issues in business income - wirc wirc...issues in business income monday , 26 th december , 2011...

TRANSCRIPT

ISSUES IN

BUSINESS INCOME

Monday , 26th December , 2011

K.C. College Auditorium

WIRC of ICAI

Pradip N. Kapasi

Chartered Accountant 1

Shares & Securities

Business or Investment

Arbitrage

Day Trading

Portfolio Management

Derivatives

Conversion form stock

Stock Lending programme

Explanation to s. 73

Pradip N. Kapasi

Chartered Accountant 2

Business or Capital Gains

• A billion $ question

• Guidelines – Instruction 1827 dt. 31.08.1989

– Cir. No. 4/2007 dt.15.06.2007

Pradip N. Kapasi

Chartered Accountant 3

Desired Parameters

• Intention • Period of holding

• Frequency • Fund utilised

• Time devoted • Set-up

• Listing • PMS

• Volume • Scale

• Alt. occupation • Bank account

• Sales/ Purchase • Post Utilisation

• Treatment in books • Statutory requirements

• MOA/AOA • Avg. holding period

• Group companies • Promoters

• No. of script • Genuineness

Pradip N. Kapasi

Chartered Accountant 4

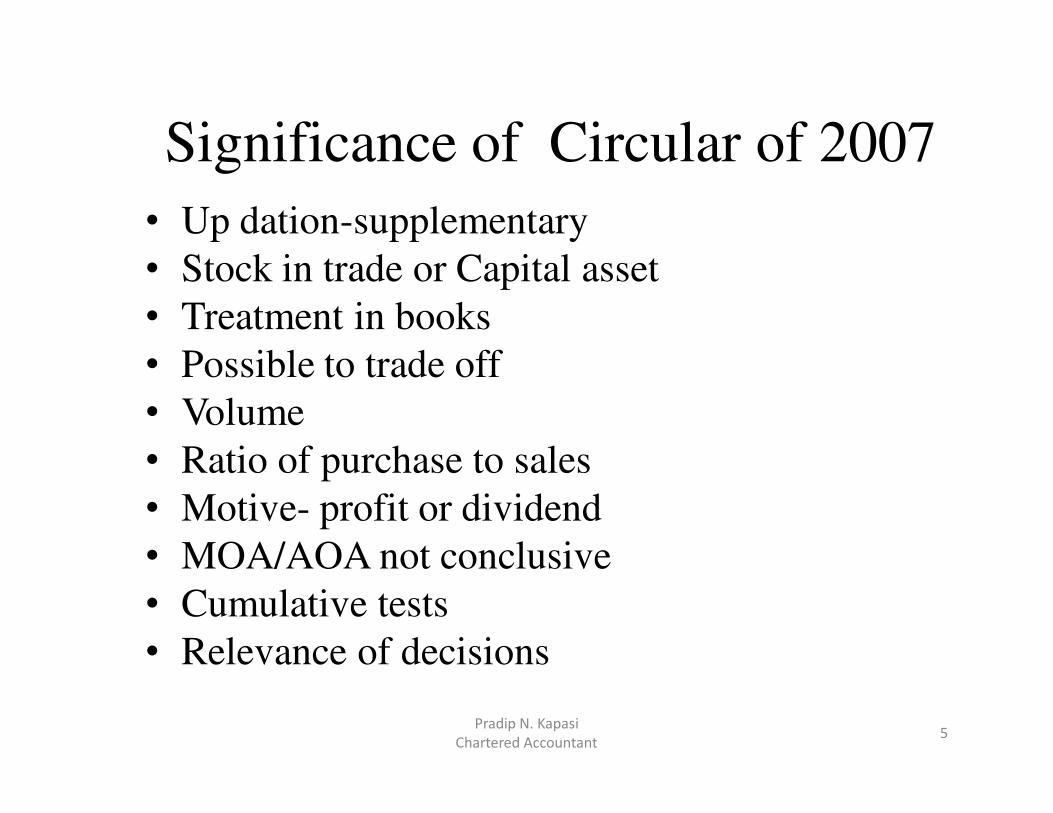

Significance of Circular of 2007

• Up dation-supplementary

• Stock in trade or Capital asset

• Treatment in books

• Possible to trade off

• Volume

• Ratio of purchase to sales

• Motive- profit or dividend

• MOA/AOA not conclusive

• Cumulative tests

• Relevance of decisions

Pradip N. Kapasi

Chartered Accountant 5

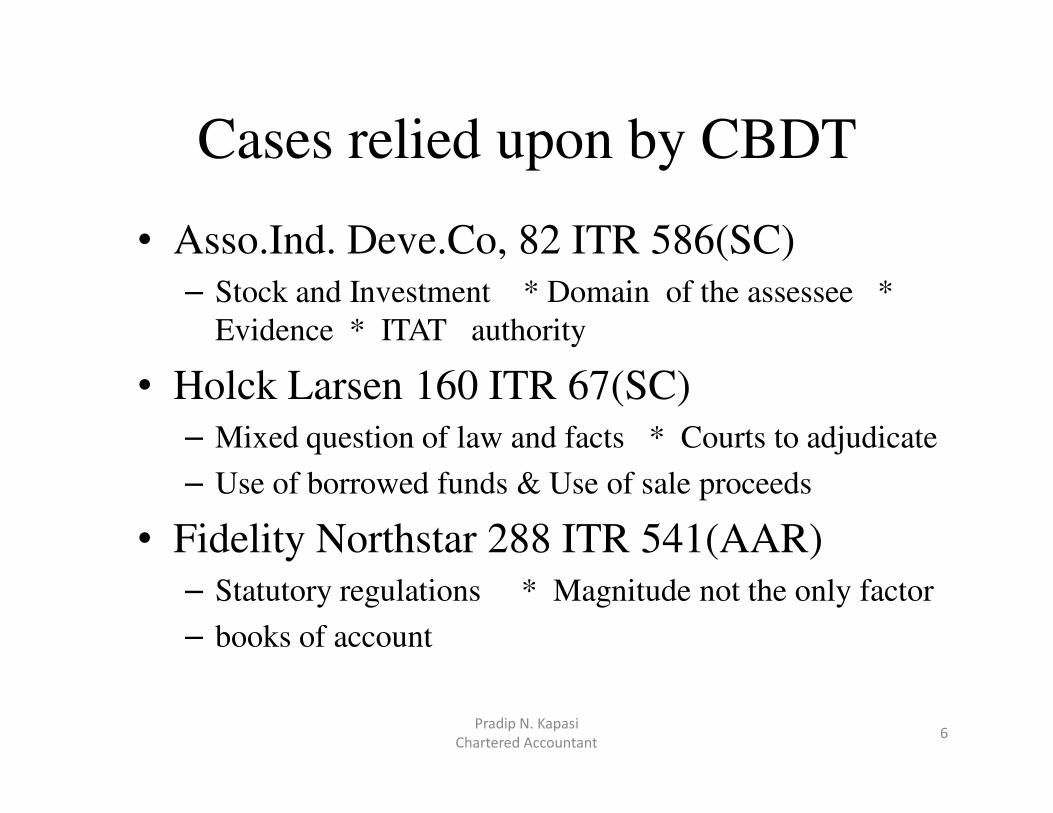

Cases relied upon by CBDT

• Asso.Ind. Deve.Co, 82 ITR 586(SC)– Stock and Investment * Domain of the assessee *

Evidence * ITAT authority

• Holck Larsen 160 ITR 67(SC)– Mixed question of law and facts * Courts to adjudicate

– Use of borrowed funds & Use of sale proceeds

• Fidelity Northstar 288 ITR 541(AAR)– Statutory regulations * Magnitude not the only factor

– books of account

Pradip N. Kapasi

Chartered Accountant 6

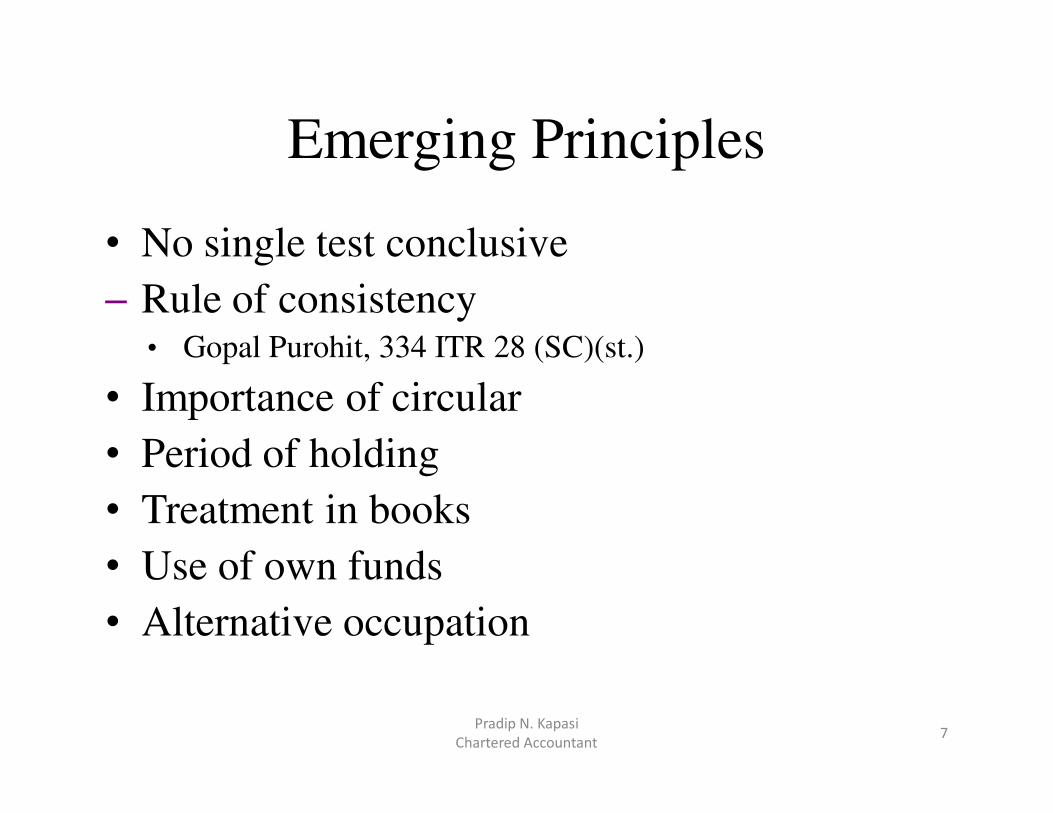

Emerging Principles

• No single test conclusive

– Rule of consistency• Gopal Purohit, 334 ITR 28 (SC)(st.)

