ita economics panel aerospace & defense: what lies ahead?

TRANSCRIPT

Please see addendum of this report for important disclosures.

ITA Economics PanelAerospace & Defense: What Lies Ahead?

Gautam [email protected]

September 15, 2009

1

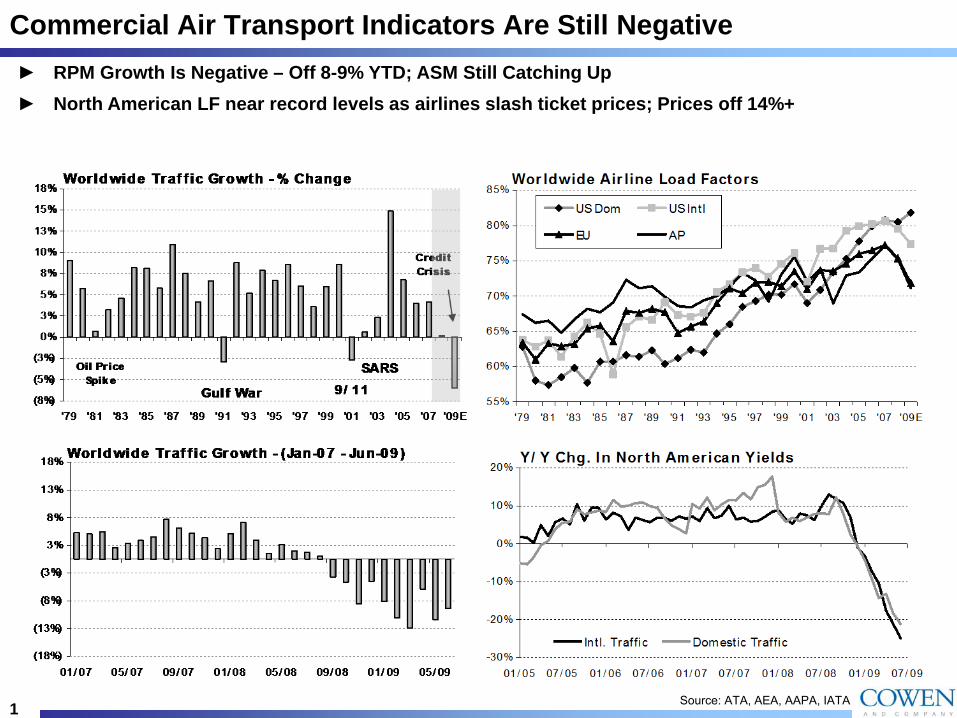

Commercial Air Transport Indicators Are Still Negative► RPM Growth Is Negative – Off 8-9% YTD; ASM Still Catching Up► North American LF near record levels as airlines slash ticket prices; Prices off 14%+

Source: ATA, AEA, AAPA, IATA

2

Commercial Air Transport Indicators Are Still Negative

► Here is the raw data

Source: ATA, AEA, AAPA, Amstat, Boeing , Airbus

3

Parked Aircraft A Growing Overhang

► Stored New Aircraft Have Doubled To 2%+ of Fleet► Older Planes Stored @ 21% Of Fleet – May Return Given Oil Price Drop

Source: Ascend

4

De-stocking Is Amplifying Aftermarket Pressure

Commercial

► Airline De-stocking Has Exaggerated Impact on Aftermarket/Spare Orders■ Reduced utilization and disappointing airline profitability encourages de-stocking■ Commercial A/M may be 2-3Q’s away from a turn

– US Domestic Carriers will most likely lead the intl. carriers, as domestics began de-stocking earlier

Source: IATA, UTX, GR, HON, GE, Moog, COL, TGI, TDG

Y/ Y Chg. In Global Traff ic vs. Y/ Y Chg. In A/ M Sales

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Q1:07 Q2:07 Q3:07 Q4:07 Q1:08 Q2:08 Q3:08 Q4:08 Q1:09 Q2:09

