larisa ortiz march 2014

TRANSCRIPT

Commercial District Classification

Successful district management begins with understanding district needs

About Me

Larisa Ortiz Principal, Larisa Ortiz Associates

Lead East Coast Consultant, LISC MetroEdge

Visiting Professor, Pratt Institute

Former Director, Coro Neighborhood Leadership Program (NYC)

Editor, The Commercial District Advisor

ICSC Alliance, Public Sector Co-Chair

Experience in Commercial District Revitalization

National

New York

New Jersey

Philadelphia, PA

Pittsburgh, PA

Martinsville, VA

Jacksonville, FL

Chicago, IL

Indianapolis, IN

Kansas City, MO

Houston, TX

California

• Bay Area

• San Diego

Seattle, WA

International

Puerto Rico

El Salvador

Chile

Strategic Positioning

Market Analysis

Administrative Management

• BID • CDC

Redevelopment

• public space improvements • private redevelopment/real estate

Retail Sales

• marketing/promotion • event marketing

Tenant Mix

• retail retention/attraction

STEP 1:

DIAGNOSE

STEP 2:

BUILD CAPACITY

STEP 3:

TAKE ACTION

©Larisa Ortiz Associates

Strategic Positioning

Market Analysis

Administrative Management

Redevelopment & Retail Sales

Tenant Mix

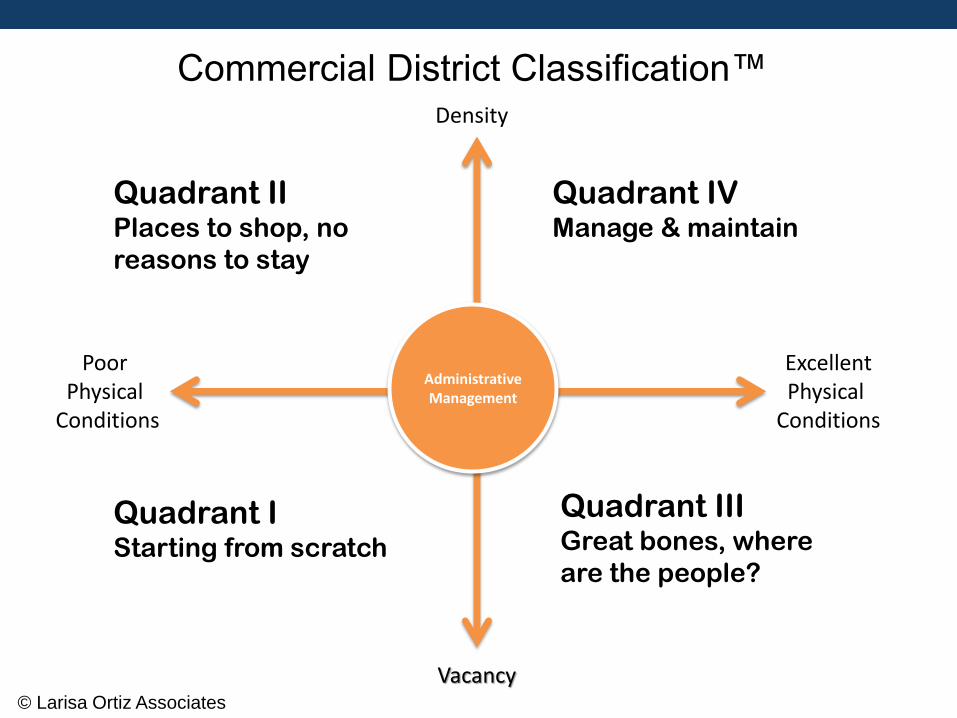

The Framework

Density

Vacancy

Poor Physical

Conditions

Administrative Management

Quadrant I Starting from scratch

Quadrant II Places to shop, no

reasons to stay

Quadrant III Great bones, where

are the people?

Quadrant IV Manage & maintain

Commercial District Classification™

© Larisa Ortiz Associates

Excellent Physical

Conditions

What do shoppers want?

Source: Verde Group/ ICSC Global Research Network,

What do shoppers want?

Source: Verde Group/ ICSC Global Research Network,

Commercial District Research

• LISC commissioned, 2009

• Funded by the William Penn Foundation

• Study Overview

– 10 year time series analysis

– 264 Commercial Corridors

– Considered the impact of various investments and corridor conditions on corridor success

What characterizes a “successful” corridor?

• Tenant Mix (offerings that reflect community needs)

• Density (retail and population)

• Physical Conditions

– Street experience (i.e. physical space/amenities)

– Access/location

What characteristics enable change?

• Leadership

• Administrative Capacity

Administrative Management

Retail Sales

Tenant Mix

Redevelopment

Clean & Safe

Tenant Mix

Redevelopment

Physical Improvements

Physical Improvements

Quadrant I: Starting from scratch

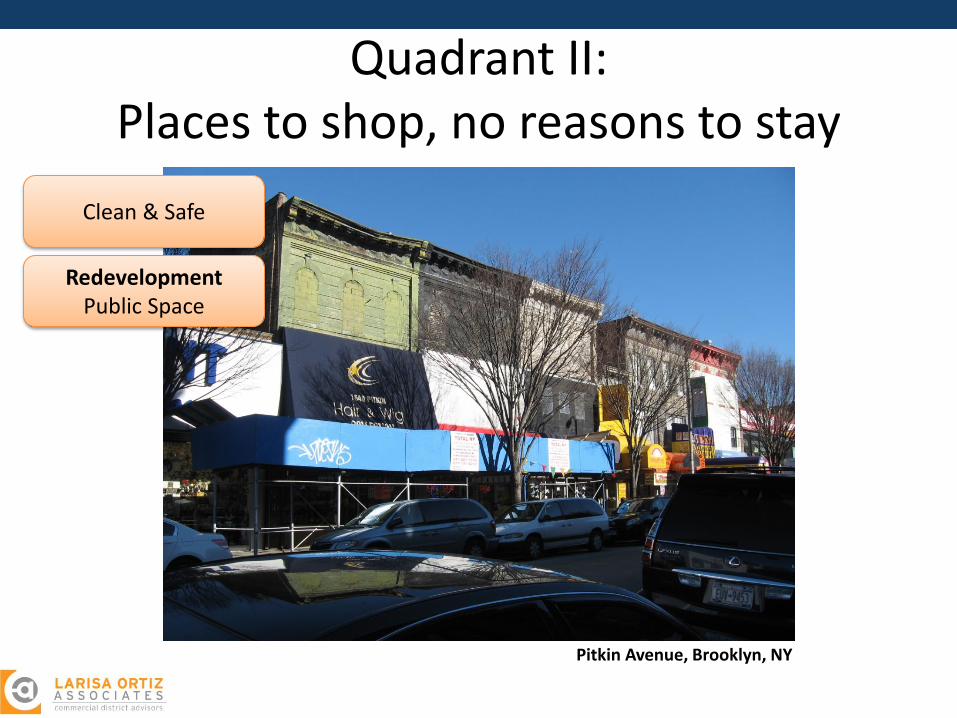

Quadrant II: Places to shop, no

reasons to stay

Quadrant III: Great bones,

where are the people?

