investing for generations - alliance trust · investing for generations. ... portfolios having only...

TRANSCRIPT

Alliance Trust PLCAnnual Report for the year ended 31 December 2016

Investing for Generations

*as rated by Willis Towers Watson (WTW)

Section I

Strategic Report 1The Year in Review 12016 Strategic Review 2Our New Business Model 5Investment Objective and Policy 5Chairman’s Statement 6Board Strategy Q&A 8Key Performance Indicators 10Investment Manager’s Report 11Non-core Investments 15Contribution Analysis 15Alliance Trust Investments 16Alliance Trust Savings 17Portfolio Listing 18Costs and Financial Measures 20Risk Management 22Corporate Responsibility 25

Section II

Directors’ Report 26Board of Directors 26Corporate Governance 28Board Evaluation 30Management Engagement Committee 31Nomination Committee 32Audit and Risk Committee 33Going Concern Statement 37Viability Statement 37Remuneration Committee 38Other Governance 45

Section III

Financial Statements 48Independent Auditors’ Report 48Consolidated income statement 54Consolidated statement of comprehensive income 54Company income statement 55Company statement of comprehensive income 55Statement of changes in equity 56Balance sheet 57Cash flow statement 58Notes 59

Information for shareholders 91 10 year record 93

www.alliancetrust.co.uk

Alliance Trust has been investing for generations since 1888. It provided access to scarce and compelling investment opportunities then and continues to build on this heritage today.

Following a Strategic Review, the Directors concluded that the optimum way to deliver an unchanged objective – generating a real return through capital and dividend growth – is to invest with a selection of the world’s best-in-class* global equity managers. Each of these managers will build a portfolio of only their best stock selections – the ‘best of the best’. The Board believes this approach is in the best interests of shareholders, whether investing for this generation or the next.

Investing for Generations

Alliance Trust PLC | Annual Report and Financial Accounts 2016

1

I Strategic Report IIIII

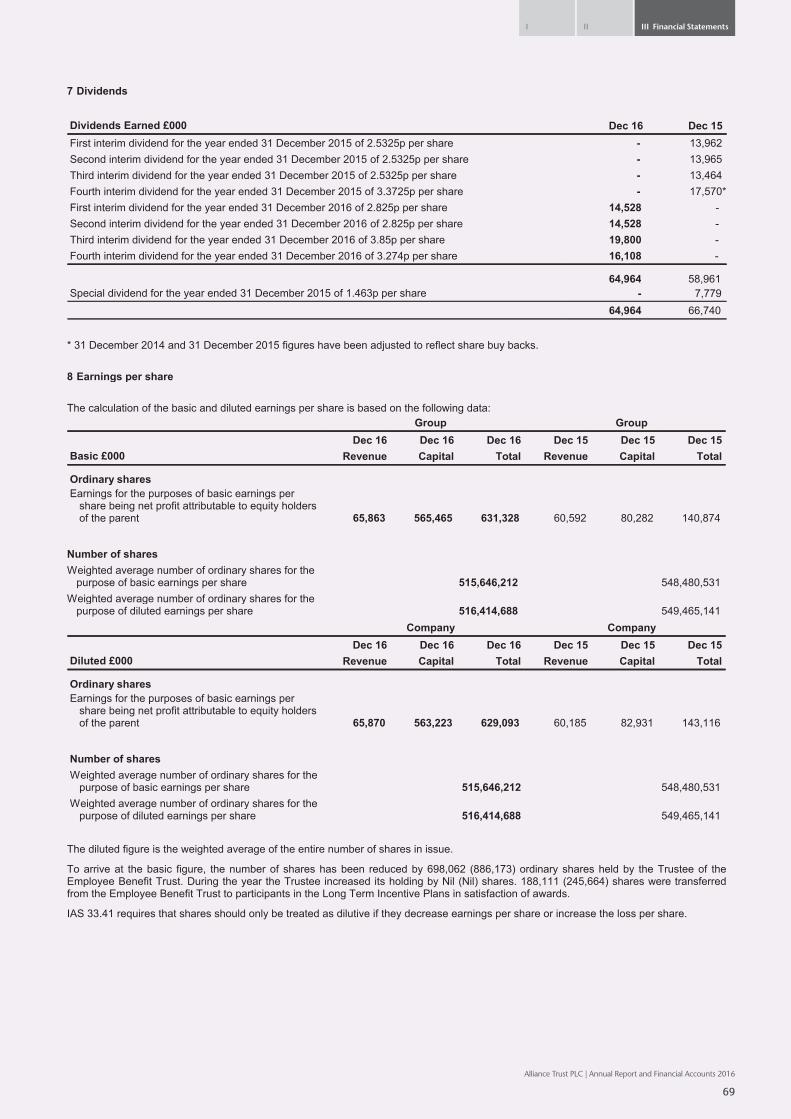

638.

0

517.

0

478.

9

450.

1

375.

3

2012 2013 2014 2015 2016

667.

5

559.

0

544.

8

516.

5

444.

9

2012* 2013* 2014* 2015* 2016*

0.43

0.59

0.60

0.75

0.67

2012 2013 2014 2015 2016

*with debt at fair valueSource: Factset Source: Factset Source: Alliance Trust

Strategic developments

The Year in Review

Financial highlights

667.5p638.0p 0.43%Net asset value (pence)*Share price (pence) Ongoing charges ratio (%)

Shareholders voted in favour of the new investment approach at our recent General Meeting. Key elements of this approach, in the process of being implemented, include:

• Alliance Trust to remain a global equity investment trust offering returns through capital and income growth over the medium to long term

• Target for our equity portfolio to outperform MSCI All Country World Index doubled from 1% to 2% p.a., net of costs, over rolling three-year periods

• Seeking outperformance at a competitive cost, below 0.65%• A new approach adopted for our investment management to increase the likelihood of

delivering consistently the enhanced performance target• Aim to build on Alliance Trust’s 50-year track record of year-on-year ordinary dividend growth• Move from a single manager to multiple equity managers, each rated ‘best-in-class’ by WTW• All of the managers to focus on high conviction stock selection with almost all of their

portfolios having only 20 stocks• An active programme of share buybacks introduced with the aim of achieving a significantly

narrower discount

Read about the Strategic Review in full on page 2

+23% +19%

Alliance Trust PLC | Annual Report and Financial Accounts 2016

2

Strategic Report

2016 Strategic Review

Since May 2016, the Board has engaged with shareholders and evaluated carefully a broad range of options, with an open mind on how best we could improve the Trust’s performance. We are confident that the approach resulting from this Review will improve Alliance Trust’s performance on a consistent basis.

Existing objectives

Investing for this generation and the next

Policy of progressive dividends

Commitment to narrow the discount

Providing good value

Simplifying our structure

Clear investment mandate to improve performance

Alliance Trust PLC | Annual Report and Financial Accounts 2016

3

I Strategic Report IIIII

Developments resulting from the Review

A new approach to investment management to be adopted to increase the likelihood of delivering consistently the performance target:

• Move from a single manager to multiple equity managers, each rated ‘best-in-class’ by WTW

• Each equity manager to create a focused portfolio of their top investment selections (more detail of this approach can be found on the next page)

• Equity portfolio outperformance target doubled to 2% p.a. net of costs over rolling three-year periods

• The Board reaffirms its commitment to its progressive dividend policy

• Aiming to build on Alliance Trust’s 50-year track record of year-on-year ordinary dividend growth

• An active programme of share buybacks has been introduced with the aim of achieving a significantly narrower discount reflecting the Board’s determination to narrow materially the discount

• Since announcing this programme the discount has reduced to below 5% and has been around this level since the end of 2016

• Increased value: the previous equity portfolio’s outperformance target above the MSCI All Country World Index (‘ACWI’) was 1% net of 0.45% ongoing costs increased to 2% outperformance with ongoing costs below 0.65% over rolling three-year periods

• The Board is setting a target of total annual costs of under 0.65% which is below the median for the investment trusts in the AIC global sector

• Alliance Trust Investments to be sold to Liontrust Asset Management PLC representing an expected gain of over £5m from its valuation at 30 June 2016

• Alliance Trust Savings continues to make good progress and remains part of the Group; it has reported a profit in 2016 and is well placed to develop further

Alliance Trust PLC | Annual Report and Financial Accounts 2016

4

Strategic Report

The Investment Manager

The Equity Managers

2016 Strategic Review continued

Blackcreek Investment ManagementBill Kanko is founder and President. Between 1999 and 2004 Bill was the lead manager for the AIM Trimark Fund and Trimark Select Growth Fund which had outstanding performance during that time.

Bill is a long-term investor, looking for companies that are growing, are leaders in their markets and gaining market share. These companies tend to benefit from huge barriers to entry and sustainable competitive advantages.

First Pacific AdvisersPierre Py and Greg Herr are co-portfolio managers with an average of 20 years investing experience.

Pierre and Greg typically employ a long-term value investment approach, investing in companies that they believe have sustainable business models, exhibit financial strength, are run by operationally strong managers and whose stocks trade at a significant discount to the FPA team’s estimate of intrinsic value.

