡𝑎𝑙 𝑠𝑒𝑐𝑢𝑟𝑖𝑡𝑖𝑒𝑠)

Note: BNM’s minimum LCR requirement for 2017 is 80%.

As such, BNM has guided for the adoption of LCR and other liquidity

indicators to better reflect the stability and diversity of funding by a

financial institution. The other liquidity indicators are:

35

370.3

615.7 542.5

830.3

386.5

2,217.0

1,759.3

3QFY2016

4QFY2016

1QFY2017

2QFY2017

3QFY2017

9MFY2016

9MFY2017

Allowances for losses on loans

74.8%

72.0% 71.2%70.1%

71.7%*

Loan loss coverage

Allowance for losses on loans

Asset QualityR

M m

illion

Note:

*Loan loss coverage including Regulatory Reserve is 93.5%

11,055 11,65812,158 12,155

Dec 16 Mar 17 Jun 17 Sep 17

RM

million

9.9% YTD

4.3% QoQ 5.4% QoQ

8,555 9,33710,568 10,240

Dec 15 Mar 16 Jun 16 Sep 16

RM

million

19.7% YTD

13.2% QoQ 9.1% QoQ

(3.1)% QoQ

Slower YTD growth in Group GIL volume

compared to 2016

0.0% QoQ

36

Asset Quality for Group and Home Markets

Group GIL Ratio Composition

GIL Ratio Components Sep 2017 Jun 2017 Mar 2017 Dec 2016 Sep 2016

Non Performing Loans (NPL) 1.97% 1.79% 1.77% 1.64% 1.35%

Restructured & Rescheduled (R&R) 0.32% 0.37% 0.33% 0.39% 0.52%

Performing Loans Impaired Due to Judgmental/

Obligatory Triggers (IPL)0.21% 0.37% 0.30% 0.25% 0.35%

GIL Ratio 2.50% 2.53% 2.40% 2.28% 2.22%

2.14% 2.06% 2.13%

2.12% 2.06%

0.98%1.30%

1.68%

2.29% 2.31%

4.06%4.36% 4.55% 4.42% 4.47%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

Malaysia Singapore Indonesia

GIL Ratio by Home Markets

37

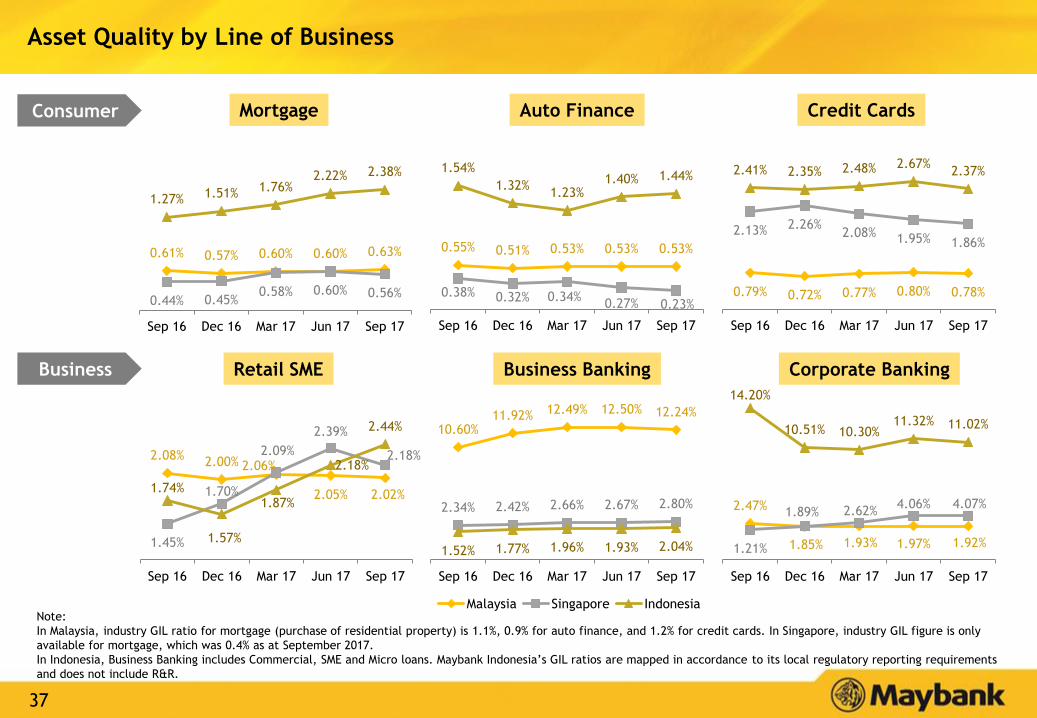

Asset Quality by Line of Business

Mortgage Auto Finance Credit Cards

Retail SME Business Banking Corporate Banking

Consumer

Business

Note:

In Malaysia, industry GIL ratio for mortgage (purchase of residential property) is 1.1%, 0.9% for auto finance, and 1.2% for credit cards. In Singapore, industry GIL figure is only

available for mortgage, which was 0.4% as at September 2017.

In Indonesia, Business Banking includes Commercial, SME and Micro loans. Maybank Indonesia’s GIL ratios are mapped in accordance to its local regulatory reporting requirements

and does not include R&R.

0.61% 0.57% 0.60% 0.60% 0.63%

0.44% 0.45%0.58% 0.60% 0.56%

1.27% 1.51% 1.76%2.22% 2.38%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

2.08%2.00% 2.06%

2.05% 2.02%

1.45%

1.70%

2.09%

2.39%

2.18%

1.74%

1.57%

1.87%

2.18%

2.44%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

0.55% 0.51% 0.53% 0.53% 0.53%

0.38% 0.32% 0.34%0.27% 0.23%

1.54%

1.32%1.23%

1.40% 1.44%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

0.79% 0.72% 0.77% 0.80% 0.78%

2.13% 2.26%2.08% 1.95% 1.86%

2.41% 2.35% 2.48% 2.67%2.37%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

10.60%11.92% 12.49% 12.50% 12.24%

2.34% 2.42% 2.66% 2.67% 2.80%

1.52% 1.77% 1.96% 1.93% 2.04%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

Malaysia Singapore Indonesia

14.20%

10.51% 10.30%11.32% 11.02%

2.47%

1.85% 1.93% 1.97% 1.92%1.21%

1.89% 2.62%4.06% 4.07%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

38

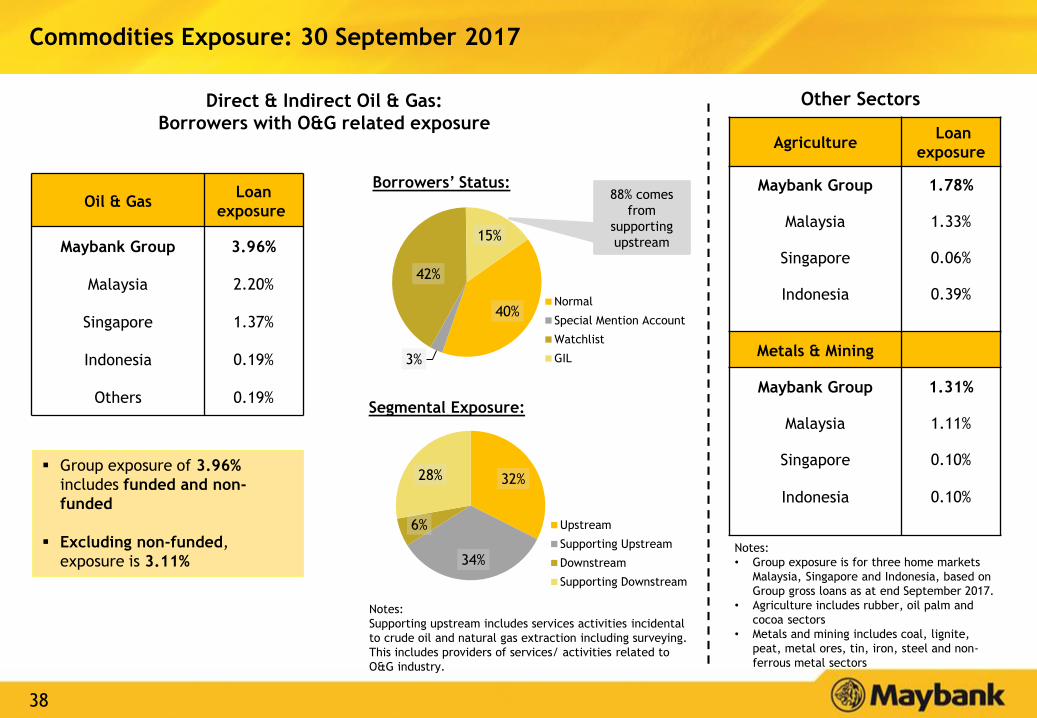

40%

3%

42%

15%

Normal

Special Mention Account

Watchlist

GIL

32%

34%

6%

28%

Upstream

Supporting Upstream

Downstream

Supporting Downstream

88% comes

from

supporting

upstream

Commodities Exposure: 30 September 2017

Notes:

• Group exposure is for three home markets

Malaysia, Singapore and Indonesia, based on

Group gross loans as at end September 2017.

• Agriculture includes rubber, oil palm and

cocoa sectors

• Metals and mining includes coal, lignite,

peat, metal ores, tin, iron, steel and non-

ferrous metal sectors

AgricultureLoan

exposure

Maybank Group 1.78%

Malaysia 1.33%

Singapore 0.06%

Indonesia 0.39%

Metals & Mining

Maybank Group 1.31%

Malaysia 1.11%

Singapore 0.10%

Indonesia 0.10%

Borrowers’ Status:

Segmental Exposure:

Direct & Indirect Oil & Gas:

Borrowers with O&G related exposure

Other Sectors

Notes:

Supporting upstream includes services activities incidental

to crude oil and natural gas extraction including surveying.

This includes providers of services/ activities related to

O&G industry.

