investor presentation - coca-cola hbc...company multon, together with the coca-cola company (tccc)...

TRANSCRIPT

Investor Presentation

February 2014

Disclaimer

Unless otherwise indicated, the condensed consolidated interim financial statements and the financial and operating data or other information included herein relate to Coca-Cola HBC AG and its subsidiaries (‚Coca-Cola HBC‛ or the ‚Company‛ or ‚we‛ or the ‚Group‛).

This document contains forward-looking statements that involve risks and uncertainties. These statements may generally, but not always, be identified by the use of words such as ‚believe‛, ‚outlook‛, ‚guidance‛, ‚intend‛, ‚expect‛, ‚anticipate‛, ‚plan‛, ‚target‛ and similar expressions to identify forward-looking statements. All statements other than statements of historical facts, including, among others, statements regarding our future financial position and results, our outlook for 2014 and future years, business strategy and the effects of the global economic slowdown, the impact of the sovereign debt crisis, currency volatility, our recent acquisitions, and restructuring initiatives on our business and financial condition, our future dealings with The Coca-Cola Company, budgets, projected levels of consumption and production, projected raw material and other costs, estimates of capital expenditure, free cash flow, effective tax rates and plans and objectives of management for future operations, are forward-looking statements. You should not place undue reliance on such forward-looking statements. By their nature, forward-looking statements involve risk and uncertainty because they reflect our current expectations and assumptions as to future events and circumstances that may not prove accurate. Our actual results and events could differ materially from those anticipated in the forward-looking statements for many reasons, including the risks described in the annual report on Form 20-F filed with the U.S. Securities and Exchange Commission (File No 1-31466.) for Coca-Cola Hellenic Bottling Company S.A. and its subsidiaries for the year ended 31 December 2012.

Although we believe that, as of the date of this document, the expectations reflected in the forward-looking statements are reasonable, we cannot assure you that our future results, level of activity, performance or achievements will meet these expectations. Moreover, neither we, nor our directors, employees, advisors nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. After the date of the condensed consolidated interim financial statements included in this document, unless we are required by law or the rules of the UK Financial Conduct Authority to update these forward-looking statements, we will not necessarily update any of these forward-looking statements to conform them either to actual results or to changes in our expectations.

2.1 billion unit

cases sold or

50 billion servings per annum

583 million

population growing on average

at a ~1% per annum

28 countries of

operation over 3

continents with significant exposure in

Emerging Markets

38,089 employees 68 plants in operation and

324 warehouses & distribution centers

Coca-Cola HBC at a glance

3 Source: All numbers are FY2013 data unless otherwise stated; market share data Nielsen

# 1 in Sparkling

Beverages in 23 out of 24 markets

€7 billion

revenues Ten consecutive

quarters of currency neutral revenue per

case growth (as at Q4 2013)

Milestones

4

Hellenic Bottling Company S.A.

(HBC) is incorporated in

Greece

CCH listed on NYSE through a

sponsored ADR programm

HBC listed on the Athens Exchange

Formation of Coca-Cola Hellenic (CCH) through the

combination of HBC and CCB. Listings in Athens, London and

Sydney Stock Exchanges

Acquisition of SOCIB, second

largest franchise

bottler of TCCC in Italy

Kar-Tess acquired HBC

CCH expands to cover whole of

Russia in addition to Lithuania, Estonia

and Latvia

CCH acquires Russian fruit juice company Multon, together with The

Coca-Cola Company (TCCC)

Delisting from Australian Stock

Exchange

Formation of Coca-Cola Beverages

(CCB) from de-merger of European

operations of Coca-Cola Amatil

Limited

Admitted to trading in the

premium segment of the London

Stock Exchange

Inclusion in the FTSE 100 and FTSE

ALL-SHARE indices

Partners in Growth

for 60 years

Owners of the Trademarks

Concentrate supply

Brand development

Consumer marketing

The Coca-Cola system

5

Bottling

Sales and distribution

Customer management

In-outlet execution

Investment in production

facilities, equipment,

vehicles

Hellenic is the second largest Coca-Cola bottler globally

Source: FY 2012 results based on publicly available information Note: Sales are translated into Euros based on the respective 2012 average exchange rates

