kempen insight · for example, abp ‘we need to combat the ... /// test xxxxx xxxxx foto xxx...

TRANSCRIPT

THE NETHERLANDSFocusing on

the long term

SiLLy SEASoN?us presidential elections

the role oF yiELDSand TRANSpARENcy

Kempen insight /// July 2016

I NS IGHTKEMPEN

7

10

4,5jr

KEM

PEN

EU

ROPE

AN

PRO

PERT

Y ST

RATE

GY

TR

AC

K R

ECO

RD

*

2012

201

3

20

14

2

015

2016

* Bron: KCM juni 2016

CO2

BEREIKBAARHEID

PLAFONDHOOGTEGOVERNANCE

20

Kempen Insight, July 20162

table oF contentstable oF contents

4

‘There is no substitute for active investors who develop a deep understanding of businesses’/// interview with dominic barton,global managing director atmcKinsey & company

Quick visit to Edinburgh/// Meet the Kempen european small-cap team

Among professors/// inaugural speech of chief strategist – and professor –

roelof salomons in words and pictures

Looking right through real estate/// New modus operandi yields greater insight

Kempen Insight, July 2016 3

/// colophon

Juli 2016 ©Kempen Capital Management

Editorial addressKempen Capital Managementto: Secretariaat KCMPostbus 756661070 AR AmsterdamT + 31 20 348 [email protected]

collaboratorsPHOTOGRAPHY Johannes Abeling,Henrike Beukema, Getty, Mario Hooglander, Philip Jenster, Henk Veenstra, Laurence WinramTEXT Jos Leijen, Daniëlle Levendig,Bas Kooman, Stephanie Lewis, Lesa Sawahata

EditorsRuth van de Belt, Lars Dijkstra, Anja Corbijn van Willenswaard, Evert Waterlander, Charlotte Wilberts

Art direction/designHenrike Beukema

Kempen Capital Management is included in the register of the Netherlands Authority for the Financial Markets (Autoriteit Financiële Mark-ten) as manager of investment funds and as asset manager. This information may not be construed as an offer and provides insufficient basis for an investment decision.

Foreword

at the start of this year we anticipated a year of high

volatility and little direction on the financial markets. so

far, our predictions have proved to be highly accurate.

as ruth van de belt rightly notes in her column, we are

witnessing brexit upheaval in the united Kingdom and

presidential elections in the united states. the summer

promises to be anything but dull for news.

at Kempen capital management we are monitoring

current events closely, and as always we look beyond

our own national borders when it comes to economic

trends. Yet we also take a good look at the netherlands.

dominic barton, global managing director of mcKinsey

& company and one of the people behind Focusing

capital on the long term, says in our interview with

him: ‘the netherlands has a proud tradition of leader-

ship on long-term investing and incorporation of

environmental, social and governance.’ We are very

pleased that he is participating in shiFt to long-term

investing, the english-language newsroom

where you will find the latest research

and opinions on long-term investing.

someone else who intends to conduct a

lot of research into the long term and the

effects on investment is our chief stra-

tegist roelof salomons. he was

recently appointed professor of

investment theory and asset

management at the university

of groningen. this edition of

Kempen insight includes a

report on his inauguration in

pictures and words.

in short: together with you, we

remain alert to the short term and

set our sights on the long term.

i look forward to hearing your

comments and suggestions on

reading this insight.

Lars Dijkstra

Chief Investment Officer

If the price is right/// relevance of cost transparency for uK and dutch pension funds 16

Books that inspire/// as selected by evert Waterlander 19

Volatility on the horizon/// politics could cause turbulence 22

Column Ruth van de Belt/// us summer spectacle 24

8

What explains the low volatility anomaly’?

4 Kempen insight, July 2016

/// by Lesa saWahata Lphoto Johannes abeling

InterviewDominic Barton, Global Managing Director McKinsey & Company

‘We need to combat thegrowing short-term mindset’

As co-author of the seminal article ‘Focusing Capital on the Long Term’ (with Mark Wiseman), Dominic Barton of McKinsey & Company triggered the long-term investing discussion that is (slowly) gaining traction in global finance. In this Q & A interview, conducted with the editors of Kempen Insight, Dominic answers key questions regarding why – and how – the shift to longterm should be implemented, and how The Netherlands is already well-placed to drive the FCLT agenda.

in your opinion, what changes must be made in asset

management in the near future?

‘asset management has a critical role to play in reorienting

the investment value chain toward long-term value crea-

tion. First, asset owners and managers must reorient their

portfolios toward longer-term performance, looking to

asset classes and investments, like infrastructure, that

provide long-term value, but may take longer to see

returns.

Kempen Insight, July 2016 5

to support these changes, asset managers

should align compensation and perfor-

mance measurement with these longer

time horizons – such as gic’s (investment

corporation of the government of

singapore) policy to evaluate manager

bonuses on 5- and 10-year performance.

Furthermore, new benchmarks have a role

to play in encouraging asset managers to

take a longer view and encourage compa-

nies to adopt and showcase sustained value

creation plans. For example, the recent

creation of the s&p long term Value crea-

tion index –and the strong interest in using

the new benchmark – is a great step

forward.

Finally, asset managers must devote more

time and resources to engagement with

management teams and boards. there is

no substitute for active investors who

develop a deep understanding of busi-

nesses and promise support for long-term

value creation. 64% of asset managers say

their engagement with boards is increasing

– and this is an encouraging sign.’

What has been your motivation in

launching the Focusing capital on the

Long Term (FcLT) initiative?

‘along with our partners, mcKinsey helped

to launch the Fclt initiative because we

saw the growing costs of short-termism.

i had spent over a decade living and

working in east asia, where corporate and

investor timelines are far longer, and when i

returned to living in london, i was

surprised by how much pressure ceos felt

to demonstrate results in a matter of quar-

ters. We saw that this was destroying

economic value, diminishing shared pros-

perity among a broader set of stakeholders,

and undermining trust in capitalism in the

wake of the financial crisis.

the initiative was launched – along with

mark Wiseman from the canadian pension

plan investment board, larry Fink from

blackrock, cyrus mistry from tata and

andrew liveris from dow – because we

believed that the issue needed more public

attention, more rigorous analysis, and

concrete action plans to help investors,

executives, and boards combat the

growing short-term mindset.’

