june2015 atlanta actuarial club presentation - individual annuity overview

TRANSCRIPT

INDIVIDUAL ANNUITY OVERVIEW

Winter Liu FSA, CFA, FRM

Atlanta Actuarial Club 2015 Spring Luncheon June 10, 2015

Agenda

18/04/2023 2

Sales trend

Product overview

Post 2008 product development

Change in market landscape

Glossary

18/04/2023 3

BB – benefit base

BV – book value (FDA)

DIA – deferred income annuity

FDA – fixed deferred annuity

FIA – fixed indexed annuity

GMxB – guaranteed minimum xxx benefit

GLWB – guaranteed lifetime withdrawal benefit

IA – indexed annuity, same as FIA

IVA – immediate variable annuity

MVA – market value adjustment (on FDA)

SPIA – single premium deferred annuity

VA – variable annuity

VIA – variable indexed annuity

U.S. Individual Annuity Sales Trend

18/04/2023 4

2008 Variable 2014 VariableCompany Share Company ShareTIAA 9% Jackson National 16%MetLife 9% Lincoln 9%ING 9% AIG 9%AXA 9% TIAA 9%Lincoln 7% Transamerica 7%Prudential 6% Prudential 7%John Hancock 6% AXA 7%AIG 5% MetLife 4%Hartford 5% Nationwide 4%Pacific Life 5% Riversource 4%Riversource 5% Pacific Life 3%Jackson National 4% New York Life 3%Other 20% Other 16%

Overall annuity sales held relatively steady since the Great Recession

VA recovered somewhat but still far below the 2007 record; some major players quit

Fixed annuity sales ballooned during the 2008 crash, partly due to liquidity driven incentives

Fixed annuity saw steady growth lately due to popularity of indexed annuity

2007 2008 2009 2010 2011 2012 2013 2014 -

50

100

150

200

250

300

184 156

128 141 159 147 145 140

67 103

105 76 76

67 79 90

U.S. Annuity Sales ($billions)

VA Fixed

Source: LIMRA

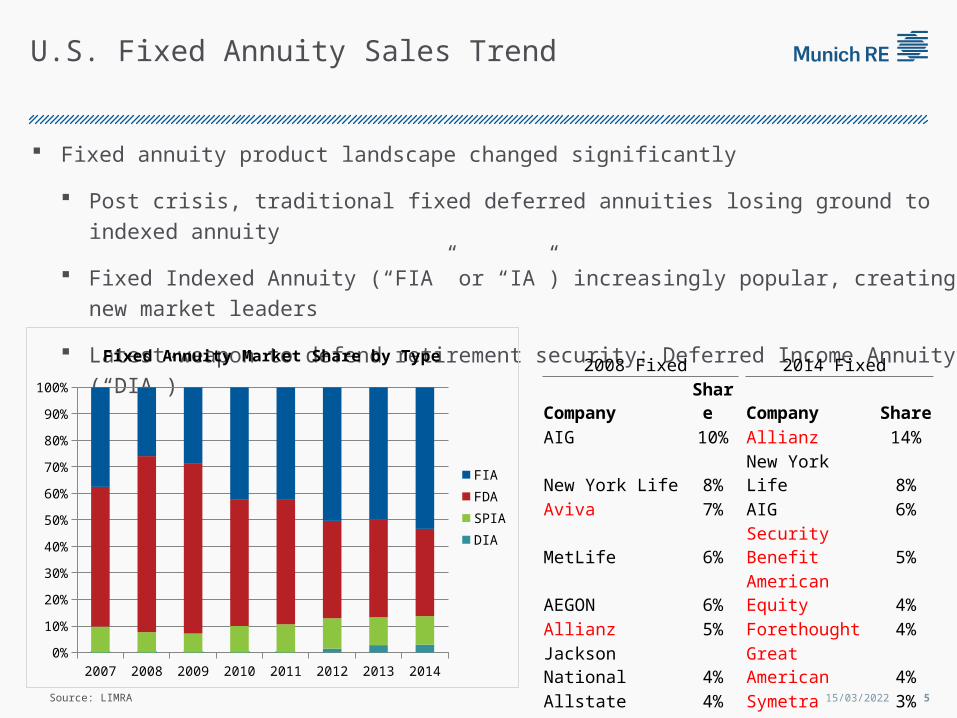

U.S. Fixed Annuity Sales Trend

18/04/2023 5

Fixed annuity product landscape changed significantly

Post crisis, traditional fixed deferred annuities losing ground to indexed annuity

