ireland and iceland. iceland and ireland: similarities and differences ireland starting points ...

TRANSCRIPT

Ireland and Iceland

Iceland and Ireland: similarities and differences

Ireland Starting points Putting the house in order: the 1980s Impact of “the death of distance” The boom and the bust Euro member

Iceland Basics The boom and bust No euro

Features of the two busts

Outline

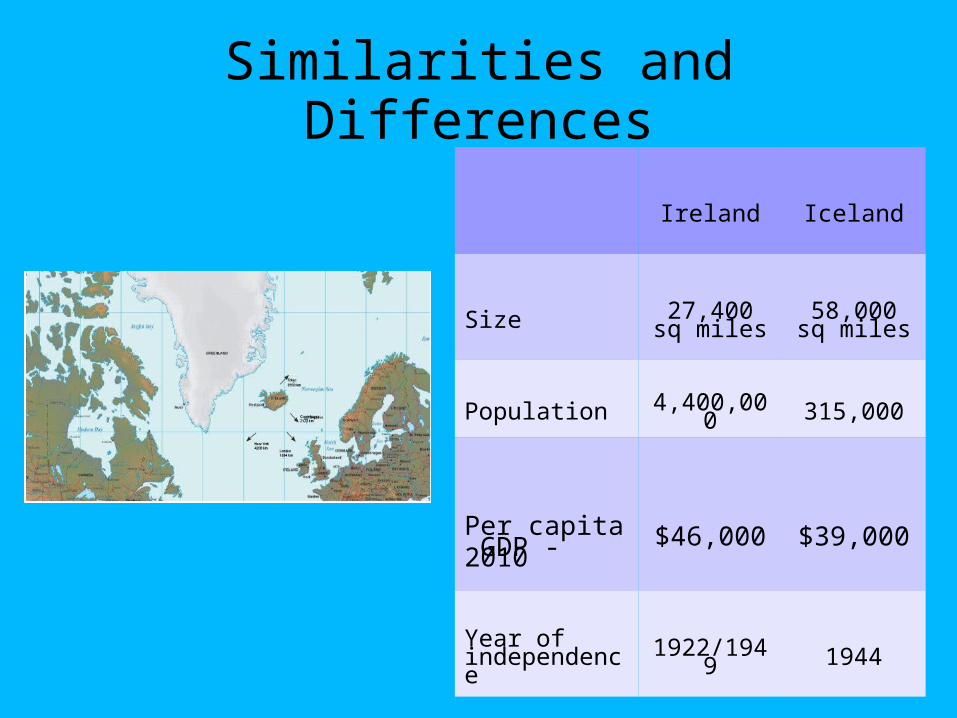

Similarities and Differences

Ireland Iceland

Size 27,400 sq miles

58,000 sq miles

Population 4,400,000 315,000

Per capita GDP - 2010

$46,000 $39,000

Year of independence

1922/1949 1944

Ireland

Ireland History in Brief

1846-50 Irish Famine (pop. peak :8 million) 1919-22 Partial independence for Ireland from

UK; Civil War 1930-1950s Industrial policy of “self sufficiency” Government: mildly “socialist” Favored small farmers and agricultural interests Promoted Irish language

1956

• Government seeks to attract foreign investment in export manufacturing industries: profits will be tax free for 15 years

1964

• Restrictions on foreign ownership of industry abolished

Industrial Development Authority

• Market Ireland to foreign direct investors

• Lobby government on behalf of investors (taxes, education, telecommunication, etc.)

Ireland – History continued

Ireland: Inherited Factors

Population (1985) 3.5 million; very young

Area 27,400 sq miles

Language English; some Irish

Legal system English common law

Government Parliamentary democracy

EARLY INVESTORS IN IRELAND

General Electric (1963) Digital (1971) Wang (1979) Mostek (1979) Apple Westinghouse (Thermo King, etc.)