Quadrant IV: Manage & maintain

© Larisa Ortiz Associates

Commercial District Classification™ Model Density

Vacancy

Poor Physical

Conditions

Excellent Physical

Conditions

C B A

Corridor Success: A Framework for Action

Administrative Management

TIM

E

EXP

ERTI

SE N

EED

S C

HA

NG

E

Quadrant I:

Starting from scratch

Quadrant IV:

Manage & maintain

Quadrant III:

Great bones, where

are the people?

Quadrant II:

Places to shop, no

reasons to stay

Retail Sales

Tenant Mix

Redevelopment Private Property

Redevelopment Public Space

Clean & Safe

Redevelopment Public Space

Tenant Mix

Redevelopment Private Property

Moving from Quadrant to Quadrant takes…

TIME,

RESOURCES,

ABILITY TO ADAPT, AND

ABILITY TO ACQUIRE NEW AREAS OF EXPERTISE

Quadrant I: Starting from scratch

Nicetown, Philadelphia, PA

Redevelopment Private Property

Redevelopment Public Space

Administrative Management

Quadrant II: Places to shop, no reasons to stay

Pitkin Avenue, Brooklyn, NY

Clean & Safe

Redevelopment Public Space

Quadrant III: Great bones, where are the people?

Uptown, Kingston, NY Administrative Management

Tenant Mix

Redevelopment Private Property

Quadrant IV: Manage & maintain

South Orange, NJ

Retail Sales

Tenant Mix

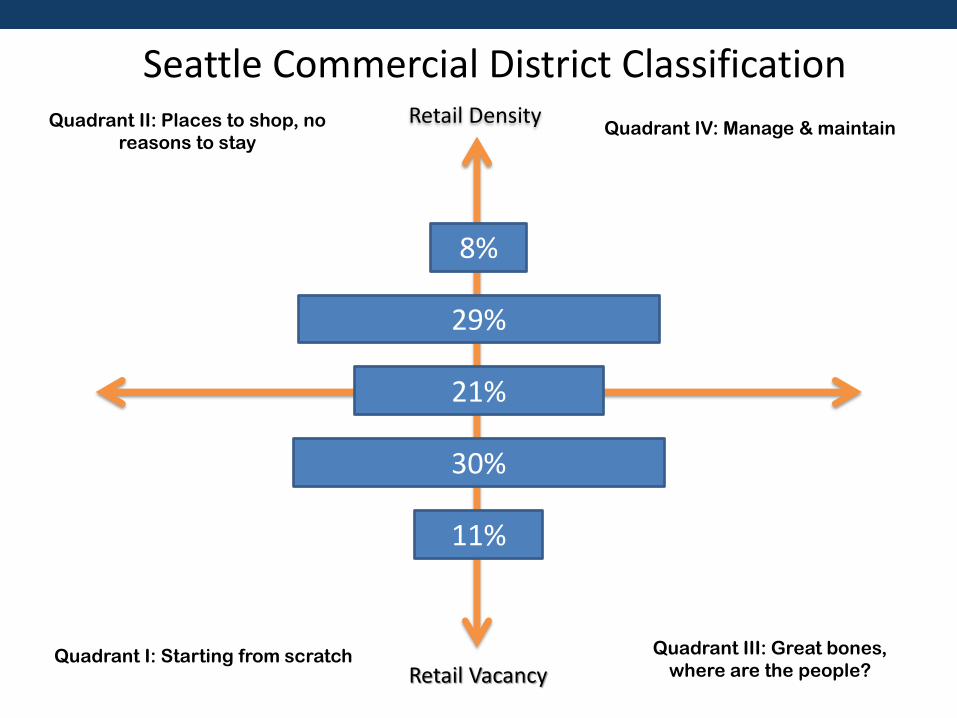

8%

21%

29%

11%

30%

Quadrant I: Starting from scratch

Quadrant II: Places to shop, no

reasons to stay

Quadrant III: Great bones,

where are the people?

Quadrant IV: Manage & maintain Retail Density

Retail Vacancy

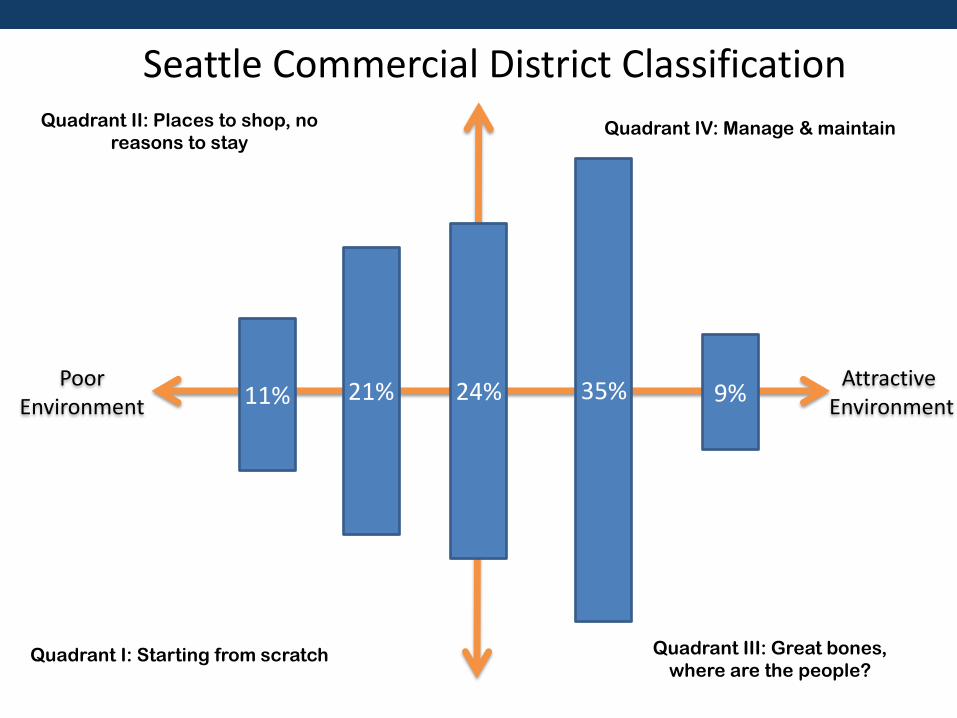

Seattle Commercial District Classification

Quadrant I: Starting from scratch

Quadrant II: Places to shop, no

reasons to stay

Quadrant III: Great bones,

where are the people?