What is the role of Dutch institutional

investors (pension funds) in the long-

term debate?

‘the netherlands has a proud tradition of

leadership on long-term investing and

incorporation of environmental, social and

governance factors, and it is a hub of

leading pension players. For example, abp

‘We need to combat thegrowing short-term mindset’

the newsroom www.shiftto.org

facilitates the debate on long-term

investing. here you can find

articles, columns and research from

thought leaders from varied

background and ages.

/// tekst XXXXX XXXXX foto XXX XXXXXXXXXXX

Kempen Insight, July 20166

dominic barton and paul gerla, ceo of Kempen capital management.

Kcm recently became a partner of the Fclt-initiative that was founded

in 2013 by mcKinsey & company en the ccpib (canadian pension

plan investment board).

results, and what value sacrifices they are

willing to make to meet short-term targets.’

What do you find particularly important

and significant in such initiatives as FcLT

and www.shiftto.org ?

‘i am impressed by the breadth of interest

in these initiatives. despite the geographic

differences in business culture or regulation,

we find that short-termism is of concern

around the world. unlike many business

associations, these efforts have attracted an

incredibly diverse set of stakeholders across

geographies and industries– from mining to

consumer products and from hedge funds

to government officials.

in addition, i believe the practical orienta-

tion of these efforts is unique. While we are

interested in studying and diagnosing the

issue, we have also worked collaboratively

with members to create concrete action

plans to pilot new approaches within

investment funds, boards, and manage-

ment teams. We hope that Fclt will

continue to take this action-oriented

approach as we grow!’

on these topics?) and the tenor of corpora-

te-investor dialogue (e.g. are analyst calls

focused on minutiae over the next quarter

or truly strategic issues?). long-term health

measures such as quality of talent pipeline,

innovation rate, trust levels with key stake-

holders, and resilience also need to be iden-

tified for each company.

at a systemic level, we can measure long-

term investing by the proportion of cash

flow and profits going back to investment

(either in capital expenditure or r & d),

and unfortunately these numbers seem to

be falling. Finally, we continue to conduct

qualitative surveys of how much pressure

managers feel to demonstrate short-term

was recently ranked by the asset owner

disclosure project as the 4th best instituti-

onal investor in the world at managing

climate risk (and was by far the largest in

terms of assets among the top 10). another

good example is pggm’s active engage-

ment with the companies in its small-cap

equities portfolio on long-term strategic

topics. institutional investors elsewhere in

the world need to consider the relevance of

these approaches to their own strategies.’

How – and with what measurements –

can you determine when long-term

investing is a success?

‘long-term investing is a notoriously diffi-

cult outcome to measure. however, there

are several areas that are key indicators.

First, and foremost, we can look to invest-

ment returns for managers over horizons

and whether asset owners are meeting their

most fundamental long-term objectives

(e.g. can pension funds meet obligations

without taking undue risk?). similarly, we

can look at corporations and boards’ dedi-

cation of time and resources to long-term

strategy (e.g. how long are they spending

about dominic bartondominic barton is the global managing director of mcKinsey &

company. in his 27 years with the firm, barton has advised clients

in banking, consumer goods, high tech and industrial. dominic

leads mcKinsey’s work on the future of capitalism, long-term

value-creation and the role of business leadership in society, and is

the author of more than 80 articles on related topics. this includes

the article ‘Focusing capital on the long term’ (co-authored with

mark Wiseman) and which sparked the ongoing Fclt discussion.

amongst his many board and advisory positions, dominic is a

member of the canadian prime minister’s advisory committee on

the public service, a trustee of the brookings institution and a

member of the editorial board of shiFt to, long term investing.

‘Despite the geographic differences in business culture or regulation,

we find that short-termism is of concern

around the world’

Kempen Insight, July 2016 7

Karen mcgrath, Vivienne taylor, erika White, mike gray, tommy bryson,

martin stockner, Kathleen dewandeleer.

Mark McCullough (in-absentia).

SoLiD FoUNDATioNS, BRiGHT FUTUREhigh conviction. Quality companies. esg engagement. Kempen has been generating

alpha in european small-caps from edinburgh since 1997.

edinburgh castle

To cASTLE RocK Visiting the european small-cap team in edinburgh

Kempen Insight, July 20168

/// by Jos leiJen visual gettY

Low volatility equities yield a higher return

than might be expected based on their level

of risk. Analysts call this the low volatility

anomaly. Until recently, the explanation for

this discrepancy was chiefly sought in investor

and analyst behaviour. Yet interest rate risk

also plays a significant role, according to

investment strategist Ivo Kuiper at Kempen

Capital Management.

low volatility equities are equities that are

subject to relatively minor price fluctua-

tions, without excessive outliers. they

belong to low–risk sectors, such as utilities

and consumer staples. these companies

enjoy stable incomes and predictable earn-

ings. dutch examples include unilever and

ahold, or further afield nestlé and brewer

anheuser-busch inbev. solid companies.

Gambleas long ago as last century researchers

discovered that low volatility equities display

a better return than they ought to given the

relatively low risk involved. the reason for

this inexplicable outperformance was chiefly

sought in analyst and investor behaviour.

investors seek higher returns and conse-

quently tend to ignore low volatility equi-

ties. they prefer to gamble on earning a

high return and accept the risk that the

return may turn out lower. another expla-

nation is that analysts are over-optimistic

about high volatility equities.

these mechanisms probably do play a part,

but according to ivo Kuiper this is smaller

than has been assumed in the past.

Sensitive to interest ratesas cashflows and earnings for low volatility

equities are easy to predict, interest rates

are important to determining the cash

value, Kuiper explains. if interest rates fall,

the future earnings are worth more.

