investing and financing decisions and the balance sheet chapter 2 mcgraw-hill/irwin © 2009 the...

TRANSCRIPT

Investing and Financing Decisions Investing and Financing Decisions and the Balance Sheetand the Balance Sheet

Chapter 2

McGraw-Hill/Irwin © 2009 The McGraw-Hill Companies, Inc.

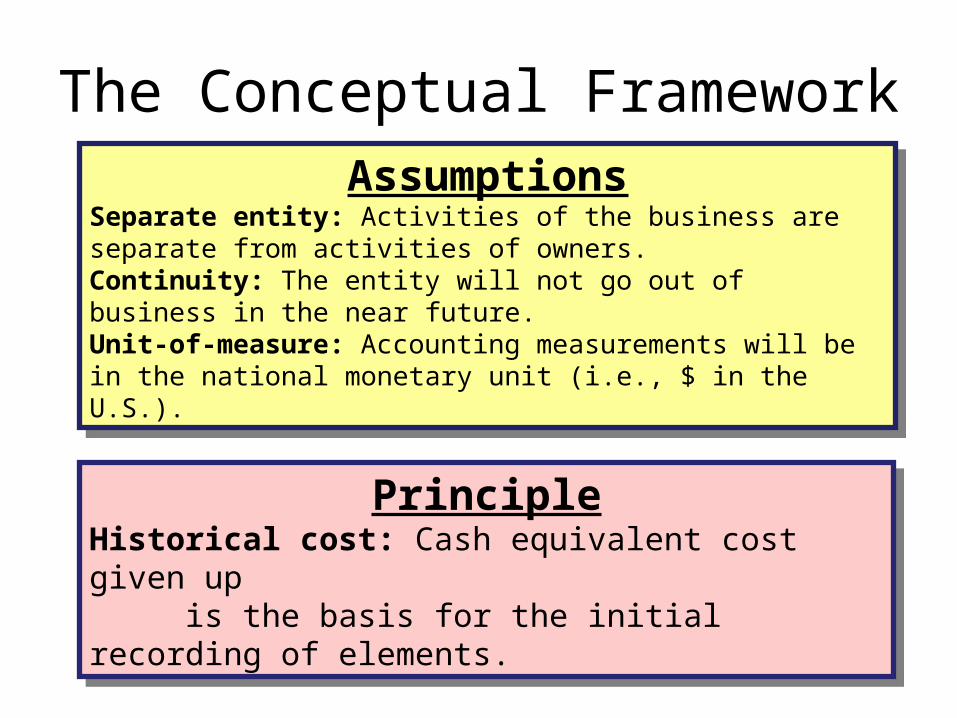

The Conceptual Framework

AssumptionsSeparate entity: Activities of the business are separate from activities of owners.Continuity: The entity will not go out of business in the near future.Unit-of-measure: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

AssumptionsSeparate entity: Activities of the business are separate from activities of owners.Continuity: The entity will not go out of business in the near future.Unit-of-measure: Accounting measurements will be in the national monetary unit (i.e., $ in the U.S.).

PrincipleHistorical cost: Cash equivalent cost given up

is the basis for the initial recording of elements.

PrincipleHistorical cost: Cash equivalent cost given up

is the basis for the initial recording of elements.