Oil & GasLoan

exposure

Maybank Group 3.96%

Malaysia 2.20%

Singapore 1.37%

Indonesia 0.19%

Others 0.19%

Group exposure of 3.96%

includes funded and non-

funded

Excluding non-funded,

exposure is 3.11%

39

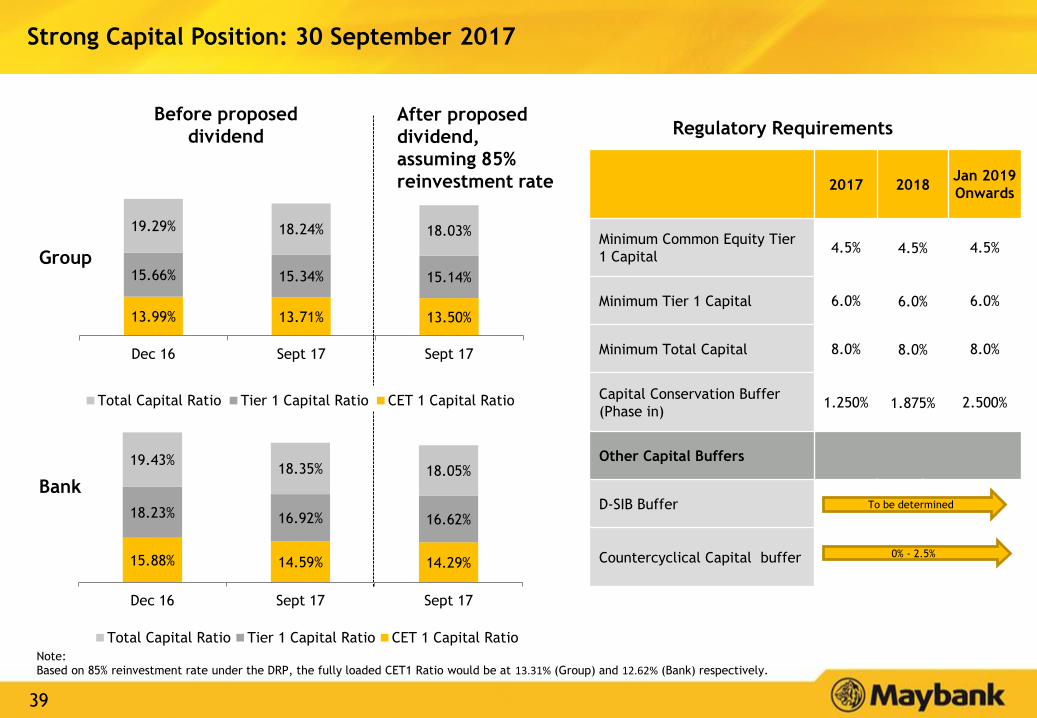

13.99% 13.71% 13.50%

15.66% 15.34% 15.14%

19.29% 18.24% 18.03%

Dec 16 Sept 17 Sept 17

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

Group

Bank

Strong Capital Position: 30 September 2017

Before proposed

dividend

After proposed

dividend,

assuming 85%

reinvestment rate 2017 2018Jan 2019

Onwards

Minimum Common Equity Tier

1 Capital4.5% 4.5% 4.5%

Minimum Tier 1 Capital 6.0% 6.0% 6.0%

Minimum Total Capital 8.0% 8.0% 8.0%

Capital Conservation Buffer

(Phase in)1.250% 1.875% 2.500%

Other Capital Buffers

D-SIB Buffer

Countercyclical Capital buffer

Regulatory Requirements

To be determined

0% - 2.5%

Note: Based on 85% reinvestment rate under the DRP, the fully loaded CET1 Ratio would be at 13.31% (Group) and 12.62% (Bank) respectively.

15.88% 14.59% 14.29%

18.23% 16.92% 16.62%

19.43%18.35% 18.05%

Dec 16 Sept 17 Sept 17

Total Capital Ratio Tier 1 Capital Ratio CET 1 Capital Ratio

40

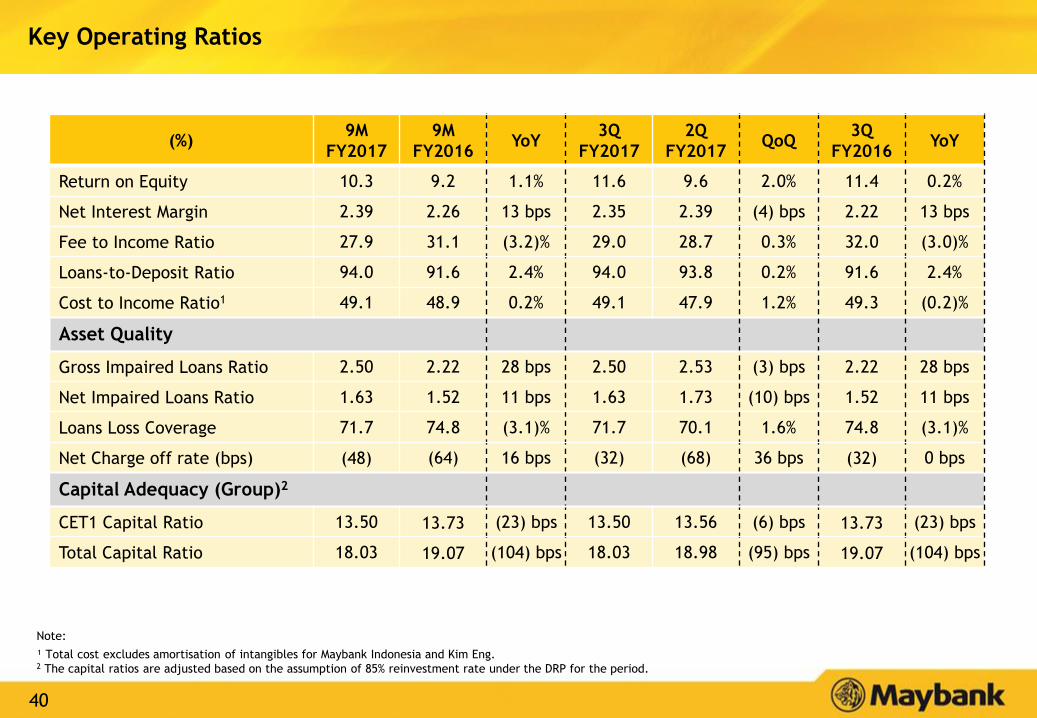

Key Operating Ratios

(%)9M

FY2017

9M

FY2016YoY

3Q

FY2017

2Q

FY2017QoQ

3Q

FY2016YoY

Return on Equity 10.3 9.2 1.1% 11.6 9.6 2.0% 11.4 0.2%

Net Interest Margin 2.39 2.26 13 bps 2.35 2.39 (4) bps 2.22 13 bps

Fee to Income Ratio 27.9 31.1 (3.2)% 29.0 28.7 0.3% 32.0 (3.0)%

Loans-to-Deposit Ratio 94.0 91.6 2.4% 94.0 93.8 0.2% 91.6 2.4%

Cost to Income Ratio1 49.1 48.9 0.2% 49.1 47.9 1.2% 49.3 (0.2)%

Asset Quality

Gross Impaired Loans Ratio 2.50 2.22 28 bps 2.50 2.53 (3) bps 2.22 28 bps

Net Impaired Loans Ratio 1.63 1.52 11 bps 1.63 1.73 (10) bps 1.52 11 bps

Loans Loss Coverage 71.7 74.8 (3.1)% 71.7 70.1 1.6% 74.8 (3.1)%

Net Charge off rate (bps) (48) (64) 16 bps (32) (68) 36 bps (32) 0 bps

Capital Adequacy (Group)2

CET1 Capital Ratio 13.50 13.73 (23) bps 13.50 13.56 (6) bps 13.73 (23) bps

Total Capital Ratio 18.03 19.07 (104) bps 18.03 18.98 (95) bps 19.07 (104) bps

Note:

¹ Total cost excludes amortisation of intangibles for Maybank Indonesia and Kim Eng.2 The capital ratios are adjusted based on the assumption of 85% reinvestment rate under the DRP for the period.

41

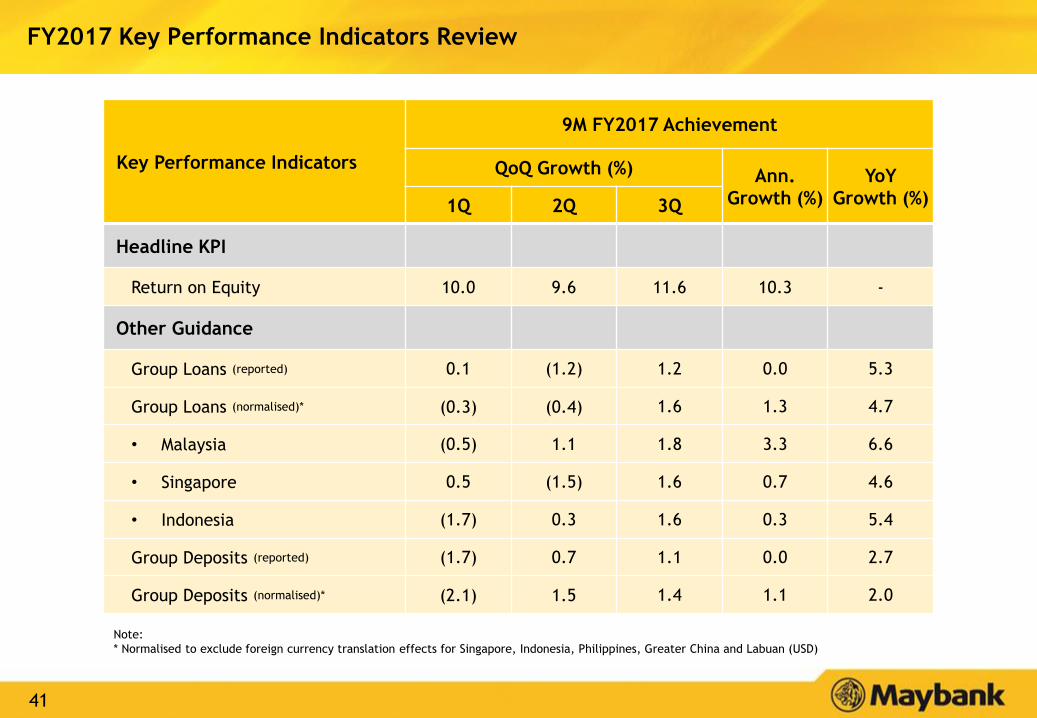

FY2017 Key Performance Indicators Review

Note:

* Normalised to exclude foreign currency translation effects for Singapore, Indonesia, Philippines, Greater China and Labuan (USD)

Key Performance Indicators

9M FY2017 Achievement

QoQ Growth (%) Ann.

