japan real estate second quarter 2013 - rreef

TRANSCRIPT

Japan Real Estate Second Quarter 2013 April 2013

Research Report

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 1

Table of Contents

Executive Summary ............................................................................. 1

Macro Economy ................................................................................... 2

Capital Market ...................................................................................... 4

Lending .................................................................................... 4

Pricing ...................................................................................... 5

Transactions ............................................................................ 6

Performance ............................................................................ 8

J-REITs .................................................................................... 8

Market Fundamentals ........................................................................ 11

Office ..................................................................................... 11

Retail ..................................................................................... 14

Residential ............................................................................. 15

Industrial ............................................................................... 16

Past Issues ......................................................................................... 18

Important Notes .................................................................................. 19

Global Research Team ...................................................................... 20

Prepared By:

Koichiro (Ko) Obu Head of Research & Strategy Japan and Korea +81 (0) 3 5156 6522 [email protected] Minxuan Hu Property Market Research +81 (0) 3 5156 6525 [email protected] Mark Roberts Head of Research & Strategy +1(212) 454-0974 [email protected]

NOTE : Following the combination of Deutsche Bank’s asset and wealth management capabilities into one new division, these previously separate businesses were unified under one identity – the Deutsche Asset & Wealth Management name and the platinum Deutsche Bank logo.

Accordingly, the global real estate investment business (formerly RREEF Real Estate) has adopted the new Deutsche Asset & Wealth Management brand in place of the RREEF name and the RREEF logo.

The following Global Real Estate Strategic Outlook follows the recently published regional Real Estate Strategic Outlooks for the United States, Europe and Asia Pacific, which were published prior to the re-branding.

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 1

Executive Summary Economy: In the first quarter of 2013, confidence in the Japanese macro economy ex-

perienced one of the most significant surges in recent history. Haruhiko Kuroda, the new

governor of the Bank of Japan, announced in April 2013 an unprecedented policy of

monetary easing that includes inflation targets and purchase commitments. Although the

eventual impact of these plans will take some time to unfold, capital markets have reacted

favourably so far, and the Japanese economy appears poised to grow strongly in the latter

half of the year.

Capital market: Given investors’ solid expectation of inflation in the future, Japanese real

estate has recently gained allure since it is expected to benefit from an inflation economic

environment. The J-REIT index has skyrocketed to its highest point since the global credit

crisis, and the aggregate amount of equity raised by J-REITs in the six months to March

2013 set an all time record. Because capital is now flowing strongly into real estate trans-

actions, further cap rate compression is expected this year.

Property markets: The leasing market for Japanese property has so far been much less

buoyant than capital markets might imply, but there have nevertheless been some positive

changes. The average rents for newly-built offices in Tokyo grew 9.2% in the first two

months of 2013, the largest growth spurt in more than five years. Among Tokyo’s central

five wards, Shibuya emerged as the strongest office submarket with a vacancy rate of

6.0% in February 2013 compared to an 8.6% average for the central five wards. Property

leasing also showed signs of broad stabilisation in the residential and logistics markets in

Japan in early 2013.

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 2

Macro Economy Forecasts for the Japanese macro economy have been revised upward a couple of times

since Prime Minister Shinzo Abe assumed power in December 2012. Financial markets

have broadly welcomed his aggressive economic policies which include monetary easing

and fiscal stimulus aimed at ending deflation and weakening the Japanese yen’s value.

Although the recovery is still nascent, Japan’s real GDP is now expected to grow by 1.4%

in 2013 according to Deutsche Bank economists. More moderate growth should follow in

2014 when a hike in the consumption tax (VAT) rate is planned. The hike will initially move

the tax rate from the current 5% to 8% next year (and eventually to 10% in 2015).

Exhibit 1 — GDP Growth Outlook for Japan

Notes: F = forecast, there is no guarantee forecast growth will materialise. Please refer to Important Notes (see end of report)

Sources: Deutsche Bank, “Japan Economics Weekly”

As of April 2013

The Diffusion Index (DI) of the Tankan Survey conducted by the Bank of Japan (BoJ) also

improved during the past quarter. The DI recovered from the previous trough of a -3 index

value in December 2012 to -1 in March 2013, with a positive outlook of +4 for the next

quarter. The recovery is less evident in the services sector than in manufacturing activities

which tend to benefit most from the weakened value of the yen. The Business Condition

Leading Index calculated by Japan’s Cabinet Office also indicates that recovery has been

underway since December 2012.

Exhibit 2 — Diffusion Index of Business Conditions

Sources: The Bank of Japan, Japan’s Cabinet Office, Deutsche Asset & Wealth Management*As of April 2013

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

F

2014

F

2015

F

2016

F

Q1 Q2 Q3 Q4 annual growth

DB Forecast

consumption tax increase

Great Tohoku Earthquake aftermathglobal financial

crisis

dot.com bubble burst

-50

-25

0

25

50

67

80

93

106

119

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Business Condition Leading Index (LHS) Diffusion Index of Tankan Survey (RHS)

Diffusion Index of Business Conditions:('favourable' minus 'unfavourable', % points)

(2005=100)

dot.com bubble burst

global financial crisis

Consumption tax increase

*

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 3

Newly appointed BoJ governor Haruhiko Kuroda announced a change of direction in

monetary policy in April 2013. The BoJ now sets a clear inflation target of 2% within two

years—an unprecedented goal. Deutsche Bank economists forecast more moderate infla-

tion of less than 1% through 2015, although prices will indeed see brief, temporary spikes

of 2.5% in April 2014 and 2.0% in October 2015 due to the planned consumption tax in-

crease. The long term government bond yield is also expected to remain steadily below

1% in these periods.

The BoJ’s new monetary policy of “quantitative and qualitative monetary easing” sets a

number of specific goals, including:

- Doubling the size of the monetary base from JPY 135 trillion to JPY 270 trillion in

two years;

- Doubling the amount of the BoJ’s long-term government debt holdings in two years;

- Extending the average maturity of long-term government debt held by the BoJ from

the current three years to seven years, with monthly gross purchases of long-term

government debt of around JPY 7 trillion.

- Increasing the BoJ’s Exchange Traded Fund (ETF) holdings by JPY 1 trillion a year,

and J-REITs by JPY 30 billion a year.

Exhibit 3 — Forecast of Interest Rate and CPI

Notes: F = forecast, there is no guarantee rates forecasted will materialise. JGB = Japanese Government Bond. CPI = Consumer Price Index. Please refer to Important Notes (see end of report)

Sources: The Bank of Japan, Japan’s Cabinet Office, Deutsche Asset & Wealth Management

As of April 2013

-3

-2

-1

0

1

2

3

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

F

2014

F

2015

F

2016

F

Call Rate (overnight) 10y JGB CPI(%)

