keller group plc full year results 2016/media/files/k/keller-v2/investor/presentations/...keller...

TRANSCRIPT

Keller Group plc

Full year results 2016

27 February 2017

Caspian regionNorth East Europe Business Unit

22

Agenda

• Summary and

business update

• Financial results

• Strategic progress

• Outlook

• Questions and answers

Summary and

business update

Entergy power project, Louisiana, US

Hayward BakerWick Drains Division

44

2016: Mixed performance

• Trading in North America and EMEA remained

strong with some areas of excellent performance

• Asia-Pacific had a very poor year but we have

taken the right steps to recover

• Order book at all time high, 20% above last year,

with some major recent contract wins

• Progressing well against strategic objectives

55

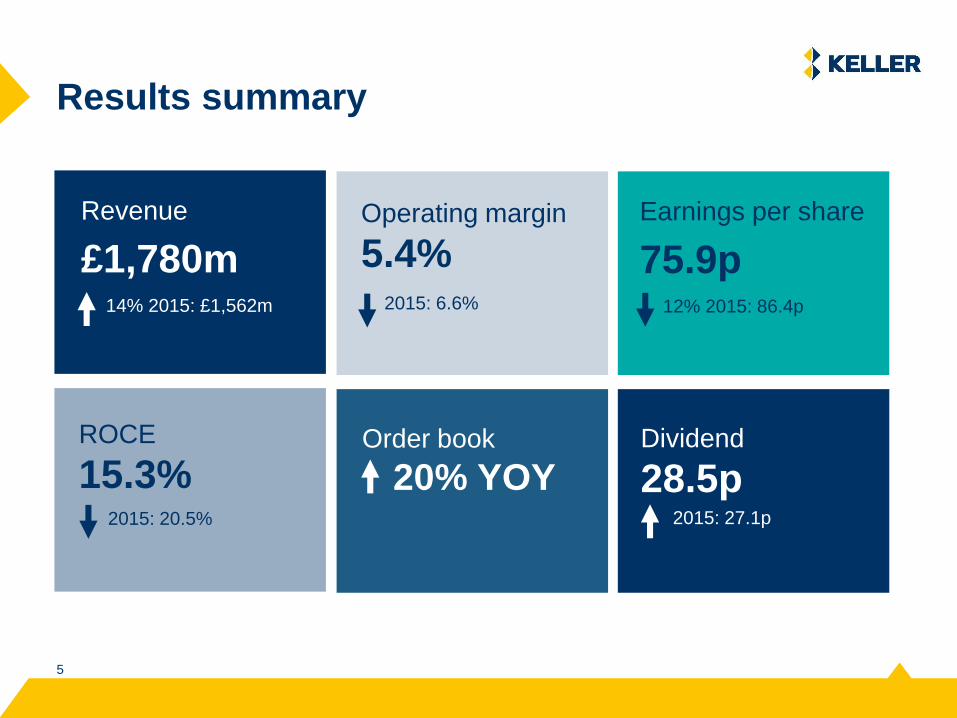

Results summary

Revenue

£1,780m

Operating margin

5.4%

Dividend

28.5p Order book

20% YOY

ROCE

15.3%

14% 2015: £1,562m 2015: 6.6%

2015: 27.1p

Earnings per share

75.9p12% 2015: 86.4p

2015: 20.5%

66

Markets in 2016

Asia-PacificEurope, Middle East

and AfricaNorth America

• Steady growth in US

• Total construction spend

up 4% on 2015

• Canada difficult,

especially Western

• Steady growth in Northern and Western Europe

• Southern Europe steady

with some weak spots

• Middle East steady

• South Africa challenging

• Brazil difficult

• South East Asia difficult, especially Singapore, heavy foundation demand and ground improvement margins

• Australia difficult

• Some pricing down 20% year-on-year

• India continuing to grow

77

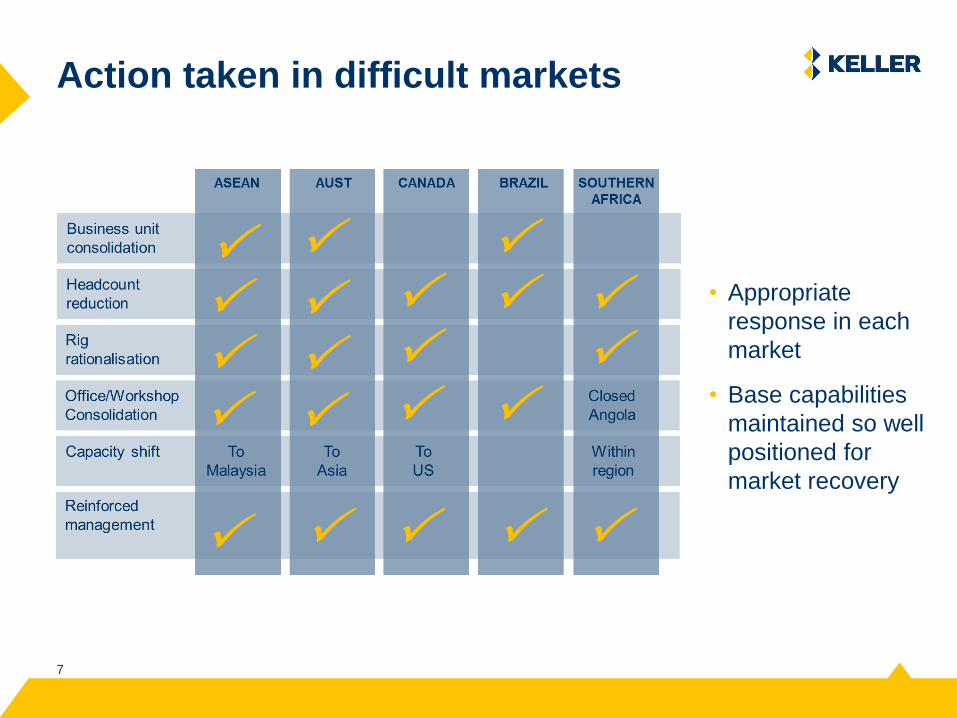

Action taken in difficult markets

• Appropriate

response in each

market

• Base capabilities

maintained so well

positioned for

market recovery

88

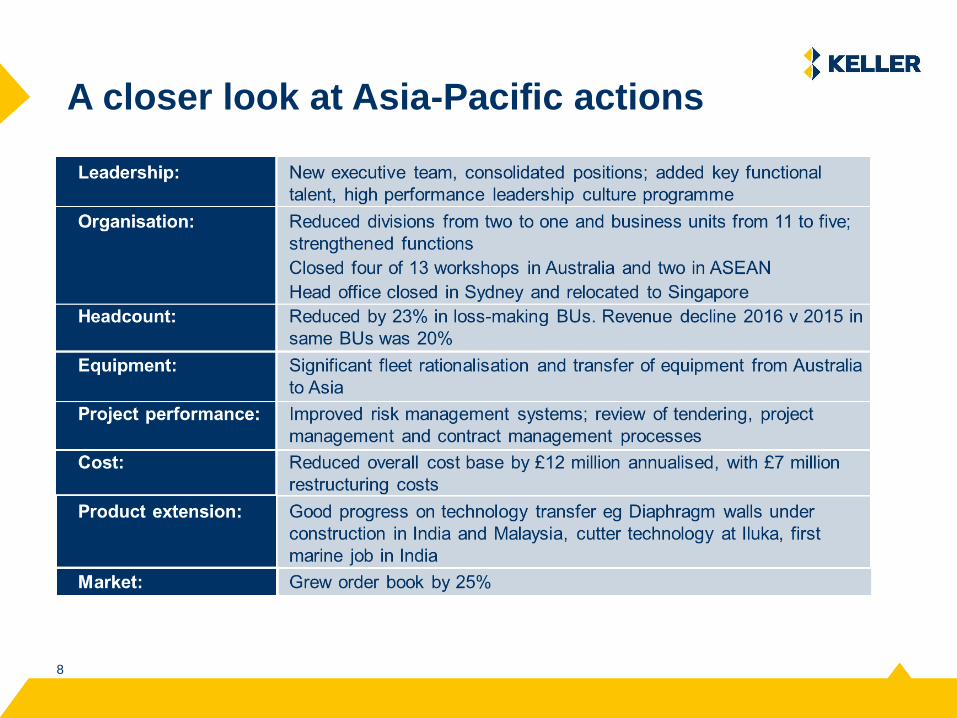

A closer look at Asia-Pacific actions

Financial results

Ritz Carlton residences, Miami

HJ Foundation

1010

Group income statement*

Record revenue

- 3% up on a constant

currency basis

£m 2016 2015 %

Change

Revenue 1,780.0 1,562.4 +14%

EBITDA 158.6 155.5 +2%

Operating profit 95.3 103.4 -8%

Net finance cost (10.2) (7.7)

Profit before tax 85.1 95.7 -11%

Tax (29.8) (33.0)

Profit after tax 55.3 62.7 -12%

EBITDA % 8.9% 10.0% -1.1bps

Operating profit % 5.4% 6.6% -1.2bps

Effective tax rate 35%

(2015: 34.5%)

