investment opportunities for uk companies in the...

TRANSCRIPT

Investment opportunities for UK Companies in the Nigerian Insurance Sector

Presentation by

Mr Babajide Oniwinde

Deputy Director, Corporate Strategy

National Insurance Commission

at the

Industry Leaders Forum of the Financial & Professional Services Mission to Nigeria held

in Lagos on 17th March 2014

Doc ID L

ast M

od

ified

P

rinte

d

|

Presentation Outline

Introduction

Regulation of the Insurance Sector

Industry Structure

Performance of Insurance Companies

Developments in the Insurance Sector

Areas of Opportunities

Conclusion

.

1

Doc ID L

ast M

od

ified

P

rinte

d

|

Introduction

Nigeria is the second highest contributor to the

GDP for sub-Sahara Africa.

Nigeria financial services market is developing

fast and 39% of the adult population have

access to banking services compared to just 2%

for insurance services. The capital market is a

top performer.

.

2

Doc ID L

ast M

od

ified

P

rinte

d

|

Introduction

There is a growing middle class emerging and

increasing number of high net worth individuals

who would need insurance for their assets.

Awareness of financial services products is

growing and the regulators and policy makers

are intervening through legislative reforms to

strengthen the banking and insurance

institutions and improve the image in the eyes

of the public.

.

.

3

Doc ID L

ast M

od

ified

P

rinte

d

|

Quick Reminder of our situation….cont’d World’s Largest Economies (GDP- Nominal)

World Bank (2011)

Rank

Country GDP (Millions of US$)

Rank Country GDP (Millions of US$)

1. United States 15,094,000 12. Spain 1,490,810

2. China 7,298,097 13. Australia 1,371,764

3. Japan 5,867,154 14. Mexico 1,155,316

4. Germany 3,570,556 15. South Korea 1,116,247

5. France 2,773,072 16. Indonesia 846,832

6. Brazil 2,476,652 17. Netherlands 836,257

7. United Kingdom 2,194,750 18. Turkey 773,091

8. Italy 2,194,750 19. Switzerland 635,650

9. India 1,859,747 20. Saudi Arabia 576,824

10. Russia 1,857,747 27. South Africa 408,237

11. Canada 1,736,051 41. Nigeria 235,923

Source: Wikipedia, www.wikipedia.org/wiki/list_of_countries_by_GDP(nominal)

Slide 4

Doc ID L

ast M

od

ified

P

rinte

d

|

African and West African Countries (International Monetary Fund, 2011)

African Countries GDP West African Countries (GDP )

Rank Country GDP (Million of US$)

Rank Country GDP (Million of US$)

1. South Africa 408,074 1. Nigeria 238,920

2. Nigeria 238,920

3. Egypt 235,719 2. Ghana 37,158

4. Algeria 190,709 3. Ivory Coast

24,096

5. Angola 75,508 4. Senegal 14,461

6. Morocco 99,241 5. Mali 10,600

7. Sudan 64,750 6. Burkina Faso

9,981

8. Tunisia 46,360 7. Benin 7,306

9. Ghana 37,158 8. Niger 6,022

10. Libya 36,874 9. Guinea 5,212

Source: Wikipedia, the Free Encyclopedia; Slide 5

Doc ID L

ast M

od

ified

P

rinte

d

|

The National Insurance Commission was established in 1997 by

the National Insurance Commission Act 1997 with the

responsibility for ensuring the effective administration,

supervision, regulation and control of insurance business in

Nigeria and protection of insurance policyholders, beneficiaries

and third parties to insurance contracts.

Regulation of Insurance Sector

Licensing Enforcement actions

Inspections Standard for professional

competence

Monitor capital and solvency Product approval

Approve annual financials Branch Approval

Complaints handling Appointment approval

Consumer education Financial inclusion

Slide 6

Doc ID L

ast M

od

ified

P

rinte

d

| 7

Industry Structure

Strengths and weaknesses of the insurance sector

1. Growing Economy 1. Little innovation to enter untapped area

2. Improved Confidence in financial system 2. Low claims ratio

3.Active and enhanced Regulation 3. Inflation affects disposable income

4. Premium is growing 4.Lack of reliable data

5. Increase in number of policyholders 5. Crime rate affects claims

6. Increase in FDI and Partnerships 6.Legal system/Length court process

7. High penetration of mobile phone subscribers

7. Unhealthy competition

8. Enforcement of compulsory insurance 8. Overconcentration on the corporate side

9. Rising Middle class and high net worth people.

9. Shortage of technical expertise

Doc ID L

ast M

od

ified

P

rinte

d

|

Strength

• Migration to Alternatives to cash • Financial Inclusion • Deepening Stock Market • Increased bank capital • Automated bank services • Risk based regulatory framework • Industry reforms in Insurance

