kbcm q4 2014 junior debt newsletter - copy

TRANSCRIPT

Disclosure : KeyBanc Capital Markets is a trade name under which corporate and investment banking products and services of KeyCorp and its subsidiaries, KeyBanc Capital Markets Inc., MemberNYSE/FINRA/SIPC, and KeyBank National Association (“KeyBank N.A.”), are marketed. Securities products and services are offered by KeyBanc Capital Markets Inc. and its licensed securities representatives, whomay also be employees of KeyBank N.A. Banking products and services are offered by KeyBank N.A. This report was not issued by our research department. The information contained in this report has beenobtained from sources deemed to be reliable but is not represented to be complete, and it should not be relied upon as such. This report does not purport to be a complete analysis of any security, issuer, or industryand is not an offer or a solicitation of an offer to buy or sell any securities. This report is prepared for general information purposes only and does not consider the specific investment objectives, financial situation andparticular needs of any individual person or entity.

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Executive Summary

� Overall, transaction dynamics and return expectations con tinue to reflect a very competitivemarketplace

� However, much like the current senior debt market, the junio r debt market is bifurcated

– At the smaller end of the market (transactions < $50 million), the competitive landscape is robust andissuers are able to push on price and terms

– The larger market (transactions > $50 million) has experienced substantial dislocation and the cost ofcapital is rising quickly, driven by

– Volatility in second lien market

– Larger BDCs have traded down in December and January

� Q4 2014 transaction activity was good but not great

– ~63% of respondents reviewed more than 50 transactions, but a substantial percentage did not close atransaction (19%) or closed just one transaction (22%)

� The vast majority of respondents (73%) indicated total retu rn expectations in the 12%-15% range

– Historically, total return expectations have been slightly higher at 15% to 18%

– There continues to be pricing pressure on the cash pay component of return

KeyBanc Capital Markets conducts a quarterly survey of juni or debt participants to measure market conditionsand transaction terms. In this newsletter, we share with you the results of the survey and provide otheranecdotal observations to bring you our state-of-the-mark et perspective.

KeyBanc Capital Markets’ Debt Capital Markets

The KeyBanc Capital Markets® Debt Capital Markets team represents oneof the strongest full-service debt-side investment banking, sales, tradingand distribution platforms in the nation. We use a blend of real worldperspectives, backed by robust capabilities and relationships, to help ourclients use leverage to grow, make acquisitions, and enhance operations.

For additional information regarding KeyBanc Capital Markets or this newsletter, please contact

the individual listed below:

Andrew Frawley216.689.4288

JUNIOR DEBT MARKET OVERVIEW

2

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Industry Breakdown Q3 2014 Q4 2014

OVERVIEW OF FUNDS

Fund Profile

Junior debt providers continue to consider a broad range of industries as the economic cycle expands and issuers seek additional capital. Current industries of note include industrial manufacturing, business services, consumer, transportation & logistics, health care and information services

Significant capital remains available to issuers seeking junior debt; 93% of the funds that responded have more than $50 million of available capital and 78% have more than $100 million available

Available Capital Typical Investment Size

Time Needed to Raise New Fund NTM New Fund RaiseFundraising sentiment appears to be slightly down from Q3’14. More than 72% of respondents feel a fund can be raised in ~ 6 – 12 months

<$5M $5M - $10M

4%

$11M - $25M 39%

$26M - $50M 32%

>$50M25%

Yes52%

No44%

Undecided4%

7%

15%

41%

19% 19%

0%

10%

20%

30%

40%

50%

<$50M $50M - $99M $100M - $250M $251M - $500M > $500M

% o

f R

esp

on

den

ts

29%

43%

29%

0%

10%

20%

30%

40%

50%

<6 months 6 - 12 months 13 - 18 months

% o

f R

esp

on

den

ts

50%

38%

28%

25%

25%

25%

22%

19%

16%

13%

13%

9%

9%

9%

6%

0%

0%

59%

50%

42%

35%

39%

39%

27%

35%

27%

31%

19%

12%

23%

15%

23%

19%

0%

0%

39%

Industrial Manufacturing

Business Services

Consumer

Health Care

Transportation and Logistics

Information Services

Education

Energy and Utilities

Finance and Insurance

Professional, Scientific, and Technical Services

Hospitality

Technology

Basic Materials

Construction, Engineering and Infrastructure Services

Real Estate

Other

Waste Management

Do not have any industry specialization

3

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Sponsored vs. Non-Sponsored Deals

