lessons in restructuring defense industry: the french

TRANSCRIPT

Lessons in Restructuring Defense Industry:The French Experience

INTRODUCTIONThroughout the post-war era, France has sought to

remain a strong and independent military power.Beyond the defense of the homeland and overseasinterests, French military forces serve a politicalrole: to confirm France’s international status as amajor power, to preserve its independence in foreignand security policy, and to restore a sense of nationalpride after the bitter military defeats in World WarII and Indochina and the loss of Algeria and the restof the colonial empire. To these ends, successiveFrench Governments have developed a small-scaleversion of a superpower arsenal with three distinctelements:

●

●

●

an independent nuclear deterrent based on a“triad” of submarines, bombers, and ballisticmissiles; l

conventional land and air forces, manned largelywith conscripts, for the defense of the Frenchhomeland and Central Europe; anda largely professional Rapid Action Force(established in 1983) and a blue-water Navy forintervention in overseas crises of limited scopeand intensity, mainly in France’s former Afri-can colonies, the Middle East, and the PersianGulf.

The U.S. defense budget is about 10 times the sizeof the French allotment, and the two defenseindustries are structured very differently. Whereasthe French defense industrial base consists mainly ofsole-source contractors owned wholly or in part bythe state, the U.S. base is dominated by competingfirms in the private sector and enjoys a much largerdomestic market. Nevertheless, the two defenseindustries share some basic characteristics that makethe French case relevant to U.S. policy. Like theUnited States, France supports a large militaryestablishment with overseas responsibilities; pro-duces the full spectrum of major weapon systems,

including fighter aircraft, main battle tanks, nuclear-powered submarines, aircraft carriers, and tacticaland ballistic missiles; and invests heavily in militaryresearch and development, devoting more than athird of all government R&D spending to defense-related programs.

Over the past few years, France has also accumu-lated some useful experience in restructuring de-fense industry. The United States pursued a militarybuildup during much of the 1980s and has onlyrecently begun to react to cuts in defense spendingresulting from the end of the cold war. France, incontrast, has had to rationalize its defense industrysince the late 1980s in response to economicconstraints, including overcapacity in the broaderEuropean industry and slumping export sales. Forthis reason, France has implemented a number ofstrategies for restructuring its defense-industrialbase while preserving core technological assets andstrengthening its competitive position in worldmarkets.

Although the French system of military procure-ment evolved in response to a different set ofeconomic and political conditions than those in theUnited States, several aspects of France’s experi-ence with restructuring its defense industry arerelevant to U.S. policymakers facing a similarchallenge in the coming years. This paper assessesthe pros and cons of the French procurement systemand draws some practical lessons from the success orfailure of various restructuring strategies.

Challenges to the Gaullist Paradigm

French autonomy in defense procurement datesback to the 17th century. During the period immedi-ately following World War II, the United Statessupplied a large share of France’s military equip-ment, but France returned to its historical tradition ofdefense-industrial autonomy after 1958, when Char-les de Gaulle became President of the Fifth Repub-

1 me Frmch ~uclem ~~e fome (&ce defiappe) ~mists of 5 Red~utabie.c@s nucl~-power~b~~tic-~ssile SUti~, which by 1993 ~be equipped with a total of 80 M-4 missiles carrying up to 480 warheads; 18 Mirage IVP bombers carrying Air-Sol Moyenne Portt?e (ASMP)air-to-surface missiles; and 18 S-3D intermediate-range brdlistic missiles equipped with single l-megaton warheads, deployed infkd silos onthe AlbionPlateau in southeastern France. France also possesses a sizable arsenal of tactical (“prestrategic”) nuclear weapons, including 45 Mirage 2000N andabout 20 SuperEtendurdaircraft armed with the ASMP missile. The current force of PMon short-range ballistic missiles, with a range of 120 @ willberepkuxdwith40Hu dt?smissiles having a range of 480~ but the new missiles will be stockpiled rather tbandeployed. Source: DiegoA. Ruiz Palmer,French Strategic Options in the 1990s, AdeZphi Papers No. 260 (Lmdon: International Institute for Strategic Studies, Summer 1991),pp. 6-8.

–3–

4 ● Lessons in Restructuring Defense Industry: The French Experience

lie. De Gaulle’s 1966 decision to withdraw Francefrom the integrated military structure of the NorthAtlantic Treaty Organization (NATO) symbolizedthe national independence sought by fostering adefense industry capable of producing the full rangeof major weapon systems.2

Since then, two “Gaullist” principles have shapedthe French approach to weapons acquisition: reli-ance on nuclear deterrence as the basis of Frenchsecurity, and the maintenance of a broad defense-industrial base to preserve France’s freedom ofaction in foreign and security policy. The prioritygiven to nuclear deterrence has resulted in theinvestment of about 30 percent of the French defensebudget for the acquisition, operation, and mainte-nance of nuclear weapons and delivery systems. Atthe same time, the pursuit of national autonomy hasled to procurement of the lion’s share of weaponsfrom French sources (sometimes in collaborationwith other countries), even when technically supe-rior or less expensive alternatives were availablefrom abroad. In order to reduce the unit costs ofFrench weapon systems to acceptable levels, thedefense industry relies on export sales, which makeit possible to amortize the costs of research anddevelopment (R&D) and industrial overheadthrough longer production runs.

Since 1989, however, the traditional Gaullistpolicies of nuclear deterrence and autonomy indefense procurement have been called into questionby a nexus of economic and political factors,including growing financial constraints, the processof European economic integration, and three majorgeopolitical changes that have transformed theglobal security environment.

The first of these major changes was the dissolu-tion of the Warsaw Pact and the disappearance of theSoviet military threat to Western Europe. With theend of the cold war, the French defense industryfaces significant cuts in defense spending ands “hrinking export markets. Over the next few years,

Photo credit: DGA/COMM

An Amethyste-class nuclear-powered attack submarineis comissioned at Cherbourg Naval Shipyard.

spending levels will remain fairly steady becauseseveral major weapon systems are still in theacquisition pipeline, including the Leclerc mainbattle tank, the Rafale fighter, the Charles de Gaulleaircraft carrier, the Amethyste-class nuclear-powered attack submarine, the Triumphant-classballistic-missile submarine, and the France-GermanTiger antitank helicopter. Nevertheless, the Frencharmed forces will be reduced in size by about 20percent by 1997, with a parallel drawdown in majorweapon systems.3 The French Air Force, for exam-ple, plans to cut its fleet of combat aircraft by morethan 10 percent over the next 5 years, from 450 toabout 390 aircraft.4

The 1992 French defense budget totals 195.5billion francs ($37.7 billion) excluding pensions, anominal increase of 0.5 percent over the previousyear but a net decline of 2.3 percent after inflation.Although 1992 procurement spending will remainunchanged at the 1991 level of F103.1 billion ($19.9billion), this figure represents a shortfall of F8.4billion ($1.6 billion) from the last 5-year planningtarget approved by the French Parliament in 1990.5

The downward trend in French defense spendingbecomes more apparent when viewed as a percent-

withdrawal the d, it has remained a member of NATO and continues to participate actively inalliance political forums such as the North Atlantic Council and the Senior Political Committee. Although France is not a member of the Conferenceof National Armaments Directors (CNAD), which coordinates NATO collaborative arms development and production programs, it does belong to theIndependent European Programme Group including all NATO allies except Iceland, and the United States. The was established

1976 for the purpose of bringing France into European collaborativearmaments programs. t. Times,

4 de “ “French Cutbacks Will Squeeze Tiger, NH-90 Copter Projects,” News, vol. 7, No. 8, Feb. 24, 1992, p. 54. de Opposition Rails Against Defense ” Defense News, vol. 6, No. 47, Nov. 25, 1991, p. 8. All

conversions are based on an exchange rate of to the U.S. dollar, the rate in effect on Jan. 6, 1992.

