liao busas final 2016 – emma waterman - uvic lss · web viewliao busas final 2016 – emma...

TRANSCRIPT

Liao BusAs Final 2016 – Emma Waterman 1

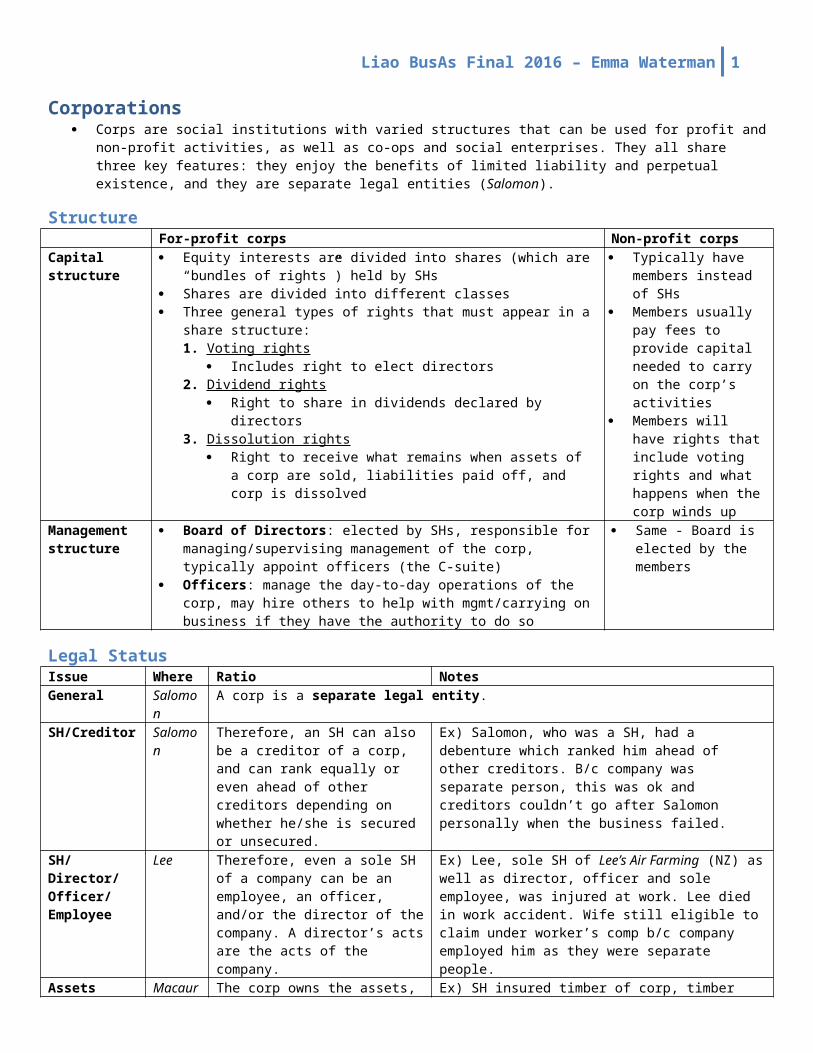

Corporations Corps are social institutions with varied structures that can be used for profit and non-profit activities, as well as co-ops and

social enterprises. They all share three key features: they enjoy the benefits of limited liability and perpetual existence, and they are separate legal entities (Salomon).

StructureFor-profit corps Non-profit corps

Capital structure Equity interests are divided into shares (which are “bundles of rights”) held by SHs

Shares are divided into different classes Three general types of rights that must appear in a share structure:

1. Voting rights Includes right to elect directors

2. Dividend rights Right to share in dividends declared by directors

3. Dissolution rights Right to receive what remains when assets of a corp are sold,

liabilities paid off, and corp is dissolved

Typically have members instead of SHs

Members usually pay fees to provide capital needed to carry on the corp’s activities

Members will have rights that include voting rights and what happens when the corp winds up

Management structure

Board of Directors: elected by SHs, responsible for managing/supervising management of the corp, typically appoint officers (the C-suite)

Officers: manage the day-to-day operations of the corp, may hire others to help with mgmt/carrying on business if they have the authority to do so

Same - Board is elected by the members

Legal StatusIssue Where Ratio NotesGeneral Salomon A corp is a separate legal entity.SH/Creditor Salomon Therefore, an SH can also be a

creditor of a corp, and can rank equally or even ahead of other creditors depending on whether he/she is secured or unsecured.

Ex) Salomon, who was a SH, had a debenture which ranked him ahead of other creditors. B/c company was separate person, this was ok and creditors couldn’t go after Salomon personally when the business failed.

SH/Director/ Officer/ Employee

Lee Therefore, even a sole SH of a company can be an employee, an officer, and/or the director of the company. A director’s acts are the acts of the company.

Ex) Lee, sole SH of Lee’s Air Farming (NZ) as well as director, officer and sole employee, was injured at work. Lee died in work accident. Wife still eligible to claim under worker’s comp b/c company employed him as they were separate people.

Assets Macaura The corp owns the assets, not the SHs, as shares are just bundles of rights that give a right of action against the company.

Ex) SH insured timber of corp, timber burned down, insurance held invalid b/c SH had no insurable interest: the corp owned the timber, not him (note insurance aspect was overruled in Kosmopolous, but for our point of ownership still good – confirmed in Sparling)

Problems Created By Legal Status:(1) SHs may cause the company to become indebted to the SHs when the company is insolvent or about to become insolvent in

order to defeat the interests of creditors(2) Company may make pay-outs to SHs when it is insolvent, defeat creditors(3) Company may enter into Ks with SHs that are unfavourable to other SHs or creditors(4) Can have a company with very little capital and defeat interests of creditors or 3P tort claimants(5) Parties may be deceived into thinking they are dealing with an individual or partnership, not a corp(6) Persons may incorporate to avoid personal obligations or restrictions i.e. not allowed to carry on a business in a certain area

due to employment K, so create corp to carry on that business (it isn’t you)

2 Liao BusAs Final 2016 – Emma Waterman

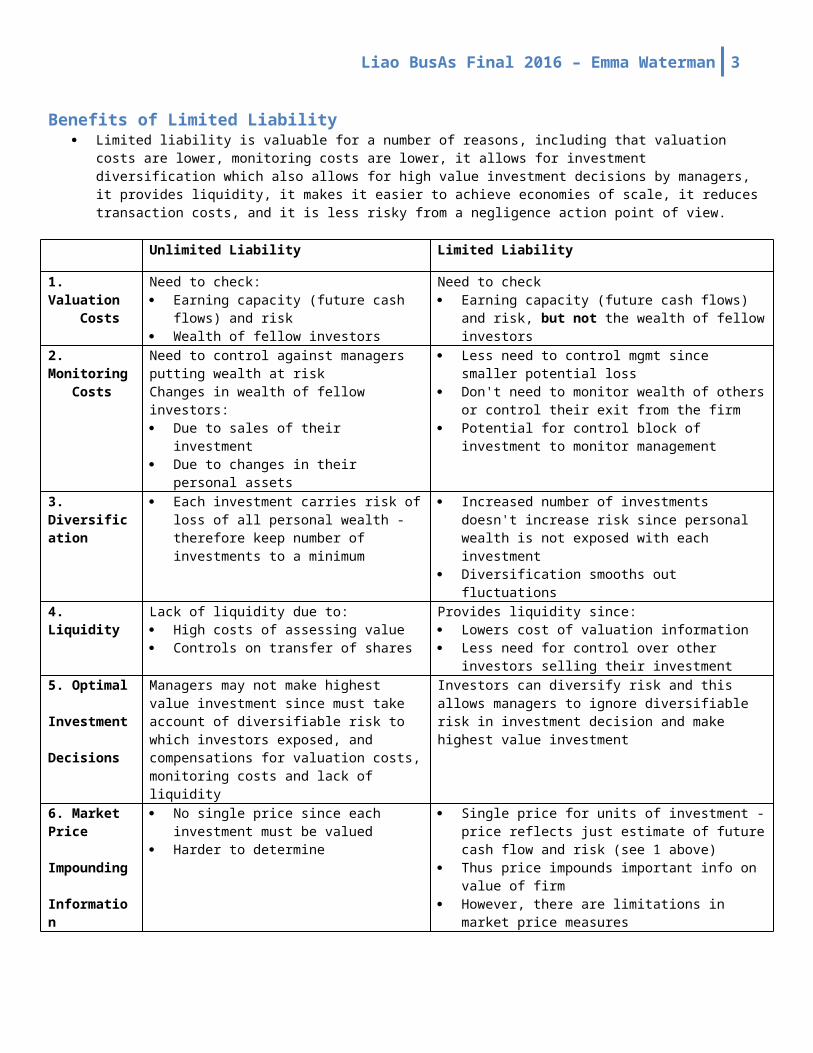

Benefits of Limited Liability Limited liability is valuable for a number of reasons, including that valuation costs are lower, monitoring costs are lower, it

allows for investment diversification which also allows for high value investment decisions by managers, it provides liquidity, it makes it easier to achieve economies of scale, it reduces transaction costs, and it is less risky from a negligence action point of view.

Unlimited Liability Limited Liability

1. Valuation Costs

Need to check: Earning capacity (future cash flows) and risk Wealth of fellow investors

Need to check Earning capacity (future cash flows) and risk, but not

the wealth of fellow investors

2. Monitoring Costs

Need to control against managers putting wealth at riskChanges in wealth of fellow investors: Due to sales of their investment Due to changes in their personal assets

Less need to control mgmt since smaller potential loss Don't need to monitor wealth of others or control their

exit from the firm Potential for control block of investment to monitor

management3. Diversification

Each investment carries risk of loss of all personal wealth - therefore keep number of investments to a minimum

Increased number of investments doesn't increase risk since personal wealth is not exposed with each investment

Diversification smooths out fluctuations4. Liquidity Lack of liquidity due to:

High costs of assessing value Controls on transfer of shares

Provides liquidity since: Lowers cost of valuation information Less need for control over other investors selling their

investment5. Optimal Investment Decisions

Managers may not make highest value investment since must take account of diversifiable risk to which investors exposed, and compensations for valuation costs, monitoring costs and lack of liquidity

Investors can diversify risk and this allows managers to ignore diversifiable risk in investment decision and make highest value investment

6. Market Price Impounding Information

No single price since each investment must be valued

Harder to determine

Single price for units of investment - price reflects just estimate of future cash flow and risk (see 1 above)

Thus price impounds important info on value of firm However, there are limitations in market price

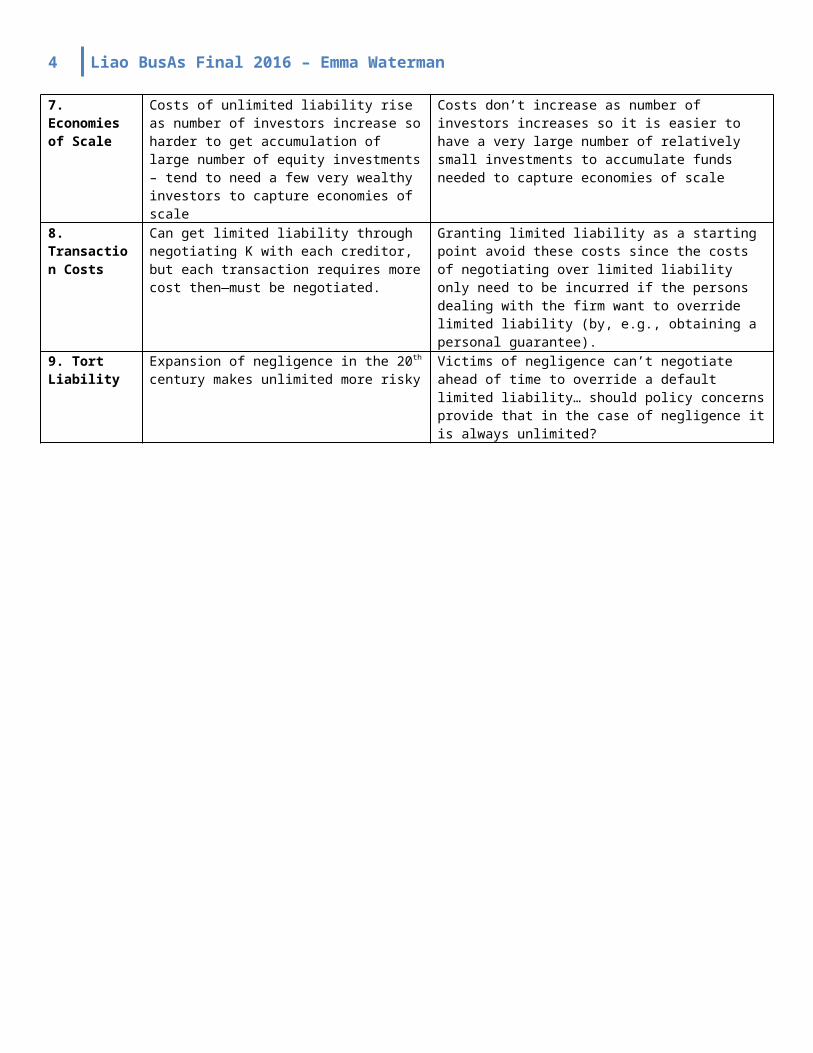

measures7. Economies of Scale

Costs of unlimited liability rise as number of investors increase so harder to get accumulation of large number of equity investments – tend to need a few very wealthy investors to capture economies of scale

Costs don’t increase as number of investors increases so it is easier to have a very large number of relatively small investments to accumulate funds needed to capture economies of scale

8. Transaction Costs

Can get limited liability through negotiating K with each creditor, but each transaction requires more cost then—must be negotiated.

