ipl plastics plc 2017 results/media/files/i/ipl-plastics-plc/...2 disclaimer this presentation and...

TRANSCRIPT

March 2018

IPL Plastics plc2017 results

2

DisclaimerThis presentation and any oral information based upon such presentation (collectively hereinafter the “Presentation”), which is personal to the recipient, has been prepared by IPL Plastics plc

(“IPL Plastics” and together with IPL Plastics subsidiaries, the “Group”). By attending the meeting at which this Presentation is made, or by accepting or reading the slides that follow, you will

be deemed to have: (i) agreed to all of the conditions and restrictions contained herein; and (ii) acknowledged that you understand the legal and regulatory sanctions attached to the misuse,

disclosure or improper circulation of this Presentation.

The information provided in this Presentation is or may be price sensitive with respect to IPL Plastics shares traded on the “grey market” operated by Investec and Davy. Use of such

information may be regulated or prohibited by applicable legislation.

This Presentation does not constitute or form part of, and should not be construed as, an offer or invitation to sell or issue, or the solicitation of an offer to subscribe for, buy or acquire,

securities of IPL Plastics, or an inducement to enter into any investment activity in Ireland or the United Kingdom or in any other jurisdiction. Neither this document nor any part of it, or the fact

of its distribution, shall form the basis of, or be relied on in connection with, any contract therefor or investment decision in relation thereto.

The information in this Presentation has not been independently verified and does not purport to contain all of the information that may be required to evaluate an investment in the Group

and/or its financial position. Any prospective investors must make their own investigation, analysis and assessments and consult with their own adviser concerning the data referred to herein

and any evaluation of the Group and its prospects. IPL Plastics is not undertaking any obligation to provide any additional information or to update this Presentation or to correct any

inaccuracies that become apparent. The information contained in this Presentation is for background purposes only and is subject to material updating, completion, revision, amendment and

verification.

No representation or warranty, express or implied, is or will be given by IPL Plastics, its subsidiaries, its shareholders or their respective directors, officers, employees or advisers as to the

accuracy or completeness of this Presentation. To the extent permitted by law, no liability whatsoever is accepted by IPL Plastics, its subsidiaries, its shareholders or their respective directors,

officers, employees or advisers or any other person for any loss howsoever arising, whether directly or indirectly, from any use of this Presentation or such information or opinions contained

herein or otherwise arising in connection herewith. In particular, without limitation, no representation or warranty is given as to the achievement or reasonableness of any projection, estimate,

target or forecast in this Presentation, which it should be noted is provided for illustrative purposes only.

This Presentation contains forward-looking statements which reflect management’s current views and estimates. These forward looking statements involve certain risks and uncertainties that

could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions,

foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

Management undertake no responsibility to revise any such forward looking statements to reflect any changes in management’s expectations or any change in circumstances, events or the

Group’s plans and strategy. Accordingly, no reliance can be placed on the figures contained in such forward looking statements and no representation or warranty is given as to the

completeness or accuracy of the forward looking statements contained in this Presentation. The Group is under no obligation to update or keep current the information contained in this

Presentation, to correct any inaccuracies which may become apparent, or to publicly announce the result of any revision to the statements made herein and any opinions expressed in the

Presentation or in any related materials are subject to change without notice.

3

Consumer PackagingReturnable Packaging Solutions Large Format Packaging and

Environmental Solutions

Rigid Plastics

IPL Plastics plc supplies products to a broad range of customers primarily in the

USA, Canada, UK, Ireland and China from 14 production facilities across 3 primary

