just the facts, 4th quarter 2014

DESCRIPTION

This publication is designed to provide general information on the subjects covered. Pursuant to IRS Circular 230, it is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market, or recommend any tax plan or arrangement. Please note that Great Plains Annuity & Life Marketing, its affiliated companies, and their representatives and employees do not give legal or tax advice. Encourage your clients to consult their tax advisor or attorney. Great Plains Annuity & Life Marketing is not affiliated with third party vendors mentioned in this magazine nor do we guaranty the accuracy or quality of their services. Although we may promote and/or recommend the services offered by these companies, financial professionals are ultimately responsible for the use of any materials or services and agree to comply with the compliance requirements of their broker/dealer and registered investment advisor, if applicable, and the insuranceTRANSCRIPT

4TH QUARTER 2014

800.710.1115 Rates available 24/7 atwww.greatplainsannuity.com 100% Independently Owned!

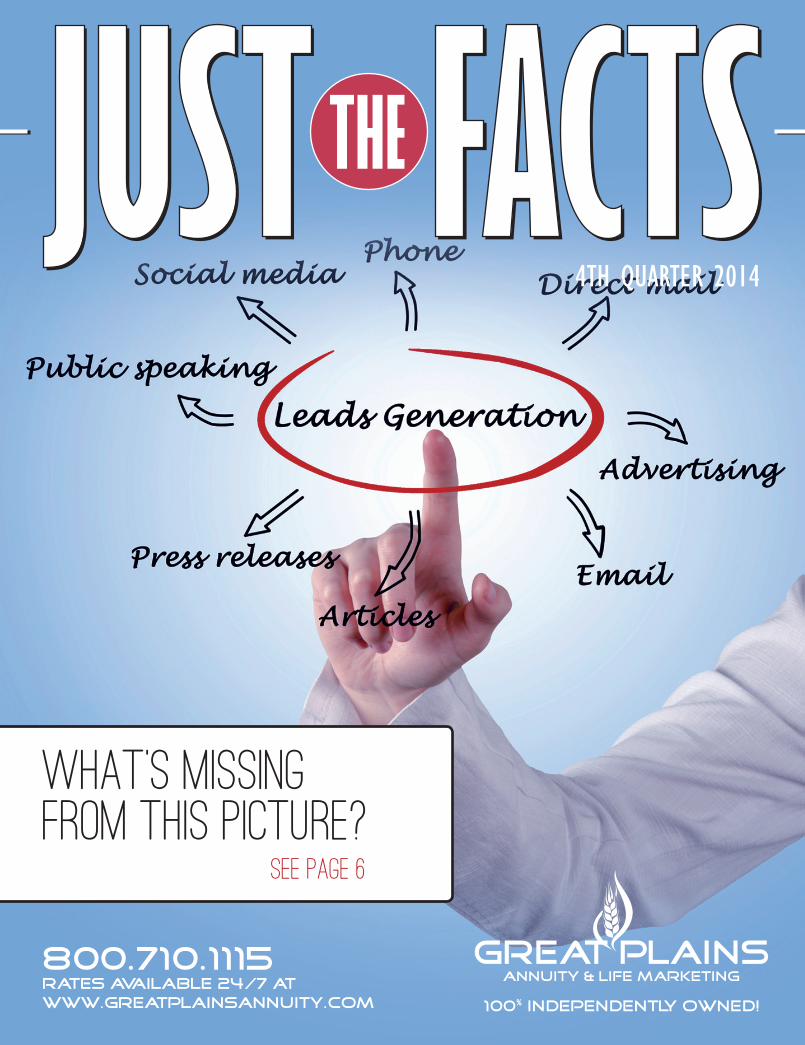

What’s Missing from this picture?

SEE PAGE 6

01.indd 1 10/14/2014 9:15:49 AM

With Safe Income Plus, it’s all about the income!

800.710.1115 www.greatplainsannuity.com

PAGE 2 JUST the FACTS | 4TH QUARTER 2014

Safe Income Plus offers:• 8%VestingPremiumBonus*• CompetitivePayoutFactors• ImpairmentDoublerandIncomeBaseBonus*

• 7%guaranteedcompoundingroll-upratefor10years

• 10yearsurrenderchargeschedule

Interest Crediting Options:• S&P500One-yearmonthlypoint-to-pointwitha1.60%cap• S&P500One-yearannualpoint-to-pointwitha3.00%cap• S&P500One-yearmonthlyaveragewitha3.25%cap• S&P500Point-to-pointfixeddeclaredrateof2.25%• Declaredfixedrateoptionof1.50%

FORPRODUCERUSEONLY–NOTFORTHEUSEWITHTHEGENERALPUBLIC.*Optionalprovisionsandridersmayhaveadditionallimitationsandrestrictions.AvailableinallstatesEXCEPTAL,CT,HI,ID,IN,MA,MN,MS,NH,NY,OR,PA,RI,VTANDWA

Fidelity&GuarantyLifeisthemarketingnameforFidelity&GuarantyLifeInsuranceCompanyissuinginsuranceintheUnitedStatesoutsideofNewYorkand,inNewYorkonly,Fidelity&GuarantyLifeInsuranceCompanyofNewYork.EachFidelity&Guaran-tyLifecompanyissolelyresponsibleforitscontractualcommitments.Fidelity&GuarantyLifeInsuranceCompany,DesMoines,IAFormNumbers:API-1018(06-11),ACI-1018(06-11)etal.

