larsen & toubro ltd.breport.myiris.com/bcl1/lartoubr_20110218.pdf · 2011-02-22 · stock idea...

TRANSCRIPT

Stock Idea – Larsen & Toubro Ltd.

1

Bajaj Capital Centre for Investment Research

Vol. 31 / 10-11 February 18, 2011

Buy CMP: 1639.15 Target: 2000.0

LARSEN & TOUBRO LTD. Upside: 22.0 % Horizon: 12 M

Analyst: Atul Kanwar

Phone: +91 11 66272300 Ext: 651

Email: [email protected]

Head of Research: Alok Agarwala

E-mail: [email protected]

Key Data

Sector Construction & Engineering

Face value (Rs.) 2.0

52-week high/low (Rs.) 2212.7 / 1410.0

Market cap (Rs. cr.) 99799.6

Book value (Rs.) 338.5

Price / book value 4.8

PE ratio (TTM) 18.8

Market cap / sales 2.3

Dividend (%) 625

Average daily volume (1 Y) 1214094

Beta 1.0

1 year return (%) 14.9

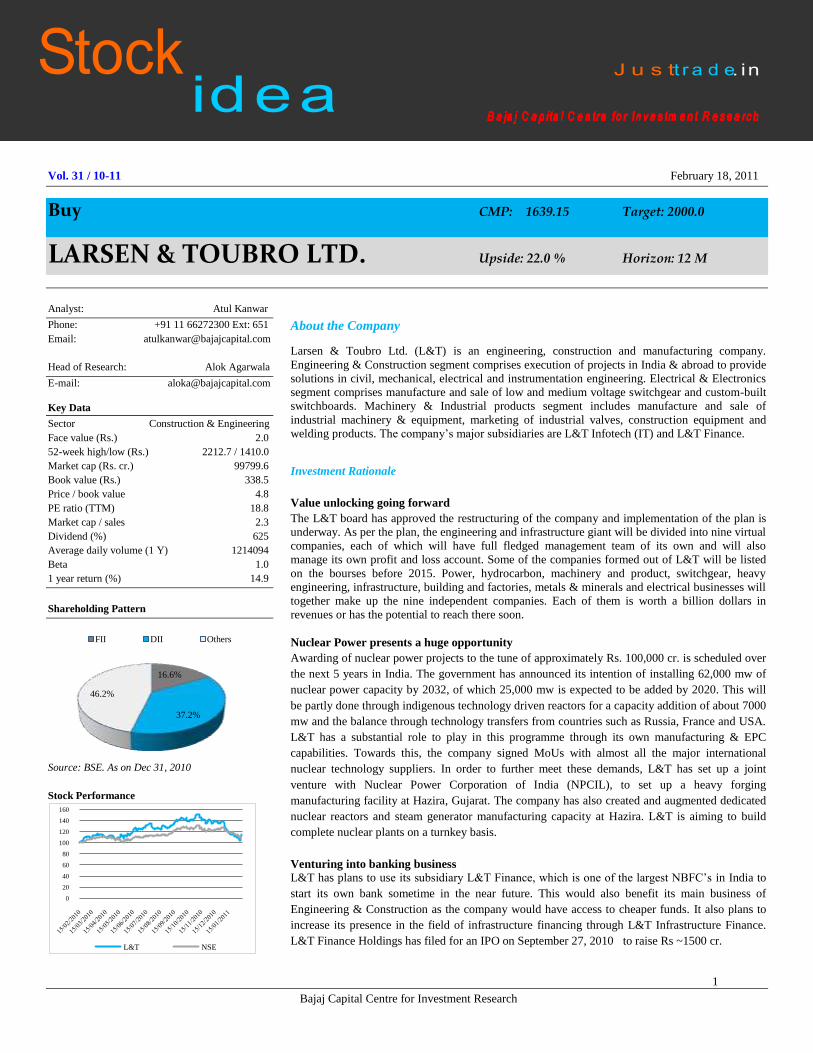

Shareholding Pattern

Source: BSE. As on Dec 31, 2010

Stock Performance

About the Company

Larsen & Toubro Ltd. (L&T) is an engineering, construction and manufacturing company.

Engineering & Construction segment comprises execution of projects in India & abroad to provide

solutions in civil, mechanical, electrical and instrumentation engineering. Electrical & Electronics

segment comprises manufacture and sale of low and medium voltage switchgear and custom-built

switchboards. Machinery & Industrial products segment includes manufacture and sale of

industrial machinery & equipment, marketing of industrial valves, construction equipment and

welding products. The company’s major subsidiaries are L&T Infotech (IT) and L&T Finance.

Investment Rationale

Value unlocking going forward

The L&T board has approved the restructuring of the company and implementation of the plan is

underway. As per the plan, the engineering and infrastructure giant will be divided into nine virtual

companies, each of which will have full fledged management team of its own and will also

manage its own profit and loss account. Some of the companies formed out of L&T will be listed

on the bourses before 2015. Power, hydrocarbon, machinery and product, switchgear, heavy

engineering, infrastructure, building and factories, metals & minerals and electrical businesses will

together make up the nine independent companies. Each of them is worth a billion dollars in

revenues or has the potential to reach there soon.

Nuclear Power presents a huge opportunity

Awarding of nuclear power projects to the tune of approximately Rs. 100,000 cr. is scheduled over

the next 5 years in India. The government has announced its intention of installing 62,000 mw of

nuclear power capacity by 2032, of which 25,000 mw is expected to be added by 2020. This will

be partly done through indigenous technology driven reactors for a capacity addition of about 7000

mw and the balance through technology transfers from countries such as Russia, France and USA.

L&T has a substantial role to play in this programme through its own manufacturing & EPC

capabilities. Towards this, the company signed MoUs with almost all the major international

nuclear technology suppliers. In order to further meet these demands, L&T has set up a joint

venture with Nuclear Power Corporation of India (NPCIL), to set up a heavy forging

manufacturing facility at Hazira, Gujarat. The company has also created and augmented dedicated

nuclear reactors and steam generator manufacturing capacity at Hazira. L&T is aiming to build

complete nuclear plants on a turnkey basis.

Venturing into banking business

L&T has plans to use its subsidiary L&T Finance, which is one of the largest NBFC’s in India to

start its own bank sometime in the near future. This would also benefit its main business of

Engineering & Construction as the company would have access to cheaper funds. It also plans to

increase its presence in the field of infrastructure financing through L&T Infrastructure Finance.

L&T Finance Holdings has filed for an IPO on September 27, 2010 to raise Rs ~1500 cr.

16.6%

37.2%

46.2%

FII DII Others

0

20

40

60

80

100

120

140

160

L&T NSE

Stock Idea – Larsen & Toubro Ltd.

2

Bajaj Capital Centre for Investment Research

L&T has kick started a restructuring plan to

divide the company into nine independent

entities.

L&T recently delivered its first tranche of

nuclear equipment to US based Transnuclear

Inc. – a Areva company.

L&T Infotech, a subsidiary of L&T plans to

come out with a IPO soon. It has set itself a

target to double its revenues in the next 3-4

years.