Lessons in Restructuring Defense Industry: The French Experience ● 5

250

200

150

100

50

0

Millions of French francs

Figure l—French Defense Budget Trends

1986 1987 1988 1989 1990 1991 1992Defense budget

SOURCE: French Ministry of Defense

age of the gross domestic product (GDP). (See figure1.) Between 1981 and 1992, the French defensebudget declined from 4.2 percent to 3.26 percent ofGDP, and Defense Ministry sources suggest that thebudget will fall to 3.15 percent of GDP after 1993.6

To support the modernization of its nuclear deterrentwithin a restricted budget, France will have to limitits investment in conventional forces, causing manyweapons programs to be stretched out and delayed.For example, the anticipated cuts in defense spend-ing will cause initial production deliveries of theFrance-German Tiger antitank helicopter to bedelayed by 2 years, until 1999.7

The second geopolitical change was the unifica-tion of Germany in October 1990. Although Franceand Germany have been close allies since the 1960s,France seeks to anchor an increasingly powerful andassertive Germany within multilateral Europeaneconomic, political, and military structures so as topreclude a resurgence of the rivalry that proved sodisastrous to French security in the past. Theongoing process of France-German security cooper-ation is likely to include a deliberate effort tointegrate the two countries’ defense industries, with

Percent of gross domestic product (GDP)*41

3 -

2 -

1-

0’1986 1987 1988 1989 1990 1991 1992 1993

(est.)*GDP corresponds to the gross added value (including

value-added taxes) of goods and market services

the political aim of strengthening bilateral militaryties at the core of an increasingly unified EuropeanCommunity. This trend was reflected in the jointproposal in October 1991 by French PresidentFrancois Mitterand and German Chancellor HelmutKohl for the creation of a European army corps builton the basis of an existing France-German brigade.8

The third geopolitical change was the PersianGulf War, which increased the salience of “out-of-area’ threats to French security. After the loss of thecolonial empire, the clear priority of French defenseplanning shifted to deterring aggression by theSoviet bloc, and Paris never envisioned the large-scale use of conventional forces outside CentralEurope.9 Instead, French expeditionary forces weredesigned for rapid, small-scale interventions inAfrica, the Middle East, and other trouble-spots. Asa result, France was not prepared for a contingencylike the Gulf War, which required the deployment ofheavy conventional forces over long distancesagainst a well-equipped adversary, and where nu-clear deterrence was not politically credible. In thecoming years, France must decide if it can affordboth a sophisticated nuclear deterrent and large

de “ “Top French Officials Debate Changes in Military,” News, vol. 6, No. 36, Sept. 9, 1991, p. 42. For purposes of the U.S. defense budget peaked at 6.5 percent of GDP in 1985, fell to 5.5 in 1992, and is expected to drop to about 3.4 percent by

1997.7 op. cit., 8 Jacques and Jean-Pierre “MM. Mitterrand et Kohl proposent de les en de

Oct. 17, 1991, p. 1. of French forces demonstrate Political

perform a test the intentions of the adversary, and conduct a national deterrent maneuver to the adversary to reassesshis objectives. See David S. France’s Deterrent Posture and Security in Europe: Part Z: Capabilities and Doctrine, Papers, No. 194(London: International Institute for Strategic Studies, Winter 1984/5).

6 ● Lessons in Restructuring Defense Industry: The French Experience

conventional forces capable of carrying out majorinterventions overseas.

France played a relatively minor supporting rolein Operation Desert Storm for a number of reasons,both political and technical.10 Constraints includedFrance’s lack of investment in conventional militaryreadiness and its heavy reliance on conscripts, whichcreated political inhibitions on their deploymentoutside Europe.

11 Earlier French arms sales to Iraqfurther complicated the situation. During the aircampaign, for example, top-of-the-line French Mi-rage fighters deployed to Saudi Arabia were not usedin combat because of concern that they might beconfused with Iraqi Mirages and shot down bycoalition forces.

The Gulf War also revealed deficiencies in Frenchweapons and power-projection capabilities.France’s small fleet of transport aircraft was notsufficient to sustain an operation requiring heavylogistical support, and the French Air Force’sobsolescent Jaguar attack aircraft were not equippedwith night avionics or advanced radar systems andthus could not fly sorties at night or in bad weather.In addition, French forces suffered from a shortageof stockpiled munitions, such as laser-guided bombs.Although the French Army’s 6th armored (“Da-guet”) division successfully carried out a flankingand screening maneuver during the ground cam-paign to liberate Kuwait, its relatively light equip-ment made it incapable of conducting a frontalassault against Iraqi armored units. Finally, thedecision to defer replacement of the French Navy’saging carrier-based aircraft until the next-generationRafale fighter becomes available meant thatFrance’s two aircraft carriers lacked an effectiveself-protection capability. As a result, the carrierswere either kept in port or served as cargo ships fordelivering trucks and helicopters to the theater ofoperations.

In sum, a nexus of economic, political, andtechnological factors will necessitate a major re-structuring of the French defense-industrial base if

France is to bridge the growing gap between theprominent role it aspires to play in world affairs andits limited economic resources.

INDUSTRIAL STRUCTUREWhile competition exists at the level of subcon-

tractors and suppliers, the French domestic marketfor military airframes, aero-engines, and armoredvehicles is not large enough to support more thanone prime contractor in each of these sectors. As aresult, the French Government has promoted theconsolidation of those portions of the defense baseconsidered vital both to national security and thecountry’s overall economic growth. Since militaryaerospace and defense electronics are closely linkedto “strategic’ civil industries (aeronautics, spacesatellites, telecommunications, computers, and elec-tronics), many defense prime contractors and theirassociated civil-sector industries have been com-bined into large conglomerates known as “nationalchampions.

The national champions dominate the domesticdefense business in their sectors, and each is the soledepository of design and systems-integration know-how for an entire category of defense equipment.12

Examples include Dassault Aviation for fighteraircraft, Aerospatiale for helicopters and ballisticmissiles, GIAT Industries for main battle tanks andartillery, Matra for air-to-air missiles, and theNational Company for the Design and Constructionof Aircraft Engines (SNECMA) for military aero-engines. (See table 1.) At the same time, the FrenchGovernment believes that vertical integration ofdefense industries is not desirable and has sought tomaintain a diverse vendor base of competing sub-contractors and suppliers, many of them small andmidsized fins.

Nearly four-fifths of the French defense industryis owned directly or indirectly by the state, either inthe form of government-owned and operated arse-nals, nationalized companies (e.g., Aerospatiale,

10 ~eufited K@jom ~i~ ~-y ~o-~d~ ~~ ~iz~ of Fr~~e’s, deploy~ to tie pers~ G~~eXpeditiO~ COrpS of 35,000 trOOpS, COIUpiUd

with the 11,000 troops in the French Daguet division. Moreover, French Defense Minister Jean-Pierre Chevimement did not want to put French forcesunder U.S. operational control and thus deployed them at Al Asha-far from the U.S. and British forces stationed at Dhahran-s o that they couldundertake operations in an autonomous fashion. Chevi2mement resigned on Jan. 29, 1991, soon after the start of the coalition’s major air offensive. Hewas replaced by Pierre Joxe, who agreed to put French forces under U.S. command during the ground campaign to liberate Kuwait.

11 k tie ~te~~ of tie Gulf War, Fr~ce has men steps to reorganize more of its conventional forces into d@rOfCMiOIUd UdS Suitable fOr USein military operations outside Europe.

12 U.S. conwe5S, offke of Technology Assessment Global Arms Trude, OTA-ISC4160 (Washington DC: U.S. Government Prinfig Office, June1991), pp. 72-73.

Lessons in Restructuring Defense Industry: The French Experience ● 7

Table l—Major French Defense Contractors

Sector/company Types of production Examples of products

AerospaceAerospatiale . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dassault Aviation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SNECMA(National Company for the Designand Construction of Aircraft Engines) . . . . . . . . . . . . . . . . . .

Matra . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SEP(European Propulsion Company) . . . . . . . . . . . . . . . . . . .Turbomeca . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Naval constructionDGA/Directorate of Naval Construction . . . . . . . . . . . . . . . . . . .

Chantiers del’Atlantique (GEC-Alsthom) . . . . . . . . . . . . . . . . .Constructions Mecaniques de Normandie . . . . . . . . . . . . . . . .Societe Francaise reconstructions Navales . . . . . . . . . . . . .

Land armamentsGIAT lndustries. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Renault Industrial Vehicles . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Thomson-Brandt Armaments . . . . . . . . . . . . . . . . . . . . . . . . . . .Creusot-Loire Industries . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Panhard et Levassor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Defense electronicsThomson-CSF . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SFIM(Company for the Fabrication ofMeasuring instruments) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Dassault Electronique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

SAGEM (Company for General Applications ofElectricity and Mechanics) . . . . . . . . . . . . . . . . . . . . . . . . . . .

Societe Anonyme deTelecommunications (SAT) . . . . . . . . . .Sextant Avionique . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Alcatel Thomson-Faisceaux Herziens . . . . . . . . . . . . . . . . . . . .

Alcatel Espace . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Unilaser . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sogitec . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

OtherSNPE(National Companyfor Powder and Explosives) . . . .Constructions lndustrielles de la Mediterranee (Calm) . . . . .

