latam bbva latam footprint - bbvaresearch.com · introduction ... fx swaps source: bis, triennial...

TRANSCRIPT

PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES ON PAGE 26 OF THIS REPORT This document has been produced by BBVA Bancomer, S.A., Institución de Banca Múltiple, Grupo Financiero BBVA BancomerFor further information please contact the areas listed in this document. No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.

Mexico 2010

BBVA Latam FootprintLatam

• Foreign Exchange Market

• Fixed Income Market

• Interest Rate Derivatives

• Equity

PAGE 2

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Contents

Introduction ......................................................................................................................3

Latin America in Context..............................................................................4

BBVA Capabilities ..................................................................................................7

Most used instruments ...................................................................................8

Argentina at a glance......................................................................................12

Brazil at a glance ..................................................................................................14

Chile at a glance ....................................................................................................16

Colombia at a glance ......................................................................................18

Mexico at a glance..............................................................................................19

Peru at a glance .....................................................................................................23

PAGE 3

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

IntroductionAs part of an ongoing effort to better serve its broad client base across the Globe, BBVA presents you the fi rst edition of its Latin American Footprint, a general introduction to the most popular Fixed Income and FX instruments as well as a brief overview of BBVA’s vast capabilities and strong presence in the region.

BBVA’s Global Markets, and its Trading, Sales, Structuring and Research subdivisions will gladly assist you in tailoring the strategies that best suit your investment or hedging needs in Latin America. We sincerely hope this publication contributes to this task.

PAGE 4

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

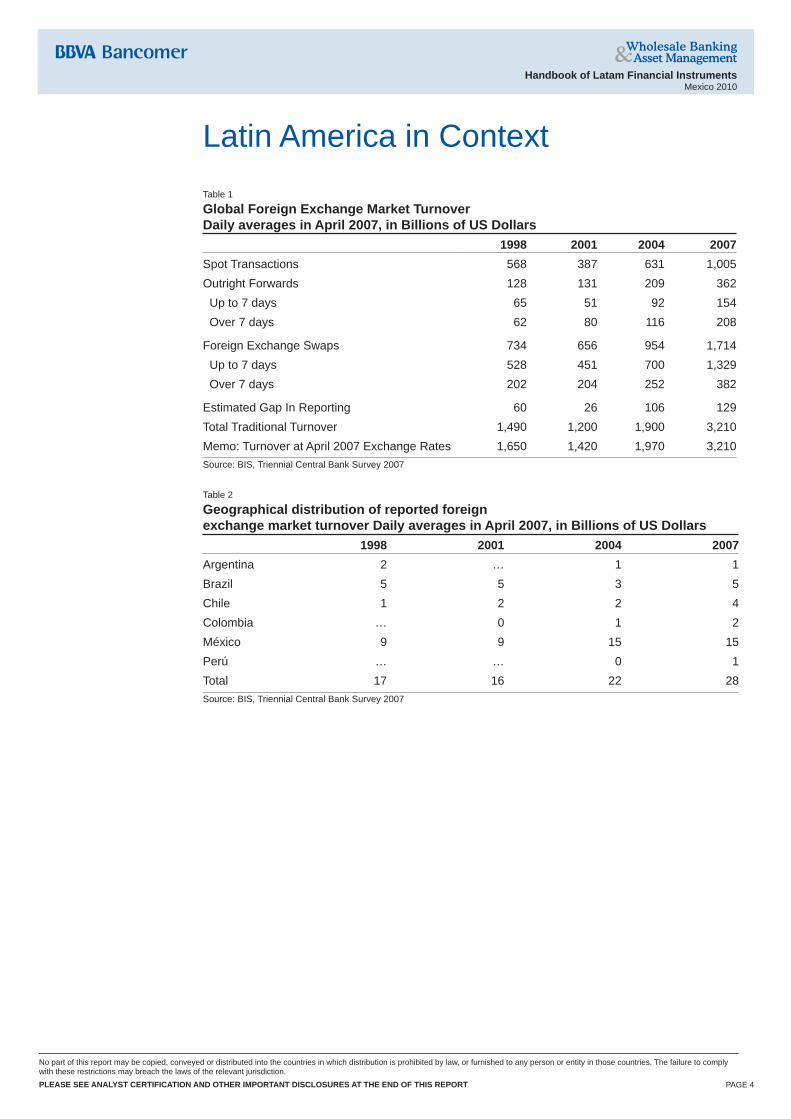

Latin America in ContextTable 1

Global Foreign Exchange Market Turnover Daily averages in April 2007, in Billions of US Dollars 1998 2001 2004 2007Spot Transactions 568 387 631 1,005Outright Forwards 128 131 209 362 Up to 7 days 65 51 92 154 Over 7 days 62 80 116 208

Foreign Exchange Swaps 734 656 954 1,714 Up to 7 days 528 451 700 1,329 Over 7 days 202 204 252 382

Estimated Gap In Reporting 60 26 106 129Total Traditional Turnover 1,490 1,200 1,900 3,210Memo: Turnover at April 2007 Exchange Rates 1,650 1,420 1,970 3,210Source: BIS, Triennial Central Bank Survey 2007

Table 2

Geographical distribution of reported foreign exchange market turnover Daily averages in April 2007, in Billions of US Dollars 1998 2001 2004 2007Argentina 2 … 1 1Brazil 5 5 3 5Chile 1 2 2 4Colombia … 0 1 2México 9 9 15 15Perú … … 0 1Total 17 16 22 28Source: BIS, Triennial Central Bank Survey 2007

PAGE 5

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

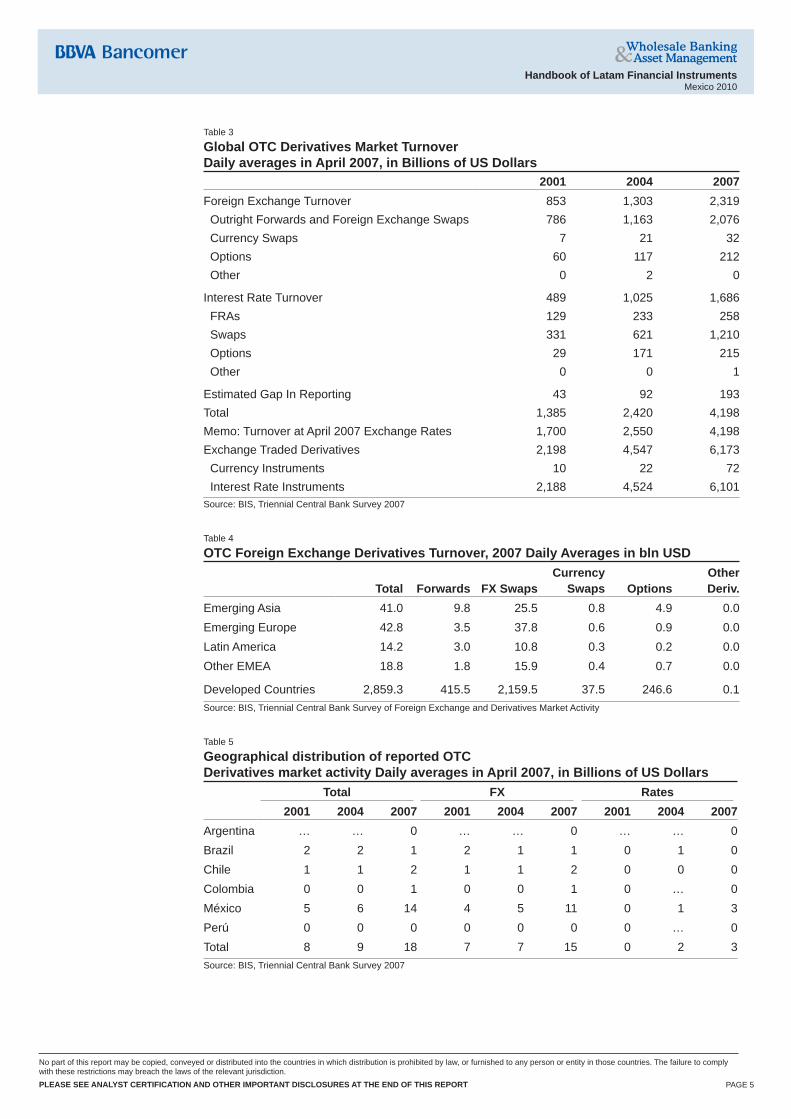

Table 3

Global OTC Derivatives Market Turnover Daily averages in April 2007, in Billions of US Dollars 2001 2004 2007Foreign Exchange Turnover 853 1,303 2,319 Outright Forwards and Foreign Exchange Swaps 786 1,163 2,076 Currency Swaps 7 21 32 Options 60 117 212 Other 0 2 0