External Economic/Trade Agreements

Not an original member of European Union Anglo-Irish Free Trade Agreement (1965) Entry into the European Union (1973) Joined Euro in 2002

Impact of 1973 EU Entry

Overall subsidy level roughly equal to Greece and Portugal

Substantial subsidies for Irish farmers Helped finance refocusing of higher

education Expanded Irish export markets, e.g.

beef Made Ireland even more attractive as a

“stepping stone” into Europe for foreign investors

Tax Policy Changes

1978: EU objects to “discriminatory” effect of low taxes just for export manufacturing

Irish solution: reduce corporate tax rate from 15% to 10% for all manufacturing

(Now around 12%)

Key Economic IndicatorsAnnual Averages 1961-1980

1961-1970 1971-1980

Real GDP % 4.2 4.8

Employment Growth 0.0 0.9

Unemployment % 4.8 6.8

Consumer Price Inflation 4.8 13.6

Net Migration -165,000 +96,000

PUTTING THE HOUSE IN ORDER - I

1980: An Bord Telecomm One of the worst European telephone

systems Largest employer in Ireland Both consumer and foreign investor

complaints Independence from Post Office, but still

state enterprise

PUTTING THE HOUSE IN ORDER – II

During 1980s: Major upgrading of technology at time of

fiscal restraint Focus: To become the lowest cost provider

of quality international telecommunications services in Europe

PUTTING THE HOUSE IN ORDER - III

1987: Focus on budget/debt control in Ireland New minority government Controlled deficit, e.g. postponed pay

raises for civil servants Forgiveness to taxpayers if they paid

overdue taxes (58% marginal rate) Agreement with unions on pay increases Then 10% corporate tax rate extended to

international financial services

PUTTING THE HOUSE IN ORDER - IV

Reform of education Reform of higher level education to stress

sciences, engineering Two new universities Technical college system emphasizing

electrical engineering and information technology

IRISH ECONOMIC POLICY, 1987 -

Not ideologically “free market,” e.g. like Margaret Thatcher in England

Very pragmatic Emphasis on agreement with unions:

Modest increases in nominal wage Real wages would not decline Reductions in personal tax rates to help

workers keep pace with inflation

Exchange Rate PolicyBefore and After the Euro

Small country dependency Irish currency historically tied to British pound

sterling Upon entry into EU, Irish “punt” created and

valued within EMS Enthusiastic member of Euro bloc Downside: no independent monetary policy

Key Economic IndicatorsAnnual Averages

1981-1986 1987-1993

Real GDP % 4.1 4.8

Employment Growth -1.3 1.1

Unemployment % 13.8 15.2

Consumer Price Inflation 10.8 2.9

Net Migration -70,000 -94,000

KEY EVENT: “THE DEATH OF DISTANCE” c. 1990

A chance event for Ireland - but “fortune favors the well prepared”

Technology events High capacity, low cost optical fiber High speed routers and switching networks. Internet/worldwide web