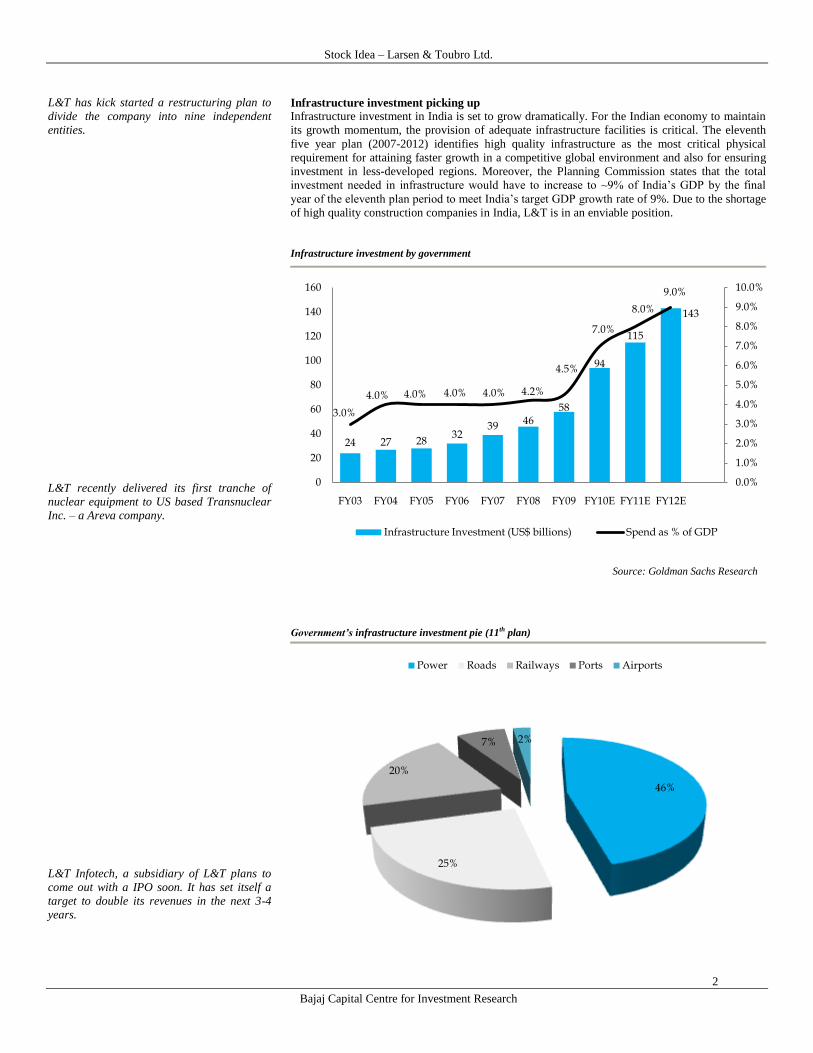

Infrastructure investment picking up

Infrastructure investment in India is set to grow dramatically. For the Indian economy to maintain

its growth momentum, the provision of adequate infrastructure facilities is critical. The eleventh

five year plan (2007-2012) identifies high quality infrastructure as the most critical physical

requirement for attaining faster growth in a competitive global environment and also for ensuring

investment in less-developed regions. Moreover, the Planning Commission states that the total

investment needed in infrastructure would have to increase to ~9% of India’s GDP by the final

year of the eleventh plan period to meet India’s target GDP growth rate of 9%. Due to the shortage

of high quality construction companies in India, L&T is in an enviable position.

Infrastructure investment by government

Source: Goldman Sachs Research

Government’s infrastructure investment pie (11th plan)

24 27 2832

39 4658

94

115

143

3.0%

4.0% 4.0% 4.0% 4.0% 4.2%

4.5%

7.0%

8.0%

9.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

0

20

40

60

80

100

120

140

160

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10E FY11E FY12E

Infrastructure Investment (US$ billions) Spend as % of GDP

46%

25%

20%

7% 2%

Power Roads Railways Ports Airports

Stock Idea – Larsen & Toubro Ltd.

3

Bajaj Capital Centre for Investment Research

L&T is also a frontrunner for the Rs. 5000 cr.

mono rail project for old Ahmedabad city

area.

The L&T Power’s BTG facilities are among

the largest of their kind in the world, with

present annual capacity of manufacturing

5000 mw of equipment , to be expanded to

6000 mw by 2012.

L&T & Europe’s Cassidian have formed a

joint venture to cater to the field of defense

electronics.

L&T concentrating on city rail projects

L&T along with Scomi rail of Malaysia has already bagged the contract for the first mono rail

project in Mumbai given by Mumbai Metropolitan Region Development Authority (MMRDA).

The company is also handling the Hyderabad metro rail project. It has bagged an order from

Chennai Metro Rail Ltd. (CMRL) for the design & construction of track work that is valued at Rs

449.2 cr. CMRL is a JV between the state govt. and the centre to set up a Rs 14000 cr. metro rail in

Chennai The railway unit of L&T has secured a slew of orders aggregating Rs 1103 cr. from

various power plant developers for the construction of dedicated railway lines to link power plant

sites to mainline rail network.

L&T’s power subsidiary growing at a brisk pace

The sales of L&T Power is expected to jump from US$ 400 mn to US$ 3 bn. L&T Power has a

joint venture with Japan's Mitsubishi Heavy Industries for manufacturing of supercritical

technology-based boilers and turbine-generator sets for thermal power units. The company has an

order book worth Rs. 32,000 cr. deliverable over the next two and a half years. With the

commissioning of the country’s largest integrated Boiler, Turbine, Generator (BTG) factory at

Hazira in Gujarat, L&T is well placed to meet its ~8,000 mw of boiler orders and ~9,000 mw of

turbine orders in hand.

Opportunities in Middle-East

The L&T-Galfar consortium, through international competitive bidding, has been awarded a US$

764 mn order for the design and development of the New Salalah International Airport in the

Sultanate of Oman. This is L&Ts largest overseas EPC order. L&T's scope will be ~US$ 500 mn

and the order is to be completed in 30 months. The Middle East comprises close to ~6% of the

company’s order-book, while other overseas geographies comprise ~2%. FIFA 2022 has been

awarded to Qatar. This will result into significant investments in the infrastructure development in

Qatar over the next decade, probably starting as soon as 12 months from now.