business categories

Group Overview

4

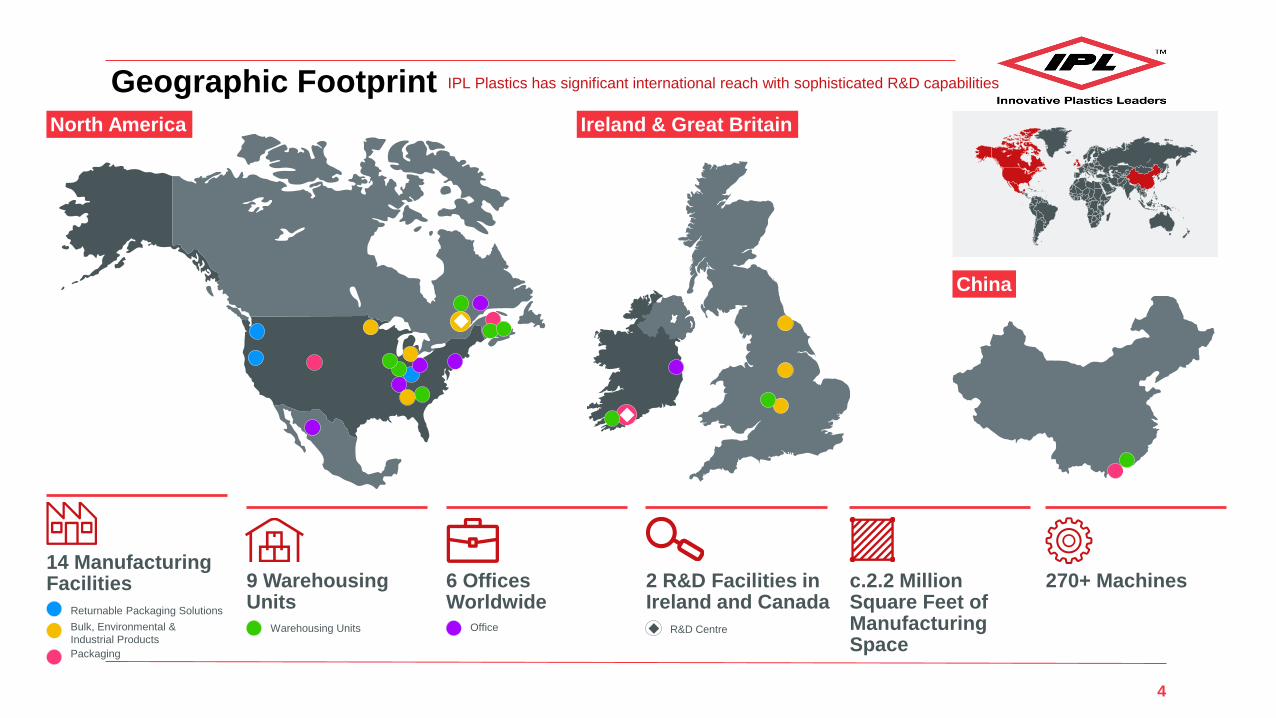

Geographic Footprint

Returnable Packaging Solutions

Bulk, Environmental &

Industrial Products

Packaging

Warehousing Units Office R&D Centre

IPL Plastics has significant international reach with sophisticated R&D capabilities

14 ManufacturingFacilities 9 Warehousing

Units6 OfficesWorldwide

2 R&D Facilities inIreland and Canada

c.2.2 MillionSquare Feet ofManufacturingSpace

270+ Machines

North America Ireland & Great Britain

China

5

2017 Trading Highlights

▪ 36.2% growth in Revenue² to €474.4m (2016: €348.2m)

▪ 46.0% increase in EBITDA² to €70.9m (2016: €48.5m)

▪ 47.3% growth in EBIT² to €41.6m (2016: €28.3m)

▪ Profit before exceptional and non-recurring items and share of equity-accounted investees profits

increased to €19.6m (2016: €17.9m)

▪ Profit for the period of €17.6m (2016: €16.1m)

▪ 8.8% increase in Adjusted diluted EPS to 12.01c (2016: 11.04c)

▪ EBITDA interest cover of 5.2x (2016: 6.2x)

▪ Total Assets of €621.9m (31 December 2016: €511.4m)

▪ Total Equity (excluding IPL Put Liability) of €202.5m (31 December 2016: €190.9m)

▪ Net Debt of €233.0m (31 December 2016: €152.5m)

1 The financial highlights should be read in conjunction with the 2017 Annual Report & Accounts.2Amounts for Revenue, EBITDA and EBIT for the year ended 31 December 2017 and prior years throughout this document exclude amounts related to

discontinued operations.3 Certain tables and numbers in this presentation may not add or compute precisely due to rounding.

6

2017 Operational Highlights

▪ The successful integration of Encore Industries into the IPL North America business since acquisition

in November 2016.

▪ The North America market has contributed significant organic growth driven by continued increased

demand in both the Consumer Packaging and Large Format Packaging and Environmental Solutions

divisions.

▪ Macro delivered results for 2017 which were ahead of expectations announced at the time of

acquisition. The integration of Macro has been completed successfully with growth anticipated for

2018 driven by a significant new contract with a global automotive customer.

▪ OPG’s Ireland and China business has been negatively impacted by reduced demand from its largest

customer following the merger of that customer with another industry participant.

▪ OPG’s financial performance in the UK in 2017 was significantly improved on 2016 with EBITDA

growth of 9% (prior to the allocation of OPG central overheads) even though turnover only increased

by 1%. Performance in 2017 was driven by growth in the packaging and industrial products business

and follows the successful reconfiguration of the operations at one of the UK sites.

7

2017 Operational Highlights (Continued)

▪ Significant development capital investment programmes continue in the Group’s North American

operations providing it with enhanced ability and capacity to serve an expanding business. A

number of these projects began to contribute to EBITDA in 2017.

▪ Renegotiated and extended the IPL Inc. Canadian syndicated loan facility to finance the

acquisition of Macro and to provide further bank facilities to the IPL Inc. Group with a revised

expiry date of July 2021.

▪ The hurricanes in the US in Quarter 3 2017 drove reduced capacity in both the resin and freight

markets resulting in significant cost increases in Quarter 4 2017, trends which have continued

into Quarter 1 2018.