Fixed Indexed Annuity (“FIA” or “IA”) increasingly popular, creating new market leaders

Latest weapon to defend retirement security: Deferred Income Annuity (“DIA”)

2008 Fixed 2014 Fixed

Company Share Company Share

AIG 10% Allianz 14%

New York Life 8% New York Life 8%

Aviva 7% AIG 6%

MetLife 6% Security Benefit 5%

AEGON 6% American Equity 4%

Allianz 5% Forethought 4%

Jackson National 4% Great American 4%

Allstate 4% Symetra 3%

Principal 4% MetLife 3%

Hartford 3% Pacific Life 3%

Other 45% Other 46%

Source: LIMRA

2007 2008 2009 2010 2011 2012 2013 20140%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Fixed Annuity Market Share by Type

FIA

FDA

SPIA

DIA

Annuity Product Design

18/04/2023 6

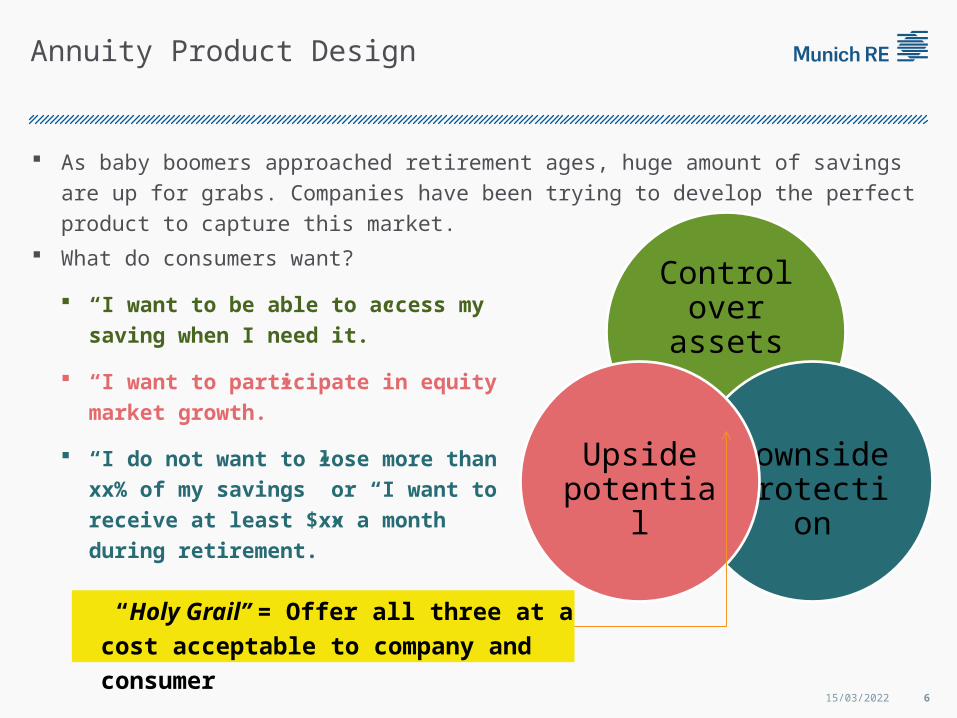

As baby boomers approached retirement ages, huge amount of savings are up for grabs.

Companies have been trying to develop the perfect product to capture this market.

Control over assets

Downside protection

Upside potential

What do consumers want?

“I want to be able to access my saving

when I need it.”

“I want to participate in equity market

growth.”

“I do not want to lose more than xx% of

my savings” or “I want to receive at

least $xx a month during retirement.”