• Importance of circular

• Period of holding

• Treatment in books

• Use of own funds

• Alternative occupation

Pradip N. Kapasi

Chartered Accountant 7

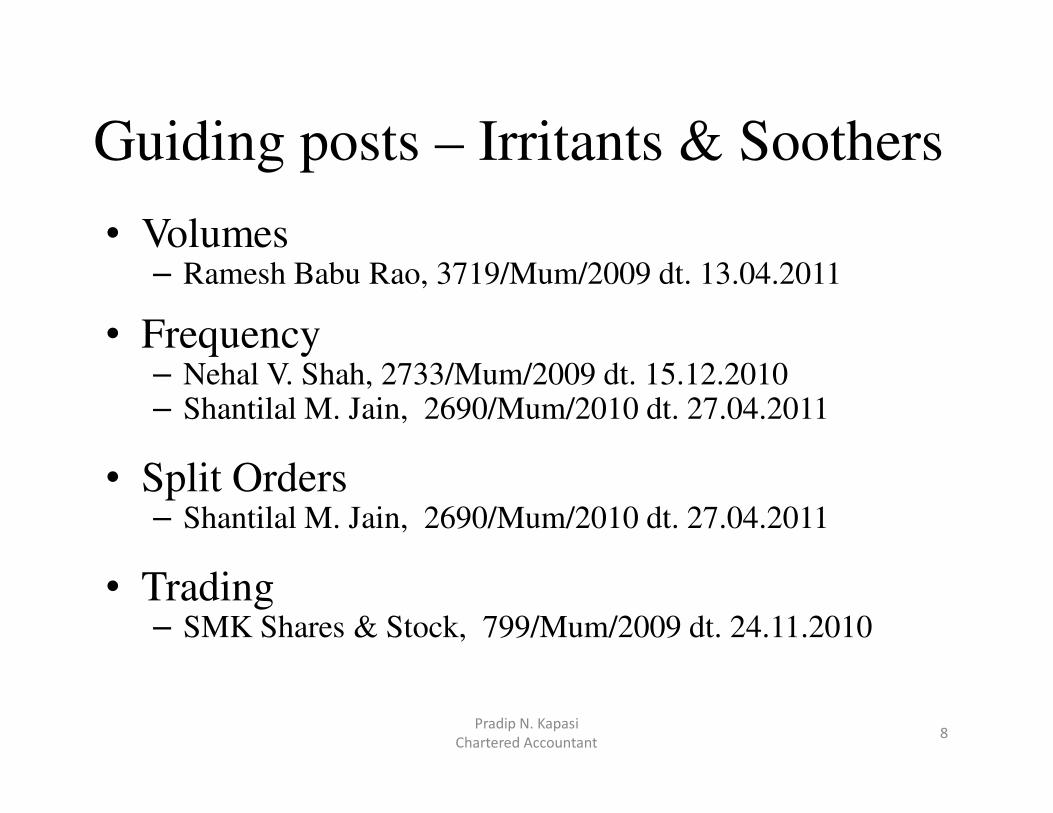

Guiding posts – Irritants & Soothers

• Volumes– Ramesh Babu Rao, 3719/Mum/2009 dt. 13.04.2011

• Frequency– Nehal V. Shah, 2733/Mum/2009 dt. 15.12.2010 – Shantilal M. Jain, 2690/Mum/2010 dt. 27.04.2011

• Split Orders– Shantilal M. Jain, 2690/Mum/2010 dt. 27.04.2011

• Trading – SMK Shares & Stock, 799/Mum/2009 dt. 24.11.2010

Pradip N. Kapasi

Chartered Accountant 8

Guiding posts – Irritants & Soothers• Speculation & Day Trading

– Gopal Purohit, 122 TTJ 87 (Mum.)

– Naishadh V. Vachharajani, 6429/Mum/2009

– Shantilal M. Jain, 2690/Mum/2010 dt. 27.04.2011

• Borrowed Funds – SMK Shares & Stock, 799/Mum/2009 dt. 24.11.2010

• No delivery cases – Nehal V. Shah, 2733/Mum/2009 dt. 15.12.2010

• Number of scrips– Nagindas P. Sheth H.U.F.No. 961/Mum/2010 dt. 05.04.2011

Pradip N. Kapasi

Chartered Accountant 9

Guiding posts – Irritants & Soothers• Less than 30 days

– Jagadish Master H.U.F., 3233/Mum/09 dt. 18.05.2011– Hitesh S. Doshi, 6603/Mum/2009 dt.15.06.2011

• Sales at higher value– Vinod K. Naevatia, 49 DTR 16 (Mum)

• Turnover ratio– Nehal V. Shah, 2733/Mum/2009 dt. 15.12.2010

• No transaction days – Nehal V. Shah, 2733/Mum/2009 dt. 15.12.2010

Pradip N. Kapasi

Chartered Accountant 10

Guiding posts – Irritants & Soothers

• 143(1) assessement– Nagindas P. Sheth H.U.F, 961/Mum/2010 dt. 05.04.2011

– Gopal Purohit, 122 TTJ 87 (Mum)

– Hitesh S. Doshi, 6603/Mum/2009 dt.15.06.2011

• IPO cases– Shantilal M. Jain, 2690/Mum/2010 dt. 27.04.2011

• LTCG accepted – Vinod K. Naevatia, 49 DTR 16 (Mum)

