learning unit 4 - bee's knees law -...

TRANSCRIPT

LEARNING UNIT 4: THE CONTRACT OF INSURANCE AND

OF AGNECY

OBJECTIVES: Explain indemnity and non- indemnity insurance Explain the requirements for the conclusion of a contract of insurance Discuss the concept on an “insurable interest” Discuss the duty of disclosure Explain the warranties in the law of insurance Apply these warranties to a set of facts Explain “subrogation” Explain “estoppel” and its requirements Explain “ratification” and its requirements Describe the duties of the principal and agent List the various ways a contract of agency may be terminated

Co

ntr

act

of

insu

ran

ce

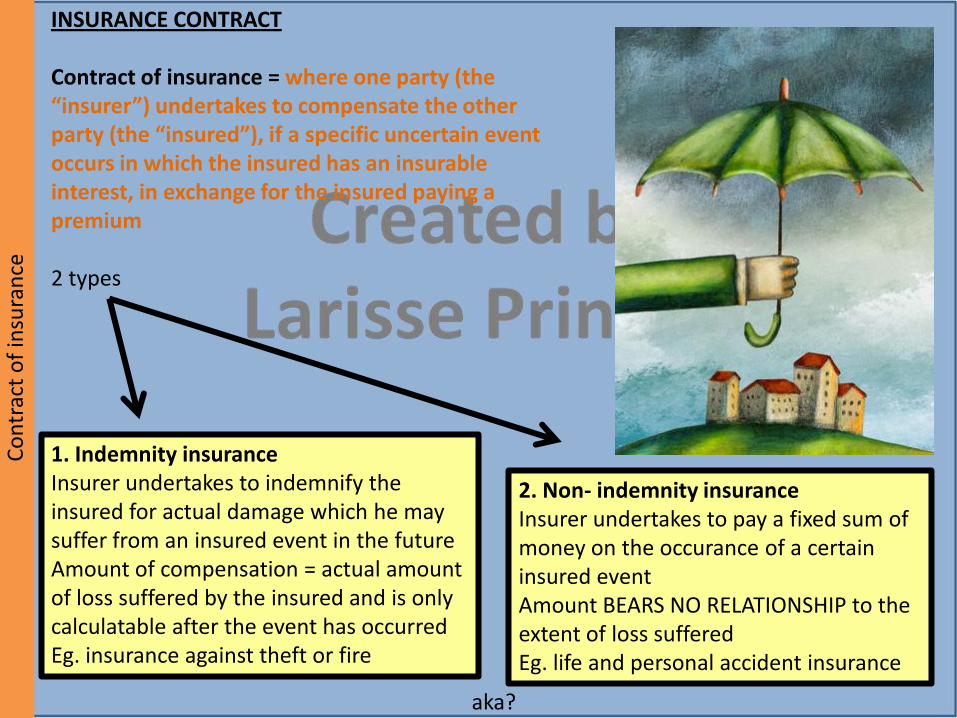

INSURANCE CONTRACT Contract of insurance = where one party (the “insurer”) undertakes to compensate the other party (the “insured”), if a specific uncertain event occurs in which the insured has an insurable interest, in exchange for the insured paying a premium 2 types

2. Non- indemnity insurance Insurer undertakes to pay a fixed sum of money on the occurance of a certain insured event Amount BEARS NO RELATIONSHIP to the extent of loss suffered Eg. life and personal accident insurance

1. Indemnity insurance Insurer undertakes to indemnify the insured for actual damage which he may suffer from an insured event in the future Amount of compensation = actual amount of loss suffered by the insured and is only calculatable after the event has occurred Eg. insurance against theft or fire

aka?