DB Forecast

Consumption Tax hike in April 2014

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 4

Capital Market

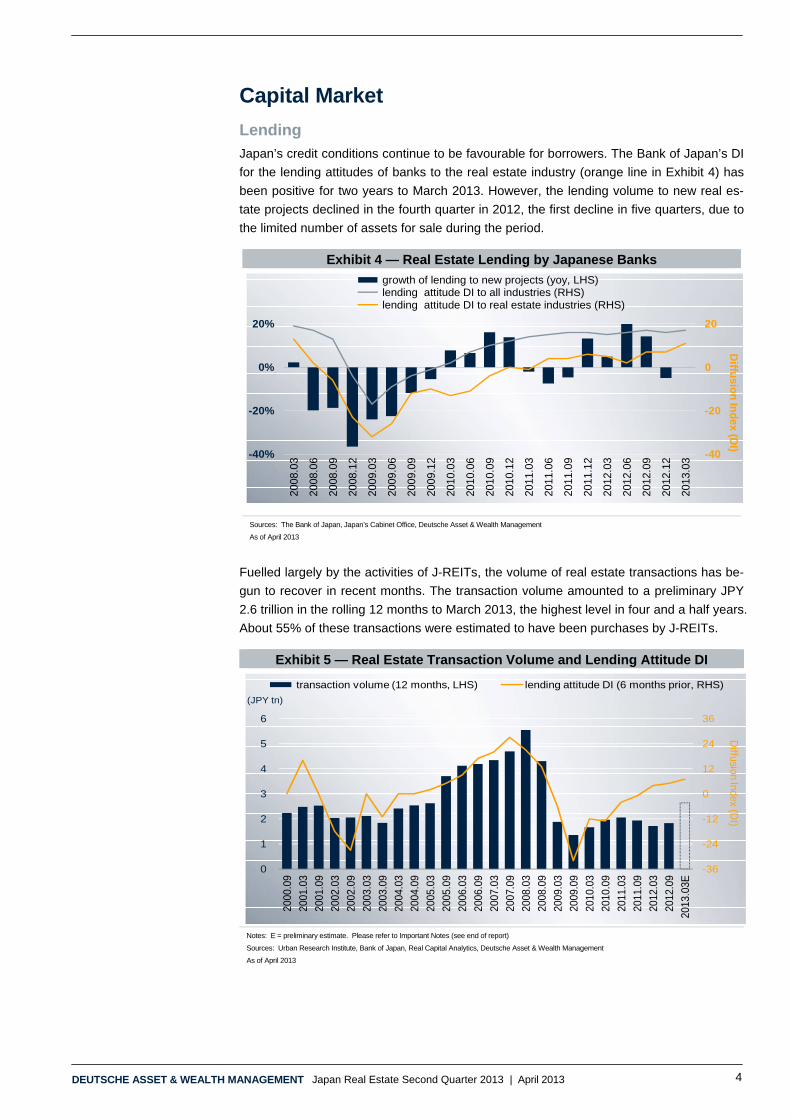

Lending

Japan’s credit conditions continue to be favourable for borrowers. The Bank of Japan’s DI

for the lending attitudes of banks to the real estate industry (orange line in Exhibit 4) has

been positive for two years to March 2013. However, the lending volume to new real es-

tate projects declined in the fourth quarter in 2012, the first decline in five quarters, due to

the limited number of assets for sale during the period.

Exhibit 4 — Real Estate Lending by Japanese Banks

Sources: The Bank of Japan, Japan’s Cabinet Office, Deutsche Asset & Wealth Management

As of April 2013

Fuelled largely by the activities of J-REITs, the volume of real estate transactions has be-

gun to recover in recent months. The transaction volume amounted to a preliminary JPY

2.6 trillion in the rolling 12 months to March 2013, the highest level in four and a half years.

About 55% of these transactions were estimated to have been purchases by J-REITs.

Exhibit 5 — Real Estate Transaction Volume and Lending Attitude DI

Notes: E = preliminary estimate. Please refer to Important Notes (see end of report)

Sources: Urban Research Institute, Bank of Japan, Real Capital Analytics, Deutsche Asset & Wealth Management

As of April 2013

-40

-20

0

20

-40%

-20%

0%

20%

2008

.03

2008

.06

2008

.09

2008

.12

2009

.03

2009

.06

2009

.09

2009

.12

2010

.03

2010

.06

2010

.09

2010

.12

2011

.03

2011

.06

2011

.09

2011

.12

2012

.03

2012

.06

2012

.09

2012

.12

2013

.03

growth of lending to new projects (yoy, LHS)lending attitude DI to all industries (RHS)lending attitude DI to real estate industries (RHS)

Diffu

sion

Ind

ex (DI)

-36

-24

-12

0

12

24

36

0

1

2

3

4

5

6

2000

.09

2001

.03

2001

.09

2002

.03

2002

.09

2003

.03

2003

.09

2004

.03

2004

.09

2005

.03

2005

.09

2006

.03

2006

.09

2007

.03

2007

.09

2008

.03

2008

.09

2009

.03

2009

.09

2010

.03

2010

.09

2011

.03

2011

.09

2012

.03

2012

.09

2013

.03E

transaction volume (12 months, LHS) lending attitude DI (6 months prior, RHS)

(JPY tn)

Diffusion Index (D

I)

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 5

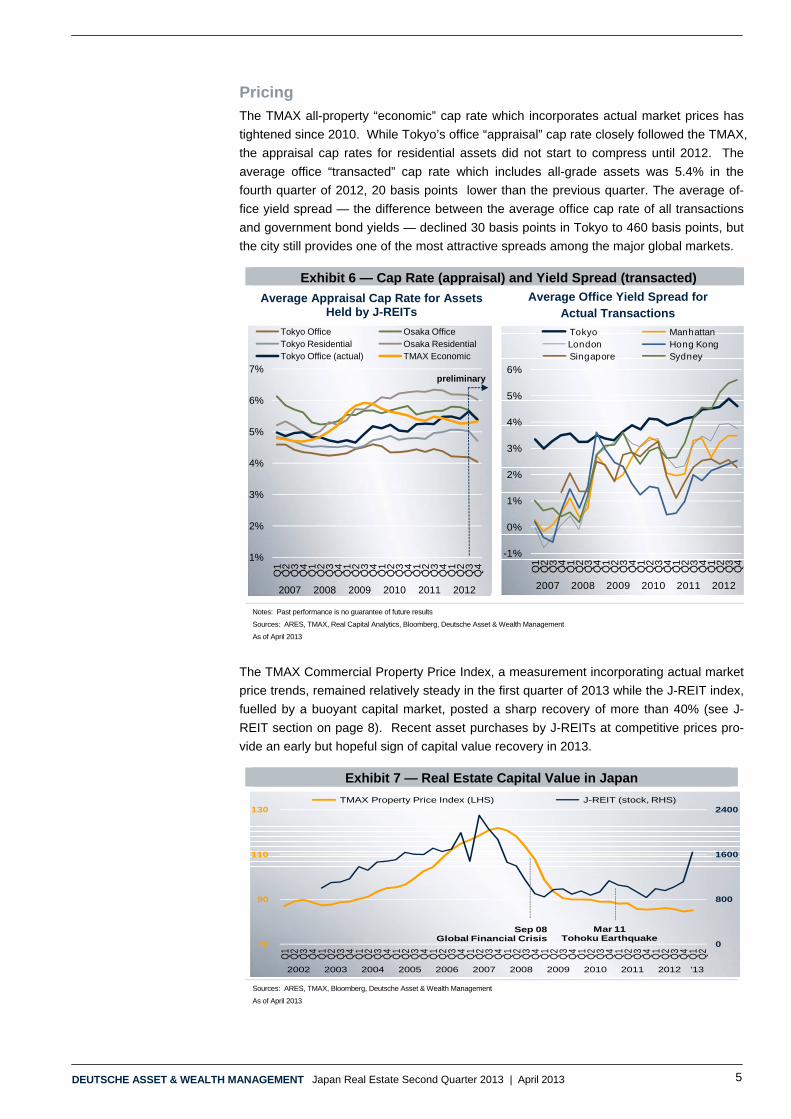

Pricing

The TMAX all-property “economic” cap rate which incorporates actual market prices has

tightened since 2010. While Tokyo’s office “appraisal” cap rate closely followed the TMAX,

the appraisal cap rates for residential assets did not start to compress until 2012. The

average office “transacted” cap rate which includes all-grade assets was 5.4% in the

fourth quarter of 2012, 20 basis points lower than the previous quarter. The average of-

fice yield spread — the difference between the average office cap rate of all transactions

and government bond yields — declined 30 basis points in Tokyo to 460 basis points, but

the city still provides one of the most attractive spreads among the major global markets.