14-799

Fidelity&GuarantyLifeisexcitedtoannouncethelaunchoftheirlatestdeferredfixedindexedannuity–Safe Income Plus.Anannuitydesignedtomaximizeincomewithcompetitiveincomeguarantees.

NowAvailable...

Safe Income PlusSafe Income Plus

02.indd 1 10/14/2014 9:16:05 AM

6

For financial professional use only. Not for use with the general public.

This publication is designed to provide general information on the subjects covered. Pursuant to IRS Circular 230, it is not, however, intended to provide specific legal or tax advice and cannot be used to avoid tax penalties or to promote, market, or recommend any tax plan or arrangement. Please note that Great Plains Annuity & Life Marketing, its affiliated companies, and their representatives and employees do not give legal or tax advice. Encourage your clients to consult their tax advisor or attorney.

Great Plains Annuity & Life Marketing is not affiliated with third party vendors mentioned in this magazine nor do we guaranty the accuracy or quality of their services. Although we may promote and/or recommend the services offered by these companies, financial professionals are ultimately responsible for the use of any materials or services and agree to comply with the compliance requirements of their broker/dealer and registered investment advisor, if applicable, and the insurance carriers they represent.

The third party links, information, and opinions included in this magazine are provided as a service to you. They have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed by Great Plains Annuity & Life Marketing. The material is being provided for information purposes only and is not a solicitation for the purchase of any product. The information is not intended to be used as the sole basis for financial decisions nor should it be construed as advice designed to meet the particular needs of clients. Financial Professionals should ensure they continue to follow the current policies on the use of any advertising, third-party materials and/or social media as required by their broker/dealer and registered investment advisor, if applicable, and the insurance carriers they represent.

TWO GREAT SALES PROGRAMS TO CONSIDER FOR 2015 NOW!

PRINCIPALS

• Rich Hellerich• Robb Edwards

ANNUITY SPECIALISTS

• Mike Lair, Sr. V.P., Annuity Marketing• Cindy Nelson, V.P., Annuity Sales• Brad Allen• Carlos Rojas • Jane Plumberg• Kara Jones• Scott Andrew

LIFE SPECIALISTS

• Dick Reynolds, CLU, V.P., Life Sales

ADMINISTRATION

• Cris Larson• Naomi Mayekawa • Mackenzie Oakley• Kathy Putnam• Gina Skiles

10901 W 84th Terrace., Ste. 125 Lenexa, KS 66214Toll Free: 800-710-1115

Local: 913-492-9994 • Fax: 913-492-9998www.greatplainsannuity.com

10 THE ART OF INCOME RIDER PRESENTATIONS

Great Plains Annuity Income Planning artist Scott Andrew illustrates why you should be using IncomePLUS to better serve your clients and close more sales.

14 SOCIAL SECURITY PLANNING REVIVED

Guest contributor Kim Magdalein has great news for agents that believe Social Security planning is DOA. Discover how this planning method is alive and well and serves a broader audience than you may have thought.

12 CHANGE

The only constant to life is change, and that’s certainly true of FIAs. Learn how to meet your client’s goal of maintaining their lifestyle in retirement regardless of the changes they experience.

4TH QUARTER 2014

Looking to add more qualified prospects to your sales pipeline? Rich Hellerich shares two ideas to get your 2015 sales off to a great start!

PAGE 3JUST the FACTS | 4TH QUARTER 2014

16 DOES YOUR MARKETING NEED A JUMPSTART?

Here are some ideas that can jumpstart your 2015 Marketing Plan! Contact your Great Plains Marketing Specialist for details on these programs and other ways we can impact your sales!

18 ARE YOU MISSING AN EASY CROSS-SALE OPPORTUNITY?

Many advisors miss the opportunity to help clients maximize the value of legacy gifts by failing to ask one simple question.

03.indd 1 10/14/2014 9:16:24 AM

As the year draws to an end, I remember an old sales adage that has served me well over the past 20 years. “What we do in the fourth quarter determines our success in the first quarter of next year”. What are you going to do in the next three months to get your 2015 off to a roaring start?