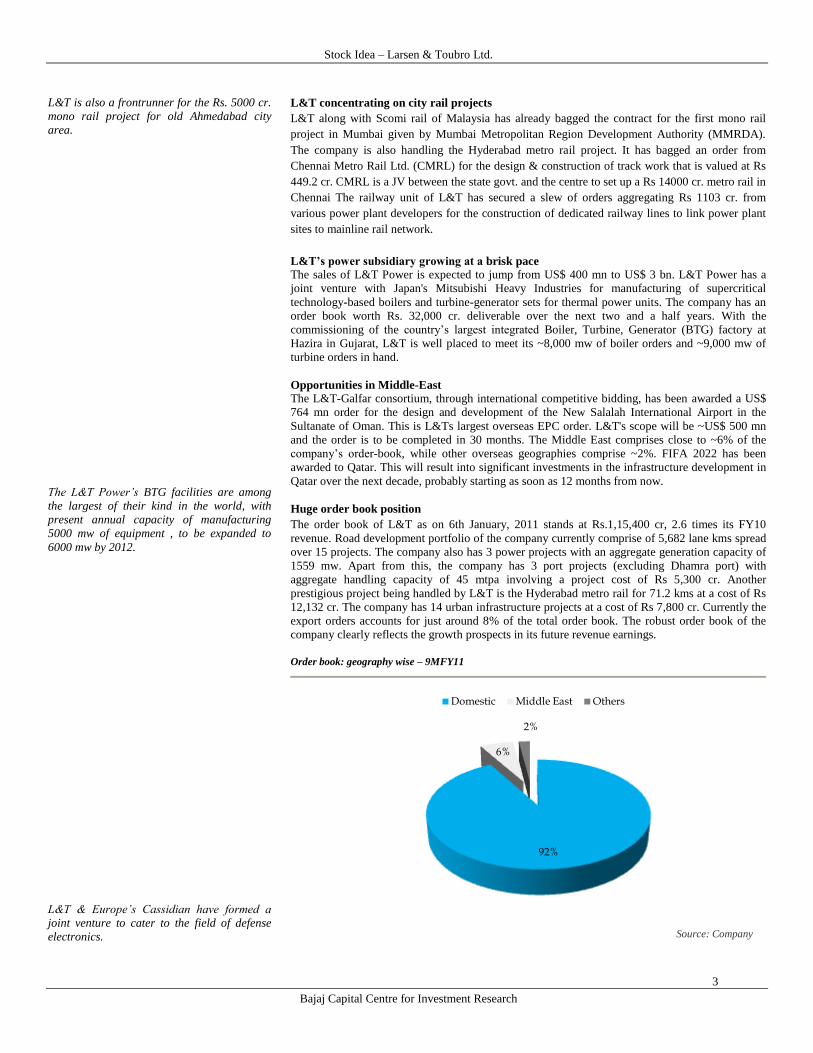

Huge order book position

The order book of L&T as on 6th January, 2011 stands at Rs.1,15,400 cr, 2.6 times its FY10

revenue. Road development portfolio of the company currently comprise of 5,682 lane kms spread

over 15 projects. The company also has 3 power projects with an aggregate generation capacity of

1559 mw. Apart from this, the company has 3 port projects (excluding Dhamra port) with

aggregate handling capacity of 45 mtpa involving a project cost of Rs 5,300 cr. Another

prestigious project being handled by L&T is the Hyderabad metro rail for 71.2 kms at a cost of Rs

12,132 cr. The company has 14 urban infrastructure projects at a cost of Rs 7,800 cr. Currently the

export orders accounts for just around 8% of the total order book. The robust order book of the

company clearly reflects the growth prospects in its future revenue earnings.

Order book: geography wise – 9MFY11

Source: Company

92%

6%

2%

Domestic Middle East Others

Stock Idea – Larsen & Toubro Ltd.

4

Bajaj Capital Centre for Investment Research

L&T's power equipment subsidiary, L&T

Power, is set to become one of the top

contributors to the company's revenue by

2015.

L&T bagged orders worth Rs 36,000 cr. in the

first half of FY11, up 29% YoY.

The master plan of Dhamra Port project

provides for 13 berths that are capable of

handling more than 100 mtpa of dry bulk,

liquid bulk, containerized and general cargo.

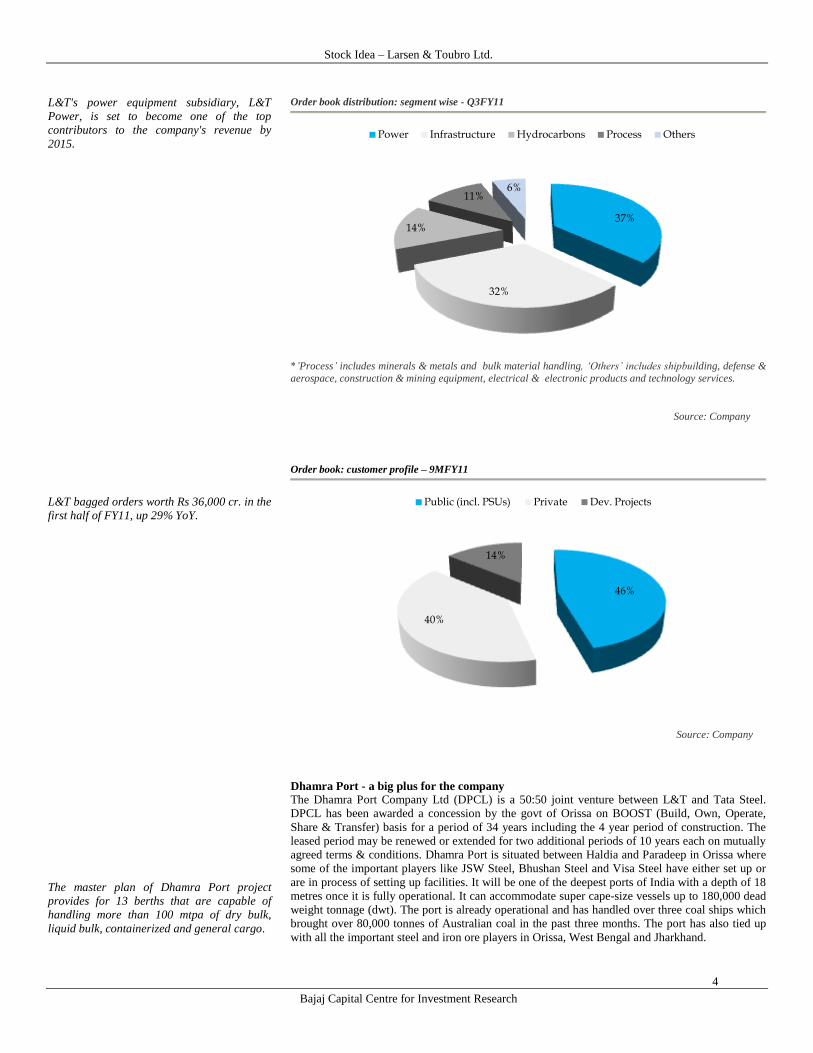

Order book distribution: segment wise - Q3FY11

*’Process’ includes minerals & metals and bulk material handling, ‘Others’ includes shipbuilding, defense &

aerospace, construction & mining equipment, electrical & electronic products and technology services.

Source: Company

Order book: customer profile – 9MFY11

Source: Company

Dhamra Port - a big plus for the company The Dhamra Port Company Ltd (DPCL) is a 50:50 joint venture between L&T and Tata Steel.

DPCL has been awarded a concession by the govt of Orissa on BOOST (Build, Own, Operate,

Share & Transfer) basis for a period of 34 years including the 4 year period of construction. The

leased period may be renewed or extended for two additional periods of 10 years each on mutually

agreed terms & conditions. Dhamra Port is situated between Haldia and Paradeep in Orissa where

some of the important players like JSW Steel, Bhushan Steel and Visa Steel have either set up or

are in process of setting up facilities. It will be one of the deepest ports of India with a depth of 18

metres once it is fully operational. It can accommodate super cape-size vessels up to 180,000 dead

weight tonnage (dwt). The port is already operational and has handled over three coal ships which

brought over 80,000 tonnes of Australian coal in the past three months. The port has also tied up

with all the important steel and iron ore players in Orissa, West Bengal and Jharkhand.

