journal of technical analysis (jota). issue 24 (1986, may)

TRANSCRIPT

Gill

m

0 t

0 c) -I

m

c)

2 c)

-am ASSOCIATIOW J- Issue 24 May 1986

l3litir: Henry 0. Pruden, Ph.D. Adjunct Professor Golden Gate University San Francisco, CA 94105

Manuscript-: Arthur T. Dietz, Ph.D. Professor of Finance Graduate School of Business Administration, mry University Atlanta, Georgia

Frederick Dickson Portfolio Manager Millbum Corporation New York, New York

Richard On-, Ph.D. Vice President for Research John Gutman Investment Corporation New Britian, CcKlnecticut

David Dpshaw, C.F.A. Director of Portfolio Strategy Research Waddell and Reed Investment Management Kansas City, Missouri

Anthony W. Tabell Technical Analyst Delafield, Harvey, Tabell Princeton, New Jersey

Robert T. Wbod, Ph.D. Associate Professor of Finance Pennsylvania State University State College, Pennsylvania

Printer: &lden Gate University 536 Mission Street San Francisco, CA 94105

Mrket Technicians Association 70 Pine Street New York, New York 10005

2

MTA Journal/May 1986

MTA JOURNAL—MAY 1986

TABLE OF CONTENTS

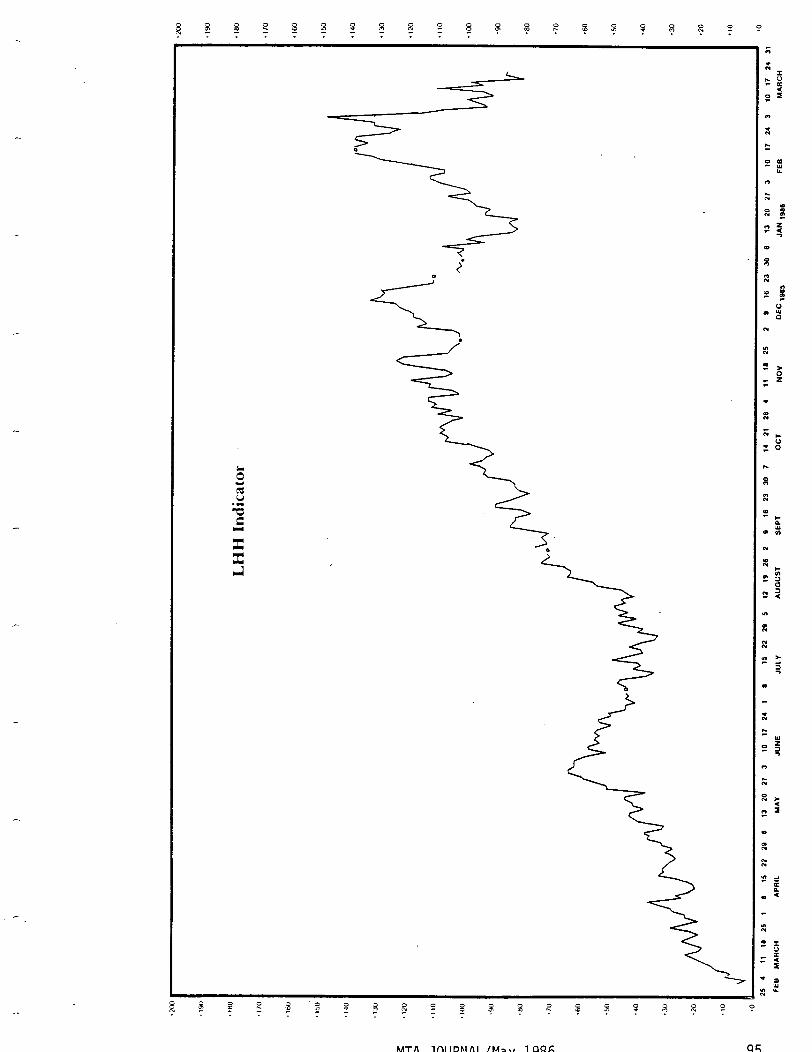

MTA OFFICERS AND COMMITTEE CHAIRPERSONS . . . . . . . . . . 3 MEMBERSHIP AND SUBSCRIBER INFORMATION . . . . . . . . . . . 4 STYLE SHEET FOR SUBMISSION OF ARTICLES . . . . . . . . . . . . 5 VOICE OF A PRO: WHAT IS PROGRAM TRADING? Joseph Gahtan and Andrew Harmstone-Rakowski . . . . . . . . . 6 ’86 PITFALLS IN THE STOCK MARKET Walter R. Deemer . . . . . . . . . . . . . . . . . . . . . . 16 SOME OBSERVATIONS FROM SAFIAN RESEARCH Kenneth Safian . . . . . . . . . . . . . . . . . . . . . . . 28 THE INSTITUTIONAL BUY-SIDER USE OF TECHNICAL ANALYSIS William Di Ianni . . . . . . . . . . . . . . . . . . . . . . 46 STATISTICAL TOOLS FOR THE TECHNICAL ANALYSIS, THE BASICS FROM A SLIGHTLY DIFFERENT PERSPECTIVE Frederic H. Dickson and Dr. Robert A. Wood . . . . . . . . . . . 48 PERSPECTIVES ON TWENTY-FOUR HOUR TRADING William A. Lupien . . . . . . . . . . . . . . . . . . . . . . 62 TIME OF DAILY HIGH AND LOW Arthur A. Merrill . . . . . . . . . . . . . . . . . . . . . . 66 DIVERGENCE ANALYSIS: SEVERAL EMPIRACLE TESTS Joseph F. Kalish . . . . . . . . . . . . . . . . . . . . . . 68 THE LAST HALF HOUR INDICATOR Bruce M. Kamich . . . . . . . . . . . . . . . . . . . . . . 93

PRES- Gail Dudack Pershing/Div. DLJ 212~312-3322

vIu3 PRsKmm Cheryl Stafford Wellington Management 617/227/9500

Officers

-. John Murphy JJM Technical Advisors 2121724-6982

TREzdmx David Krell New York Stock Exchange

VIC33 PRESlDBW (Semimr) Robert Sinpokins Delafield, Harvey, Tabell 609/924-9660

Cozdttee Chairpersons

Robert Colby 212/399-6002

EZTlICS & -/=C REXATXCXS Tony Tabell 609/924-9660

Robert Prechter John Brooks 404/536-0309 404/266-6262

Henry Pruden 415/459-1319

-ll!ATIm Charles Comer & John Brooks 212/825-4367 404/266-6262

Phil Roth 212/742-6535

Ralph Acanlpora 212/510-3750

liaxmrrIrn E&d Dickson 212/398-8489

-smmw John Finley 203/762-0229

E7m3zus~IALI-GKouP William Byers 212/925-6651

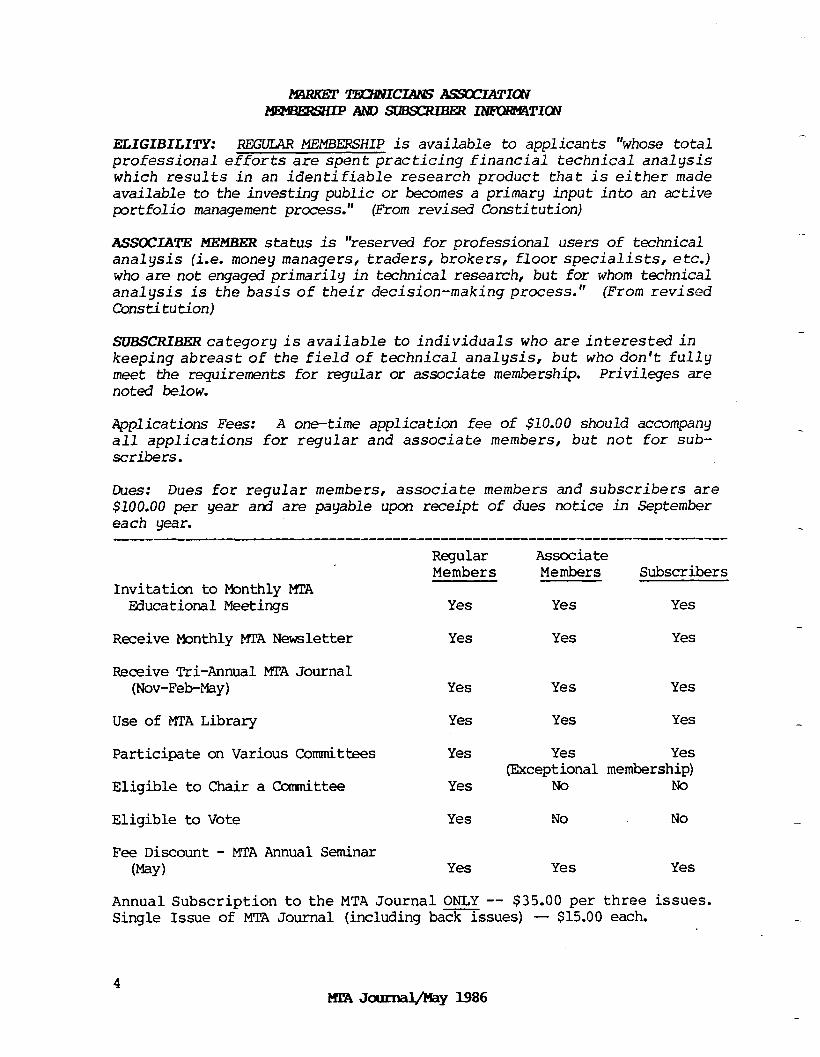

ELIGIBILITY: REGULAR MEMBERSHIP is available to applicants "whose total professional efforts are spent practicing financial technical analysis which results in an identifiable research product that is either made available to the investing public or becomes a primary input into an active portfolio management process." (From revised Constitution)

ASSOCIAT!E MEMRER status is "reserved for professional users of technical analysis (i.e. money managers, traders, brokers, floor specialists,etc.) who are not engaged primarily in technical research, but for whom technical analysis is the basis of their decision-making process." (From revised Constitution)

SUBSCRIBER category is available to individuals who are interested in keeping abreast of the field of technical analysis, but who don't fully meet the requirements for regular or associate membership. Privileges are noted below.

Applications Fees: A one-time application fee of $10.00 should accompany all applications for regular and associate members, but not for sub- scribers.

Dues: Dues for regular members, associate $100.00 per year and are payable upon receipt each year.

members and subscribers are of dues notice in September

-------------------------------------------------------------------------

Regular Associate Members Members Subscribers

Invitation to Monthly MTA Educational Meetings

Receive Monthly MTA Newsletter

Receive Tri-Annual MTA Journal (Nov-Feb-May)

Use of MTA Library

Participate on Various Committees

Eligible to Chair a Corranittee

Eligible to Vote

Fee Discount - MTA Annual Seminar (May)

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes Yes

Yes Yes

Yes Yes (Exceptional membership)

No No

No No

Yes

Yes

Yes

Yes

Annual Subscription to the MTA Journal ONLY -- $35.00 per three issues. Single Issue of MTA Journal (including bmssues) - $15.00 each.