The role of interest rate

in addition to his job as an

investment strategist at

Kempen capital management,

Kuiper is a part-time researcher

at tilburg university. Kempen

capital management and the

university have worked together

since 2011. its master’s

students can complete their

degrees at Kempen capital

management. among other

things, Kuiper is conducting

research into the relationship

between low volatility equity

prices and interest rate trends.

interest rate risk partially explains outperformance by low volatility equities

9Kempen insight, July 2016

What is more important is that investors

take the interest rate effects on low volati-

lity equities into account in their investment

strategies, Kuiper says. “say that your

strategy involves your portfolio containing

one third equities, one third bonds and one

third other securities. in this case, you need

to be aware that low volatility equities

move more in line with bonds than other

equities do. You therefore hold a higher

interest rate risk in your portfolio.”’

Ivo Kuiper

Investment Strategist

play a role, but a smaller one than has

previously been assumed. We also see that

the reward for interest rate risk is relatively

high. Further research should reveal the

reason for this. We do not yet understand

everything.”

Cautionover the past few years, low volatility

equities have profited more from the

declining interest rates than other equities.

Kuiper predicts that low volatility equities

will underperform when interest rates rise.

as Kempen capital management expects

interest rates to rise in the long term, we

are cautious about recommending this

strategy at the moment.

if interest rates rise, these equities become

less interesting. this effect can be

compared to the value growth of bonds.

“the more easily earnings can be

predicted, the more sensitive the equities

are to interest rate trends. Yet if this is the

case, you should also expect to receive a

reward for the interest rate risk. after all, if

interest rates rise, the future earnings and

due dividends will be worth less in relative

terms. the research i have conducted

together with master’s student robbert

beilo demonstrates that this effect does

exist.”

the interest rate effect explains part of the

low volatility anomaly, but not all of it.

“the behaviour factors undoubtedly also

10 Kempen insight, July 2016

/// by roeloF salomons photo henK Veenstra

Predicting returns

On investment theory and asset management

noise in the data, the latest crazes.... in the short term, investment is speculation. in the long term, however, predictability can work in your favour, roelof salomons argues in his inaugural speech as professor of investment theory and asset management at the university of groningen.

Predicting returnsRector Magnificus, esteemed guests, each year, i play a variant of the beauty contest as described in such lively terms by John

maynard Keynes (1936) with my students. the idea is to get everyone in the lecture theatre

to write down a number between 0 and 100, whereby the winner is the player with the

number closest to 2/3 of the average. as all the players possess all the information and are

completely rational, there is only one ‘correct’ number: 0. unfortunately, it doesn’t work like

that. most players start by randomly choosing a number from the set (50) and then think one

step ahead (33). step 2 thinkers end up at 22, while those who think one step further name

the number 15. and each year i have a few students (mostly those with quantitative back-

grounds) who then go through all the steps and come up with 0.

the game shows all too clearly that it’s not about who is ‘pretty’ but about the expectation of

what the consensus considers to be ‘pretty’. the same goes for modern investment practice.

it is not so much about the predictability of earnings, growth and discount rates, but rather

about ‘predicting’ what others expect of them: it’s all about ‘predicting’ market psychology.

in this case investment becomes speculation, and the short term cannot be predicted.

Noise dominates the short termthe latter becomes clear if we analyse time series of financial assets over different horizons.

smith (1924) and siegel (1998) demonstrated many years ago that investors require a great

deal of patience. in the long term, equities outperform bonds and there is a lower risk of a

negative return. You can depict this graphically using moving average yields as shown in

figure 1.Yet there is more. the longer the investment horizon, the more ‘normal’ the distribu-

tion of the returns. in the short term, noise has the upper hand and predictions are difficult.

the opposite applies to the long term.

* this article is a highly-abridged version of ‘beyond the noise – on investment theory, towards long-term asset management’, the inaugural speech given by roelof salomons on 14 June 2016 on acceptance of the professorship of investment theory and asset management.

read the unabridged inaugural lecture on www.kempen.nl

11Kempen insight, July 2016

Kempen Insight, July 201612

Figure 1Moving average yields

-100

-50

0

50

100%

1872 1892 1912 1932 1952 1972 1992 2012-10

-5

0

5

10

15

20%

1881 1901 1621 1941 1961 1981 2001 2011

the top graphs show the real total returns (adjusted for inflation and includingdividends) on equities over 1-year and 10-year periods. the data periodis 1871 – 2015.the monthly data for the s&p500 index, a market capitalisation equity index,come from shiller and standard & poor’s.the bond market data are from global Financial data and bloomberg.

sources: shiller and standard & poor’s

Kempen Insight, July 2016 13

0

10

20

30

50

40

1872 1892 1912 1932 1952 1972 1992 2012

Predicting returns over the last two decades it has become clear that returns can be predicted to a certain extent based on valuation

criteria. campbell and nobel prize winner shiller (1998, 2001) were the first to demonstrate this. in my own doctoral

thesis (salomons, 2005 - ed.), i show that the value - ranking prices based on underlying fundamental indicators such

as earnings (Figure 2) - at the time of purchase is a sound indicator of future returns.

the predictability derives from the ‘reversion to trend’ in the valuation variables. if p/e ratios revert to trend, this may

be due to changes to the price, the earnings or a combination of the two. this is worth remembering. as a lecturer

this is when i say to my students: “i would make a note of this.”

high valuations go hand-in-hand with low expected returns and vice versa. there is predictive value in the long term.

there is no relationship in the short term between current valuations and future earnings or future returns. in the

short term there is noise. Yet this relationship does exist in the long term, but only for future returns. Valuations tell us

nothing about future earnings. p/e ratios revert to trend, but it is the prices that prompt that reversion to trend. so if

as an investor you cherish the hope that although current valuations are on the high side this means that earnings

will grow more quickly in future, i’m afraid you are hoping in vain. Figure 3 demonstrates this.

Improved investment within marketsa long-term investment horizon therefore helps us to predict the returns on a market index. it is also beneficial to

seeking returns within asset classes, in the cross-section. i will quickly lead you through the literature on the subject.

the capital asset pricing model (capm) was created in the 1960s. in it a single factor, the beta of the equity, or the

correlation between the equity and the general equity index, determines the risk and expected return. by the time i

graduated in the late 1990s, two additional factors were generally accepted. nobel prize winner Fama and French

(1993) described how small companies (size, measured by market capitalisation, small minus big or smb) and cheap

companies (value, measured as book-to-market value, high minus low or hml) also explain the cross-section of

returns. the momentum (momentum, measured as the difference between returns over the past year, winners minus

losers or Wml) effect of Jegadeesh and titman (1993) and carhart (1997) was added later.