Interest Rate Turnover 489 1,025 1,686 FRAs 129 233 258 Swaps 331 621 1,210 Options 29 171 215 Other 0 0 1

Estimated Gap In Reporting 43 92 193Total 1,385 2,420 4,198Memo: Turnover at April 2007 Exchange Rates 1,700 2,550 4,198Exchange Traded Derivatives 2,198 4,547 6,173 Currency Instruments 10 22 72 Interest Rate Instruments 2,188 4,524 6,101Source: BIS, Triennial Central Bank Survey 2007

Table 4

OTC Foreign Exchange Derivatives Turnover, 2007 Daily Averages in bln USD

Total Forwards FX SwapsCurrency

Swaps OptionsOther Deriv.

Emerging Asia 41.0 9.8 25.5 0.8 4.9 0.0Emerging Europe 42.8 3.5 37.8 0.6 0.9 0.0Latin America 14.2 3.0 10.8 0.3 0.2 0.0Other EMEA 18.8 1.8 15.9 0.4 0.7 0.0

Developed Countries 2,859.3 415.5 2,159.5 37.5 246.6 0.1Source: BIS, Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity

Table 5

Geographical distribution of reported OTC Derivatives market activity Daily averages in April 2007, in Billions of US Dollars

Total FX Rates 2001 2004 2007 2001 2004 2007 2001 2004 2007

Argentina … … 0 … … 0 … … 0Brazil 2 2 1 2 1 1 0 1 0Chile 1 1 2 1 1 2 0 0 0Colombia 0 0 1 0 0 1 0 … 0México 5 6 14 4 5 11 0 1 3Perú 0 0 0 0 0 0 0 … 0Total 8 9 18 7 7 15 0 2 3Source: BIS, Triennial Central Bank Survey 2007

PAGE 6

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

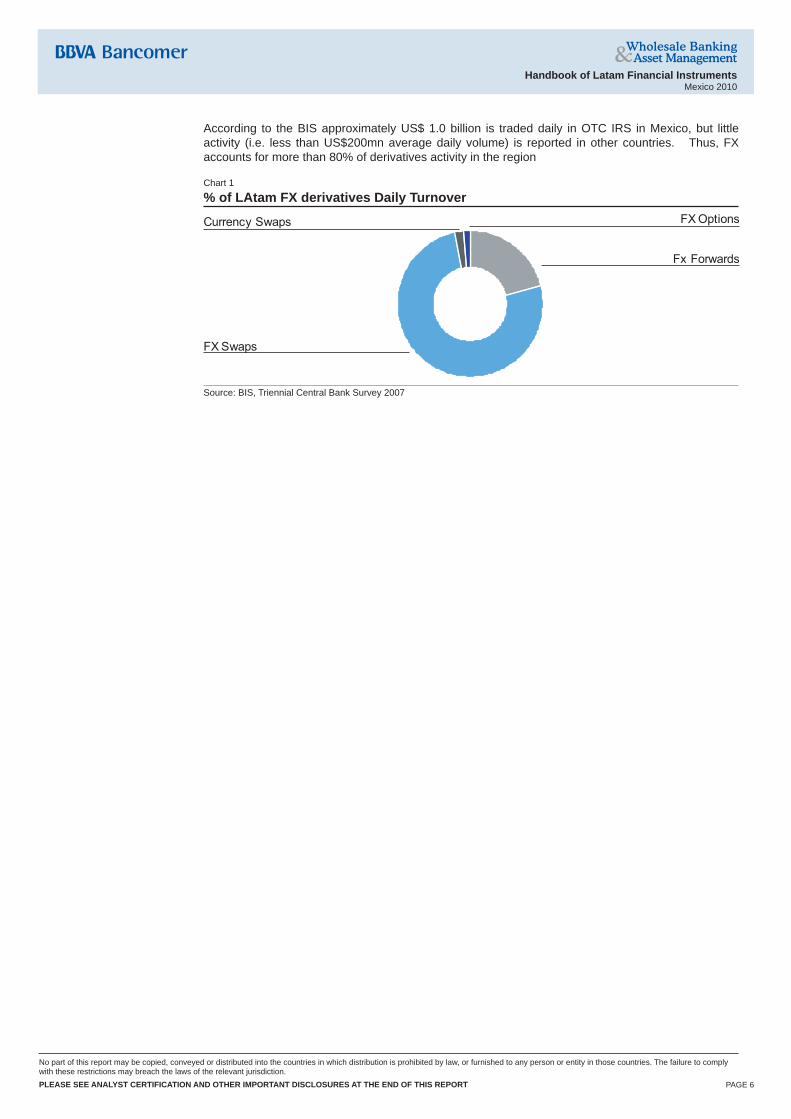

According to the BIS approximately US$ 1.0 billion is traded daily in OTC IRS in Mexico, but little activity (i.e. less than US$200mn average daily volume) is reported in other countries. Thus, FX accounts for more than 80% of derivatives activity in the region

