jeffrey d. hiatt - the new england graduate...

TRANSCRIPT

6/14/2017

1

Cost Segregation Studies,

Tangible Property Regulations,

PATH Act, Depreciation,

& More

© MS Consultants, LLC 2017

Updates - June 2017

Jeffrey D. HiattHeads the New England office

87 Lafayette Rd.

Suite 11

Hampton Falls, NH 03844

Toll Free: 888.989.0054

Phone: 508.878.4846

Fax: 603.926.2811

Jeffrey D. Hiatt• Has been affiliated with MS Consultants, LLC since 1999

• Helped MS Consultants become leading provider of Cost Segregation Studies in the Northeast

• Developed and fostered relationships with individual clients, accounting firms and Societies.

• Organized and run a practice helping Commercial property owners reduce expenses on all types of commercial properties.

• Jeff once had the lead in his High School Musical production of Beauty and the Beast – which one was he?

© MS Consultants, LLC 2017

6/14/2017

2

David A. FabianDirector, MS Consultants LLC

Office: 716‐633‐9840Cell : 716‐573‐9378Fax : 716‐633‐9469

© MS Consultants, LLC 2017

David A. Fabian• 25+ years’ tax and accounting experience

• Joined MS Consultants in 1999

• Personally involved in over 10,000 Cost Segregation projects in more than 30 states

• Presented on a variety of topics including depreciation & cost segregation, energy modeling, tangible property regs, & more

• Developed comprehensive in-house training and quality control programs

© MS Consultants, LLC 2017

MS Consultants, LLC• We’re made up of tax, construction, and engineering professionals.

• Years of experience:

– Cost Segregation Studies since 1996

– §179D certifications since 2006

– §45L certification since 2008

– Tangible Property Regulation analyses since 2008

– DeMinimis Studies beginning in 2015© MS Consultants, LLC 2017

6/14/2017

3

Our ServicesWith recent changes in the tax code including the extension and expansion of bonus depreciation and §179 expensing elections there has never been a better time to have a cost segregation study completed. In addition, new laws enacted by Congress and regulations issued by the Internal Revenue Service now enable taxpayers to take further tax advantage of their real estate holdings. At MS Consultants, LLC we refer to it as & More.

1-Cost Segregation Studies (CSS)

• Internal Revenue Service (IRS) approved methodology to properly classify assets into 5,7,15, 27.5 and 39 year depreciable lives

• Taxpayers may go back as far as 1987 to claim any missed depreciation (No amended returns are required)

• MS Consultants has completed over 12,000 studies since 1996

In 2015 a CSS was completed on a $3,000,000 retail plaza (originally placed in service in 2010) and resulted in additional depreciation of over $450,000 in 2015.

• Identify assets eligible for an immediate write off. IRS rules now allow for the immediate expensing of expenditures typically under $2,500 per unit of property (UOP)

• The de minimis safe harbor is an elective provision that requires guidance in invoice preparation and knowledge of unit of properties and building systems

An $800,000 hotel renovation was completed in 2015. A de minimis study resulted in over $500,000 eligible for expensing in 2015.

2-De Minimis Studies

6/14/2017

4

3-Fixed Asset Studies (FAS)

• For assets abandoned or physically removed from a building, the IRS now allows taxpayers to write‐off the remaining net tax value of the asset typically resulting in a large tax deduction

• Opportunities to expense current year expenditures for roofs, windows, HVAC and other structural components as a result of the IRS Tangible Property Regulations (TPR)

A $4,000,000 renovation of retail plaza was completed in 2015 (originally placed in service in 2002). The study resulted in expensing over $600,000 of removed assets. In addition, approximately $400,000 of the 2015 expenditures were deemed to be repairs under the TPR and were expensed in 2015.

• Up to $1.80 per square foot tax deduction for increasing the energy efficiency of HVAC, lighting, and building envelope that meet prescribed energy use reduction standards established by the IRS

• Architects, designers and engineering firms can receive tax deduction for providing services to a government owned building

A 90,000 square foot office building was constructed in 2013. The project met the energy use reduction standards resulting in a $162,000 tax deduction in 2013.

4-§179D Energy Efficient Commercial Building Tax Deduction

5-§45L Energy Efficient Home Credit (Great for Apartments)

• Up to a $2,000 tax credit per dwelling unit that meets prescribed energy use reduction standards established by the IRS

• Includes apartment buildings, adult care facilities, single and multi‐family residences

A 120 unit garden style apartment complex was constructed in 2014. The project met the prescribed energy use reduction standards resulting in $240,000 of tax credits in 2014

6/14/2017

5

6-§1031 Exchange Tax Planning (We are not an intermediary)

• Opportunity to complete a CSS and FAS on a building before it is sold and the election is made to complete a §1031 Exchange. Typically results in tax deduction prior to sale

• This will increase the gain on sale but the gain is being deferred anyway as a result of the §1031 Exchange

MS Consultants performed a CSS in 2015 on an office building (originally placed in service in 2003) sold (exchanged) in 2016 resulting in a 2015 tax deduction of $400,000.

MS Consultants, LLC

• Cost Segregation Studies

© MS Consultants, LLC 2017

What is a cost segregation study?

• IRS approved method to accelerate depreciation of specific assets

• Allocates a portion of “39 and 27.5 year” property into 5, 7, and 15 year property

• IRS Tax codes §1245 and §1250

© MS Consultants, LLC 2017

6/14/2017

6

We perform cost segregation studies because…

Taxpayers under-depreciate their assets.

© MS Consultants, LLC 2017

Why?• Rules are very complex

• Properly segregating a property is a complex process, requiring the right combination of know‐how:

o Tax expertise and familiarity with prior tax litigation

o Engineering and construction knowledge

© MS Consultants, LLC 2017

Sample Study

Client purchases a building for $5,000,000 in 2008, and has taken depreciation over 39 years.

© MS Consultants, LLC 2017

6/14/2017

7

Example: Medium-Size Office Building

© MS Consultants, LLC 2017

Example:Office Building - Acquisition

100,000500,000750,000

3,650,000

$325,950 $763,369 $437,419$258,710

$258,710

$366,266

$5,000,000

Example:Office Building – New Construction

100,000500,000750,000

3,650,000

$325,950 $1,175,656 $849,706$426,381

$426,381

$446,653

$5,000,000

6/14/2017

8

Real Property: 27.5 or 39 Year(Structural Components)

• HVAC units

• Ceramic tile floors

• Exterior doors

• Windows

• Interior plumbing

• Siding

• Concrete flatwork & foundations

• Roof© MS Consultants, LLC 2017

HVAC Units

Ceramic Tile

SidingConcrete flatwork

& foundations

Exterior Doors & Windows

Roofs

Interior Plumbing

Where does the money come from?

© MS Consultants, LLC 2017

15-year Property(Land Improvements)

• Removable site improvements

• Certain Site utilities & drainage

• Fencing & gates

• Recreational equipment

• Signs & decoration

• & More

© MS Consultants, LLC 2017

6/14/2017

9

Where does the money come from?

Paving

Sidewalks, Stepsand Curbing

Retaining Walls

Site Lighting

Trees, Landscapingand Irrigation

Grid Striping andPavement Symbols

Flagpoles

Benches and otherOutdoor equipment

15-year PropertyLand Improvements

& More

© MS Consultants, LLC 2017

Other 5- & 7-year Property(Personal Property)

• Specialty plumbing & electric

• Decorative wall coverings

• Carpet and other removable flooring

• Decorative lighting

• Trim, cabinetry & millwork

• Window treatments

• & More

© MS Consultants, LLC 2017

Where does the money come from?

