italy in the eu: economic perspectives and challenges italy's public debt-to-gdp ratio -8-6-4-2...

TRANSCRIPT

Lucio Pench Director, Fiscal Policy

European Commission DG Economic and Financial Affairs

INTERNATIONAL BANKING FORUM 2011

Brescia, 13-14 June 2013

Italy in the EU: Economic

Perspectives and challenges

2 2

EUROPEAN

CONTEXT

3 3

Gradual recovery in the Euro area

100

102

104

106

108

110

112

114

116

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22

Past recoveries Developments since 2009Q2

Quarters

Index

Note: Real GDP following the recessions of the mid 1970s, early 1980s and early 1990s

*European Economic Forecast – Spring 2013

forecast*

4 4

Europe's answer to the crisis

FINANCIAL

STABILITY

PUBLIC

DEBT

ECONOMIC

GROWTH

Breaking the

vicious circle

Structural

reforms

Fiscal

discipline

Banks Banks

recapitalization

Firewalls

Differentiated, growth-

friendly fiscal

consolidation

Commission proposal for

a single surveillance

mechanism

ESM: fully

implemented

since October

2012

ECB: Outright

Market

Transactions

Compact for

Growth and

Jobs

Further fiscal

measures and

structural reforms in

some Member states

€100bn to cover

financial

requirements of

Spanish banks

COMPLETE MONETARY UNION

EU and

national fiscal

governance

reform:

• Six pack

• Two pack

5 5

Annual Growth Survey 2013

1. Pursuing differentiated, growth-friendly fiscal

consolidation

2. Restoring normal lending to the economy

3. Promoting growth and competitiveness for

today and tomorrow

4. Tackling unemployment and the social

consequences of the crisis

5. Modernising public administration

6 6

ITALY

7 7

Slow growth and low employment

-6

-4

-2

0

2

4

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

IT - Hours worked EA - Hours worked IT - Real GDP EA - Real GDP

Forecast

8 8

Loss of external competitiveness (1)

95

100

105

110

115

90 92 94 96 98 00 02 04 06 08 10 12

Index (

1990 =

100)

EA-12 IT

-8

-6

-4

-2

0

2

4

6

8

10

12

14

16

99 00 01 02 03 04 05 06 07 08 09 10 11 12Cum

ula

tive c

hange s

ince 1

998 (

%)

ULC contribution NEER contribution

REER

-4

-3

-2

-1

0

1

2

3

4

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12*

% o

f G

DP

Capital accountCurrent transfersIncome balanceTrade balance - servicesTrade balance - goodsTrade balanceCurrent account balance (CA)

