investing in the future: february 2012

DESCRIPTION

New opportunities for business.TRANSCRIPT

Apple | February 2012

MEASURESAP ON FINDING THE R I G H T A N A LY T I C S

S U R V E YU.S. MANUFACTURING WHAT IS HAPPENING

INVESTINGN E W I D E A S F O R O L D C O M PA N I E S

11%

25%

27%

37%

SellersHiring

Tech Investing

Both

Neither

Neither

11%

28%

26%

35%

BuyersHiring

Tech Investing

Both

Where Could APPLE Invest $100 Billion?

3

In a recession, business hold fast, reducing costs and overhead while waiting out the slow economy. The return of the economy heralds a return — often very much like to the one that existed before the recession — except with some new efficiencies .

The Great Recession is different.

By the start of this year, businesses seemed to understand that waiting for a return to business-as-usual was not going to happen. There is a realization that oil and energy prices are now fundamental to decision making at all levels. (One example is the auto industry, which fought fuel efficiencies for years. Now they are entering new markets with innovative cars, and bringing back buyers who have bought foreign for years.) Limitations in global outsourcing — including customer dissatisfaction and the costs of doing business abroad — are making board rooms re-examine policies once held as best practices. There is talk about supply-chain efficiencies that are broader and more complex than ever before. Companies with the technologies and skills to manage that process are beconming the new Google and the new Microsoft. Amidst the on-going malaise at the federal level, states and local communities are moving ahead with water and air quality policies. Innovative leaders are leaping ahead of those regulations, developing new products that manage resources better, either in the manufacturing process or as used by consumers.

Yet, with all this opportunity, at the beginning of January, Reuters reported that Apple Computer (APPL) had $93 Billion in cash, as well as long and short term investments. In September of 2011, the Wall Street Journal reported that corporations had a higher share of cash on their balance sheets than at any time in nearly half a century, with the Federal Reserve reporting that nonfinancial companies had more than $2 trillion in cash and other liquid assets, up more than $88 billion from the end of March of last year.

There are many reasons that businesses chooses to hold onto cash, including concerns over bank lending practices. In order to examine the future, however, THE GREEN ECONOMY took the opportunity to ask the question: “What could Apple do?” We are not picking on Apple, a famously inventive and resourceful company [Apple did not choose to respond], but rather reporting on ideas that have been tested by resourceful companies. This is not a one-time conversation, but an on-going issue that we will continue to follow throughout 2012.

This is a new economy, and a new economy needs a voice. THE GREEN ECONOMY is that voice.

A. Tana Kantor, Publisher

4 Features

04. Readers Speak | Readers

write.

14. Design | Futuristic proposal for a

South Korean

“Power

Center”.

25. Alloterra | Growing grass for profit

and energy.

26. Hybrids | Commercial hybrids for

fleets and

industry.

Stay Connected Join the Conversation

Each month THE GREEN ECONOMY posts questions to be included in the next issue

of the eMagazine. Questions are posted on Facebook and our Linkedin group, and our

monthly eNewsletter.

You can respond by sending letters to [email protected], or joining any of the

social networks listed above. Some letters are edited for brevity. Readers must include

name, title and affiliation.

TGEink: Follow us

TGEFlash: News we follow

Green Econ

Green Economy Group

Our RSS

5

THE GREEN ECONOMYFebruary | 2012

THIS ISSUE

Corporate Investing

08. Measure, Analyse Decide | SAP measures

to give board rooms more data.

16. Invest in Innovation | New innovations and the

companies that are investing them.

20. 2nd Generation Ethanol | The new ethanol is

better technology, uses better sources

and can be part of a local economy.

28. U.S. Factory Report | On-shoring, exporting and other

surprising results from manufacturers.

34. Solar is Big Business for Business | Not

just rooftops, unlikely businesses invest

in financing, M&A, and new technologies.

What Readers Apple Computer [APPL]:

What Could they do with their $100 billion ($97.5 billion) in cash, and long and short term securities?6

1. Recycle all the plastic in the world 2. Clean up the ocean. 3. Pay for me to write for one year without financial concern!

Lexis De Rothschild, Writer

MANUFACTURING

There are currently 1,223 comments and counting since this article [article on working conditions in Chinese factories] was published a day ago: To sustain its popularity and profitability, it would be a good idea for Apple to ensure in the future that fewer of these stories are printed on the front page of the New York Times.

Qi Fu, MS Operations Research Candidate Columbia University

Establishing the Global Workplace Standards and living by them.

Steve Reichenstein, CEO BioMart

Perhaps they should invest in manufacturing technologies, supply chains and infrastructure here in the US! The auto industry has figured out how to overcome low foreign labor rates, surely Apple can do the same.

Gary Sorin, Managing Partner Interra Consulting

EDUCATION

Here’s my suggestion: Give every school in a large city unified school district, like Los Angeles, enough ipads for every student. AND, work with curriculum developers and the Department of Education to standardize high quality curriculum that can be taught through an ipad. AND, work with teacher colleges to instruct teachers on how to best teach using the ipad. If it works, replicate it and scale it. If students are coming home with an ipad, and are learning all these amazing things through it, don’t you think mom and dad will want to buy one for themselves? It would be self-interested philanthropy, as Apple would likely see a big increase in ipad sales over time.

Jeremy Kranowitz, Director, Youth Policy Summit; Director, Education Policy Roundtable

Keystone Center

SHAREHOLDERS, RECYCLING, DIVEST, INVEST

Thinking like a shareholder, AAPL should consider a piece of that very large “pie” of a cash “war-chest” to be used as a benefit to shareholders, whether as a buyback, or as in the case with MSFT, issue a special one-time dividend, or as a stock-split.

Looking at Apple as an environmental laggard as compared to its peers in the high-tech industry, with all the plastic the company uses in the

What Readers Apple Computer [APPL]:

What Could they do with their $100 billion ($97.5 billion) in cash, and long and short term securities?

7

manufacture of its vast products line, the company should invest in evaluating the use of bio-plastics, as others have done in their product lines.

For the e-waste itself, Apple should consider setting aside a portion of its remaining hoard of cash to establish a recycling center where its unwanted computers could be brought — at no cost to its customers — for eventual and proper management by certified eSteward recyclers.

Gabe Crognale, book author/editor Prentice-Hall, PTR

We need to convince Apple and all other large corporations to divest of fossil fuels like they divested from diamond mines.

Margaret Rose, Consultant Data Architect

Apple should look to new electricity storage technologies like one from France that is capable of commercialization today. They should spend $28 billion to lock it in and become the sole provider of tablets and phones with a smaller battery that can charge in a minute and last for over 15 days. This would repeat what Apple did with the iPhone, crushing the competition with a model that everybody wants.

Mark Cox, Founder New Energy Fund LP

KEEP ON KEEPING ON

Apple should do what it has been doing -- investing in new technologies, improved design, etc. — AND beginning paying some of the hoard out in dividends. I do NOT believe there are very interesting acquisitions available for such an iconic company.

Tom Bryant, Trustee Meadowlands Museum

I cannot think of one company that has had such a positive impact on people’s lives than Apple. WIth a little bit of effort Apple could be giving universities a run for their money with regard to education. Instead of eight semesters in class you learn more and faster through 50 Apps that are each purchased for $9.99. $500 bucks plus a Mac and you get a degree that has prepared you for a breakthrough career.

They have earned their $100b and I would have to believe that based on consistent record-breaking results the company is probably the best entity to determine how that money gets used next.