Sector, Pensions & Capital Market. • Pension reforms

Weakness

• Infrastructure Lag • Poor corporate governance • Poor risk management framework • Poor credit level as percent of the

GDP • Insurance & Capital market

challenges

Opportunities

• Sound banking systems • Good international financial ratings • Increased credit to private sector • Available human and material

resources • Effective utilization of the Pension

funds

Threats

• Challenges of the fight against corruption

• Lack of professional manpower • Market volitility • Political uncertainties • Social unrest • Fiscal Discipline

Financial Sector SWOT

Slide 8

Industry Structure

Doc ID L

ast M

od

ified

P

rinte

d

| 9

2 Reinsurance Companies (Minimum Capital N10b

576 Insurance Brokers.

2250 Insurance Agents

48 Loss Adjusters

700 branches of Insurance Cos.

10 companies have majority foreign share ownership.

One Government owned NAIC – for Agric Insurance

Industry Structure

Industry Structure

17 • Life Insurance

Companies ( N2b minimum Capital)

33

• General Insurance Companies ( N3b minimum Capital)

9

• Composite Insurance Companies( N5b minimum Capital)

59 Insurance Companies

Doc ID L

ast M

od

ified

P

rinte

d

|

Increase interest of foreign investors in the market.

Investors are

bring capital, manpower as well as innovation into the market.

Huge reinsurance to London market

Insurance

Company Foreign Interest

ADIC NSIA

Oceanic Insurance

Old Mutual

Mansard Insurance

European Consortium

Prestige Assurance

New India, India

FBN Life Samlam South Africa

UBA Metro Met Life South Africa

Continental Reinsurance

US Private equity

Femi Johnson Marsh (MMC) UK

10

Industry Structure

Foreign Interest in Insurance

Doc ID L

ast M

od

ified

P

rinte

d

|

.

11

COMPANIES WITH LARGEST SHARE OF THE MARKET

Industry Structure

Doc ID L

ast M

od

ified

P

rinte

d

|

Performance

DISTRIBUTION OF PERFORMANCE OF COMPOSITE INSURANCE BUSINESSES BY MARKET SHARE IN MILLIONS OF NAIRA AND PERCENTAGE IN 2012

Chart 12

FIRE 24,990.02

11%

ACCIDENT 30,706.67

13%

MOTOR 45,421.77

19%

W/COMP 1,008.87

0% MARINE 22,558.84

10%

OIL & GAS 37,289.39

16%

LIFE 57,996.13

25%

MISC 13,781.19

6%

Doc ID L

ast M

od

ified

P

rinte

d

|

.