Co

ntr

act

of

insu

ran

ce

REQUIREMENTS FOR VALID INSURANCE CONTRACT 4 essential requirements for the conclusion of a valid contract of INSURANCE (REMEMBER! The general requirements for the conclusion of a valid contract must be met and these requirements then are essential to the INSURANCE contract and are “additional”)

1.Obligation of insured to pay premium •premium must carry monetary value •undertaking to pay premium is sufficient unless otherwise stipulated by the agreement •premium is normally payable in advance

2. Obligation for the insurer to pay sum of money or its equivalent •indemnity insurance – the insurer has the obligation to pay a determinable amount.

o Exact amount payable is only determinable after the insured event has taken place

o Amount payable is equal to the value of the insured’s actual loss o In order to place insured in same position as he was prior to the occurrence of

the event •non- indemnity insurance – the insurer has the obligation to pay a predetermined amount

Consensus Capacity Legal possibility Physical possibility Formalities

4

Co

ntr

act

of

insu

ran

ce

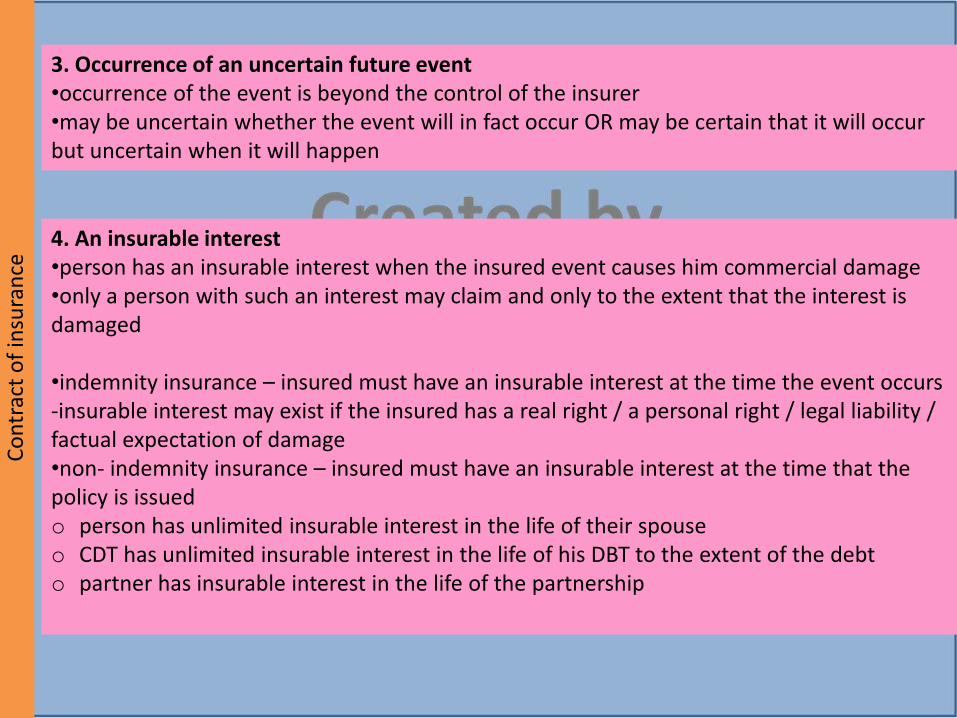

3. Occurrence of an uncertain future event •occurrence of the event is beyond the control of the insurer •may be uncertain whether the event will in fact occur OR may be certain that it will occur but uncertain when it will happen

4. An insurable interest •person has an insurable interest when the insured event causes him commercial damage •only a person with such an interest may claim and only to the extent that the interest is damaged •indemnity insurance – insured must have an insurable interest at the time the event occurs -insurable interest may exist if the insured has a real right / a personal right / legal liability / factual expectation of damage •non- indemnity insurance – insured must have an insurable interest at the time that the policy is issued o person has unlimited insurable interest in the life of their spouse o CDT has unlimited insurable interest in the life of his DBT to the extent of the debt o partner has insurable interest in the life of the partnership

