low carbon economy

TRANSCRIPT

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

1

TOWARDS A LOW CARBON ECONOMY: RENEWABLES AND ENERGY EFFICIENCY IN SPAIN

Sofía MartínezInstitute for Diversification and Saving of Energy, IDAE(Ministry of Industry, Tourism and Trade)

Beyond Copenhagen: Climate Beyond Copenhagen: Climate

Change and Renewable Energies in Change and Renewable Energies in

Asia and EuropeAsia and Europe

China Europe International Business School China Europe International Business School

Shanghai, 28Shanghai, 28thth July 2010July 2010

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

2

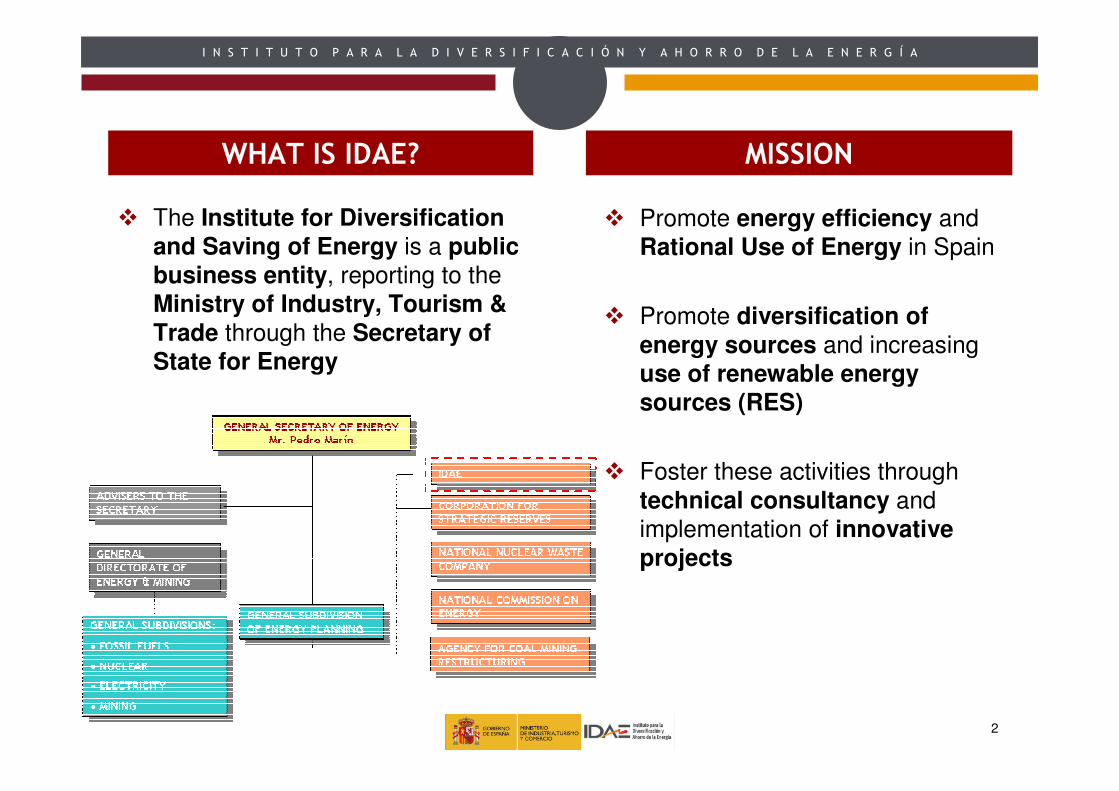

WHAT IS IDAE? MISSION

� Promote energy efficiency and

Rational Use of Energy in Spain

� Promote diversification of

energy sources and increasing

use of renewable energy

sources (RES)