A deteriorating current account …

… mainly driven by a subdued total factor productivity trend …

… not reflected in wage dynamics and exacerbated by NEER*

* Nominal effective exchange rate

9 9

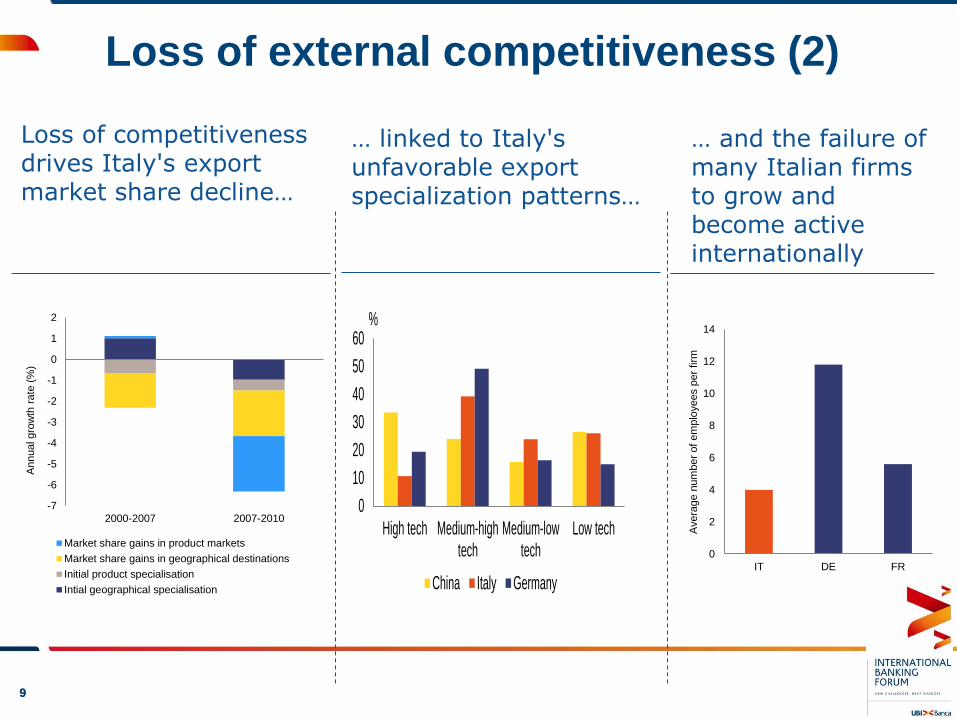

Loss of external competitiveness (2)

-7

-6

-5

-4

-3

-2

-1

0

1

2

2000-2007 2007-2010

Annual gro

wth

rate

(%

)

Market share gains in product markets

Market share gains in geographical destinations

Initial product specialisation

Intial geographical specialisation

0

10

20

30

40

50

60

High tech Medium-hightech

Medium-lowtech

Low tech

China Italy Germany

%

Loss of competitiveness drives Italy's export market share decline…

… linked to Italy's unfavorable export specialization patterns…

0

2

4

6

8

10

12

14

IT DE FR

Avera

ge n

um

ber

of

em

plo

yees p

er

firm

… and the failure of many Italian firms to grow and become active internationally

10 10

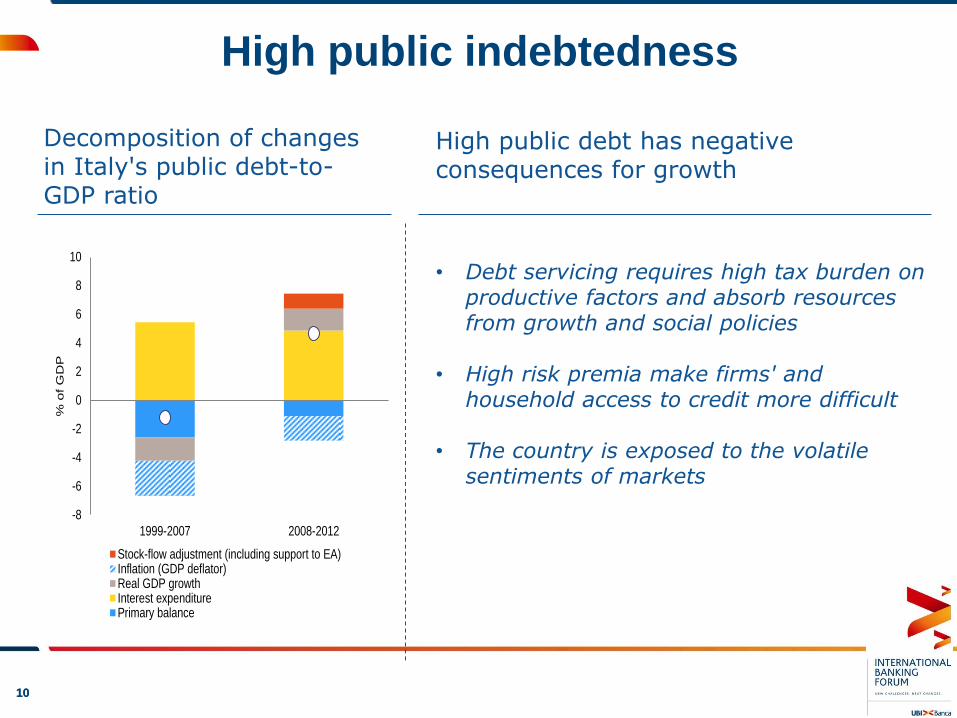

High public indebtedness

Decomposition of changes in Italy's public debt-to-GDP ratio

-8

-6

-4

-2

0

2

4

6

8

10

1999-2007 2008-2012

% o

f G

DP

Stock-flow adjustment (including support to EA)Inflation (GDP deflator)Real GDP growthInterest expenditurePrimary balance

• Debt servicing requires high tax burden on productive factors and absorb resources from growth and social policies