Quadrant IV: Manage & maintain

11% 21% 24% 35% 9% Poor

Environment Attractive

Environment

Seattle Commercial District Classification

Administrative Capacity

31%

12%

58%

Strong Moderate Weak

{

{

{

Seattle Commercial District Classification

Quadrant I: Starting from scratch

Quadrant II: Places to shop, no

reasons to stay

Quadrant III: Great bones,

where are the people?

Quadrant IV: Manage & maintain

Poor Environment

Attractive Environment

High Density

Low Density

First Hill

Beacon Hill

First Hill

First Hill

Fremont West Seattle Columbia City Wallingford Ballard Georgetown Roosevelt

Montlake

Roosevelt

Uptown/Lower Queen Anne

Washington State

= Lacks Admin Capacity

Participant Outcomes

Othello/Graham/MLK Lake City Rainier Beach West Seattle International District

Pioneer Square

Beacon Hill Othello/Graham/MLK

What’s your Classification? – Breakout Discussion

Identify a “recorder” and a “reporter”

• Discuss and list three major similarities between your districts

• Discuss and list three major differences between your districts

• Discuss your most successful activities – why were they successful

• Discuss your most unsuccessful activities – why were they unsuccessful

• Are there any similarities or trends with respect to the kinds of activities that are successful or not successful

The Basics of Interpreting and Using Market Data March 11, 2014

Prepared for the City of Seattle

Office of Economic Development

Learning objectives

1.Defining Trade Area

2.Understanding your District’s “Strategic Positioning”

3.Basic Market Leakage Analysis

4.Interpreting Data and Applying Analysis

Information Foundation

60% Interpretation

40% Information

Trade Area

70%

Some thoughts on Trade Area

Primary trade area vs. secondary trade area The 1:4 ratio. Travel versus Time Expended. Districts with more shopping options typically have a

larger trade area. Why? People will travel farther for better selection and more options.

Different BUSINESSES have different trade areas. i.e Furniture versus grocery. Or destination restaurant versus local restaurant.

For a DISTRICT or SHOPPING CENTER, trade area size is typically defined by the anchor.

“Anchors” do not have to be retail stores.

Drugstore

Specialty Food Store

Department Store/Big Box Retail

Disneyworld

Convenience/Neighborhood – 5-10 min

Comparison/General – 15-30 min

Destination/Regional – 30 + min

Trade Area

International

1. Differs by retail category – but for a district it is typically defined by the anchor

2. Influenced by geography, natural and psychological boundaries

3. NOT defined by political boundaries

What is Strategic Positioning?

Trade Area Size Customer Profile Merchandise offerings Price point Lifestyle

Which best describes your commercial district?

Convenience Retail/Services – Neighborhood Center – Neighborhood Commercial District – Main Street – Necessity Retail – Convenience Retail

Comparison/General

– Main Street – Mix of Convenience and Specialty Retail

Destination Retail/Services

– Lifestyle Center – Entertainment Districts – Regional Center – Central Business District – Destination Retail

Elmora, Elizabeth, NJ

Pitkin Avenue, Brooklyn, NY

Strategic Positioning

Drugstore

Specialty Food Store

Department Store/Big Box Retail

Disneyworld

Convenience/Neighborhood – 5-10 min

Comparison/General – 15-30 min

Destination/Regional – 30 + min

What is your Trade Area?

International

Important caveats about the data you have in hand

The market data you have MAY NOT correspond with your district’s trade area. Therefore, today’s analysis MAY NOT be accurate for your district.

This is an exercise… this is only an exercise. It is not a substitute for proper market analysis.

If you need to re-pull data, you can do so for a nominal fee at Esri Business Analyst Online

There is no substitute for visiting the market.

Strategic Position defines Trade Area

11

Market Data: Secondary Sources Sources of Standard Market Data - Census

- Esri

- Claritas

Additional Market Data - Home Mortgage Disclosure Act

- New Housing Units

- Crime statistics

Esri Reports for Reference - Retail Marketplace Profile

- Demographic & Income Profile

- Retail Goods & Services

- Traffic Counts

- Business Summary

Shortcomings of Secondary Market Data - Census Undercount

- Income Underreporting

- Business Turnover

- Business Reporting

- Measures only residential demand

Market Data: Secondary Sources

How do we compensate for the failure of secondary sources?

Primary Market Data: Consumer Research Compensate for shortcomings of market data

Helps in profile non-residential customer

Identify non-demand related barriers to retail attraction and marketing

Market Data

14

Standard Sources of Consumer Data

- Consumer Surveys

- In-store

- Online (SurveyMonkey, Facebook)

- Focus Groups

- Employees

- Merchants

- Residents

- Merchant Surveys

Market Data: Primary Sources

15

Standard market analysis is typically based on secondary sources.

Primary market data can be expensive to collect and analyze.

Market Data

Market Analysis: Understanding Secondary Market Data

Demand Supply

$$

Question: If a new store

opens in the trade area,

how much of that leakage

can we reasonably

capture? This is called

“capture rate”

General Overview: Retail Marketplace Profile

Spot-check Number of Businesses

General Overview: Retail Marketplace Profile

General Overview: Retail Marketplace Profile

Workshop Exercise

How much additional square footage of new retail

can your district support in a particular retail category?

Which retail categories offer opportunities for growth and expansion

Where should you focus your efforts to improve you tenant mix?

What strategies can we use to build weak markets?

Workshop Exercise

Column A: Select a retail category • (for this exercise, select “Health + Personal Care ”)

Column A, B, C: Select Category and Determine Supply, Demand and Gap

Health + Personal Care Retail gap within .5 miles Heath + Personal Care Retail Gap within .5 miles = $3,719,740

