joyce e. berg, forrest d. nelson george r. neumann thomas

TRANSCRIPT

1

Joyce E. Berg,Forrest D. NelsonGeorge R. NeumannThomas A. Rietz

Note: References are in the handout “Research Bibliography”

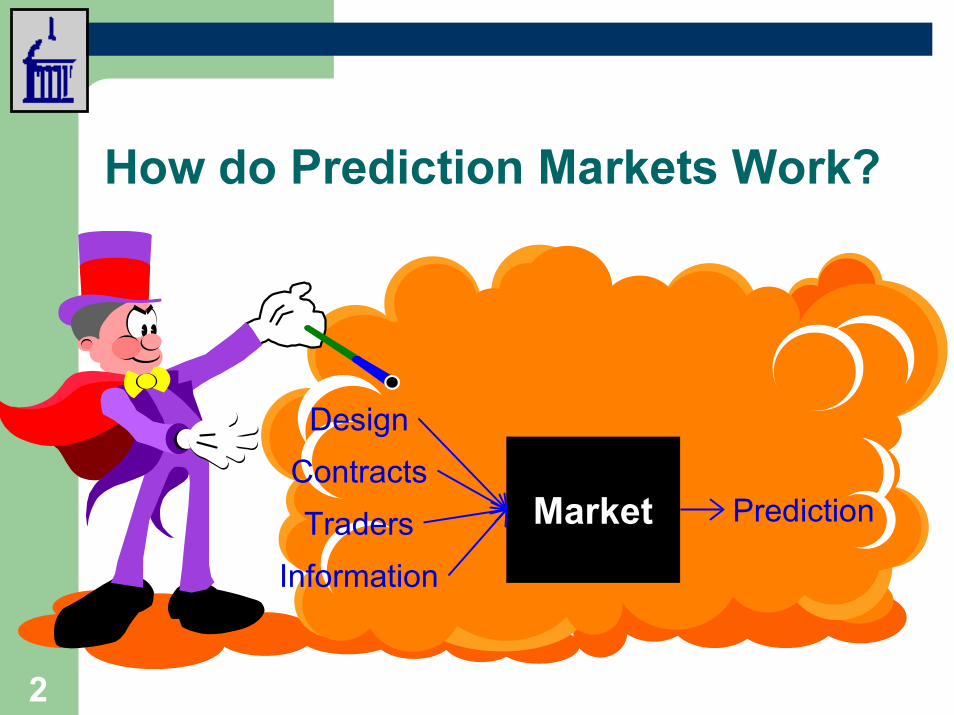

2

MarketInformation

Design

TradersContracts

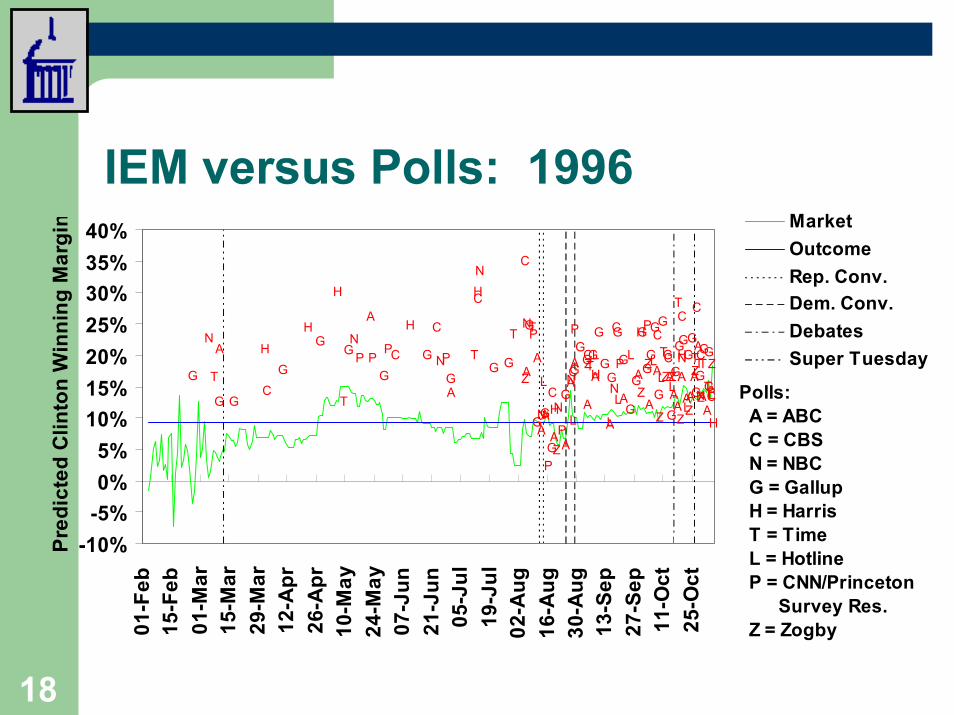

Prediction

3

� Accuracy� Polls and Markets� Market Dynamics� Forecast Standard Errors� Trader Characteristics� Trader Interaction� Biases and Small Markets� Other Arenas� Opportunities and Issues

4

� At short horizons, prices are accurate and unbiased predictors

– Berg, Forsythe, Nelson and Rietz, 2001– Berg and Rietz, 2001a

� At long horizons, bid/ask midpoints are efficient forecasts

– Berg, Nelson and Rietz, 2001� Incentives matter

– Gruca, Berg and Cipriano, 2002– Camerer and Hogarth, 1999

5

Berg, Forsythe, Nelson and Rietz (2001)

0

10

20

30

40

50

60

70

80

90

100

0 10 20 30 40 50 60 70 80 90 100Actual Outcome (%)

Pred

icte

d O

utco

me

(%)