Decorative Trim

Decorative andaccent lighting

Window Treatments

Decorative wood panels, wallpaperAnd other wallcoverings

Specialty electricand plumbing

Carpet andremovable flooring

5-year Property–Personal Property

& Much, Much More

© MS Consultants, LLC 2017

6/14/2017

10

Where does the money come from?… a look inside our very own conference room

• Carpet

• Wallpaper

• Decorative Lighting…• Audio/ Visual Electronics…

• Trim & Millwork

• … the wiring and hookups for all special equipment that you can’t see!

• & More…

What are the benefits of Cost Segregation Studies?

‐ Increased depreciation in earlier years, less taxes = more cash flow

‐ Permanent savings when buildings are sold (capital gains vs. ordinary deduction)

‐ Allows for future write‐offs when structural components are replaced

© MS Consultants, LLC 2017

What are the benefits of Cost Segregation Studies, cont?

‐ No amended return for catch‐up depreciation ‐ Savings taken all in one year‐ Taxpayers receive an extra 30% ‐ 100% on “non‐real estate” assets (for assets acquired after 9/11/01)

© MS Consultants, LLC 2017

6/14/2017

11

Things to consider• Profitability

• Impact of alternative minimum tax

• Early disposition

• Passive loss limitations

• Estate planning

• Intent to demolish (95‐27)

• Impact of 1031 Exchange

How much can be reclassified?

Average Hotels Office buildings Apartments Medical office buildings Shopping plazas Manufacturing facilities Restaurants

20 – 30%12 – 30%20 – 35%15 – 32%20 – 38%20 – 45%15 – 40%

What buildings are eligible?

• New buildings under construction

• Existing buildings undergoing renovation

• Purchases of existing properties

• Buildings purchased or constructed since 1987

• Inherited buildings

© MS Consultants, LLC 2017

6/14/2017

12

Types of Cost Segregation Studies Performed

Airport Hangars Apartment Buildings Automobile Dealerships Automobile Service

Centers Banks Casual & Fine Dining

Restaurants Daycare Centers Department Stores Distribution Centers

Fast Food (Quick Service) Restaurants

Fitness Centers Flex Industrial Gas Stations Golf Resorts Grocery Stores Healthcare Centers High Rise Buildings Hospitals Hotels

Laboratory Facilities Manufacturing &

Processing Facilities Marinas Nursing Homes Office Buildings Retail Plazas Senior Assisted

Living Facilities Truck Terminals Warehouses ALL BUILDINGS

MS Consultants, LLC

Tangible Property Regulations

© MS Consultants, LLC 2017

TPR - Lessons Learned

• Taxpayers willing to pay for services

• Many taxpayers took advantage of opportunities for large tax savings

• But some taxpayers and practitioners ignored the rules (only 500k‐600k 3115’s filed)

• Most of the provisions in the TPR’s can be utilized in 2015, 2016, and forward

6/14/2017

13

TPR Takeaways

• Rev‐Proc 2015‐20 still applies going forward

• Annual elections under the TPR’s can still be made

• Knowing what makes up Unit of Property (UOP) is key element going forward

• Change #21 – expensing of demolition costs ‐can only apply going forward beginning in 2015 ‐ no retroactive application

© MS Consultants, LLC 2017

TPR Takeaways

• Improperly capitalized repairs can still be expensed ‐ Change #184

• Replaced structural components can still be written off ‐ Change #205

• Only change #196 ‐ late partial asset disposition is gone for good

© MS Consultants, LLC 2017

4 Newer Items to Consider for 2016

• Rev‐Proc‐2015‐56: Safe harbor for betterment, restoration and adaptation tests

• New de minimis amount‐Notice 2015‐82

• New Form 3115 Application for Change in Accounting method

• Qualified Improvement Property

© MS Consultants, LLC 2017

6/14/2017

14

Rev Proc 2015-56

• Safe Harbor provided for remodeling costs for Retail and Restaurant operations

• If Qualified taxpayer chooses this option, Form 3115 will be required (Automatic Method Change)

• Write off 75% of remodeling costs as expense

• Capitalize 25% of costs

• Specifically excludes offices, apartments, automobile dealerships, gas stations, and more

© MS Consultants, LLC 2016

Rev-Proc. 2015-56 con’t • Won’t be used often because…….

– Only taxpayers who have Applicable Financial Statements (i.e. audits) can use this approach. Reviewed, Compiled or tax return only clients will not be able to utilize the rev‐proc.

– This is an accounting method change that applies to all costs. Taxpayers cannot choose which remodeling costs to apply this approach to.

– There are approximately thirty (30!) exceptions and/or changes a taxpayer will need to consider in order to use this Safe Harbor.

– For example, if a taxpayer decides to follow this approach, they are required to make a late General Asset Account (GAA) election for the original building and all improvements. Because of rules regarding GAA, these taxpayers will no longer be able to take a partial disposition on their buildings (for example you will not be able to write off your old roof when you capitalize your new roof),

– May have to reverse prior year partial dispositions.

© MS Consultants, LLC 2017

3115 Updates

• File one signed original with timely filed return• Send one signed original to Kentucky (previously was Utah)

• Affirmative statement that you are eligible to file automatic changes

• 12 spaces for concurrent designated change numbers (previously was one line)

• New instructions caution not to rely only on the instructions, must go to website to determine if there has been any newly published guidance

© MS Consultants, LLC 2016

6/14/2017

15

3115 Filing’s-Cant do after 2014

• #196 – Late Partial Asset Disposition (PAD)

– #205 Structural Write‐off’s might apply

– #206 – Non‐structural write‐off’s might apply

• # 21 – Removal costs

– Can’t do retroactive

– Can do in current year and going forward

© MS Consultants, LLC 2017

Common 3115 filings applicable for 2015and beyond

• They are automatic if assigned a method number – also no filing fee

• Fix bonus election problems and cost segs (CHANGE #7)

• Write‐off prior improperly capitalized repairs (CHANGE #184)

• Write‐off replaced structural components currently being depreciated (CHANGE #205)

© MS Consultants, LLC 2016

Common 3115 filings applicable for 2015and beyond

• Write‐off replaced non‐structural components currently being depreciated (CHANGE #206)

• Write‐off prior or future removal costs associated with an improvement (CHANGE #21)

© MS Consultants, LLC 2017

6/14/2017

16

Other Takeaways for 2016• Annual elections under the TPR’s can still be made

• Some change #’s are gone for good such as #196 and retroactive change #21.

• Many change #’s are can still be utilized

• Taxpayers can still take advantage of disposition rules

• New de minimis limits create enormous tax savings opportunities

• Unit of Property(UOP) and Capitalization Standards knowledge critical in taking advantage of TPR.

© MS Consultants, LLC 2016

Common annual elections under the new rules

• De minimis Safe Harbor‐attach DMSH statement

• Small Business Safe Harbor‐attach SHST statement

• Partial asset disposition‐in year of replacement‐Form 4797‐Section 1‐filling out Form is considered an election

• Election to capitalize M&S and depreciate‐just do it

• Election to capitalize R&M and depreciate‐just do it

• WE RECOMMEND FILING 1‐3 FOR ALL TAXPAYERS

© MS Consultants, LLC 2017

De Minimis Applies to All of These

Rules for Materials and Supplies

Repairs and maintenance

General Rules for capital expenditure

Rules for amounts paid for the acquisitions or production of tangible property

Rules for amounts paid for the improvement of tangible property

De minimis rules

© MS Consultants, LLC 2017

6/14/2017

17

De minimis Expensing Rule-1.263(a)-1(f)

– Definition:

– Useful life less than 12 months» OR

– Property costing less than certain dollar amount» AND

– Must be expensed on books/financial statements

© MS Consultants, LLC 2017

De minimis Expensing Rule-1.263(a)-1(f)

• 3 Threshholds:

–Applicable Financial Statements‐(AFS)‐$5,000

–No written policy, if consistently applied ‐$2,500 (raised from $500)

–Do nothing ‐$200

© MS Consultants, LLC 2017

De minimis Expensing Rule-1.263(a)-1(f)

• A taxpayer can elect to apply the de minimis rule in one year and not the next

• The de minimis safe harbor is elected annually by including a statement on the taxpayer’s tax return (including extensions) for the year elected

© MS Consultants, LLC 2017

6/14/2017

18

De minimis Expensing Rule-1.263(a)-1(f)

• Basic de minimis rules

– New safe harbor determined at invoice item level.