4 ma ~aurnayMay 1986

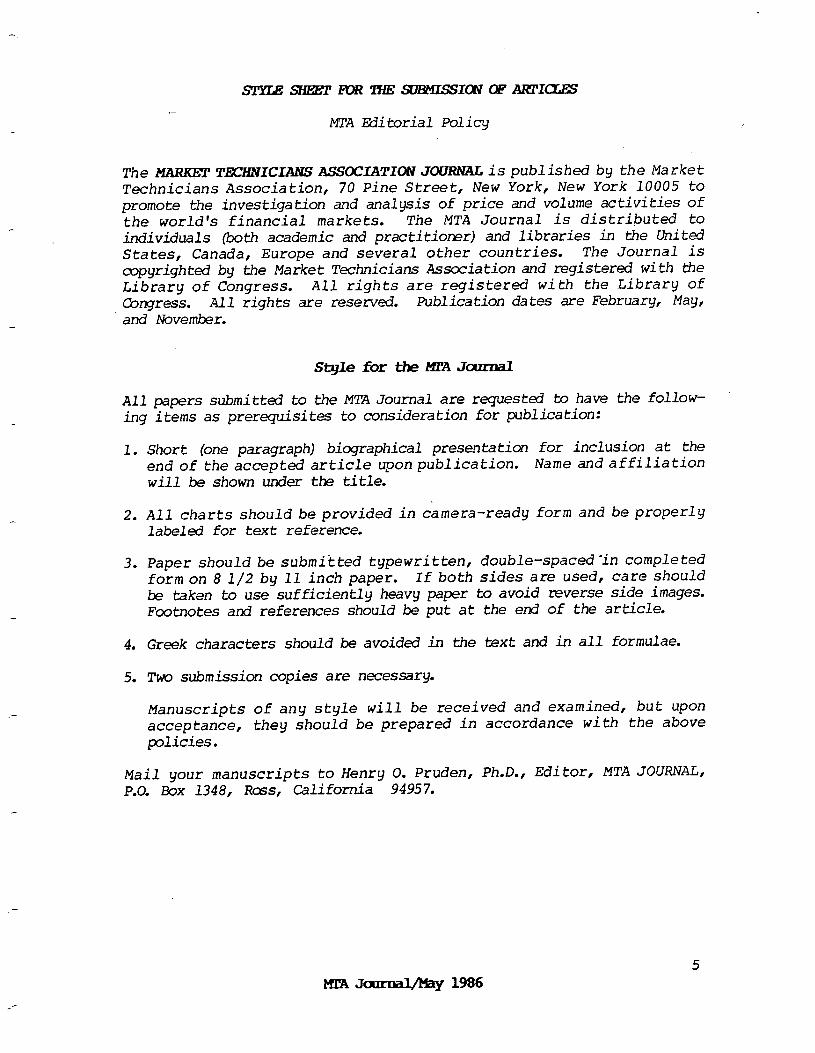

sryLEsHETm!mE slB!asIrn OF AR!rIrn

MTA Editorial Policy

The MAR@T!l'XBWICIANS ASSOCIATIONJOURNAL is published by the Market Technicians Association, 70 Pine Street, New York, New York 10005 to promote the investigation and analysis of price and volume activities of the world's financial markets. The MTA Journal is distributed to individuals (both academic and practitioner) and libraries in the United States, Canada, Europe and several other countries. The Journal is copyrighted by the Market Technicians Association and registered with tie Library of Congress. All rights are registered with the Library of Congress. All rights are reserved. Publication dates are February, May, and November.

Style for #eMTAJcmma.l

All papers submitted to the MTA Journal are requested to have the follow- ing items as prerequisites to consideration for publication:

1. Short (one paragraph) biographical presentation for inclusion at the end of the accepted article upon publication. Name andaffiliation will be shown under the title.

2. All charts should be provided in camera-ready form and be properly labeled for text reference.

3. Paper should be submitted typewritten, double-spaced'in completed form on 8 l/2 by 11 inch paper. If both sides are used, care should be taken to use sufficiently heavy paper to avoid reverse side images. Footnotes and references should be put at the end of the article.

4. Greek characters should be avoided in the text and in all formulae.

5. Two submission copies are necessary.

Manuscripts of any style will be received and examined, but upon acceptance, they should be prepared in accordance with the above policies.

Mail your manuscripts to Henry 0. Pruden, Ph.D., Editor, MTA JOURNAL, P.O. E!ox 1348, Ross, California 94957.

5 M!m Joumd/by 1986

The subject of our interview is a discussion on program trading by two promi- nent experts in the field: Joseph Gahtan, Vice President, Options and Futures Trading, Salomon Brothers and Andrew Harmstone-Rakowski, Stock Index Special- ist at Paine Webber Capital Markets.

Joe's name is well recognized in the options business. He has been actively involved in derivative products for many years, Andrew brings a quantitative and analytical perspective to tiis topic, through his active involvement with stock index futures and options evaluation techniques and models.

Q. What is program trading, in general?

Gahtan: Program trading as it relates to index options or futures is the buying or selling of securities while simultaneously buying or selling index options or futures.

Q. Does this only involve futures and options or are there programs involving other types of instruments?

Gahtan: There are other programs, but the traditional ones done include the futures and index options such as XMI, OEX or NYA and the underlying securities.

Q. Andrew, would you define for our readers what the term basket trade means?

Harmstone: Basically, a basket or program trade is an arbitrage. It is called a basket because you are trading a large number of stocks simultaneously. You don't care that much about any one individual stock. You care about the prices of all the stocks together.

You may buy some stocks at higher prices than anticipated and others at lower, but mainly you are concerned with the net average price of the stocks you trade. The reason for the basket is that the future is mispriced so you want toarbitrage against the future. You are buying or selling the stocks as a hedge against your future contract.

Q. What are the mechanics of executing this type of arbitrage?

Harmstone: One of the most important things is tohave an on-line system of prices showing the spread between the bid or ask and the last sale of the stocks themselves. Typically, a single phone call down to the floor is used to execute a program. The floor traders execute program A, program B or whatever it is. The tickets are already down on the floor so they just take those tickets ard execute them.

You typically take whatever price is available in the market. You want to execute the trade as quickly as possible because the conditions to the other side of the trade can change very quickly. So what you end up doing is making two phone calls , one to the futures pit and one to the floor of the stock

6

exchange. Both sides are executed simultaneously. The tricky part is the futures side since it is-the most volatile.

Q. What side do you normally execute first, the stocks or futures?

Harmstone: You try to execute them as simultaneously as possible. Because the futures are so volatile, the spread may be there for only a few seconds after you actually put the order in.

Gahtan: If you are willing to take the risk, you mightexecutethe one side and then the other. If you thought the market was declining, you could sell stocks first and buy your futures later. But of course, that becomes more risky.

Q. How long does it take to complete one of these program trades?

Gahtan: Well, it really depends on the size. If it is a ten million dollar program, which is a relatively small program, it could take two to three minutes. Aprogram of $25-50 million encompasses a little more time. The real issue is how many stocks are involved. It takes less time to execute 250 stocks than 500 stocks; The faster the stocks are executed the less the variation in price. The number of stocks will impact the speed with which the program is executed.

Q. On the average, how many stocks are normally used?

Gahtan: I don't know if there is an average. We tailor each program to the need of the client and the basis risk he is willing to assume over that period of time. You are going to have some tracking error risk over a period depending on the number of stocks used. .

Certainly this year if you had something like 200 to 250 stocks you had every takeover stock there was. So you certainly beat the index. Had you used fewer stocks your performance might have been somewhat lower.

Harmstone: That is absolutely right. The takeover situations have made a large basket really critical. A lot of people started doing the arbitrage with only 60 stocks to replicate a 500 stock index. Sometimes baskets were used with fewer than 60 stocks. However, if you left out cne takeover stock you were in bad shape. Most people who are doing this in a serious way have gone to 250-300 or even 400 stocks.

Gahtan: We never traded with fewer than 150 stocks and the maximum we used was 480. The right number depends on the particular custaner.

Q. What's the general dollar aunt of these programs?

Gahtan: I don't think there is a general dollar amount. Programs that range between $10-25 million are medium size. We have executed $50-100 million using the futures, but it becomes difficult with the other side.

Harmstone: When the program is less than $10 million, there are restraints on

7 m"A Jound&ay 1986

the number of stocks that can be included.

Q. How many dollars are you talking about to include 250 stocks in the basket?

Harmstone: $10-25. million is enough to trade 250 stocks. Usually $25 million is the size of a market basket. If you are doing a program which involves more money than that you would put on one basket after another. In other words, you could execute one basket and then if the futures spread is still wide you could do a second one for another $25 million.

Gahtan: Sometimes, one person executing a program tends to feed the next person. So speed and timing are critical.

Q. We have talked up to this point about buy programs. Is there a sell program for every buy program and vice-versa?

Harmstone: There is. The usual sell program is the unwinding of a buy program. There are exceptions to that, but this is true most of the time. In terms of the exceptions there is something called the swap program as opposed to an arbitrage.

What I mean by that is that people who own long stocks already, will sell the stocks and buy the future. They do that because the future is cheap. That sort of program is done by an index fund, for example, whose investment objective is to be long the market in either stocks or futures. A swap program is not necessarily related to buy program. You probably will see them swap back, down the read, into stocks so what you really are seeing is a sell program which leads to a buy program.

Q. Are the majority of sell programs we saw during the summer the unwinding of buy programs?

Gahtan: Yes, but the other part of that is that it's really a functionof the marketplace in either the future or the particular option. If you are able to roll your particular position from one month to the next, there is no need to unwind what you have on. That effect, as long as premiums are fairly priced for the client, enables the client to continuously roll until such time that he is not able to roll at a rate that he deems attractive. Then if he can't roll there will be an unwinding at some point in time.

Q.Do any of these sell programs involve short selling? Is it realistic to think that one could do that?

Gahtan: I believe that many institutions are mt allowed to sell short. That activity would probably be taken on by a firm proprietary account, if the proprietary account was willing to accept the fact that they may not be able to get everything off on a plus tick because there is no guarantee of that, and that only a partial basket may be executed any given time.

One might attempt to do it ina rising market on a day that some news might have come out, or something that may have triggered euphoria in the marketplace, and a trader may say that today is a day he can get something

-

8 ma Jaxnal&y 1986

off. But he then has to look at the other derivative market to see if that side is in line. So he is never certain that he can get that short sale off while the other condition that he is dependent on is there.