� Foster these activities through

technical consultancy and

implementation of innovative

projects

� The Institute for Diversification and Saving of Energy is a public

business entity, reporting to the

Ministry of Industry, Tourism &

Trade through the Secretary of

State for Energy

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

3

ENERGY AND RENEWABLE ENERGY IN SPAINENERGY AND RENEWABLE ENERGY IN SPAIN

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

4

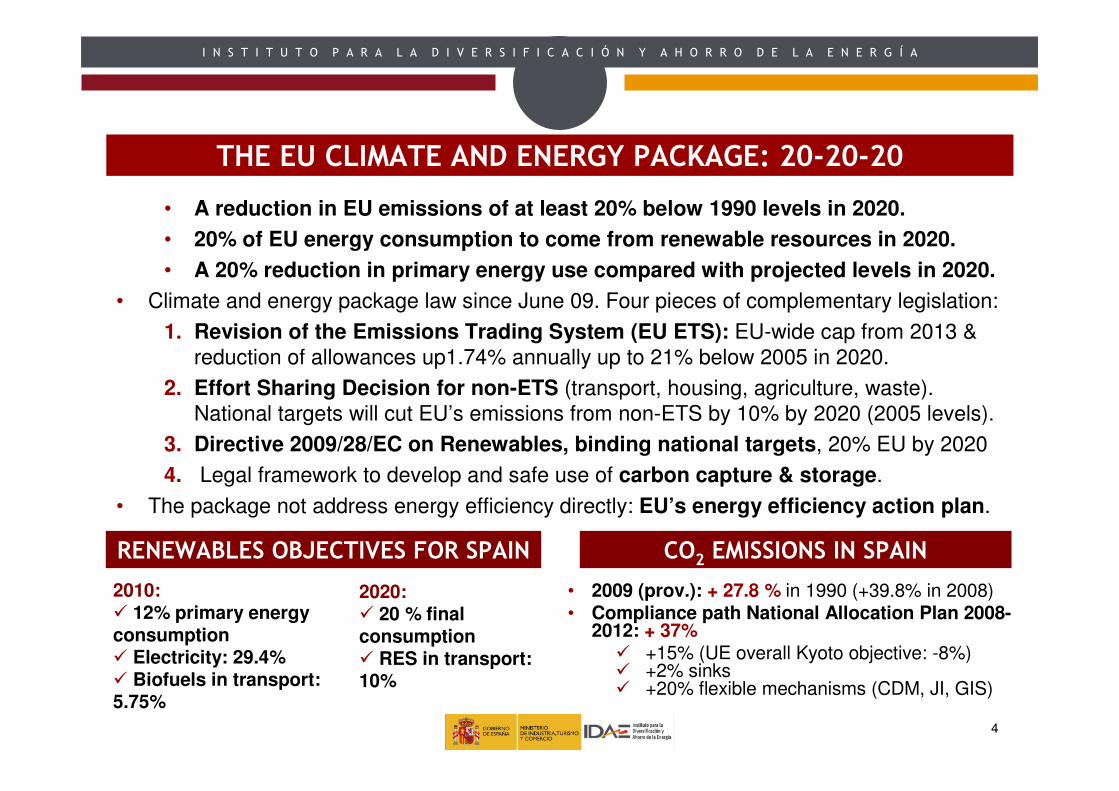

THE EU CLIMATE AND ENERGY PACKAGE: 20-20-20

• A reduction in EU emissions of at least 20% below 1990 levels in 2020.

• 20% of EU energy consumption to come from renewable resources in 2020.

• A 20% reduction in primary energy use compared with projected levels in 2020.

• Climate and energy package law since June 09. Four pieces of complementary legislation:

1. Revision of the Emissions Trading System (EU ETS): EU-wide cap from 2013 &

reduction of allowances up1.74% annually up to 21% below 2005 in 2020.

2. Effort Sharing Decision for non-ETS (transport, housing, agriculture, waste).

National targets will cut EU’s emissions from non-ETS by 10% by 2020 (2005 levels).

3. Directive 2009/28/EC on Renewables, binding national targets, 20% EU by 2020

4. Legal framework to develop and safe use of carbon capture & storage.

• The package not address energy efficiency directly: EU’s energy efficiency action plan.

CO2 EMISSIONS IN SPAIN

• 2009 (prov.): + 27.8 % in 1990 (+39.8% in 2008)• Compliance path National Allocation Plan 2008-

2012: + 37%� +15% (UE overall Kyoto objective: -8%)� +2% sinks� +20% flexible mechanisms (CDM, JI, GIS)

2020:� 20 % final consumption� RES in transport: 10%

2010:� 12% primary energy consumption� Electricity: 29.4%� Biofuels in transport: 5.75%