– A taxpayer may rely on de minimis safe harbor only if the amount paid for property does not exceed $2,500 per invoice, or per item as substantiated by the invoice. Limit is $5,000 if AFS applies

© MS Consultants, LLC 2017

De minimis Expensing Rule-1.263(a)-1(f)

• The de minimis safe harbor does not preclude a taxpayer from reaching an agreement with the IRS that the IRS examining agents will not review certain items‐same as Temporary regs

• Must apply same treatment to books and tax return

© MS Consultants, LLC 2017

De minimis Expensing Rule-1.263(a)-1(f)

• A taxpayer is not required to include in the cost of the property the additional costs if these costs are not included on the same invoice as the tangible property

• However, a taxpayer electing the de minimis must include in the cost of the property all additional costs (for example, delivery fees, installation services, or similar costs) of acquiring or producing the property if these costs are included on the same invoice with the tangible property

© MS Consultants, LLC 2017

6/14/2017

19

De minimis Expensing Rule-1.263(a)-1(f)

• Written Capitalization Policy

• For tax years beginning _________, and forward, (Name of Business) elects to treat as an expense for both book and income tax purposes property with a cost of $____________ or less, including items that have a useful life of 12 months or less. It is (Name of Business’s) intention that this election complies with the IRS Section 1.263(a)‐1(f) de minimis safe harbor election.

© MS Consultants, LLC 2017

Safe Harbor Election• Statement must be attached annually to a timely filed (including extensions) income tax return

• Statement must be titled “Section 1.263(a)‐1(f) de minimis safe harbor election” and contain the following information:– Taxpayer’s name

– Taxpayer’s address

– Taxpayer identification number

– Statement that the taxpayer is making the de minimis safe harbor election under Section 1.263(a)‐1(f)

© MS Consultants, LLC 2017

Project Cost Summary

© MS Consultants, LLC 2017

SAMPLE LLCHotel - TPR Analysis1 Sample AvenueSample, California

Site Concrete 15 - - - 57,549 - 57,549 Site Fencing & Gates 15 - - - 34,413 - 34,413 Landscape Planters 15 - - - 30,777 - 30,777 Roofing 39 - - 97,684 - - 97,684 Drop Ceilings (203 Rooms 39 - - 454,365 - - 454,365 Cermanic Tile Upgrade 39 - - 34,868 - - 34,868 Awnings & Sunscreens 5 - - - - 62,010 62,010 Breakfast Room Cabinets 5 - - - - 46,260 46,260 Reception Desk 5 - - - - 4,569 4,569 Kitchen Equipment 5 - - - - 16,772 16,772 Wireless Access Points 5 - - - - 38,710 38,710 Oracle Equipment 5 - - - - 7,995 7,995 De Minimis D 1,598,716 - - - - 1,598,716 General Repairs R - 355,060 - - - 355,060 Exercise Room Refresh R - 15,397 - - - 15,397 Restroom Room Refresh R - 6,366 - - - 6,366 Front Desk Area Refresh R - 13,528 - - - 13,528 Float Walls (203 Rooms) R - 269,100 - - - 269,100

1,598,716 659,450 586,917 122,738 176,316 3,144,136

50.85% 20.97% 18.67% 3.90% 5.61% 100%

Description Life DE MINIMIS EXPENSE

REPAIR EXPENSE 39 YEAR 15 YEAR 5 YEAR TOTAL

Totals

Percentages

6/14/2017

20

Tax tips

• Elect de minimis annually

• Have clients set up capitalization policies and include in permanent tax file

• Obtain separate invoices for shipping installation etc. to keep below thresholds

• Sales tax must be used in the computation.

© MS Consultants, LLC 2017

Unit of Property

• Determining the Unit of Property is very important when dealing with the new TPR’s

© MS Consultants, LLC 2017

Determining the Unit of Property (UOP)

• Building and its structural components are a single UOP

– The regulations define the building structure as the building (as defined in §1.48‐1(e)(1)) and its structural components (as defined in §1.48‐1(e)(2)) other than the components specifically enumerated as building systems.

© MS Consultants, LLC 2017

6/14/2017

21

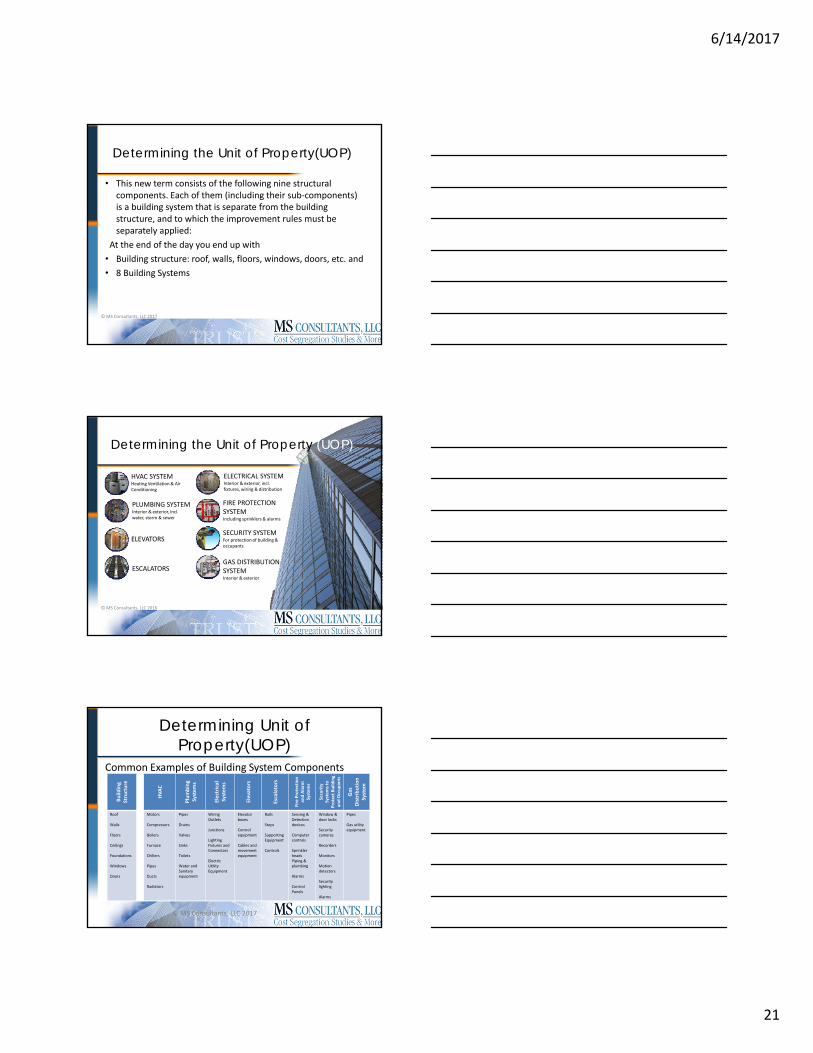

Determining the Unit of Property(UOP)

• This new term consists of the following nine structural components. Each of them (including their sub‐components) is a building system that is separate from the building structure, and to which the improvement rules must be separately applied:

At the end of the day you end up with

• Building structure: roof, walls, floors, windows, doors, etc. and

• 8 Building Systems

© MS Consultants, LLC 2017

Determining the Unit of Property (UOP)

