irwin/mcgraw-hill © the mcgraw-hill companies, inc., 1999 acquisitions and consolidated statements...

TRANSCRIPT

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Acquisitions and Consolidated Statements

© The McGraw-Hill Companies, Inc., 1999

12Part One: Financial Accounting

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Slide 12-1

If an investor company owns less than 20 percent of an investee company’s common stock, and the

stock’s fair value is readily determinable, the investment is reported using the fair value method.

If an investor company owns less than 20 percent of an investee company’s common stock, and the

stock’s fair value is readily determinable, the investment is reported using the fair value method.

Fair-Value Method

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Fair-Value Method Slide 12-2

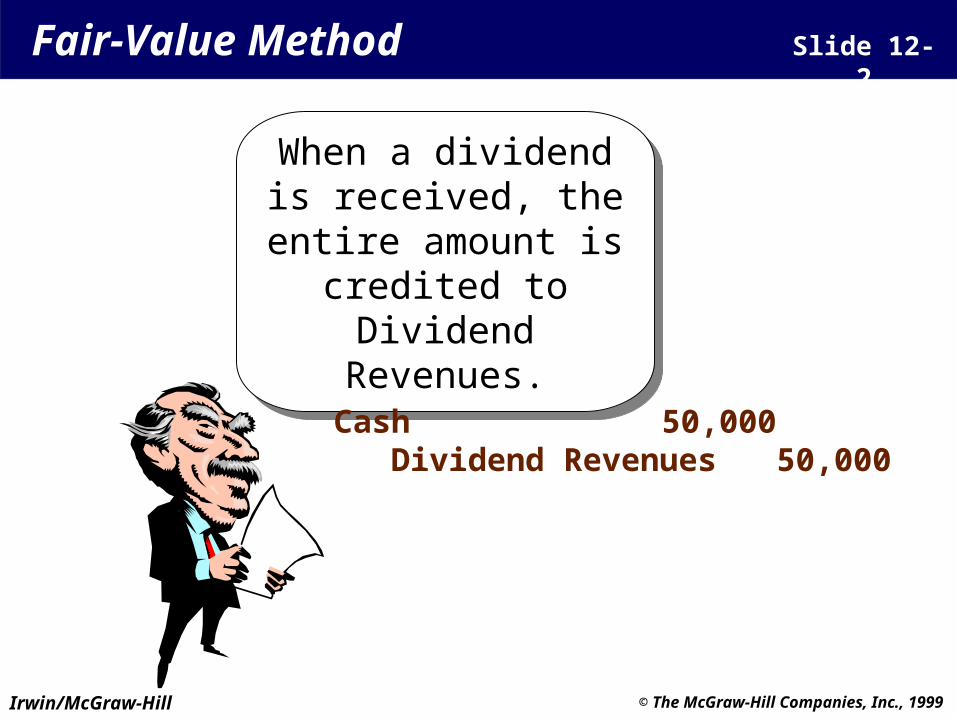

When a dividend is received, the entire

amount is credited to Dividend Revenues.

When a dividend is received, the entire

amount is credited to Dividend Revenues.

Cash 50,000 Dividend Revenues 50,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Cost Method Slide 12-3

If an investor company owns less than 20 percent of an investee company’s common stock, and the stock’s fair value is not readily determinable, the

investment is reported at its cost.

If an investor company owns less than 20 percent of an investee company’s common stock, and the stock’s fair value is not readily determinable, the

investment is reported at its cost.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Equity Method Slide 12-4