Charlie Kamps, Managing Director American Sustainability Initiative

WHAT KINDS OF INITIATIVES MIGHT, APPLE COMPUTER WANT TO THINK INVEST IN TO BE EVEN MORE COMPETITIVE IN THE COMING YEARS?

SAP: MEASURE, ANALYZE, DECIDE

8

SAP: MEASURE, ANALYZE, DECIDE

9

THE GREEN ECONOMY asked Scott Bolick, VP of Sustainability Solutions at SAP,

“What kinds of initiatives might a company, like Apple Computer [APPL], want to think about investing in to become even more competitive in the coming years?”. After mentioning that he couldn’t make specific recommendations for Apple, he noted that the conversation around controlling costs of energy and other resources was reaching higher up in corporations.

Robin Meyerhoff, Director of Sustainability Public Relations at SAP, added that customers are increasingly using reporting and analytics to improve overall business performance. “Since measurement, reporting and analysis is now automated and much quicker, companies can more quickly see how they’re doing against key performance indicators (KPIs) and pro-actively address shortcomings. Because the process of measuring and reporting is so much more efficient, they can also expand the number of KPIs they set.”

“When we look at how the world’s changing, we believe that how business was done in the

past is not going to work going forward. You’re starting to see board rooms and investors asking questions that they weren’t

asking a few years ago.”

Scott Bolick,

VP of Sustainability Solutions at SAP

10

“Internally, at the board level, you have a chairman or CEO who is looking for a key differentiator, and there are more and more proxy battles depending on the industry sector.”

SAP focuses on four key areas, which

follow the logical steps in decision making:

� Set targets � Engage in change � Manage risk and � Report to stakeholders

Setting Targets: Energy and environmental resource managementSetting targets in order to manage energy and other environmental processes is a two step process: measure what you have, and then develop a strategy that is realistic and appropriate.

MeasureMeasuring resources across a company can be a daunting

task. The starting point is a data collection system that allows management to view usage across many departments and operational areas. As a starting point, Mr. Bolick pointed to SAP’s partnership with the CDP (Carbon Disclosure Project), which has lead to a lightweight Emissions Reporting Tool that can standardize carbon disclosure and analysis. CDP is an independent, not-for-profit organization working to drive greenhouse gas (GHG) emissions reduction and sustainable water use by business and cities. They also work with major investors —including banks — to analyze long term carbon risk in investment portfolios. Registering for free at the CDP website gives users access to numerous reports, tools, and case studies. Joining is voluntary, but many major corporations, such as SAP, are members and pride themselves on their high reporting scores.

“In order to drive behavior that will change in an embedded environmental footprint,

companies need to show goals.”

11

Strategy

The reason to focus on GHG output is that carbon is an effective measure of energy use, especially across a complex supply chain. The “cleaner” the process, the less GHG is emitted. Signing onto the CDP and using the tool is a cost efficient way to start collecting information and, as Mr. Bolick said, to select the most efficient and highest ROI initiatives.

He added that in addition to internal monitoring, “As companies take energy seriously, they need to know how to benchmark themselves against their peers.” Moving too aggressively, compared to others, could have a negative effect on cost competitiveness and their innovation pacing. Low goals could leave a company behind as competitors streamline their operations.

Companies who subscribe to SAP’s Business Intelligence on Demand can use SAPs

analytical tools along with CDPs data to compare their metrics against companies targeted by geography, enterprise size, or industry. Since this is not just quantitative data, but also qualitative, companies can see what their peers are putting in place. This helps executives make strategic decisions about where best to invest time and resources.

Companies know that energy is a major issue, Mr. Bolick added. With oil at over $100 per barrel and price volatility that has been 40%, more volatile in the first decade of this century compared to the last decade of the last century. This rise in prices puts increased pressure on all industries, especially those with energy as a high percentage of their operating expenses. In addition, customers are beginning to ask about a company’s policy regarding energy conservation, as those policies affect prices and possibly availability for chemical

and other processes that use petroleum as a raw material.

Rather than treating energy costs as indirect overhead, companies want to account for it as a direct material so they can manage its consumption like any other material. For manufacturers, this is particularly important. They need to be able to more accurately anticipate how they’ll be using energy and how it will impact their bottom line.

An example that Mr. Bolick cited is Valero. Valero was a single refinery company that expanded to 16 plants, largely through acquisition. There was little similarity across their acquisitions, and therefore seeing “the big picture” was difficult — if not impossible. What Valero needed was manufacturing information and intelligence that could aggregate data at 8 different levels across all their unique platforms. The goal was to ensure that every day the executive team could

“Rather than treating energy costs as indirect overhead, companies want to account for it as a direct material so they can manage its consumption like any other material.”

12look to see the consumption at each plant, narrowing down to individual machines if needed. With the system in place, Valero has seen savings of over $129 million per year in energy: more than making up for the cost of the system.

Managing Change: Sustainable Supply Chain.“In order to drive behavior that will change in an embedded environmental footprint, companies need to show goals.” The challenge for corporate leaders, with goals to reduce energy and GHG, is that resources are used and managed locally — at the operational level. For many companies this means that there is not enough visibility across the organization, Mr Bolick noted.

A company-wide data collection system can input data from automated devices on the shop floor or from data historians (applications that collect data from shop floor on health, energy, water and more), and output that data in easy-to-read dashboards that can be viewed by people up and down the supply chain.

That means that everyone, from the guy on the floor to the CEO, has real time visibility. That transparency helps drive organizational change, because everyone can be a participant, and view the results of behavioral changes in real time.

One example that Mr. Bolick mentioned is Danone, which makes a wide range of yogurt and other milk, water and juice products: in fact, they market 35,000 separate SKUs (product numbers) across 30 countries. Their brands include Activia, Dannon, Stonyfield and many others. In an extremely low margin business, efficiency and uniformity is critical. The system developed, with SAP, allows Danone brands to compare the footprint — carbon, water and energy — of one cup of yogurt produced in one place to that produced in another. Internally, Danone can see if the footprint of a product produced in one place has changed over time and develop strategies based on those fluctuations. Each manager, across all their locations, has access to the tool. Mr. Bolick noted an unexpected plus in that t h e

transparencies lead to managers talking to each other to solve problems and pass along best practices. For example, a manager in one country could see, and then ask, how a manager in a similar plant in another country was getting better results for the same or similar product.

Increased visibility also drives another key element of sustainable supply chains: making sure that products do not contain substances that are harmful to people or the environment. That can only happen by getting insight into massive amounts of data across the supply chain so that a medical device manufacturer, for example, knows exactly what chemicals are used in every component, sub-component and product their company develops or ships.

Investing in compliance makes financial sense: regulations like REACH and RoHSin, in the E u r o p e a n U n i o n ,

b a n

13

dangerous chemicals. The cost of non-compliance can be very expensive. Increasingly, consumers, NGOs and industry consortiums are putting pressure on companies to disclose exactly what is in their products. To meet these terms companies must have complete visibility across their supply chain. Bolick believes that SAP customers can achieve compliance 75 percent faster than companies not using SAP software.

Reporting: Risk and Operational ManagementThe final step is reporting, to

ensure compliance across a very wide range of issues.

Risk Management

As Mr. Bolick pointed out, “The business community can’t

stand bad press — or injury — from OSHA violations.

Pro-active prevention in mining, oil and gas industries prevents real threats to business continuity.”