8

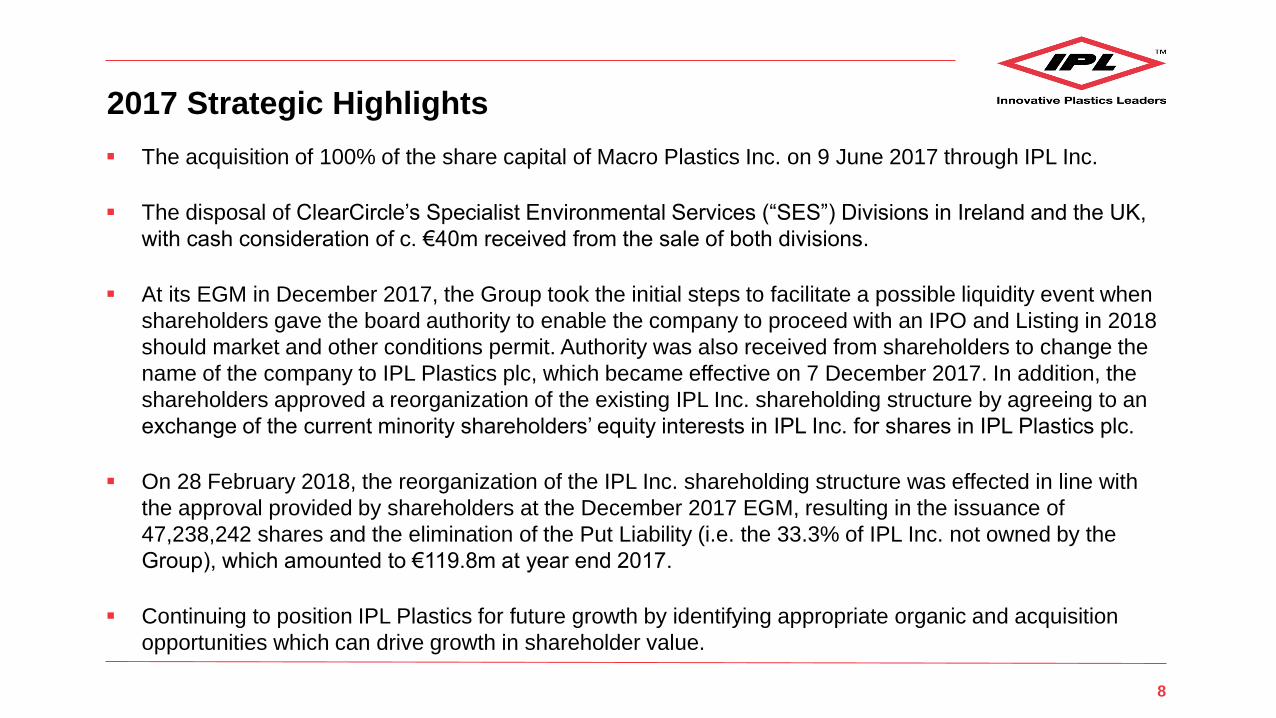

2017 Strategic Highlights

▪ The acquisition of 100% of the share capital of Macro Plastics Inc. on 9 June 2017 through IPL Inc.

▪ The disposal of ClearCircle’s Specialist Environmental Services (“SES”) Divisions in Ireland and the UK,

with cash consideration of c. €40m received from the sale of both divisions.

▪ At its EGM in December 2017, the Group took the initial steps to facilitate a possible liquidity event when

shareholders gave the board authority to enable the company to proceed with an IPO and Listing in 2018

should market and other conditions permit. Authority was also received from shareholders to change the

name of the company to IPL Plastics plc, which became effective on 7 December 2017. In addition, the

shareholders approved a reorganization of the existing IPL Inc. shareholding structure by agreeing to an

exchange of the current minority shareholders’ equity interests in IPL Inc. for shares in IPL Plastics plc.

▪ On 28 February 2018, the reorganization of the IPL Inc. shareholding structure was effected in line with

the approval provided by shareholders at the December 2017 EGM, resulting in the issuance of

47,238,242 shares and the elimination of the Put Liability (i.e. the 33.3% of IPL Inc. not owned by the

Group), which amounted to €119.8m at year end 2017.

▪ Continuing to position IPL Plastics for future growth by identifying appropriate organic and acquisition

opportunities which can drive growth in shareholder value.