JUNIOR DEBT DEAL FLOWScreening (10/1/2014 – 12/31/2014)

Transactions Reviewed LOIs Submitted

Closed transaction activity was slightly down this quarter as the number of respondents that closed at least one transaction decreased to 82% in Q4’14, compared to 89% in Q3’14 and 79% in Q2’14

Portfolio Investment Sources

Junior debt providers reviewed slightly more transactions in Q4’14 - 89% of respondents reviewed more than 25 opportunities (versus 82% and 84% in the prior two quarters), and all respondents submitted at least one LOI during the fourth quarter (flat from the prior three quarters)

Transactions Closed

Sponsored66%

Non-Sponsored34%

1-5 LOIs52%

6-10 LOIs15%

10+ LOIs33%

19%

22%

19% 19%

7%

15%

0 1 2 3 4 ≥5

1-5 transactions7%

11-25 transactions4%

26-50 transactions26%

>50 transactions63%

Investment Banks27%

PE Sponsor Groups

46%

Other Mezzanine Funds

8%

Other19%

4

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Realization

Equity (On a % Basis) That Must Be Below the Junior Debt

Junior Debt as a Percentage of Overall Capital Stru cture

Market Average Multiples

Debt/EBITDARatios

<1.5 1.5-1.9 2.0-2.5 2.6-3.0 3.1-3.5 3.6-4.0 4.1-4.5 4.6-5.0 >5.0

Senior Debt - 4% 12% 39% 19% 19% 7% - -

Total Debt - - - - 15% 30% 15% 30% 11%

77% of transactions in the last twelve months got done at 2.6x – 4.0x senior leverage

Total leverage is down slightly in Q4’14, with 11.1% of transactions levered >5.0x from 12% in Q3’14

Consistent with prior surveys, junior debt funds continue to realize exits through M&A and recapitalizations / refinancings

FUND INVESTMENTS

Mezz Debt as a % of Total

Capital Structure

<5% 5%-10% 11%-15% 16%-20% 21%-25% >25%

Respondents - - 33% 33% 30% 4%

% of Equity Below Junior

Debt< 20% 20-29% 30-39% 40-50% >50%

Respondents 4% 26% 56% 15% -

Nearly all respondents indicated that there needs to be 20% -50% of equity below junior debt, with 55.6% in the 30% - 39% range (consistent with prior quarters)

Junior debt investment continues to occupy 11% - 25% of the total capital structure

Internal Cash Flow13%

Refinancing34%

Sale of Company46%

IPO5%

Other1%

5

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

PIK

Equity

Equity as a Percentage of Fully-Diluted Equity

TRANSACTION SPECIFICS

Interestingly, 42% of respondents are at a 11% cash pay and 8% are <10%

~73% of respondents aim for a base-case, all-in IRR of 12% - 15%

Base Case Averages

IRR

<10% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19% 20% >20%

Cash Pay 8% 23% 42% 27% - - - - - - - - -

All-in IRR - 4% 4% 12% 19% 27% 15% 12% 4% 4% - - -

The pressure on cash pay and total returns is seen in the PIK component

PIK has moved from 3% to 2%

PIK Rate

Rarely or Never Have PIK Rate

≤1% 2% 3% 4% 5% >5%

4% 12% 73% 8% - - 4%

% of Transactions with Warrants / Equity Participation Approximately 54% of

respondents reported over half of their transactions have warrants or other equity upside (including purchased equity), including 12% that have warrants on all transactions (up from 6% in Q3’14)