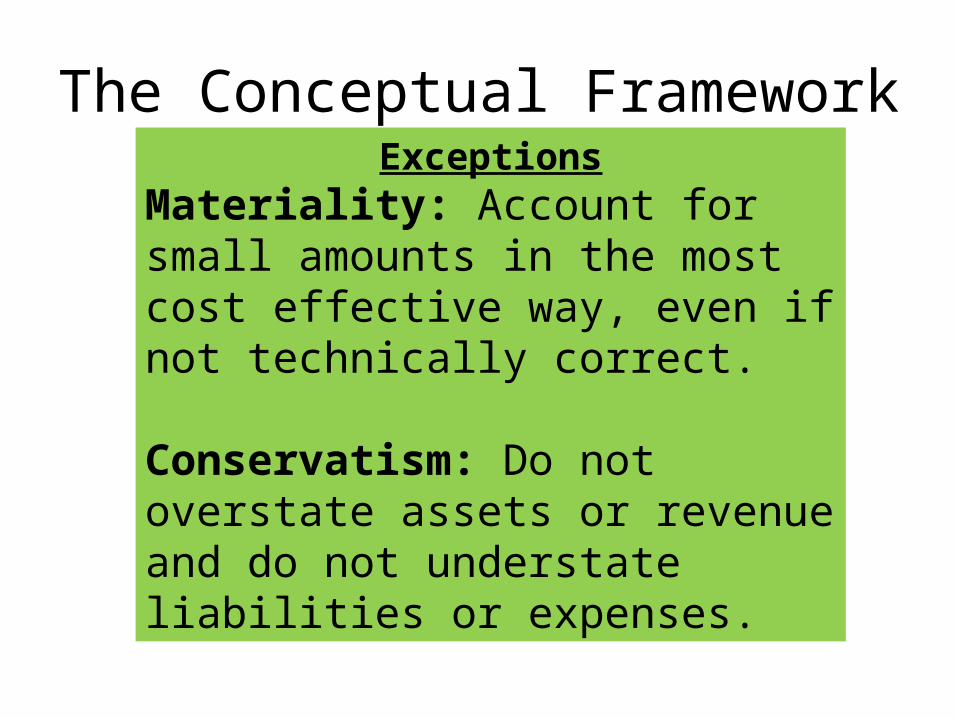

The Conceptual FrameworkExceptions

Materiality: Account for small amounts in the most cost effective way, even if not technically correct.

Conservatism: Do not overstate assets or revenue and do not understate liabilities or expenses.

Nature of Business Transactions

Most transactions with external parties involve an

exchange exchange where the business entity gives up gives up something but receivesreceives

something in return.

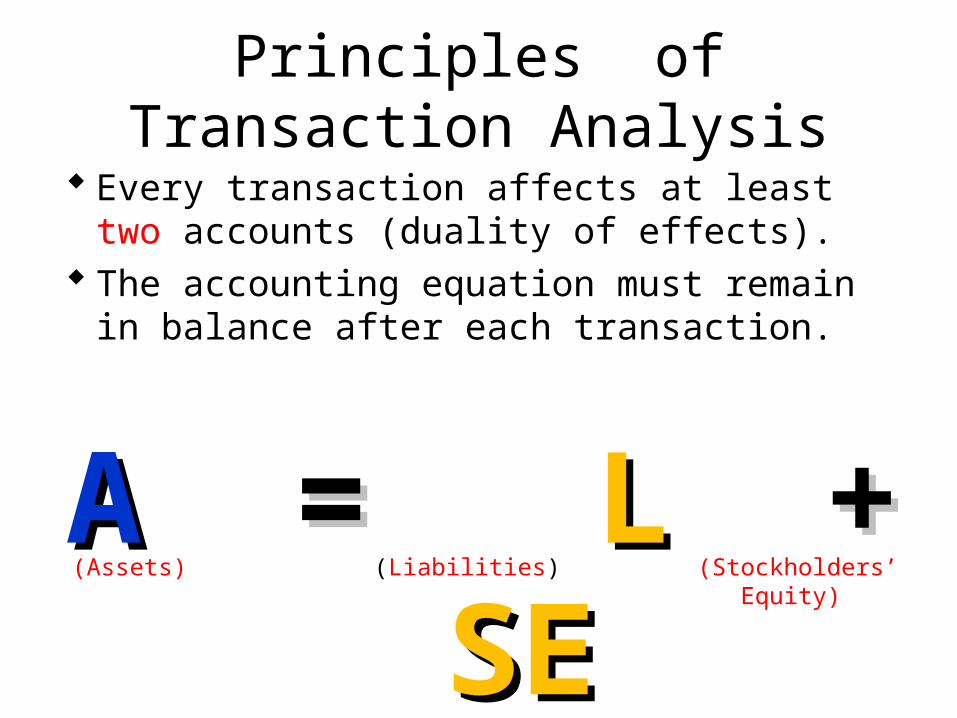

Principles of Transaction Analysis

Every transaction affects at least two accounts (duality of effects).

The accounting equation must remain in balance after each transaction.