9

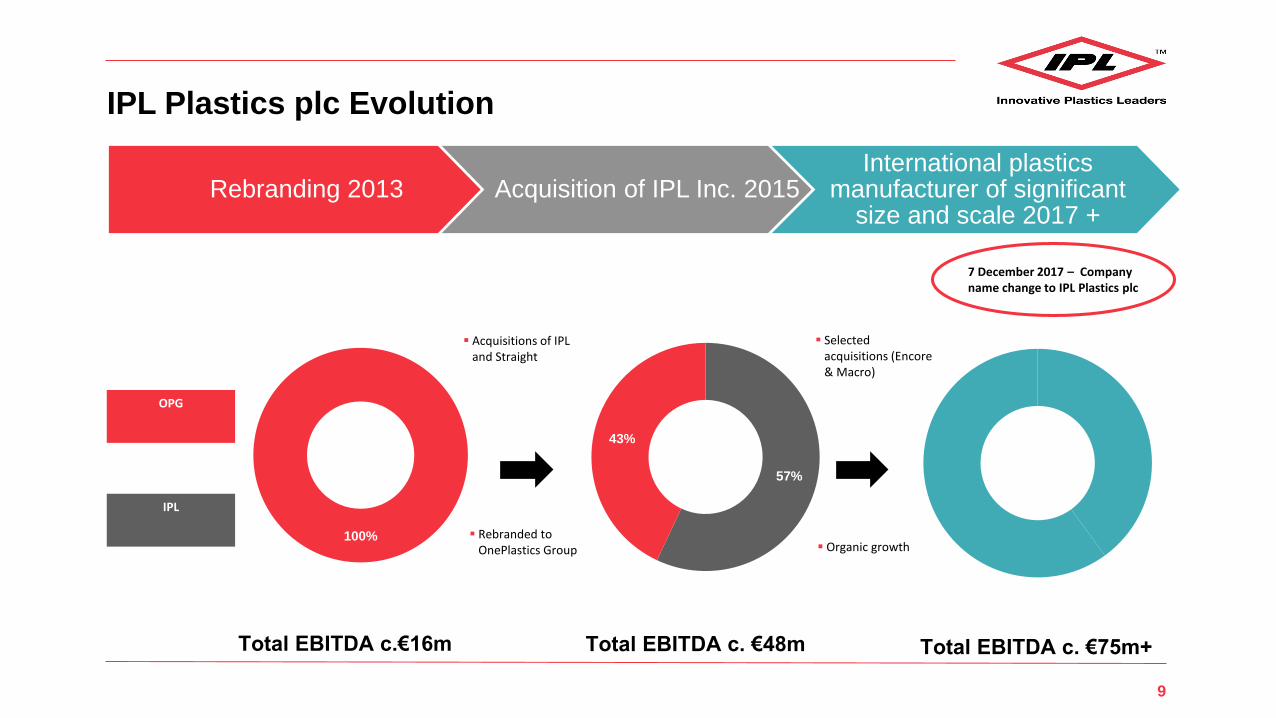

IPL Plastics plc Evolution

Rebranding 2013 Acquisition of IPL Inc. 2015International plastics

manufacturer of significant size and scale 2017 +

100%

Total EBITDA c.€16m

57%

43%

Total EBITDA c. €48m Total EBITDA c. €75m+

OPG

IPL

▪ Acquisitions of IPL and Straight

▪ Rebranded to OnePlastics Group

▪ Selected acquisitions (Encore & Macro)

▪ Organic growth

7 December 2017 – Company name change to IPL Plastics plc

10

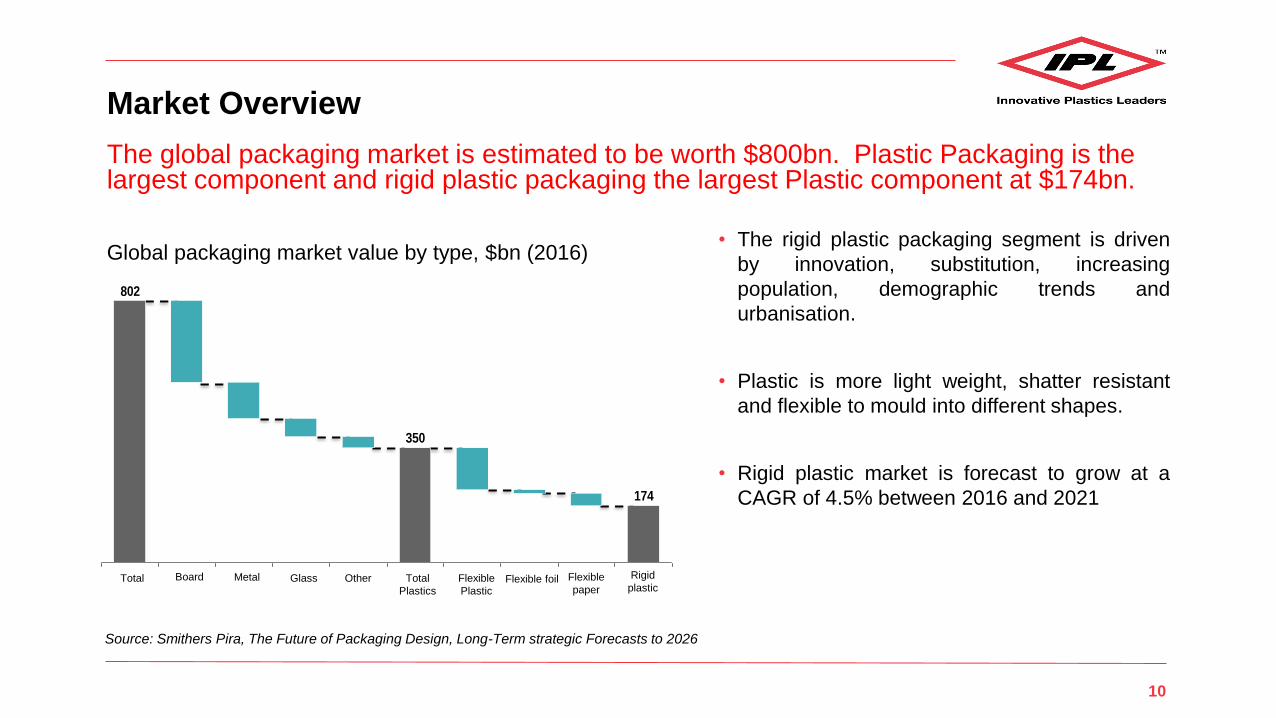

The global packaging market is estimated to be worth $800bn. Plastic Packaging is the largest component and rigid plastic packaging the largest Plastic component at $174bn.

Market Overview

Global packaging market value by type, $bn (2016)• The rigid plastic packaging segment is driven

by innovation, substitution, increasing

population, demographic trends and

urbanisation.

• Plastic is more light weight, shatter resistant

and flexible to mould into different shapes.

