lazard european roadshow july 2009

TRANSCRIPT

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 1/17

Capst one Managem ent Presenta t ion

July 2009

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 2/17

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 3/17

2

2

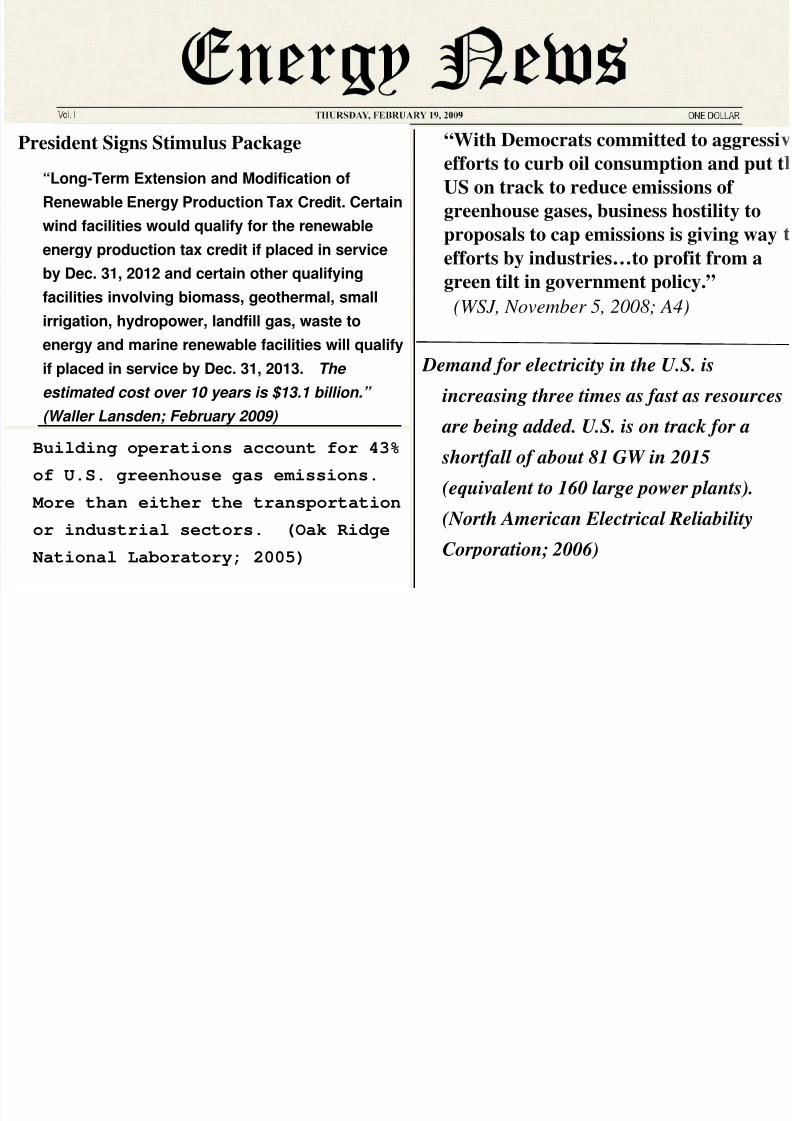

“With Democrats committed to aggressi

efforts to curb oil consumption and put t

US on track to reduce emissions of

greenhouse gases, business hostility toproposals to cap emissions is giving way

efforts by industries…to profit from a

green tilt in government policy.”

(WSJ, November 5, 2008; A4)

Demand for electricity in the U.S. is

increasing three times as fast as resources

are being added. U.S. is on track for a

shortfall of about 81 GW in 2015

(equivalent to 160 large power plants).

(North American Electrical Reliability

Corporation; 2006)

Building operations account for 43%

of U.S. greenhouse gas emissions.

More than either the transportation

or industrial sectors. (Oak Ridge

National Laboratory; 2005)

President Signs Stimulus Package

“Long-Term Extension and Modification of

Renewable Energy Production Tax Credit. Certainwind facilities would qualify for the renewable

energy production tax credit if placed in service

by Dec. 31, 2012 and certain other qualifying

facilities involving biomass, geothermal, small

irrigation, hydropower, landfill gas, waste to

energy and marine renewable facilities will qualify

if placed in service by Dec. 31, 2013. The

estimated cost over 10 years is $13.1 billion.”