An example is Baker Hughes, a global oil and gas services company. Baker Hughes has used SAP’s Environment, Health and Safety Management software to implement a proactive and risk-based approach to operational safety. As a result, they now have one global incident management system that covers 51,000 employees in 90 countries. This creates a holistic, cross-systems incident reporting, investigation, analysis, and prevention system, which has led to better communication, faster knowledge transfer, and a renewed commitment to proactive safety.

Sustainabi l i ty reporting and analytics

Increasingly, questions are being asked by investors, shareholders and boards of directors. Some large nonprofits and pension funds are demanding to see more analytics and a longer term resource reduction strategy as a part of their due diligence. Baker Hughes data collection not only monitors safety, but cost-effectively monitors water emissions management and reporting.

A small but growing number of private equity funds, such as Reference Capital, Portfolio 21 and Calvert Investments, offer funds based on sustainability metrics or responsible environmental policies, and major investment firms such as Duetsche Bank and Bank of America Merrill Lynch (A CDP investment member) have global research departments with a focus on carbon and water.

In addition, regulatory agencies are asking for environmental information: SEC (Securities and Exchange Commission) started asking for companies to report on their Carbon Risk in 2009; state environmental departments are being pressured by citizens to control air pollution; and local city authorities are increasingly worried about water conservation and grey-water reclamation.

As these pressures mount, it is easy to imagine that in five years – or less – energy and water data will be as routine as a profit & loss statement for businesses.

14

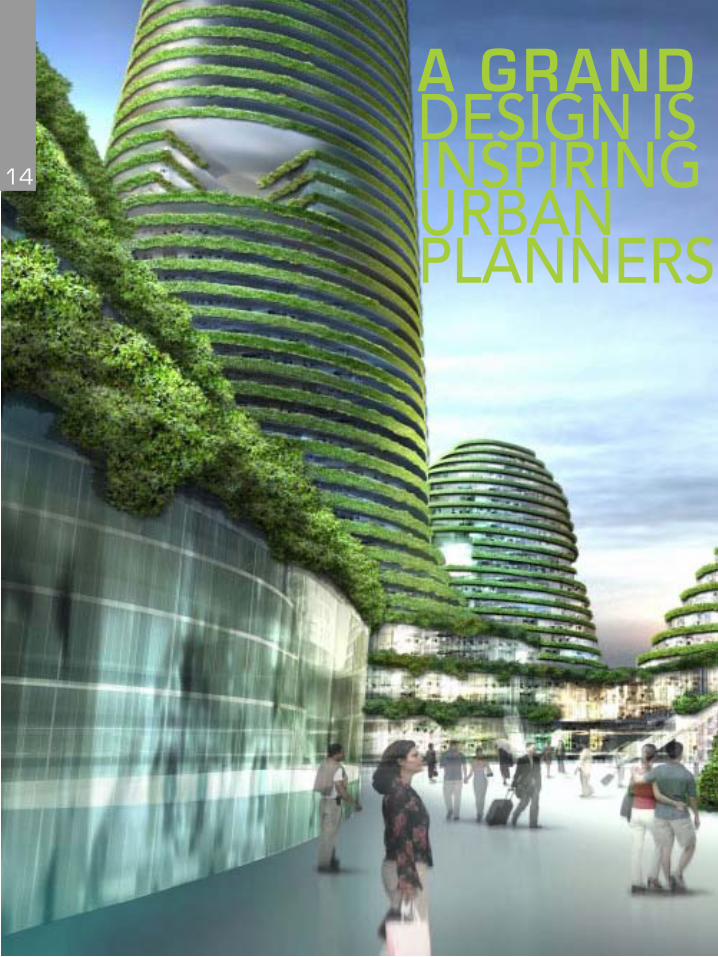

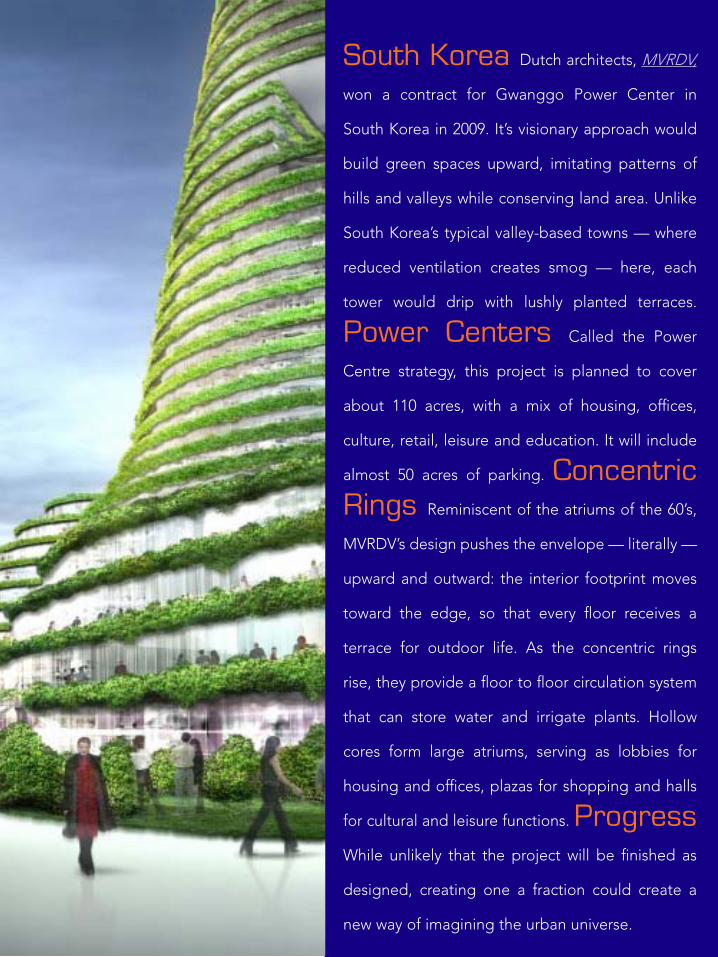

A GRAND DESIGN IS INSPIRING URBAN PLANNERS

A GRAND DESIGN IS INSPIRING URBAN PLANNERS

South Korea Dutch architects, MVRDV,

won a contract for Gwanggo Power Center in

South Korea in 2009. It’s visionary approach would

build green spaces upward, imitating patterns of

hills and valleys while conserving land area. Unlike

South Korea’s typical valley-based towns — where

reduced ventilation creates smog — here, each

tower would drip with lushly planted terraces.

Power Centers Called the Power

Centre strategy, this project is planned to cover

about 110 acres, with a mix of housing, offices,

culture, retail, leisure and education. It will include

almost 50 acres of parking. Concentric Rings Reminiscent of the atriums of the 60’s,

MVRDV’s design pushes the envelope — literally —

upward and outward: the interior footprint moves

toward the edge, so that every floor receives a

terrace for outdoor life. As the concentric rings

rise, they provide a floor to floor circulation system

that can store water and irrigate plants. Hollow

cores form large atriums, serving as lobbies for

housing and offices, plazas for shopping and halls

for cultural and leisure functions. Progress While unlikely that the project will be finished as

designed, creating one a fraction could create a

new way of imagining the urban universe.

Startup innovators

can take corporations in profitable new directions. But the challenges

may defeat the best of intentions.