US Presidential ElectionsAvg. Abs. Err. = 1.37%(5 Markets, 12 Contracts)Other US ElectionsAvg. Abs. Err. = 3.43%(14 Markets, 50 Contracts)Non-US ElectionsAvg. Abs. Err. = 2.12%(30 Markets, 175 Contracts)

6

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

.00-.20 .20-.40 .40-.60 .60-.80 .80-1.00

Price Range

Pred

icte

d an

d Ac

tual

Fre

quen

cy

IEM Price Payoff

Berg and Rietz, 2002a

7

� At short horizons, markets are on par with polls– Berg, Forsythe, Nelson and Rietz, 2001

� At long horizons, markets outperform polls– Berg, Nelson and Rietz, 2001

� Polls do not drive the market, the market leads polls according to Granger tests

– Forsythe, Nelson, Neumann and Wright, 1992

8

Berg, Forsythe, Nelson and Rietz (2001)

0.0%0.5%1.0%1.5%2.0%2.5%3.0%3.5%4.0%4.5%5.0%

88 U

S P

res.

92 U

S P

res.

(2w

ay)

92 U

S P

res.

(3w

ay)

96 U

S P

res.

00 U

S P

res.

95 A

ustr

ia

96 A

ustr

ia (E

P)

90 D

enm

ark

95 F

ranc

e

90 G

erm

any(

B)

90 G

erm

any(

F)

90 G

erm

any(

L)

94 G

erm

any

98 G

erm

any

91 T

urke

y

Ave

rage

Mea

n A

bsol

ute

Err

or

Final PollsMarket-Election eveMarket-Last Week

9

(Berg, Nelson and Rietz, 2001)