Granting limited liability as a starting point avoid these costs since the costs of negotiating over limited liability only need to be incurred if the persons dealing with the firm want to override limited liability (by, e.g., obtaining a personal guarantee).

9. Tort Liability Expansion of negligence in the 20th century makes unlimited more risky

Victims of negligence can’t negotiate ahead of time to override a default limited liability… should policy concerns provide that in the case of negligence it is always unlimited?

Liao BusAs Final 2016 – Emma Waterman 3

Incorporation

Why Incorporate? Incorporation is valuable for a number of reasons. Incorporation provides for limited liability, perpetual succession, ease of

share transfers, facilities for a body corporate to secure additional capital, and tax advantages. Further, it allows shareholders to contract with the corp and ensures that shareholders alone cannot make binding contracts on behalf of the corp. I note that there is a cost associated with incorporating.

Reasons Pro ConLimited Liability (see chart above)

o May give protection against relatively insignificant trade credit

o Protection against personal liability in tort

o May not provide benefit if you just have to give a personal covenant to get credit anyway

o Possible to pierce corporate veil for tort claimso Need to buy tort insurance regardless of whether

you incorporatePerpetual Succession o SP may have to assign Ks etc when they

sell and this may be hard to do w/o PSo Can head the problem of reconstituting with

death of partners or SPs before it happens in KEase of Transfer of Share o Freely transferable unless there is an

express restrictiono Securities laws do put certain restrictions on

shares (esp for closely held corps)o Added expense for compliance w/ securities law

SHs Alone Cannot Bind o They’re typically not agents o In closely held corps the individual SHs are usually the officers and have authority to bind

o Partners can constrain authority of partners anyway through express agreement

SH Can Contract with Corp

o Because it’s a separate legal entity o Can achieve a very similar thing in partnership, can enter into K, which is separate from partnership with the other partners.

Facilities for a Body Corporate to Secure Additional Capital

o Share and debentureso Don’t need the partners to be the ones

who put in more money - can be anyoneo Can sells shares – often why non-profits

incorporate, so they can sell shares

o In partnership you could just get more partners or get partners to invest more funds

o Anyone can make debentures, just a doc that shows debt i.e. IOU

o Still have to comply with securities legislation when selling shares so hardly more ready source

Tax Advantages o “Small business deduction” can provide a tax advantage

o Private corps incorporated in Canada and carrying on active business can get a reduced rate on the first $500K of income

o Can control the timing of the distribution through corp which allows tax planning

o Losses incurred at the start up phase cannot be passed on to investors

Costs of Incorp o Fee for incorp itself, few hundred dollarso Legal feeso Filing annual reports with a modest feeo Maintaining certain recordso Filing additional tax return

Which Act to Choose? CBCA or BCBCA? You have to file everywhere you carry on business but can only incorporate under one Act A BCBCA company doing business in BC will incorporate in BC and then file an extra-provincial registration form in AB As a CBCA company you incorporate under the CBCA and then file extra-provincial forms in BC & AB

CBCA BCCA(i) Name protection(ii) No restriction on maintaining an action(iii) Lawyers and SHs in other provinces are familiar

with it

(i) Lawyers here are more familiar(ii) Easier to deal with Victoria than Ottawa(iii) It is cheaper

4 Liao BusAs Final 2016 – Emma Waterman

CBCA IncorporationIssue Section NotesWho may incorporate?

5(1) One or more individuals, none of the individuals may be:(a) under 18(b) of unsound mind as found by a court in Canada or elsewhere or(c) bankrupt

May incorporate by signing articles of incorp and complying with section 7.5(2) One or more bodies corporate may incorporate by signing articles and complying with s. 7

Company vs corp

2(1) A corp is “a body corporate incorporated or continued under [the CBCA]A body corporate is “a company or other body corporate wherever or however incorporated”

Who is in charge?

2(1), 260 2(1) The “Director” is appointed under s260 by the Minister and carries out the duties and exercises the powers of the Director under the Act.

Articles 6(1) Must set out:(a) Corporate name(b) The province in Canada where the registered offices of the corp will be situated(c) The classes of shares and any max number of share that the corp is authorized to issue

(i) If there will be two or more classes of shares, the rights, privileges, restrictions and conditions attaching to each class of shares [voting, dividends, dissolution rights];

(ii) If a class of shares may be issues in series, the authority give to the directors to fix the number of shares in and to determine the designation of, and the rights, privileges, restrictions and conditions attaching to the shares of each series;

(d) Any restrictions on the transfer of shares(e) The number of directors the corp is to have, or the minimum and max number of

directors it is to have(f) Any restrictions on the business of the corp

6(2) Can also put in provisions that are permitted by the Act or by law to be set out in the corp by-laws6(3) Can set out a greater number of votes of Directors or SHs than required by Act in the articles (or USA)6(4) Except for the required number of votes to remove a director under 109

Signing of Documents

7 Must send articles of incorp to the Director along with docs that are required by s19 and 10619(2) Must send notice of the registered office of the corp to the Director106(1) Must send notice of the directors of the corp to the Director

Naming **See below*

Cannot have a name that is confusingly similar to another corp or business. Can get numbered name with “Canada Ltd.” on the end OR if you want a different name, must file a NUANS name search report.

Fees Reg 97 Sched 5

Must pay prescribed fees

Issuance of Certificate

8 and 12(1)

If all the requirements are met, the Director shall issue the certificate of incorp. Granted as of right.

Date of existence

9 Corp comes into existence on the date shown in the certificate of incorp.

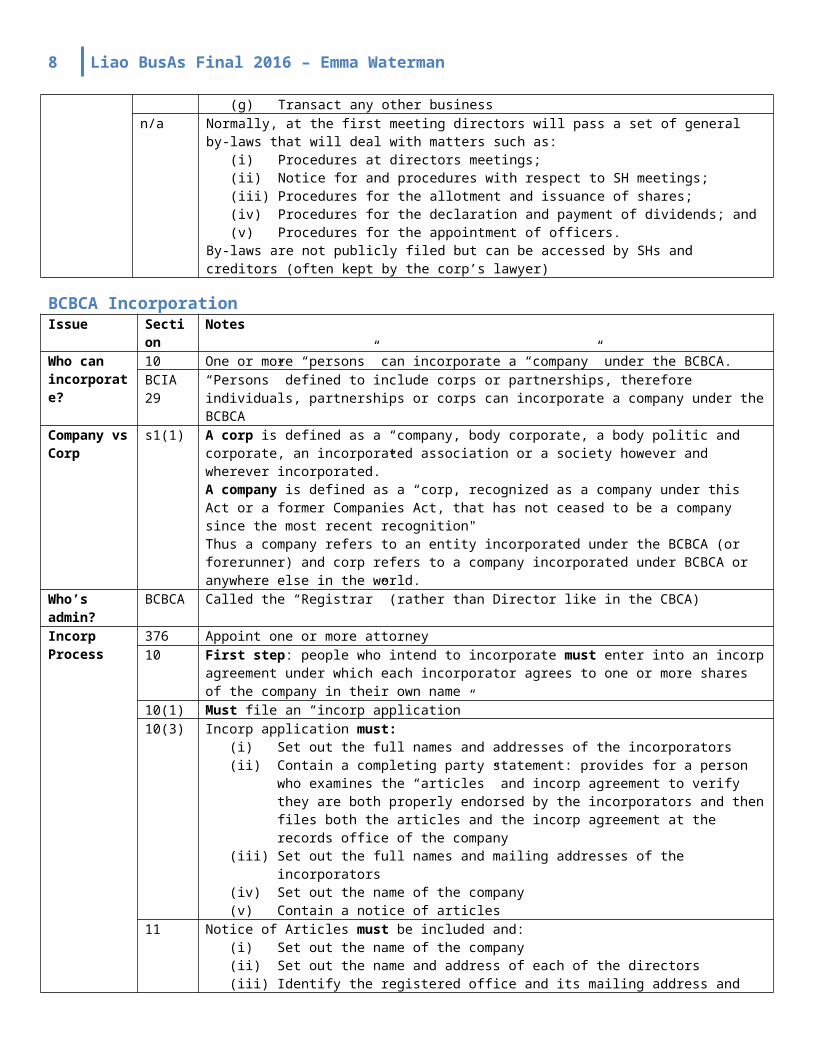

Post-Incorp 104 After the issue of the certificate, directors shall meet and they may:(a) Make bylaws(b) Adopt forms of security certificates and corporate records;(c) Authorize the issuance of shares;(d) Appoint officers;(e) Appoint an auditor to hold office until the first meeting of SHs(f) Make banking arrangements; and(g) Transact any other business

n/a Normally, at the first meeting directors will pass a set of general by-laws that will deal with matters such as:

(i) Procedures at directors meetings;(ii) Notice for and procedures with respect to SH meetings;(iii) Procedures for the allotment and issuance of shares;(iv) Procedures for the declaration and payment of dividends; and(v) Procedures for the appointment of officers.

By-laws are not publicly filed but can be accessed by SHs and creditors (often kept by the corp’s lawyer)

Liao BusAs Final 2016 – Emma Waterman 5

BCBCA IncorporationIssue Section NotesWho can incorporate?

10 One or more “persons” can incorporate a “company” under the BCBCA.BCIA 29 “Persons” defined to include corps or partnerships, therefore individuals, partnerships or corps can

incorporate a company under the BCBCACompany vs Corp

s1(1) A corp is defined as a “company, body corporate, a body politic and corporate, an incorporated association or a society however and wherever incorporated.”A company is defined as a “corp, recognized as a company under this Act or a former Companies Act, that has not ceased to be a company since the most recent recognition"Thus a company refers to an entity incorporated under the BCBCA (or forerunner) and corp refers to a company incorporated under BCBCA or anywhere else in the world.

Who’s admin? BCBCA Called the “Registrar” (rather than Director like in the CBCA)Incorp Process 376 Appoint one or more attorney

10 First step: people who intend to incorporate must enter into an incorp agreement under which each incorporator agrees to one or more shares of the company in their own name

10(1) Must file an “incorp application”10(3) Incorp application must:

(i) Set out the full names and addresses of the incorporators(ii) Contain a completing party statement: provides for a person who examines the “articles”

and incorp agreement to verify they are both properly endorsed by the incorporators and then files both the articles and the incorp agreement at the records office of the company

(iii) Set out the full names and mailing addresses of the incorporators(iv) Set out the name of the company(v) Contain a notice of articles

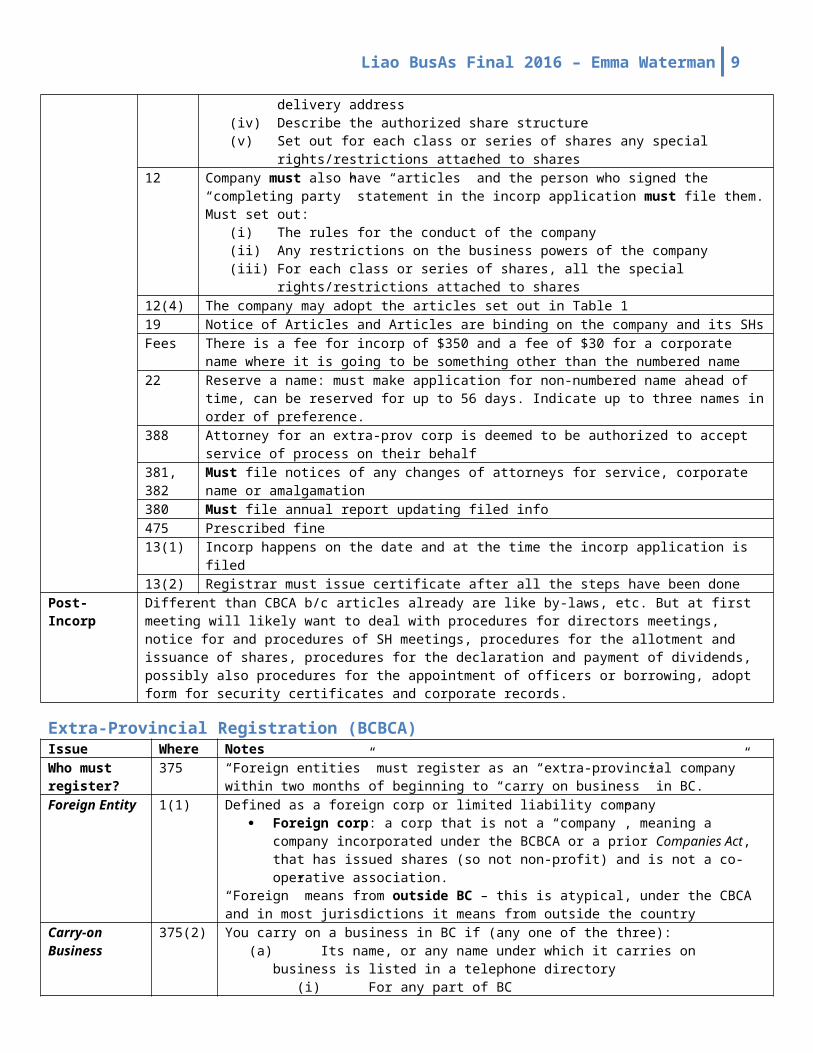

11 Notice of Articles must be included and:(i) Set out the name of the company(ii) Set out the name and address of each of the directors(iii) Identify the registered office and its mailing address and delivery address(iv) Describe the authorized share structure(v) Set out for each class or series of shares any special rights/restrictions attached to shares