Exhibit 6 — Cap Rate (appraisal) and Yield Spread (transacted)

Average Appraisal Cap Rate for Assets Held by J-REITs

Average Office Yield Spread for Actual Transactions

Notes: Past performance is no guarantee of future results

Sources: ARES, TMAX, Real Capital Analytics, Bloomberg, Deutsche Asset & Wealth Management

As of April 2013

The TMAX Commercial Property Price Index, a measurement incorporating actual market

price trends, remained relatively steady in the first quarter of 2013 while the J-REIT index,

fuelled by a buoyant capital market, posted a sharp recovery of more than 40% (see J-

REIT section on page 8). Recent asset purchases by J-REITs at competitive prices pro-

vide an early but hopeful sign of capital value recovery in 2013.

Exhibit 7 — Real Estate Capital Value in Japan

Sources: ARES, TMAX, Bloomberg, Deutsche Asset & Wealth Management

As of April 2013

1%

2%

3%

4%

5%

6%

7%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2007 2008 2009 2010 2011 2012

Tokyo Office Osaka OfficeTokyo Residential Osaka ResidentialTokyo Office (actual) TMAX Economic

preliminary

-1%

0%

1%

2%

3%

4%

5%

6%

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2007 2008 2009 2010 2011 2012

Tokyo ManhattanLondon Hong KongSingapore Sydney

0

800

1600

2400

70

90

110

130

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 '13

TMAX Property Price Index (LHS) J-REIT (stock, RHS)

Sep 08Global Financial Crisis

Mar 11Tohoku Earthquake

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 6

Transactions

The number of major real estate transactions (either completed or announced) increased

since the beginning of 2013, especially in the office sector, and J-REITs dominated the list

of buyers. The prices of some of the deals were very competitive, with cap rates near or

even below 4%. It was symbolic that troubled Japanese electronics giants such as Sony

and Panasonic sold their office buildings in Central Tokyo to J-REITs and other firms in

order to slim down the balance sheets.

Exhibit 8 — Major Transactions in the First Quarter 2013

Notes: Non-office deals, assets outside Tokyo, and acquisitions by foreign managers are highlighted in gray. This table is prepared solely for information purposes and not intended to recommend or endorse any specific company's shares or other products.

Sources: Real Capital Analytics, Nikkei Real Estate Market Report, Deutsche Asset & Wealth Management

As of April 2013

Tokyo’s volume of commercial real estate transactions for the rolling 12-month period

ending in March was US$22.4 billion, almost the same amount as the previous 12-month

run. Tokyo ranked fourth among global cities in transaction volume over the past 12

months and first among cities in the Asia Pacific region. About 55% of these transactions

were by J-REITs in Tokyo, according to our own estimate.

JPY1 billion = US$10 million

Month Type AssetPrice(JPY

billion)

Unit price(JPY m/sqm)

Caprates

Pre-fecture

Acquired byInvestor

origin

Sep-12 office KUDAN PLAZA BUILDING - - - Tokyo Goldman Sachs USNov-12 office Tokyo Panasonic Building 2 - - - Tokyo Mitsubishi Estate Japan

Nov-12 retail Shinsaibashi GATE - - - Osaka MetLife Alico US

Dec-12 office Toyokawa Bldg - - - Tokyo Goldman Sachs USDec-12 office Tokyo Panasonic Building 3 - - - Tokyo Nomura Real Estate JapanDec-12 office Navi Shibuya V - - - Tokyo Goldman Sachs USDec-12 retail NORBESA - - - Hokkaido Oaktree Capital US

Jan-13office /

residentialOnarimon M-SQUARE 14 0.88 - Tokyo Mitsui Soko Japan

Feb-13 retail Ikebukuro Square 20 1.71 6.8% Tokyo Frontier Real Estate (REIT) JapanFeb-13 dev. site Morinaga & Co Tsukaguchi facto 12 0.14 - Hyogo Haseko Corporation Japan

Feb-13 residentialIris Nihonbashi Suitengu etc(3 properties)

18 0.56 5.3%Tokyo,

KanagawaNippon AccommodationsFund (REIT)

Japan

Feb-13 officePart of Atago Green Hills andARK Mori Building

20 1.42 4.7% Tokyo Mori Hills REIT Japan

Feb-13 office Part of GranTokyo South Tower 35 3.21 - Tokyo Mitsui Fudosan JapanFeb-13 hotel Hyatt Regency Kyoto - - - Kyoto ORIX Real Estate JapanFeb-13 M&A Brighton Hotels - - - Chiba, Kyoto Oriental Land Japan

Feb-13 office Sony City Osaki 111 0.90 4.3% TokyoNippon Building Fund (REIT,60%), Domestic Investor (40%)

Japan

Mar-13 retail Fukuoka PARCO 27 1.09 - Fukuoka PARCO Japan

Mar-13 retail / hotelYodobashi-Kichijouji etc(4 properties)

28 0.74 5.2%Tokyo, Chiba

and AichiUnited Urban (REIT) Japan

Mar-13 office Shibuya Garden Front (50%) 12 1.40 4.3% Tokyo Nippon Building Fund (REIT) Japan

Mar-13 officePanasonic Tokyo ShiodomeBldg

51 1.11 4.3% TokyoSumitomo Mitsui Financeand Leasing (90%), NipponBuilding Fund (REIT, 10%)

Japan

Mar-13 residentialApartments in Nagoya city(4 properties)

5 - - AichiJV of Sparinvest PropertyInvestors and Idera Capital

Denmark

Mar-13 retail / landORE Yurakucho etc(4 properties)

33 2.31 4.1%Kanagawa,

Tokyo, OsakaORIX REIT Japan

Mar-13 landGround of Tokyo PanasonicBuilding 1

- - - Tokyo Sumitomo Realty Japan

Mar-13 office / retailPart of Hankyu NishinomiyaGardens, Hankyu Railway HQs

29 0.44 6.0% Hyogo, Osaka Hankyu REIT Japan

Mar-13 retail HEP FIVE 17 1.18 4.5% Osaka Hankyu Realty JapanMar-13 retail NU chayamachi 14 0.91 3.7% Osaka Hankyu Railway Japan

Mar-13 office Shinjuku Sanchome Bldg - - - TokyoJV of AXA Real Estate andSumitomo Mitsui Trust RealEstate Investment

France/Japan

Mar-13 residential Cosmos Kokura Eki Mae 1 0.22 6.5% Fukuoka Saizen REIT SingaporeApr-13 hotel Hilton Tokyo Bay 26 0.40 6.1% Chiba Japan Hotel REIT Japan

Apr-13 residentialLieto court Kinshicho,Lieto court Oshima

14 - - TokyoJV of Sekisui House andSpring Investment

Japan

May-13 residentialApartments in Tokyo(12 properties)

15 0.48 5.4% Tokyo Sekisui House SI (REIT) Japan

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 7

Exhibit 9.1 — Real Estate Transaction Volume by City (12 months to Mar 2013)

Notes: Commercial real estate transactions exclude non-income producing assets, such as development site transactions

Sources: Real Capital Analytics, Deutsche Asset & Wealth Management

As of April 2013

Exhibit 9.2 shows commercial real estate transaction volumes by property sector in Japan.

With J-REITs among the leading buyers, office transactions recovered to post the highest

volume in nine quarters.