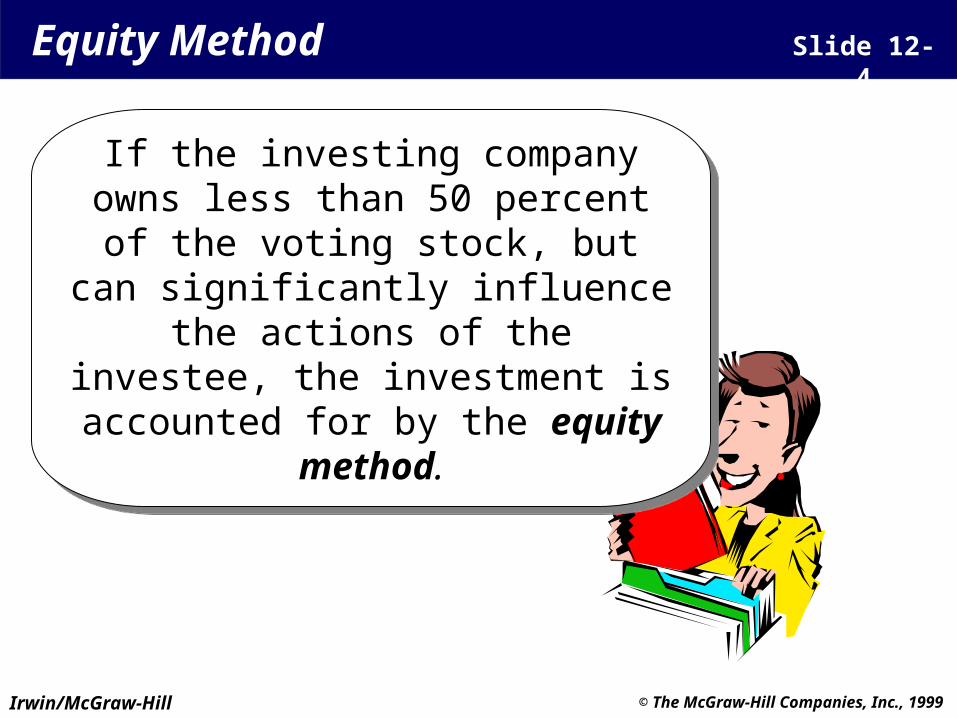

If the investing company owns less than 50 percent of the voting stock, but can

significantly influence the actions of the investee, the investment is accounted for

by the equity method.

If the investing company owns less than 50 percent of the voting stock, but can

significantly influence the actions of the investee, the investment is accounted for

by the equity method.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Equity Method Slide 12-5

Merkle Company acquired 25 percent of the common stock of Pentel Company on January 2, 1998, for $250,000.

Merkle Company acquired 25 percent of the common stock of Pentel Company on January 2, 1998, for $250,000.

Investments 250,000Cash 250,000

Pentel’s net income for 1998 was $100,000.Pentel’s net income for 1998 was $100,000.

Investments 25,000Investment Revenue 25,000

25% of $100,00025% of $100,00025% of $100,00025% of $100,000

Assume thatAssume thatMerkle Company hasMerkle Company has significant influencesignificant influence

Assume thatAssume thatMerkle Company hasMerkle Company has significant influencesignificant influence

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Equity Method Slide 12-6

During 1998, Merkle Company received $10,000 in dividends from Pentel Company.

During 1998, Merkle Company received $10,000 in dividends from Pentel Company.