• High risk premia make firms' and household access to credit more difficult

• The country is exposed to the volatile sentiments of markets

High public debt has negative consequences for growth

11 11

High public indebtedness: current

perspectives

96

100

104

108

112

116

120

124

128

132

136

140

2010 2011 2012 2013 2014 2015 2016 2017

(% of GDP)

Stochastic debt projections 2013-17, ITALY

p10_p20 p20_p40 p40_p60

p60_p80 p80_p90 p50 gdebt_gdp_DSM

Source: Commission Services

12 12

The need to mobilize publicly-owned assets

13 13

State aid to Italian financial institutions has been among the lowest in the EU so far

0%

50%

100%

150%

200%

250%

300%

350%

400%

IE DK

BE

GR

ES

NL

UK

LV

PT

SW S

I

AT FI

CY

DE

LU

FR

PL

HU IT SL

LT

BG

CZ

EE

MT

RO

EU

27

Recapitalisation measures Other measures*

Source: European Commission (Facts and figures on state aid in the EU Member States, Commission Staff working document – autumn 2012 update, SEC(2012) 443 final). * Includes guarantees, asset relief interventions and liquidity measures.

Approved amounts of aid to financial institutions per Member State (% of 2011 GDP, measures between 1

October 2008 and 1 October 2012)

14 14

Bank loans to firms contract, and SMEs in particular suffer from tight credit conditions

-6

-4

-2

0

2

4

6

8

10

12

14

16

Jan 0

3

Sep 0

3

May 0

4

Jan 0

5

Sep 0

5

May 0

6

Jan 0

7

Sep 0

7

May 0

8

Jan 0

9

Sep 0

9

May 1

0

Jan 1

1

Sep 1

1

May 1

2

Jan 1

3

%

0

1

2

3

4

5

6

7

Ja

n 0

3

Se

p 0

3

Ma

y 0

4

Ja

n 0

5

Se

p 0

5

Ma

y 0

6

Ja

n 0

7

Se

p 0

7

Ma

y 0

8

Ja

n 0

9

Se

p 0

9

Ma

y 1

0

Ja

n 1

1

Se

p 1

1

Ma

y 1

2

Ja

n 1

3

%

All loans Up to EUR 250k

Up to EUR 1m Over EUR 1m

ECB policy rate

12-month % change in stock of loans to non-financial corporations in Italy

Interest rate on new bank loans to non-financial corporations in Italy

Source: Bank of Italy

15 15

Banks' total bad debts have tripled since 2009, while bad debt coverage has trended down

0

20

40

60

80

100

120

140Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

Oct-

12

Ja

n-1

3

Ap

r-1

3

EU

R b

illio

n

Gross bad debts - total

Gross bad debts - productive sectors*

Provisions and direct writedownsSource: Bank of Italy. There is a statistical break in January 2011. 'Bad debts' in Italian are 'sofferenze'. * 'Productive sectors' includes non-financial corporations and producer households.

16 16

What policy mix, then?

1. Deploying growth- and equity-friendly

fiscal consolidation

2. Enacting structural measures addressing

competitiveness challenge

3. Restoring the supply of credit to the

economy

hand-in-hand to start a virtuous circle

17 17

Fiscal consolidation (1)

Little room for reducing the current level of

expenditure (and, consequently, of taxation)

18 18

Fiscal consolidation (2)

..but ample scope for improvement, by

• Reducing expenditure inefficiencies and prioritise

spending on growth levers

• Improving efficiency of tax system and reducing

distortions by shifting the tax burden away from labour

and capital and fighting tax evasion

19 19

Improving public expenditure quality Illustrative QPF indicators for sub-dimension QPF 3 (composition, efficiency and effectiveness of expenditure)

Composition Education Health R&D and

innovation Public

infrastructures Public order

Public administration

Country Average Rank Average Rank Average Rank Average Rank Average Rank Average Rank Average Rank BE -0.5 19 5.6 4 -1.8 13 1.6 9 0.4 8 -1.8 13 -3.4 12