These fourth quarter activities can include efforts like extra sales efforts for the rest of this year, or reviewing your results so far this year and building a “killer” marketing plan for next year. Maybe you need to address your time-management skills, invest in better technology tools or enhance your education on fixed annuity, life insurance and retirement topics. In addition to these ideas, and If you are an experienced producer and doing business with Great Plains, I believe I have something you will want to consider for a fourth quarter activity.

I have been working with a select group of experienced agents testing a new program to generate more sales opportunities. Based on initial results, I know this program is successful when faithfully practiced and executed. It is not rocket science. It is not expensive. It requires patience, persistence, and commitment. Again, a critical component of the program is experienced knowledgeable agents can expect better results.

Please see page six of this issue and check in with your Great Plains Annuity Specialist for more information on building powerful referral networks. We have been working on this program for some time, and we are going to help a select group of agents expand their goals for next year. We have developed a straightforward marketing process that has been validated and is repeatable. If you have an interest, it is important that you act quickly and begin the process as soon as possible.

Are you a Power Partner?

Rich Hellerich

POWERPARTNERSNETWORK

800.710.1115

PAGE 4 JUST the FACTS | 4TH QUARTER 2014

04.indd 3 10/14/2014 9:16:43 AM

Agent NameCompany NameAddressCity, State, ZipPhone NumberWebsite

PAGE 5JUST the FACTS | 4TH QUARTER 2014

800.710.1115 www.greatplainsannuity.com

Call today for more information!

05.indd 1 10/14/2014 9:17:03 AM

Two Great Sales Programs to consider for 2015 NOW!Are you achieving a steady volume of quality of prospects for your annuity and life insurance practice? The vast majority of agents and producers we work with never feel like they have enough qualified leads in their sales pipeline. Most agents are frustrated with direct mail, newspaper, seminar, and other traditional lead generation methods that continue to produce declining response rates of qualified prospects and increasing costs. While seminar and direct mail programs may be effective, the glory days of response rates above 2%, or filling two to three seminar sessions by mailing just 1,500 prospects are nearly non-existent. The bottom line is today’s agents spend more marketing dollars on these methods for fewer responses and declining results.Part of the problem is the dynamic change in where we go to get

our information. Newspapers and periodicals are dealing with dwindling subscriber bases, while costs of printing, postage and delivery have greatly increased. The same can be said for direct mail, with increased printing and postage expense. I believe market saturation is another culprit for direct mail.

Just as you continually pursue qualified consumer prospects, Great Plains is constantly seeking qualified agents to work with. We spent thousands of dollars annually to reach agents through industry trade magazines, direct mail and e-mail blasts to generate thousands of agent responses. Just as many agents were taught that sales are a result of the “law of numbers”, we have blindly pursued trying to follow up agents that respond to generate conversations that

generate relationships. Are you old enough to remember the 10/3/1 training (10 leads = 3 appointments = 1 sale) many insurance companies gave new agents 30-40 years ago? Just as consumer response rates have declined, so has agent response. Why?

We believe there are several parallels to both consumer and agent groups:

• Saturation: we are constantly barraged with advertising messages

• Time Demands: we are too busy to be interrupted

• Distracted: we have shorter attention spans

(Continued on Page 8)

PAGE 6 JUST the FACTS | 4TH QUARTER 2014

06-08.indd 3 10/14/2014 9:17:30 AM

LibertyMark 7, LibertyMark 10, 10 LT (Policy Series 411/4182), and LibertyMark 10 Plus, 10 LT Plus (Policy Series 411/4179/4182/4184) are single premium deferred fixed indexed annuities underwritten by Americo Financial Life and Annuity Insurance Company (Americo), Kansas City, MO, and may vary in accordance with state laws. Products are distributed by Legacy Marketing Group®. Some products and benefits may not be available in all states. Certain restrictions and variations apply. Consult policy and riders for all limitations and exclusions. Legacy Marketing Group and Richard Hellerich (Great Plains Annuity & Life Marketing) are independent, authorized agencies of Americo.Past performance is no guarantee of future results. Any such illustration must not be regarded as guaranteed or as an estimate of future performance, unless it is based solely on the minimum guaranteed interest rates. The S&P 500 Index is a product of S&P Dow Jones Indices LLC (“SPDJI”), and has been licensed for use by Americo Financial Life and Annuity Insurance Company (“Americo”). Standard & Poor’s®, S&P® and S&P 500® are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by Americo. Americo’s LibertyMark annuities are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index. * Includes application of 1.25% Liberty Optimizer Fee on LibertyMark 10 no bonus product.** 80% is current first-year participation rate effective May 8, 2014. Rates are not guaranteed and are subject to change. † “Winks Sales & Market Report,” www.annuityspecs.com (March 10, 2014). Average Annual Reset Pt-to-Pt cap, no bonus products. AF1049v0414_GP 14-609-9 (04/14) FOR BROKER USE ONLY. NOT FOR USE WITH CONSUMERS.