Messier-Bugatti . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Hispano-Suiza . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Auxilec . . . . . . . . . . . . . .. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .SAFT(Company for Fixed Accumulators and Traction) . . . .Intertechnique. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Labinal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sochata-SNECMA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sopelem . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .Sogerma-Socea . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Souriau et Cie . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Ballistic missiles

Prestrategic missilesTactical missiles

Helicopters

Transport aircraftFighter aircraftTrainersMaritime patrol planes

Aero-enginesAirdelivered missilesTactical missilesMilitary satellitesSolid-fuel propulsionAircraft and helicopter engines

Submarines, warships

Frigates, corvettes, support shipsShips of less than 1,500 metric tonsShips of less than 1,000 metric tons

Armored vehicles, tanks, artillery, munitionsArmored vehicles, tactical vehiclesMortars, munitions, air-delivered bombsArmored vehiclesArmored vehicles, tactical vehicles

S-3, S-4 ICBMsM-4, M-45, M-5 SLBMsPluton, Hades, ASMPAntitank (HOT, Milan)Ground-air (Roland, Aster)Air-ground (AS-1 5, AS-30, Exocet, ANS)Gazelle, Dauphin, Lynx, Super Puma,

Tiger, NH-90Transall, EpsilonMirage F1, Jaguar, Mirage 2000, RafaleAlpha JetAtlantic 2

ATAR, M53, M88, TyneAir-air Magic, Super 530, MICAGround-air Crotale, MistralSyracuse, HeliosSolid fuel for ballistic and tactical missilesArriel, Makila, RTM 322, MTM 390

Ballistic missile submarines, attack submarines,nuclear aircraft carriers, frigates

Test and measurement ships, patrol frigatesRapid patrol boatsVarious ships

AMX-10, AMX-30, Leclerc, 155mm AUF1Armored reconnaissance vehiclesBAP-1OO bombAMX-13Light Armored Vehicle (VBL), Light Auto-

Machinegun (AML), P4 tactical vehicle

Command-control systems, antiair weaponsystems, radars, sonars, optoelectronics,simulation, telecommunications, electronicwarfare, components

Stabilized sighting systemsRadars, seekers, calculators, counter-

measures

Navigation systems, fire-control systems,optoelectronics

Radio communications, optoelectronicsAvionics, navigation systems, fire-control,

automatic testingMicrowave links, satellite communication earth

stationsSatellite communication systemsLasersSimulators

Solid fuel, powder and explosivesCombat engineering equipment, welded

assembliesLanding gearsAeronautical equipmentMotors and electric generatorsBatteries, power suppliesFuel systems, air conditioning, oxygenCable, connectors, motorsEngine repairOptics, night-vision systemsVarious aeronautic equipment, aircraft main-

tenanceConnectors

SOURCE: DGA/COMM, L’lndustrie Frerpise de D4fense, June 1990, pp. 20-21.

8 ● Lessons in Restructuring Defense Industry: The French Experience

GIAT Industries, and SNECMA13), or firms inwhich the government owns a large share of thestock (e.g., Dassault Aviation, Matra, and Thomson-Brandt Armaments) .14 The nationalized French de-fense firms do not face the same pressures as privatefirms to provide a short-term return on investmentand can also obtain loans and government subsidiesthat private firms would not receive. In recent years,however, the downturn in defense spending hascaused the nationalized companies to have relativelylittle capital compared to private firms.

Since 1981, when Francois Mitterrand becamePresident, the French Government has only partiallynationalized the private defense sector so as to givethese firms continued access to capital markets.Thus, although the government holds 59 percent ofthe stock of the defense-electronics firm Thomson-CSF and 49 percent of the stock of DassaultAviation, both companies are still listed on the Parisstock exchange. At the same time, ownership of alarge share of the stock gives the governmentconsiderable influence over the semiprivate defensefins. In the case of Dassault, the state is a minoritystockholder but controls more than 50 percent of thevoting rights by virtue of some double-vote shares.The government has yet to exercise its majorityvoting power, but Dassault management must takethis possibility into account.

Export Dependence

The small size of the French domestic armsmarket means that the defense industry reliesheavily on export sales to permit the economicprocurement of weapons for France’s own use byamortizing research and development (R&D) andoverhead costs over longer production runs. Becauseof the spiraling cost of defense R&D, the exportdependence of the French industry has grownrapidly: exports accounted for 18 percent of defenseproduction in 1970, rose to 42 percent in 1985, andstabilized at about 33 percent in 1988.15 Some

Figure 2—French Arms Exports, 1974-90

Billions of current French francs70

60

50

40

3020

10

07 4 7 5 7 6 7 7 7 8 7 9 8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0

Year

Orders

SOURCE: DGA

defense-industrial sectors

Deliveries

are heavily dependent onexports: Aerospatiale sells 90 percent of its helicop-ters and Dassault 60 percent of its combat aircraft toother countries. Because of this structural depend-ence on foreign sales, the French Government takesexport potential into consideration when launchinga new development program, and the timing ofFrench military procurements is often tailored tomeet the needs of overseas customers.l6

Despite such efforts, however, French arms ex-ports have declined sharply in recent years, particu-larly since the end of the Iran-Iraq war in 1988. (Seefigure 2.) From a highpoint of F61.8 billion ($11.9billion) in 1984, orders fell to F25.3 billion ($4.8billion) in 1986 and F20 billion ($3.9 billion) in1989. Although the industry recovered some lostground in 1990 with orders of F33.4 billion ($6.4billion), they declined again in 1991. For DassaultAviation, for example, 1991 sales dropped 16percent and new orders by 25 percent from their1990 levels.17 (See figure 3.) Aerospatiale’s neworders in 1991 also plunged 50 percent from the yearbefore.18 SNECMA is facing an all-time low in

of French state 97.11 percent of shares, United Corp. 1.73 Annual Report 1990, p. 25. (Paris: Presses Universities de France, P. 30.

15 de

June 1990), p. 12. programs are completely independent of the export

de “ BAe Expect Contracts on Anglo-French Fighter,“ News, vol. 7, No. 8, Feb. 24, 1992, p. 20.

18“Aerospatiale the vol. 17, No. 14, Apr. 4, 1992, p. 555.

Lessons in Restructuring Defense Industry: The French Experience ● 9

Figure 3-Dassault Aviation Annual Orders, 1986-91

-- Billions of French francs20

15

10

5

01986 1987 1988 1989 1990 1991

SOURCE: Aviation

orders of military aero-engines, and Matra’s sales oftactical missiles have declined because missileexports are linked to purchases of military aircraft.Moreover, France will probably have to write offmore than F7 billion ($1.4 billion) in unpaid armssales to Iraq. According to one analysis, “Withinflation factored in, France’s arms industry hasbeen losing ground year after year.”19 A forecast ofaerospace sales by the Group of French AerospaceIndustries (GIFAS), an industry association, predictsa decline in defense business until after 1995, whensome weak growth is expected because of the needto replace current-generation equipment.20

French arms exports have been adversely affectedby a number of factors, including falling oil prices,growing competition from traditional suppliers (theUnited States and Britain), the emergence of newcompetitors (Israel, Brazil, and China), and thedumping of used East European weapons on theworld market. The effectiveness of U.S. armamentscombat-tested in the Gulf War may also reduce thecompetitiveness of French products. Finally, theleading Western supplier nations may agree to limitarms transfers to the Mideast, historically France’slargest export market. Indeed, the French role inproviding 20 percent of Iraq’s major weapon sys-tems between 1980 and 1989 has provoked at leasta temporary reassessment of the wisdom of large-scale arms transfers to areas of conflict.

The decline in French arms exports has affectedthe defense-industrial base both directly, by reduc-ing levels of production, and indirectly, by under-mining the funding mechanism for defense R&D.Although the government pays for most defense-related research, industry must cover a significantshare of the costs of weapon-system developmentout of profits from foreign sales. During the negotia-tion of an R&D contract, the government and thecompany make an initial assessment of the system’sexport potential and determine on this basis aformula for an equitable sharing of R&D costs.Thus, the greater a system’s predicted export sales,the larger the share of development costs that mustbe borne by industry. This cost-sharing formula maybe renegotiated later if the export prospects of thesystem improve or worsen significantly. On average,government funding for weapon-development pro-grams covers only about 40 to 60 percent of industryneeds--compared to about 80 percent in the UnitedStates. The precise funding split can vary consider-ably, however, depending on the industrial sector,the firm, and the system being developed. (Fundingsplits for Thomson-CSF and SNECMA are shown infigure 4.)

The requirement that defense contractors inter-nally finance a significant share of their develop-ment costs has given rise to a number of problems.First, joint funding has created strong pressures forarms exports, leading to some questionable sales.Second, company financing of R&D has enabled theFrench Government to launch more weapons-development programs than it can afford to carrythrough to completion, resulting in costly stretch-outs and delays. (This problem has also beencommon in the United States.) Third, the recentdecline in arms sales has reduced the pool of moneyavailable for company-funded R&D.

