looking beyond the numbers review of banks' 2011 annual reports

TRANSCRIPT

Looking beyond the numbersReview of banks’ 2011 annual reports

Contents

Nature of review and executive summary 1

Sovereign debt risk 4

Liquidity and funding 15

Loan impairment 30

Financial instrument valuation 38

Regulatory capital disclosures 45

Risk disclosures 54

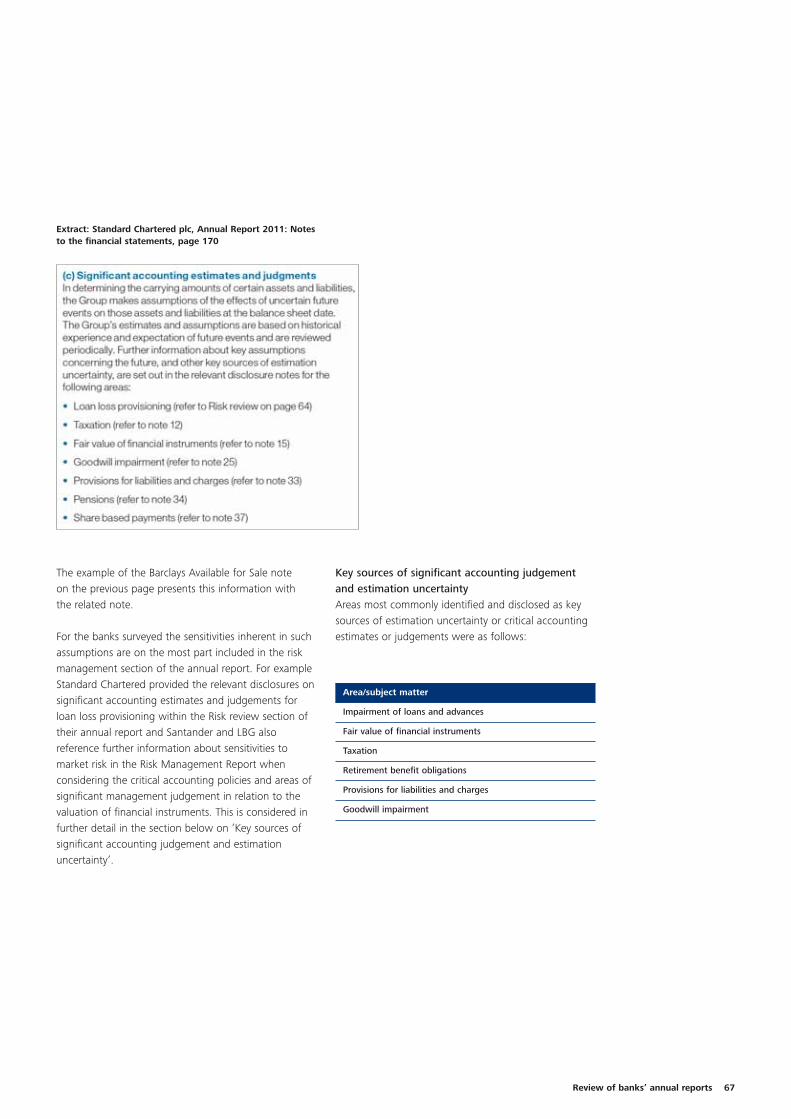

Critical accounting policies and key sources of estimation uncertainty 64

Other disclosure focus areas 76

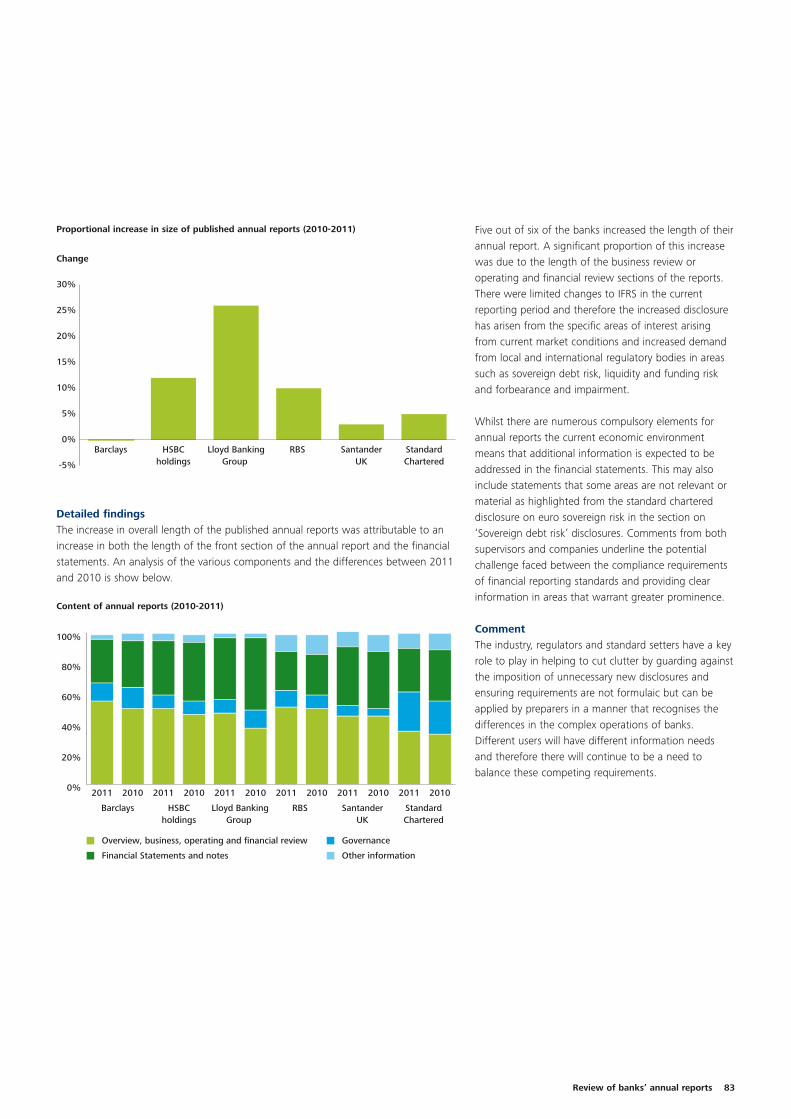

Length of annual reports 82

Glossary 84

Contacts 85

Review of banks’ annual reports 1

BackgroundThere has been an unprecedented level of interest inbanks’ financial statements during the last few years.Debate has taken place at G20 meetings and inparliamentary enquiries and stories about banks,including their reported performance, feature dailyin our newspapers. The new Interim Financial PolicyCommittee (FPC) and the Financial Services Authority(FSA) are taking an active interest in informationreported by banks. Given this scrutiny, it is timely totake a step back and evaluate the UK banks’ mostrecent annual reports. The key objective of this review isto provide insights and information on various aspectsof UK banks’ financial and non-financial reporting fromtheir 2011 annual reports. Our review focuses on thesix main UK listed banks: Barclays plc (Barclays), HSBCHoldings plc (HSBC), Lloyds Banking Group plc (LBG),the Royal Bank of Scotland Group plc (RBS), SantanderUK plc (Santander) and Standard Chartered plc(Standard Chartered). We highlight some of the newdisclosures and areas where there is likely to be morechange in the future.

The UK’s major banks have recognised the importanceof making their annual reports clear and concise tosatisfy the needs of different users including shareholders,regulators and analysts. There has been a concertedeffort to improve the disclosures provided in annualreports with continued dialogue between the banksand the UK regulators.

As the financial crisis has segued into a sovereign debtcrisis attention needs to be paid to developingdisclosures that enable the market to understand theissues and risks faced by banks. As far as possible thesedisclosures need to enable readers to draw comparisonsbetween the banks. Shareholders’ and otherstakeholders’ interests change rapidly and it is vital thatthese disclosures evolve in response to the economicenvironment.

Reporting initiativesThere were a number of international and UK initiativesto improve the level and consistency of disclosuresduring the 2011 reporting season. These included thefollowing:

• In March 2011 the Financial Stability Board (FSB)published its thematic review of 2009 financialstatements. A number of the themes emerging fromthat review are recognised in enhanced disclosures in2011 annual reports.

• In December 2011, the Basel Committee on BankingSupervision published proposed disclosure requirementsaiming to improve the transparency and comparabilityof a bank’s capital base.

• The European Securities and Market Authority (ESMA)issued two Public Statements in July 2011 andNovember 2011 on the need for increasedtransparency in relation to issuers’ exposure tosovereign debt1.

• Throughout 2011, the FSA outlined significant areas forfurther disclosure such as sovereign debt and countryexposures, liquidity and funding risk and impairmentjudgements particularly the significance of forbearanceactivities as highlighted in its October 2011 publication:‘Forbearance and Impairment Provisions’.

• During 2011 and the first half of 2012, the UK’sFinancial Reporting Council (FRC) issued furtherconsultations and reports on disclosures included infinancial reports and also reminded directors of theirfinancial reporting responsibilities. This work included:

– A report titled ‘Cutting Clutter: Combating Clutter inAnnual Reports’ (April 2011);

– ‘An Update for Directors of Listed Companies:Responding to Increased Country and Currency Riskin Financial Reports’. The Update aimed to drawtogether some of the significant issues directorsneeded to reflect on when considering how best toprovide a balanced and understandable assessment ofa company’s position and prospects in the context ofincreased country and currency risk (January 2012).

– The final report arising from the Sharman Inquiry2011 Going Concern and Liquidity Risks: Lessonsfor Companies and Auditors (The Sharman Inquiry)(June 2012). The draft report was published during2011 with one of the aims to recommend measuresto improve the existing reporting regime in relationto going concern and liquidity risks.

Nature of review and executive summary

1 Further, In July 2012 ESMAissued a report on aReview of GreekGovernment Bondsaccounting practices in theIFRS Financial Statementsfor the year ended 31 December 2011.

2

• In January 2012, the US Securities and ExchangeCommission’s (SEC’s) Division of Corporation Financealso issued ‘Disclosure Guidance Topic No. 4European Sovereign Debt Exposures’. The guidanceset out the information the SEC expected registrantsto provide on sovereign debt exposures.

2011 disclosure themesA number of the disclosure recommendations from thepublications and initiatives noted above outlined thesignificant areas where more extensive disclosure detailsshould be provided. Some of these key areas were:

• Sovereign debt and country exposures;

• Liquidity and funding risk including encumbrance;

• Impairment judgements and the significance offorbearance activities;

• Valuation methodologies and the information onvaluation adjustments and other judgement areas;

• Enhanced disclosures in relation to credit riskincluding the quality of collateral;

• Regulatory versus accounting disclosures; and

• Comparability generally.

In the UK the British Bankers’ Authority (BBA)responded to a number of these initiatives through theBBA Disclosure Working Party. A summary of the 2011recommendations of the BBA Disclosure Party werepublished in The BBA’s Financial Reporting Newsletter(December 2011). This included:

• Eurozone exposures; it was proposed that banksprovide disclosure of Eurozone sovereign debt andcountry exposures consistent with the disclosuresprovided in the 2011 interim result announcements;

• Enhanced disclosures on forbearance and impairmentin response to the FSA paper in October 2011;

• A reconciliation of statutory equity as presentedunder International Financial Reporting Standards(IFRSs) to regulatory capital as defined by the FSA;

• Where material, separate disclosures on Paymentprotection insurance (PPI) provisions;

• For deferred tax assets banks should providedisclosure where relevant on key judgements forrecognising deferred tax assets; and

• Separate disclosure on the Bank levy as at31 December 2011 where material.

At the time of their report, the BBA were stillformulating their response to the Sharman Inquiryhowever a number of the UK banks have providedadditional disclosure on liquidity and funding in their2011 annual reports.

Key findingsBanks’ annual reports have evolved over the last fewyears in an effort to provide all stakeholders with theinformation they demand. Change has also been drivenby demands from regulators for enhanced and moreclearly comparable disclosures on current focus areas.Consequently disclosures have extended beyond thatmandated by accounting standards.

In particular, further detail has been provided in relationto the current market focus areas including moreextensive risk disclosures particularly funding and liquidityrisk, specific reporting on exposures to sovereign risk, andenhanced detail on loans subject to forbearance.

Given that some of the regulatory guidance andinitiatives are new in 2011 there is some divergence inthe information included in annual reports e.g. the levelof detail on liquidity and funding and the amount ofqualitative versus quantitative information in valuationdisclosures. We expect that reporting will continue todevelop and become more standardised as banks reacha consensus on best practice reporting.

Standardisation in certain areas may be appropriate; butwhat appears to be most beneficial is for managementto explain in a clear and coherent what mattersincluding the principal risks, the extent of exposures andhow these are managed. It is important that disclosuresevolve over time in response to the areas that warrantgreater prominence from period to period.

Whilst the length of some of the annual reports by UKbanks has grown to comply with the additionalexpectation on disclosures there has been an attemptto ‘reduce the clutter’ by aggregating key disclosures.

Review of banks’ annual reports 3

In May 2012 the FSB announced the establishment ofan Enhanced Disclosure Task Force (EDTF). The primaryobjectives of the EDTF are to (i) to develop principles forenhanced disclosures, based on current marketconditions and risks, including ways to enhance thecomparability of disclosures, and (ii) to identify leadingpractice risk disclosures presented in annual reports for2011 year ends. On balance, the UK banks surveyedhave and are continuing to make great efforts to meetthis challenge. It is clear that annual reports of bankshave improved over the recent past. Continueddialogue between investors, standard setters,regulators, auditors and the banks will remain vital toensure information is appropriate and useful.

The future: 2012 reportingIn addition to the FSB EDTF there are other proposalsand projects to improve the financial reportingdisclosures of banks such as Basel consultations onimproved disclosures and continued dialogue betweenthe industry and local and international regulators.

In 2012, we expect certain themes to continue to beof importance with the push for further granularityin these areas in addition to focus in new areas.This includes the following:

• Further assessment of country risk reporting.

• Improved consistency on liquidity and fundingreporting including, more detail on encumberedassets; the quality of assets included in liquidity pools,and the potential requirement to report certain Baselregulatory measures such as the Liquidity CoverageRatio (LCR) and the Net Stable Funding Ratio (NSFR).

• Additional detail on forbearance specifically corporateforbearance.

• Enhanced disclosures on credit risk particularlycollateral and collateral valuation.

• Valuation disclosures, notably to assist with thecomparability of understanding valuation adjustments.

• The basis for determining key provisions including keyjudgements and sensitivities e.g. PPI.

• The reporting of non statutory measures and howthese reconcile to the statutory informationpresented.

• The reporting of intra period movements so risks areunderstood in the context of highs, lows andaverages over a reporting period.

Banks will need to continue to develop a disclosureframework that presents clear and coherent informationin their annual report that is responsive to the changingeconomic environment and the expectations ofshareholders and other stakeholders. Part of thechallenge will be to continue to present the specificcircumstances and risks faced by individual banks but ina manner that enables comparability between them.

Mike LloydEditor

4

BackgroundThe current crisis in Eurozone countries has increasedmarket interest in disclosures of banks’ exposures tosovereign debt. In the current environment detailed andconsistent disclosures in this area are important tounderstanding the financial position and performanceof financial institutions.

There are existing requirements in UK Companies Actfor the disclosure of the principal risks and uncertaintiesin the annual report. In addition to this are IFRSmandated disclosures for financial instruments in IFRS 7Financial Instruments: Disclosures (IFRS 7). However,given the systemic importance of banks and thedeterioration in the economic environment of certainEurozone countries, additional guidance for disclosureson this topic has emanated from various sourcesincluding the following:

• The ESMA issued two Public Statements in July 2011and November 2011 stressing the importance ofconsistent application of recognition and measurementprinciples in IFRSs and the need for enhancedtransparency in relation to issuers’ exposure tosovereign debt. In July 2012 ESMA has published afurther report on its review of the accounting anddisclosure of Greek government bonds and othersovereign debt in 2011 financial statements.

• In their note on year end hot accounting anddisclosure issues (December 2011), the FSA, whilstnoting that improvements had been made in 2011interim statements, believed there could be improveddisclosures for 2011 annual reports. The areas ofcomparability, credit default swaps (CDS) and otherinstruments where the maximum exposure may notbe reflected in the balance sheet carrying value andindirect exposures were issues it focused on.

• In January 2012 the FRC published ‘An Update forDirectors of Listed Companies: Responding toIncreased Country and Currency Risk in FinancialReports’. The Update aimed to draw together someof the significant issues directors needed to reflect onwhen considering how best to provide a balancedand understandable assessment of a company’sposition and prospects in the context of increasedcountry and currency risk. This was subsequentlyupdated in June 2012.

• In January 2012 the SEC’s Division of CorporationFinance issued ‘Disclosure Guidance Topic No. 4European Sovereign Debt Exposures’. The guidancesetout information the SEC expected registrants toprovide.

• The BBA Disclosure Working Party maderecommendations for 2011 annual reports inresponse to the FSA interim recommendations.

Overall commentsCountry and currency risks have seen significant changeover the last year. Transparent disclosures are criticalin helping investors and other users of the financialstatements to understand the financial position andperformance of entities that have material exposuresto sovereign debt. The information provided by the UKbanks has developed compared with the prior period.All of the banks surveyed included a specific section oncountry risk and specifically Eurozone risk where thiswas relevant to their business. The focus was on thefollowing areas, consistent with the themes identifiedby the regulatory bodies and the banks’ own responsethrough the BBA.

• risk management disclosures including an overallassessment by the directors’ of country and currencyrisk and the impact on a bank’s future prospects;

• the basis for the selection of the countries includedin more detailed disclosures;

• disclosure of direct exposures both funded andunfunded based on IAS 39 Financial Instrument:Recognition and Measurement (IAS 39) categories;

• the disclosure of the impact of credit defaultprotection and credit default exposures; and

• the level of indirect exposure.

Sovereign debt risk

Review of banks’ annual reports 5

Detailed findings

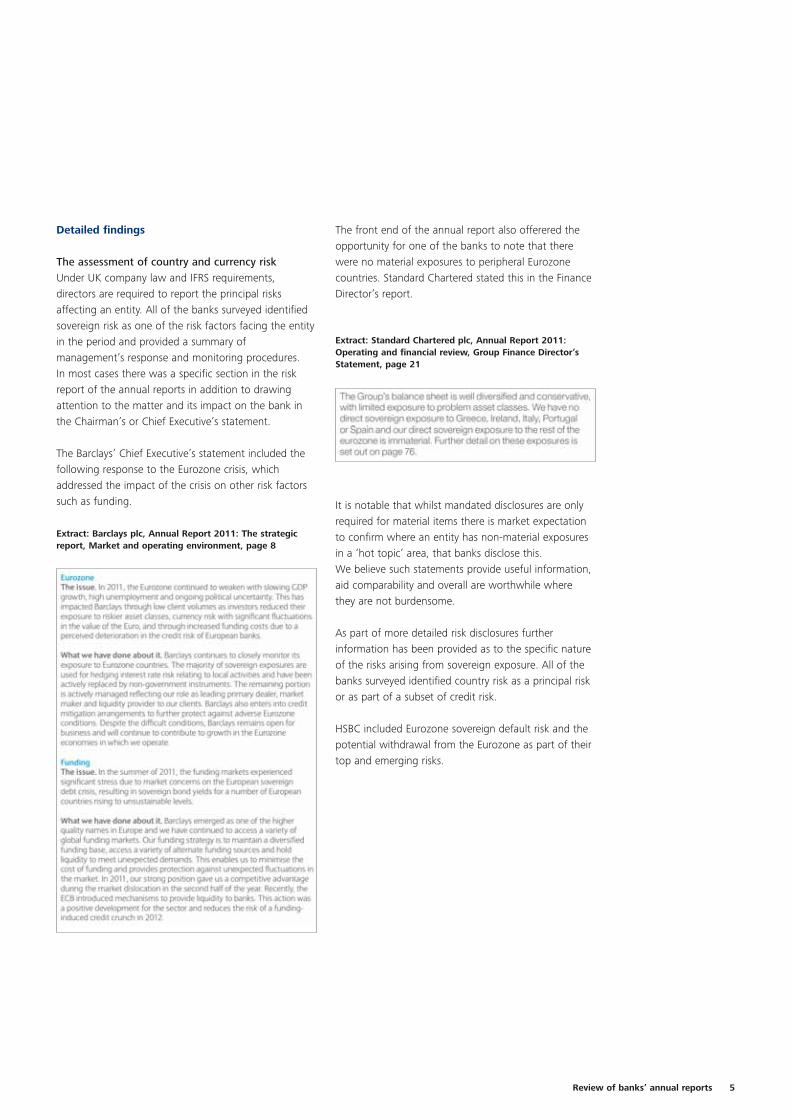

The assessment of country and currency riskUnder UK company law and IFRS requirements,directors are required to report the principal risksaffecting an entity. All of the banks surveyed identifiedsovereign risk as one of the risk factors facing the entityin the period and provided a summary ofmanagement’s response and monitoring procedures.In most cases there was a specific section in the riskreport of the annual reports in addition to drawingattention to the matter and its impact on the bank inthe Chairman’s or Chief Executive’s statement.