Chart 1

% of LAtam FX derivatives Daily TurnoverFX OptionsCurrency Swaps

Fx Forwards

FX Swaps

Source: BIS, Triennial Central Bank Survey 2007

PAGE 7

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

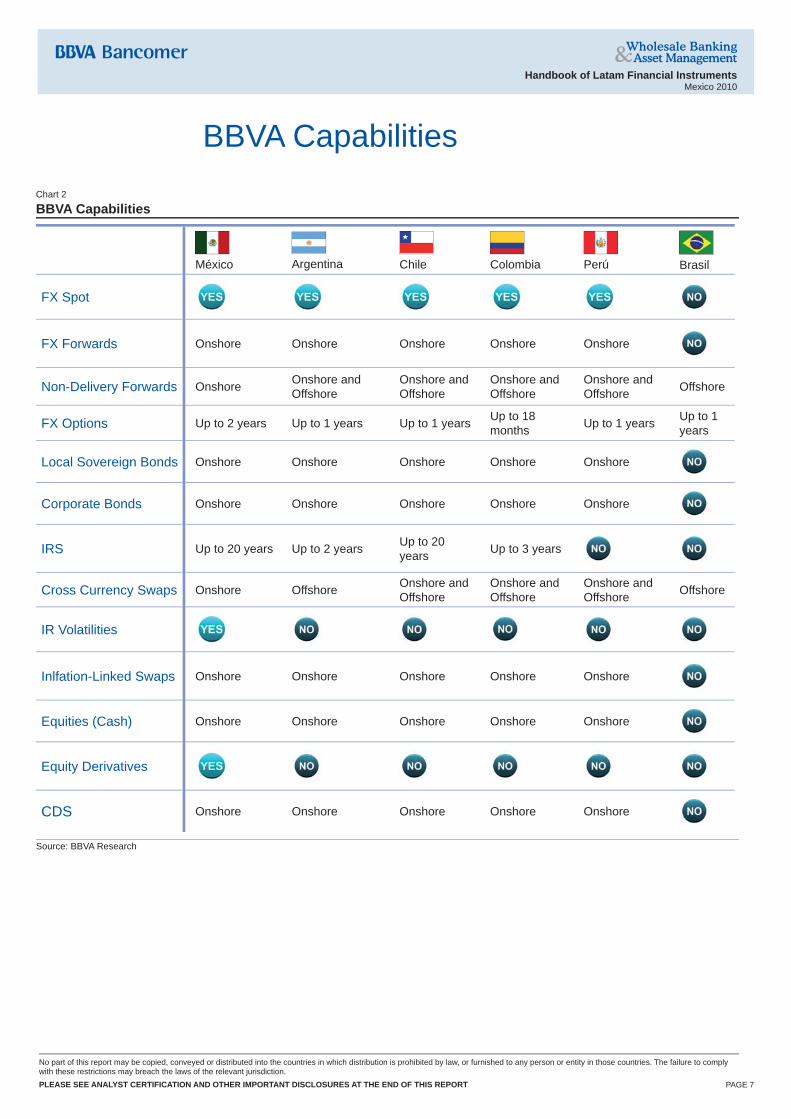

BBVA CapabilitiesChart 2

BBVA Capabilities

México

Argentina

Chile

Colombia

Perú

Brasil

FX Spot

FX Forwards Onshore Onshore Onshore Onshore Onshore

Non-Delivery Forwards Onshore Onshore and Offshore

Onshore and Offshore

Onshore and Offshore

Onshore and Offshore Offshore

FX Options Up to 2 years Up to 1 years Up to 1 years Up to 18 months Up to 1 years Up to 1

years

Local Sovereign Bonds Onshore Onshore Onshore Onshore Onshore

Corporate Bonds Onshore Onshore Onshore Onshore Onshore

IRS Up to 20 years Up to 2 years Up to 20 years Up to 3 years

Cross Currency Swaps Onshore Offshore Onshore and Offshore

Onshore and Offshore

Onshore and Offshore Offshore

IR Volatilities

Inlfation-Linked Swaps Onshore Onshore Onshore Onshore Onshore

Equities (Cash) Onshore Onshore Onshore Onshore Onshore

Equity Derivatives

CDS Onshore Onshore Onshore Onshore Onshore

Source: BBVA Research

PAGE 8

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Most used instruments

Dollar Forwards and Non Deliverable Forwards (NDF)This derivative instrument eliminates exchange risk by protecting against currencies’ depreciation or appreciation against the dollar. Deliverable forwards guarantee physical delivery of foreign currency. Non-deliverable forwards are cash-settled.

Advantages for customers in using dollar forwards

General CharacteristicsExchange rate: the forward exchange rate is calculated based on the spot date exchange rate (48 hours value) of a foreign currency against the dollar plus some basis points (forward points). The basis points are determined in line with the following factors:

a. Interest rate differential between local currency and USD – Formula (1).

b. Market expectations with respect to prevailing cash exchange rates in the future

Formula 1

FXspottenorRusd

tenorR

*

3601

360$1

rate exchange Fwd

where:R$ = Domestic risk-free rate.Rusd = USD Risk-free rate.tenor = Period of reference interest rate and forward contract.FXSpot = spot exchange rate (48 hours value date)

Indicative References: we have our own Bloomberg page with indicative prices on LATAM NDFs which is BCMR7. In it you’ll be able to fi nd the indicative bid-offer for the spot and indicative forward points up to 2y.

Chart 3

BBVA Bancomer Bloomberg Page

Source: BBVA Research

PAGE 9

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

FX Options (OTC)Derivative instrument for protection against currency appreciation/depreciation, with which the buyer acquires the right, but not the obligation, to purchase (call option) or sell (put option) USD on a future date(s), at a price specifi ed in advance (strike) in return for payment of a premium. When the option is exercised, the operation may be physically delivered or settled either in USD or MXN.

Types of operation

a) Call optionsPurchase of a call: The customer buys the right to buy USD versus local currency (BRL in the example) at an agreed strike price on a specifi ed date in exchange for an option price (premium).

Sale of a call: The customer sells the right to buy USDat an agreed strike price on a specifi ed date in exchange for an option price (premium). Hence, he receives the premium but he is obliged to sell USD in case the option holder decides to exercise it.

Chart 4

Payoff Profi le of a Call Option+ Profit

- Loss

S

S*=$1

Option price=$0.3474

-

Source: BBVA Research

b) Put optionsPurchase of a put: The customer buys the right to sell USD against local currency (BRL in the example) at an agreed strike price on a specifi ed date in exchange for an option price (premium).

Sale of a put: The customer sells the right to sell USD at an agreed strike price on a specifi ed date in exchange for an option price (premium). Hence, he receives the premium but he is obliged to buy USD in case the option holder decides to exercise it.

Chart 5

Payoff Profi le of a Put Option + Profit

- Loss

S

Option price=$0.3474

- Loss

S

S*=$1.71

Source: BBVA Research

PAGE 10

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

FX swaps

Defi nition

Exchange operations which enable customers to obtain fi nancing or perform investments in either pesos or dollars in short term periods by simultaneously buying and selling the same amount of one currency with different maturity dates.

The main advantages are permitting synthetic investment in USD or domestic currency, in line with customer requirements; and permitting synthetic fi nancing (funding) of a position in dollars or domestic currency.

Classifi cation

• Cash-Tom: Sale/purchase of currency today and purchase/sale in 24 hours (Tom=tomorrow)

• Cash-Spot: Sale/purchase of currency today and purchase/sale in 48 hours

• Tom-Next: Sale/purchase of currency in 24 hours and purchase/sale in 48 hours

Formula

DDR

SFR USDMex

3601360

1

DDR

FSR MexUSD

3601360

1

Implicit interest rates in Local Currency (MXN in the example) and dollars:Where:Rmex = Domestic currencyF = Final exchange rate = Initial exchange rate plus swap points.S = Initial exchange rate.Rusd = Interest rate in USD.D = Contract period in days