Why limit your client’s earnings when you can offer UNCAPPED interest crediting strategies?

PArtiCiPAtioN rAtEs!the Power of

that’s 283% more earnings!

Call today for more information on LibertyMark participation rate strategies!

Hypothetical example based on S&P 500® Index performance 8/28/1990–8/28/2000. Assumes no withdrawals.

Traditional One-Year S&P 500 Point-to-Point With 4.65% Cap* VS.

LibertyMark Two-Year S&P 500 Point-to-Point With 80% Par. Rate**

$317,12512.23% yield

†

$156,6804.59% yield

$100,000Premium

$100,000Premium

$317,12512.23% yield*

$156,6804.59% yield

Traditional One-Year S&P 500 Point-to-Point With 4.65% Cap* VS.

LibertyMark Two-Year S&P 500 Point-to-Point With 80% Par. Rate**

$317,12512.23% yield

†

$156,6804.59% yield

$100,000Premium

Traditional One-Year S&P 500 Point-to-Point With 4.65% Cap* VS.

LibertyMark Two-Year S&P 500 Point-to-Point With 80% Par. Rate**

$317,12512.23% yield

†

$156,6804.59% yield

$100,000Premium

traditional One-Year S&P 500® Point-to-Point With 4.65% Cap†

LibertyMark Two-Year S&P 500® Point-to-Point With 80% Par. Rate**

800-710-1115 www.greatplainsannuity.com

PAGE 7JUST the FACTS | 4TH QUARTER 2014

07.indd 1 10/14/2014 9:18:12 AM

Rich Hellerich

POWERPARTNERSNETWORK

Two Great Sales Programs to consider for 2015 NOW!

PAGE 8 JUST the FACTS | 4TH QUARTER 2014

(Continued from Page 6) During a review of all our lead generation efforts over the past 10 years, we were surprised to learn what our most effective lead generation tool is, in terms of cost and results. To reinforce the value of this tool, we found it outperformed the next two top lead generation methods combined! We also learned that our most effective sales team members excelled with this lead-generation method because of the value they brought to the relationship... and our most effective lead generation method is... REFERRALS!

I have been working with a select group of our producers this year on a program that can ultimately become a constant source of new business for seasoned producers with a firm grasp of the annuity and life business and know what they are doing. We are far enough along, and have achieved sufficient results to convince me that now is the time to share this idea and offer this program to select producers working with Great Plains.

1. Introducing POWER PARTNERS NETWORK:Great Plains is helping our top producers create Referrals through professional relationships. Our initial focus is centered on reaching CPAs with the introduction of another sphere of influence later in the year. The beauty of this

program is its simplicity. We have put together the tools and items needed to approach and engage other professional advisors who...

• Need access to your knowledge and products

• Want to better serve their client base

• Want to grow their business and revenue

• Know their competitors are doing the same

While this program allows the insurance agent to benefit from the referring professional’s credibility and relationship, it is imperative that the advice and solutions presented fit for both the client and the referring advisor. We are excited to launch this program and have high expectations for its success in the coming year and beyond! Contact your Annuity Marketing Specialist for more information.

2. Learn how to TAP into the 401(k) Market:What financial liability do employers potentially face with soon-to-retire employees in the event of a market turndown? Remember 2000 and 2008?

Great Plains knows what you must do to succeed in this market. In fact, we made the necessary changes in our own company 401(k) plan to ensure all employees have the ability to avoid market risk and lock in their gains.

There are two basic options:• In –Service Withdrawals• Complete 401(k) Takeover

In our experience, finding 401(k) plan documents that permit In-Services Withdrawals is rare at best. When you do find this opportunity, your challenge is to be the resource of choice for that company and both their younger and soon-to-retire employees looking for help and guidance.

While the complete 401(k) takeover is more complicated, you can take advantage of what we have learned and the solutions we can provide in helping employers avoid potential liability, assisting pre-retirement (and younger) employees with options they previously did not have access to, and generating new business.

Contact your Great Plains Annuity Marketing Specialist if you have an interest in either of these programs. Also watch for our Webinar Wednesday schedule as we will be covering both of these programs for the rest of this year.

06-08.indd 4 10/14/2014 9:17:44 AM

800.710.1115 www.greatplainsannuity.com

Preserve Multi-Year Guaranteed Annuity offers a Tasteful Selection...

• Guarantee Options from 3-10 Years• 10% Free Withdrawals

• Full Account Value at Death• Issued to Age 90

The Preserve MYGA Series is one of the most popular MYGAs Great Plains offers! Sample all the available guaranteed rate flavors and sweet compensation by calling your GPALM Annuity Marketing Specialist now!