The Barclays’ Chief Executive’s statement included thefollowing response to the Eurozone crisis, whichaddressed the impact of the crisis on other risk factorssuch as funding.

The front end of the annual report also offerered theopportunity for one of the banks to note that therewere no material exposures to peripheral Eurozonecountries. Standard Chartered stated this in the FinanceDirector’s report.

It is notable that whilst mandated disclosures are onlyrequired for material items there is market expectationto confirm where an entity has non-material exposuresin a ‘hot topic’ area, that banks disclose this.We believe such statements provide useful information,aid comparability and overall are worthwhile where they are not burdensome.

As part of more detailed risk disclosures furtherinformation has been provided as to the specific natureof the risks arising from sovereign exposure. All of thebanks surveyed identified country risk as a principal riskor as part of a subset of credit risk.

HSBC included Eurozone sovereign default risk and thepotential withdrawal from the Eurozone as part of theirtop and emerging risks.

Extract: Barclays plc, Annual Report 2011: The strategicreport, Market and operating environment, page 8

Extract: Standard Chartered plc, Annual Report 2011:Operating and financial review, Group Finance Director’sStatement, page 21

6

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Operating and Financial Review, Risk, page 99

Review of banks’ annual reports 7

Disclosures also covered the monitoring role of theAudit or Risk Committee in relation to sovereign riskand exposure, and other management responses.The majority of banks noted that these committees hadconsidered sovereign debt risk during the financial yearincluding the level of exposure, impact on funding, riskmitigation plans and stress testing. Barclays provided agood example of explaining what these considerationsinvolved.

LBG also disclosed specific mangement responses tomonitor Eurozone exposures.

Extract: Barclays plc, Annual Report 2011: CorporateGovernance Report, Board and Risk Committee Chairman’sReport, page 44

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Business review, Risk management, page 156

Extract: RBS Group, Annual Report and Accounts 2011:Business review, Risk and balance sheet management, page209

8

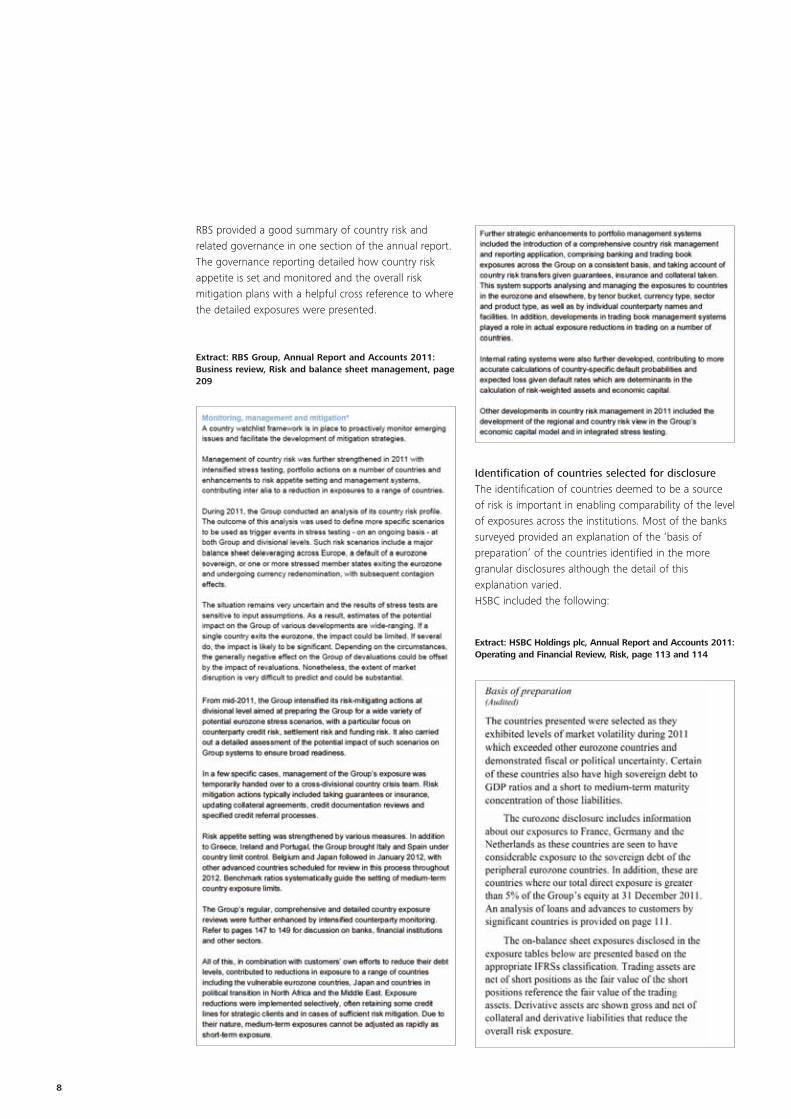

RBS provided a good summary of country risk andrelated governance in one section of the annual report.The governance reporting detailed how country riskappetite is set and monitored and the overall riskmitigation plans with a helpful cross reference to wherethe detailed exposures were presented.

Identification of countries selected for disclosureThe identification of countries deemed to be a sourceof risk is important in enabling comparability of the levelof exposures across the institutions. Most of the bankssurveyed provided an explanation of the ‘basis ofpreparation’ of the countries identified in the moregranular disclosures although the detail of thisexplanation varied.HSBC included the following:

Extract: HSBC Holdings plc, Annual Report and Accounts 2011:Operating and Financial Review, Risk, page 113 and 114

Review of banks’ annual reports 9

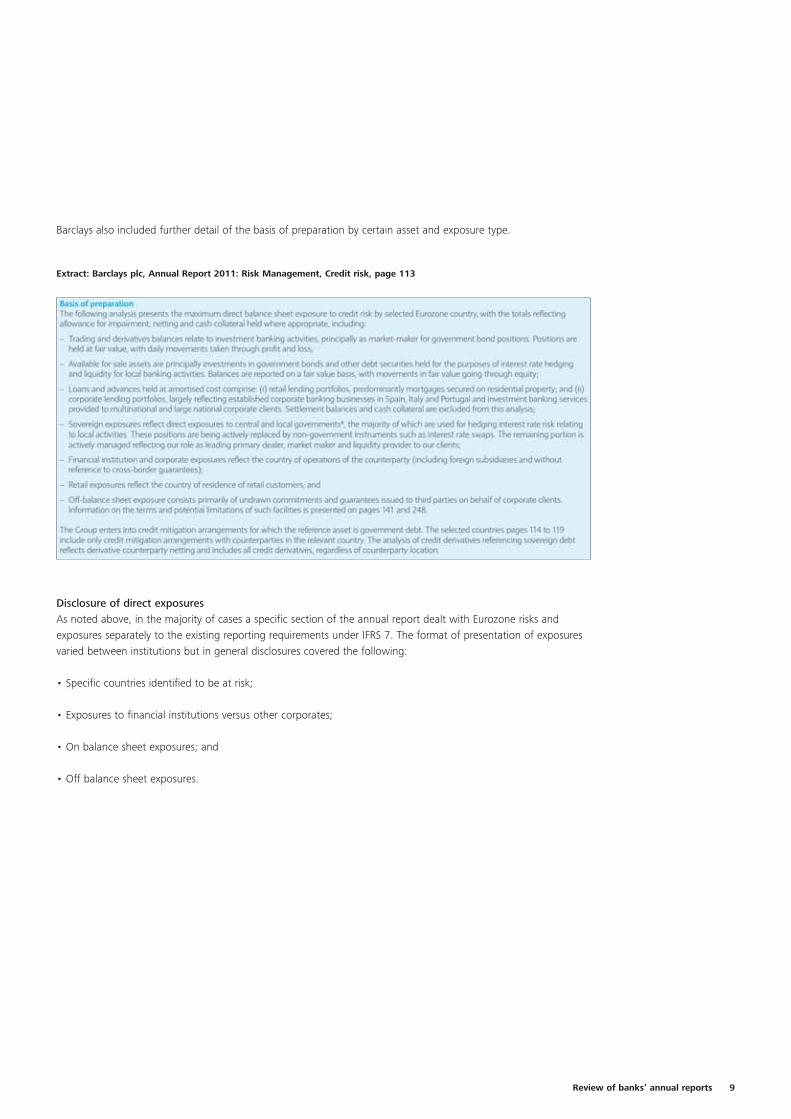

Barclays also included further detail of the basis of preparation by certain asset and exposure type.

Extract: Barclays plc, Annual Report 2011: Risk Management, Credit risk, page 113

Disclosure of direct exposuresAs noted above, in the majority of cases a specific section of the annual report dealt with Eurozone risks andexposures separately to the existing reporting requirements under IFRS 7. The format of presentation of exposuresvaried between institutions but in general disclosures covered the following:

• Specific countries identified to be at risk;

• Exposures to financial institutions versus other corporates;

• On balance sheet exposures; and

• Off balance sheet exposures.

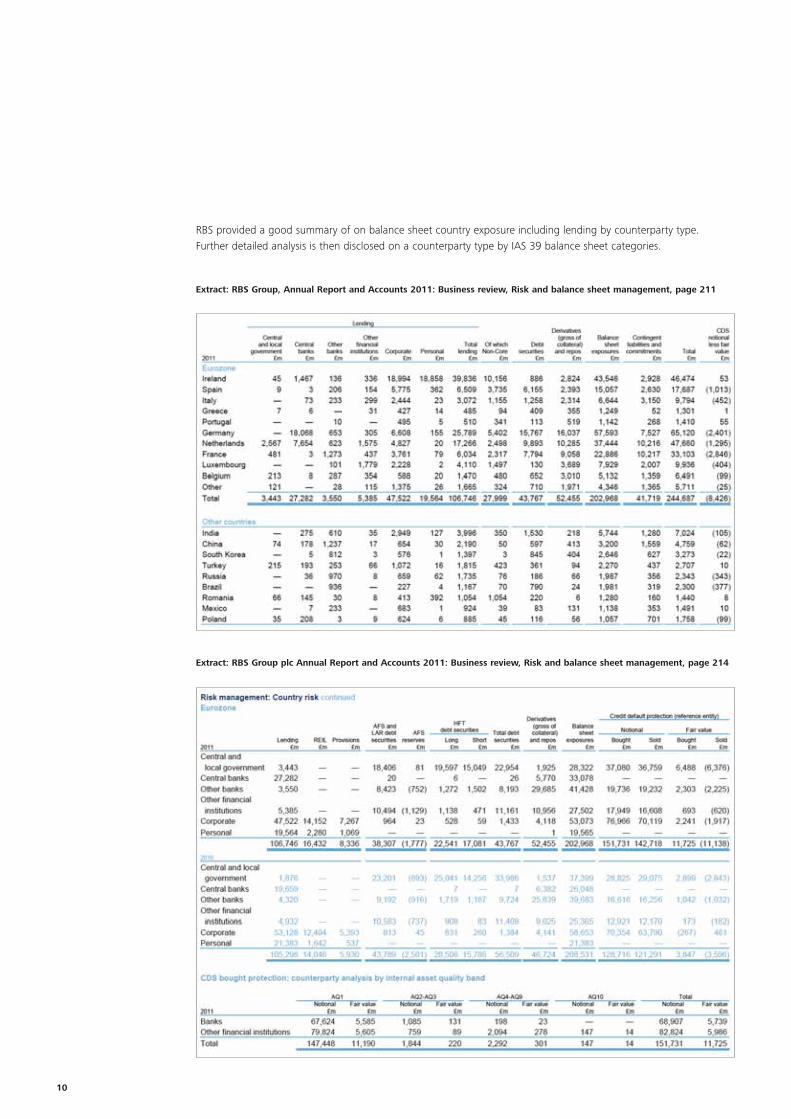

Extract: RBS Group plc Annual Report and Accounts 2011: Business review, Risk and balance sheet management, page 214

10

RBS provided a good summary of on balance sheet country exposure including lending by counterparty type.Further detailed analysis is then disclosed on a counterparty type by IAS 39 balance sheet categories.

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, page 211

Review of banks’ annual reports 11

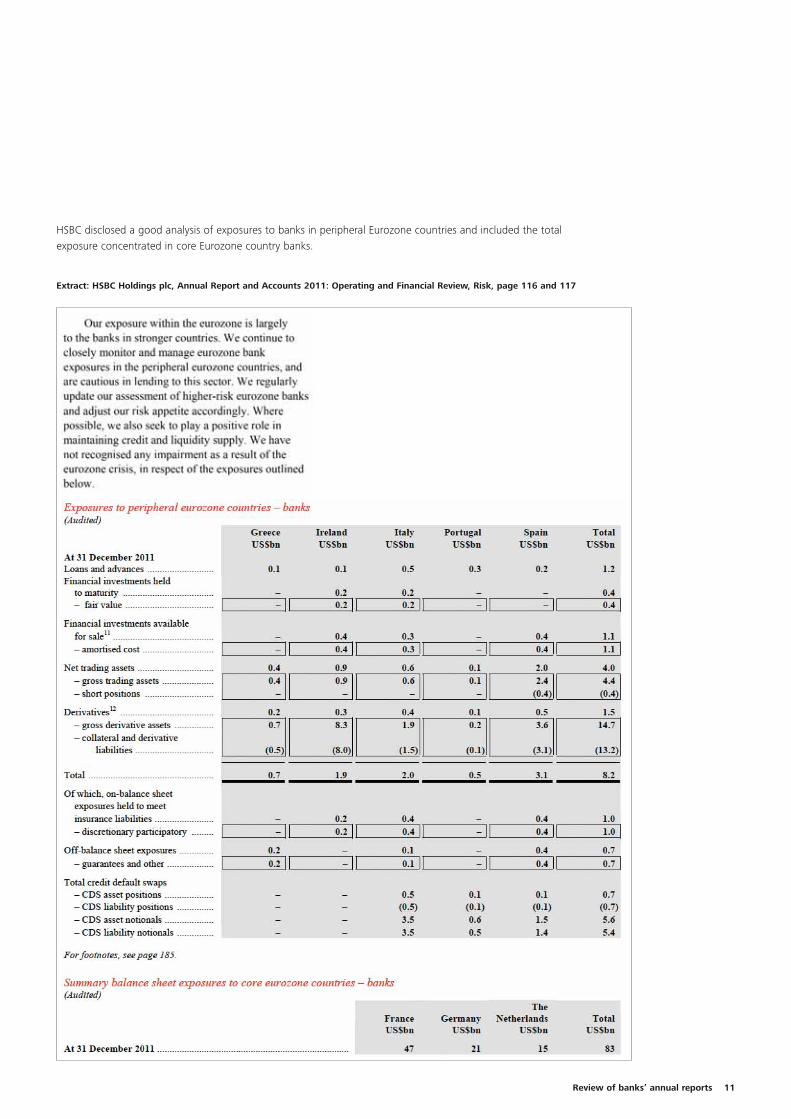

HSBC disclosed a good analysis of exposures to banks in peripheral Eurozone countries and included the totalexposure concentrated in core Eurozone country banks.

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Operating and Financial Review, Risk, page 116 and 117

12

Whilst a significant amount of the information provided by the banks is quantitative in nature there are somequalitative explanations. RBS extend their quantitative analysis on specific countries with additional commentaryexplaining the business areas in which the exposures arose and the key movements in the period, giving users of thefinancial statements a wider context in which to understand the risks.

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, pages 215and 216

Review of banks’ annual reports 13

The impact of credit default protection and credit derivative exposuresAs some of the examples above indicate, some of the banks included the impact of credit default protection andcredit derivative exposures with their main sovereign risk disclosures. The level of detail is different between each ofthe banks surveyed with the majority disclosing credit default protection bought and net credit derivative exposure.

Barclays disclose a more granular analysis in respect of selected Eurozone countries, including the gross fair valuesof exposures and the contractual notional amounts of bought and sold credit derivatives.

We expect 2012 will see further guidance by UK and international bodies to help promote more consistency inthis area.

Extract: Barclays plc , Annual Report 2011: Risk Management, Credit risk, page 120

14

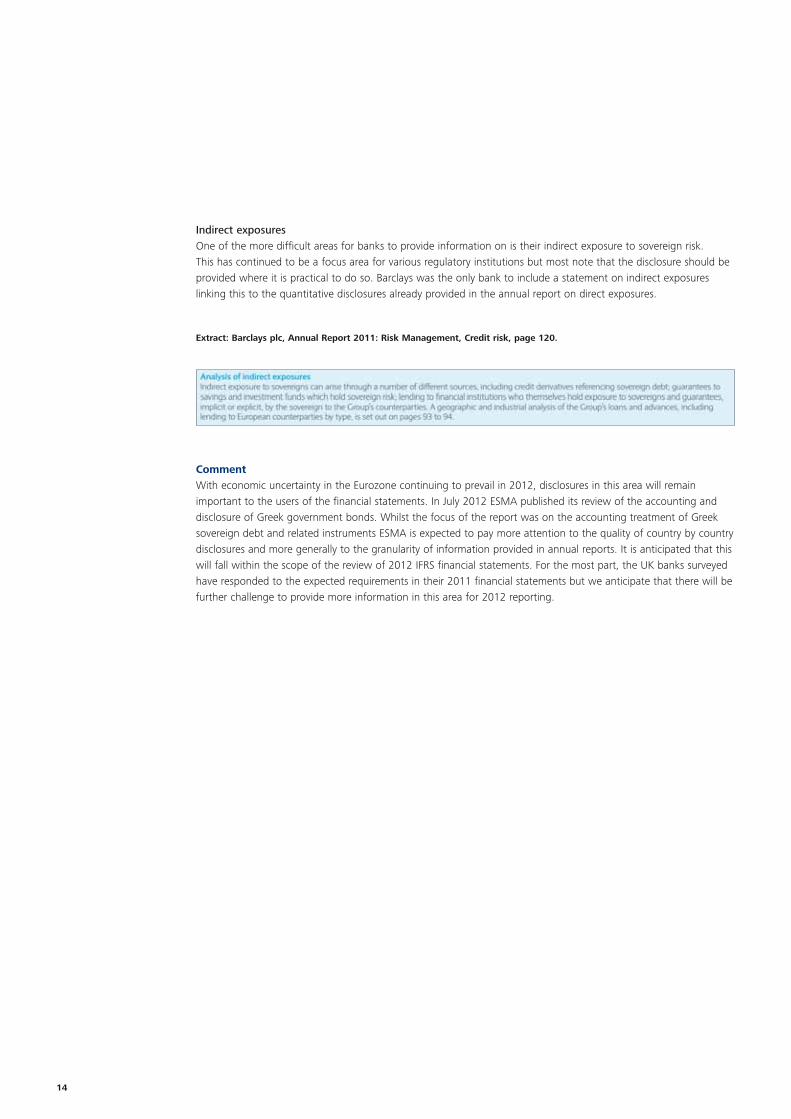

Indirect exposuresOne of the more difficult areas for banks to provide information on is their indirect exposure to sovereign risk.This has continued to be a focus area for various regulatory institutions but most note that the disclosure should beprovided where it is practical to do so. Barclays was the only bank to include a statement on indirect exposureslinking this to the quantitative disclosures already provided in the annual report on direct exposures.

CommentWith economic uncertainty in the Eurozone continuing to prevail in 2012, disclosures in this area will remainimportant to the users of the financial statements. In July 2012 ESMA published its review of the accounting anddisclosure of Greek government bonds. Whilst the focus of the report was on the accounting treatment of Greeksovereign debt and related instruments ESMA is expected to pay more attention to the quality of country by countrydisclosures and more generally to the granularity of information provided in annual reports. It is anticipated that thiswill fall within the scope of the review of 2012 IFRS financial statements. For the most part, the UK banks surveyedhave responded to the expected requirements in their 2011 financial statements but we anticipate that there will befurther challenge to provide more information in this area for 2012 reporting.

Extract: Barclays plc, Annual Report 2011: Risk Management, Credit risk, page 120.

Review of banks’ annual reports 15

BackgroundIn the past few months there has been a deteriorationof liquidity and funding in the Eurozone. Other factorsare also having an impact including the rules for banksin the Eurozone to meet higher capital requirements byJune 2012. The macroeconomic environment andchanging regulatory landscape has meant there hasbeen continued scrutiny on the transparency of banks’business models and the impact of the business strategyand risks on liquidity and funding. The focus on theliquidity and funding structures of banks due to theirsystemic importance to the financial system has resultedin increased disclosures on liquidity and funding in bankannual reports.