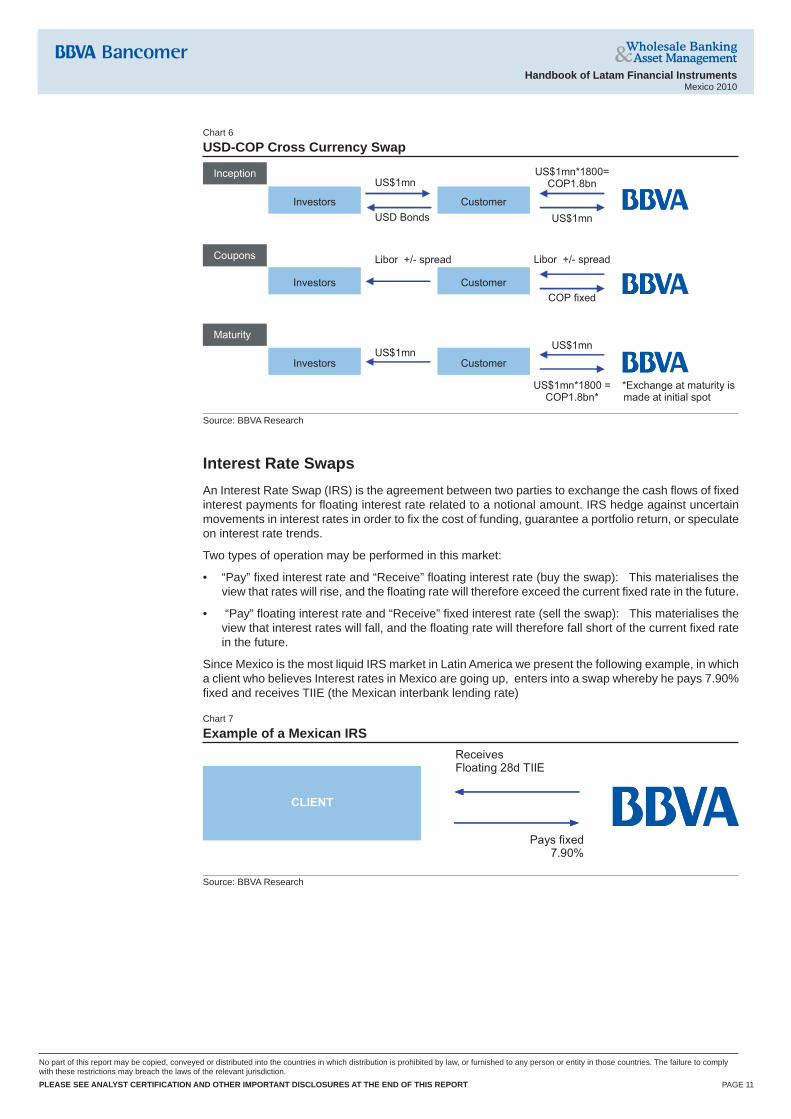

Cross currency Swaps

Defi nitionCross currency swaps (CCS) involve the exchange of a series of cash fl ows in one currency, for a series of payments in another currency. The conditions and frequency of swap payments are agreed in advance by the parties. The CCS may be set at a fi xed rate for fi xed rate, fi xed for fl oating (and vice-versa) or fl oating for fl oating. In recent years, there has been increasing demand for this type of operation. They allow the substitution of debt fl ows (principal and/or interest payments) from one currency to another and even from one interest rate type to another (fi xed for fl oating and vice-versa). This type of swaps are generally transacted OTC (over the counter), i.e. between counterparties, since they are contracts tailored to customers’ requirements. When CCS are traded, the buyer and seller agree on the “reference amount”, the “number of coupons”, the “maturity date” of the operation, Notional amounts, exchanges of the principal, amortizations (where applicable), etc.

As an example, consider the following case. A Colombian corporation issues a USD Bond referenced to Libor, but wants to hedge the FX risk. The company enters into a swap whereby it pays COP fi xed and receives US Libor.

PAGE 11

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Chart 6

USD-COP Cross Currency Swap

Customer Investors

Libor +/- spread

Customer US$1mn

US$1mn*1800=COP1.8bn

Investors

Customer

US$1mn

Investors

COP fixed

US$1mn*1800 =COP1.8bn* *Exchange at maturity is

made at initial spot

US$1mn

US$1mn Inception

Coupons

Maturity

USD Bonds

Libor +/- spread

Source: BBVA Research

Interest Rate SwapsAn Interest Rate Swap (IRS) is the agreement between two parties to exchange the cash fl ows of fi xed interest payments for fl oating interest rate related to a notional amount. IRS hedge against uncertain movements in interest rates in order to fi x the cost of funding, guarantee a portfolio return, or speculate on interest rate trends.

Two types of operation may be performed in this market:

• “Pay” fi xed interest rate and “Receive” fl oating interest rate (buy the swap): This materialises the view that rates will rise, and the fl oating rate will therefore exceed the current fi xed rate in the future.

• “Pay” fl oating interest rate and “Receive” fi xed interest rate (sell the swap): This materialises the view that interest rates will fall, and the fl oating rate will therefore fall short of the current fi xed rate in the future.

Since Mexico is the most liquid IRS market in Latin America we present the following example, in which a client who believes Interest rates in Mexico are going up, enters into a swap whereby he pays 7.90% fi xed and receives TIIE (the Mexican interbank lending rate)

Chart 7

Example of a Mexican IRSReceives Floating 28d TIIE

Pays fixed7.90%

CLIENT

Source: BBVA Research

PAGE 12

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Argentina at a glanceBBVA is active in the following products:

• Onshore NDF up to 1.5 years

• Offshore FX options up to 1y

• CCS Swaps up to 2y

• Government bonds and Repos

• Corporate bonds and Repos

• Fixed income forwards

• Interest Rate Futures

• Credit Default Swaps

• Short-term interest rate swaps

• Infl ation-linked swaps

• Equities (cash)

Main characteristics of the FX market:

• The conventional market quotation is the number of pesos per US dollar.

• Free fl otation. The currency regime is a managed fl oat. The market trades spot onshore with delivery of ARS and non delivery forwards in the offshore market

• Regulated Convertibility. The physical conversion of ARS into other currencies is regulated and not freely done.

• FX Spot Average Daily Volume is USD 616 million.

• FX Forward Offshore Average Daily Volume is USD 150-220 million.

• The market trades onshore on local Argentine time and offshore during the 9:00 – 14:00 New York time.

Main Characteristics of the Fixed Income Market

• The main government securities are LEBAC (Letra de banco Central de la República Argentina), which are zero-coupon, ARS denominated, short-term discounted bills, and NOBAC (Nota de banco Central de la República Argentina), Which are medium and long term (up to 23 yrs), fi xed or fl oating (referred to BADLAR or CER –see below-) government securities.

• The main reference rates are BADLAR and CER. BADLAR is the average interest rate paid by private and/or public banks for deposits above 1 million pesos or US dollars. The information is published with a 2-day delay. CER is the Argentine offi cial infl ation rate.

• The average daily volume in government securities is US$258mn (of which approximately 50% is traded offshore) and the average bid-offer spread is 0.25%-0.40%

• The average daily volume in corporate securities is US$4mn (of which approximately 5% is traded offshore) and the average bid-offer spread is 0.5%-0.75%

• Both Sovereign and corporate bonds settle through Argenclear

Population1: 40,913,000Capital City: Buenos Aires

Nominal GDP in USD2: US$315bn

¹ All population fi gures are from the CIA World Factbook² All GDP fi gures are BBVA 2009estimates

PAGE 13

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Main Characteristics of the Derivatives Market

• Most used derivatives (NDFs, Cross Currency swaps, FX options and IRS) trade under ISDA defi nitions.

• The fi xing rate for NDFs and options is usually the EMTA ARS industry rate

• The USD reference rate in Cross Currency swaps (CCS) is usually 6-month LIBOR, whereas the ARS leg is referred to BADLAR. Coupons are usually semi-annual in both legs, and the basis is 30/360 for ARS fi xed; ACT/ACT for ARS fl oating and Actual/360 for USD leg. Liquidity in CCS is low (around US$2.5mn offshore.

• Interest rate futures market (referenced to BADLAR) is very liquid, around US$ 209mn is traded onshore, vs. US$ 17mn in short-term IRS.

• Incipient market in infl ation-linked swaps referenced to CER with very poor liquidity

PAGE 14

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Brazil at a glanceBBVA is active in the following products:

• NDF up to 3 years

• FX futures in the BM&F up to 2 years

• FX options up to 1y

• CCS Swaps up to 1y

Main characteristics of the FX market:

• The exchange-rate regime is one of free fl otation (in effect since 1999), subject to occasional intervention by the central bank depending on market volatility or current reserve accumulation policy.

• The real is a non-convertible currency. This means that there are no BRL outside of Brazil and the physical conversion of BRL into other currencies is regulated and not freely done.

• Spot transactions must be performed through an authorized fi nancial institution and registered with the Banco Central do Brasil.

• Average trading volume in 48-hour (spot) rate: USD2bn-USD4bn. Spot transactions can only be done onshore. It is worth mentioning that Brazil has currently one of the biggest derivatives exchanges and clearing system in the world (particularly big in commodities and foreign exchange), called BM & F. Therefore the fi gure that we provide as an estimate for the average daily volume is a result of the trades registered within that exchange.