Coca-Cola Enterprises (Belgium, France, GB, Netherlands, Luxemburg, Norway, Sweden) Volume 1.25bn uc Sales €6.2bn 7 countries

Coca-Cola Femsa (Mexico,

Central America-Guatemala, Nicaragua, Costa Rica, Panama, Colombia, Venezuela, Brazil, Argentina- Philippines)

Volume 3.0bn uc Sales €8.8bn 9 Countries

Coca-Cola Icecek (Turkey,

Pakistan, Kazakhstan, Azerbaijan, Kyrgyzstan, Turkmenistan, Jordan, Iraq, Syria and Tajikistan) Volume 0.85bn uc Sales €1.8bn 10 Countries

Coca-Cola Amatil (Australia, New Zealand, Fiji, Indonesia and Papua New Guinea)

Volume 0.6bn uc Sales €3.5bn 5 Countries

ARCA Continental (Mexico, Ecuador and Northern Argentina)

Volume 1.35 bn uc Sales € 3.3 bn 3 Countries

Coca-Cola HBC Volume 2.1bn uc Sales €7.0bn 28 Countries

6

33%

37%

32%

9%

16%

18%

58%

47%

50%

Comparable EBIT

Net sales revenue

Volume unit cases

A diverse and balanced country portfolio

Total = €454 M

Total = €6,874M

Total = 2,061M

2013 Split

7

Population: 77 million

GDP: $ 12,559 Population: 415 million

GDP: $ 7,199

Population: 91 million

GDP: $ 36,917

Our extensive territorial reach offers a balanced volume profile

8

FY 2013 Volume Split

Russia19%

Italy14%

Nigeria10%

Poland8%

Romania7%

Greece5%

Austria4%

Switzerland4%

Serbia and Montenegro

4%

Ukraine4%

Other Developing11%

Other Emerging6%

Other Established4%

Meeting consumer needs with a diverse

product portfolio

9

Juice 6.0%

Sparkling

beverages 63.1%

2013

volume:

2.1 bn u.c.

2001 2013

Water 18.5%

RTD Tea 4.8%

2001

volume:

1.1 bn u.c.

Other still 0.7%

Energy drinks 0.7%

Low-calorie sparkling

beverages 6.2%

Sparkling

beverages 90%

Water 6%

Still beverages 4%

10

Emerging markets

Sparkling

beverages, 67%

Low-calorie

sparkling beverages,

2%

Energy Drinks,

1%

Water, 17%

Juice, 8%

RTD Tea, 5%

2013 Volume

288

218

210

135

103

Industry Sparkling Per Capita

Emerging

Coca-Cola HBC Average

Established

Developing

European Average

Sparkling Volume Market Share: 42% Sparkling Market Size Opportunity : ~1bn unit cases NARTD Volume Market Share: 23% NARTD Market Size Opportunity: ~3.4bn unit cases

Source: The Coca-Cola Company

Source: Nielsen FY12; Adjusted for coverage ratios

Russia38%

Nigeria20%

Romania14%

Serbia and Montenegro

8%

Ukraine8%

Other Countries

12%

Poland, 44%

Hungary, 20%

Czech Republic,

15%

Croatia, 7%

Baltics, 7%

Slovakia, 6%

Slovenia, 2%

Developing markets

2013 Volume

Sparkling beverages,

65%

Low-calorie

sparkling beverages,

6%

Energy

Drinks, 1%

Water, 14%

Juice, 5%

RTD Tea, 8% Other Still, 1%

288

218

210

135

103

Industry Sparkling Per Capita

Emerging

Coca-Cola HBC Markets

Established

Developing

European Average

Sparkling Volume Market Share: 34% Sparkling Market Size Opportunity : ~540m unit cases NARTD Volume Market Share: 14% NARTD Market Size Opportunity: ~2.3bn unit cases

Source: Nielsen FY12; Adjusted for coverage ratios

Source: The Coca-Cola Company

11

288218

210

135

103

Industry Sparkling Per Capita

Emerging

Coca-Cola HBC Markets

Established

Developing

European Average

Sparkling Volume Market Share: 53% Sparkling Market Size Opportunity : ~410 m unit cases NARTD Volume Market Share: 13% NARTD Market Size Opportunity: ~4.4bn unit cases