In the UK there has been specific guidance in this area:

• In June 2012 the FRC published the final report of theSharman Inquiry. One of the aims of the SharmanInquiry was to recommend measures to improve theexisting reporting regime and related guidance forcompanies and auditors in relation to going concernand liquidity risks. There was consideration as towhether banks were different necessitating a specificapproach for financial reporting. The conclusion wasthat a separate reporting regime was not required forbanks.

• The FSA also highlighted this as one of the key areasfor the 2011 year end reporting season with anexpectation that firms would use their best efforts toprovide disclosures that would help users tounderstand the structure and flexibility of theirfunding arrangements.

• The BBA have also conducted work streams toenhance the quality and consistency of disclosuresand this includes the disclosure of going concern andliquidity risk.

Overall commentsIn the UK the increased disclosure has been regulatorand market driven rather than mandated by accountingstandards and as such there is not currently astandardised approach across the banks surveyed as tohow the information is presented and the level of detailprovided. In general all the banks have covered thefollowing themes:

• A definition of liquidity and funding risk;

• An overview of liquidity and funding in the reportingperiod;

• The management of liquidity and funding risk;

• The sources and usage of funding;

• Liquidity and funding metrics;

• Disclosures on encumbered assets; and

• Linkage to going concern statements.

Detailed findings

Defining liquidity and funding riskThe banks surveyed provide a definition of liquidity risk.RBS included the following definition:

Liquidity and funding

Extract: RBS Group, Annual Report and Accounts 2011:Business review, Risk and balance sheet management,page 116

16

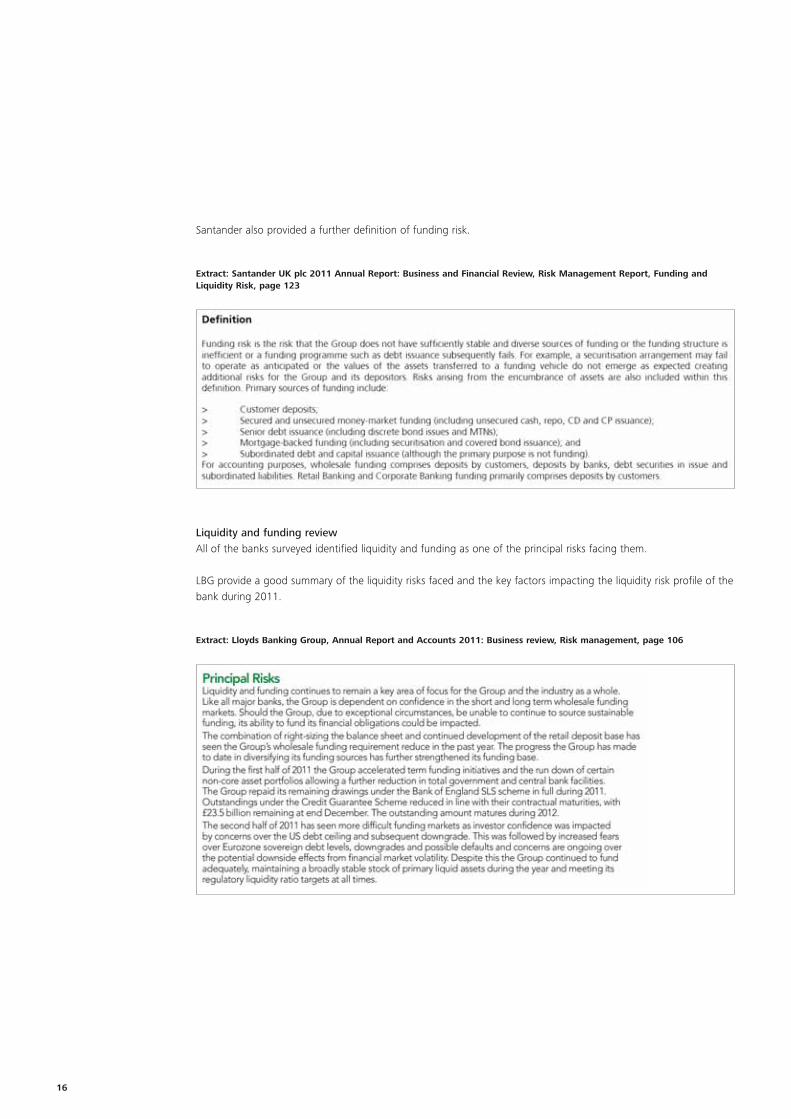

Santander also provided a further definition of funding risk.

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, Funding andLiquidity Risk, page 123

Liquidity and funding reviewAll of the banks surveyed identified liquidity and funding as one of the principal risks facing them.

LBG provide a good summary of the liquidity risks faced and the key factors impacting the liquidity risk profile of thebank during 2011.

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Business review, Risk management, page 106

Review of banks’ annual reports 17

The majority of banks also referred to recent fundingactivities and future funding arrangements in theChairman’s statement or Chief Executive’s report.Some banks also provided a qualitative assessment ofthe improvements in liquidity in this section of theannual report whilst others provided a more quantitativeanalysis, disclosing certain funding ratios as one of thekey metrics in the reporting of annual results.

Barclays commented on capital, liquidity and funding aspart of the Chief Executive’s Report.

Extract: Barclays plc, Annual Report 2011: The strategicreport, Chief Executive’s review, page 7

18

Santander included the following statement in the Chief Executive’s review:

Extract: Santander UK plc 2011 Annual Report: Chief Executive Officer’s Review, pages 3 to 4

The management of liquidity and funding risksThere has been an increased analysis of the key risks facing banks and how these are managed by the institutions.All of the banks disclosed how liquidity and funding risks are managed. A good example was Barclays whichincluded an overview of how the risk is managed within the overall bank’s governance structure.

Review of banks’ annual reports 19

Extract: Barclays plc, Annual Report 2011: Risk management, Funding risk with liquidity , page 139 to 140

20

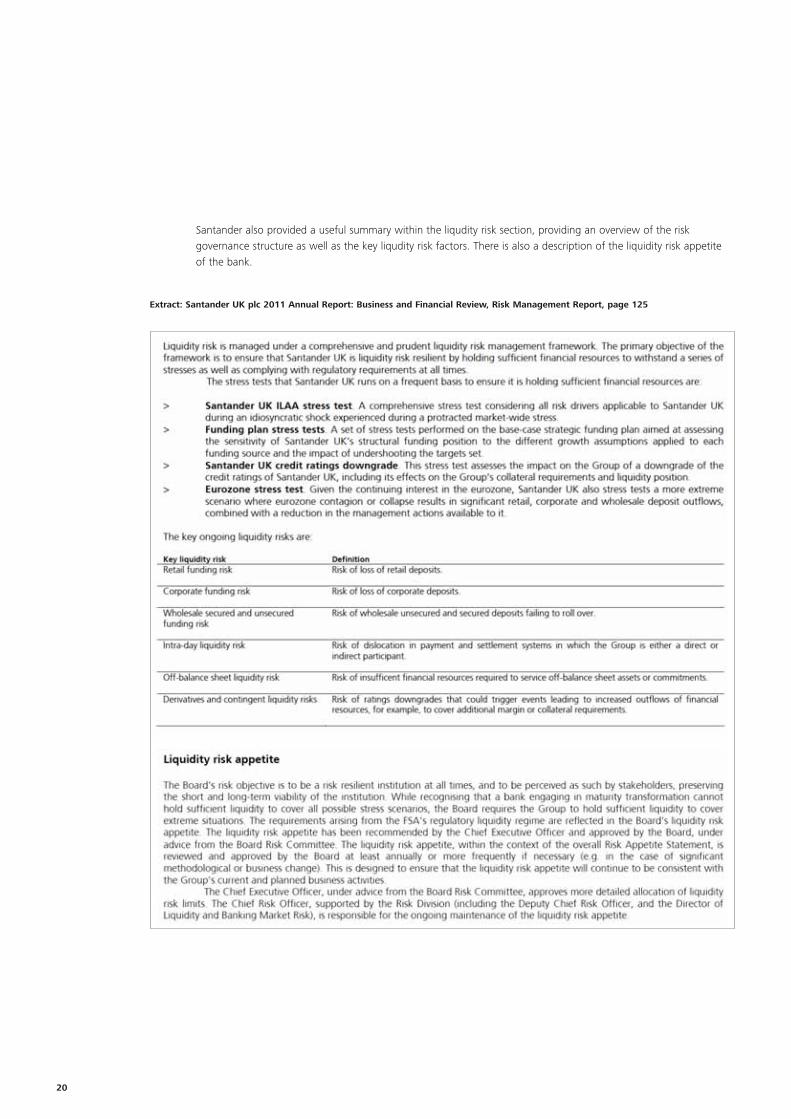

Santander also provided a useful summary within the liqudity risk section, providing an overview of the riskgovernance structure as well as the key liqudity risk factors. There is also a description of the liquidity risk appetiteof the bank.

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, page 125

Review of banks’ annual reports 21

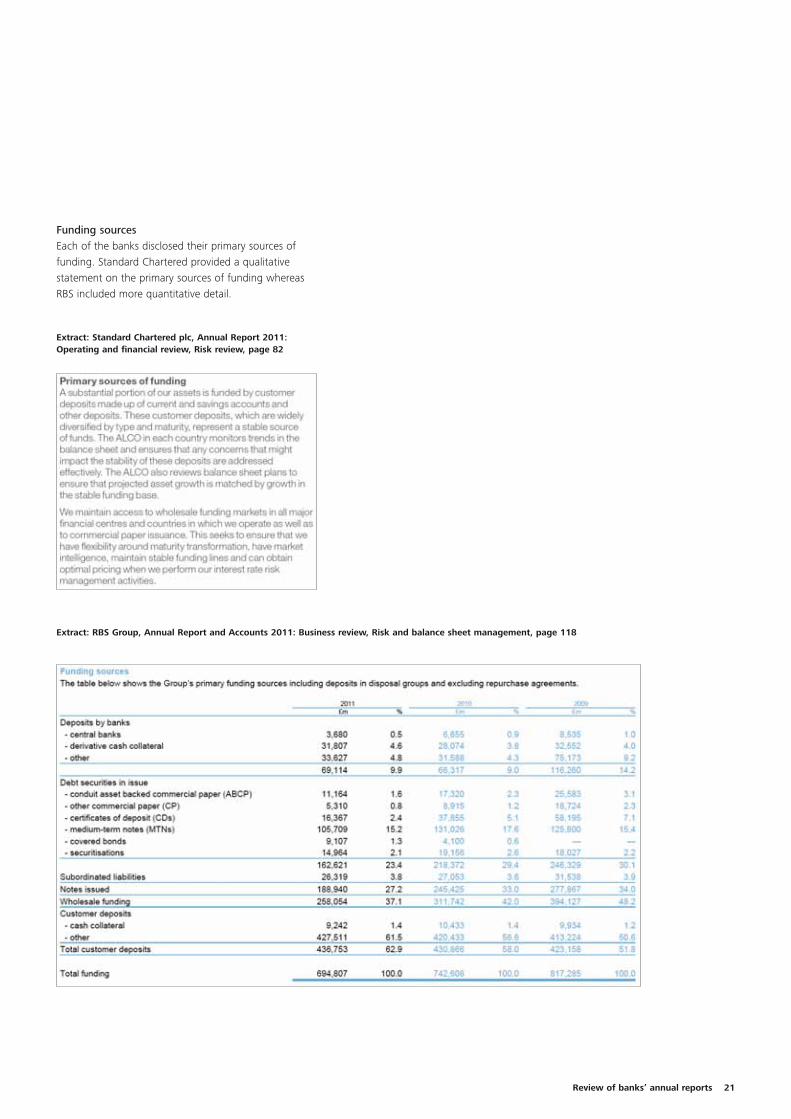

Funding sourcesEach of the banks disclosed their primary sources offunding. Standard Chartered provided a qualitativestatement on the primary sources of funding whereasRBS included more quantitative detail.

Extract: Standard Chartered plc, Annual Report 2011:Operating and financial review, Risk review, page 82

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, page 118

22

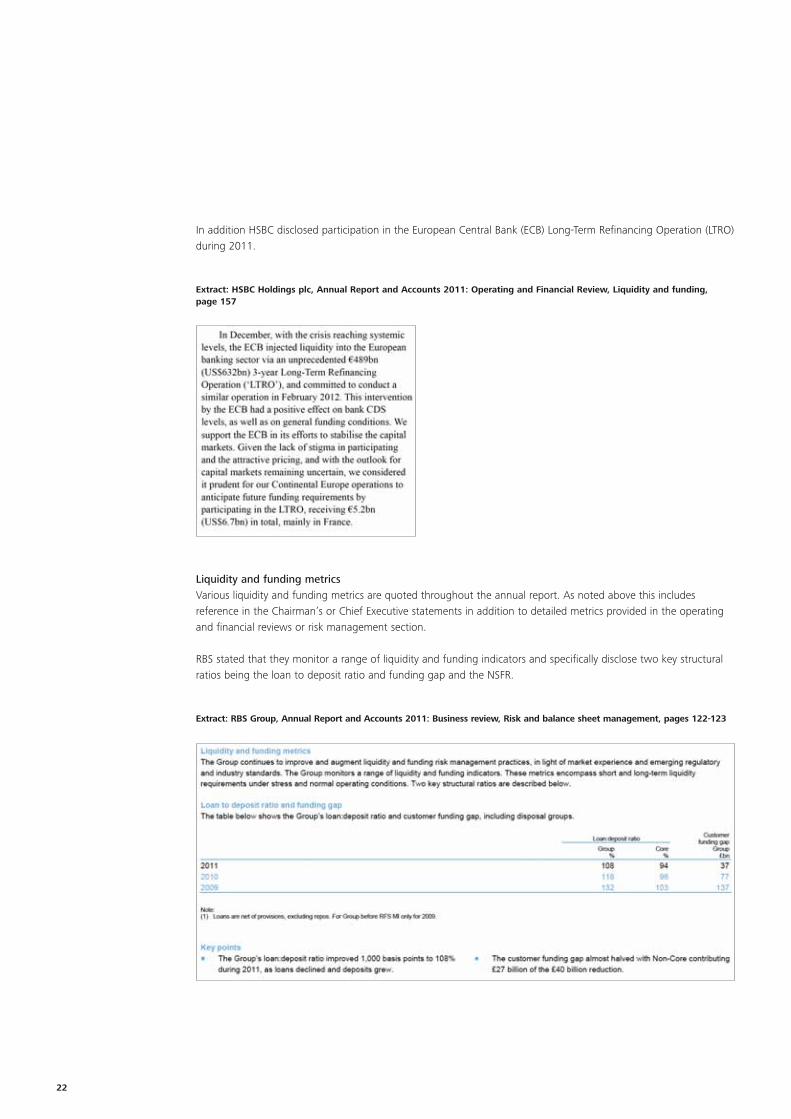

In addition HSBC disclosed participation in the European Central Bank (ECB) Long-Term Refinancing Operation (LTRO)during 2011.

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Operating and Financial Review, Liquidity and funding,page 157

Liquidity and funding metricsVarious liquidity and funding metrics are quoted throughout the annual report. As noted above this includesreference in the Chairman’s or Chief Executive statements in addition to detailed metrics provided in the operatingand financial reviews or risk management section.

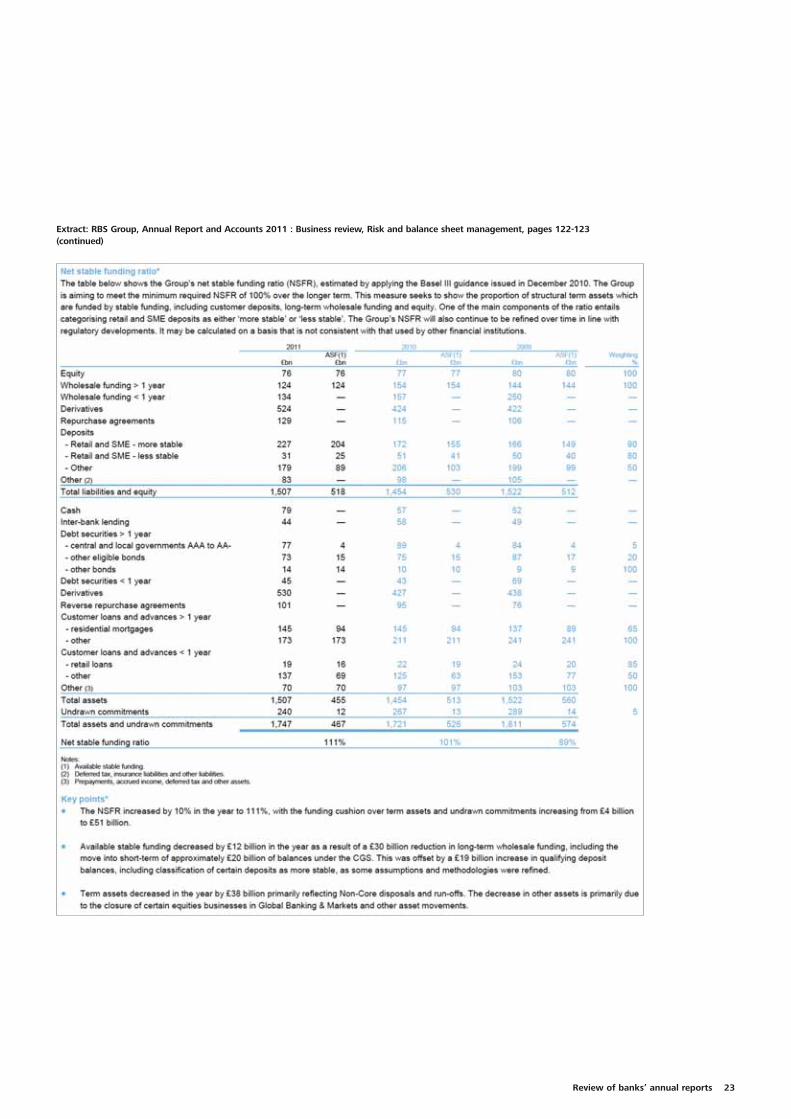

RBS stated that they monitor a range of liquidity and funding indicators and specifically disclose two key structuralratios being the loan to deposit ratio and funding gap and the NSFR.

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, pages 122-123

Review of banks’ annual reports 23

Extract: RBS Group, Annual Report and Accounts 2011 : Business review, Risk and balance sheet management, pages 122-123(continued)

24

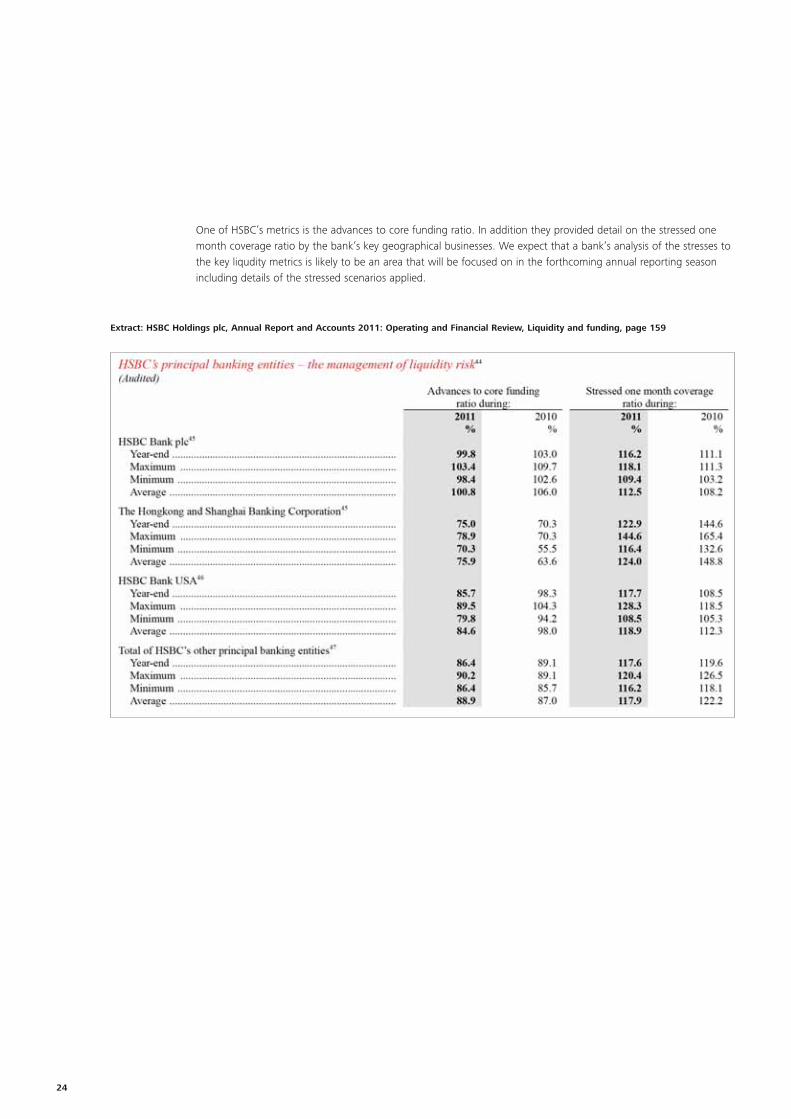

One of HSBC’s metrics is the advances to core funding ratio. In addition they provided detail on the stressed onemonth coverage ratio by the bank’s key geographical businesses. We expect that a bank’s analysis of the stresses tothe key liqudity metrics is likely to be an area that will be focused on in the forthcoming annual reporting seasonincluding details of the stressed scenarios applied.