Example: Othello/MLK

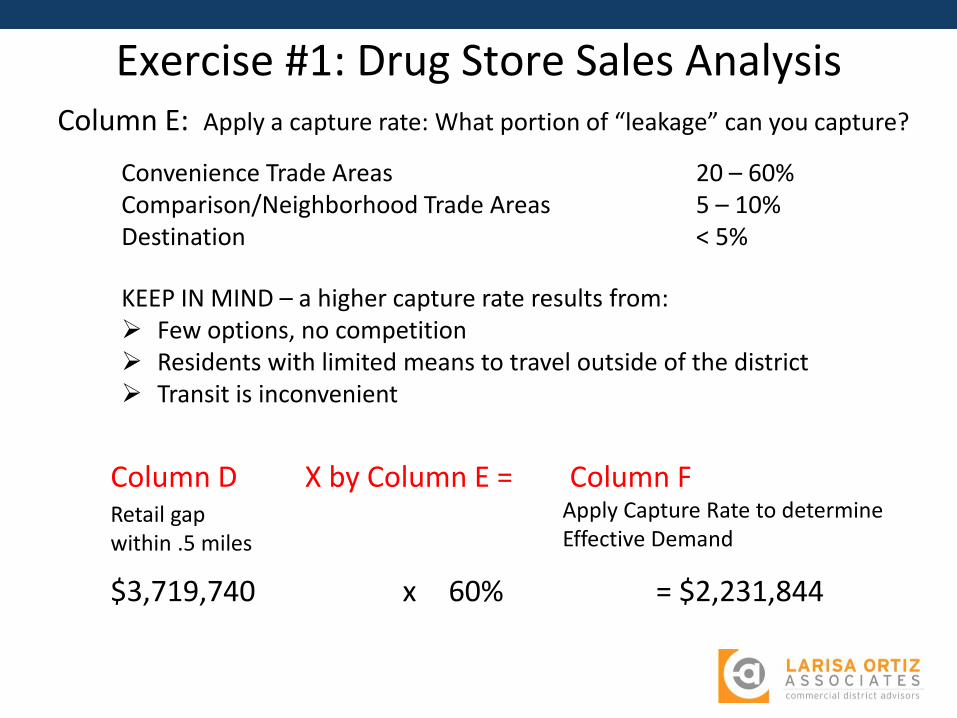

Exercise #1: Drug Store Sales Analysis

Retail gap within .5 miles

Column E: Apply a capture rate: What portion of “leakage” can you capture?

Convenience Trade Areas 20 – 60% Comparison/Neighborhood Trade Areas 5 – 10% Destination < 5%

Column D Column F Apply Capture Rate to determine Effective Demand

$3,719,740 x 60% = $2,231,844

KEEP IN MIND – a higher capture rate results from: Few options, no competition Residents with limited means to travel outside of the district Transit is inconvenient

Exercise #1: Drug Store Sales Analysis

X by Column E =

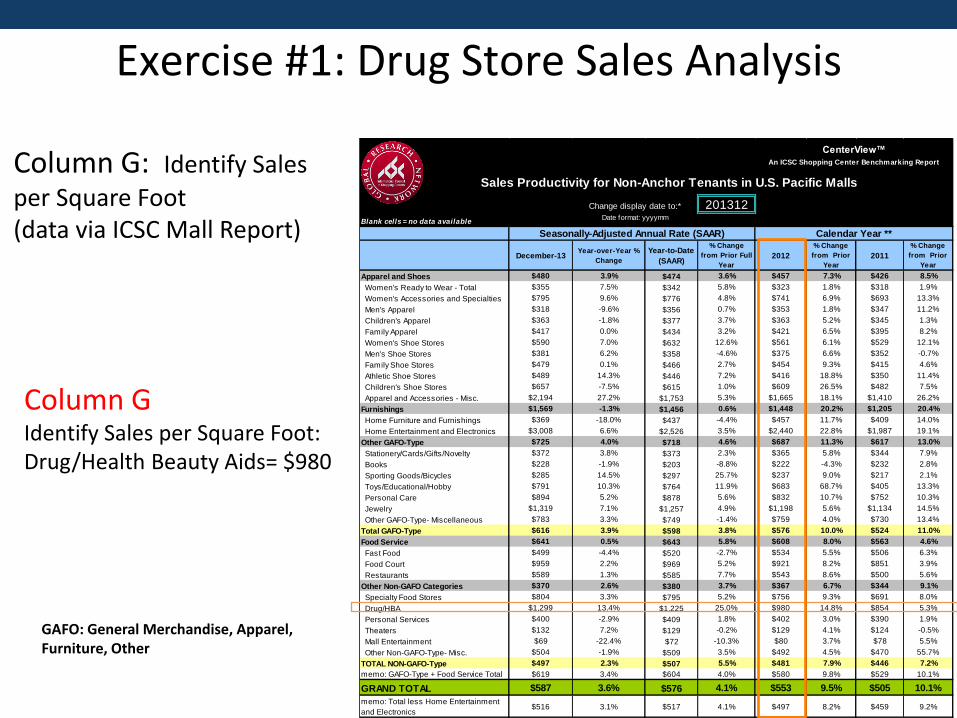

Column G: Identify Sales

per Square Foot (data via ICSC Mall Report)

Column G Identify Sales per Square Foot: Drug/Health Beauty Aids= $980

GAFO: General Merchandise, Apparel, Furniture, Other

201312

Blank cells = no data available

December-13Year-over-Year %

Change

Year-to-Date

(SAAR)

% Change

from Prior Full

Year

2012

% Change

from Prior

Year

2011

% Change

from Prior

Year

Apparel and Shoes $480 3.9% $474 3.6% $457 7.3% $426 8.5%

Women's Ready to Wear - Total $355 7.5% $342 5.8% $323 1.8% $318 1.9%

Women's Accessories and Specialties $795 9.6% $776 4.8% $741 6.9% $693 13.3%

Men's Apparel $318 -9.6% $356 0.7% $353 1.8% $347 11.2%

Children's Apparel $363 -1.8% $377 3.7% $363 5.2% $345 1.3%

Family Apparel $417 0.0% $434 3.2% $421 6.5% $395 8.2%

Women's Shoe Stores $590 7.0% $632 12.6% $561 6.1% $529 12.1%

Men's Shoe Stores $381 6.2% $358 -4.6% $375 6.6% $352 -0.7%

Family Shoe Stores $479 0.1% $466 2.7% $454 9.3% $415 4.6%

Athletic Shoe Stores $489 14.3% $446 7.2% $416 18.8% $350 11.4%

Children's Shoe Stores $657 -7.5% $615 1.0% $609 26.5% $482 7.5%

Apparel and Accessories - Misc. $2,194 27.2% $1,753 5.3% $1,665 18.1% $1,410 26.2%

Furnishings $1,569 -1.3% $1,456 0.6% $1,448 20.2% $1,205 20.4%

Home Furniture and Furnishings $369 -18.0% $437 -4.4% $457 11.7% $409 14.0%

Home Entertainment and Electronics $3,008 6.6% $2,526 3.5% $2,440 22.8% $1,987 19.1%