“Holy Grail” = Offer all three at a cost

acceptable to company and consumer

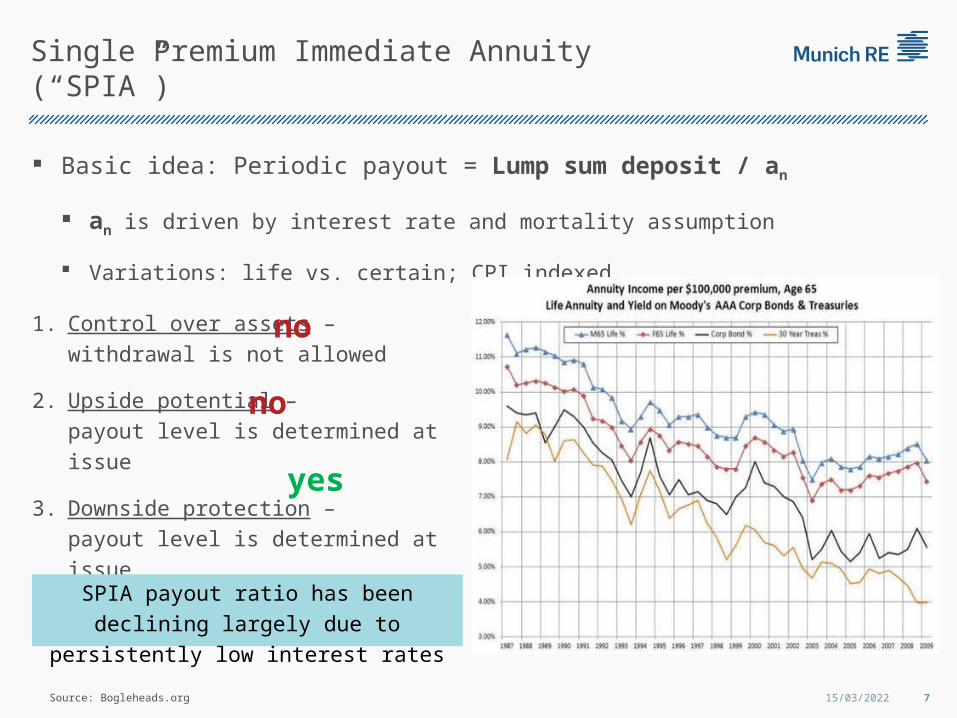

Single Premium Immediate Annuity (“SPIA”)

18/04/2023 7

Basic idea: Periodic payout = Lump sum deposit / an

an is driven by interest rate and mortality assumption

Variations: life vs. certain; CPI indexed

1. Control over assets – withdrawal

is not allowed

2. Upside potential – payout level is

determined at issue

3. Downside protection – payout

level is determined at issue

no

no

yes

Source: Bogleheads.org

SPIA payout ratio has been declining largely

due to persistently low interest rates

Fixed Deferred Annuity (“FDA”)

18/04/2023 8

Basic idea: medium term savings account that pays a credited rate. The credited

rate is reset periodically but no less than a guaranteed rate.

Surrender charge applies, typically 3 to 7 years; free withdrawal allowed, typically 10%

Positioned between multi-year CD and bond fund; “book value” withdrawal

Credited rate typically follows a N+1 structure: initially guaranteed for N years, then

reset annually; determined based on portfolio yield less a spread

Guarantee rates prescribed, now between 1.0% ~ 1.5%

Significant variation: Market Value Adjustment (“MVA”), shifting some interest risk to

policyholders. Otherwise, contracts referred to as Book Value FDA.

1. Control over assets – withdrawal is allowed

2. Upside potential – declared rates follow a stable bond portfolio yield

3. Downside protection – principal is not at risk; credited rate has guarantee

no

yes

yes

Fixed Indexed Annuity (“FIA”)