Z

Z

ZZ

ZZ

Z

Z

Z

Z

Z

ZZ

T

TTTT

T

TTT

T

T

T

P

P

P

P

P

P

PP

PP

P

N

NN

NN

N

N

N

NN

NL

LLLL

L

L

L

L

LL

H

H

H

H

H

H

H

HH

H

G

G

GG

GG

GG

G

G

G

G

G

G

GG

G

G

G

G

G

GG

G

GGG

G

G

G

GG

G

GGG

GG

GG

G

GG

G

GC

CC

CC

C

CC

C

C

C

C

C

C CA

A

A

AAA

A

AA

AA

A

A

A

A

A

A

AA

AA

AA

AA

A

A

A

-10%-5%0%5%

10%15%20%25%30%35%40%

01-F

eb15

-Feb

01-M

ar15

-Mar

29-M

ar12

-Apr

26-A

pr10

-May

24-M

ay07

-Jun

21-J

un05

-Jul

19-J

ul02

-Aug

16-A

ug30

-Aug

13-S

ep27

-Sep

11-O

ct25

-Oct

Pred

icte

d Cl

into

n W

inni

ng M

argi

n MarketOutcomeRep. Conv.Dem. Conv.DebatesSuper Tuesday

Polls: A = ABC C = CBS N = NBC G = Gallup H = Harris T = Time L = Hotline P = CNN/Princeton Survey Res. Z = Zogby

10

Berg, Nelson and Rietz, 2001

� The market dominates polls at long horizons

Days included in sample Item 1988 1992 1996 2000 all years

All (from the beginning of the market

Number of pollspoll “wins”

market “wins”% market

p-value (1sided)

59 25 34

58% 0.148

151 43 108 72% 0.000

157 21 136 87% 0.000

229 56 173 76% 0.000

596 145 451 76% 0.000

Last 100 Number of pollspoll “wins”

market “wins”% market

p-value (1sided)

45 24 21

47% 0.724

82 23 59

72% 0.000

124 18 106 85% 0.000

180 54 126 70% 0.000

431 119 312 72% 0.000

11

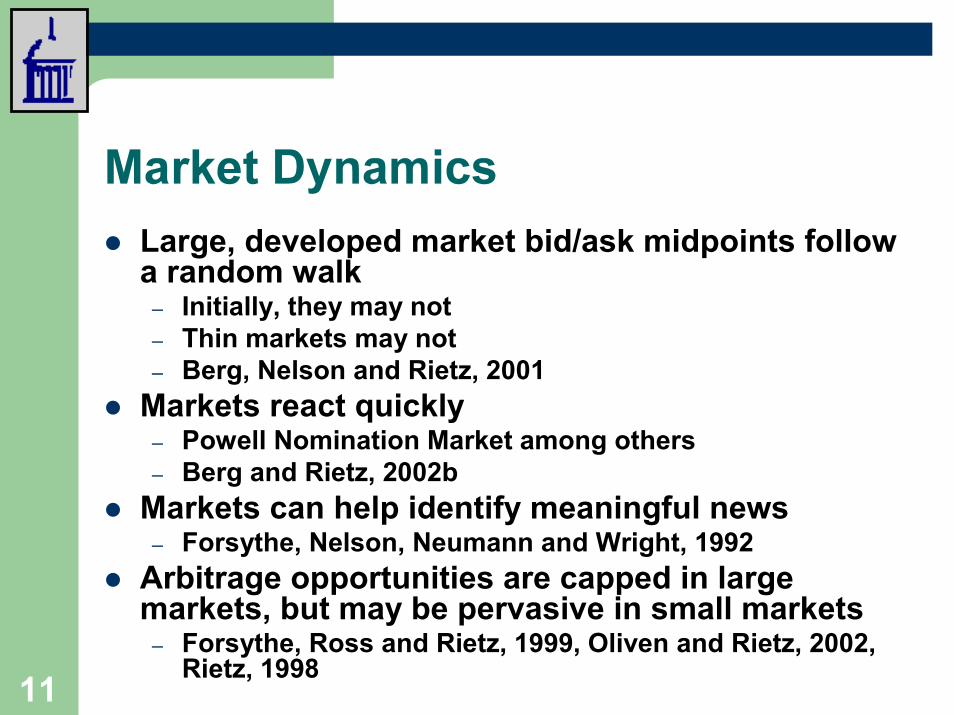

� Large, developed market bid/ask midpoints follow a random walk

– Initially, they may not– Thin markets may not– Berg, Nelson and Rietz, 2001

� Markets react quickly– Powell Nomination Market among others– Berg and Rietz, 2002b

� Markets can help identify meaningful news– Forsythe, Nelson, Neumann and Wright, 1992

� Arbitrage opportunities are capped in large markets, but may be pervasive in small markets