Other GAFO-Type $725 4.0% $718 4.6% $687 11.3% $617 13.0%

Stationery/Cards/Gifts/Novelty $372 3.8% $373 2.3% $365 5.8% $344 7.9%

Books $228 -1.9% $203 -8.8% $222 -4.3% $232 2.8%

Sporting Goods/Bicycles $285 14.5% $297 25.7% $237 9.0% $217 2.1%

Toys/Educational/Hobby $791 10.3% $764 11.9% $683 68.7% $405 13.3%

Personal Care $894 5.2% $878 5.6% $832 10.7% $752 10.3%

Jewelry $1,319 7.1% $1,257 4.9% $1,198 5.6% $1,134 14.5%

Other GAFO-Type- Miscellaneous $783 3.3% $749 -1.4% $759 4.0% $730 13.4%

Total GAFO-Type $616 3.9% $598 3.8% $576 10.0% $524 11.0%

Food Service $641 0.5% $643 5.8% $608 8.0% $563 4.6%

Fast Food $499 -4.4% $520 -2.7% $534 5.5% $506 6.3%

Food Court $959 2.2% $969 5.2% $921 8.2% $851 3.9%

Restaurants $589 1.3% $585 7.7% $543 8.6% $500 5.6%

Other Non-GAFO Categories $370 2.6% $380 3.7% $367 6.7% $344 9.1%

Specialty Food Stores $804 3.3% $795 5.2% $756 9.3% $691 8.0%

Drug/HBA $1,299 13.4% $1,225 25.0% $980 14.8% $854 5.3%

Personal Services $400 -2.9% $409 1.8% $402 3.0% $390 1.9%

Theaters $132 7.2% $129 -0.2% $129 4.1% $124 -0.5%

Mall Entertainment $69 -22.4% $72 -10.3% $80 3.7% $78 5.5%

Other Non-GAFO-Type- Misc. $504 -1.9% $509 3.5% $492 4.5% $470 55.7%

TOTAL NON-GAFO-Type $497 2.3% $507 5.5% $481 7.9% $446 7.2%

memo: GAFO-Type + Food Service Total $619 3.4% $604 4.0% $580 9.8% $529 10.1%

GRAND TOTAL $587 3.6% $576 4.1% $553 9.5% $505 10.1%

memo: Total less Home Entertainment

and Electronics$516 3.1% $517 4.1% $497 8.2% $459 9.2%

An ICSC Shopping Center Benchmarking Report

CenterView™

Calendar Year **Seasonally-Adjusted Annual Rate (SAAR)

Sales Productivity for Non-Anchor Tenants in U.S. Pacific Malls

Change display date to:*

Date format: yyyymm

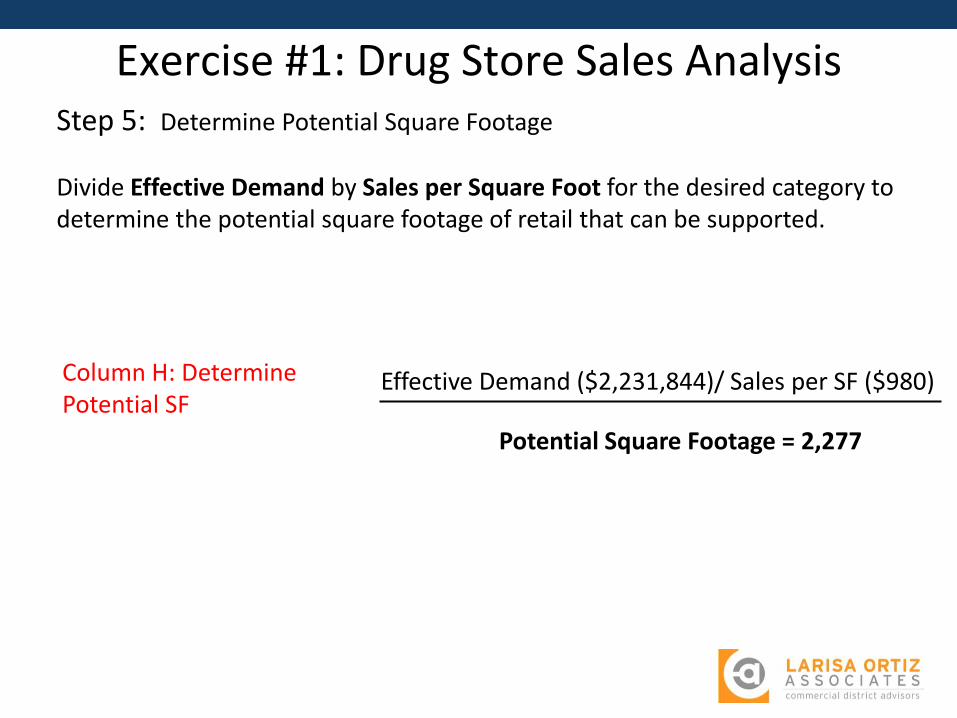

Exercise #1: Drug Store Sales Analysis

Step 5: Determine Potential Square Footage

Divide Effective Demand by Sales per Square Foot for the desired category to determine the potential square footage of retail that can be supported.

Exercise #1: Drug Store Sales Analysis

Effective Demand ($2,231,844)/ Sales per SF ($980) Column H: Determine Potential SF

Potential Square Footage = 2,277

• International Council of Shopping Centers Mall Report

• Dollars and Cents of Shopping Centers, ICSC (Used versions can be purchased at significant discount) – last version is 2008.

• Industry-specific trade associations (i.e. Food Marketing Institute)

• Local brokers

• Local retailers

• City sales data

• Google search

Resources for Sales Per Square Foot KEEP IN MIND ICSC Sales/SF data is based on primarily on suburban sites Finding local sales/SF is the most effective alternative Retailers do not like to share sales data

What does it all mean?

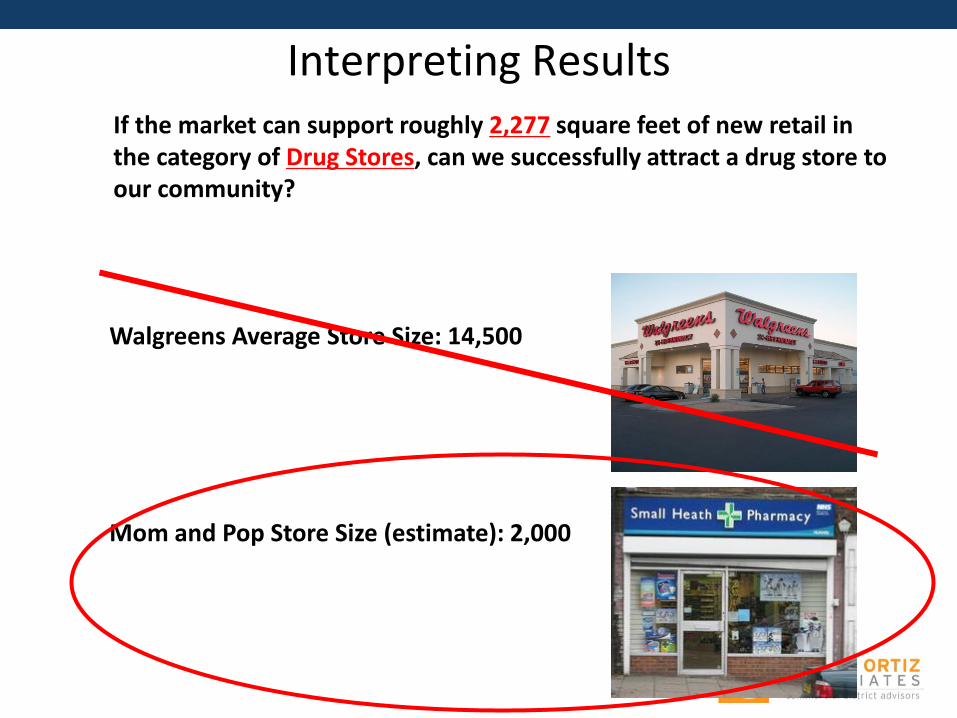

If the market can support roughly 2,277 square feet of new retail in the category of Drug Stores, can we successfully attract a drug store to our community?