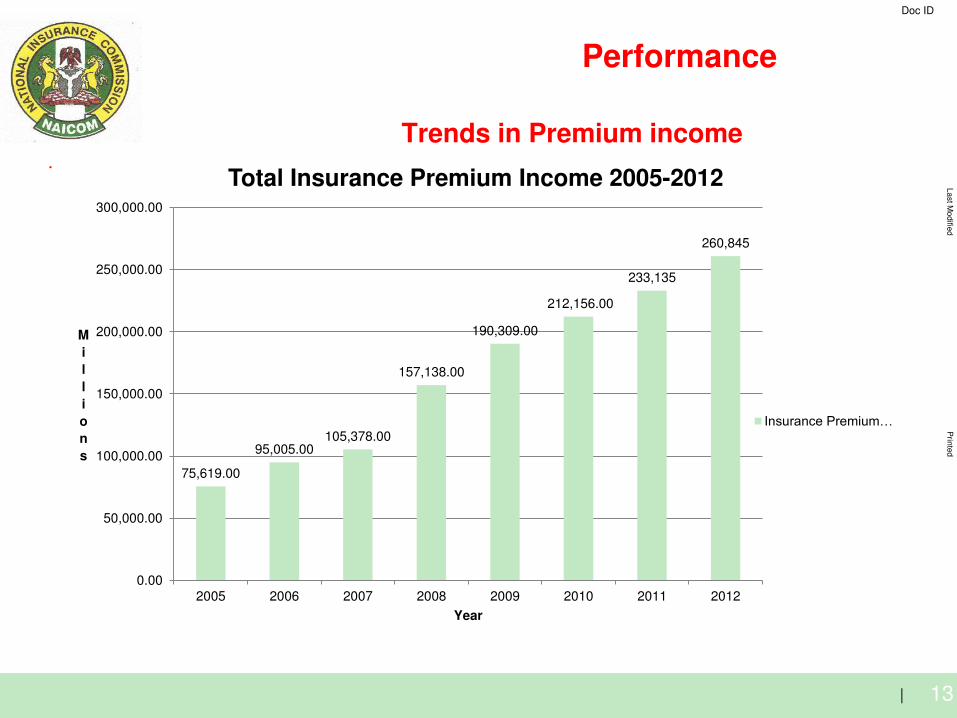

13

Trends in Premium income

Performance

75,619.00

95,005.00 105,378.00

157,138.00

190,309.00

212,156.00

233,135

260,845

0.00

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

2005 2006 2007 2008 2009 2010 2011 2012

M

i

l

l

i

o

n

s

Year

Total Insurance Premium Income 2005-2012

Insurance Premium…

Doc ID L

ast M

od

ified

P

rinte

d

|

.

14

Industry performance trend

Performance

December

2010

December

2011

December

2012

1

Total Assets (N’b) 585

621

635

Technical Reserves (N”b) 141

170

204

2

Total Premium (N’b) 212

233

260

3

Total Claims paid (N’b) 53

60

75

4

Number of Branches 658

658

655

6

Claims Ratio (%) 20

25

24

Doc ID L

ast M

od

ified

P

rinte

d

| 15

Developments in the Insurance Sector

Insurance companies have started sending in their accounts in IFRS formats.

NAICOM is working closely with FRC on monitoring compliance with IFRS.

Sensitization workshops have been conducted throughout 2012 for CEOs, Board members, CFOs, External Auditors on IFRS.

IFRS

Doc ID L

ast M

od

ified

P

rinte

d

| 16

Developments in the Insurance Sector .

Forced resignation of the Board of one insurance company over issues of Corporate Governance and financial reporting.

Interim Managing Board appointed to control the affairs of the company.

Suspension of another insurance company from taking on New business pending investigation regarding Corporate Governance issues.

Corporate Governance

Doc ID L

ast M

od

ified

P

rinte

d

| 17

Developments in the Insurance Sector

Guidelines on Risk management Framework for insurers and reinsurers was released in February 2012.

Companies are employing various tools for identifying, analyzing and monitoring risk to which they are exposed.

Risk Management

Doc ID L

ast M

od

ified

P

rinte

d

| 18

Developments in the Insurance Sector .

The guideline requires that cover will not take effect until premium is paid in full by the insured.

There has been a considerable improvement in the prompt payment of premiums to insurance companies as a result of this guideline this improved liquidity and cash flow.

No Premium No Cover

Doc ID L

ast M

od

ified

P

rinte

d

|

Enforcement of Compulsory Insurance

MARKET DEVELOPMENT

COMPULSORY INSURANCE AWARENESS CAMPAIGN

Compulsory insurance – mandatory by law for the protection of 3rd parties and the general public. Motor – all vehicle owners. Group life – where 4 or more employees are is compulsory to insure life of the employees. Medical professional liability – doctors , nurses and other health care team in case of medical negligence that cause death or injury. Public building – to which members of the public have access must be insured. Building under construction – for owners of building of more than two floors under construction. Employers liability – for employers of labour. 19

. Developments in the Insurance Sector

Doc ID L

ast M

od

ified

P

rinte

d

|

Agriculture Insurance

Continue to protect policyholders that are farmers by the regulation of the the Nigerian Agriculture Insurance Corporation that manages the Agricultural Insurance Scheme. It covers the risk of flood, drought, fire, storms, outbreak of disease, sale of seeds, fertilizers, pesticides etc. protect against financial consequences of this losses.