BG -2.8 21 -8.3 23 -23.2 25 -13.5 27 -14.7 26 -22.2 27 -19.4 27

CZ 8.7 6 5.6 5 -5.9 19 -6.8 16 -5.4 16 -10.0 22 -14.5 23

DK 3.5 11 4.7 7 -4.8 17 1.9 8 5.2 3 4.4 6 13.1 1

DE -9.2 26 1.7 14 -0.3 9 6.3 2 5.0 4 6.3 3 0.5 7

EE 8.5 7 2.1 12 -15.4 22 -4.6 14 -3.7 14 -7.5 20 -2.9 10

IE 7.0 8 7.4 2 -0.3 10 2.6 7 -8.6 21 -4.5 17 -0.4 8

EL -13.6 27 -6.9 21 -1.1 12 -9.9 24 -7.2 19 -1.5 12 -10.9 18

ES 0.7 15 -12.6 25 2.1 3 -9.5 22 -3.3 13 -3.7 16 -5.4 13

FR 2.7 12 1.0 16 1.2 5 4.9 3 2.3 6 -0.6 11 -2.9 11

IT -1.7 20 -8.3 22 0.9 6 -7.2 18 -7.2 18 -8.5 21 -15.4 24 CY 1.3 13 3.6 10 -2.6 15 -11.8 26 -2.3 11 6.6 2 -6.9 15

LV 11.6 2 -1.2 19 -25.1 27 -9.1 19 -10.5 24 -2.1 14 -13.3 20

LT 10.1 3 1.8 13 -20.7 24 -3.7 13 -6.2 17 -11.7 23 -14.2 22

LU -3.0 22 -2.9 20 1.6 4 0.0 10 8.5 1 2.2 8 4.5 6

HU -0.2 17 0.4 17 -16.2 23 -7.0 17 -7.6 20 -3.1 15 -13.0 19

MT 0.2 16 -15.8 26 -5.0 18 -5.3 15 -10.3 22 9.3 1 -6.7 14

NL -4.0 24 4.5 8 -0.6 11 4.1 4 6.8 2 0.0 9 6.9 4

AT -3.7 23 6.6 3 0.3 8 3.4 5 3.6 5 6.2 4 5.1 5

PL 1.0 14 3.0 11 -12.2 20 -10.1 25 -13.9 25 -16.1 25 -17.4 25

PT 12.9 1 -18.4 27 2.2 2 -9.6 23 -3.0 12 -0.4 10 -8.1 17

RO 9.0 4 -9.4 24 -24.5 26 -9.3 20 -17.4 27 -16.9 26 -17.9 26

SI 8.9 5 3.7 9 -2.4 14 -3.6 12 -5.3 15 -4.8 18 -7.4 16

SK -6.5 25 1.5 15 -14.9 21 -9.4 21 -10.3 23 -12.3 24 -14.0 21

FI -0.5 18 12.6 1 0.7 7 9.3 1 -0.6 9 5.8 5 9.7 2

SE 4.1 10 5.1 6 3.2 1 2.9 6 1.2 7 2.4 7 7.1 3

UK 5.3 9 -0.2 18 -3.3 16 -0.7 11 -2.1 10 -5.8 19 -0.9 9

Average 1.8 -0.5 -6.2 -3.5 4.0 -3.3 -5.5

Std. Dev. 6.5 7.5 9.1 6.4 6.7 7.9 9.2

20 20

Improving the structure of taxation Overview table: Tax policy challenges in Member States

Contribution

of tax

increases to

consolidation

Need

and

room

for tax

shift

Labour tax

reforms for

specific

groups

Broadening tax bases Tax governance

challenges Special topics

Need to

review

tax

expend.

in PIT

Need to

review

tax

expend.

in CIT**

Debt bias

in

corporate

taxation

Increase

VAT

efficiency

Tax

compliance

Tax

admin.