AA = = LL + + SESE(Assets) (Liabilities) (Stockholders’ Equity)

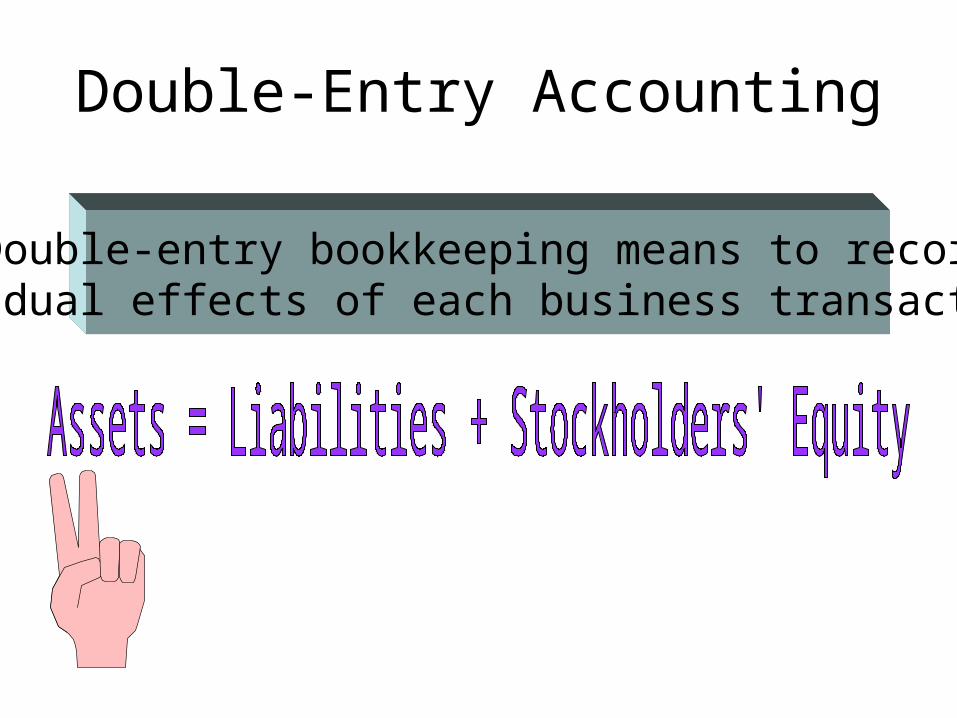

Double-Entry Accounting

Double-entry bookkeeping means to recordthe dual effects of each business transaction.

Accounting for Business Transactions

The Lyons invest $50,000 to beginthe business, and Air & Sea Travel

issues common stock.

Stockholders’ Assets = Liabilities + Equity

(1) Cash + 50,000 = + 50,000*

*Common stock

Accounting for Business Transactions

Air & Sea purchases land for anoffice location, paying $40,000 in cash.