37%

32%

14%

11%6%

Power Infrastructure Hydrocarbons Process Others

46%

40%

14%

Public (incl. PSUs) Private Dev. Projects

Stock Idea – Larsen & Toubro Ltd.

5

Bajaj Capital Centre for Investment Research

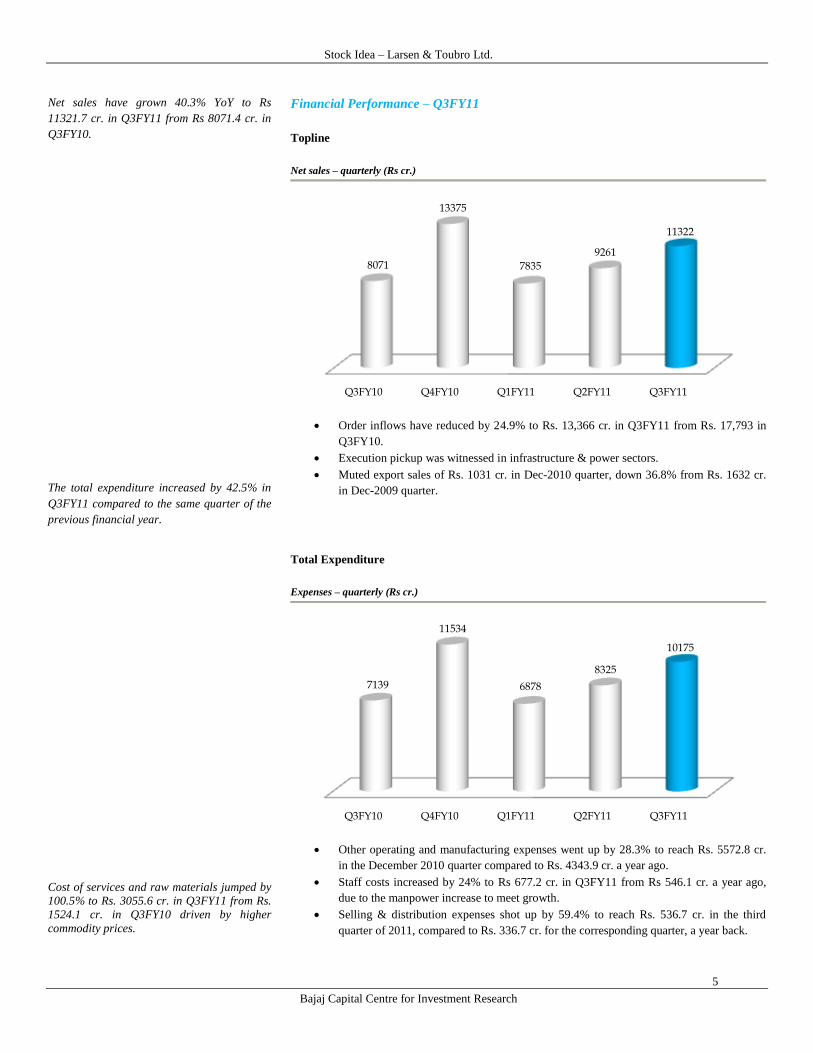

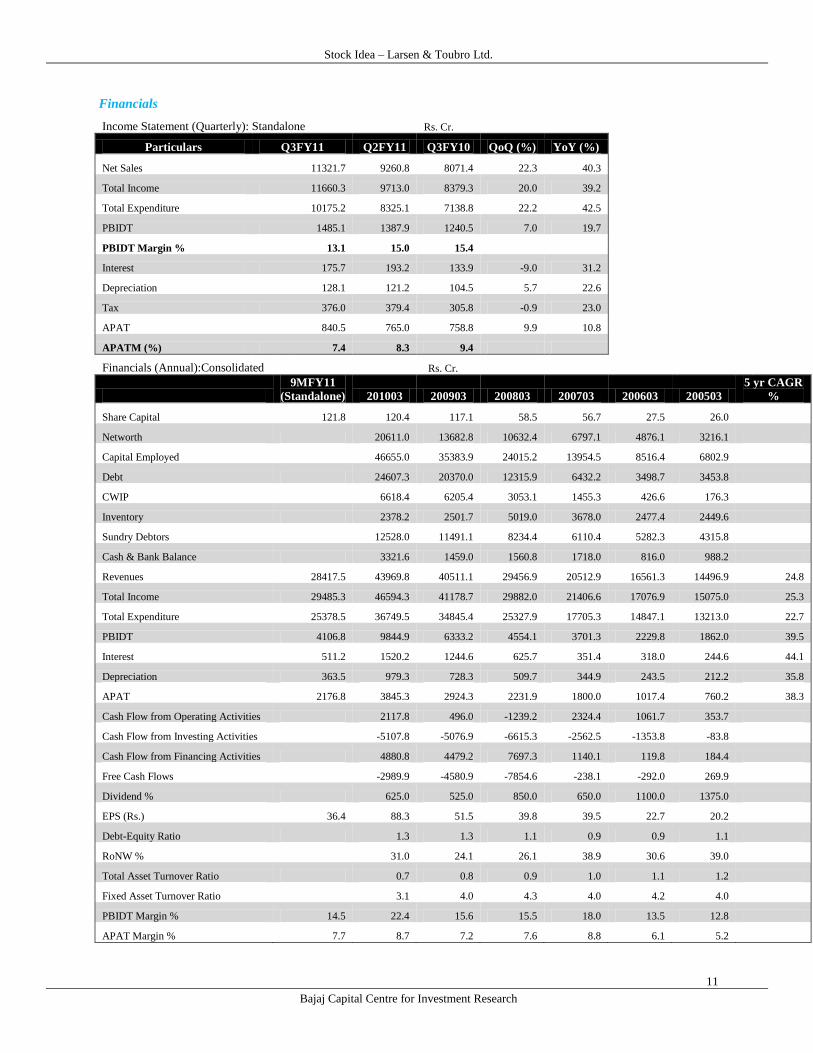

Net sales have grown 40.3% YoY to Rs

11321.7 cr. in Q3FY11 from Rs 8071.4 cr. in

Q3FY10.

The total expenditure increased by 42.5% in

Q3FY11 compared to the same quarter of the

previous financial year.

Cost of services and raw materials jumped by

100.5% to Rs. 3055.6 cr. in Q3FY11 from Rs.

1524.1 cr. in Q3FY10 driven by higher

commodity prices.

Financial Performance – Q3FY11

Topline

Net sales – quarterly (Rs cr.)

Order inflows have reduced by 24.9% to Rs. 13,366 cr. in Q3FY11 from Rs. 17,793 in

Q3FY10.

Execution pickup was witnessed in infrastructure & power sectors.

Muted export sales of Rs. 1031 cr. in Dec-2010 quarter, down 36.8% from Rs. 1632 cr.

in Dec-2009 quarter.

Total Expenditure

Expenses – quarterly (Rs cr.)

Other operating and manufacturing expenses went up by 28.3% to reach Rs. 5572.8 cr.

in the December 2010 quarter compared to Rs. 4343.9 cr. a year ago.