• Average trading volume on futures market (onshore transactions, through the BM&F): USD15bn

• Average trading volume on the offshore forwards market (NDF): US$2.1bn. In this market two types of trades usually take place: (1) offshore against offshore and (2) offshore against onshore. The fi rst type is not subject to registry and therefore does not appear in statistics. The second type only very recently is subject to registry with the BM&F.

• Trading hours: The market in Brazil is offi cially open from 9:00am to 1:00pm and from 2:30pm to 4:30pb local time. The market trades only on local Brazilian time as there is no convertibility and therefore cannot operate without the local market.

Fixing mechanism

In offshore transactions, cash is settled at maturity in USD. The fi xing is two days prior to settlement through the PTAX rate posted in the BCB electronic system.

PTAX - This is a set of reference Forex rates, calculated and reported by the Banco Central do Brasil at the close of each day, typically used for fi xing FX transactions. The PTAX USDBRL rate is the weighted average of interbank spot transactions. The rate is generally used as a reference for defi ning the settlement value of transactions involving some foreign-exchange conversion. The PTAX for crosses between the real and other currencies is calculated on the basis of crosses between that currency and the USD, drawn from international quotations and determined by the central bank using the PTAX USDBRL.

Population3: 198,000,000Capital City: Brasilia

Nominal GDP in USD4: US$1.4 Trillion

3 All population fi gures are from the CIA World Factbook4 All GDP fi gures are BBVA 2009 estimates

PAGE 15

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

USD futures

One of the main instruments used by investors either to form currency hedge positions or adopt an exposure to a certain currency are futures contracts tradable on the BM&F. There are futures contracts on the USDBRL exchange rate as well as the EURBRL and EURBRL, but in this section we will focus on the USD contract, because it has the most heavily-traded on the market (all forex derivatives make up 24% of contract trading volume on the BM&F, and of these USD transactions account for around 94%). Because these are used as a proxy for the spot exchange rate (since the currency is not convertible), most of the liquidity is concentrated in 1-2 month terms (in fact, these terms account for 95% of the total liquidity). There are currently 573,755 contracts open. Finally, structured transactions can also be performed on USD contracts, such as volatility, rollover, and forward points.

Main characteristics:Underlying: USDBRL SpotQuotation: BRL per USD1,000 up to three decimal pointsTick: BRL 0.001 per USD1,000Trading: GTS (electronic) and open marketContract size: USD50,000Position limit: Maximum of 10,000 contracts or 20% of monthly total contractsLast trading day: Last business day before expiration dateExpiration date: First business day of contract monthTicker: DOL/UCSettlement: In cash on expiration date, at price as of last trading day in BRL

NDF USD/BRL

Because the real is a non-convertible currency, local and foreign investors can use what is called a Non Deliverable Forward (NDF) for currency hedging or investment. These transactions are over-the-counter and can be performed on the domestic market (registered with the CETIP and settled in BRL) or offshore (free of local regulations and restrictions, with no need for domestic accounts and dollar settlement).

The NDF is similar to a standard forward, meaning it entails the obligation to buy or sell a certain currency at a prefi xed exchange rate (the “forward” rate) at a certain agreed-upon date in the future.

eldlSxF

1

1

Where:F = forward, S = spot, id = domestic rate, ie = foreign rate

The main difference between these instruments and standard forwards lies in settlement at expiration: while the standard forward involves physical delivery of the agreed-upon currency amounts, an NDF is settled by payment of the difference between the agreed-upon exchange rate and the exchange rate on the expiration date (typically using the PTAX rate from one business day for onshore contracts or two business days for offshore market before the expiration date), either in dollars (on the offshore market) or in BRL (on the CETIP).

PTAX

FNx 1

Where:F = forward, N = notional

Daily trading volume in NDF USDBRL (monthly average) is around US$20bn.

FX options

Daily volume in FX options (listed and OTC) is around 500 M USD

PAGE 16

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Chile at a glanceBBVA is active in the following products:

• BBVA is active in the following products:

• FX forwards and NDF up to 10 years

• FX options up to 1y

• CCS Swaps up to 10y

• Government bonds and Repos

• Corporate bonds and Repos

• Fixed income forwards

• Credit Default Swaps

• Interest Rate Swaps

• Infl ation-linked swaps

• Equities (cash)

Main characteristics of the FX market

• The conventional market quotation is the number of CLP per USD.

• Free fl otation. The currency regime is a managed fl oat. The market trades spot onshore with delivery of CLP and non delivery forwards in the offshore market

• There is full conversion.

• FX Spot Average Daily Volume is USD1.5 billion.

• FX Forward Onshore Average Daily Volume is USD 980 million

• FX Forward Offshore Average Daily Volume is USD 1.0 billion.

• The market trades onshore on local Chilean time and offshore during New York hours 8:30 – 13:30. Liquidity is poor when Chile is closed.

Main Characteristics of the Fixed Income Market

• The main government securities are BCP (nominal bonds denominated in CLP) and BCU (infl ation linked bonds, denominated in UF, see below)

• The main reference rate is the Camara Rate (CAM), an average interbank lending rate.

• The infl ation currency is the UF (Unidad de Fomento)

• The average daily volume in government securities is US$210mn (of which approximately 50% is traded offshore) and the average bid-offer spread is 4-12 bps

• The average daily volume in corporate securities is US$100mn.

• Both Sovereign and corporate bonds settle through DCV.

Population5: 16,600,000Capital City: Santiago

de ChileNominal GDP in USD6:

US$170bn

5 All population fi gures are from the CIA World Factbook6 All GDP fi gures are BBVA 2009 estimates

PAGE 17

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Main Characteristics of the Derivatives Market

• Most used derivatives (NDFs, Cross Currency swaps, FX options and IRS) trade under ISDA defi nitions.

• The fi xing rate for NDFs and options is usually the DO (Dólar observado) rate

• The USD reference rate in Cross Currency swaps (CCS) is usually 6-month LIBOR, whereas the CLP leg is referred to DO. Coupons are usually semi-annual in both legs, and the day-count basis is Actual/360 for both legs. Liquidity in CCS is around US$100mn daily, of which 40%-60% is done offshore

• Active market in infl ation-linked derivatives referenced to UF. (around US$500mn traded daily)

PAGE 18

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Colombia at a glanceBBVA is active in the following products:

• NDF up to 3 years

• Sovereign bonds

• Corporate bonds

• Long-term IRS

• FX options up to 18 months

• CCS Swaps up to 15 years

Main characteristics of the forex market:

• The conventional market quotation is the number of COP per US dollar.

• Free fl otation. The market trades spot onshore with delivery of COP and non delivery forwards in the offshore market

• The COP is not convertible

• FX Spot Average Daily Volume is US$1 billion.

• NDF Average Daily Volume is US$700 million, of which around 30% is done offshore

• The market trades onshore on local Colombian time and offshore during New york hours but liquidity is low when the Colombian market is closed.

Main Characteristics of the Fixed Income Market

• The main government securities are Bonos TES, with maturities up to 2014 (local) and 2041 (global)

• The main reference fl oating rate is the DTF (Depósitos a Térrmino Fijo)

• The infl ation currency is UVR, (Unidad de Valor Real)

• The average daily volume in government securities is US$1 Billion and the average bid-offer spread is 10bps

• The average daily volume in corporate securities is US$25mn (of which approximately 10% is traded offshore) and the average bid-offer spread is -0.75%

• Sovereign bonds settle through DCVAL and DCV and corporate bonds settle through DCVAL

Main Characteristics of the Derivatives Market

• Most used derivatives (NDFs, Cross Currency swaps and FX options) trade under ISDA defi nitions.

• The Fixing rate for NDF, FX options and Cross Currency Swaps is the TRM (Tasa Representativa del Mercado)

• The USD reference rate in Cross Currency swaps (CCS) is usually 6-month LIBOR, whereas the COP leg is referred to DTF, but more frequently isdenominated in COP fi xed. Coupons are usually semi-annual and ACT/360 in both legs. Liquidity in CCS is low (around US$2.5mn offshore.