– SMK Shares & Stock, 799/Mum/2009

Pradip N. Kapasi

Chartered Accountant 11

Guiding posts – Irritants & Soothers

• Dissenting views considered– SMK Shares & stock, 799/Mum/2009 – Hitesh S. Doshi 6603/Mum/2009 dt.15.06.2011

• Intention and books of Account– Kunverji N. Kenia, 131 TTJ 87 (Mum)

• Regular Shuffling– Hitesh S. Doshi, 6603/Mum/2009 dt.15.06.2011

• Profit Motive– Hitesh S. Doshi, 6603/Mum/2009 dt.15.06.2011– Gopal Purohit, 122 TTJ 87 (Mum)

Pradip N. Kapasi

Chartered Accountant 12

Guiding posts - Irritants & Soothers

• Sale on same day– Hitesh S. Doshi, 6603/Mum/2009 dt.15.06.2011

• Dissenting decisions– Deepaben A. Shah, 99 ITD 219(Ahd)– Harsha N. Mehta, 43 SOT 332(Mum)– Jayshree Pradip Shah, 51 DTR 344 (Mum)– Rakesh J. Sanghvi, 4607/Mum/08 dt.31.08.2010– Sadhana Naberia , 41 DTR 393 (Mum)– Sughamchandra Shah, 37 DTR 3 (Ahd)– Synthetic Fibers Trading, 3022/Mum/09 dt.29.09.09– Smt.Rekha Khandelwal, 785/Mum/09 dt.17.03.10– Shailesh L. Shah – H.U.F., 3991/Mum/2008 dt.13.01.10

Pradip N. Kapasi

Chartered Accountant 13

Arbitrage & Day Trading

• Arbitrage– Nature of activity - Objectives– Char. of Income , Omega Sec. & Tdg. 39-B, BCAJ 538– Speculative transactions - Delivery - Hedging– Losses - S. 43(5) - Explanation to s. 73– Expenses - Credit for STT - Tax Audit– Sharing - TDS Deductibility

• Day trading– Nature of operations- Business Expl.2 to s.28– Volume , Frequency– Delivery – STT - Audit

Pradip N. Kapasi

Chartered Accountant 14

PMS - I

• Arrangements – Participating & Non participating– Sharing & Non sharing

• Nature of fees – Advisory & Management – Brokerage– Termination

• Relationship & Treatment– Investment or Business – Deductibility of expenses

Pradip N. Kapasi

Chartered Accountant 15

PMS - II

• Connotation Of Investment – No presumption of business– Smt. Radha Birju Patel, 46 SOT 23 (Mum)(URO)– KRA Trading & Investment P.Ltd ,46 SOT 19(Pune)

• Expenses deductibility– Fees for unsold shares – Return based fees– Termination fees – Maintenance fees– Year of deduction– KRA Holding & Trading (P)Ltd., 46 SOT 19(Pune)– Devendra Motilal Kothari, 136 TTJ 188(Mum)– Alternatively, COA

Pradip N. Kapasi

Chartered Accountant 16

Derivatives –I

Amendment & Notifications

• Amendment in s. 43(5), FA, 2005

• Clause (d) from 01.04.2006

• Deemed Non speculation

• Notification dated 25.01.2006 for BSE & NSE

• Notification dated 22.05.2009 for MCX SE

• Notification dated 25.02. 2011 for USE

Pradip N. Kapasi

Chartered Accountant 17

Derivatives -II

• Commodity– Nirmal Trading Co., 82 ITR 382 (Cal)

– Bharat R. Ruia (H.U.F), 10 Taxman.com 265(Bom)

• Delivery -“lex non congit ad imposibilia”– Bharat R. Ruia (H.U.F), 10 Taxman.com 265(Bom)

• Amendment of 05–prospective w.e.f 01.04.06– Bharat R. Ruia (H.U.F), 10 Taxman.com 265(Bom)

Pradip N. Kapasi

Chartered Accountant 18

Derivatives -III• Effective date of Notification

– A.Y. 2006-07 onwards for BSE and NSE• Prem Associates Adv., 6947/M/09 dt. 17.09.2010• Wipra Financial Services, 4605/M/09 dt 30.09.2010• Hitesh S. Doshi 6603/M/2009 dt.15.06.2011• G.K. Anand Bros Buildwell, 34 SOT 439 (Delhi)• Claris Life Science 112 ITD 307 (Ahd)• Hiren Jaswantrai Shah , 46SOT 276(Ahd.)

– For MCX SE and USE – debatable

• MCX SE Forex Derivatives – S.2(h) and S.2(ac) of SCRA– S.43(5)(d) r.w. Explanation

Pradip N. Kapasi

Chartered Accountant 19

Derivatives -IV• Broker and benefit of clause (d)

– Need for ‘Eligible transaction’

– Contextual compliance

• Emerging understanding– Security derivative up to A.Y.2005-06, speculative

– Other derivatives – speculative

– Shares & Stock are commodities

– No set-off for non security deri. & Expl. toS.73 losses

• Derivatives and Explanation to S.73– Scope, Apollo Tyres Ltd. 255 ITR 273 (SC)

– Inter se set-off

– Hedging profit and fiction of ExplanationPradip N. Kapasi

Chartered Accountant 20

Derivatives -V• Derivatives and hedging

– Applicability of clause (a) and (b)– Nifty and Sensex– Non security Derivatives– Dinesh K. Mehta H.U.F., 976/M/2009 dt. 30.04.2010

• Index Derivatives, – LG Asian Plus Ltd. 46 SOT 159(Mum.)