Housing taxation

Recurrent

tax low

Debt

bias

Structural

shift

BE X X (X) X (X) X X X

DE (X) (X) (X) X

EE X X

EI p - X (X)

EL p - X X X X X X X X

ES X X X (X) X X X X

FR X X X X X (X) X

IT X X X X X X X CY p - (X) X

LU X X X X

MT X X X X X

NL (X) X X

AT (X) (X) X X

PT p - X X X (X) X X X X

SI X X X X

SK X (X) X X X

FI X

BG X X X

CZ X X (X) X X X X

DK X

LV X X X X

LT X (X) X X

HU (X) X (X) X X

PL (X) (X) X X

RO p X X X X X X

SE (X) (X) X

UK X X X

21 21

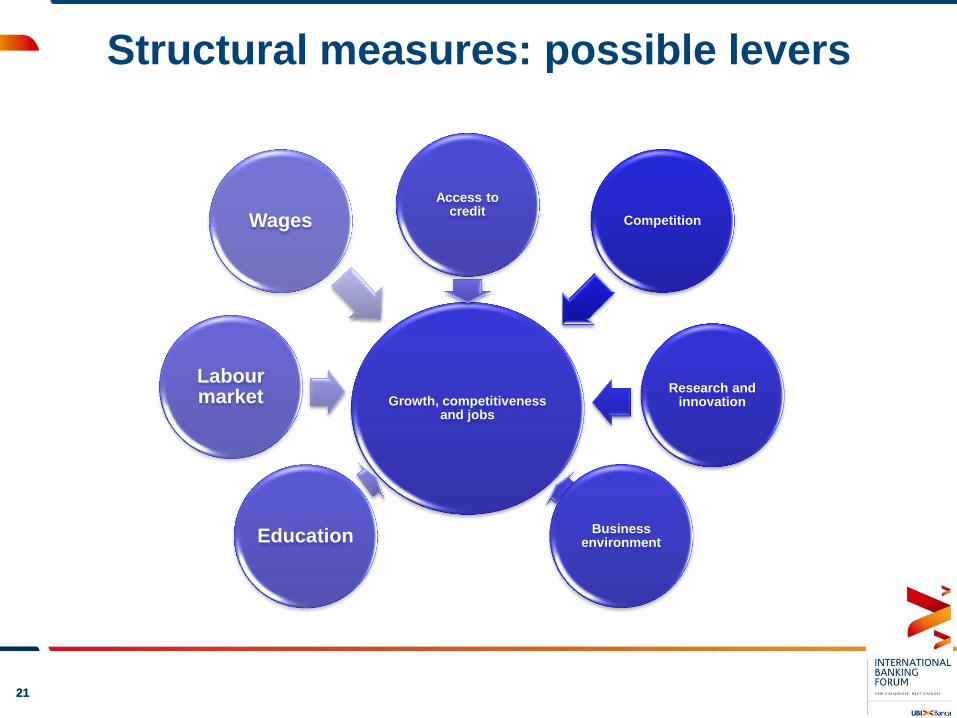

Structural measures: possible levers

Growth, competitiveness and jobs

Competition

Research and innovation

Business environment

Access to credit

Education

Labour market

Wages

22 22

Important steps already taken

• Reducing the deficit and moving towards fiscal

consolidation

• Shifting tax burden from labour and capital

onto property, consumption and environment

• Improving functioning of labour and product

markets

• Improving business environment

• Fostering human capital and favouring

research and innovation

23 23

Reform momentum to be maintained

• No backtracking on fiscal consolidation as

pre-condition for growth enhancing strategy

• Continue structural reforms to remove

bottlenecks to the adjustment of the economy

and boost long-term growth potential

(education, competition, business

environment, tax administration efficiency,

social protection)

• Tackle constrains to financing of

enterprises

24 24

The challenge of implementation

Need to adopt the required implementing legislation…

44%

16%

16%

24%

published/adopted

not adopted and no expiringdate

Not adopted, but defined bythe competent Ministry

not adopted/expired

…and follow up with concrete implementation measures

25 25

Country-specific recommendations:

Italy 2013 1. Pursue growth-friendly fiscal consolidation. Improve the efficiency and

quality of public expenditure.

2. Reinforce the administrative and business environment. Ensure timely

implementation of on-going reforms.

3. Promote banking sector corporate governance, asset-quality screening

and the resolution of non-performing loans on banks’ balance sheets.

Promote further the development of capital markets to diversify and enhance

firms' access to finance.

4. Ensure the effective implementation of the labour market and wage setting

reforms. Foster labour market participation and prevent early school leaving.

5. Shift the tax burden from labour and capital to consumption, property and

the environment in a budgetary neutral manner. Pursue the fight against tax

evasion.

6. Promote market opening in the services sector and foster market access

to local public services. Upgrade infrastructure capacity in network industries.