Strong performances from

North America and EMEA

- Offset by APAC loss

* Before non-underlying items

1111

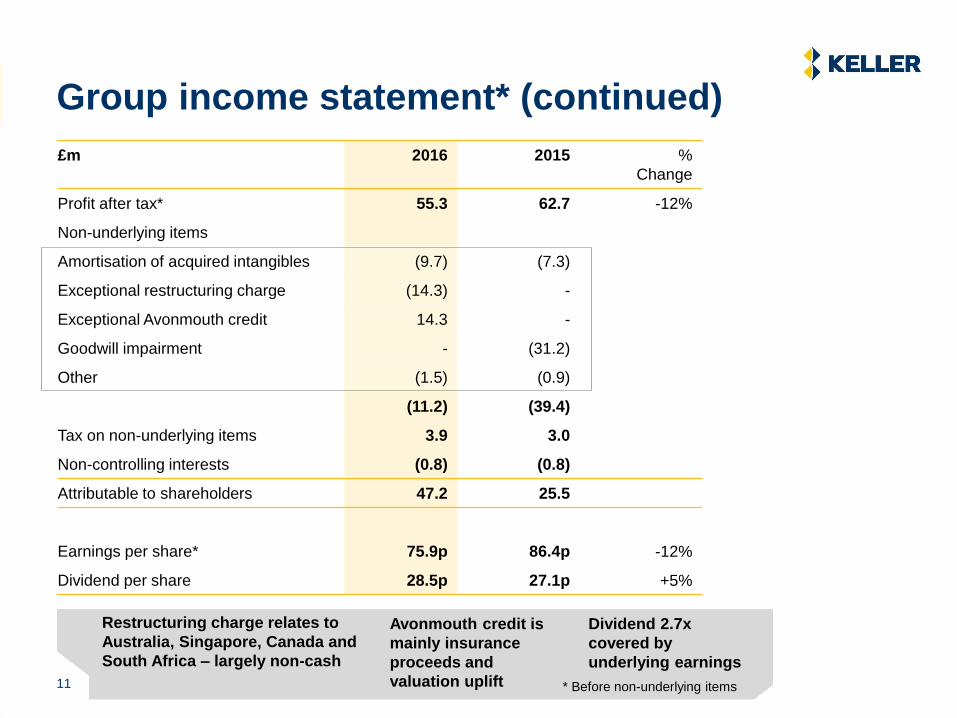

Group income statement* (continued)

£m 2016 2015 %

Change

Profit after tax* 55.3 62.7 -12%

Non-underlying items

Amortisation of acquired intangibles (9.7) (7.3)

Exceptional restructuring charge (14.3) -

Exceptional Avonmouth credit 14.3 -

Goodwill impairment - (31.2)

Other (1.5) (0.9)

(11.2) (39.4)

Tax on non-underlying items 3.9 3.0

Non-controlling interests (0.8) (0.8)

Attributable to shareholders 47.2 25.5

Earnings per share* 75.9p 86.4p -12%

Dividend per share 28.5p 27.1p +5%

Restructuring charge relates to

Australia, Singapore, Canada and

South Africa – largely non-cash

* Before non-underlying items

Avonmouth credit is

mainly insurance

proceeds and

valuation uplift

Dividend 2.7x

covered by

underlying earnings

11

1212

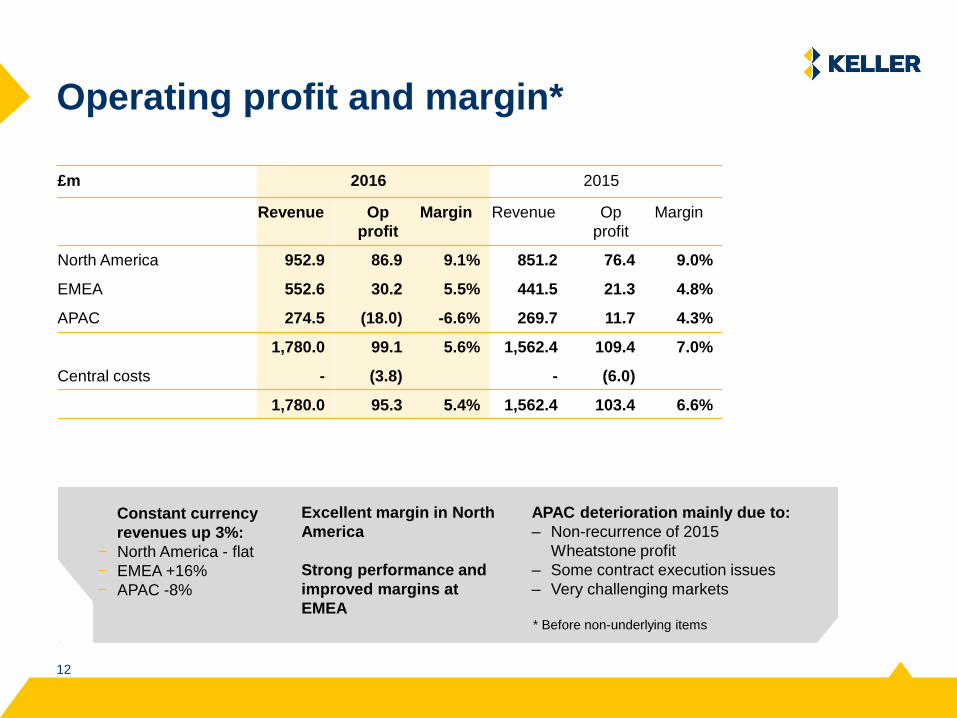

Operating profit and margin*

Constant currency

revenues up 3%:

− North America - flat

− EMEA +16%

− APAC -8%

£m 2016 2015

Revenue Op

profit

Margin Revenue Op

profit

Margin

North America 952.9 86.9 9.1% 851.2 76.4 9.0%

EMEA 552.6 30.2 5.5% 441.5 21.3 4.8%

APAC 274.5 (18.0) -6.6% 269.7 11.7 4.3%

1,780.0 99.1 5.6% 1,562.4 109.4 7.0%

Central costs - (3.8) - (6.0)

1,780.0 95.3 5.4% 1,562.4 103.4 6.6%

* Before non-underlying items

Excellent margin in North

America

Strong performance and

improved margins at

EMEA

APAC deterioration mainly due to:

– Non-recurrence of 2015

Wheatstone profit

– Some contract execution issues

– Very challenging markets

1313

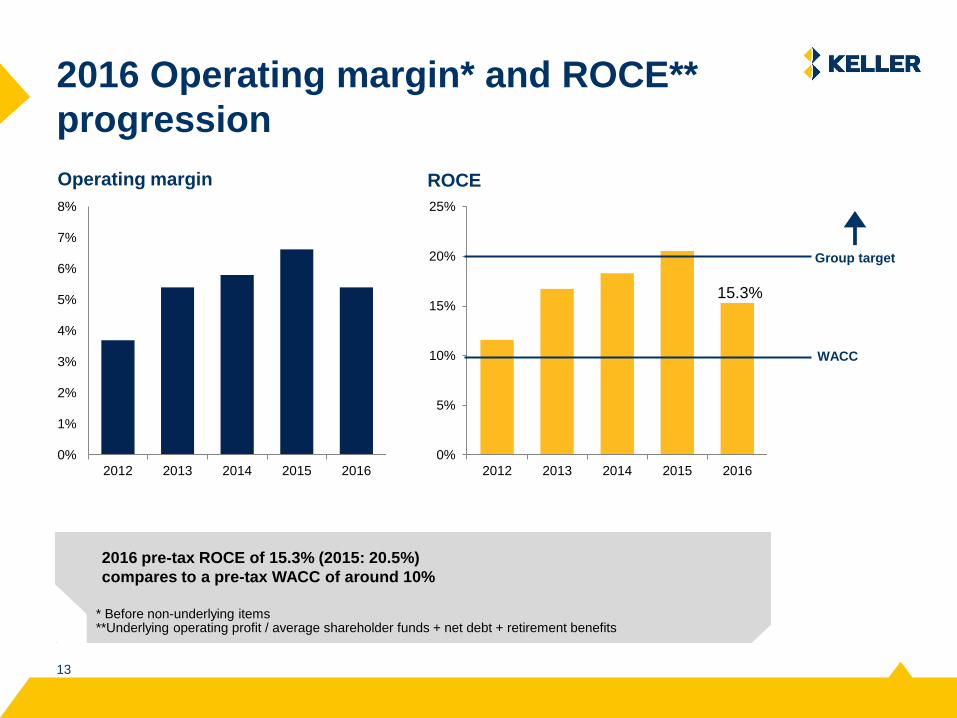

2016 Operating margin* and ROCE**

progression

0%

1%

2%

3%

4%

5%

6%

7%

8%

2012 2013 2014 2015 2016

**Underlying operating profit / average shareholder funds + net debt + retirement benefits

0%

5%

10%

15%

20%

25%

2012 2013 2014 2015 2016

Operating margin ROCE

* Before non-underlying items

2016 pre-tax ROCE of 15.3% (2015: 20.5%)