GQG PartnersRajiv Jain founded GQG Partners in June 2016, having previously worked at Vontobel Asset Management for 22 years as lead portfolio manager, Head of Equities, CIO and Co-CEO, responsible for over £30bn of assets.

Rajiv looks for high-quality and sustainable businesses through a fundamental investment process utilising both traditional and non-traditional sources of information. Ideally, these quality businesses have enduring underlying strengths, which manifest in a variety of economic environments. The result has been portfolios designed to provide capital protection in down markets and attractive returns to long-term investors over a full market cycle. In addition, GQG will manage a global portfolio for the Company with particular focus on emerging market companies.

Jupiter Asset ManagementBen Whitmore has over 20 years of experience and joined Jupiter in 2006. Ben worked at Schroders, managing both retail and institutional portfolios and around £2 billion of assets. Ben will be supported by Dermot Murphy, Assistant Fund Manager.

Ben is well known as a long-standing practitioner of contrarian value investing, investing in companies he considers to be out-of-favour and under-valued. This approach has proved successful, with the Jupiter UK Special Situations Fund being top quartile in its sector over one, three, five and ten years.

Lyrical Asset ManagementLyrical Asset Management’s investment management team is led by Co-Founder and Chief Investment Officer, Andrew Wellington.

Value matters most to Lyrical and the team also maintains a strict discipline of investing in quality companies that they believe are relatively easy to analyse. They believe the combination of value, quality and straightforward business model creates resiliency in the portfolio and the greatest likelihood of long-term absolute performance and outperformance.

River and Mercantile Asset ManagementHugh Sergeant is the CIO of Equities having previously been in a similar role at Societe Generale Asset Management (‘SGAM’) and prior to that at UBS/Phillips & Drew and Gartmore.

The team invests in Recovery Equities, through an investment philosophy called PVT (Potential, Valuation & Timing) and a process that helps them identify value at different stages of a company’s lifecycle and to give signals from a timing perspective as to when that value might be unlocked.

Sustainable Growth AdvisersSGA was founded in 2003 by George Fraise, Gordon Marchand and Rob Rohn. They average over 30 years of investment experience.

SGA focuses on building concentrated portfolios of unique, high quality global growth businesses that possess strong pricing power, offer recurring revenue generation and benefit from attractive, long runways of growth.

Veritas Asset ManagementAndy Headley is Head of Global strategies at Veritas Asset Management. Andy has over 20 years investment experience and is supported by Charles Richardson, co-portfolio manager who has 30 years’ experience.

Veritas focuses on active equity management, utilising its proprietary Real Return Approach since inception of the firm. Veritas employs an absolute mind-set when valuing companies and dispenses with any reference to indices when constructing the portfolio. Veritas describes the firm’s overall approach as investing in a concentrated portfolio of good quality companies at the right price.

Willis Towers WatsonWillis Towers Watson is a leading investment group that is focused on creating financial value for investors through its expertise in risk assessment, strategic asset allocation, manager evaluation and investment management. It has over 900 investment associates worldwide, assets under advisory of around US$2.3 trillion and over US$87 billion of assets under management. It is part of Willis Towers Watson (NASDAQ: WLTW) which has over 39,000 employees in more than 120 territories and has roots dating to 1828.

They have worked, for many years, with equity managers to create tailored high-conviction portfolios for large institutional clients, with notable success over more than ten years for a large charitable foundation. More recently it launched an open-ended, high-conviction multi-manager vehicle for institutional investors, the Global Equity Focus Fund, which has outperformed its benchmark by 2.2% per annum net of underlying managers’ fees since the fund’s inception on 17 August 2015 to 28 February 2017.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

5

I Strategic Report IIIII

Invest in:

• Global equities

We have investments in:• Our subsidiary business – Alliance Trust Savings• Non-core investments*

– Mineral Rights – Private Equity – Funds

*These will be disposed of at the appropriate time

How we will do it• A multiple manager approach, each rated best-in-class by WTW with oversight by them• Each equity manager creates its own focused portfolio of its top investment selections• Equity portfolio outperformance target of the MSCI All Country World Index by 2% p.a. net of costs over rolling three-year periods• One of only four FTSE All-Share Index companies with a record of increasing their ordinary dividend for the last 50 years.

How we create an attractive return for our shareholders• Capital growth in our investment portfolio

• Progressive income growth funded by dividends and income received from our investments

• Competitive costs

Global equities Subsidiary entities Non-core investments

Focused on equities

What we will do

Our New Business Model

Investment Objective and Policy

Alliance Trust is an investment company with investment trust status. The Company’s objective is to be a core investment for investors seeking increasing value over the long term. The Company has no fixed asset allocation benchmark and it invests in a wide range of asset classes throughout the world to achieve its objective. The Company’s focus is to generate a real return for shareholders over the medium to long term by a combination of capital growth and a rising dividend.

The Company pursues its objective by investing in both quoted and unquoted equities across the globe in different sectors and industries; investing internationally in fixed income securities; investing in other asset classes and financial instruments, either directly or through investment vehicles and investing in subsidiaries and associated businesses which allow us to expand into other related activities.

The Company is prepared to invest any proportion of the total corporate capital in any of the above asset classes, subject only to the restrictions imposed on the Company by the regulatory or fiscal regime within which we operate. However, the Company would expect equities to comprise at least 50% of its portfolio. Changes to the asset allocation will be dependent upon attractive investment opportunities being available.

Where market conditions permit, the Company will use gearing of not more than 30% of its net assets at any given time. The Company can use derivative instruments to hedge, enhance and protect positions, including currency exposures.

The existing Investment Objective and Policy allows the Board to pursue the new investment approach.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

6

Strategic Report

During 2016 the Board spent a great deal of time consulting with shareholders on the future of Alliance Trust and what investors really wanted from their investment in the Trust. We evaluated a broad range of options to decide on the best way to improve the Trust’s performance and to position the Trust as a core holding for investors.

As I have commented before, it was clear that the appetite for a global equity investment trust remained strong, but that change was required to better differentiate Alliance Trust’s investment proposition and to improve performance.

Looking ahead, the Board and the new investment manager will now focus on delivering real returns for shareholders through a combination of capital growth and a rising dividend.

Strategic ReviewWith the aim of building on the progress achieved following last year’s AGM, the Board announced in May 2016 that it would conduct a Strategic Review of the Trust. As part of this, we assessed the potential courses of further action open to the Trust and the best way forward. On 15 December 2016, the Board announced the outcome of its review and set out a proposed new approach to managing the Trust’s equity portfolio.

This will see the adoption of a high conviction, multi-manager approach overseen by Willis Towers Watson (WTW), a leading investment group, targeting outperformance of the MSCI All Country World Index by 2% per annum, net of costs, over rolling three-year periods. WTW will be the overall investment manager of the Trust’s equity portfolio, providing access to and selecting and managing the sub-managers who in turn will create concentrated portfolios for the Trust. By leveraging the scale of Alliance Trust and WTW, total annual costs will also be targeted to be below 0.65%. This is highly competitive for an investment trust targeting such outperformance.

The aim of the new approach is to:

• deliver consistently the outperformance target, which has been doubled;

• maintain our long track record of growing dividends; and

• maintain the Trust’s competitive cost ratio.

Whilst it was not required, the Board wanted to provide shareholders with the opportunity to vote on the new approach to investment. We were delighted with the strong support at the General Meeting in February 2017 when over 96% of the votes cast by shareholders favoured the change. The transition to the new portfolio is well underway and I look forward to telling you more about this at our AGM in April, when WTW will also make a presentation.

Chairman’s Statement

We care about the long-term interests of all of our shareholders

Alliance Trust PLC | Annual Report and Financial Accounts 2016

7

I Strategic Report IIIII

During 2016 Alliance Trust Investments (ATI) made good progress. An independent Board was established, third-party funds under management increased, costs were reduced and the business recorded a profit for the year. As part of the Strategic Review, the Board reached agreement to sell ATI to Liontrust Asset Management PLC, a specialist independent fund management group. This transaction is expected to complete in April. As a result, Alliance Trust’s structure will be simplified and ATI will be provided with an exciting opportunity to continue to develop its third party fund management business.

Alliance Trust Savings also made significant progress during the last year and remains part of the Group, headquartered in Dundee. Assets under administration have grown by 60%, reflecting the benefit of the Stocktrade acquisition. In the year ended December 2016 ATS achieved a profit before tax of £1.2m, compared to a loss of £5.2m in the prior year.

When we announced the outcome of the Strategic Review, we introduced a more active approach to share buybacks, reflecting our determination to narrow the Trust’s discount to Net Asset Value (NAV). This has helped to narrow the discount to 4.4% as at the end of December 2016. We also announced in January 2017 that the Board had reached agreement with Elliott, the Company’s largest shareholder, to repurchase the shares in which it had a disclosable interest (approximately 20% of the issued share capital as at December 2016). Given the size of its shareholding Elliott was unable to participate in the share buyback programme without obtaining the approval of other, independent shareholders. This approval was granted at the General Meeting in February and the repurchase of Elliott’s shares has now been completed. The impact of this repurchase has been an uplift in the NAV for other shareholders of around 1%, as well as the removal of a share overhang, allowing the Trust to move forward with a more stable shareholder register.