As long as arms-export markets were strong, thestructural problems associated with corporate fund-ing of development out of profits from foreign saleswere not apparent. Dassault’s export profits, forexample, enabled the company to finance 50 percentof its R&D costs and gave it the flexibility to pursueindependent programs like the Mirage 2000-5,which was developed strictly for export without

19+ ’ FBIS translation of article by L. Main Paris, Dec. 26, 1990, p. 5 Jan. 18, 1991, pp. 33-34).

20 “French Down 1990, But Deliveries Aviation Week & Space Technology, vol. 135, No. 13, Sept.30, 1991, p. 25.

323-947 0 – 92 – 3 QL:3

10 ● Lessons in Restructuring Defense Industry: The French Experience

10

9

8

7

6

5

4

3

2

1

0

Figure 4-Funding of Defense Research and Development

Thomson - CSF

Billions of French francs

1986

47% 39%

I I ,

1987 1988 1989 1990

percent of costs, company-funded

3

2

1

0

SNECMA

Billions of French francs

1

55%

I 1

58%

1986 1987 1988 1989 1990

Percent of costs, government-funded

SOURCE: Thomson-CSF, 1990 p. 4; Report 1990, p. 3.

The French Government takes a broad view ofstate assistance. (Ironically, Dassault was unable tosell this aircraft because foreign customers werereluctant to buy a system that the French Air Forcedid not plan to procure.) As export sales decline andfirms are less able to finance their development workinternally, the French Government will either haveto assume a greater share of the burden or engage inmore collaborative development programs withforeign partners.

MANAGEMENT OF THE BASE

The French Government, as favored customer andowner of a large portion of the defense-industrialbase, has two partially competing objectives: main-taining a broad defense-industrial base capable offurnishing the full range of equipment required bythe armed forces (even when superior or lessexpensive weapons are available from foreign sources);and procuring military systems at an affordable cost.Because of the central importance of the armsindustry to the country’s independent defense pos-ture and technology policy, France places consider-able emphasis on identifying and preserving keydesign and manufacturing skills in the major defensefins. The results of this comprehensive planning,programming, and budgeting effort are embodied inthe 5-year military programming law (which setsfinancial targets for defense procurement) and theannual defense budgets.

national defense as covering military forces, civildefense, and their economic and industrial underpin-nings, and integrates defense-industrial policy withother industrial, economic, and social policies. Thus,while the Ministry of Defense has the lead indefense-industrial policymaking, several nondefenseagencies also play important roles. At the highestlevel, there is a division of responsibility betweenthe French President and Prime Minister. ThePresident is supreme commander of the armed forcesand in charge of formulating national securitypolicy, whereas the Prime Minister coordinates themore routine aspects of defense planning, includingindustrial mobilization, wartime rationing, and civildefense. Reporting to the Prime Minister is theGeneral Secretariat of National Defense (SGDN), anadvisory body analogous to the U.S. NationalSecurity Council staff, whose activities includegeopolitical analysis, export controls on arms anddual-use technologies, and nonproliferation policy.The Ministry of Economics, Finance, and theBudget exerts a significant influence over the extentand content of French defense spending; the Minis-try of Industry and Foreign Trade is responsible forthe supply and rationing of industrial raw materialsin wartime; and the Ministry of Transportationcontrols the air and sea transport fleets. Oversightfunctions are performed by the Cour des Comptes,an investigative agency similar to the U.S. General

Lessons in Restructuring Defense Industry: The French Experience ● 11

Accounting Office, which audits the accounts of thenationalized firms and ensures that defense funds arespent within the guidelines of the law.

The French weapons-acquisition system reflectsFrance’s “statist” political system, with a strongexecutive and a relatively weak legislative branch.In contrast to the U.S. political system, which isbased on the principle of checks and balances amongcompeting power centers, the French parliamentarysystem involves a greater fusion of the legislatureand the executive. Thus, while each chamber of theFrench Parliament (National Assembly and Senate)has a Committee on National Defense and ArmedForces, these bodies exert much less oversight ofdefense and procurement policy than the ArmedServices Committees of the U.S. Congress.21 TheFrench Parliament votes the annual defense budgetand a 5-year military programmingg law providingfinancial targets for future procurement, but thesebills are largely spending envelopes and permit littleif any legislative control over individual weaponsprograms.

The General Delegation for Armaments

De Gaulle’s political goal of achieving nationalautonomy in the full range of armaments—particularly nuclear weapons—in the face of tightbudgetary constraints required the careful husband-ing and allocation of resources. To this end, in 1961de Gaulle replaced the weapons directorates report-ing to the individual armed services with a central-ized procurement agency known as the GeneralDelegation for Armaments (Delegation Generalepour l’Armement, or DGA).22 This organizationincludes all of the services and organizations withinthe Ministry of Defense responsible for the research,development, and production of defense equipment.The DGA is the linchpin of the French arms-procurement system, mediating among the politicalauthorities, the defense industry, and the militaryoperators. After the Parliament votes the defenseprocurement budget, the DGA allocates funds among

specific weapons programs. Because of this powerof allocation, DGA can ensure multiyear funding ofhigh-priority systems even within a shrinking de-fense budget.

The director of the DGA reports directly to theMinister of Defense and “has greater control overresearch, engineering, and industrial matters thanany other European-or American-defense offi-cial. ’ ’23 He oversees a staff of about 54,000 people,including career military or civil servants in scien-tific, technical, and management positions, andseveral thousand workers in the government-runarsenals, depots, and factories. Thanks to an elabo-rate system of recruitment and training, the seniormanagement positions in the DGA attract some ofthe best and brightest French students of engineeringand administration, who become specialists indeveloping sophisticated armaments and sellingthem abroad. At the top of the hierarchy is an elitecorps of about 1,000 “armament engineers,’ 80percent of them graduates of the prestigious EcolePolytechnique in Paris and 20 percent recruitedinternally. Increasingly, armament engineers alsooccupy the top executive positions in the national-ized and semiprivate sectors of the defense industry.

According to political scientist Edward A. Ko-lodziej, the DGA’s primary mission is “the preser-vation and promotion of an ever-modernizing armsindustry within an internationally competitiveFrench industrial system."24 The major tasks of theDGA are

●

●

●

●

to manage the definition, development, andproduction of military equipment for theFrench armed forces and for export;to certify that technical performance and costsare acceptable;to supervise the government-run arsenals andguide the nationalized and semiprivate defensefirms;to ensure the long-term health of the Frenchdefense industry; and

21 See David S. Yost “French Defense Budgeting: Executive DO minance and Resource Constraints,” Orbis, vol. 23, fall 1979, pp. 579-608.z ~o~er fipo~t motive for de Ga~e’s d~ision to shift authority over arms procurement from the individual armed services @ a cen@*d

agency reporting directly to the French President was to help gain control over the rebellious oflicer corps, which had brought down the Fourth Republicin protest over the loss of Algeria and threatened to destabilize the Fifth Republic as well. See Edward A. Kolo&iej, Making and Mar&eting Arms: TheFrench Experience andZts Implications for the International System (Princeto~ NJ: Princeton University Press, 1987), p. 243.

23 U.S. ConWess, office of ~~olog Assessment, Holding the Edge: ~ainraining ~~e ~e~ense T’&~nozogyBase, OTA-lSC-420 ~dlk@O~ ~:

U.S. Government Printing Office, Apr. 1989), p. 101.24 Kolo&iej, op. cit., fOoblOte 22, P. 258.

12 ● Lessons in Restructuring Defense Industry: The French Experience

● to adapt the defense industry to France overallindustrial needs.25

Since France relies primarily on single-sourcenational champions for most of its major weaponsystems, the DGA must impose administrativecontrols on price and quality, while simultaneouslycooperating with industry to maintain profits, em-ployment, and investment in new technologies sothat France will remain internationally competitive.In order to preserve the competencies of the defenseindustry, DGA officials often balance long-termindustrial considerations, such as the need to pre-serve design teams or to keep production lines open,against the operational requirements of the Frenchmilitary. The DGA’s industrial-policy goals must, ofcourse, be harmonized with the interests of theMinistries of Defense, Foreign Affairs, and Eco-nomics and Finance. When interagency conflictsarise, they are decided at the political level.