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Operating and Financial Review, Liquidity and funding, page 159

Review of banks’ annual reports 25

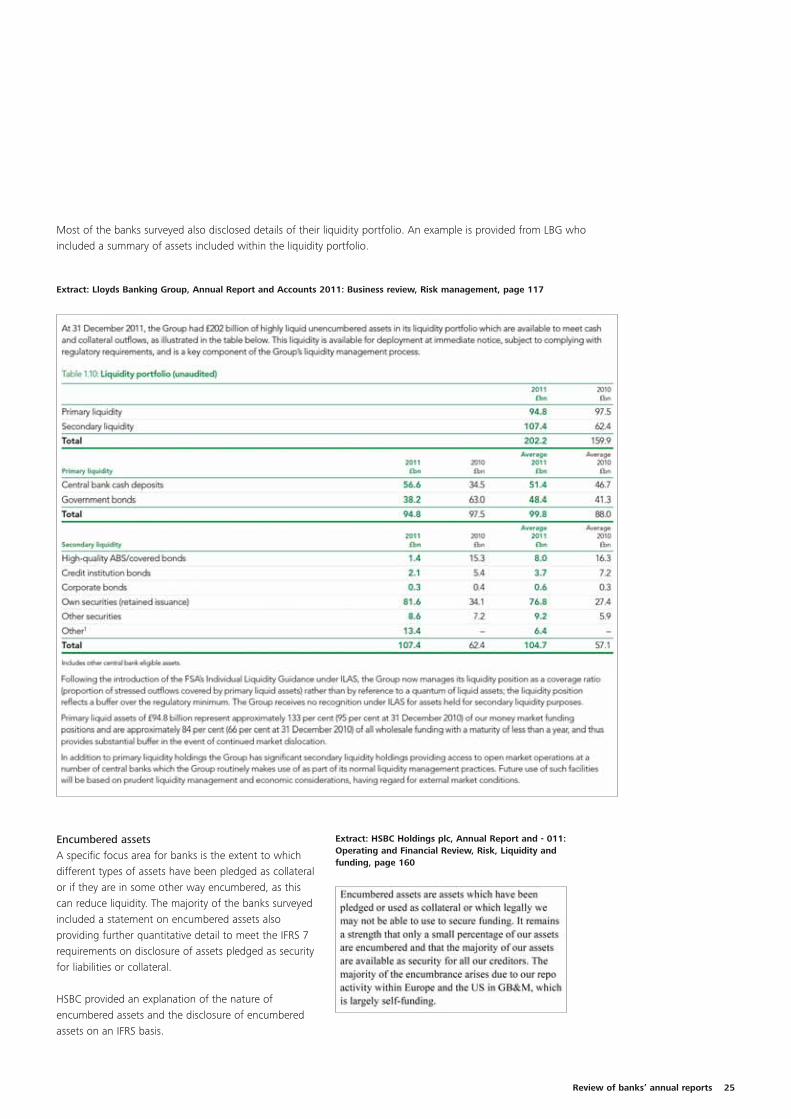

Most of the banks surveyed also disclosed details of their liquidity portfolio. An example is provided from LBG whoincluded a summary of assets included within the liquidity portfolio.

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Business review, Risk management, page 117

Encumbered assetsA specific focus area for banks is the extent to whichdifferent types of assets have been pledged as collateralor if they are in some other way encumbered, as thiscan reduce liquidity. The majority of the banks surveyedincluded a statement on encumbered assets alsoproviding further quantitative detail to meet the IFRS 7requirements on disclosure of assets pledged as securityfor liabilities or collateral.

HSBC provided an explanation of the nature ofencumbered assets and the disclosure of encumberedassets on an IFRS basis.

Extract: HSBC Holdings plc, Annual Report and - 011:Operating and Financial Review, Risk, Liquidity andfunding, page 160

26

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Financial Statements, Notes on the Financial Statements,page 392

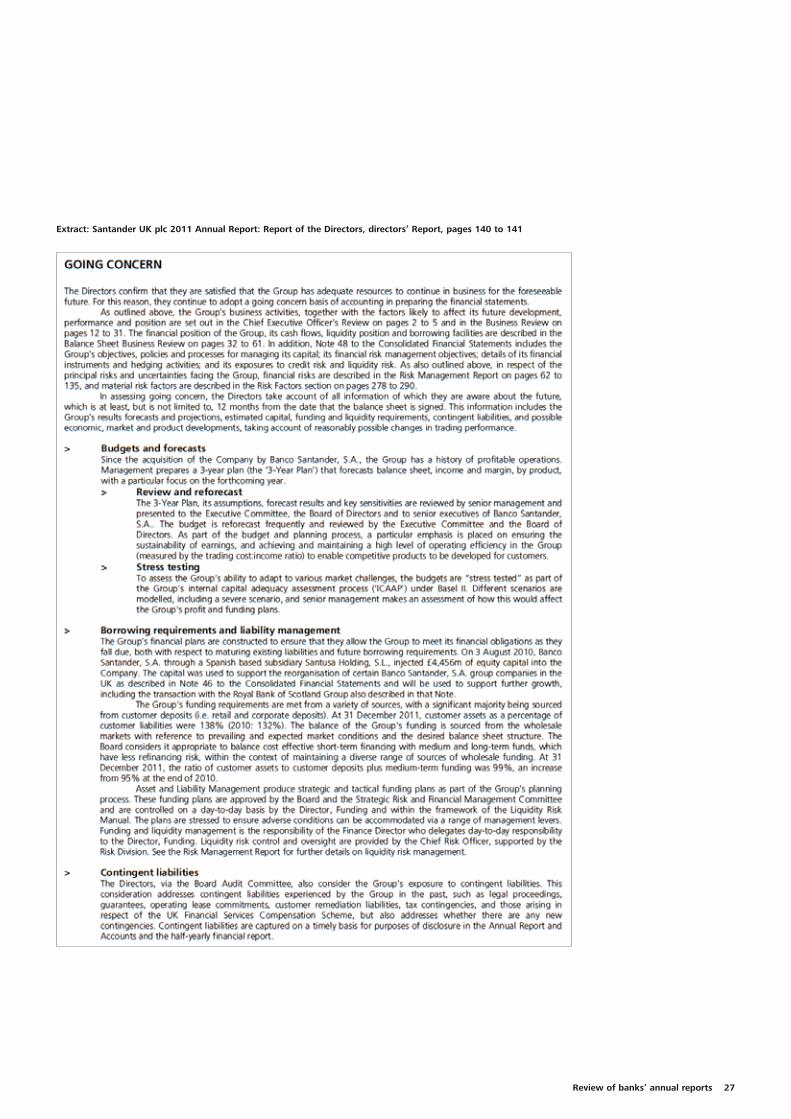

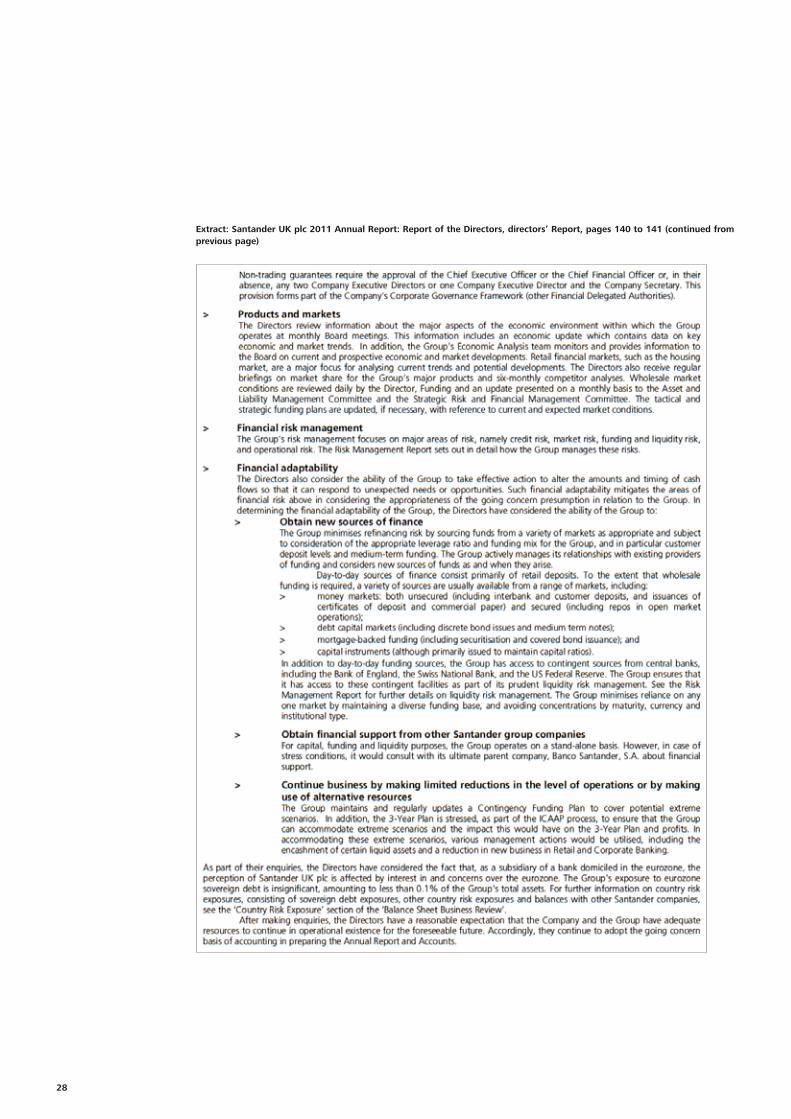

Link to going concern disclosuresThe Sharman Inquiry report focuses on the linkages of the risks to the company’s going concern status and how thisis integrated within the directors’ business planning and risk management processes. Liquidity and funding is a keyarea in this respect. In the 2011 reporting season, the majority of the banks surveyed referred to a review of liquidityand funding as part of the going concern assessment in their specific going concern statements with cross referenceto where the detailed disclosure was provided in the annual report. Santander provided a good summary of theconsiderations applied in assessing going concern within their directors’ statement on going concern.

Review of banks’ annual reports 27

Extract: Santander UK plc 2011 Annual Report: Report of the Directors, directors’ R eport, pages 140 to 141

28

Extract: Santander UK plc 2011 Annual Report: Report of the Directors, directors’ R eport, pages 140 to 141 (continued fromprevious page)

Review of banks’ annual reports 29

The increased disclosure on liquidity and funding in2011 annual reports suggests that there has beenconsideration of the additional level of informationanticipated from the final recommendations of theSharman Inquiry. Standard Chartered specifically refer tothe fact that their Audit Committee presented aresponse to the Sharman Inquiry.

CommentThe systemic importance of banks means that liquidityand funding disclosures will be a continued area offocus for the users of financial statements. The finalSharman Inquiry highlighted that a separate reportingregime was not required for banks however we expectthe disclosures in this area to evolve over the nextfinancial reporting period as institutions respond to thefinal report recommendations and with increasingrequirements expressed by regulators. The FSB’s EDT isalso considering liquidity and funding disclosures, and islikely to make recommendations in a report expectedtowards the end of 2012.

30

BackgroundThe past five years have seen an unprecedented levelof interest in the loan impairment charges banksdisclose and also in how these amounts are calculated.Whilst 2011 loan impairment charges have generallyfallen from their 2010 levels, they continue to have asignificant impact on banks’ profitability and henceattract attention.

We have focused our review of impairment disclosuresto those relating to loan forbearance, where newguidance on provisioning methodologies and disclosureand the results of reviews by regulators have beenissued during 2011. The key publications were:

• the FSA’s Guidance entitled: Forbearance andImpairment Provisions – Mortgages issued in October2011.

• the Bank of England’s FPC’s December 2011 Issue 30 Financial Stability Report. This includes the resultsof a review by the FSA on forbearance relating toother consumer debt and commercial real estate.

Some of the principal regulatory concerns expressed inthese publications were:

• Loan impairment methodologies may not be effectivelycapturing the impacts of forbearance, reducing theaccuracy of lender performance reporting.

• Forbearance may not always be employed in the bestinterests of the customer as it could lead to the loanmoving permanently onto non-sustainable terms andincrease customer losses.

• Forbearance related disclosures may not besufficiently granular for the users of the accounts todetermine the true impact of these strategies.

The FSA stated that forbearance disclosures should bemade under the auspices of IFRS 7, where forbearanceis material. They also encouraged careful considerationof the type and levels of forbearance used by firms andalso of firms’ policies for managing credit risk in thiscontext.

A further area of concern in 2011 was the level ofimpairment on commercial real estate (‘CRE’) assets andtherefore we have considered these disclosures in ourreview.

Overall commentsAs a result of the regulatory initiatives there issignificantly more information provided by the UK bankson forbearance disclosures and the impact onprovisioning in the 2011 annual reports. The detailprovided is broadly consistent with the areas identifiedin the regulatory releases and covered the following:

• defining forbearance activities in the glossaries;

• including forbearance within the key accountingpolicies;

• separating retail and corporate forbearancedisclosures;

• identifying the impact on provisioning betweenprovisions on loans subject to forbearance versus therest of the loan portfolios; and

• specific disclosures on CRE portfolios.

Detailed findings

Definition of forbearanceThe FSA have defined forbearance as occurring “whena bank, for reasons relating to the actual or apparentfinancial stress of a borrower grants a concessionwhether temporarily or permanently to that borrower”.Providing definitions is helpful to the users of theaccounts to understand the basis of managementdecisions and how these have been applied in thecontext of financial reporting. The banks surveyed haveincluded different specific definitions Two examples arefrom the glossaries of HSBC and LBG. Both banksinclude in the definition what they consider toconstitute forbearance arrangements.

Loan impairment

Review of banks’ annual reports 31

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Shareholder Information, Glossary, page 428

Accounting policiesThere has been some difference in practice as to wherethe accounting policies describing the approach toforbearance has been included in the annual report.

LBG have included a specific accounting policy onforbearance as per the extract below as have StandardChartered and Santander. Other banks have chosen toinclude similar disclosures but have included themwithin their credit risk sections rather than specificallydisclosing this within the accounting policies section ofthe annual report.

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Other information, Glossary, page 361

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Financial statements, Notes to consolidated financialstatements, page 222

In the section ‘Critical accounting policies and keysources of estimation uncertainty’ we have considereddevelopments in the format and presentation ofaccounting policy information more generally.

Retail forbearanceThe FSA forbearance guidance suggests an inclusionof the description and quantification of types offorbearance where material. All banks surveyeddisclosed a description of the types of forbearance usedand the total retail loans subject to forbearancearrangements.

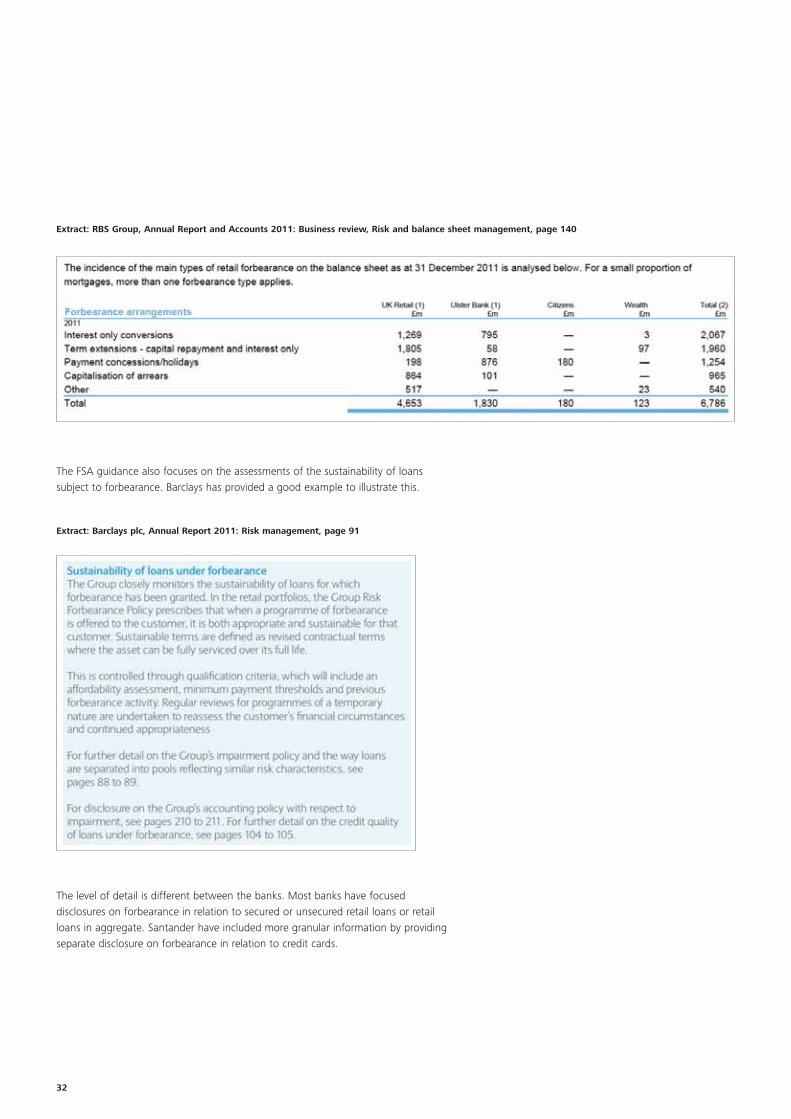

Both RBS and Santander quantify forbearancearrangements by type of strategy employed. The RBSexample is shown on the following page. The examplealso helpfully analyses the type of forbearance betweenthe different RBS business divisions.

32

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, page 140

The FSA guidance also focuses on the assessments of the sustainability of loanssubject to forbearance. Barclays has provided a good example to illustrate this.

Extract: Barclays plc, Annual Report 2011: Risk management, page 91

The level of detail is different between the banks. Most banks have focuseddisclosures on forbearance in relation to secured or unsecured retail loans or retailloans in aggregate. Santander have included more granular information by providingseparate disclosure on forbearance in relation to credit cards.

Review of banks’ annual reports 33

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, page 99

Corporate forbearanceThe FSA guidance specifically relates to mortgages but could be deemed best practice in application to corporateloan portfolios. In general there has been less disclosure in relation to corporate loan portfolios subject toforbearance (often referred to as restructured loans) than for retail portfolios. All of the banks have disclosed thetypes of forbearance practices that have been applied in their corporate portfolio, however the level of informationvaries. RBS provided one of the more detailed disclosures.