• Derivative Contract and ‘Capital Asset’– LG Asian Plus Ltd. 46 SOT 159(Mum.)

• S.43(5) and s.115AD – Capital gains – LG Asian Plus Ltd. 46 SOT 159(Mum.)

• Set-off of unabsorbed losses for A.Y. 2005-06– Gajendra Kumar Agarwal, 11 ITR(Trib.) 640 dt.31.05.2011– Rakesh Agarwal, ITA 5843/Mum/2009 dt. 07.01.2011– Possibility of set-off against business Income

Pradip N. Kapasi

Chartered Accountant 21

Derivatives -VI

• Valuation of open contract at the year end – Circular 3 of 2010 dt.23.03.2010

– Bank of Bahrain & Kuwait 132 TTJ 505 (Mum)SB)

– ONGC Ltd. 322 ITR 180 (SC)

• Treatment of premium and transaction costs

• Turnover for Audit

Pradip N. Kapasi

Chartered Accountant 22

Derivatives -VII

• Forex Forward Contracts and Derivatives– Independent Allowability

– Roadblocks• Circular 3 of 2010 dt.23.03.2010

• NACAS & ICAI

• Intergold(I) ltd., 27 SOT 239 (Mum)

• Woodward Governor’s guidelines

• S.43(5)(d) and MCX SE Notification

Pradip N. Kapasi

Chartered Accountant 23

Business loss

• In the course of business;– Safeguard against fluctuation

– Backed by actual transactions in trade

– Trade necessity

– Not a dealer in derivatives

• Soorajmull Nagarmull, 129 ITR 169 (Cal)

• Badridas Gauridu, 261 ITR 256 (Bom)

• Bank of Baharain & Kuwait (Mum)(SB)

• D. Kishore Kumar & Co., 2 SOT 769 (Mum)

• Intergold (I) Ltd., 27 SOT 239 (Mum)Pradip N. Kapasi

Chartered Accountant 24

Conversion from stock• S.45(2) inapplicable

• Whether transfer – Kikabhai Premchand, 24 ITR 506(SC)– Sharkey vs.Wernher, 29 ITR 962 (HL)– Shirinbai Kooka,46 ITR 86(SC)– Dhanuka & Sons, 124 ITR 24 (Cal)

• COA, POH and Indexation for capital asset – B.K.A.V. Birla, 36 ITD 136 (Cal)– Kalyani Exports, 78 ITD 95 (Pune)– Jhanvi Invst. Ltd., 215 CTR 72 (Bom)– Brightstar, 120 TTJ 498 (Mum)DTR 246(Chennai)– Lohia Metals (P)Ltd. 40– Splendid Construction, 122 TTJ 534 (Delhi)

Pradip N. Kapasi

Chartered Accountant 25

Stock Lending

• Objective and utility

• SLS, 1997 * ALBM, BLESS, ‘Badla’

• SEBI’s restriction – Intermediaries

• Tax Implications– Circular No. 751 dated 10th February, 1997

– Section 47(xv) & 45 (2A)

– Applicability to borrower

– SLP offshoots & difficulties

– Corporate Benefits taxation

– STT credits

– Mukesh D. Ambani, 7604/Mum/07 dt. 10.11.2010

– Phoolchand & Sons,46 SOT 83(Mum)

– Reliance Communications infra. 34 SOT 241(Mum.)

Pradip N. Kapasi

Chartered Accountant 26

Deemed Speculation -I

• Valuation loss/ No purchase– Nirvan , 35 BCAJ 399(Mum), Paharpur Cooling , 85 ITD 745(Kol),

– Krishmalaxmi Multitraders, 42B BCAJ 493

• IPO deals– AMP Spg. & Wvg. Mills’s case, 101 TTJ 1113 (Ahd)(SB)

• Set-off of dividend against deemed losses– Torrent Fin., 108 TTJ615(Ahd.), - Excellent Comm.,282 ITR 426(Del.)

• Badla Bill discounting– Tanna Electronics, 7 SOT 121(Mum),Omega Sec, 39-B BCAJ 539(Mum)

• Loans and Advances company– Years – Funds - Income – years - discounting & badla.

– Gujarat Credit,116 TTJ 619 (Ahd) (SB)

• Negative GTI/Business income– Associated Cap, 1103/M/2001,103 TTJ 180(Mum) IIT Inv. Ltd., 106 TTJ 1037(Mum),

Pradip N. Kapasi

Chartered Accountant 27

Deemed Speculation -II

• Loss & Profit– Samba Trading& Investment, 58 TTJ 360(Mum)

– Synergy Enterpreneur Solutions P.Ltd. 46 SOT 111(Mum.)

– Lokmat Newspapers(P) Ltd. 322 ITR 43(Bom.)

• Application to a Broker– Priyasha Mever Finance P.Ltd., 5 ITR 441 (Mum)(Trib.)

• Relevance of legislative intent– AMP Spg. & Wvg. Mills (P) Ltd., 101 TTJ 1113 (Ahd.)(SB)

• Excl. of speculation loss for deciding applicability – Paramount Info. Systems P.Ltd. 42-A BCAJ 169(Mum),

• Set-off of Explanation loss and amendment of 2006– Virendrakumar Jain, 42-A BCAJ, 169(Mum.)