Interest rate shown is as of 10/2/2014, is subject to change and may vary in accord with state regulations. Preserve Annuities are issued by and are obligations of Guggenheim Life and Annuity Company, home office at 401 Pennsylvania Pkwy., Suite 300, Indianapolis, Indiana 46280. Annuity products are not insured by the FDIC. Annuity contracts contain charges and limitations. Preserve annuities have varying surrender charge periods with substantial penalties for early withdrawal, and may be subject to a market value adjustment. Preserve annuities and/or certain optional features of such annuities may not be available in all states. Guggenheim Life and Annuity Company is not licensed in New Jersey and New York. The contract is issued on form numbers GLA-MYGA-01 or variations of such. 101401A

Experience. Security. Loyalty.

3-Year:1.85%

5-Year:2.75%

6-Year:2.90%

7-Year:3.00%

10-Year:3.30%

PAGE 9JUST the FACTS | 4TH QUARTER 2014

09.indd 1 10/14/2014 9:18:55 AM

PAGE 10 JUST the FACTS | 4TH QUARTER 2014

How has Great Plains helped producers place millions of Fixed and Fixed Indexed Annuity business (with a fair amount of target life premium as well)? The answer is simple – our INCOMEPLUS Tools! We have assisted literally hundreds of agents in helping their clients design individual principal-protected, guaranteed income solutions with additional benefits and riders to protect their financial future. With one phone call and some information about your prospects, you can receive our Income Rider Comparison worksheet in a matter of minutes. Many times we can e-mail the comparison and discuss case development with you during that same call. Your Great Plains Annuity Marketing Specialist can help you find the top income solutions depending on your client’s age, deferral period and when they want to start their income stream to create a retirement income masterpiece. Besides determining the top income results, your Annuity Marketing Specialist can also help you consider additional carrier, product and rider features that may be of importance to your client such as Chronic Care, Enhanced Death and Inflationary benefits.INCOMEPLUS is a comprehensive breakdown of the assets your client has set aside for their secure retirement. It shows how several different annuities can be structured to provide a lifetime of income for them, based on the performance of the different products. Unlike other programs out there, this leaves the ultimate control in your hands, the trusted advisor. Here are some examples of how you can create your client’s financial masterpiece:

1. Your client wants to maximize their lifetime income to be level for all years so they know exactly what they are going to get each year.

2. Your client wants to protect their income against the rising cost of inflation. This can be done by building in inflationary adjustments to their plan.

3. Your client wants to spend the early years of their retirement to travel and enjoy their new found freedom from the 9-5. This can be done by increasing the income in the early years of the plan and dropping the income to a lower level once they plan on settling down.

4. Your client wants to make sure that their principal is protected to leave to their beneficiaries at their death. This can be done by adding life insurance to the plan or by taking advantage of some features on the annuities.

5. Your client wants flexibility in case of changes that might occur later on in life. For example, they receive an inheritance and don’t need to trigger one of the

legs of income, or something has arisen that requires additional income for a short period of time. This flexibility is built into the INCOMEPLUS plan to allow for these unforeseen changes to your client’s circumstances.

There are infinite possibilities and each one as unique as your client is. You shouldn’t have to submit to them a cookie-cutter approach to the most important decision of their lives. Provide them with the power to embrace their dreams, the power of INCOMEPLUS. Call Great Plains today to learn more about how INCOMEPLUS can improve your sales.

The Art of Income Rider Presentations...

Scott AndrewAnnuity Marketing [email protected]

10.indd 3 10/14/2014 9:23:56 AM

if all you have is a hammer,

If you want to help clients find the highest GLWB income options for the least amount of premium, call us to run a comparison and have the results at your fingertips in just a few minutes - not hours!

• Discover the surprising “sweet spots” and top income solutions based on when your client wants to trigger income!

• See when the highest Roll-up Rate does not equal the highest income!

• Discuss additional benefits that may meet your client’s concerns!

everything looks like a nail!

Use the right GLWB research tool for the job!

from Great Plains Annuity & Life Marketing

Call Great Plains NOW for more information and a sample of our IncomePLUS Income Rider Comparison Tool!

JUST the FACTS | 4TH QUARTER 2014 PAGE 11

800.710.1115 www.greatplainsannuity.com

11.indd 1 10/14/2014 9:24:16 AM

We have all heard some version of this statement in the past – and most of us, especially those of us in the FIA world know this to be 100% accurate. Product, rates, features…the list goes on and on – all aspects of our industry and business that we have seen change over the years.

This aspect of change also resonates with your clients – and impacts the decisions and choices you make as part of an income and financial solution. And in the end, what are we endlessly trying to protect when putting a solution together for a client? CHANGE. Our goal is to provide a solution that maintains their lifestyle regardless of their situation – and the change they experience.