Global ASM Aftermarket Sales Global RPM

5

Aftermarket “Double-Dip” Hasn’t Occurred Since Early 1990s

Commercial

► P&W Aftermarket “Double Dip” Has Proven An Exception To The “Normal” Aftermarket Cyclical Recovery Pattern

► Weaker airline pricing power raises this risk and unique cyclical downturn drivers (credit crisis; extremely weak economy) make double-dip tough to rule out

► RPM/ASM compares get a lot easier in November

Source: IATA, UTX, GR, HON, GE, Moog, COL, TGI, TDG

6

Positives: Backlog Is Bigger & More Diverse Than In Prior Peaks

► Record Commercial Air Transport Backlog of 7,005 Aircraft■ Net Orders YTD of 158; 269 new a/c orders; 111 cancellations■ 68% of Current Backlog is to Asian, European and Middle Eastern Countries

Source: Ascend

1660

107183

318398

493850

2,1312,449

0 500 1,000 1,500 2,000 2,500 3,000

A340767747

A380777

A330A350

787737

A320Single Aisle

Wid

ebod

y

Back log by Air cr af t Type

7

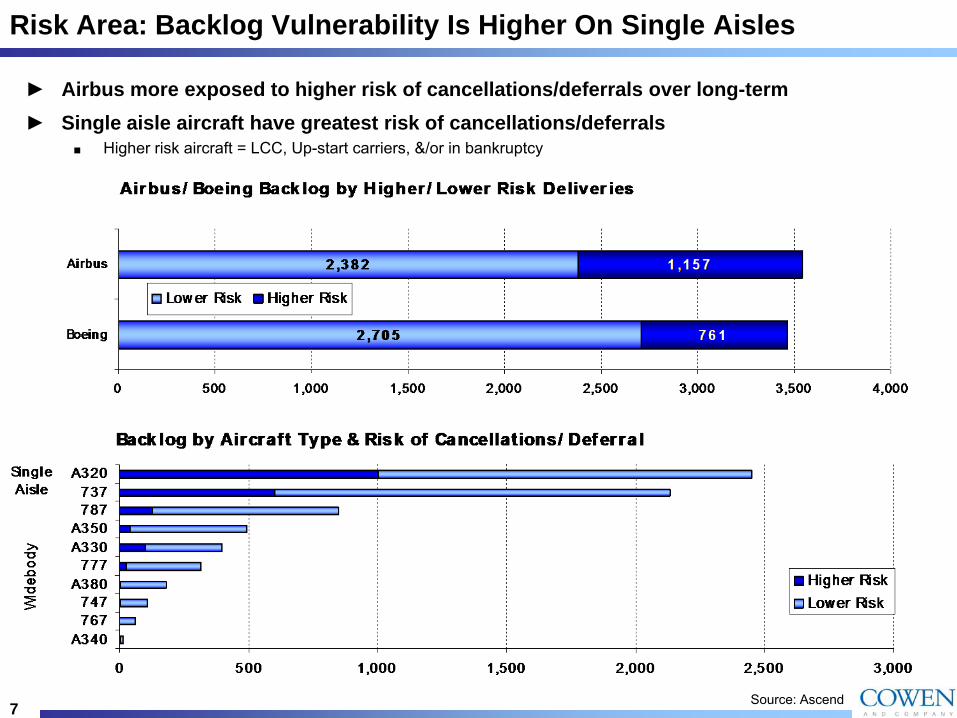

Risk Area: Backlog Vulnerability Is Higher On Single Aisles

► Airbus more exposed to higher risk of cancellations/deferrals over long-term► Single aisle aircraft have greatest risk of cancellations/deferrals

■ Higher risk aircraft = LCC, Up-start carriers, &/or in bankruptcy

Source: Ascend

8

YTD Cancellations/Deferrals Mostly Hit C10 Single Aisle Slots

Source: Ascend

1 52 6

6 7 1 03

6

4 3

3 01 4 4

00

10

20

30

40

50

60

70

80

2009 2010 2011 2012 2013 2014

BoeingAirbus

Impact on Manufactur er Pr oduct ion Book Fr om 2009 YTD Announced A/ C Defer r als