Exhibit 9.2 — Quarterly Real Estate Transaction Volumes by Sector in Japan

Notes: Commercial real estate transactions exclude non-income producing assets, such as development site transactions

Sources: Real Capital Analytics, Deutsche Asset & Wealth Management

As of April 2013

0 5 10 15 20 25 30 35 40 45

NYC Metro

London Metro

LA Metro

SF Metro

DC Metro

Hong Kong

Paris

Chicago

Singapore

Sydney

Seoul

Shanghai

Taipei

Guangzhou

Beijing

Office Retail Apartment Industrial Hotel

Tokyo

($bn)

othersJ-REITs

Osaka

-120%

-60%

0%

60%

120%

180%

240%

300%

$(8)

$(4)

$-

$4

$8

$12

$16

$20

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

'07 '08 '09 '10 '11 '12 '13

land/other

hotel

industrial

residential

retail

office

growth % (yoy)

(bn)

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 8

Performance

IPD reported that the average annual total return for unlevered direct real estate invest-

ment in Japan held at a preliminary 3.8% in December 2012 (the latest period available).

While this represents the same return level as the previous quarter, we expect a moderate

recovery in the capital value return to materialise during 2013. Among the major property

sectors, office returns lagged in 2012 due to the recent supply surge and the relatively

weak leasing market during the year. Beginning with this edition of Japan Real Estate,

returns in the industrial sector are now included in Exhibit 10 due to the growing interest of

investors in industrial assets as well as the increasing maturity of the sector itself.

Exhibit 10 — Real Estate Total Returns in Japan (unlevered) Total Return by Component Total Return by Sector

Notes: There is a time lag because of raw data being collected through semi-annual reports. Past performance is not indicative of future results

Sources: IPD Japan Monthly Indicator, Deutsche Asset & Wealth Management

As of April 2013

J-REITs

J-REITs have recently emerged as the hottest sector in Japanese capital markets. The J-

REIT index skyrocketed from 1,115 points at the end of December 2012 to 1,643 points at

the end of March 2013, a 47% increase in just three months. This represents a record

high since the global credit crisis, and it reflects a strong belief among investors in the

possibility of inflation. The BoJ’s announced goal is to keep purchasing J-REITs continu-

ously at a pace of JPY 30 billion each year (see page 3). The concern, however, is that

rents have not yet started to recover for average-class assets (see Exhibit 18).

-15%

-10%

-5%

0%

5%

10%

15%

2003

2005

2007

2008

.06

2008

.12

2009

.06

2009

.12

2010

.06

2010

.12

2011

.06

2011

.12

2012

.06

2012

.12

Total Return Income Return

Capital Growth

preliminary

-15%

-10%

-5%

0%

5%

10%

15%

20

03

20

05

20

07

20

08.0

6

20

08.1

2

20

09.0

6

20

09.1

2

20

10.0

6

20

10.1

2

20

11.0

6

20

11.1

2

20

12.0

6

20

12.1

2

Office Retail

Residential Industrial

preliminary

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 9

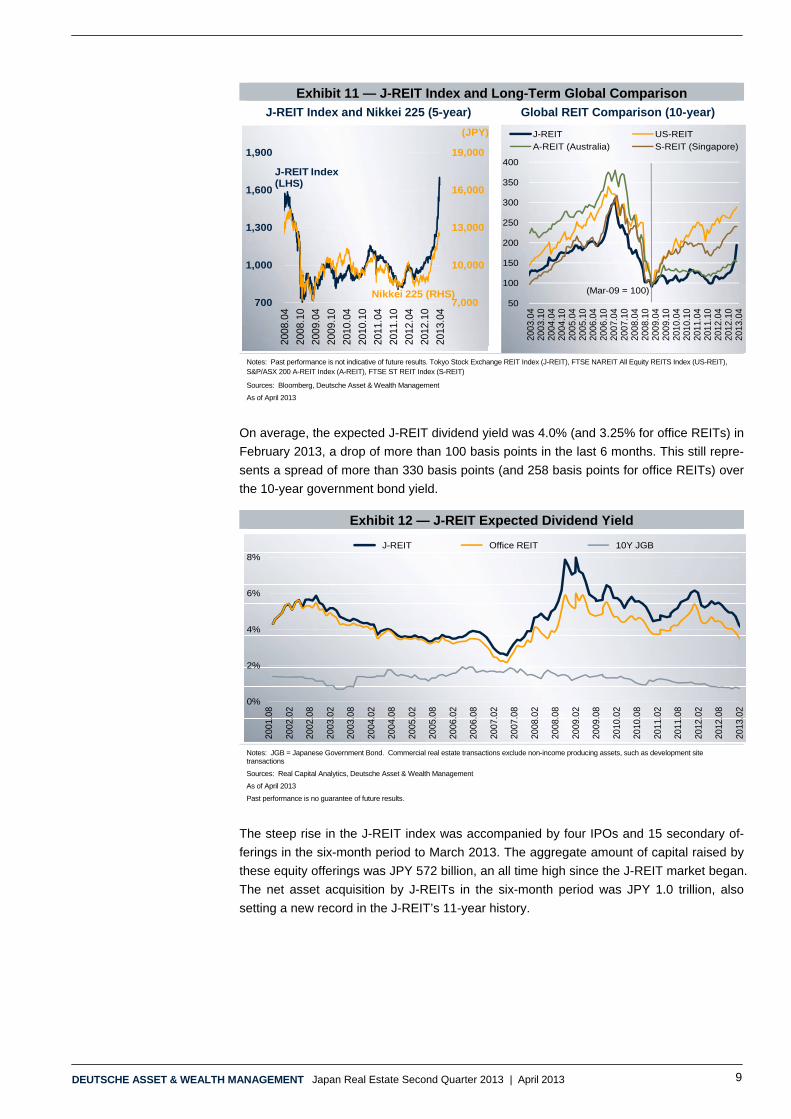

Exhibit 11 — J-REIT Index and Long-Term Global Comparison J-REIT Index and Nikkei 225 (5-year) Global REIT Comparison (10-year)

Notes: Past performance is not indicative of future results. Tokyo Stock Exchange REIT Index (J-REIT), FTSE NAREIT All Equity REITS Index (US-REIT), S&P/ASX 200 A-REIT Index (A-REIT), FTSE ST REIT Index (S-REIT)

Sources: Bloomberg, Deutsche Asset & Wealth Management

As of April 2013

On average, the expected J-REIT dividend yield was 4.0% (and 3.25% for office REITs) in

February 2013, a drop of more than 100 basis points in the last 6 months. This still repre-

sents a spread of more than 330 basis points (and 258 basis points for office REITs) over

the 10-year government bond yield.

Exhibit 12 — J-REIT Expected Dividend Yield

Notes: JGB = Japanese Government Bond. Commercial real estate transactions exclude non-income producing assets, such as development site transactions

Sources: Real Capital Analytics, Deutsche Asset & Wealth Management

As of April 2013

Past performance is no guarantee of future results.

The steep rise in the J-REIT index was accompanied by four IPOs and 15 secondary of-

ferings in the six-month period to March 2013. The aggregate amount of capital raised by

these equity offerings was JPY 572 billion, an all time high since the J-REIT market began.

The net asset acquisition by J-REITs in the six-month period was JPY 1.0 trillion, also

setting a new record in the J-REIT’s 11-year history.