Pradip N. Kapasi

Chartered Accountant 28

Immovable Properties

Income recognition of Developers & Builders

Income from House property or Business

Business Income or Capital gains

Pradip N. Kapasi

Chartered Accountant 29

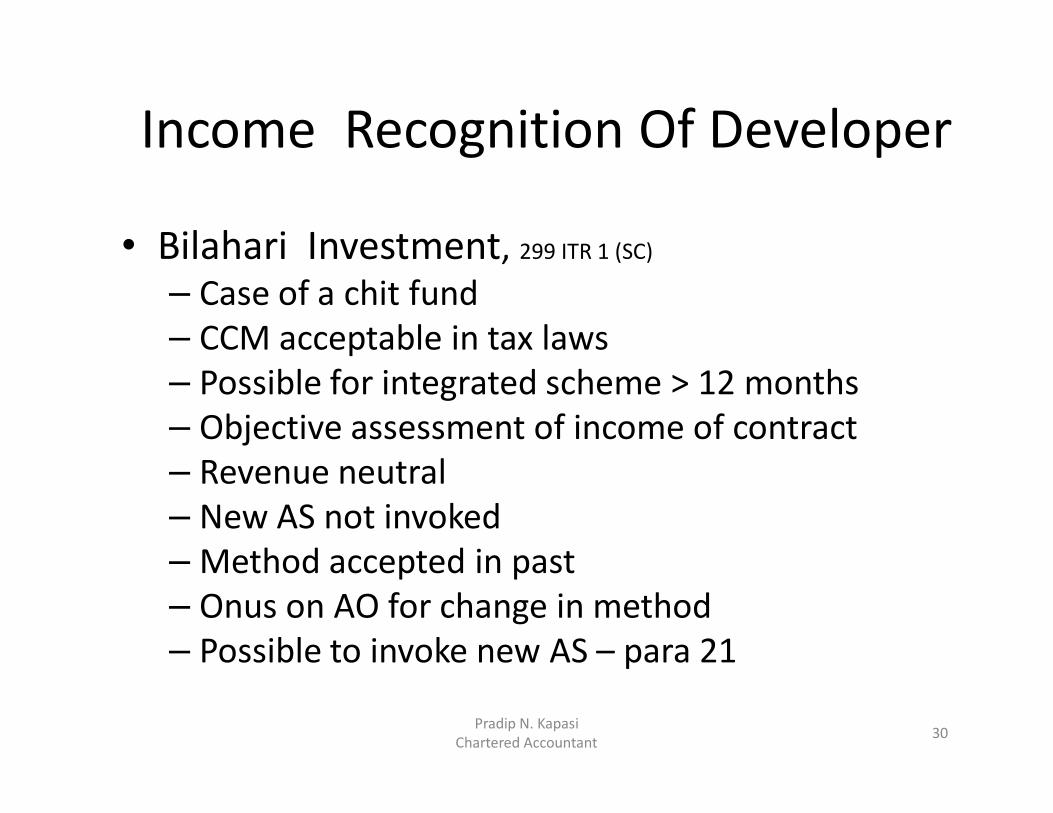

Income Recognition Of Developer

• Bilahari Investment, 299 ITR 1 (SC)