HVAC SYSTEMHeating Ventilation & Air Conditioning

PLUMBING SYSTEMInterior & exterior, incl. water, storm & sewer

ELECTRICAL SYSTEMInterior & exterior, incl. fixtures, wiring & distribution

ESCALATORS

FIRE PROTECTION SYSTEMIncluding sprinklers & alarms

SECURITY SYSTEMFor protection of building & occupants

ELEVATORS

GAS DISTRIBUTION SYSTEMInterior & exterior

© MS Consultants, LLC 2016

Determining Unit of Property(UOP)

Common Examples of Building System Components

Building

Structure

HVAC

Plumbing

System

s

Electrical

System

s

Elevators

Escalators

Fire Protection

and Alarm

System

s

Security

System

s to

ProtectBuild

ing

and Occupants

Gas

Distribution

System

Roof

Walls

Floors

Ceilings

Foundations

Windows

Doors

Motors

Compressors

Boilers

Furnace

Chillers

Pipes

Ducts

Radiators

Pipes

Drains

Valves

Sinks

Toilets

Water and Sanitary equipment

Wiring Outlets

Junctions

Lighting Fixtures and Connectors

Electric Utility Equipment

Elevator boxes

Control equipment

Cables and movement equipment

Rails

Steps

Supporting Equipment

Controls

Sensing & Detectiondevices

Computer controls

Sprinkler headsPiping & plumbing

Alarms

Control Panels

Window & door locks

Security cameras

Recorders

Monitors

Motion detectors

Security lighting

Alarms

Pipes

Gas utility equipment

© MS Consultants, LLC 2017

6/14/2017

22

Determining the Unit of Property(UOP)

Real Property Expenditure UOP

Retail Store – Stand alone Store Refresh – Lighting replacement

Electrical System

Retail Store – Shoppingmall (leased space)

Store refresh – lighting replacement

Leased portion of building electrical system

Office – owned building Remove conference room wall

Building structure

Office – leased building Remove conference room wall

Building structure within leased space

Office condo HVAC unit replacement Leased portion of building HVAC system

Apartment building Single unit hear/air replacement

Building HVAC system

© MS Consultants, LLC 2017

Determining the Unit of Property(UOP)

• UOP for assets other than buildings. In general, for real or personal property that isn't classified as a building by the temp regs. all the components that are functionally interdependent comprise a single UOP. Components of property are functionally interdependent if the placing in service of one component by the taxpayer is dependent on the placing in service of the other component by the taxpayer.

© MS Consultants, LLC 2017

Determining the Unit of Property(UOP)

• UOP for Plant property.— Functional interdependence test is used to determine UOP

• Discreet and major function standard must be applied. (example ahead)

• Each machine is typically treated as it own UOP

• Applies to manufacturing, power generation, distribution and warehousing

© MS Consultants, LLC 2017

6/14/2017

23

Determining the Unit of Property for Plant Property

PLANT PROPERTY

SEPARATE INTODISCRETE & CRITICALFUNCTIONS = 7 UOPs!

- sorter - boiler- washer - dryer- ironer - folder- waste water treatment

system

Dispositions of Property• Taxpayer may file form 3115 for prior years for full asset

disposition (#205, #206).

• Taxpayer may dispose of partial asset in year of disposition (current year) on Form 4797.

• Simplified rules for writing off old assets– Cost Segregation – Specific Identification

– PPI computation

– Pro‐rata method

• GAA election is no longer necessary for buildings –however, can present an opportunity in the right situation

© MS Consultants, LLC 2017

Disposition Calculation #1• Taxpayer spends $100,000 in current year to replace a

10 year old roof

• PPI rates at acquisition date October 2004 = 152.0 and disposal date April 2016 = 202.0

• Doing the PPI rollback of $100,000 is calculated as follows:– $100,000 times 152.0 divided by 202.0 = $75,248

• Now reduce the accumulated depreciation from the newly recalculated basis:– $75,248 less $17,767 = ($57,481) recorded on Form 4797

6/14/2017

24

Disposition Calculation #2• Taxpayer spends $100,000 in current year to replace a 10 year old roof

• Building was built 10 years ago – Cost Segregation Study in year built

• Original cost of roof was $75,000 on AIA

• Starting point for write off is $97,500 (which includes proper allocation of indirect costs)– $97,500 less $23,021 = ($74,479) recorded on Form 4797

Disposition Calculation #3• Taxpayer spends $100,000 in current year to replace a 10 year old roof

• Building was built 10 years ago for $2M

• Taxpayer purchased building 5 yrs ago for $4M

• Cost Segregation Study in year of purchase allocates $195,000 to roof.

• Starting point for write off is $195,000– $195,000 less $22,712 = ($172,288) recorded on Form 4797

And don’t forget to file change #21

• Taxpayer spends $100,000 in current year to replace a 10 year old roof

• File Form 3115 change #21

• Change is automatic

• Have contractor breakout removal costs of old roof. (sometimes up to 25%)

• Obtain additional tax deduction

© MS Consultants, LLC 2017

6/14/2017

25

Disposition of Property

• Tenant & Landlord Dispositions

– Can a landlord take a partial disposition for a new roof paid for by the tenant?

• Yes, the landlord still has a disposition and may take a deduction for the adjusted basis in the roof replaced

• However, demolition costs incurred by the tenant must be capitalized since tenant has no disposition

Capitalization Standards thru 2013

You are required to capitalize expenditures that:

• 1) Materially increase the value of the PROPERTY

• 2) Substantially prolong the useful life of the PROPERTY, or

• 3) Adapt the PROPERTY to a new or different use

Excerpted from Reg. 1.263(a)‐1(b)

Current Capitalization Standards

You are required to capitalize expenditures that:

• 1) Materially increase the value of the PROPERTY

Betterment of the Unit of Property

• 2) Substantially prolong the useful life of the PROPERTY, or

• 3) Adapt the PROPERTY to a new or different use

6/14/2017

26

Current Capitalization Standards

You are required to capitalize expenditures that:

• 1) Betterment of the Unit of Property

• 2) Substantially prolong the useful life of the

PROPERTY, Restoration of the Unit of Propertyor

• 3) Adapt the PROPERTY to a new or different use

Current Capitalization Standards

You are required to capitalize expenditures that:

• 1) Betterment of the Unit of Property

• 2) Restoration of the Unit of Property or

• 3) Adapt the PROPERTY Unit of Property to a new or different use

Applying the Capitalization standards

BETTERMENT of the Unit of Property• 1‐ Ameliorate a material condition or defect that existed

prior to the acquisition of the property or arose during the production of the property;

• 2‐ Material addition to the unit of property (including the physical enlargement, expansion, or extension);

• 3‐ Material increase in the capacity, productivity, efficiency, strength, or quality of the unit of property or its output

© MS Consultants, LLC 2017

6/14/2017

27

Applying the Capitalization standards

BETTERMENT of the Unit of Property• 1‐ Ameliorate a material condition or defect that existed

prior to the acquisition of the property or arose during the production of the property.– Example 2: Taxpayer bought a store that had previously been used as a gas

station, located on land that had contained underground gasoline storage tanks. At the time of purchase, taxpayer did not know that the tanks had leaked, causing soil contamination. In 2012, taxpayer discovered the contamination and incurred costs to remediate the soil

• Result = Costs are CAPITALIZED (The remediation costs result in a betterment of the land, because the costs ameliorate a material condition or defect that existed prior to the taxpayer’s purchase of the land. Because there is a betterment, there is an improvement, and therefore is a capitalized cost.)

© MS Consultants, LLC 2017

Applying the Capitalization standards

BETTERMENT of the Unit of Property‐con’t

• 2‐ Material addition to the unit of property (including the physical enlargement, expansion, or extension);– Example 1: Taxpayer owns a 100,000 SF manufacturing building

that needed to extend the production area for their growing business. They construct a 30,000 SF addition.