Performance in 2016Over 2016 the Trust delivered a Total Shareholder Return of 26.4% and a NAV Total Return of 21.5%. The Trust’s share price rose 23% to 638p, while the NAV increased 19% to 667.5p, resulting in a discount at the year-end of 4.4%. The Equity portfolio underperformed the benchmark, which returned 29.4%, primarily through stock selection. The Board is delighted that the Trust has achieved 50 years of consecutive dividend growth, with a total declared dividend for the year of 12.774p per ordinary share.

As regards our objective to reduce costs, we fulfilled our commitment to reduce the OCR, which stood at 0.43% at the end of the year, below our target of 0.45%. This reflects the level of cost we expected under the old investment management approach. Going forward we will see this increasing to just under 0.65% which we believe provides excellent value for the targeted level of outperformance.

Significant Event During the year the Board received an unsolicited approach from RIT Capital Partners plc (RIT) with an informal proposal for a merger of the two companies. No detailed terms were provided by RIT with regard to the proposal. The Board of Alliance Trust announced that it would incorporate any formal merger proposal received from RIT into its Strategic Review, alongside the other options being considered. RIT subsequently withdrew their interest.

Board ChangesSince my appointment as Chairman last year there have been three changes to the Board. Following the conclusion of the AGM held in 2016, John Hylands retired as a Director of the Company. I would like to thank John for his contribution and consistent support to the Company over nine years.

In May, we welcomed Clare Dobie to the Board. Clare, who has had a successful career in marketing and client service in asset management companies, has made an excellent contribution to our Strategic Review.

Finally, and very sadly, Rory Macnamara passed away on 17 December 2016 after a period of illness. Rory, who joined the Board in June 2015, played a significant role during the Strategic Review.

The last two years have seen considerable change for Alliance Trust and we are very appreciative of the high level of support shareholders have shown. I am also extremely grateful for the commitment and diligence with which all of my fellow Directors have set about the task to establish a compelling and refreshed strategy for the Trust. With a clear course of direction and a settled shareholder register, we believe that Alliance Trust is well placed for the future.

Lord Smith of KelvinChairman

Alliance Trust PLC | Annual Report and Financial Accounts 2016

8

Strategic Report

Board Strategy Q&A

We met with hundreds of our shareholders to explain, and answer questions on, the changes we are making. Here are some of the questions that were asked and answered during these meetings.

Q Who are Willis Towers Watson?

A WTW is a leading investment group. The investment business at Willis Towers Watson has global assets under advice of more

than US$2.3 trillion and assets under management of more than US$87bn. Willis Towers Watson’s clients include some of the largest and most sophisticated investors in the world including pension funds, sovereign wealth funds, endowments and foundations.

Q How did you choose WTW as your investment manager?

A The Board ran a competitive process and WTW was selected to become the investment manager, as announced on 15th

December 2016.

Q What experience do Willis Towers Watson have of managing multi‐manager equity portfolios?

A For more than 20 years WTW has provided advice on the management of equity portfolios to large sophisticated

investors and has had a key role to play in managing multi‐manager portfolios for more than a decade.

Q How will the Trust’s portfolio be designed?

A It is anticipated that the Trust’s portfolio will have approximately 200 stocks held across the eight underlying equity managers.

The Company’s equity portfolio will be shared broadly equally between the eight equity managers. WTW believes that the combination of these managers’ best stock ideas will create a highly compelling equity portfolio for the Trust, where the long-term return relative to benchmark will be primarily driven by stock selection rather than macroeconomic factors.

Q What is the benefit of this approach?

A The underlying investment managers are chosen for their skill as stock pickers. Through asking each manager to focus on their

highest conviction ideas, we gain exposure to only the best ideas from each manager. This is achieved without increasing overall risk through the diversification of using multiple managers with different approaches to investing that are expected to perform differently in various market environments.

Q By moving to a multi‐ manager approach are you not moving the portfolio closer to the index and hence reducing the expected outperformance?

A Although the number of stocks in the overall portfolio increases from around 60 to around 200 (and hence the stock specific risk

reduces), every single stock is now one of the managers’ very best ideas, which is not possible in a single manager approach, where a number of stocks are inevitably held for risk control purposes.

Q What would cause you to review a manager?

A The most likely reason to replace a manager is if the research or portfolio management team feels that the skill of the manager

has eroded over time. This could be in an absolute sense or relative to other managers that would be suitable for inclusion in the portfolio. It is unlikely that poor performance, on its own, would be a reason for removing a manager except if that poor performance was caused by reduced skill from the manager. Poor performance (relative to a benchmark) that is attributable to style, size or sector weightings that were known features of the investment approach would not necessarily change our view of the manager’s skill.

The other reason a manager could be replaced is an inability to meet the terms of the mandate such as maintaining a very high level of active share and the restricted number of stocks. It is possible that we will be able to identify managers who combine better with the other managers in the portfolio than one initially chosen and therefore the portfolio management team may make changes for this reason.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

9

I Strategic Report IIIII

Q Can you describe how the multi‐manager portfolio will be built:

A The portfolio can be thought of as being the result of two complementary components. The assets are all managed

by a group of focused active equity managers with varying styles. In addition there is risk control, oversight, manager selection, operational due diligence and monitoring performed by WTW.

The first component is a group of highly active (active share typically 90%+) concentrated, ‘best‐in‐class’, active equity managers. Each underlying portfolio usually has a named lead portfolio manager overseeing a portfolio of around 20 of their best equity ideas.

The second component is used to balance the risks within the active managers’ portfolios. It is the role of WTW to source appropriate managers from around the world, look at their risk and return characteristics and how they can be combined to minimise risks that can be diversified away whilst maximising the impact of the stock selection skills of the managers.

Q Why use concentrated mandates?

A There is significant evidence supporting better returns from concentrated mandates over more diversified portfolios.

Research supports the view that over 90% of risk associated with individual stocks is diversified away within the first 20‐30 holdings and there is little incremental benefit beyond this.

Q Will the managers have track records and does the strategy?

A All the portfolio managers selected for the Trust have long, successful track records at either their existing or previous asset

management firms. The managers’ track records and the quality of their investment approach is examined as part of the rating process conducted by WTW. The vast majority of the managers have also managed concentrated mandates similar to those intended for Alliance Trust, in many cases only for WTW clients.

Q How many stocks will be in the portfolio?

A Up to 200 stocks will be contained in the portfolio. The developed market managers typically have around 20 holdings each and

one manager also manages a dedicated emerging markets mandate which can hold up to 50 stocks.

Q What will be the target level of performance and risk of the Trust?

A The Trust is targeting 2% p.a. outperformance for the equity portfolio over the MSCI World ACWI, net of fees, over three year

rolling periods. The forecast tracking error of the Trust is expected to be 2‐4% (a guide, not a limit).

Q What will be the target yield on the portfolio and the dividend policy?

A The underlying yield on the stocks in the current proposed multi‐manager portfolio is roughly the same as the existing

portfolio. This leaves the strategy well placed to support the existing level of dividend payments and to continue the record of 50 years of consecutive dividend growth into the future.

Q What will be the target total annual costs of the Trust and how does this break down?

A The Trust’s OCR will be targeted to be below 0.65%. The fees payable to WTW are detailed on page 46.

Q Is the Trust intended to invest in developed or emerging markets?

A The Trust is benchmarked against the MSCI ACWI (an index that covers both developed and emerging markets). Each manager is

allowed to invest across both developed and emerging markets within their 20 stock portfolio, but one manager also has a specialist emerging market mandate which may have around 50 stocks.

Q What level of manager turnover is expected?

A A 10‐15% per annum manager turnover could be expected as a long‐term guide.

Q What level of portfolio turnover is expected in the sub‐manager’s underlying portfolios?

A Overall we would expect average turnover to be in the range 20% to 40% per annum.

Q What will be the approach to gearing?

A The approach is unchanged. The Board is ultimately responsible for setting the strategic level of gearing and WTW will then have

an element of discretion around this target.

We would not anticipate the level of gearing changing at all at the time of transition to the new arrangements.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

10

Strategic Report

0.60

0.59

0.43

2014 2015 2016

2.55

1.46

12.8

2014 2015 2016

12.3

8

12.4

3

12.7

7412

.774

10.9

7

9.832014* 2015* 2016*

12.1

7.5

4.45.

6

4.6

4.6

1 Year 3 Year 5 Year

26.4

53.1

111.

1

29.4

49.5

102.

2

1 Year* 3 Year* 5 Year*

21.5

38.3

83.4

29.4

49.5

102.

2

1 Year 3 Year 5 Year

22.9

36.9

88.5

29.4

49.5

102.

2

Key Performance Indicators – 2016

Our Key Performance Indicators measure how well we are achieving our objectives of capital and income growth, investment performance and a narrowing discount.

This demonstrates the real return our shareholders receive through dividends paid and capital growth.

Why this is important

Total Shareholder Return (%)

Why this is important

This demonstrates the growth of our total portfolio including non-core investments. *NAV calculated with debt at fair value.

NAV* Total Return (%)

Read more in the Investment Manager’s Report on page 11

This measures how our equity portfolio investment managers perform. The equity portfolio accounted for 93% of our net asset value at the year end.