0 20 40 60 80 100

A340A350

767A330

777747

A380A320

737787

Cancellat ionsDeferrals

2009 YT D Cancellat ions & Deferrals

* Excludes aircraft without firm delivery dates

9

C10 Rate Cuts Possible Given Big RPM/ASM Gap; Downturns Tend To Endure

► Sharp 2009 traffic drop (est. 5-7%) vs. 4% growth in airline rated capacity (includes stored aircraft) augurs OE capacity cuts & extended downturn■ RSM/ASM Gap A Whopping 10%+ in 2009■ LT traffic growth in the 4-5% range; we expect C10 RPM gains to remain below LT average

■ Delivery downturns normally last 3-4 years; with avg. annual unit declines of 14-15%

10

We Expect Single Aisle Rate Cuts In 2010

► 2009 Peak Deliveries of 940 aircraft; 746 Single Aisle, 194 Wide body■ See an 11% decline in Comml OE deliveries through 2011; Extended Dip Possible■ Single Aisles the Hardest Hit; look for 13% per annum decline through 2011

– 737 rate cut to 275/yr by 2011, vs. 370 in 2009– A320 rate cut to 280/yr by 2011, vs. 365 in 2009

■ Wide body cut mitigated by ramp in 787 & A380

► 787 1st Flight Q4:09; Entry Into Service Q4:10

Source: Cowen and Company, Ascend

11

787: Still Has Lead Time & Order Book Advantages; But Schedule Uncertain

Source: Cowen and Company

1523

975

386

11161036

862

556

102122132149112114140

896

493

165 179 142

896

493

202

446

249

41%

27%

15%11%

24%

17%

10%

36%

12%

82%

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

787 A350 XWB A380 747 A330 A340 777 767 707 DC-8 DC-10 L-10110%

10%

20%

30%

40%

50%

60%

70%

80%

90%Orders before first delivery Total orders Orders before first delivery as % of total orders

