iowa agriscope 2030 - home | iowa soybean association · charged with developing a comprehensive,...

TRANSCRIPT

Iowa AgriScope 2030

The report is organized in a chapter format

Chapter 6: Appendix

A | Summary of Steering Committee Meetings 365-369

B | Final Steering Committee Meeting Prioritization Exercise

Results 370-434

C | Responsibilities 435-555

Priority Strategies, Recommendations & Actions organized by

Who is Responsible

Secondary Strategies, Recommendations & Actions organized by

Who is Responsible

D | Resources 556-559

Chapter 1: Introduction 3-11

Background | Process

Economic Importance of Iowa Agriculture

Chapter 2: Executive Summary 12-37

Goal & Strategic Framework

Priority Strategies including Recommendations

Secondary Strategies including Recommendations

Chapter 3: Full Report 38-161

Goal & Strategic Framework

Priority Strategies including Recommendations, Actions,

Rationale & Responsibilities

Secondary Strategies including Recommendations, Actions,

Rationale & Responsibilities

Chapter 4: Situational Analysis 162-184

Chapter 5: Value Chains/Competitiveness Assessments 185-363

Corn | Soybeans | Pork | Beef | Dairy

Eggs | Turkeys | Biofuels

Report Contents1

2

Report

Appendices

Slide Navigation Icons:

Return to Table of Contents slide

Return to previous slide

2 | Context | Iowa AgriScope 2030

Chapter 1: Introduction

3 | Context | Iowa AgriScope 2030

Charged with developing a comprehensive, credible and practical plan

to strengthen and grow Iowa agriculture

Background– “Iowa will lead the world in agriculture, doubling production of our crops and value-added products while increasing

personal income, creating value and creating jobs. This plan will address systems to better handle, store, transport and transfer the increased production of agricultural crops, renewables, energy and added products,” according to Iowa Governor Terry Branstad in September 2010.

Project Objective– A comprehensive, credible, practical plan that Iowa leaders may use to strengthen and build Iowa’s agriculture, food,

fiber, alternative energy and supporting services sectors.

Project Sanctioned by Governor Terry Branstad and Secretary of Agriculture Bill Northey– Both the Governor and the Secretary endorsed and participated in the project. However, this did not indicate an

automatic endorsement of the final product.

Components– Five Context team members conducted extensive research and interviews.

– Twenty Iowa leaders provided feedback and direction through Steering Committee participation.

– One hundred interviewees provided insights into specific aspects of Iowa’s agriculture, food, fiber, alternative energy and supporting services sectors.

Timeline– February to November 2011

Conceived of and Funded by– Iowa Soybean Association, Iowa Pork Producers Association, and Iowa Corn Growers Association

4 | Context | Iowa AgriScope 2030

The Steering Committee chosen represented a diverse cross-section of

thought leaders throughout Iowa agriculture

5 | Context | Iowa AgriScope 2030

James Borel, DuPont/Pioneer

Don Borgman, farmer and John Deere

Bill Couser, cattleman and ethanol

entrepreneur

Rich Degner, Iowa Pork Producers

Association

Kaye DeLange, Cargill Eddyville Plant

Debi Durham, Iowa Department of Economic

Development

Dermot Hayes, Iowa State University (ISU)

professor and Pioneer Chair in

Agribusiness

Dakota Hoben, ISU student and former Iowa

FFA officer

Kirk Leeds, Iowa Soybean Association

Ron Litterer, farmer and Iowa Corn Growers

Association representative

Jim Knuth, Farm Credit Services of Iowa

David Miller, Iowa Farm Bureau

Bill Northey, Iowa Secretary of Agriculture

Craig Rowles, DVM, pork producer and

entrepreneur

Jeff Strohburg, West Central Cooperative

Roger Underwood, Becker Underwood co-

founder and venture investor

Kevin Vinchattle, Iowa Poultry Association

Paul Willis, pork producer and Niman Ranch

Wendy Wintersteen, dean, ISU College of

Agriculture and Life Sciences

Noel White, Tyson

The Steering Committee met three times for facilitated, productive feedback and guidance and

were interviewed individually.

Comprehensive and methodical process was designed and executed to

capture high-level strategy as well as detailed actions

6 | Context | Iowa AgriScope 2030

Feb thru Apr May thru July Aug thru Oct November

• Steering

Committee (SC)

Selection

• Situation analysis

• SC meeting to define

opportunities and

obstacles

• Research and

analysis

• Clarification interviews

• Secondary research

• Priority analysis and

report completion

• Governor

• Sponsors

Preparation Data Collection Analysis Presentation

• SC interviews

• Key opinion leader

interviews

• Secondary research

• SC meeting to review,

recommend, and

prioritize growth

opportunities

• SC meeting to prioritize

recommendations

Engaged nearly 100 key opinion leaders on discussions regarding

Iowa’s opportunities in agricultural economic development

7 | Context | Iowa AgriScope 2030

Expertise of respondents reflect a diverse cross section of Iowa agriculture

Approach

Key Opinion

Leaders

96 executive-style interviews completed

–Performed with open-ended questions that were

administered in a conversational style

– In-depth, duration between 45-90 minutes

– ‘Face-to-face’ with all Steering Committee members

Crop Producers (Row crop, Fruit/Vegetable)

Livestock Producers (Pork, Beef, Poultry/Eggs, Dairy)

Organic/Local/Fresh Producer & Processor

Cooperatives/Retailers

Organizations/Associations

Co-Products/Specialty Crops

Grain Handling/Processing

Ag. Research/Innovation

Seed

Ag. Chemicals

Ag. Equipment

Energy (Ethanol, Electric)

Food Manufacturing/Meat Processing

Grocery/Downstream Consumer

Transportation (Railway, Roads, Rivers)

Information Technology

Education

Legal

Entrepreneurial Investment Community

Natural Resources

Next Generation of Agriculture

Sustainability

Support Services – Banking/Financing, Economic Development

State Government

Interviews distributed throughout Iowa

Economic Importance of Iowa Agriculture

8 | Context | Iowa AgriScope 2030

The agriculture industry is and will continue to be a driving force in the

global marketplace

9 | Context | Iowa AgriScope 2030

Source: FAO data and projections

World demand for cereals, 1965 to 2030

“Iowa has a rich tradition of exporting its agricultural know-how to the world, best illustrated by Roswell Garst and John Chrystal . . . . The World Food Prize presents a fresh opportunity for Iowa to continue that tradition in bigger and better ways of being an international leader in agriculture and food security.”

World average meat consumption,

per person, 1964 to 2030

Source: The Des Moines Register, Editorial, October 15, 2011

Iowa is an important and large contributor to the US agricultural

economy

10 | Context | Iowa AgriScope 2030

Zoom

In 2009, Iowa was second only to California

in supplying agriculture commodities for US

utilization, consumption and for global trade.

“You are the Silicon Valley of ag biosciences. Youhave assets here that exist nowhere else in the world.You have a perfect storm of opportunities coming together, in terms of . . . . the powerhouse global multinationals in ag biosciences, some of the best research universities in the world, with tremendous resource assets, and of course the land.” - Simon Tripp, BMI, Ohio

Commodity (2009, % of US) Rank

Corn (18%) #1

Soybeans (15%) #1

Hogs (28%) #1

Eggs (16%) #1

Cattle #4 to 6

Source: USDA-ERS and NAS

Source: USDA

The agriculture industry is a critical factor to Iowa’s GSP and

employment as well as individual household income

11 | Context | Iowa AgriScope 2030

Agriculture employment = 332,000

Or more than 16% of Iowa’s total 1.946M

“In 2008, this engine of economic growth created $26.3 billion in agriculture production value in the

state. Currently, increased federal and state regulatory actions have created an environment non-supportive of increased productivity, innovation and

job creation. The lack of regulatory stability is driving business out of the state and causing those

who remain to limit or eliminate additional investment in their businesses and employees.”