Guaranteed income for life is a main solution to this challenge. Regardless of how long an individual lives, they are not able to outlive the income provided in an Indexed annuity with an Income Rider included. But with longer life expectancies, other challenges potentially arise; change in health, desire to impact future generations, and impact to immediate family in caring for lifestyle changes among other challenges.

If you could provide a solution that addressed each of these potential changes, in one product, wouldn’t you feel that you are providing a more well-rounded solution to your client? If they were to go into a nursing home, you could increase their guaranteed income by up to 250% for a period of time, or if they needed assisted living they could see income increase up to 175%. This is in addition to being able to offer an income stream that can never be outlived, even if their actual account balance decreased to $0.

You have now presented your client with a solution that will address income needs (by offering a 14% annual roll-up to their income benefit base), but also taken the pressure off the table your client may feel if their health were to deteriorate, and the impact that would have on siblings or children.

One final solution you have the ability to provide is that of creating a legacy. So often, life insurance is thought of too late for a client to qualify. Not because it was never presented, but because the client didn’t see the immediate need. You now have the ability to offer an enhanced death benefit – in addition to a guaranteed income stream and care protection – that will grow at a rate of up to 10% per year.

Your client can be confident that while they live, they are guaranteed a competitive income stream for life – with enhancements for changes that may take place affecting their ability to care for themselves. They can also rest easy knowing their money has the opportunity to not only address changes in their life, but create an opportunity for their beneficiaries to also start planning for changes that may occur in their lives.

Change is inevitable. Embrace it. Contact your Great Plains Annuity Marketing Specialist to discuss our ever changing marketplace – and learn about a product that meets this challenge head on, providing multiple solutions in one location.

PAGE 12 JUST the FACTS | 4TH QUARTER 2014

CHANGEIf you stick around long enough, the only constant in life is change.

12.indd 3 10/14/2014 9:26:58 AM

Phoenix Indexed Annuities are issued by PHL Variable Insurance Company (PHLVIC) (Hartford, CT). PHLVIC is not authorized to conduct business in Maine and New York. For Agent Use Only. Not intended for public sales.BPD39202 10/14

800.710.1115 www.greatplainsannuity.com

Do you have clients not sure if they will:• Need Income?

• Need Assisted Living or Nursing Home Care?

• Have anything to leave to their heirs?

Your clients know change is coming.Give them the flexibility to cope with the unknown by offering them an annuity that provides multiple solutions and quality income!

Contact us today for more information!

JUST the FACTS | 4TH QUARTER 2014 PAGE 13

13.indd 1 10/14/2014 9:29:07 AM

PAGE 14 JUST the FACTS | 4TH QUARTER 2014

Kim MagdaleinKim Magdalein is a mega-producer who has written over $150 million dollars worth of annuity premium. He was named as one of the top five advisors by Senior Market Advisor magazine in 2005. Kim also owns Seminars For Less, Inc. SFL has produced and mailed thousands of seminar events all over the country. He creates seminars and coaches advisors on best practices for results. He also creates effective seminar presentations that he personally tests and uses. He can be reached at www.seminarsforless.com and at 800-909-9894.

Social Security planning is not dead, it just needed a little rehabilitation. For those of you who have tried Social Security planning, and have abandoned the concept as a marketing method, I have great news. It has been revived. Before I reveal the new opportunities, let me go over the difficulties with this planning method and the remedies which, actually, are very simple.

The first problem is with the amount of assets necessary to fund a delayed Social Security check. If an age 62 person is to receive a $1500 per month check ($18,000 per year) it takes over $300,000 to fund the delay utilizing an income rider to receive income. Not many people are willing or even capable of setting aside this much money for the purpose of funding the delay.

The second problem is with the number of people attending a seminar who are already taking the check and can’t change it.

The third problem is convincing someone to delay if they don’t want to delay. They just don’t like the idea.

The fourth problem is sick people. If someone is in declining health, they won’t delay because they don’t believe they’ll be here and they may need the extra money now for health-care expenses.

So, how do you overcome these major objections? By utilizing what I call the “Gap Strategy”. The gap strategy will allow you to capture the smaller cases like $70,000-$150,000 for example. It will give you everyone in the room the capability of creating their own delay method, therefore creating a full room of qualified prospects.

Let’s say a person has $1500 a month in income at age 62 and if he delays it will increase to $2000 per month. That’s a gap of $500 per month. If he takes his check of $1500 for four years we need to add the Social Security cost-of-living increases to determine the real gap at age 66. Using a 1 1/2% annual cost-of-living allowance the check would grow to $1600 per month. That is an adjusted gap of $400 per month. Assuming a 5% joint payout on an income rider at age 66, the income value would be $97,000. Assuming a rollup rate of 5%, he would need to buy

the annuity for $79,000, which is the present value of the premium. You have now funded the gap and given your client the $2000 per month he seeks from delaying, without delaying. There are several advantages to this strategy. It takes less money so more people can participate. It allows you to do business with those that are already taking a check. The cost of living allowance on the annuity may be greater than the Social Security cost-of-living allowance. The annuity has residual value that Social Security does not offer.