Developments in the Insurance Sector

Doc ID L

ast M

od

ified

P

rinte

d

|

Oil & Gas Risk Retention

The local content Act allows companies to retain insurancee risk by up to 70% provided they have the capacity.

Developments in the Insurance Sector

Doc ID L

ast M

od

ified

P

rinte

d

| 22

Developments in the Insurance Sector .

Micro Insurance diagnostic study was conducted to assess the demand and supply of insurance policies to the low income to facilitate financial inclusion

Legal frameworks for Micro-insurance Telecom service providers distribution. micro insurance scheme to support their poverty alleviation programmes.

Micro Insurance

Doc ID L

ast M

od

ified

P

rinte

d

| 23

Developments in the Insurance Sector .

A framework has been developed for Takaful operation. This is in consultation process.

The Commission has also become a full member of the standard setting organization Islamic Financial Services Board(IFSB).

There are proposals for a standalone Takaful company.

Takaful Guideline

Doc ID L

ast M

od

ified

P

rinte

d

| 24

Developments in the Insurance Sector .

The IMF Technical Assistance Mission helped in populating and testing the AML/CFT Risk-based Supervision Matrix and the production of a Draft AML/CFT On-Site Supervision Manual.

NAICOM carried out a review of the AML/CFT Regulations for the insurance industry. The printing and gazetting of the revised regulations.

AML/CFT

Doc ID L

ast M

od

ified

P

rinte

d

| 25

Developments in the Insurance Sector .

10 insurance companies have subsidiaries outside Nigeria spread over West Africa – Cameroun, Cote d’Voire, the Gambia, Ghana, Liberia, Sierra Leone. In Uganda, Kenya.

NAICOM has signed an MOU with the National Insurance Commission of Ghana for information sharing and joint inspection.

Cross Border Supervision

Doc ID L

ast M

od

ified

P

rinte

d

| 26

Developments in the Insurance Sector .

The Complaints Bureau of NAICOM received over 300 fresh complaints yearly, most of which are resolved and settled while the others are on course for resolution.

The Commission have been monitoring the payment of compensations to claimants.

Complaint Bureau & Consumer Protection

Doc ID L

ast M

od

ified

P

rinte

d

| 27

Developments in the Insurance Sector .

Several initiatives to improve the image of the industry includes the TV programme “ Insurance & Claims” sponsored by NAICOM. Media adverts, billboards, radio jingles, distribution of leaflets.

Financial literacy events. School Outreach. Road shows and stakeholder workshops for enlightenment and financial education.

Awareness Campaign & Public Education

Doc ID L

ast M

od

ified

P

rinte

d

|

IMF FSAP Assessment

IAIS ICP assessment to be carried out by an independent consultant experienced in assessing compliance of national jurisdictions with the IAIS insurance core principles. The report will focuses on the identification of key areas for improvement in the regulatory and supervisory approach benchmarked against the international standard.

28

Developments in the Insurance Sector

Doc ID L

ast M

od

ified

P

rinte

d

|

.

29

IMF FSAP Assessment

The IMF assessment concluded that: “NAICOM has made a lot of effort over the past five years to improve the regulatory environment.” IMF marked NAICOM as fully observed in certain insurance core principles and largely observed in several others. Work has started in earnest in the identified areas that require improvement.

Developments in the Insurance Sector

GOAL 1:

To facilitate deeper market penetration in the insurance industry.

30

OBJECTIVE/

INITIATIVES

ACTIVITIES/

ACTION PLAN

EXPECTED OUTCOME

KEY PERFORMANCE

INDICATORS

CHALLENGES/

CONSTRAINTS

Enforcing

compliance with

compulsory

insurance;

Awareness and

enforcement

campaign in

states of the

Federation TV

and advert

publicity.

•Increase insurance policy

protection for individuals.

•Increase Contribution to GDP

from less than 1%

• Close Insurance Gap

• Increase premium income for

insurers and liquidity for payment

of claims.