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, page 137

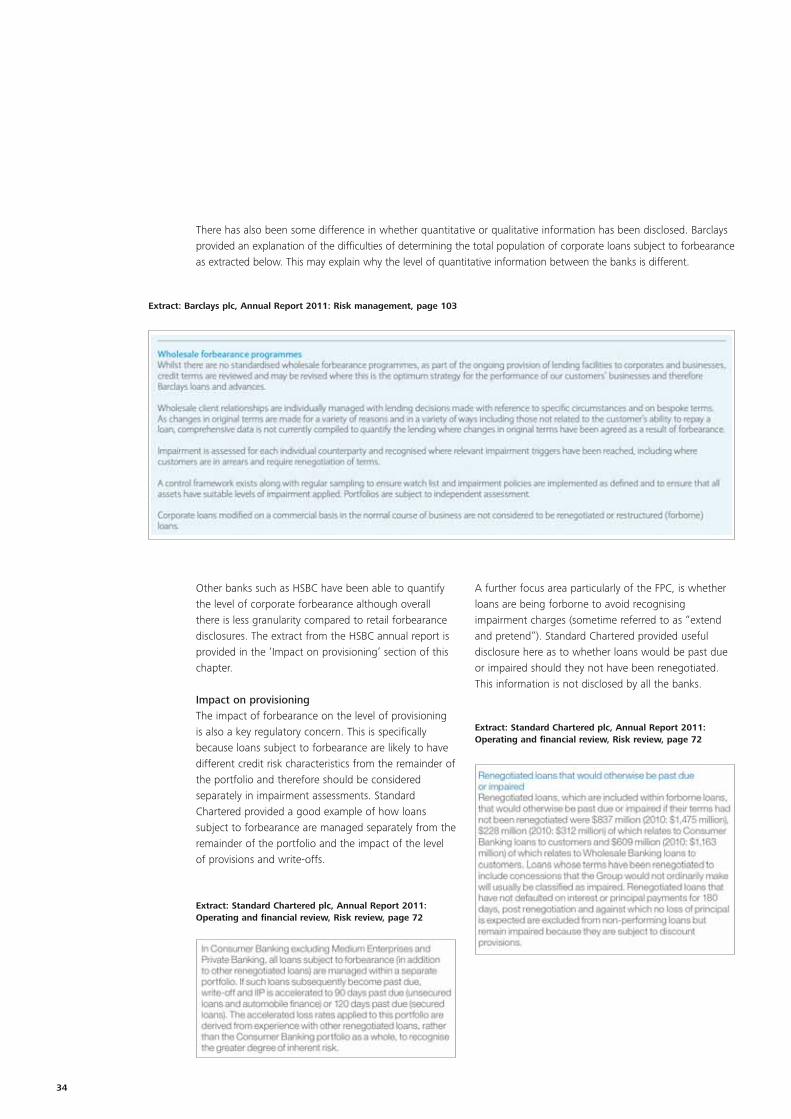

A further focus area particularly of the FPC, is whetherloans are being forborne to avoid recognisingimpairment charges (sometime referred to as “extendand pretend”). Standard Chartered provided usefuldisclosure here as to whether loans would be past dueor impaired should they not have been renegotiated.This information is not disclosed by all the banks.

Extract: Standard Chartered plc, Annual Report 2011:Operating and financial review, Risk review, page 72

34

There has also been some difference in whether quantitative or qualitative information has been disclosed. Barclaysprovided an explanation of the difficulties of determining the total population of corporate loans subject to forbearanceas extracted below. This may explain why the level of quantitative information between the banks is different.

Other banks such as HSBC have been able to quantifythe level of corporate forbearance although overallthere is less granularity compared to retail forbearancedisclosures. The extract from the HSBC annual report isprovided in the ‘Impact on provisioning’ section of thischapter.

Impact on provisioningThe impact of forbearance on the level of provisioningis also a key regulatory concern. This is specificallybecause loans subject to forbearance are likely to havedifferent credit risk characteristics from the remainder ofthe portfolio and therefore should be consideredseparately in impairment assessments. StandardChartered provided a good example of how loanssubject to forbearance are managed separately from theremainder of the portfolio and the impact of the levelof provisions and write-offs.

Extract: Standard Chartered plc, Annual Report 2011:Operating and financial review, Risk review, page 72

Extract: Barclays plc, Annual Report 2011: Risk management, page 103

Review of banks’ annual reports 35

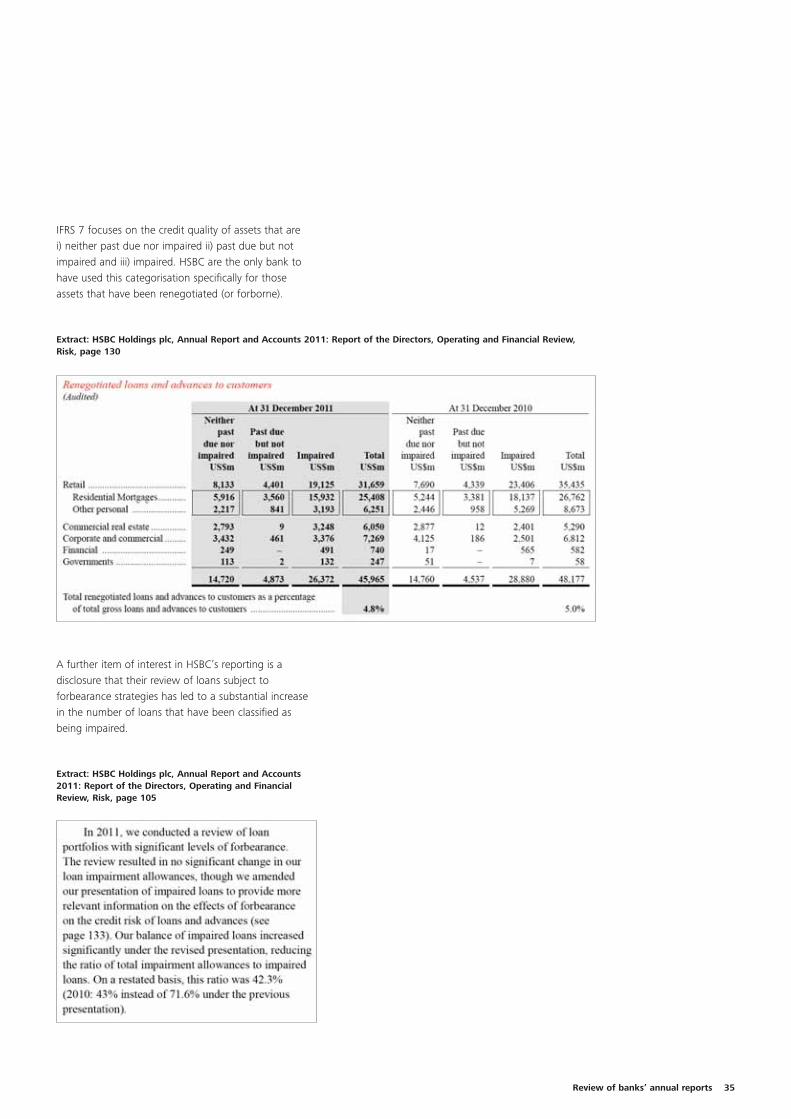

IFRS 7 focuses on the credit quality of assets that arei) neither past due nor impaired ii) past due but notimpaired and iii) impaired. HSBC are the only bank tohave used this categorisation specifically for thoseassets that have been renegotiated (or forborne).

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Report of the Directors, Operating and Financial Review,Risk, page 130

A further item of interest in HSBC’s reporting is adisclosure that their review of loans subject toforbearance strategies has led to a substantial increasein the number of loans that have been classified asbeing impaired.

Extract: HSBC Holdings plc, Annual Report and Accounts2011: Report of the Directors, Operating and FinancialReview, Risk, page 105

36

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Report of the Directors, Operating and Financial Review,Risk, page 138

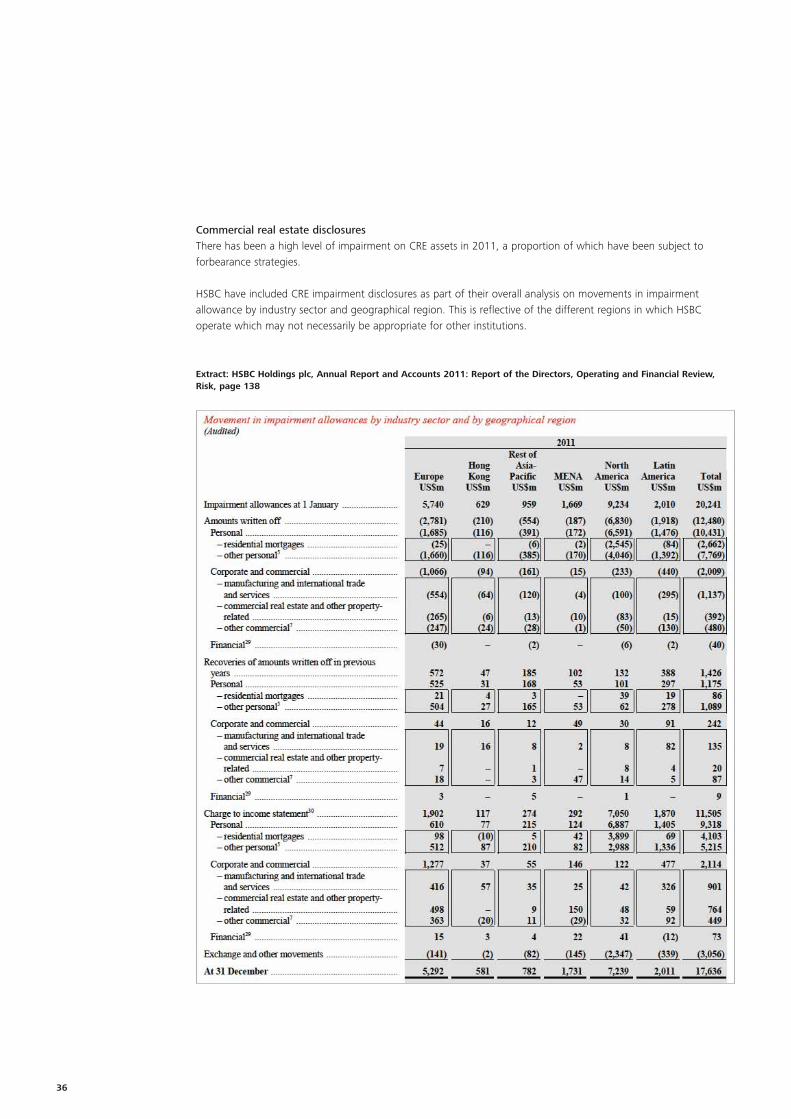

Commercial real estate disclosuresThere has been a high level of impairment on CRE assets in 2011, a proportion of which have been subject toforbearance strategies.

HSBC have included CRE impairment disclosures as part of their overall analysis on movements in impairmentallowance by industry sector and geographical region. This is reflective of the different regions in which HSBCoperate which may not necessarily be appropriate for other institutions.

Review of banks’ annual reports 37

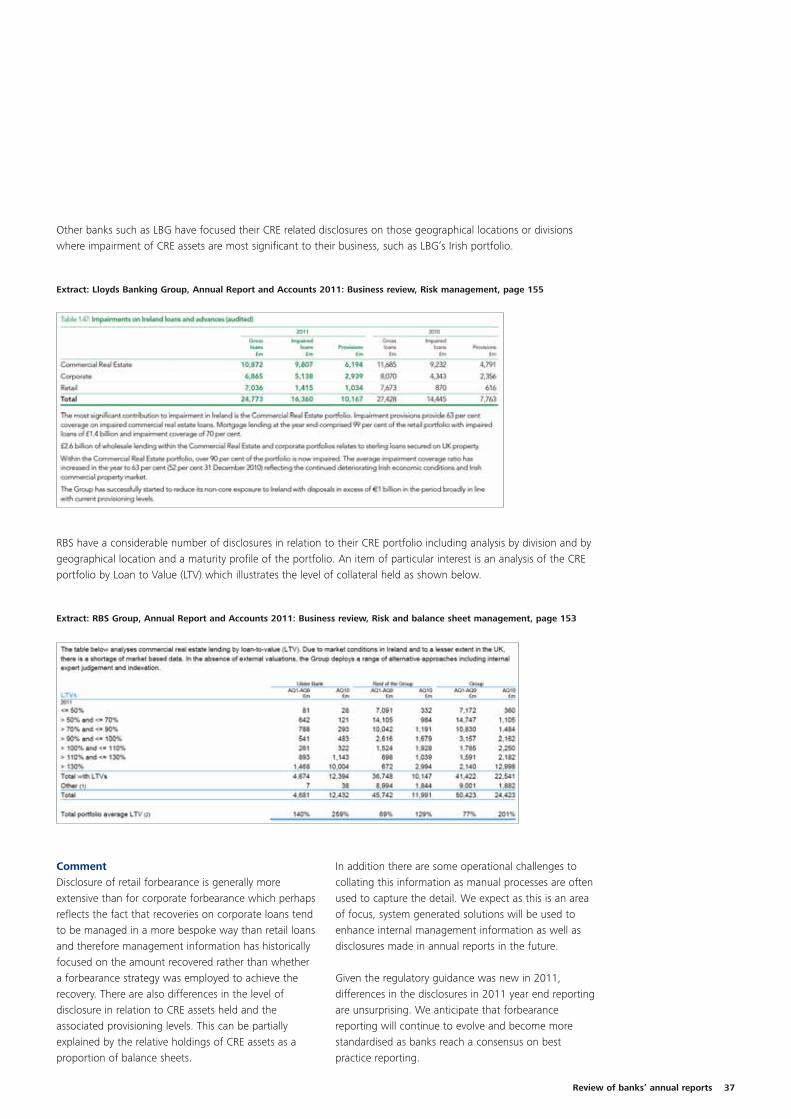

Other banks such as LBG have focused their CRE related disclosures on those geographical locations or divisionswhere impairment of CRE assets are most significant to their business, such as LBG’s Irish portfolio.

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Business review, Risk management, page 155

RBS have a considerable number of disclosures in relation to their CRE portfolio including analysis by division and bygeographical location and a maturity profile of the portfolio. An item of particular interest is an analysis of the CREportfolio by Loan to Value (LTV) which illustrates the level of collateral held as shown below.

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk and balance sheet management, page 153

CommentDisclosure of retail forbearance is generally moreextensive than for corporate forbearance which perhapsreflects the fact that recoveries on corporate loans tendto be managed in a more bespoke way than retail loansand therefore management information has historicallyfocused on the amount recovered rather than whethera forbearance strategy was employed to achieve therecovery. There are also differences in the level ofdisclosure in relation to CRE assets held and theassociated provisioning levels. This can be partiallyexplained by the relative holdings of CRE assets as aproportion of balance sheets.

In addition there are some operational challenges tocollating this information as manual processes are oftenused to capture the detail. We expect as this is an areaof focus, system generated solutions will be used toenhance internal management information as well asdisclosures made in annual reports in the future.

Given the regulatory guidance was new in 2011,differences in the disclosures in 2011 year end reportingare unsurprising. We anticipate that forbearancereporting will continue to evolve and become morestandardised as banks reach a consensus on bestpractice reporting.

38

BackgroundThe valuation of financial instruments at fair value bybanks remains a critical area of judgement in thepreparation of financial statements. Market conditionsfor some assets have improved since our lastpublication and pricing transparency has increased.Nevertheless many markets remain highly illiquidrequiring banks to estimate the values of positions usinglimited observable data. The ongoing measurementuncertainty has led to regulators and investorscontinuing to increase their expectations around thelevel of disclosure provided by banks around theirprocesses and controls, and assumptions related to thefair value financial of instruments.

The requirements for disclosures on financial instrumentvaluation are contained within IFRS 7 and also in IAS 1Presentation of Financial Statements (IAS 1) whichrequires disclosure on key sources of estimationuncertainty. It has also been a recurring theme of theFSA for firms to provide improved disclosures onvaluation assumptions and methodologies.

Overall commentsThere are three areas which we expect to remain anongoing area of interest due to the key judgements anduncertainties in the valuation of financial instrumentsand the significant impact these have on a bank’sreported results. The three areas are:

• The valuation control environment;

• Credit valuation adjustments; and

• Other valuation adjustments.

Detailed findings

Valuation control environmentOn a bank balance sheet, a financial instrument held atfair value is represented by a single value. Whilst thisinformation is useful for users of financial statements,there is increasing demand for banks to provide moreexplanation as to how that value is determined, andwhat that value might potentially be were differentassumptions to be applied.

In 2009 the International Accounting Standards Board(IASB) made significant enhancements to the fairvaluation disclosure requirements in IFRS 7 byintroducing a fair value hierarchy. This has led to anincrease in disclosure of quantitative information whichcontinues to grow in response to demands frominvestors and regulators. From the review of banks’annual reports in this survey, significant improvementhas also been made to the qualitative aspects ofvaluation, and in particular disclosures around thegovernance processes and control environments thatbanks have put in place to determine fair value andreview the associated subjectivities.

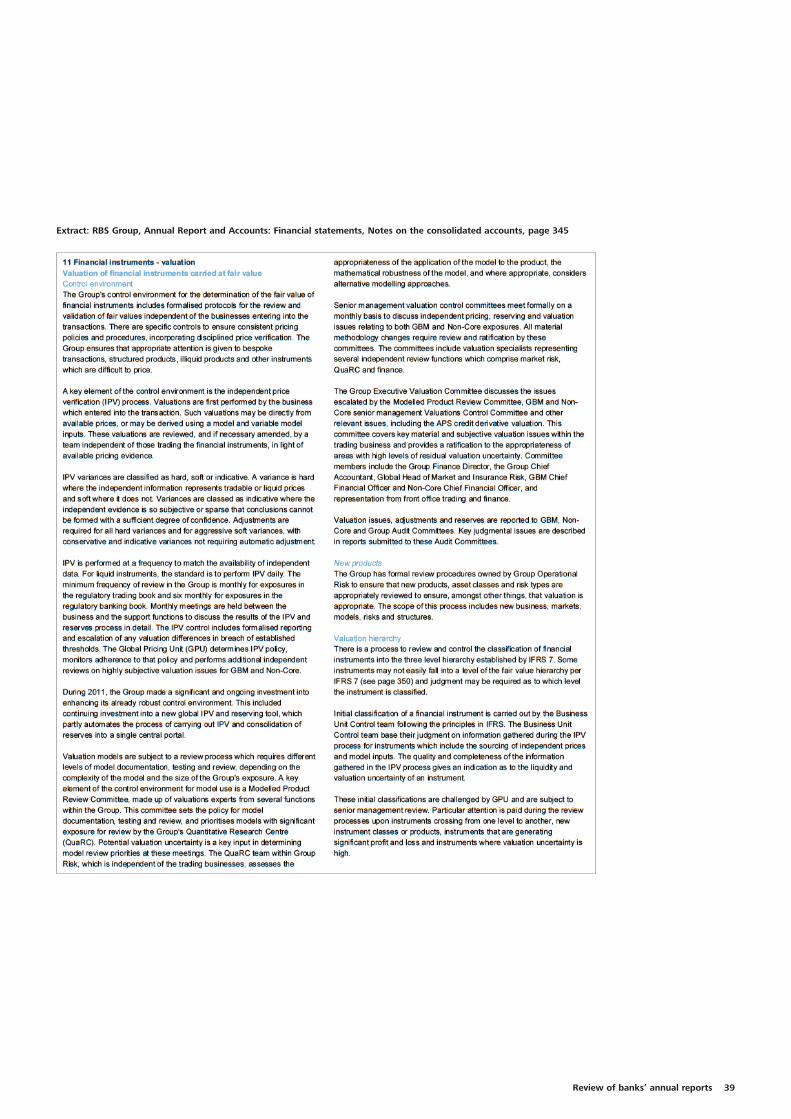

For example, RBS begin their financial instrumentsvaluation note with a detailed overview of the valuationcontrol environment. In particular, it details theindependent price verification (IPV) process, how IPVdifferences are characterised and reviewed, the modelcontrol process, and the various management meetingsand committees at which such topics are discussed.