Follow the rainbow and the gold pot you’ll find at the end is a treasure trove of financial reserves that corporations can’t seem to relinquish. What to do about companies like Apple – they recently announced they had $97.5 billion in combined cash, short and long-term investments – that have money they can’t quite decide how to use?

bloo

mfie

ldkn

oble

Interview by Maryruth Bresley Priebe

16

INV E S T I NINNOVATION

Michael Holman has experience with the kind of partnerships that are changing the economic (and energy) landscape. We chatted with him to see how his firm might work with a company, like Apple, to help them loosen their grip on their money to make them profitable and address important national issues at the same time.

Securing a Mega TrendThere remains a lot of uncertainty at most corporations, according to Mr. Holman. “Companies usually spend their money on developing new products or increasing manufacturing,” he explains. But during a time when demand for new products and increased production are relatively low, there’s little motivation to spend.

However, despite the uncertainty, smart companies do look for growth, especially in areas not being served well by the current solutions. Emerging companies have helped corporations take over market share and turn a

slow time into one of increased prosperity.

So how do they find that golden opportunity? “Companies are looking for global mega trends,” says Holman, who identified a few mega trends Lux is currently watching:

� Impact of fossil fuels on the environment.

� Sustainable energy generation.

� Service requirements for an aging population.

� The availability of clean water worldwide.

� Growing urbanization.

Mr. Holman expanded by giving some examples in areas he has been following.

Sustainable energy. As Mr. Holman puts it, whether or not you buy into anthropocentric climate change, the demand for more efficient fuels and alternative forms of energy is growing rapidly. That means profit.

And though some technologies are still economically unviable,

there are many others that are feasible in their own right, regardless of whether governments subsidize them or not.

Electronics and their role in efficiency.

A great deal of research is going on in electronics that convert one form of energy to another (AC to DC or vice versa); computer chips that transfer power from a car battery to the motor; and conversion devices that transform high voltage energy in order to transport it over long distances. These are technologies that can work as a market differentiator for a larger partner.

Alternat ives to the fossil fuel economy.

What Mr. Holman referred to as a renewable economy is seeing a lot of movement. Bio-based materials, for example, that can replace plastics and other petroleum-based products. They have a chance at competing, especially if the refining process

Michael Holman, PhD Director of Research Lux Research

17

can be made economically attractive.

Transportat ion. “You’re going to see a lot of incremental changes rather than big ones in vehicle technology.” He listed off innovations, like micro-hybrid technologies that provide small amounts of power to the wheels or the stereo system as examples. Lighter weight materials and better manufacturing techniques also play well in the green transportation field.

S t u m b l i n g BlocksWe asked about battery technologies as a potentially hot area for technology companies that sell devices dependent on small scale energy storage. Mr. Holman noted that the biggest restraint for any approach to manufacturing a new battery is the lack of capital. Since traditional VCs are generally not interested because of the time and size of the financial commitment, this might seem like a natural fit for companies with large financial war chests. However, it is not always that simple.

Mr. Holman notes that Lux Research’s strategy involves a

multi-step approach, starting with the development of a portfolio of relationships with startups. After proof of concept, Lux works with companies that have cash reserves, looking for a fit so that the larger company can take the project to scale, providing the funds and expertise for marketing it successfully.

However, there are some roadblocks that can get in the way of good partnerships.

For starters, Mr. Holman believes that start-ups need to be willing to take a risk, engaging with companies sooner in the process. “I was talking to someone who’s in business development in a multi-national Japanese company. He said that sometimes they come across a start-up that has gone on their own path so long, that they’ve gone too far in the wrong direction to be useful.”

Corporations can have a difficult time understanding what would-be partners really want. Since the larger partner has a wealth of marketing and production information — what works and what doesn’t — they want to have an open dialogue with a startups inventors and management. That way, the corporation can use their proprietary market expertise to help inventors tailor solutions to solve real problems.

But for a new company with little industry experience, this can be a daunting prospect. They regard the corporate partner’s need for due diligence with suspicion. As a result, there is a communication mismatch.

Holman sees — and facilitates — a real need for more back and forth. A slower process than many startups want, it can lead to a better and more robust outcome. The larger partner may not acquire or license the technology immediately, starting instead with small funding along the way while ensuring that the inventor is working on something that will lead to a successful licensing deal down the line. This is what Lux calls “integrative innovation,” which is perhaps a bit messier than open innovation, but much more effective in the long run.

About Lux ResearchLux Research is an independent research

and advisory firm providing strategic

advice and ongoing intelligence on

emerging technologies, and helping

clients profit from science-driven

innovation.

Michael Holman, PhD, and his teams

help clients — Global 500 corporations,

leading institutional investors, thoughtful

public policy makers – make better

strategic decisions.

18

“Really enjoyed the latest issue of THE GREEN ECONOMY — great stuff. The content reminds me of the reports McKinsey sends out, but focused on environmental issues.”

Arthur Dobelis

CEO, EVIV.IO

THE GREEN ECONOMY347 w36th Street, 1002New York, NY 10018

Editorial: [email protected]: 609-304-2452Sales@theGreenEconomy.comwww.theGreenEconomy.comTwitter @TGEinkTwitter @TGEexecwww.facebook.com/GreenEcon

:

Advertise With Us

19

2ND GEN. ETHANOL: BETTER TECH, ECONOMICS AND SOURCING

20

In 2010 the United States manufactured 13.2 billion gallons of ethanol, generating $825 million in export revenues. That’s the good news.

The not so good news is that the first generation relies on corn (important sources of fuel for people); has technological challenges; is reliant on federal and other subsidies; and hasn’t been able to build industries in the non-farm states.

George Boyajian, is VP of Business Development at Primus Green Energy, a company that is amongst the leaders meeting these challenges with the next generation of bio-fuels.

Primus Green Energy is producing Octane (93) that really is a tiger in your tank. And they are doing it from wood waste in New Jersey.

2ND GEN. ETHANOL: BETTER TECH, ECONOMICS AND SOURCING

21

George Boyajian, VP of Business Development at Primus Green Energy

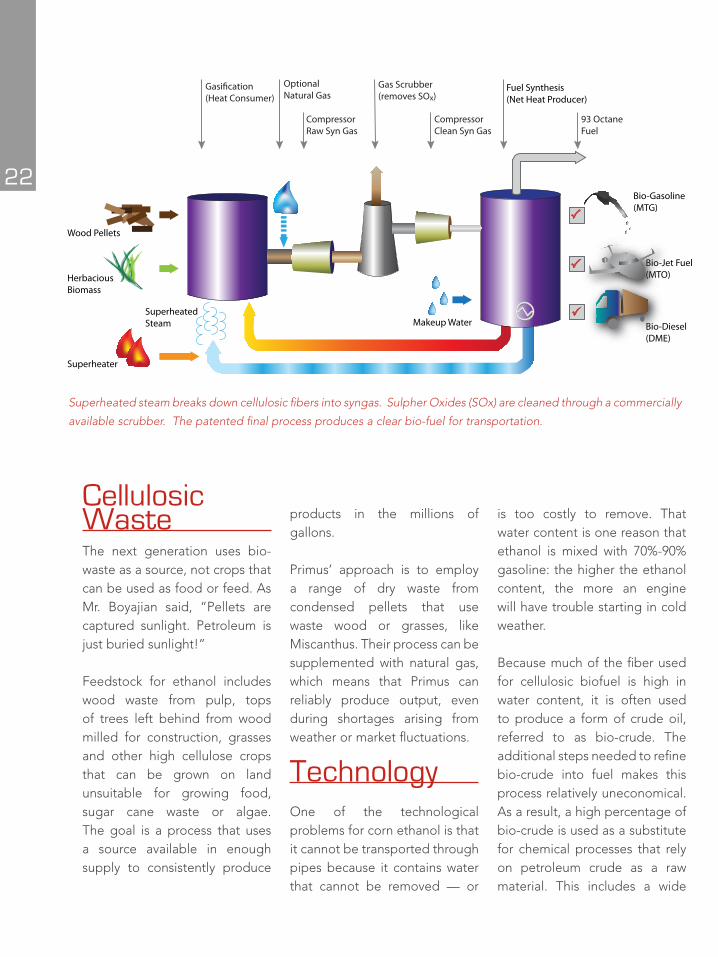

Gasi�cation (Heat Consumer)