% level of compliance with

compulsory insurance

% increase in premium

income

•Public

resistance to

insurance.

Ensuring

government

assets insurance

coverage;

Workshop on

insurance of

government

assets

•Adequate cover for Government

Assets . Reduced dependence on

government funds in the event of

losses.

% level of insured

government assets

•Inadequate

budgetary

provision for

insurance

Eradicating fake

insurance agents

and forged

policies from the

market;

Raids and

Prosecution of

offenders.

Collaboration

with NIA, FRSC.

Job creation

•Public hold genuine policy for

which they can be paid claims.

•Out of 10m vehicles only 500,000

have genuine cover.

•50,000 insurance agents to be

licensed.

% reduction in avenues where

fake insurance certificates are

sold (licensing Offices, Ports

etc)

Resistance to

enforcement

Facilitating

financial inclusion

through micro

insurance and

Takaful.

Conduct

diagnostic study

of Micro

Insurance e&

Takaful Issue

•Suitable policy to meet needs of

all including the poor and

vulnerable. Only 3 insurance

companies provide Takaful

insurance products.

% of informed stakeholders Poor standard of

living toward

purchase of

insurance

GOAL 2:

To manage stakeholders expectation in order to ensure transparency and public

confidence.

31

OBJECTIVES/

INITIATIVES

ACTIVITIES/

ACTION PLAN

EXPECTED OUTCOME

KEY PERFORMANCE

INDICATORS

CHALLENGES/

CONSTRAINTS

Conduct reviews

in all insurance

companies on

claims payment

and complaints

handling

policyholder

protection.

Ongoing

TV/Radio

programme on

rights of the

consumer in

Insurance and

Claims Financial

education.

•All genuine claims are paid in a

timely fashion

•No unjustified delay or rejection

of claims.

•Public has more trust and

confidence in the industry.

•Public complaint are

immediately dealt with.

•Complaints bureau received 337

complaints in 2010 and settled

107 to value of N1b.

% of planned interaction

with stakeholders achieved

annually

% of genuine claims paid by

insurance companies.

Time taken to settle claims

Inadequate

understanding of the

principles of

insurance contract

and inefficient postal

system.

Conducting

regular

stakeholder

surveys,

consumer

education

Conduct survey

on public

perception on

insurance

•More informed consumers that

have trust and confidence in the

Industry.

Number of stakeholders

survey carried out in each

quarter

•Public awareness

GOAL 3:

To strengthen insurance institutions by creating an effective regulatory framework

32

OBJECTIVE/

INITIATIVES

ACTIVITIES/

ACTION PLAN

EXPECTED OUTCOME

KEY PERFORMANCE

INDICATORS

CHALLENGES/

CONSTRAINTS

Adopt Risk Based

Supervision and

Risk Based Capital

(Solvency II)

Appoint consultants to draft

supervision manual and risk

Rating model Collaborating

with other regulators and

conduct pilot examination

using Risk Based Approach

•Better assessment of the

industry

•Correlation between risk profile

and scale of supervision

% increase in the number of

sound insurance companies

•Technical expertise

Risk Management

framework

Guideline released

Conduct in-house training of

staff and inspectors.

Workshop for industry

•Instilling a risk culture and

Corporate Governance within the

industry and preparing the

industry for a risk based regime.

% increase in the number of

sound insurance companies

•Change management

Pursue the passing

of the new

Insurance bill into

Law

Facilitate liaison with National

Assembly through the FMF

•More up-to-date legislation in line

with international best practice

Passage of the framework

Insurance Bill into Law

Delay in passing of the

bill

Facilitate

Transition to IFRS

Accounting

systems

Engage consultants. IFRS

training and seminars

conducted Guideline drafted

Less effort and time in the

assessment of financial reports

•Easier access to foreign

investment for insurance

companies.

•- financials are more transparent

with more disclosure of credible

financial position

% of insurance companies’ financials that are IFRS

compliant with international

financial reporting standards

Human Capital

Conduct special

inspection report

and follow up

remedial action

Consultants Inspectors utilized •Proper supervision and

monitoring of Insurance

Companies.

% of cases of insurers with

post inspection issues

concluded (categorization &

rating)

Skilled Inspectors

GOAL 4:

To enhance regulatory oversight by transforming the Commission’s processes, people and systems.