(Waller Lansden; February 2009)

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 4/173

• 96 U.S. technology patents• Air bearing technology

• One moving part

• No coolants, oils or grease

• Flexible and economic clean technology• Flexible configuration

• Lightweight & small footprint• Multi-fuel capability

• Ultra-low emissions

• Capstone’s product family• C30 – 30kW• C65 – 65kW• C200 – 200kW (First shipment August 2008)

• C1000 Series – 600kW, 800kW, 1,000kW

(First shipment January 2009)

Capst one’s Mic rot urb ine

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 5/174

Mic roTurbine Com pet i t ion

IngersollIngersoll--RandRand

(250kW)(250kW)

Elliott EnergyElliott Energy

Systems (100kW)Systems (100kW)

TurbecTurbec

(100kW)(100kW)

MicroTurbine Industry Leader With Majority Market Share

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 6/175

Current Mark et Segm ent s

Hospitals

Data CentersHotels & Schools

Large Retailers

Oil & Gas

U.S. Gov’t

Waste Water Plants

Telecom

DigestersLandfills

Hybrid EV

Office Buildings

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 7/176

New C200 & C1000 Produc t s

• Competitive Pricing

• Low maintenance

• High reliability

• High efficiency

• Ultra low emissions

• Built-in redundancy

• Small Footprint

Piston Engine Price, Fuel Cell Emissions, Turbine Reliability

0

500

1,000

1,500

2,000

2,500

3,000

3,500

M

a r k e t P o t e n t i a l $ M

i l l i o n s

28-300 kW .3-1 MW 1-5 MW 5-10 MW 10-20 MW 20-50 MW

Source: Resource Dynamics Corporation (extrapolated based on industrial uses)

Microturbine Market

C200/C1000 Market Expansion

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 8/177

Uni t ed Tec hnologies (NYSE: UTX)

• Worldwide OEM Partner for PureComfort

– Private labeling Capstone Microturbines

– Match with Carrier Absorption Chiller forCHP/CCHP Markets

– Focus on big customers:• Wal-Mart

• Tesco

• Marriot International/Ritz Carlton

– Development Partner for C200 Systems

• $12.8 in cash and engineering support

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 9/178

Value Com par ison First Cost

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

Solar PV Fuel Cells Wind Microturbine Recip

$ P e r

Equivalent Cars Removed (CO2) for 1 MW Project

0

200

400

600

800

1,000

1,200

Solar PV Wind Recip Fuel Cells Microturbine

N u m b e r o f C a r s

Assumptions: Capstone C200 System, Combined Heat and Power Systems, Natural Gas Fueled,

California Emission Standards, Initial Investment Data: CA Statewide SGIP Program

Statistics through Q4 2007, Analysis assumes no incentives

Total Cost of Ownership

$(6,000)

$(5,000)

$(4,000)

$(3,000)

$(2,000)

$(1,000)

$-

$1,000

$2,000

$3,000

$4,000

Solar PV Fuel Cells Wind Recip CHP Microturbine CHP

$ P e r k

Source: CA Statewide SGIP Program Statistics

Best Value Proposition

1. Microturbine Combined Heat & Power2. Reciprocating Combined Heat & Power

3. Wind Turbine

4. Fuel Cells

5. Solar PV

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 10/179

Gas Turb ine Com par ison

Solar Turbines Mercury 50

Kawasaki GPB30D

Dresser-Rand KG2-3E

Capstone C200 Capstone C1000

Siemens SGT-100

Ingersol Rand MT250

Elliott TA100R

Rolls Royce 501-KB5S

Kawasaki GPB15

OPRA Turbines OP16-3B

(DLE)

Solar Turbines Saturn 20

Solar Turbines Centaur 40

Solar Turbines Centaur 50

Kawasaki GPB60D

Rolls Royce 501-KB7S

Dresser-Rand KG2-3

General Electric GE5-1 (DLN)

14

16

18

20

22

24

26

28

30

32

34

36

38

40

0 1 2 3 4 5 6

Power Output (MW)

E l e c t r i c a l E f f i c i e n

Capstone offers the highest efficiency alternatives below 4.5 MW Source: Company Websites. Data and results are based on publicly available information from manufacturers and except for Capstone’s products, not from Capstone tests.

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 11/1710

Capst one Value Proposi t ion

• 120 hrs planned maintenance per year• Scheduled/unscheduled maintenance

$0.018 to 0.022 / kW-hr

• Average uptime 82%

Op. Hours Item Action

1,000 – 2,000Air & Oil Filters, Oil,

Spark PlugsInspect orReplace

1,500 Top End Inspect

20,000 Top End Overhaul

40,000 Bottom End Overhaul

• 6 hrs planned maintenance per year• Scheduled/unscheduled maintenance

$0.015 / kW-hr

• Average uptime 99%

Op. Hours Item Action

8,000 Air/Fuel Filters, IgniterInspect,Replace

20,000 Injectors, Batteries Replace

40,000Engine/Generator,

Injectors, BatteriesOverhaul

Maintenance Costs 25% Lower on Average = Lower TCO

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 12/17

11

• CARB 2007 - extremely stringentemissions standard that exceeds therequirements of federal standards