Governor Terry BranstadIowa’s farm households are 2½ times more

dependent on farm income than the average

US farmer

Zoom

Chapter 2: Executive Summary

12 | Context | Iowa AgriScope 2030

Goal & Strategic Framework

13 | Context | Iowa AgriScope 2030

Early in the process, a simple yet powerful goal was articulated

14 | Context | Iowa AgriScope 2030

Increase the Size and Scope

of Iowa Agriculture

15 | Context | Iowa AgriScope 2030

Increase the Size and Scope of Iowa Agriculture

Expansion of Iowa agriculture’s

economic activity requires a rock-

solid foundation, so this project

began with an exploration of what

can be done to protect and improve

Iowa’s existing strengths.

With a strong foundation, Iowa

agriculture can expand in several

directions, depicted as four

opportunities in the top half of the

graphic.

Using analysis and Steering Committee input, a vision was developed to

depict the areas of focus most essential to achieve the goal

Objectives

Strategies

Leadership

This strategic framework was built on nearly 100 interviews and

Steering Committee discussion

16 | Context | Iowa AgriScope 2030

GoalIncrease the size

and scope of Iowa agriculture

Protect Comparative Advantages

Strong Soil, Safe Water

Qualified, Adequate Workforce

Improved Transportation Infrastructure

Improve Business Climate

Reasonable Regulations &

Taxes

Business Environment

Encourage Innovation

World Class Research & Education

Innovation Reputation

Expand Economic Activity

Build the Base

Add Value

Expand Exports

Nurture the New

Objectives

Strategies

Leadership

Priorities within the Strategic Framework were identified with support

from the Steering Committee

17 | Context | Iowa AgriScope 2030

GoalIncrease the size

and scope of Iowa agriculture

Protect Comparative Advantages

Strong Soil, Safe Water

Qualified, Adequate Workforce

Improved Transportation Infrastructure

Improve Business Climate

Reasonable Regulations &

Taxes

Business Environment

Encourage Innovation

World Class Research & Education

Innovation Reputation

Expand Economic Activity

Build the Base

Add Value

Expand Exports

Nurture the NewPriority Strategies Secondary Strategies

Recommendations were developed for all Strategies and prioritized with

support from the Steering Committee

18 | Context | Iowa AgriScope 2030

Objectives

Strategies

Recommendations

Protect Comparative Advantages

Strong Soil, Safe Water

Re-energize Iowa’s commitment to soil

stewardship, addressing both retention and quality

concerns.

Protect Iowa’s ground water and surface water while

optimizing efficient utilization for both production &

processing.

Prioritize vulnerable landscapes and soils for

federal and state incentive programs.

Priority Recommendations Secondary Recommendations

EXAMPLE

Actions, rationales and responsibilities were designated for each

recommendation (an example can be found in the next three slides)

19 | Context | Iowa AgriScope 2030

Strategies

Recommendations

Actions

EXAMPLEStrong Soil, Safe Water

Re-energize Iowa’s commitment to soil

stewardship, addressing both retention

and quality concerns.

Work toward and maintain a limit of soil loss tolerance (T) or

less.

Protect and retain current soil saving structures/practices

and resist incentives to farm through or over them.

Research use of cover crops as a potential mitigation for

soil loss created by the increasing number of heavy rain

events in Iowa.

Encourage landlords to use leases that include incentives

for improving the quality of their soil and conservation

practices.

Promote the value of adding organic matter to Iowa soils by

proving long-term enhancement of productive capacity and

retention of top soil.

Employ practices recommended to increase organic carbon

levels in soil such as no-till, cover crops, crop rotation and

use of livestock manure for fertilizer.

Educate landlords about the value of their asset and the

potential to lose that value through tillage practices that do

not protect the soil from eroding and losing organic matter.

20 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

Re-energize Iowa’s commitment to soil stewardship, addressing

both retention and quality concerns.

Reco

m.

Strong Soil, Safe Water

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

• Work toward and maintain a limit of soil loss tolerance (T) or less.

• Protect and retain current soil saving structures/practices and resist incentives

to farm through or over them.

• Research use of cover crops as a potential mitigation for soil loss created by

the increasing number of heavy rain events in Iowa.

• Educate landlords about the value of their asset and the potential to lose that

value through tillage practices that do not protect the soil from eroding and

losing organic matter.

• Encourage landlords to use leases that include incentives for improving the

quality of their soil and conservation practices.

• Promote the value of adding organic matter to Iowa soils by proving long-term

enhancement of productive capacity and retention of top soil.

• Employ practices recommended to increase organic carbon levels in soil such

as no-till, cover crops, crop rotation and use of livestock manure for fertilizer.

Actio

ns

EXAMPLE

21 | Context | Iowa AgriScope 2030

Iowa is blessed with some of the most productive soil on earth, and

Iowa producers have long recognized the value of protecting those

soils. As costs of production increase, though, many find it tempting to

till vulnerable land or employ tillage systems that are less than

protective. Both farmers and landowners are encouraged to recommit to

saving soil and, in fact, improving its quality when possible. Leadership

levels of production and soil stewardship can be achieved through a

continuing quest for reduced tillage practices, appropriate balances of

livestock manure and other nutrient sources, and emerging production

technologies.

According to an ISU study, compaction, erosion and loss of organic

matter have led to a decline in the quality of Iowa’s soils over the past

50 years. Organic matter content in Iowa soils has dropped from an

average of 10% to two percent. However, regaining soil quality can be

achieved by adding organic matter and employing tillage methods that

reverse compaction and reduce erosion

Strong Soil, Safe Water - Rationale

Re-energize Iowa’s commitment to soil stewardship, addressing both retention and quality

concerns.

Sources: Soil Quality, Better Lawns Made Easy, Polk Soil & Water Conservation District and Iowa Storm

Water Education Program; ISU Research: Iowa has lower-quality topsoil than 50 years ago,

EXAMPLE

Photo Source: ISU Extension – Agronomy

22 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Responsibilities

Re-energize Iowa’s commitment to soil stewardship, addressing both retention and quality

concerns.

Actions Team Leader(s) Team Member(s)

Work toward and maintain a limit of soil loss tolerance

(T) or less.IDALS Ag Producers, SWCDs

Protect and retain current soil saving

structures/practices and resist incentives to farm

through or over them.

Ag Producers

Research use of cover crops as a potential mitigation

for soil loss created by the increasing number of heavy

rain events in Iowa.

ISU

Educate landlords about the value of their asset and

the potential to lose that value through tillage practices

that do not protect the soil from eroding and losing

organic matter.

SWCDs USDA NRCS, ISU, Ag Producers

Encourage landlords to use leases that include

incentives for improving the quality of their soil and

conservation practices.

IDALS, Ag Producers, SWCDs ISU

Promote the value of adding organic matter to Iowa

soils by proving long-term enhancement of productive

capacity and retention of top soil.

SWCDs USDA NRCS, IDALS, Ag Producers

Employ practices recommended to increase organic

carbon levels in soil such as no-till, cover crops, crop

rotation and use of livestock manure for fertilizer.

Ag Producers

EXAMPLE

23 | Context | Iowa AgriScope 2030

Priority StrategiesIncluding Recommendations

24 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

• Re-energize Iowa’s commitment to soil stewardship, addressing both retention

and quality concerns.

• Protect Iowa’s ground and surface water while optimizing efficient utilization for

both production and processing.

• Prioritize vulnerable landscapes and soils for federal and state incentive

programs.

Reco

mm

end

ation

s

Strong Soil, Safe Water

Through producers’ adoption of innovative tillage methods and

technologies, achieve optimum quality levels for Iowa soils and

limit soil loss to replacement levels. Eliminate water quality

concerns, and assure abundant, clean water supplies that provide

an advantage when attracting and growing agriculture-related

manufacturing and processing.