Co

ntr

act

of

insu

ran

ce

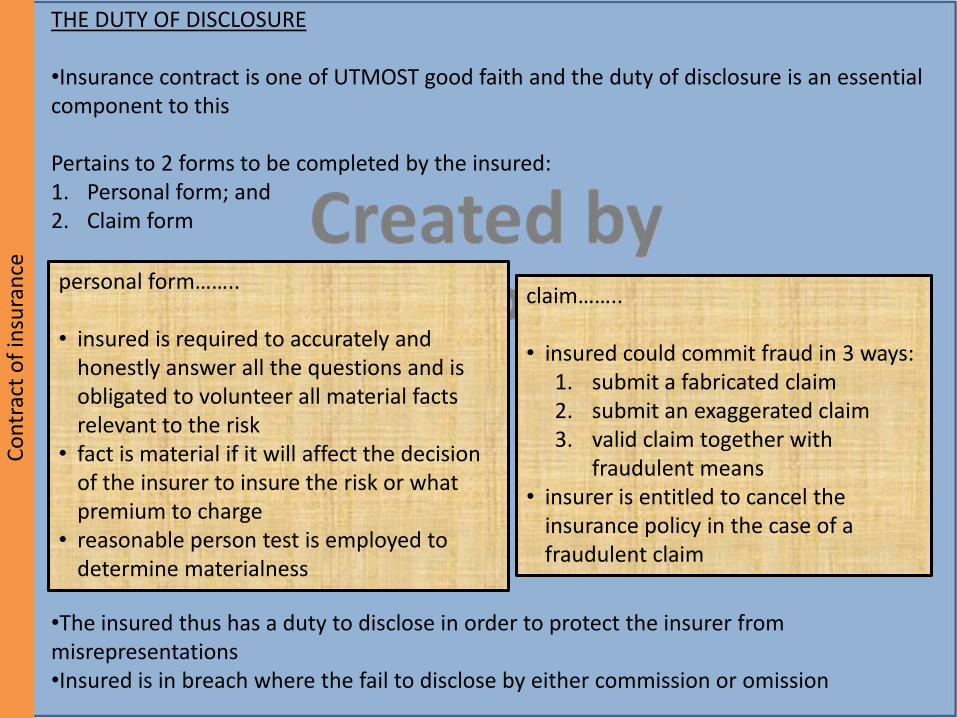

THE DUTY OF DISCLOSURE •Insurance contract is one of UTMOST good faith and the duty of disclosure is an essential component to this Pertains to 2 forms to be completed by the insured: 1. Personal form; and 2. Claim form

•The insured thus has a duty to disclose in order to protect the insurer from misrepresentations •Insured is in breach where the fail to disclose by either commission or omission

personal form…….. • insured is required to accurately and

honestly answer all the questions and is obligated to volunteer all material facts relevant to the risk

• fact is material if it will affect the decision of the insurer to insure the risk or what premium to charge

• reasonable person test is employed to determine materialness

claim…….. • insured could commit fraud in 3 ways:

1. submit a fabricated claim 2. submit an exaggerated claim 3. valid claim together with