– Forsythe, Ross and Rietz, 1999, Oliven and Rietz, 2002, Rietz, 1998

12

NLLS versus Time Series Estimation Results (Berg, Nelson and Rietz, 2001)

Election Year Item 1988 1992 1996 2000

OLS/Bootstrap Time Series Estimates Constant -0.0011 0.0031 0.0077 0.0001

Robust Std. Err. 0.0007 0.0014 0.0056 0.0009 Lagged Spread 0.9874 0.9282* 0.9312 0.9480

Robust Std. Err. 0.0189 0.0316 0.0547 0.0411 Bootstrap Std. Err. 0.0185 0.0882 0.0948 0.0870

NLLS Estimates Lagged Spread 1.0149 1.0028 1.0093

Robust Std. Err. 0.0068 0.0014 0.0073 Z-Test vs Bootstrap -0.9804 -0.7552 -0.7021

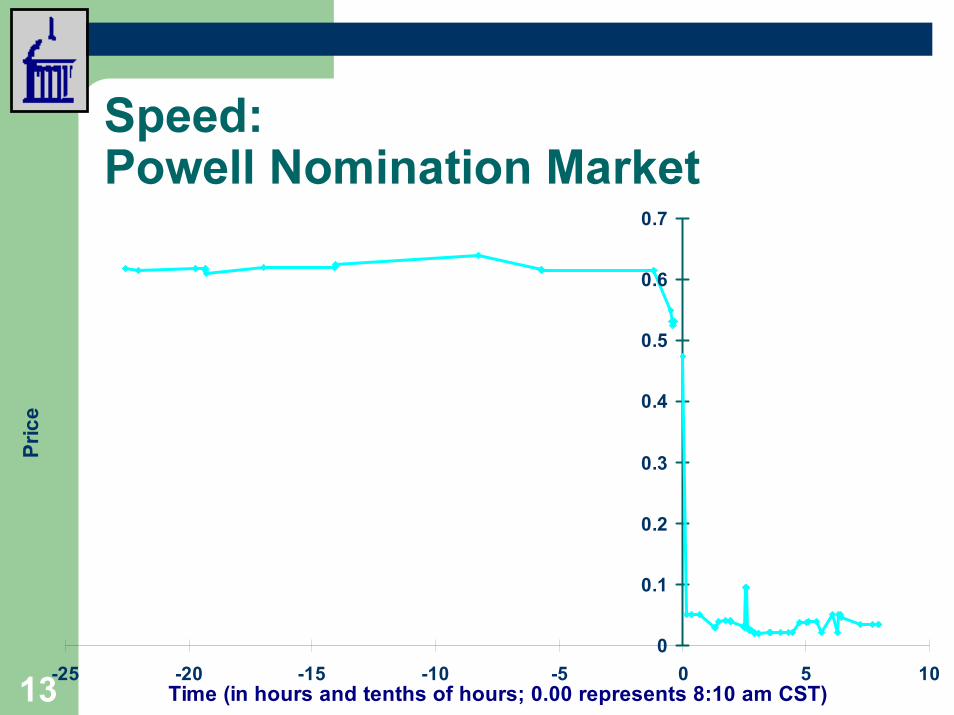

130

0.1

0.2

0.3

0.4

0.5

0.6

0.7

-25 -20 -15 -10 -5 0 5 10Time (in hours and tenths of hours; 0.00 represents 8:10 am CST)

Pric

e

14

Berg, Nelson and Rietz, 2001

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1/1

1/8

1/15

1/22

1/29 2/

52/

122/

192/

26 3/4

3/11

3/18

3/25 4/

14/

84/

154/

224/

29 5/6

5/13

5/20

5/27 6/

36/

10

Pred

icte

d Vo

te S

hare

Events D&R Final Perot D&R

Pero

t “D

rops

”

Dem

. C

onv.

Pero

t Ent

ers

Rep

. Con

v.

