key features of ifrs 17

TRANSCRIPT

willistowerswatson.com

IFRS 17 Insurance Contracts: the countdown to 2021 has begun!

May 2017

© 2017 Willis Towers Watson. All rights reserved.

willistowerswatson.com

IFRS 17 Insurance Contracts: the countdown to 2021 has begun!

2© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

On 18 May 2017, the International Accounting Standards

Board (IASB) published IFRS 17 Insurance Contracts,

twenty years after the IASB’s predecessor initiated the

insurance contracts project. The new standard, which will

replace IFRS 4 for accounting periods beginning on or after

1 January 2021, is a major milestone for the insurance

industry as it represents the first ever near global

accounting standard for insurance contracts.

The standard sets out a comprehensive methodology

applicable to all insurance and reinsurance contracts, both

long- and short-term, as well as investment contracts with

discretionary participation features. IFRS 17 represents a

major departure from current insurance accounting

practices in many jurisdictions, which will fundamentally

change both how and what insurance companies report to

shareholders, policyholders and other stakeholders.

This is more than “just” an accounting change: IFRS 17 will

have a wide and significant impact on insurers’ operations

and implementation will be a major challenge.

willistowerswatson.com

Key features of IFRS 17

3© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

The main feature of IFRS 17 is the building block approach,

or General Measurement Model, for the insurance

contract liability that includes (1) discounted cash flows, (2)

a risk adjustment to reflect the uncertainty in the cash flows

and (3) a contractual service margin to eliminate any gain at

issue.

The Insurance Contract Liability will consist of a fulfilment

cash flow element and an unearned profit element (the

Contractual Service Margin, or CSM, which cannot be

negative). The value of the fulfilment cash flows will be a

current amount at any point in time, reflecting economic

conditions at and expectations of future experience from the

time of the valuation.

A simplified measurement, the Premium-Allocation

Approach, is permitted for short-duration pre-claims

liabilities and is similar to existing unearned premium

approaches (i.e. using the premium less acquisition costs

as the liability on day one, subject to an onerous contracts

test, then running it off simply over time). This provides a

simpler alternative for many A&H and P&C contracts and

some Life contracts.

Cash flows

Time value of

money

Risk adjustment

Contractual service

margin

Total

Insurance

Contract

Liability Fulfilment cash flows:

Component

representing the risk-

adjusted present value

of future cash flows

needed to fulfil the

contract

Component representing

unearned profit the

insurer expects to earn

as it fulfils the contract

IFRS 17 – The General Measurement Model

willistowerswatson.com

Key Features of IFRS 17 (continued)

4© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

A Variable Fee Approach will be applicable to contracts with

direct participation features. The Variable Fee Approach

has the same components as the General Measurement

Model.

The difference is that the CSM can be adjusted in response

to variations in underlying items, most particularly

investment returns, such that investment return and other

relevant variations will not immediately affect profit or loss.

This will be applicable to a range of product types, including

UK style participating contracts and investment

linked/variable life insurance and annuities.

CSM

T=0

Present

Value of

Cash

Outflows

Assets

Risk

adjustment

T=1

Present

Value of

Cash

Outflows

Risk

adjustment

CSM

Initial

measurement

CSM/

Variable

Fee

Subsequent

measurement

Example: CSM responds to movement in asset values,

aligning the insurance contract liability with the value of

assets underlying the participation feature.

Con

trib

ution

willistowerswatson.com

Key considerations for both life and general insurers

Issue Why is it an issue?

Disclosure There will be new line items for the income statement presentation and reconciliations which

will take time to get used to, and also significant additional disclosure requirements,

particularly to cover areas of significant judgement and the nature and extent of risk.

Difference to approaches

for other purposes, such

as capital requirements

Differences between IFRS 17 and approaches which are applied concurrently for other

purposes, such as the determination of capital requirements under Solvency II and other

regimes, are likely. For example, which contracts and which cash flows are to be included.

Reinsurance There are potential differences in measurement approach between primary insurance and

reinsurance, including that any net cost or net gain on origination of reinsurance contracts

held is to be recognised as a CSM and the Variable Fee Approach may not be applied.

Discount rates Discount rates are not prescribed, and either bottom-up or top-down approaches may be

utilised. The extent to which the illiquidity of cash flows should be reflected in discount rates

requires consideration.

Risk adjustment Unlike the specified risk margin of Solvency II, for example, IFRS 17 is principles-based,

allowing companies to set their own approach to determine the risk adjustment allowing for

management’s views on the compensation required for bearing risk.

Interaction with IFRS 9 How the insurance contract liability interacts with asset measurement will be key to

understanding and managing volatility of profits.

5© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

Key considerations primarily for life insurers

Issue Why is it an issue?