compares to a pre-tax WACC of around 10%

Group target

WACC

15.3%

1414

North America

Summary

• Another strong year in North America

• Outstanding performance from Suncoast

− Benefitted from strong residential market in its

region and lower steel prices

− New automated cut-lines will improve

efficiency

• Hayward Baker, Case and HJ Foundation all

performed well

• New organisation structure at McKinney

• Canada continues to be challenging

− £25m Toronto subway due to start spring 2017

− Annualised overheads reduced by £5m

• Year-end order book stable

Post-tension systemTempe Town Lake , Arizona

Suncoast

1515

EMEA

Summary• Strong growth in revenue and profit

• Operating margin improved from 4.8% to 5.5% -

highest since 2009

• Driven by main European businesses and

project in Caspian region

− Best result in Europe for many years

• Other markets remain difficult

− Middle East relatively quiet in 2016

− South Africa very challenging

− Brazil: concentrating on integrating Tecnogeo

• Excellent orders in H2

− Very large orders in Middle East, South Africa,

Caspian region

• Year-end order book up more than 50% - major

projects should mean excellent result in 2017

St KanzianKeller Austria

1616

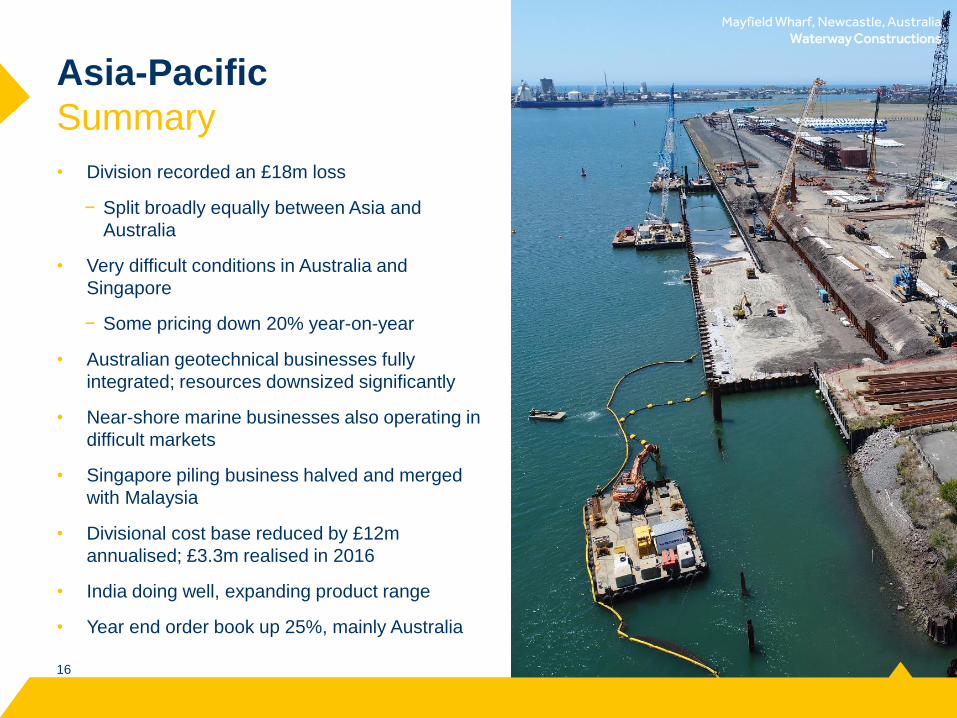

Asia-Pacific

Summary

16

• Division recorded an £18m loss

− Split broadly equally between Asia and

Australia

• Very difficult conditions in Australia and

Singapore

− Some pricing down 20% year-on-year

• Australian geotechnical businesses fully

integrated; resources downsized significantly

• Near-shore marine businesses also operating in

difficult markets

• Singapore piling business halved and merged

with Malaysia

• Divisional cost base reduced by £12m

annualised; £3.3m realised in 2016

• India doing well, expanding product range

• Year end order book up 25%, mainly Australia

Mayfield Wharf, Newcastle, AustraliaWaterway Constructions

1717

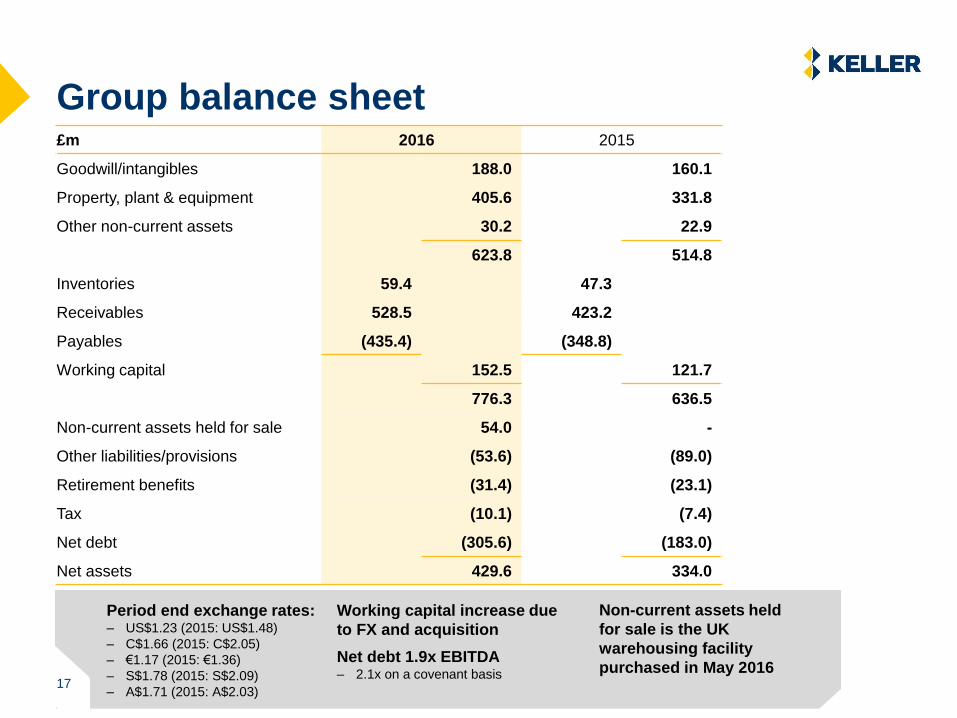

Group balance sheet£m 2016 2015

Goodwill/intangibles 188.0 160.1

Property, plant & equipment 405.6 331.8

Other non-current assets 30.2 22.9

623.8 514.8

Inventories 59.4 47.3

Receivables 528.5 423.2

Payables (435.4) (348.8)

Working capital 152.5 121.7

776.3 636.5

Non-current assets held for sale 54.0 -

Other liabilities/provisions (53.6) (89.0)

Retirement benefits (31.4) (23.1)

Tax (10.1) (7.4)

Net debt (305.6) (183.0)

Net assets 429.6 334.0

Period end exchange rates:– US$1.23 (2015: US$1.48)

– C$1.66 (2015: C$2.05)

– €1.17 (2015: €1.36)

– S$1.78 (2015: S$2.09)

– A$1.71 (2015: A$2.03)

Working capital increase due

to FX and acquisition

Net debt 1.9x EBITDA– 2.1x on a covenant basis

Non-current assets held

for sale is the UK

warehousing facility

purchased in May 201617

1818

UK warehousing facility update

• Property purchased in May 2016 for £62m

− On balance sheet as ‘held for sale’ at £54m

• Gross annual rental of £4.25m

• Insurance recoveries progressing

− £7.5m received in 2016, £5.9m in 2017

− Further discussions ongoing

• £14.3m exceptional credit in 2016

1919

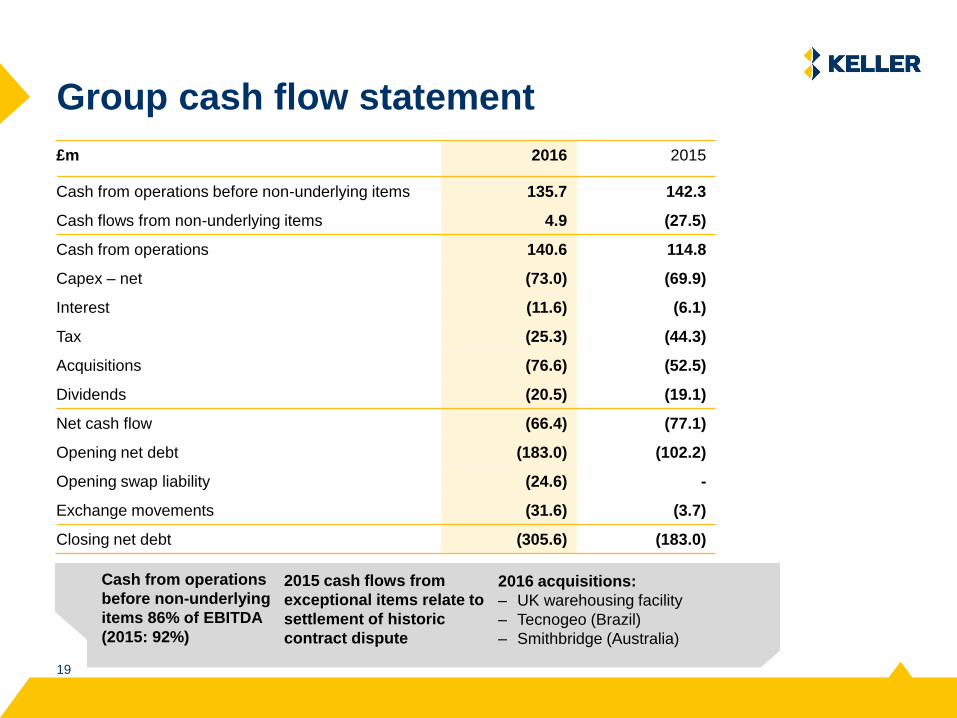

Group cash flow statement

Cash from operations

before non-underlying

items 86% of EBITDA

(2015: 92%)