The DGA is divided into functional and technicalunits. (See figure 5.) Reporting to the director aretwo policymaking bureaus. The Delegation forArmament Programs (DPA) draws up plans forweapons development and procurement over theannual and 5-year budget cycles, while the Delega-tion for International Relations (DRI) negotiatesforeign arms sales and collaborative agreementswith other countries for the joint development andproduction of military equipment. In order to facili-tate arms sales, the DRI arranges attactive credit andfinance terms for foreign arms buyers, guaranteesloans, and provides insurance for companies andbanks against the special risks of the arms trade.

The DGA’s program-management functions arethe responsibility of five functional directorates andservices (for defense research, personnel, industrialaffairs, cost accounting, and quality control) and fivetechnical directorates (for ground armaments, navalconstruction, aeronautics, missiles and space, andelectronics and computing). The technical director-ates function in different ways depending on thedefense-industrial sector. Whereas the Directorate ofNaval Construction directs a complex of government-owned shipyards that produce, maintain, and over-haul most of the French Navy’s warships andsubmarines, the Directorate of Aeronautics negoti-

ates contracts with private and nationalized compa-nies.

The technical directorates also coordinate withthe French armed services to define R&D andproduction programs and priorities. Committeesmade up of service representatives and DGA offi-cials identify operational military requirements andtransform them into technical specifications. Al-though both sides strive to reach consensus, theDGA has the final say in the launching of adevelopment program. As a result, DGA officialsmay choose to balance short-term military needsagainst technical feasibility, export potential, andindustrial-base considerations.

Defense Research

France spends about F30 billion ($5.8 billion) ondefense research and development, or more than athird of the government’s entire R&D budget.Although civil and defense R&D are budgeted andadministered separately, defense R&D is expectedto benefit the overall economy. Some F8 billion($1.54 billion) of the defense R&D budget isallocated to “research,’ of which 20 percent goes tonuclear-weapons work under the auspices of theFrench Atomic Energy Commission and the rest isdivided up among other areas. In addition tocontracted R&D, the French Government draws onindependent research conducted by defense compa-nies. A portion of these R&D expenses are reim-bursed as overhead costs on defense contracts, in amanner similar to the U.S. Independent Researchand Development (IR&D) program. The reimburse-ment rate varies from 2 to 6 percent of contract cost,depending on the industrial sector and other criteria.

In May 1977, DGA reorganized its organizationfor defense research by creating a new Directoratefor Research, Studies, and Techniques (DRET). Thisorganization is analogous to the U.S. DefenseAdvanced Research Projects Agency (DARPA),although it lacks the latter’s flexibility and respon-siveness. With a staff of about 2,000, DRETcoordinates all defense-related research in the publicand private sectors, including work on “dual-use”technologies with both military and civil applica-tions. Each year DRET directly funds about 200medium- and long-term research programs at twogovernment-supervised laboratories: the Institut de

~ U.S. Cowess, Office of lbchnoloW Assessment, Holding the Edge: Volume 2: Appendices (Wdingtonj DC: U.S. Gov-ent fi@ Office,1989), p. 139.

Lessons in Restructuring Defense Industry: The French Experience ● 13

Figure 5-Organization of the DGA

GeneralDelegate

for Armaments

Assistant Director

m mPrograms Relations

I

I II

CentralService

forIndustrial

Affairs

Servicefor the

Investigationof

Armamentcosts

1

Servicefor

IndustrialSurveillance

ofArmament

I

Directoratefor

Research,Studies,

andTechniques

Directoratefor

Personneland

GeneralAffairs(DPAG)

ArmamentSchools

I

I

Centerfor

AdvancedArmament

Studies

Technical Directorates

SOURCE: DGA/COMM

14 ● Lessons in Restructuring Defense Industry: The French Experience

Saint Louis (ISL), a France-German center forballistics and explosives research, and the NationalOffice for Aerospace Studies and Research (ONERA).DRET also awards contracts to industrial labs and touniversities, which conduct 10 to 15 percent ofFrench defense research. Since university personnelare paid by the Ministry of Education, DRET canleverage its assets by financing only those additionalfacilities required for defense research.

In addition to its funding role, DRET is responsi-ble for monitoring defense-related developments inscience and technology both within and outsideFrance, and bringing them to the attention of thetechnical directorates. DRET also defines the na-tion’s defense research priorities on an annual basis.This task is carried out by 30 internal workinggroups staffed by armed-service representatives andDGA engineers. The working groups are organizedaccording to scientific field (e.g., materials, elec-tronic components, aeronautical systems) and opera-tional area (e.g., air defense, artillery). Eight “syn-thetic” working groups then assess research priori-ties for each armed service and allocate findingshares. (DRET attempted to develop a “CriticalTechnologies List” but abandoned the effort asinconclusive.)

French defense-research priorities are shifting inresponse to the emerging international securityenvironment. The Gulf War demonstrated the funda-mental importance of command, control, and com-munication technologies; of surveillance from spaceand on the battlefield; of stealthy weapon systems;and of long-range, precision-guided weapons likethe U.S. Tomahawk cruise missile. In response tothese lessons, DRET is intensifying its researcheffort in electronics, sensors, space systems, andadvanced munitions, while reducing its emphasis onthe fining platforms themselves. Funding for militaryspace programs rose by more than 17 percent in the1992 defense budget. Current plans call for develop-ing a series of military reconnaissance satellites thatwill be equipped with optical cameras, equipmentfor intercepting signals and communications, andsynthetic-aperture radar for 24-hour, all-weatherimaging. 26

Controls on Price and Quality

Two functional services within DGA are respon-sible for oversight and control of the defense

industry. The Service for Industrial Surveillance ofArmament (SIAR) certifies the technical quality oftested French weapons and foreign equipment pur-chased for the French forces, while the Service forthe Investigation of Armament Costs (SECAR)performs cost audits of all major procurementprograms. DGA officials contend that because thestate is the single dominant customer for defenseproducts, administrative controls on quality andcosts are more effective than relying on marketmechanisms such as competition. According to thisview, competing prime contractors tend to makeunrealistically low bids, resulting in cost overrunsthat must be absorbed by the government. Incontrast, if single-source firms are assured of aregular flow of business, they can engage inlonger-term planning that reduces overhead costs.

The DGA has used fixed-price contracts success-fully by working closely with industry to ensure anequitable sharing of costs based on a system’stechnical specifications and export potential. Con-tracts are renegotiated if export prospects change orperformance specifications become more demand-ing. DGA officials also contend that the intern-ational competition for export markets creates incen-tives for quality and price discipline, although theyadmit that arms sales are greatly influenced bypolitical and strategic considerations. In recentyears, however, the costs of some major weaponsprograms (such as the Leclerc tank and the Charlesde Gaulle aircraft carrier) have spiraled-in somecases 40 percent over initial estimates-raisingquestions about the effectiveness of administrativecontrols and the lack of domestic competition at theprime-contractor level.

Control of Arms Exports

French arms-export policy has been formulatedsince 1955 by an interdepartmental coordinatingbody called the Interministerial Commission for theStudy and Export of War Materials (CIEEMG),chaired by the General Secretariat for NationalDefense. Made up of representatives from theMinistries of Defense, Foreign Affairs, Economicsand Finance, and Industry and Foreign Trade, thisgroup is responsible for advising the Prime Ministeron proposed arms sales and for recommendingchanges in overall arms-export policy. In evaluatingproposed sales, the CIEEMG considers both defense-

X Giov@ de Briganr.i and Peter B. de Selding, “France TO Widen Spwe Efforts,” Defense News, vol. 7, No. 5, Feb. 3, 1992, pp. 4,37.