fraudulent means • insurer is entitled to cancel the

insurance policy in the case of a fraudulent claim

Co

ntr

act

of

insu

ran

ce

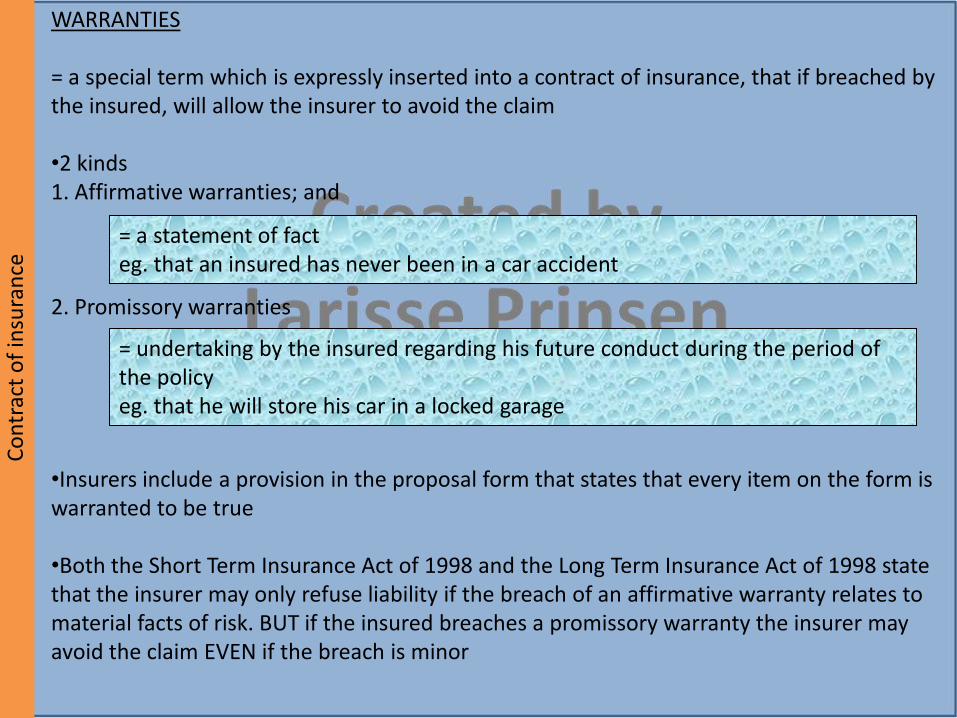

WARRANTIES = a special term which is expressly inserted into a contract of insurance, that if breached by the insured, will allow the insurer to avoid the claim •2 kinds 1. Affirmative warranties; and 2. Promissory warranties •Insurers include a provision in the proposal form that states that every item on the form is warranted to be true •Both the Short Term Insurance Act of 1998 and the Long Term Insurance Act of 1998 state that the insurer may only refuse liability if the breach of an affirmative warranty relates to material facts of risk. BUT if the insured breaches a promissory warranty the insurer may avoid the claim EVEN if the breach is minor

= a statement of fact eg. that an insured has never been in a car accident

= undertaking by the insured regarding his future conduct during the period of the policy eg. that he will store his car in a locked garage

Co

ntr

act

of

insu

ran

ce

SUBROGATION •Insurer has the right of subrogation •= once the insurer has paid the claim to the insured in full, the insurer may obtain all the rights and benefits of the insured against a third party •Means that the insurer “steps into the shoes” of the insured ito the claim against the third party and may thus sue the third party in the name of the insured •Only once the insurer has fully settled the insured’s claim •Only where the insured has a claim against the third party