Interpreting Results

Walgreens Average Store Size: 14,500

Mom and Pop Store Size (estimate): 2,000

Demand Supply Leakage

Capture

Rate*

Effective

Demand Sales PSF Potential

(Retail Potential) (Retail Sales) by Category SF

A B C D E F G H

NAICS CATEGORY Given Given B-C Given D*E Given F/G

Take 10 minutes and conduct this exercise for another retail category

Health + Personal Care $3,719,740

60% $2,231,844 $980 2,277 0 $3,719,740

• Do you have the space? • Do you have willing property owners?

• Business Expansion: Are there existing drug stores that can

improve their capture rate of existing retail leakage? • Business Attraction: Are existing drug stores servicing the

vicinity poorly? Is competition in the interest of the community?

• Is there opportunity within a larger trade area? • Look at another category

The Market Data say yes.

The Market Data say no.

The Market Data is not definitive.

Using Data to Define Strategy

Interpreting Results

Using the Data

• Attract more customers from your existing trade area (Mount Washington) – Improve “Tenant Mix” through Retail Attraction – Help Existing Businesses

• Improve Visibility/Access • Support Marketing/Promotion

– Address necessary Physical Improvements • Improve Cleanliness/Safety

– Grow the Market • Grow the trade area (add more shoppers by growing the primary

trade area) • Build density through development (add more shoppers to existing

trade area)

Using the Data: Develop a “Tenant Mix” Strategy

Develop a Retail Sales and Tenant Mix Strategy

• Springfield, Jacksonville, Fl

• Combined market data and consumer preference data to develop a “nodal” retail attraction strategy

• A Comprehensive Strategy for Improvements

• Lower Broadway, Newark, NJ

Potential grocery store site.

Five years of resources and staff time went

towards identifying and attracting a grocer to this

location

Using the Data: Recalibrate your Strategy

1 Mile Radius

Using the Data: Help Existing Merchants

Using the Data: Improve Visibility

Mt. Washington, Pittsburgh

• Challenge: – 1.5 million visitors annually

– Very few venture down Shiloh

Shiloh Street.

Curve in street reduced visibility

1.5 million visitors ride

incline annually

Using the Data: Improve Visibility Mt. Washington, Pittsburgh, PA

• Solution: Increase visibility through signage – Businesses were allocated $500 per sign

– Pedestrian counts increased by nearly 30%

– Business report increased sales

– A local business went from part time to full time hours

– Other businesses want to replicate signage

Using the Data: Grow Customer Base

• Improve access my multiple means of transportation

Jackson Heights, NY

Using the Data: Grow Customer Base

39

125th Street, Harlem, NY Map retailers, retail categories to match space configuration and availability.

Rezoning to encourage new development

Major Development Opportunities

Using the Data: Redevelopment

Opportunities for Independent Retail

Questions?

RETAIL

LEASING

Identifying and Attracting Appropriate Retailer & Developers

Instructor: Larisa Ortiz, Larisa Ortiz Associates, LLC

www.larisaortizassociates.com

www.commercialdistrictadvisor.com

Twitter: @cdadvisor

RETAIL

LEASING

INTRODUCTION

About you

urban vs. suburban?

upper-income vs. middle-income vs. lower income

years of experience

retail attraction (multi-site)

previous experience with retail attraction?

RETAIL

LEASING

Why does tenant mix matter?

There must be a reason why you are here…

RETAIL

LEASING

COURSE AGENDA

1. Develop a Strategy for Retail Attraction

2. Get “Retail Ready” – Addressing barriers to retail attraction

3. Know your Retailer

4. Turn Plans into Action – examples of successful retail attraction

RETAIL

LEASING

1. DEVELOP A STRATEGY

RETAIL

LEASING

How do we define “success”?

• Shopper choice • Retail sales • Property values

Source: Econsult , “A Strategic In vestment Framework for Philadelphia”, 2009

RETAIL

LEASING

What makes a successful commercial district?

– Density of retail

– Tenant mix

– Convenience (parking and transit accessibility)

– Condition of the physical environment

RETAIL

LEASING

Density of Retail

• The ability of a shopper to visit multiple stores in the same area

• Corridors with more stores out-perform lower density corridors and have a consistently positive impact on real estate values and retail sales

• Commercial districts with more offerings typically draw customers from a larger geographic area

RETAIL

LEASING

Density of Retail Impact Trade Area

U.S. Shopping Center Classifications

Center Type Average SF Typical # of Tenants

Trade Area Size

Travel Time

Regional Mall 400k – 800k 40-80 5 – 25 miles ≤ 30 min

Community Center

125k – 400k 15 – 40 5 – 15 miles ≤ 20 min

Neighborhood Center

30k – 125k 5 – 20 3 miles ≤ 10 min

Strip/Convenience

< 30k NA < 1 mile ~ 5 min

Size and location impact the relative distance a customer would be willing to travel

Source: International Council of Shopping Centers

RETAIL

LEASING

Know your target customer

– Residents

– Daytime employees

– Visitors

Defining your project’s “strategic position” in the marketplace

– retail offerings

– price point

– Customer preference

The importance of co-tenancy

Tenant Mix: Getting it Right

RETAIL

LEASING

Strategic Positioning

TJ Maxx

Brooklyn

Industries

Macy’s

Retailer Price Point and

relative Income Benchmarks.

Dollar Store

Talbots

Blink Gym

LOA Strategic Positioning Matrix

Mapping your District’s Business Mix

RETAIL

LEASING

Strategic positioning in action

Rego Park Center, Queens, NY

RETAIL

LEASING

Co-tenancy

• Retailers like to be grouped with retailers who are attracting the same customer

• Competitive retailers like to be near one another to give customers opportunities to comparison shop (apparel, jewelry, shoes, etc.)

• Some retailers include co-tenancy provisions in their leases – Co-tenancy provisions give retail tenants the right to pay reduced

rent or to terminate their leases, or both, if other specific tenants or a percentage of tenants do not open or if they leave a shopping center.