12 Company must also have “articles” and the person who signed the “completing party” statement in the incorp application must file them. Must set out:

(i) The rules for the conduct of the company(ii) Any restrictions on the business powers of the company(iii) For each class or series of shares, all the special rights/restrictions attached to shares

12(4) The company may adopt the articles set out in Table 119 Notice of Articles and Articles are binding on the company and its SHsFees There is a fee for incorp of $350 and a fee of $30 for a corporate name where it is going to be

something other than the numbered name22 Reserve a name: must make application for non-numbered name ahead of time, can be reserved for up

to 56 days. Indicate up to three names in order of preference.388 Attorney for an extra-prov corp is deemed to be authorized to accept service of process on their behalf381, 382

Must file notices of any changes of attorneys for service, corporate name or amalgamation

380 Must file annual report updating filed info475 Prescribed fine13(1) Incorp happens on the date and at the time the incorp application is filed13(2) Registrar must issue certificate after all the steps have been done

Post-Incorp Different than CBCA b/c articles already are like by-laws, etc. But at first meeting will likely want to deal with procedures for directors meetings, notice for and procedures of SH meetings, procedures for the allotment and issuance of shares, procedures for the declaration and payment of dividends, possibly also procedures for the appointment of officers or borrowing, adopt form for security certificates and corporate records.

6 Liao BusAs Final 2016 – Emma Waterman

Extra-Provincial Registration (BCBCA)Issue Where NotesWho must register?

375 “Foreign entities” must register as an “extra-provincial company” within two months of beginning to “carry on business” in BC.

Foreign Entity 1(1) Defined as a foreign corp or limited liability company Foreign corp: a corp that is not a “company”, meaning a company incorporated under the

BCBCA or a prior Companies Act, that has issued shares (so not non-profit) and is not a co-operative association.

“Foreign” means from outside BC – this is atypical, under the CBCA and in most jurisdictions it means from outside the country

Carry-on Business

375(2) You carry on a business in BC if (any one of the three):(a) Its name, or any name under which it carries on business is listed in a telephone directory

(i) For any part of BC(ii) Together with an address or telephone number in BC

(b) Name appears or is announced in any advertisement in which an address or telephone number in BC is given for the corp

(c) In BC it has,(i) A resident agent(ii) A warehouse, office or place of business

If none of this applies, it’s a question of degree of presence in the province – simply shipping goods into the province has been held not to be carrying on business in the province

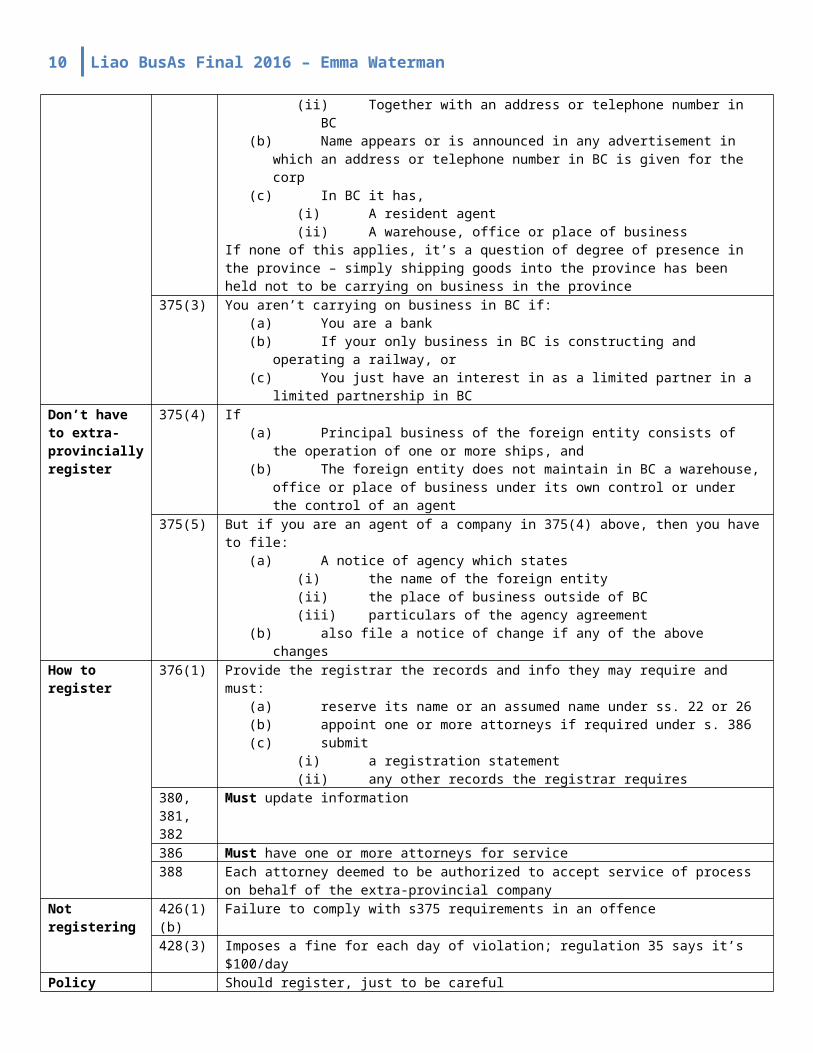

375(3) You aren’t carrying on business in BC if:(a) You are a bank(b) If your only business in BC is constructing and operating a railway, or(c) You just have an interest in as a limited partner in a limited partnership in BC

Don’t have to extra- provincially register

375(4) If(a) Principal business of the foreign entity consists of the operation of one or more ships, and(b) The foreign entity does not maintain in BC a warehouse, office or place of business under

its own control or under the control of an agent375(5) But if you are an agent of a company in 375(4) above, then you have to file:

(a) A notice of agency which states(i) the name of the foreign entity(ii) the place of business outside of BC(iii) particulars of the agency agreement

(b) also file a notice of change if any of the above changesHow to register 376(1) Provide the registrar the records and info they may require and must:

(a) reserve its name or an assumed name under ss. 22 or 26(b) appoint one or more attorneys if required under s. 386(c) submit

(i) a registration statement(ii) any other records the registrar requires

380, 381, 382

Must update information

386 Must have one or more attorneys for service388 Each attorney deemed to be authorized to accept service of process on behalf of the extra-

provincial companyNot registering 426(1)(b) Failure to comply with s375 requirements in an offence

428(3) Imposes a fine for each day of violation; regulation 35 says it’s $100/dayPolicy Should register, just to be careful

Liao BusAs Final 2016 – Emma Waterman 7

Reincorporation and ContinuanceReincorporation Continuance

What is it? When a corp that has been incorporated in one jurisdiction decides to becomes incorporated under a different statute in another jurisdiction

Why do it? Prefer a corporate climate in different jurisdiction Tax reasons

Several incorp statutes in Canada allow for it – more convenient than reincorp, same effect

How do you do it?

Incorporate a new corp (corp B) under another jurisdiction’s statute

Have corp B issue corp B shares to SHs of existing corp A in exchange for their shares of corp A

Result is that corp B owns the shares of corp A Wind up corp A

Export - CBCA company wanting to immigrate: S188(1),(5): obtain a resolution from SHs

permitting a continuance S188(1): obtain approval from Director Register in another jurisdiction – make

amendments to incorp docs to cooperate with the new jurisdiction’s requirements

Import – company wanting a continuance into CBCA: Must be incorporated under another Act that

allows for continuance – follow its rules S187(1) apply to CBCA Director for certificate of

continuance S187(3) do so by filing articles of continuance and

notice of directors

AmalgamationRule 181 Two or more corps, including holding and subsidiary corps, may amalgamate and continue as

one corpLong-form amalgamation

183(1) Special resolution from SHs required (everyone can vote – voting shares or not) SHs of corp A merge with SHs of corp B to make everyone SHs of corp C 183(1) has a bunch of requirements for the amalgamation agreement 185(1) requires that once the amalgamation is approved the articles of amalgamation have to

be sent to the Director, yadda yadda Complicated

Vertical short-form

184(1) Only Board approval required Already have a subsidiary corp and merge it with the holding/parent corp Simpler 184(1)(b) requires that the resolutions approving the amalgamation provide that the shares of

the amalgamating sub corp are to be cancelled with no repayment of capital re: shares, (subject to…) the articles of amalgamation have to be same as the articles of the holding corp and no securities can be issued re: the amalgamation, and the stated capital of the amalgamated corp shall be the same as the stated capital of the amalgamating holding corp

Horizontal short-form

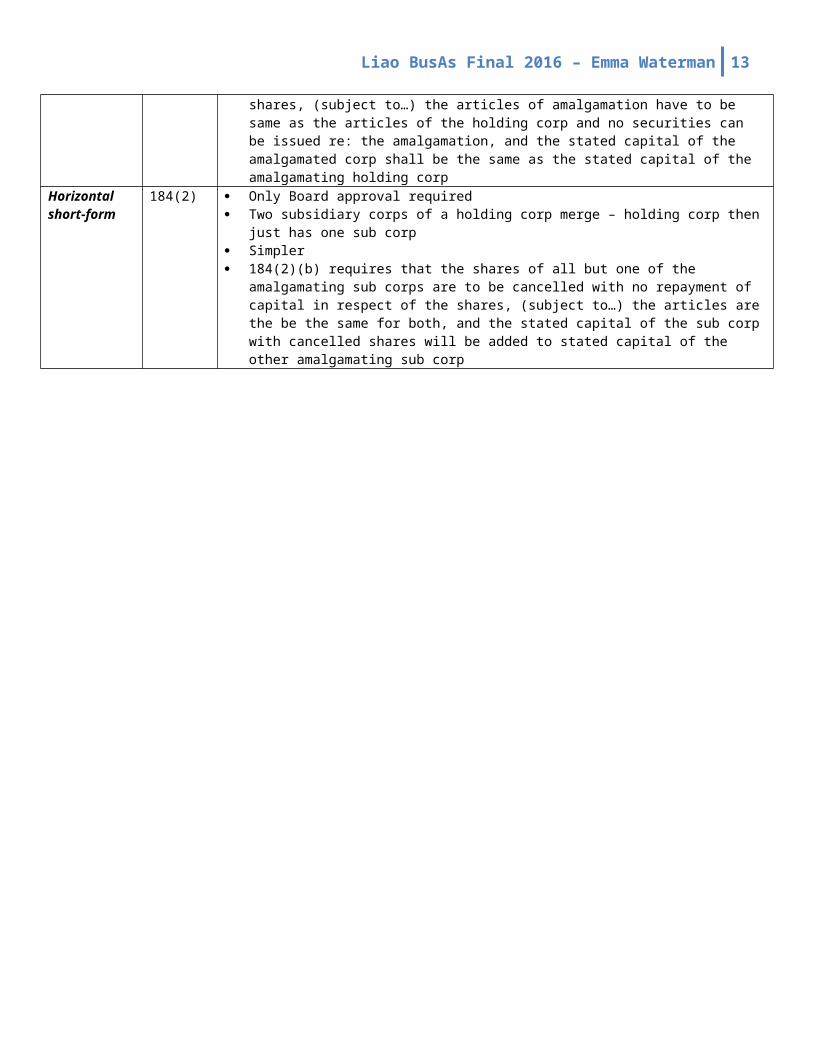

184(2) Only Board approval required Two subsidiary corps of a holding corp merge – holding corp then just has one sub corp Simpler 184(2)(b) requires that the shares of all but one of the amalgamating sub corps are to be

cancelled with no repayment of capital in respect of the shares, (subject to…) the articles are the be the same for both, and the stated capital of the sub corp with cancelled shares will be added to stated capital of the other amalgamating sub corp