Q.Areyou saying that there isn't a greatdealof short selling as a part of these programs?

Gahtan: In my opinion, it is almost non-existent.

Harmstone: I would agree with that. We have done some experimenting with that, but it is a very unusual sort of trade.

Q. Andrew, hm do you determine when a buy program should be executed?

Harmstone: You look for a mispriced future, actually an overpriced future or an overpriced call relative to a put, depending on what derivative product you are looking at.

Gahtan: Or an underpriced situation. It really has to be looked at both ways.

Harmstone: Yes, that is correct. For a swap, underpriced futures have to be looked at. Mispricing is the key. In order to justify doing a program make sure that the mispricing is large enough to cover the costs when you do the trade. The largest part of the cost, interestingly enough, is the market impact of the stock side of the trade.

For a customer, you have to consider the commissions on the futures and the stocks, as well as the impact on the market. If you are doing the buy program, which means the future is overpriced, what you want to see is the future overpriced in excess'of the market impact plus the commission cost of the trade. Similarly, if you are doing a sell program, what you want to see is that the future is mispriced cheaply enough to cover the costs plus get you out at the rate that you require.

Q. Joe, if we are dealing with a three-month period, what type of premium is needed in the index futures in order to consider doing a buy program?

Gahtan: If you can tell me where interest rates will be and what the customer's particular needs over the T-bill rate or CD-rate may be etc., then I will be able to tell you what level it might be.

Every client has a different rate by which he needs to be either above T- bills, CD's or whatever his interest rate is. So, therefore, to say that there is a particular price by which a buy or sell program will triggered is really to say that this has all become standardized.

It really is not a standardized kind of thing because a client may have different needs whether that be 200 or 300 basis points over a ?Lbill or even more or less. On any one day it is certainly not dictated by the brokerage firms. It is client driven. It is client initiated.

Harmstone: You fir-d that there are two things that decide those levels. One

9 MTA Jcmnd&aY 19%

criterion is the trading range of the spread. People will usually execute buy programs at the top of the trading in terms of the spread. The second cri- terion is definitely, as Joe pointed out, the required return that the cus- tomers have and that is usually stated as basis points over T-bills something like 200 or 300 basis points over T-bills.

************************************************

Our interview with Joseph Gahtan and Andrew Harmstone-Rakowski will con- tinue. We'll talk about: Kinds of customers involved in basket trades; Effects of mergers cn market baskets; Programs and the individual investor; and How a broker can anticipate buy or sell programs.

10

WICE OF A PRJ: ProgramTrading. PartII

Our interview with Joseph Gahtan, Vice President, Options and Futures Trading, Salomon Brothers, and Andrew Harmstone-Rakowski, Stock Index Specialist at PaineWebber Capital Markets is concluded in this issue. This candid discussion of program trading should help many stock and options investors to understand one of the newest developments to occur in the equity marketplace.

Q. What kind of customers are involved in buy and sell programs?

Gahtan: Corporate and pension custczners.

Q. Is it the aim of corporate treasurers to invest excess funds available to them for short periods of time at some rate above a given interest rate, whether it is CD's or short term treasuries?

Gahtan: That's correct. Particularly now that interest rates have been dropping, the futures arbitrage has been a particularly attractive vehicle since its rate stayed up longer than actual rates on.other money market instruments. Recently, of course, we have seen the rates dropping. But for a long time you were able to get very nice rates using the arbitrage.

Q. What both of you are saying is that the stock market is being used as a vehicle for managing short term cash assets. Is that right?

Gahtan: In part, but certainly it is used for investment purposes as well. If a money manager had a portfolio of stocks , some of which he wanted to weed out, he might sell futures'outright against that portfolio in order to hedge the portfolio until such time that he was ready to make his stock selections. This strategy is basically being employed by money managers and not the corporate accounts.

Q. How are money managers using these derivative products for market timing, asset allccaticn and hedging?

Gahtan: If futures are cheap, a money manager may consider buying futures, especially if they're below fair value and then at a later time select the securities that he wants. As the stocks are added to the portofolio, the futures are sold.

The future, from my view, is a sentiment indicator. Someone's sentiment in the futures pit may not be the sentiment of an equity manager. If the equity manager finds the market cheap and feels it should be bought, but the futures' crowd believes the market is going lower and they want to sell a little below fair value, then there is an opportunity for an equity manager to replace his portfolio or buy futures and decide on that portfolio at a later time.

Q. Are there diverse reasons why users may at times want to consider using these instruments?

11 MpAJomml/May I986

Harmstone: Right now you are probably seeing a large number of hedgers participating in the market. As Joe pointed out, a lot of people are bearish on the market now. They are selling the futures against their portfolio to raise cash.

Alternatively, they are doing a portfolio protection strategy. If the market goes down they sell futures against their portfolio ard reduce their overall market exposure. Both of these strategies are at work right now.

Q. Joe, what happens if one of the holdings is involved in a merger?

Gahtan: We would check withour arbitrage area. Based on their opinion, we would suggest to the client that he tenders all or part of those shares in whatever the terms are of that tender offer. So, it would really be a function of the terms and whether you believe the merger is really going to happen.

'Ib just sell the stock out may also be the right answer. The other answer may be to tender it. Each individual deal is different and so each individual analysis would have to be made each time.

Q. If one of the issues is a particularly large holding within the basket and it is taken over, is there an adjustment to the portfolio? Is there a substi- tution? Is the cash being replaced?

Harmstone: Basically, you would try to take advantage of the merger or tender offers so as to track the indexes properly. Typically, you actually drop that stock out of the basket and substitute a similar stock. You have that flexibility. The individual stocks in the basket are less important than the overall basket.

Almost every stock with the exception of IBM or similar stock can be substituted for by other stocks that are also in a popular index. In a lot of cases, you can simply take a stock out of the basket, have aprofiton it and substitute another stock in its place.

Q. Let's get into something that is a concern to many brokers around the country. What effect do you think these programs have had on the general market?

Harmstone: Well, theprograms,since they involvebuying or selling a large groupof stocks canhave an impact on the market. It depends on the overall conditions of the market and how many people are trading.

When a firm is unwinding they will try to find buyers for the other side. They will find their other customers who are interested in buying those stocks. Often, the total market impact is less than you might think because it is possible to find the other side.

I think another important thing to realize is that whenever there is a big move in the market, programs get blamed because that's the easiest explanation. In some cases it is justified. In many cases there are other

12 HL7AJoumal/hy1986

things that are going on, but people frequently blame programs.

Q. Joe, what's your response?

Gahan: I think certainly at the onset of futures there may have been an impact. I think that impact has lessened over the last two years. If you are alluding to the last day phenomenon, which I think you are, that impact has been dissipated with each and every expiration because investors are very smart and have learned very quickly how to take advantage of these programs.

We have asked our customer base tobe prepared on expiration days to either buy or sell above or below the market and that has had a tendency to stabilize the market. We actively solicit clients to be there for any advantage that may be achieved by a buy or sell program on a particular last day. But in general, I think that if you look at the volatility of the market over the last two years, you will find that since the index futures and options have started we have been in a less volatile market than in the past.

I think if you were to look at the numberoftimes 4% moves have happened in the marketplace, you would see that they happen less often today than two years ago and much less than three years prior. If you were to look at 1980 to 1985 you would find that the percentage has decreased enormously. While we may have intra-day swings of some measure, the overallmarketvolatility has a- bated.

Q. If there is an impact on the market, is that impact very short in duration?

Gahtan: In my opinion, the impact is short induration. Now, there may be a level in the marketplace where people will say it has broken its traditional support or resistance zones, .-which may have been triggered by a buy or sell program. But I think the impact has lessened.

I think people have become futures and options wise and have been less likely to react to the buy or the sellprogram. I think the buy side has certainly learned not to react to it and is much more creative in its purchases and sales, apart from whatever these programs are doing.

Harmstone: The futures premiums do tend to indicate the sentiment of the futures traders about the direction of the market. Frequently, futures premiums are low because the market is heading dawn. Its the "chicken-and- the-egg" kind of thing. Is the selling the cause, or the effect, of a weak market?

Q. In your opinion, are individual investors disadvantaged by this activity in any way?

Harmstone: It seems to me that the impact on the individual investor is due largely tothedominance of large institutions trading in the stock market generally. With a large institution, the size of a trade can be so substantial that it affects the market.

Also, an individual may not have the same information that the institutions

13 ma Jamd./MaY 1986

do. Institutions can afford to pay for a lot of fundamental research, technical analysis and advice which an individual investor as a rule can't afford. I think there is a valid point that the individual investor has a more difficult time than in the past. I think this is due primarily to the institutional participation in the market with the fact.that these institutions typically have a lot more information than an individual investor can afford to obtain.

Gahtan: I think you should also look at how much the individual investor has gained by having these programs. I will take the positive side of that by saying that if an investor had something to sell at a specific price and a buy program went into effect he probably received an execution that he may not have received had the market not'risen to his level.

The same could be true with buying; if it were not for a sell program, an investor may not have been able to buy the stock he was considering at an attractive price. So as much as one would like to highlight the disadvantages of the program trading, I think there are advantages for public mstomers that were not present before.

Q. How can an individual investor , or a broker who deals with individuals, anticipate whenbuy programs and sell programs might occur? Are there any telltale signs that cne might look for?

Harmstone: I think that the most important thing that any individual investor or stockbroker can do is to monitor the price of the S&P 500 future. Not only because he can anticipate the programs but also because the future has frequently tended to lead the market , at least in a very short-term period.

It is one more sentiment indicator, something like a put/call ratio or the short position ard so on. It is another indicator that people should be aware of and look at. It could have predictive value and could help their cus- tomers.

If they watch the future they should specifically look at the difference between the price of the future and the underlying index.

If the future's premium starts to increase substantially, the broker should be aware of the possibility that the market may go up. It may go up because of a change in sentiment which is reflected faster in the futures market.

-

Secondly, when the future's premium goes up, it becomes more attractive to do program trading. You could have significant buying occur in many stocks because of the expansion of the future's premium.

I feel very strongly that an individual investor or stockbroker should watch the future's premium on a continuous basis. That's very easy to do. You just have to get a subscription to a quote service that provides futures prices.

You should watch those futures contracts very closely, continuously, through the day. When you see a big positive change in the premium, be aware that it

14 MlR Je 1986

could be foreshadowing a rise in the market. Similarly, a weakening in the futures premium could be foreshadowing weakness in the market.

**********************************************

'Ehank you both for sharing with our readers your insights ~1 program trading and helping us understand hw it arks.

This article was made available through the courtesy of the Members of the New York Stock l&change and is reproduced with their permission.