Approximately 48% of respondents reported warrants were ≥4% of fully diluted equity, lower than 56% in Q3’14

Returns

We rarely or never make an equity co-investment

4%

≤10%19%

11% - 25% 11%

26% - 50%12%

51% - 99% 42%

100%12% 2%

20%

3%32%

4%4%

5%8%

>5%36%

6

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

No-Call Provision

Percentage of Transactions with No-Call Periods

Average Length of No-Call Periods

TRANSACTION SPECIFICS (CONTINUED)

Respondents indicated 42% of transactions do not have call protection, down from 47% in Q3’14

Another 19% of respondents indicated all of their transactions have no-call periods

Average length of no-call periods is 1-2 years

42%

12%

4%8%

15%19%

-10%

5%

20%

35%

50%

0% 1% - 10% 11% - 25% 26% - 50% 51% - 99% 100%

% o

f R

esp

on

den

ts

47% 47%

6%0%

20%

40%

60%

1 Year 2 Years >3 Years

% o

f R

esp

on

den

ts

Equity (CONTINUED)

Equity co-investment or

purchased equity%

72%

Warrants issued as a result of

providng junior debt 28%

Origin

Almost 75% of equity participation is in the form of purchased equity (as opposed to warrants)

7

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

TRANSACTION SPECIFICS (CONTINUED)

Percentage of Transactions with Prepayment Penaltie s

Average Prepayment Penalty for First Year Debt

Most transactions have some form of prepayment penalty

The majority of prepayment penalties is typically 3% of the principal amount in year 1

Prepayment

0.0% 0.0%

0.0%

8%

19%

73%

0%

16%

32%

48%

64%

80%

0% 1% - 10% 11% - 25% 26% - 50% 51% - 99% 100%

% o

f R

esp

on

den

ts

19%

54%

19%

8%

0.0%0%

20%

40%

60%

≤2% 3% 4% 5% >5%

% o

f R

esp

on

den

ts

8

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Second Lien Providers are Active Market Participant s