7,000

10,000

13,000

16,000

19,000

700

1,000

1,300

1,600

1,900

2008

.04

2008

.10

2009

.04

2009

.10

2010

.04

2010

.10

2011

.04

2011

.10

2012

.04

2012

.10

2013

.04

J-REIT Index (LHS)

Nikkei 225 (RHS)

(JPY)

50

100

150

200

250

300

350

400

2003

.04

2003

.10

2004

.04

2004

.10

2005

.04

2005

.10

2006

.04

2006

.10

2007

.04

2007

.10

2008

.04

2008

.10

2009

.04

2009

.10

2010

.04

2010

.10

2011

.04

2011

.10

2012

.04

2012

.10

2013

.04

J-REIT US-REIT

A-REIT (Australia) S-REIT (Singapore)

(Mar-09 = 100)

0%

2%

4%

6%

8%

2001

.08

2002

.02

2002

.08

2003

.02

2003

.08

2004

.02

2004

.08

2005

.02

2005

.08

2006

.02

2006

.08

2007

.02

2007

.08

2008

.02

2008

.08

2009

.02

2009

.08

2010

.02

2010

.08

2011

.02

2011

.08

2012

.02

2012

.08

2013

.02

J-REIT Office REIT 10Y JGB

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 10

Exhibit 13 — Capital Raising and Transactions by REITs in Japan

Notes: Commercial real estate transactions exclude non-income producing assets, such as development site transactions

Sources: Real Capital Analytics, Deutsche Asset & Wealth Management

As of April 2013

The preliminary volume of commercial real estate transactions in Japan in the six months

to March 2013 was JPY 1.8 trillion, the highest six-month total in 5 years and more than

double the increase from the previous six months. It is estimated that about 60% of trans-

actions were acquired by J-REITs in the period.

Exhibit 14 — Real Estate Transactions in Japan and J-REIT Share

Notes: E = preliminary estimate. Commercial real estate transactions exclude non-income producing assets, such as development site transactions

Sources: Real Capital Analytics, Deutsche Asset & Wealth Management

As of April 2013

Major Public Offerings (JPY bn)Name of REIT Month Amount

Nippon Building Fund Jan-13 68

Advance Residence Jan-13 22

Nippon Accommodations Fund Feb-13 22

Frontier REIT Feb-13 17

United Urban Feb-13 23

ORIX REIT Mar-13 19

Initial Public Offerings

Daiwa House REIT Nov-12 52

GLP REIT Dec-12 102

Comforia Residential Feb-13 10

Nippon Prologis REIT Feb-13 97

Planned: Aeon, Hulic, Shinsei Bank, Hoshino resort

0.0

0.5

1.0

2001.0

92002.0

32002.0

92003.0

32003.0

92004.0

32004.0

92005.0

32005.0

92006.0

32006.0

92007.0

32007.0

92008.0

32008.0

92009.0

32009.0

92010.0

32010.0

92011.0

32011.0

92012.0

32012.0

92013.0

3

Bond3rd Party AllotmentPublic Of feringIPO

JPY tn

net acquisition by J-REITs

-15%

5%

25%

45%

65%

-1

0

1

2

3

200

0.0

9

200

1.0

3

200

1.0

9

200

2.0

3

200

2.0

9

200

3.0

3

200

3.0

9

200

4.0

3

200

4.0

9

200

5.0

3

200

5.0

9

200

6.0

3

200

6.0

9

200

7.0

3

200

7.0

9

200

8.0

3

200

8.0

9

200

9.0

3

200

9.0

9

201

0.0

3

201

0.0

9

201

1.0

3

201

1.0

9

201

2.0

3

201

2.0

9

201

3.0

3E

acquisition by othersacquisition by J-REITs disposition by J-REITs

(JPY tn)

J-REIT share (%) of all transactions (RHS)

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 11

Market Fundamentals

Office

The amount of new office supply in Tokyo peaked in 2012, and the office vacancy rate in

the central five wards has since begun to recover. The average office vacancy rate was

8.6% in February 2013, an improvement from the recent cyclical peak of 9.4% in June

2012. The vacancy rate for newly developed buildings also declined to 24.0% in February

2013, down from 39.2% in May 2012. Among the central five wards, Shibuya had the

tightest submarket with a vacancy rate of 6.0% in February 2013.

Exhibit 15 — Office Vacancy Rate in Central Tokyo (5 wards)

Notes: GFA = gross floor area. sqm = square metres

Sources: Miki Shoji, Deutsche Asset & Wealth Management

As of April 2013

Between December 2012 and February 2013, the vacancy rate in Tokyo declined across

all categories of floor plate sizes. For larger assets with a floor plate size of more than 200

tsubos (660 square metres), the vacancy rate dropped from 6.6% to 5.8% in the period

while it declined only marginally from 11.5% to 11.4% for the smallest category of assets,

i.e., floor plates of 50-100 tsubos (165-330 square metres).

0 %

10 %

20 %

30 %

40 %

0 %

5 %

10 %

15 %

20 %

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Feb-

13

all buildings (LHS) new buildings (RHS)

newly d

eveloped

build

ings

Vac

ancy

rat

e fo

r al

l bui

ldin

gs

Building Date FloorsGFA

(sqm)

Mar-12 10 East 39,025May-12 21 South 190,000

JP Tower May-12 38 213,323Ark Hills Sengokuyama Mori Tower Aug-12 47 143,720

Sep-12 31 North 110,000Sep-12 35 South 132,500

WATERRAS TOWER Feb-13 41 129,223New Kabuki-za Theater Building Feb-13 29 94,097Kyobashi 3-1 Project Mar-13 24 117,025Ochanomizu Sola City Mar-13 23 102,179

ARK Hills south tower Jun-13 20 55,061

Nakano Central Park

Otemachi Financial City

Major Office Supply in Tokyo

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 12

Exhibit 16 — Office Vacancy Rate in Central Tokyo by Building Floor Plate

Notes: sqm = square metres

Sources: Sanko Estate, Deutsche Asset & Wealth Management

As of April 2013

Office rental growth rates correlate inversely to the vacancy rate. Historically in Tokyo,

office rents start to increase when the vacancy rate falls below 5%. The vacancy rate for

buildings with floor plates of 200 tsubos (660 square meters) or more was 5.8% in Tokyo

in February 2013, and a level that is just above the pivotal 5% threshold.

Exhibit 17 — Vacancy Rate and Rent Growth in Tokyo (floor plate > 660 sqm)

*The tsubo is a traditional measure of floor area in Japan. It is equivalent to 3.3 square metres (35.6 square feet)

Sources: Miki Shoji, Sanko Estate, Deutsche Asset & Wealth Management

As of April 2013

Just as the decline began for Tokyo’s office vacancy rate, signs arose of a possible re-

covery in office rents, especially rents for high quality buildings. The average rent for

newly-built offices in Tokyo grew 9.2% in the two months to February 2013, the fastest

pace of growth in more than five years. The all-class average rent softened slightly during

the same period, but only by -0.2%. Given the above-average vacancy rate, we still ex-

pect the marginal declining trend to persist for all-class average rents at least until sum-

mer 2013, but it is becoming increasingly likely that rents will stabilise by the end of the

year.

0%

4%

8%

12%

1996

.08

1997

.02

1997

.08

1998

.02

1998

.08

1999

.02

1999

.08

2000

.02

2000

.08

2001

.02

2001

.08

2002

.02

2002

.08

2003

.02

2003

.08

2004

.02

2004

.08

2005

.02

2005

.08

2006

.02

2006

.08

2007

.02

2007

.08

2008

.02

2008

.08

2009

.02

2009

.08

2010

.02

2010

.08

2011

.02

2011

.08

2012

.02

2012

.08

2013

.02

floor plate : 165 sqm - 330sqm floor plate : 330 sqm - 660 sqmfloor plate > 660 sqm average

1%

3%

5%

7%

9%

11%-12%

-8%

-4%

0%

4%

8%

199

5.02

199

6.02

199

7.02

199

8.02

199

9.02

200

0.02

200

1.02

200

2.02

200

3.02

200

4.02

200

5.02

200

6.02

200

7.02

200

8.02

200

9.02

201

0.02

201

1.02

201

2.02

201

3.02

Actual Rent Growth (QoQ, 3Q rolling avg.) Vacancy Rate (RHS)