• Incipient market in infl ation-linked swaps referenced to UVR with minimal liquidity.

Population7: 43,680,000Capital City: Bogotá

Nominal GDP in USD8: US$210bn

7 All population fi gures are from the CIA World Factbook8 All GDP fi gures are BBVA 2009 estimates

PAGE 19

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Mexico at a GlanceBBVA is active in the following products:

• FX Spot

• NDF up to 2 years

• Sovereign Bonds

• Corporate Bonds

• FX futures in CME and Mexder

• FX options, OTC and Mexder

• CCS Swaps

• IRS

• Interest Rate volatilities

• CDS

• Infl ation linked-swaps

• Equities (cash and derivatives)

Main characteristics of the forex market:

• Since December 1994, the exchange-rate regime has been pf free fl otation, subject to occasional intervention by the central bank depending on market volatility or current reserve accumulation policy (which we explain below)

• The MXN is a free convertible currency

• Average trading volume in 48-hour (spot) rate: US$15bn

• Average trading volume on forwards/futures market

• Liquidity hours: 6am-3pm NYT

Fixing mechanism

1. FIX exchange rateThis is currently the most representative currency exchange rate in the wholesale market. Every banking day, Banxico obtains US dollar sale and purchase exchange rates for operations payable on the second next banking business day, of credit institutions whose operations in its view refl ect the prevailing conditions in the wholesale foreign exchange market. These rates are requested three times per morning from 9:00 to 12:00 p.m. Each credit institution quotes rates in only one period per day. For this purpose, Banco de México randomly selects within each of these periods an interval of fi fteen minutes to request the aforementioned rates of at least four credit institutions. The CB requests these rates for an amount which, in its judgment, refl ects the prevailing practice in the wholesale foreign exchange market. The FIX exchange rate is released unoffi cially on the same day it is determined after 12:00hrs, and offi cially on the following day in the Offi cial Gazette. The FIX exchange rate, given its transparency, is generally used to settle NDF and FX option contracts.

2. Spot Exchange RatesThis exchange rate is used for wholesale operations among banks, brokerage houses, exchange houses, corporations and private individuals. It is applicable to settle operations on the second banking business day immediately following the date it is determined.

Population9: 111,200,000Capital City: Mexico CityNominal GDP in USD10:

US$ 1.1 Trillion

9 All population fi gures are from the CIA World Factbook10 All GDP fi gures are BBVA 2009 estimates

PAGE 20

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Mechanisms used to moderate exchange rate volatility

The interventions that the Exchange Rate Commission has approved are the following:

• 1995 Discretionary Intervention in the Foreign Exchange Market

• August 1996- June 2001 Auction of USD put options

• February 1997-June 2001 USD auctions

• May 2003 – July 2008 Mechanism to slow the pace of reserve accumulation

• October 2008 USD Extraordinary auctions

• October 2008 – April 2010 USD auctions with minimum price

• March 2009 – September 2009 USD auctions without minimum price

• April 2009 – February – 2010 Disposition of swap line with US Fed

• February 2010 – to date Auction of USD put options

FX Transactions

1. Cash-Tom and Tom-Next swaps (OTC)Exchange operations which enable customer to obtain fi nancing or perform investments in either pesos or dollars in short term periods by simultaneously buying and selling the same amount of one currency with different maturity dates (cash, 24hrs or 48hrs).

2. USD Futures in MEXDER and MXN Futures in Chicago (CME)Derivative instruments used for protection against exchange rate devaluation or appreciation. They are standard listed contracts either in MEXDER and the Chicago Mercantile Exchange (CME), subject to ongoing market valuation, which implies possible “margin calls” to cover guarantees.

Some advantages of trading this type of contract in MEXDER are: contract size is smaller than in the CME, which can attract a broader base of investors; accounts may be located in Mexico in pesos, whereas in the CME the accounts must be held abroad (USD).

Table 4

Characteristics In the MEXDER In the CMEParticipants: Mexican or Foreign nationals Mexican or foreign nationals.

Contract size: $10,000 US dollars $500,000 MXNMaturity period or date:

The maturity dates of futures contracts in pesos are the third Wednesday of the month: In the MEXDER, they are traded in a monthly and quarterly cycle for up to three years. When the day is a bank holiday, the maturity date is changed to the immediately previous bank business day (Preceding Business Day conven-tion).The last trading date will be on Monday of the week corresponding to the maturity date, or the previous business day in case of a bank holiday.

The maturity dates of futures contracts in pesos are the third Wednesday of the month. In the CME they are traded for thirteen consecutive months plus two months in a quarterly cycle. When the day is a bank holiday, the maturity date is changed to the immediately previous bank business day (Preceding Business day convention).The last trading date will be on Monday of the week corresponding to the maturity date, or the previous business day in case of a bank holiday.

Settlement date: The second business day following the maturity date (T+2), Settlement date must be a working day both in Mexico and the US

Physical delivery takes place on the third Wednes-day of the contract month in the country of issuance at a bank designated by the Clearing House.

Agreed exchange rate:

The applicable exchange rate agreed by the parties, which is traded in pesos per US dollar in the MEX-DER.

The applicable exchange rate agreed by the parties, which is traded in US dollars for pesos in the CME.

* continued on next page

PAGE 21

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

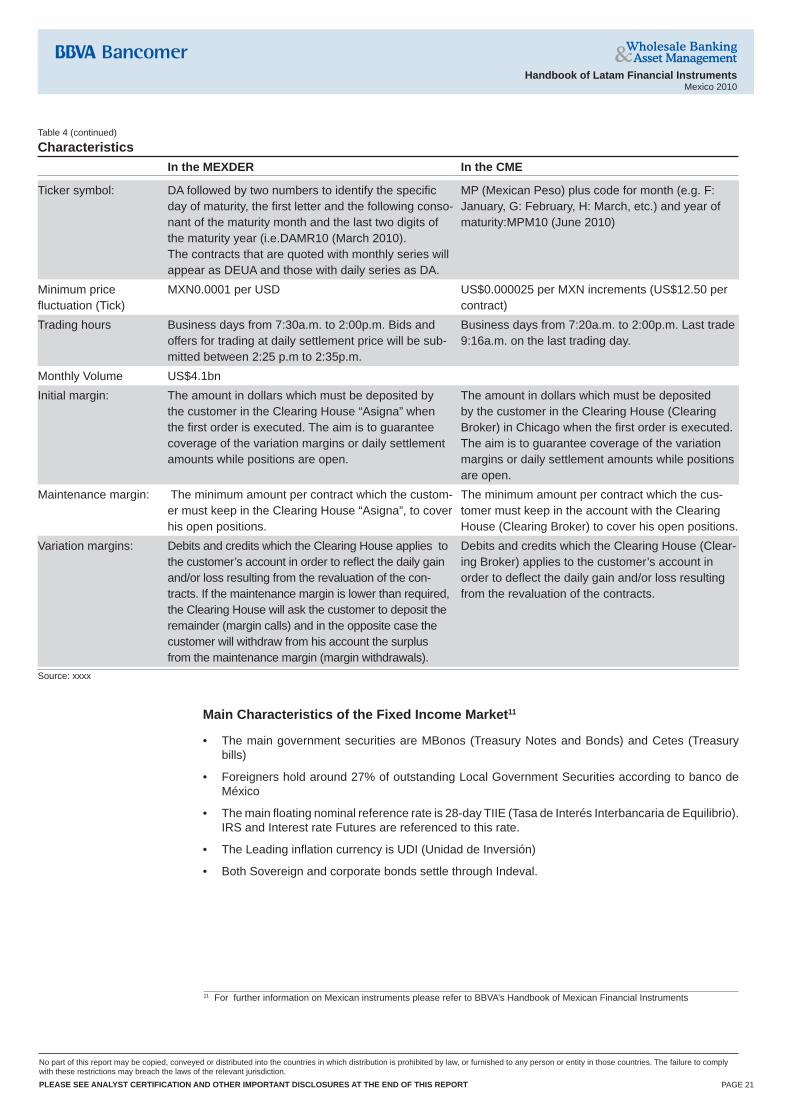

Table 4 (continued)

Characteristics In the MEXDER In the CME

Ticker symbol: DA followed by two numbers to identify the specifi c day of maturity, the fi rst letter and the following conso-nant of the maturity month and the last two digits of the maturity year (i.e.DAMR10 (March 2010).The contracts that are quoted with monthly series will appear as DEUA and those with daily series as DA.