Figure 2price/earnings (p/E) ratio

the graph depicts the cape (cyclically-adjusted price earnings) for the s&p500. here, prices are divided by the reported earnings over the past ten years, filtering out the effect of the economic cycle on the valuations. the data period is 1881 – 2015. the monthly data for the s&p500 index, a market capitalisation equity index.

source: shiller

Kempen Insight, July 201614

these are the factors about which there is a general consensus. the academic and financial worlds have not stood

still since then. in a recent article, harvey, liu and Zhu (2015) discuss the more than 300 different factors that have

since been tested and are supposed to lead to improved investment results. Yet the statistical relevance of a positive

result needs to be viewed with some scepticism, especially if several strategies are tested simultaneously.

in Figure 1 you saw that investors in equities need a great deal of patience. the same applies to the underlying

factors in the equity market. there are long periods in which factors do not work. time is a restrictive factor.

Predictable additional returnsby introducing the correct long-term exposure within their portfolios, investors can therefore earn a higher than

average return. Yet, as is the case with equity risk premiums, these premiums are not stable. this immediately begs

the question of whether it is possible to predict these premiums. in my humble opinion, the answer is: yes, although

research into this is still in its infancy.

the top graphs show the relationship between the cape (cyclically-adjusted price earnings) on the x-axis and the correspond-ing 1-year and 10-year real total return (adjusted for inflation and including dividends) on the y-axis.

the bottom graphs depict the relationship between the cape and the corre-sponding 1-year and 10-year earnings growth.

the data period is 1881 – 2015.

Figure 3Relationship between current valuations and future returns

sources: shiller and standard & poor’s

-100

-50

0

50

100%

0 5 10 15 20 25 30 35 40 45 50

-100

-50

0

50

100%

0 5 10 15 20 25 30 35 40 45 50

-20

-10

0

10

20%

0 5 10 15 20 25 30 35 40 45 50

-20

-10

0

10

20%

0 5 10 15 20 25 30 35 40 45 50

Kempen Insight, July 2016 15

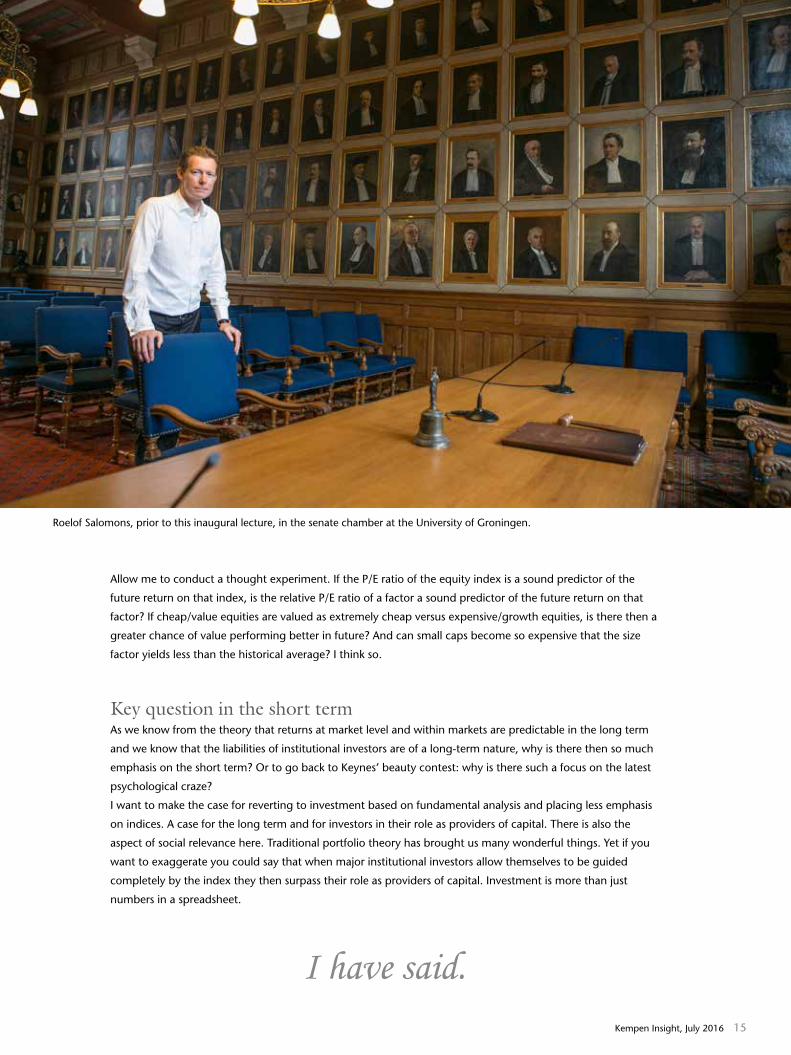

allow me to conduct a thought experiment. if the p/e ratio of the equity index is a sound predictor of the

future return on that index, is the relative p/e ratio of a factor a sound predictor of the future return on that

factor? if cheap/value equities are valued as extremely cheap versus expensive/growth equities, is there then a

greater chance of value performing better in future? and can small caps become so expensive that the size

factor yields less than the historical average? i think so.

Key question in the short termas we know from the theory that returns at market level and within markets are predictable in the long term

and we know that the liabilities of institutional investors are of a long-term nature, why is there then so much

emphasis on the short term? or to go back to Keynes’ beauty contest: why is there such a focus on the latest

psychological craze?

i want to make the case for reverting to investment based on fundamental analysis and placing less emphasis

on indices. a case for the long term and for investors in their role as providers of capital. there is also the

aspect of social relevance here. traditional portfolio theory has brought us many wonderful things. Yet if you

want to exaggerate you could say that when major institutional investors allow themselves to be guided

completely by the index they then surpass their role as providers of capital. investment is more than just

numbers in a spreadsheet.