£m 2016 2015

Cash from operations before non-underlying items 135.7 142.3

Cash flows from non-underlying items 4.9 (27.5)

Cash from operations 140.6 114.8

Capex – net (73.0) (69.9)

Interest (11.6) (6.1)

Tax (25.3) (44.3)

Acquisitions (76.6) (52.5)

Dividends (20.5) (19.1)

Net cash flow (66.4) (77.1)

Opening net debt (183.0) (102.2)

Opening swap liability (24.6) -

Exchange movements (31.6) (3.7)

Closing net debt (305.6) (183.0)

2016 acquisitions:

– UK warehousing facility

– Tecnogeo (Brazil)

– Smithbridge (Australia)

2015 cash flows from

exceptional items relate to

settlement of historic

contract dispute

2020

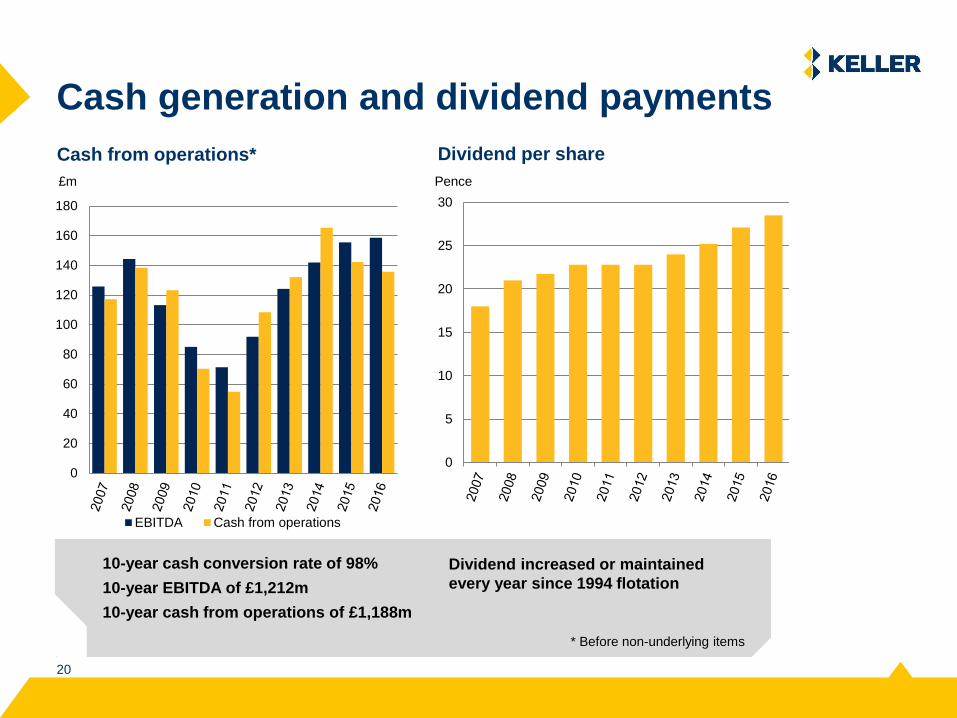

Cash generation and dividend payments

0

5

10

15

20

25

30

Cash from operations* Dividend per share

0

20

40

60

80

100

120

140

160

180

EBITDA Cash from operations

10-year cash conversion rate of 98%

10-year EBITDA of £1,212m

10-year cash from operations of £1,188m

Dividend increased or maintained

every year since 1994 flotation

* Before non-underlying items

£m Pence

Strategic progress

2222

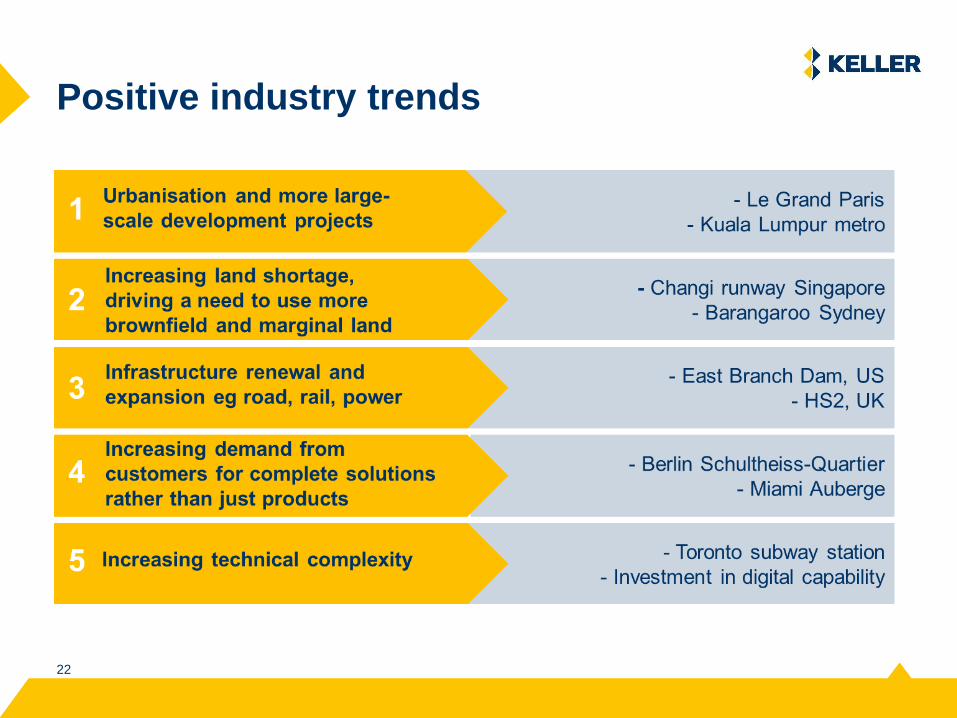

Positive industry trends

2323

Vision and strategy

Growing our product range and entering new

markets, organically and by acquisition

Building strong, customer-focused businesses

Leveraging the scale and expertise of the group

Enhancing our engineering and operational

capabilities

Investing in our people

Strategy

To be the world leader in geotechnical solutionsVision

2424

Progressing well against strategy

What has been changing?

• Company is more connected and collaborative

• Strategic alignment is much improved

• Our capabilities are expanding

− Larger projects

− Knowledge sharing

− Intra-company benchmarking

− Product technology

• Uncovering much more opportunity

2525

Progressing well against strategy

Examples

• Technology transfer: eg Secured first ever diaphragm wall

contracts in India and Malaysia

• A stronger, more unified Keller brand: Emphasising all our

companies are connected and ensuring worldwide brand

recognition

• Increased business unit collaboration: Securing and delivering

contracts they wouldn’t have won on their own eg Hayward Baker

and HJ Foundation

• Leveraging global product teams: Achieving success on bid

assistance; new design methods; technology transfer; and

equipment development

• Improving productivity: Investing in DAQ systems for our 400

vibrocats and jet grouting rigs enables remote fault-finding and

fixing

2626

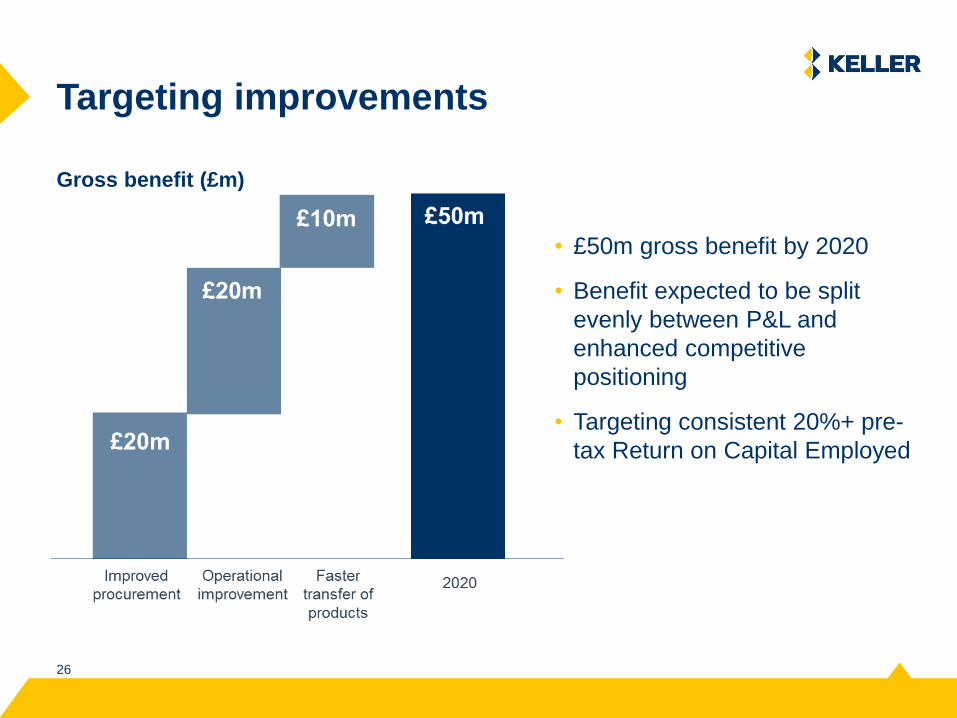

Targeting improvements

• £50m gross benefit by 2020

• Benefit expected to be split

evenly between P&L and

enhanced competitive

positioning

• Targeting consistent 20%+ pre-

tax Return on Capital Employed

Gross benefit (£m)