Competition among suppliers of international telecommunications services

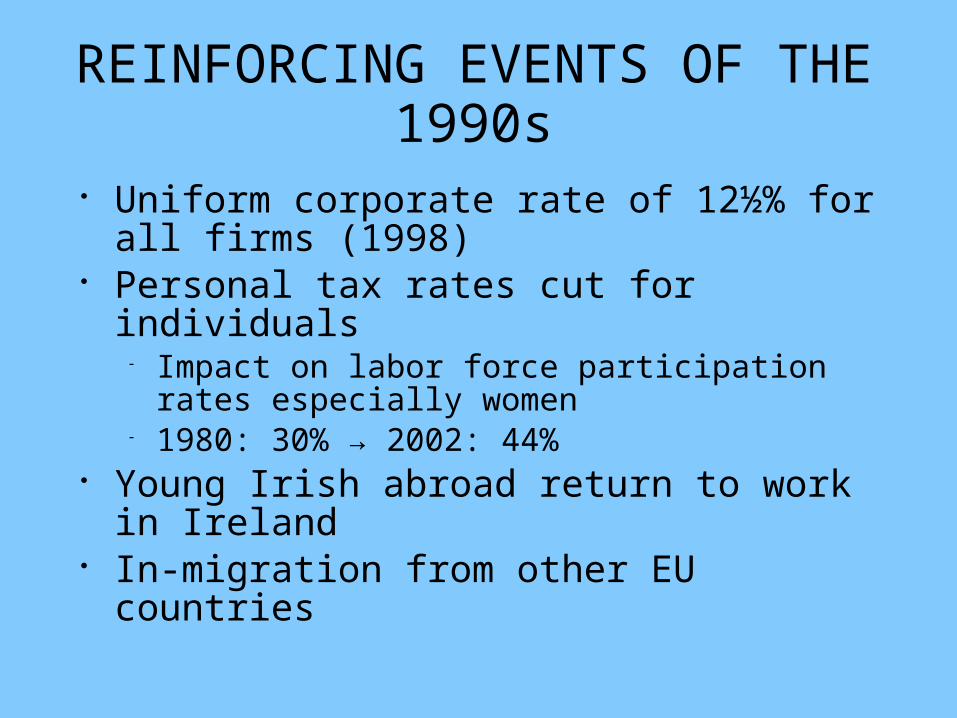

REINFORCING EVENTS OF THE 1990s

Uniform corporate rate of 12½% for all firms (1998)

Personal tax rates cut for individuals Impact on labor force participation rates especially

women 1980: 30% → 2002: 44%

Young Irish abroad return to work in Ireland In-migration from other EU countries

Ireland's BoomAnnual Averages

1994-2000 2005 2006 2007

Real GDP % 9.0 5.5 5.75 6.0

Employment Growth 5.1 4.7 4.5 3.6

Unemployment % 9.5 4.4 4.3 4.5

Consumer Price Inflation 2.5 2.5 3.9 4.9

Net Migration -72,400 55,100 71,800 67,300

Policy Implication of theIrish Boom

Get the fiscal policy fundamentals right Positive attitude towards investment, foreign

and domestic, with special attention to taxes and educational requirements of private sector employers

Create an environment for the rapid deployment of modern telecommunications technology, e.g. encourages investment and entrepreneurship

Policy Implication of theIrish Boom (continued)

Sometimes crises can be helpful (necessary?)

Get the fundamental fiscal policies right Reform/investment for telecommunications

infrastructure critical “Luck” plays a role … . . . but “fortune favors the well-prepared” Booms have a tendency to get out-of-hand

Boom to Bust:The Housing Bubble

1992-2006: Housing stock rises by 150% Demand factors:

Favorable demographics Rising real incomes No property taxes Mortgage interest deductibility Favorable capital gains on housing Low interest rates

Financial institutions aggressive in liberal lending terms (e.g. no money down) – but very little subprime lending

Boom to Bust (continued)

Property-related lending goes from 40% to 60% of banking system credits by 2007

Substantial speculative demand, e.g. “buy-to-let” mortgages were 26% of residential lending

Late 2007: home prices began to weaken October 2008: Lehman Bros. failure seizes up

interbank lending market; Irish banks lose deposits Irish government guarantees all deposits and debts in

Ireland of 6 largest banks

Housing prices soared relative to rents

(Bank of Ireland 2006)

Actual and Predicted Long-run Irish House prices

(Bank of Ireland 2006)

The Bubble Begins to Burst

IRELAND HOUSE PRICE Source: Central Bank of Ireland

Ireland's Housing Crash

Ireland TodayAnnual Averages

2007 2008 2009 2010

Real GDP % 6.0 -3.0 -7.5 -1.0

Employment Growth 3.6 -0.4 -4.6

Unemployment % 4.5 6.2 9.4 13.4

Consumer Price Inflation 4.9 4.1 -1.6 -1.5

Net Migration 67,300

Ireland Real GDP (YOY)

Ireland CPI

Ireland's Currency – the Euro

Ireland's Asset Bubble - Housing Boom to Bust

• Average national house price in Ireland fell 18.5% in 2009 vs a drop of 9.1 % in 2008