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 13

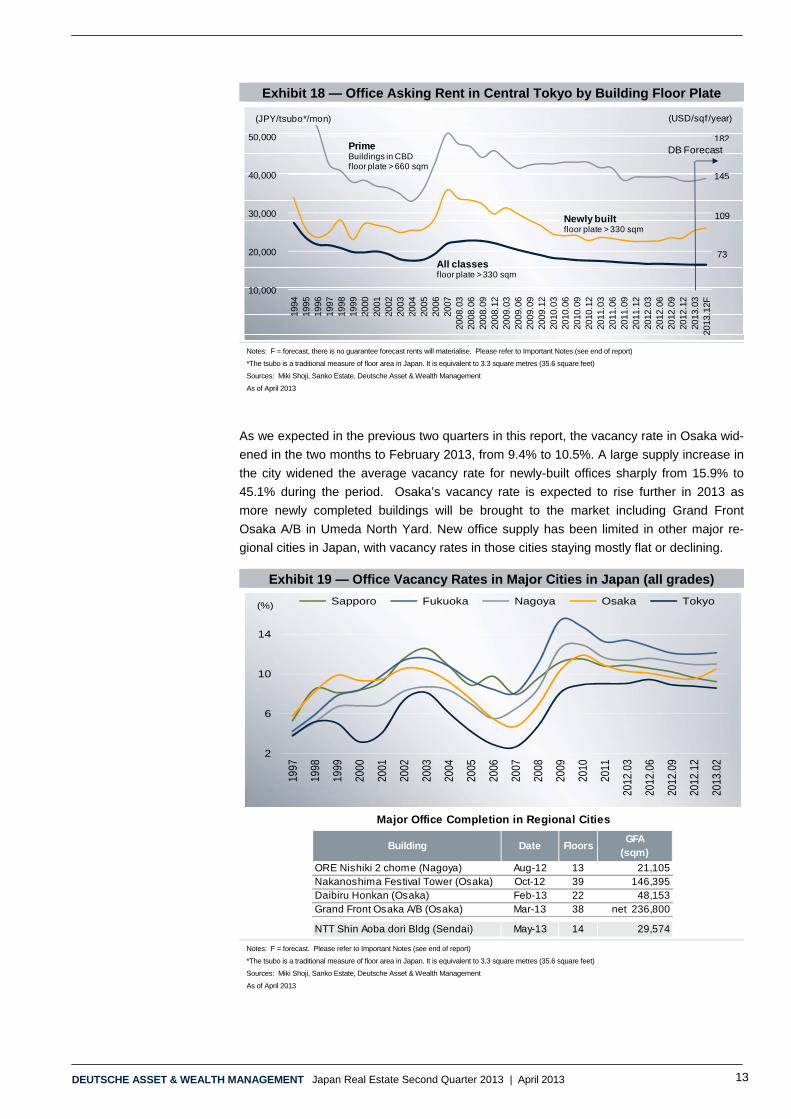

Exhibit 18 — Office Asking Rent in Central Tokyo by Building Floor Plate

Notes: F = forecast, there is no guarantee forecast rents will materialise. Please refer to Important Notes (see end of report)

*The tsubo is a traditional measure of floor area in Japan. It is equivalent to 3.3 square metres (35.6 square feet)

Sources: Miki Shoji, Sanko Estate, Deutsche Asset & Wealth Management

As of April 2013

As we expected in the previous two quarters in this report, the vacancy rate in Osaka wid-

ened in the two months to February 2013, from 9.4% to 10.5%. A large supply increase in

the city widened the average vacancy rate for newly-built offices sharply from 15.9% to

45.1% during the period. Osaka’s vacancy rate is expected to rise further in 2013 as

more newly completed buildings will be brought to the market including Grand Front

Osaka A/B in Umeda North Yard. New office supply has been limited in other major re-

gional cities in Japan, with vacancy rates in those cities staying mostly flat or declining.

Exhibit 19 — Office Vacancy Rates in Major Cities in Japan (all grades)

Notes: F = forecast. Please refer to Important Notes (see end of report)

*The tsubo is a traditional measure of floor area in Japan. It is equivalent to 3.3 square metres (35.6 square feet)

Sources: Miki Shoji, Sanko Estate, Deutsche Asset & Wealth Management

As of April 2013

10,000

20,000

30,000

40,000

50,000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

.03

2008

.06

2008

.09

2008

.12

2009

.03

2009

.06

2009

.09

2009

.12

2010

.03

2010

.06

2010

.09

2010

.12

2011

.03

2011

.06

2011

.09

2011

.12

2012

.03

2012

.06

2012

.09

2012

.12

2013

.03

2013

.12F

(JPY/tsubo*/mon) (USD/sqf/year)

109

182

145

73

Prime Buildings in CBDfloor plate > 660 sqm

All classesfloor plate > 330 sqm

Newly builtfloor plate > 330 sqm

DB Forecast

2

6

10

14

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

.03

2012

.06

2012

.09

2012

.12

2013

.02

Sapporo Fukuoka Nagoya Osaka Tokyo(%)

Building Date FloorsGFA

(sqm)

ORE Nishiki 2 chome (Nagoya) Aug-12 13 21,105Nakanoshima Festival Tower (Osaka) Oct-12 39 146,395Daibiru Honkan (Osaka) Feb-13 22 48,153Grand Front Osaka A/B (Osaka) Mar-13 38 net 236,800

NTT Shin Aoba dori Bldg (Sendai) May-13 14 29,574

Major Office Completion in Regional Cities

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 14

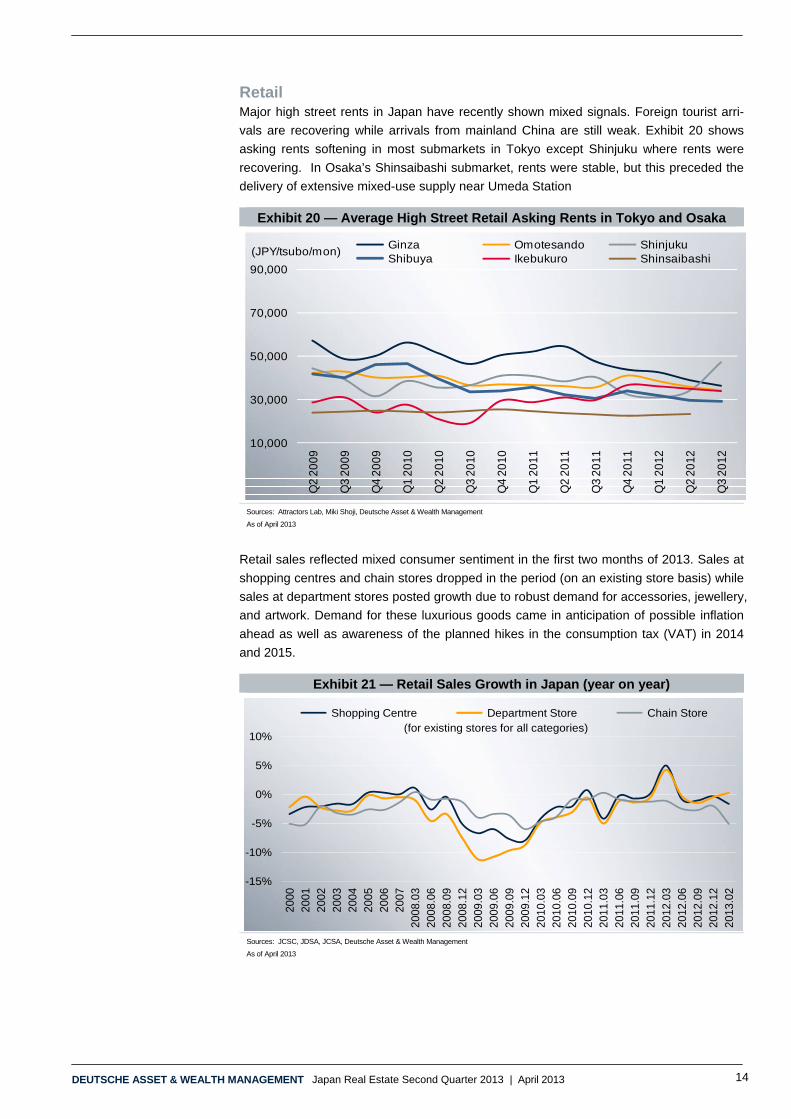

Retail Major high street rents in Japan have recently shown mixed signals. Foreign tourist arri-