Balance + 50,000 = + 50,000*

*Common stock

(2) Cash – 40,000 Land + 40,000

50,000 = + 50,000*

Stockholders’ Assets = Liabilities + Equity

Analytical Tool: The T-Account

Account Title

Debit

LEFT SIDE RIGHT SIDE

Credit

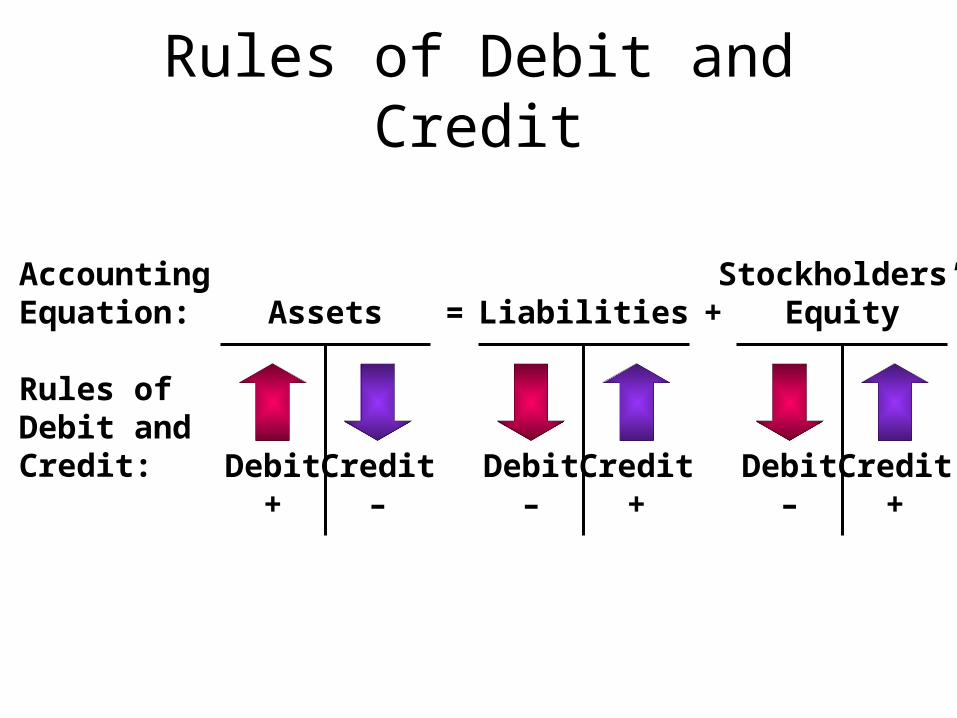

Rules of Debit and Credit

AccountingEquation: Assets = Liabilities +

Stockholders’Equity

Rules ofDebit andCredit: Debit

+Debit

–Debit

–Credit

–Credit

+Credit

+

Rules of Debit and Credit

Air & Sea received $50,000 and issued stock.

Assets = Liabilities +Stockholders’

Equity

Debitfor

Increase,50,000

Creditfor

Increase,50,000

Cash Common Stock

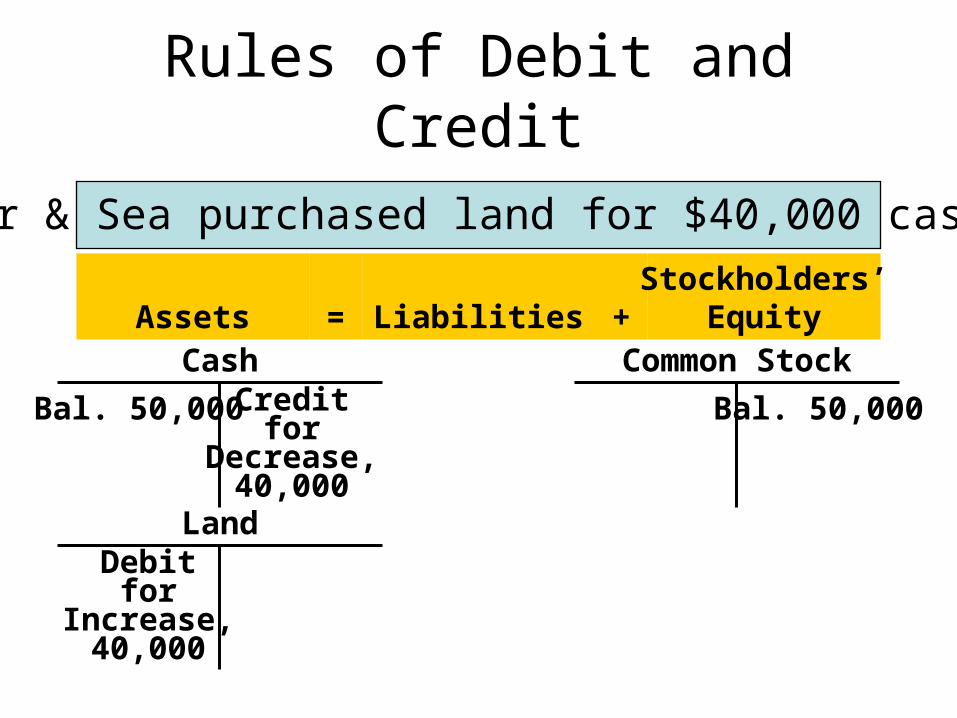

Rules of Debit and Credit

Air & Sea purchased land for $40,000 cash.

Common Stock

Bal. 50,000

CashCredit

forDecrease,

40,000

Bal. 50,000

LandDebit

forIncrease,

40,000

Assets = Liabilities +Stockholders’

Equity

The Journal Entry

A journal entry might look like this:(c) Property and Equipment (+A) 10,000

Cash (-A) 2,000 Notes Payable (+L) 8,000

To record purchase of P+E for cash and notes

Reference:Reference:Letter, Letter, number, or number, or date.date.