Growth (%)

YoY

Growth (%)1Q 2Q 3Q

Headline KPI

Return on Equity 10.0 9.6 11.6 10.3 -

Other Guidance

Group Loans (reported) 0.1 (1.2) 1.2 0.0 5.3

Group Loans (normalised)* (0.3) (0.4) 1.6 1.3 4.7

• Malaysia (0.5) 1.1 1.8 3.3 6.6

• Singapore 0.5 (1.5) 1.6 0.7 4.6

• Indonesia (1.7) 0.3 1.6 0.3 5.4

Group Deposits (reported) (1.7) 0.7 1.1 0.0 2.7

Group Deposits (normalised)* (2.1) 1.5 1.4 1.1 2.0

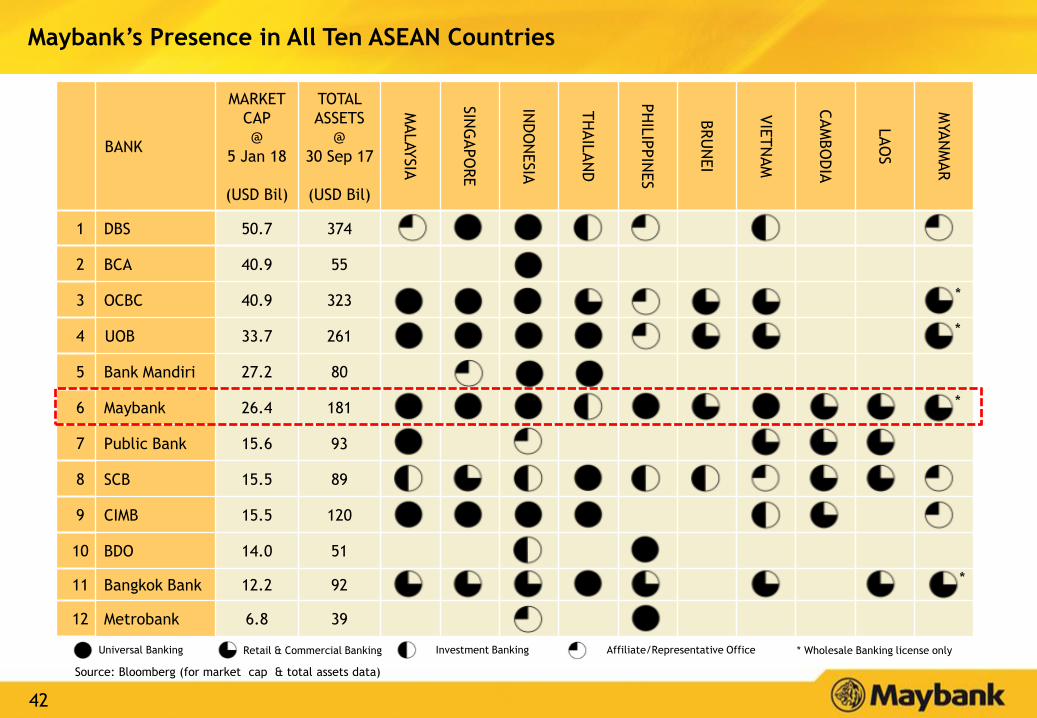

42

Universal Banking Retail & Commercial Banking Investment Banking Affiliate/Representative Office * Wholesale Banking license only

Source: Bloomberg (for market cap & total assets data)

Maybank’s Presence in All Ten ASEAN Countries

BANK

MARKET

CAP

@

5 Jan 18

(USD Bil)

TOTAL

ASSETS

@

30 Sep 17

(USD Bil)

MALAYSIA

SIN

GAPO

RE

IND

ON

ESIA

TH

AIL

AN

D

PH

ILIP

PIN

ES

BRU

NEI

VIE

TN

AM

CAM

BO

DIA

LAO

S

MYA

NM

AR

1 DBS 50.7 374

2 BCA 40.9 55

3 OCBC 40.9 323

4 UOB 33.7 261

5 Bank Mandiri 27.2 80

6 Maybank 26.4 181

7 Public Bank 15.6 93

8 SCB 15.5 89

9 CIMB 15.5 120

10 BDO 14.0 51

11 Bangkok Bank 12.2 92

12 Metrobank 6.8 39

*

*

*

*

43

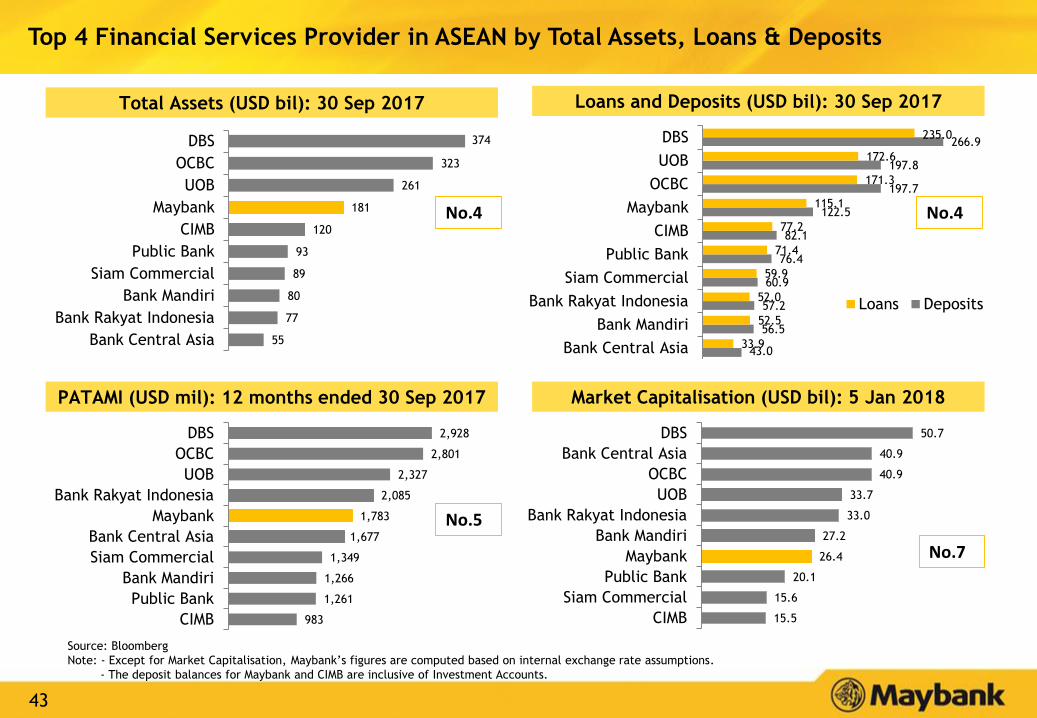

Top 4 Financial Services Provider in ASEAN by Total Assets, Loans & Deposits

50.7

40.9

40.9

33.7

33.0

27.2

26.4

20.1

15.6

15.5

DBS

Bank Central Asia

OCBC

UOB

Bank Rakyat Indonesia

Bank Mandiri

Maybank

Public Bank

Siam Commercial

CIMB

55

77

80

89

93

120

181

261

323

374

Bank Central Asia

Bank Rakyat Indonesia

Bank Mandiri

Siam Commercial

Public Bank

CIMB

Maybank

UOB

OCBC

DBS

43.0

56.5

57.2

60.9

76.4

82.1

122.5

197.7

197.8

266.9

33.9

52.5

52.0

59.9

71.4

77.2

115.1

171.3

172.6

235.0

Bank Central Asia

Bank Mandiri

Bank Rakyat Indonesia

Siam Commercial

Public Bank

CIMB

Maybank

OCBC

UOB

DBS

Loans Deposits

983

1,261

1,266

1,349

1,677

1,783

2,085

2,327

2,801

2,928

CIMB

Public Bank

Bank Mandiri

Siam Commercial

Bank Central Asia

Maybank

Bank Rakyat Indonesia

UOB

OCBC

DBS

No.7

No.4 No.4

No.5

Total Assets (USD bil): 30 Sep 2017 Loans and Deposits (USD bil): 30 Sep 2017

PATAMI (USD mil): 12 months ended 30 Sep 2017 Market Capitalisation (USD bil): 5 Jan 2018

Source: Bloomberg

Note: - Except for Market Capitalisation, Maybank’s figures are computed based on internal exchange rate assumptions.

- The deposit balances for Maybank and CIMB are inclusive of Investment Accounts.

44

Table of Contents

Appendix:

1. Financial Performance 32

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

45

Community Financial Services: Overview of Market Share for Malaysia

Note:¹ Rebased market share due to adjustment made to Industry data by BNM from

Jan-15 to Jun-17.

* Refers to housing, shophouse and other mortgage loans

** Credit cards market share refer to receivables for commercial

*** Total bank deposits inclusive of investment asset (“IA”)

^ Without IA. With IA, the market share as at June’17 for Total Core Retail Deposits,

Retail CASA, Retail Savings, Demand Deposits and Retail Fixed Deposits are 19.1%,

25.8%, 28.3%, 21.9% and 16.5% respectively (against MBB retail IA).