15

'86PIW INmEt4?Iax~

by Walter R. Deemer

Introduction by Arnold Wood, Batterymarch Financial Management

The Boston Security Analysts Society has about sixty luncheon meetings a y-b and all but one or two of them are devoted to company presentations. This meeting is the one out of the sixty. We're going to look at the market from the inside. We're going to look at that little thing in the capital asset pricing model (for those of you who are familiar with that) called the "mu" out on the end. It is the little thing the academics use when they say "I can't explain why it happened.' It helps to explain how we behave as investors.

We have a very appropriate person here to do so. I didn't realize the following that Walter Deemer has. I was actually quite surprised at the number of people here today - about 50 plus, 49-plus of whom are old friends of Wally Deemer which is just terrific. He started in the business in 1963 with Merrill Lynch. He joined shortly Tsai Management, then went to Putnam for ten years, and now has his own firm, Deemer Technical Research, which he started in July 1980. We are delighted to have him here to tell us about the inside of the market.

Remarks by Walter Deemer

Thank you, Arnie. It's a real pleasure to be back in Boston again. Bostonhas always been a very special city to me; as you just heard, I spent most of my professional career here in Boston. I also happened to meet and marry my wife here in Boston, so there are a lot of fond memories for me here. I am glad to be back in the home of the bean and the cod... and the football teamthatsquished the fish, but had a real rough time with the bears in the Super Bowl yesterday. As you know, the outcome of the game has a great deal of impact on what the stock market is going to do this year, and we will get into that later. First, though, I'd like to express my appreciation to the Boston Society for inviting me here - for letting me be the one out of sixty -- and for giving me the opportunity to see so many of my old friends today.

For those of you who don't know me very well, just my being here today tells you a couple of important things about me. First, I have a terrific sense of timing, since I waited for the Super Bowl to be played yesterday so I would know what the market was going to do for the rest of the year. The Chicago Bears, of course, were from ths old NFL; since if the team from the old NFL wins the Super Bowl the stock market goes up for the year, you now know what the market is going to do this year. Youdon'tneed technicians to tell you, you don't need economists, you don't even need MPT. You just need the football score. The only problem is that I have a bit of trepidation this year, because if the market happens to go down during the year someone is going to get up and say "Well of course the market went down; the Bears won. How can the market go up when the Bears win?" So I think there will be a Super Bowl indicator around next year - but maybe with an asterisk. Besides my astute

16 M!I!A JoumaljBy 1986

sense of timing you also know that I am also quite contrary, since I came from Florida toBoston at the end of January to deliver a talk. Everybody else is headed the other way for any reason they can think of, so there is a big sense of contrariness about me, too.

For those of you who are not all that familiar with what I am doing now, let me take just a minute ard explain. Basically I am doing two things. When I left Putnam in 1980 I started a consulting firm, Deemer Technical Research, in Florida. We provide a consulting service to institutional clients, giving them the same sort of research information as I generated at Putnam during the ten years I was there. The second thing is more recent; when I moved to Florida I had a long-range goal -- or dream -- of starting a market letter, and after a lot of hard work, we got it going last October. It is called Mr. Technician, and we are having a lot of fun with it. So Deemer Technical Research now has two arms: the market letter and the institutional consulting service.

I must tell you that the title of my talk was selected very carefully. After deep consultation with Rich Gula, my successor at Putnam, we came up with the title "'86 Pitfalls In The Market." We thought the word "pitfalls" would bring out the nervous people -- and I hear that there are a lot of nervous people in Boston. We also thought by using "'86 Pitfalls," many people would not know I meant1986 and thought I would stand uphere and rattle all 86 off - so I thought this would bring the hard core bears out. I will get to the 86 pitfalls later on but they are really not all that serious.

Seriously, though, I do think 1986 will be a lot trickier year than last year for investors to deal with. It's funny. If I had come here a year ago and told you that the market was going to go up most of the year, that there would be only one reaction during the year -- but that it wouldn't be even as much as 10 percent, and that by the end of the year the averages would be at all time highs, you would have said "ah-hah...vintageyear...isn't this great" and spent the year on Cape Cod. But we all fretted all year; it was one of the most nerve wracking years I have ever been through. I think the fact we were all nervous all the year through made it happen. Butgettingtwoyears like that back to back is going to be kind of difficult, I think, which is why I suspect that 1986 is going to be a little trickier than 1985 was.

I am going to tell you this afternoon how you can get through the next 11 months with most of your sanity intact. Tb do this I am going to break my talk into 3 different parts. First, a few thoughts on how you might be able to get more use and benefit out of this thing we call technical analysis. You do not need to be a technician or technical analyst to get some use out of technical analysis; you do not need to even admit publicly that you even look at the stuff. Secondly, I will discuss the market's technical position; where we are now, and how we got there. This sets up the third and finalpartof my talk: where we might be going.

I had actually toyed with calling the first part of my talk "The Death of Technical Analysis" -- or at least "The Death of Institutional Technical Analysis." This fits in with what someone said to me earlier today, that technical analysis has fallen into ill repute. I must confess that knowing

17 MTA JarrndypfaY 1986

Dean &Baron for many, many years, as technical analysis swings more and more over into the so-called "ill repute" category I keep waiting for Dean, as a big contrarian, to start a war room over at Batterymarch. Dean, though, once had my predecessor at Putnam, John Bennett,over there working for him,and told John to hide his charts in the drawer with the false bottom in it until after five o'clock. Rich Gula, my successor at Putnam, is over at Batterymarch glow, but he's got John Bennett's old desk, and Rich has still got to use the same drawer, and Dean still doesn't have a war room. I don't know how long the whole process takes but I don't knew whether I can wait that much longer.

Actually, I was reminiscing about all this the other day. Back in the early 1970's there were 13 in-house technical analysts at insti.tutions in Boston, and 6 of us were operating at fairly senior levels. The number is now down from 13 to four; more regrettably, the number of senior analysts has fallen from six to one. I don't know why; I don't thinkour records havebeen that bad, and in some cases they've been quite good. Perhaps it's just economics. Technical analysis may have already gone through what the field of economics is going through now, which is reductions of in-house efforts. I may also be that the severe reductions in soft dollar commission budgets has caused the number of available sources to institutions to diminish, so the need for in-house coordination is down.

Technical analysis, I dare say, is not dead. I suspect everybody in this room reads Bob Farrell or StanBergeor John Mendelson. I think the problem that technical analysis has gotten into is that most people, for various reasons, now rely on just a few analysts for input on any given stock or group. As a result, most people tend to know exactly the same thing about almost everything, including the market, as everybody else does. The answer, of course, is to be contrary, but with everybody knowing the same thing, everybody has sort of a standard contrary. Also, as far as contrary investing goes, there are so many little Batterymarches around now that they are making life miserable for everybody (in that they are all using essentially the same screening process. This means that everybody is either coming up with nothing or, in order to get a jump on the guy down the street, they're fudging their screens a little bit, making the risk factor higher and the performance lower.

I think that being contrary is a big part of technical analysis (or "market analysis"' which I prefer. But I think that basic technical analysis has to be integrated with all the other factors. This is a key thing which John Bennett, who taught me a lot when I worked for him at Putnam, and to whom I owe a great deal, taught me. John did a great job of showing, on a practical basis, how technical analysis should be integrated with the other elements: economic, fundamental, political, monetary - it all blends together. It would be nice to have technical analysis all summed up by a black box with a red light and a greenlightonit ; when the green light is on, you're in, and when the red light is on, you're out. But its not that simple, especially if you realize (and I think this is the basic underlying rationale for technical analysis) that the market is the sum of all of our knowledge -- those of us here in this room and everywhere else. As such, the market "knows" more than any single person in it; by studying the market, you can learn, by inference, a lot of things about things like strength ard weakness in the economy.

18 HINJanodLFfayU86

How can you use technical analysis most effectively? Well, a writer named Dostoevsky once said "Be simple -- and rediscover the world." I think that's as good a place to start as anywhere. Everybody seems to want to fine tune things until they lose value from it rather than adding, so I think as we go through the rest of this presentation - and as you go through the rest of the year -- you should just keep asking yourself a couple of basic questions. These questions are what you should be finding out from technical analysis -- and what technical analysis can tell you. So just keep a couple of simple questions in mind: Is the trend -- intermediate or major -- up or down; is the market going upordown? Is the.market gaining or losing momentum? Is the move broad or narrow; can you buy almost anything and make money, or do you have to be very selective? Is the tone of the market speculative or conserva- tive? There are times, during a speculative binge, when you have to have a high beta -- and there are times when, if you have a high beta, you will have your head handed to you. Also, is the market's tone getting more speculative or more conservative? Finally, the most important question for those who manage money: where's the leadership? What's leading the market up or down? Is there any theme to it? (There is abig theme now called deflation, and it is blending a couple of things together that might not ordinarily have been blended together). Just keep these things in mind as we go through where the market is now and where the market is going, and I think you will be able to find out some insights that market analysis can give you.

There is a basic underlying factor about the market here that you can't forget (even though we all tend to because we are in the heat of battle day after day): we are in a secular bull market. A secular bull market is a bull market that extends over more than one conventional 4-year cycle. This one happened to begin in 1974; it followed the secular bear market that started in 1968 which followed the secular bull market that started in the 1940's. So you are now in the midst of a' secular bull market which started with the once in a generation valuation lows of 1974, and it is not likely to end until you get once in a generation valuation or speculation highs as you did in 1968. And, whatever else this,is, "itain'ta secular top." This is not a once in a generation high yet; as a matter of act, if you envision a pendulum swinging fr0m.a secular low, with its undervaluation, underenthusiasm and disinterest, to the overenthusiasm and overspeculation of a secular high, you are probably about halfway there. So that puts the end of this secular bull market somewhere in the 1990's. It is an important underlying factor, since the major underlying trend is with equity investors now, not against them. And as technicians like to say, "the trend is your friend."

I don't think this secular bull market is going to end until the public is back in the market with both feet. I think they are going to come back in a big way; I suspect our friends at Fidelity will have a hundred billion dollars before this whole thing is through. The public is going to be very excited about stocks again, just as they have been excited about other things in recent years; they will rediscover the stock market. This is one reason Mr. Techni- cian, my market letter, was created; when they come back I want to have some- thing for them to read -- and I think they are going to be back in a big way before we are through.

"Secular Bull Market" - I almost think that we ought to put a little sign

19 MllA Jourd&ay 1986

on our desk that says "This is a Secular Bull Market;" the first thing every morning; you look at it, and the last thing every night, you look at it. It is something you tend to forget, but it is something very basic -- the most basic building block of where the market is now.