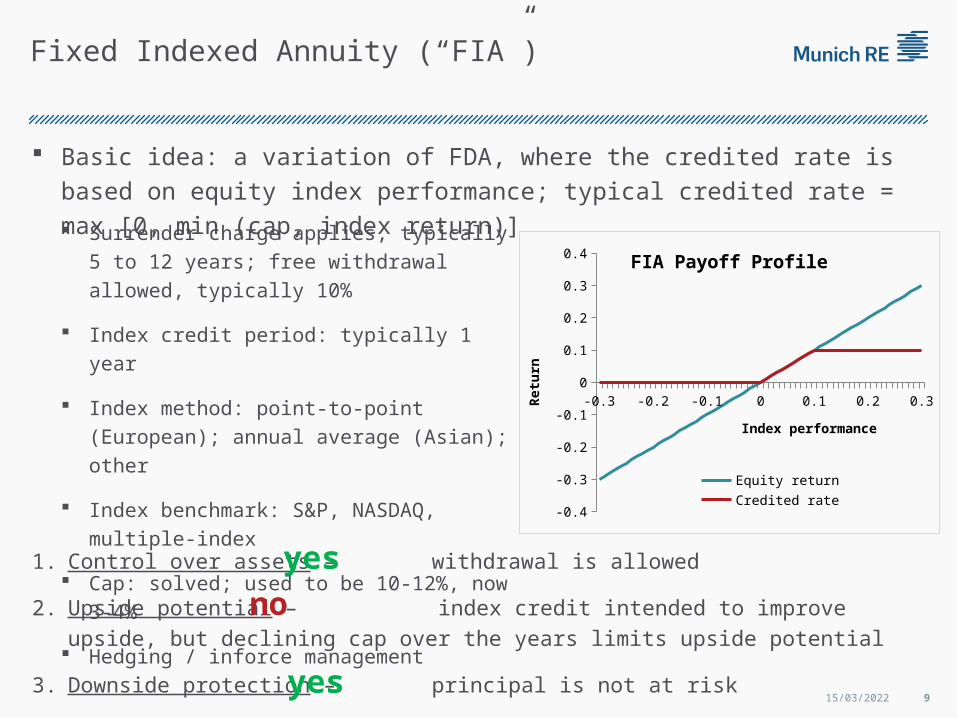

18/04/2023 9

Basic idea: a variation of FDA, where the credited rate is based on equity index

performance; typical credited rate = max [0, min (cap, index return)]

1. Control over assets – withdrawal is allowed

2. Upside potential – index credit intended to improve upside, but declining cap

over the years limits upside potential

3. Downside protection – principal is not at risk

no

yes

yes

-0.3 -0.2 -0.1 0 0.1 0.2 0.3

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

0.3

0.4 FIA Payoff Profile

Equity return

Credited rate

Index performance

Ret

urn

Surrender charge applies, typically 5 to 12 years;

free withdrawal allowed, typically 10%

Index credit period: typically 1 year

Index method: point-to-point (European); annual

average (Asian); other

Index benchmark: S&P, NASDAQ, multiple-index

Cap: solved; used to be 10-12%, now 3-4%

Hedging / inforce management

Variable Annuity – Base product

18/04/2023 10

Basic idea: a mutual fund type account with tax deferral advantage

Surrender charge applies, typically 4 to 6 years; free withdrawal allowed, typically 10%

Multiple investment options, with management fees from 10bps to 200bps

Fixed rate account sometimes available, similar to FDA

Loads or fees deducted from account value

Often sold with riders (GMxB)

1. Control over assets – withdrawal is allowed

2. Upside potential – return similar to mutual funds

3. Downside protection – similar to mutual funds, principal is at riskno

yes

yes

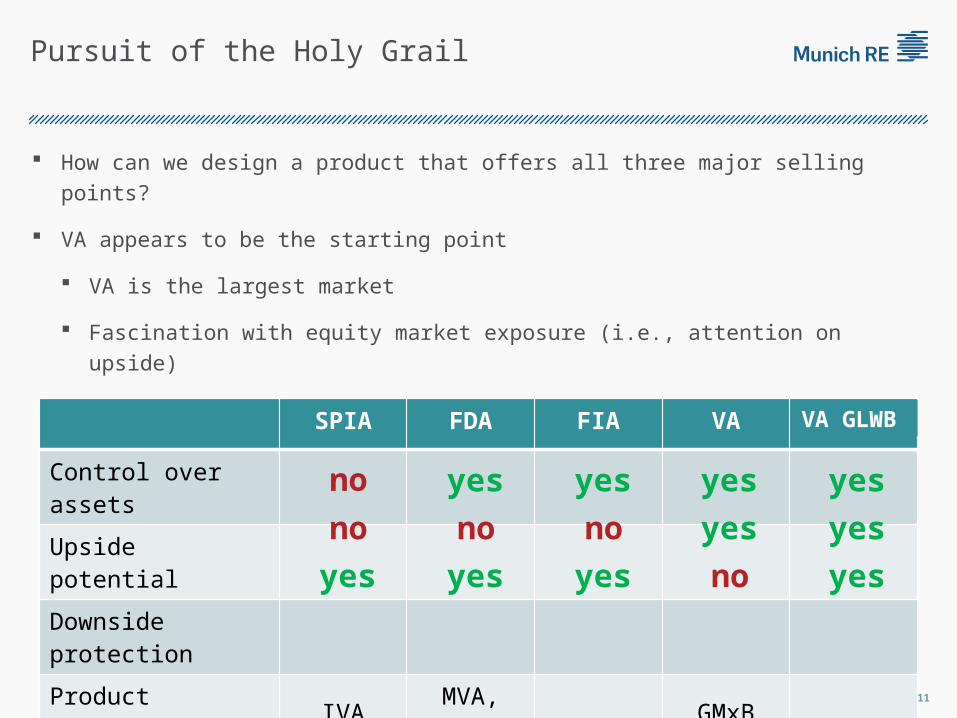

Pursuit of the Holy Grail

18/04/2023 11

How can we design a product that offers all three major selling points?