The figures shown are the total dividends paid, ordinary and special dividends.

This is the cost of running the Company as a percentage of the average net assets of the Trust. It is an indicator of how efficiently the Company is managed.

Why this is important

Why this is importantWhy this is important

Equity Portfolio Total Return (%)

Total Dividend (pence) year to 31 Dec

Ongoing Charges Ratio (%) as at 31 Dec

Why this is important

This is the difference between the share price of the Company and its net asset value and is an indicator of demand for our shares.

*Discount calculated using debt at fair value.

Discount* (%) as at 31 Dec

Read more in Costs and Financial Measures on page 20

Read more in Costs and Financial Measures on page 20

Read more in the Investment Manager’s Report on page 11

Read more in Costs and Financial Measures on page 20

Read more in the Investment Manager’s Report on page 11

Global sector Weighted Average Alliance Trust

MSCI ACWI Alliance Trust MSCI ACWI Alliance Trust MSCI ACWI Alliance Trust

Ordinary Dividend Special Dividend

Alliance Trust PLC | Annual Report and Financial Accounts 2016

11

I Strategic Report IIIII

Investment Manager’s Report – 2016

SummaryDuring 2016, the Trust’s equity portfolio delivered a Total Return of 22.9%. Taking into account the performance of non-core investments, the impact of buybacks and a one-off contribution to the pension scheme the Trust’s overall NAV Total Return was 21.5%. The Total Shareholder Return, which takes account of discount narrowing, was 26.4%.

The equity portfolio finished the year 6.5% behind the MSCI ACWI. This was driven largely by stock selection although sectoral allocation also contributed to the lag in performance. In the latter half of the year mid- and small-cap value stocks outperformed the larger, quality growth companies that constitute the Trust’s portfolio.

The investment team maintained the number of holdings within the portfolio to around 60, reflecting our continued conviction in the benefits of holding a portfolio of best-in-class global companies.

Review of PerformanceAfter a turbulent start to the year share prices rebounded in February as fears of a Chinese hard landing and a US industrial slow down faded. Despite some significant shocks to financial markets, such as Brexit, markets continued to make progress, driven by increasing signs of self-sustaining global growth and continued monetary laxity.

Over the year our decisions to increase our weightings in Industrials and remain overweight in Technology benefited performance. However, our decisions to improve the quality of holdings in Financials and Energy in 2015 did not continue to provide the uplift in performance achieved that year as lower quality companies rebounded strongly in 2016, outperforming our stock selections. The most important sectoral decision we got wrong in 2016 was to remain overweight in Health Care ahead of the US elections, during which investor concerns over the sustainability of drug pricing increased.

Industrials were the strongest contributor to performance in 2016. We increased our exposure to these stocks, ending the year overweight against the index. The star performers were Daikin and Melrose.

Information Technology was also a positive contributor to performance. The portfolio benefited from the significant Merger and Acquisition activity in the semi-conductor market, notably the sale of ARM which returned 61% and contributed just over 1% to the portfolio’s return. Holdings in Linear Tech and NXP are also subject to takeovers by ADI and Qualcomm respectively. The growth in electric and hybrid electric vehicles has translated to strong growth for the semi-conductor industry in the auto segment, as the car of the future requires significantly more electronic content to deliver improvements in safety and fuel efficiency. We also focus on thematic drivers within the technology sector such as the increase in Cloud computing and the need to invest in digital infrastructure. We believe that these are important drivers of performance and why we hold Accenture, Microsoft and SAP.

The Health Care sector reversed the strong gains of 2015 and was the second-worst performing sector in 2016. The investment process targets companies which deliver differentiated, life-saving therapies and products that makes healthcare more accessible or affordable. We believed that this sector and these sorts of companies would be able to deliver defensive growth in a tough economic environment and therefore maintained an overweight position during the year. In the US, the source of the majority of global healthcare profits, the Election raised questions on the sustainability of drug pricing, and this hurt performance over 2016. Our holding in GlaxoSmithKline did relatively well in the year thanks to its more diversified business, with its Consumer and Vaccine divisions providing opportunities for growth. Roche was out of favour over 2016, due to pricing pressure in the US, combined with investor concern over the results in early 2016 of the important “Aphinity” trial. The trial results are considered key to Roche’s global leadership in breast cancer and the nature of the news led to weakness in the stock. We believe that their approach of meeting unmet medical need across its whole portfolio and its innovative record of discovering new molecules with breakthrough potential, will be rewarded and command improved pricing.

The Financial sector contributed negatively to portfolio performance over the year. A substantial portion of the underperformance came from our position in the Italian bank Intesa Sanpaolo as investor concerns around its non-performing loans in Italy, and political uncertainty, led to large declines in the share prices of Italian financials. We decided to sell the position and switch the proceeds into DNB. Our underperformance came from the absence of investment banks which underwent a strong re-rating from a very low base. Visa, however, performed well and, as one of the portfolio’s largest positions, was a strong contributor to performance. We increased the portfolio’s exposure to Financials during the year.

Energy was again a focus for the market in 2016. After the turbulent markets in 2015 oil rallied from below US$30 a barrel in the first quarter of 2016 to above US$50 when producers reached an agreement to reduce their output. The Energy sector rallied impressively and delivered 54%. The portfolio’s underweight position through 2016 contributed negatively to asset allocation as did stock selection: lower quality companies rallied the most in response to higher oil prices. Our investment process’ focus on quality companies attracts us to companies with higher quality hydrocarbon assets that can deliver better investment returns from lower oil prices. We believe that over the medium term this will be a winning investment strategy for businesses that sell this volatile commodity.

Going into 2017 the portfolio remains overweight in Health Care, Information Technology and underweight in Consumer Discretionary, Consumer Staples and Energy.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

12

Strategic Report

Investment case: Health CarePortfolio ActivityIn 2016 we added the Norwegian bank DNB and Microsoft to our portfolio. We believed that DNB’s valuation was attractive following market concerns related to oil-related economies as it remained one of the best capitalised banks in Europe. Microsoft is embracing the Cloud through Azure, which provides developers and IT professionals with a collection of integrated cloud services through a global network of data centres, and the shift in the sale of its Office software suite to a subscription model.

Significant sales in 2016 included Novo Nordisk and ARM. The former continues to benefit from innovations in insulin design but the weaker outlook for insulin sales, due to concerns about the sustainability of its US pricing model, resulted in lower profit expectations. ARM was sold following a bid by Softbank, a Japanese telecom and technology company. The proceeds from these sales were invested in the US company Cadence which develops electronic design automation software. We continued to use market weakness to add to positions where the team have strong long-term convictions such as Acuity Brands and Roche.

Our Top 10 holdings at the end of the year included for the first time Acuity Brands, Ecolab, Blackstone Group, Macquarie Infrastructure and the Toronto & Dominion group. Acuity is the US lighting market leader with a diversified product mix. It has steadily gained market share in an already relatively consolidated industry. It offers a full array of technologies, including LED, which suit the needs of its customers. Ecolab is a global leader in water, hygiene and energy technologies which are used across different industries to maintain clean and safe environments. Blackstone is possibly the best positioned ‘alternative’ asset manager globally and should benefit from the shift to that style of management.

Immuno-oncology is an innovation that is set to revolutionise cancer treatment. The ability to utilise the body’s immune system to fight a cancer tumour, rather than directly targeting the tumour itself, has produced some promising results. Long term survival in metastatic cancer is now a reality. The Trust’s portfolio has exposure to this innovation through Roche and Pfizer, both of whom are key players in the immune oncology revolution. We see Roche as remaining a global leader in the broader oncology setting however it was out of favour in 2016 and made a small relative contribution in the year. Pfizer is developing an exciting suite of treatments, including both immuno-oncology treatments and the recently launched Ibrance, in breast cancer. Pfizer also acquired Medivation, which has promising complementary products in the oncology setting which should allow it to build a profitable and growing oncology suite of products. Health Care stocks provided around one-tenth of the equity portfolio’s total return and this part of the portfolio outperformed the MSCI ACWI in the year.

The treatment of cancer remains one of the key areas in healthcare where innovation is increasingly important.

Investment Manager’s Report – 2016 continued

(%) Relative Contribution2014 2015 2016

Pfizer 0.24 0.31 0.60

Roche 0.02 0.07 0.03

Source: Alliance Trust

Alliance Trust PLC | Annual Report and Financial Accounts 2016

13

I Strategic Report IIIII

Portfolio RiskWe maintained the number of stocks in the portfolio at around 60, reflecting the conviction we had in those stocks which we considered to be best-in-class. The portfolio’s active share, which is the weighting of the stocks in the portfolio that is different from the stock weightings in the MSCI ACWI, was above 90%, a level that demonstrates that the portfolio was very structurally different to the index with just a 10% weighting overlap. The portfolio was sufficiently concentrated to deliver meaningful levels of outperformance yet diversified enough through only the highest quality global companies that there was the expectation of lower volatility than that of the index.

The portfolio started 2016 with a tracking error of 2.61% against the MSCI ACWI, finishing the year largely unchanged at 2.91%.