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

Black = Priority Recommendation Gray = Secondary Recommendation

25 | Context | Iowa AgriScope 2030

• Effect lasting improvement to the state regulatory and permitting processes.

• Administer reasonable, fair and relevant regulatory enforcement.

• Determine the effect that Iowa’s business tax ranking is having on the retention

and attraction of bio based businesses to Iowa.

Reco

mm

end

ation

s

Reasonable Regulations and Taxes

Adopt only regulations that are effective and sufficient to protect

Iowans and Iowa’s resources and that are based on science:

reasonable, consistent and practical. Assure a competitive

business tax structure and economic development incentives.

Strateg

y

Improve

Business Climate

Black = Priority Recommendation Gray = Secondary Recommendation

Business Environment

Regulations & Taxes

26 | Context | Iowa AgriScope 2030

• Support, to the greatest extent possible, research and innovation that builds

Iowa's agriculture production and value added endeavors.

• Recognize the value of research as both a basis and a catalyst for innovation

and provide Iowa's public research institutions with the resources needed to

effectively foster innovation.

• Establish and foster an innovative and entrepreneurial climate throughout

Iowa’s education systems.

• Strengthen the exchange of knowledge between science and

business/industry.

Reco

mm

end

ation

s

World Class Research and Education

Assure that Iowa State University is second to none in its

agriculture and related sectors’ research, development and

education, due to leadership levels of funding and focused

administration. Gain global respect for Iowa’s public and private

research communities. Develop education systems that provide

knowledge and training for the many jobs to be created in

agriculture production and related processing and support sectors.

Strateg

y

Encourage

Innovation

Innovation Reputation

Research & Education

Black = Priority Recommendation Gray = Secondary Recommendation

27 | Context | Iowa AgriScope 2030

• Increase the production of established Iowa commodities, both crop and

livestock.

Reco

mm

end

ation

s

Build the Base

Meet both local and world demand by increasing production of

Iowa’s leading agriculture crops, livestock and products. Lead the

world in quality and reliability with Iowa’s diverse spectrum of

commodities that are raised via innovative and sustainable

production methods.

Strateg

y

Build

the Base

Black = Priority Recommendation Gray = Secondary Recommendation

28 | Context | Iowa AgriScope 2030

• Lead efforts to open markets for Iowa commodities and value-added products.

• Include Iowa-based animal health products and production systems in

promotion efforts, as livestock production continues to increase globally.

• Promote and market Iowa agriculture and processing knowledge, expertise and

management skills: Knowledge based consulting for bio fuels processing, food

safety, food processing, livestock production, etc.

Reco

mm

end

ation

s

Expand Exports

Lead the US in export of basic commodities and processed bio

products due to Iowa’s great productivity and even greater

reputation for high quality production and processing.

Strateg

y

Expand Exports

Black = Priority Recommendation Gray = Secondary Recommendation

29 | Context | Iowa AgriScope 2030

• Build on global leadership in value-added products (i.e. bio-fuels, meat and

other food processing).

• Add value to the value-added and build on the success of Iowa businesses.

• Recruit further processing businesses to locate and grow in Iowa, especially in

rural communities.

• Develop infrastructure and systems that support segregation, storage,

movement and marketing of value-added crops and products, specialty crops,

livestock, etc.

Reco

mm

end

ation

s

Add Value

Utilize cutting edge technologies and Iowa’s quality workforce to

convert an abundance of basic commodities and cutting edge

technologies, systems into value-added products.

Strateg

y

Add Value

Black = Priority Recommendation Gray = Secondary Recommendation

30 | Context | Iowa AgriScope 2030

Secondary StrategiesIncluding Recommendations

31 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

• Influence Congress to appropriate funding for lock expansion projects on the

Upper Mississippi and Illinois rivers authorized in the 2007 Water Resources

Development Act.

• Assure that the Missouri River is maintained as a viable option for commercial

movement of western Iowa commodities and related products into the

extensive US inland waterway system and global markets.

• Plan for projected increases in Iowa crop and livestock production, food and

fuel processing and manufacturing, and resultant truck traffic increases.

• Assure adequate freight rail line capacity, access and provider options to serve

agricultural production and processed product rail needs.

Reco

mm

end

ation

s

Improved Transportation Infrastructure

Build a healthy mix of transportation systems that give producers,

processors, manufacturers and input providers the options they

need for competitive pricing and market access flexibility. Costs to

move Iowa’s products to national and world markets are as low as

any competing state or country.

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

Black = Priority Recommendation Gray = Secondary Recommendation

32 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

• Educate, recruit, attract and retain a workforce with knowledge of and passion

about production agriculture, processing and the businesses that serve

agriculture and processing.

Reco

mm

end

ation

s

Qualified, Adequate Workforce

Create opportunities in the bio economy that encourage the best

and brightest to remain in Iowa and become involved in aspects of

the broad agriculture field. Educate and prepare Iowans to take

leadership roles, advancing technology and developing

innovations that improve Iowa’s agriculture production and

processing sectors. Assure that there is enough available labor to

meet needs.

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

Black = Priority Recommendation Gray = Secondary Recommendation

33 | Context | Iowa AgriScope 2030

• Convince Iowa businesses and those considering locating or investing here

that Iowa is “Open for Business” and is ready to help resolve problems or

share opportunities.

• Support the new Iowa Partnership for Economic Progress (I-PEP) and its

public-private approach to economic development. Assure the new system is

supportive of a bio based economy and that its needs are prioritized.

• Assure broadband transmission is available to Iowa communities for use by

agriculture businesses, processing businesses, input providers and assure the

integrity of satellite transmissions to GPS receivers.

Reco

mm

end

ation

s

Supportive Business Environment

Develop a reputation for a progressive and supportive form of

government economic development that helps established

businesses resolve problems and new businesses more easily

establish, grow, and prosper. Create a business climate that

encourages commodity processing and further processing

businesses to start in Iowa, come to Iowa and create Iowa jobs.

Strateg

y

Improve

Business Climate

Black = Priority Recommendation Gray = Secondary Recommendation

Business Environment

Regulations & Taxes

34 | Context | Iowa AgriScope 2030

• Create a climate for innovation in agriculture, food, fiber, f(ph)armaceutical and

renewable fuel businesses, and in the supporting sciences.

• Encourage and support entrepreneurism.

Reco

mm

end

ation

s

Innovation Reputation

Strive to make Iowa known for its culture of innovation and

technology development, and develop valuable support systems

for both. Once those systems are firmly in place, protect them for

use by Iowa’s business, academia and government leaders.

Support entrepreneurism with actions that help translate

innovation into increased economic activity.

Strateg

y

Encourage

Innovation

Innovation Reputation

Research & Education

Black = Priority Recommendation Gray = Secondary Recommendation

35 | Context | Iowa AgriScope 2030

• Provide an environment in which non-traditional ideas, farming operations and

businesses may establish a foothold and grow.

• Review the needs of new, innovative agriculture production and processing and

prioritize efforts to help with those needs.

• Assist ‘new to Iowa’ production and processing in their efforts to access

investment capital.

Reco

mm

end

ation

s

Nurture the New

Embrace diversity in agriculture production to provide food and

other agriculture products for a variety of markets, especially

Iowans who prefer locally-sourced and/or organic foodstuffs.

Strateg

y

Nurture

the New

Black = Priority Recommendation Gray = Secondary Recommendation

36 | Context | Iowa AgriScope 2030

• Lead campaign to increase the size and scope of Iowa agriculture.

• Achieve effective collaboration between agriculture and related sectors by

encouraging formation of an organization or system that becomes a foundation

for cooperation and issue prioritization across Iowa’s diverse agriculture sector.

Reco

mm

end

ation

s

Leadership

Black = Priority Recommendation Gray = Secondary Recommendation

Leadership

Iowa’s government, business and association leaders believe in

the importance of agriculture and associated sectors to Iowa’s

economy and align their efforts to maintain growth. They are

supported in their efforts by a cohesive industry that sets priorities

and proves itself worthy of leadership’s efforts.