• Rigid plastic market is forecast to grow at a

CAGR of 4.5% between 2016 and 2021174

350

802

Source: Smithers Pira, The Future of Packaging Design, Long-Term strategic Forecasts to 2026

Rigid

plasticFlexible

paperFlexible foilFlexible

Plastic

Total

Plastics

OtherGlassMetalBoardTotal

11

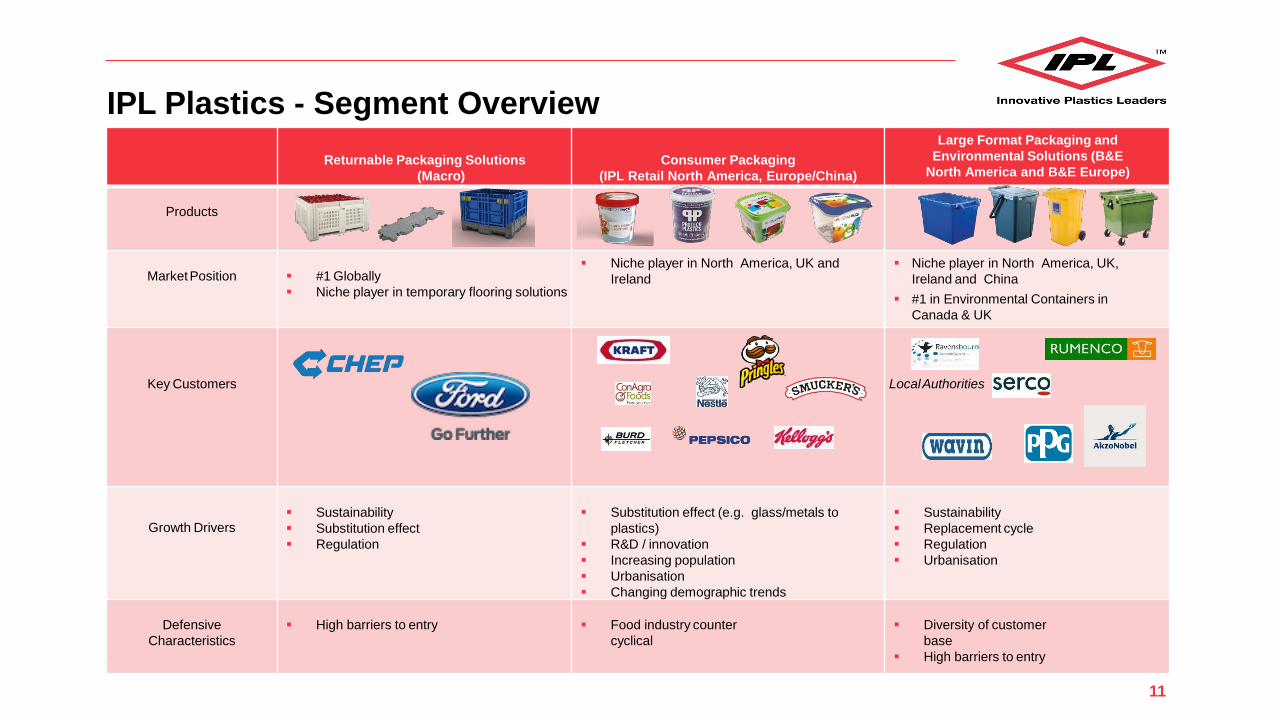

IPL Plastics - Segment Overview

Returnable Packaging Solutions

(Macro)

Consumer Packaging

(IPL Retail North America, Europe/China)

Large Format Packaging and

Environmental Solutions (B&E

North America and B&E Europe)

Products

MarketPosition ▪ #1 Globally

▪ Niche player in temporary flooring solutions

▪ Niche player in North America, UK and

Ireland

▪ Niche player in North America, UK,

Ireland and China

▪ #1 in Environmental Containers in

Canada & UK

Key Customers LocalAuthorities

Growth Drivers▪ Sustainability

▪ Substitution effect

▪ Regulation

▪ Substitution effect (e.g. glass/metals to

plastics)

▪ R&D / innovation

▪ Increasing population

▪ Urbanisation

▪ Changing demographic trends

▪ Sustainability

▪ Replacement cycle

▪ Regulation

▪ Urbanisation

Defensive

Characteristics

▪ High barriers to entry ▪ Food industry counter

cyclical

▪ Diversity of customer

base

▪ High barriers to entry

12

Clear growth strategy – organic growth and targeted M&AFavourable Market Backdrop

Fragmented

market place

Growing rigid

plastics demand

Substitution

effect

Increasing product

innovationRegulation

Clear Strategy

M&A

higher growth niche segments of the▪ Focus on

market

▪ European & North American geographic focus

▪ Synergy potential

▪ Target EBITDA > €10m and margin of 13% - 15%

▪ Target ROCE 10% - 15%

▪ Significant acquisition pipeline developed

Organic Growth

▪ Investment in manufacturing facilities

▪ Focused capital investment projects in USA & Canada

▪ Deliver manufacturing efficiencies

▪ Continued investment in R&D

▪ Leverage synergies & cross selling opportunities

Future MarketFocus

Continue to focus on

existing segments

which exhibit

significantgrowth

Leverage existing

capabilities forentry

into new segments

Expand product range

driven by customer/market

demand relying on

in-house R&D facilities

Continue to review market

opportunities to add new

plastics manufacturing

technologies and product

types

13

Summary Financial Information

14

Income Statement

• Revenue increased by 36.2% on the prior year to

€474.4m, driven principally by strong organic growth

in IPL Inc. and the impact of the Encore and Macro

acquisitions.