8 Liao BusAs Final 2016 – Emma Waterman

Corporate Names

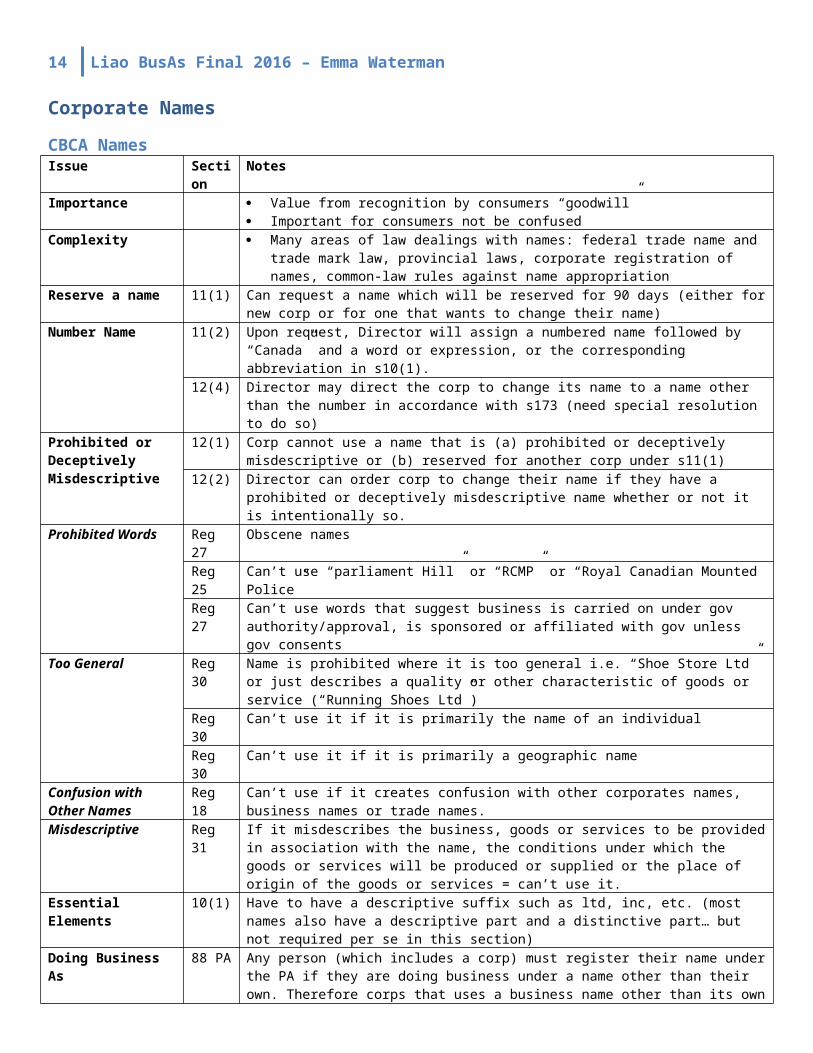

CBCA NamesIssue Section NotesImportance Value from recognition by consumers “goodwill”

Important for consumers not be confusedComplexity Many areas of law dealings with names: federal trade name and trade mark law, provincial

laws, corporate registration of names, common-law rules against name appropriationReserve a name 11(1) Can request a name which will be reserved for 90 days (either for new corp or for one that

wants to change their name)Number Name 11(2) Upon request, Director will assign a numbered name followed by “Canada” and a word or

expression, or the corresponding abbreviation in s10(1).12(4) Director may direct the corp to change its name to a name other than the number in

accordance with s173 (need special resolution to do so)Prohibited or Deceptively Misdescriptive

12(1) Corp cannot use a name that is (a) prohibited or deceptively misdescriptive or (b) reserved for another corp under s11(1)

12(2) Director can order corp to change their name if they have a prohibited or deceptively misdescriptive name whether or not it is intentionally so.

Prohibited Words Reg 27 Obscene namesReg 25 Can’t use “parliament Hill” or “RCMP” or “Royal Canadian Mounted Police”Reg 27 Can’t use words that suggest business is carried on under gov authority/approval, is sponsored

or affiliated with gov unless gov consentsToo General Reg 30 Name is prohibited where it is too general i.e. “Shoe Store Ltd” or just describes a quality or

other characteristic of goods or service (“Running Shoes Ltd”)Reg 30 Can’t use it if it is primarily the name of an individualReg 30 Can’t use it if it is primarily a geographic name

Confusion with Other Names

Reg 18 Can’t use if it creates confusion with other corporates names, business names or trade names.

Misdescriptive Reg 31 If it misdescribes the business, goods or services to be provided in association with the name, the conditions under which the goods or services will be produced or supplied or the place of origin of the goods or services = can’t use it.

Essential Elements 10(1) Have to have a descriptive suffix such as ltd, inc, etc. (most names also have a descriptive part and a distinctive part… but not required per se in this section)

Doing Business As 88 PA Any person (which includes a corp) must register their name under the PA if they are doing business under a name other than their own. Therefore corps that uses a business name other than its own corporate name must register that business name.

BCBCA NamesIssue Where NotesWhat is the name 21(1) Once it becomes a company under this act the name is

(a) The name on the application ifi. the name has been reserved for the company

ii. the reservation is in effect at the date of recognition(b) Otherwise, the incorp number followed by “BC Ltd”

How to reserve 22(1) Apply to the registrar22(2) Registrar may reserve the name for 56 days or any longer period they think is appropriate22(3) Registrar can extend if they receive a request to do so before the expiry of the reservation.22(4) Registrar can’t reserve a name if it doesn’t comply with the other requirements in the Act22(5) If the registrar disapproves of a name for good, valid reasons, it contravenes other requirements

Form of name 23(1) Have to have “limited”, “limitee”, “incorporated”, “incorporee”, “corp”, “ltd”, “ltee”, “inc” or “corp” as part and at the end of its name

Restrictions 24(1) Can’t use any of the above terms unless(a) You are a corp or required to use those words(b) In the case of “limited” or “limitee” the person is

Liao BusAs Final 2016 – Emma Waterman 9

(i) A limited liability company registered under 377 as an extraprovincial company(ii) A limited partnership

Use the name 27 Have to display your name in legible English or French(a) In a conspicuous position at each place of business in BC(b) In all notices and official publications in BC(c) On all contracts, business letters and orders for goods, and on all its invoice, statements of

account, receipts and letters of credit used in BC(d) On all bills of exchange, promissory notes, endorsements, cheques and orders for money

used in BC and signed by it or on its behalf.Change name 28(1) Registrar may order a change of name if, for any reason the name of a company contravenes

(a) Any of the prescribed requirements(b) Any of the other requirements in this division or(c) Any of the requirements in s.51.21

28(2) Can also do so for an extra-provincial company28(3) But this doesn’t apply for federal corps

10 Liao BusAs Final 2016 – Emma Waterman

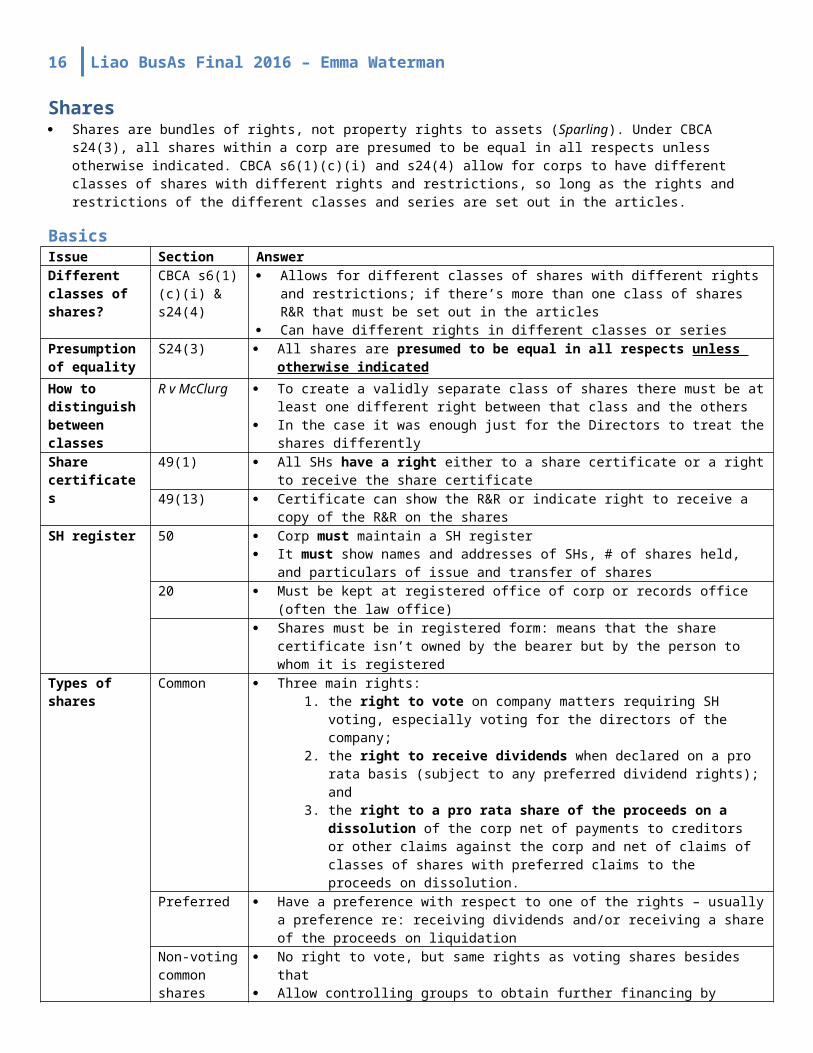

Shares Shares are bundles of rights, not property rights to assets (Sparling). Under CBCA s24(3), all shares within a corp are presumed

to be equal in all respects unless otherwise indicated. CBCA s6(1)(c)(i) and s24(4) allow for corps to have different classes of shares with different rights and restrictions, so long as the rights and restrictions of the different classes and series are set out in the articles.

BasicsIssue Section AnswerDifferent classes of shares?

CBCA s6(1)(c)(i) & s24(4)

Allows for different classes of shares with different rights and restrictions; if there’s more than one class of shares R&R that must be set out in the articles

Can have different rights in different classes or seriesPresumption of equality

S24(3) All shares are presumed to be equal in all respects unless otherwise indicated

How to distinguish between classes

R v McClurg To create a validly separate class of shares there must be at least one different right between that class and the others

In the case it was enough just for the Directors to treat the shares differentlyShare certificates 49(1) All SHs have a right either to a share certificate or a right to receive the share certificate

49(13) Certificate can show the R&R or indicate right to receive a copy of the R&R on the sharesSH register 50 Corp must maintain a SH register

It must show names and addresses of SHs, # of shares held, and particulars of issue and transfer of shares

20 Must be kept at registered office of corp or records office (often the law office) Shares must be in registered form: means that the share certificate isn’t owned by the

bearer but by the person to whom it is registeredTypes of shares Common Three main rights:

1. the right to vote on company matters requiring SH voting, especially voting for the directors of the company;

2. the right to receive dividends when declared on a pro rata basis (subject to any preferred dividend rights); and

3. the right to a pro rata share of the proceeds on a dissolution of the corp net of payments to creditors or other claims against the corp and net of claims of classes of shares with preferred claims to the proceeds on dissolution.

Preferred Have a preference with respect to one of the rights – usually a preference re: receiving dividends and/or receiving a share of the proceeds on liquidation

Non-voting common shares

No right to vote, but same rights as voting shares besides that Allow controlling groups to obtain further financing by selling non-voting shares without

losing much in the way of control over the corp Good for investors who don’t want to control the corp – can buy non-voting shares for

cheaper than voting shares Policy concerns with this – two ways to create a class of non-voting shares:

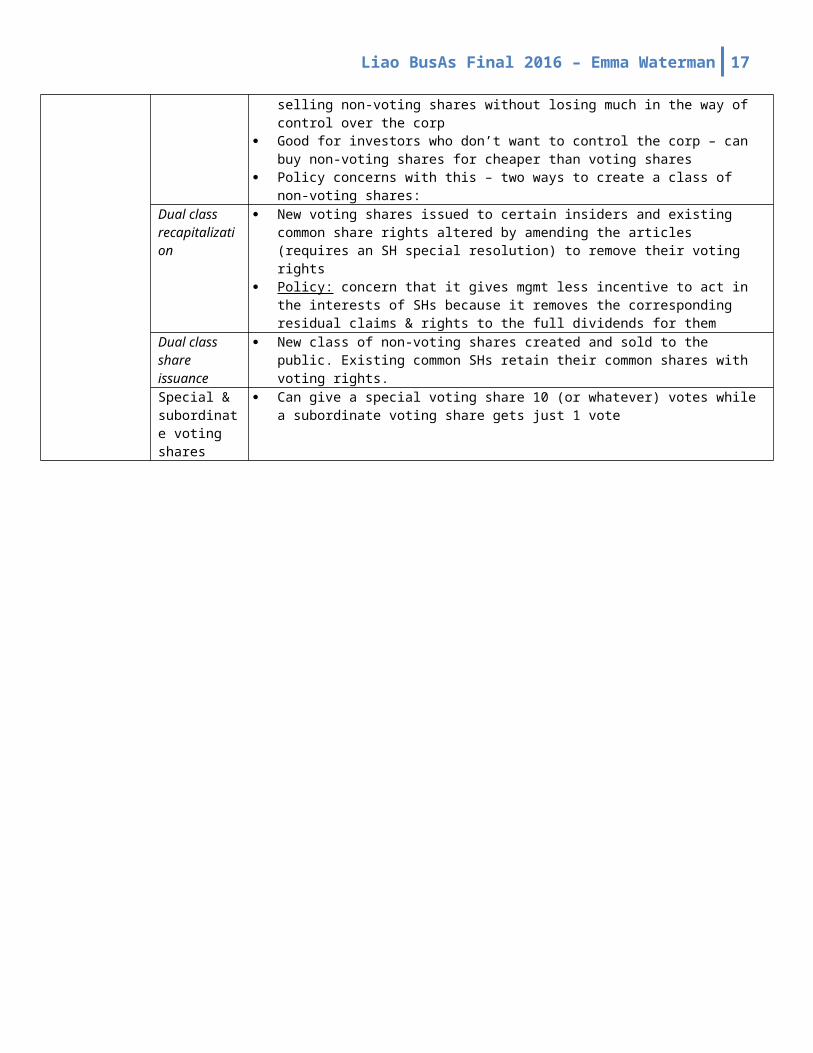

Dual class recapitalization

New voting shares issued to certain insiders and existing common share rights altered by amending the articles (requires an SH special resolution) to remove their voting rights

Policy: concern that it gives mgmt less incentive to act in the interests of SHs because it removes the corresponding residual claims & rights to the full dividends for them

Dual class share issuance

New class of non-voting shares created and sold to the public. Existing common SHs retain their common shares with voting rights.