Strateg

y

Questions

For Further Information,

Please Contact:

THE CONTEXT NETWORK4401 Westown Parkway, Suite 214

West Des Moines, IA 50266

Phone: 515/225-2204

Fax: 515/225-0039

www.contextnet.com

37 | Context | Iowa AgriScope 2030

Chapter 3: Full Report

38 | Context | Iowa AgriScope 2030

Goal & Strategic Framework

39 | Context | Iowa AgriScope 2030

Early in the process, a simple yet powerful goal was articulated

40 | Context | Iowa AgriScope 2030

Increase the Size and Scope

of Iowa Agriculture

41 | Context | Iowa AgriScope 2030

Increase the Size and Scope of Iowa Agriculture

Expansion of Iowa agriculture’s

economic activity requires a rock-

solid foundation, so this project

began with an exploration of what

can be done to protect and improve

Iowa’s existing strengths.

With a strong foundation, Iowa

agriculture can expand in several

directions, depicted as four

opportunities in the top half of the

graphic.

Using analysis and Steering Committee input, a vision was developed to

depict the areas of focus most essential to achieve the goal

Objectives

Strategies

Leadership

This strategic framework was built on nearly 100 interviews and

Steering Committee discussion

42 | Context | Iowa AgriScope 2030

GoalIncrease the size

and scope of Iowa agriculture

Protect Comparative Advantages

Strong Soil, Safe Water

Qualified, Adequate Workforce

Improved Transportation Infrastructure

Improve Business Climate

Reasonable Regulations &

Taxes

Business Environment

Encourage Innovation

World Class Research & Education

Innovation Reputation

Expand Economic Activity

Build the Base

Add Value

Expand Exports

Nurture the New

Objectives

Strategies

Leadership

Priorities within the Strategic Framework were identified with support

from the Steering Committee

43 | Context | Iowa AgriScope 2030

GoalIncrease the size

and scope of Iowa agriculture

Protect Comparative Advantages

Strong Soil, Safe Water

Qualified, Adequate Workforce

Improved Transportation Infrastructure

Improve Business Climate

Reasonable Regulations &

Taxes

Business Environment

Encourage Innovation

World Class Research & Education

Innovation Reputation

Expand Economic Activity

Build the Base

Add Value

Expand Exports

Nurture the NewPriority Strategies Secondary Strategies

Recommendations were developed for all Strategies and prioritized with

support from the Steering Committee

44 | Context | Iowa AgriScope 2030

Objectives

Strategies

Recommendations

Protect Comparative Advantages

Strong Soil, Safe Water

Re-energize Iowa’s commitment to soil

stewardship, addressing both retention and quality

concerns.

Protect Iowa’s ground water and surface water while

optimizing efficient utilization for both production &

processing.

Prioritize vulnerable landscapes and soils for

federal and state incentive programs.

Priority Recommendations Secondary Recommendations

EXAMPLE

Actions were identified for all Recommendations as were Rationale and

Responsibilities

45 | Context | Iowa AgriScope 2030

Strategies

Recommendations

Actions

EXAMPLEStrong Soil, Safe Water

Re-energize Iowa’s commitment to soil

stewardship, addressing both retention

and quality concerns.

Work toward and maintain a limit of soil loss tolerance (T) or

less.

Protect and retain current soil saving structures/practices

and resist incentives to farm through or over them.

Research use of cover crops as a potential mitigation for

soil loss created by the increasing number of heavy rain

events in Iowa.

Encourage landlords to use leases that include incentives

for improving the quality of their soil and conservation

practices.

Promote the value of adding organic matter to Iowa soils by

proving long-term enhancement of productive capacity and

retention of top soil.

Employ practices recommended to increase organic carbon

levels in soil such as no-till, cover crops, crop rotation and

use of livestock manure for fertilizer.

Educate landlords about the value of their asset and the

potential to lose that value through tillage practices that do

not protect the soil from eroding and losing organic matter.

46 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

Re-energize Iowa’s commitment to soil stewardship, addressing

both retention and quality concerns.

Reco

m.

Strong Soil, Safe Water

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

• Work toward and maintain a limit of soil loss tolerance (T) or less.

• Protect and retain current soil saving structures/practices and resist incentives

to farm through or over them.

• Research use of cover crops as a potential mitigation for soil loss created by

the increasing number of heavy rain events in Iowa.

• Educate landlords about the value of their asset and the potential to lose that

value through tillage practices that do not protect the soil from eroding and

losing organic matter.

• Encourage landlords to use leases that include incentives for improving the

quality of their soil and conservation practices.

• Promote the value of adding organic matter to Iowa soils by proving long-term

enhancement of productive capacity and retention of top soil.

• Employ practices recommended to increase organic carbon levels in soil such

as no-till, cover crops, crop rotation and use of livestock manure for fertilizer.

Actio

ns

EXAMPLE

47 | Context | Iowa AgriScope 2030

Iowa is blessed with some of the most productive soil on earth, and

Iowa producers have long recognized the value of protecting those

soils. As costs of production increase, though, many find it tempting to

till vulnerable land or employ tillage systems that are less than

protective. Both farmers and landowners are encouraged to recommit to

saving soil and, in fact, improving its quality when possible. Leadership

levels of production and soil stewardship can be achieved through a

continuing quest for reduced tillage practices, appropriate balances of

livestock manure and other nutrient sources, and emerging production

technologies.

According to an ISU study, compaction, erosion and loss of organic

matter have led to a decline in the quality of Iowa’s soils over the past

50 years. Organic matter content in Iowa soils has dropped from an

average of 10% to two percent. However, regaining soil quality can be

achieved by adding organic matter and employing tillage methods that

reverse compaction and reduce erosion

Strong Soil, Safe Water - Rationale

Re-energize Iowa’s commitment to soil stewardship, addressing both retention and quality

concerns.

Sources: Soil Quality, Better Lawns Made Easy, Polk Soil & Water Conservation District and Iowa Storm

Water Education Program; ISU Research: Iowa has lower-quality topsoil than 50 years ago,

EXAMPLE

Photo Source: ISU Extension – Agronomy

48 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Responsibilities

Re-energize Iowa’s commitment to soil stewardship, addressing both retention and quality

concerns.

Actions Team Leader(s) Team Member(s)

Work toward and maintain a limit of soil loss tolerance

(T) or less.IDALS Ag Producers, SWCDs

Protect and retain current soil saving

structures/practices and resist incentives to farm

through or over them.

Ag Producers

Research use of cover crops as a potential mitigation

for soil loss created by the increasing number of heavy

rain events in Iowa.

ISU

Educate landlords about the value of their asset and

the potential to lose that value through tillage practices

that do not protect the soil from eroding and losing

organic matter.

SWCDs USDA NRCS, ISU, Ag Producers

Encourage landlords to use leases that include

incentives for improving the quality of their soil and

conservation practices.

IDALS, Ag Producers, SWCDs ISU

Promote the value of adding organic matter to Iowa

soils by proving long-term enhancement of productive

capacity and retention of top soil.

SWCDs USDA NRCS, IDALS, Ag Producers

Employ practices recommended to increase organic

carbon levels in soil such as no-till, cover crops, crop

rotation and use of livestock manure for fertilizer.

Ag Producers

EXAMPLE

Priority StrategiesIncluding Recommendations, Actions, Rationales and Responsibilities

49 | Context | Iowa AgriScope 2030

50 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

• Re-energize Iowa’s commitment to soil stewardship, addressing both retention

and quality concerns.

• Protect Iowa’s ground and surface water while optimizing efficient utilization for

both production and processing.

• Prioritize vulnerable landscapes and soils for federal and state incentive

programs.