Staff costs increased by 24% to Rs 677.2 cr. in Q3FY11 from Rs 546.1 cr. a year ago,

due to the manpower increase to meet growth.

Selling & distribution expenses shot up by 59.4% to reach Rs. 536.7 cr. in the third

quarter of 2011, compared to Rs. 336.7 cr. for the corresponding quarter, a year back.

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

8071

13375

7835

9261

11322

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

7139

11534

6878

8325

10175

Stock Idea – Larsen & Toubro Ltd.

6

Bajaj Capital Centre for Investment Research

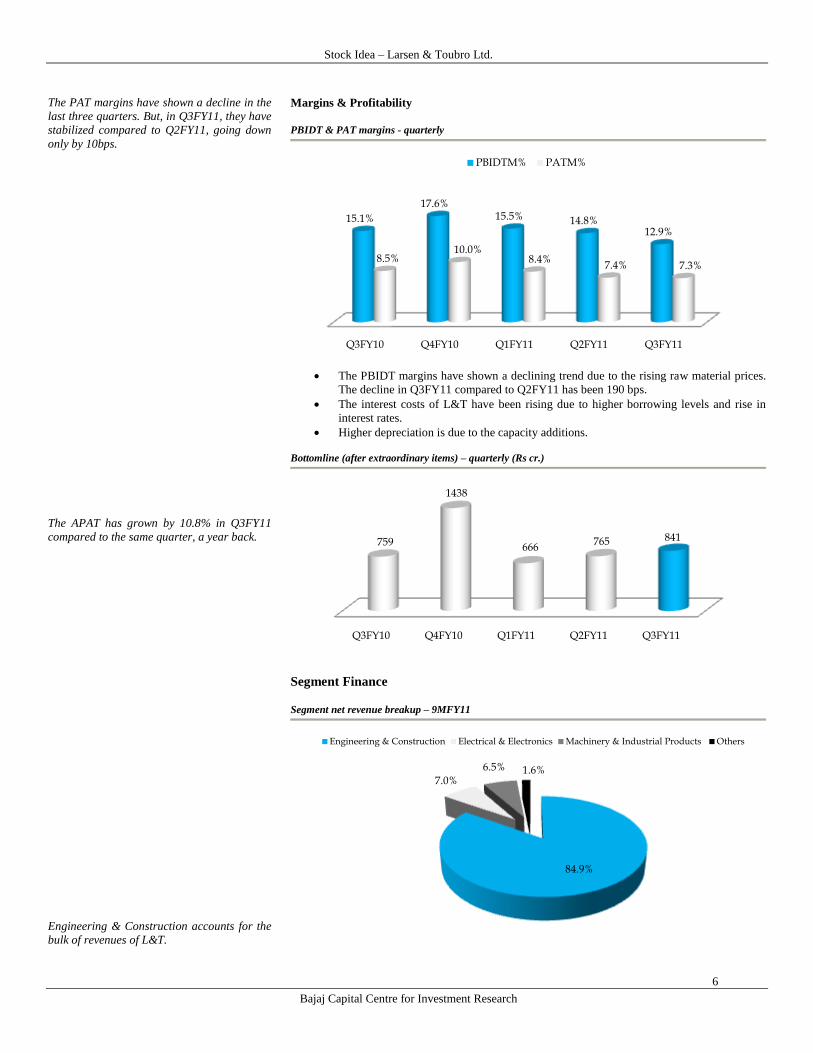

The PAT margins have shown a decline in the

last three quarters. But, in Q3FY11, they have

stabilized compared to Q2FY11, going down

only by 10bps.

The APAT has grown by 10.8% in Q3FY11

compared to the same quarter, a year back.

Engineering & Construction accounts for the

bulk of revenues of L&T.

Margins & Profitability

PBIDT & PAT margins - quarterly

The PBIDT margins have shown a declining trend due to the rising raw material prices.

The decline in Q3FY11 compared to Q2FY11 has been 190 bps.

The interest costs of L&T have been rising due to higher borrowing levels and rise in

interest rates.

Higher depreciation is due to the capacity additions.

Bottomline (after extraordinary items) – quarterly (Rs cr.)

Segment Finance

Segment net revenue breakup – 9MFY11

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

15.1%

17.6%15.5% 14.8%

12.9%

8.5%10.0%

8.4%7.4% 7.3%

PBIDTM% PATM%

Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11

759

1438

666765 841

84.9%

7.0%

6.5% 1.6%

Engineering & Construction Electrical & Electronics Machinery & Industrial Products Others

Stock Idea – Larsen & Toubro Ltd.

7

Bajaj Capital Centre for Investment Research

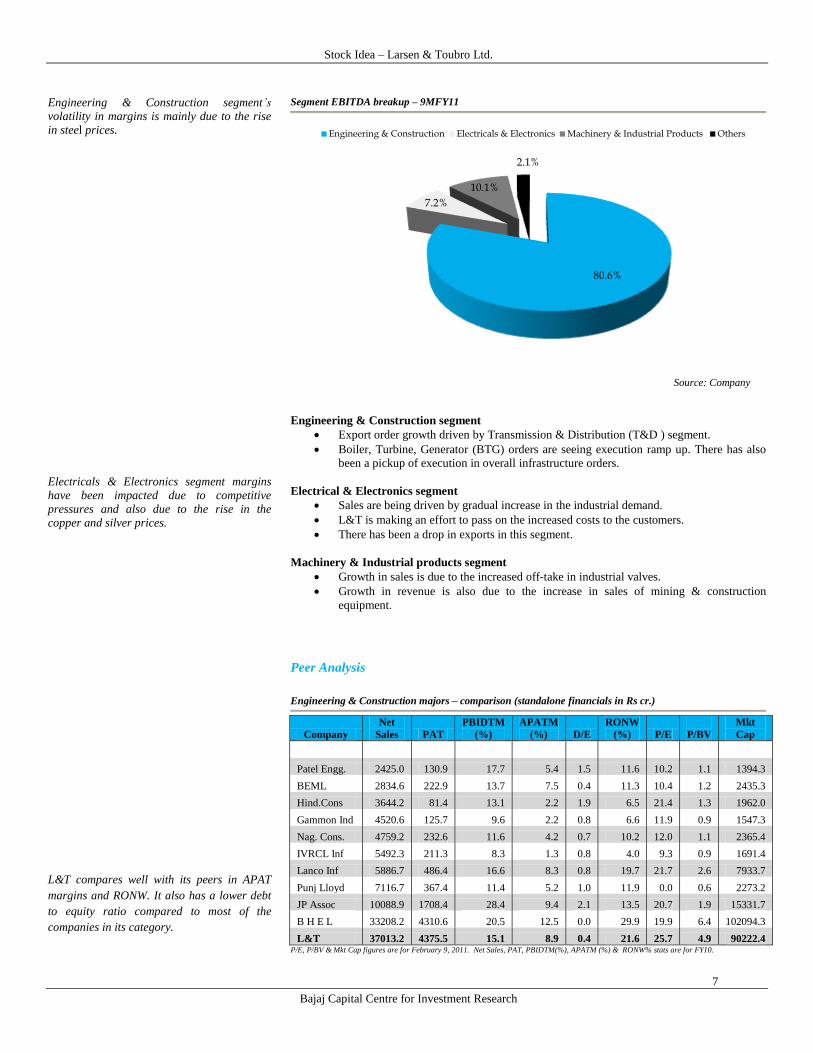

Engineering & Construction segment’s

volatility in margins is mainly due to the rise

in steel prices.