• A 48.2% drop since the peak in 3rd Q 2007 to January 2012

Ireland CDS

Source: http://www.spiegel.de/international/europe/0,1518,670294,00.html

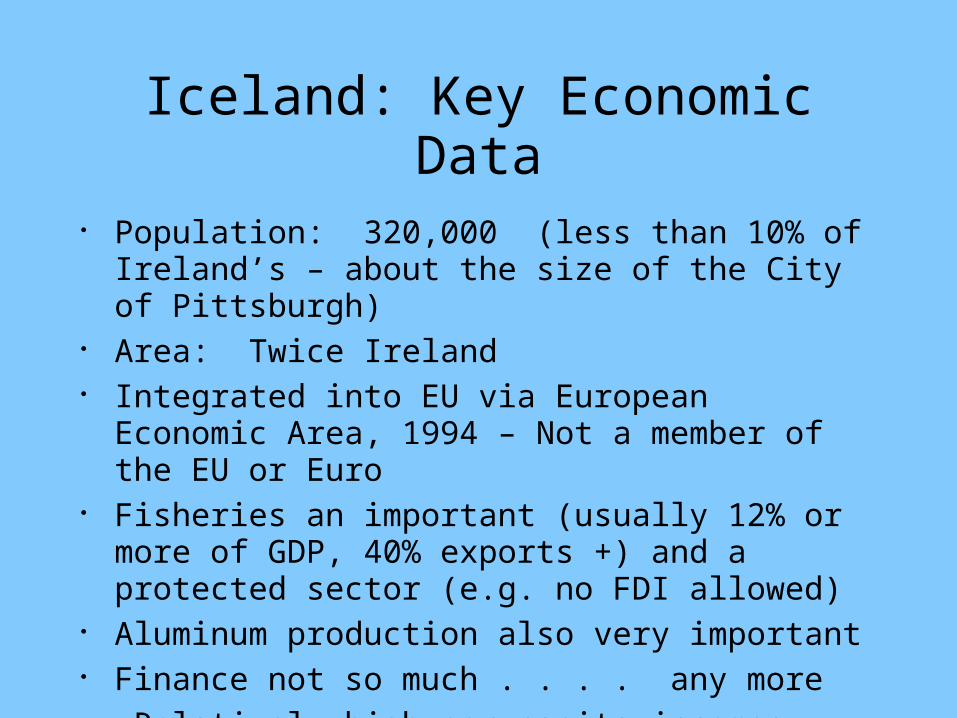

Iceland: Key Economic Data

Population: 320,000 (less than 10% of Ireland’s – about the size of the City of Pittsburgh)

Area: Twice Ireland Integrated into EU via European Economic Area,

1994 – Not a member of the EU or Euro Fisheries an important (usually 12% or more of GDP,

40% exports +) and a protected sector (e.g. no FDI allowed)

Aluminum production also very important Finance not so much . . . . any more Relatively high per capita incomes $40,000 vs

$65,000 at its peak in 2007-08.

Opening up the Economy Joined GATT in 1964 Privatization of key sectors starting in 1980s Trade and financial sectors liberalized in the

1990s Multinational aluminum company investment

in 1990s Krona floated in March 2001 Substantial investment and lending abroad by

Icelandic companies in 2000s

A Formerly “Fishy” Economy.... peaked in 2007

Iceland's Bubble

- 2003-2007: foreign funded boom lifted GDP 25%, strengthened krona

- Beginning in 2004: Rapid expansion of three major banks into overseas markets – borrowed ~$100 billion to buy foreign assets

- Further expansion funded with short-term deposits, e.g. from UK retail branches of Icelandic banks

- Other corporations and individuals became heavy borrowers in foreign currencies (lower interest rates than 16% charged on krona debt)