^^ Excluding non-financial transactions as per BNM guidelines

^^^ Industry numbers only available half yearly

46

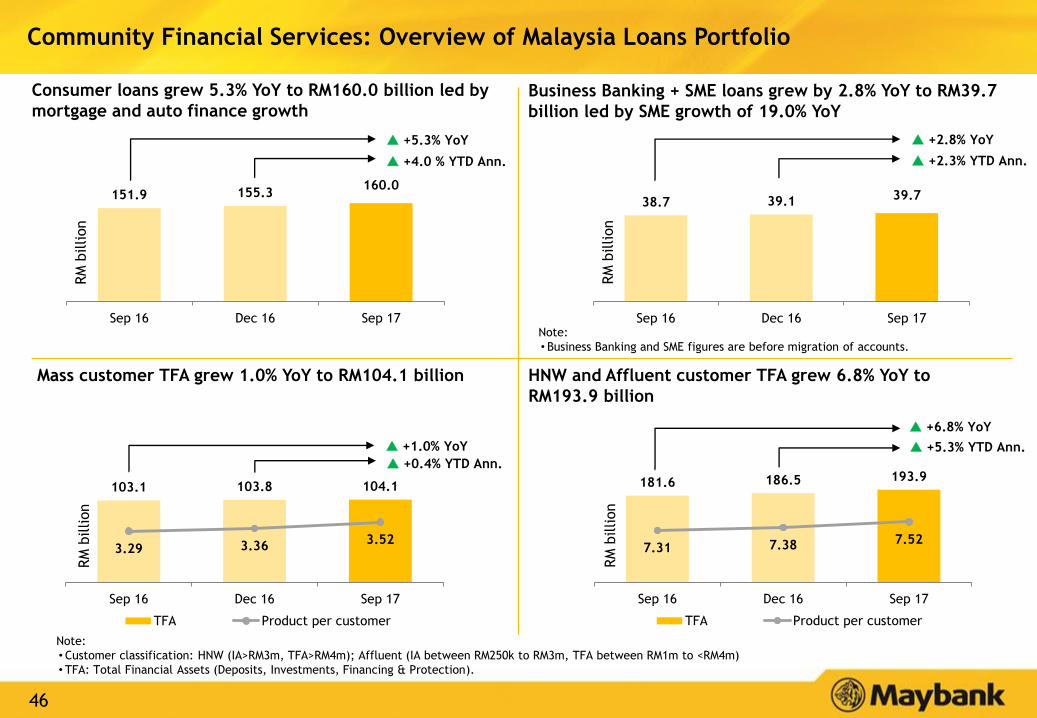

Business Banking + SME loans grew by 2.8% YoY to RM39.7

billion led by SME growth of 19.0% YoY

Community Financial Services: Overview of Malaysia Loans Portfolio

181.6 186.5 193.9

7.31 7.38 7.52

Sep 16 Dec 16 Sep 17

TFA Product per customer

103.1 103.8 104.1

3.29 3.363.52

Sep 16 Dec 16 Sep 17

TFA Product per customer

38.7 39.1 39.7

Sep 16 Dec 16 Sep 17

151.9 155.3160.0

Sep 16 Dec 16 Sep 17

+5.3% YoY

Consumer loans grew 5.3% YoY to RM160.0 billion led by

mortgage and auto finance growth

Note:

• Customer classification: HNW (IA>RM3m, TFA>RM4m); Affluent (IA between RM250k to RM3m, TFA between RM1m to <RM4m)

• TFA: Total Financial Assets (Deposits, Investments, Financing & Protection).

+4.0 % YTD Ann.

HNW and Affluent customer TFA grew 6.8% YoY to

RM193.9 billion

Mass customer TFA grew 1.0% YoY to RM104.1 billion

+2.8% YoY

+2.3% YTD Ann.

RM

billion

+1.0% YoY

RM

billion

+6.8% YoY

RM

billion

RM

billion

+5.3% YTD Ann.

Note:

• Business Banking and SME figures are before migration of accounts.

+0.4% YTD Ann.

47

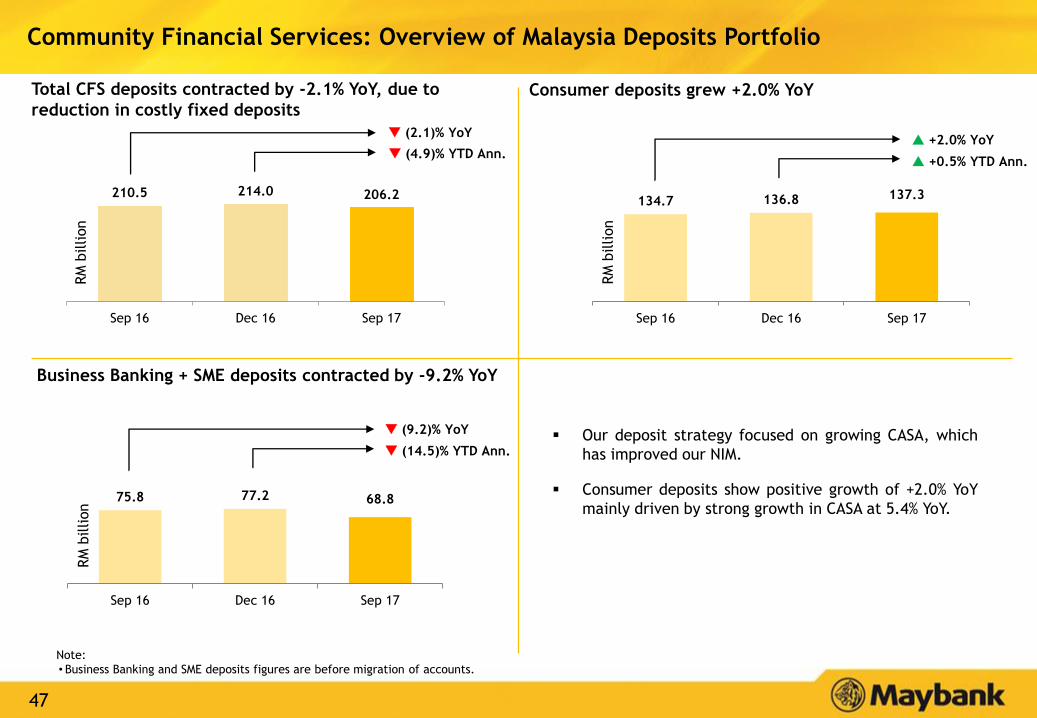

Community Financial Services: Overview of Malaysia Deposits Portfolio

210.5 214.0 206.2

Sep 16 Dec 16 Sep 17

(4.9)% YTD Ann.

134.7 136.8 137.3

Sep 16 Dec 16 Sep 17

+2.0% YoY

+0.5% YTD Ann.

Our deposit strategy focused on growing CASA, which

has improved our NIM.

Consumer deposits show positive growth of +2.0% YoY

mainly driven by strong growth in CASA at 5.4% YoY.75.8 77.2 68.8

Sep 16 Dec 16 Sep 17

(9.2)% YoY

(14.5)% YTD Ann.

RM

billion

Total CFS deposits contracted by -2.1% YoY, due to

reduction in costly fixed deposits

Business Banking + SME deposits contracted by -9.2% YoY

Consumer deposits grew +2.0% YoY

(2.1)% YoY

RM

billion

RM

billion

Note:

• Business Banking and SME deposits figures are before migration of accounts.

48

Table of Contents

Appendix:

1. Financial Performance 32

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

49

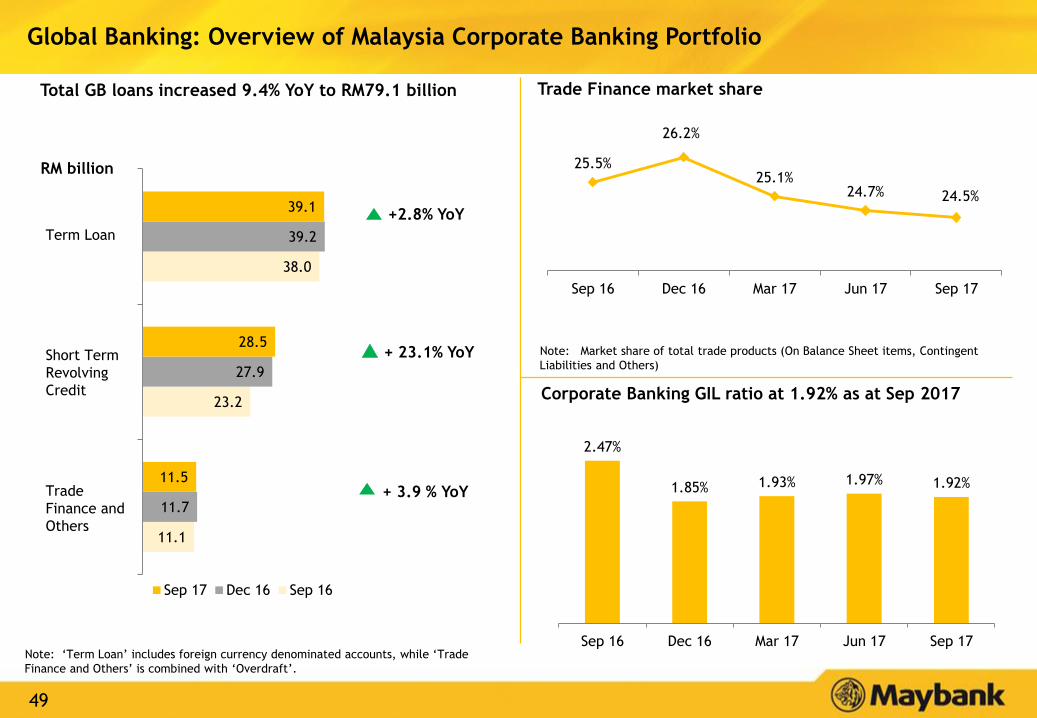

11.1

23.2

38.0

11.7

27.9

39.2

11.5

28.5

39.1

Sep 17 Dec 16 Sep 16

RM billion

Note: ‘Term Loan’ includes foreign currency denominated accounts, while ‘Trade

Finance and Others’ is combined with ‘Overdraft’.