Reference:Reference:Letter, Letter, number, or number, or date.date.

Account Titles:Account Titles:Debited accounts on top.Debited accounts on top.Credited accounts on bottom Credited accounts on bottom usually indented.usually indented.

Account Titles:Account Titles:Debited accounts on top.Debited accounts on top.Credited accounts on bottom Credited accounts on bottom usually indented.usually indented.

Amounts:Amounts:Debited amounts on left.Debited amounts on left.Credited amounts on right.Credited amounts on right.

Amounts:Amounts:Debited amounts on left.Debited amounts on left.Credited amounts on right.Credited amounts on right.

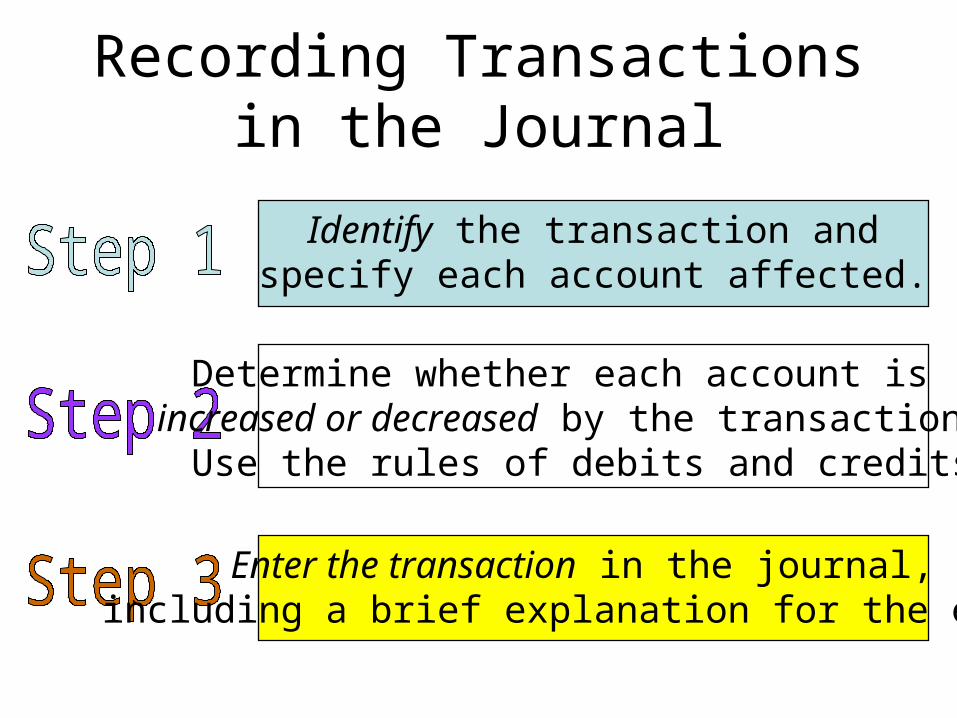

Recording Transactionsin the Journal

Identify the transaction andspecify each account affected.

Determine whether each account is increased or decreased by the transaction.

Use the rules of debits and credits.

Enter the transaction in the journal, including a brief explanation for the entry.

How Do Companies Keep Track of Account Balances?