Deb

ates

15

� Since markets follow a random walk, forecast standard errors increase at approximately root-t

– Berg, Nelson and Rietz, 2001� Inter-market relationships also show this

– Berg, Nelson and Rietz, 2001

16

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

7/30

8/13

8/27

9/10

9/24

10/8

10/2

2

11/5

Dem

-Rep

Vot

e Sh

are

Market PredictionActual95% Conf. (Random Walk)95% Conf. (AR(1))95% Conf (Imp. Volatility)95% Conf. (Fitted AR(1))

Random Walk Sigma: 0.85%

Call election for Bush10/29 (-9 days) &

11/6 (-1 day)

17

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

7/28

8/11

8/25 9/

8

9/22

10/6

10/2

0

11/3

Dem

-Rep

Vot

e Sh

are

Market PredictionActual95% Conf. (Random Walk)95% Conf. (AR(1))95% Conf (Imp. Volatility)95% Conf. (Fitted AR(1))

Random Walk Sigma: 0.75%

Call election for Clinton9/14 (-52 days)

18

Z

Z

ZZ

ZZ

Z

Z

Z

Z

Z

ZZ

T

TTTT

T

TTT

T

T

T

P

P

P

P

P

P

PP

PP

P

N

NN

NN

N

N

NNN

NL

LL

LL

L

L

L

L

LL

H

H

H

H

H

H

H

HH

H

G

G

GG

GG

GG

G

G

G

G

G

G

GG

G

G

G

G

G

GG

G

GGG

G

G

G

GG

G

GGG

GG

GG

G

GG

G

GC

CC

C

CC

CC

C

C

C

C

C

C CA

A

A

AAA

A

AA

AA

A

A

A

A

A

A

AA

AAA

A

AA

A

A

A

-10%-5%0%5%

10%15%20%25%30%35%40%

01-F

eb15

-Feb

01-M

ar15

-Mar

29-M

ar12

-Apr

26-A

pr10

-May

24-M

ay07

-Jun

21-J

un05

-Jul

19-J

ul02

-Aug

16-A

ug30

-Aug

13-S

ep27

-Sep

11-O

ct25

-Oct

Pred

icte

d C

linto

n W

inni

ng M

argi

n MarketOutcomeRep. Conv.Dem. Conv.DebatesSuper Tuesday

Polls: A = ABC C = CBS N = NBC G = Gallup H = Harris T = Time L = Hotline P = CNN/Princeton Survey Res. Z = Zogby

19

� A representative sample is not necessary – Forsythe, Nelson, Neumann and Wright, 1992, Forsythe,

Ross and Rietz, 1999, Berg, Nelson and Rietz, 2001� Many traders are biased

– Forsythe, Nelson, Neumann and Wright, 1992, Forsythe, Ross and Rietz, 1999

� Large markets overcome this– Forsythe, Nelson, Neumann and Wright, 1992, Forsythe,

Ross and Rietz, 1999� Small market may not

– Forsythe, Ross and Rietz, 1999

20

� Traders self-select into roles– Forsythe, Nelson, Neumann and Wright, 1992, Forsythe,

Ross and Rietz, 1999, Oliven and Rietz, 2002� “Marginal” traders seem less affected by bias

– Forsythe, Nelson, Neumann and Wright, 1992, Forsythe, Ross and Rietz, 1999

� Market makers seem more rational– Forsythe, Ross and Rietz, 1999, Oliven and Rietz, 2002

21

� Small markets may be more affected by irrationality and biases

– Forsythe, Ross and Rietz, 1999, Oliven and Rietz, 2002, and Rietz, 1998

� Market structure matters– Protects traders from their own mistakes and minimizes

impact on prices in large markets– Oliven and Rietz, 2002

� WTA markets may have a slight overconfidence bias at intermediate horizons

– Berg and Rietz, 2001a

22

� Markets have been run successfully in:– Accounting projections

� Berg, Dickhaut, Hughes, McCabe and Rayburn, 1995– Movie box office projections

� Gruca, 2000, and Gruca, Berg and Cipriano, 2002 � Hollywood Stock Exchange

– Corporate sales� Plott, 1999

– Completion dates� Ortner, 1997 & 1998

– Conditional markets� Berg and Rietz, 2002b

23

Berg and Rietz, 2002b

� Could markets tell us about things that may or may not happen?