Term Loan

Global Banking: Overview of Malaysia Corporate Banking Portfolio

Trade Finance market shareTotal GB loans increased 9.4% YoY to RM79.1 billion

Corporate Banking GIL ratio at 1.92% as at Sep 2017

Short Term

Revolving

Credit

Trade

Finance and

Others

Note: Market share of total trade products (On Balance Sheet items, Contingent

Liabilities and Others) + 23.1% YoY

+ 3.9 % YoY

+2.8% YoY

25.5%

26.2%

25.1%24.7% 24.5%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

2.47%

1.85% 1.93% 1.97% 1.92%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

50

Others, 69.1%

AAA, 14.3%

AA, 14.8%

A, 0.3%

< A, 0.2%

Commercial Papers, 1.3%

RM26.7

billion

24.7%

21.3%29.1%

19.0%

5.9%

RM 160.2

billion

Government

Securities

- Domestic

Government

Securities

- Foreign

PDS/Corp

Bonds

- Domestic

PDS –

Foreign

Others

(NIDs, BA, etc)

19.2%

25.2%28.7%

17.5%

9.4%

RM 138.0

billion

Government

Securities

- Domestic

Government

Securities

- Foreign

PDS/Corp

Bonds

- Domestic

PDS –

Foreign

Others

(NIDs, BA, etc)

Group Securities Portfolio¹: 40.3% Foreign Securities as at 9M FY2017

Group Securities Portfolio¹ grew 16.1% YoY

29% of PDS (Maybank Conventional Malaysia) rated “AA” or

above as at 9M FY2017

Global Banking: Overview of Group Securities and Global Markets Portfolio

9M FY20179M FY2016

61.4 57.968.2 67.7 73.6

63.762.8

68.6 71.477.1

12.910.2

11.9 9.6

9.5

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

Govt. Securities PDS/Corp Bonds Others

+16.1 %

RM

billion

138.0130.9

148.7 148.7

9M FY2016 9M FY2017

Note:

¹ Group Securities Portfolio is inclusive of Financial assets designated upon initial

recognition( part of FVTPL)

160.2

Note: ‘Others’ category refers to Government Guaranteed bonds, Partially Government

Guaranteed bonds and non rated bonds

Others, 47.3%

AAA, 21.2%

AA, 18.8%

A, 3.0%

< A, 0.6%

Commercial Papers,

9.1%

RM27.2

billion

51

Malaysia37%

Singapore26%

Thailand22%

Indonesia4%

Philippines2%

Hong Kong5%

Others4%

9M FY2017 Brokerage Market Share by Country

1 Singapore & Vietnam’s YTD ranking data are not available.

Note: Maybank Kim Eng represents the combined business of Maybank IB and business

segments under Maybank Kim Eng Holdings

Global Banking: Overview of Group Investment Banking Portfolio

Country RankMarket

Share

Trading Value

(USD’mil)

Thailand 1 6.9% 31,842.9

Malaysia 2 10.0% 20,866.0

Philippines 7 4.4% 2,598.7

Indonesia >10 2.2% 4,255.7

Hong Kong Tier 2 0.6% 23,608.2

Singapore N/A1 3.9% 12,754.0

Vietnam N/A1 2.0% 1,524.1

9M FY2017 Fee-based Income for Malaysia

Brokerage Fees50.7%

Arranger Fees8.9%

Underwriting & Placement

Fees9.3%

Advisory Fees11.0%

Agency/ Guarantee Fees

3.5%

Other Fee Income16.7%

9M FY2017 Total Income Breakdown by Country

RM992.7 mil

Total Income for Maybank Kim Eng

1,065.3992.7

9M FY2016 9M FY2017

(6.8)%

RM

mil

52

Table of Contents

Appendix:

1. Financial Performance 32

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

53

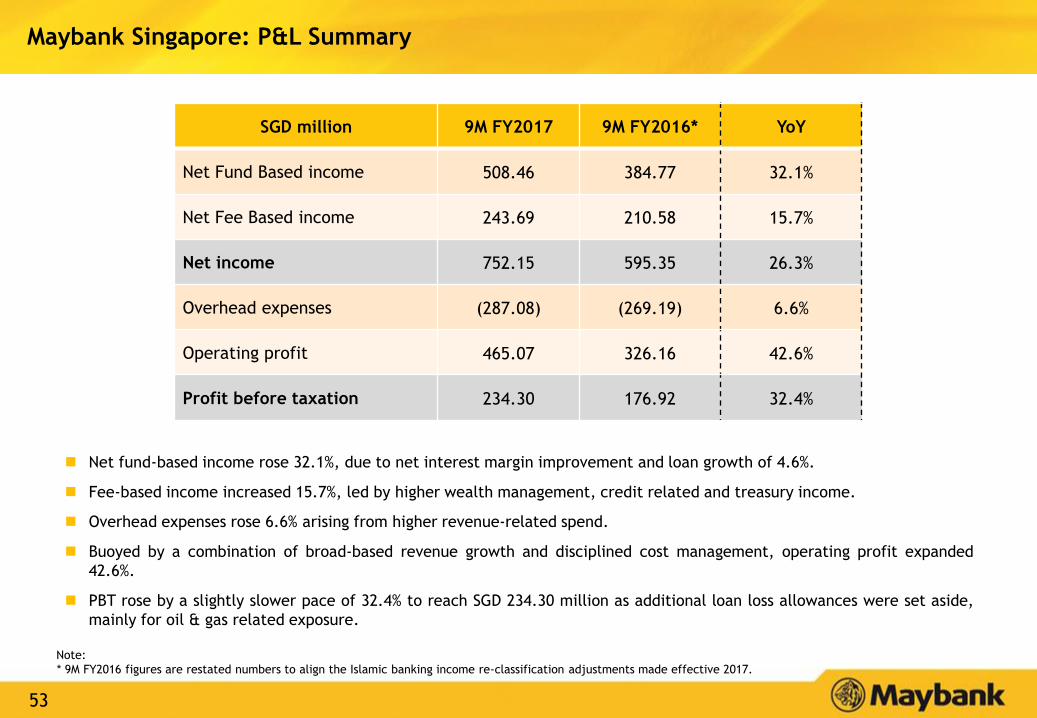

Maybank Singapore: P&L Summary

SGD million 9M FY2017 9M FY2016* YoY

Net Fund Based income 508.46 384.77 32.1%

Net Fee Based income 243.69 210.58 15.7%

Net income 752.15 595.35 26.3%

Overhead expenses (287.08) (269.19) 6.6%

Operating profit 465.07 326.16 42.6%

Profit before taxation 234.30 176.92 32.4%

Net fund-based income rose 32.1%, due to net interest margin improvement and loan growth of 4.6%.

Fee-based income increased 15.7%, led by higher wealth management, credit related and treasury income.

Overhead expenses rose 6.6% arising from higher revenue-related spend.

Buoyed by a combination of broad-based revenue growth and disciplined cost management, operating profit expanded

42.6%.

PBT rose by a slightly slower pace of 32.4% to reach SGD 234.30 million as additional loan loss allowances were set aside,

mainly for oil & gas related exposure.

Note:

* 9M FY2016 figures are restated numbers to align the Islamic banking income re-classification adjustments made effective 2017.

54

5.9 6.1 6.8

15.3 14.9 15.0

5.6 6.4 7.3

19.4 17.1 15.0

Sep 16 Dec 16 Sep 17

Consumer -Time Deposits

Consumer CASA

Business TimeDeposits

Business CASA

4.9 5.7 6.46.7 6.8 7.6

34.6 32.0 30.1

Sep 16 Dec 16 Sep 17

Time Deposits

Demand Deposits

Savings

8.4 8.4 8.5

4.4 4.9 4.4

3.7 4.2 4.1

6.1 6.3 6.2

9.5 9.7 10.4

1.8 1.8 2.03.4 3.5 3.5

Sep 16 Dec 16 Sep 17

Other(Consumer)

Car Loan

Housing Loan

Others(Corporate)

Non-Bankfinancial Inst

GeneralCommerce

Building &Construction

Maybank Singapore loans rose 4.6% YoY

Diversified Loan Portfolio

38.9

Consumer

40%

Corporate

60%

-1.9%

4.5%6.4%

4.9%4.6%

-5.0%0.5%

5.8%

6.4% 8.1%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

Maybank Singapore Growth Industry Growth

+4.6% YoY

Maybank Singapore: Overview of Loans and Deposits Portfolio

% YoY change

39.137.4

(4.4)% YoY

Consumer

50%

Corporate

50%

SG

D b

illion

Consumer deposits account for 50% of deposits

SG

D b

illion

CASA Ratio:

31.9%SG

D b

illion

Robust CASA growth of 21.7% YoY; CASA ratio also

improved to 31.9% in Sep 2017 from 25.1% a year ago

Consumer deposits reduced to S$22.3 billion due to lower FDs,

though this was partially mitigated by strong CASA growth

Business deposits higher on the back of a 14.8% increase in CASA

44.5 44.246.2

55

Table of Contents

Appendix:

1. Financial Performance 32

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

56

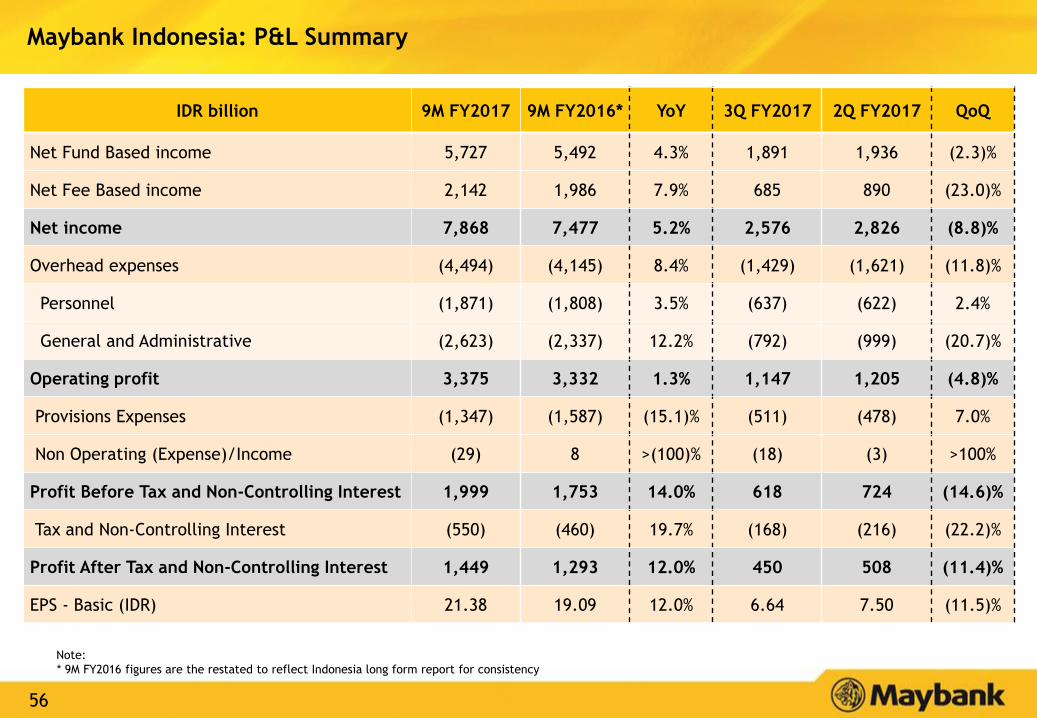

Maybank Indonesia: P&L Summary

IDR billion 9M FY2017 9M FY2016* YoY 3Q FY2017 2Q FY2017 QoQ

Net Fund Based income 5,727 5,492 4.3% 1,891 1,936 (2.3)%

Net Fee Based income 2,142 1,986 7.9% 685 890 (23.0)%

Net income 7,868 7,477 5.2% 2,576 2,826 (8.8)%

Overhead expenses (4,494) (4,145) 8.4% (1,429) (1,621) (11.8)%

Personnel (1,871) (1,808) 3.5% (637) (622) 2.4%

General and Administrative (2,623) (2,337) 12.2% (792) (999) (20.7)%

Operating profit 3,375 3,332 1.3% 1,147 1,205 (4.8)%

Provisions Expenses (1,347) (1,587) (15.1)% (511) (478) 7.0%

Non Operating (Expense)/Income (29) 8 >(100)% (18) (3) >100%

Profit Before Tax and Non-Controlling Interest 1,999 1,753 14.0% 618 724 (14.6)%

Tax and Non-Controlling Interest (550) (460) 19.7% (168) (216) (22.2)%

Profit After Tax and Non-Controlling Interest 1,449 1,293 12.0% 450 508 (11.4)%

EPS - Basic (IDR) 21.38 19.09 12.0% 6.64 7.50 (11.5)%

Note:

* 9M FY2016 figures are the restated to reflect Indonesia long form report for consistency

57

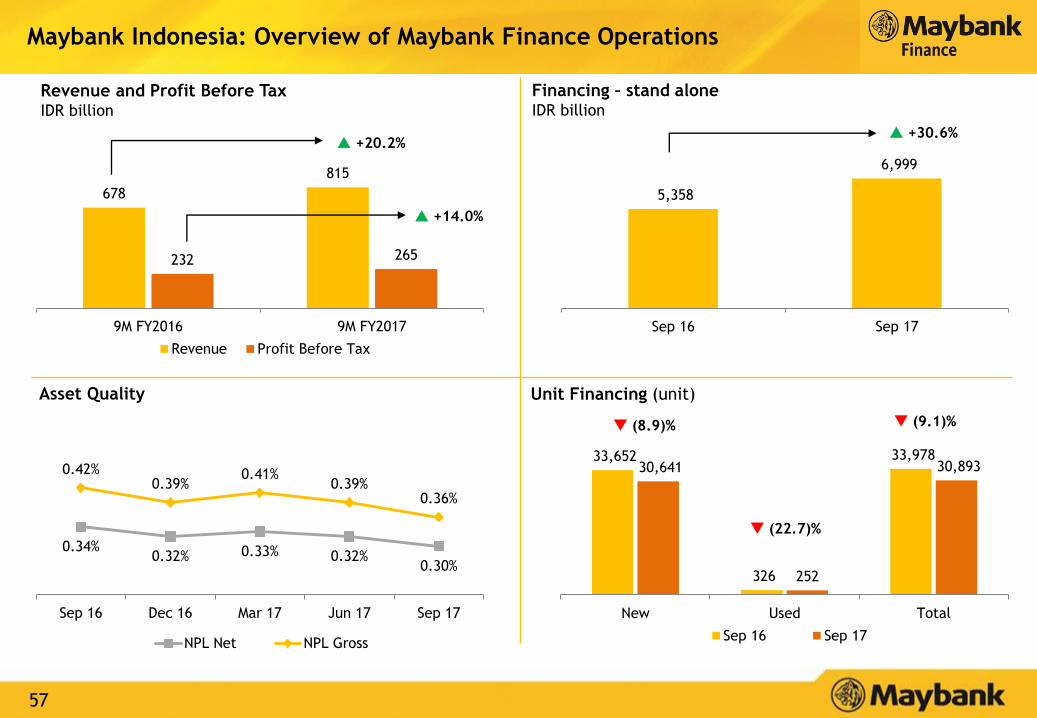

33,652

326

33,978 30,641

252

30,893

New Used Total

Sep 16 Sep 17

678

815

232 265

9M FY2016 9M FY2017

Revenue Profit Before Tax

Financing – stand aloneIDR billion

(8.9)%

(22.7)%

(9.1)%

+20.2% +30.6%

Asset Quality Unit Financing (unit)

Revenue and Profit Before Tax IDR billion

Maybank Indonesia: Overview of Maybank Finance Operations

+14.0%

0.34%0.32% 0.33% 0.32%

0.30%

0.42%0.39%

0.41%0.39%

0.36%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

NPL Net NPL Gross

5,358

6,999

Sep 16 Sep 17

58

176

41

107

324

169

24

134

327

New Used Multipurpose Total

Sep 16 Sep 17

1,422 1,554

73 132

9M FY2016 9M FY2017

Revenue Profit Before Tax

Financing – stand aloneIDR billion

+9.3% +6.7%

Asset Quality Unit Financing (‘000 unit)

Revenue and Profit Before Tax IDR billion

+81.5%

1.36% 1.25% 1.17% 1.21% 1.08%

3.84%3.32%

2.96% 2.84%2.60%

Sep 16 Dec 16 Mar 17 Jun 17 Sep 17

NPL Net NPL Gross

5,695 6,074

Sep 16 Sep 17

(4.3)% (41.5)%

+0.8%

+25.0%

Maybank Indonesia: Overview of WOM Finance Operations

59

Table of Contents

Appendix:

1. Financial Performance 32

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

60

31.1

36.4

33.0

5.3

18.1 16.9

32.2

41.2

34.5

5.8

20.6 23.0

AITAB Mortgage Term Financing Others (CFS) Term Financing Others (GB)