Investment case: Technology

The ‘Internet of Things’, Advanced Driver Assistance Systems (ADAS) and Electric Vehicles are all examples of areas where technology is penetrating new areas. The Internet of Things enables a refrigerator to manage its power usage to optimise the use of lower cost energy. ADAS will help reduce the number of casualties on the road through the use of predictive algorithms using data generated from radars, lidars and cameras. Electric vehicles will reduce CO2 emissions, make our cities cleaner and improve energy efficiency. All these are admirable goals but they do require significant processing power as well as software capability. Our exposure to digitalisation, beyond ARM and Linear Technology, has been through Cadence and, to a lesser extent, Accenture. Technology stocks provided around one-third of the equity portfolio’s total return in 2016.

The acquisition of both ARM and Linear Technology in 2016 was confirmation that within the technology sector, digitalisation is spreading to new areas.

(%) Relative Contribution2014 2015 2016

Accenture 0.36 0.59 0.98

ARM 0.01 0.08 0.99

Cadence 0.34 0.16 0.63

Linear Technologies 0.12 0.00 0.84

Benchmark relative risk (%)

Dec2015

Mar2016

Jun2016

Sep2016

Dec2016

2.6

2.7

2.8

2.9

3.0

Predicted tracking error

Source: MSCI Barra

Source: Alliance Trust

Alliance Trust PLC | Annual Report and Financial Accounts 2016

14

Strategic Report

Investment Manager’s Report – 2016 continued

Asset Allocation and Gearing in 2016Asset allocation is undertaken to enhance or protect the returns of the core investment portfolio. When strong returns are anticipated from equity markets the exposure to equities is increased by increasing borrowing. In contrast when equity valuations appear full and the outlook uncertain then exposure to equities is reduced.

Overall gearing levels were limited by the Board in the year to a maximum of 18%.

In 2016 four significant moves were implemented at an asset allocation level.

The year started with gearing on the core portfolio of 13%. In March, having ascertained that the UK Referendum on Leaving the EU could lead to a fall in the Pound, we hedged Sterling against the US Dollar equivalent to 5% of the portfolio. This mitigated the overweight of the equity portfolio towards Sterling.

Then in May gearing was reduced following a six month rally in global equities and mounting political and economic uncertainties. This brought gearing down to 10.2% of the equity portfolio.

Following the referendum result on 24 June the concern was to protect the portfolio from a disorderly fall in equity markets. To this end we sold FTSE 100 index futures to hedge the UK exposure of the portfolio – representing 4% of the overall portfolio. The position was closed on 1 July as it became apparent that currency markets were taking the impact while the FTSE 100 appreciated.

In October gearing was reduced further to 6%, given the risks surrounding the US election, anticipated US interest rate hikes and very strong equity market performance. In November the FX hedge was closed following Sterling’s 15% depreciation versus the US Dollar.

Overall the net impact of being geared into a rising market enhanced the return from the core investments, and while the index future short post the referendum had a negative impact this was more than covered by the positive contribution from the FX hedge.

StewardshipIn 2016 we voted at 161 meetings. For 123 of these meetings we voted against, withheld or abstained on one or more resolutions. These votes related to concerns about matters including: excessiveor opaque remuneration arrangements; auditors tenure and non audit fee; tenure and board and committee independence; and effectiveness or lack of transparency around lobbying activities and fair business policies. We added the issue of gender diversity on boards to our voting policy during the year and we voted against the company’s report & accounts where there were less than 15% women on the board and abstained from voting on report & accounts where there were less than 30% women on the board. This applied to just under one third of eligible meetings. The Financial Reporting Council awarded Alliance Trust Investments with a Tier 1 status on the quality of reporting against the Stewardship Code. Alliance Trust Investments is a signatory to the UN Principles for Responsible Investment (PRI), where representatives from the investment team sit on the PRI Sustainable Palm Oil Investor working group, PRI Engagement on Water Risks group, PRI Global Investor Taskforce on Corporate Tax Responsibility group. Alliance Trust Investments is also a signatory to the Paris Pledge for Action: Climate Change, PRI Montreal pledge.

Attribution analysis (%)Alliance Trust MSCI AC World Index Attribution

Equity Portfolio Only (look through basis)

AverageWeight

TotalReturn

Contribution to Total Return

AverageWeight

TotalReturn

Contribution to Total Return

Allocation Effect

SelectionEffect

TotalEffect

Consumer Discretionary 8.4 10.8 0.7 12.3 23.0 2.8 0.2 -0.8 -0.6

Consumer Staples 8.3 11.7 1.5 10.4 21.9 2.7 0.1 -0.7 -0.6

Energy 4.9 44.8 2.2 6.7 53.4 3.4 -0.4 -0.3 -0.7

Financials 17.8 19.6 3.1 17.3 32.9 4.9 0.0 -2.1 -2.1

Health Care 16.7 9.3 1.8 12.0 11.6 1.6 -0.7 -0.3 -1.0

Industrials 8.5 39.7 3.1 10.6 34.1 3.6 -0.1 0.4 0.3

Information Technology 20.0 33.3 7.1 15.5 34.7 5.3 0.2 -0.2 0.0

Materials 4.7 32.3 1.5 4.9 48.5 2.2 -0.1 -0.6 -0.7

Real Estate 4.6 25.5 1.5 3.2 22.9 0.8 -0.1 0.1 0.0

Telecommunication Services 3.2 6.1 0.2 3.8 26.2 1.1 0.0 -0.5 -0.5

Utilities 2.9 0.6 0.2 3.3 27.3 1.0 0.1 -0.7 -0.6

100.0 22.9 100.0 29.4 -0.8 -5.7 -6.5

Source: Alliance Trust and Factset

Alliance Trust PLC | Annual Report and Financial Accounts 2016

15

I Strategic Report IIIII

The divestment of non-core investments continued to gather momentum in 2016. Fixed interest investments were sold in their entirety by mid–year. The Trust has £9.5m in indirect property held through investments in Limited Partnerships. There are no direct property investments left in the portfolio although the Trust still owns its registered office, 8 West Marketgait, Dundee, DD1 1QN which was valued at £4.5m as at the end of 2016 (unchanged from 2015). This office accommodates Alliance Trust Savings’ operations and the Trust’s small executive function in Dundee. The Trust acts as landlord for Alliance Trust Savings on a commercial basis.

A sale process of the mineral rights holdings was held in the early part of the year but bids received were considered unacceptable in a distressed market environment of very weak oil prices. The sale of the holdings remains part of the divestment strategy for non-core assets but this is unlikely until there is a sustained period of energy price stability. At the year end, the mineral rights holdings were valued at £13.2m compared with a valuation of £17.5m in 2015.

The majority of investments in the private equity portfolio are held in seven externally managed private equity funds. These seven funds are largely mid-market European buyout funds and are held in our own fund of fund limited partnerships. These investments are now delivering strong returns. In 2016 the Trust saw a marked improvement in portfolio valuations and we experienced an increase in realisations resulting in healthy distributions back to the Trust. The value of our private equity investments is £103.5m. The unfunded commitment to private equity investments, which includes recallable distributions, is £28.5m. We have made no new private equity investments since 2014 and anticipate a continuation of the trend of further realisations within the private equity portfolio in 2017 generating more distributions back to the Trust.

For the non-core investments of private equity, property, fixed income and the mineral rights holdings, which together represents 3.7% of the total assets of the Trust, a positive contribution of 0.5% to investment returns was recorded in 2016.

Non-core Investments

Contribution Analysis – 2016

Whilst the Board is committed to reducing its exposure to these assets, they provided good returns and a strong income stream during the year.

The NAV total return for 2016 was 21.5% versus the benchmark MSCIACWI return of 29.4%. This is a result of the investment returns fromthe global equity portfolio, investments in fixed income, private equityand mineral rights and the change in value of the subsidiary companies. Over 2016 the shareholder total return was 26.4%, outstripping the NAV total return so capturing the benefit of a narrowing in the discount. Equities, at 93% of our total investment at the year end, are by far the most significant asset class and contributor to total return. The decision taken to fund the Company’s Final Salary Pension Schemeto allow it to buy in its liabilities through a bulk annuity policy had anegative effect on performance in the year. Average gearing was 10.7% over 2016, this had the effect of enhancingthe return from the equity portion of the portfolio over 2016.

Contribution Analysis (%) Contribution to Total Return

Equity Portfolio* 22.9

FX Contracts and Index Futures 0.2

Non-core Investments 0.5

Net Gearing Effect 0.2

Investment Portfolio Total 23.8

Subsidiaries -0.2

Pension Fund Adjustments -0.8

Effect of Change to Fair Value of Debt -0.5

Share buybacks, Cash and Accruals -0.3

Total Operating Costs -0.5

NAV Cum Income Total Return 21.5

Effect of Discount 4.9

Share Price Total Return 26.4

MSCI ACWI Total Return 29.4

*includes investments in Funds

Source: Alliance Trust and Factset

Alliance Trust PLC | Annual Report and Financial Accounts 2016

16

Strategic Report

2016

2015

£28.3m

£19.8m

2016

2015

67%

78%

2016

2015

£2.3bn

£2.1bn

2016

2015

£51m

£81m

Alliance Trust Investments

The focus of Alliance Trust Investments has been on managing the Trust’s investment portfolio and promoting its range of Sustainable Future (SF) equity and corporate bond funds alongside the Monthly Income Bond fund. These are open to both institutional and retail investors.

