lightbox is ready to melt

TRANSCRIPT

1

2 ©LIGHTBOX

3 ©LIGHTBOX

4

The tech economy Next big things

©LIGHTBOX

5

THE MOST EXCITING TECH

MARKET ON THE PLANET

©LIGHTBOX

6

Only billion person market in the world going through this

change ©LIGHTBOX

7 ©LIGHTBOX

8

WHAT IF…

©LIGHTBOX

9

What is disruption?

©LIGHTBOX

10 ©LIGHTBOX

11

75MM installs

13MM wallets

12MM downloads

47% revenue from mobile

100% on app

100MM views for IPL

1,15,000 cars

5 BN monthly views ©LIGHTBOX

800MM monthly active users

12

That’s only 11% of the Indian population

Penetration of leading social networks in India as of 4th quarter 2014

©LIGHTBOX

13

MANY CHANGES IN PARALLEL

Consumption per capita

Urbanisation

Organised retail

Technology adoption

Business models ©LIGHTBOX

14

To millions of Indians, shopping on mobile is not an electronic form of commerce,

it’s commerce pure and simple

©LIGHTBOX

15

Disruptive models hit harder here

©LIGHTBOX

16 ©LIGHTBOX

115,000 cabs makes Ola in India bigger than Uber in America

Source: vccircle, ‘We are now bigger in India than Uber in its home country US:” Ola CEO Bhavish Aggarwal , 2 March 2015

17

A 7 year old tech startup is India’s largest retail company by volume, value and growth

©LIGHTBOX

18

Localization and user experience win

©LIGHTBOX

19

Soundbites from the Indian tech scene

Abandoning premium to go mass

©LIGHTBOX

20

The tech economy Next big things

©LIGHTBOX

21

17 October, 2014

Growing Vibrant Emerging Potential Large Hot Dynamic Bursting Energetic

©LIGHTBOX ©LIGHTBOX

22

17 October, 2014

Growing Vibrant Emerging Potential Large Hot Dynamic Bursting Energetic

Inefficient Fragmented Disorganized Chaotic Bureaucratic Complicated Dysfunctional Slow Difficult

©LIGHTBOX ©LIGHTBOX

23

TECHNOLOGY

©LIGHTBOX

24

BUILDING vs

BETTING

©LIGHTBOX

25 ©LIGHTBOX

26 ©LIGHTBOX

Fintech 27%

Content 3%

Food 9%

Out of 2.5BN spent in the market so far, 971MM (39%) has gone into one of those three sectors

27

NEEDS

EXPERIENCES ©LIGHTBOX

28

NEEDS

EXPERIENCES ©LIGHTBOX

29

Financial services

©LIGHTBOX

30 ©LIGHTBOX

41% India is unbanked

31 ©LIGHTBOX

61% India unbanked in rural areas

32 ©LIGHTBOX

86% Under-banked (don’t have access to loans or formal sources of credit)

33 ©LIGHTBOX

34 ©LIGHTBOX

“Banks and financial institutions have not created products that serve younger generations in the most efficient way” –Max Levchin, co-founder of PayPal

35 ©LIGHTBOX

The new borrowing From: Credit card High interest rate Government papers Loan approval Access to banks

To: Micro-loan Small fee upfront Social networks Real-time approval Access to capital

©LIGHTBOX

36

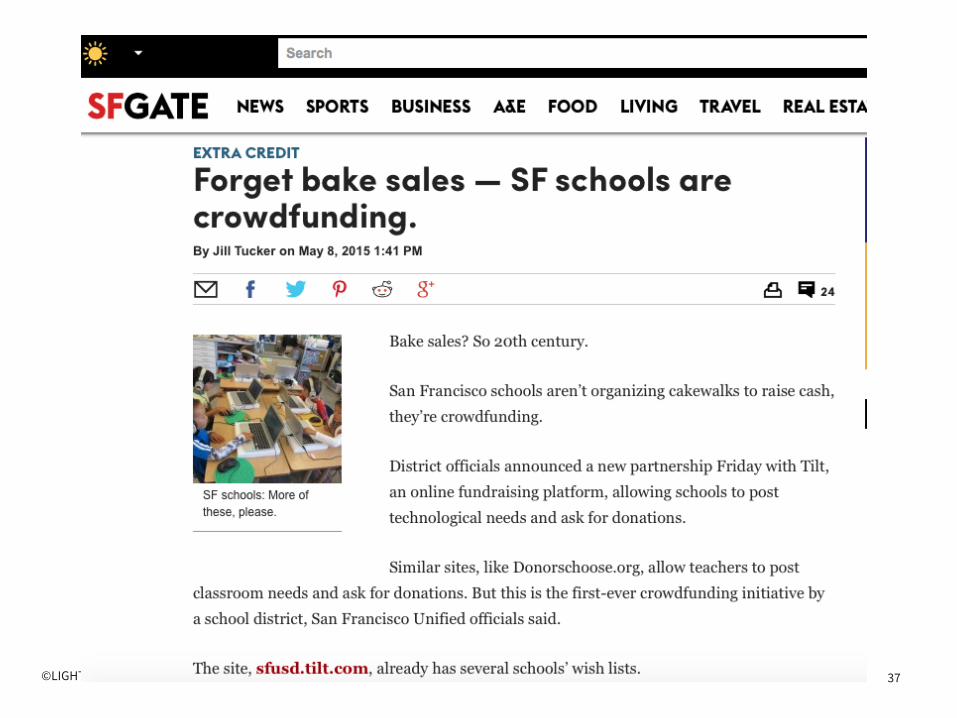

Crowd-funding is the new fundraising

©LIGHTBOX

37 ©LIGHTBOX

38

Re-thinking borrowing

©LIGHTBOX

39

Health

©LIGHTBOX

40 ©LIGHTBOX ©LIGHTBOX

41 ©LIGHTBOX

India: ratio of doctors to people

0.7doctors : 1000people

©LIGHTBOX

42 ©LIGHTBOX

The new healthy From: Treatment Doctor is god General

To: Prevention Informed patient Personalised

©LIGHTBOX

43

Education

©LIGHTBOX

44 ©LIGHTBOX

Failure is not a person, it is an event.

45 ©LIGHTBOX

The education eco-system setup

C+

46 ©LIGHTBOX

The education eco-system setup

C+

47 ©LIGHTBOX

For students to get all the blame

C+

48 ©LIGHTBOX

Failure is not a person, it is an event.

49

Data is inadequately used to prevent failure

©LIGHTBOX

50

Too little too late

©LIGHTBOX

©LIGHTBOX

©LIGHTBOX

Could this be a reality for mainstream education?

©LIGHTBOX

Data is inadequately used to prevent failure

©LIGHTBOX

©LIGHTBOX

©LIGHTBOX

©LIGHTBOX

Brands

©LIGHTBOX

59

17 October, 2014

©LIGHTBOX

Power has shifted from companies to consumers

and expectations have never been higher. Bad product reviews

trump clever marketing. Great products win

©LIGHTBOX