– Result = Costs are CAPITALIZED (Betterment)

© MS Consultants, LLC 2017

Applying the Capitalization standards

BETTERMENT of the Unit of Property‐con’t

• 3‐ Material increase in the capacity, productivity, efficiency, strength, or quality of the unit of property or its output– Example 1: Taxpayer owns a factory building with a storage area

on the 2nd floor, they replace columns and girder supports to permit greater weight capacity in the area for new products.

– Result = Costs are CAPITALIZED (Betterment)

© MS Consultants, LLC 2017

6/14/2017

28

Applying the Capitalization standards

RESTORATION of the Unit of Property

• A taxpayer must capitalize amounts paid to restore a unit of property, including amounts paid in making good the exhaustion for which an allowance is or has been made.

© MS Consultants, LLC 2017

Applying the Capitalization standards

RESTORATION of the Unit of Property‐con’t• 1. Replacement of a component of a UOP and the taxpayer

has properly deducted a loss for that component;

• 2. Replacement of a component of a UOP and the taxpayer has properly taken into account the adjusted basis of the component in realizing gain or loss resulting from the sale or exchange of the component;

© MS Consultants, LLC 2017

Applying the Capitalization standards

RESTORATION of the Unit of Property‐con’t• 3. Repair of damage to a UOP for which the taxpayer has

properly taken into account the basis adjustment as a result of a casualty loss under Sec. 165 or relating to and event described in Sec. 165;‐different from old casualty rules

• 4. Returns the UOP to its ordinarily efficient operating condition if the property has deteriorated to a state of disrepair and was no longer functional for its intended use;

© MS Consultants, LLC 2016

6/14/2017

29

Applying the Capitalization standards

RESTORATION of the Unit of Property‐con’t

• 5. Results in the rebuilding of the UOP to a like‐new condition after the end of its asset class life;

• 6. Replacement of a major component or a substantial structural part of the UOP;

© MS Consultants, LLC 2017

Remodeling ExpendituresBuilding Refresh (ex. B6) – refresh the look and layout. In order to display the merchandise better, the Store

– Relocates lighting

– Moves one wall to accommodate displays

– Cleans and repairs flooring throughout the building

– Patches holes in the walls, replaces damaged ceiling tiles

– Repaints the interior & exterior for the new color scheme

– RESULT = Costs are expensed

© MS Consultants, LLC 2017

86

Remodeling ExpendituresBuilding Refresh; Limited Improvement (ex. B7) –refresh the look and layout, along with adding building addition for additional storage space and loading dock. In order to accomplish this, the store:

– All of the above, plus

– Add the storage space and loading dock

– Expand the electrical system for the new additionRESULT =

– Refresh costs are EXPENSED (not a Betterment)

– Building Addition costs are CAPITALIZED (Structural/Building system)

87

© MS Consultants, LLC 2017

6/14/2017

30

Remodeling ExpendituresBuilding Remodel (Ex. B8) – upgrade the look and layout to compete for a different type of customer. In order to accomplish this, the store:

– Replace flooring

– Replace large parts of exterior walls to insert windows

– Add a new all glass elevator

– Replace ceiling tiles with acoustic tiles

– Repaint the interior and exterior

– RESULT = Costs are capitalized© MS Consultants, LLC 2017

88

New Cap Standards

RESTORATION of the Unit of Property

EXAMPLE – Taxpayer replaces 3 HVAC Units out of 10 on top of their office building –

Do you need to Capitalize these costs?

Summary of Building Examples from the Final Regulations

REPAIR• 3/10 roof units (Ex. R18)

CAPITALIZE• One chiller HVAC (Ex. R17)

© MS Consultants, LLC 2017

6/14/2017

31

Summary of Building Examples from the Final Regulations

REPAIR• Roof membrane (Ex. B13)

• 3/10 roof units (Ex. R18)

• 30% electrical wiring (Ex. R21)

• 100/300 windows (Ex.R25)

• Floors in lobby (10%) (Ex. R28)

CAPITALIZE• Large portion of roof (Ex. R14)

• One chiller HVAC (Ex. R17)

• 100% electrical wiring (Ex. R20)

• 200/300 windows (Ex. R26)

• Floors in all public areas (40%) (Ex.R29)

33% seems to be the “unofficial” bright line - everything does not need to be capitalized. May have previously

capitalized items that now can be written off

© MS Consultants, LLC 2017

Parts of a Roofing System

Applying the Capitalization Standards

© MS Consultants, LLC 2017

6/14/2017

32

Ways to Save #3-Apply new TPR to current projects

© MS Consultants, LLC 2017

SAMPLE LLCHotel - TPR Analysis1 Sample AvenueSample, California

Site Concrete 15 - - - 57,549 - 57,549 Site Fencing & Gates 15 - - - 34,413 - 34,413 Landscape Planters 15 - - - 30,777 - 30,777 Roofing 39 - - 97,684 - - 97,684 Drop Ceilings (203 Rooms 39 - - 454,365 - - 454,365 Cermanic Tile Upgrade 39 - - 34,868 - - 34,868 Awnings & Sunscreens 5 - - - - 62,010 62,010 Breakfast Room Cabinets 5 - - - - 46,260 46,260 Reception Desk 5 - - - - 4,569 4,569 Kitchen Equipment 5 - - - - 16,772 16,772 Wireless Access Points 5 - - - - 38,710 38,710 Oracle Equipment 5 - - - - 7,995 7,995 De Minimis D 1,598,716 - - - - 1,598,716 General Repairs R - 355,060 - - - 355,060 Exercise Room Refresh R - 15,397 - - - 15,397 Restroom Room Refresh R - 6,366 - - - 6,366 Front Desk Area Refresh R - 13,528 - - - 13,528 Float Walls (203 Rooms) R - 269,100 - - - 269,100

1,598,716 659,450 586,917 122,738 176,316 3,144,136

50.85% 20.97% 18.67% 3.90% 5.61% 100%

Description Life DE MINIMIS EXPENSE

REPAIR EXPENSE 39 YEAR 15 YEAR 5 YEAR TOTAL

Totals

Percentages

9 Things to Think About

• If a TP expends costs in consideration of capitalization issues, the TP will go through the following “filters”

1. De minimis application (will not be on depreciation schedule)2. Are the costs indirect or removal and not capital in nature? 3. Are the costs M&S?4. Are they safe harbor for small taxpayers?5. Are they routine maintenance costs?6. Are they betterments, improvements, adaptions, restorations?

If not, they are R&M7. If the above do allow a 162, does the taxpayer elect to

capitalize?8. Section 179? (will be on depreciation schedule) 9. Bonus? (will be on depreciation schedule)

© MS Consultants, LLC 2017

1245 Property - Options

• Expense under de minimis

• Expense using 179

• Expense under Routine Maintenance Safe Harbor

• Capitalize, and depreciate per prescribed life

• Capitalize with Bonus, if applicable

6/14/2017

33

1250 Property - Options• Expense under unofficial IRS 33% rule• Expense under “traditional” repair rules

– (A sewer repair is still a sewer repair)

• Expense under Routine Maintenance Safe Harbor• Expense under 179, if qualified property• Expense removal or demo costs with Change #21• Expense or Capitalize based on new capitalization

standards – (Betterment, Restoration, Adaptation)

• Capitalize, and depreciate over 27.5 or 39 years• Capitalize with Bonus, if applicable

Depreciation Today

• PATH Act of 2015– Signed December 18, 2015

– Extends Bonus Depreciation

• 50% deduction on qualified assets acquired & placed in service in 2015 through 2017

• Applies to most qualified tangible personal property and land improvements, as well as qualified leasehold improvements

© MS Consultants, LLC 2017

• Bonus Depreciation rules:

– 50% deduction (currently)

– Must be a new Unit of Property

– Original use of the Unit of Property must begin with the taxpayer

– Must have a depreciable life less than 20 years

• Personal property, land improvements

• Importance of Cost Segregation Studies

– Can elect out by recovery class© MS Consultants, LLC 2017

6/14/2017

34

• Bonus has been extended thru 2019

• 2015 = 50%

• 2016 = 50%

• 2017 = 50%

• 2018 = 40%

• 2019 = 30%

• This will allow for more effective tax planning© MS Consultants, LLC 2017

• The Act retroactively extends and makes permanentthe 15 year straight line depreciation option for:

• Qualified Leasehold Improvement Property (QLI)

• Qualified Restaurant Property (QRP)

• Qualified Retail Improvement Property (QRIP)

• Remember 15 year tax life with SL depreciation, not 150% declining balance.