We now come to the regular bull and bear market cycle; the four-year cycle. The four-year cycle is working very well: in 1982 we got a conventional 4-year cycle low, which followed the prior lows in 1978, 1974, 1970, 1966 and 1962. The four-year cycle (which happens, if you track it very closely, to be 51 months) means that if you add 51 months to the last low, you come up with October of 1986 as the next one. And, since in order to get a four-year low, you need a decline of some magnitude, you can't go all the way to September of 1986 to get your peak; you need some sort of a significant decline to get a four-year low. From a four-year cycle standpoint, then, 1986 looks like a bad Y-r -- except for one thing. And that's what the Fed did last year; something they weren't supposed to do three years into the four-year cycle -- they cut the discount rate twice at the end of 1984... and once more, in May, for good measure. They aren't supposed to do this. They are supposed to be tightening; they aren't supposed to be loosening. And, as a result, I suspect that the Fed has blown the four-year cycle out of the water this time around. It has certainly put it in limbo. This leaves two possibilities. Number one: the four-year cycle is still there, so you get a low in October 1986 (give or take a coupleof months). Number two is that the Fed has indeed changed the four- year cycle (and if I were going to vote, this is the one I would vote for).

This means that the market is now doing something similar to what it did in 1960-62, when it sort of skipped a step in the four-year cycle: we had a major low in 1960, which was economically related, and we had another major low in 1962 which was all technical. The 1962 decline had nothing to do with a recession; although there were fears of a recession, there was no actual recession. But there was rampant speculation in the market in 1961; May of that year saw the only day in history when the Amex volume was bigger than the NYSE volume, and the new issue market was red hot. Nineteen sixty-two was a correction of 1961's over-speculation and over-valuation (the Dow-Jones Industrials were selling at 25 times trailing 12 months earnings at the end of 1961). It was a purely technical decline. Nevertheless, you had a major low in 1960, another one in 1962, and, since then,one every 4 years. If the Fed did what it usually does early in the four-year cycle back at the end of 1984 and in early 1985, we may have skipped a step again, and the four-year low may now be dating back to 1984, not 1982. There is certainly a strong possibility that the next four-year low is not scheduled for 1986, but 1988.

I am really saying only one thing. I don't think you can be bearish this year just because of the four-year cycle. You aregoing tohavetohave some other reasons too, because there is an offsetting argument this time, which says that the next four-year low will not be in 1986 -- but 1988. And all the sentiment factors that we touch on later suggest that this is not a major top, but only part way up.

Now to the intermediate term. We had a top last summer, but there was no particular technical deterioration. We started the decline last summer with the classic early leaders (the financial stocks, the interest-sensitive stocks,

20 e Jourd&ay I386

the utilities) starting down first. The Dow Jones Utility average, as I remember, had the biggest one day decline in history a day or two off the July top. And so the early leaders led the market down last summer. As the market started down, the longer term indicators quickly turned bullish. (They were never really bearish to begin with). The shorter-term indicators (the sentiment factors, etc.) quickly turned bullish afterwards. We were then sitting there waiting for strength to reappear in the areas (foods, financial, utilities, etc.) that led us down in the first place. It took us until early October, but we finally got it. It showed up first in foods, but that was due to the General Foods buyout. Thenit showed up in utilities; finally, in the first week of October it showed up in the financial stocks, interest sensitive stocks, and quality growth stocks.

In hindsight, getting outlast summer was easy, but getting back in was almost impossible. Now that was the low; the last low of short to intermedi- ate-term significance. What was sentiment like at that low? You are going to have to remember; if you forget, you are going to have to relive history. This is because sentiment was unbelievably bearish at that low -- and it stayed that way almost all the way up. To give you an idea, let me just read this, which was written on September 20 because I was getting so much pressure from people about why we should be bearish. (Editor's Note: this now seems almost unbelievable -- ~10~ that the KJI has broken 1700).

"We set forth our 'not a bear market' case in considerable detail in last week's report. Nothing has changed since then, so we will not repeat our case here. We would like, however, to briefly respond to a few of the most common investor concerns. 1) Important uptrend lines have been broken. True. But this is not necessarily fatal -- especially given the lack of traditional bear market evidence (as we discussed last week); mid-1965 decline.

To see a classic example of this, look at the 2) The four-year cycle is bearish. Maybe -- but

there is also some strong evidence it may not be. 3) Institutional cash levels are very low. Also true, but this is usually the case during intermediate market declines (as opposed to bear markets). We still think, as we have since late last year, that there is more than enough cash available to support a significant advance in the hands of (a) the public (b) corporations and (c) (possibly) foreigners."

The thing to remember is that people were unbelievably bearish at the time of the last low, last September and they should be just as bullish at the next top. They aren't now. And until they get that way, I don't think you have an intermediate top.

So we got a good intermediate low last September. We then started a traditional rally sequence, which came in exactly the right order. It was led by defensive groups (the financial index, utilities, etc.) and quickly spread into quality growth stocks. Leadership then spread to the more cyclical ele- ments, as the Transportation average hit anew high. The next stop when you are going through a rally sequence, is usually the more speculative areas of market; finally, the last area to go up is the energy area (which doesn't seem to be doing that yet). So you are probably somewhere in the middle of the rally sequence now; where you start the sequence again really depends on how

21 KCAJaxnal&ay 1986

severe and how long the decline goes. I don't think the decline is going to be bad, as you'll hear in a minute, but if I'm wrong, and if the decline lasts longer than I think (if the market erodes away for a while, as it did last September), you may start the rally sequence back further towards the beginning of the leadership sequence -- the financial and quality.growth stocks -- rather than picking it up in the middle again.

As we rolled into 1986, the advance sort of got caught up in the turn-of- the-year cross-currents. On Tuesday, January 7th, the Dow broke free and made an all time high. It was a confirmed new high, which in technical lingo means that all the things -- the advance-decline line, financial index, etc. -- that were supposed to make new highs along with the broad averages did so. There were only two exceptions; the same ones that dogged the market during the whole November-December advance: the Transportation average (which, as it usually does, lagged and then caught up) and the one remaining divergence, the number of new highs , which was higher last spring thatitis now. Thus, onJanuary 7th you had a confirmed new high; there were no divergences waving all over the place. The important thing about that is that big declines don't usually begin from confirmed new highs; only short-term corrections begin from confirmed new highs.

Then, the next day -- Wednesday -- the market followed through on the upside, but then we got what we technicians call an "outside day," which means the market high that day was higher than the previous day, but then it turned all the way around and closed below the previous day's low. That's a significant reversal ; it's usually tough to go up above the prior day's high and then turn around and come all the way back down and close below the previous day's low. You did that Wednesday, though -- and you did it in a whole bunch of averages. That usually means it takes a while for the market to settle down afterwards, but the fact the we had a "record 39-point decline" (which the media all picked up) was really not all that significant. It was 2 l/2% declne; I can tell you about many 2 l/2% one-day declines. As a matter of fact, there was a 36-point decline on October 25th of 1982 - but it started at 1030, not 1570, so it was 3 l/2% instead of 2 l/2%. That one ended up being a 6.1% decline, on an hourly basis, that lasted about three days. The market then rallied, and came back to test the low three weeks later and again seven weeks later; then it was off and running again.

The 1982 decline came after a long advance without a correction -- as this last decline did. So short-term declines in bull markets can begin very suddenly, but then they don't usually follow through. So call this a short- term correction rather than something serious. It doesn't appear to be quite over yet. I don't want to get too short-term but the fact that we bounced off 1500 last week only lets me know that a lot of people still know how to divide by 100. The very short-term numbers were not particularly good last Wednesday, Thursday, and Friday, so technically it doesn't look like a terrific bottom. I would rather seethe market go down in continuing response to the decline in early January (in what I would call "aftershocks" to it) and break 1500. If youbreak 1500 you willsetupabetter bottom and have abetter advance than if you go up from here. This bottom is not as solid a bottom yet, by a long shot, as the one last Septe&er and October was.

22 Kl!A J-y 1986

The funny thing in all this was that the right decision in the last year, or more than a year , was to just stay bullish. Maybe you could have gotten out in July and August and gotten back in September and October, but I doubt it. That decline was an 8% decline (I was saying all along that it would be less than a 5% decline, which it was in the Dow-Jones, but that was fudged by General Foods. So call it an 8% decline). Can a major institution get out and get back in again in 8%? I don't know. The problem, too, was that there was a great hue and cry then about leadership shifting, and I suspect if you got out of the Bell operating companies and the regional banks then you never got back into them -- and that was more costly than avoiding an 8% decline. So where the market is now is a short-term correction in an angoing intermediate uptrend in an ongoing bull market in an ongoing secular bull market.

Where are we going? Is the bullmarketending? There don'tseemtobe any signs of a major top. There is IIO overspeculation. I was in Jerry Tsai's war room in 1968; I have seen what speculation looks like -- and "this ain't it." Nineteen sixty-eight was the time when the Amex tape ran more than half an hour late. Think about that; the Amex tape is so slow now they can rent 30- second commercials on it and sell advertising on there ("Merrill Lynch is bullish on America") - then report two more trades. Nineteen sixty-eight was also the time when the analyst who followed a stock called Parvin/Dohrmann' showed me a subpoena he had gotten. There were some shenanigans going on, and somebody wanted to talk to him. A couple of weeks later he got a second subpcena, leading to his sell rule: "When you get the second subpoena, sell!" There's nothing like that going on now; there's 1k0 overspeculation.

There also aren't any major divergences , which is usually the sign of a serious loss of momentum. Breadth is surprisingly good in here. The Transportation average has now.made a new high. The financial index has made a new high. Utilities are hanging. in there. So there are-no major divergences. There may be some short-term ones building up; maybe not. If you goback up from here without first going back under 1500 you may set up some shorter term divergences -- but nothing major.

Is there overconfidence here? No sir! I haven't had to tone anybody's enthusiasm down in the last year and I don't think I will have to start this afternoon. Sentiment is surprisingly shaky yet. Nobody believes the bull market is for real. Institutional brokers don't believe it. Public brokers don't believe it. The public doesn't believe it. Believe me -- the public doesn't believe it. I am in the market letter business now, and sometimes it generates some very good sentiment figures. Some of my cohorts have very heavy advertising budgets, and they know down to a hundredth of a percent what their response should be to a given ad they run in Barron's, or to a given 50,000 piece mailing. These are proven ads; the same ads they run over and over. When the market went up through 1400, their response rates (which had been running about half of normal) remained there until we got to 1500 -- at which point they fell off even further. The public just isn't coming in here -- and the various wirehouse trading figures show it. And institutions don't believe it either. That's why I went into the sentiment of last September in such detail. That was just an intermediate low, but everyone was very gloomy back then. By the time this bull market ends the majority of people will be long-' term bullish -- just the opposite of last fall. We have a long way to go

23 MpAJouad&iy 1986

before to get to that point.