The business operates in a competitive marketplace and in the year was successful in continuing to attract net inflows of £51m into its funds.

During the year it carried out a significant reorganisation which reduced ongoing costs while maintaining its team of experienced investment professionals.

2016 saw strong performance from the SF Corporate Bond and Monthly Income Bond funds, with the former ending the year in the top quartile over 1, 2 and 5 years. Against the full Corporate Bond sector the Monthly Income Bond fund ended the year just below median.

Alliance Trust Investments saw net revenue grow to £22.0m, making an operating profit in the year of £3.1m, and a profit, after one-off and exceptional costs, of £0.4m, compared to its loss of £2.1m last year.

The total investment in the business by the Trust was £45.4m. At the end of 2016 the Directors had attributed a fair value to the business of £28.3m.

In December 2016 the Board announced that the Board had reached agreement to sell ATI to Liontrust Asset Management PLC (Liontrust), a specialist fund management group that has been listed on the London Stock Exchange since 1999. It is expected that net proceeds will be not less than £25m, before any future contingent consideration. The actual value which the Trust will finally receive will be dependent on the movement in the price of the Liontrust shares acquired as part of the consideration. This compares to its fair value of £19.8m as at the end of June 2016.

Alliance Trust Investments is a specialist fund management business offering open-ended funds and investment solutions. Agreement was reached in December 2016 to sell this business representing an expected gain of over £5m from its valuation at 30 June 2016. This is expected to be completed in April 2017.

Key Performance Indicatorsfor the year to 31 December

2016 (£m) 2015 (£m)

Net revenue 22.0 10.5

Ongoing expenses (18.9) (12.6)

Operating profit/(loss) 3.1 (2.1)

One-off expenses (2.7) -

Profit/(loss) before tax 0.4 (2.1)

£28.3mFair value

+43%

67% Funds above median over 3 years

-14%

£2.3bnThird party assets under management*

+11.5%

£51mThird party net inflows*

*Excludes effect of Alliance Trust mandate in February 2016.

-37%

Alliance Trust PLC | Annual Report and Financial Accounts 2016

17

I Strategic Report IIIII

2016

2015

£61.5m

£54.0m

2016

2015

£13.6bn

£8.5bn

2016

2015

110,962

84,746

2016

2015

673,486

539,222

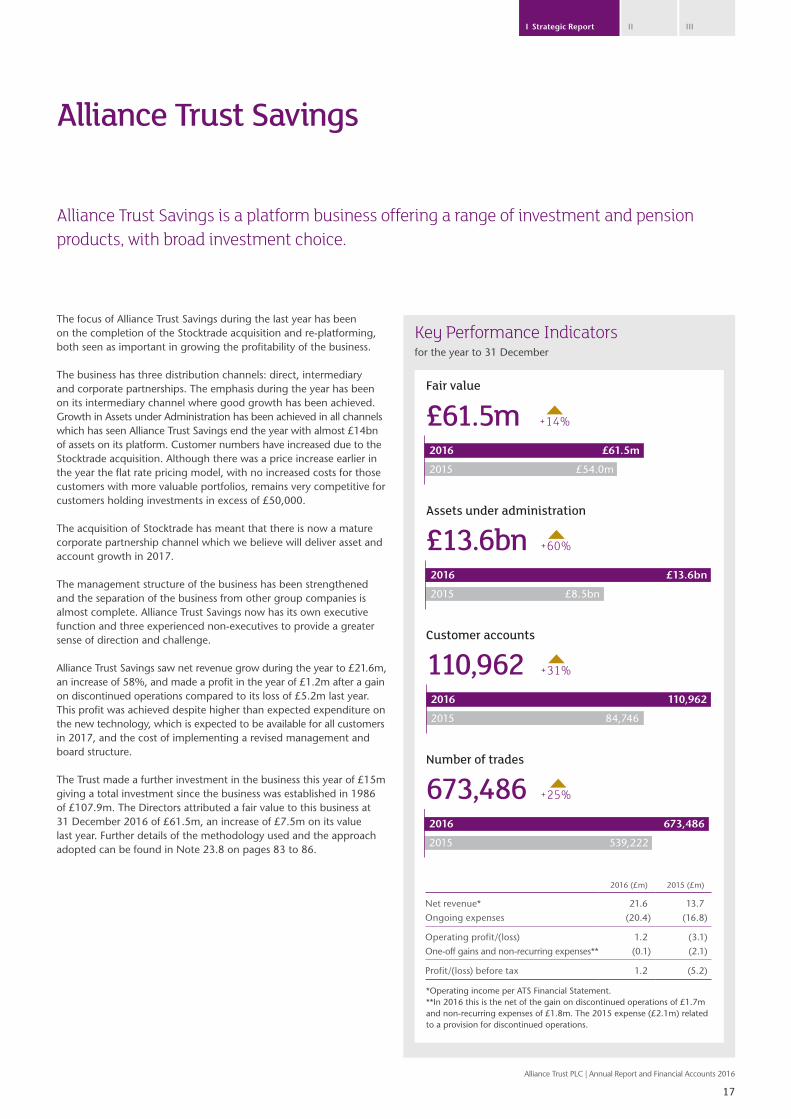

Alliance Trust Savings

The focus of Alliance Trust Savings during the last year has been on the completion of the Stocktrade acquisition and re-platforming, both seen as important in growing the profitability of the business.

The business has three distribution channels: direct, intermediary and corporate partnerships. The emphasis during the year has been on its intermediary channel where good growth has been achieved. Growth in Assets under Administration has been achieved in all channels which has seen Alliance Trust Savings end the year with almost £14bn of assets on its platform. Customer numbers have increased due to the Stocktrade acquisition. Although there was a price increase earlier in the year the flat rate pricing model, with no increased costs for those customers with more valuable portfolios, remains very competitive for customers holding investments in excess of £50,000.

The acquisition of Stocktrade has meant that there is now a mature corporate partnership channel which we believe will deliver asset and account growth in 2017.

The management structure of the business has been strengthened and the separation of the business from other group companies is almost complete. Alliance Trust Savings now has its own executive function and three experienced non-executives to provide a greater sense of direction and challenge.

Alliance Trust Savings saw net revenue grow during the year to £21.6m, an increase of 58%, and made a profit in the year of £1.2m after a gain on discontinued operations compared to its loss of £5.2m last year. This profit was achieved despite higher than expected expenditure on the new technology, which is expected to be available for all customers in 2017, and the cost of implementing a revised management and board structure.

The Trust made a further investment in the business this year of £15m giving a total investment since the business was established in 1986 of £107.9m. The Directors attributed a fair value to this business at 31 December 2016 of £61.5m, an increase of £7.5m on its value last year. Further details of the methodology used and the approach adopted can be found in Note 23.8 on pages 83 to 86.

Alliance Trust Savings is a platform business offering a range of investment and pension products, with broad investment choice.

Key Performance Indicatorsfor the year to 31 December

2016 (£m) 2015 (£m)

Net revenue* 21.6 13.7

Ongoing expenses (20.4) (16.8)

Operating profit/(loss) 1.2 (3.1)

One-off gains and non-recurring expenses** (0.1) (2.1)

Profit/(loss) before tax 1.2 (5.2)

£61.5mFair value

+14%

£13.6bnAssets under administration

+60%

110,962Customer accounts

+31%

+25%673,486

*Operating income per ATS Financial Statement.**In 2016 this is the net of the gain on discontinued operations of £1.7m and non-recurring expenses of £1.8m. The 2015 expense (£2.1m) related to a provision for discontinued operations.