Outlook

Keller’s in-house equipment manufacturing

Renchen, Germany

2828

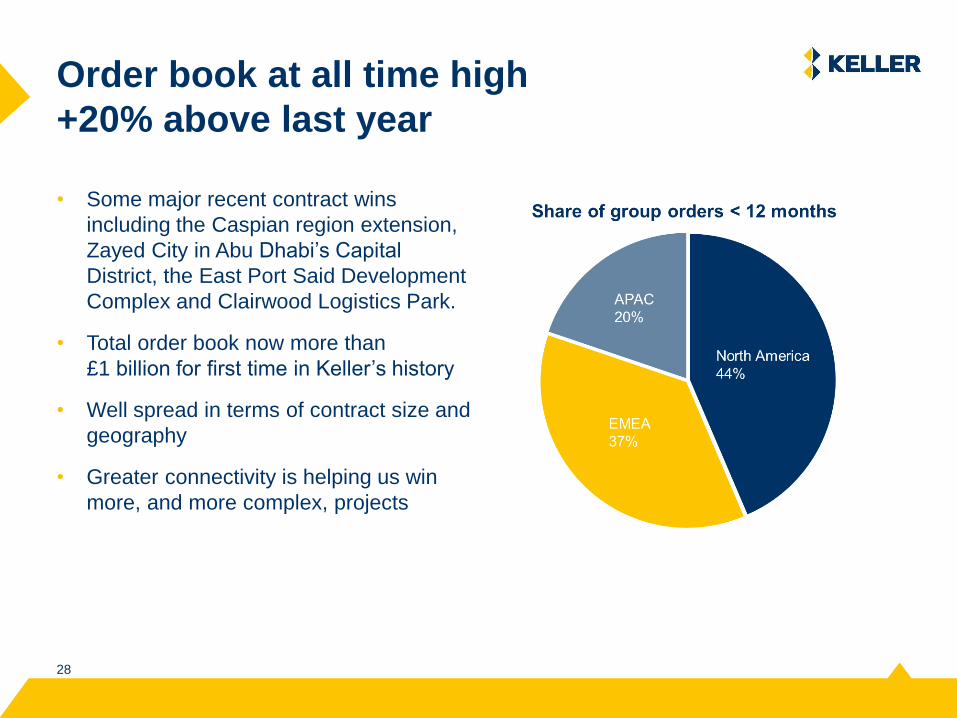

Order book at all time high

+20% above last year

• Some major recent contract wins

including the Caspian region extension,

Zayed City in Abu Dhabi’s Capital

District, the East Port Said Development

Complex and Clairwood Logistics Park.

• Total order book now more than

£1 billion for first time in Keller’s history

• Well spread in terms of contract size and

geography

• Greater connectivity is helping us win

more, and more complex, projects

2929

We expect US to remain a strong market

Market still below long-term average,

forecast to continue to grow steadily

US Housing Starts (000s)Source: US Census Bureau Housing Starts

US housing starts continue to increase,

up 6% in the year and still well below the

long term norm

US Construction spend as % GDPSource: IHS global insight and World Bank

3030

US infrastructure opportunities

• Keller US revenue from infrastructure £276m in 2016

• Current work includes bridges, combined sewer outflow (Case) and

East Branch Dam (Bencor)

• Keller well placed to support infrastructure spending acceleration

California Department of Water Resources via Reuters

• Recent Oroville

dam issues

illustrate national

challenge

• Emerging political

consensus for

significant

investment

3131

Outlook

• Long term drivers of market growth remain robust

− We are well placed to take advantage of any acceleration

in public infrastructure spending

− We remain an active consolidator in a fragmented market

• Our strategy remains clear and consistent and we’re making

good progress

− Significant opportunities to improve the business

− Targeting £50m of gross benefits by 2020

• APAC performance expected to improve in 2017 and return

to profit in 2018

• Steadily growing construction markets in US and Europe,

and management actions, give us confidence for 2017

3232

3333

Cautionary statements

This document contains certain ‘forward looking statements’ with

respect to Keller’s financial condition, results of operations and

business and certain of Keller’s plans and objectives with respect to

these items.

Forward looking statements are sometimes, but not always, identified

by their use of a date in the future or such words as ‘anticipates’,

‘aims’, ‘due’, ‘could’, ‘may’, ‘should’, ‘expects’, ‘believes’, ‘intends’,

‘plans’, ‘potential’, ‘reasonably possible’, ‘targets’, ‘goal’ or ‘estimates’.

By their very nature forward-looking statements are inherently

unpredictable, speculative and involve risk and uncertainty because

they relate to events and depend on circumstances that will occur in

the future.

There are a number of factors that could cause actual results and

developments to differ materially from those expressed or implied by

these forward-looking statements. These factors include, but are not

limited to, changes in the economies and markets in which the Group

operates; changes in the regulatory and competition frameworks in

which the Group operates; the impact of legal or other proceedings

against or which affect the Group; and changes in interest and

exchange rates.

All written or verbal forward looking statements, made in this

document or made subsequently, which are attributable to Keller or

any other member of the Group or persons acting on their behalf are

expressly qualified in their entirety by the factors referred to above.

Keller does not intend to update these forward looking statements.

Nothing in this document should be regarded as a

profits forecast.

This document is not an offer to sell, exchange or transfer any

securities of Keller Group plc or any of its subsidiaries and is not

soliciting an offer to purchase, exchange or transfer such securities in

any jurisdiction. Securities may not be offered, sold or transferred in

the United States absent registration or an applicable exemption from

the registration requirements of the US Securities Act of 1933 (as

amended).

Appendices

3535

What we do

• Keller is renowned for providing technically advanced and cost effective ground

engineering solutions to the construction industry

• We offer a wide portfolio of products, unrivalled by our competitors and manufacture

our own equipment where there’s a competitive advantage in doing so

Ground

improvement

Grouting Heavy

foundation

Earth retention Post-tension

systems

Instrumentation

and monitoring

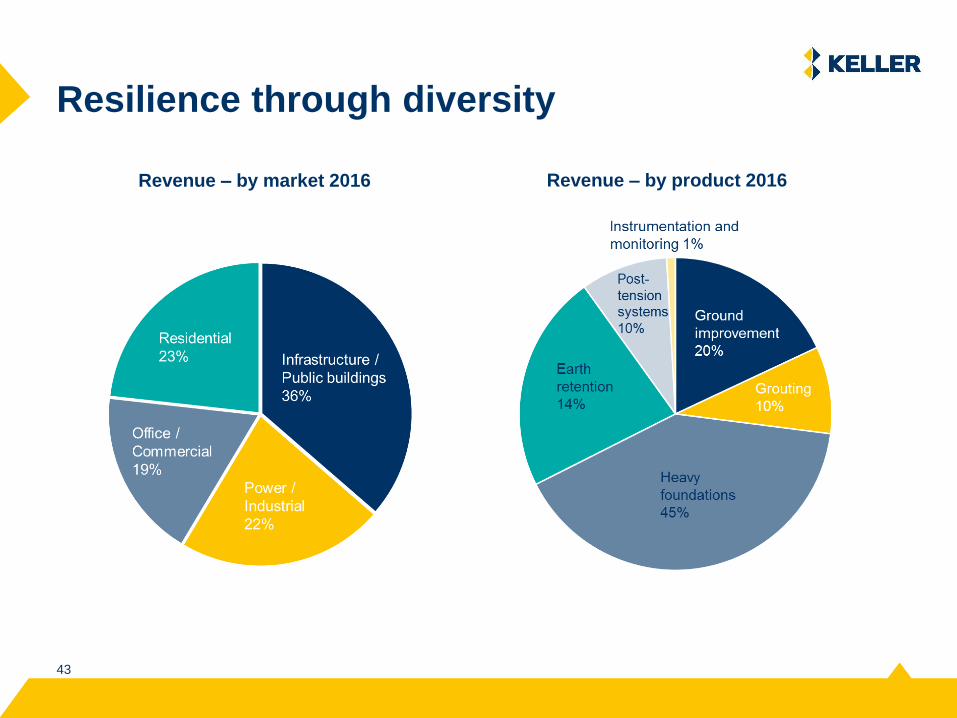

20% 10% 45% 14% 10% 1%

• Vibro

Compaction

• Vibro

replacement

• Rigid Inclusions

• Soil mixing

• Vertical drains

• Dynamic

compaction

• Dynamic

replacement

• Jet Grouting

• Compensation

Grouting

• Compaction

Grouting

• Fracture

Grouting

• Cavity Grouting

• Chemical

Grouting

• Bored Piles

• Continuous

flight auger

Piles

• Driven Piles

• Micro Piles

• Push Piers

• Marine and

near-short

structures

• Diaphragm walls

• Secant walls

• Contiguous walls

• Sheet pile walls

• Soldier pile walls

• Micro pile walls

• Gravity walls

• Ground anchors

• Soil nails

• Slab-on-grade

foundations

• High-rise

structures

• Data capture of

structures and

project attributes

3636

Number one globally

with strong local presence

• Operations in more

than 40 countries

across five

continents

• 21 business units

• Strong local

relationships that

keep us responsive

and competitive

locally Countries where we’re operational

Top three in terms

of market share in

11 countries:

• United States

• Canada

• Germany

• Poland

• Austria

• Slovakia

• Bahrain

• Brazil

• South Africa

• Australia

• Malaysia

3737

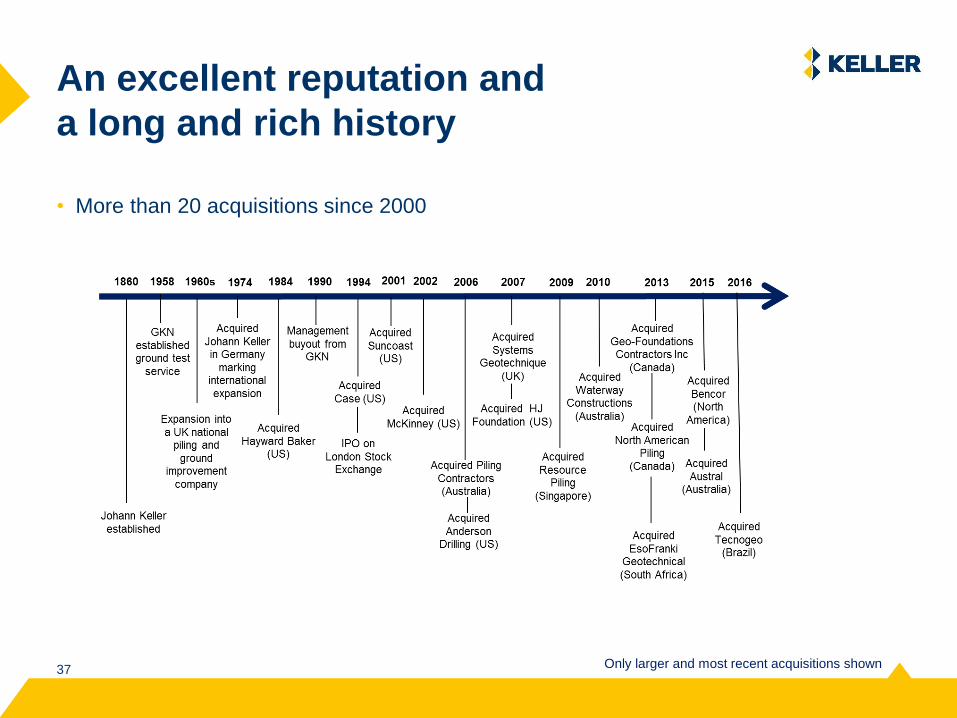

An excellent reputation and

a long and rich history

Only larger and most recent acquisitions shown

• More than 20 acquisitions since 2000

3838

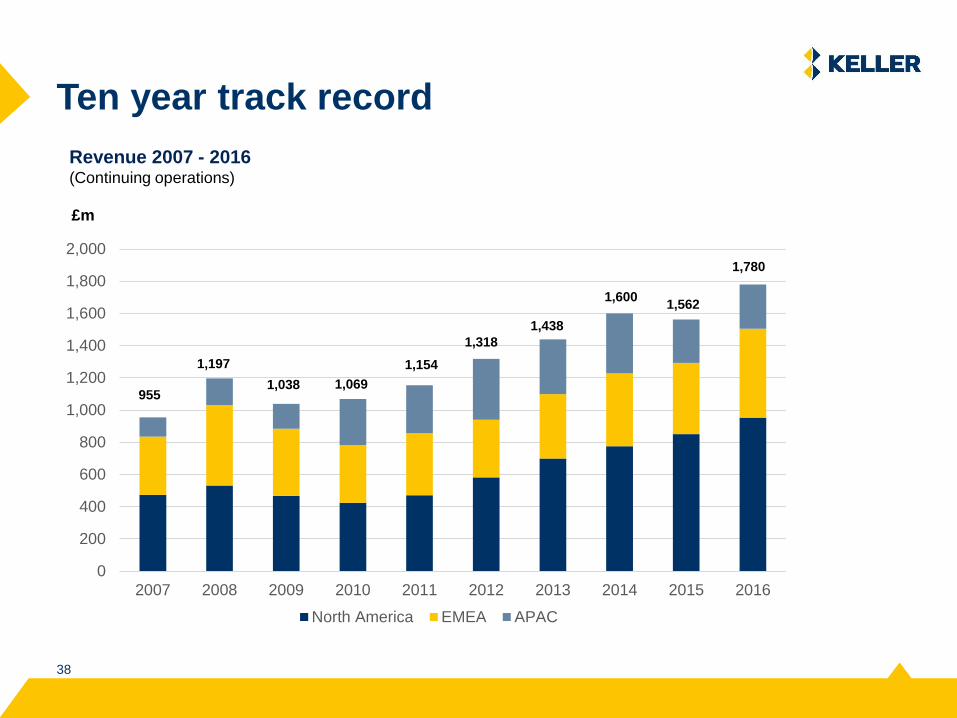

Revenue 2007 - 2016(Continuing operations)

Ten year track record

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

North America EMEA APAC

1,197

1,038 1,069

1,438

1,600

1,780

1,562

955

1,154

1,318

£m

3939

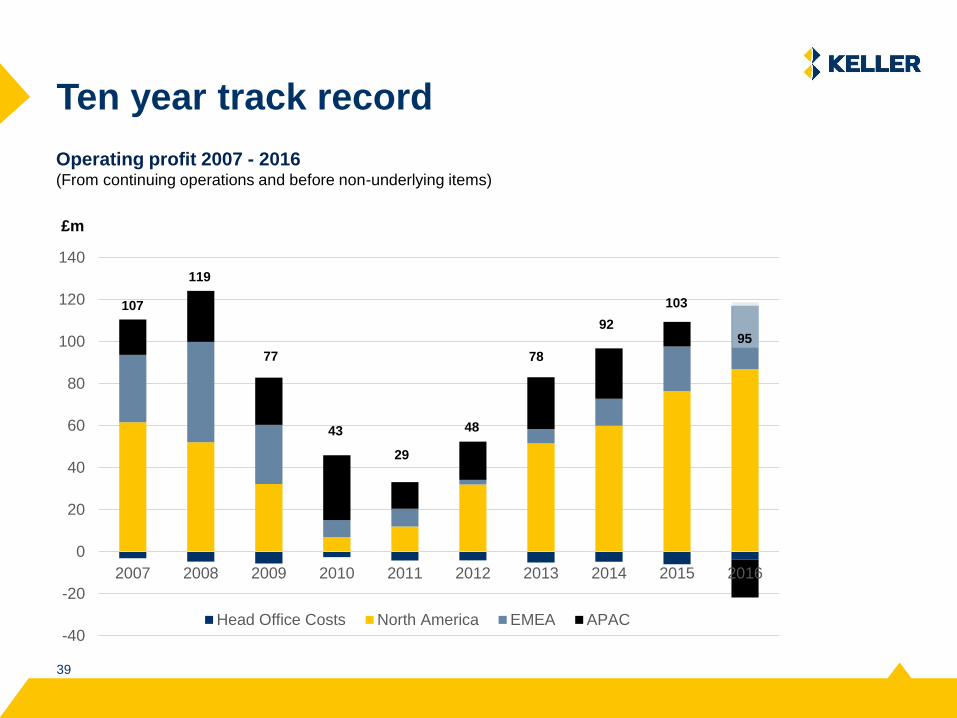

Operating profit 2007 - 2016(From continuing operations and before non-underlying items)

Ten year track record

-40

-20

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Head Office Costs North America EMEA APAC