I will mention two uncertainties here. Number one is this four-year cycle thing. Are interest rates going to stay low? They have stayed low for a long time now. I have no idea where interest rates are going; I have always followed interest rates because they tend to lead the stock market, and I like anything that leads the stock market. If the planet Venus led the stock market I would follow the planet Venus. But thequestion is whether interest rates can avoid going up before long, thus putting pressure on stocks? In other words, is there going to be a four-year cycle low this year, as scheduled? The other uncertainty is whether corporations will continue to buy their own stocks and acquire other companies at the same rate as a year ago. It looks like this trend is starting to slow down; if it does slow down, the question then is whether the public will take up the slack. The public has the bucks -- more bucks than anybody else. What they do with those bucks determines what a lot of financial markets - including the stock market - do. The public doesn't have to put the bucks directly in the stock market; they don't have to walk into their Merrill Lynch office and buy 100 shares of Cray Research. They can put the money into mutual funds, which then go into the stock market. But the question of public participation in the stock market is the imponderable.

With that, I think we can come up with some conclusions, and then I can answer some questions. Here are my conclusions. First, the major and intermediate trends are still up. However, 1986 is likely to be a much choppier year than 1985 was. This is partly why 1986 is going to make you long for 1985 before it's over. I know you didn't like 1985, but after this year is over 1985 will look better and better to you. Second, the odds are that there is going to be at least cne correction of more than 10 percent sometime during the year. Before that, though, since all the technical problems here seem to be very short-term in nature, there should be at least one more push to the upside. Third, the market is getting more specxawinnature. I suspect that this trend is going to continue, but I suspect that the big wave of speculation -- the sort of insane wave that is going to be even stronger than 1982-83 was -- is still out there a few years, rather than just around the comer.

Finally, as far as leadership is concerned, regrettably, this is the point in the market cycle when technicians have a hard time, because the leadership is so well established but is also very extended, and the market advance is also broad enough that there are literally hundreds of good looking stocks. During the last couple of days I have had a chance to look at a lotofcharts; I thought I would come up with all sorts of ideas, but ended with very few, since it is of no use to give you a list of 200 over-the-counter stocks that look very good (which I could easily do). How do you narrow the 200 stocks down? Anyway, the old conservative leadership - disinflation or deflation or whatever -- is still there; regional banks are still there, and insurance is still there. But they are very extended. If you don't awn them now you have a rough decision to make, because that's where your leadership is - ax-d it is as extended as can be. As far as new ideas, given the rotational nature of the market and the fact that we are getting a little bit more aggressive in nature - usually this combination of factors (the fact that the rotation has gotten beyond the financial and growth stocks, and has worked its way down towards the

24 MI!4 Jarmal/pfay 19%

more cyclical growth stocks, a nd the fact that you are also starting to pick up secondary stocks) -- the normal thing that is at the confluence of all these forces is technology. So I think if I were a research director I would have my technology analyst working very hard to uncover ideas. There are a lot of them that look interesting tichnically (again, most of them are extended); over-the- counter stocks like National Computer or Reynolds & Reynolds, for example. This is where you need fundamentals to sort them out ; a technician cannot do it for you. But I would be looking for ideas from the technology sector and the cyclical growth sector.

Energy stocks are laggards; they are traditionally the last ones to move during a rally. It is probably too soon to anticipate strength rotating there, but I would suspect that at some point during the year you are going to wish that you owned a bunch of energy stocks. I don't know when -- and I don't think it's tomorrow. But I think I would be looking for ideas in that area now. In other words, your decision now is when to sell a regional bank and go on to an energy stock. I don't think that point has come yet -- but at some point it probably will. And you will need to know then what to buy within the energy area: oils or oil service or gas or whatever; traditionally institutions used to think of the energy area as Schlumberger and Halliburton, but I suspect that there are going to have to be some oils in there this time -- and some of them will have to be overseas oils. And finally, with all this I see, the one thing that comes up as the beneficiaries of it is the stock brokers. If the public's coming back, I suspect brokers are going to make a buck or two. And I think the reason that brokerage stocks have not done well so far is simply because they are a barometer of institutional confidence; institutional confi- dence never got restored, and therefore brokerage stocks never went up. So I think that I would want to own a brokerage stock or two here (or a mutual fund management stock or two).

Before I conclude, I ought to give you the 86 pitfalls I promised the hard core bears at the beginning of my presentation. The 86 pitfalls -- the biggest pitfalls I see this year -- are the 52 money supply reports, the 30 stocks in the DowJones Industrial average , and your four quarterly performance reports.

Now to answer the questions I told you to keep in mind -- and remember there is no reason to be a hard core bear here. Is the trend up or down? Intermediate up, long term up. Is the movegainingor losing momentum? It appears to be losing it. After all, you're up 200 points in the Dow-Jones; you can't gain momentum in here, you're going to lose it - but it is dissipating

slowly. very Is the move broad or narrow? Surprisingly braad. Is it getting broader or more selective? It is remaining surprisingly broad; it has not narrowed all that much yet. When it starts to narrow, probably the first to drop by the wayside will be the conservative leaders such as the financial and utility stocks. Is the move speculative or conservative? At the moment it is not too speculative; it looks like it's getting more speculative; we'll have to see how speculative it gets over the next couple of months. I think it will be more speculative, but I don't think that it will be the big speculative push. I will say this, though: this is a secular bull market; ithasn'ttopped out. No portion of the market has topped out - including the NASDAQ Industrials, which is still well below its 1983 all time high. The NASDAQ Composite index hit a new high this month, but I follow the industrial index because it doesn't

25 MA J-Y 1986

have banks and insurance companies in it, so it is a much better proxy for smaller growth stocks. The NASDAQ industrial average at the moment is about 330 and its all time high is about 420; I don't think that will be its all time high by the time this bull market is over. Percentagewise, that gives you a fair amount on the upside. Finally, where is the leadership here? In the same old places: the same old insurance group, the same old Digital Equipment, or whatever. I see no real change in leadership here -- except I think it will get more aggressive.

With that, I will stop and see if anybody has any questions.

Questions

The question is do I have an updated nifty-fifty growth stock index? The answer is no. It's funny; when I was at Putnam my big boss asked me the exact same question, because we were following a nifty-fifty index at the time. I quickly assured him that our index was not up to date. He was disappointed - until I explained that if I knew when Eadd a stock to the nifty-fifty index, and when to remove stocks that were already in it, he wouldn't need any portfolio managers. What I am trying to do with my growth stock index is to measure what proven growth stocks are doing in the market (as opposed to emerging growth stocks), so I am sticking with my growth stock index -- which is still a good leading indicator of the market. This is because if you decide the market is going up, the first thing you buy is IBM, not some little over- the-counter stock. That happens the next day.

"What are some leading indicators that will tell us when individuals are coming back into the market?" Probably the brokerage house trading statistics - plus the fact that when people talk to you at cocktail parties, instead of walking away when you tell them you're in the investment business, they ask you what you would buy instead. I think they are just now starting to do this, but they are certainly not doing it very frequently. As far as the brokerage house figures are concerned, I tend to follow the Merrill Lynch figures more closely than I do the others simply because I calculated and plotted them back in the 1960's, so I got more familiar with them than anything else. The general public, according to those figures -- and others -- has generally been disinte- rested in the market during the last year. They have shown a flicker of interest during the lastcoupleof weeks, but they are certainly not rampant buyers at this point. I think the public will come back into mutual funds before they come into individual stocks, though.

"DO you have forecasts on overseas' markets and currencies?" No. The reason I don't do work on foreign markets or foreign currencies is that my whole approach to analyzing the stock market is to find things that lead the stock market, and then to use those things that lead the stock market to predict what the stock market is going to do. These "things" are concentrated pretty heavily in sentiment factors. I have difficulty finding leading techni- cal indicators in those other markets, and therefore I let other people worry about them.

"What impact are options' arbitrage programs and the like having on tech- nical analysis?" They are increasing the sales of Maalox considerably. As I

26 KQi Jourd&ay 1986

understand it, you literally have to be sitting on a trading desk to do these programs, and what triggers them can be an almost instantaneous price movement. I think these programs are accelerating moves, particularly from a short-term standpoint, but I'm not sure they have that much of an effect on long-term mves .

','Have you thrown away any traditional technical indicators and replaced them with new ones?" Yes; I have thrown away a lot of indicators, but I haven't been able to replace them with that many new ones that are coming along. It makes life very difficult. For example, the whole short-selling spectrum of indicators may have gotten mucked up by those arbitrage activities, but most of them still seem to be working okay -- and the ones on the American Stock Exchange seem not to be distorted much at all. The problem with the Amex figures is that you can't always get them on a timely basis,and there are a lot more mistakes in them than there should be. I have, unfortunately, had much less success finding new indicators to replace the old ones that are thrown away. I will say that, whatever its problems, the put/call ratio seems to be a pretty good sentiment indicator, even with all this arbitrage activity that is taking place. I spent a couple of days on my computer breaking the put/call ratio down into index and non-index ratios, and I finally decided that it was really a waste of time -- that the plain old put/call ratio worked best of all.

Thank you.

A presentation to the Boston Security Analysts Society, January 27, 1986. Walter R Deemer is a member of the Market Technicians Association and is the President of Deemar Technical Research.

27

by Kenneth Safian

Overview of Safian F&search, Inc.

Safian Investment Research provides the institutional money manager, both here and abrmd, with a research service totally dedicated to analyzing and forecasting stock market and ecoRomic trends.

A uniqueaspect ofourfirm , and an underlying thesis to our analysis, is that the stock market is not homogeneous, but rather is compromised of major sectors each of whose movements reflect the divergent trends present in the economy. This sectoralization -- of the economy and stock market - is the thrust of our research effort. Importantly, a combination of original fundamental and technical considerations is incorporated within our analysis.