Cash 10,000Investments 10,000

Note that the dividend

reduces the Investments

account.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

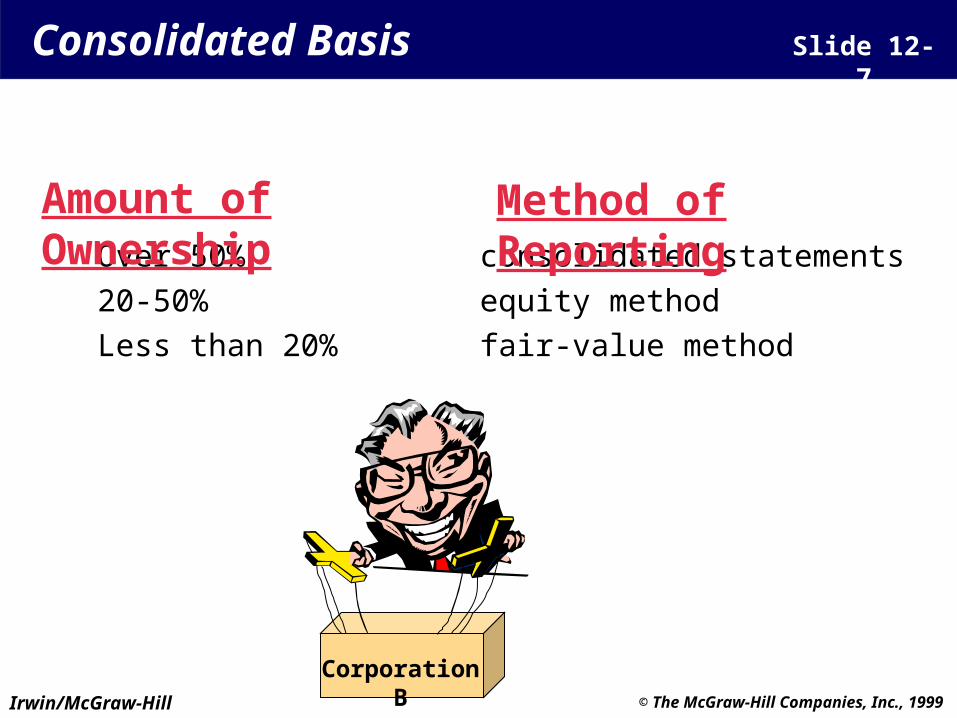

Over 50% consolidated statements

20-50% equity method

Less than 20% fair-value method

Consolidated Basis Slide 12-7

Amount of Ownership Method of Reporting

Corporation B

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

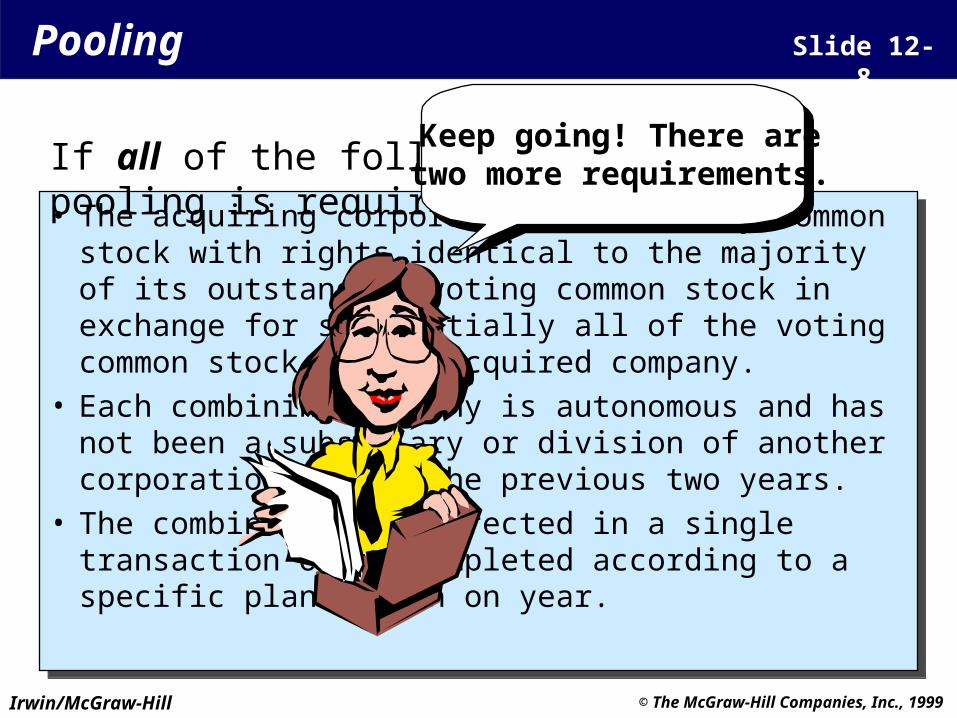

• The acquiring corporation issues only common stock with rights identical to the majority of its outstanding voting common stock in exchange for substantially all of the voting common stock of the acquired company.

• Each combining company is autonomous and has not been a subsidiary or division of another corporation within the previous two years.

• The combination is effected in a single transaction or is completed according to a specific plan within on year.

• The acquiring corporation issues only common stock with rights identical to the majority of its outstanding voting common stock in exchange for substantially all of the voting common stock of the acquired company.

• Each combining company is autonomous and has not been a subsidiary or division of another corporation within the previous two years.

• The combination is effected in a single transaction or is completed according to a specific plan within on year.

Pooling Slide 12-8

If all of the following are met, pooling is required:Keep going! There are

two more requirements.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

• Following the combination the acquiring corporation does not reacquire its voting common stock for a six-month period other than for normal business purposes, such as the issuance of shares under stock option programs.

• The combined corporation does not intend to dispose of a significant part of the assets of the combining companies within two years after the combination.

• Following the combination the acquiring corporation does not reacquire its voting common stock for a six-month period other than for normal business purposes, such as the issuance of shares under stock option programs.

• The combined corporation does not intend to dispose of a significant part of the assets of the combining companies within two years after the combination.