Number of trades

Alliance Trust PLC | Annual Report and Financial Accounts 2016

18

Strategic Report

Portfolio Listing

All quoted equity holdings as at 31 December 2016

Stock Sector Country of listing% of

quoted equitiesValue

£m

Pfizer Inc. Health Care United States 2.8 88.2Walt Disney Company Consumer Discretionary United States 2.6 83.4Visa Inc. Class A Information Technology United States 2.5 80.1Accenture Plc Information Technology United States 2.5 79.0Ecolab Inc. Materials United States 2.4 76.4Macquarie Infrastructure Corporation Industrials United States 2.4 75.3Amgen Inc. Health Care United States 2.3 74.1Toronto-Dominion Bank Financials Canada 2.3 74.0Acuity Brands, Inc. Industrials United States 2.3 73.2Microsoft Corporation Information Technology United States 2.3 71.5Blackstone Group L.P. Financials United States 2.2 69.8Roche Holding Ltd Genusssch. Health Care Switzerland 2.1 67.3Daikin Industries, Ltd. Industrials Japan 2.1 66.3DNB ASA Financials Norway 2.1 65.7Prudential plc Financials United Kingdom 2.1 65.6American Tower Corporation Real Estate United States 2.1 64.8Deutsche Telekom AG Telecommunication Services Germany 2.0 63.8First Republic Bank Financials United States 2.0 63.0Danaher Corporation Health Care United States 2.0 62.4Thermo Fisher Scientific Inc. Health Care United States 2.0 62.1Swedbank AB Class A Financials Sweden 1.9 61.0Norsk Hydro ASA Materials Norway 1.9 60.2Eli Lilly and Company Health Care United States 1.9 60.1Total SA Energy France 1.9 59.4National Grid plc Utilities United Kingdom 1.9 59.2Statoil ASA Energy Norway 1.9 58.6Tencent Holdings Ltd. Information Technology China 1.9 58.6WPP Plc Consumer Discretionary United Kingdom 1.8 57.5Nasdaq, Inc. Financials United States 1.8 57.1NXP Semiconductors NV Information Technology Netherlands 1.7 55.2Cadence Design Systems, Inc. Information Technology United States 1.7 53.9Enterprise Products Partners L.P. Energy United States 1.7 53.1ASML Holding NV Information Technology Netherlands 1.7 52.5Activision Blizzard, Inc. Information Technology United States 1.7 52.4CVS Health Corporation Consumer Staples United States 1.6 50.3TJX Companies Inc Consumer Discretionary United States 1.6 49.6SS&C Technologies Holdings, Inc. Information Technology United States 1.6 49.2Equinix, Inc. Real Estate United States 1.5 47.9Wells Fargo & Company Financials United States 1.5 46.4ORIX Corporation Financials Japan 1.5 45.9SAP SE Information Technology Germany 1.4 42.8Alphabet Inc. Class A Information Technology United States 1.3 41.8GlaxoSmithKline plc Health Care United Kingdom 1.3 41.6Vodafone Group Plc Telecommunication Services United Kingdom 1.3 40.8Reckitt Benckiser Group plc Consumer Staples United Kingdom 1.3 40.7CSL Limited Health Care Australia 1.3 39.9Henkel AG & Co. KGaA Pref Consumer Staples Germany 1.2 38.4Legal & General Group Plc Financials United Kingdom 1.2 37.3Melrose Industries PLC Industrials United Kingdom 1.1 35.7Schneider Electric SE Industrials France 1.1 35.2Unilever PLC Consumer Staples United Kingdom 1.0 33.0Valeo SA Consumer Discretionary France 1.0 33.0AmerisourceBergen Corporation Health Care United States 1.0 31.5Dentsu Inc. Consumer Discretionary Japan 1.0 31.0Roper Technologies, Inc. Industrials United States 1.0 30.8Ambev SA Sponsored ADR Consumer Staples Brazil 1.0 30.4Keyence Corporation Industrials Japan 0.9 29.9Bangkok Bank Public Company Limited (Alien Mkt) Financials Thailand 0.9 29.0

100.0% Total Value 3,156.9

Alliance Trust PLC | Annual Report and Financial Accounts 2016

19

I Strategic Report IIIII

Funds as at 31 December 2016

Alliance Trust Investment Funds Country of registrationValue

£m

Sustainable Future Pan-European Equity Fund Luxembourg 69.5Sustainable Future Cautious Managed Fund United Kingdom 11.9Sustainable Future Defensive Managed Fund United Kingdom 11.7

Total Value 93.1

Non-core investments as at 31 December 2016

Investment Region Value £m

Private Equity United Kingdom/Europe 103.6Mineral Rights North America 13.2Indirect Property United Kingdom 9.5Other United Kingdom 1.2Foreign Currency Exchange Contract 6.9

Total Value 134.4

Total investments as at 31 December 2016

InvestmentValue

£m

Quoted Equities 3,156.9Funds 93.1Investments in operating subsidiary companies 89.8Non-core investments 134.4

Total Value 3,474.2

Source: Alliance TrustA full portfolio listing, similar to that displayed above, is available on a monthly basis on our website at www.alliancetrust.co.uk

Investments in operating subsidiary companies as at 31 December 2016

Investment RegionValue

£m

Alliance Trust Savings United Kingdom 61.5Alliance Trust Investments United Kingdom 28.3

Total Value 89.8

Alliance Trust PLC | Annual Report and Financial Accounts 2016

20

Strategic Report

0.43

0.59

0.60

0.75

0.67

2012 2013 2014 2015 2016

Cost savings across the Investment BusinessIn October 2015 we announced targeted cost savings of £6m, equivalent to more than 20% of the combined recurring costs borne by the Trust and ATI in 2015. By Investment Business we mean the combined costs of the investment manager, ATI, and the direct costs of the Trust after the Group reorganisation implemented in the last quarter of 2015.

The targeted £6m of costs savings were achieved and in total we reduced annual costs by over £9m; achieved through a combination of the initial cost target savings and an additional £3m cost saving in ATI as the business moved to profitability. The cost base of ATI was restructured in 2016 through staff reductions, a change in premises and management of discretionary spend; this enabled ATI to generate monthly profits from July 2016.

The ongoing costs of the Trust are now driven by a variable management fee. Other costs of running the Trust are directly under the control of the Board. In 2016 the Board sought to reduce ongoing costs to a level consistent with running the Trust efficiently and restoring shareholder value.

DividendsAlliance Trust has increased the ordinary dividend in each of the last 50 years and is one of only four companies in the FTSE All-Share index with such a track record. The Board’s current policy is to pay a progressive dividend and under normal market conditions to pay all net income received as ordinary dividends.

The ordinary dividend for 2016 will rise by 16% to 12.774p. A fourth interim dividend of 3.274p will be paid on 31 March 2017 to shareholders who were on the Company’s share register on 10 March 2017.

DiscountOur policy is to buyback shares where we judge it to be beneficial to shareholders. Through the use of our share buyback programme we narrowed the discount significantly at the year end closing the year at 4.4% slightly less than the AIC Global Sector’s average of 4.6%. Since the year end the discount has remained on or around 5%. All the shares bought back have been cancelled.

Costs and Financial Measures – 2016

Ongoing Charges Ratio (OCR)In October 2015 we announced a targeted Ongoing Charges Ratio (‘OCR’) of 0.45% or less by the end of 2016 (compared to 0.59% in 2015 and 0.60% in 2014). The actual 2016 OCR which is calculated on ongoing expenses was 0.43%. This reduction in OCR has been achieved through the appointment of Alliance Trust Investments (ATI) to manage the portfolio at an investment management charge of 0.35% of an adjusted NAV (excluding holdings in ATI managed funds and the fair value of ATS and ATI), effective management of ongoing direct expenses for the Trust and the Group reorganisation whereby direct expenses of ATI and Alliance Trust Savings are now borne directly by these entities. Ongoing expenses exclude non-recurring expenses relating to the Strategic Review and restructuring costs. Non-recurring costs in 2016 relating to the Strategic Review, indirect ATI sale costs and reorganisation costs are £3.4m.

The Trust implemented a new cost allocation policy in 2016. Where consistent with AIC SORP guidelines we now allocate management fees and other indirect expenditure one third to revenue profits and two thirds to capital profits. In prior years, with the exception of capital incentives, all expenses were recorded against revenue profits. The 2016 OCR of 0.43% is based on total ongoing costs, the corresponding OCR on total ongoing costs would have been 0.63% rather than the reported 0.59% based on revenue costs.

As in prior years the OCR excludes one-off or non-recurring costs. Non-recurring costs in 2016 were £3.4m (2015: £5.2m). Further disclosure of non-recurring costs is on the next page.

We provide here a breakdown of how our Ongoing Charges Ratio is calculated and cost savings achieved across the investment business.

Ongoing charges ratio (%)

Source: Alliance Trust

Alliance Trust PLC | Annual Report and Financial Accounts 2016

21

I Strategic Report IIIII

Alliance Trust PLCOngoing Charges Ratio (OCR) Summary 2016

£'0002016

Revenue Capital Total2015

Revenue Capital Total

Average net assets 3,111,711 2,983,253

Total administrative expenses 7,960 8,810 16,770 22,835 1,133 23,968

Non-recurring expenses (1,782) (1,590) (3,372) (5,233) - (5,233)

Ongoing expenses 6,178 7,220 13,398 17,602 1,133 18,735

Non-recurring expenses

Reorganisaton 556 179 735 2,880 - 2,880

Strategic Review 457 1,221 1,678 - - -

Indirect disposal costs of ATI 769 189 959 - - -

AGM requisition - - - 2,353 - 2,353

1,782 1,590 3,372 5,233 - 5,233

OCR ongoing expenses* 0.43% 0.59% 0.63%

Total Expenses Ratio (TER)* 0.54% 0.77% 0.80%

*We have not shown an OCR or TER for 2016 revenue expenses because from 1 January 2016 these measures are calculated on total expenses.

The expenses relating to Alliance Trust Investments and Alliance Trust Savings can be found on pages 16 and 17.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

22

Strategic Report

Risk Management

This section of the report deals with the structure of the Group’s Risk Management Framework and risk reporting.

Risk Management FrameworkThe Group has a Risk Management Framework that provides a robust and comprehensive approach for the identification and management of key risks facing the business. The Framework helps in the assessment and management of current and future risks. Principal Risk categories include Market and Prudential, Operational, Strategic and Regulatory and Conduct Risk. The Risk Management Framework supports two key processes:

• the ICAAP (Internal Capital Adequacy Assessment Process), which helps to determine the capital requirements (including potential stress points) of the Group; and

• the ILAAP (Internal Liquidity Adequacy Assessment Process), which helps to determine the liquidity requirements (including potential stress points) of the Group.