103

48

107

119

77

43

29

78

92

£m

95

4040

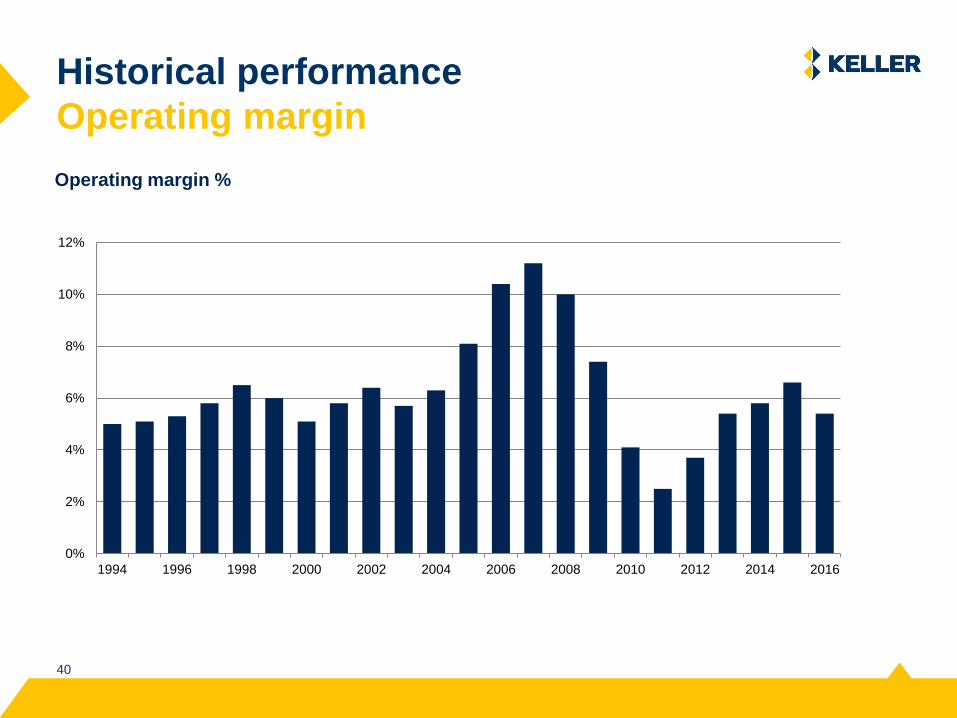

Historical performance

Operating margin

Operating margin %

0%

2%

4%

6%

8%

10%

12%

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

4141

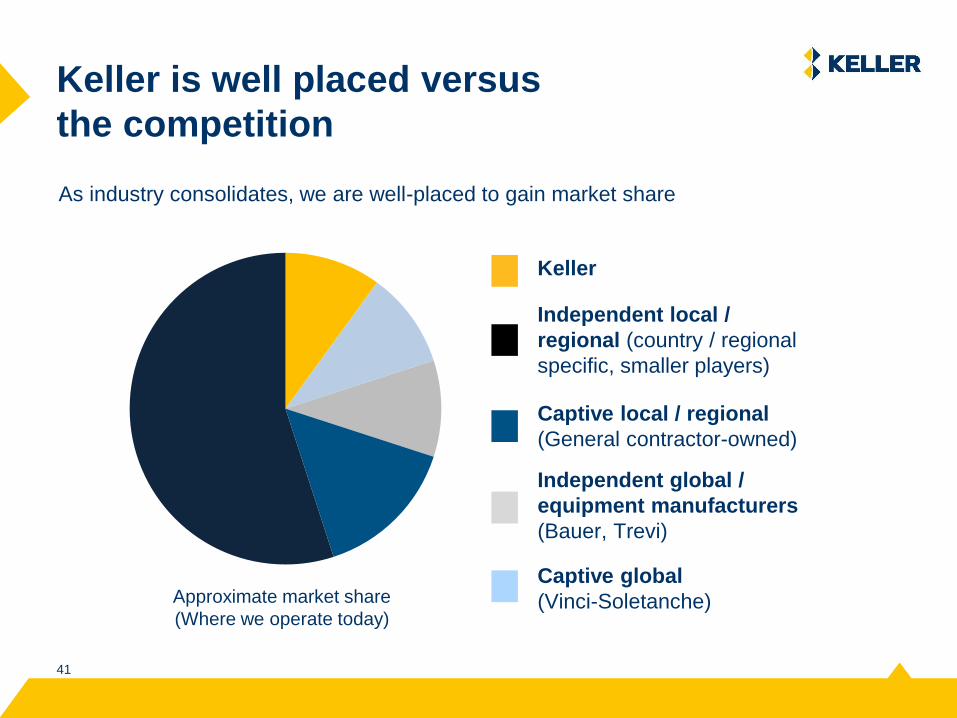

Keller is well placed versus

the competition

Independent global /

equipment manufacturers

(Bauer, Trevi)

Captive global

(Vinci-Soletanche)

Keller

Captive local / regional

(General contractor-owned)

Approximate market share

(Where we operate today)

Independent local /

regional (country / regional

specific, smaller players)

As industry consolidates, we are well-placed to gain market share

4242

Strong local relationships keep us

responsive and competitive locally

• 21 business units

• Typical revenues of £40m to £100m

“Other competitors do not have

the same knowledge base

related to execution, design

and quality control as Keller”

Project Superintendent,

Industrial Client, NA

“Excellent delivery of project in

limited time, from procurement of

materials to installation”

Commercial Lead,

Manufacturing Client, APAC

“Having used Keller for many

years, we like the fact they have a

wide range of solutions…a real

benefit when determining the

most cost effective option”

Commercial Director,

Residential Developer, EMEA

4343

Resilience through diversity

Revenue – by product 2016Revenue – by market 2016

4444

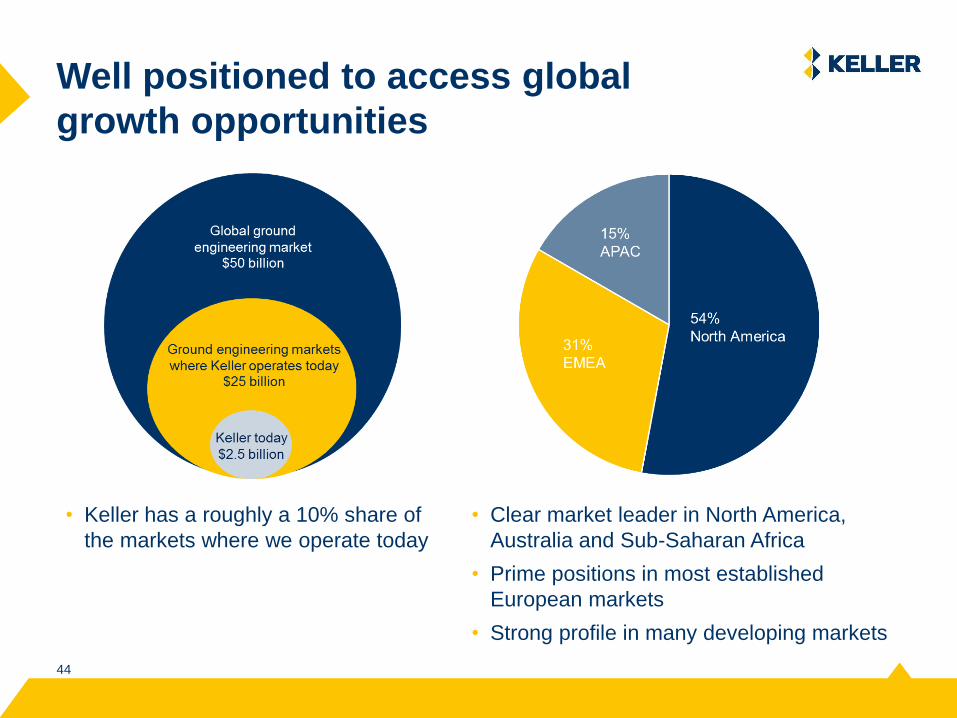

Well positioned to access global

growth opportunities

• Keller has a roughly a 10% share of

the markets where we operate today

• Clear market leader in North America,

Australia and Sub-Saharan Africa

• Prime positions in most established

European markets

• Strong profile in many developing markets

4545

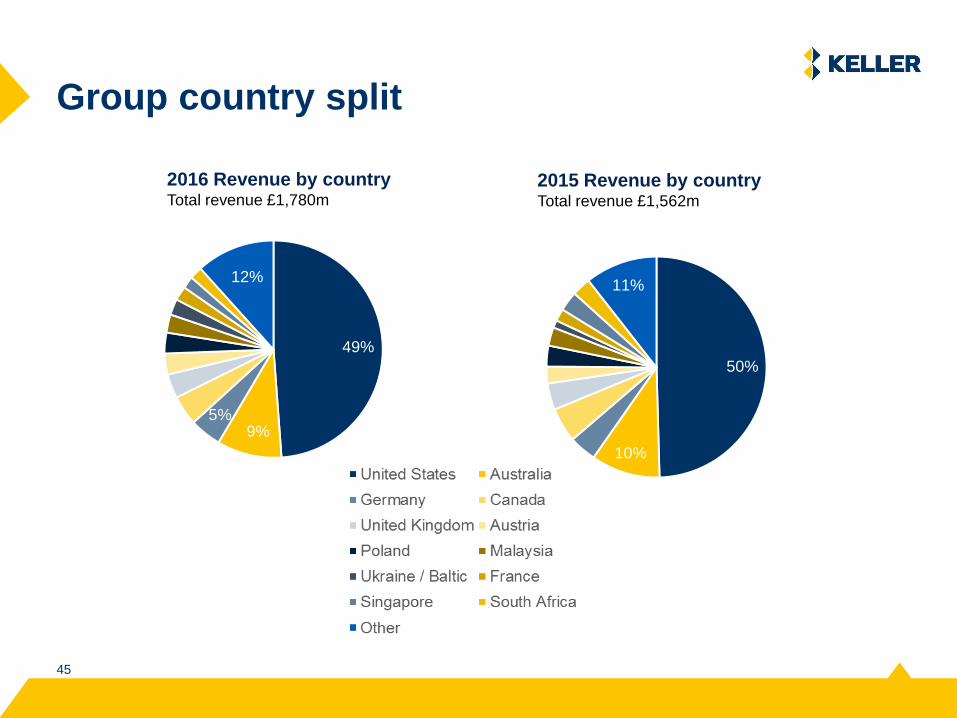

Group country split

2016 Revenue by countryTotal revenue £1,780m

2015 Revenue by countryTotal revenue £1,562m

49%

9%5%

12%

50%

10%

11%

4646

Geographical market approach

4747

Two routes to high margin

HJ Foundation

• Mainly ‘construct only’