• CARB 2010 – C30 internal testingcomplies with standard

• Only Microturbines, Fuel Cells, Solar and

Wind meet standard

Capst one Value Propos i t ion

Units 2003 2007 Reduction

NOx lb/MWh 0.5 0.07 86%

CO lb/MWh 6.0 0.10 98%

VOC lb/MWh 1.0 0.02 98%

CARB Natural Gas Emission Standard

Relative NOx Emissions

US Grid

Avg

NG

Recip

C200

Source: EPA and ASME

Capstone Emissions Less Than 1/10th of Internal Combustion Engines

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 13/17

12

Grow ing Produc t Bac k log

0

10

20

3040

50

60

70

80

Q1'08 Q2'08 Q3'08 Q4'08 Q1'09 Q2'09 Q3'09 Q4'09

M w

C30 C60 SeriesC200 C1000 Series

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 14/17

Y/Y Net Revenue Grow t h

$5.6

$7.2

$9.2 $9.3

$7.5

$13.1$11.5 $11.8

Q1 Q2 Q3 Q4

FY'08 FY'09

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 15/17

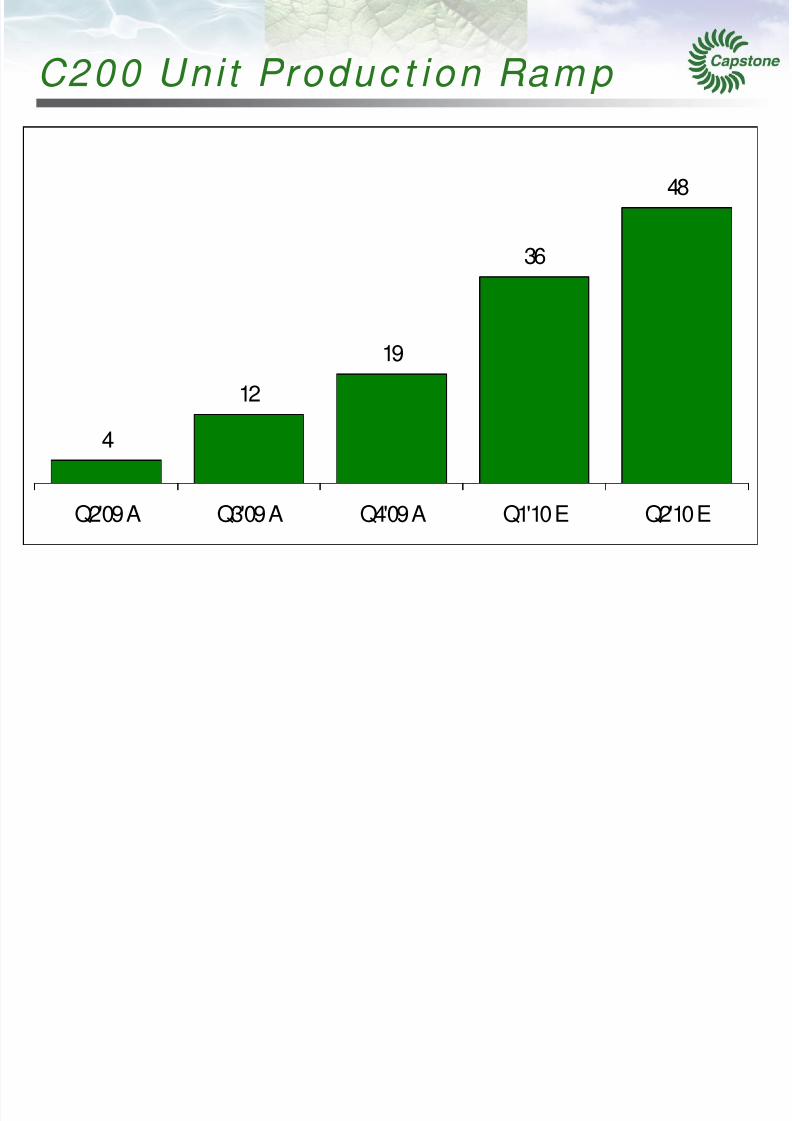

C200 Uni t Produc t ion Ram p

4

12

19

36

48

Q2'09 A Q3'09 A Q4'09 A Q1'10 E Q2'10 E

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 16/17

15

Clear Pat h t o Prof i t ab i l i t y

Increased

ProductionProfitability

ProductAcceptance

• C200/C1000 production rates

• Increased Robotics

• Tier One Suppliers

• Just in Time Deliveries

• Significant Inventory Reduction

• 4,000 unit maximum capacity

• FY09 Backlog $61.5

million

• Y/Y Revenue 40%

growth

• Multiple Markets

• Not experiencingorder cancellations

• C200/C1000 direct material

improvement of 30% through

FY2010

• Overhead reductions in FY2010

• Gross margin 35-40% by end

FY2010

• Operating expense lower by

15% in FY2010

7/29/2019 Lazard European Roadshow July 2009

http://slidepdf.com/reader/full/lazard-european-roadshow-july-2009 17/17

16

Posi t ioned For Grow t h

• Strong International market drivers

• U.S. Policy now focusing on energy efficiencyand renewable power

• Positioned as Green ultra low emission andhighly efficient technology

• New C200/C1000 product enables megawattsolutions in a $4 Billion Annual Market

• Backlog as of March 31, 2009, up 120% from

March 31, 2008