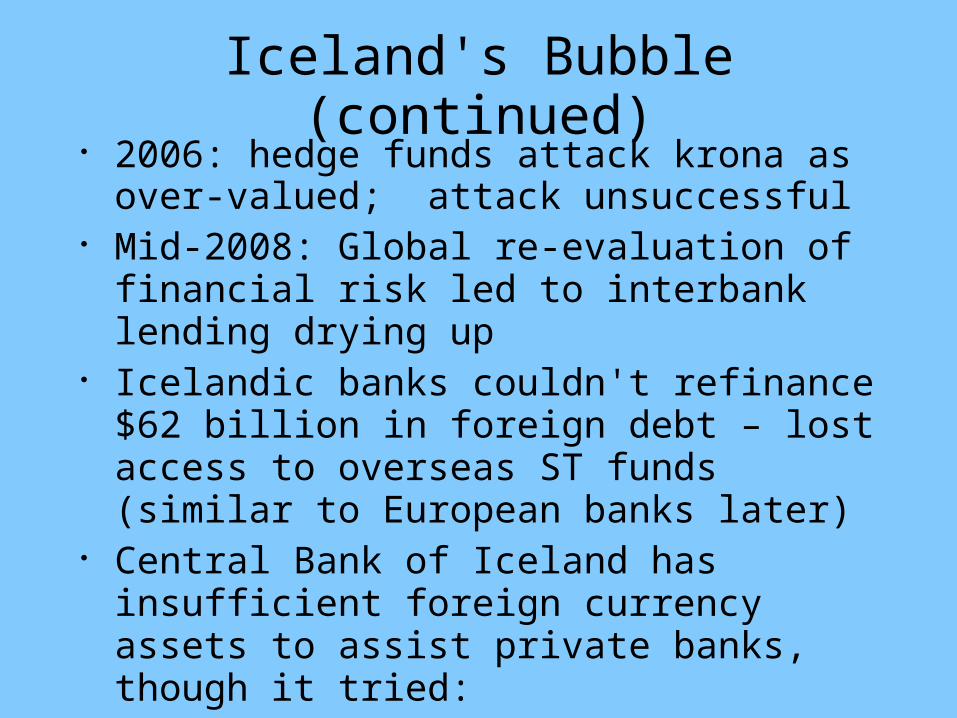

Iceland's Bubble (continued) 2006: hedge funds attack krona as over-

valued; attack unsuccessful Mid-2008: Global re-evaluation of financial

risk led to interbank lending drying up Icelandic banks couldn't refinance $62 billion

in foreign debt – lost access to overseas ST funds (similar to European banks later)

Central Bank of Iceland has insufficient foreign currency assets to assist private banks, though it tried:

One September 28 2008 government injected capital into Glitnir Bank (taking 75% stake)

Run on UK branches of other Icelandic banks

Iceland's Official Foreign Exchange Reserves

(About $7.2 billion)

ICELAND’S BUBBLE - cont.

Krona devalued (60 ISK → 125 ISK – now about 116.8 ISK/USD)

GDP growth 2009: - 6.5%, 2010: ~ -3.5% 2011: 2-3 % 2009 : Arranged a $2.1 billion IMF facility

ICELAND’S BUBBLE - cont

Government has not quite reached agreement with UK and Netherlands to repay over $5.3 billion in debts owed depositors of failed Iceland banks

Iceland President refused to sign agreement, forcing referendum on repayment

In March 2010 93% voted against repaying debts under existing terms. Voters continue to oppose repayment

Meanwhile, Parliament voted to pursue EU membership – no real movement

Iceland (Volatile) Real GDP

Iceland Real GDP Growth Rate

Iceland Krona

IcelandTotal Public Debt (% of GDP)

Iceland Unemployment Rate

Iceland CPI

Iceland CDS

FEATURES OF THE TWO BUSTS

Sustained booms; rapid bank expansion, e.g. increasing leverage

Bank reliance on foreign short-term deposits Liquidity crises for major banks Massive government intervention in the

banking sector

Common features

FEATURES OF THE TWO BUSTS

Irish banks’ over-expansion was in domestic real estate lending

Ireland government took over banks assets and liabilities

Icelandic banks over-expansion mainly in lending overseas, frequently to Icelandic companies

Iceland had major FX crisis (not a Euro member)

Large depositors in Icelandic banks in the UK lost substantial sums; Irish depositors still whole

Distinguishing features

Iceland in pictures . . . .