Special & subordinate voting shares

Can give a special voting share 10 (or whatever) votes while a subordinate voting share gets just 1 vote

Liao BusAs Final 2016 – Emma Waterman 11

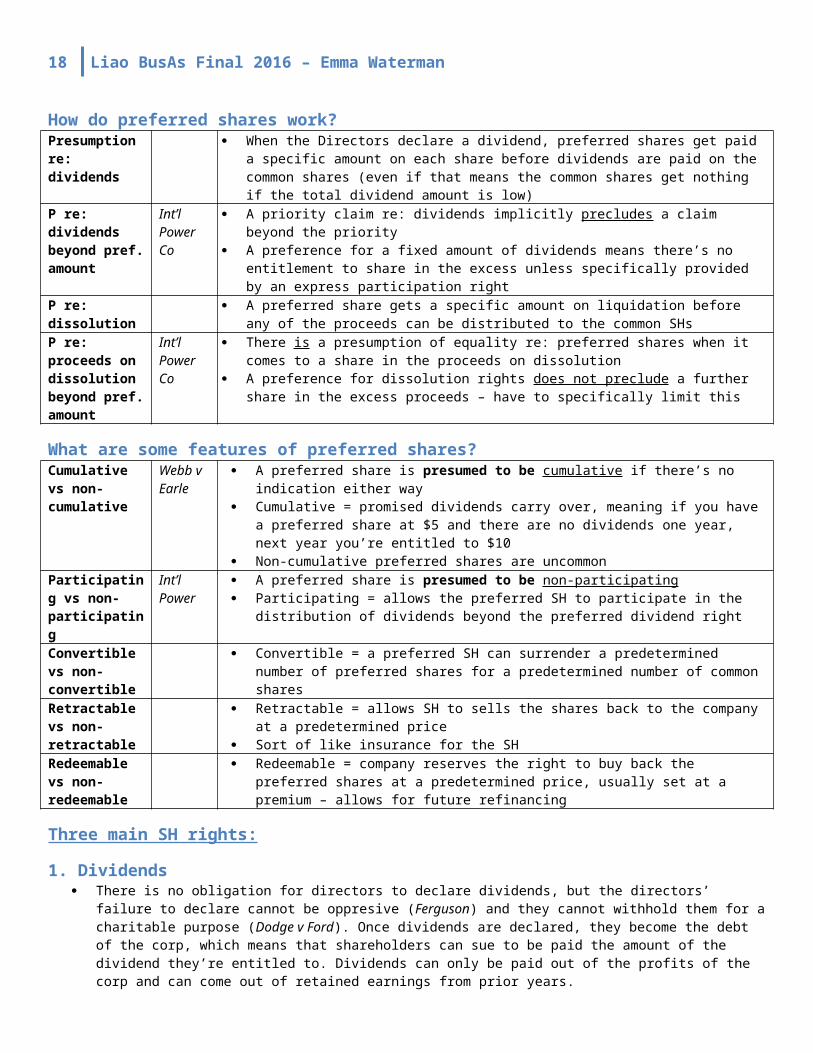

How do preferred shares work?Presumption re: dividends

When the Directors declare a dividend, preferred shares get paid a specific amount on each share before dividends are paid on the common shares (even if that means the common shares get nothing if the total dividend amount is low)

P re: dividends beyond pref. amount

Int’l Power Co

A priority claim re: dividends implicitly precludes a claim beyond the priority A preference for a fixed amount of dividends means there’s no entitlement to share in the

excess unless specifically provided by an express participation rightP re: dissolution A preferred share gets a specific amount on liquidation before any of the proceeds can be

distributed to the common SHsP re: proceeds on dissolution beyond pref. amount

Int’l Power Co

There is a presumption of equality re: preferred shares when it comes to a share in the proceeds on dissolution

A preference for dissolution rights does not preclude a further share in the excess proceeds – have to specifically limit this

What are some features of preferred shares?Cumulative vs non-cumulative

Webb v Earle

A preferred share is presumed to be cumulative if there’s no indication either way Cumulative = promised dividends carry over, meaning if you have a preferred share at $5 and

there are no dividends one year, next year you’re entitled to $10 Non-cumulative preferred shares are uncommon

Participating vs non-participating

Int’l Power

A preferred share is presumed to be non-participating Participating = allows the preferred SH to participate in the distribution of dividends beyond

the preferred dividend rightConvertible vs non-convertible

Convertible = a preferred SH can surrender a predetermined number of preferred shares for a predetermined number of common shares

Retractable vs non-retractable

Retractable = allows SH to sells the shares back to the company at a predetermined price Sort of like insurance for the SH

Redeemable vs non-redeemable

Redeemable = company reserves the right to buy back the preferred shares at a predetermined price, usually set at a premium – allows for future refinancing

Three main SH rights:

1. Dividends There is no obligation for directors to declare dividends, but the directors’ failure to declare cannot be oppresive (Ferguson)

and they cannot withhold them for a charitable purpose (Dodge v Ford). Once dividends are declared, they become the debt of the corp, which means that shareholders can sue to be paid the amount of the dividend they’re entitled to. Dividends can only be paid out of the profits of the corp and can come out of retained earnings from prior years.

Issue Where Rule

How are dividends paid?

CBCA 43 Payment in cash, specie, and stock dividends permittedo In specie: through other forms of property or inventoryo Stock: by paying out dividends by giving SHs additional stocks in the company

(basically just allows for more access to assets on dissolution102 Declared by directors, unless otherwise provided by unanimous SH agreement. Reinforced by

s115(3)(d) – they can’t delegate the power.When can’t they be paid?

42 Dividend cannot be paid if:(i) the corp is, or would be after the payment of the dividend, unable to pay its liabilities as

they come due; or(ii) the realizable value of the corp’s assets would, after the payment, be less than the

aggregate value of its liabilities and stated capital of all classes.Bottom line: can’t be paid if it would leave the company insolvent

118(2)(c) Directors are personally liable if they consent to a resolution that a dividend be declared where there are reasonable grounds for believing that the corp is:

(a) insolvent or(b) unable to pay its liabilities.

12 Liao BusAs Final 2016 – Emma Waterman

118(5) An SH who has received dividends in such circumstances can also be ordered to pay to directors any money the SH received as a result of a distribution of dividends contrary to s42

SHs get the dividends, but what about when the shares change hands?

134(1) Allows for the setting of a record date for the payment of dividends. The company will prepare a list of SHs of record on that date and the dividend will be paid to

“SHs of record” on that date. Shares that are publicly traded are said to go “ex dividend” on a date a few days ahead of the record date to allow for processing. Shares traded after the ex dividend date will not receive the dividend.

134(3) If no record date is set then the record date is the close of business on the day on which the directors pass the resolution declaring the dividend

2. Voting Voting rights are particularly important because a shareholder with a voting right has influence on the election of directors, and

through the directors, how the corp will be managed. Section Notes

Function of voting: electing directors

CBCA 2(1)

Directors are elected by “ordinary resolution” which is defined in 2(1) as a resolution passed by a majority of the votes cast by the SHs who voted in respect of the resolution

Function of voting: changing stuff

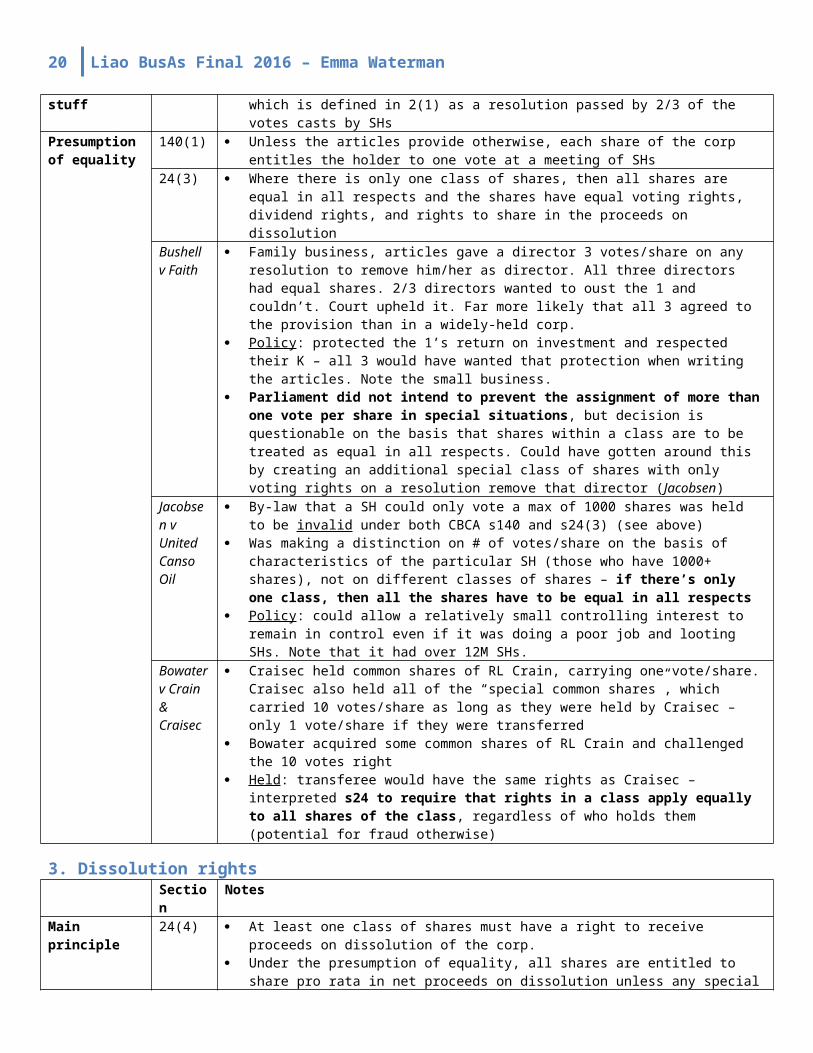

2(1) Holders of voting rights have to approve changes to the articles of incorp or certain major corporate transactions (amalgamation, continuance, or dissolution) through a “special resolution” which is defined in 2(1) as a resolution passed by 2/3 of the votes casts by SHs

Presumption of equality

140(1) Unless the articles provide otherwise, each share of the corp entitles the holder to one vote at a meeting of SHs

24(3) Where there is only one class of shares, then all shares are equal in all respects and the shares have equal voting rights, dividend rights, and rights to share in the proceeds on dissolution

Bushell v Faith

Family business, articles gave a director 3 votes/share on any resolution to remove him/her as director. All three directors had equal shares. 2/3 directors wanted to oust the 1 and couldn’t. Court upheld it. Far more likely that all 3 agreed to the provision than in a widely-held corp.

Policy : protected the 1’s return on investment and respected their K – all 3 would have wanted that protection when writing the articles. Note the small business.

Parliament did not intend to prevent the assignment of more than one vote per share in special situations, but decision is questionable on the basis that shares within a class are to be treated as equal in all respects. Could have gotten around this by creating an additional special class of shares with only voting rights on a resolution remove that director (Jacobsen)

Jacobsen v United Canso Oil

By-law that a SH could only vote a max of 1000 shares was held to be invalid under both CBCA s140 and s24(3) (see above)

Was making a distinction on # of votes/share on the basis of characteristics of the particular SH (those who have 1000+ shares), not on different classes of shares – if there’s only one class, then all the shares have to be equal in all respects

Policy : could allow a relatively small controlling interest to remain in control even if it was doing a poor job and looting SHs. Note that it had over 12M SHs.