Italy, 45%

Greece, 15%

Austria, 14%

Switzerland, 13%

Island of Ireland,

11%

Cyprus, 2%

Established markets

2013 Volume Split

Sparkling

beverages, 55%

Low-

calorie sparkling

beverages, 13%

Water;

23%

Juice;

4%

RTD Tea;

3%Other Still;

2%

Source: The Coca-Cola Company

Source: Nielsen FY12; Adjusted for coverage ratios

12

2.069

2.105

2.087 2.085

2.061

1. 950

2. 040

2. 130

2009 2010 2011 2012 2013

2.467 2.760 2.828 3.195 3.229

1.1491.140 1.162

1.148 1.106

2.928 2.862 2.835 2.702 2.540

- 500

500

1. 500

2. 500

3. 500

4. 500

5. 500

6. 500

7. 500

2009 2010 2011 2012 2013Established Developing Emerging

651687

523453 454

0

100

200

300

400

500

600

700

800

2009 2010 2011 2012 2013

Financial highlights

in million unit cases

in million Euros

9,9% 10,1%

7,7% 6,4% 6,6%

Net Sales Revenue

6,544 6,762 6,824 7,045

13

Volume Reported NSR per unit case

3,163,23

3,27

3,383,34

2, 50

3, 50

2009 2010 2011 2012 2013

40,3% 40,4%37,7%

35,9% 35,5%

- 5, 0%

5, 0%

15, 0%

25, 0%

35, 0%

45, 0%

2009 2010 2011 2012 2013

Gross Profit Margin

30,4% 30,3%30,0%

29,4%

28,9%

27, 0%

28, 5%

30, 0%

31, 5%

2009 2010 2011 2012 2013

OPEX as a % of revenue Comparable EBIT and

EBIT margin

6,874

Split by segment

Cost structure

Concentrate, 34%

Sugar, 13%

PET, 8%

Aluminium, 5%

Other Raw Materials, 18%

Depreciation, 4%

Overheads & Haulage, 18%

Sales, 37%

Warehouse &

Distribution, 31%

Administration,

22%

Marketing, 10%

These are based on our FY 2013 numbers

14

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

Jan/12 Mar/12 May/12 Jul/12 Sep/12 Nov/12 Jan/13 Mar/13 May/13 Jul/13 Sep/13 Nov/13 Jan/14

CCHBC 4.250% '16 YTW CCHBC 2.3750% '20 YTW

15

June 2012: •Second Greek Elections •Scenarios on Grexit become stronger •CCH Spreads are at peak levels •Moody’s & S&P downgrade CCH due to Country Risk •CCH access to Debt Capital Market becomes very expensive

May 2012: •First Greek Elections •Scenarios on Grexit •CCH Spreads start to rise

October 2012: • Re-listing &

Re-domiciliation Announcement

April 2013: • Re-domiciliation CCHBC AG • Trading of CCHBC AG shares on

LSE

10th June 2013:

• Announcement and Pricing of the NEW €800M Bond

• Announcement to Tender the 2014 €500m Bond

18th June 2013:

• Settlement of new €800M Bond (& €500M Bond Tender)

Very Successful Refinancing

Source: Bloomberg as at 11 February 2014.

Yie

ld o

f o

ur

20

16

/20

20

Bo

nd

s(%

)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

Jan-11 Jun-11 Nov-11 Apr-12 Sep-12 Feb-13 Jul-13 Dec-13

Volume 1 year average Since London Listing

Shareholder structure

US 19%

UK 23%

Continental Europe

39%

Rest of the world 16%

Retail Investors 3%

Free Float54%

Kar-Tess23%

The Coca-Cola Company

23%

16 Shareholders as of 31 December 2013 * Source: Bloomberg as at 31 Dec 2013; ADV= Average Daily Volume

Corporate governance

17

• ADR program on NYSE since 2002

• Full SOX compliance history

• Enhancement of corporate governance through:

1. Appointment of an additional independent non-executive director

2. Board members subject to re-election on an annual basis

3. Nominations committee, majority of its members independent

• Committed to adhering to the UK Corporate Governance Code

Making good progress towards our sustainability goals

2,40

2,30

2,24 2,25

2,20

2009 2010 2011 2012 2013

Water use ratio l/lpb

- 23% from 2004

baseline

21,617,6

14,512,3 10,8

2009 2010 2011 2012 2013

million kg

Landfilled waste

- 74% from 2004

baseline

CO2 ratio Waste ratio Gr/lpb

71,570,1

66,1

61,660,1

2009 2010 2011 2012 2013 E

gCO2/lpb

-32% from 2004

baseline

11,210,2 9,4

8,5 8,7

2009 2010 2011 2012 2013

-37% from 2004

baseline

Further details on our sustainability goals and initiatives can be found at www.coca-colahellenic.com 18

An industry leader in Sustainability

Included for a sixth consecutive year in both the Dow Jones Sustainability World Index and Dow Jones STOXX Sustainability Index. 1st on the DJSI Europe Index 2nd on the DJSI World Index of the top ranking beverage companies in sustainability

Member 2012/13

In 2010: The only European non-alcoholic ready-to-drink beverage company to achieve GRI A+ ranking for comprehensiveness and transparency

GRI A+

For more information please see our sustainability reports at http://www.coca-colahellenic.com/sustainability/

Listed on the FTSE4Good index

19

Overview of Our Strategy

20

The Opportunity We See…

• Emerging markets exposure

• Market Share Growth

• Per Capita development

Business Growth

Margin Leverage

• Operating cost control

• Production Infrastructure rationalisation

• Logistics and route-to-market optimisation

• Revenue-generating Capex investments

21

39

98

135 139

173 182

223 226 232 237

298307

340 340

423

468

596

We have a diverse geographical footprint offering long-term attractive growth potential

2012 Total sparkling category servings per capita

Source: The Coca-Cola Company, as of 2012 data

‘per capita consumption’: Average number of 237ml or 8oz servings consumed per person per year in a specific market. Coca-Cola Hellenic’s per capita consumption is calculated by multiplying our unit case volume by 24 and dividing by the population.

Established

Developing

Emerging

210

219

103

22

Winning in the marketplace

Focus on Cost leadership

Generate solid Free Cash Flow

Revenue ahead of volume

Our Strategy

23

Solid track record of winning in the marketplace

24

We are #1 in volume share in sparkling beverages*

We gained volume and value share in sparkling beverages*

Market shares are measured by Nielsen; Cyprus, FYROM, Moldova and Montenegro are not measured.

in 20 out of 24

in 23 out of 24

We reached highest ever sparkling share in 12 countries

out of 24

12

Package mix- Channel Mix: Driving revenue ahead of volume

25

39% 61%

*

(*) FY2013 Volume Split

Sparkling beverages,

63,1%Low calorie

sparkling beverages,

6,2%

Water, 18,5%

Juice, 6,0%

RTD Tea, 4,8% Energy

drinks, 0,7% Other still, 0,7%

Category Mix (Brand)

Package-mix Single serve Multi serve Future Consumption

69%

Channel Mix* Immediate Consumption

31%

We have clear category priorities: Sparkling, RTD-Tea and Energy

Energy

Sparkling •Leverage Trademark Coca-Cola with focus on Regular and Zero

• Increase per capita consumption

• Further grow Fanta, focusing on orange flavour

•Drive Sprite availability in immediate consumption channels

•Single-serve focus, OBPPC

Water

RTD-Tea

Juice • Focus on profitability, capitalising on strong local

brands

• Single serve packs

• Flavoured water and HORECA

• Focus on increasing market penetration and trial

• Bring new people to the category

• Reinforce naturalness and low calorie refreshment

• Best tasting products with premium quality

• Leverage strong brand equity in Cappy, Amita, Dobry

• Innovation

• Approach driven by stage of development of local energy category

• Focus on ‚on-the-go‛ channels

Drive Growth in:

Selective approach in:

26

Driving Trademark Coca-Cola is a key priority

2%

4%4%

2% 2%

-2%

2%

-1%

0%

-1%

2009 2010 2011 2012 2013

TM Coca-Cola Total Volume

27

Optimising our cost base to enhance competitiveness

Infrastructure optimisation

Logistics excellence

Manage OPEX and Working Capital

SAP is a key enabler

28

Shared Services Centre enables to centralise and standardise processes

Benefits:

• Leverage SAP benefits

• Improve productivity

• Enhance business support

• Improve internal control / governance

• Enable local management to focus on value added activities

Roll Out:

• Phase I: Live in 22 countries for key Finance and HR functions

• Phase II: Pilot live in Q4 2013, starting with Bulgaria, Romania (Finance) , Switzerland (Finance) and Italy (HR)

• Integration of more countries and processes planned ” followed by best practice application

Standardising

processes

Consolidating synergies

Applying global best

practice

29

Infrastructure optimisation

1. The right physical distribution network

2. Leverage scale by exploiting collaborative opportunities

3. Efficient solutions matching customer/channel requirements

4. Accurate and automated data exchange

5. With the right people in the right roles

Number of plants

-26% since 2009*

Number of distribution centers

-9% since 2009

Number of warehouses

-17% since 2009

30

(*) In established and developing markets; for the group -15%

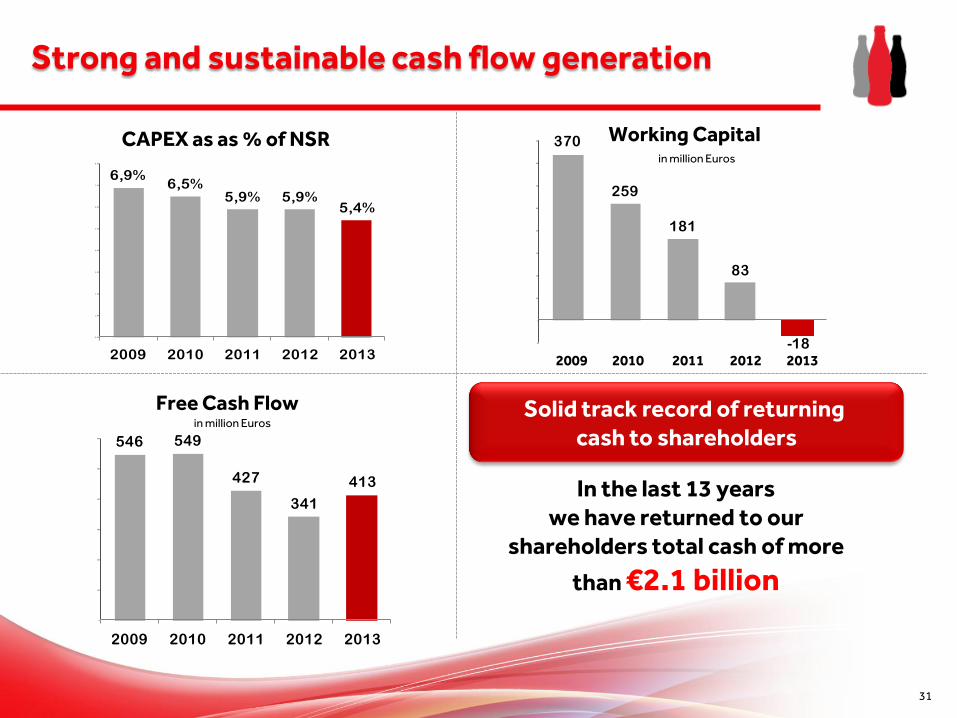

Strong and sustainable cash flow generation

31

in million Euros

in million Euros Solid track record of returning

cash to shareholders

In the last 13 years we have returned to our

shareholders total cash of more

than €2.1 billion

6,9%6,5%

5,9% 5,9%5,4%

0, 0%

1, 0%

2, 0%

3, 0%

4, 0%

5, 0%

6, 0%

7, 0%

8, 0%

2009 2010 2011 2012 2013

CAPEX as as % of NSR 370

259

181

83

-18- 50

0

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013

2009 2010 2011 2012 2013

Working Capital

546 549

427

341

413

0

100

200

300

400

500

600

2009 2010 2011 2012 2013

Free Cash Flow

Overview of fourth quarter and full-year 2013 results

33

Key messages for the fourth quarter

Volume growth

Continuing market share gains

Increase in currency neutral revenue per case for the tenth

consecutive quarter

Improvement in OPEX as a % of net sales revenue

Growth in absolute EBIT, margin and EPS

Negative working capital position

Strong free cash flow growth

Financial performance overview

34

Q4 ’13 Q4 ’12 Ch. FY ’13 FY ’12 Ch.