Reco

mm

end

ation

s

Strong Soil, Safe Water

Through producers’ adoption of innovative tillage methods and

technologies, achieve optimum quality levels for Iowa soils and

limit soil loss to replacement levels. Eliminate water quality

concerns, and assure abundant, clean water supplies that provide

an advantage when attracting and growing agriculture-related

manufacturing and processing.

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

Black = Priority Recommendation Gray = Secondary Recommendation

51 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

Re-energize Iowa’s commitment to soil stewardship, addressing

both retention and quality concerns.

Reco

m.

Strong Soil, Safe Water

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

• Work toward and maintain a limit of soil loss tolerance (T) or less.

• Protect and retain current soil saving structures/practices and resist incentives

to farm through or over them.

• Research use of cover crops as a potential mitigation for soil loss created by

the increasing number of heavy rain events in Iowa.

• Educate landlords about the value of their asset and the potential to lose that

value through tillage practices that do not protect the soil from eroding and

losing organic matter.

• Encourage landlords to use leases that include incentives for improving the

quality of their soil and conservation practices.

• Promote the value of adding organic matter to Iowa soils by proving long-term

enhancement of productive capacity and retention of top soil.

• Employ practices recommended to increase organic carbon levels in soil such

as no-till, cover crops, crop rotation and use of livestock manure for fertilizer.

Actio

ns

52 | Context | Iowa AgriScope 2030

Iowa is blessed with some of the most productive soil on earth, and

Iowa producers have long recognized the value of protecting those

soils. As costs of production increase, though, many find it tempting to

till vulnerable land or employ tillage systems that are less than

protective. Both farmers and landowners are encouraged to recommit to

saving soil and, in fact, improving its quality when possible. Leadership

levels of production and soil stewardship can be achieved through a

continuing quest for reduced tillage practices, appropriate balances of

livestock manure and other nutrient sources, and emerging production

technologies.

According to an ISU study, compaction, erosion and loss of organic

matter have led to a decline in the quality of Iowa’s soils over the past

50 years. Organic matter content in Iowa soils has dropped from an

average of 10% to two percent. However, regaining soil quality can be

achieved by adding organic matter and employing tillage methods that

reverse compaction and reduce erosion.

Strong Soil, Safe Water - Rationale

Re-energize Iowa’s commitment to soil stewardship, addressing both retention and quality

concerns.

Sources: Soil Quality, Better Lawns Made Easy, Polk Soil & Water Conservation District and Iowa Storm

Water Education Program; ISU Research: Iowa has lower-quality topsoil than 50 years ago,

Photo Source: ISU Extension – Agronomy

53 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Responsibilities

Re-energize Iowa’s commitment to soil stewardship, addressing both retention and quality

concerns.

Actions Team Leader(s) Team Member(s)

Work toward and maintain a limit of soil loss tolerance

(T) or less.IDALS Ag Producers, SWCDs

Protect and retain current soil saving

structures/practices and resist incentives to farm

through or over them.

Ag Producers

Research use of cover crops as a potential mitigation

for soil loss created by the increasing number of heavy

rain events in Iowa.

ISU

Educate landlords about the value of their asset and

the potential to lose that value through tillage practices

that do not protect the soil from eroding and losing

organic matter.

SWCDs USDA NRCS, ISU, Ag Producers

Encourage landlords to use leases that include

incentives for improving the quality of their soil and

conservation practices.

IDALS, Ag Producers, SWCDs ISU

Promote the value of adding organic matter to Iowa

soils by proving long-term enhancement of productive

capacity and retention of top soil.

SWCDs USDA NRCS, IDALS, Ag Producers

Employ practices recommended to increase organic

carbon levels in soil such as no-till, cover crops, crop

rotation and use of livestock manure for fertilizer.

Ag Producers

54 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

Protect Iowa’s ground and surface water while optimizing

efficient utilization for both production and processing.

Reco

m.

Strong Soil, Safe Water

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

• Take a national leadership role, through a Nutrient Management Strategy, in

developing approaches to water quality protection that do not unnecessarily

compromise production practices or processing needs.

• Continue to administer fair and reasonable regulations that prevent run-off from

production agriculture and processing businesses into surface water supplies.

Actio

ns

55 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Rationale

Protect Iowa’s ground and surface water while optimizing efficient utilization for both

production and processing.

Suggestions for the Iowa NMS:

Adoption of innovative, cost effective technologies that prevent the

tools and methods of production agriculture from compromising the

water resources of Iowa.

Prioritization of voluntary compliance over mandated regulation.

Organization of recommended actions on a watershed basis.

Inclusion of all vested interests in formulating watershed goals.

Source: Iowa Geology 1995, Iowa Department of Natural Resources

The Mississippi River flows through a narrow valley between

Davenport and Rock Island-Moline.

Globally, water is becoming an ever more precious

resource, so Iowa’s abundant water supply is a distinct

competitive advantage for economic growth built on

agriculture production and processing. Iowans are well

aware of the need to protect the quality of Iowa’s water

supplies both for its productive capacity and for the many

other benefits it affords Iowa’s citizens.

IDALS, IDNR, ISU and several ag organizations have

begun a comprehensive, thoughtful and proactive

process to build a Nutrient Management Strategy (NMS)

for the state. The goal of the strategy is to protect the

state’s waters but will also lead to more efficient use of

applied production inputs, further reduction in soil loss

and possible mitigation of the hypoxia situation in the

Gulf of Mexico

56 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Actions and Responsibilities

Protect Iowa’s ground and surface water while optimizing efficient utilization for both

production and processing.

Actions Team Leader(s) Team Member(s)

Take a national leadership role, through a Nutrient

Management Strategy, in developing approaches to

water quality protection that do not unnecessarily

compromise production practices or processing

needs.

Iowa Secretary of AgIDALS, Ag & Commodity Organizations,

Ag Producers, SWCDs

Continue to administer fair and reasonable regulations

that prevent run-off from production agriculture and

processing businesses into surface water supplies.

IDNR

57 | Context | Iowa AgriScope 2030

Protect Comparative Advantage

Prioritize vulnerable landscapes and soils for federal and state

incentive programs.

Reco

m.

Strong Soil, Safe Water

Strateg

y

Workforce

Soil &

Water

Transportation

Infrastructure

• Target vulnerable landscapes that need more protective measures and,

possibly, more incentive for set-aside.

• Release non-vulnerable land from protection, or set-aside, in order to meet

growing production needs.

Actio

ns

58 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Rationale

Prioritize vulnerable landscapes and soils for federal and state incentive programs.

The original purposes of federal land diversion

programs, to protect vulnerable soils and to reduce

chronic production surpluses, have become

overshadowed in the past couple decades by their

popularity as a means to provide wildlife habitat

and recreational opportunities.

This trend has pulled current policies and programs

away from adequately protecting vulnerable

landscapes. According to ISU economist Chad

Hart, “Given the strength of crop prices, both in

recent years and projected into the future, land

diversion subsidies are no longer needed by U.S.

agriculture. Biofuel and international markets have

grown tremendously, removing excess

supplies. High prices indicate the need for more

crop production to meet demands, requiring that

land be brought back into production.

In order to meet this challenge, those crafting

federal farm policy should explore innovative,

strategic, and selective approaches to land

retirement and conservation programs that protect

the most environmentally sensitive lands, while

maintaining the environmental benefits from

previous programs and allowing other land to

reenter production in order to meet various food,

feed, fuel, and fiber demands.”

Source: Chad Hart, ISU, Assistant Professor Economics, Extension Economist, Grain Market Specialist

59 | Context | Iowa AgriScope 2030

Strong Soil, Safe Water - Responsibilities

Prioritize vulnerable landscapes and soils for federal and state incentive programs.

Actions Team Leader(s) Team Member(s)

Target vulnerable landscapes that need more

protective measures and, possibly, more incentive for

set-aside.

USDA NRCS Congress

Release non-vulnerable land from protection, or set-

aside, in order to meet growing production needs.USDA NRCS

60 | Context | Iowa AgriScope 2030

• Effect lasting improvement to the state regulatory and permitting processes.