Bowater v Crain & Craisec

Craisec held common shares of RL Crain, carrying one vote/share. Craisec also held all of the “special common shares”, which carried 10 votes/share as long as they were held by Craisec – only 1 vote/share if they were transferred

Bowater acquired some common shares of RL Crain and challenged the 10 votes right Held : transferee would have the same rights as Craisec – interpreted s24 to require that rights

in a class apply equally to all shares of the class, regardless of who holds them (potential for fraud otherwise)

3. Dissolution rights Section Notes

Main principle 24(4) At least one class of shares must have a right to receive proceeds on dissolution of the corp. Under the presumption of equality, all shares are entitled to share pro rata in net proceeds on

dissolution unless any special entitlements indicated in the articles

Liao BusAs Final 2016 – Emma Waterman 13

Pre-emptive rightsNotes

What? Give existing SHs of a class of shares the right to purchase any newly issued shares of that classHow? If an SH owns 50% of the shares and the company decides to issue an additional 20K shares, the SH gets the

pro rata right to purchase 10K of themWhy? To maintain the SH’s proportionate interests of shares in a given classWhere? Optional under s28 of the CBCA

Issuing and paying for sharesIssue Section NotesWho decides? CBCA

25(1) Subject to the articles, the by-laws or any USA, it is the directors who decide on when

to issue shares, who to issue them to and for what consideration.115(3) This is a power that the directors cannot delegate (“non-delegable power”)

Does the limit exist?

6(1)(c) The corp can set out an authorized amount in the articles if a limit on the amount of shares the directors can issue without going back to the SHs is desired

CBCA also allows the articles to not set out an authorized limit Basically, it’s optional and there’s no super convincing reason to do it

Subscriptions and allotment

115(3) The directors will decide which subscriptions to accept and thus to whom the shares will be issued. When directors make this decision they are said to “allot” the shares.

“Subscriptions for shares” means an application to purchase shares; “subscription” is normally an offer to buy shares which can be accepted by the corp.

14Re Canadian Tractor Co;Timing of subscription

The subscription is normally treated as an offer. The corp could not validly accept the offer until it became incorporated. The SH could, therefore, withdraw her or his offer before acceptance by the corp and, since it is merely an offer, the corp, once incorporated, is not bound to accept the offer

25(3)Fully paid for

Requires that shares be fully paid for. A promissory note or promise to pay is not considered property for which shares may be issued (see 25(5)).

In the past, companies would take a down payment on the shares called “subscriptions receivable” – deceiving to creditors

Assessable vs non-assessable

25(2) Shares must be non-assessable. Can’t make SHs make further contributions to the company on top of their shares.

Consideration 25 Allows the directors to issue shares for whatever consideration (money, property, or past services) the directors determine.

“Watered stock” problem

Watered stock is an asset with an artificially inflated value. The term is most often used to refer to a form of securities fraud common under older corporate laws that placed a heavy emphasis upon the par value of stock - deceiving to the creditors

Corps often attribute the inflation to “goodwill”25(3) A share shall not be issued until the consideration for the share is fully paid in money,

or in property or past services that are not less in value than the fair equivalent of the money that the corp would have received if the shares had been issued for money

Basically, watered stock isn’t allowedRemedies 118(1)

Directors J&S liable

Directors of a corp who vote for or consent to a resolution authorizing the issue of a share under s25 for a consideration other than money are jointly and severally liable to the corp to make good any amount by which the consideration received is less than the fair equivalent of the money that the corp would have received if the share had been issued for money on the date of the resolution

118(6)Defence

Defence to this^ – if they did not know and could not reasonably have known that the share was issued for consideration way less than what it as worth

251 Directors who issue watered stock can go to jail for breaching a provision of the CBCAActions against SHs

Possible to bring actions against SHs who contributed consideration for way less than the recorded price of the shares, and for creditors to make such a claim under OR

Note 26(1) Remember, you need a stated capital account for all classes and series of shares issued

14 Liao BusAs Final 2016 – Emma Waterman

Repurchase and redemption of shares Issue Section Rule

Repurchase“Anyone want to sell shares back?

CBCA 34(2) A corp can repurchase its own shares as long as when it does so it does not violate financial solvency tests:1. The corp is, or would after the payment be, unable to pay its liabilities as they come

due; or2. The realizable value of the corp’s assets would after the payment be less than the

aggregate value of its liabilities and stated capital of all classes. Policy: the corp must be able to pay its liabilities and return capital to SHs, otherwise

creditors or minority SHs could be taken advantage ofSelf-shareholding

s. 30(1) A CBCA corp is not permitted to hold shares in itself (to hold “treasury stock”) If it does repurchase its own shares, it must cancel them, or, where it has a limit on the

number of authorized shares, it can restore the shares to the status of authorized but unissued shares.

Redemption“Sell us your shares back”

36(1) A corp may also purchase its own shares as a result of an express term for the repurchase of shares in its articles (eg as part of a redemption right on a particular class of shares)

Policy : protects creditors and SHs with prior claims/higher preference:o If a corp has class A common shares, class B shares w/ a liquidation preference

over A, and class C shares w/ a liquidation preference over A & B, C shares would lose their liquidation preference if B shares could be redeemed at a price that would cause the corp to be unable to pay C shares their pref amount on liquidation

36(2) The corp may not redeem the shares if… -> same as 34(2) test for repurchaseRemedy Directors can be personally liable to restore to the corp any amounts paid contrary to the

financial solvency tests in 34(2) or 36(2). SHs who receive amounts paid contrary to these provisions may be required to return the amounts to the directors (118(5))

Series of sharesIssue Where Rule

When?Used when funds are needed ASAP

CBCA 27 Directors can be allowed to issue shares of a class in a “series” to make them more marketable at a particular time

Each series of a given class of shares can be given separate rights and restrictions that may be more appropriate for marketing shares at the time the directors choose to issue them

The authority to issue shares of a particular class in series has to be given to the directors when the class is created – it must appear in the original articles or the articles have to be amended subsequently (more of a hassle) to allow it

Allows for expediency – w/o this provision the directors would have to go to SHs for approval to amend the articles to create a whole new class of shares – can take too long

Exceptions 27(3) No series in a class can be given any priority over any other class in the series with respect to dividends or proceeds on liquidation

Protects against unfair surprise to existing SHs

Par value shares and no par value shares History The par value of a share was originally the minimum amount the SH was required to contribute on the shares.

The PV of contribution would be attributed to all the shares in a given class. If shares were sold at a price less than PV, the SH’s liability was not limited to the amount paid in. It was a ready

source of finance b/c the corp could call up those who had paid less than PV for their shares to pay the difference The PV might also be said to provide creditors with a basis for assessing the amount of capital they could access

to cover the credit they extended. They could do this by multiplying the number of shares by the PV. If the company were to become bankrupt the creditors could seek payment from SHs who paid a price for their

shares of less than the PV and could force them to pay the difference between the PV and the price they paid.Currently

PV figure has become meaningless because there was no source of finance and no relation to the available capital – it contributed to deceiving surplus and deceiving investors as to the worth of a share

24(1) of the CBCA provides for shares without PV only

Liao BusAs Final 2016 – Emma Waterman 15

The stated capital account Issue Where Rule

Contents CBCA s26(1)

A stated capital account is maintained for each class or series of shares that has been issued Consists of the total amount (what you’ve made) for which shares of the class or series have

been issuedNature Stated capital is not cash

It’s a bookkeeping entry to indicate how much was raised by selling particular classes/series of shares The funds received will appear as an asset on the balance sheet It’s a historical record – doesn’t go up or down with increases or decreases in value of assets

Accounting for changes

39 If more shares of a class or series are issued the applicable stated capital account must be adjusted to reflect the increase in the total amount of funds raised by the sale of shares of that class or series

Need to disclose stated capital per share multiplied by the number of shares purchased, redeemed or acquired

Have to adjust the stated capital account if more shares of a class or series are issued or if the shares are redeemed or repurchased

SH approval of reduction of stated capital

CBCA 38(1) (approval)(per s. 38(3)(rules

SHs can approve a reduction in the stated capital account – might choose to if there’s a desire to distribute capital to SHs

The return of capital has an affect on the success of the business and can have tax consequences for individual SHs

A return of capital cannot be made unless:(i) the corp is, or after the reduction would be, unable to pay its liabilities as they become

due; or(ii) the realizable value of the corp’s assets would thereby be less than the aggregate of its

liabilities.

16 Liao BusAs Final 2016 – Emma Waterman

Directors and Officers

Directors: elections, qualifications, authority, power, delegation, removal of officers, meetingsIssue Section NotesWhat do they do?

CBCA 102 Manage, or supervise management of, the corp121 Appoint officers that conduct day to day business/mgmt of the company

Who’s eligible? 105 Must be: Natural persons Over 18 years of age Not adjudicated as mental incompetents or bankrupts

Do they need to own shares?

105(2) No, unless specified in the articles Why should they? Many in business agree that directors should own shares – then have skin in

the game and will personally suffer financially if a poor decision is made for the company Why shouldn’t they? Directors could get too focused on only share value and might have to be

at a certain level of wealth to afford buying inHow many are needed?

102 Minimum of one for a non-distributing (private) corp Minimum of three for distributing (public) corp No maximum, seven – nine is usually ideal

Where do they have to live?

105(3) At least 25% of directors on a board must be “resident Canadians” (citizen or permanent resident under reg 13 of CBCA)

If there are less than four directors, at least one must be a “resident Canadian”How do they get elected?

106(1)1st round

Must send a notice of the first directors of the corp in to the Director to form a corpo They hold office until the first AGM (106(2))

106(3)Elected

Directors are elected at the first AGM and every meeting thereafter by an “ordinary resolution” of the SHs (majority of votes cast by SHs)

o Can’t waive this or alter this in the articles – SHs have to elect the directors106(8)Exception

Articles can allow for 1/3 of the total number of directors to be appointed by the directors elected by the SHs

What is slate voting?

A group of directors are nominated for election by the mgmt of the company and they’re voted on as “all or nothing”

o Pro: can have a really cohesive groupo Con: less SH input

What is plurality voting?

A candidate who receives the most votes wins Votes are either “for” or “withheld” Means that if one vote is “for” and 999 are “withheld”, that director still gets elected

Terms of office-> Term limit? 106(3),(5) Normally the limit is until the next AGM but articles can provide for a term of up to three years-> Limit on re-election?

106(6) No limit - incumbent directors remain in office until successors are chosen if no new directors get elected at a meeting

-> Staggered boards?

106(4) Articles can provide that not all directors be elected at the same meetingo Pros: stability – can’t flip the whole board in a yearo Cons: transition costs, familiarity issues, needing to gel

-> If there’s a controversy?

145 Corp, SH, or director may apply to the court to resolve controversy concerning elections of appointments of a director

-> Ceasing to be a director?

108 Director ceases to hold office during his or her term of office if she dies, resigns, becomes disqualified, or is removed from office by ordinary resolution of the SHs

How to remove a director?

109(1) Through ordinary resolution of SHs (majority votes cast at a special meeting) Articles cannot provide a greater majority than that called for in 109(1) Bushell: majority of votes cast still works since there were special voting shares (questionable)

What are their mgmt powers?

102 General power to manage or supervise mgmt (subject to unanimous SH agreement) Operates as a residual power – if a power isn’t allocated elsewhere, it’s probably a mgmt power

What can’t they delegate?

115(3) Cannot delegate the following: submitting any Q/matter requiring approval of SHs to the SHs, declaring dividends, buying/redeeming/acquiring shares issued by corp, approval of mgmt proxy circular, approval of takeover bid by corp or director’s circular, approval of financial

Liao BusAs Final 2016 – Emma Waterman 17

statement put before SHsDelegation case law

Hayes v Canada-Atlantic

Directors cannot delegate all of their powers Later codified in 115(3)

Sherman & Ellis

Can delegate some mgmt powers but only for a limited period and can only delegate certain powers (20 years was too long)

Kennerson v Burbank

A Board can delegate its authority to act but cannot delegate its function to govern As long as a corp exists, its affairs must be managed by its duly elected board

Do they appoint officers?

121 Yes, subject to the articles, by-laws, or USA They also delegate powers to offers, subject to the articles/by-laws, or USA

What about compensation?

125 Directors determine officer compensation (& compensation for employees and the directors themselves – clear conflict of interest), subject to the articles/b-l/USA

Removal of officers

Re Paramount

Directors can remove a person from office or agency but if they dismissed the person from employment it still leads to damages for breach of the employment K – terms are still relevant

Shindler Where a party enters into a K, there is implied engagement on his part that he shall do nothing of his own motion to put end to that state of circumstances

Pros & cons

Courts tend to enforce long-term employment Ks for officers – if not, corps would have to pay more to account for the lack of job security

Downside – directors have to deal a bad officer or pay out if they want to fire herGolden/ tin parachute

Perform an important function: reduce incentive for mgmt to resist takeovers (since they get such a pay out when they get fired) and attracts top talent, but when is it too much?

CEO of Walt Disney got $1B when he was asked to step downDo they have to call meetings?