Lessons in Restructuring Defense Industry: The French Experience ● 15

industrial needs and the political and strategic statusof the requesting country. For example, the transferof French arms to Iraq during the Iran-Iraq War wasauthorized by the highest political levels for strate-gic reasons, with industrial considerations playing asecondary role. Even so, the CIEEMG is stronglyinfluenced by the DGA’s Directorate of Interna-tional Relations, which prepares all of the files forcommission review and tends to be a proponentrather than an arbiter of arms sales within the FrenchGovernment.27

Defense Industrial Policy

The functional directorate of the DGA responsiblefor defense industrial policy and planning is theCentral Service for Industrial Affairs (SCAI). Itmonitors the activities and financial health ofdefense fins, maintains a centralized databasecontaining this information, and prepares analysesof actions aimed at improving the competitivenessand profitability of the French defense industry.SCAI also sets out guidelines for defense contractsand industrial practices and suggests ways to en-hance the contribution of the defense industry toFrance’s economic development and the competi-tiveness of its civil industries.28

In contrast to the technical directorates, SCAI hasa broad vision of France’s defense-industrial needsthat focuses on industrial development and theexpansion of defense trade over the immediaterequirements of the armed services. This emphasison the long-term health of the French defenseindustry sometimes conflicts with the DGA’s otherroles as producer, controller, and customer ofmilitary equipment. For example, in order to pre-serve sufficient industrial capacity to meet nationalprocurement objectives, SCAI might advise theDirectorate for Aeronautics to award a developmentcontract on a competitive basis but give the losingbidder a share of the production work to keep bothfirms in business, even if this approach increasesoverall procurement costs. Similarly, SCAI mightrecommend keeping an assembly line open bystretching out the procurement of a current item untilthe next system enters production.29

Administrative Guidance

State directives assign the DGA responsibility foradministrative guidance (tutelle) of the defenseindustry. DGA officials seek a balance betweengiving the industry the freedom to compete ininternational markets and preserving a nationaldefense-industrial base that responds to Frenchmilitary and social needs. One type of administrativeguidance involves the direct management of gov-ernment-owned and operated arsenals, such as thenaval shipyards run by the Directorate for NavalConstruction. A second type of guidance derivesfrom the power of the French state as the primarycustomer of the defense industry and a majorshareholder of the nationalized and semiprivatedefense companies. The chairmen of the national-ized defense firms are named by the President on therecommendation of the Prime Minister and theMinisters of Defense, Finance, and Industry, andgovernment representatives sit on the companies’boards of directors. While DGA officials do notintervene in day-to-day company operations, theymust concur in major strategic decisions such aslarge investments, new ventures, or internationalcollaborative programs.

When conflicts of interest between governmentand industry arise, they are worked out in secret, farfrom the public spotlight. The DGA’s influence overthe defense industry is offset to some extent by thefact that the national-champion firms enjoy a func-tional monopoly in their respective industrial sec-tors. For example, since Dassault Aviation possessesthe only design team in France capable of develop-ing combat aircraft, the government must keep itsupplied with contracts to preserve its unique skills.In recent years, however, DGA officials havepromoted international collaborative programs as astrategy for countering the monopolistic practices ofnational-champion fins.

Industrial Mobilization

France no longer plans to complement peacetimedefense production with reserve industrial capacitythat could mobilize in crisis and war. Since theFrench defense base is increasingly integrated intothe broader civil economy, competitive pressures to

27 Kolodziej, op. cit., footnote 22, p. 266.

2 Ibid, p. 259.~Fer-d MeMe, “Un Compl~e Mili@ro-~dustriel Fmn@is?” Jean-Christophe Victor (cd.), ARM-ES: France 3t%ze Grand: NOS SticZtegieS,

Chercheurs, Fabricants et Vendeurs (Paris: Autrement Revue, No. 73, Oct. 1985), p. 92.

16 ● Lessons in Restructuring Defense Industry: The French Experience

reduce overhead costs militate against maintainingsurplus capacity for wartime mobilization. As aresult, surge production of defense equipment incrisis or war would be limited to battlefield consum-ables such as conventional munitions, food, uni-forms, and selected spare parts. France also plans torely on its European allies to supplement domesticproduction.

In the belief that the conventional phase of anywar in Europe would be short, France has stockpiledrelatively small quantities of munitions. Moreover,the armed services typically protect high-priorityweapons programs from budget cuts by paring backspending on military readiness. The 1991 munitionsbudget, for example, was down 28 percent from theyear before and contained no money to purchaseantirunway bombs, cluster bombs, or laser-guidedbombs. As a result, France had to purchase laser-guided bombs and antitank missiles from Germanyduring the Gulf War; without this external source,there would have been only enough stockpiledmunitions for a week of combat.30 Of course, greaterreliance on allies assumes the compatibility offoreign munitions with French weapons, creating astrong incentive for collaborative development.

Pros and Cons of the FrenchProcurement System

France’s centralized, professional procurementsystem offers four main advantages. First, seniorDGA officials enjoy high prestige and morale andmanifest a strong sense of responsibility to the state.Moreover, whereas military officers move fre-quently from one position to another, DGA officialsremain with major weapons programs for severalyears, providing managerial expertise and institu-tional memory. Second, there is a more cooperativerelationship between the French Government andthe defense industry, in contrast to the largelyadversarial relationship in the United States. Onereason for the greater apparent harmony in theFrench case is that in an industry consisting largelyof monopoly suppliers and a single buyer, there islittle incentive for either party to criticize the systemopenly.

A third advantage of the French system is thatcentralization has enabled the French state to engagein multiservice procurements and to consolidate

R&D programs to avoid redundancy. In some cases,it has been possible to develop a single weaponsystem for all three armed services, such as theMistral air-defense system, or a basic airframe thatis then modified for Air Force and Navy missions,such as the Rafale fighter. More frequently, the DGAfunds joint programs to develop technologies of useto all three services, including missile guidance,command-and-control systems, and logistics man-agement; these technologies are then incorporatedinto service-specific weapon systems.

A final advantage of the French system is that theDGA has pursued a coherent strategy for managingthe defense industry. DGA officials seek to balancea variety of objectives, including force requirements,the health of both the defense base and the largercivilian industrial base, and political goals such asFrance-German cooperation. Because of the needfor tradeoffs among these objectives, the Frenchprocurement system is not designed to optimizeindividual weapon systems but rather to further thenation’s military, industrial, and political interests.

The frost two benefits of the French system—thehigh prestige of government service and cooperativegovernment-industry relations—are characteristicof most European countries and Japan, whereas thesecond two benefits—multiservice procurement pro-grams and a coherent defense-industrial strategy—are unique to France. Despite these advantages,however, the French procurement system suffersfrom a number of problems. The DGA’s mission ofpreserving an autonomous defense-industrial basehas sometimes been achieved by procuring nationalsystems that cost more, perform less well, or takelonger to procure than foreign-sourced weapons.France’s heavy reliance on exports also tends toovershadow domestic procurement needs; in somecases, foreign contracts for French weapons havereceived higher priority than national orders.

Thus, while French procurement policy is gener-ally coherent and well-managed, some critics ques-tion its overall effectiveness. In particular, the criticsargue that the political insulation of the Frenchprocurement system has resulted in a defense-industrial base that is too broad to be competitive,either economically or militarily. This overexten-sion is suggested by the undercapitalization of thenationalized defense companies. Furthermore,

~~erre ~~ouche, “L’Ecole de Guerre,” Le Point, MaK. 4, 1991, pp. 35-37.

Lessons in Restructuring Defense Industry: The French Experience ● 17

France’s extensive reliance on national championspromotes efficiency but lacks the benefits of compe-tition in promoting innovation and reducing costs.The existence of only one prime contractor in severalkey sectors also makes the system as a whole proneto a certain brittleness. If a monopoly producer likeDassault Aviation or SNECMA were to go out ofbusiness, France would lose a vital piece of itsdefense-industrial base.

Over the past decade, the French armed serviceshave become increasingly vocal in questioningDGA’s continued emphasis on domestic productionof the full range of weapon systems, which has ledin some cases to serious delays and cost overruns. Awell-publicized example was the decision to protectthe national program to develop the Rafale fighteraircraft despite soaring development costs31, diplo-matic pressures on France to participate in thefive-country European Fighter Aircraft program,and the French Navy’s preference for purchasing theU.S. F/A-18 Hornet to replace its obsolescentCrusader carrier-based fighter aircraft. A key moti-vation behind the decision to forge ahead with theRafale program was to maintain the design teams atDassault and SNECMA. French journalist JeanGuisnel has described the “collusion” among in-dustry executives seeking to preserve their exclusiveknow-how, Air Force officers reluctant to compro-mise their performance specifications, and DGAofficials determined to exercise their power andauthority .32 Because of the decision to proceed withthe Rafale program, the French Navy will have tokeep its aging Crusader fighters in service untilaround the year 2000, when the naval version of theRafale is scheduled to replace them. The negativeconsequences of this decision for the militaryeffectiveness of the French Navy during the GulfWar have already been mentioned.