Volume (m u.c.) 481 477 +1% 2,061 2,085 -1%

Net Sales Revenue (€m) 1,575 1,605 -2% 6,874 7,045 -2%

Comp. Gross Profit

Margin % 34.1% 34.6% -50bps 35.5% 35.9% -40bps

Opex % NSR 29.8% 31.1% -130bps 28.9% 29.4% -50bps

Comp. EBIT (€ m) 68 56 +23% 454 453 -

Comp. EBIT

Margin % 4.3% 3.5% +90bps 6.6% 6.4% +20bps

Comparable EPS (€) 0.09 0.06 +50% 0.81 0.78 +4%

Free Cash Flow (€m) 68 -21 nm 413 341 +21%

Financial indicators on a comparable basis exclude the recognition of restructuring costs, unrealised commodity hedging results and non-recurring items.

Total Coca-Cola HBC

Established markets

Developing markets

Emerging markets

Volume +1% -1%

Currency neutral revenue per case +0.9% +1.1%

Q4 ‘13 FY ‘13

Volume stable -4%

Currency neutral revenue per case -4.3% -1.2%

Volume -5% -3%

Currency neutral revenue per case +3.4% +0.8%

Volume +4% +2%

Currency neutral revenue per case +3.9% +3.5%

Tenth consecutive quarter of growth in currency neutral net sales revenue per case

35

Input cost increase in line with our expectations

“ Q4 2013

Currency neutral input cost per case increased by low single digits

EU sugar costs increased year-on-year

World sugar costs remained on a downward trend

PET resin costs increased year-on-year

Lower aluminium costs in the quarter

36

Q4 ’13 Q4 ’12 Ch.

Net Sales Revenue (€ m) 1,575 1,605 -2%

Comp. Operating Expenses (€ m) (469) (499) -6%

Comp. OPEX as % of NSR 29.8% 31.1% -130bps

FY ’13 FY ’12 Ch.

Net Sales Revenue (€ m) 6,874 7,045 -2%

Comp. Operating Expenses (€ m) (1,987) (2,074) -4%

Comp. OPEX as % of NSR 28.9% 29.4% -50bps

Financial indicators on a comparable basis exclude the recognition of restructuring costs, unrealized commodity hedging results and specific non-recurring items.

Continued focus on increasing operational efficiency

37

Financial indicators on a comparable basis exclude the recognition of restructuring costs, unrealised commodity hedging results and specific non-recurring items

12

Change vs. Q4 ‘12 m Euros % Ch.

Emerging

Developing

Established

Group

1

5

6

23%

9%

nm

13%

Q4 ’12 comparable EBIT Q4 ‘13 comparable EBIT

Q4 comparable EBIT

m Euros

All segments contributed to growth in operating profit

38

Q4 & FY 2013 summary

Benefits from 2013 restructuring initiatives expected at €32m on an annualised basis

Total benefits in 2013 (from 2012 and 2013 initiatives) were approximately €57m

Total pre-tax restructuring charges amounted to €56m in 2013 (€31m in Q4)

Restructuring focus continued to be in established markets

FY 2014 targets

We expect pre-tax restructuring charges of €35m

Total benefits in 2014 (from 2013 and 2014 initiatives) are expected at €33m YTD

Benefits from 2014 initiatives are expected to amount to €25m on an annualised basis

Restructuring update

39

EBITDA

Change in Working Capital

Net Capital Expenditure

Free Cash Flow

Q4 ’13 Q4 ’12 Abs Ch.

FY ’13 FY ’12 Abs Ch.