� Examples: – Would Powell have won if he ran against Clinton in 1996?– Was Dole the right candidate to run against Clinton?– Will this movie idea be a blockbuster?– Will a terrorist attack occur and, if so, under what National

Security Threat Level?� Combinations of regular and conditional markets

can help answer such questions

24

� Republican nomination (event probability) market – Question: Who will win the Republican nomination?– Contracts

� Dole: $1 if Dole is the Republican nominee� Forbes: $1 if Forbes is the Republican nominee� Etc.

� Presidential winner-takes-all (event probability) market

– Question: Who will win the Presidency?– Contracts

� Clin: $1 if Clinton wins the popular vote� OTDem: $1 if another Democrat wins the popular vote� Rep: $1 if a Republican wins the popular vote� Other: $1 if another candidate wins the popular vote

25

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2/4/19

96

2/11/1

996

2/18/1

996

2/25/1

996

3/3/19

96

3/10/1

996

Fore

cast

Pro

babi

litie

s fo

r Dol

e's

Nom

inat

ion/

Perc

ent o

f Del

egat

es

Com

mitt

ed to

Dol

e

0.42

0.44

0.46

0.48

0.5

0.52

0.54

Fore

cast

Pro

babi

litie

s fo

r Clin

ton

Elec

tion

Win

Dole Win Nomination Dole Percent of Delegates Clinton Win Election

26

� Conditional Vote Share Market– Contracts

� V.DOLE: $1 * Doles vote share if Dole is nominated� CL|DOLE: $1 * Clinton’s vote share against Dole if

Dole is nominated� V.FORB: $1 * Forbes vote share if Forbes is nominated� CL|FORB: $1 * Clinton’s vote share against Forbes if

Forbes is nominated� Etc.

� Prices predict conditional vote shares

27

Republicans vs. Clinton

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2/4/

1996

2/6/

1996

2/8/

1996

2/10

/199

6

2/12

/199

6

2/14

/199

6

2/16

/199

6

2/18

/199

6

2/20

/199

6

2/22

/199

6

2/24

/199

6

2/26

/199

6

2/28

/199

6

3/1/

1996

3/3/

1996

3/5/

1996

3/7/

1996

3/9/

1996

3/11

/199

6

3/13

/199

6

Date

Rep

ublic

an V

ote

Mar

gin

Dole Alexander Forbes GrammOther Max Others Avg. Others

LA IA NH DEAZ, ND & SD SC

Multi.2

Multi.1

Primaries and Caucauses

NY

28

� Powell nomination (event probability) market – Question: Will Powell’s name be placed in nomination at

the 1996 Republican Convention?– Contracts

� P.YES: $1 if Powell’s name placed in nomination� P.NO: $1 if Powell’s name not placed in nomination

� Presidential winner-takes-all (event probability) market

– Question: Who will win the Presidency?– Contracts

� Clin: $1 if Clinton wins the popular vote� OTDem: $1 if another Democrat wins the popular vote� Rep: $1 if a Republican wins the popular vote� Other: $1 if another candidate wins the popular vote

29

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

9/1/

1995

9/8/

1995

9/15

/199

5

9/22

/199

5

9/29

/199

5

10/6

/199

5

10/1

3/19

95

10/2

0/19

95

10/2

7/19

95

11/3

/199

5

11/1

0/19

95

11/1

7/19

95

11/2

4/19

95

Date

Fore

cast

Pro

babi

litie

s fo

r Po

well's

Nom

inat

ion

0.400.420.440.460.480.500.520.540.560.580.60

Fore

cast

Pro

babi

litie

s fo

r Cl

into

n El

ectio

n W

in

Powell Nomination Clinton Win

30

� The good news:– Markets are good information aggregators

� Absolutely� Relative to next best alternative

– Markets seem to be good forecasters– Markets can even tell us about what might have been

� Caveats and Issues– Incentives and market structure important– Subject pool important

� Markets can only aggregate what’s known– Traders make mistakes and display biases

� Do they affect markets and, if so, when and how?– Small markets