Electricals & Electronics segment margins

have been impacted due to competitive

pressures and also due to the rise in the

copper and silver prices.

L&T compares well with its peers in APAT

margins and RONW. It also has a lower debt

to equity ratio compared to most of the

companies in its category.

Segment EBITDA breakup – 9MFY11

Source: Company

Engineering & Construction segment

Export order growth driven by Transmission & Distribution (T&D ) segment.

Boiler, Turbine, Generator (BTG) orders are seeing execution ramp up. There has also

been a pickup of execution in overall infrastructure orders.

Electrical & Electronics segment

Sales are being driven by gradual increase in the industrial demand.

L&T is making an effort to pass on the increased costs to the customers.

There has been a drop in exports in this segment.

Machinery & Industrial products segment

Growth in sales is due to the increased off-take in industrial valves.

Growth in revenue is also due to the increase in sales of mining & construction

equipment.

Peer Analysis

Engineering & Construction majors – comparison (standalone financials in Rs cr.)

Company

Net

Sales PAT

PBIDTM

(%)

APATM

(%) D/E

RONW

(%) P/E

P/BV

Mkt

Cap

Patel Engg. 2425.0 130.9 17.7 5.4 1.5 11.6 10.2 1.1 1394.3

BEML 2834.6 222.9 13.7 7.5 0.4 11.3 10.4 1.2 2435.3

Hind.Cons 3644.2 81.4 13.1 2.2 1.9 6.5 21.4 1.3 1962.0

Gammon Ind 4520.6 125.7 9.6 2.2 0.8 6.6 11.9 0.9 1547.3

Nag. Cons. 4759.2 232.6 11.6 4.2 0.7 10.2 12.0 1.1 2365.4

IVRCL Inf 5492.3 211.3 8.3 1.3 0.8 4.0 9.3 0.9 1691.4

Lanco Inf 5886.7 486.4 16.6 8.3 0.8 19.7 21.7 2.6 7933.7

Punj Lloyd 7116.7 367.4 11.4 5.2 1.0 11.9 0.0 0.6 2273.2

JP Assoc 10088.9 1708.4 28.4 9.4 2.1 13.5 20.7 1.9 15331.7

B H E L 33208.2 4310.6 20.5 12.5 0.0 29.9 19.9 6.4 102094.3

L&T 37013.2 4375.5 15.1 8.9 0.4 21.6 25.7 4.9 90222.4 P/E, P/BV & Mkt Cap figures are for February 9, 2011. Net Sales, PAT, PBIDTM(%), APATM (%) & RONW% stats are for FY10.

80.6%

7.2%

10.1%

2.1%

Engineering & Construction Electricals & Electronics Machinery & Industrial Products Others

Stock Idea – Larsen & Toubro Ltd.

8

Bajaj Capital Centre for Investment Research

As L&T has 6% of their order book from

Middle –East , the evolving political situation

over there might hamper its business in these

countries.

Decision making in the hydrocarbon segment

has been slow and tardy at the very best in

terms of the overall projects in the space.

Also, L&T has been facing tough competition

from the foreigners especially the Koreans in

this field.

Given the scale of execution by L&T, any

delay in executing the projects would have an

adverse impact on the company’s finances.

Key Concerns

Economic slowdown

L&T covers the entire physical infrastructure field and thus is totally linked to the India growth

story. So, a slowdown of the Indian economy would automatically lead to a slowdown of the

company’s growth prospects.

Political instability

In 9MFY11, 46% of L&T’s customers have been from the government sector including PSU’s. So

any political instability or delay in awarding of projects could hamper the company’s growth

prospects.

Escalating raw material prices to hit margins

Rising prices of commodities like steel, copper, aluminium, cement etc. are bound to increase costs

and thus affect the margins of L&T negatively.

Increase in interest rates

The increase in interest rates is not good news for a company like L&T that is involved in building

the country’s infrastructure, as it means borrowing at higher rates that would impact its PAT

margins negatively.

Conclusion

L&T being the largest company in the Engineering/Construction/Infrastructure sector has a big

role to play in the coming years as India plans to revamp its Infrastrcuture drastically, to make sure

that its economy has a stable high single digit or even double digit GDP growth. The government

of India, realizing the acute necessity of improving the infrastructure is expected to take the

infrastructure spending to 9% of the GDP in FY12. L&T is taking a major restructuring exercise

where it is dividing the company into 9 separate profit centres. These divisions are going to be

listed in due time leading to value unlocking for the shareholders. L&T has geared up for the

massive need for power equipment in the coming years with the commissioning of its BTG facility

in Gujarat. In the field of nuclear power, the government of India plans awarding 100,000 cr. of

projects in the next 5 years. L&T has signed agreements with major nuclear equipment

manufacturers around the world to cater to this demand. In the long run, the company is planning

to develop its own nuclear power plants. After the success of the Delhi Metro, similar projects are

being planned in major Indian cities. L&T has already bagged the Mumbai mono rail project and is

the frontrunner for the Ahmedabad old city mono rail project. It also has the Hyderabad metro rail

project in its bag. Dhamra port, a 50:50 JV with Tata steel is going to provide L&T with revenues

for at least 30 years. With Dhamra being one of the deepest ports in India and a lot of steel plants

located in the vicinity, the port has good prospects. The current orderbook of the company stands

at Rs 1,15,400 cr.which is ~2.6 times its FY10 sales. L&T also has plans to open its own bank in

the near future.

L&T has a market capitalization of Rs 99799.6 cr. and is trading at a share price of Rs. 1639.15.

The consolidated TTM EPS is Rs. 87.2 translating into a TTM PE of 18.8. The price to book value

stands at 4.8. The stock is an attractive buy considering the growth prospects of the industry as

well as the company.

We recommend a “BUY” on the stock with an investment horizon of 12 months and target

price of Rs. 2000.

Stock Idea – Larsen & Toubro Ltd.