RM

billion

Sep-16 Sep-17

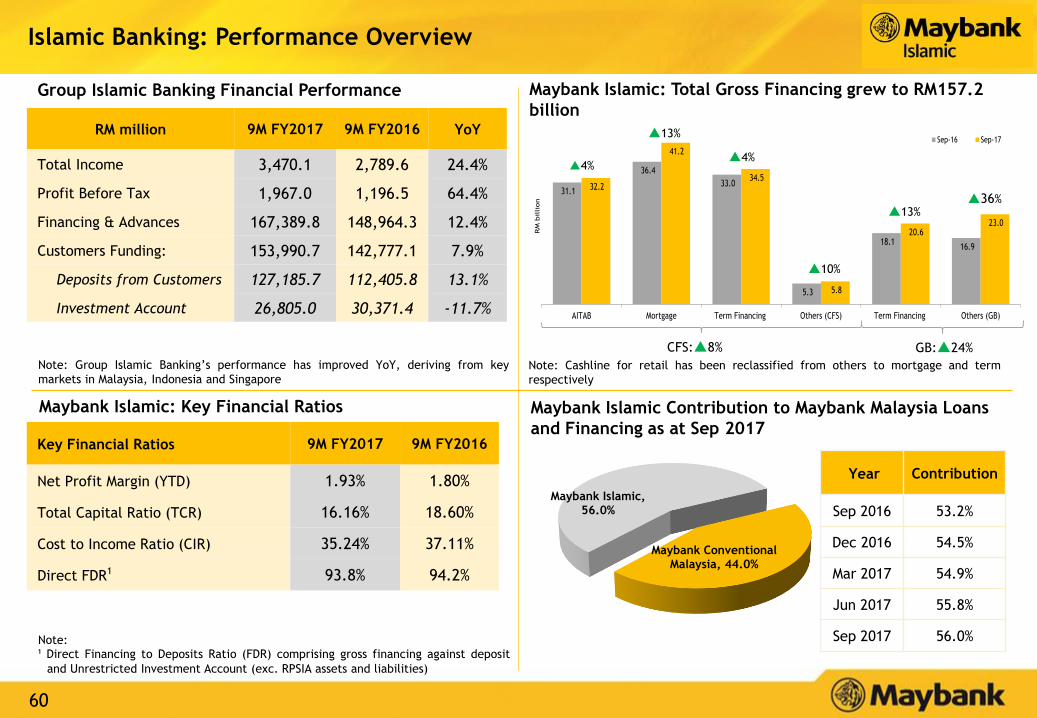

Islamic Banking: Performance Overview

Group Islamic Banking Financial Performance

Maybank Islamic: Key Financial Ratios

Maybank Islamic: Total Gross Financing grew to RM157.2

billion

CFS:8%

RM million 9M FY2017 9M FY2016 YoY

Total Income 3,470.1 2,789.6 24.4%

Profit Before Tax 1,967.0 1,196.5 64.4%

Financing & Advances 167,389.8 148,964.3 12.4%

Customers Funding: 153,990.7 142,777.1 7.9%

Deposits from Customers 127,185.7 112,405.8 13.1%

Investment Account 26,805.0 30,371.4 -11.7%

Key Financial Ratios 9M FY2017 9M FY2016

Net Profit Margin (YTD) 1.93% 1.80%

Total Capital Ratio (TCR) 16.16% 18.60%

Cost to Income Ratio (CIR) 35.24% 37.11%

Direct FDR1 93.8% 94.2%

Maybank Islamic Contribution to Maybank Malaysia Loans

and Financing as at Sep 2017

Year Contribution

Sep 2016 53.2%

Dec 2016 54.5%

Mar 2017 54.9%

Jun 2017 55.8%

Sep 2017 56.0%Note:¹ Direct Financing to Deposits Ratio (FDR) comprising gross financing against deposit

and Unrestricted Investment Account (exc. RPSIA assets and liabilities)

GB:24%

13%

4%

10%

36%

4%

13%

Note: Cashline for retail has been reclassified from others to mortgage and term

respectively

Note: Group Islamic Banking’s performance has improved YoY, deriving from key

markets in Malaysia, Indonesia and Singapore

Maybank Islamic, 56.0%

Maybank Conventional Malaysia, 44.0%

61

Maybank Islamic Market Share (Malaysia) as of Sep 17

Maybank Islamic ranks No.1 by Asset Market Share

in Malaysia

Source: BNM monthly statistical bulletin and latest respective Bank’s Financial

Statements

MalaysiaAsset Market Share

Jun 17Rank

Maybank Islamic 30% 1

CIMB Islamic 12% 2

Public Islamic 9% 3

Source: Bloomberg

Sukuk League Table Ranking Sep 2017

Key Products Sep 17 Sep 16

Automobile Financing 44.9% 43.7%

Home 27.9% 28.1%

Term Financing 29.6% 30.3%

Source for industry numbers: BNM Monthly Statistical Bulletin

Islamic Banking: Market Share

Market Share by Product (Malaysia) as of Sep 17

Source for industry numbers: BNM Monthly Statistical Bulletin

Market Share

(%)

Amount

(USD million)Issues

#2 Maybank 10.15% 4,203 98

Market Share

(%)

Amount

(USD million)Issues

#1 Maybank 29.69% 19,907 143

Global Sukuk League Table

Ranking

MYR Sukuk League Table

Ranking

33.5%34.1%

33.5% 33.6% 33.6%

30.4% 30.4%29.8% 29.6% 29.7%

Sep-16 Dec-16 Mar-17 Jun-17 Sep-17

Financing Deposits & Investment Accounts

62

554.1 641.6

9M FY16 9M FY17

32.4 31.9 32.9

Sep 16 Dec 16 Sep 17

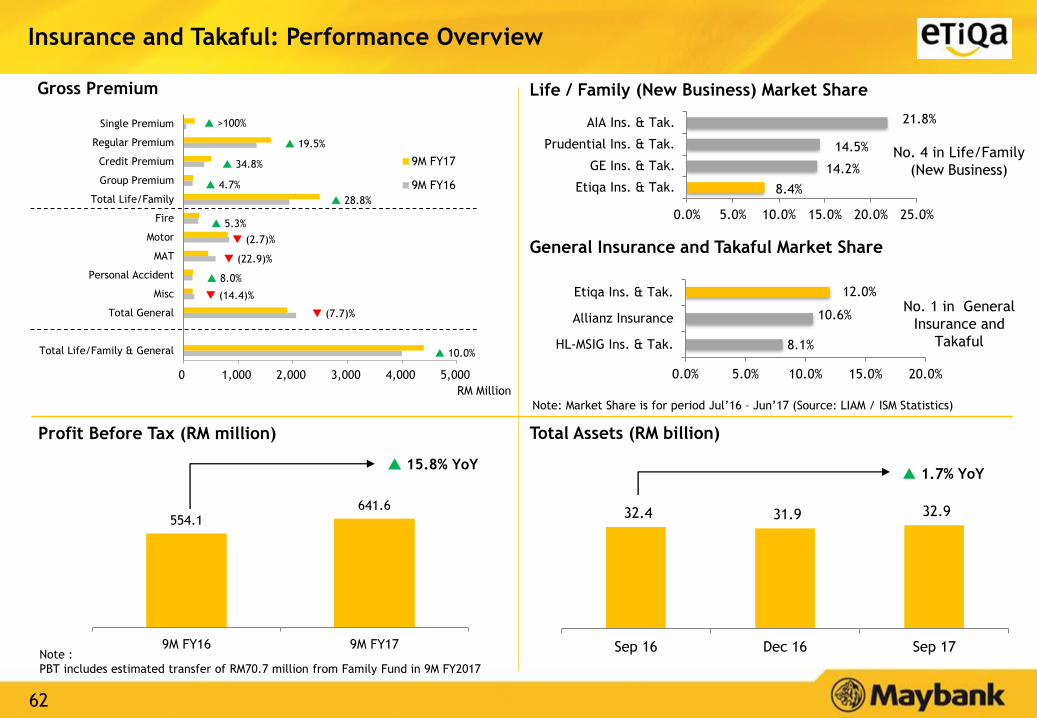

Insurance and Takaful: Performance Overview

Total Assets (RM billion)

Gross Premium

Profit Before Tax (RM million)

Life / Family (New Business) Market Share

No. 4 in Life/Family

(New Business)

No. 1 in General

Insurance and

Takaful

General Insurance and Takaful Market Share

15.8% YoY 1.7% YoY

Note :

PBT includes estimated transfer of RM70.7 million from Family Fund in 9M FY2017

Note: Market Share is for period Jul’16 – Jun’17 (Source: LIAM / ISM Statistics)

8.4%

14.2%

14.5%

21.8%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Etiqa Ins. & Tak.

GE Ins. & Tak.

Prudential Ins. & Tak.

AIA Ins. & Tak.

8.1%

10.6%

12.0%

0.0% 5.0% 10.0% 15.0% 20.0%

HL-MSIG Ins. & Tak.

Allianz Insurance

Etiqa Ins. & Tak.

0 1,000 2,000 3,000 4,000 5,000

Total Life/Family & General

Total General

Misc

Personal Accident

MAT

Motor

Fire

Total Life/Family

Group Premium

Credit Premium

Regular Premium

Single Premium

RM Million

9M FY17

9M FY16

>100%

19.5%

34.8%

4.7%

28.8%

5.3%

8.0%

(2.7)%

(22.9)%

(14.4)%

(7.7)%

10.0%

63

3,968.6 4,354.6

(87.9)

1,032.9

9M FY2016 9M FY2017

Revenue

PBT

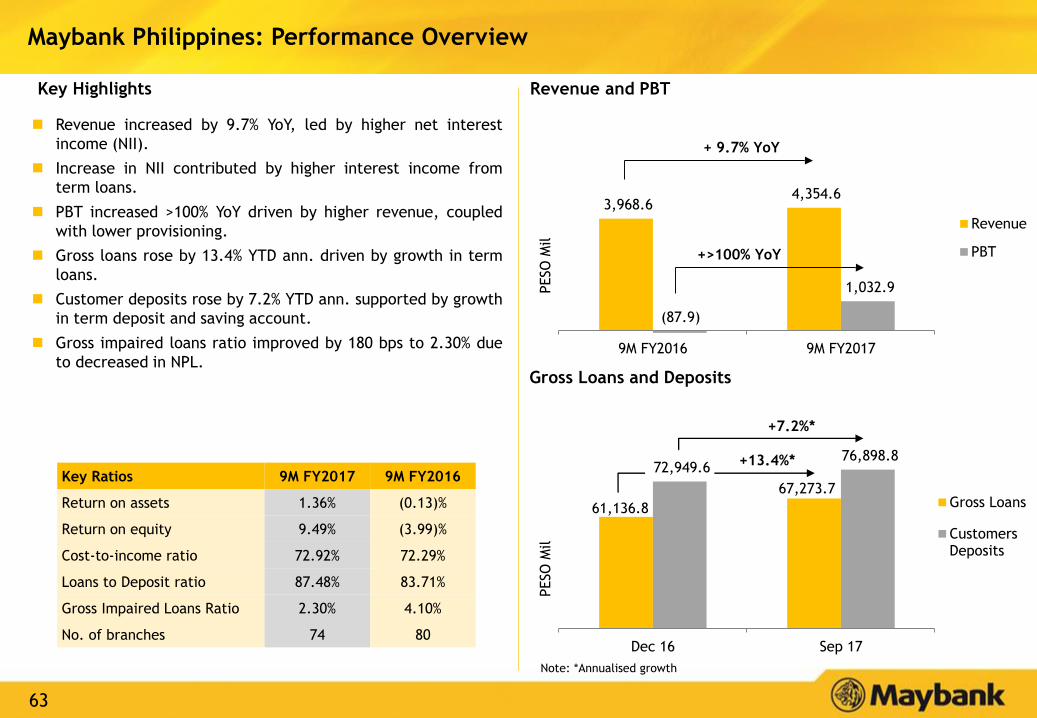

Maybank Philippines: Performance Overview

Revenue increased by 9.7% YoY, led by higher net interest

income (NII).