A final drawback of the French procurementsystem is its lack of accountability to the Parliamentand the public. Hidden behind a veil of secrecy,DGA technocrats make procurement decisions in atop-down manner, and the lack of effective legisla-tive oversight mechanisms enables the DGA and thedefense industry to shield themselves from objectivecriticism. The absence of oversight in this closed,inbred system introduces a higher potential for abuse

Photo credit: DGA/COMM

A test pilot flies a prototype of the designedand built by Aviation.

or error. In addition, a dense network of informalitiesbetween the DGA and the defense industry results ina lack of bureaucratic checks and balances. Al-though France has conflict-of-interest statutes for-bidding ‘‘revolving-door’ moves between gov-ernment and industry (known as pantouflage inFrench), these laws have never been enforced. As aresult, senior DGA officials have moved to high-level jobs with the major defense firms. (Mobility inthe reverse direction also occurs to a lesser extent.)Since many top procurement and industry officialswent to the same schools and know one anothersocially, this old-boys’ network gives the armscomplex powerful political influence within theFrench Government and helps insulate it fromparliamentary and public scrutiny. According toKolodziej, the lack of external controls on theFrench military-industrial complex “hinders at-tempts to evaluate independently the economic andmilitary performance of the arms industry or topropose feasible and practical alternatives to theheavy reliance on foreign arms exports in maintain-ing economic productivity and in supporting Frenchtechnological development and competitiveness. ”33

STRATEGIES FOR INDUSTRIALRESTRUCTURING

Over the near-term, the major armaments pro-grams launched during the 1980s will slow the rate

and development of the through the demonstration and cost billion ($6.75 billion). en France (Paris: La 1990), PP.

op. cit., footnote 22, p. 298.

18 ● Lessons in Restructuring Defense Industry: The French Experience

of decline in French defense budgets. Even so, thedefense-industrial base has already begun to shrinkin response to the combined effects of reducedspending, increased competition for export markets,and the growing number of collaborative programs,which require the sharing of development andproduction work with other countries. Diminishedprocurement will force a major restructuring of theFrench defense-industrial base, with far-reachingconsequences for employment and regional plan-ning.

In 1989, the French defense industry directlyemployed about 261,000 people (including about75,000 engineers), or about 5.4 percent of thecountry’s industrial workforce. Taking account ofall the raw materials and components required forarms production, more than 400,000 French workerswere employed directly or indirectly by the defenseindustry .34 As a result of lower export sales andplanned cuts in defense spending, many of these jobsmay be at risk. A wave of aerospace layoffs inDecember 1991 was just the beginning; according tounofficial government estimates, defense-industrialrestructuring could ultimately result in the elimina-tion of between 10,000 and 100,000 jobs. TheFrench Government and the defense industry there-fore face a major challenge in managing the eco-nomic and social consequences of cuts in defensespending.

Because of the strength of French labor unions,industrial restructuring is more difficult in Francethan in the United States. Not only is it costly forFrench firms to fire workers, but large-scale layoffscan trigger strikes. Thus, while U.S. firms can adjustemployment levels on a short-term basis, Frenchdefense firms must engage in long-term socialplanning. Another problem is that, for historicalreasons, French defense industries and arsenals areconcentrated far from the border with Germany inless developed regions of central and southwesternFrance, which are heavily dependent on defenseproduction. (See figure 6.) As a result, closing downdefense plants may result in severe unemploymentin areas that are already economically depressed. Inorder to develop an economic conversion plan to

mitigate the social consequences of downsizing thedefense industry, French Defense Minister PierreJoxe established a “Restructuring Committee”within the Defense Ministry on August 30, 1991.35

At the same time, the DGA is pursuing arestructuring strategy that aims to consolidate thedefense industry but retain its strengths. The goal isto reduce overcapacity while maintaining sufficientactivity in key defense-industrial sectors to exceedthe threshold of economic production. According toa parliamentary report, the government’s strategy isfocused along two axes. The first axis seeks topreserve a broad range of technological competen-cies in individual firms, while the second axis aimsto give the French defense industry a leading role inthe restructuring of defense production on a Euro-pean scale.36 Although the DGA provides overallguidelines for industrial restructuring and intervenesto ensure the overall coherence of the transitionprocess, it is up to the companies themselves to takeinitiatives for adapting to the new environment(except in the special case of state-run arsenals). Themajor restructuring strategies are summarized in thefollowing sections.

Commercializing the Arsenals

While the aerospace and defense-electronics sec-tors in France consist of a mixture of private,semiprivate, and nationalized firms, the FrenchGovernment has traditionally owned and operatedarsenals for land armaments and naval vessels. Inrecent years, however, the government has moved tocommercialize these operations, freeing them fromlegal constraints and burdensome regulations thathave prevented the most economic use of equipmentand labor. Under French law, government-ownedand operated arsenals are not allowed to work forcommercial advantage and lack flexibility in ac-counting practices, inventory control, and invest-ment. They cannot produce goods in anticipation offoreign sales, use export-derived “profits” to fi-nance the development of new products, or keepproduction lines open between government orders inanticipation of foreign sales. Moreover, each pro-duction facility must be managed independently,

~D&6gation Wn6r~e pour l’hnernent, L’Indusm”e Fran~aise de ZXfense (Paris: DGA/COMM, June 1990), P. 12.35 De J3rigmti, op. cit., footnote 6.36 J~.~~hel Bouchemm Rapport fait au nom de la Commission de la D~ense Nationale et des Forces Armbes (1) sur 1e projet de loi de

programmation (no. 733) relatifd l’kquipment nu”litairepour les anm?es 1990-1993, Assembk$e Nationale, Premkre session ordinaire de 1989-1990,No. 879, Oct. 2, 1989, p. 683.

Lessons in Restructuring Defense Industry: The French Experience ● 19

Figure 6-Geographical Distribution of Defense-Industry Employment, 1988

Percentage employment indefense industry

less than 10/0

u 1 to

❑ .

%1% 2.5 to 50/0

5 to 7.5%0

❑ greater than 7.5°/0

SOURCE: DGA/COMM

without an overall corporate strategy. Because ofthese bureaucratic and commercial inefficiencies,the arsenals have been unable to compete effectivelyin export markets.

In July 1990, the Army arsenal, or IndustrialGroup of Land Armaments (GIAT), was convertedthrough legislation into a nationalized companycalled GIAT Industries.37 Although the FrenchGovernment still owns nearly all the firm’s capitaland retains considerable influence, GIAT has gainedfinancial autonomy, access to capital markets, anddecision-making authority. The new company hasset up a personnel department and sales office,negotiated collaborative agreements with a networkof international partners (including the British firm

vVickers and the German firm Rheinmetall), anddiversified its industrial activities into new fields,such as aircraft cannon pods and subcontracts for theproduction of aircraft parts. Nevertheless, the factthat the more than 11,000 GIAT workers retain theirprivileged job status within the civil-service systemstill limits the fro’s flexibility.

GIAT Industries’ largest weapons program is thenew Leclerc main battle tank, whose prospects areuncertain. When the program was launched in 1978,the French Army planned to purchase 1,400 Leclerctanks to replace its existing fleet of obsolescentAMX-30s on a one-for-one basis. Because of costoverruns and troop cuts, however, the Army nowplans to procure only 800 Leclerc tanks, and budget

No. 38, Sept. p.

20 ● Lessons in Restructuring Defense Industry: The French Experience

Photo credit: GIAT Industries

The new Leclerc main battle tank is produced by GIATIndustries, formerly a government-operated arsenal and

now a nationalized company.

cuts are likely to reduce the production rate from 100per year to less than 40.38 As a result, the unit costof the Leclerc is expected to reach about F37 million,or more than $7 million-compared to about $3million for the U.S. M-1 Abrams tank. Despite thishigh price, GIAT Industries still hopes to obtainmajor orders for the Leclerc from Saudi Arabia, theUnited Arab Emirates, Sweden, and Qatar.39

The last remaining French arsenals are the flight-test centers and aeronautical depots operated by theDirectorate for Aeronautics, which test, repair, andmaintain military aircraft and aero-engines andmanufacture spare parts; and the shipyards run bythe Directorate of Naval Construction (DCN), whichproduce all of France’s major warships and subma-rines. In October 1990, DCN established a privatesubsidiary called DCN International to manage itsinternational marketing and collaborative activities.Even so, full commercialization and rationalizationof the naval shipyards will take several yearsbecause the DCN’s 26,800 employees enjoy lifetimejob security under a special statute. Although manyof these workers could be paid a bonus to take earlyretirement or accept a new job status, the cost of thetransition would be high.

In addition to commercializing the arsenals, therehas been some talk of privatizing the nationalizeddefense firms. In September 1991, French President

Mitterrand approved a partial privatization (up to 49percent) of the entire nationalized sector, includingbanks and insurance companies as well as defensecontractors. Nevertheless, even partial privatizationof the nationalized defense firms faces a number ofobstacles. First, it will be necessary to find buyerswho are prepared to pay a good price for the shares,despite uncertainties over future government con-tracts and export sales. Second, since the FrenchGovernment is bound to remain heavily involved indefense-industrial policy, people may be cautiousabout buying shares in a state-controlled firm whosepriorities and goals may differ from those of theprivate investor. Because of these difficulties, priva-tization of the nationalized defense companiesremains unlikely.