Market and Prudential RisksRisk Description Mitigating activities Change in year

Investment under-performance

Investment performance fails to deliver sufficient capital growth due to poor stock selection, sector allocation or wider market movements.

• Asset allocation strategy and governance• Robust investment process• Compliance with investment parameters regularly tested• Stress and scenario testing of portfolios• Risk and performance management information

regularly reviewed by the Board

Liquidity The Company does not have sufficient liquid resources to ensure that it can meet its liabilities as they fall due during normal and stressed times.

• Majority of investments are in listed equities• Daily monitoring of cash positions• Gearing availability

Operational RisksRisk Description Mitigating activities Change in year

Cyber attack Failure to ensure that the business is adequately protected against the threat of cyber attack, which may lead to significant business disruption or external fraud.

Despite action taken by management to improve systems the increasing trend is due to the general growth in cyber related incidents across the industry.

• Systems and controls to protect the business regularly tested

• Ongoing monitoring of environment to understand threat landscape

• Programme of enhancements to keep pace with latest defence strategies

• Business continuity plans in place should an incident occur

Change of Investment Manager

The Company changed its investment manager to Alliance Trust Investments in 2016 and will change it to Willis Towers Watson in 2017.

• Experienced investment managers• Use of transition manager for the investment switch

to Willis Towers Watson

Alliance Trust PLC | Annual Report and Financial Accounts 2016

23

I Strategic Report IIIII

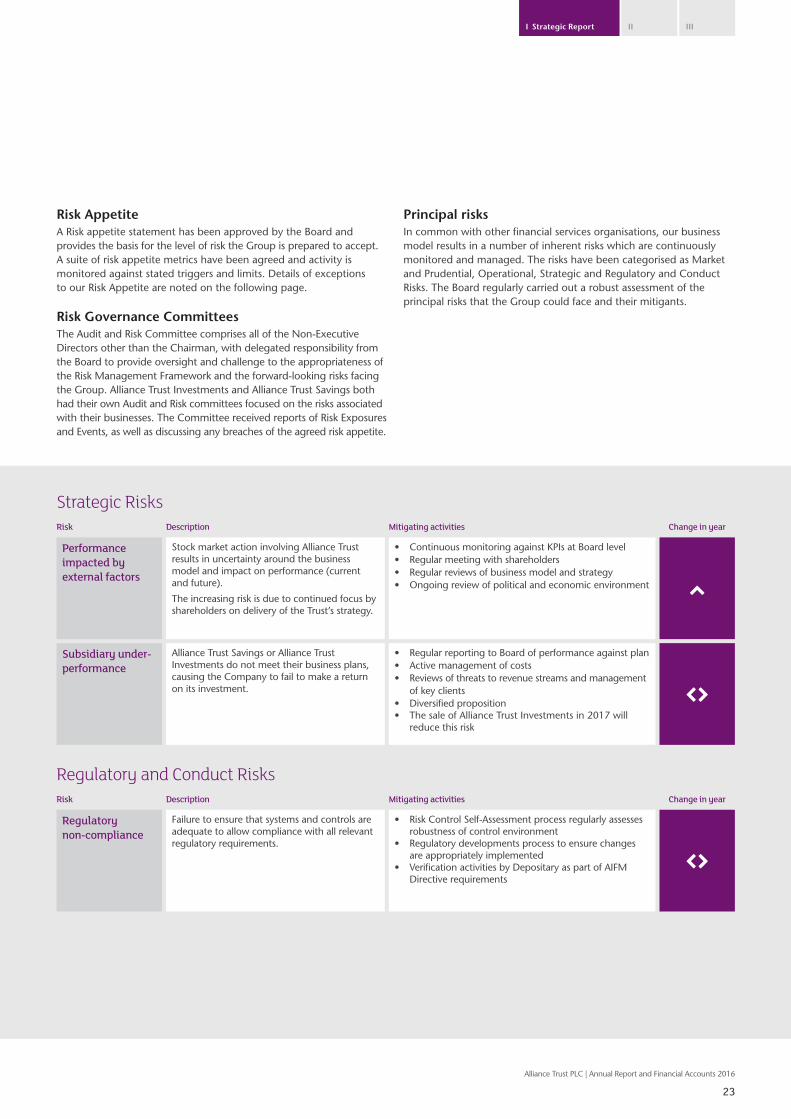

Strategic RisksRisk Description Mitigating activities Change in year

Performance impacted by external factors

Stock market action involving Alliance Trust results in uncertainty around the business model and impact on performance (current and future).

The increasing risk is due to continued focus by shareholders on delivery of the Trust’s strategy.

• Continuous monitoring against KPIs at Board level• Regular meeting with shareholders• Regular reviews of business model and strategy• Ongoing review of political and economic environment

Subsidiary under-performance

Alliance Trust Savings or Alliance Trust Investments do not meet their business plans, causing the Company to fail to make a return on its investment.

• Regular reporting to Board of performance against plan• Active management of costs • Reviews of threats to revenue streams and management

of key clients• Diversified proposition• The sale of Alliance Trust Investments in 2017 will

reduce this risk

Regulatory and Conduct RisksRisk Description Mitigating activities Change in year

Regulatory non-compliance

Failure to ensure that systems and controls are adequate to allow compliance with all relevant regulatory requirements.

• Risk Control Self-Assessment process regularly assesses robustness of control environment

• Regulatory developments process to ensure changes are appropriately implemented

• Verification activities by Depositary as part of AIFM Directive requirements

Risk AppetiteA Risk appetite statement has been approved by the Board andprovides the basis for the level of risk the Group is prepared to accept.A suite of risk appetite metrics have been agreed and activity ismonitored against stated triggers and limits. Details of exceptions to our Risk Appetite are noted on the following page.

Risk Governance CommitteesThe Audit and Risk Committee comprises all of the Non-Executive Directors other than the Chairman, with delegated responsibility from the Board to provide oversight and challenge to the appropriateness of the Risk Management Framework and the forward-looking risks facing the Group. Alliance Trust Investments and Alliance Trust Savings both had their own Audit and Risk committees focused on the risks associated with their businesses. The Committee received reports of Risk Exposures and Events, as well as discussing any breaches of the agreed risk appetite.

Principal risksIn common with other financial services organisations, our businessmodel results in a number of inherent risks which are continuouslymonitored and managed. The risks have been categorised as Market and Prudential, Operational, Strategic and Regulatory and Conduct Risks. The Board regularly carried out a robust assessment of the principal risks that the Group could face and their mitigants.

Risk AppetiteRisk Appetite measures which at the year end and in each quarter of 2016 were outside the limits approved by the Board were:

• Net Asset Value relative to MSCI ACWI

• Management of Alliance Trust PLC Direct Costs

The Board believes that the output from the Strategic Review and the actions being taken to implement a new investment approach will see these measures return to within our risk appetite limits.

The other measures which breached the agreed risk appetite during the year were:

• Discount – Breached from Q1 to Q3, with an improvement to within target following the Strategic Review announcement in December and the commencement of an active programme of share buybacks.

• Performance of subsidiaries against business plan – Breached in Q1 and Q2, with improvements made in the second half of the year with Alliance Trust Investments moving to operational profitability; however, Alliance Trust Savings profit finished the year below budget.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

24

Strategic Report

Policies

Risk appetite

Risk universe

CultureEmbed risk practices Conduct

Risk management organisation Risk measurement

Governance Management information

Risk Management continued

Risk frameworkWe undertake an annual assessment of the effectiveness of the Risk Framework (see the diagram opposite). The most recent assessment was presented to the Audit and Risk Committee following the year end and noted that there were no significant concerns to highlight.

An annual report on the effectiveness of the internal control systems is provided to the Board. This includes a review of all material financial, prudential, operational and compliance controls. The report builds on the reporting of each line of defence that is provided across the course of the year through the governance committees up to the Board. The latest report was presented to the Audit and Risk Committee following the year end and no material issues were identified.

Alliance Trust PLC | Annual Report and Financial Accounts 2016

25

I Strategic Report IIIII

Corporate Responsibility

We report in our Investment Manager’s report how we exercise our stewardship responsibilities demonstrating our commitment to good corporate governance.

As an investment trust we have no customers however we do believe that we should maintain an open dialogue with our shareholders and during the year we met with our significant shareholders as well as individual shareholders and their representatives to hear their views and to update them on the progress of the Trust. This helps the Board to act fairly between the members of the Company by ensuring that it captures a range of shareholder views.

We have supported the Alliance Trust Foundation charity, which raises money through the Alliance Trust Cateran Yomp and fundraising activities by staff, for 3 years. Over that period the Company has donated £93,167. The Alliance Trust Foundation distributed £156,034 to charities including £87,423 to 28 charities in 2016. The charities supported are, in the main, those which are based in the communities where we have offices or where employees of the Group companies live i.e. Dundee, Edinburgh and London. We ceased our sponsorship of the Cateran Yomp after the 2016 event.