• Few products

• Strong market presence

• Highly efficient

North East Europe (Poland)

• ‘Design and construct’

• Multiple products

• Strong design capability

• Good market share

4848

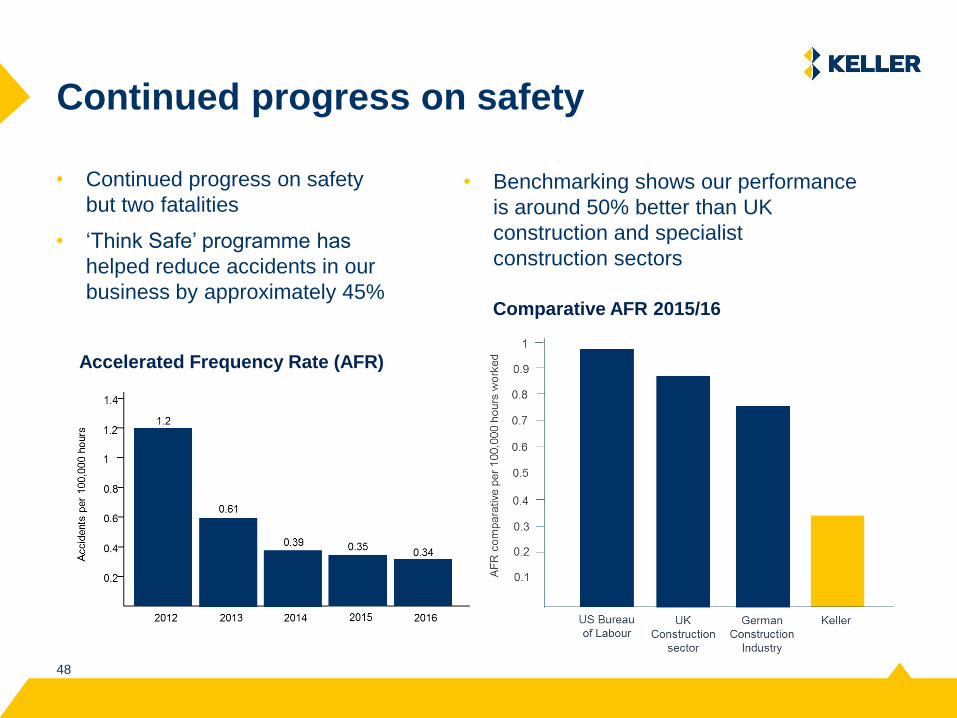

Continued progress on safety

• Continued progress on safety

but two fatalities

• ‘Think Safe’ programme has

helped reduce accidents in our

business by approximately 45%

• Benchmarking shows our performance

is around 50% better than UK

construction and specialist

construction sectors

Accelerated Frequency Rate (AFR)

Comparative AFR 2015/16

4949

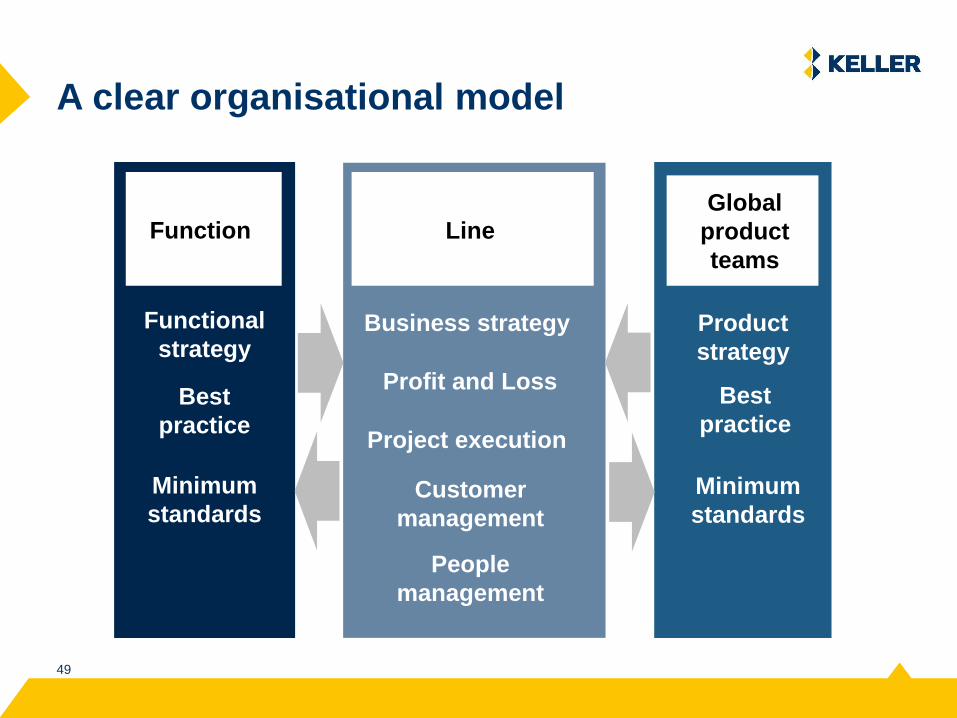

A clear organisational model

Line

Project execution

Customer

management

People

management

Business strategyFunctional

strategy

Best

practice

Minimum

standards

Global

product

teams

Best

practice

Minimum

standards

Product

strategy

Profit and Loss

Function

5050

A stronger, more unified Keller brand

5151

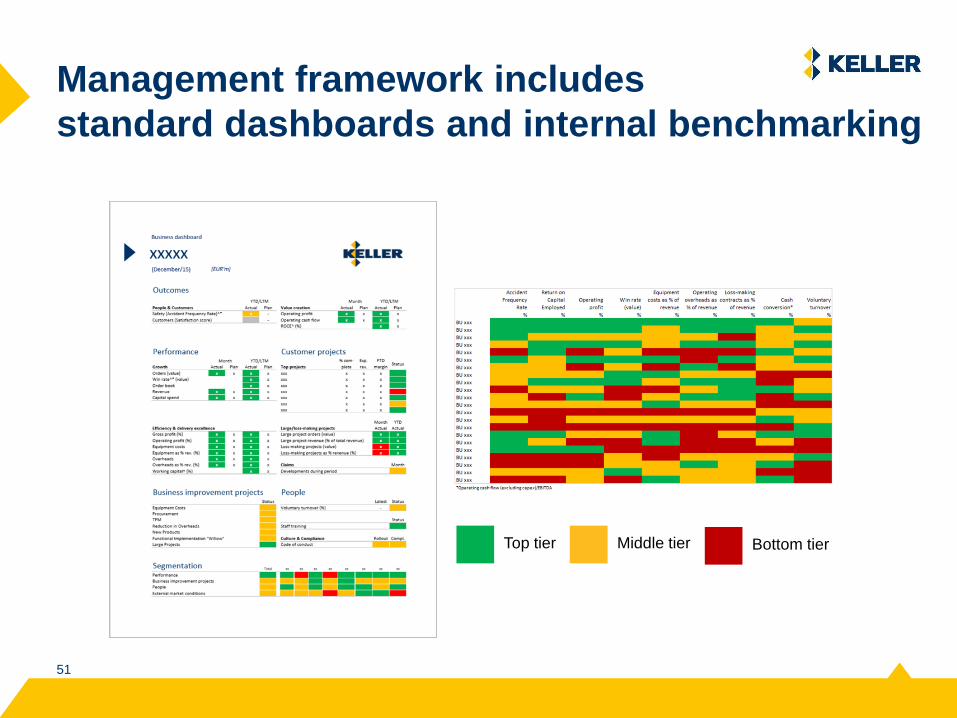

Management framework includes

standard dashboards and internal benchmarking

Top tier Middle tier Bottom tier

5252

Notable contract awards

East Port Said Development Complex, Egypt

5353

Notable contract awards

Clairwood Logistics Park, Durban, South Africa

5454

Notable contract awards

Zayed city infrastructure works, Abu Dhabi

5555

Capital allocation priorities

1. Profitable organic growth opportunities

2. Bolt-on acquisitions meeting Keller’s investment criteria

3. Ordinary dividends

• At a level allowing dividend growth through the cycle

4. Deploying funds for the benefit of shareholders

• Only where the balance sheet allows

• Unlikely to be considered if could take net debt to > 1.5x EBITDA

- After taking account of other investment opportunities/cash requirements

Leverage typically to be

maintained at between 1.0x and

2.0x EBITDA

Any short term return of capital likely

to be share buy-back