In Production Out of ProductionIn Development

12

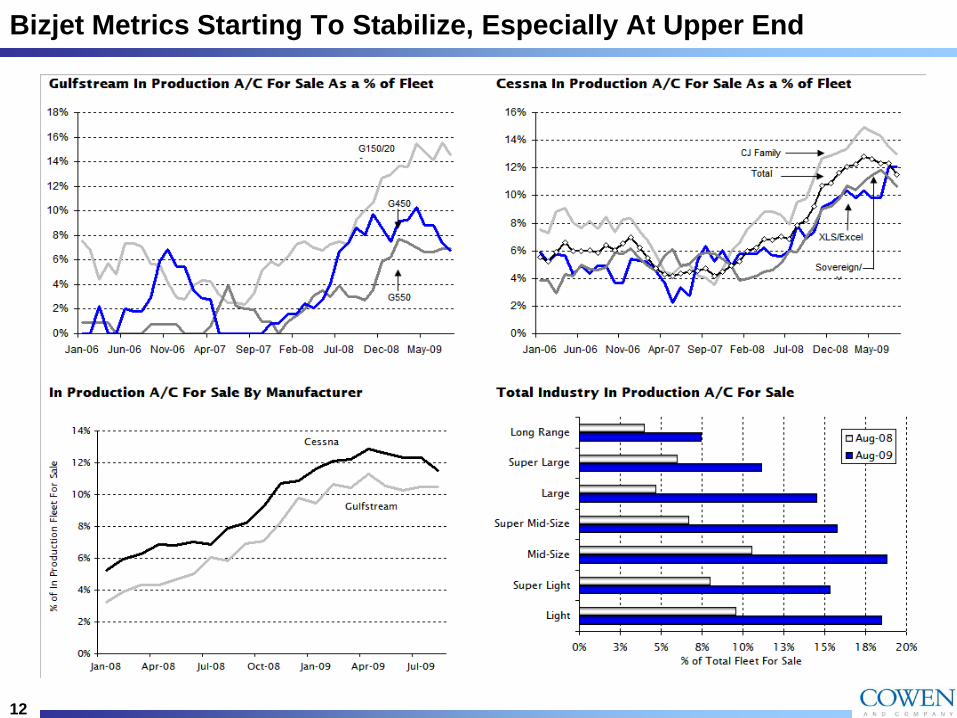

Bizjet Metrics Starting To Stabilize, Especially At Upper End

13

Bizjet Cycle In Sharp Drop; But Past Downturns Only Lasted 2 years

► Pre-Owned Trends Starting To Stabilize ► 2009-10 Delivery Collapse Matches Past Nasty, Two-Year Downswings

Source: Amstat, Company Documents

14

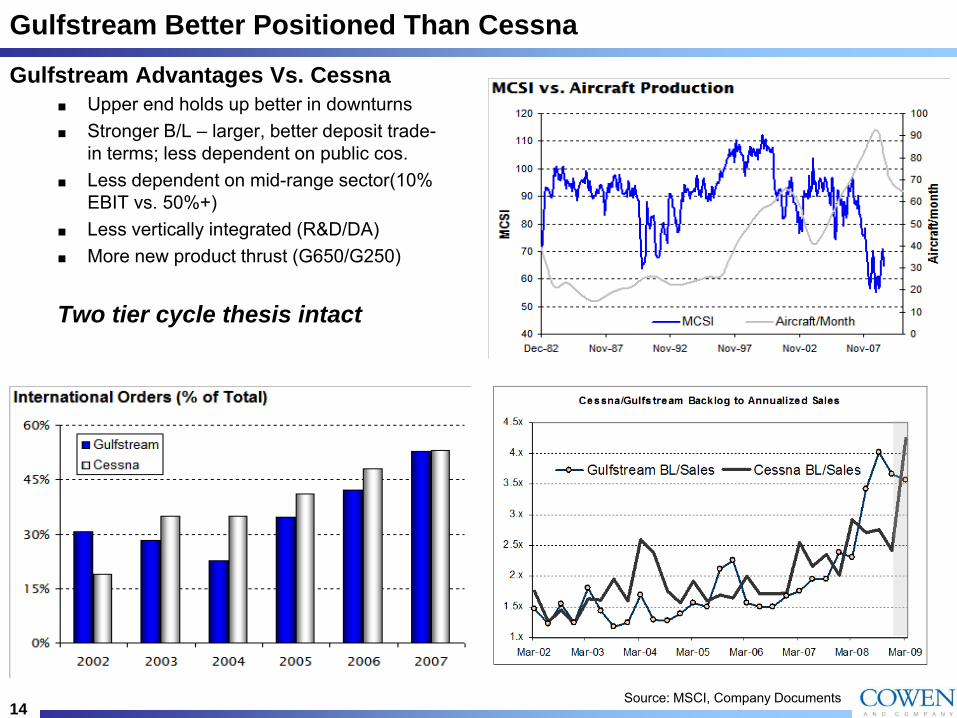

Gulfstream Better Positioned Than CessnaGulfstream Advantages Vs. Cessna

■ Upper end holds up better in downturns■ Stronger B/L – larger, better deposit trade-

in terms; less dependent on public cos. ■ Less dependent on mid-range sector(10%

EBIT vs. 50%+)■ Less vertically integrated (R&D/DA)■ More new product thrust (G650/G250)

Two tier cycle thesis intact

Source: MSCI, Company Documents

Please see addendum of this report for important disclosures.