• EBITDA increased by 46.0% to €70.9m with IPL Inc’s

contribution being €45.9m and Macro’s €12.6m.

• Exceptional and non-recurring items, discontinued

operations and share of equity accounted investees

resulted in a charge of €11.2m in the year (2016:

credit of €0.3m). Included in this is €2.7m of costs

associated with the acquisition of Macro Plastics and

€3.2m of a loss on discontinued operations.

• Finance costs increased from the comparative period

by €4.9m to €13.8m, primarily as a result of the

drawdown of bank borrowings for the purposes of

acquiring Encore and Macro.

• There was a net income tax credit for the year of

€0.9m (2016: charge of €3.5m), which includes a

non-recurring income tax credit of €8.1m.

• Adjusted Diluted Earnings per share is 8.8% higher

than prior year, reflecting the improvement in

EBITDA.

€’m 2015 2016 2017

Revenue 251.4 348.2 474.4

Operating profit before exceptional items 17.9 30.4 38.4

Non-recurring items 1.7 (2.2) 3.3

Depreciation & Amortisation 11.7 20.3 29.2

EBITDA 31.3 48.5 70.9

EBITDA margin (%) 12.5% 13.9% 14.9%

EBIT 19.6 28.3 41.6

Exceptional/non-recurring items (4.4) 0.7 (9.8)

Share of profit of equity-accounted investee 24.3 3.9 1.8

Discontinued operations (12.8) (4.3) (3.2)

Finance costs (5.7) (8.9) (13.8)

Income tax expense (2.7) (3.5) (7.2)

Non-recurring income tax credit - - 8.1

Profit for year 18.4 16.1 17.6

Adjusted EPS (Diluted) 6.98c 11.04c 12.01c

15

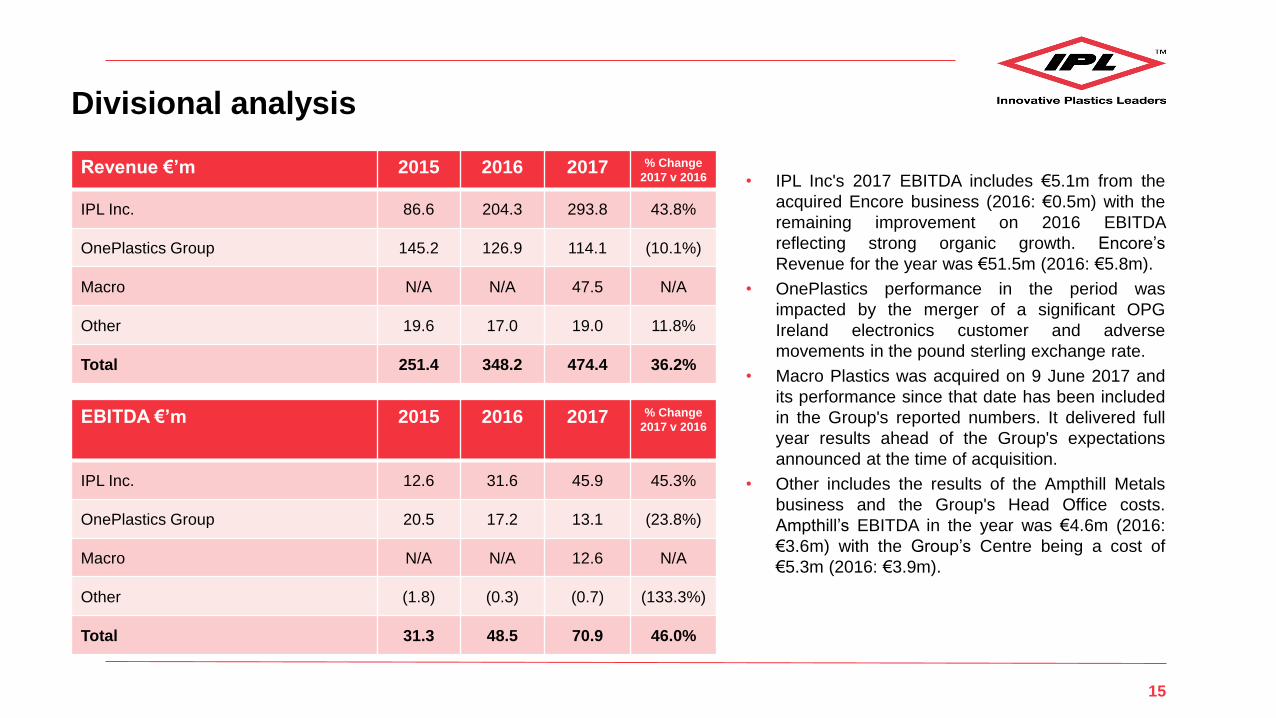

Divisional analysis

• IPL Inc's 2017 EBITDA includes €5.1m from the

acquired Encore business (2016: €0.5m) with the

remaining improvement on 2016 EBITDA

reflecting strong organic growth. Encore’s

Revenue for the year was €51.5m (2016: €5.8m).

• OnePlastics performance in the period was

impacted by the merger of a significant OPG

Ireland electronics customer and adverse

movements in the pound sterling exchange rate.

• Macro Plastics was acquired on 9 June 2017 and

its performance since that date has been included

in the Group's reported numbers. It delivered full

year results ahead of the Group's expectations

announced at the time of acquisition.