vals are recovering while arrivals from mainland China are still weak. Exhibit 20 shows

asking rents softening in most submarkets in Tokyo except Shinjuku where rents were

recovering. In Osaka’s Shinsaibashi submarket, rents were stable, but this preceded the

delivery of extensive mixed-use supply near Umeda Station

Exhibit 20 — Average High Street Retail Asking Rents in Tokyo and Osaka

Sources: Attractors Lab, Miki Shoji, Deutsche Asset & Wealth Management

As of April 2013

Retail sales reflected mixed consumer sentiment in the first two months of 2013. Sales at

shopping centres and chain stores dropped in the period (on an existing store basis) while

sales at department stores posted growth due to robust demand for accessories, jewellery,

and artwork. Demand for these luxurious goods came in anticipation of possible inflation

ahead as well as awareness of the planned hikes in the consumption tax (VAT) in 2014

and 2015.

Exhibit 21 — Retail Sales Growth in Japan (year on year)

Sources: JCSC, JDSA, JCSA, Deutsche Asset & Wealth Management

As of April 2013

10,000

30,000

50,000

70,000

90,000

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Ginza Omotesando ShinjukuShibuya Ikebukuro Shinsaibashi

(JPY/tsubo/mon)

-15%

-10%

-5%

0%

5%

10%

2000

2001

2002

2003

2004

2005

2006

2007

2008

.03

2008

.06

2008

.09

2008

.12

2009

.03

2009

.06

2009

.09

2009

.12

2010

.03

2010

.06

2010

.09

2010

.12

2011

.03

2011

.06

2011

.09

2011

.12

2012

.03

2012

.06

2012

.09

2012

.12

2013

.02

Shopping Centre Department Store Chain Store(for existing stores for all categories)

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 15

Residential

The average sales price per unit for newly-built for-sale condos in Greater Tokyo in the

first two months in 2013 declined 3.4% to JPY 44.3 million from the previous period. Sea-

sonal price softening is typical in the first two months of the year (although Exhibit 22 be-

low does not show prices broken out for either January or February of previous years).

The contract rate1 (orange line in Exhibit 22) also softened to 74.2% in the period, still

above the pivotal 70% threshold which is associated with healthy market conditions. We

expect the average sales price to rise again in the latter half of 2013 due to the current

buoyant economic sentiment and also because of our expectation that the housing tax

credit will be expanded in April 2014.2

Exhibit 22 — New Condo Unit Price and Contract Rate in Greater Tokyo

Sources: REEI, Deutsche Asset & Wealth Management

As of April 2013

Limited development of new residential rental units in Tokyo in the last two years kept the

vacancy rate on a recovering trend. It improved to 9.99% in January 2013 in the 23-ward

area (orange line in Exhibit 22), putting it below 10% for the first time in more than three

years. Asking rents showed corresponding year-on-year growth of 1.4% in the central five-

ward area in February 2013 (dark blue bar), marking 12 months of consecutive growth.

Rents were flat in the broader 23-ward area of Tokyo (gray bar) in the same period.

Exhibit 23 — Residential Rent and Vacancy in Tokyo

Notes: The tsubo is a traditional measure of floor area in Japan. It is equivalent to 3.3 square metres (35.6 square feet)

Sources: TAS Corporation with data sourced from At Home Co. Ltd. (23-ward vacancy), Leasing Management Consulting (5-ward asking rent), IPD-RECRUIT Residential Index (23-ward rent index)

As of April 2013

1 The contract rate is the ratio of units contracted (sold) to the number of units delivered for sale. 2 Please refer to the research topic of the previous edition of this report, Japan Real Estate Quarterly First Quarter 2013.

50

60

70

80

35

40

45

50

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

.03

2007

.06

2007

.09

2007

.12

2008

.03

2008

.06

2008

.09

2008

.12

2009

.03

2009

.06

2009

.09

2009

.12

2010

.03

2010

.06

2010

.09

2010

.12

2011

.03

2011

.06

2011

.09

2011

.12

2012

.03

2012

.06

2012

.09

2012

.12

2013

.02

Avg. unit price (LHS) Contract rate (RHS)

(JPY mn/unit) (%)

7

8

9

10

11

13,100

13,500

13,900

14,300

14,700

2005

.03

2005

.12

2006

.09

2007

.06

2008

.03

2008

.12

2009

.09

2010

.02

2010

.05

2010

.08

2010

.11

2011

.02

2011

.05

2011

.08

2011

.11

2012

.02

2012

.05

2012

.08

2012

.11

2013

.02

23 ward Rent Index5 ward Asking Rent

(JPY/tsubo) (%)(Index)

103

106

109

100

97

23 ward Vacancy (RHS)

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 16

The high-end residential market correlates closely with the office leasing market. This

high-end segment of the market is strongly affected by business conditions of the corpo-

rate sector, especially financial services. The vacancy rate of high-end apartments in To-

kyo rose from 7.9% in the third quarter to 8.6% in the fourth quarter of 2012, while aver-

age rents rose 1.6% from the previous quarter. It was the second consecutive quarter of

rising rents. The rental market for the high-end residential units appears to have stabilised,

but a robust recovery may take some time. Demand draws significantly from financial ser-

vices workers, and this segment of the labour market has not yet begun to recover.

Exhibit 24 — High-end Residential Rent and Vacancy Rate in Tokyo

Sources: Ken Real Estate Investment Advisors Ltd., Miki Shoji, Deutsche Asset & Wealth Management

As of April 2013

Industrial

Due to a combination of limited supply and healthy demand for quality spaces, the leasing

market for multi-tenant logistics assets remained very tight in the fourth quarter of 2012,

with 2.2% vacancy in Greater Tokyo and 1.5% in Greater Osaka, respectively, according

to Ichigo Real Estate Service. With a number of new completions scheduled in 2013,

however, the vacancy rate is expected to increase moderately in the medium term in both

cities.

Rents declined 0.5% in Tokyo and 0.6% in Osaka respectively in the fourth quarter of

2012 while the demand outlook remains positive for the rest of 2013, with rents expected

to hold broadly steady in the period.