Why Iceland was Different .... via Bloomberg interview

Zim

bab

we

Jap

an

Sai

nt

Kit

ts a

nd

Nev

is

Gre

ece

Leb

ano

n

Jam

aica

Icel

and

Ital

y

Sin

gap

ore

Bar

bad

os

Bel

giu

m

Irel

and

Po

rtu

gal

Su

dan

Can

ada

Ger

man

y

Fra

nce

Sri

Lan

ka

Hu

ng

ary

Bel

ize

Eg

ypt

Do

min

ica

Nic

arag

ua

Un

ited

Kin

gd

om

Isra

el

Au

stri

a

Mal

ta

Bah

rain

Co

te d

'Ivo

ire

Jord

an

Net

her

lan

ds

Un

ited

Sta

tes

Mo

rocc

o

Cyp

rus

Sp

ain

Alb

ania

Bra

zil

Cro

atia

Bh

uta

n

Mau

riti

us

Vie

tnam

Gu

yan

a

Uru

gu

ay

Ph

ilip

pin

es

Sey

chel

les

Po

lan

d

El S

alva

do

r

Mal

aysi

a

Ind

ia

Un

ited

Ara

b E

mir

ates

0

50

100

150

200

250

Government Debt

(as percent of GDP: 2010)Source: CIA

US Government Budget Deficit as Percent of GDP

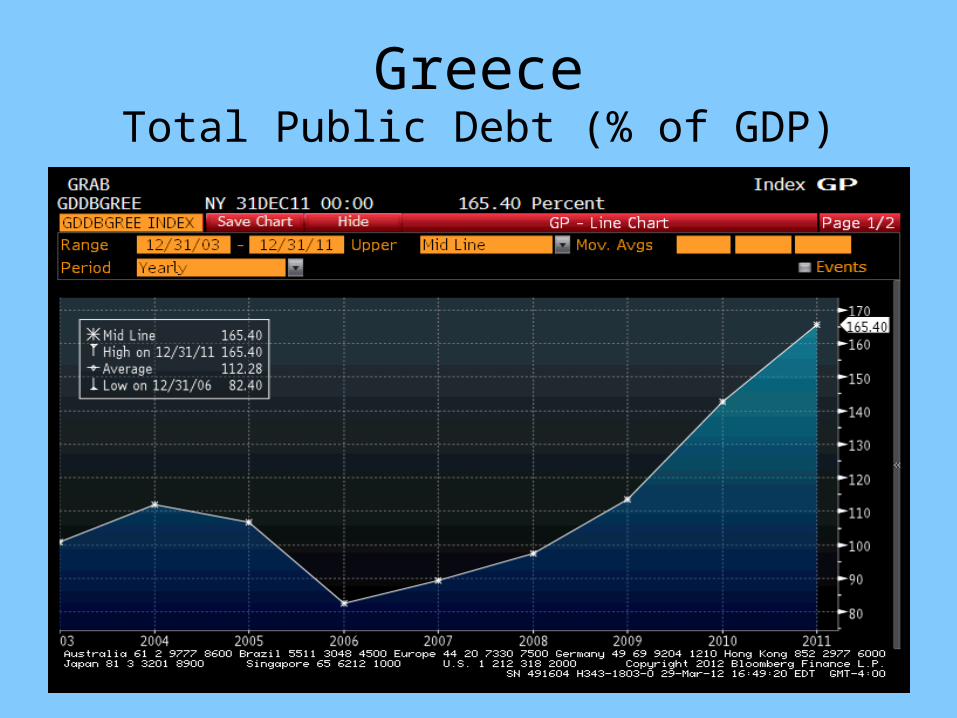

GreeceTotal Public Debt (% of GDP)

IrelandTotal Public Debt (% of GDP)

ItalyTotal Public Debt (% of GDP)

SpainTotal Public Debt (% of GDP)