© MS Consultants, LLC 2017

Qualified Leasehold Improvement Property

– QLI property includes• Code Sec. 1250 property

– The improvement is made "under or pursuant to a lease”

– The portion of the building is to be occupied exclusively by the lessee

– The improvement is placed in service more than 3 years after the date the building was first placed in‐service

– NOT eligible if related party

© MS Consultants, LLC 2017

6/14/2017

35

Qualified Leasehold Improvement Property

– QLI property DOES include:

• Plumbing and electrical systems

• Drywall

• Ceramic tile

• Lighting fixtures

• Acoustic ceiling tiles

• & more

© MS Consultants, LLC 2016

Qualified Leasehold Improvement Property

– QLI property DOES NOT include:

• enlargement of the building

• any elevator or escalator

• any structural component benefiting a common area

• the internal structural framework of the building

© MS Consultants, LLC 2017

• Internal Structural Framework• Regs. Sec. 1.48‐12

– (3) DEFINITION OF INTERNAL STRUCTURAL FRAMEWORK. For purposes of this section, the term “internal structural framework” includes all load‐bearing internal walls and any other internal structural supports, including the columns, girders, beams, trusses, spandrels, and all other members that are essential to the stability of the building. (THIS MEANS MOST IMPROVEMENTS ARE ELIGIBLE such as drywall, plumbing, electric, etc…)

Depreciation Today, cont.

© MS Consultants, LLC 2017

6/14/2017

36

Qualified Leasehold Improvement Property

• Qualified Leasehold Improvements

– 09/11/01 – 10/22/04 – 39 year QLI qualifies for Bonus

– 10/23/04 – 12/31/04 – 15 year QLI qualifies for Bonus

– 01/01/05 – 12/31/07 – 15 year QLI – NO Bonus

– 01/01/08 – 12/31/13 – 15 year QLI qualifies for Bonus

– 01/01/14 – permanent – 15 yr QLI qualifies for Bonus

© MS Consultants, LLC 2017

Qualified Restaurant Property– QRP includes:

–An improvement to a building, if more than 50% of the building's square footage is devoted to preparation of, and seating for on‐premises consumption of, prepared meals.

–Can be related party

© MS Consultants, LLC 2017

Qualified Restaurant Property– QRP includes:

– Interior Improvements only ‐ 2004‐2008

– Interior and exterior, including all 1250 property – 2009‐current

–No 3 year rule, meaning QRP is applicable for a newly constructed restaurant – 2009‐current

– 50 % Bonus DOES apply on 5 and 15‐yr assets

– 50 % Bonus DOES NOT apply for 15‐yr SL assets

© MS Consultants, LLC 2016

6/14/2017

37

Qualified Restaurant Property

• Qualified Restaurant Property

– 10/23/04 – 12/31/07 – 15 year QRP – NO Bonus

– 01/01/08 – 12/31/08 – 15 year QRP qualifies for Bonus

– 01/01/09 – 12/31/13 – 15 year QRP – NO Bonus

– 01/01/14 – permanent – 15 year QRP – NO Bonus

– Rev Proc. 2011‐26 – QRP is bonus eligible if meets the “dual characteristic” test of QLI

© MS Consultants, LLC 2017

Qualified Retail Improvement Property

– QRIP

–open to the general public and is used in the retail trade or business of selling tangible personal property to the general public,

–placed in service more than 3 years after the date the building was first placed in service.

–made by the owner of that improvement will be qualified retail improvement property

© MS Consultants, LLC 2017

Qualified Retail Improvement Property

• Qualified Retail Improvement Property

– 01/01/09 – 12/31/13 – 15 year QRIP – NO Bonus

– 01/01/14 – permanent – 15 year QRIP – NO Bonus

– Rev Proc. 2011‐26 – QRIP is bonus eligible if meets the “dual characteristic” test of QLI

© MS Consultants, LLC 2017

6/14/2017

38

Qualified ImprovementProperty

• New “Q” on the block – effective 01/01/16

– Similar to QLI, but can be self‐owned building

• Bonus eligible

– YES ‐ 39‐yr with BONUS

– No in service requirement pursuant to a lease

• Eligible for your own building

– No 3 year old requirement

• Improvements still have to be done after building is PIS

– Common areas are eligible for Bonus© MS Consultants, LLC 2017

Qualified ImprovementProperty

• New “Q” on the block

– Example

• An internal improvement (structural component) that benefits a common area does not qualify for a 15‐yr recovery period in the case of a leased building property or a retail building. HOWEVER, QI property does not contain this restriction. Therefore, such an internal improvement to a common area may nevertheless qualify for bonus depreciation as qualified improvement property.

© MS Consultants, LLC 2017

Qualified ImprovementProperty

• QLI, QRP, QRIP all have been made permanent with the PATH act

• QIP has been introduced as part of the Bonus depreciation extensions. Will QIP expire at the end of 2019?