Financial instrument valuation

Review of banks’ annual reports 39

Extract: RBS Group, Annual Report and Accounts: Financial statements, Notes on the consolidated accounts, page 345

40

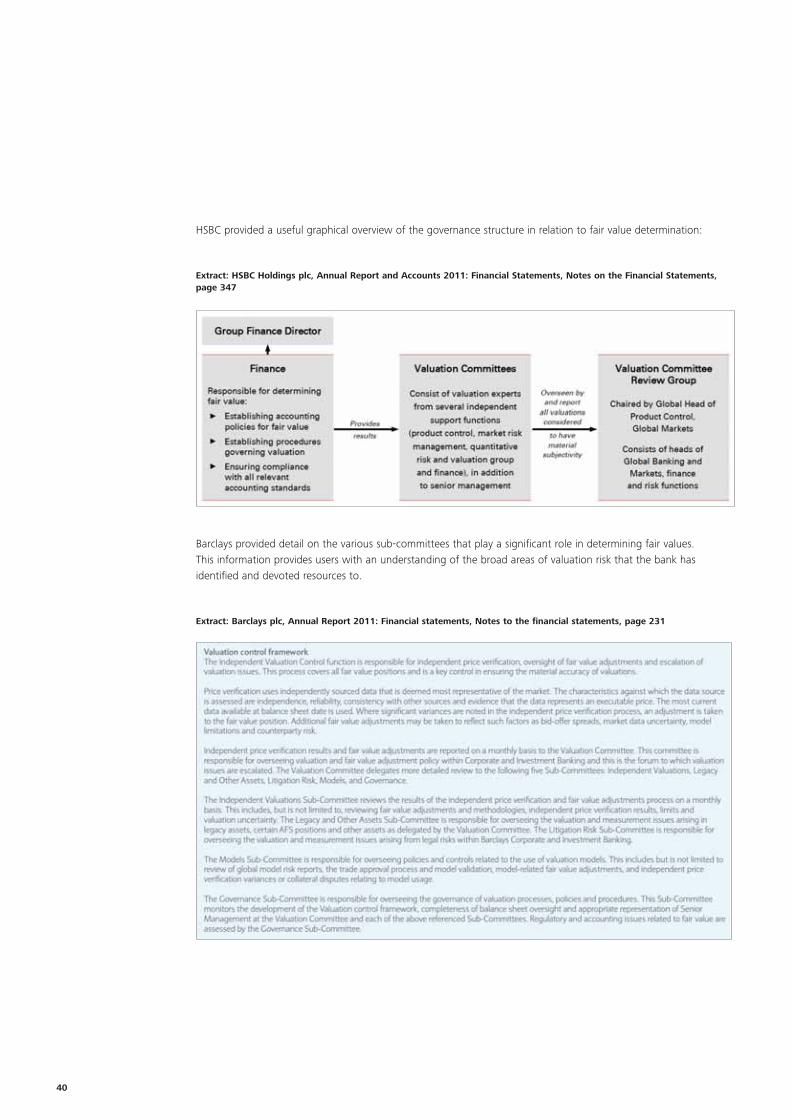

HSBC provided a useful graphical overview of the governance structure in relation to fair value determination:

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Financial Statements, Notes on the Financial Statements,page 347

Barclays provided detail on the various sub-committees that play a significant role in determining fair values. This information provides users with an understanding of the broad areas of valuation risk that the bank hasidentified and devoted resources to.

Extract: Barclays plc, Annual Report 2011: Financial statements, Notes to the financial statements, page 231

Review of banks’ annual reports 41

The development and improvement of disclosures in thisarea is welcome, as they help to shed light on what isoften seen as an opaque area of banking. By detailingthe control environment in place, users of the financialstatements get a clearer picture of the processes that thebanks go through in order to ensure the accuracy andintegrity of reported fair values, as well as the potentialchallenges that a bank faces when determining them.

Credit valuation adjustmentsCredit risk is a focus area for all key bank stakeholders.Of particular interest when markets are turbulent is theCredit Valuation Adjustment (CVA) that is applied whenfair valuing Over the Counter (OTC) derivative portfolios.CVA is a necessary input in a derivatives valuation as inmost cases there are not traded prices for derivativesand fair valuation must reflect credit risk. Whilst CVAmethodologies have become more sophisticated and wellunderstood, they still remain one of the most judgementaland subjective areas of fair value accounting.

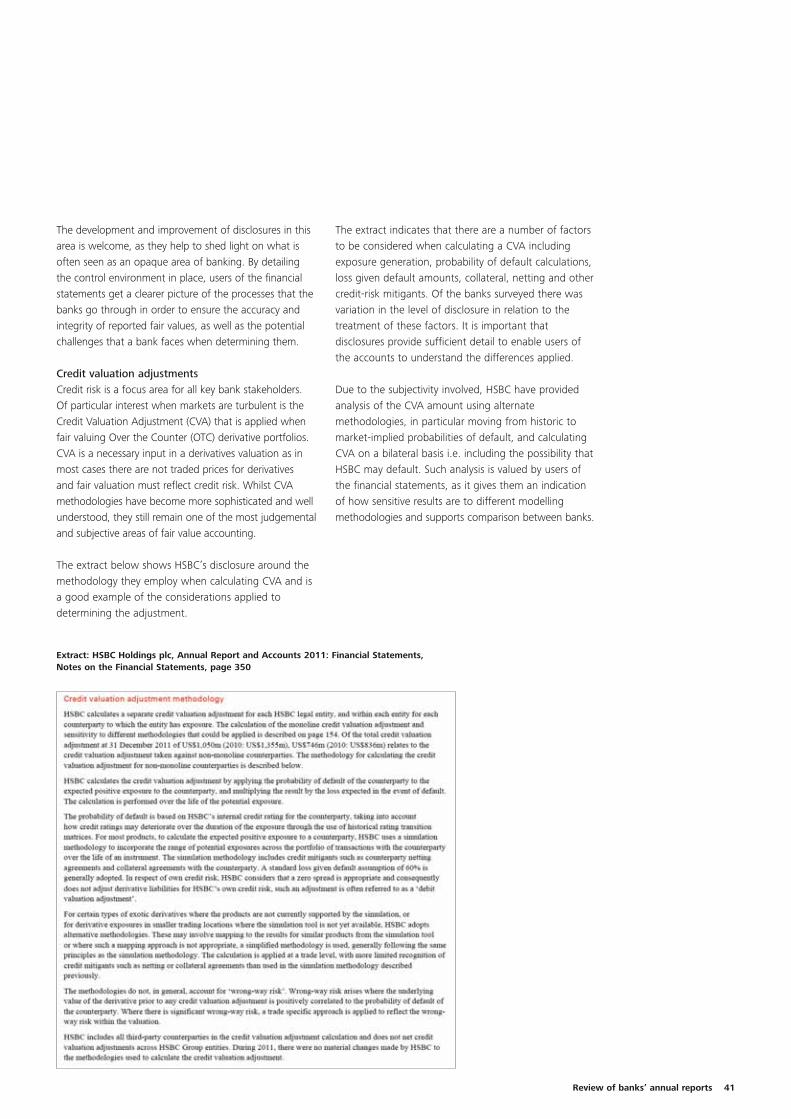

The extract below shows HSBC’s disclosure around themethodology they employ when calculating CVA and isa good example of the considerations applied todetermining the adjustment.

The extract indicates that there are a number of factorsto be considered when calculating a CVA includingexposure generation, probability of default calculations,loss given default amounts, collateral, netting and othercredit-risk mitigants. Of the banks surveyed there wasvariation in the level of disclosure in relation to thetreatment of these factors. It is important thatdisclosures provide sufficient detail to enable users ofthe accounts to understand the differences applied.

Due to the subjectivity involved, HSBC have providedanalysis of the CVA amount using alternatemethodologies, in particular moving from historic tomarket-implied probabilities of default, and calculatingCVA on a bilateral basis i.e. including the possibility thatHSBC may default. Such analysis is valued by users ofthe financial statements, as it gives them an indicationof how sensitive results are to different modellingmethodologies and supports comparison between banks.

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Financial Statements,Notes on the Financial Statements, page 350

42

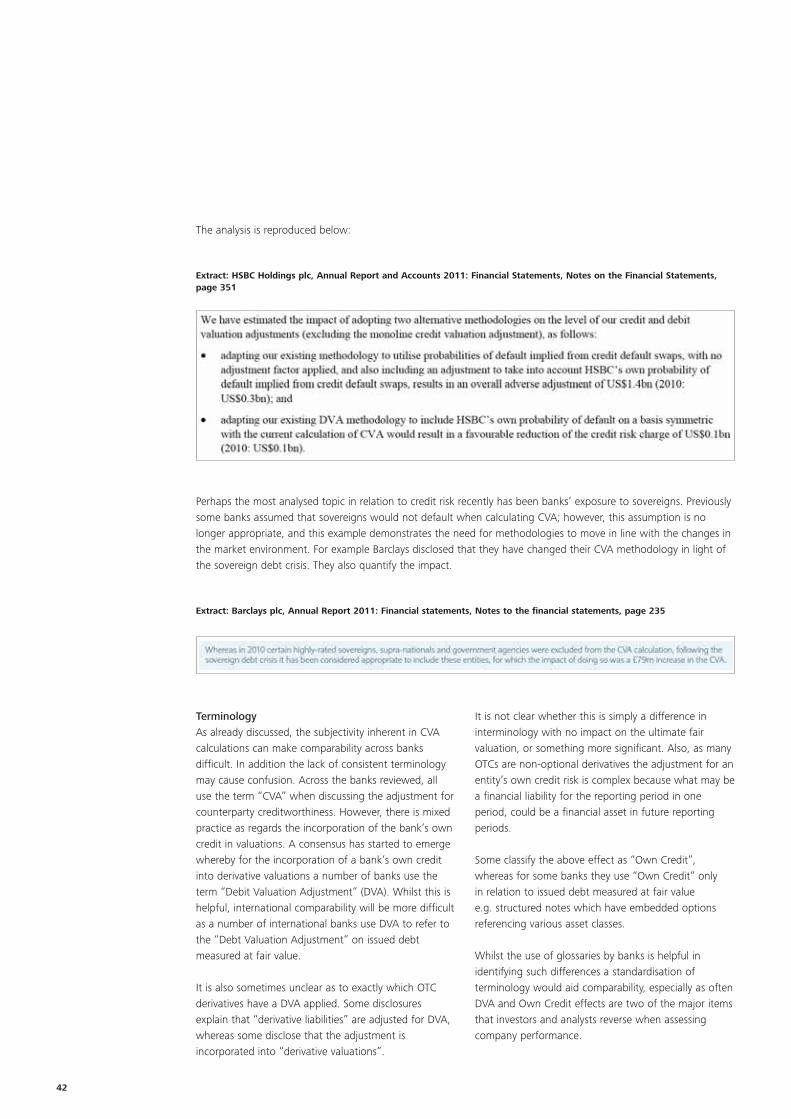

The analysis is reproduced below:

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Financial Statements, Notes on the Financial Statements,page 351

Perhaps the most analysed topic in relation to credit risk recently has been banks’ exposure to sovereigns. Previouslysome banks assumed that sovereigns would not default when calculating CVA; however, this assumption is nolonger appropriate, and this example demonstrates the need for methodologies to move in line with the changes inthe market environment. For example Barclays disclosed that they have changed their CVA methodology in light ofthe sovereign debt crisis. They also quantify the impact.

TerminologyAs already discussed, the subjectivity inherent in CVAcalculations can make comparability across banksdifficult. In addition the lack of consistent terminologymay cause confusion. Across the banks reviewed, alluse the term “CVA” when discussing the adjustment forcounterparty creditworthiness. However, there is mixedpractice as regards the incorporation of the bank’s owncredit in valuations. A consensus has started to emergewhereby for the incorporation of a bank’s own creditinto derivative valuations a number of banks use theterm “Debit Valuation Adjustment” (DVA). Whilst this ishelpful, international comparability will be more difficultas a number of international banks use DVA to refer tothe “Debt Valuation Adjustment” on issued debtmeasured at fair value.

It is also sometimes unclear as to exactly which OTCderivatives have a DVA applied. Some disclosuresexplain that “derivative liabilities” are adjusted for DVA,whereas some disclose that the adjustment isincorporated into “derivative valuations”.

It is not clear whether this is simply a difference ininterminology with no impact on the ultimate fairvaluation, or something more significant. Also, as manyOTCs are non-optional derivatives the adjustment for anentity’s own credit risk is complex because what may bea financial liability for the reporting period in oneperiod, could be a financial asset in future reportingperiods.

Some classify the above effect as “Own Credit”,whereas for some banks they use “Own Credit” only in relation to issued debt measured at fair value e.g. structured notes which have embedded optionsreferencing various asset classes.

Whilst the use of glossaries by banks is helpful inidentifying such differences a standardisation ofterminology would aid comparability, especially as oftenDVA and Own Credit effects are two of the major itemsthat investors and analysts reverse when assessingcompany performance.

Extract: Barclays plc, Annual Report 2011: Financial statements, Notes to the financial statements, page 235

Review of banks’ annual reports 43

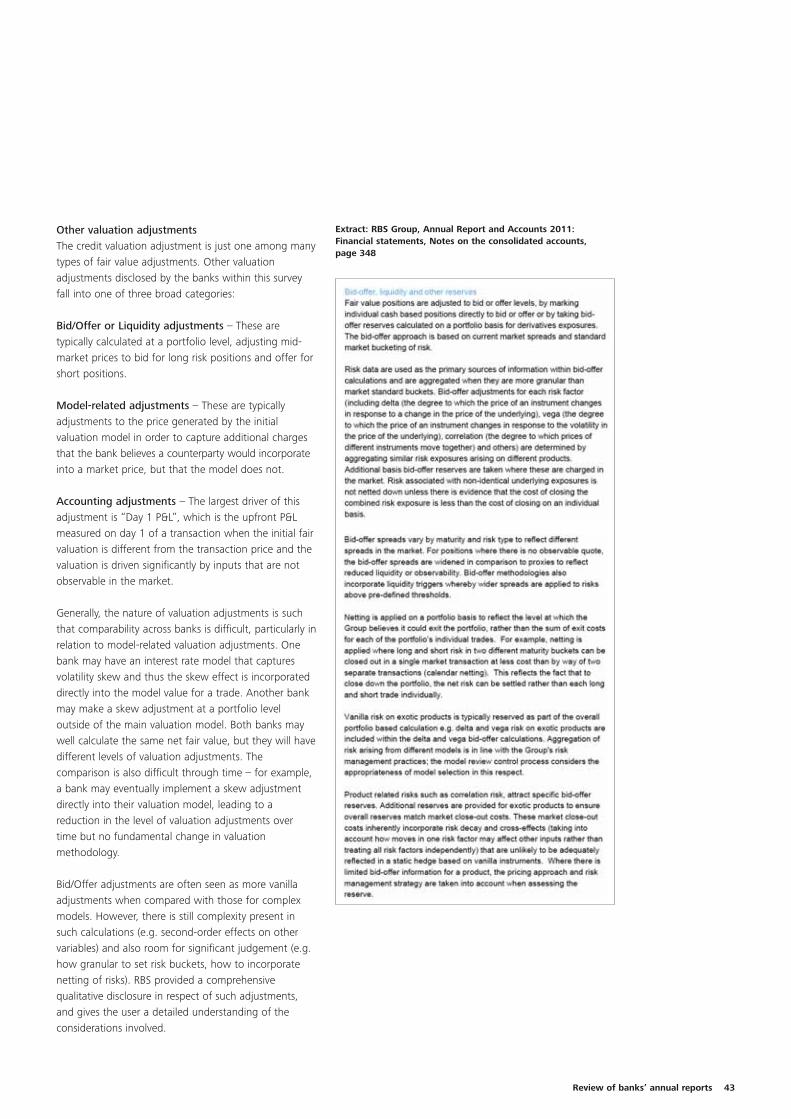

Other valuation adjustmentsThe credit valuation adjustment is just one among manytypes of fair value adjustments. Other valuationadjustments disclosed by the banks within this surveyfall into one of three broad categories:

Bid/Offer or Liquidity adjustments – These aretypically calculated at a portfolio level, adjusting mid-market prices to bid for long risk positions and offer forshort positions.

Model-related adjustments – These are typicallyadjustments to the price generated by the initialvaluation model in order to capture additional chargesthat the bank believes a counterparty would incorporateinto a market price, but that the model does not.

Accounting adjustments – The largest driver of thisadjustment is “Day 1 P&L”, which is the upfront P&Lmeasured on day 1 of a transaction when the initial fairvaluation is different from the transaction price and thevaluation is driven significantly by inputs that are notobservable in the market.

Generally, the nature of valuation adjustments is suchthat comparability across banks is difficult, particularly inrelation to model-related valuation adjustments. Onebank may have an interest rate model that capturesvolatility skew and thus the skew effect is incorporateddirectly into the model value for a trade. Another bankmay make a skew adjustment at a portfolio leveloutside of the main valuation model. Both banks maywell calculate the same net fair value, but they will havedifferent levels of valuation adjustments. Thecomparison is also difficult through time – for example,a bank may eventually implement a skew adjustmentdirectly into their valuation model, leading to areduction in the level of valuation adjustments overtime but no fundamental change in valuationmethodology.

Bid/Offer adjustments are often seen as more vanillaadjustments when compared with those for complexmodels. However, there is still complexity present insuch calculations (e.g. second-order effects on othervariables) and also room for significant judgement (e.g.how granular to set risk buckets, how to incorporatenetting of risks). RBS provided a comprehensivequalitative disclosure in respect of such adjustments,and gives the user a detailed understanding of theconsiderations involved.

Extract: RBS Group, Annual Report and Accounts 2011:Financial statements, Notes on the consolidated accounts,page 348

44

One area of recent debate has been the incorporation of funding adjustments into the valuation of uncollateralisedderivatives. The example below shows LBG’s disclosure in relation to this adjustment, together with sensitivityanalysis:

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Financial statements, Notes to the consolidated financialstatements, page 319

A related debate concerns the embedded optionality in collateral agreements. Banks and their counterparties mayhave the option to deliver different types of collateral, and in different currencies. Many market participants see“value” in this option. The disclosure below is taken from Barclays, and indicates that they incorporate such anadjustment into their fair values.

Extract: Barclays plc, Annual Report 2011: Financial statements, Notes to the financial statements, page 234

CommentWhilst explanations of the control environment andprocesses around making adjustments are useful, moredetailed disclosure is also sought by users, includingfurther sensitivity analysis in relation to inputs andmodelling assumptions. Valuation adjustments varysignificantly across institutions, not least becausesometimes a potential adjustment is embedded in avaluation and sometimes it is a top up. This makes itdifficult for users to draw comparisons between banksunless there are sufficiently detailed qualitativedescriptions explaining a bank’s approach to calculatingvaluation adjustments. For example, setting outwhether adjustments have been made at a trade orportfolio level is helpful to those seeking to understandexactly what adjustments a bank has made and tocompare banks’ approaches. Our review has found thatvaluation disclosures have become fuller since our lastsurvey. We think they are likely to continue to developin response to investors’ interests and initiatives such asthe FSB’s Enhanced Disclosure Taskforce.

Review of banks’ annual reports 45

BackgroundFrom January 2013 global banks will have six years toprogressively increase their capital reserves under theBasel III requirements. As part of this capital reform,banks will be required to hold more and safer kinds ofcapital commensurate with the risks they take, whichshould make them more resistant to financial shocks.It also explicitly introduces minimum liquidity standards,a minimum leverage ratio, and enhances overallgovernance mechanisms. The quality of banks’disclosures in this area will be of particular importance.Regulatory capital disclosures in bank annual reportshave already become more extensive in recent yearsand enhanced reporting is likely to increase as theBasel III requirements start to become effective.

The IFRS reporting requirements for regulatory capital inannual reports are contained within IAS 1. IAS 1 statesthat entities should disclose the way they managecapital including any capital requirements imposed byregulators. In addition in the UK, the FSA required allbanks to disclose further information, specifically, areconciliation of a bank’s regulatory capital to theiraccounting capital.

Overall commentsThe disclosures around regulatory capital havedeveloped over the last few years in response to theBasel requirements and additional informationrequested by local regulators. Our survey has focusedon the following themes included in the 2011 annualreports:

• Accounting capital to regulatory capitalreconciliations;

• The disclosure of risk weighted assets (RWAs);

• The impact of Basel III; and

• The disclosure of other Basel III measures.

Detailed findings

A reconciliation of accounting capital to regulatorycapital resourcesThe disclosure of a reconciliation from accountingcapital to regulatory capital resources has become oneof the key disclosures for investors over the past threeyears. This reconciliation has now become fairlystandardised across all the six biggest UK banks, andprovides a clear link back to the balance sheet in thecase of all six banks surveyed. An example of thisreconciliation from Standard Chartered is shown on the next page.

Regulatory capital disclosures

46

Extract: Standard Chartered plc, Annual Report 2011: Operating and financial review, Capital, page 89

Review of banks’ annual reports 47

The technical adjustments to accounting capital are insome cases complex and disclosure providingexplanation of these technical areas can be useful.In addition to the quantitative table some of the banksprovided further granularity on the nature of thesetechnical adjustments.

One of the key adjustments to accounting capital forregulatory purposes is the deduction of the excess ofexpected losses calculated under the Basel InternalRatings Based Approach, to the extent that theseoutweigh accounting provisions calculated under IFRS.This in most cases is a significant deduction as IAS 39requires provisions to be recognised on an ‘incurredloss’ basis. Santander provided an explanation of thisadjustment in their annual report as part of thecommentary on core tier one deductions.