Contractual Service

Margin

The CSM can significantly change the recognition of accounting profit:

Consistent with other industries there will be no day 1 profit from the writing of a new

contract.

The impact of changes in demographic and expense assumptions will be spread over

the lifetime of the contracts rather than posted immediately to profit in the income

statement.

Transition There will be a one-time transition exercise to the new standard, notably to determine the

CSM applicable to existing business as at 1 January 2020 (as at least one year of

comparatives is required).

The default position is for full retrospective application to determine what the CSM would

have been at the start and end of 2020 as if IFRS 17 had always applied, with simplified

approaches available if full retrospective application is impracticable.

Options and guarantees Incorporating allowance for any options and guarantees in the valuation of the fulfilment cash

flows will potentially require more complex stochastic models relative to those currently in

use.

Participating business The Variable Fee Approach should allow investment and other gains and losses to be

recognised over time through the CSM. The key considerations for any insurer will be to what

extent and how the Variable Fee Approach can be applied.

Investment components Reported insurance contract revenue is to exclude any investment component of the

premium.

6© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

Key considerations primarily for general insurers

Issue Why is it an issue?

Applying the General

Measurement Model

If companies are not able to apply the Premium Allocation Approach for all their business,

then the General Measurement Model and all its complexity will apply.

Liability for incurred claims Liabilities for incurred claims must reflect a fulfilment cash flow measure, as per the General

Measurement Model, including a risk adjustment.

Onerous contract liability Where a portfolio of contracts is potentially onerous, companies will need to evaluate the

value of the fulfilment cash as per the General Measurement Model, and immediately

recognise a loss to the extent the portfolio is onerous.

7© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

It is now time for action

8© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Many insurers that are or are going to be subject IFRS accounting will already be somewhere along the road to adopting

IFRS 17, some further than others. Now that the final standard is available, it is more imperative than ever to start

activities to implement IFRS 17:

likely business and reporting impacts. This helps to narrow down the implementation options into a clearly defined

accounting policy – with the benefit of fewer surprises for all post implementation.

Assess information and I.T. systems impact, gaps and solutions

Starting from your current insurance contracts project status and using your existing

actuarial IT reporting landscape, we will guide you through IFRS 17 system

requirements. Throughout the project we will partner with your actuarial, IT, and

reporting experts, to develop an initial, high-level blue print, with planning and budget

estimates for the full IFRS 17 project.

Analyse the business impact

IFRS 17 is principles-based and as such comes with a range of options, each with

different potential impacts on the business, as well as on the profit or loss statement.

In advance of performing large-scale implementation, companies can first assess the

After assessing the impact on your IT systems, we will work with you to identify and implement pragmatic steps to fill

any gaps identified, leveraging any Solvency II synergies we can as effectively as possible.

As the World’s largest supplier of actuarial software, we are able to offer a wide range of modular software solutions to

help in your IFRS 17 implementation

willistowerswatson.com

It is now time for action

9© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Design, implement and test IT and reporting processes

As a result of the introduction of IFRS 17, there will be a significant change for

insurance groups in the content and structure of data captured from business units to

support group statutory and regulatory reporting. A key challenge will be to ensure

that these different types of data are available and that systems have the flexibility to

accommodate differences between Solvency II and IFRS 17.

We are an integrated consulting and software provider, and our experts provide business advice, solutions and software.

We will work with you to help specify the actuarial IFRS 17 requirements for your specific situation. We can then design,

implement and automate your actuarial reporting processes, taking into account best practice processes, and the latest

IT and software solutions.

For many insurers, the optimisation of existing actuarial processes will already be underway. However, if you haven’t yet

started to optimise your processes, there is still time and we can help you to undertake the necessary steps. And if you

are already working towards optimising your systems, we can provide an independent view to help ensure you are on

track to deliver the right processes, with the right specifications, at the right time – and crucially that it is suitable for

IFRS 17.

Finally, as experts in software development and implementation, we have developed an implementation process and

standards guide that can be adapted to best meet our client’s needs for the IFRS implementation project. And a phased

test process for predefined test cases assures the functionality and quality of the implementation.

willistowerswatson.com

It is now time for action

10© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

Employee and management training

The processes developed to report under the new insurance accounting standard

will need to be auditable. To successfully implement and embed all the changes

required under IFRS 17 insurers will need a proper understanding and buy in

across their teams.

Monitor developments

While IFRS 17 is final, there is still possibility of further development. The IASB is

establishing a Transition Resource Group later this year that will advise the IASB on

implementation issues.

Actuarial staff need to be in a position to specify necessary cash-flow modelling changes and amendments for IFRS 17.

This requires investment of time and resources into educating and training staff and management.