– Case of a chit fund

– CCM acceptable in tax laws

– Possible for integrated scheme > 12 months

– Objective assessment of income of contract

– Revenue neutral

– New AS not invoked

– Method accepted in past

– Onus on AO for change in method

– Possible to invoke new AS – para 21

Pradip N. Kapasi

Chartered Accountant 30

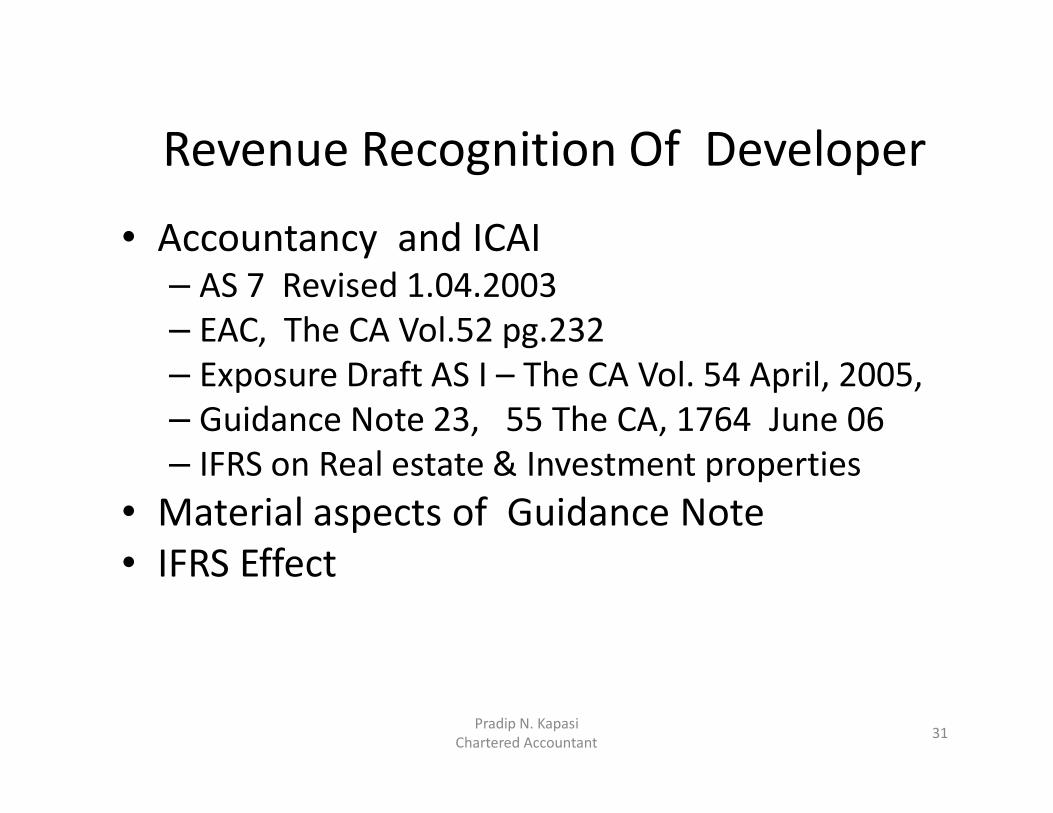

Revenue Recognition Of Developer

• Accountancy and ICAI – AS 7 Revised 1.04.2003

– EAC, The CA Vol.52 pg.232

– Exposure Draft AS I – The CA Vol. 54 April, 2005,

– Guidance Note 23, 55 The CA, 1764 June 06

– IFRS on Real estate & Investment properties

• Material aspects of Guidance Note

• IFRS Effect

Pradip N. Kapasi

Chartered Accountant 31

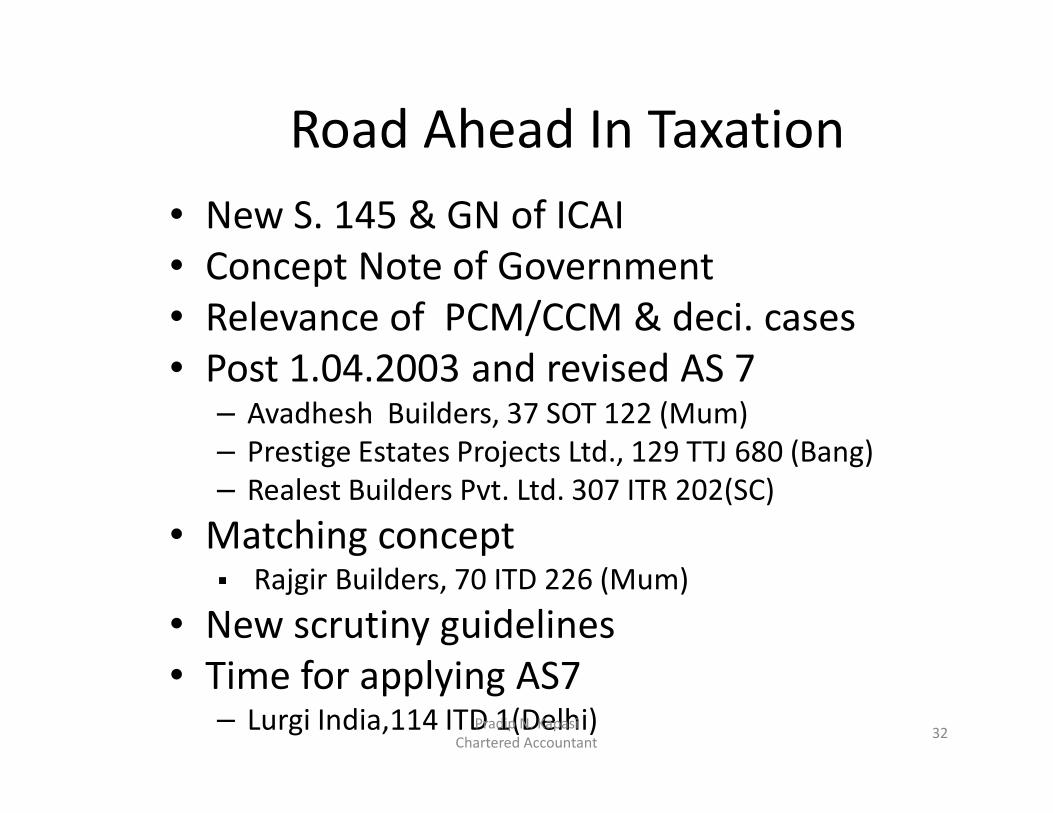

Road Ahead In Taxation

• New S. 145 & GN of ICAI

• Concept Note of Government

• Relevance of PCM/CCM & deci. cases

• Post 1.04.2003 and revised AS 7– Avadhesh Builders, 37 SOT 122 (Mum)

– Prestige Estates Projects Ltd., 129 TTJ 680 (Bang)

– Realest Builders Pvt. Ltd. 307 ITR 202(SC)

• Matching concept� Rajgir Builders, 70 ITD 226 (Mum)