6/14/2017

39

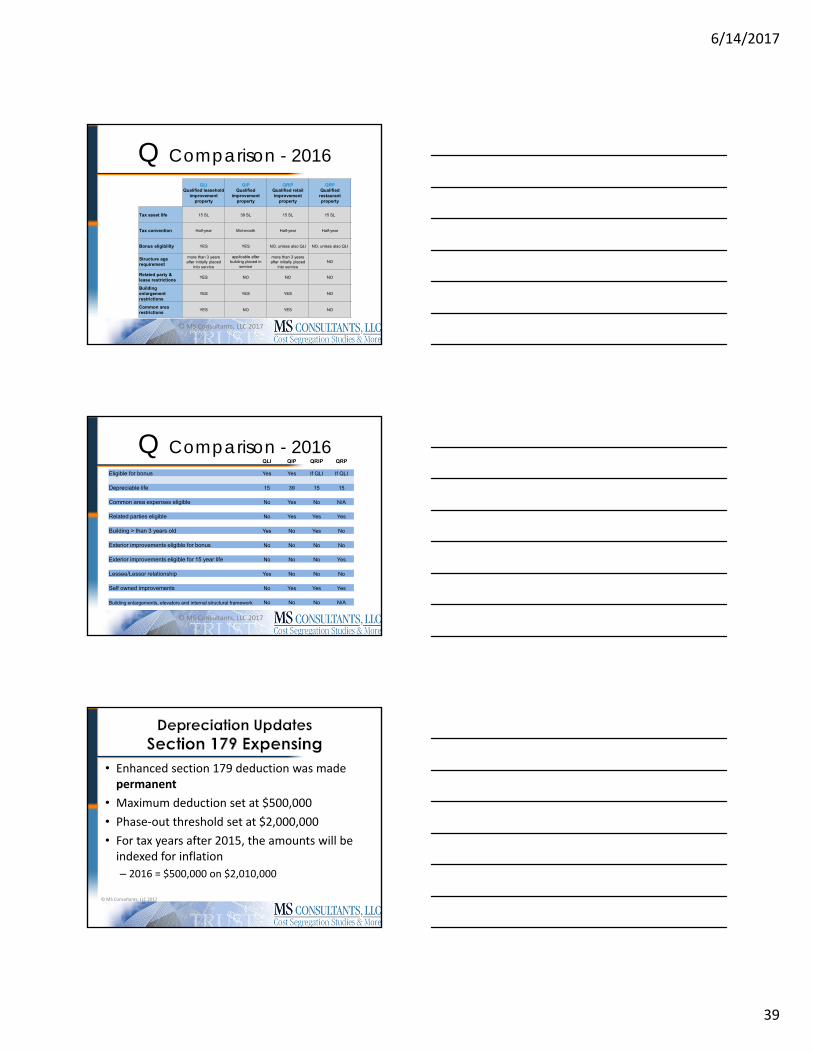

Q Comparison - 2016

© MS Consultants, LLC 2017

QLIQualified leasehold

improvement property

QIPQualified

improvement property

QRIPQualified retail improvement

property

QRPQualified

restaurant property

Tax asset life 15 SL 39 SL 15 SL 15 SL

Tax convention Half-year Mid-month Half-year Half-year

Bonus eligibility YES YES NO, unless also QLI NO, unless also QLI

Structure age requirement

more than 3 years after initially placed

into service

applicable after building placed in

service

more than 3 years after initially placed

into serviceNO

Related party & lease restrictions

YES NO NO NO

Building enlargement restrictions

YES YES YES NO

Common area restrictions

YES NO YES NO

Q Comparison - 2016

© MS Consultants, LLC 2017

QLI QIP QRIP QRP

Eligible for bonus Yes Yes If QLI If QLI

Depreciable life 15 39 15 15

Common area expenses eligible No Yes No N/A

Related parties eligible No Yes Yes Yes

Building > than 3 years old Yes No Yes No

Exterior improvements eligible for bonus No No No No

Exterior improvements eligible for 15 year life No No No Yes

Lessee/Lessor relationship Yes No No No

Self owned improvements No Yes Yes Yes

Building enlargements, elevators and internal structural framework No No No N/A

• Enhanced section 179 deduction was made permanent

• Maximum deduction set at $500,000

• Phase‐out threshold set at $2,000,000

• For tax years after 2015, the amounts will be indexed for inflation

– 2016 = $500,000 on $2,010,000

© MS Consultants, LLC 2017

6/14/2017

40

• An eligible Unit of Property has to be “New to You”. So it can be “used” property, unlike Bonus eligible property must be new

• Must be used at least 50% for business in the first year it is placed in service

• Tangible personal property

• Section 179 cannot create a loss

– Carryforwards are available© MS Consultants, LLC 2017

Section 179 Planning– Taxpayer is allowed $500,000 (total)

• Includes any 179 expense on 1245 personal property (up to $500,000)

• Includes any 179 expense on 1250 (QLI, QRP, or QRIP) real property (up to $500,000 for 2016 & forward)

– Overall purchases limited to $2,000,000

© MS Consultants, LLC 2017

Section 179 Planning– Deduction is elected asset by asset

– (In comparison to Bonus, which is elected by asset class)

– More “surgical” than Bonus as far as asset selection

© MS Consultants, LLC 2017

6/14/2017

41

Section 179 Planning– Limitations:

• Can elect personal property only, or

• If taxpayer elects both (PP & QP), a proportionate amount must be taken

– Example ahead

• Husband and wife are treated as one taxpayer with regard to the maximum dollar limit

• Only available to your aggregate taxable income derived from the active conduct of any trade or business during the taxable year

© MS Consultants, LLC 2017

Section 179 PlanningFor taxable years beginning in 2015, the provision extends the limitation on carryovers and the maximum amount available with respect to qualified real property of $250,000.

The provision removes the limitation related to the amount of section 179 property that may be attributable to qualified real property for taxable years beginning after 2015.

© MS Consultants, LLC 2017

Section 179 Planning Section 179 on Real Property ‐ Yes it’s for Real

– Qualified Real Property is:

• (QLI) Qualified Leasehold Improvement Property

• (QRP) Qualified Restaurant Property

• (QRIP) Qualified Retail Improvement Property

© MS Consultants, LLC 2017

6/14/2017

42

Section 179 Planning• Section 179 on Real Property ‐ Yes it’s for Real (cont.)

• QLI ‐ Eligible for bonus depreciation

• QLI ‐ Eligible for Section 179 real estate tax expense

• QLI Reminders:

• Interior improvements

• Pursuant to a lease

• Building at least 3 years old

• No related parties

© MS Consultants, LLC 2017

Section 179 Planning• Section 179 on Real Property ‐ Yes it’s for Real (cont.) Example:

• Tenant spends $800,000 on 2016 build‐out and will have income. Entire amount is QLI 1250 Property.

• Tenant can first take $500,000 179 expense on 1250 property and 50% bonus on remaining $300,000 ($800,000 ‐ $500,000)

• First year depreciation on these items would be $650,000 made up of $500,000 section 179 and $150,000 bonus ($300,000 x 50%)

© MS Consultants, LLC 2017

Section 179 Planning• Section 179 on Real Property ‐ Yes it’s for Real (cont.)

– Depreciation on remaining basis of $150,000

– ($800,000 ‐ 500,000 – 150,000) x 15 year S/L amount = $5,000

• Total year one depreciation would be $655,000

• Depreciation if neither bonus or 179 applied would be $800,000 x 2.5%(39 years) or $20,000.

© MS Consultants, LLC 2017

6/14/2017

43

Section 179 Planning• Section 179 on Real Property ‐ Yes it’s for Real (cont.)

– QRP

– Taxpayer spends $800,000 on a new restaurant and will have income. Entire amount is attributable to QRP 1250 property

• Tenant can first take $500,000 section 179 expense on 1250 property

• Depreciation on remaining basis of $300,000 x 3.3%(1/2 year 15 yr s/l) = $9,900

• Total year one depreciation would be $509,900

• Depreciation if neither bonus or 179 applied would be $800,000 x 2.5% (39 yr s/l)or $20,000.

© MS Consultants, LLC 2017

Section 179 Planning• Section 179 on Real Property ‐ Yes it’s for Real (cont.)

QRIP Taxpayer spends $800,000 on renovating its shoe store

and will have income. Entire amount is attributable to QRIP 1250 property Tenant can first take $500,000 section 179 expense on 1250 property

Depreciation on remaining basis of $300,000 x 3.3%(1/2 year 15 yr s/l) = $9,900

Total year one depreciation would be $509,900

Depreciation if neither bonus or 179 applied would be $800,000 x 2.5% (39 yr s/l)or $20,000.