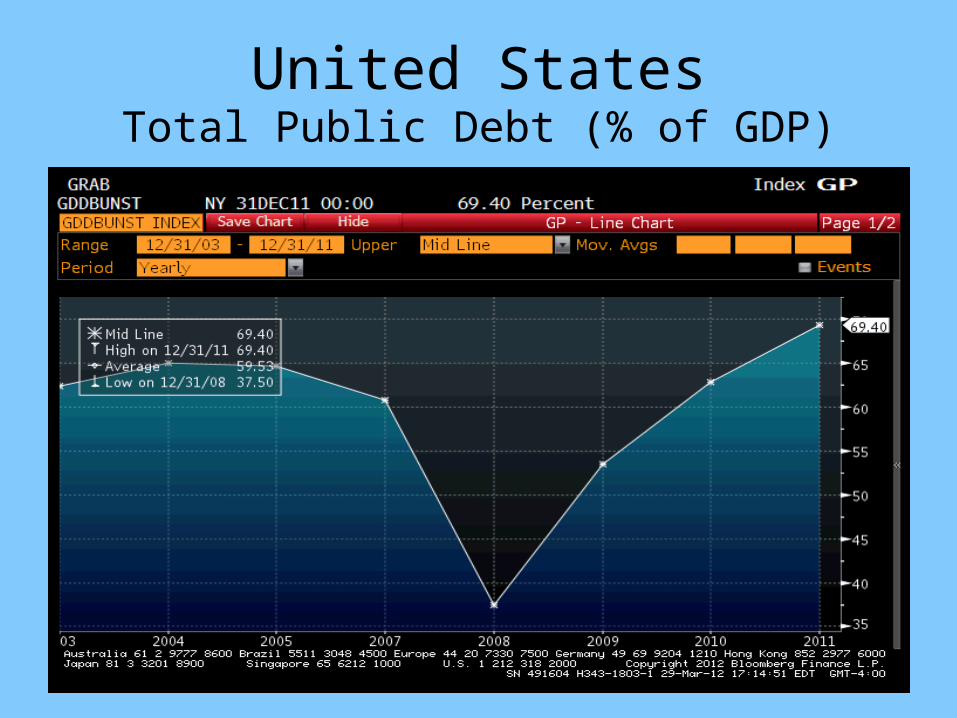

United StatesTotal Public Debt (% of GDP)

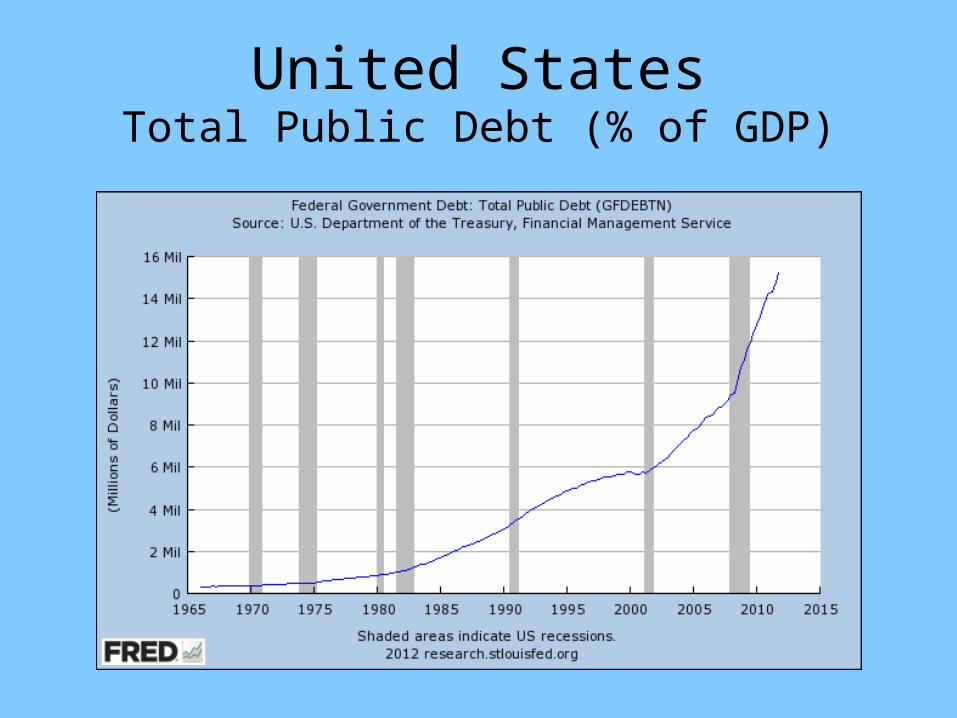

United StatesTotal Public Debt (% of GDP)

United StatesTotal Public Debt (% of GDP)

United StatesTotal Public Debt (% of GDP)