133 Yes, have to call annual or special meetings of the SHs Directors also determine the agenda for these meetings, which allows them considerable

control over the governance of the corpHow are meetings run?

N/A Details of directors’ meetings are left to the corp’s by-laws114 Subject to articles or by-laws, directors meet at any place and on such notice as by-laws require114(2) Subject to articles or by-laws, quorum is the majority of the board or a majority of the

minimum number of directors in the articles114(5) If a meeting deals with a matter in 115(3), notice of the meeting must specifically indicate that

Besides that, no requirement to specify the purpose of the meeting114(6) Can waive notice of a meeting in any manner114(9) Can conduct meetings by conference call or electronically and a director participating by such

means is deemed to be present114(8) If there’s only one director, that director may constitute a meeting117 If all directors sign a written resolution in lieu of a meeting, you don’t have to hold one –

common in closely-held corps where all the directors agree on a matter to be dealt withOther miscellaneous powers

103 Power to adopt, amend, or repeal by-laws, subject to articles/b-l/USA189(1) Power to borrow, subject to the articles, by-laws, or USA25 Power to issue shares106(8) Appointment of additional directors (no more than 1/3 of the total number of directors)

Can they fill vacancies of directors or auditors?

111(1) Yes, due to death or resignation, but not due to an increase in number, a minimum number of directors, or the SHs failure to elect the required number of directors

109(3) Can fill a vacancy on the removal of a director if the SHs do not166(1) Auditors are normally appointed by the SHs at an AGM, but directors can replace the auditor if

she resigns during the year unless the articles forbid it (166(3))

18 Liao BusAs Final 2016 – Emma Waterman

Shareholder rightsIssue Section NotesWhat do they do?

Mandatory: SHs with voting shares elect directors, approve by-law amendments, and approve fundamental changes – these are non-delegable powers

o However, non-voting shares can vote as a class where the rights of the class would be prejudicially affected by a proposed change

Default: certain director powers can be allocated to SHs subject to articles/b-l/USA like power to appoint officers (121) & borrowing power (189(1)); can also reallocate the mgmt/supervision of mgmt power but must be done by unanimous SH agreement (102)

Power to manage

Automatic Self-Cleansing

SHs voted to sell assets and wanted Court to order the Directors to do so, but the Court refused Directors aren’t agents to SHs and SHs aren’t principals with power to dictate to directors Pros: SHs can be reactionary, Directors have responsibilities for interests of whole corp, not just

profits, Directors have long-term plans*Business judgment rule

A Board has the right to make whatever decisions it would like within a reasonable, broad set of alternatives – as long as it is within its fiduciary duties, the Court won’t question it (Brant, Ford Canada)

Power in cases of deadlock

Barron v Potter

Two directors required for quorum, but there were only two directors total and one was refusing to come to meetings, so they couldn’t get quorum

There was a deadlock – Barron wanted an extraordinary meeting of SHs to appoint additional directors, while Potter wanted the directors to exercise their power to appoint additional directors in the interim period

Held that SHs could appoint new directors at an extraordinary meeting since “for practical purposes there was no board of directors at all” – unclear how persuasive this is since appointing directors is a power SHs normally have

Power to elect directors

106(3) SHs have the power to elect directors at AGMs – one of their most important rights

Power to amend by-laws

103 The default is that directors have the right to initiate by-laws changes, but these changes must be ratified by the SHs at the next AGM (by ordinary resolution)

This can be altered in the articles, bylaws, or by unanimous SH agreementFundamental changes (all need special resolutions)

173 173(1) sets out several fundamental changes that require a special resolution of the SHs – they all involve changes to the articles of incorp:a) Change the corp nameb) Change the province of the registered officec) Change a restriction on the business of the corpd) Change any max number of shares that the corp is authorized to issuee) Create a new class of sharesf) Reduce or increase its stated capital, if its stated capital is set out in the articlesg) Increase or decrease the number, or the minimum or maximum number, of directorsh) Change restrictions on share transfer

Special resolution: defined in 2(1) as requiring 2/3 of the votes cast in respect of the particular resolution at an SH meeting

183 To approve amalgamation of corp with another corp188 Continuance of corp under laws of another jurisdiction - every share can vote, not just voting189(3) Sale or lease of all or substantially all of a corp’s assets - every share can vote, not just voting211 Liquidation and dissolution of corp – requires special resolution from each class of shares

Note: who changes articles?

175(1) A director or an SH who is entitled to vote at an annual meeting of SHs may, in accordance with 137, make a proposal to amend the articles

What is class voting?

When classes of shares vote collectively in a separate resolution to approve (or not approve) a change that alters or prejudices the rights of that class – requires a special resolution

It is a mandatory right – cannot be taken awayWhen is class voting required?

176(1) (i) to increase or decrease any authorized limit on class of shares(ii) where there is an exchange, reclassification, or cancellation of shares(iii) to add, change or remove rights, privileges or restrictions on class of shares(iv) to increase rights or privileges of any class of shares having rights equal to or superior to shares

Liao BusAs Final 2016 – Emma Waterman 19

of such class(v) to create a new class of shares equal to or superior to a particular class (176(1)(e))(vi) to make an inferior class of shares equal or superior to a particular class

What is a series vote?

176(4) When a series of shares within a class are affected by a resolution in some manner different from the other series in that class, then that series has the right to vote separately

What if they’re non-voting shares?

176(5) Confirms that in certain circumstances, including where class rights arise, all classes of shares get to vote even if they don’t have voting rights

This happens after the special resolution vote cast by the voting shares that decide to open the issue up in the first place

Separate resolution required?

176(6) Yes, a separate resolution of the class is required and it must be a special resolution of the class

Class voting rights in fundamental changes

183(4) On amalgamation, the SHs of a class or series of shares of each amalgamating corp are entitled to vote separately as a class or series re: the amalgamation agreement if the amalgamation agreement contains a provision that, if contained in a proposed amendment to the articles, would entitle such holders to vote as a class or series under s176

189(7) May arise on sale, lease, or exchange of all or substantially all of the assets of a corp211(3) May arise on liquidation and dissolution

May arise on continuanceDoes voting matter?

Many SHs have small stakes and there’s a free rider problem (SHs free ride on monitoring effects of other SHs) = rational SH apathy develops

Some argue that it’s bad for institutional democracy not to vote Can just sell your shares if you don’t like how the company’s being run

SH monitoring Control blocks of shares (like an SH who owns 20%) typically do monitor management – they sell at a premium to other shares and where trades happen, changes in senior mgmt often follow

Market for corp control

Promoters of a corp often publically distribute voting shares because it exposes them to takeover risks, so incentivizes effective mgmt – this looks good to investors and facilitates raising the required capital

20 Liao BusAs Final 2016 – Emma Waterman

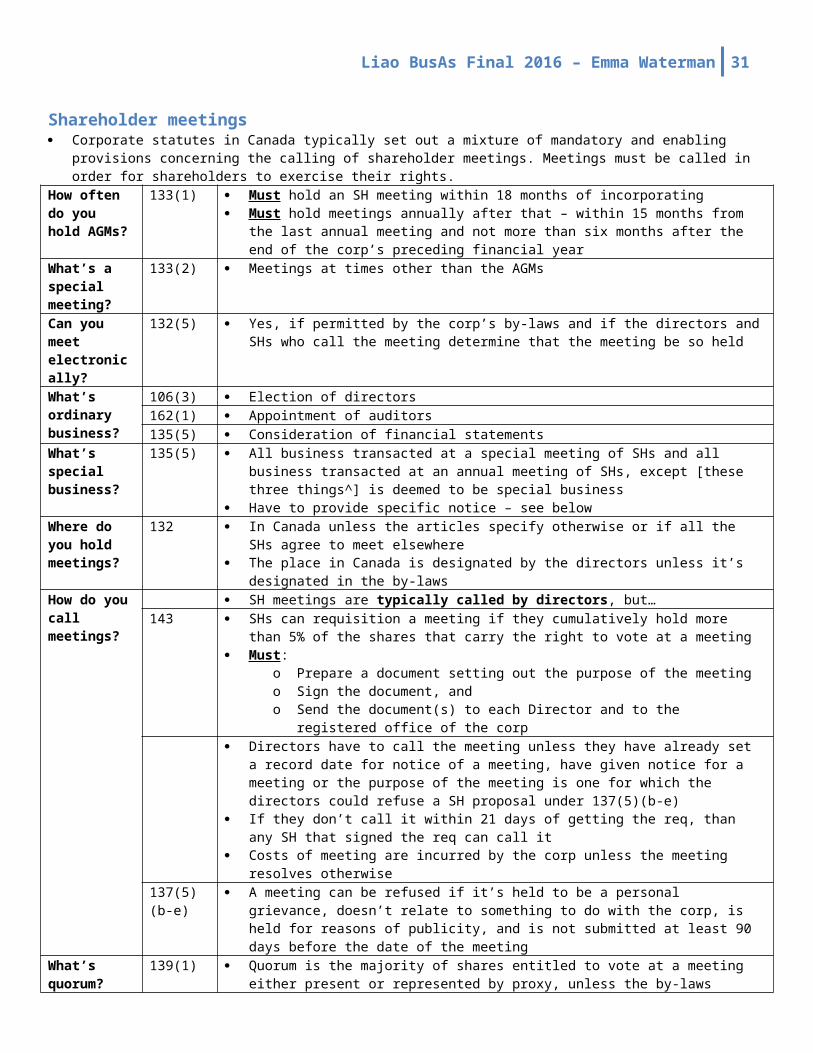

Shareholder meetings Corporate statutes in Canada typically set out a mixture of mandatory and enabling provisions concerning the calling of

shareholder meetings. Meetings must be called in order for shareholders to exercise their rights.How often do you hold AGMs?

133(1) Must hold an SH meeting within 18 months of incorporating Must hold meetings annually after that – within 15 months from the last annual meeting and

not more than six months after the end of the corp’s preceding financial yearWhat’s a special meeting?

133(2) Meetings at times other than the AGMs

Can you meet electronically?

132(5) Yes, if permitted by the corp’s by-laws and if the directors and SHs who call the meeting determine that the meeting be so held

What’s ordinary business?

106(3) Election of directors162(1) Appointment of auditors135(5) Consideration of financial statements

What’s special business?

135(5) All business transacted at a special meeting of SHs and all business transacted at an annual meeting of SHs, except [these three things^] is deemed to be special business

Have to provide specific notice – see belowWhere do you hold meetings?

132 In Canada unless the articles specify otherwise or if all the SHs agree to meet elsewhere The place in Canada is designated by the directors unless it’s designated in the by-laws

How do you call meetings?

SH meetings are typically called by directors, but…143 SHs can requisition a meeting if they cumulatively hold more than 5% of the shares that carry

the right to vote at a meeting Must :

o Prepare a document setting out the purpose of the meetingo Sign the document, ando Send the document(s) to each Director and to the registered office of the corp

Directors have to call the meeting unless they have already set a record date for notice of a meeting, have given notice for a meeting or the purpose of the meeting is one for which the directors could refuse a SH proposal under 137(5)(b-e)

If they don’t call it within 21 days of getting the req, than any SH that signed the req can call it Costs of meeting are incurred by the corp unless the meeting resolves otherwise

137(5)(b-e) A meeting can be refused if it’s held to be a personal grievance, doesn’t relate to something to do with the corp, is held for reasons of publicity, and is not submitted at least 90 days before the date of the meeting

What’s quorum?

139(1) Quorum is the majority of shares entitled to vote at a meeting either present or represented by proxy, unless the by-laws provide otherwise

139(2) It doesn’t have to continue through the meeting – people can leave139(3) If there’s no quorum at the beginning of the meeting, SHs can’t transact any business

How much notice do you have to give?

135(1) and reg 44

Require a notice period of at least 21 days but not more than 60 days in advance of meeting

134 The record date (date that current SHs are considered entitled to vote at the meeting) cannot be set more than 60 days ahead of the meeting

135(6) Notice of special business must state the nature of the business in sufficient detail to allow an SH to make a reasoned judgment on whether to vote for or against the resolution

Normal meeting process

Designated person takes Chair Chair receives report of scrutineers on proof of notice of meeting and presence of a quorum Motion typically requested to dispense with reading of minutes of last annual meeting and motion for

approval of minutes of last annual meeting then requested Annual report then typically presented with president’s remarks, auditor’s report read out, and then typically

a SH vote on motion to financial statements Election of directors: slate typically proposed by mgmt ahead of time with no additional nominations (motion

for approval of the slate then voted on)o Where there are additional nominations, procedure is to distribute ballots where the SHs or

proxyholders can mark in the nominees in favour of whom they wish to vote their shares

Liao BusAs Final 2016 – Emma Waterman 21

A motion for appointment of auditors (normally the previous year’s auditors) and meeting may then approve motion concerning remuneration of the auditors

How do you vote?

141(1) Done by show of hands unless a poll is demanded141(2) Poll can be demanded before or after a vote by show of hands

Do you have to keep minutes?

20(1))b) Yes, and they must be signed by the Chair

Who is Chair? By-laws normally provide that the Chair of the Board or the President chairs SH meetingsWhat are the Chair’s duties?