People are still turning 62 at the rate of 8000 per day. That will remain steady for the next 18 years. Since they must make a decision about Social Security, you should take advantage of this fantastic opportunity.

At Seminars For Less, we have the seminars available to utilize this method.

SOCIAL SECURITY PLANNING

REVIVED

14.indd 3 10/14/2014 9:33:32 AM

JUST the FACTS | 4TH QUARTER 2014 PAGE 15

Don’t be an annuity “product peddler”!Help clients maximize their income potential with the least amount of premium necessary! Why push “one product fits all” retirement income solutions when your Great Plains Annuity Specialist can help you evaluate the fixed indexed marketplace in just minutes utilizing our IncomePLUS Compari-son Worksheet?

Just one call to Great Plains allows you to tailor a custom income solution to the specific needs of your client and benefit from discussing additional options and features that can help you close the sale. Take advantage of our income planning tools that can save you hours or research, give your clients’ flexibility and access to the best strategies to reach their dreams, desires and goals!

• Call us if your want to increase your clients income!

• Call us if want to increase your closing ratio!

from Great Plains Annuity & Life Marketing

15.indd 1 10/14/2014 9:34:32 AM

800.710.1115 www.greatplainsannuity.com

PAGE 16 JUST the FACTS | 4TH QUARTER 2014

MARKETING NEED A START?

Many of us are starting to consider our annual sales and marketing planning for the coming year. How did your actual sales measure up against your prog-nostications for 2014? Do you plan on doing more of what was successful so far this year, or is your marketing in need of a jumpstart?

Here are some items designed to turbo-charge your annuity and life sales in the coming year:

• IncomePLUS: If you are actively working in the Income Market and not utilizing this toolset you could be spending unnecessary hours under the hood and missing sales. Ask for a sample Income Rider Comparison worksheet and more informa-tion.

•SinglePremiumLifeOpportunities: Many clients have assets earmarked for heirs or charity and unaware of this important planning product! Many of our agents have increased sales by ask-ing just one more question at each client inter-view. Ask about our expanded SPL carrier and product offerings and tools to help you succeed in this market!

•PowerPartnersNetwork: Learn how to create referrals through professional relationships. See page 6 of this issue and call your marketing spe-cialist for details.

•Tapinto401(k)SalesOpportunities: New from Great Plains - Help employees nearing retirement protect their nest egg and show employers how to reduce their potential liability. See page 6 of this issue for more details.

•SeminarMarketing:Call your Annuity Market-ing Specialist or Robb Edwards for help with your seminar marketing plans.

•On-lineLeadGeneration:Our exclusive internet lead generation tool, Annuity Help Center, will introduce a major enhancement before the end of this year. Call Robb Edwards for details.

•YourPersonalMarketingSpecialist: This is the most important advantage Great Plains offers for case development and backroom support. Your Great Plains Marketing Specialists and the rest of our team are eager to help you tune up your sales engine and put you in the winner’s circle in 2015!

Don’t wait until late December or early next year to discuss your marketing plans and sales goals for the coming year! Contact your Great Plains Market-ing Specialist now for service and suggestions to keep you running smoothly all for 2015.

Whatyoudointhefourthquartergreatlydeterminesyoursalesinthefirstquarterandtherestofthecomingyear!

Jumpstart your 2015 Marketing plans with...

16.indd 1 10/14/2014 9:34:59 AM

PAGE 17JUST the FACTS | 4TH QUARTER 2014

800.710.1115 www.greatplainsannuity.com

Tackle your clients’ retirement needs with the American Custom 10!

Annuities

Plus, your clients can customize their strategy with one of our optional riders2

The American Custom 10SM fixed-indexed annuity from Great American Life® offers:

1 Participation rate applies to strategy.2 There is an annual charge for each rider. Only one rider may be selected and must be added at the time of purchase.Products issued by Great American Life Insurance Company® under contract form number P1104314NW and P1104414NW and rider forms R6046814NW, R6046914NW and R6047014NW. Contract and rider form numbers may vary by state. Products not available in all states.

For producer use only. Not for use in sales solicitation.F1106514NW 10/14

l 10-year early withdrawal charge schedulel 5% penalty-free withdrawalsl Multiple indexed strategies including a strategy that offers uncapped growth potential!1

l Four competitive commission options for you!

Liquidity

Cumulative Free-Withdrawal Option

Growth + income

Simple Income Option Stacked Income Option

Growth + increasinG income

American Custom 101 simple product

3 competitive riders

25% maximum-10% income rollup for 10 years

-Early income enhancement

5% income rollup for 10 years, plus 100% of account value interest for the

life of the contract.

Tackle your clients’ retirement needs with the American Custom 10!