9

Bajaj Capital Centre for Investment Research

SWOT Analysis

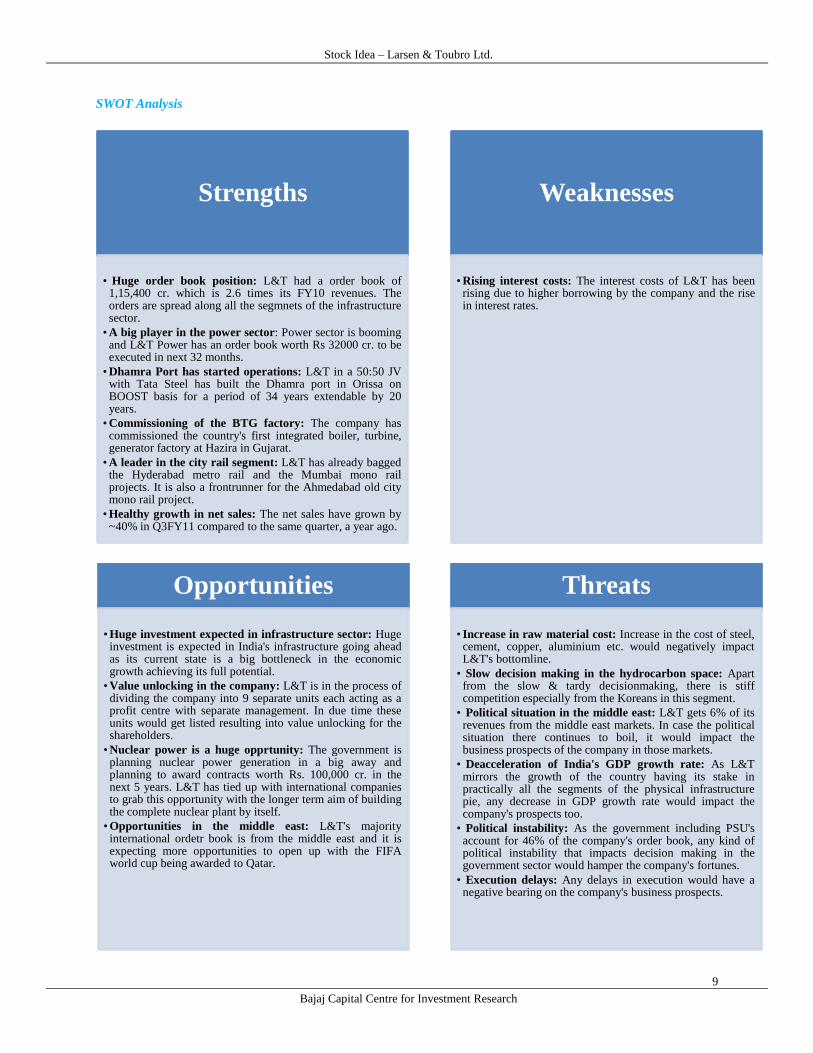

Strengths

• Huge order book position: L&T had a order book of1,15,400 cr. which is 2.6 times its FY10 revenues. Theorders are spread along all the segmnets of the infrastructuresector.

• A big player in the power sector: Power sector is boomingand L&T Power has an order book worth Rs 32000 cr. to beexecuted in next 32 months.

• Dhamra Port has started operations: L&T in a 50:50 JVwith Tata Steel has built the Dhamra port in Orissa onBOOST basis for a period of 34 years extendable by 20years.

• Commissioning of the BTG factory: The company hascommissioned the country's first integrated boiler, turbine,generator factory at Hazira in Gujarat.

• A leader in the city rail segment: L&T has already baggedthe Hyderabad metro rail and the Mumbai mono railprojects. It is also a frontrunner for the Ahmedabad old citymono rail project.

• Healthy growth in net sales: The net sales have grown by~40% in Q3FY11 compared to the same quarter, a year ago.

Weaknesses

• Rising interest costs: The interest costs of L&T has beenrising due to higher borrowing by the company and the risein interest rates.

Opportunities

• Huge investment expected in infrastructure sector: Hugeinvestment is expected in India's infrastructure going aheadas its current state is a big bottleneck in the economicgrowth achieving its full potential.

• Value unlocking in the company: L&T is in the process ofdividing the company into 9 separate units each acting as aprofit centre with separate management. In due time theseunits would get listed resulting into value unlocking for theshareholders.

• Nuclear power is a huge opprtunity: The government isplanning nuclear power generation in a big away andplanning to award contracts worth Rs. 100,000 cr. in thenext 5 years. L&T has tied up with international companiesto grab this opportunity with the longer term aim of buildingthe complete nuclear plant by itself.

• Opportunities in the middle east: L&T's majorityinternational ordetr book is from the middle east and it isexpecting more opportunities to open up with the FIFAworld cup being awarded to Qatar.

Threats

• Increase in raw material cost: Increase in the cost of steel,cement, copper, aluminium etc. would negatively impactL&T's bottomline.

• Slow decision making in the hydrocarbon space: Apartfrom the slow & tardy decisionmaking, there is stiffcompetition especially from the Koreans in this segment.

• Political situation in the middle east: L&T gets 6% of itsrevenues from the middle east markets. In case the politicalsituation there continues to boil, it would impact thebusiness prospects of the company in those markets.

• Deacceleration of India's GDP growth rate: As L&Tmirrors the growth of the country having its stake inpractically all the segments of the physical infrastructurepie, any decrease in GDP growth rate would impact thecompany's prospects too.

• Political instability: As the government including PSU'saccount for 46% of the company's order book, any kind ofpolitical instability that impacts decision making in thegovernment sector would hamper the company's fortunes.

• Execution delays: Any delays in execution would have anegative bearing on the company's business prospects.

Stock Idea – Larsen & Toubro Ltd.

10

Bajaj Capital Centre for Investment Research

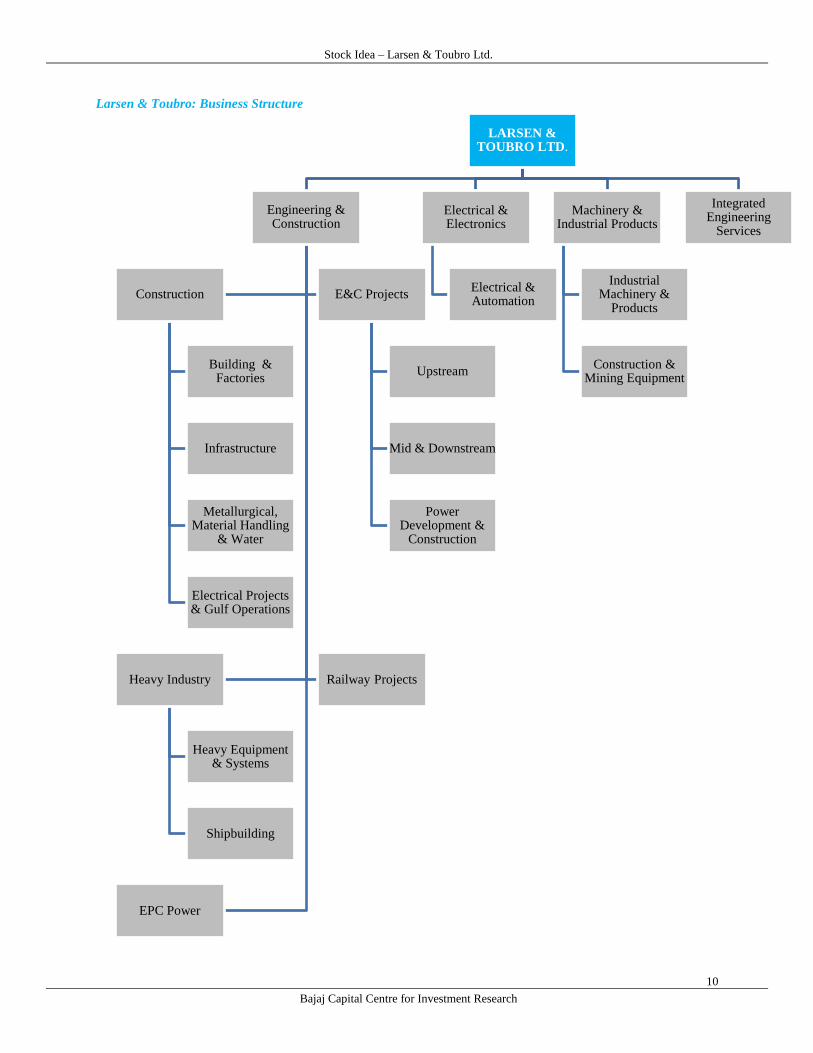

Larsen & Toubro: Business Structure

LARSEN & TOUBRO LTD.