Willingness to do a Second Lien Deal

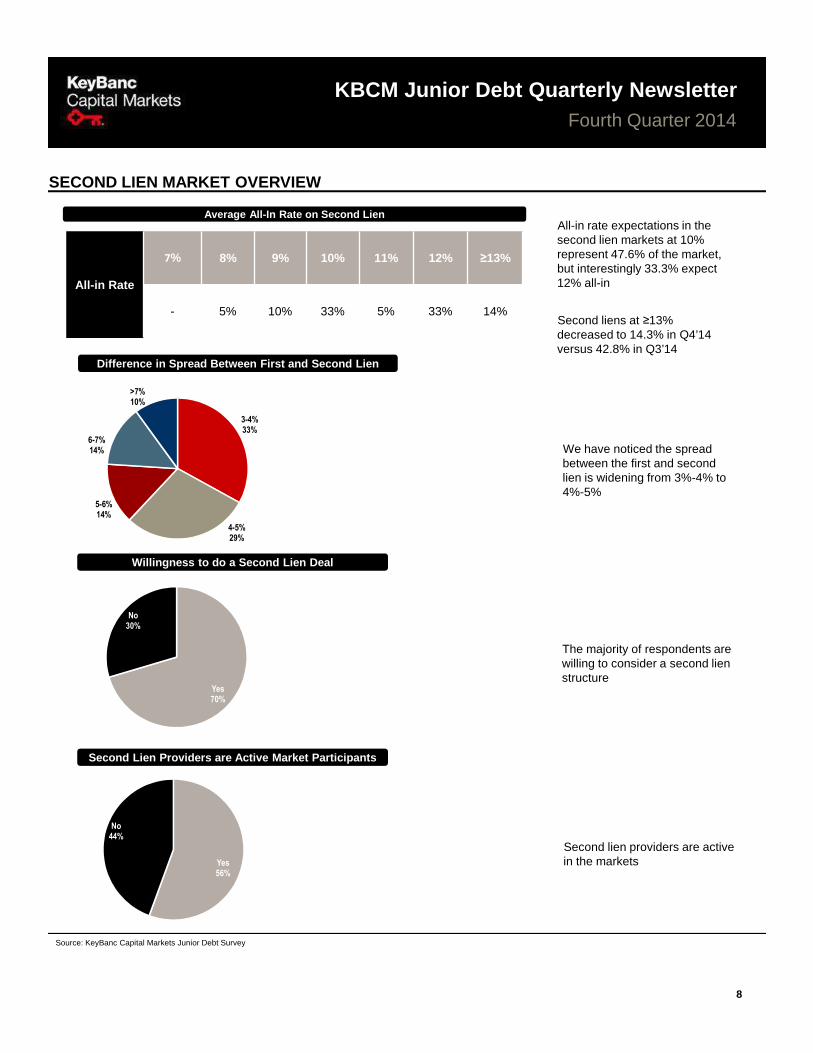

SECOND LIEN MARKET OVERVIEW

Average All-In Rate on Second Lien

All-in Rate

7% 8% 9% 10% 11% 12% ≥13%

- 5% 10% 33% 5% 33% 14%

All-in rate expectations in the second lien markets at 10% represent 47.6% of the market, but interestingly 33.3% expect 12% all-in

Second liens at ≥13% decreased to 14.3% in Q4’14 versus 42.8% in Q3’14

The majority of respondents are willing to consider a second lien structure

Second lien providers are active in the markets

Yes70%

No30%

Yes56%

No44%

Difference in Spread Between First and Second Lien

3-4%33%

4-5%29%

5-6%14%

6-7%14%

>7%10%

We have noticed the spread between the first and second lien is widening from 3%-4% to 4%-5%

9

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Unitranche Overview

12%6%

11%24%

14%12%

<=10%59%

Willingness to Provide a Unitranche Structure

Yes63%

No37%

Unitranche structures are becoming more widely accepted, 63% of respondents will consider it, up from Q3’14 (59%)

Average All-In Rate on Unitranche

We have seen a proliferation of capital providers willing to do an entire capital structure

We have seen the all-in rate on unitranche structures in the 8% range

We intend to revise the scale on future surveys to provide more detail on sub 10% pricing

10

Source: KeyBanc Capital Markets Junior Debt Survey

KBCM Junior Debt Quarterly NewsletterFourth Quarter 2014

Covenants and Defaults

Market Perspective on Ratios

Biggest Challenge Facing Junior Debt Providers

Junior debt providers anticipate the market to be consistent as leverage levels are expected to stay the same compared to the previous quarter…

…67% of respondents believe that enterprise valuations will remain the same…

…with a decrease in the number of expected realizations (48% expect an increase in activity, down from 72% in Q3’14)

MARKET EXPECTATIONS

Respondents remain relatively evenly split regarding challenges facing the current junior debt market; however, having a unitranche structure that combines senior debt and junior debt into one layer of capital, competition from other junior capital providers and aggressive senior debt markets are the top concerns

Aggressive Senior Debt Market

22%

A Unitranche Structure that

Combines Senior Debt and Junior Debt Into One

Layer of Capital24%

Competition from Other Junior

Capital Providers22%

Uncertainty Regarding

Companies' Current / Future

Performance16%

Volatile Macroeconomic

Environment11%

Other5%

19% 15%22%

48%11%11%

11%

11%

70% 74%67%

41%

0%

25%

50%

75%

100%

Senior Debt/EBITDA Total Debt/EBITDA EV/EBITDA Realizations

% o

f Res

po

nden

ts

Increase Decrease Stay the Same

37%

11%

30%

7%

11%

15%

56%

78%

56%

0%

25%

50%

75%

100%

Covenant defaults Monetary defaults Portfolio companies needing to'amend and extend'

% o

f Res

pond

ents

Increase Decrease Stay the Same