• Administer reasonable, fair and relevant regulatory enforcement.

• Determine the effect that Iowa’s business tax ranking is having on the retention

and attraction of bio based businesses to Iowa.

Reco

mm

end

ation

s

Reasonable Regulations and Taxes

Adopt only regulations that are effective and sufficient to protect

Iowans and Iowa’s resources and that are based on science:

reasonable, consistent and practical. Assure a competitive

business tax structure and economic development incentives.

Strateg

y

Improve

Business Climate

Black = Priority Recommendation Gray = Secondary Recommendation

Business Environment

Regulations & Taxes

61 | Context | Iowa AgriScope 2030

Effect lasting improvement to the state regulatory and permitting

processes.

Reco

m.

Reasonable Regulations and Taxes

Strateg

y

• Pass only laws/regulations with sunset dates so that they must be revisited within a few

years and determined to be still valid, or not.

• Perform an in-depth scan of regulatory and permitting programs to identify those that are

not delivering the legislated intent.

• Evaluate systems proven to bring about improvement and choose one best suited to

Iowa’s government (i.e. Six Sigma, Good to Great, Lean Manufacturing, etc.).

• Provide funding and lead application of the chosen system to government agencies and

systems, beginning with regulatory and permitting programs that affect agriculture and

related businesses.

• Process applications and permits in a timely, professional manner. Notify applicants

immediately if there is a problem with the application and/or notify of delays in the

process.

• Reform the permit system to allow applications and permits to cover the entire state, not

just a particular jurisdiction.

• Reform the permit system to allow amendment of permits, so that reapplication is not

necessary each time regulations change or when businesses change only one aspect of

their operation.

Actio

ns

Business Environment

Regulations & Taxes

Improve

Business Climate

62 | Context | Iowa AgriScope 2030

Reasonable Regulations and Taxes - Rationale

Effect lasting improvement to the state regulatory and permitting processes.

Concerns and criticisms about Iowa’s regulatory and permitting systems have been an

overarching theme of this project. Interviewees feel strongly that the systems are not

administered consistently and that rules, regulations and permitting processes change too

often. Conflicts arise when systems and processes are not applied with an understanding of

business pressures, causing costly delays or unnecessary adaptations.

Costs of regulation are often regarded as ‘hidden taxes’ that provide revenue for the state in

lieu of raising taxes. If regulations and the permitting process are also inefficient, the cost is

increased, but without benefit to either the state or the business being regulated. Studies show

that small businesses bear a disproportionate burden for most regulations, and the vast

majority of Iowa’s businesses employ fewer than 100 people.

“Environmental and tax compliance regulations appear to be the main cost drivers in determining the severity of the disproportionate impact on small firms.Compliance with environmental regulations costs 364 percent more in small firms than in large firms.The cost of tax compliance is 206 percent higher in small firms than the cost in large firms.”

Source: The impact of regulatory costs on small firms, Nicole V. Crain and W. Mark Crain, Lafayette College, 2010

63 | Context | Iowa AgriScope 2030

Reasonable Regulations and Taxes - Responsibilities

Effect lasting improvement to the state regulatory and permitting processes.

Actions Team Leader(s) Team Member(s)

Pass only laws/regulations with sunset dates so that

they must be revisited within a few years and

determined to be still valid, or not.

Iowa Legislature Iowa Governor

Perform an in-depth scan of regulatory and permitting

programs to identify those that are not delivering the

legislated intent.

Iowa Governor IDNR and Other Regulatory Agencies

Evaluate systems proven to bring about improvement

and choose one best suited to Iowa’s government (i.e.

Six Sigma, Good to Great, Lean Manufacturing, etc.).

Iowa Governor

Provide funding and lead application of the chosen

system to government agencies and systems,

beginning with regulatory and permitting programs that

affect agriculture and related businesses.

Iowa Governor Iowa Legislature

Process applications and permits in a timely,

professional manner. Notify applicants immediately if

there is a problem with the application and/or notify of

delays in the process.

IDNR and Other Regulatory Agencies

Reform the permit system to allow applications and

permits to cover the entire state, not just a particular

jurisdiction.

IDNR and Other Regulatory AgenciesIowa Governor, Iowa Legislature, Rural

Counties/Communities

Reform the permit system to allow amendment of

permits, so that reapplication is not necessary each

time regulations change or when businesses change

only one aspect of their operation.

IDNR and Other Regulatory AgenciesIowa Governor, Iowa Legislature, Rural

Counties/Communities

64 | Context | Iowa AgriScope 2030

Administer reasonable, fair and relevant regulatory enforcement.

Reco

m.

Reasonable Regulations and Taxes

Strateg

y

• Punish habitual offenders and scofflaws, but bring reason to bear on apparent

mistakes, misunderstandings or alternative interpretation of the regulation,

especially for first-time offenders.

• Create a culture of goal-directed enforcement within state regulatory agencies

(enforcement should be directed by the goal of the regulation) and discourage

a ‘gotcha’ approach.

Actio

ns

Business Environment

Regulations & Taxes

Improve

Business Climate

65 | Context | Iowa AgriScope 2030

Reasonable Regulations and Taxes - Rationale

Administer reasonable, fair and relevant regulatory enforcement.

There is general agreement among those interviewed for this project that habitual offenders of

state and federal regulations should be dealt with harshly and, when appropriate, made to

leave the state and/or give up their business or enterprise in Iowa. They also acknowledge a

need for certain regulations and permits.

However, they expressed concerns about unreasonable enforcement of the regulations,

especially when a “gotcha” approach is used. Most agree that the goal of the regulation will be

achieved more readily if the enforcement effort leads to greater understanding and compliance

than if the enforcement is arbitrary and unevenly administered.

Environmental and tax compliance regulations

appear to be the main cost drivers in determining

the severity of the disproportionate impact on

small firms. Compliance with environmental

regulations costs 364% more in small firms than

in large firms. The cost of tax compliance is 206%

higher in small firms than the cost in large firms.

Source: The Impact of Regulatory Costs on Small Firms, US Commerce Department

Photo Source: Iowa Pork Producer Association, Vol 47, No. 6-7, July 2010

66 | Context | Iowa AgriScope 2030

Reasonable Regulations and Taxes - Responsibilities

Administer reasonable, fair and relevant regulatory enforcement.

Actions Team Leader(s) Team Member(s)

Punish habitual offenders and scofflaws, but bring

reason to bear on apparent mistakes,

misunderstandings or alternative interpretation of the

regulation, especially for first-time offenders.

IDNR and Other Regulatory Agencies

Create a culture of goal-directed enforcement within

state regulatory agencies (enforcement should be

directed by the goal of the regulation) and discourage

a ‘gotcha’ approach.

IDNR and Other Regulatory Agencies Iowa Governor

67 | Context | Iowa AgriScope 2030

Determine the effect that Iowa’s business tax ranking is having

on the retention and attraction of bio based businesses to Iowa.

Reco

m.

Reasonable Regulations and Taxes

Strateg

y

• If analysis proves advisable, take measures to improve Iowa’s business tax

ranking over the next five years, then continue to strive for an ever more

business-friendly tax structure.

• Lower corporate income tax or provide a tax credit for investment to offset

inhibiting effect of business tax.

Actio

ns

Business Environment

Regulations & Taxes

Improve

Business Climate

68 | Context | Iowa AgriScope 2030

Reasonable Regulations and Taxes - Rationale

Iowa ranks 45th in the Tax Foundation‘s 2011 State Business Tax Climate Index.

The Index compares the states in five areas of taxation that impact business: corporate

taxes; individual income taxes; sales taxes; unemployment insurance taxes; and taxes on

property, including residential and commercial property.