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Balance Sheet Business Review, page 55

48

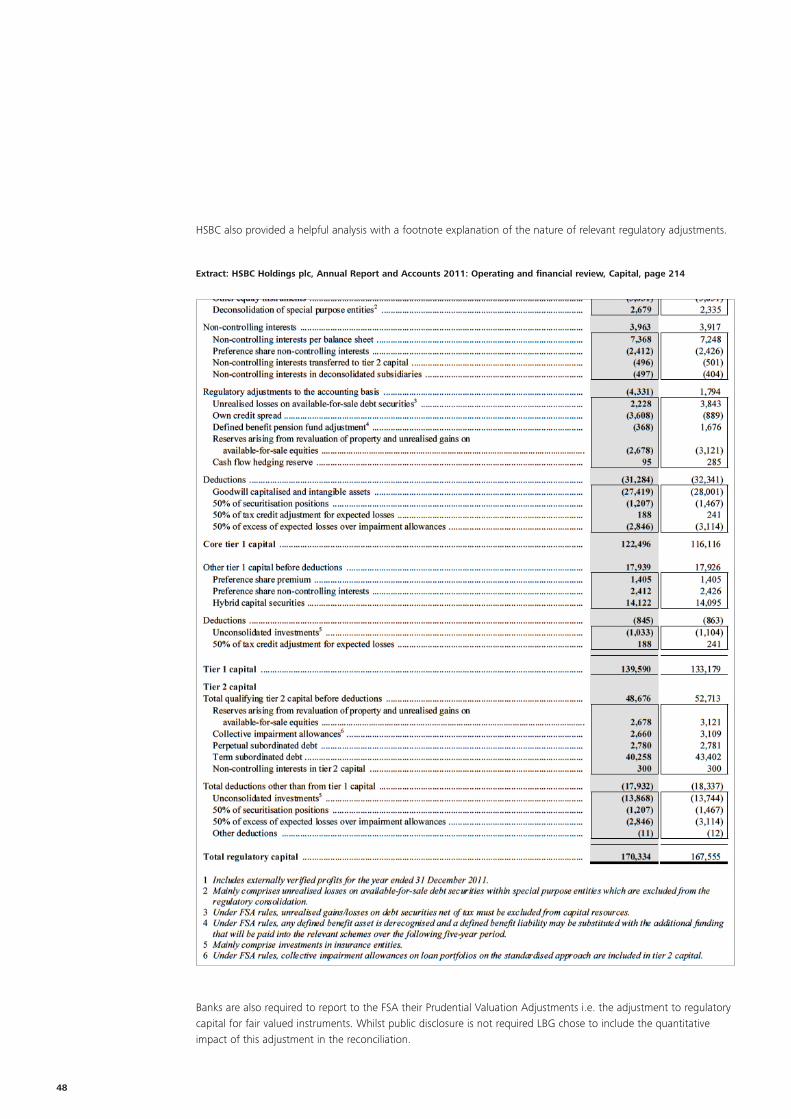

HSBC also provided a helpful analysis with a footnote explanation of the nature of relevant regulatory adjustments.

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Operating and financial review, Capital, page 214

Banks are also required to report to the FSA their Prudential Valuation Adjustments i.e. the adjustment to regulatorycapital for fair valued instruments. Whilst public disclosure is not required LBG chose to include the quantitativeimpact of this adjustment in the reconciliation.

Review of banks’ annual reports 49

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Business review, Risk management, page 120

Disclosure of risk weighted assetsThe disclosure of RWAs by business divisions is also considered good practice as it shows where capital consumptionis distributed within a group. All of the banks surveyed disclosed RWAs by business segment or geography. Anexample is included from the RBS annual report where this is included in the quantitative results of each respectivebusiness division, the extract below is for the RBS Retail business division.

Extract: RBS Group, Annual Report and Accounts 2011: Business review, page 63

The impact of Basel IIIAll of the banks surveyed mention the introduction of Basel III as part of the business review, due to the significantimpact that this new regulation will have, once fully adopted by the European Union (EU). The level of commentaryappears to be reduced compared to the prior year. However the banks surveyed refer to this as part of theirprincipal risk considerations given the uncertainty over the exact nature of the final EU adoption of Basel III in theCapital Requirements Directive/Capital Requirements Regulation. Santander included this as part of the commentaryon the impact of regulatory capital and liquidity requirements.

Extract: Santander UK plc 2011 Annual Report: Shareholder information, Risk factors, page 281

50

The disclosure of movements in RWAs is also a useful tool for investors. Banks are struggling to raise core tier oneequity capital in current market conditions, and therefore are targeting RWA deductions as the primary tool to meethigher capital ratio targets. A clear explanation of such movements was provided by LBG.

Extract: Lloyds Banking Group, Annual Report and Accounts 2011: Business review, Risk management, page 121

Review of banks’ annual reports 51

All banks included qualitative statements on thepotential impact of Basel III. In addition four of thebanks surveyed, provided further information on thequantitative impact of Basel III on their core tier oneratios, compared to five of the six banks that producedquantitative analysis in their 2010 annual reports.

Two of the banks disclosed this in terms of the changeto core tier one ratio at the proposed implementationdate of 1 January 2013 whereas the other two banksrefer to the day 1 RWA increase as a result of higher riskweighted assets for counterparty credit risk. Basel IIIintroduces tougher measures to the quality of capital(capital resources) and the capital requirements thatbanks are obliged to meet. However, the changes to thequality of capital are phased in over a five to ten yearperiod, whereas the requirements for RWA are applicablein full from the 1 January 2013 implementation datehence it is understandable why banks have focused onproviding disclosure on the RWA impact in their 2011annual reports. As all of the adjustments to core tier onecapital resources are to happen over a five year ‘phasein’ period it is unsurprising that banks should solelyconsider the RWA impact as at 1 January 2013.

Extract: HSBC Holdings plc, Annual Report 2011: Report of theDirectors, Operating and Financial Review, Capital, page 213

Extract: RBS Group, Annual Report and Accounts 2011: Business review, Risk andbalance sheet management, page 115

Further useful information is disclosed by HSBC whichprovided additional information on the actionsmanagement is taking to reduce the negative impact of Basel III on its core tier one ratio.

An example of the disclosure is extracted from the RBSannual report.

52

The disclosure of other Basel III measuresAs Basel III has also introduced minimum liquidity standards some additional disclosure is provided in this area in theannual reports. This included information on the LCR, the NSFR and the Leverage Ratio.

Barclays specifically disclosed it currently meets the Basel III minimum leverage ratio

Extract: Barclays plc, Annual Report 2011: Risk management, Funding risk – Capital, page 138

Three of the banks surveyed also disclosed their current LCR and NSFR against the mandated Basel III level.Examples from Barclays and Standard Chartered are shown below.

Extract: Barclays plc, Annual Report 2011: Risk management, Funding risk – Capital, page 143

Extract: Standard Chartered plc, Annual Report 2011: Operating and financial review, Risk review, page 82

Review of banks’ annual reports 53

Further consideration of the enhanced liquidity andfunding disclosures is included in the section on‘Liquidity and funding’ of this survey.

CommentThe reconciliation that banks provided betweenaccounting and regulatory capital in their 2011 annualreports has become more consistent between thebanks, and the disclosure of the source of quantitativedifferences between IFRS provisioning and Basel modelsis particularly insightful.

Basel III introduces a significant increase in the numberof regulatory adjustments to accounting capital whichwill make it difficult to produce disclosures in a conciseformat, especially with the many grandfathering and‘phasing in’ provisions.

Given the uncertainty over the final EU adoption of theBasel III requirements there are some differences in thelevel of granularity provided by the banks of the impactof the regulatory and capital changes. As the impact ofthe requirements begins to be phased in we expect thatthere will be further disclosure of the quantitativeimpact of these new capital requirements in addition tocommentary linking this to the overall managementstrategies of these institutions.

54

BackgroundThe financial crisis highlighted the importance ofunderstanding the risks faced by banks. High qualitydisclosures of a bank’s risk exposures and managementpractices to address them are critical for stakeholders toassess the business and the quality of its management.Since the financial crisis, UK bank risk disclosures haveevolved and 2011 annual reports have seen furtherimprovement in this area, with additional disclosure onkey risks most relevant to current market conditionssuch as liquidity and funding risks, loans subject toforbearance, and sovereign debt exposures.

For UK listed entities the requirements to considerprincipal risks and uncertainties and the riskidentification and mitigation of these risks are includedwithin several sources including: the Companies Act, aspart of the Reporting Statement Operating andFinancial Review issued by the Accounting StandardsBoard, the Listing Rules, the FSA Disclosure andTransparency Rules, the Combined Code and IFRS 7.

There has also been a significant volume of work on thequality of bank risk disclosures in the aftermath of thefinancial crisis.

• The Institute of Chartered Accountants in England &Wales (ICAEW) report Audit of banks: lessons fromthe crisis published in June 2010. One of the report’smain findings was that prior to the crisis, relevant riskinformation was often provided in banks’ annualreports but it was not easy to understand nor indeedto find. This was because risk information was foundin many parts of the annual report, such as theoperating and financial review at the front of thereport and in various parts of the notes to theaccounts in the back part of the report.

• A briefing report by Philip Linsley, published by ICAEWin 2011, on UK bank risk disclosures in the periodthrough to the onset of the financial crisis looked atthe risk disclosures in the annual accounts of 8 largeUK banks for the seven years between 2002 and2008. One of the key findings in this report was thatover the period of the review, risk disclosures in bankaccounts before the credit crisis gave little idea of theimpending problems that many banks were toexperience but that following the crisis risk disclosuresdid improve.

• The FSB’s Thematic Review on Risk DisclosurePractices March 2011 published a thematic review ofrisk disclosures making recommendations for areas forimprovement and focus such as improvements inareas of uncertainty, the timeliness of disclosures anddisclosures to enable comparability.

Overall commentsA key feature of the improvements in risk disclosures inthe UK has been that most have been market orregulatory driven rather than specifically required byaccounting standards. This has been influenced by theBBA’s Code (‘the Code’) for financial reportingdisclosure. The Code was developed with input fromthe large UK banks and the Nationwide Building Society(Nationwide). The overarching principle of the Codewas the commitment by the banks to provide high-quality, meaningful and decision-useful disclosures tousers of accounts to enable them to understand thefinancial position and performance of the institution.The Code was drafted partly in response to the FSA’sdesire to see enhanced financial reporting disclosures by banks and other credit institutions.

An assessment of the disclosures on liquidity andfunding risks, sovereign debt risk and forbearance havebeen reviewed in separate sections of this survey andtherefore this section considers the following areas ofdisclosure:

• The overall presentation of risk information;

• An explanation of the bank’s risk profile and riskappetite; and

• The approach to the management of risk.

Detailed findings

Presentation of risk disclosuresThere has been significant development in the analysisof risks that might affect an institution. Prior to thecrisis there was little in the way of these types ofdisclosure and a critique that the information wasdifficult to understand because it was presented indifferent parts of the annual report. In more recentannual reports such disclosures are common and insome cases very comprehensive. Communicating suchinformation clearly is important and effectivepresentation can enhance the transparency ofdisclosures.

Risk disclosures

Review of banks’ annual reports 55

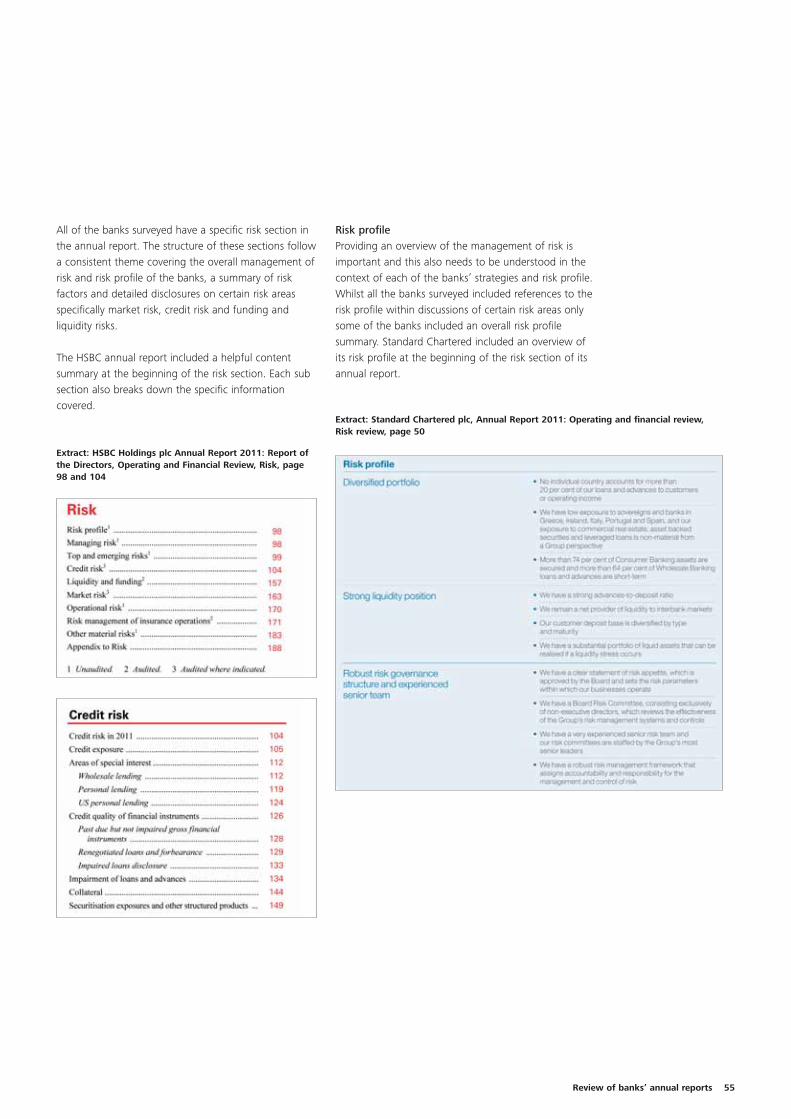

All of the banks surveyed have a specific risk section inthe annual report. The structure of these sections followa consistent theme covering the overall management ofrisk and risk profile of the banks, a summary of riskfactors and detailed disclosures on certain risk areasspecifically market risk, credit risk and funding andliquidity risks.

The HSBC annual report included a helpful contentsummary at the beginning of the risk section. Each subsection also breaks down the specific informationcovered.

Extract: HSBC Holdings plc Annual Report 2011: Report ofthe Directors, Operating and Financial Review, Risk, page98 and 104

Risk profileProviding an overview of the management of risk isimportant and this also needs to be understood in thecontext of each of the banks’ strategies and risk profile.Whilst all the banks surveyed included references to therisk profile within discussions of certain risk areas onlysome of the banks included an overall risk profilesummary. Standard Chartered included an overview ofits risk profile at the beginning of the risk section of itsannual report.

Extract: Standard Chartered plc, Annual Report 2011: Operating and financial review, Risk review, page 50

56

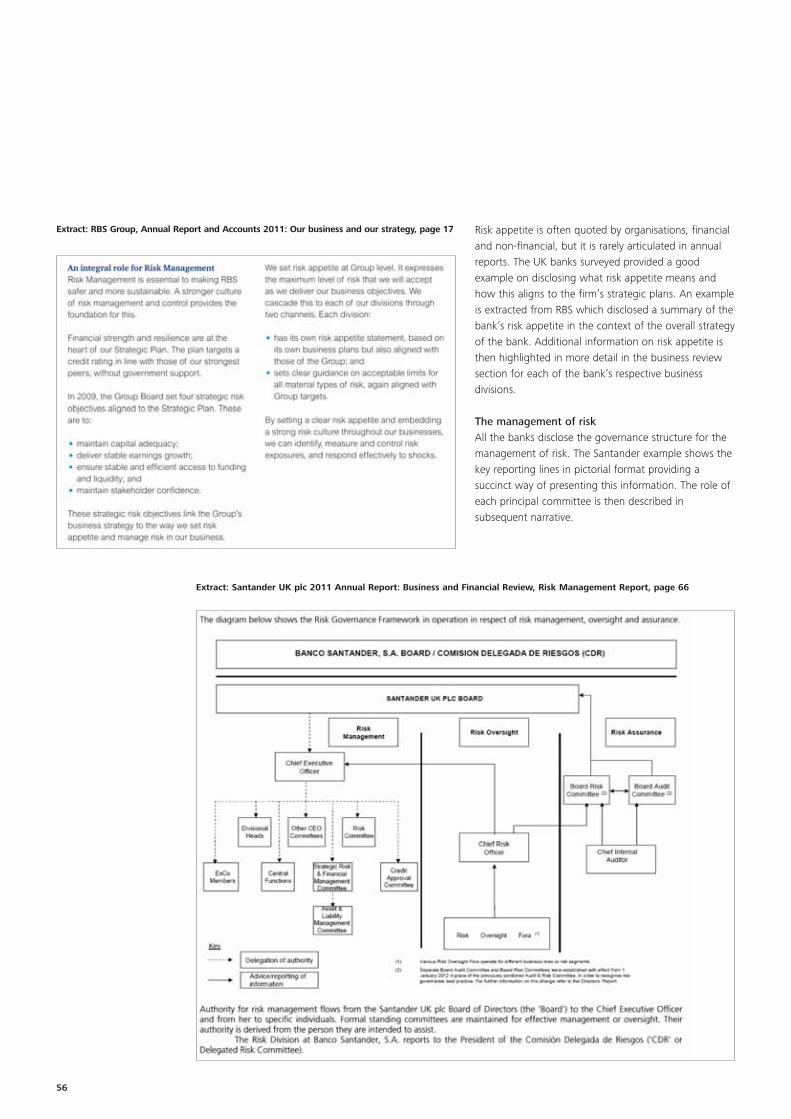

Risk appetite is often quoted by organisations, financialand non-financial, but it is rarely articulated in annualreports. The UK banks surveyed provided a goodexample on disclosing what risk appetite means andhow this aligns to the firm’s strategic plans. An exampleis extracted from RBS which disclosed a summary of thebank’s risk appetite in the context of the overall strategyof the bank. Additional information on risk appetite isthen highlighted in more detail in the business reviewsection for each of the bank’s respective businessdivisions.

The management of riskAll the banks disclose the governance structure for themanagement of risk. The Santander example shows thekey reporting lines in pictorial format providing asuccinct way of presenting this information. The role ofeach principal committee is then described insubsequent narrative.

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, page 66

Extract: RBS Group, Annual Report and Accounts 2011: Our business and our strategy, page 17

Review of banks’ annual reports 57

The governance structure is also then described in the context of the bank’s principal risks.

The narrative approach to describing the management of risk is different between the six banks. Some of theinstitutions provided an explanation of the external risk factors impacting the bank and how these are managedwhilst other banks explained the internal processes used to evaluate and manage risk.

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, page 72

58

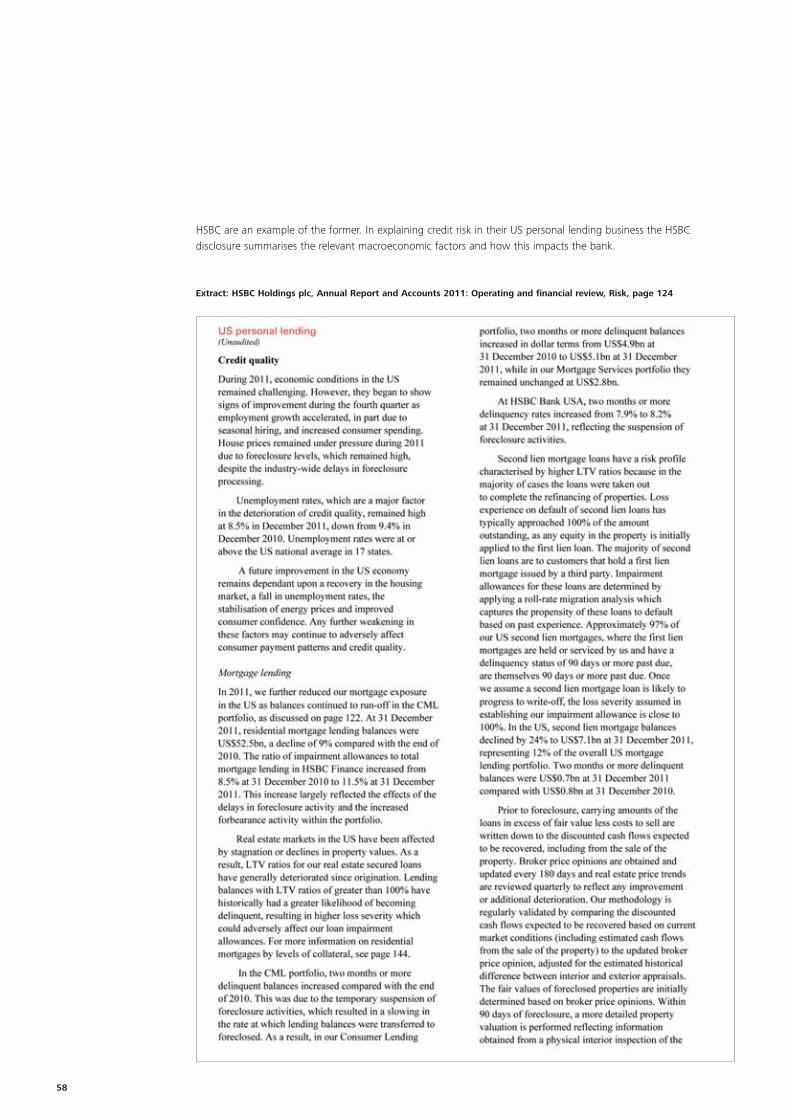

HSBC are an example of the former. In explaining credit risk in their US personal lending business the HSBCdisclosure summarises the relevant macroeconomic factors and how this impacts the bank.