General JournalGeneral JournalGeneral JournalGeneral Journal

General LedgerGeneral Ledger

PostLedger

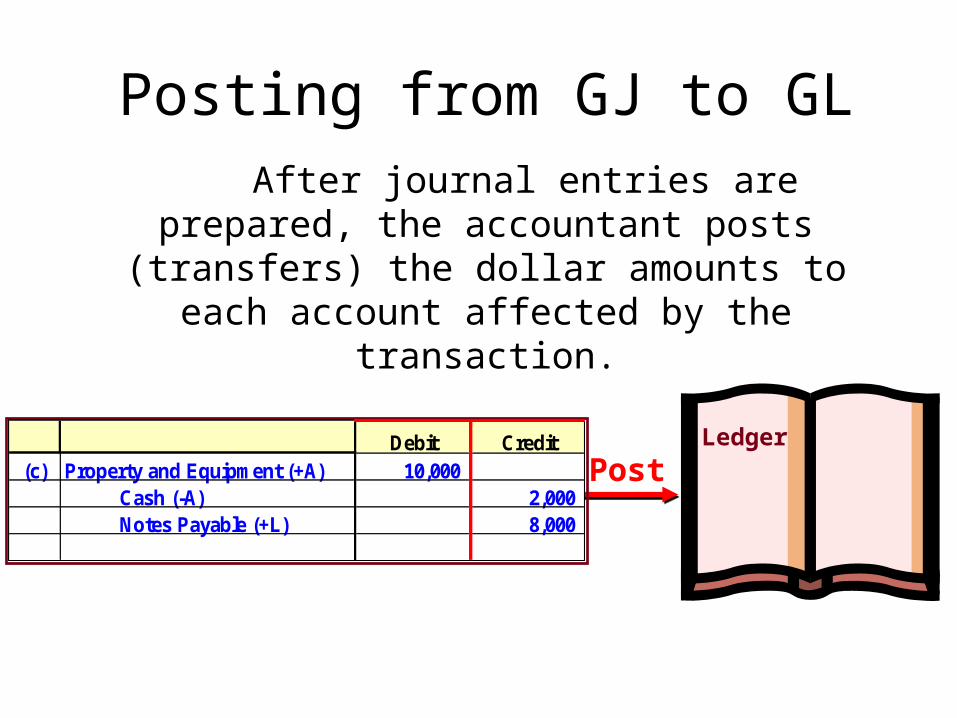

Posting from GJ to GL

After journal entries are prepared, the accountant posts (transfers) the dollar amounts to each account affected by

the transaction.

Debit Credit(c) Property and Equipment (+A) 10,000

Cash (-A) 2,000 Notes Payable (+L) 8,000

Key Ratio Analysis

CurrentRatio

Current AssetsCurrent Liabilities

=

The 2011 current ratio for Chipotle:The 2011 current ratio for Chipotle:

The current ratio for Chipotle shows a high level of liquidity, well above 1.0, and the ratio has varied slightly around the 3.1 level since 2009. Chipotle has high growth strategies requiring cash to fund expansion.

$501,200$157,500

= 3.182

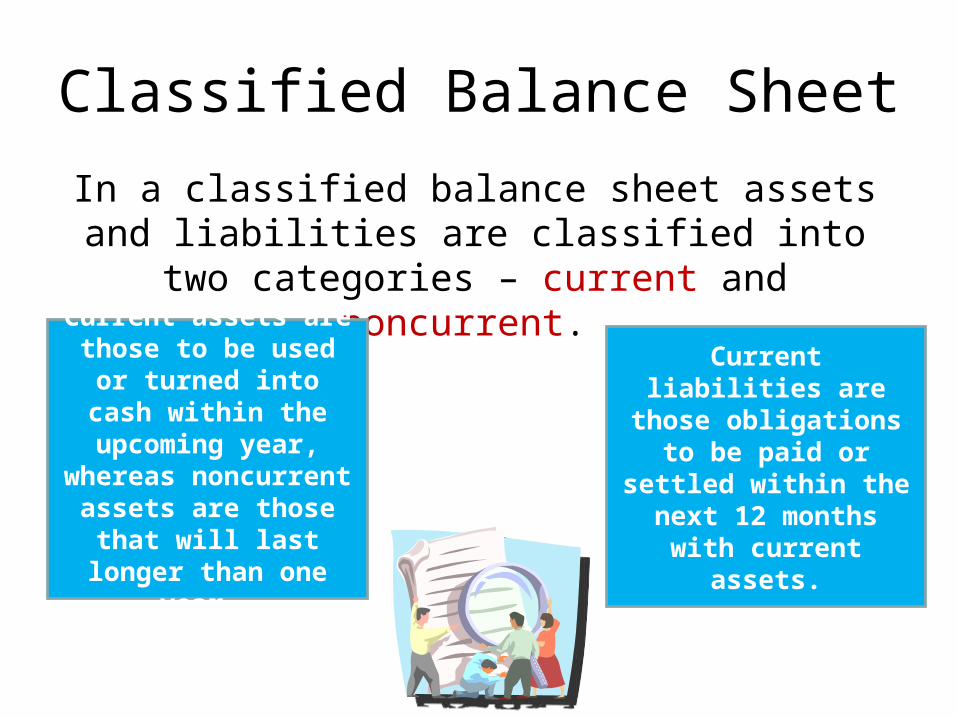

Classified Balance Sheet

In a classified balance sheet assets and liabilities are classified into two categories – current and

noncurrent.