2009 State Business Tax Ranks

Iowa (45th)

Minnesota (43rd)

Wisconsin (40th)

Illinois (23rd)

Missouri (16th)

Nebraska (29th)South Dakota (1st)

State leaders and those intent on adding value to

Iowa commodities are concerned that business

taxes are a factor in businesses’ decisions to locate

or grow in another state. A focused study would

determine the actual effect that taxes are having on

businesses considering locating in Iowa and

determine the changes that would have the most impact.

Determine the effect that Iowa’s business tax ranking is having on the retention and attraction

of bio based businesses to Iowa.

Source: Tax Foundation website

69 | Context | Iowa AgriScope 2030

Reasonable Regulations and Taxes - Responsibilities

Determine the effect that Iowa’s business tax ranking is having on the retention and attraction of bio

based businesses to Iowa.

Actions Team Leader(s) Team Member(s)

If analysis proves advisable, take measures to improve

Iowa’s business tax ranking over the next five years,

then continue to strive for an ever more business-

friendly tax structure.

Iowa Governor Iowa Legislature

Lower corporate income tax or provide a tax credit for

investment to offset inhibiting effect of business tax.Iowa Legislature Iowa Governor

70 | Context | Iowa AgriScope 2030

• Support, to the greatest extent possible, research and innovation that builds

Iowa's agriculture production and value added endeavors.

• Recognize the value of research as both a basis and a catalyst for innovation

and provide Iowa's public research institutions with the resources needed to

effectively foster innovation.

• Establish and foster an innovative and entrepreneurial climate throughout

Iowa’s education systems.

• Strengthen the exchange of knowledge between science and

business/industry.

Reco

mm

end

ation

s

World Class Research and Education

Assure that Iowa State University is second to none in its

agriculture and related sectors’ research, development and

education, due to leadership levels of funding and focused

administration. Gain global respect for Iowa’s public and private

research communities. Develop education systems that provide

knowledge and training for the many jobs to be created in

agriculture production and related processing and support sectors.

Strateg

y

Encourage

Innovation

Innovation Reputation

Research & Education

Black = Priority Recommendation Gray = Secondary Recommendation

71 | Context | Iowa AgriScope 2030

Support, to the greatest extent possible, research and innovation

that builds Iowa's agriculture production and value added

endeavors.

Reco

m.

World Class Research and Education

Strateg

y

• Increase funding levels for public research that develops pathways for

sustainable production increases and profitability: solving problems of

commercial crop and livestock production.

• Support research and development of processes that turn bi-products and

waste materials into usable products.

• Support biofuels research and development to stay on the cutting edge of new

efficiencies and technologies.

Actio

ns

Innovation Reputation

Research & Education

Encourage

Innovation

72 | Context | Iowa AgriScope 2030

World Class Research and Education - Rationale

Support, to the greatest extent possible, research and innovation that builds Iowa's

agriculture production and value added endeavors.

It is widely accepted that there have been four key factors in the success of Midwest

agriculture: natural resources, transportation infrastructure, people . . . .and research.

More than a century of basic agriculture research, supported by the federal and state

governments and conducted at public universities, has brought Iowa and neighboring states

from subsistence farming to global powerhouse.

That productivity and competitive advantage is in jeopardy, as government funding for basic

research dissipates and institutions struggle to find replacement funding.

The National Agricultural Research, Extension,

Education and Economics Advisory Board has

recommended “ at least a 25% increase in the

annual growth rate of funding of agricultural

productivity enhancing research and extension” to

counter “a number of adverse consequences, both

nationally and internationally” resulting from two

decades of stagnate funding.

Source: A Report on Agricultural Productivity and Agricultural Research,

National Agricultural Research, Extension, Education and Economics

Advisory Board, 2011

Photo Source: West Liberty Foods

73 | Context | Iowa AgriScope 2030

World Class Research and Education – Responsibilities

Support, to the greatest extent possible, research and innovation that builds Iowa's

agriculture production and value added endeavors.

Actions Team Leader(s) Team Member(s)

Increase funding levels for public research that

develops pathways for sustainable production

increases and profitability: solving problems of

commercial crop and livestock production.

Congress, Iowa Legislature

USDA, Iowa Governor, Iowa Secretary of

Ag, ISU, Ag & Commodity Organizations,

Ag Producers

Support research and development of processes that

turn bi-products and waste materials into usable

products.

Businesses

USDA, Iowa Governor, Iowa Legislature,

ISU, Ag & Commodity Organizations, Ag

Producers

Support biofuels research and development to stay on

the cutting edge of new efficiencies and technologies.Businesses

USDA, Iowa Governor, Iowa Legislature,

ISU, Ag & Commodity Organizations

74 | Context | Iowa AgriScope 2030

Recognize the value of research as both a basis and a catalyst

for innovation and provide Iowa's public research institutions with

the resources needed to effectively foster innovation.

Reco

m.

World Class Research and Education

Strateg

y

• Focus currently available state funding on research and development programs

that foster innovation and lead to economic activity.

• Reward those institutions or individuals who focus their research on innovative,

cutting edge solutions to current and emerging challenges in Iowa’s agriculture

industry.

• Increase state support of research and development that improves Iowa’s

position as an agriculture, food and renewable fuel innovator.

• Maximize resources and achieve better, quicker research results by providing

leadership for collaboration with other states’ and countries’ research

institutions.

• Provide an information infrastructure that makes it possible for Iowa

researchers to monitor and manage research and development around the

world.

• Tie state research funding to an incentive to develop and commercialize in

Iowa.

Actio

ns

Innovation Reputation

Research & Education

Encourage

Innovation

75 | Context | Iowa AgriScope 2030

World Class Research and Education - Rationale

Recognize the value of research as both a basis and a catalyst for innovation and provide

Iowa's public research institutions with the resources needed to effectively foster innovation.

Iowa’s research institutions, businesses,

producers and associations are actually quite

innovative and entrepreneurial. However,

Iowa is not yet known for this asset, so greater

efforts are needed to raise its profile while

further improving its innovation base and

entrepreneurial support.

While increased funding for innovative

research is an important first step, other

incentives and encouragements can be

employed to attract and keep the most

innovative, problem-solving researcher teams

in Iowa.

The chain linked model of innovation, portraying the interplay of research

and innovation. Source: The Role of Basic Research in Innovation, Magnus Gulbrandsen

76 | Context | Iowa AgriScope 2030

World Class Research and Education – Responsibilities

Recognize the value of research as both a basis and a catalyst for innovation and provide

Iowa's public research institutions with the resources needed to effectively foster innovation.

Actions Team Leader(s) Team Member(s)

Focus currently available state funding on research

and development programs that foster innovation and

lead to economic activity.

ISUIowa Governor, Iowa Legislature, Other

Universities

Reward those institutions or individuals who focus their

research on innovative, cutting edge solutions to

current and emerging challenges in Iowa’s agriculture

industry.

Board of RegentsIowa Governor, Iowa Legislature, IDALS, I-

PEP

Increase state support of research and development

that improves Iowa’s position as an agriculture, food

and renewable fuel innovator.

Iowa Governor, Iowa Legislature

Maximize resources and achieve better, quicker

research results by providing leadership for

collaboration with other states’ and countries’ research

institutions.

ISU Other Universities

Provide an information infrastructure that makes it

possible for Iowa researchers to monitor and manage

research and development around the world.

BusinessesIowa Governor, Iowa Legislature, ISU,

Other Universities

Tie state research funding to an incentive to develop

and commercialize in Iowa.ISU Iowa Governor, Iowa Legislature

77 | Context | Iowa AgriScope 2030

Establish and foster an innovative and entrepreneurial climate

throughout Iowa’s education systems.

Reco

m.

World Class Research and Education

Strateg

y

• Develop and encourage K-12 and post-secondary education programs that

support entrepreneurial activities and innovation.

• Encourage an innovation and entrepreneurship component for STEM.

• Support, encourage and raise the profile of community college and university

education programs that foster innovation.