• Other includes the results of the Ampthill Metals

business and the Group's Head Office costs.

Ampthill’s EBITDA in the year was €4.6m (2016:

€3.6m) with the Group’s Centre being a cost of

€5.3m (2016: €3.9m).

Revenue €’m 2015 2016 2017 % Change

2017 v 2016

IPL Inc. 86.6 204.3 293.8 43.8%

OnePlastics Group 145.2 126.9 114.1 (10.1%)

Macro N/A N/A 47.5 N/A

Other 19.6 17.0 19.0 11.8%

Total 251.4 348.2 474.4 36.2%

EBITDA €’m 2015 2016 2017 % Change

2017 v 2016

IPL Inc. 12.6 31.6 45.9 45.3%

OnePlastics Group 20.5 17.2 13.1 (23.8%)

Macro N/A N/A 12.6 N/A

Other (1.8) (0.3) (0.7) (133.3%)

Total 31.3 48.5 70.9 46.0%

16

Balance Sheet

• The year-on-year movement in Goodwill and Intangible

assets arises principally as a result of the acquisition of

Macro Plastics, with €85.4m recognised on the date of

acquisition.

• The increase in Tangible assets from 31 December

2016 is due primarily to the acquisition of Macro

Plastics (€42.0m) and the Group's continued significant

expenditure as part of its capital investment

programme.

• Working capital balances at 31 December 2017 were

€49.9m (2016: €27.7m). The increase has arisen

primarily due to the acquisition of Macro Plastics

(€13.5m balance at year end) and an increase in IPL

Inc. as a result of its strong organic growth.

• Total Equity (after the Put Liability) has decreased by

30.3% at year end 2017 to €82.7m driven primarily by

the increase in the Put Liability of €47.6m and

unfavourable currency translation movements, partially

offset by the profit recorded for the year.

• Net Debt at 31 December 2017 was €233.0m (31

December 2016: €152.5m). The increase has been

caused primarily by the drawdown of borrowings to

fund the acquisition of Macro Plastics during the year.

€’m 20152016

(Restated)2017

Goodwill & Intangible Assets 140.7 140.1 206.9

Tangible Assets 161.9 160.8 214.6

Financial and Other Assets 14.3 22.2 24.6

Non-Current Assets 316.9 323.1 446.1

Current Assets 126.2 188.3 175.8

Total Assets 443.1 511.4 621.9

Creditors: within 1yr (92.9) (101.9) (130.4)

Creditors: more than 1yr (165.2) (218.6) (289.0)

Total Equity (Before Put Liability) 184.9 190.9 202.5

IPL Put Liability 32.4 72.2 119.8

Total Equity (After Put Liability) 152.6 118.6 82.7

Net Debt 120.3 152.5 233.0

Net Debt/EBITDA* 3.3x 2.5x 3.0x

*Calculated by reference to EBITDA as reported in each year, adjusted in 2016 and 2017 to reflect the pro forma EBITDA of acquisitions made in each respective year.