VA appears to be the starting point

VA is the largest market

Fascination with equity market exposure (i.e., attention on upside)

Biggest risk is not taking any risk at all: principal protection ≠ downside protection

SPIA FDA FIA VA ??

Control over assets

Upside potential

Downside protection

Product variation IVA MVA, FIA GMxB

yes

yes

no

yes

yes

no yes

yes

noyes

yesno

no

yes

yes

VA GLWB

Guaranteed Lifetime Withdrawal Benefit (“GLWB”) RiderThe pursuit of Holy Grail is over – VA with GLWB rider

18/04/2023 12

Basic idea: GLWB allows policyholder to withdraw x% of Benefit Base (“BB”)

every year for life, regardless of account value performance, even if fund runs

out completely

1 2 3 4 5 6 7 8 9 10 -

500

1,000

1,500

2,000

2,500

GLWB Benefit Base Growth Pattern

AV

BB - Ratchet

BB - Rollup

Policy year

Benefit Base is a side calculation

Ratchet BBt = max (AV, BBt-1 )

Rollup BBt = BBt-1 x (1 + rollup rate)

Withdrawal %age increases by age when

GLWB is exercised (e.g., 4% at age 60)

Once GLWB is triggered, BB does not

decline unless excess withdrawal

GLWB type riders soon dominated VA sales

Companies designed complex dynamic hedging process to manage

cost and risk of GLWB … … Everything worked until it didn’t

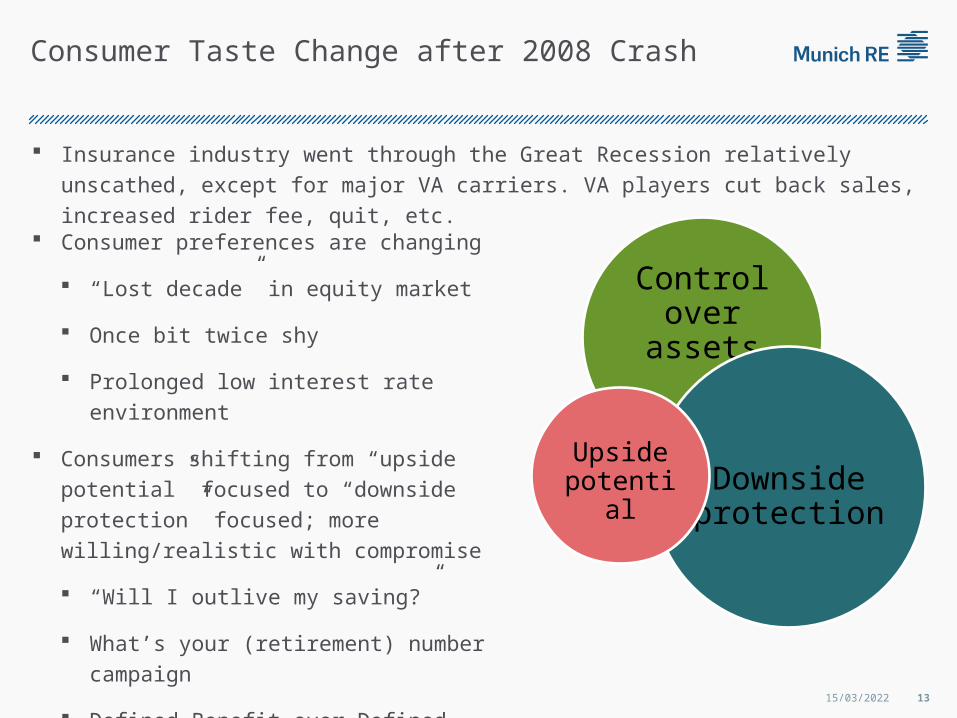

Consumer Taste Change after 2008 Crash

18/04/2023 13

Insurance industry went through the Great Recession relatively unscathed, except for

major VA carriers. VA players cut back sales, increased rider fee, quit, etc.

Control over assets

Downside protection

Upside potential

Consumer preferences are changing

“Lost decade” in equity market

Once bit twice shy

Prolonged low interest rate environment

Consumers shifting from “upside potential”

focused to “downside protection” focused; more

willing/realistic with compromise

“Will I outlive my saving?”

What’s your (retirement) number campaign

Defined Benefit over Defined Contribution

Post 2008 Product Trend

18/04/2023 14

The GLWB Holy Grail failed, or did it?