0

3

6

9

12

15

7,000

10,000

13,000

16,000

19,000

22,000

25,000 19

99

2000

2001

2002

2003

2004

2005

2006

2007

2008

.03

2008

.06

2008

.09

2008

.12

2009

.03

2009

.06

2009

.09

2009

.12

2010

.03

2010

.06

2010

.09

2010

.12

2011

.03

2011

.06

2011

.09

2011

.12

2012

.03

2012

.06

2012

.09

2012

.12

2013

.03

office rent high end residential rent

office vacancy high end residential vacancy(Yen/tsubo/month) (%)

QuarterlyAnnually

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 17

Exhibit 25 — Logistic Leasing Market in Greater Tokyo and Greater Osaka Vacancy Rate of Multi-tenant Logistics Logistics Rent

Notes: F = forecast, there is no guarantee forecast returns will materialise. Past performance is not indicative of future results. Tokyo Stock Exchange REIT Index (J-REIT), FTSE NAREIT All Equity REITS Index (US-REIT), S&P/ASX 200 A-REIT Index (A-REIT), FTSE ST REIT Index (S-REIT)

Sources: Bloomberg, Deutsche Asset & Wealth Management

As of April 2013

0%

5%

10%

15%

20%

20

08

.06

20

08

.12

20

09

.06

20

09

.12

20

10

.06

20

10

.12

20

11

.06

20

11

.12

20

12

.06

20

12

.12

20

13

.12F

Greater Tokyo Greater Osaka

forecast by Ichigo

1,000

2,000

3,000

4,000

5,000

2008

.06

2008

.12

2009

.06

2009

.12

2010

.06

2010

.12

2011

.06

2011

.12

2012

.06

2012

.12

2013

.12F

Greater Tokyo

Greater Osaka (JPY/tsubo/month)

forecast by Ichigo

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 18

Past Issues

Vol Year

1 Q2 Jun-08 Making sense of the rental market in Japan

2 Q3 Sep-08 Impact of the credit crunch

3 Q4 Dec-08 Revitalisation of ailing J-REITs

4 Q1 Mar-09 Tokyo office market in its global context

5 Q2 Jul-09 Japan residential market

6 Q3 Oct-09History repeats itself? A comparison of the ‘Year 2003 Problem’ with 2009

7 Q4 Jan-10 Introducing unit pricing analysis in Japan

8 Q1 Apr-10 Portfolio optimisation analysis in Japan

9 Q2 Jul-10 Japan’s capital market in a global context

10 Q3 Oct-10 Quarterly Report

11 Q4 Jan-11 Cross-border investment into and out of Japan

12 Q1 Apr-11The Great Tohoku Earthquake and its impact on the Japanese real estate market

13 Q2 Jul-11 Adapting Japan’s land price index for real estate analysis

14 Q3 Oct-11 Quarterly Report

15 Q1 Jan-12 The J-REITs next 10 years

16 Q2 Apr-12 Quarterly Report

17 Q3 Jul-12 Quarterly Report

18 Q4 Oct-12The inward-looking focus of the real estate investors in Japan

19 Q1 Jan-13 Can the housing tax credit boost demand?

20 Q2 Apr-13 Quarterly Report

2011

2012

2013

Publication Research Topic

2008

2009

2010

DEUTSCHE ASSET & WEALTH MANAGEMENT Japan Real Estate Second Quarter 2013 | April 2013 19

Important Notes © 2013. All rights reserved. This has been issued and approved by Deutsche Asset & Wealth Manage-ment represents the asset management and wealth management activities conducted by Deutsche Bank AG or any of its subsidiaries. Deutsche Asset & Wealth Management’s real estate investment business is part of the Alternatives and Real Assets platform. In the US, Deutsche Asset & Wealth Management re-lates to the asset management activities of RREEF America L.L.C.; in Germany: RREEF Investment GmbH, RREEF Management GmbH, and RREEF Spezial Invest GmbH; in Australia: Deutsche Asset Management (Australia) Limited (ABN 63 116 232 154) Australian financial services license holder; in Ja-pan: Deutsche Securities Inc.*; in Hong Kong: Deutsche Bank Aktiengesellschaft, Hong Kong Branch (for direct real estate business), and Deutsche Asset Management Hong Kong (for real estate securities busi-ness), in Singapore, Deutsche Asset Management (Asia) Limited (Company Reg. No. 198701485N) and in the United Kingdom, Deutsche Alternative Asset Management (UK) Limited, Deutsche Alternative Asset Management (Global) Limited, and Deutsche Asset Management (UK) Limited; in Italy: RREEF Fondim-mobiliari SGR S.p.A; and in Denmark, Finland, Norway and Sweden: Deutsche Alternative Asset Manage-ment (UK) Ltd and Deutsche Alternative Asset Management (Global) Ltd; in addition to other regional enti-ties in the Deutsche Bank Group (*) For DSI, financial advisory (not investment advisory) and distribution services only.

Key Deutsche Asset & Wealth Management research personnel are voting members of various investment committees. Members of the investment committees vote with respect to underlying investments and/or transactions and certain other matters subjected to a vote of such investment committee. Additionally, research personnel receive, and may in the future receive incentive compensation based on the perform-ance of a certain investment accounts and investment vehicles managed by Deutsche Asset & Wealth Management and its affiliates.

This material was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. It is intended for informational purposes only. It does not constitute investment advice, a recommendation, an offer, solicitation, the basis for any contract to purchase or sell any security or other instrument, or for Deutsche Bank AG or its affiliates to enter into or arrange any type of transaction as a consequence of any information contained herein. Neither Deutsche Bank AG nor any of its affiliates gives any warranty as to the accuracy, reliability or completeness of information which is contained in this document. Except insofar as liability under any statute cannot be excluded, no member of the Deutsche Bank Group, the Issuer or any officer, employee or associate of them accepts any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this document or for any resulting loss or damage whether direct, indirect, consequential or otherwise suffered by the recipi-ent of this document or any other person.

The views expressed in this document constitute Deutsche Bank AG or its affiliates’ judgment at the time of issue and are subject to change. This document is only for professional investors. This document was prepared without regard to the specific objectives, financial situation or needs of any particular person who may receive it. No further distribution is allowed without prior written consent of the Issuer.

An investment in real estate involves a high degree of risk, including possible loss of principal amount in-vested, and is suitable only for sophisticated investors who can bear such losses. The value of shares/ units and their derived income may fall or rise. Any forecasts provided herein are based upon Deutsche Asset & Wealth Management’s opinion of the market at this date and are subject to change dependent on the market. Past performance or any prediction, projection or forecast on the economy or markets is not indicative of future performance.

The forecasts provided are based upon our opinion of the market as at this date and are subject to change, dependent on future changes in the market. Any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets is not necessarily indicative of the future or likely performance.

I-031300-1.0

www.rreef.com

I-031300-1.1

Global Research Team Global

Mark Roberts Head of Research & Strategy [email protected]

Americas

Ross Adams Industrial Specialist [email protected] Bill Hersler Office Specialist [email protected] Ana Leon Property Market Research [email protected] Andrew J. Nelson Retail & Sustainability Specialist [email protected] Jaimala Patel Quantitative Strategy [email protected]

Alexander Makarovski Performance & Risk Analysis [email protected] Alex Symes Economic & Quantitative Analysis [email protected] Brooks Wells Apartment Specialist [email protected] Jay Wengang Performance & Risk Analysis [email protected]

Europe

Simon Durkin Head of Research & Strategy, Europe [email protected] Jaroslaw Morawski Property Market Research [email protected]

Maren Vaeth Property Market Research [email protected] Simon Wallace Property Market Research [email protected]

Asia Pacific

Leslie Chua Head of Research & Strategy, Asia Pacific ex-Japan & Korea [email protected] Koichiro Obu Head of Research & Strategy, Japan & Korea [email protected]

Minxuan Hu Property Market Research [email protected] Natasha Lee Property Market Research [email protected]

Office Locations:

Chicago 875 North Michigan Avenue 41st Floor Chicago IL 60611-1901 United States Tel: +1 312 266 9300 Frankfurt Mainzer Landstraße 178-190 60327 Frankfurt am Main Germany Tel: +49 69 71909 0 London One Appold Street London EC2A 2UU United Kingdom Tel: +44 20 754 58000 New York 345 Park Avenue 24th Floor New York NY 10154-0102 United States Tel: +1 212 454 6260 San Francisco 101 California Street 26th Floor San Francisco CA 94111 United States Tel: +1 415 781 3300 Singapore One Raffles Quay South Tower Singapore 048583 Tel: +65 6538 7011 Tokyo Floor 17 Sanno Park Tower 2-11-1 Nagata-cho Chiyoda-Ku Tokyo Japan Tel: +81 3 5156 6000