OptionalNatural Gas

CompressorRaw Syn Gas

Gas Scrubber(removes SOx)

CompressorClean Syn Gas

93 Octane Fuel

Fuel Synthesis(Net Heat Producer)

Wood Pellets

Bio-Gasoline(MTG)

Bio-Jet Fuel(MTO)

Bio-Diesel(DME)

Makeup Water

HerbaciousBiomass

Superheater

Superheated Steam

P

P

P

Superheated steam breaks down cellulosic fibers into syngas. Sulpher Oxides (SOx) are cleaned through a commercially

available scrubber. The patented final process produces a clear bio-fuel for transportation.

22

Cellulosic WasteThe next generation uses bio-waste as a source, not crops that can be used as food or feed. As Mr. Boyajian said, “Pellets are captured sunlight. Petroleum is just buried sunlight!”

Feedstock for ethanol includes wood waste from pulp, tops of trees left behind from wood milled for construction, grasses and other high cellulose crops that can be grown on land unsuitable for growing food, sugar cane waste or algae. The goal is a process that uses a source available in enough supply to consistently produce

products in the millions of gallons.

Primus’ approach is to employ a range of dry waste from condensed pellets that use waste wood or grasses, like Miscanthus. Their process can be supplemented with natural gas, which means that Primus can reliably produce output, even during shortages arising from weather or market fluctuations.

TechnologyOne of the technological problems for corn ethanol is that it cannot be transported through pipes because it contains water that cannot be removed — or

is too costly to remove. That water content is one reason that ethanol is mixed with 70%-90% gasoline: the higher the ethanol content, the more an engine will have trouble starting in cold weather.

Because much of the fiber used for cellulosic biofuel is high in water content, it is often used to produce a form of crude oil, referred to as bio-crude. The additional steps needed to refine bio-crude into fuel makes this process relatively uneconomical. As a result, a high percentage of bio-crude is used as a substitute for chemical processes that rely on petroleum crude as a raw material. This includes a wide

23

range of plastics, polymers and textiles, a very large market. However, it does not address the need for a “home grown” fuel to meet the need for fuel security, nor as replacement for corn ethanol.

Primus’s process, however, produces a high grade octane (93), which must be mixed with 20% gas to bring it down to high test. As Mr. Boyajian put it, “You can put it right in your tank, but it is such a high octane it doesn’t produce enough vapor to start in a standard engine. But once it’s going, you’ll really cruse!”

Reducing the water content is a two-step process for Pimus. First, they begin with dry pellets. Primus plans to produce 500 pounds of gasoline from a ton of pellets: 25% output per mass. The goal is 33%, which Primus claims is considerably higher than the 12% produced from other processes. The second step is that the water that is produced, floats to the top of the high octane fuel as a greyish fluid within minutes. It is easily removed during the final phase and returned to the first phase

as superheated steam used for breaking down cellulosic fibers into syngas.

Business ModelMr. Boyajian noted that “we all knew in the 90s that 1st generation ethanol wouldn’t work without government subsidies.” As new technologies bring the costs of production down, and as oil prices continue to climb, he believes that the next generation can compete on its own.

A key differentiator for Primus, says Mr. Boyajian, is that the company is really smart about the industry. They look to de-risk development and deployment, often by milling their own parts on site. This saves time and is more efficient, cutting down costs of sending parts out to be fabricated, and then having to tweak them later, and keeps the expertise in house. Once the prototype is developed, Primus works with Bechtell to ensure that the model is scalable ti size and to pre-test any construction issues that might arise.

Secondly, the 2nd generation is able to develop products working with seasoned engineers and technologists that have experience with the market, as well as with products, production and technology. Many who come out of retirement because they are intrigued by Primus’s technology, are also invested in creating a country that’s green, clean and secure for their kids and grandchildren. Mr. Boyajian noted that those who have come out of the armed forces see the economic benefits of not sending expeditionary forces into foreign lands in the hunt for fuel.

Finally, they are entering into long term contracts, with companies like Aloterra, for supplies of miscanthus giganteus as it develops, and with pellet manufacturers. In addition, the company is starting plans now for new sites, as well as exploring leasing options, especially near producers of cellulosic waste such as wood millers, pulp plants and shellers with large quantities of nut casing waste, and pellet manufacturers who can use the heat generated by Primus’s

“Pellets are captured

sunlight. Petroleum is just

buried sunlight!”

“You can put it right in your

tank, but it is such a high

octane it doesn’t produce

enough vapor to start in a

standard engine. But once it’s

going, you’ll really cruse!”

“I am very sanguine about the

US, I think we can reduce our

dependency on foreign oil by

as much 40% in the next few

years,”

24

process to defray the costs of heat used for drying fiber.

Jobs“I am very sanguine about the US, I think we can reduce our dependency on foreign oil by as much 40% in the next few years,” summarized Mr. Boyajian. In investing in New Jersey, he notes that it has a history of technological innovation dating back to Thomas Edison, and including Bell Labs and the Princeton Plasma Physics

Laboratory. “There’s a lot of talent here, “ he added. “We find trained people whose families came from all over the globe.”

He also noted that the United States has good intellectual property laws, which is very important to a company that has invested heavily in research and development.

Primus itself began with a staff of 2 and are now up to 40. As they build, they will need

pipe fitters, values, pumps, fire safety, and even fencing and basic construction on their first commercial facility which will start construction in 2013, with plans to be online in 2015. As important, the company is not planning to build a demonstration plant, cash out and start something else: they want to be around for the long haul.

ALOTERRAAloterra is banking on the 2nd generation of bio-fuels. They are building a national network that is enhancing small and large farmers across the country.

25

Similar to the establishment of the major oil refineries fifty years ago, biomass refineries require a consistent and economical feedstock supply to justify major investments. The strengths in a conversion technology alone cannot overcome the massive logistical challenges associated with feedstock.

In 2010 and 2011, Aloterra leveraged the Biomass Crop Assistance Program (BCAP) to become the Project Sponsor of four separate BCAP Project Areas in the United States. Aloterra now has a total of 18,000 acres of the energy crop miscanthus giganteus under contract to be grown in Ohio, Pennsylvania, Missouri, and Arkansas. The Project Areas located in Missouri and Arkansas are being established through a 40,000 member farmer cooperative based in Missouri.

At maturity, each Project Area will produce 600,000 dry tons of annual biomass for a total of 2.4 million tons of biomass each year. Initial yields of 100,000 tons per year will be harvested after the 2013 growing season.

For more, see their website.