Engineering & Construction

Construction

Building & Factories

Infrastructure

Metallurgical, Material Handling

& Water

Electrical Projects & Gulf Operations

E&C Projects

Upstream

Mid & Downstream

Power Development &

Construction

Heavy Industry

Heavy Equipment & Systems

Shipbuilding

Railway Projects

EPC Power

Electrical & Electronics

Electrical & Automation

Machinery & Industrial Products

Industrial Machinery &

Products

Construction & Mining Equipment

Integrated Engineering

Services

Stock Idea – Larsen & Toubro Ltd.

11

Bajaj Capital Centre for Investment Research

Financials

Income Statement (Quarterly): Standalone

Rs. Cr.

Particulars Q3FY11 Q2FY11 Q3FY10 QoQ (%) YoY (%)

Net Sales 11321.7 9260.8 8071.4 22.3 40.3

Total Income 11660.3 9713.0 8379.3 20.0 39.2

Total Expenditure 10175.2 8325.1 7138.8 22.2 42.5

PBIDT 1485.1 1387.9 1240.5 7.0 19.7

PBIDT Margin % 13.1 15.0 15.4

Interest 175.7 193.2 133.9 -9.0 31.2

Depreciation 128.1 121.2 104.5 5.7 22.6

Tax 376.0 379.4 305.8 -0.9 23.0

APAT 840.5 765.0 758.8 9.9 10.8

APATM (%) 7.4 8.3 9.4

Financials (Annual):Consolidated

Rs. Cr.

9MFY11

(Standalone) 201003 200903 200803 200703 200603 200503

5 yr CAGR

%

Share Capital 121.8 120.4 117.1 58.5 56.7 27.5 26.0

Networth 20611.0 13682.8 10632.4 6797.1 4876.1 3216.1

Capital Employed

46655.0 35383.9 24015.2 13954.5 8516.4 6802.9

Debt 24607.3 20370.0 12315.9 6432.2 3498.7 3453.8

CWIP

6618.4 6205.4 3053.1 1455.3 426.6 176.3

Inventory 2378.2 2501.7 5019.0 3678.0 2477.4 2449.6

Sundry Debtors

12528.0 11491.1 8234.4 6110.4 5282.3 4315.8

Cash & Bank Balance 3321.6 1459.0 1560.8 1718.0 816.0 988.2

Revenues 28417.5 43969.8 40511.1 29456.9 20512.9 16561.3 14496.9 24.8

Total Income 29485.3 46594.3 41178.7 29882.0 21406.6 17076.9 15075.0 25.3

Total Expenditure 25378.5 36749.5 34845.4 25327.9 17705.3 14847.1 13213.0 22.7

PBIDT 4106.8 9844.9 6333.2 4554.1 3701.3 2229.8 1862.0 39.5

Interest 511.2 1520.2 1244.6 625.7 351.4 318.0 244.6 44.1

Depreciation 363.5 979.3 728.3 509.7 344.9 243.5 212.2 35.8

APAT 2176.8 3845.3 2924.3 2231.9 1800.0 1017.4 760.2 38.3

Cash Flow from Operating Activities 2117.8 496.0 -1239.2 2324.4 1061.7 353.7

Cash Flow from Investing Activities

-5107.8 -5076.9 -6615.3 -2562.5 -1353.8 -83.8

Cash Flow from Financing Activities 4880.8 4479.2 7697.3 1140.1 119.8 184.4

Free Cash Flows

-2989.9 -4580.9 -7854.6 -238.1 -292.0 269.9

Dividend % 625.0 525.0 850.0 650.0 1100.0 1375.0

EPS (Rs.) 36.4 88.3 51.5 39.8 39.5 22.7 20.2

Debt-Equity Ratio 1.3 1.3 1.1 0.9 0.9 1.1

RoNW %

31.0 24.1 26.1 38.9 30.6 39.0

Total Asset Turnover Ratio 0.7 0.8 0.9 1.0 1.1 1.2

Fixed Asset Turnover Ratio

3.1 4.0 4.3 4.0 4.2 4.0

PBIDT Margin % 14.5 22.4 15.6 15.5 18.0 13.5 12.8

APAT Margin % 7.7 8.7 7.2 7.6 8.8 6.1 5.2

Stock Idea – Larsen & Toubro Ltd.

12

Bajaj Capital Centre for Investment Research

Disclaimer:

This document has been prepared by Bajaj Capital Centre for Investment Research (BCCIR), a unit of Bajaj Capital Limited (BCL). BCL and its subsidiaries

and associated companies form an integrated unit imparting investment banking, investment advisory and brokerage services in stocks, mutual funds, debt,

real estate, personal finance etc. Our research analysts and sales persons provide important input into our investment banking and advisory activities.

This document does not constitute an offer or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any

transaction.

The information contained herein is from publicly available data or other sources believed to be reliable. We do not represent that information contained

herein is accurate or complete and it should not be relied upon as such. This document is prepared for assistance only and is not intended to be and must not

alone be taken as the basis for an investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document

should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in

this document (including the merits and risks involved). The investment discussed or views expressed may not be suitable for all investors.

Affiliates of BCL may have issued other reports that are inconsistent with and reach to a different conclusion from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state,

country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject BCL and

affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all

jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe

such restriction.

BCL & affiliates may have used the information set forth herein before publication and may have positions in, may from time to time purchase or sell or may

be materially interested in any of the securities mentioned or related securities. BCL and affiliates may from time to time solicit from, or perform investment

banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall BCL, any of its affiliates or any third

party involved in, or related to, computing or compiling the information have any liability for any damages of any kind. Any comments or statements made

herein are those of the analyst and do not necessarily reflect those of BCL and affiliates.

This Document is subject to changes without prior notice and is intended only for the person or entity to which it is addressed and may contain confidential

and/or privileged material and is not for any type of circulation. Any review, retransmission, or any other use is prohibited.

Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. BCL will not treat recipients as

customers by virtue of their receiving this report.

Disclosure of interest:

1. BCL and its affiliates have not received compensation from the company covered herein in the past twelve months for Issue Management, Capital

Structure, Mergers & Acquisitions, Buyback of shares and other corporate advisory services.

2. Affiliates of BCL are currently not having any mandate from the subject company.

3. BCL and its affiliates do not hold paid up capital of the company.

4. The Equity Analyst and his/her relatives/dependents hold no shares of the company covered as on the date of publication of research on the subject

company.

© Copyright in this document vests exclusively with BCL.

Bajaj Capital Centre for Investment Research

Bajaj Capital Ltd

97, Bajaj House, Nehru Place

New Delhi 110019

Tel 4169 3000, 4169 2900, Ext. 651

Email: [email protected]