I have said.

roelof salomons, prior to this inaugural lecture, in the senate chamber at the university of groningen.

Kempen Insight, July 201616

If the price is rightJohan Cras is ideally placed to discuss the strengths of the UK and Dutch ‘cultures’ in his position as Managing Director of Kempen’s London based business given his experience working in both financial markets. In this Q&A, he offers his perspectives on why cost transparency – an important and specific focus of Dutch funds – should matter to the UK.

Johan cras on cost transparency

Johan Cras stresses the importance of cost transparency during an interview with PMI-tv.

Kempen Insight, July 2016 17

/// by lesa sawahata photo PMI/tv

what In your oPInIon are the bIg dIfferenCes

between uK and dutCh PensIon funds?

‘what I like about working in the uK pension market is this

notion that people invest with ambition. It’s the ambition to

effectively give a pension to members which is geared towards

a real income rather than a nominal income - and the diffe-

rence between the two is the inflation rate. and although infla-

tion is very low at the moment, we do believe that in the longer

term it has an enormous impact on what people can actually

spend their pension on. the longer term focus on investments

provides greater opportunities to realise a

pension with real value. uK pension

schemes are much more focused on provi-

ding that real income than dutch pension

schemes. so that would be a plus for the

uK.’

and In the netherlands?

‘In the netherlands, people are more

geared towards answering the question

‘how’- how we do things rather than a single sided focus on

what the outcome is. Investment is a profession which is pretty

difficult in terms of garanteeing outcomes, and so in the

netherlands we’ve gotten used to defining prudency as process

rather than just outcome. from my point of view we would

encourage uK schemes to spend a bit more time on finding out

how things are being done rather than just focusing on the

outcome.

another thing where I think dutch funds have really progressed

is this cost transparency issue. a lot of effort is being made by

the industry to make sure that people understand what costs

are being paid to whom, and with what ambition in mind.’

so why Is Cost transParenCy relevant?

‘ultimately it’s about good value for money. are we paying a

‘fair’ amount of money given the return ambitions that we have

as a scheme?

so the first element is to understand whether what you’re

paying is a fair price. this is not a game about ‘the good, the

bad and the ugly’ – this is about whether you’re paying the

right price, given your investment ambitions.

the second element is that every pensioner pays premiums for

his pension, and I think there’s a fiduciary duty - not only for

the providers but also for the trustees - to

understand what specific amount of money,

given those premiums, is paid to the different

providers. once you understand what’s being

provided you can also start to judge whether

what you’re paying is the right price for the

service provided and potentially make some

adjustments there. It seems prudent that the

ultimate owners of the assets - the members,

and the trustees on their behalf - know who,

how and where money being is made from these assets. this is

one of the few industries where customers are not allowed to

know what the price of their services is.’

what should the uK be doIng to start organIsIng

Itself for greater Cost transParenCy?

‘first start with raising the question; make sure that every time

you meet with the provider you raise the question about fees.

and then the second stage is to ensure that you understand

what you hear back - and if you don’t, raise the next question.

the final question should be ‘Can you confirm that there are no

other costs involved? that there are no costs or fees being

charged against these assets?

‘We feel very strongly about transparency’

in raising questions you make it clear to the provider that this is

an issue which is important and on your agenda; that you truly

want to understand what’s happening, who’s earning what for

what purpose and what the benefit might be. as mentioned

earlier it’s not about the good, the bad or the ugly, it’s under-

standing whether given your investment ambitions, you pay the

right price for the services you’re getting.’

is there practical guidance You proVide to

pension schemes to address this challenge?

‘at Kempen we have developed a document that we refer to as

a ‘heath check’, a document that trustees find very useful. the

objectives of the ‘health check’ is to draw out key points of

note – looking at all services provided and both the implicit and

explicit costs/charges, then to present what these findings mean

for the pension scheme and suggest areas for improvement.

the benefits of this approach is that the scheme, in a timely

way, gains insight in their current approach to investments, it

enhances their understanding of what’s being paid for thus

improving transparency, they will see their costs being

compared to the existing investment strategy and compared to

alternatives, putting them in a better position to evaluate and in

some cases rethink their strategy or the fees paid.’

anY Further adVice about hoW to get beYond the

current challenges around cost transparencY?

‘there’s relatively little availability of cost transparency informa-

tion at the moment, and we would urge everybody – together

- to raise questions around that.

one of the things we would encourage uK plans to do is to take

this on in collaboration with each other; form a group of people

who together will start raising those questions as an industry,

rather than as an individual scheme. We would certainly support

an initiative from uK schemes to collaborate on cost transpa-

rency. We feel very strongly about transparency.’

Kempen Insight, July 201618

pensionsmanagementinstitute

the pensions management

institute (pmi) is the uK’s largest

and most recognisable professional

body for employee benefit and

retirement savings professionals,

supporting over 6,500 members.

pmi have partnered with firms in

sectors relevant for the industry to

provide knowledge and thought

leadership in their respective areas.

Kempen is the pmi expert partner

in the area of Fiduciary manage-

ment. pmi recently interviewed

Johan cras, managing director at

Kempen, to discuss the main chal-

lenges for uK pension schemes,

preparing the uK for cost transpar-

ency and the future of fiduciary

management.

www.pensions-pmi.org.uk

Kempen Insight, July 2016 19

Banks as the Achilles heel of the economy

a former governor of the bank of

england who chooses the title ‘the end

of alchemy’ for his book on money, the

role of the banking system and how

our economic future depends on these

is guaranteed to capture our attention. don’t expect any

memoirs: this is an experienced expert’s reflections on the

financial system. on the basis of long-term economic trends,

King concludes that banks are not fulfilling their role of drivers

of economic growth. banks earn money by creating money

through the confidence placed in them: alchemy. Yet this acti-

vity makes banks the achilles heel of our economy at times of

crisis. as a result, capitalism experiences frequent and long

periods of economic stagnation. central banks can steer the

economy less well than they think at such times. Just look at the

persisting moderate economic growth since 2008, in spite of

large-scale, global quantitative easing. We need a new vision for

the role of banks. like other policymakers, King also points to

measures that allot a central role to maintaining confidence in

the banking system. For commercial banks, that may well be

more important than being an alchemist.