17

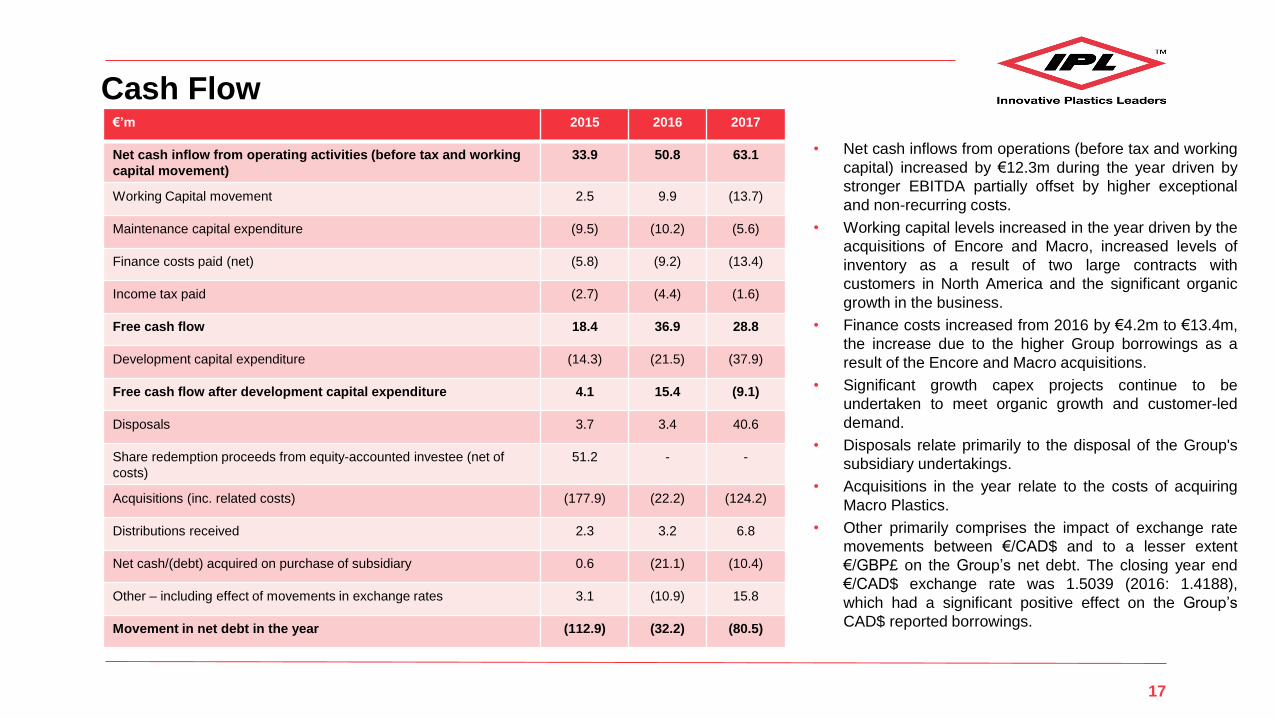

Cash Flow

• Net cash inflows from operations (before tax and working

capital) increased by €12.3m during the year driven by

stronger EBITDA partially offset by higher exceptional

and non-recurring costs.

• Working capital levels increased in the year driven by the

acquisitions of Encore and Macro, increased levels of

inventory as a result of two large contracts with

customers in North America and the significant organic

growth in the business.

• Finance costs increased from 2016 by €4.2m to €13.4m,

the increase due to the higher Group borrowings as a

result of the Encore and Macro acquisitions.

• Significant growth capex projects continue to be

undertaken to meet organic growth and customer-led

demand.

• Disposals relate primarily to the disposal of the Group's

subsidiary undertakings.

• Acquisitions in the year relate to the costs of acquiring

Macro Plastics.

• Other primarily comprises the impact of exchange rate

movements between €/CAD$ and to a lesser extent

€/GBP£ on the Group’s net debt. The closing year end

€/CAD$ exchange rate was 1.5039 (2016: 1.4188),

which had a significant positive effect on the Group’s

CAD$ reported borrowings.

€’m 2015 2016 2017

Net cash inflow from operating activities (before tax and working

capital movement)

33.9 50.8 63.1

Working Capital movement 2.5 9.9 (13.7)

Maintenance capital expenditure (9.5) (10.2) (5.6)

Finance costs paid (net) (5.8) (9.2) (13.4)

Income tax paid (2.7) (4.4) (1.6)

Free cash flow 18.4 36.9 28.8

Development capital expenditure (14.3) (21.5) (37.9)

Free cash flow after development capital expenditure 4.1 15.4 (9.1)

Disposals 3.7 3.4 40.6

Share redemption proceeds from equity-accounted investee (net of

costs)

51.2 - -

Acquisitions (inc. related costs) (177.9) (22.2) (124.2)

Distributions received 2.3 3.2 6.8

Net cash/(debt) acquired on purchase of subsidiary 0.6 (21.1) (10.4)

Other – including effect of movements in exchange rates 3.1 (10.9) 15.8

Movement in net debt in the year (112.9) (32.2) (80.5)

18

Strategy

19

• IPL Plastics’ strategy is focused on the development and growth of the Group’s core operations,

through both organic and acquisition led initiatives, to become a leading global player in the Rigid

Plastics market.

• The rigid plastic packaging market is the largest component of the plastics packaging market. It is

a segment driven by innovation, the substitution effect (from traditional forms of packaging),

increasing population growth and urbanisation.

• Rigid plastics’ growth has primarily come as a result of growing demand in emerging markets, but

also at the expense of traditional packaging types such as glass bottles and jars, liquid cartons

and metal cans.

• The operating model for the coming years is focused on:

– Fully realising the synergy potential across the business units, including sharing of technical

expertise, leveraging collective intellectual property and customer relationships, and

procurement efficiencies;

– The pursuit and realisation of higher margin sales opportunities, focusing on customers with

value-add requirement;

Group Strategy

20

– A more systematic targeting of US and European markets for retail packaging, waste carts

and bulk packaging through a stronger and more coordinated sales effort and through

acquisition; and

– The realisation of cost efficiencies in production including, but not limited to, a more stringent

commercial evaluation of capital investments and the increased automation of production.

• Given the strong organic growth experienced in North America, including the recent acquisitions,

the Group is investing heavily in development capital investment projects to facilitate an

expansion of the product range and to drive continued improvements in operating margins.

Group Strategy (Continued)

21

• The Group continues to experience strong demand for its products and its operations are underpinned by

favourable market dynamics, particularly in North America.

• Group results in the second half of 2017 were adversely impacted by increased resin and transport costs

following the impact of significant hurricanes recorded in the US. Results were also impacted by a decline

in the value of the US dollar and the Canadian dollar versus the Euro. The trading performance at the start

of 2018 continues to be impacted by these factors. The Group’s overall 2018 results, however, should start

to see the full year impact of some of the new capital expenditure programmes commissioned in the latter

half of 2017, together with a full year’s contribution from Macro.

• Given the many alternative options available to grow and develop the business, both organically and

through acquisition, the Group is confident in the ability of the business to continue to grow profitably into

the future and to create shareholder value.

• In line with the authority given by the Group’s shareholders at its EGM on 6 December 2017, and together

with the recent reorganisation of the IPL Inc. structure, progress has been made towards a possible IPO

and stock market listing on the Toronto TSX in 2018, subject to market conditions. This would allow the

Group to access further equity capital to finance growth opportunities and provide liquidity for the Group’s

shareholders. The Group will update shareholders further in relation to the possible IPO as the

arrangements progress.

Conclusion

Thank you