26

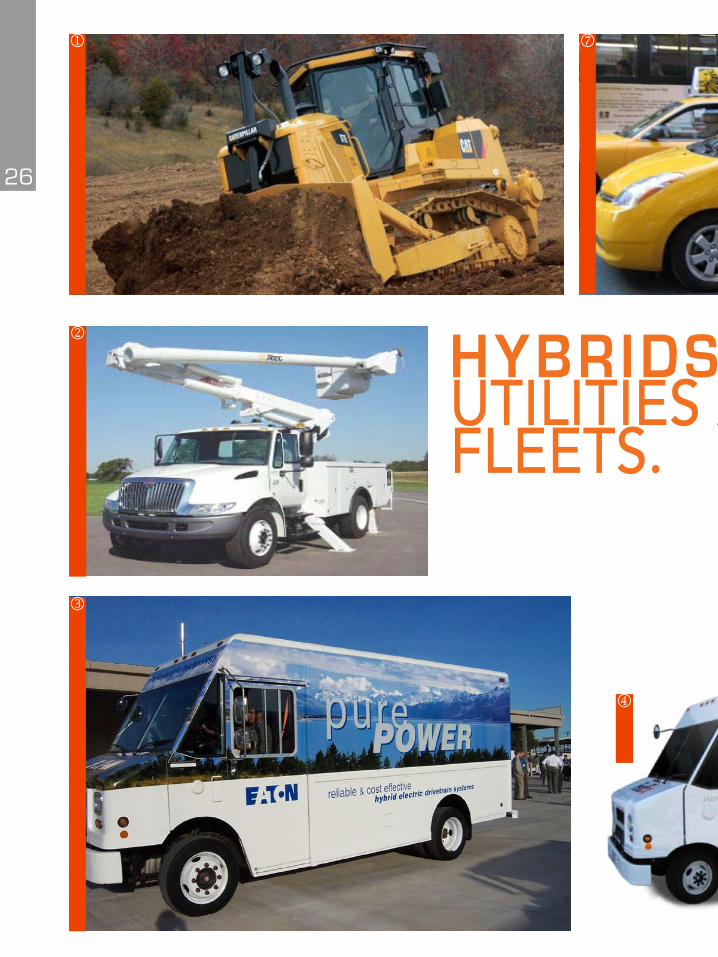

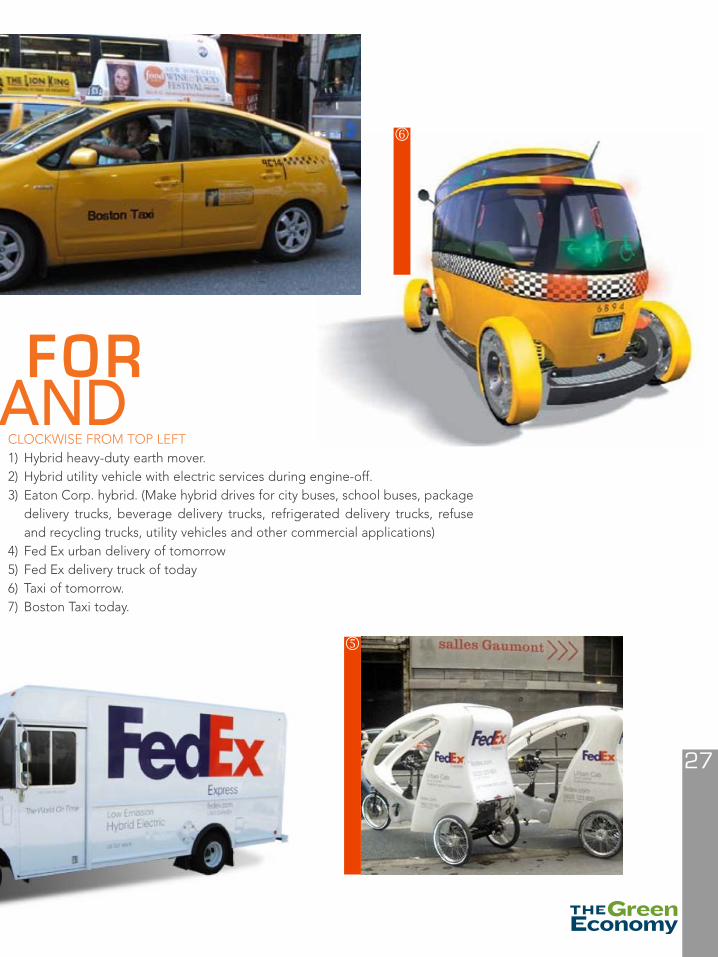

HYBRIDS FOR UTILITIES AND FLEETS.

j

k

l

m

p

27

CLOCKWISE FROM TOP LEFT1) Hybrid heavy-duty earth mover. 2) Hybrid utility vehicle with electric services during engine-off. 3) Eaton Corp. hybrid. (Make hybrid drives for city buses, school buses, package

delivery trucks, beverage delivery trucks, refrigerated delivery trucks, refuse and recycling trucks, utility vehicles and other commercial applications)

4) Fed Ex urban delivery of tomorrow 5) Fed Ex delivery truck of today 6) Taxi of tomorrow. 7) Boston Taxi today.

HYBRIDS FOR UTILITIES AND FLEETS.

n

o

NORTH AMERICAN FACTORY ACTIVITY HAS INCREASED FOR THE 30TH CONSECUTIVE MONTH.65% ARE INVESTING IN NEW TECHNOLOGY

28

29

“These are both very positive signs for expanding growth in the manufacturing sector,” explains Mitch Free, CEO of MFG.com, the world’s largest online marketplace for the industry, often called the “eBay of manufacturing”.

Mitch Free, CEO @ MFG.com

0%

10%

20%

30%

40%

50%

60%

Q4 Q3 Q2 Q1 Q4 Q3 Q2 Q1

2010 2011

Returned a portion of production to US

Researching

In the current quarter, for your North American consumers, did your company return, or research returning, any portion of production into or closer to North America from a low-cost country?

30

Re-shoring: bringing it back home22% of companies have or are the process of reshoring back to North America, a 3% uptick, 33%

of manufacturers researching reshoring, an increase of 7%, There are several factors that are contributing to moving sourcing from a low-cost country, such as China.

Supply Chain Disruption

Buy-side product manufacturers have taken measures to mitigate their supply chain risk, ramping up several suppliers and diversifying geographically. Reasons include:

� Over the last few years, many small manufacturers that supply bigger companies got wiped out during recession: a major supply chain disruption for those larger manufacturers. These larger companies have had to find a new

11%

25%

27%

37%

SellersHiring

Tech Investing

Both

Neither

Neither

11%

28%

26%

35%

BuyersHiring

Tech Investing

Both

31

suppliers, which is a long-term task: they must send drawings, produce parts and components, and often manage a lengthy quality control process in order to get quality right.

� Disasters such the earthquake and tsunami took out a lot of suppliers, leaving large supply chain gaps that resulted in lengthy product delays.

This practice is a change from LEAN manufacturing, where the goal is to reduce vendors and complexity in the supply chain. As Mr. Free said, “We’re a society that likes to customize — different colors, patterns and so forth. The days of orders of 1 million that are exactly the same is over. It isn’t a strategy that resonates, because consumers like new versions.”

RisksBusiness and operational risks are driving

some companies to seek the safety of U.S. shores.

� The total landed cost of products. For example, the price of production in Vietnam may not defray the costs of shipping, delivering through customs, and the travel and manpower needed to manage development and quality control,

� The current high price of fuel, and the expectation of higher prices to come, are a big concern.

� The U.S. dollar is currently cheap, which can add in incremental benefit.