Extract: HSBC Holdings plc, Annual Report and Accounts 2011: Operating and financial review, Risk, page 124

Review of banks’ annual reports 59

Santander adopt a more internal focus explaining their internal processes and management responses. An exampleis provided from the qualitative sections of the bank’s credit risk disclosure for their corporate banking business.

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, Credit risk,pages 103, 105 and 106

60

Extract: Santander UK plc 2011 Annual Report: Business and Financial Review, Risk Management Report, Credit risk, pages 103, 105and 106 (continued from previous page)

Review of banks’ annual reports 61

The disclosure of the management culture and approach to risk is less detailed than the disclosures of structures inplace to manage risk. Commercial sensitivities will mean certain disclosures and metrics are not provided however itis vital that investors and regulators comprehend the way this feeds into the operations of a bank’s strategy. There issome disclosure of the behavioural considerations in the banks surveyed but the detail varies.

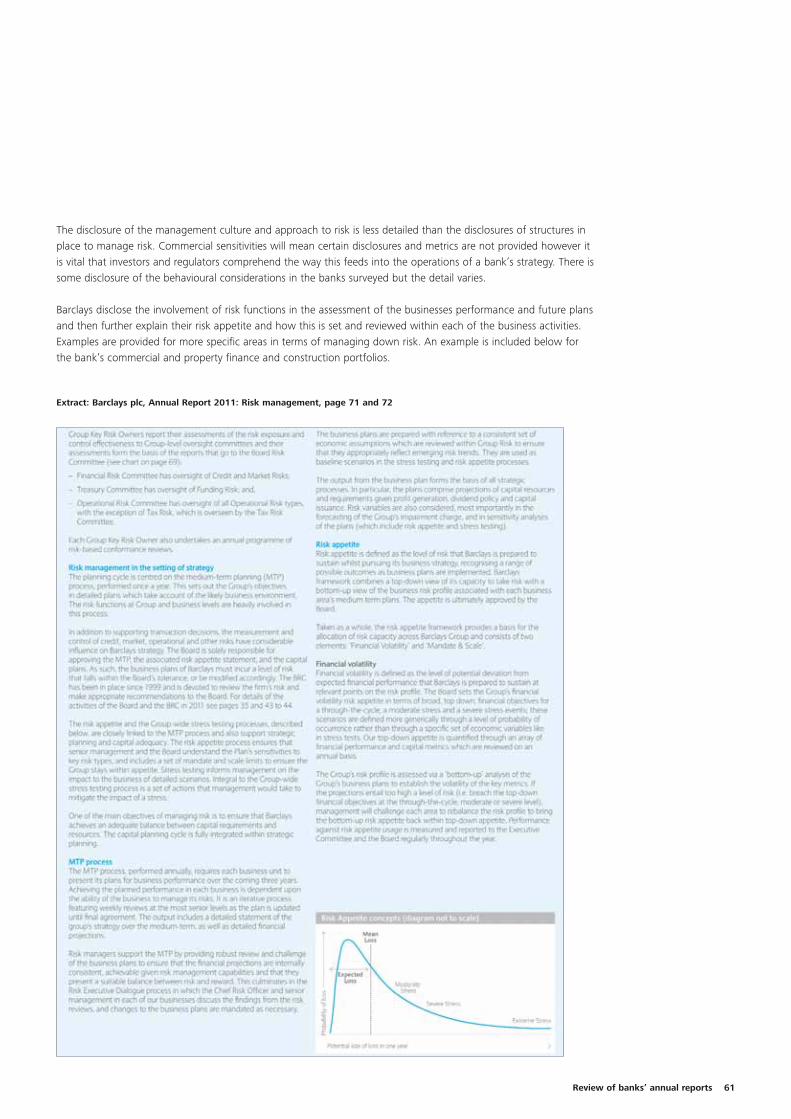

Barclays disclose the involvement of risk functions in the assessment of the businesses performance and future plansand then further explain their risk appetite and how this is set and reviewed within each of the business activities.Examples are provided for more specific areas in terms of managing down risk. An example is included below forthe bank’s commercial and property finance and construction portfolios.

Extract: Barclays plc, Annual Report 2011: Risk management, page 71 and 72

62

Extract: Barclays plc, Annual Report 2011: Risk management, page 71 and 72 (continued from previous page)

Review of banks’ annual reports 63

CommentThe quantum of bank risk information has increasedover the last few years and detailed risk disclosures readmore like a risk section in a prospectus but theinformation clearly highlights the risks faced by thebank and provides a good summary of what can gowrong for the organisation. The disclosures in respectof business strategy, risk profile and risk appetite willhelp a broad range of users understand better theinstitution’s business. However risk disclosure can be acomplex issue and it is inappropriate to prescribe astandard form or length because risk narratives shouldreflect the internal risk discussions that occur in eachbank, and these will differ from bank to bank. Furtherdisclosures will continue to evolve in the light ofinitiatives such as the FSB’s project to improve riskdisclosures in financial institutions and the Sharmanreport on going concern and liquidity risks. Futureevents are always likely to generate demands on banksto publish additional information to allow the market toassess their impact on an individual institution. Wherethis occurs it does not necessarily mean a deficiency inpast risk reporting but will probably reflect the inabilityto predict the future.

64

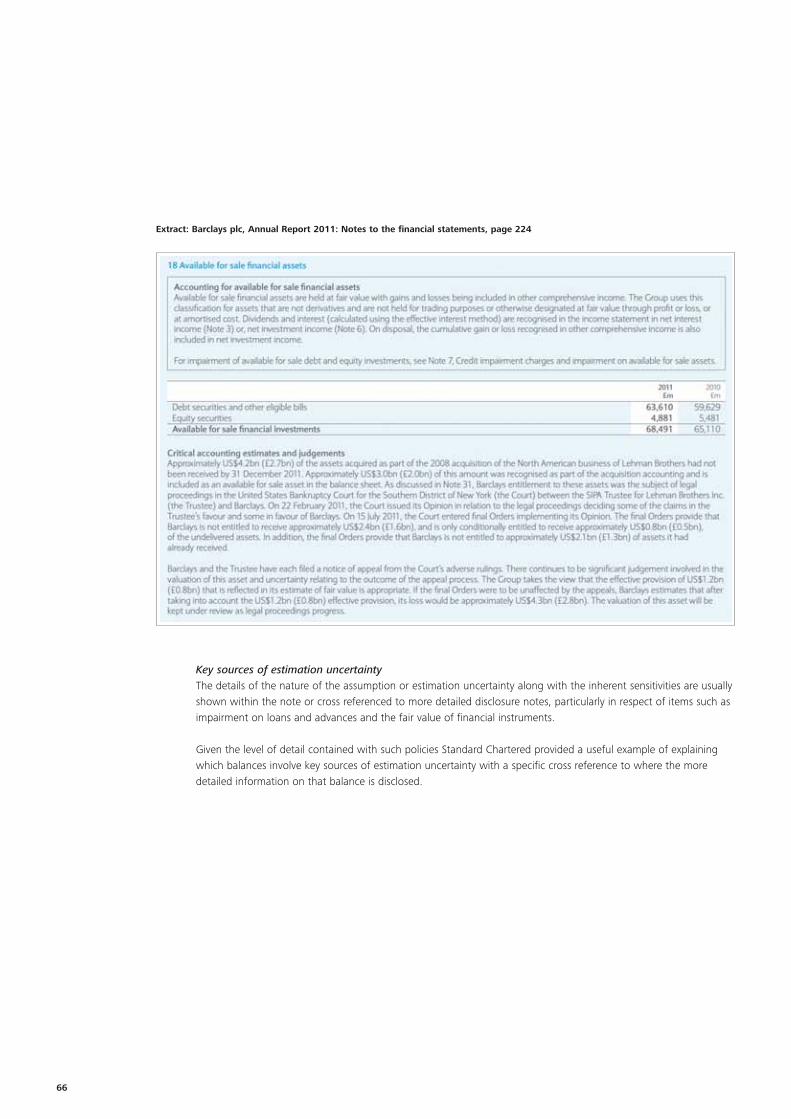

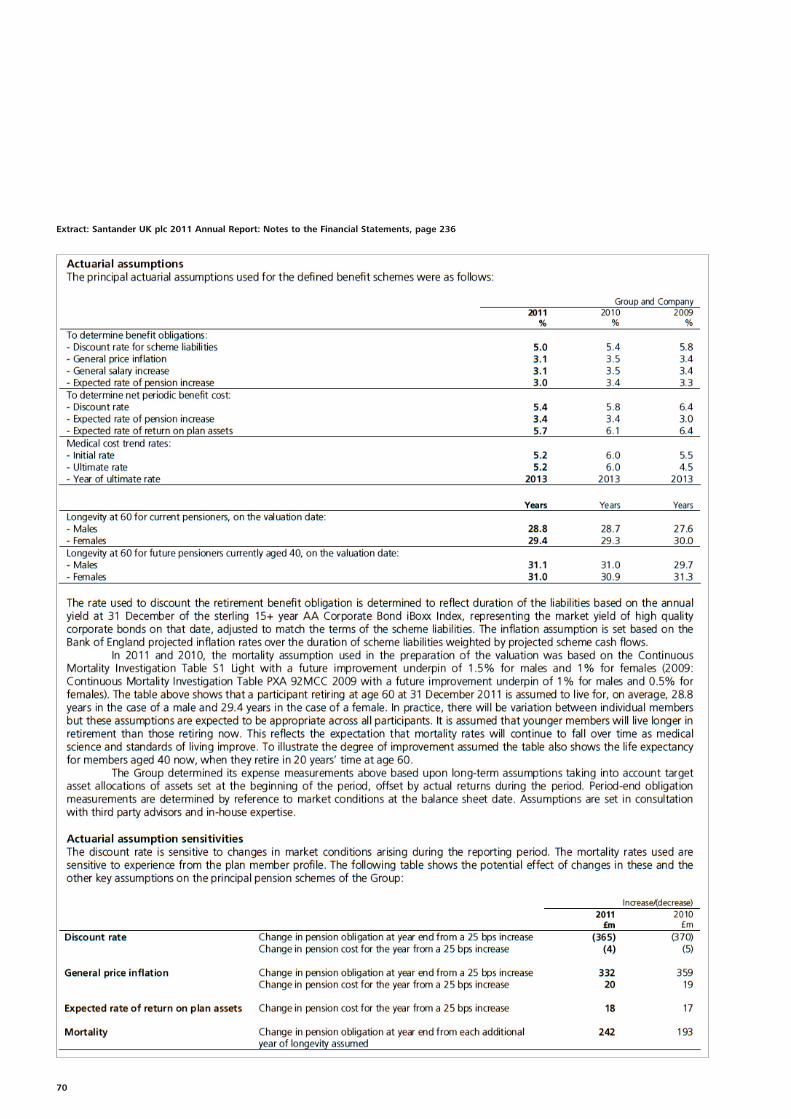

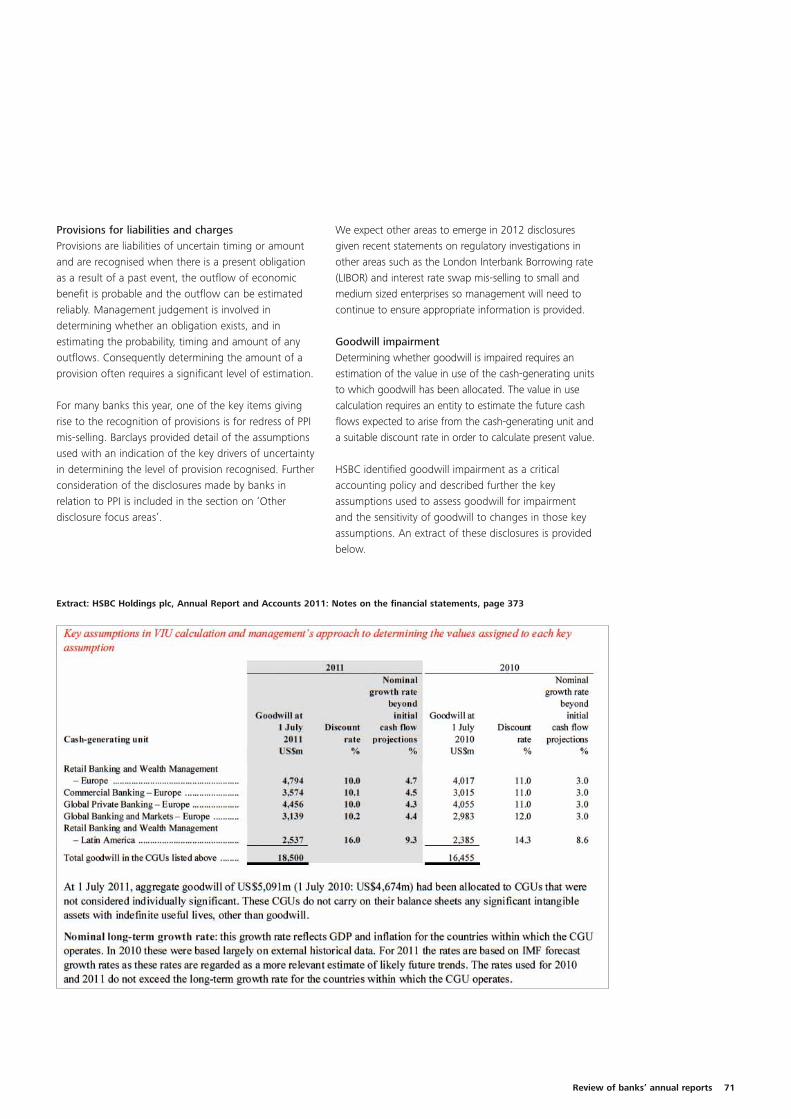

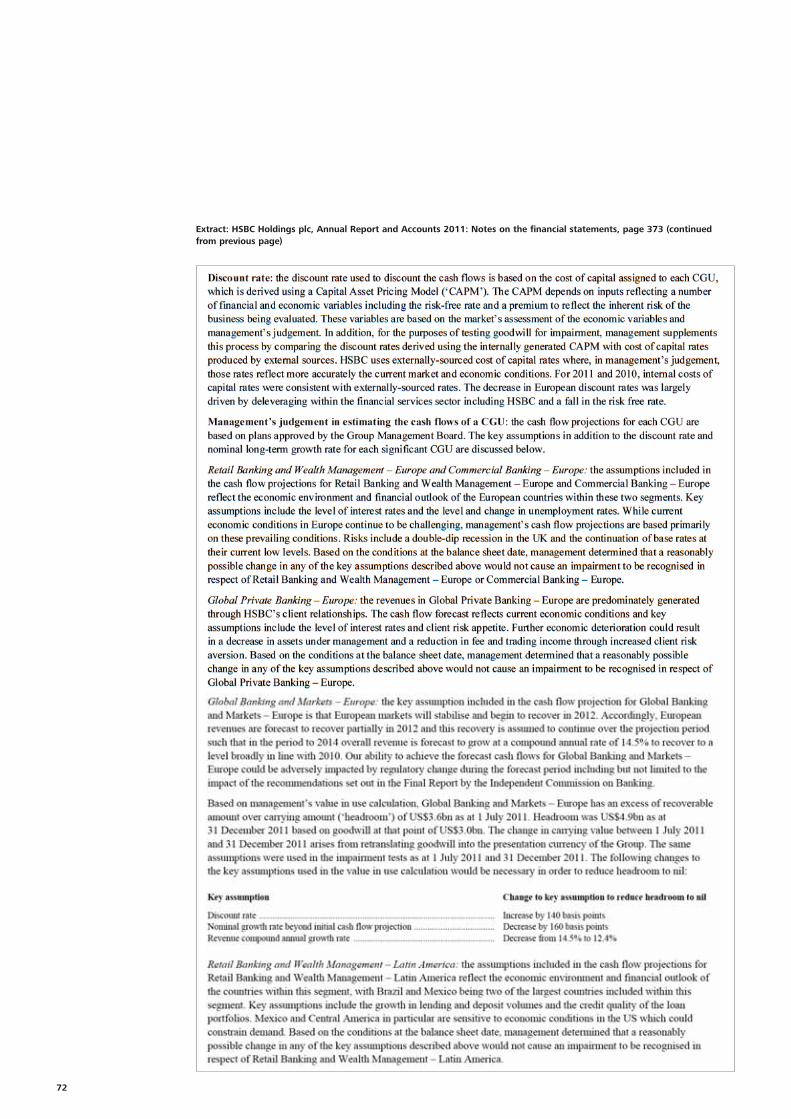

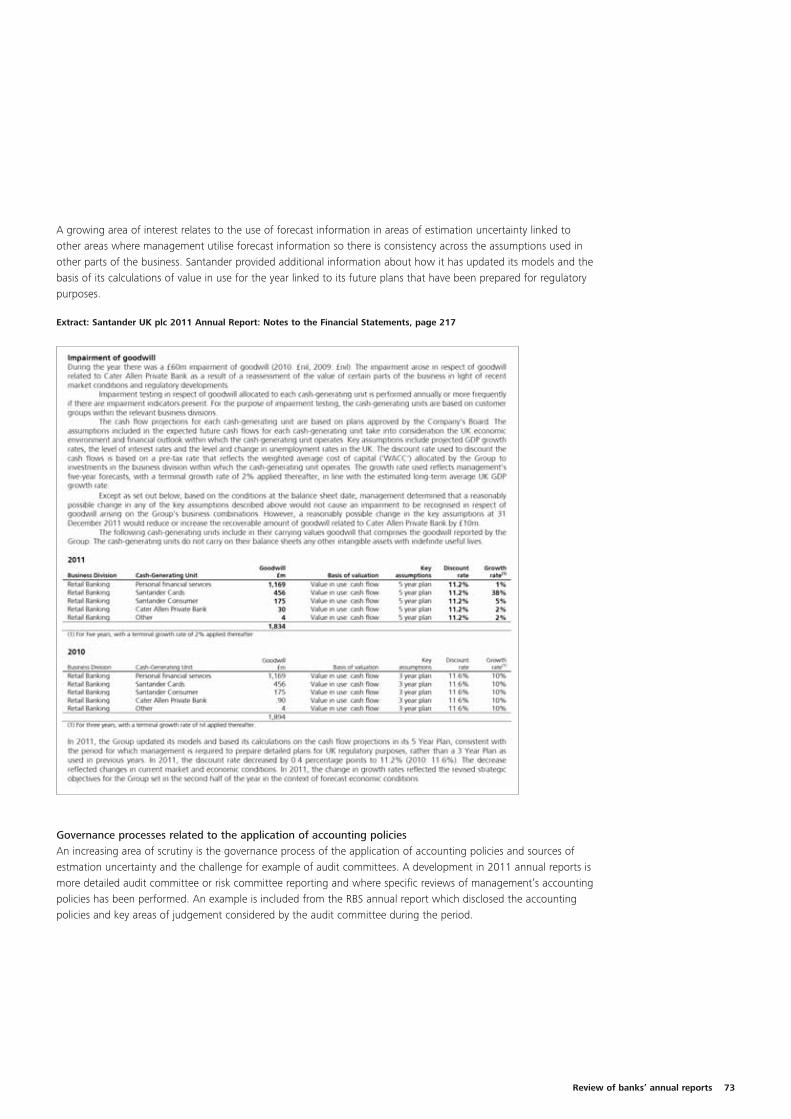

BackgroundThe disclosure of critical accounting policies and keysources of estimation uncertainty provides valuableinformation to users of financial statements. For banks,estimates and judgements in determining loanprovisioning, goodwill, financial instrument valuationadjustments and deferred tax can have a significantimpact on results. Therefore it is important that theusers of the accounts understand the judgementsmanagement has made in the application of certainaccounting policies.

The existing requirements for the disclosure of criticalaccounting policies and key sources of estimation arecontained within IAS 1 which requires:

• a summary of significant accounting policies or othernotes to disclose the judgements that managementhas made, in the process of applying the entity’saccounting policies that have the most significanteffect on the amounts recognised in the financialstatements (IAS 1:122).