MP (Mexican Peso) plus code for month (e.g. F: January, G: February, H: March, etc.) and year of maturity:MPM10 (June 2010)

Minimum pricefl uctuation (Tick)

MXN0.0001 per USD US$0.000025 per MXN increments (US$12.50 per contract)

Trading hours Business days from 7:30a.m. to 2:00p.m. Bids and offers for trading at daily settlement price will be sub-mitted between 2:25 p.m to 2:35p.m.

Business days from 7:20a.m. to 2:00p.m. Last trade 9:16a.m. on the last trading day.

Monthly Volume US$4.1bnInitial margin: The amount in dollars which must be deposited by

the customer in the Clearing House “Asigna” when the fi rst order is executed. The aim is to guarantee coverage of the variation margins or daily settlement amounts while positions are open.

The amount in dollars which must be deposited by the customer in the Clearing House (Clearing Broker) in Chicago when the fi rst order is executed. The aim is to guarantee coverage of the variation margins or daily settlement amounts while positions are open.

Maintenance margin: The minimum amount per contract which the custom-er must keep in the Clearing House “Asigna”, to cover his open positions.

The minimum amount per contract which the cus-tomer must keep in the account with the Clearing House (Clearing Broker) to cover his open positions.

Variation margins: Debits and credits which the Clearing House applies to the customer’s account in order to refl ect the daily gain and/or loss resulting from the revaluation of the con-tracts. If the maintenance margin is lower than required, the Clearing House will ask the customer to deposit the remainder (margin calls) and in the opposite case the customer will withdraw from his account the surplus from the maintenance margin (margin withdrawals).

Debits and credits which the Clearing House (Clear-ing Broker) applies to the customer’s account in order to defl ect the daily gain and/or loss resulting from the revaluation of the contracts.

Source: xxxx

Main Characteristics of the Fixed Income Market11

• The main government securities are MBonos (Treasury Notes and Bonds) and Cetes (Treasury bills)

• Foreigners hold around 27% of outstanding Local Government Securities according to banco de México

• The main fl oating nominal reference rate is 28-day TIIE (Tasa de Interés Interbancaria de Equilibrio). IRS and Interest rate Futures are referenced to this rate.

• The Leading infl ation currency is UDI (Unidad de Inversión)

• Both Sovereign and corporate bonds settle through Indeval.

11 For further information on Mexican instruments please refer to BBVA’s Handbook of Mexican Financial Instruments

PAGE 22

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Main Characteristics of the Derivatives Market

• Most used derivatives (NDFs, Cross Currency swaps, FX options, IRS and Interest rate options) trade under ISDA defi nitions in the OTC market.

• MEXDER12 is the listed options an futures market, where TIIE Futures, USD futures, Local equity index (IPC) futures trade very actively.

• The fi xing rate for NDFs and options is usually the Banxico Fixing Rate, published daily at www.banxico.gob.mx

• The USD reference rate in Cross Currency swaps (CCS) is usually 6-month LIBOR, whereas the MXN leg is referred to 28 d TIIE. Coupons are usually semi-annual in both legs, and the basis is 30/360 for LIBOR leg and Actual/360 for MXN leg. Liquidity in CCS is IRS and CCS is high (above US$1bn average daily volume in IRS and US$500 mn in CCS)

• Interest rate futures (referenced to TIIE) are quoted in MEXDER (over US$2 bn traded daily)

• Active OTC market in infl ation-linked swaps referenced to UDI (UDI-TIIE or UDI-LIBOR)

12 See table above for a comparison between MEXDER and CME regarding USDMXN futures

PAGE 23

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Peru at a GlanceBBVA is active in the following products:

• BBVA is active in the following products:

• NDF up to 3 years

• FX options up to 1y

• CCS Swaps up to 10y

Main characteristics of the forex market:

• The conventional market quotation is the number of nuevos soles per US dollar.

• Free fl otation. The market trades spot onshore with delivery of PEN and non delivery forwards in the offshore market

• There is full conversion. When dollars from the offshore are converted into soles the ITF tax of 0.05% is applied, but no taxes are applied between local USD and PEN accounts.

• FX Spot Average Daily Volume is USD 350 million.

• FX Forward Onshore Average Daily Volume is USD 246 million

• FX Forward Offshore Average Daily Volume is USD 100 million.

• The market trades onshore on local Peruvian time and offshore during the New York time 10:30 – 14:00. The liquidity is very low when Peru is closed.

Main Characteristics of the Fixed Income Market

• Government securities have maturities of up to 32 years.

• Average volume in government securities is US$50 million, of which around 24% is done offshore. Bid- offer spreads range from 5 to 30bps

• There is no fl oating reference rate in Peru

• The local infl ation currency is VAC (Valor Adquistivo Constante)

• The average daily volume in corporate securities is US$4mn, traded mainly onshore.

• Global bonds settle through Euroclear and local bonds through Cavali

Main Characteristics of the Derivatives Market

• Most used derivatives (NDFs, Cross Currency swaps and FX options) trade under ISDA defi nitions.

• The fi xing rate for NDFs and options is usually the SBS (Superintendencia de Banca y Seguros) rate

• The USD reference rate in Cross Currency swaps (CCS) is usually 6-month LIBOR, whereas the PEN leg is fi xed since there is no fl oating rate in Peru. Coupons are usually semi-annual and the basis ACT/360 in both legs. Liquidity in CCS is low (average daily volume is around US$30mn of which 90% is done offshore).

• Incipient market in infl ation-linked swaps referenced to VAC with very poor liquidity.

Population13: 29,546,000Nominal GDP in USD14:

US$127bn

13 All population fi gures are from the CIA World Factbook14 All GDP fi gures are BBVA 2009 estimates

PAGE 24

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Fixed Income TradingHeadÁlvaro [email protected]

Propietary Trading

Head Tomás [email protected]

Global Markets SalesHeadÓscar Álvarez de la [email protected]

Equity TradingHeadJosé Alberto Galvá[email protected]

Global Markets, MexicoManaging Director Global MarketsJosé Antonio [email protected]

CRD Trading

Head Luis [email protected]

Hernán Vázquez del [email protected]

Global Markets Colombia

Head David Rey [email protected]

Global Markets USA

Head Kenneth S. [email protected]

CRD Structuring Europe

Head Alonso Fernández de [email protected]

Cecilia Gil [email protected]

Global Markets Chile

Head Fernando Pardo [email protected]

Global Markets Argentina

HeadJuan Alberto [email protected]

CRD Structuring Latam

Head Pilar Guzmá[email protected]

Wilfrido Castillo [email protected]

Global Markets Peru

Head José Goldszmidt [email protected]

BBVA ResearchGroup Chief EconomistJosé Luis Escrivá[email protected]

Chief Economists&Chief Strategists

Regulatory Affairs, Financial and Economic Scenarios:Mayte [email protected]

Market & Client Strategy:Antonio [email protected]

Spain and Europe:Rafael Domé[email protected]

Emerging MarketsAlicia Garcí[email protected]