© MS Consultants, LLC 2017

Section 179 Planning‐ Three examples of 179 involving personal property and qualified property

‐ Example 1 = Allocation

‐ Example 2 = QP only

‐ Example 3 = PP only

© MS Consultants, LLC 2017

6/14/2017

44

Section 179 Planning• Example 1 ‐ Allocation

– Taxpayer acquires $500,000 in 1245 property in 2015 and elects 179 for personal property

– Taxpayer acquires $1,800,000 in QLI property in 2015 and DOESelect 179 for Q real property

– Taxpayer is limited to $200,000 of 179 expense in total: • Purchases of personal property $ 500,000 (22%)

• Purchases of QLI property $1,800,000 (78%)

• Total $2,300,000 (100%)

• Phase out begins at $2,000,000

• Amount ineligible for 179 expense $ 300,000

• Amount of section 179 expense $ 200,000 – 1245 property, personal property = $ 43,478

– QLI property, real property = $156,522

© MS Consultants, LLC 2017

Allocation required per Notice 2013‐59

Section 179 Planning• Example 2 – QLI only

– Taxpayer acquires no ($‐0‐) 1245 property in 2016

– Taxpayer acquires $1,800,000 in QLI property in 2016 and DOESelect 179 expense

– Taxpayer is limited to $500,000 of 179 expense in total:

• Purchases of personal property $ 0

• Purchases of QLI property $1,800,000

• Total $ 500,000

• Phase out begins at $2,000,000

• Amount eligible for 179 expense $ 500,000

© MS Consultants, LLC 2017

Section 179 Planning• Example 3 – PP only

– Taxpayer acquires $500,000 in 1245 property in 2015 and elects 179 for personal property

– Taxpayer acquires $1,800,000 in QLI property in 2015 and DOES NOT elect 179 expense

– Taxpayer is limited to $500,000 of 179 expense in total:

• Purchases of personal property $ 500,000

• Purchases of QLI property $ 0

• Total $ 500,000

• Phase out begins at $2,000,000

• Amount eligible for 179 expense $ 500,000

© MS Consultants, LLC 2017

6/14/2017

45

Section 179 Planning• Section 179 on real property can now be carried past

2 years-example– Taxpayer purchases $500,000 of qualified real property in 2015.– Eligible for $500,000 of Section 179 expense and elects full

$500,000.– Taxable income is $150,000 in 2015– Section 179 expense is limited to $150,000 in 2015 and $350,000 is

carried forward– Section 179 expense is limited to $250,000 in 2016 and $100,000 is

carried forward– In 2017 taxable income is $400,000– Remaining $100,000 of section 179 expense is used up in 2017

– Result is 3 year write-off of $500,000 of 1250 property

© MS Consultants, LLC 2017

Section 179 Planning

• Taxpayers can change their minds– May revoke section 179 election without IRS

consent by filing a timely amended return. – Useful if original election turns out

unfavorable.– This was originally supposed to sunset in

2015. It is now permanent.

© MS Consultants, LLC 2017

© MS Consultants, LLC 2017

§179D Energy Efficient Tax Deduction

6/14/2017

46

What is §179D?• A tax deduction for energy‐efficient expenditures made

to depreciable commercial, government/municipal, or large (3+ stories) residential buildings that reduce energy use by 50% compared with similar structure built to ASHRAE/IES Standard 90.1‐2001.

• NOTE: Beginning in 2016 a taxpayer must utilize ASHRAE/IES Standard 90.1‐2007. SET to EXPIRE in 2016

• Maximum deduction: $1.80/SFPartial deductions allowable of $0.60/SF for buildings that do not meet overall threshold but have systems which are individually energy efficient

© MS Consultants, LLC 2017

What qualifies under §179D?• Buildings constructed or improved between January 1, 2006 and December 31, 2016 are eligible for deductions

• Owner of a building, or lessee who installs energy‐efficient systemsIf multiple taxpayers install energy‐efficient systems in the same building, the deduction may be split between them, as long as the total deduction does not exceed the maximum $1.80/SF

© MS Consultants, LLC 2017

Energy Efficient Systems

• Three building systems are analyzed under §179D:

Building Envelope (exterior walls, roof, windows, exterior doors, foundation, & basement)

© MS Consultants, LLC 2017

6/14/2017

47

Energy Efficient Systems

• Important Considerations for Building Envelope:

– Wall insulation & airtightness

– Window SHGC & U‐Value

– Orientation & Climate Zone

– Window‐to‐wall ratio

© MS Consultants, LLC 2017

Energy Efficient Systems• HVAC Systems that Tend to Qualify:

– Geothermal– Thermal Storage– High Energy VRF Units– Centralized HVAC in Apartments– Energy Recovery ventilation– Chillers (buildings > 150,000 SF)– Direct Fired Heaters– VAV (Variable Air Volume) in smaller buildings– Chilled Beam– Magnetic Bearing Chillers– Gas‐fired Chillers Combined with electric chillers

© MS Consultants, LLC 2017

Energy Efficient Systems

© MS Consultants, LLC 2017

• Lighting most common deduction

• New constructions or retrofits adhering to most current building codes will qualify for at least partial deduction

• Interim lighting rule gives much greater flexibility to lighting than other systems

6/14/2017

48

Government Owned Buildings

• For government‐owned buildings, the deduction may be taken by the designer of the building or system qualifying for the deduction

• NOTE‐IRS Code Section 501(C)(3) organizations are not eligible. This means tax‐exempt or non‐profits do not qualify.

© MS Consultants, LLC 2017

Government owned Buildings include:

• Schools‐Beverly Hills High School

• Courthouses‐US district court

• Libraries Mecklenburg County Library

• Colleges‐State University of New York at Buffalo

• Municipal Buildings‐Macon County Administration Building.

Government Buildings do not include:

• Not‐for‐profit tax‐exempt entities

• Colleges ‐ Harvard doesn’t, Arkansas does

• Schools ‐ Pace Academy for the Arts doesn’t, School 54 does

6/14/2017

49

§179D for architects and designers

• With Notice 2008‐40, the IRS solidified its rules allowing architects, designers, and builders to take advantage of §179D for government‐owned buildings. Because of this, we’ve seen a large influx of these projects.

• Any project built since 2006 could potentially qualify, and most modern buildings qualify for at least one of the three systems

© MS Consultants, LLC 2017

§179D for architects and designers

Two Catches:

Architecture and engineering firms can’t certify their own deduction—an independent certification is necessary:

• Per IRS Notice 2006‐40, Section 5.05 (1), a “qualified individual” capable of certifying a given property is:

‐an individual that is not related to the taxpayer claiming the deduction under §179D.

Architecture and designers cannot file Form 3115, but they can amend prior returns. (IRS Rev. Proc. 2012‐39)

© MS Consultants, LLC 2017

§179D for architects and designers

© MS Consultants, LLC 2017

6/14/2017

50

§45L – Residential Energy Efficient Tax Credits

§45L- Energy Efficient Dwelling Units

• Like §179D, §45L requires units to achieve 50% energy savings.

However, savings are compared against 2006 IECC standards rather than 2001 ASHRAE/IES (2012 change, previously 2003 IECC standards)

Additionally, §45L requires 10% savings from the building shell as well—having super‐efficient lighting and HVAC systems alone are not enough

§45L- Energy Efficient Dwelling Units

• While §179D is a deduction, §45L offers a credit

• Available for any dwelling (residential unit) of 3 stories or less:Single‐family dwellings

Duplexes and multi‐unit houses

Apartment buildings and complexes (under 3 stories above‐ground)

Also $1,000 credit available to qualifying manufactured homes

• Credit goes to building owner

6/14/2017

51

§45L- Energy Efficient Dwelling Units

• Applicable for open tax years

• Taking the credit:

– In the year the property was placed in service

– Amend a return from open tax years

• Unfortunately, cannot use a Form 3115 to go further back

• Set to expire in 2016

§45L- Energy Efficient Dwelling Units

However, the tax benefits can be incredible.

For example, a qualifying apartment complex with 200 units would earn a $400,000 tax credit!

$2,000 credit

x 200 units .

$400,000 total tax credit!The amount of the credit reduces the basis in the property

§45L Case Study

$254,000

• Garden‐style apartment complex

• New Construction

• Located in southern US, so for obvious reasons, performance of air conditioning systems extremely important

6/14/2017

52

§45L Case Study

§45L Case Study

Deduction $254,000

Number of Units Qualifying(Computer Model Simulation) 127

Property Type Apartment Complex - Garden Style

Year Constructed 2011

Number of Units 150

$254,000Credit

Thank you for listening!

Questions?

Additionally, please don’t hesitate to contact with questions later:

© MS Consultants, LLC 2017

David A. FabianDirector, MS Consultants LLC

Office: 716‐580‐1553Cell : 716‐573‐9378Fax : 716‐633‐9469