Title: The end of AlchemyAuthor: Mervyn KingPublisher: W.W. Norton & Company

ISBN: 978-0-393-24702-2

The excessive power of short-term investors

how is it possible that a deliberate stra-

tegy to increase shareholder value over

the past few decades has gone hand-in-

hand with lower economic growth rates

in the Western world? masouros demon-

strates that changes to corporate law

aimed at encouraging the free movement

of capital have simultaneously – and partly

unintentionally – increased the power base

of investors with a short-term focus. this book posits a post-Key-

nesian theory: these investors are ensuring that these companies

have less capital available for investment, which is in turn affec-

ting future growth. masouros illustrates his theory using several

case studies and international comparisons.

amendments to corporate law that give greater weight to long-

term interests could play a role in achieving economic growth.

take situations involving weighing up stakeholders interests to the

disadvantage of shareholders, or moving away from the principle

of equality between shareholders. after all, the interests of short-

term investors differ from those of loyal long-term investors.

Title: Corporate law and economic stagnationAuthor: Pavlos E, MasourosPublisher: Eleven International PublishingISBN: 978 – 94-90947-8

booKsto inspire

Evert Waterlander is Director Client Solutions at Kempen Capital Management. He selects for Kempen Insight books on [email protected]

19

A behind-the-scenes look at pensions

this is the fourth book by canadian

pension guru Keith ambachtsheer in

barely twenty years. this time he

reviews trends in the pension sector in

different countries since 2008. the

book provides evidence of the high

dynamics in this sector and of the tough challenge of maintai-

ning an affordable and reliable pension system. For pension

industry leaders, the trick is to apply an integrated strategy to

the pension system, the governance model and their invest-

ment convictions. ambachtsheer discusses several aspects of

each of these areas. sometimes using academic research, some-

times by taking a look behind the scenes at a prestigious

pension fund. each chapter closes with practical and feasible

policy options which often merit classification as best practices.

Title: The Future of Pension ManagementAuthor: Keith P AmbachtsheerPublisher: WileyISBN: 978-1-119-19103-2

Kempen insight, July 2016

/// by Jos leiJen visual henriKe beuKema

20

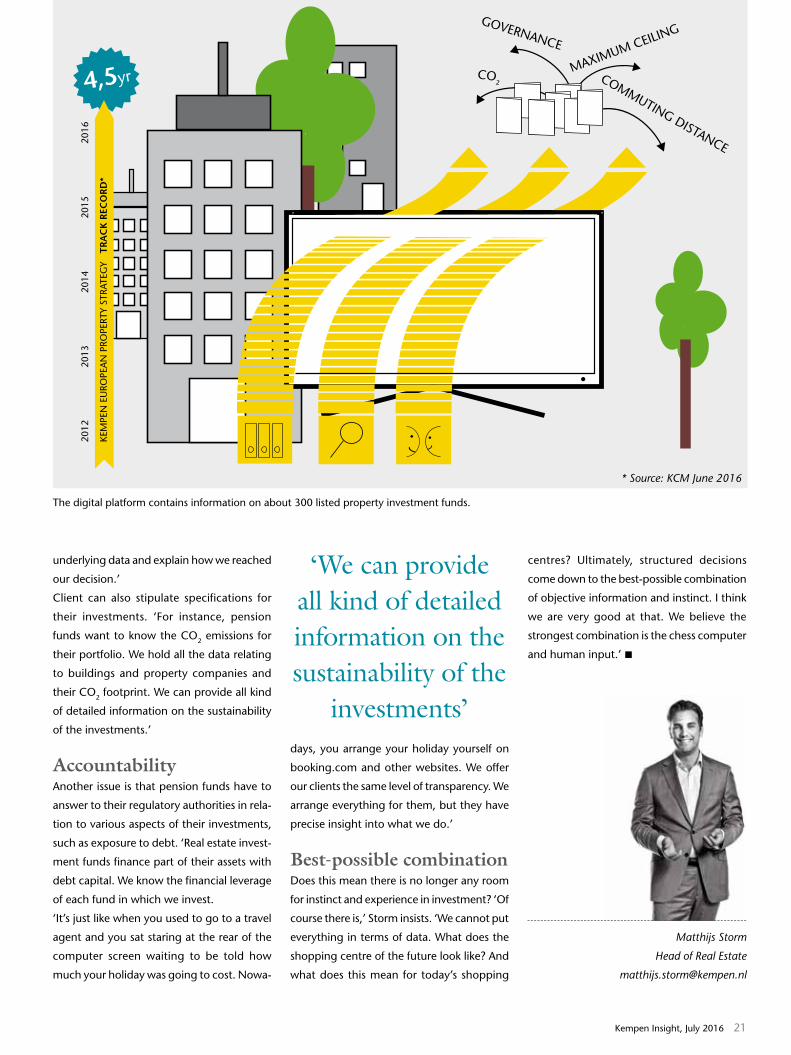

‘there are several different methods for

deciding which property funds to invest in,’

head of real estate matthijs storm explains.

‘You can allow yourself to be guided by

macro market data, or you can examine the

underlying information on the property

investment funds and their properties. We

apply the latter method, bottom-up.’

Kempen capital management real estate has

developed a digital platform containing

information on about 300 listed property

investment funds in which it can potentially

invest. the data are derived from various

sources, such as information provided by the

companies themselves, Kempens own

research and information purchased from

specialist providers.

Chess computerour proprietary data infrastructure processes

the information and supports the deci-

sion-making. ‘You can compare it to a chess

computer,’ storm says. ‘it is important that

it is properly programmed. With the help of

the team we worked out different scenarios

and inputted these into the platform. this is

how we achieve data-based property invest-

ment, as rationally as possible.’

apart from the platform itself, the information

it contains also needs to be reliable. ‘We have

selected our sources with great care. From

time to time we test their reliability, for instance

by personally visiting a shopping centre that

our source tells us has high-quality tenants.

this allows us to obtain an accurate picture.’