Wall v London

Chairs must act in good faith, be impartial, and allow SHs to speak to a matter before the meeting, BUT need only to allow a reasonable time for debate

Re Marshall

Chair does not have to go behind legal title to see if the beneficial owner’s instructions have been followedo If a bank, brokerage, or trustee is holding shares for the beneficial owner (the person

who owns the security in equity) and is voting, Chair has no responsibility to figure out what the beneficial owner’s instructions were/are

Re United Canso Oil

Chair did not act impartially because he refused to accept a tabulation of votes from professional tabulators, he refused to accept certain proxy votes, and ruled that quorum was not present and adjourned the meeting

Blair Blair was Chair and President, he asked his lawyer about whether proxies could be voted for or against the mgmt slate of directors, lawyer said yes and Blair followed that advice

The company was bought by another, and the new company sued Blair for that vote – issue was whether he had acted honestly and in good faith (as required for an indemnification order)

Held: legal advice does not automatically exonerate the Chair, but it helps

22 Liao BusAs Final 2016 – Emma Waterman

Miscellaneous: proxy solicitation, financial disclosure, access to SH lists, court-ordered meetings

Proxy Solicitation Proxy solicitation arguably provides shareholders with a greater scope for the exercise of shareholder democracy in that

they are given a better opportunity to be represented at the shareholders’ meeting and have information to make a more informed use of their voting rights in advance. It can help to combat the problems of “free-riding” and shareholder apathy. However, it can be difficult to collect all of the required information in advance.

What’s a proxy? 147 A form signed by an SH that appoints a proxyholder (PH)What’s a proxyholder?

147 A person appointed to act on behalf of the SH

Who can appoint a PH?

148 An SH entitled to vote at a meeting of SHs

What are a PH’s rights?

148 Same as the SH subject to authority granted by SH (think agency law) They can demand polls

Who must solicit proxies?

149(1) Mgmt must solicit proxies from each SH entitled to vote Failing to do so is an offence under 149(3)&(4) Can be enforced through a compliance order under 247 Policy: to ensure democracy and a fair process

Exception 149(2) Mgmt isn’t required to do so if the corp isn’t a distributing corp (public) and has 50 or fewer SHs entitled to vote at a meeting

What is the form of proxy?

The forms for proxies are set out a Canadian Securities Regulators “National Instrument (NI 51-102)” – the instrument was adopted by regulation under provincial securities regulation

o Requires clear indication that someone other than designated person can be appointed (9.4(3))

o Requires that person soliciting proxies state who is soliciting (9.4(1))o Allowing voting for or against resolutions or bold-face indication of how PH will vote

shares (9.4(4)o Providing means by which SH can vote in favour of or withhold voting with respect to

appointment of auditor or election of directors (9.4(6))What is a proxy circular?

A document containing sufficient info to allow SH to make voting decisions on business matters The statutory form sets out certain required info, per provincial securities regulation Must contain additional info to the extent required to allow an SH to make a reasoned choice

What is solicitation?

147 A request to execute or not to execute a form of proxy or to revoke a proxy and the sending of a form of proxy or other communication to an SH under circumstances calculated to result in the procurement, withholding or revocation of a proxy

Buckley Letter saying “we ask you not to sign any proxy for the Buckley slate of directors” was held to be a solicitation under the definition in 147

Can SHs put their own proposals forward?

137 Yes, registered or beneficial SHs can put proposals before the meeting and put a supporting statement on the managing proxy circular

Relatively low cost137(1.1) & reg 46

SH or group of SH can only put the proposal forward if he/she/they has at least 1% of the voting shares or market value of shares held is at least $2K, and shares have been held for at least 6 months

137(5) Proposal must be submitted at least 90 days ahead of the meeting, must not be for the primary purpose of redressing a personal grievance, must relate in a significant way to affairs of the corp, can’t be to secure publicity

What if corp refuses proposal?

137(7) Must give notice of refusal137(8) SHs can apply to court for consideration of whether the proposal was properly refused137(9) Corp can als apply to the court to determine whether proposal can be properly refused

Remedies 154 Talked about this with Kayli & Robin, but not in class

Liao BusAs Final 2016 – Emma Waterman 23

Financial DisclosureFinancial disclosure requirements

155 Directors have to put comparative annual financial statements before SHs158 The statements have to be formally approved by the directorsReg 72 They must include a balance sheet, income statement, statement of retained earnings

(showing increases to and decreases in retained earnings) and statement of changes in financial position (showing sources and uses of funds)

Auditor & audits

162, 163 Distributing corp must appoint an auditor who’s in good standing and w/ no conflict of interest A non-distributing corp can dispense with the appointment of an auditor via resolution

155 Auditor’s report has to be put before the SHs171 A distributing corp must have an audit committee consisting of a minimum of three directors,

majority of whom aren’t officers or employees of the corp Committee must review financial statements before the directors approve them Corp auditor is allowed to attend all their meetings

National Instrument

NI 52-109 Annual and interim financial statements must be certified by the CFO and CEO of the reporting issuer; the certificate requires officers to certify that the annual financial statements, based on their knowledge, fairly present the financial condition of the issuer – an additional layer

Access to List of SHsWhy is it important?

For engaging in proxy solicitations, requisitioning a meeting, and making a takeover bid

Who has the list?

Only the company – typically left at their lawyer’s office

Who can request it?

For a distributing corp, anyone (21(3)) For a non-distributing corp, SHs and creditors

How do you request it?

21 By paying a reasonable fee set by the corp and sending an affidavit with name and address Must indicate that the list will not be used for a purpose other than an effort to influence the

voting of shares of the corp; an offer to acquires shares of the corp; or any other matter relating to the affairs of the corp

What must the corp do?

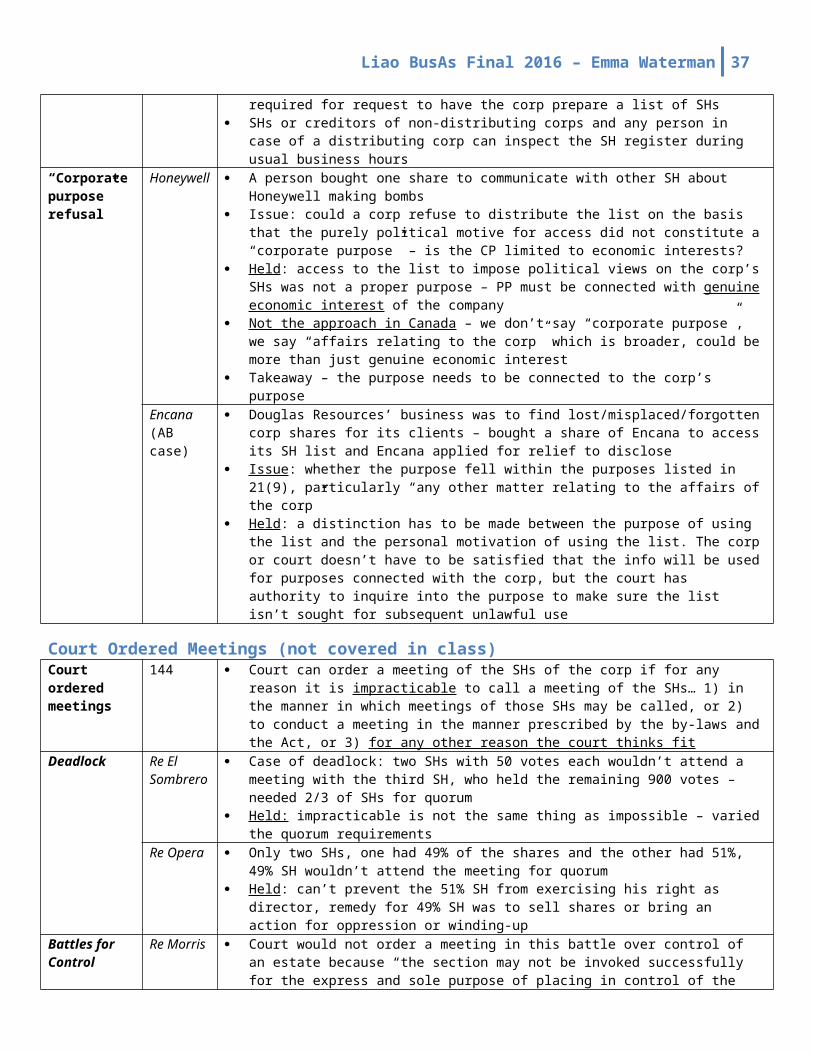

21(3) It must provide the list within 10 days and it must be made up within 10 days prior to the receipt of the affidavit

This gives them time to respond – might know something is up when someone requests itAccess to SH register?

20(1)(d) The corp is required to keep an SH register with the names and addresses of all SHs21(1) Right to inspect the list at the records office of the corp during usual business hours

The person seeking access must provide the same affidavit required for request to have the corp prepare a list of SHs

SHs or creditors of non-distributing corps and any person in case of a distributing corp can inspect the SH register during usual business hours

“Corporate purpose” refusal

Honeywell A person bought one share to communicate with other SH about Honeywell making bombs Issue: could a corp refuse to distribute the list on the basis that the purely political motive for

access did not constitute a “corporate purpose” – is the CP limited to economic interests? Held : access to the list to impose political views on the corp’s SHs was not a proper purpose –

PP must be connected with genuine economic interest of the company Not the approach in Canada – we don’t say “corporate purpose”, we say “affairs relating to the

corp” which is broader, could be more than just genuine economic interest Takeaway – the purpose needs to be connected to the corp’s purpose

Encana (AB case)

Douglas Resources’ business was to find lost/misplaced/forgotten corp shares for its clients – bought a share of Encana to access its SH list and Encana applied for relief to disclose

Issue : whether the purpose fell within the purposes listed in 21(9), particularly “any other matter relating to the affairs of the corp”

Held : a distinction has to be made between the purpose of using the list and the personal motivation of using the list. The corp or court doesn’t have to be satisfied that the info will be used for purposes connected with the corp, but the court has authority to inquire into the purpose to make sure the list isn’t sought for subsequent unlawful use

24 Liao BusAs Final 2016 – Emma Waterman

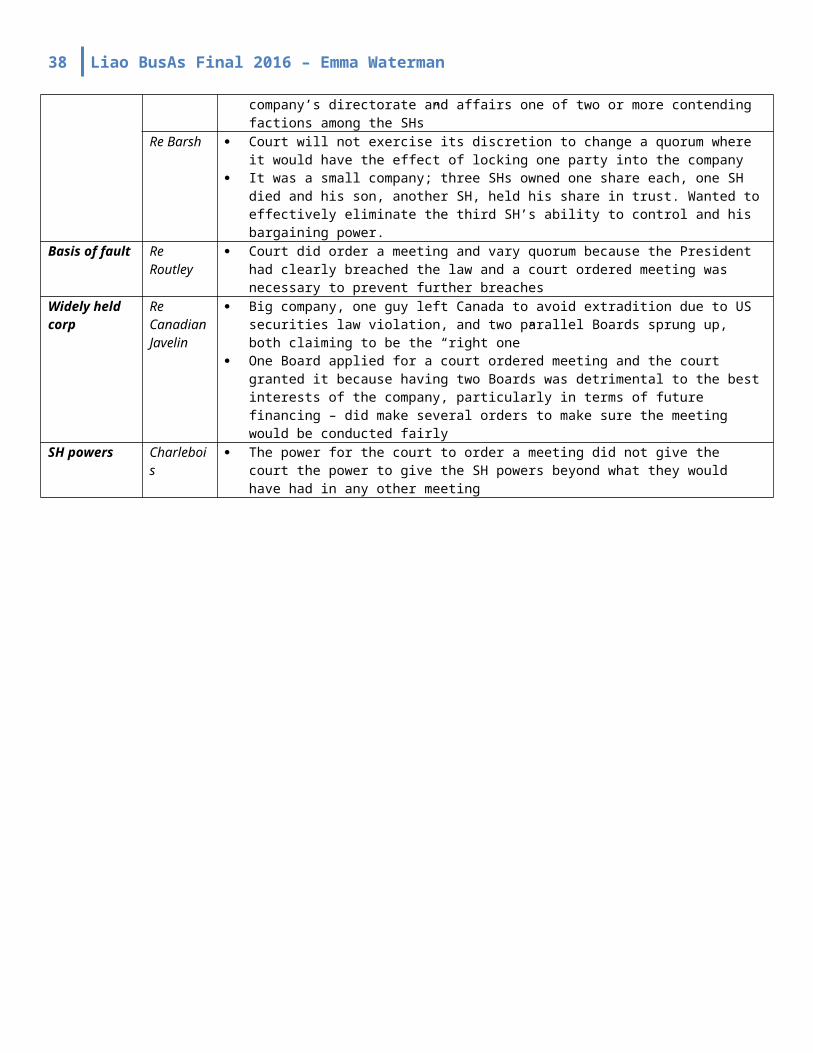

Court Ordered Meetings (not covered in class)Court ordered meetings