Pooling Slide 12-9

If all of the following are met, pooling is required:

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

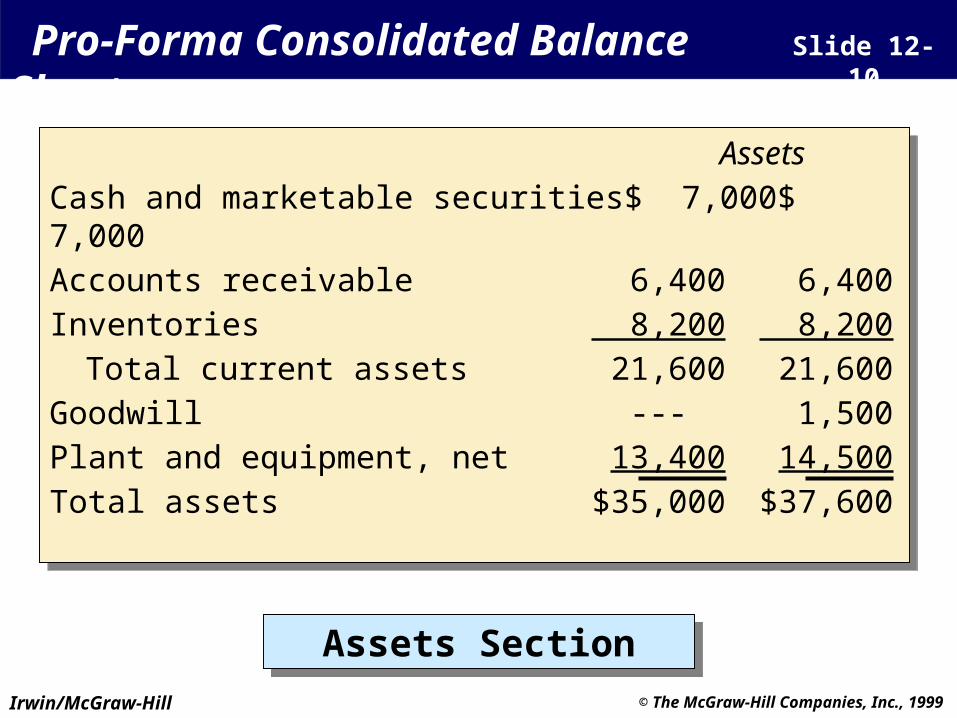

Pro-Forma Consolidated Balance Sheet Slide 12-10

Pooling Purchase

Assets

Cash and marketable securities $ 7,000 $ 7,000

Accounts receivable 6,400 6,400

Inventories 8,200 8,200

Total current assets 21,600 21,600

Goodwill --- 1,500

Plant and equipment, net 13,400 14,500

Total assets $35,000 $37,600

Assets

Cash and marketable securities $ 7,000 $ 7,000

Accounts receivable 6,400 6,400

Inventories 8,200 8,200

Total current assets 21,600 21,600

Goodwill --- 1,500

Plant and equipment, net 13,400 14,500

Total assets $35,000 $37,600

Assets SectionAssets Section

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Pro-Forma Consolidated Balance Sheet Slide 12-11

Pooling Purchase

Liabilities and Shareholders’ Equity

Accounts payable $ 7,700 $ 7,700

Other current liabilities 1,800 1,800

Total current liabilities 9,500 9,500

Long-term debt 9,800 9,800

Total liabilities 19,300 19,300

Common stock (par plus paid-in capital) 3,200 8,500

Retained earnings 12,500 9,800

Total shareholders’ equity 15,700 18,300

Total liabilities and shareholders’ equity $35,000 $37,600

Liabilities and Shareholders’ Equity SectionLiabilities and Shareholders’ Equity Section

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Accounting as a Pooling Slide 12-12

There is a “marriage” of the two entities. The

two balance sheets simply are added together at book

value to arrive at a consolidated

balance sheet for the surviving entity.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Accounting as a Purchase Slide 12-13

First, B’s identifiable net assets are revalued to their fair value.

First, B’s identifiable net assets are revalued to their fair value.

Plant and equipment had a book value of $2.8 million, but a fair value of $3.9 million.

Plant and equipment had a book value of $2.8 million, but a fair value of $3.9 million.

The consolidated plant and equipment account shows

$14.5 million.