Latin America:Joaquín [email protected]

Marking Market

Head Guillermo Gó[email protected]

Short Term Trading

Head Manuel [email protected]

Global Markets Latam Managing Director Mercados Globales America del Sur y USAAngel L. Sánchez Aristi [email protected]

PAGE 25

No part of this report may be copied, conveyed or distributed into the countries in which distribution is prohibited by law, or furnished to any person or entity in those countries. The failure to comply with these restrictions may breach the laws of the relevant jurisdiction.PLEASE SEE ANALYST CERTIFICATION AND OTHER IMPORTANT DISCLOSURES AT THE END OF THIS REPORT

Handbook of Latam Financial InstrumentsMexico 2010

Market & Client Strategy

DirectorANTONIO PULIDO [email protected] +34 91 374 31 81

Global Equity and Credit

DirectorANA [email protected]+34 91 374 36 72

Equity Latam

Chief AnalystRODRIGO [email protected]+52 55 5621 9701

Equity Mexico, Chief AnalystFRANCISCO [email protected]+52 55 5621 9703

Global Fixed Income

DirectorLUIS ENRIQUE RODRIGUEZ, CFA [email protected]+34 91 537 35 87

FX Latam

Chief StrategistMOISES JUNCA, CFA, [email protected] +5255 5621 9380

Claudia Ceja [email protected] +5255 5621 9715

Interest Rates Latam

Interest Rates Mexico, Chief StrategistOCIEL [email protected]

Liliana Solí[email protected]+5255 5621 98 77

Macro Latam Strategy

OCTAVIO [email protected]+52 55 5621 9245

Handbook of Latam Financial InstrumentsMexico 2010

IMPORTANT DISCLOSURES

This document and the information, opinions, estimates and recommendations expressed herein, have been prepared by BBVA Global Markets Research an affi liate of Banco Bilbao Vizcaya Argentaria, S.A. (BBVA) and/or BBVA Bancomer, to provide their or its customers with general information as of the date of the report and are subject to changes without prior notice. BBVA Bancomer is not liable for giving notice of such changes or for updating the contents hereof. This document and its contents do not constitute an offer, invitation or solicitation to purchase or subscribe to any securities or other instruments, or to undertake or divest investments. Neither shall this document nor its contents form the basis of any contract, commitment or decision of any kind. For more information please contact the persons included in the directory of this document.

The determination of a price target does not imply any warranty that it will be attained. For a discussion of the risks associated with the attainment of price targets, which depend on intrinsic and extrinsic factors that affect both the performance and trends prevailing in the market on which the recommended securities is traded and/or offered, please refer to our recently published documents, which are available via e-mail, contact our analysts or visit our internet site www.bancomer.com.

Investors who have access to this document should be aware that the securities, instruments or investments to which it refers may not be appropriate for them due to their specifi c investment goal, fi nancial position or risk profi le, for these have not been taken into account in the preparation of this report. Therefore, investors should make their own investment decisions considering the said circumstances and obtaining such specialized advice as may be necessary.

The contents of this document are based upon information available to the public that has been obtained from sources considered to be reliable. However, such information has not been independently verifi ed by BBVA Bancomer, and therefore no warranty, either express or implicit, is given regarding its accuracy, integrity or correctness. BBVA Bancomer, accepts no liability of any type for any direct or indirect losses arising from the use of the document or its contents.

Investors should note that the past performance of securities or instruments or the historical results of investments do not guarantee future performance. The market prices of securities or instruments or the results of investments could fl uctuate against the interests of investors. Investors should be aware that they could even face a loss of their investment.

Transactions in futures, options or high-yield securities can involve high risk and are not appropriate for every investor. Indeed, in the case of some investments, the potential losses may exceed the amount of the initial investment; in such circumstance, investors may be required to pay more money to support those losses. Thus, before undertaking any transaction with these instruments, investors should be aware of their characteristics, as well as the rights, liabilities and risks associated with these securities and their underlying investments. Investors should also be aware that secondary markets for the said instruments may be limited or may not exist.

BBVA Bancomer, or any of its affi liates, as well as their respective executives and employees, may have a position in any of the securities or instruments referred to, directly or indirectly, in this document, or in any other related thereto; they may trade for their own account or for third-party account in those securities, provide consulting or other services to the issuer of the aforementioned securities or instruments or to companies related thereto or to their shareholders, executives or employees, or may have interests or perform transactions in those securities or instruments or related investments before or after the publication of this report, to the extent permitted by the applicable law.

BBVA Bancomer or any of its affi liates´ salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies to its clients that refl ect opinions that are contrary to the opinions expressed herein. Furthermore, BBVA Bancomer or any of its affi liates’ proprietary trading and investment businesses may make investment decisions that are inconsistent with the recommendations expressed herein.

No part of this document may be (i) copied, photocopied or duplicated by any other form or means (ii); redistributed or forwarded; or (iii) quoted, without the prior written consent of BBVA Bancomer. No part of this report may be copied, conveyed, distributed or furnished to any person or entity in any country (or persons or entities in the same) in which its distribution is prohibited by law. Failure to comply with these restrictions may breach the laws of the relevant jurisdiction.

This document is provided in the United Kingdom solely to those persons to whom it may be addressed according to the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 and it is not to be directly or indirectly delivered to or distributed among any other type of persons or entities. In particular, this document is only aimed at and can be delivered to the following persons or entities (i) those outside the United Kingdom (ii) those with expertise regarding investments as mentioned under Section 19(5) of Order 2001, (iii) high net-worth entities; and (iv) any other person or entity under Section 49(1) of Order 2001 to whom the contents hereof can be legally revealed.

The remuneration system concerning the analyst/s author/s of this report is based on multiple criteria, including the results obtained by BBVA Bancomer and by BBVA Group in the fi scal year, which, in turn, include the results generated by the investment banking business, common representation or credit related services; nevertheless, they do not receive any remuneration based on revenues from the mentioned areas or a specifi c transaction in investment banking, common representation or credit related services.

The information contained in this document should be taken only a general guide on matters that may be of interest. The application and impact of the laws may vary substantially depending on specifi c circumstances. Changes in regulations and the risks inherent in electronic communication may cause delays, omissions, or inaccuracy in the information contained in this site. Accordingly, the information contained in the site is supplied on the understanding that the authors and editors do not hereby intend to supply any form of consulting, legal, accounting or other advice. As such, it should not be considered a substitute for the direct advice provided by accounting and fi scal advisors or other competent consultants.

Handbook of Latam Financial InstrumentsMexico 2010

All images and texts and texts are the property of BBVA Bancomer and may not be downloaded from the Internet, distributed, stored, re-used, re-transmitted, modifi ed or used in any way, except as specifi ed in this document, without the express written consent of BBVA Bancomer. BBVA Bancomer reserves all intellectual property rights to the fullest extent of the law. None of the information contained herein may be interpreted as a concession by implication, exclusion or any other means, of any patent or brand of BBVA Bancomer or of any third party. Nothing established herein should be interpreted as a concession of any license or right under any BBVA Bancomer copyright.

BBVA Bancomer, as web as its executives and employees have adopted the Código de Conducta de Grupo Financiero BBVA Bancomer, which is available in our internet site www.bancomer.com.

BBVA Bancomer is regulated by the Comisión Nacional Bancaria y de Valores.

BBVA Bancomer as well as other entities in the BBVA Group that are not members of the FINRA (Financial Industry Regulatory Authority), are not subject to the rules of disclosure affecting such members.

This material is being distributed into the United States in reliance on an exemption from broker-dealer registration under Rule 15a-6 of the Rules under the Securities Exchange Act of 1934. Any trades in the securities discussed in this report must be effected through a U.S. registered broker/dealer as we are not authorized to accept any order to effect trades in any security discussed in this report within the U.S.