132 100 +32 756 758 -2

76 19 +57 98 84 +14

(115) (122) +7 (372) (412) +40

68 -21 +89 413 341 +71

* Differences in the absolute year-over-year change are due to rounding

in million Euros

Impressive Working Capital performance and Free Cash Flow growth

40

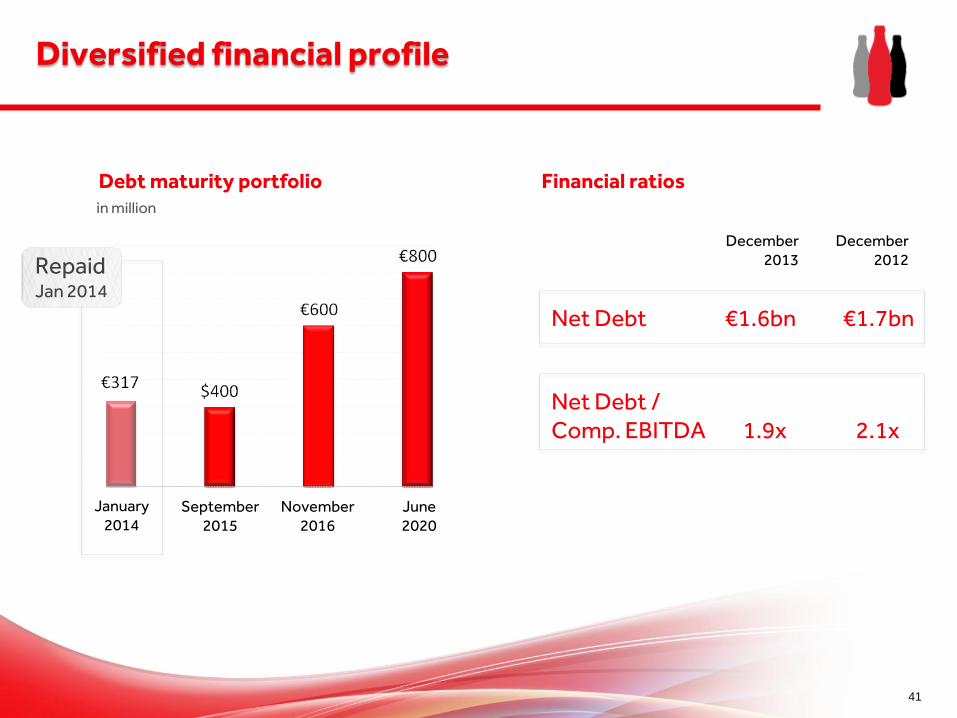

in million

January 2014

September 2015

November 2016

June 2020

Repaid Jan 2014

Financial ratios

December 2013

December 2012

Net Debt €1.6bn €1.7bn

Net Debt / Comp. EBITDA 1.9x 2.1x

Debt maturity portfolio

Diversified financial profile

41

Currency neutral net sales revenue per case is expected to grow year-on-year at a

higher rate than 2013

Currency neutral input costs per case to remain broadly stable year-on-year

FX headwind is estimated to be significantly higher than the 2013 hit on EBIT

Comparable Effective Tax Rate between 24%-26%

Annual Capital Expenditure 5.5% - 6.5% of net sales revenue for the medium term

Reiterating our expectations for approximately €1.3bn of Free Cash Flow in the 2013-

2015 period

Financial indicators on a comparable basis exclude the recognition of restructuring costs, unrealised commodity hedging results and specific non-recurring items

2014 Financial outlook

42

Operational review and strategy

43

Stable -5%

481m u.c.

477m u.c.