Co

ntr

act

of

agen

cy

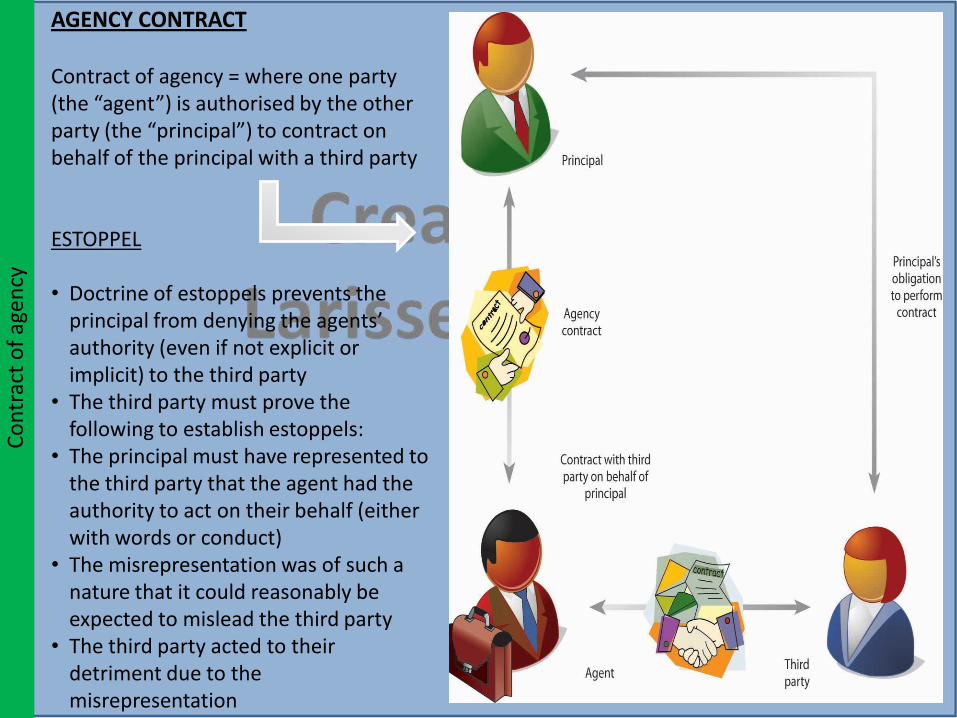

AGENCY CONTRACT Contract of agency = where one party (the “agent”) is authorised by the other party (the “principal”) to contract on behalf of the principal with a third party ESTOPPEL • Doctrine of estoppels prevents the

principal from denying the agents’ authority (even if not explicit or implicit) to the third party

• The third party must prove the following to establish estoppels:

• The principal must have represented to the third party that the agent had the authority to act on their behalf (either with words or conduct)

• The misrepresentation was of such a nature that it could reasonably be expected to mislead the third party

• The third party acted to their detriment due to the misrepresentation

Co

ntr

act

of

agen

cy

RATIFICATION •Where a professed agent enters into a contract with a third party BUT does not have the authority to do so, the principal may ratify the contract •Effect of ratification = contract is deemed to have been authorised from the start •5 requirements for valid ratification:

1. Purported agent must profess that he has authority 2. Principal must be names or ascertained 3. The act must not have been contra boni mores or illegal 4. Principal must have existed at the time of the transaction 5. Principal must ratify the contract within a reasonable time after

the unauthorised act

Co

ntr

act

of

agen

cy

DUTIES OF THE AGENT 1. To perform the mandate • agent must perform the mandate fully and faithfully • enough where the agent substantially performs 2. To be honest and act in good faith • agency creates a fiduciary relationship of trust and therefore the agent must act in the interest

of the principal and not his own benefit • agent cannot make secret profits • agent cannot place himself in apposition where there might be a conflict of interests • agent must personally perform and cannot delegate the authority to another person • cannot disclose confidential information which may be to the detriment of the principal 3. To exercise due care • agent must perform mandate with the care, skill and diligence which is reasonably required 4. To act in accordance with the principal’s instructions • agent must act according to and within the scope of the given authority 5. To allow the principal to inspect the books and to render an account to the principal • agent must render a true and full account of all the transactions performed as agent • the principal must be allowed to inspect all the books regarding the transaction • the property of the agent and the property of the principal must be kept separately

Co

ntr

act

of

agen

cy

DUTIES OF THE PRINCIPAL 1. To pay the agent the agreed remuneration if the mandate is (substantially) performed • only when the agent has substantially performed and there was an agreement that

remuneration would be paid or it is a trade usage to trade • where there is no agreement regarding remuneration the principal must pay a

reasonable remuneration in the circumstances 2. To reimburse the agent for expenses incurred • for all the necessary expenses incurred 3. To indemnify the agent for all the losses suffered as a result of executing the mandate • the agent must be indemnified by the principal for all the loss and liability incurred in

the execution of the mandate OR which is directly caused by the mandate • only losses incurred in execution of the mandate

Corresponding counter right/duty

Co

ntr

act

of

agen

cy

TERMINATION OF THE AGENCY CONTRACT There are 8 ways wherein a contract of agency may be terminated: 1. Mutual consent of the parties; 2. Revocation by the principal; 3. Renunciation by the agent; 4. Due performance of the respective obligations; 5. On expiry of the period of time for which the authority was

granted; 6. Death of either party; 7. Where the principal is no longer mentally fit; and 8. Where the principal becomes insolvent.