Whether or not this leads to any specific changes to IFRS 17, it is likely that further clarification from and guidance will

result from this feedback process. Companies will need to be aware of and adapt their implementation for such

developments.

willistowerswatson.com

About Willis Towers Watson

Willis Towers Watson (NASDAQ: WLTW) is a leading global advisory, broking and

solutions company that helps clients around the world turn risk into a path for

growth. With roots dating to 1828, Willis Towers Watson has 40,000 employees

serving more than 140 countries. We design and deliver solutions that manage risk,

optimize benefits, cultivate talent, and expand the power of capital to protect and

strengthen institutions and individuals. Our unique perspective allows us to see the

critical intersections between talent, assets and ideas — the dynamic formula that

drives business performance. Together, we unlock potential.

Willis Towers Watson

71 High Holborn

London

WC1V 6TP

Towers Watson Limited (trading as Willis Towers Watson) is authorised and

regulated by the Financial Conduct Authority in the UK.

The information in this publication is of general interest and guidance. Action should

not be taken on the basis of any article without seeking specific advice.

To unsubscribe, email [email protected] with the publication

name as the subject and include your name, title and company address.

11

Willis Towers Watson is uniquely placed to help

both Life and P&C insurers interpret and

implement the new standard developed by the

IASB. We:

Advise more than three-quarters of the

world's leading insurers

Are the industry's leading risk specialist and

a leader in financial modelling

Are the largest provider of actuarial

software in the world

Have more actuaries and chartered

enterprise risk analysts (CERAs) serving the

insurance industry than any other professional

services company

Willis Towers Watson and IFRS17

© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

willistowerswatson.com

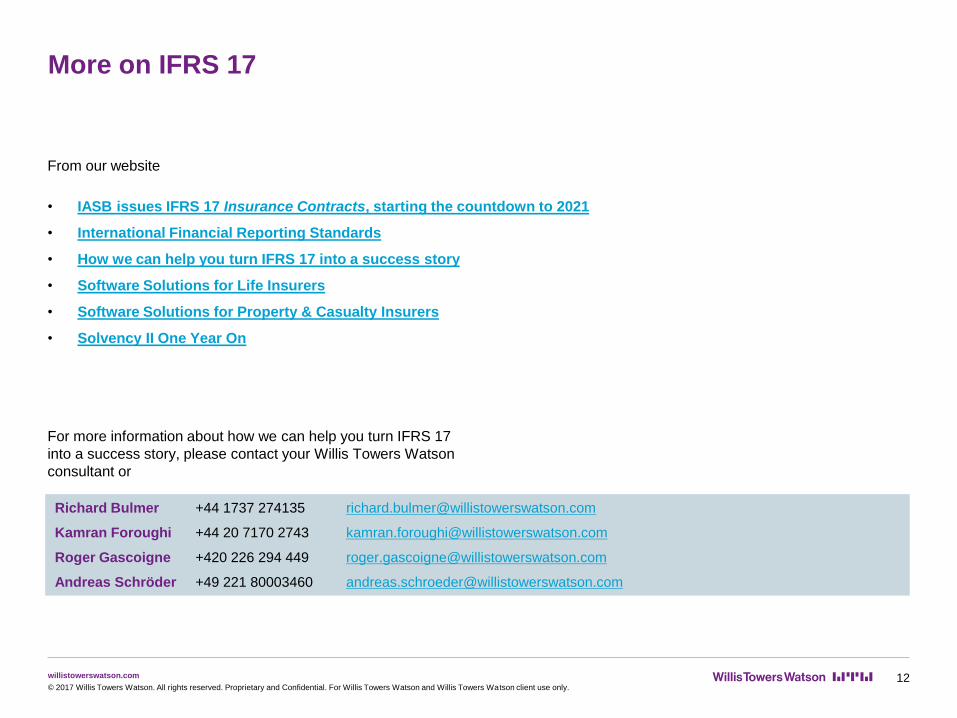

More on IFRS 17

12© 2017 Willis Towers Watson. All rights reserved. Proprietary and Confidential. For Willis Towers Watson and Willis Towers Watson client use only.

From our website

• IASB issues IFRS 17 Insurance Contracts, starting the countdown to 2021

• International Financial Reporting Standards

• How we can help you turn IFRS 17 into a success story

• Software Solutions for Life Insurers

• Software Solutions for Property & Casualty Insurers

• Solvency II One Year On

For more information about how we can help you turn IFRS 17

into a success story, please contact your Willis Towers Watson

consultant or

Richard Bulmer +44 1737 274135 [email protected]

Kamran Foroughi +44 20 7170 2743 [email protected]

Roger Gascoigne +420 226 294 449 [email protected]

Andreas Schröder +49 221 80003460 [email protected]