Actio

ns

Innovation Reputation

Research & Education

Encourage

Innovation

78 | Context | Iowa AgriScope 2030

World Class Research and Education - Rationale

Establish and foster an innovative and entrepreneurial climate throughout Iowa’s education

systems.

Important steps have been taken to foster bio economy innovation

and entrepreneurship in Iowa’s school children through Iowa’s

STEM program.

By giving Iowa’s students, from kindergarten

through post-secondary, the tools and

encouragement they need to excel in science,

technology, engineering and math, Iowa is also

creating a workforce ideally prepared for 21st

century agriculture innovation. Providing industry-

specific information and learning opportunities will

enhance Iowa youth’s understanding of agriculture,

food, fuel and f(ph)arma opportunities.

79 | Context | Iowa AgriScope 2030

World Class Research and Education – Responsibilities

Establish and foster an innovative and entrepreneurial climate throughout Iowa’s education

systems.

Actions Team Leader(s) Team Member(s)

Develop and encourage K-12 and post-secondary

education programs that support entrepreneurial

activities and innovation.

IDE local school boards

Encourage an innovation and entrepreneurship

component for STEM.IDE

Ag & Commodity Organizations,

Businesses

Support, encourage and raise the profile of community

college and university education programs that foster

innovation.

IDEISU, Other Universities, Community

Colleges, Board of Regents

80 | Context | Iowa AgriScope 2030

Strengthen the exchange of knowledge between science and

business/industry.

Reco

m.

World Class Research and Education

Strateg

y

• Fully utilize viable results of Iowa-based research to add value to Iowa

products.

Actio

ns

Innovation Reputation

Research & Education

Encourage

Innovation

81 | Context | Iowa AgriScope 2030

World Class Research and Education - Rationale

Strengthen the exchange of knowledge between science and business/industry.

Those interviewed for this project saw this recommendation as an

important component of expanding the scope of Iowa’s agriculture.

Universities are seen as economic drivers in developing and

transferring knowledge to the commercial marketplace.

They also provide fertile ground for creating a more innovative society

by imbuing students with entrepreneurial attitudes and approaches to

problem-solving.

This ‘third mission’, extension and outreach, is not universally

embraced, but if embraced in Iowa’s agriculture sector, would support

many of the recommendations developed during this project. Through

research and extension programs, ISU partners with businesses to

make fundamental and applied discoveries and then assure their

applicability to the marketplace.

82 | Context | Iowa AgriScope 2030

World Class Research and Education – Responsibilities

Strengthen the exchange of knowledge between science and business/industry.

Actions Team Leader(s) Team Member(s)

Fully utilize viable results of Iowa-based research to

add value to Iowa products.Businesses

ISU, Ag & Commodity Organizations, Ag

Producers

83 | Context | Iowa AgriScope 2030

• Increase the production of established Iowa commodities, both crop and

livestock.

Reco

mm

end

ation

s

Build the Base

Meet both local and world demand by increasing production of

Iowa’s leading agriculture crops, livestock and products. Lead the

world in quality and reliability with Iowa’s diverse spectrum of

commodities that are raised via innovative and sustainable

production methods.

Strateg

y

Build

the Base

Black = Priority Recommendation Gray = Secondary Recommendation

84 | Context | Iowa AgriScope 2030

Increase the production of established Iowa commodities, both

crop and livestock.

Reco

m.

Build the Base

Strateg

y

• Facilitate approval and adoption of technologies that will increase yields without

depleting or compromising resources.

• Promote and utilize livestock manure as a valuable, natural, locally-produced

source of nitrogen and organic matter.

• Capitalize on Iowa’s competitive advantage for livestock production and establish a

‘Protein Pro Team’ approach to promoting responsible growth in the sector.

• Adopt a pro-active, self-regulating attitude in order to prevent problems.

• Encourage and assist local communities that want to attract and support local

livestock production and food processing.

• Mitigate concerns/conflicts that arise from erroneous perceptions or cavalier

attitudes.

• Prevent the need for subsidy programs by providing access to revenue insurance,

loan guarantees, etc.

• Recognize the debt and equity capital needs of commodity producers, and

processors that source commodities, caused by increasingly volatile market cycles.

Actio

ns

Build

the Base

85 | Context | Iowa AgriScope 2030

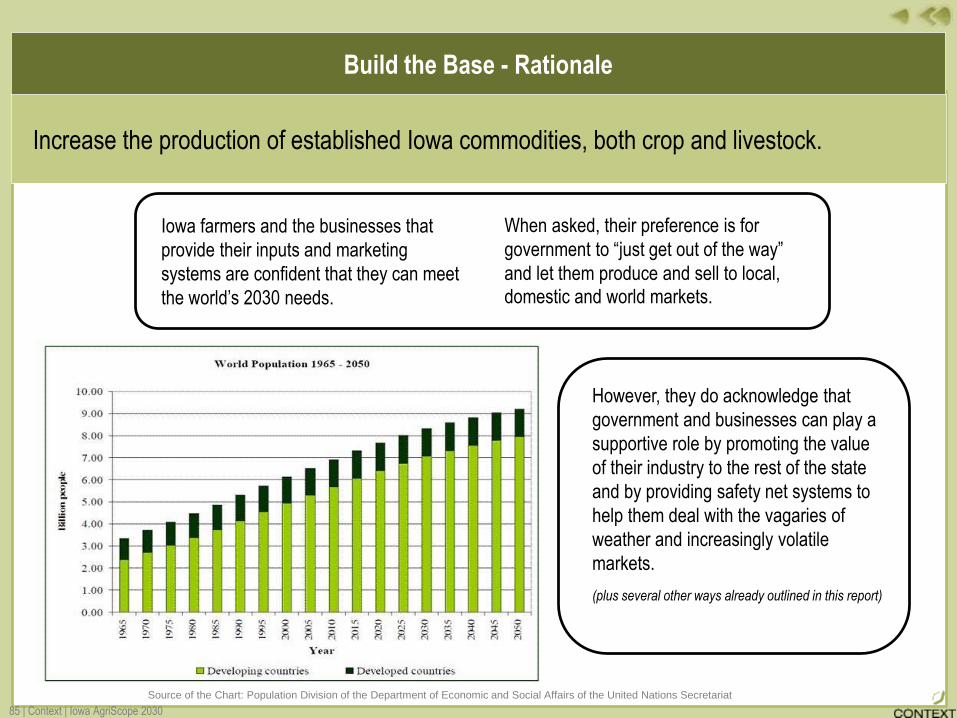

Build the Base - Rationale

Increase the production of established Iowa commodities, both crop and livestock.

Iowa farmers and the businesses that

provide their inputs and marketing

systems are confident that they can meet

the world’s 2030 needs.

Source of the Chart: Population Division of the Department of Economic and Social Affairs of the United Nations Secretariat

However, they do acknowledge that

government and businesses can play a

supportive role by promoting the value

of their industry to the rest of the state

and by providing safety net systems to

help them deal with the vagaries of

weather and increasingly volatile

markets.

(plus several other ways already outlined in this report)

When asked, their preference is for

government to “just get out of the way”

and let them produce and sell to local, domestic and world markets.

86 | Context | Iowa AgriScope 2030

Build the Base – Responsibilities

Increase the production of established Iowa commodities, both crop and livestock.

Actions Team Leader(s) Team Member(s)

Facilitate approval and adoption of technologies that

will increase yields without depleting or compromising

resources.

USDA

Congress, Iowa Secretary of Ag, ISU, Ag

& Commodity Organizations, Ag

Producers

Promote and utilize livestock manure as a valuable,

natural, locally-produced source of nitrogen and

organic matter.

Iowa Secretary of Ag

USDA, Iowa Legislature, IDALS, ISU, Ag

& Commodity Organizations, Ag

Producers, SWCDs, Coalition to Support

Farmers

Capitalize on Iowa’s competitive advantage for