The consolidated plant and equipment account shows

$14.5 million.

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Accounting as a Purchase Slide 12-14

Second, any excess of the purchase price over the total amount of the revalued identifiable net assets is

shown on the consolidated balance sheet as an asset called goodwill.

Second, any excess of the purchase price over the total amount of the revalued identifiable net assets is

shown on the consolidated balance sheet as an asset called goodwill.

Purchase price $6,000,000Less: Book value of net assets acquired 3,400,000

2,600,000Less: Write-up of identifiable assets to fair value 1,100,000Goodwill $1,500,000

Purchase price $6,000,000Less: Book value of net assets acquired 3,400,000

2,600,000Less: Write-up of identifiable assets to fair value 1,100,000Goodwill $1,500,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Pro Forma Consolidated Income Statement Slide 12-15

Corporation A Corporation B

If independent corporation:Income before taxes $3,780 $945Income tax expense (40%) 1,512 378Net income $2,268 $567Number of outstanding shares 1,000,000 100,000Earnings per share $2.27 $5.67

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Pro Forma Consolidated Income Statement Slide 12-16

Combined A-B, pooling treatment:Income before taxes $4,725Income tax expense (40%) 1,890Net income $2,835Number of outstanding shares 1,200,000Earnings per share $2.36

Combined Corporations A-B

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Pro Forma Consolidated Income Statement Slide 12-17

Combined A-B, purchase treatment:Income before taxes $4,725Less: Additional depreciation expense 110Less: Amortization of goodwill 100 Income before taxes 4,515Income tax expense (40%) 1,806Net income $2,709Number of outstanding shares 1,200,000Earnings per share $2.26

Combined Corporations A-B

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

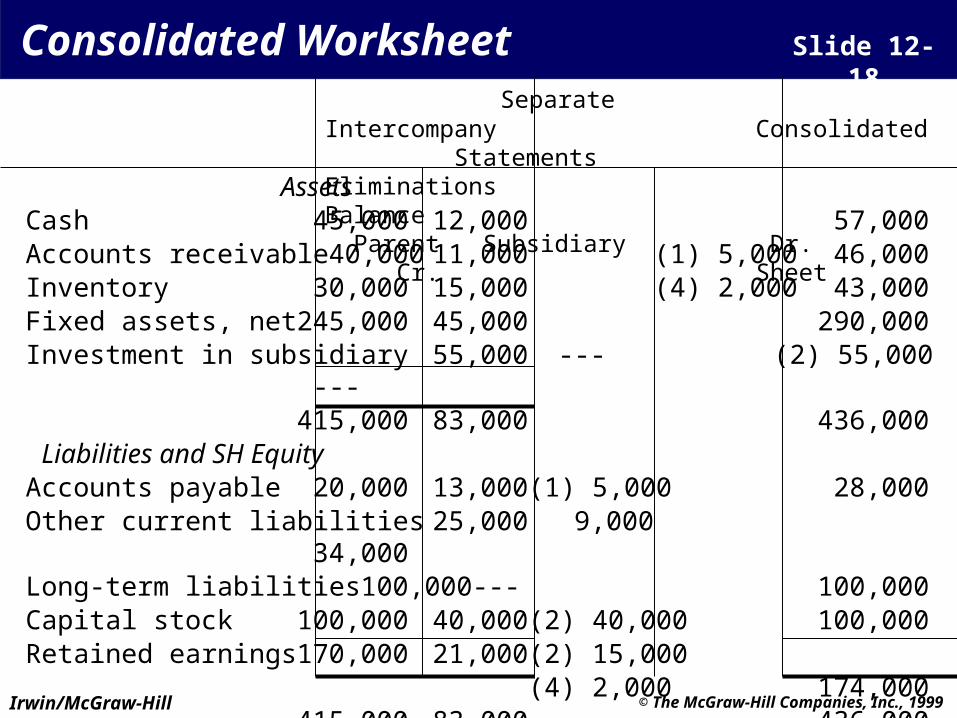

AssetsCash 45,000 12,000 57,000Accounts receivable 40,000 11,000 (1) 5,000 46,000Inventory 30,000 15,000 (4) 2,000 43,000Fixed assets, net 245,000 45,000 290,000Investment in subsidiary 55,000 --- (2) 55,000 ---