Identifying undervalued fundsthe bottom-up strategy applied by storm

and his team also enables them to identify

undervalued investment funds. ‘there are

different types of investors in the real estate

market, which results in inefficiencies. We

assess the ratio with respect to the price and

quality of the real estate. For example, we

examine the debt position and rental income.

this is how we decide whether or not to

select a property investment fund.’

this strategy yields benefits for Kempen & co

clients. to start with, there is the sound return

(January 2012 – april 2016, compared to the

Ftse epra nareit deVeloped europe

indeX). ‘We have applied our strategy for

four and a half years now, the past eighteen

months as a global strategy,’ storm continues.

‘each year we have succeeded in earning an

above-average return. on average, the return

is 200 basis points higher than the bench-

mark.’ (the value of your investment may

fluctuate. past performance provides no

guarantee for the future.)

Transparencyanother benefit is that Kempen & co can

very easily explain the reasons behind invest-

ment decisions. ‘the real estate market is by

its very nature highly opaque. We provide

complete transparency about what we do

and why we do it. We can show clients the

See through real estateKempen Capital Management has a unique system for determining the value and quality of property companies. This enables the Real Estate team to take well-founded investment decisions. Clients consequently obtain greater insight into their investments.

the digital platform contains information on about 300 listed property investment funds.

/// tekst XXXXX XXXXX foto XXX XXXXXXXXXXX

Kempen Insight, July 2016 21

underlying data and explain how we reached

our decision.’

client can also stipulate specifications for

their investments. ‘For instance, pension

funds want to know the co2 emissions for

their portfolio. We hold all the data relating

to buildings and property companies and

their co2 footprint. We can provide all kind

of detailed information on the sustainability

of the investments.’

Accountabilityanother issue is that pension funds have to

answer to their regulatory authorities in rela-

tion to various aspects of their investments,

such as exposure to debt. ‘real estate invest-

ment funds finance part of their assets with

debt capital. We know the financial leverage

of each fund in which we invest.

‘it’s just like when you used to go to a travel

agent and you sat staring at the rear of the

computer screen waiting to be told how

much your holiday was going to cost. nowa-

days, you arrange your holiday yourself on

booking.com and other websites. We offer

our clients the same level of transparency. We

arrange everything for them, but they have

precise insight into what we do.’

Best-possible combinationdoes this mean there is no longer any room

for instinct and experience in investment? ‘of

course there is,’ storm insists. ‘We cannot put

everything in terms of data. What does the

shopping centre of the future look like? and

what does this mean for today’s shopping

centres? ultimately, structured decisions

come down to the best-possible combination

of objective information and instinct. i think

we are very good at that. We believe the

strongest combination is the chess computer

and human input.’

Matthijs Storm

Head of Real Estate

4,5yrKE

MPE

N E

URO

PEA

N P

ROPE

RTY

STRA

TEG

Y T

RA

CK

REC

OR

D*

2012

201

3

20

14

2

015

2016

* Source: KCM June 2016

CO2 COMMUTING DISTANCE

MAXIMUM CEILINGGOVERNANCE

‘We can provide all kind of detailed information on the sustainability of the

investments’

Kempen Insight, July 201622

Valuations form the basis for investment

decisions taken by investors with a long-

term outlook. With valuations above-average levels for several years now,

investment strategist Marius Bakker argues in favour of selective

risk-taking.

For some time now, financial market valua-

tions have been significantly higher than

the long-term (10 years or more) average

across virtually the whole investment spec-

trum. We do not view this as a stable situa-

tion in the long term and anticipate that

valuations will be lower. during this period,

we are being cautious about taking risk and

believe capital retention to be at least as

important as the return on capital.

Yields are at historically low levels thanks to

the repeated intervention of central banks.

an increasingly large portion of the

outstanding sovereign debt offers no yield

at all, and sometimes even a negative one.

this has driven investors towards riskier

investment classes, such as equities and

credits, blowing valuations up even further.

credit spreads are the most obvious

example from the past few months. the

ecb’s latest package of stimulatory meas-

ures – they are now also buying corporate

bonds - has placed further pressure on

credit spreads in the european market.

hence lending to large corporations is not

rewarded in terms of risk. in our opinion,

investors are no longer sufficiently compen-

sated for the higher credit risk compared to

government bonds.

Emerging markets We see selective opportunities for the

equity markets, chiefly at regional level.

after a volatile first quarter, the stock-

market has calmed down again some-

what. While sentiment was recovering,

however, prices once again started to rise.

although valuations became slightly more

attractive during the turbulent start to the

year, we are seeing them increase again

now that the market is calming down

again.