• New scrutiny guidelines

• Time for applying AS7 – Lurgi India,114 ITD 1(Delhi)Pradip N. Kapasi

Chartered Accountant 32

Contractors Perspective

• Continued application of AS7 Revised

• TKP, PMC also

• Permissible method – PCM only

• Synchronization with IAS 11

• Estimation and basis of estimation

Pradip N. Kapasi

Chartered Accountant 33

34

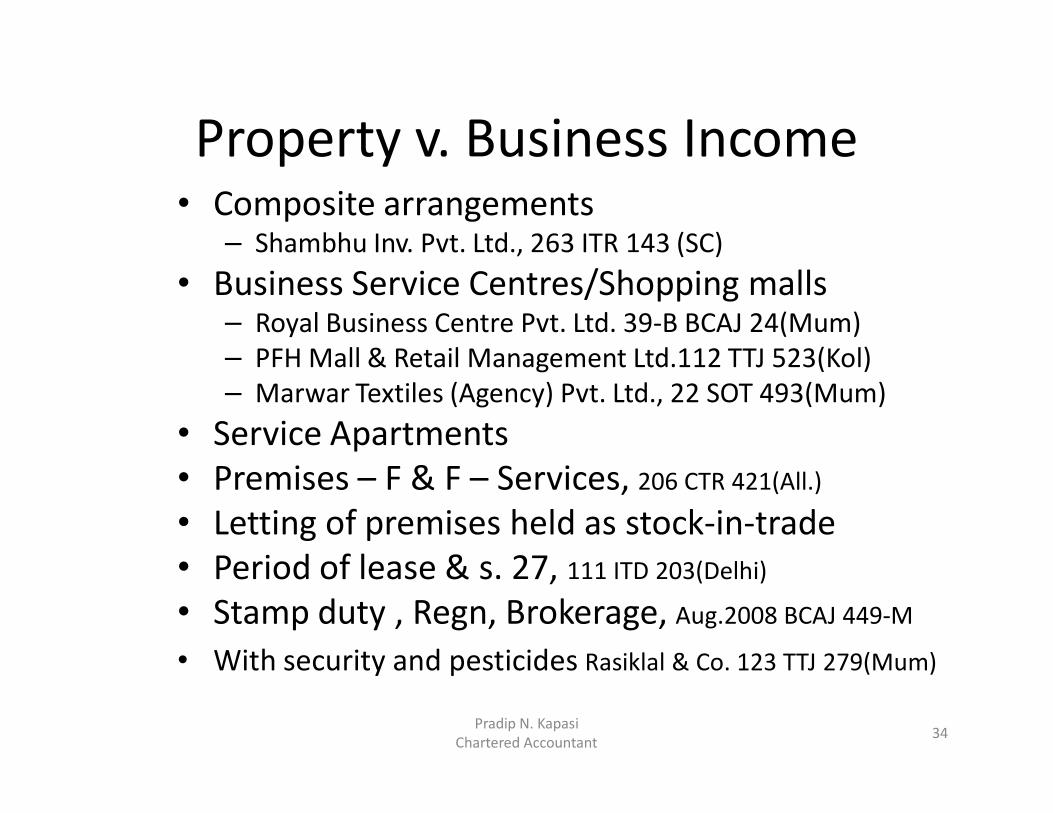

Property v. Business Income• Composite arrangements

– Shambhu Inv. Pvt. Ltd., 263 ITR 143 (SC)

• Business Service Centres/Shopping malls– Royal Business Centre Pvt. Ltd. 39-B BCAJ 24(Mum)

– PFH Mall & Retail Management Ltd.112 TTJ 523(Kol)

– Marwar Textiles (Agency) Pvt. Ltd., 22 SOT 493(Mum)

• Service Apartments

• Premises – F & F – Services, 206 CTR 421(All.)

• Letting of premises held as stock-in-trade

• Period of lease & s. 27, 111 ITD 203(Delhi)

• Stamp duty , Regn, Brokerage, Aug.2008 BCAJ 449-M

• With security and pesticides Rasiklal & Co. 123 TTJ 279(Mum)

Pradip N. Kapasi

Chartered Accountant

Pradip N. Kapasi

Chartered Accountant 35

Business v. Capital Gains

• Plotting and Infrastructure development– Nature of income

• P.M.Mohammed Mira Khan, 73 ITR 735(SC)• Shashikumar Agarwala, 195 ITR 767(All)• Premji Gopalbhai, 113 ITR 785(Guj)• R.V. Gupta, 177 CTR 101(Del.)• G.Venkataswamy Naidu & Co. 35 ITR 594(SC)

– Year of accrual • Madanlal Ahuja, 136 ITR 649(All)• Ashaland Corpn,133 ITR 55(Guj)• Estate Investment, 121 ITR 580(Bom)

OTHERS

STCG or Business Income

Non –Compete Fees

DEPB

Pradip N. Kapasi

Chartered Accountant 36

Non –Compete Fees

• Capital gains or Business Income

• S. 2(24)- S.17-S.28(v) –s.45

– Not to Carry on or Share

– Transfer of Manufacturing rights or Carry business

Pradip N. Kapasi

Chartered Accountant 37

STCG v. Business Income

• Transfer of Depreciable asset

• Gains thereon

• Unabsorbed business loss and s. 72

• Restriction for set off

– Kampli Co-op Sugar Factory Ltd., 83 ITD 460(Bang.)

– Digital Electronics Ltd., 135 TTJ 419(Mum.)

– J.K. Chemicals Ltd., 33 BCAJ 36(Mum.)

– Master Silk Millls P. Ltd. 77 ITD 530(Ahd.)

Pradip N. Kapasi

Chartered Accountant 38

DEPB Income

• Amendments in s. 80HHC and 28(iiia to iiie)

– Topman Exports Ltd. 124 ITD 1 (Mum.)(SB)

– Kalpatru Colours & Chemicals 328 ITR 451(Bom.)

Pradip N. Kapasi

Chartered Accountant 39

Thank You

Pradip N. Kapasi

Chartered Accountant 40