RETAIL

LEASING

Retail Clusters

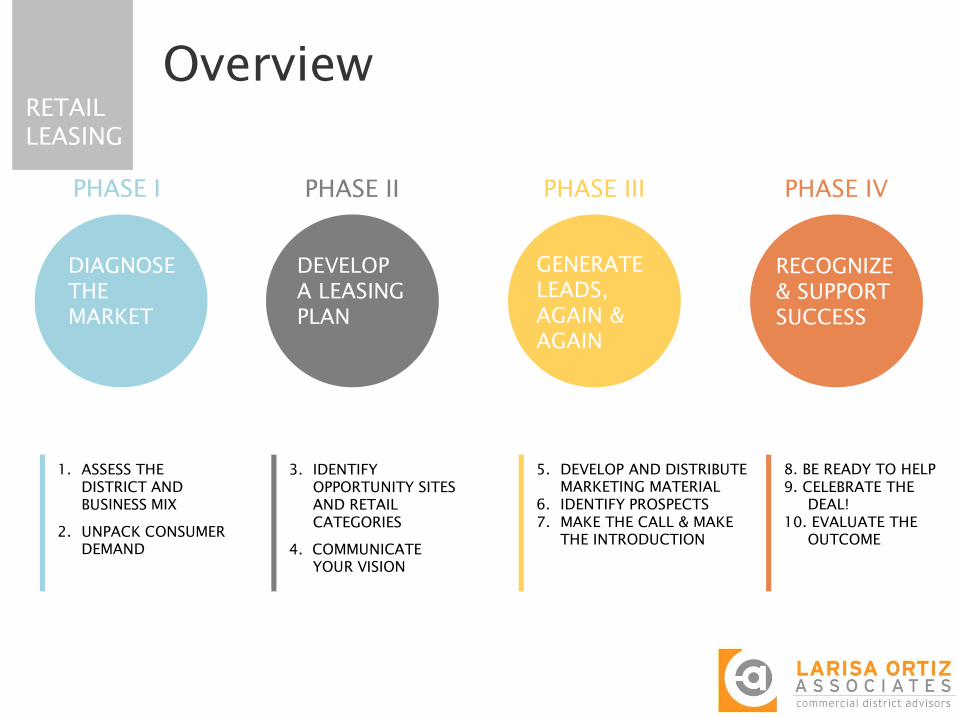

Overview

RETAIL

LEASING

PHASE I

DIAGNOSE

THE

MARKET

PHASE II

DEVELOP

A LEASING

PLAN

PHASE III

GENERATE

LEADS,

AGAIN &

AGAIN

PHASE IV

RECOGNIZE

& SUPPORT

SUCCESS

1. ASSESS THE

DISTRICT AND

BUSINESS MIX

2. UNPACK CONSUMER

DEMAND

3. IDENTIFY

OPPORTUNITY SITES

AND RETAIL

CATEGORIES

4. COMMUNICATE

YOUR VISION

5. DEVELOP AND DISTRIBUTE

MARKETING MATERIAL

6. IDENTIFY PROSPECTS

7. MAKE THE CALL & MAKE

THE INTRODUCTION

8. BE READY TO HELP

9. CELEBRATE THE

DEAL!

10. EVALUATE THE

OUTCOME

The Process

RETAIL

LEASING

PHASE I

DIAGNOSE

THE

MARKET

Walk your district and observe the existing retail mix

Assess the physical shopping environment

Identify your traffic generators

Talk to those in the know

STEP 1: ASSESS THE DISTRICT AND BUSINESS MIX

The Process

RETAIL

LEASING

PHASE I

DIAGNOSE

THE

MARKET

STEP 2: UNPACK CONSUMER DEMAND DYNAMICS

Determine trade area

Estimate leakage by category (leakage refers to

retail sales lost by a community to businesses

outside of trade area)

Consumer profile data (i.e. psychographics)

RETAIL

LEASING

PHASE II

DEVELOP

A LEASING

PLAN

TJ Maxx

Brooklyn

Industries

Macy’s

Retailer Price Point and

relative Income Benchmarks.

Dollar Store

Talbots

Blink Gym

• What is “Strategic

Positioning”?

LOA Strategic Positioning Matrix

Mapping your District’s Business Mix

The Process

RETAIL

LEASING

PHASE II

DEVELOP

A LEASING

PLAN

1. Map your Businesses

LOA Strategic Positioning Matrix

Mapping your District’s Business Mix

TJ Maxx

Brooklyn

Industries

Macy’s

Retailer Price Point and

relative Income Benchmarks.

Dollar Store

Talbots

Blink Gym

RETAIL

LEASING

PHASE II

DEVELOP

A LEASING

PLAN

Develop an opportunity site inventory

STEP 3: IDENTIFY SITES & RETAIL CATEGORIES

Lease expiration dates

Owner expectations – lease rates, uses

Owner interest - don’t engage if an owner is recalcitrant to

share information.

Typically you do not want to go to a retailer without some

assurance that you have a viable site

RETAIL

LEASING

PHASE II

DEVELOP

A LEASING

PLAN

Property Owner Engagement

Opportunity Site Identification

Identify requirements

Engage early through market

research

Communicate your strategy

Move on if recalcitrant

Don’t give up. Revisit after

successful execution

Request formal commitment

before expending

time/resources

RETAIL

LEASING

PHASE II

DEVELOP

A LEASING

PLAN

STEP 3: IDENTIFY SITES & RETAIL CATEGORIES

Identify Retail Categories to Target

Consumer demand

Community preference

Size and configuration of opportunity sites

RETAIL

LEASING

PHASE II

DEVELOP

A LEASING

PLAN

Make the commercial real estate community aware of your

targeted retail approach

STEP 4: COMMUNICATE YOUR VISION

Share your findings and vision with the stakeholders

Become a vehicle connections

• monthly real estate alerts (vacancies, new business openings,

businesses for sale, business testimonials

RETAIL

LEASING

PHASE III

GENERATE

LEADS,

AGAIN &

AGAIN

STEP 5: DEVELOP AND DISTRIBUTE MARKETING MATERIAL

Map of the district that clearly identifies major activity generators

Information about any incentives or resources for retail

Testimonials from merchants

Sales figures for your district

RETAIL

LEASING

PHASE III

GENERATE

LEADS,

AGAIN &

AGAIN

STEP 6: IDENTIFY PROSPECTS

Seek Out Prospects. National vs. Regional Independents

- Trade shows vs. brokers vs. good ‘ole shoe leather

Network, shop, and advertise

Get creative!