+4%

Q4 ‘12 Established Developing Emerging Q4 ‘13

Emerging markets were the key volume driver in Q4

44

45

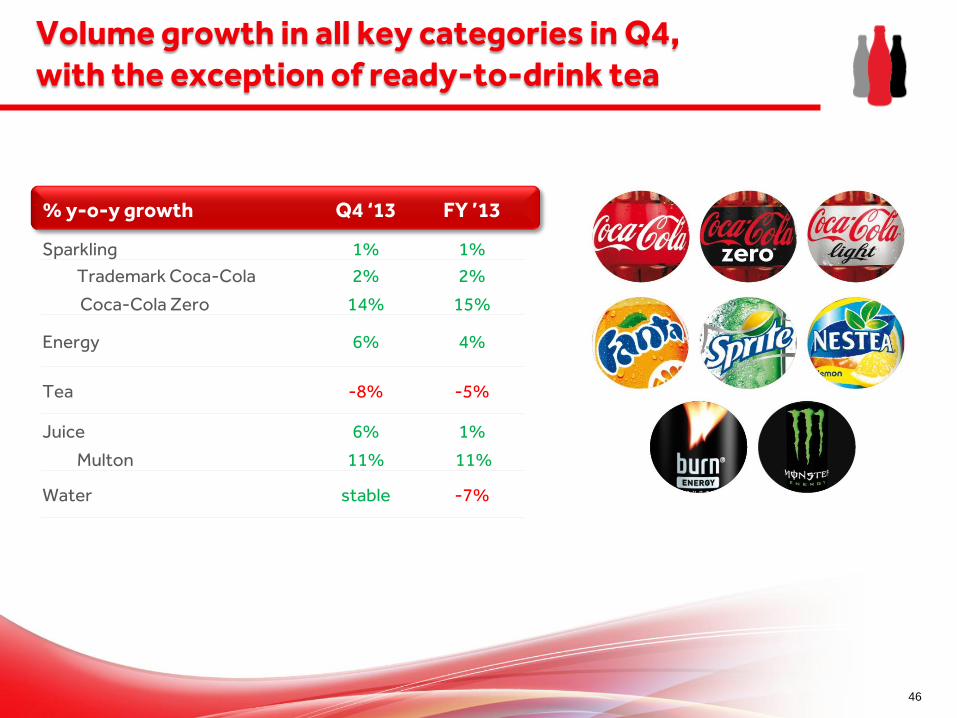

We continued to win in the marketplace

% y-o-y growth Q4 ‘13 FY ’13

Sparkling 1% 1%

Trademark Coca-Cola 2% 2%

Coca-Cola Zero 14% 15%

Energy 6% 4%

Tea -8% -5%

Juice 6% 1%

Multon 11% 11%

Water stable -7%

Volume growth in all key categories in Q4, with the exception of ready-to-drink tea

46

“ Italy: Volume declined by low single digits in the quarter, with Coca-Cola Zero up by 21%. Underlying macroeconomic and trading environment remains challenging.

“ Greece: Volume declined by low single digits, with the rate of decline steadily moderating through the year. All key categories showed sequential improvements in the rate of decline with the exception of ready-to-drink tea.

“ Switzerland: Volume increased by low single digits. Underlying trading conditions have remained stable.

Trademark Coca-Cola

+1%

Coca-Cola Zero

+13%

RTD-Tea -13%

Volume Stable

Currency neutral net sales revenue per case

-4%

Juice +4%

Established markets – stable performance in a challenging consumer environment

47

“ Poland: Volume declined by high single digits, following a mid single-digit increase in the prior year. Sparkling declined by high single digits, while our juice category grew by mid-teens.

“ Hungary: Volume declined by low single digits, Coca-Cola Zero was the key outperformer growing by high-teens for another quarter.

“ Czech Rep.: Volume declined by mid single digits, driven by a low-teens decline in water. Trademark Coca-Cola products grew by low single digits.

Trademark Coca-Cola

-5%

Juice +10%

Volume -5%

Currency neutral net sales revenue per case

+3%

Coca-Cola Zero +3%

Developing markets – negative trends in a volatile environment

48

“ Russia: Volume grew by high single-digits in the fourth quarter, following mid-teens increase in the prior-year period. Growth in all key categories with the exception of water. Multon juice business grew by low double digits for the eighth consecutive quarter.

“ Nigeria: Volume grew by high single digits in the fourth quarter, cycling a high single-digit growth rate in the prior year. Sparkling beverages grew by mid single digits and water by strong double digits.

“ Romania: Volume declined by low single digits, mainly due to a difficult macroeconomic environment; Coca-Cola Zero and juice grew by strong double digits.

Trademark Coca-Cola

+5%

Water +5%

Juice +5%

Volume +4%

Currency neutral net sales revenue per case

+4%

Emerging markets – improved performance supported by strong activation

49

Most known brands in the world Diverse geographic footprint with strong emerging market exposure

Low per capita consumption with great potential to grow

Solid track record of winning in the marketplace

Strong focus on cost leadership and history of solid cash generation

Long-term growth drivers

51

For further information on Coca-Cola Hellenic please visit our website at:

www.coca-colahellenic.com or contact our Investor Relations team

[email protected] +30.210.6183 100