Annuities

Plus, your clients can customize their strategy with one of our optional riders2

The American Custom 10SM fixed-indexed annuity from Great American Life® offers:

1 Participation rate applies to strategy.2 There is an annual charge for each rider. Only one rider may be selected and must be added at the time of purchase.Products issued by Great American Life Insurance Company® under contract form number P1104314NW and P1104414NW and rider forms R6046814NW, R6046914NW and R6047014NW. Contract and rider form numbers may vary by state. Products not available in all states.

For producer use only. Not for use in sales solicitation.F1106514NW 10/14

l 10-year early withdrawal charge schedulel 5% penalty-free withdrawalsl Multiple indexed strategies including a strategy that offers uncapped growth potential!1

l Four competitive commission options for you!

Liquidity

Cumulative Free-Withdrawal Option

Growth + income

Simple Income Option Stacked Income Option

Growth + increasinG income

American Custom 101 simple product

3 competitive riders

25% maximum-10% income rollup for 10 years

-Early income enhancement

5% income rollup for 10 years, plus 100% of account value interest for the

life of the contract.

17.indd 1 10/14/2014 9:35:19 AM

PAGE 18 JUST the FACTS | 4TH QUARTER 2014

They’re out there – clients that have $10,000 or more earmarked for heirs or charity but worried that they may need access to those funds in the event of a chronic illness or long term care event arises. While they don’t need the money, and their greatest desire is to pass it to loved ones or charity, they hold these funds in CDs, money market accounts and short-term MYGA’s “just in case” a major financial need occurs.

The Center on Wealth and Philanthropy recently updated its 1999 report stating that Baby Boomers would pass $41 trillion in accumulated assets on to heirs by the year 2052 (ask us for a copy of the study). The new figure has been upgraded to figure to $59 trillion. You can take advantage of this wealth transfer opportunity and better serve your clients by asking one simple question of every Senior or Boomer prospect/client you meet. This could result in greatly improving the amount of their legacy, and passing it tax-free to their beneficiaries! When it comes to wealth transfer, few solutions work as simply or as well as single premium life (SPL) insurance.

Tapping this trillion-dollar market initially can be accomplished by reviewing your existing LTC, med-sup and annuity clients to identify prospects for wealth transfer products. Just asking one more question on your next appointment could uncover a

cross-sale opportunity for Single-Premium Life beneficial to your clients and generating thousands in commissions.

SPL Prospect Profile Single premium life insurance is an excellent wealth transfer option for clients who:

• Are in or near retirement (ages 60 to 80)

• Are in fairly good health to meet minimal underwriting requirements

• Have $10,000 or more set aside for loved ones

• Are concerned about how income taxes, final expenses and probate could impact their beneficiaries

• Love guarantees

You are in an ideal position to identify potential SPL clients in your current book of business, help them understand its legacy-building features, and successfully pair them with the SPL product that delivers great all-around value, not just the largest benefit amount.

A single premium life policy (SPL) could be an excellent solution for those over 65 interested in passing a tax-free death benefit to their heirs. Clients that have aside some “leave-behind” assets for beneficiaries, but concerned about not having enough to care for their own potential health care needs, could also find SPL an appropriate answer.

SPL is a life insurance product that allows you to pay a single lump sum premium to obtain a death benefit guaranteed to remain paid up for the rest of your life. The size of the death benefit depends on the amount paid into the policy, age and health of the insured.

Great Plains has recently added several new carriers and products to our SPL lineup. I encourage you to call your Great Plains Marketing Specialist for our SPL Producers Guide with more information regarding this opportunity and learn the one question you need to ask wealth transfer prospects!

Carlos RojasSenior Annuity [email protected]

Are You Missing an Easy Cross-Sale Opportunity?Many Advisors miss the opportunity to help clients maximize their legacy to heirs by failing to ask one simple question.

18.indd 3 10/14/2014 9:35:50 AM

Agent NameCompany Name

AddressCity, State Zip

PhoneWebsite

Agent NameCompany Name

AddressCity, State Zip

PhoneWebsite

800.710.1115 www.greatplainsannuity.com

JUST the FACTS | 4TH QUARTER 2014 PAGE 19

Agent NameCompany Name

AddressCity, State Zip

PhoneWebsite

19.indd 1 10/14/2014 9:36:10 AM

10901 W 84th Terrace., Ste. 125Lenexa, KS 66214

800.710.1115 www.greatplainsannuity.com

100% Independently Owned!

GPALM PRODUCERS ACCESS ANNUITY & LIFE RATES 24 HOURS A DAY!

Are you paying too much for E&O?Before you purchase or renew your E&O Coverage call 800.710.1115 and ask your Great Plains Marketing Specialist for details regarding our E&O Program!

20.indd 1 10/14/2014 9:36:30 AM