� Companies are looking to be nimble and place smaller orders. An oversees supplier may need a million part order, and that order will take a long time to be delivered. If consumer demands falls, than the manufacturer may be stuck with a large inventory of unsalable units. In order to be in closer lock step with consumer demand, industrial buyers would like to place smaller

orders and receive delivery in a more timely manner.

� There are intellectual property protection that threaten sourcing strategies. This is a big barrier when owners — or employees — of foreign companies can easily start new ventures based on a U.S. intellectual property.

New InvestmentIn spite of some of these challenges, 63% of

sellers, and 65% of buy-side product manufacturers are aggressively investing in new technology, hiring, or investing in new technologies and hiring. This is a positive sign for growth.

Buy side companies that design and produce products generally don’t manufacture themselves. Apparel and other consumer product companies own the brand, but not their own factories. They are investing in technologies that allow them to customize faster: new colors for electronics, new materials that are customizable on the fly, and more durable.

0% 10% 20% 30% 40% 50% 60%

Extensive GovernmentRegulations

Logistics, Shipping& Energy Costs

Operating Costs

Rising Taxes

Trade PolicyReform and Deficit

GovernmentBudget Deficit

Availablity ofQualified Labor

Access toCapital Q2 2011

SUPPLIERS

BUYERS

Q3 2011

Q4 2011

Q2 2011

Q3 2011

Q4 2011

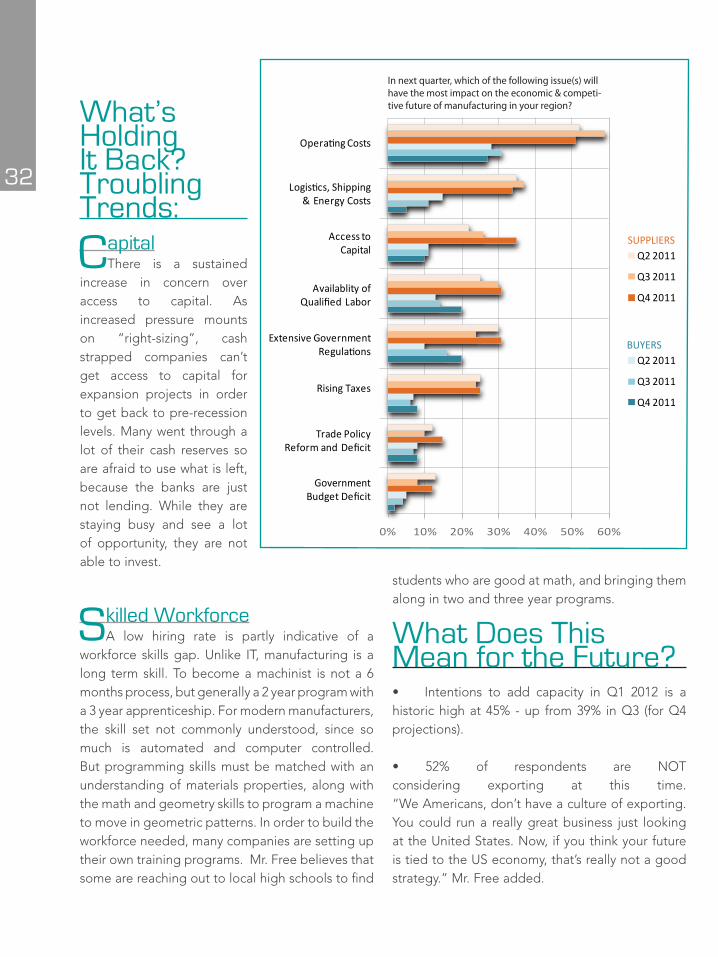

In next quarter, which of the following issue(s) will have the most impact on the economic & competi-tive future of manufacturing in your region?

32

What’s Holding It Back? Troubling Trends:

CapitalThere is a sustained

increase in concern over access to capital. As increased pressure mounts on “right-sizing”, cash strapped companies can’t get access to capital for expansion projects in order to get back to pre-recession levels. Many went through a lot of their cash reserves so are afraid to use what is left, because the banks are just not lending. While they are staying busy and see a lot of opportunity, they are not able to invest.

Skilled WorkforceA low hiring rate is partly indicative of a

workforce skills gap. Unlike IT, manufacturing is a long term skill. To become a machinist is not a 6 months process, but generally a 2 year program with a 3 year apprenticeship. For modern manufacturers, the skill set not commonly understood, since so much is automated and computer controlled. But programming skills must be matched with an understanding of materials properties, along with the math and geometry skills to program a machine to move in geometric patterns. In order to build the workforce needed, many companies are setting up their own training programs. Mr. Free believes that some are reaching out to local high schools to find

students who are good at math, and bringing them along in two and three year programs.

What Does This Mean for the Future? • Intentions to add capacity in Q1 2012 is a historic high at 45% - up from 39% in Q3 (for Q4 projections).

• 52% of respondents are NOT considering exporting at this time. “We Americans, don’t have a culture of exporting. You could run a really great business just looking at the United States. Now, if you think your future is tied to the US economy, that’s really not a good strategy.” Mr. Free added.

What’s Missing from Your Wind Project?

When Competitive Power Ventures Inc. (CPV), a power generation development and asset management company with extensive wind energy development experience, decided to sell Phase I of its Keenan wind farm project to Oklahoma Gas & Electric Company, CPV turned to Dickstein Shapiro’s experienced wind energy and corporate counsel to structure, negotiate, and document the transaction. CPV continues to rely on Dickstein Shapiro’s energy transactional and regulatory attorneys in connection with all aspects of its wind energy development program to help ensure that it remains a signifi cant player in the North American wind energy sector.

“In today’s ever-changing energy market, the success of our power generation development program requires a unique mix of regulatory and transactional experience, and Dickstein Shapiro excels in both.”

Doug Egan Chairman, Competitive Power VenturesCEO, CPV Renewable Energy Company

WASHINGTON, DC | NEW YORK | LOS ANGELES | IRVINE

Prior results do not guarantee a similar outcome. 1825 Eye Street NW, Washington, DC 20006© 2010 Dickstein Shapiro LLP. All Rights Reserved. (202) 420-2200 | dicksteinshapiro.com

Larry Eisenstat, Energy Practice Leader

(202) 420-2224 I [email protected]

33

• More education needed on the benefits of exporting for small business.

• Operating costs will continue to be a major concern in 2012

CEO, Mitch Free adds, “Our reshoring statistics tend to indicate that economic conditions have started to produce sound business reasons for bringing work back to North America and product manufacturers continue to see value in exploring this option for their business.”

About MFG.comFounded in 2000, MFG.com is the largest global online marketplace for manufacturers looking to source custom parts, standard components, assemblies and textiles. MFG.com has

revolutionized the way parts get sourced, bringing tremendous efficiencies to its users. Since 2000, $117,982,615,784 has been sourced through MFG.com.

MFGWatch is a quarterly, recurring survey conducted by MFG.com of North American Supply-Side Job Shop and Contract Manufactures as well as Buy-Side OEMs and Product Manufacturing companies. The survey is conducted via e-mail from a sampling of MFG.com member companies (over 100,000), and is intended to reflect projected (intent) and reported (actual) behaviors of companies in the North American manufacturing sector. Industries represented include aerospace/aeronautics, automotive, medical, defense, textiles and consumer products manufacturers.

Full report available for download here.