33

OBJECTIVE/

INITIATIVES

ACTIVITIES/

ACTION PLAN

EXPECTED OUTCOME

KEY PERFORMANCE

INDICATORS

CHALLENGES/

CONSTRAINTS

International

Assessment

and

benchmarking

May 2012 IAIS Insurance

Core principles assessment

of Regulators by GIZ

•Identification of key areas

of improvement in our

regulatory approach.

% score of good observations

by Assessors

Developing a

performance

management

framework

Design and implement the

performance management

system

•Environment where

employees can excel.

Implementation of

performance management

system

•Change

management

Staff

Competency

framework;

Job description analysis

and profiling by all

directorates

•Internal efficiency Completion of competency

profile

•Change

management

Deploying ICT

into business

processes,

Develop an industry portal

Automation of HR and

Finance and account

process.

•Enhance internal

effectiveness and service

delivery Technology

Industry portal developed and

quality of information obtained.

Quality of financial information

and accounting systems.

IT Infrastructure

Developing

effective

succession

and manpower

planning.

Staff deployment

Staff recruitment

Leadership training

programme

•Enhance effectiveness of

regulatory process

Design of training and date

training is concluded

Human Capital

Geographical Opening of new zonal •More national coverage Number of zonal offices Human capacity

GOAL 5:

To optimize revenue collection and effective management of the resources available to

the Commission.

34

OBJECTIVE/

INITIATIVES

ACTIVITIES/

ACTION PLAN

EXPECTED OUTCOME

KEY PERFORMANCE

INDICATORS

CHALLENGES/

CONSTRAINTS

Effective

assessment

and timely

collection of

levies

Collection of

levy from all

insurance

operators

High collection

rate

•Levy to support policyholders

protection fund and Road safety

Fund and hit & Run

Compensation fund

100% levy collected for

insurance returns approved

(including fines imposed for non

compliance

•Funding

Expanding the

revenue base of

the Commission

Identify the

number of

additional

source of

revenue

available

•Other source of revenue

identified and exploited

Number of revenue sources

identified.

Install best

practice internal

control systems

Deployment of

internal control

system

•Efficiency in internal regulatory

processes

Internal control system installed •Funding

Doc ID L

ast M

od

ified

P

rinte

d

|

Areas of Opportunities

Insurance Sector will require the assistance in the following areas:

i. Investment and asset Management : Improving profitability by creative investment in real estate power and capital market.

ii. Technology: to ease operations, efficiency speed and customer satisfaction. Online real time transaction processing.

iii. Human Capital: Recruitment of people with the right attitude, with the right exposure, with technical expertise (e.g. Actuaries).

iv. Legal Drafting: Joint venture, acquisition, due diligence, Share purchase agreements, regulatory, claims litigation.

5/7/2014 35

Doc ID L

ast M

od

ified

P

rinte

d

|

v. IFRS conversion: Need for firms who have experience from jurisdictions where IFRS is already in place.

vi. Business and product Development: Strategy, innovation, identification of market opportunities.

vii. Governance: Good corporate governance to prevent unfair treatment to the insured. Also the areas of Enterpise Risk management.

viii. Loss prevention: Safety measure, security system.

36 5/7/2014

Areas of Opportunities

Doc ID L

ast M

od

ified

P

rinte

d

|

Foreign Investment points

Ownership

Profits

Reinsurance

Registration

• Foreign reinsuers not currently required to hold our licence to take business but approval to reinsurer is required for certain risk e.g. Oil & Gas.

• Profits and dividends can be repatriated after tax has been paid

• No limit to ownership can own 100%

• New licence or acquisition of an existing company.

Doc ID L

ast M

od

ified

P

rinte

d

| 38

Conclusion .

Despite its challenges the Nigerian insurance sector is growing at a fast rate. The fact that the insurance gap is very wide right now is an indication of the vast growth opportunity. The industry will need services in the area of manpower & skill, investment capabilities, innovation, IT systems. Several big names in the international market are already gaining entry to seize the opportunities and there is an ambitious agenda put in place to continue to deepen the insurance market.

Doc ID L

ast M

od

ified

P

rinte

d

| 39

.

Thank you