Current assets are those to be used or

turned into cash within the upcoming year, whereas noncurrent assets are those that will last longer than

one year.

Current liabilities are those obligations to be paid or settled within the next 12 months with current assets.

k

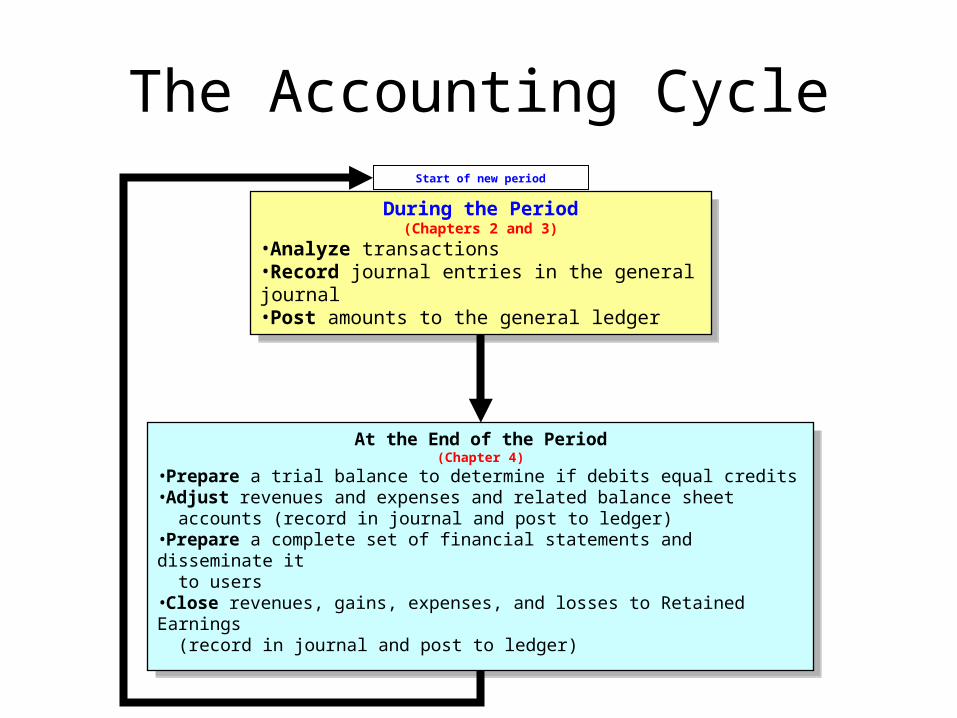

The Accounting Cycle

During the Period(Chapters 2 and 3)

•Analyze transactions•Record journal entries in the general journal•Post amounts to the general ledger

During the Period(Chapters 2 and 3)

•Analyze transactions•Record journal entries in the general journal•Post amounts to the general ledger

Start of new period

At the End of the Period(Chapter 4)

•Prepare a trial balance to determine if debits equal credits•Adjust revenues and expenses and related balance sheet accounts (record in journal and post to ledger) •Prepare a complete set of financial statements and disseminate it to users•Close revenues, gains, expenses, and losses to Retained Earnings (record in journal and post to ledger)

At the End of the Period(Chapter 4)

•Prepare a trial balance to determine if debits equal credits•Adjust revenues and expenses and related balance sheet accounts (record in journal and post to ledger) •Prepare a complete set of financial statements and disseminate it to users•Close revenues, gains, expenses, and losses to Retained Earnings (record in journal and post to ledger)

Focus on Cash Flows

Operating activities (Covered in the next chapter.)Investing Activities Purchasing long-term assets and investments for cash – Selling long-term assets and investments for cash + Lending cash to others – Receiving principal payments on loans made to others +Financing Activities Borrowing cash from banks + Repaying the principal on borrowings from banks – Issuing stock for cash + Repurchasing stock with cash – Paying cash dividends –

Companies report cash inflows and outflows over a period in their statement of cash flows.

End of Chapter 2