The multi-billion dollar solar market is capturing the attention of companies looking for long term opportunities with stable technologies, a captive audience of energy users, and a source of free raw materials: the sun.Electricity users spent $368,906,000,000 ($368 billion) in 2010, keeping the lights on, computers running, temperatures from rising or falling, and much more, according to the US Energy Information Administration. At under 5% of the market, $14 billion is attributed to renewables including solar, wind and geothermal.

This is a large enough market to move companies to see solar as a strategic corporate investment, said Pallavi Madakasira, Analyst at Lux Research. That investment is essential to ramp capacities

and building process efficiency, taking up the slack as Venture Capital for energy weakens. She went on to highlight compelling reasons for corporate engagement, including the price of solar dropping, a move by Utilities into development, the need to open new markets, continued government action and long term stability.

PV Prices DroppingEconomies of scale are becoming increasingly important as module prices have fallen dramatically in the last 2-3 years. One factor is the drop in silicon prices, which have gone from a high of $400/kilo in 2008 to as low as $25/kilo today. Of the leaders in mono-crystalline silicon panels, Ms. Madakasira mentioned SunPower in the top three listed solar companies with a market capitalization of $750m, and Sanyo Electric, which has been bought by Panasonic. She expects that the pressure on size will contribute to more mergers and acquisitions in 2012 and beyond.

Utilities Invest in DevelopmentUtilities started looking at development as prices approached grid parity–that is costs close to that of natural gas or other fuels. This trend is in addition to their traditional role buying the output from other developers through Power Purchase Agreements (PPA). As an example, Duke Energy‘s 14-megawatt Blue Wing Solar Project in San Antonio, Texas,

SOLAR IS BIG BUSINESS FOR BUSINESS34

consists of nearly 215,000 PV panels and is among the largest solar farms in the country. PSEG owns almost 50 Megawatts at their Wyandot, JEA and Mars Solar Farms. American Electric Power (AEP) is investing $20 million in an Ohio solar farm that will generate 49.9-megawatt (MW), will be built on approximately 750 acres of reclaimed land, and will generate more than 600 direct jobs and approximately 300 during the construction and installation.

Those who continue taking advantage of PPAs include many players throughout the world. As an example, Integrys Energy Services and Duke Energy have invested in projects developed by Smart Energy Capital. Smart Energy Capital’s PPA is an agreement between them and their clients: commercial, government and utility customers. Their model builds (including costs of design, permitting, installation and so forth) and owns projects on client sites. The client agrees to purchase the output at a price below their utility fees, but invests no capital up front.

Global Partnerships Open Up New MarketsSome partnerships are multidimensional, transferring skills that US Corporations have that newer or smaller companies need. For example, DuPont is partnering with Suntech, providing not just technology advancements –such as DuPont’s

Tedlar® polyvinyl fluoride film which is used in the process of making solar panels — but also supply chain optimization, cost reduction and co-marketing.

Others are looking for expanding markets, especially in emerging economies where power needs are growing faster than energy production, and where localization and climate are likely to favor solar. GE recently invested in a Kenyan solar field. US based BrightSource Energy is working with the clean energy unit of Sasol (a South African company best known for the conversion of coal and gas into fuels and chemicals) to study plans for a utility-scale solar power plant in their home country.

Ms. Madakasira noted that China is looking abroad in order to expand their markets, especially into Asian nations like India and Malaysia. However, many, like India, have regulations on percentages of local sourcing that make Chinese products non-competitive. As a result, companies like JA Solar and LDK Solar are looking for partners who can build locally. Yingli, another Chinese company, has agreed to supply 180 MW of multicrystalline and monocrystalline (Panda) PV modules to IBC SOLAR AG, a German company. TSMC (Taiwan Semiconductor Manufacturing Co.) put $50 million into Stion, a somewhat secretive solar module maker that uses copper indium gallium selenide (CIGS), and has plans for a two-for-one solution

35

with another layer that can generate power chalcopyrite.

Les Hinton, then President of Dow Jones & Publisher of the Wall Street Journal in July 2011, at opening ceremonies.

Governments Continue to Play a RoleSolarWorld, one of the world’s largest solar energy businesses with 3,300 employees, has been actively lobbying for a tariff on Chinese products, which are heavily subsidized by the Chinese government. Ms. Madakasira sees this as a mixed blessing. On the one hand, it could be good for Western solar manufacturers. On the other, it could drive prices up, which would not be good for consumers. She believes that a U.S. Tariff is a real possibility, but a possibility is a long way from a certainty.

While U.S. Federal incentives for solar and renewables are ending, a great deal of local support is still in place. One of the incentives for utilities to enter into PPAs with solar developers are Renewable Portfolio Standards (PRS) set by states, which mandate a percentage of power that must be derived from renewable sources. For utilities, PPAs can be a triple win: the Utility meets a local mandate, can avoid development costs and hassles, and locks in power at a price that is likely to rise in the future–meaning they can sell the power for more than they pay for it. For developers, the project produces long-term revenue and, in

the case of installations with power costs–such as buildings–the owners may get long-term set rates for energy they use as part of the PPA. For corporations, this can be an opportunity to work with developers on the upfront costs of getting to a PPA, in return for a percentage of the gains from the sale of the power to utilities.

Kitson & Partners is teaming with Florida Power & Light to create a city powered entirely by solar energy.

Corporations with large physical plants can use such agreements to stabilize energy costs, providing long-term savings, as well as marketing and brand benefits. In Princeton, New Jersey, Dow Jones and the reinsurance giant Munich RE put in place solar panels that shelter parking lots and provide energy.

Long-Term, Solar Value Will Remain StableFor the long-term, a technology “game changer” has not appeared on the horizon. Solar paneled satellites that work 24/7 and beam energy to earth are still a pipe dream; not yet near production. However, efficiencies of 25% are on the horizon: the best panels now boast 22% under optimal conditions. Yet demand is building in Africa and Asia, and the U.S. market will continue to grow steadily. For corporations looking to minimize risk, invest for the long run or expand revenue, solar can be a great strategic investment.

36

37

Speakers from:Brown Rudnick

CapitalFusion Partners

CH2M Hill

Clearpoint Ventures

ConEdison

Deutsche Bank

Environmental Defense Fund

IBM

Jane Capital

JP Morgan

New York Power Authority

PepsiCo

SNL Energy

United States Energy Association

In its 11th year,the Wall Street Green Summit is where to meet decis ion makers in f inance,

Register for the event, virtual booth or after event materials

Agenda for two day event

Sponsorship opportunities

Speakers A Global Change Event

Not what you know today.

It’s what’s in the future.

Yesterday it

was enough

to know

a c ce l e ra te d

depreciation, EBITDA, earnings per share, capital ratio. Today, leading

companies are reporting carbon risk, developing the ROI for efficient

energy and resource management, and looking at ESI statistics. With

all these new initiatives, how do you measure the opportunities and

avoid the risks in new investment strategies?

Finding the right metrics—and having

the tools to analyze them—is the job of

CRD Analytics.CRD reports on the market strength of companies by analyzing their

reporting procedures through a series of metrics including financial,

environmental, social, governance and patent information. The Smart-

Viewtm algorithms give a better, holistic view of corporate perfor-

mance, as well as an index for measuring the competitive advantage

of a company witin their market sector.

For more information, to obtain a listing

of all CRD Analytics indexes, or to find out

more about CRD, please visit us online or

call our office.

www.crdanalytics.com

New York

116 West 23rd Street, 5th Floor

New York, NY 10011

646-375-2122 x2281