415,000 83,000 436,000 Liabilities and SH EquityAccounts payable 20,000 13,000 (1) 5,000 28,000Other current liabilities 25,000 9,000 34,000Long-term liabilities 100,000 --- 100,000Capital stock 100,000 40,000 (2) 40,000 100,000Retained earnings 170,000 21,000 (2) 15,000

(4) 2,000 174,000415,000 83,000 436,000

Consolidated Worksheet Slide 12-18

Separate Intercompany Consolidated Statements Eliminations Balance Parent Subsidiary Dr. Cr. Sheet

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Asset Valuation Slide 12-19

Assume that the Parent purchased Subsidiary stock for $70,000 rather than $55,000. If

Subsidiary’s assets were found to be recorded at their fair value, there would be goodwill of

$15,000. The elimination entry would have been:

Assume that the Parent purchased Subsidiary stock for $70,000 rather than $55,000. If

Subsidiary’s assets were found to be recorded at their fair value, there would be goodwill of

$15,000. The elimination entry would have been:

Goodwill 15,000Capital Stock (Subsidiary) 40,000Retained Earnings (Subsidiary) 15,000

Investment in Subsidiary (Parent) 70,000

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

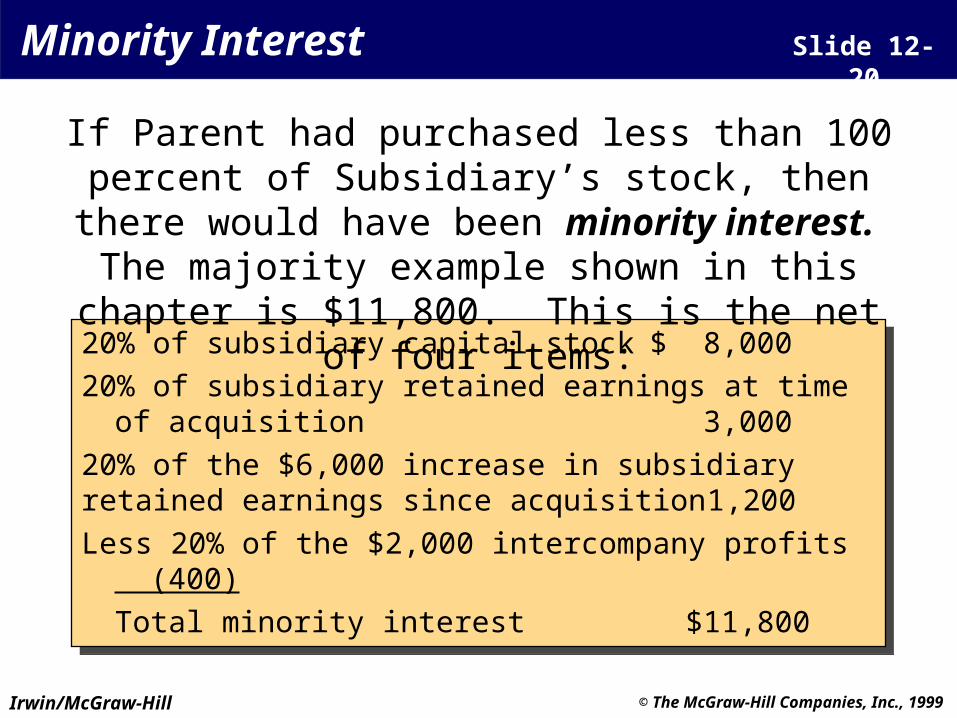

20% of subsidiary capital stock $ 8,000

20% of subsidiary retained earnings at timeof acquisition 3,000

20% of the $6,000 increase in subsidiaryretained earnings since acquisition 1,200

Less 20% of the $2,000 intercompany profits (400)

Total minority interest $11,800

20% of subsidiary capital stock $ 8,000

20% of subsidiary retained earnings at timeof acquisition 3,000

20% of the $6,000 increase in subsidiaryretained earnings since acquisition 1,200

Less 20% of the $2,000 intercompany profits (400)

Total minority interest $11,800

Minority Interest Slide 12-20

If Parent had purchased less than 100 percent of Subsidiary’s stock, then there would have been

minority interest. The majority example shown in this chapter is $11,800. This is the net of four items:

Irwin/McGraw-Hill

© The McGraw-Hill Companies, Inc., 1999

Chapter 12

The End