VA development

Back to basics (i.e., no significant living benefit rider) - but sales still driven heavily by

GLWB due to consumer desire for downside protection

Volatility control funds – shift some hedging to consumer side; consumers appear to be

willing to shoulder the (implied) cost

Introduce a deferred income annuity (“DIA”) element

FIA development

Innovation in indexing strategy, e.g., Variable Indexed Annuity (“VIA”)

FIA a better chassis for GLWB? Lower AV volatility, more predictable Benefit Base pattern

GLWB popularity powered FIA sales; more than 85% FIA sold carries GLWB

Downside protection sells

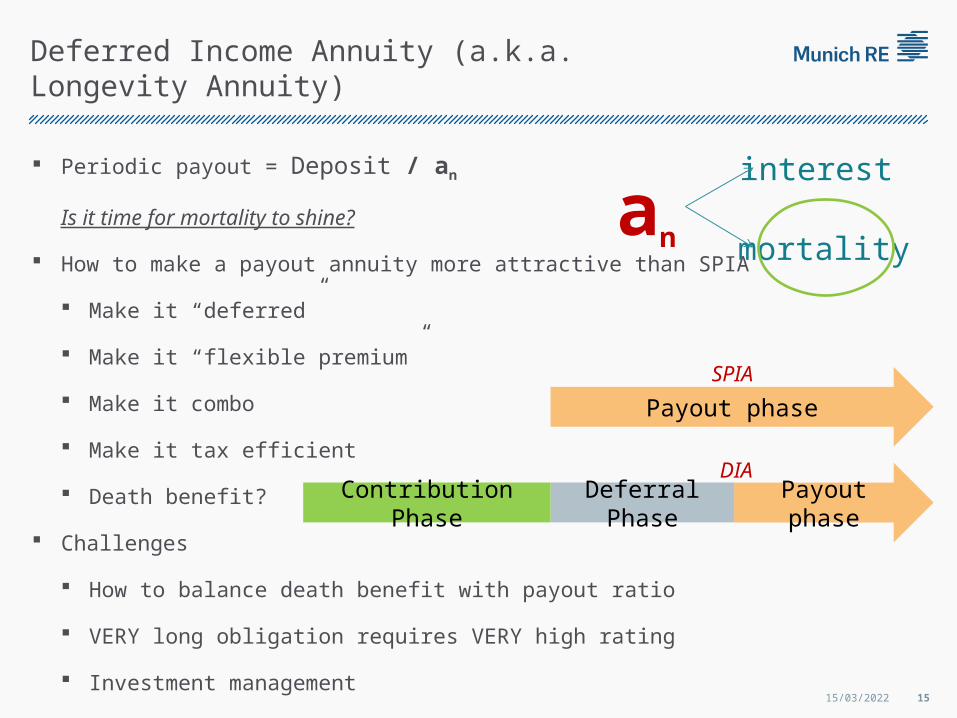

Deferred Income Annuity (a.k.a. Longevity Annuity)

18/04/2023 15

Periodic payout = Deposit / an

Is it time for mortality to shine?

How to make a payout annuity more attractive than SPIA

Make it “deferred”

Make it “flexible premium”

Make it combo

Make it tax efficient

Death benefit?

Challenges

How to balance death benefit with payout ratio

VERY long obligation requires VERY high rating

Investment management

an mortality

interest

Payout phase

Payout phaseDeferral PhaseContribution Phase

SPIA

DIA

Change in Market Landscape

18/04/2023 16

Private equity and alternative buyers enter market via acquisition

Inforce blocks viewed as a cheaper way to acquire assets under management

FDA / FIA particularly popular

Asset intensive

Relatively simple liabilities

Unattractive under market consistent valuation framework

Wave of M&A activities in the past 4 years

Apollo / Athene - RBC USA 2010, Aviva USA (annuity) 2012

Guggenheim - Security Benefit 2010, Equitrust 2011, SunLife USA (Annuity) 2012

Harbinger - Old Mutual 2010

Goldman / Global Atlantic - Forethought 2013, Aviva USA (life) 2013

Resolution - Lincoln Benefit 2013

New Valuation / Appraisal Framework

18/04/2023 17

New players with significant banking and asset expertise brought in a new

valuation/appraisal approach

Liability cost of fund (“COF”)

Asset transfer upon sales = NPV(COF, Product cash flow)

ROE = (Asset return – COF) x Leverage + Asset return

where Leverage = Liability / Required Surplus

Assuming 10x leverage

Asset return (over Swap)COF (over

Swap) 1% 2% 3%

0% 11.0% 22.0% 33.0%

1% 1.0% 12.0% 23.0%

2% -9.0% 2.0% 13.0%