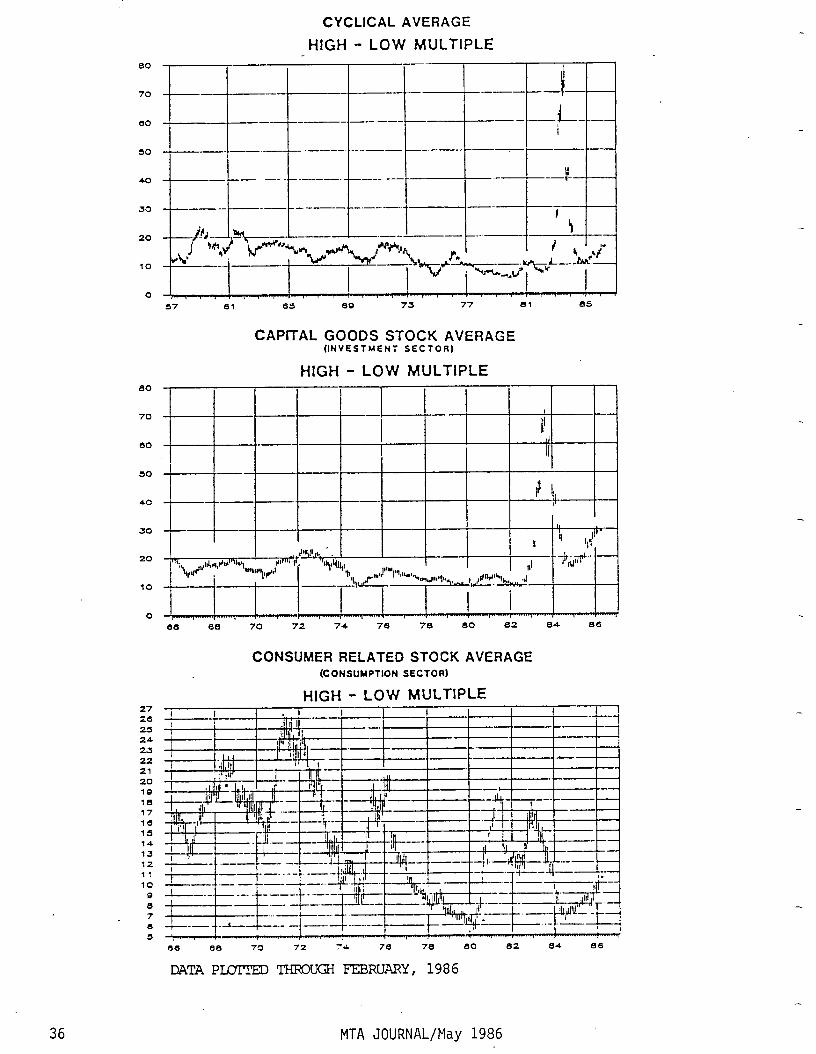

Nearly twenty-five years ago, the principal of our firm co-introduced what we believe was the second major attempt to sectoralize the stock market (the first having been accomplished by Charles Dow in the late 1800's). This segmentation divides the stock market into two major sectors - Growth and Cyclical. The approach has been particularly useful in identifying major divergences which have occurred in the market such as the 1964-1973 period when growth-related stocks outperformed cyclical-related securities, 1588 to 88.

This dichotomy between sectors of the market was further confirmed by earnings and prioe earnings multiples data, which cr>ntinue to be maintained on a sector basis. The Earnings Divergence Ratio in particular has proven very valuable in signaling when shifts between sectors are most likely to occur.

In addition, we analyze macroeconomic, technical, political, and demogra- phic trends as they relate to the stock market. After determining which sectors appear to be most attractive, we look to select within those sec- tors those major companies which appear relatively undervalued.

ccxporate Profits -AnEvaluatial- 4th Quarter 1985 Data

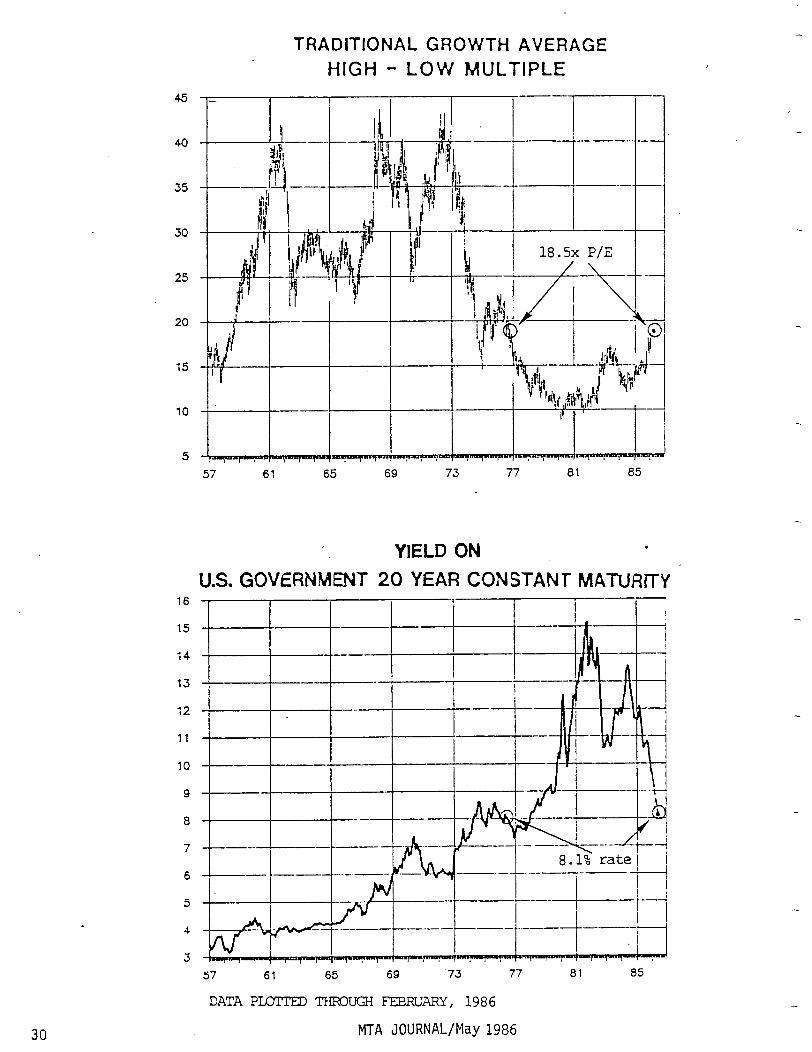

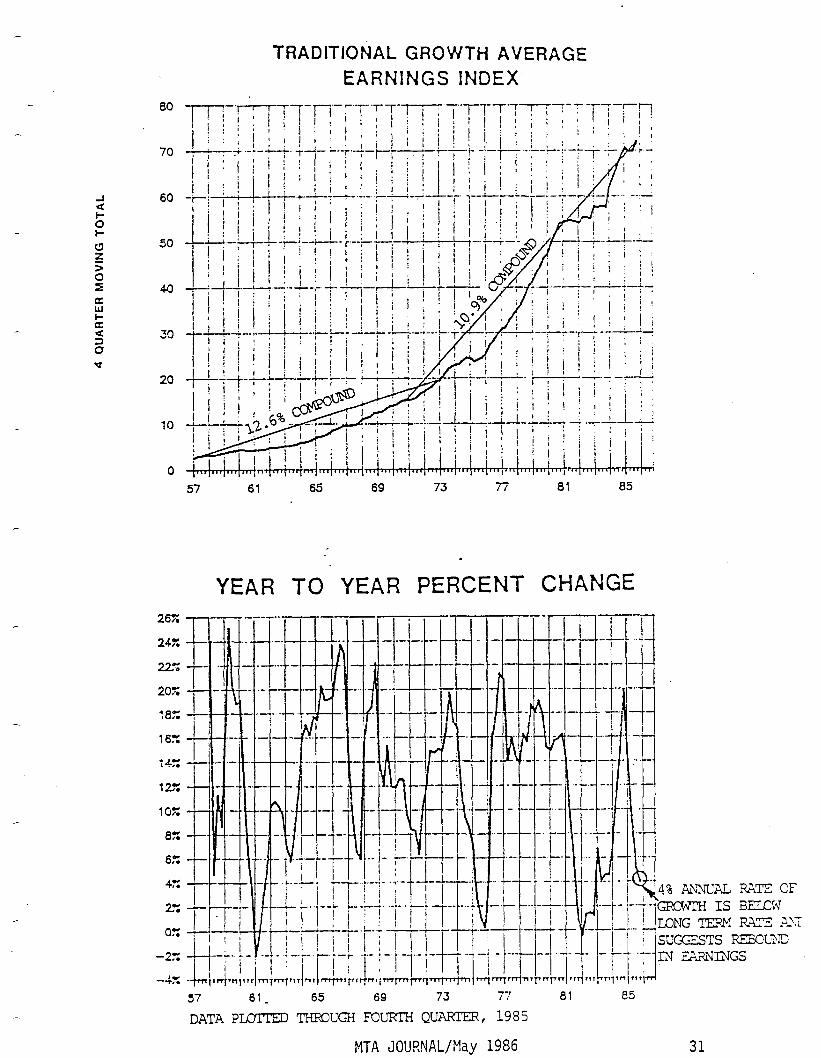

The earnings of our Traditional Growth Average over the past 15 years have grown at a 10.9% compounded rate compared to 12.7% for the lS-year period which ended in 1972. In1972 year end, our Growth Index sold at about 40 times earnings and at the end of last year it sold at 17 times the four quarter trailing profits. The yield cc1 long term U.S. Government bonds was less that 6% in the earlier period compared to 9.75% in December 1985. If interest rates were the same in December 1985 as they were at the end of 1972, we would expect the price/earnings multiple for our growth average to be lower in the more recent period due to the lower rate of growth in earnings.

28 KCA Joumd/HaY 1986

Since the return on government bonds is in the same area today as it was in the 1974-1975 period and since the annual rates of growth in earnings are also at a similar level, then multiples should also be approximately the same, which is the case. (See pages 30 and 31 and circled periods). This reveals to us that both growth stock prices and bond prices are in sync and that it will take higher earnings growth to keep prices rising in the event interest rates do not decline significantly from these levels.