Defense Spending & JSF

16

DoD’s Aging, Declining Equipment Inventory An Ongoing Issue

Navy Ships USAF Fighter Aircraft

Ground Combat Vehicles

Source: Cowen estimates derived from Congressional Budget Office (CBO) and Naval Historical Center

USAF Tankers

17

“Discretionary” DoD Budget Likely To Be Pressure From Record Deficits

► 2009 Deficit Likely to Surpass $1.8 Trillion► OMB Forecast 2010-2019 Deficit to Exceed $7.1T; DoD Budget Likely a Bill Payer

18

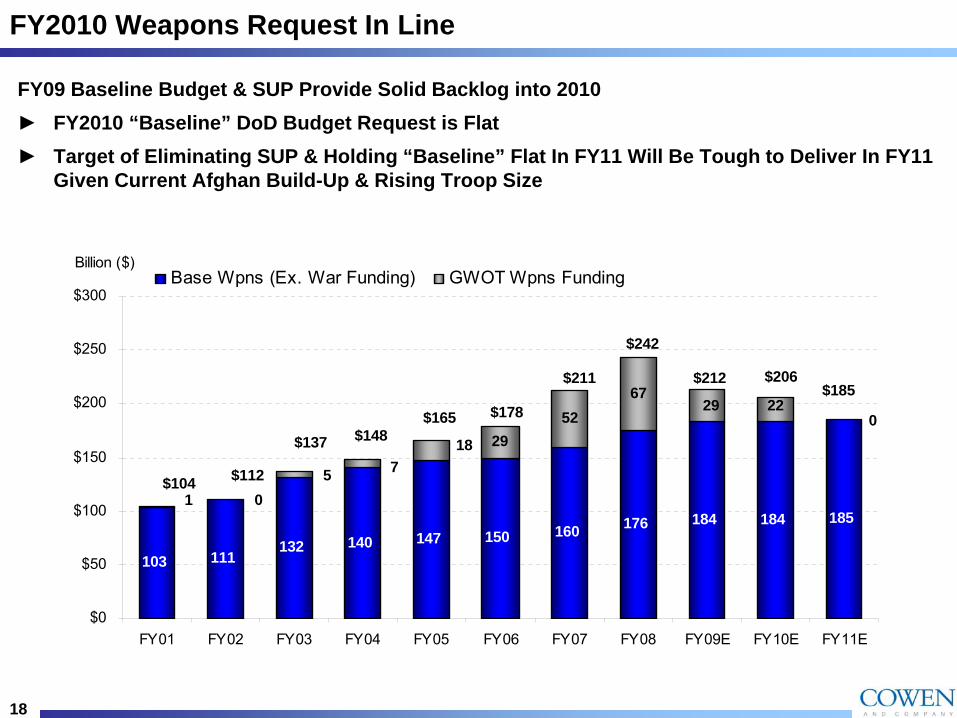

FY2010 Weapons Request In Line

FY09 Baseline Budget & SUP Provide Solid Backlog into 2010► FY2010 “Baseline” DoD Budget Request is Flat ► Target of Eliminating SUP & Holding “Baseline” Flat In FY11 Will Be Tough to Deliver In FY11

Given Current Afghan Build-Up & Rising Troop Size

103 111132 140 147 150 160 176 184 184 185

2952

67

501

718

0

$0

$50

$100

$150

$200

$250

$300

FY01 FY02 FY03 FY04 FY05 FY06 FY07 FY08 FY09E FY10E FY11E

Base Wpns (Ex. War Funding) GWOT Wpns Funding

$137 $148$165 $178

$211

$242

$212 $206

$104

$185

$112

29 22

Billion ($)

19

Procurement The “Swing Item” When DoD Budgets Move Dramatically

20

Headcount Strongly Correlated With Weapons Spending

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1968 1973 1978 1983 1988 1993 1998 2003 2008

Y/Y

Ch

g. (

%)

Manpower Weapons Spending - BA

► Weapons spending correlated to military headcount ---- which is rising

► Perceived threat level is high► But, Iraq withdrawal likely will pressure weapons accounts

21

Joint Strike Fighter Appears On Track

► 2010 Budget Request of $10.4B ($6.8B for procurement) is up 53% from $6.8B ($3.3 for procurement) in 2009■ Est. buy weight of 20 mts; Production ramps through 2015

22

Joint Strike Fighter Snapshot

► JSF ramps aggressively through 2015 ► Israel (not in table below) also interested in buying 25 aircraft with 50 options

23