Keep a Prospect Database

RETAIL

LEASING

PHASE III

GENERATE

LEADS,

AGAIN &

AGAIN

PROSPECT DATABASE

Keep a Prospect Database

• Business Contact Information

• Broker Contact Information

• Lifestyle/Price point

• Square Footage Needed

• Desired Rent

• Other locations

• Strength of prospect (hot/warm/cold)

- Keep track of when to follow up

- Be persistent

RETAIL

LEASING

PHASE III

GENERATE

LEADS,

AGAIN &

AGAIN

STEP 7: MAKE THE CALL

Conduct Prospect Outreach

Invite prospects on a Choreographed Tour of your District

RETAIL

LEASING

PHASE III

GENERATE

LEADS,

AGAIN &

AGAIN

STEP 8: BE READY TO HELP

Play the mediator to negotiations , don’t be the broker (unless

you have to)

Be prepared with resources that will help tenants in

their interactions with the landlord

Don’t be discouraged, getting to “yes” can mean

hearing “no” multiple times

RETAIL

LEASING

RECOGNIZE

& MEASURE

SUCCESS

PHASE IV STEP 9: CELEBRATE THE DEAL!

A grand opening is an exciting recognition

Best way to build credibility, engage more property

owners, and attract more retail

Issue press release, invite local leaders, cut that

bright red ribbon

RETAIL

LEASING

RECOGNIZE

& MEASURE

SUCCESS

PHASE IV

RETAIL

LEASING

RECOGNIZE

& MEASURE

SUCCESS

PHASE IV STEP 10: TRACK PROGRESS, AND THEN KEEP GOING

Have a system in place to measure success as well as failure

Sharing your success will provide your organization with

valuable recognition

Rinse, wash, and repeat!

RETAIL

LEASING

2. GET “RETAIL READY”

RETAIL

LEASING

Lessons Learned: What role can you play?

• The good and bad news…. – 30/70 rule

– There is no silver bullet

• Retailers have varied approaches to site selection, get acquainted with site selection criteria for the categories you plan to pursue

– Urban communities still confound.

– Physical constraints matter (though less so where there is density)

• Access/Parking

• Visibility

• Retail density and a reliance on individual property owners participation

RETAIL

LEASING

Setting the Stage: Clean and Safe

P. 34

Source: John Skinner, Verde Group/ ICSC Global Research Network

Summary of Strategies

RETAIL

LEASING

Setting the Stage: Clean and Safe

P. 35

Source: John Skinner, Verde Group/ ICSC Global Research Network

Summary of Strategies

RETAIL

LEASING

“Getting Retail Ready” Hierarchy

P. 36

Tenant Mix

Safe Clean

Access/Visibility

Attraction

Retention

Fundamental

Advanced

Summary of Strategies

Redevelopment

RETAIL

LEASING

3. KNOW YOUR MARKET

RETAIL

LEASING

What indicators matter to retailers?

Generally…

– Median Household Income (not average)

– Total number of households

RETAIL

LEASING

Specifically…

Source: ICSC, Social Compact, “Inside Site Selection.

Retailers’ search for strategic business locations”, 2008

Site Selection Indicators

1. Average Household Size

2. Average Income

3. Competition (presence, type, location)

4. Crime

5. Daytime Population

6. Educational Attainment

7. Ethnic Composition

8. Homeownership

9. Home Sales Values

10. Income Change

11. Major Employers in the Area

12. Median Income

13. Neighborhood Orientation

14. Number of Households

15. Pedestrian Traffic

16. Population Change

17. Population Size

18. Visibility

What indicators matter to retailers?

RETAIL

LEASING

Industry Research

Characteristics Duane-Reade CVS Walgreens

Trade Area Size 3-5 miles

Trade Area Population 25,000 18,000 20,000

Store Size SF 12,900 (96 x 137) 14,560sf (112 x 130)

Site Preferences High visibility, high traffic count Signalized intersection with heavy traffic count

Parking Requirements 75-80 cars 70+ cars

DRUGSTORE

GROCERY STORE

RETAIL

LEASING

What indicators matter to retailers?

Specialized retailers rely on additional indicators…

RETAIL

LEASING

Do you have the

right kind of

space?

Do you have the enough

of the “right” residents?

RETAIL

LEASING

Do your homework before making the pitch…

• Tenant Specific Research

– Do you have the right people? • Einstein Bros. Bagels 70% some college education

• Mandee’s trendy young women with mod/low incomes

– Do you have enough pedestrian traffic? • Auntie Anne’s 30 pp. every 5 minutes during off-peak

– Do you have the right space?

• CB2 6,000 – 9,000 sf stores targeting young professionals

• Pinkberry 600 – 1,600 sf

RETAIL

LEASING

Prospect Research

Where do you find tenant specific information?

– Websites

– Tradeshows

– Brokers/Leasing Agents

– Regional Real Estate Reps

– Networking

– Industry publications

• Shopping Centers Today

• Retail Traffic

• Reference USA (sales psf)

44

RETAIL

LEASING

Data retailers want but struggle to get…

• Generally includes data NOT captured by the census

• Short-term change at the neighborhood level (one year, two years, five years) – Retailers unaware of new data sets, notably the Home Mortgage

Disclosure Act (HMDA)

• Daytime population information

• Visitor population information

• Pedestrian traffic counts

• Detailed ethnic composition (i.e. Latino market)

Hint, Hint. This is where you come in….

RETAIL

LEASING

Barriers to Retail Development

• Land availability

• Market demand to support a particular business

• Evidence of that market demand

RETAIL

LEASING

What can economic development professionals do?

• Do your homework. Know the retailers perspective.

• Offer information on future neighborhood change, i.e. development plans, new housing

• Demonstrate a commitment and willingness to overcome obstacles, i.e. licensing, permitting, incentives, etc.

• Stir up the competitive juices

Harvey Gutman, Brookside Advisors

ICSC , “Inside Site Selection”

RETAIL

LEASING

Offer evidence of market demand

• Marketing Material – they will do their own research. So don’t stress too much about this.

• Sometimes its about getting on their radar

• Site Visit

RETAIL

LEASING

4. TURN PLANS INTO ACTION

RETAIL

LEASING

Downtown Brooklyn. Nightlife.

RETAIL

LEASING

South Bronx. Aspirational Staging

Vacancy: Before

RETAIL

LEASING

South Bronx. Aspirational Staging

Vacancy: After

RETAIL

LEASING

Woonsocket, RI. Main Street Open House

RETAIL

LEASING

Bed-Stuy Social Media

It takes a team… Grand Opening!

RETAIL

LEASING

Parting Words

• Retail attraction efforts are not a “quick fix”

• Relationships are key to successful leasing

• Engage your board and local residents to serve as district ambassadors

• Don’t get discouraged – there may be many “no’s” before a “yes”

RETAIL

LEASING

THANK YOU!

Larisa Ortiz

718-205-5116

Twitter: @cdadvisor

Facebook: Commercial District Advisor

Blog: www.commercialdistrictadvisor.com