Increase in NII contributed by higher interest income from

term loans.

PBT increased >100% YoY driven by higher revenue, coupled

with lower provisioning.

Gross loans rose by 13.4% YTD ann. driven by growth in term

loans.

Customer deposits rose by 7.2% YTD ann. supported by growth

in term deposit and saving account.

Gross impaired loans ratio improved by 180 bps to 2.30% due

to decreased in NPL.

+ 9.7% YoY

+>100% YoY

Revenue and PBT

Gross Loans and Deposits

Key Highlights

PESO

Mil

PESO

Mil

+13.4%*

+7.2%*

Key Ratios 9M FY2017 9M FY2016

Return on assets 1.36% (0.13)%

Return on equity 9.49% (3.99)%

Cost-to-income ratio 72.92% 72.29%

Loans to Deposit ratio 87.48% 83.71%

Gross Impaired Loans Ratio 2.30% 4.10%

No. of branches 74 80

Note: *Annualised growth

61,136.8

67,273.7

72,949.6 76,898.8

Dec 16 Sep 17

Gross Loans

CustomersDeposits

64

Table of Contents

Appendix:

1. Financial Performance 32

2. Community Financial Services 45

3. Global Banking 49

4. Maybank Singapore 53

5. Maybank Indonesia 56

6. Other segments 60

7. Affiliates 65

65

1,470.2

1,960.6

193.5 428.9

9M FY2016 9M FY2017

Revenue

PBT

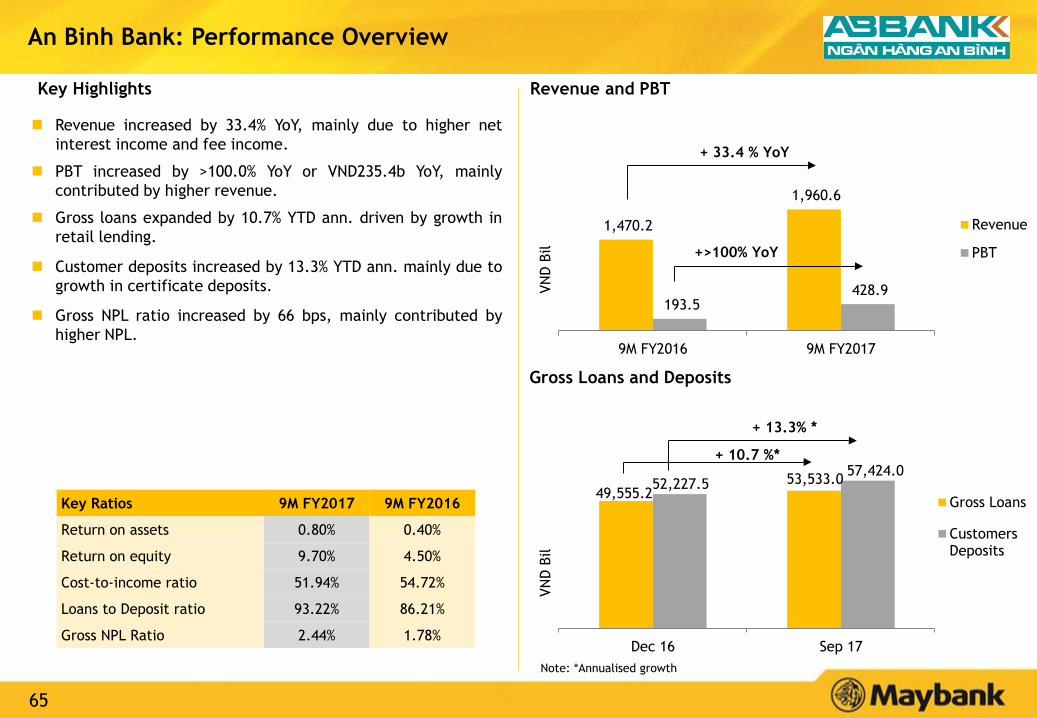

An Binh Bank: Performance Overview

Revenue increased by 33.4% YoY, mainly due to higher net

interest income and fee income.

PBT increased by >100.0% YoY or VND235.4b YoY, mainly

contributed by higher revenue.

Gross loans expanded by 10.7% YTD ann. driven by growth in

retail lending.

Customer deposits increased by 13.3% YTD ann. mainly due to

growth in certificate deposits.

Gross NPL ratio increased by 66 bps, mainly contributed by

higher NPL.

Key Ratios 9M FY2017 9M FY2016

Return on assets 0.80% 0.40%

Return on equity 9.70% 4.50%

Cost-to-income ratio 51.94% 54.72%

Loans to Deposit ratio 93.22% 86.21%

Gross NPL Ratio 2.44% 1.78%

VN

D B

ilVN

D B

il

+ 33.4 % YoY

+>100% YoY

49,555.2 53,533.0 52,227.5

57,424.0

Dec 16 Sep 17

Gross Loans

CustomersDeposits

+ 10.7 %*

+ 13.3% *

Gross Loans and Deposits

Revenue and PBTKey Highlights

Note: *Annualised growth

66

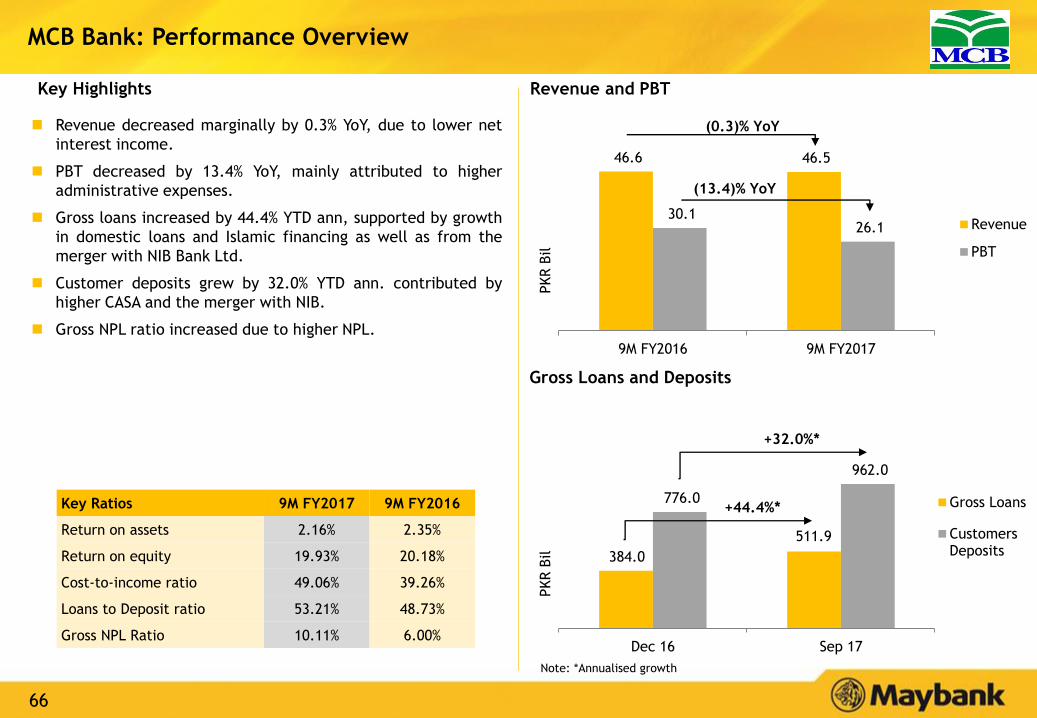

46.6 46.5

30.1 26.1

9M FY2016 9M FY2017

Revenue

PBT

MCB Bank: Performance Overview

(0.3)% YoY

(13.4)% YoY

384.0

511.9

776.0

962.0

Dec 16 Sep 17

Gross Loans

CustomersDeposits

+32.0%*

+44.4%*

PKR B

ilPKR B

il

Key Ratios 9M FY2017 9M FY2016

Return on assets 2.16% 2.35%

Return on equity 19.93% 20.18%

Cost-to-income ratio 49.06% 39.26%

Loans to Deposit ratio 53.21% 48.73%

Gross NPL Ratio 10.11% 6.00%

Gross Loans and Deposits

Revenue decreased marginally by 0.3% YoY, due to lower net

interest income.

PBT decreased by 13.4% YoY, mainly attributed to higher

administrative expenses.

Gross loans increased by 44.4% YTD ann, supported by growth

in domestic loans and Islamic financing as well as from the

merger with NIB Bank Ltd.

Customer deposits grew by 32.0% YTD ann. contributed by

higher CASA and the merger with NIB.

Gross NPL ratio increased due to higher NPL.

Revenue and PBTKey Highlights

Note: *Annualised growth

67

Dato’ Amirul Feisal Wan Zahir

Group Chief Financial Officer

Contact: (6)03-2074 7703

Email: [email protected]

MALAYAN BANKING BERHAD

14th Floor, Menara Maybank

100, Jalan Tun Perak

50050 Kuala Lumpur, Malaysia

Tel : (6)03-2070 8833

www.maybank.com

Jeeva Arulampalam

Head, Group Investor Relations

Contact: (6)03-2074 8017

Email: [email protected]

Disclaimer. This presentation has been prepared by Malayan Banking Berhad (the “Company”) for information purposes only and does not purport to contain all the

information that may be required to evaluate the Company or its financial position. No representation or warranty, express or implied, is given by or on behalf of the

Company as to the accuracy or completeness of the information or opinions contained in this presentation.

The presentation does not constitute or form part of an offer, solicitation or invitation of any offer, to buy or subscribe for any securities, nor should it or any part of

it form the basis of, or be relied in any connection with, any contract, investment decision or commitment whatsoever.

The Company does not accept any liability whatsoever for any loss howsoever arising from any use of this presentation or their contents or otherwise arising in

connection therewith.

Investor Relations Contact

Humanising Financial Services