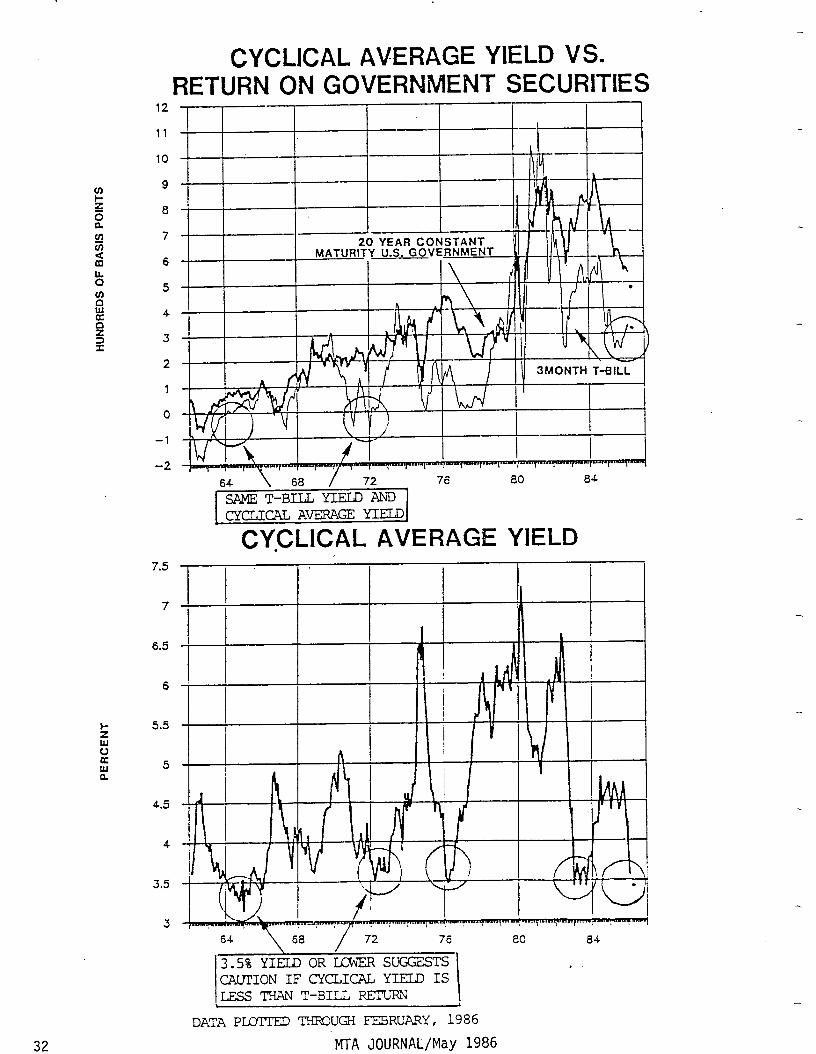

Price to earnings ratios for Cyclical companies, as noted in our past studies, do not seem significant unless normalized earnings are used. Such earnings projections require quite a few assumptions. The yield relation- ship for cyclical companies, however, has been very helpful in determining when stock prices have discounted earnings increases for this group of companies. Typically, a 3 l/2% dividend return has been quite low for our Cyclical Average. This dividend yield must also be viewed in conjunction with the rate of returns on treasury bills and long termbonds. In early 1964 the Cyclical Average dividend yield was below 3 l/2% but the return on treasury bills was the same as cyclical stocks suggesting little downside risk in the event earnings declined and short-term interest rates remained the same. This is not the case currently since treasury bill rates are about 3% higher than the dividend yield for our Cyclical Average Page 32).

Given these data, itseemsthatstock prices are generally vulnerable in the event earnings do not rebound sharply in coming quarters. We do expect corporate profits to rise primarily due to lower interest costs, reduced operating outlays, large write-offs, weakness in the dollar, and greater financial leverage within corporations. Three of our four Averagesdid show higher earnings in the fourth quarter than the third quarter with the exception of our Capital MS Average (Pages 33 to 36). Corporate profits after taxes recorded a similar rising pattern (Page 37). Thus, unless interest rates decline further, we would expect a more selective advance in equity prices,as disappointing earnings statements for individual companies penalize holders of those shares while the reverse is the case for those firms which are able to exceed analysts' earnings projections.

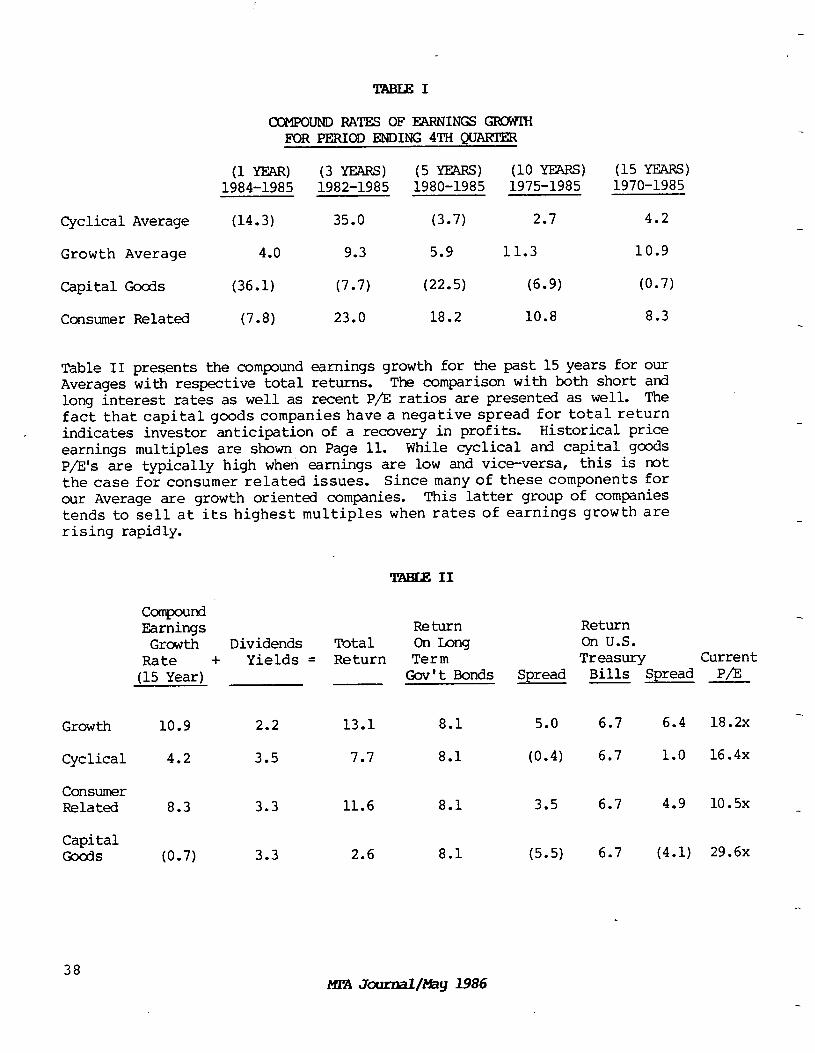

Table I presents compound rates of growth for the earnings of our Averages over varying time periods and clearly shows the relatively low rates of earnings growth for 1985. Growth companies were the only ones to show gains in profits in the year of the four categories we maintain. The divergence in the rate of change for earnings for the different time periods vividly expresses the basis for quity price disparity in recent years.

29

TRADlTfONAL GROWTH AVERAGE

HIGH - LOW MULTIPLE

30 MTA JOURNAL/May 1986

16

15

14

13

12

11

10

9

a

7

6

5

4

3

61 65 69 ai a5

YIELD ON .

U.S. GOVERNMENT 20 YEAR CONSTANT IMATURiTY

- , , , , , , , , , , , .

57 61 65 69 '73 77 ai a5

DATA PL#ITED THROUGH FEBRUARY, 1986

TRADITlOtiAL GROWTH AVERAGE

EARNINGS INDEX

60

26Z

24%

225

20x

1az

16::

14%

12::

10%

a:: 6P;

4::

2.

0.7

-2z

-4::

-i-i-i-1-~/-1-... __,-

57 61 65 69 73 77 ai a5

.

YEAR TO YEAR PERCENT CHANGE

57 61_ 65 69 73 77

DATA PLLXTED THFXXa -KX’RTH QU-, 1985

MTA JOURNAL/May 1986

81 a5

31

12

11

10

9

0

7

6

5

4

3

2

1

0

-1

-2

7.5

7

6.5

6

CYCLlCALAVERAGEYlELD VS. RETURNONGOVERNMENTSECURITIES

I I

3MONTH T-BILL

SAN T-BU;L YIELD AI'D CYCLICALA~GEYIELD

CY.CLiCAL AVERAGE YIELD

64 \ 68 / 72 76 60 84 \

13.5% YIELD OR ihER SUGGESTS 1 CYCLICAL YIELD IS

T-BILL FEt'LL?L?J I

32

DATA PLD-!XED TJXDJGH FEBRUARY, 1986

MTA JOURNAL/May 1986

16

1.5

14

13

12

11

10

9

0

7

6

5

4

3

2

1

CYCLICAL AVERAGE

EARNINGS INDEX

57 ' 61 65 69 i3 n 81 a5

YEAR TO YEAR PERCENT CHANGE -

I

b-TM

- _. - -. ..-

1 i

- -----.- _ .._- -

!

. -. . .-

‘/

‘-I,;;l

;, --i-,!J

j

2-v-e _ -.-- - ._- .-. _..

I 1

1 - _-

;41i’ irili’.l.il

j -’

l-qTqqm.,r ‘. r

97 61 65 69 73 7i

DATA PLDITED THBOUGI FOURTH QU-, 1985

MTA JOURNAL/May 1986

81 8.5

33

160

t 80

60

CONSUMER RELATED STOCK AVERAGE (O~NSUMPTI~N SECTOR)

EARNINGS INDEX .- -j--~;--~~--~-y--~-‘ ;--1--r -r- -y

!n. r I

66 68 70 72 74 76 78 80 82 84

YEAR TO YEAR PERCENT CHANGE - ---

i-n-- --‘---f. .-.i e-e. I -_ - ___- i...

11

___*_- 1 ! . . .- -. .-- - -.- -- - .-, - - .I -

’ I ._ _.- --! .-..- -- .-.. ;;!

_ - _ 1. ..I--. . ..I r ..-. .-

__I 1 r----- --- --. ..I . .._.. +-be. _I -f - -. -. I I -. _ --. w--y i j -. .

1 i ;y.;.- ._ t _ ._.. -c.- -- -- , - - I- - 4 111 _ ._ __ - - . .__-

--_- .

--.-. --- .--I -_- .- .--I-- - .-. -. -- .- - I

j --. - ._. _- 1-

~

_ . . .- -. _- _ J .- .- -.

1 7-l. 7.T 72 74 76 78 80 82 8-:

-_---. -- --. .---.-. I . ..- 1 ‘d . _. -. . .- _. _

1 1 -.

_. . ..I-.- 1 1

- ._ --_.. .-.-.-. .

-a[. . ,_ / . .- __ i. .-.

Pi*.-.~--- g -‘I

.__, . -- - r-- -. -- .!

-- I ! .- cm__ _ .- . .

! l

-- r- - ..-

’ i

_ _. _-..-

ntt-r-v 7-l ,‘”

34 MTA JOURNAL/May 1986

DATA E'IMIrI'ED THROUGH FOURTH QUARER, 1985

CAPiTAL GOODS STOCK AVERAGE

240

230

220

210

200

190

180

170

160

150

l-40

130

120

110

100

90

80

70

60

50

40

30

20

220%

200%

180%

160X

14X

120::

100%

80%

60%

40%

20%

OX

-20::

-40%

-69%

-80::

-100%

(INVESTMENT SECTOR)

EARNINGS INDEX

-LA- .!iL.i--, .____ #!--i-l-r--~

’ ’ ! 1 -:- -i.- ! ; ! i ! i i i I I ! -iv ; L--J:

YEAR TO'YEAR PERCENT CHANGE

. 66 68 70 72 74 76 78 80 82 84