For some time now, we have been selective

about risk-taking in those markets in which

the reward for this is marginal. moreover,

our fundamentals that form the basis for

our expected returns deteriorated in the

first quarter of 2016. corporate results and

margins are being squeezed in all the major

economies. on the other hand, we have

seen yields fall further, especially in the

eurozone. We believe that premiums on

european equities still offer sufficient

compensation for the higher risk compared

to government bonds. emerging market

equities are the most attractive option in

the equity universe with respect to valua-

tion, but at the same time they are the risk-

iest. in spite of this, in the wake of years of

Volatility on the horizon

Kempen Insight, July 2016 23

%

10

8

6

4

2

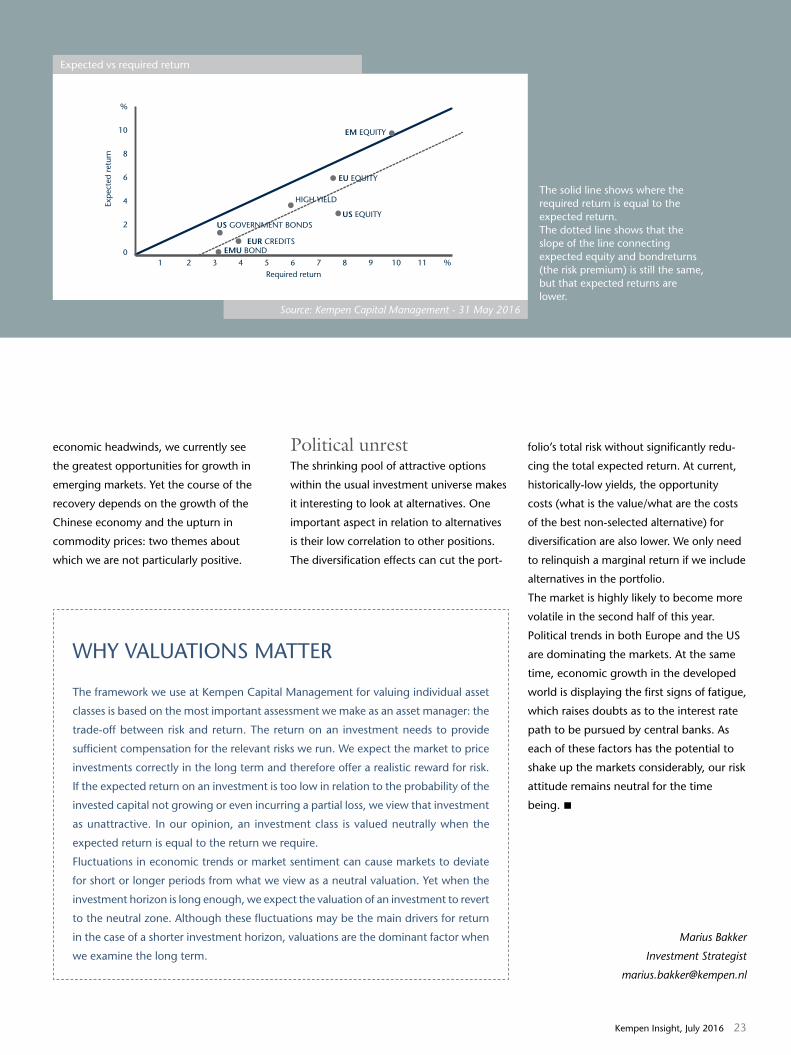

021 3 4 5 6 7 8 9 10 11 %

Exp

ecte

d re

turn

Required return

EMU BONDEUR CREDITS

US GOVERNMENT BONDSUS EQUITY

HIGH YIELD

EU EQUITY

EM EQUITY

economic headwinds, we currently see

the greatest opportunities for growth in

emerging markets. Yet the course of the

recovery depends on the growth of the

chinese economy and the upturn in

commodity prices: two themes about

which we are not particularly positive.

Political unrestthe shrinking pool of attractive options

within the usual investment universe makes

it interesting to look at alternatives. one

important aspect in relation to alternatives

is their low correlation to other positions.

the diversification effects can cut the port-

folio’s total risk without significantly redu-

cing the total expected return. at current,

historically-low yields, the opportunity

costs (what is the value/what are the costs

of the best non-selected alternative) for

diversification are also lower. We only need

to relinquish a marginal return if we include

alternatives in the portfolio.

the market is highly likely to become more

volatile in the second half of this year.

political trends in both europe and the us

are dominating the markets. at the same

time, economic growth in the developed

world is displaying the first signs of fatigue,

which raises doubts as to the interest rate

path to be pursued by central banks. as

each of these factors has the potential to

shake up the markets considerably, our risk

attitude remains neutral for the time

being.

Marius Bakker

Investment Strategist

expected vs required return

Source: Kempen Capital Management - 31 May 2016

the solid line shows where the required return is equal to the expected return. the dotted line shows that the slope of the line connecting expected equity and bondreturns (the risk premium) is still the same, but that expected returns are lower.

WhY Valuations matter

the framework we use at Kempen capital management for valuing individual asset

classes is based on the most important assessment we make as an asset manager: the

trade-off between risk and return. the return on an investment needs to provide

sufficient compensation for the relevant risks we run. We expect the market to price

investments correctly in the long term and therefore offer a realistic reward for risk.

if the expected return on an investment is too low in relation to the probability of the

invested capital not growing or even incurring a partial loss, we view that investment

as unattractive. in our opinion, an investment class is valued neutrally when the

expected return is equal to the return we require.

Fluctuations in economic trends or market sentiment can cause markets to deviate

for short or longer periods from what we view as a neutral valuation. Yet when the

investment horizon is long enough, we expect the valuation of an investment to revert

to the neutral zone. although these fluctuations may be the main drivers for return

in the case of a shorter investment horizon, valuations are the dominant factor when

we examine the long term.

24 Kempen insight, July 2016

Kempen Insight, July 2016 25

/// visual philip Jenster

US spectacle with repercussions

summer is usually the silly season for

news. Yet this summer proves to be

anything but dull. We have the us

political spectacle to entertain us.

donald trump and hillary clinton are

expected to battle it out for the key to

the White house on 8 november.

trump is like a bull in a china shop. he

couldn’t care less about the unwritten

rules of conducting a campaign,

adopts politically incorrect stances

and is not afraid to pick a fight with

everything and everyone. in doing so,

against the expectations of the elite,

he knows that he appeals to a section

of us society. he is harnessing the

anger and frustration felt by part of

the population and convincing them

that someone is finally listening to

them, whereas they often feel the

ruling elite fails to take them seriously.

this is an issue that has long been a

problem in europe.

this is an indication that the populism

in the us will not simply go away.

even if trump fails to win the us presi-

dential elections (as we currently

assume), the phenomenon is here to

stay as it is has deeper economic

causes. over the past decade, income

inequality in the us has increased

further. the average household

income has fallen, partly due to job

losses in industry. these job losses can

in turn partly be attributed to us

trade policy, for example with china.

it is no coincidence that trump

strongly opposes free trade agree-

ments. the changing political climate

has also prompted clinton to reverse

her support for the trans-pacific part-

nership. greater protectionism, which

cannot be ruled out under either

trump or clinton, is bad news for

multinationals that rely on internati-

onal trade.

Yet the us presidential elections not

only have a high entertainment factor,

they are also important from an invest-

ment perspective. What will the political

manifestos look like? this, and therefore

the impact on individual asset classes,

should become clear over the coming

months. one thing is certain: it will be a

politically hot summer on the other side

of the atlantic.

Ruth van de Belt

Investment Strategist