Preserving Core Competencies

Given the changes in the international securityenvironment and the downward trends in defensespending and export sales, France is graduallymoving away from its traditional Gaullist emphasison national autonomy in arms production. The DGAhas concluded that France no longer has the financialmeans to maintain an independent capability acrossthe full spectrum of weapon systems and mustincreasingly rationalize defense production on aEuropean scale, while concentrating on its competi-tive strengths. In an effort to reduce overcapacityand eliminate redundancies, the French Governmenthas urged defense companies to pare back theirproduct lines, collaborate with other European firmsthat have complementary technological assets, andfocus on “poles of excellence’ where France enjoysa technical or market advantage, such as fighters,helicopters, defense electronics, and tactical mis-siles.40 Other priority areas include those hightechnologies having both military and civil applica-tions (e.g., optoelectronics, satellites, telecommuni-cations) and sectors considered vital for preservingthe independence of the French nuclear deterrent(e.g., nuclear weapons and strategic delivery sys-tems).

Although the DGA is determined to maintain thetechnological potential of the defense industry todevelop the next generation of advanced weapons, itis up to the individual firms to identify their “core

F. Future Crucial to Weekly, vol. 16, No. 12, Sept. 12, 1991, p. 499.39 Jane’ Weekly, vol. 16, No. 24, Dec. 14, 1991, p. 1141.

op. cit., footnote p.

Lessons in Restructuring Defense Industry: The French Experience ● 21

competencies."DGA officials will then help pre-serve them by selectively awarding procurement andR&D contracts. Dassault Aviation, for example, hasestablished an internal working group to identify thetechnologies it must keep in-house for the designand assembly of high-performance combat aircraft,while subcontracting out less critical subsystemsand manufacturing activities. Dassault’s identifiedcore competencies include new materials, stealth,computer-aided design and manufacturing, advancedfabrication technologies (such as superplastic form-ing and diffusion bonding), and robotics. For Chan-tiers de l’Atlantique, a shipyard that does both civiland naval work, the firm’s core competencies lie inthe design of architectural interfaces between a shipand its communications and weapon systems, whiletaking account of such factors as electromagneticinterference, shock, and noise. Thus, while subcon-tracting the development of command-control sys-tems, data links, andarmaments, Chantiers willfocus on integrating these systems with the vessel’ssuperstructure.

Thomson-CSF has chosen several fields in whichto focus its efforts, including electronic warfare,flight simulators, sonars, radars, and naval combatsystems. For each of these areas, the company hasidentified technologies, techniques, and manufac-turing know-how that give it a competitive edge incurrent and future markets, so that these corecompetencies can be preserved and further strength-ened. Like Dassault, Thomson-CSF plans to spinoffnonessential activities to subcontractors with whomit will establish long-term partnerships. The com-pany has also streamlined its R&D capabilities bymerging design teams in different divisions that dosimilar work. For example, two divisions at Thomson-CSF were engaged in developing X-band radars:low-power radars for combat aircraft and high-power radars for air-traffic control. Since thesesystems involve similar technologies and approaches,the merger of the two design teams has enabled thecompany to reduce the total number of engineersworking in this area and to bring some formerlysubcontracted work in-house.

Diversification Into Civil Sector

The DGA has encouraged French prime con-tractors-and their less visible network of thousandsof subcontractors and suppliers-to limit theirdependence on defense work and expand theirmarket share in commerical areas. In the current

Figure 7—Thomson-CSF Revenueby Business Group, 1990

21%

ommunicationnd command

16%

c

2 3 %

SOURCE: Thomson-CSF

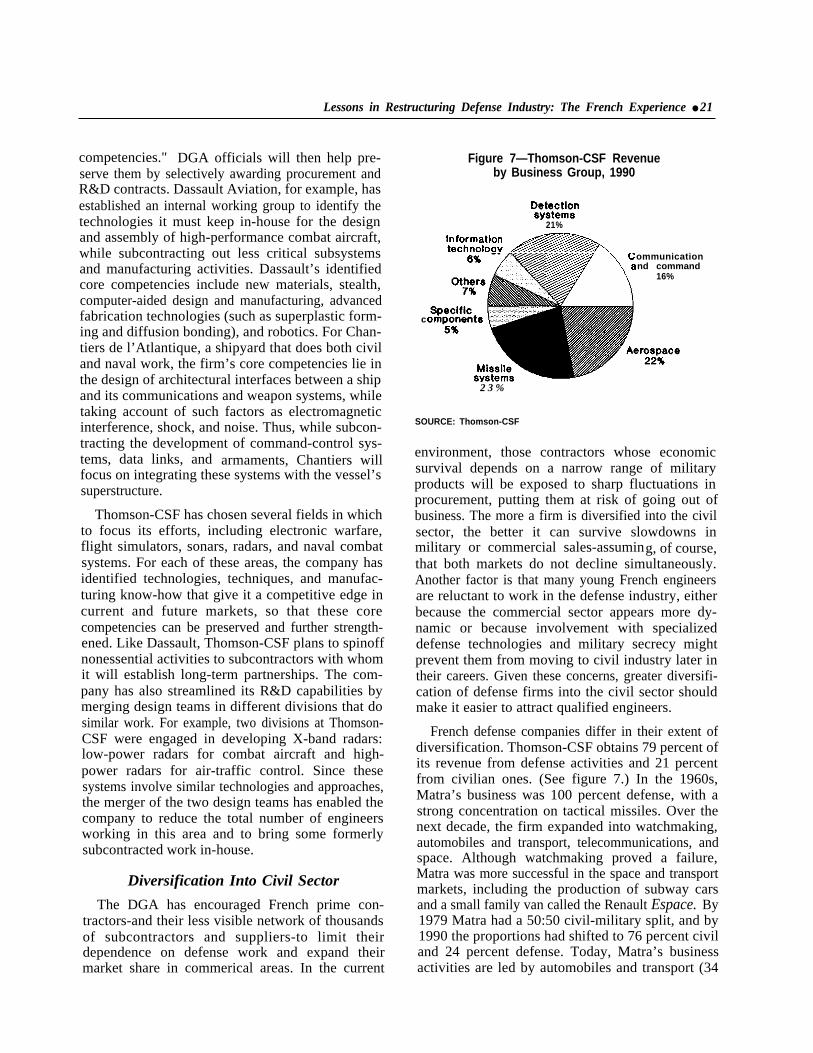

environment, those contractors whose economicsurvival depends on a narrow range of militaryproducts will be exposed to sharp fluctuations inprocurement, putting them at risk of going out ofbusiness. The more a firm is diversified into the civilsector, the better it can survive slowdowns inmilitary or commercial sales-assuming, of course,that both markets do not decline simultaneously.Another factor is that many young French engineersare reluctant to work in the defense industry, eitherbecause the commercial sector appears more dy-namic or because involvement with specializeddefense technologies and military secrecy mightprevent them from moving to civil industry later intheir careers. Given these concerns, greater diversifi-cation of defense firms into the civil sector shouldmake it easier to attract qualified engineers.

French defense companies differ in their extent ofdiversification. Thomson-CSF obtains 79 percent ofits revenue from defense activities and 21 percentfrom civilian ones. (See figure 7.) In the 1960s,Matra’s business was 100 percent defense, with astrong concentration on tactical missiles. Over thenext decade, the firm expanded into watchmaking,automobiles and transport, telecommunications, andspace. Although watchmaking proved a failure,Matra was more successful in the space and transportmarkets, including the production of subway carsand a small family van called the Renault Espace. By1979 Matra had a 50:50 civil-military split, and by1990 the proportions had shifted to 76 percent civiland 24 percent defense. Today, Matra’s businessactivities are led by automobiles and transport (34

22 ● Lessons in Restructuring Defense Industry: The French Experience

percent of sales), followed by missiles (24 percent),telecommunications and software (24 percent), andspace (18 percent). The company’s long-term goal isto divide its business equally among the three sectorsof defense/aerospace, transport, and telecommuni-cations. Since Matra’s corporate identity is closelylinked to missiles, however, the firm plans to remainactive in the defense sector.

Constructions Industrielles de la Mediterranee(CNIM), a midsize company with about 1,000employees, is currently divided equally betweenmilitary and civil work. Its defense products includebridging equipment and floating bridges for theFrench Army, and submarine missile tubes andlaunching equipment for the Navy; its commercialproducts are cogeneration boilers and other environ-mental systems. Although CNIM’s military saleshave not yet begun to drop, company executives seedefense cutbacks on the horizon and are graduallyreorienting the firm toward the civil sector.

The French aerospace industry is already fairlywell diversified, falling well below the 60 to 80percent reliance on defense work characteristic ofU.S. prime contractors. In 1991, commercial busi-ness accounted for 52 percent of total industry sales,exceeding military business for the first time.41