RENEWABLES OBJECTIVES FOR SPAIN

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

5

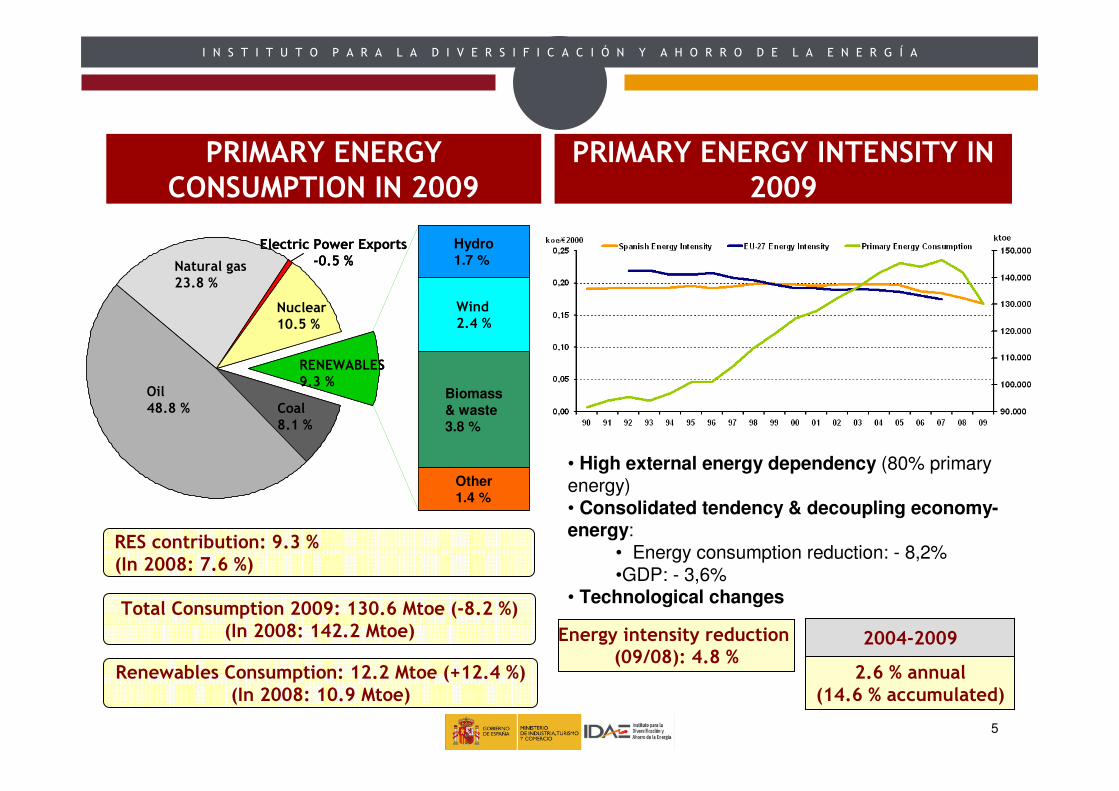

Total Consumption 2009: 130.6 Mtoe (-8.2 %)(In 2008: 142.2 Mtoe)

Renewables Consumption: 12.2 Mtoe (+12.4 %)(In 2008: 10.9 Mtoe)

RES contribution: 9.3 %(In 2008: 7.6 %)

Hydro1.7 %

Wind2.4 %

Biomass & waste3.8 %

Other1.4 %

Electric Power Exports-0.5 %

Nuclear10.5 %

Coal 8.1 %

Oil48.8 %

RENEWABLES9.3 %

Natural gas23.8 %

Hydro1.7 %

Wind2.4 %

Biomass & waste3.8 %

Other1.4 %

Electric Power Exports-0.5 %

Nuclear10.5 %

Coal 8.1 %

Oil48.8 %

RENEWABLES9.3 %

Natural gas23.8 %

Energy intensity reduction (09/08): 4.8 %

2.6 % annual(14.6 % accumulated)

2004-2009

PRIMARY ENERGY CONSUMPTION IN 2009

• High external energy dependency (80% primary energy)• Consolidated tendency & decoupling economy-energy:

• Energy consumption reduction: - 8,2%•GDP: - 3,6%

• Technological changes

PRIMARY ENERGY INTENSITY IN 2009

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

6

RES CONTRIBUTION TO ELECTRICITY PRODUCTION in 2009

Coal 12.61%Nuclear 17.78%

PV 2.04%

Natural Gas 37.23%

Biomass 1.28%

Pumping 0.95%Oil 6.87%

CSP 0.03%

RENEWABLES24.6%

Hydro 8.85%

Wind 12.35%

RES production: 72.8 TWh(Total: 296.5 TWh)

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

7

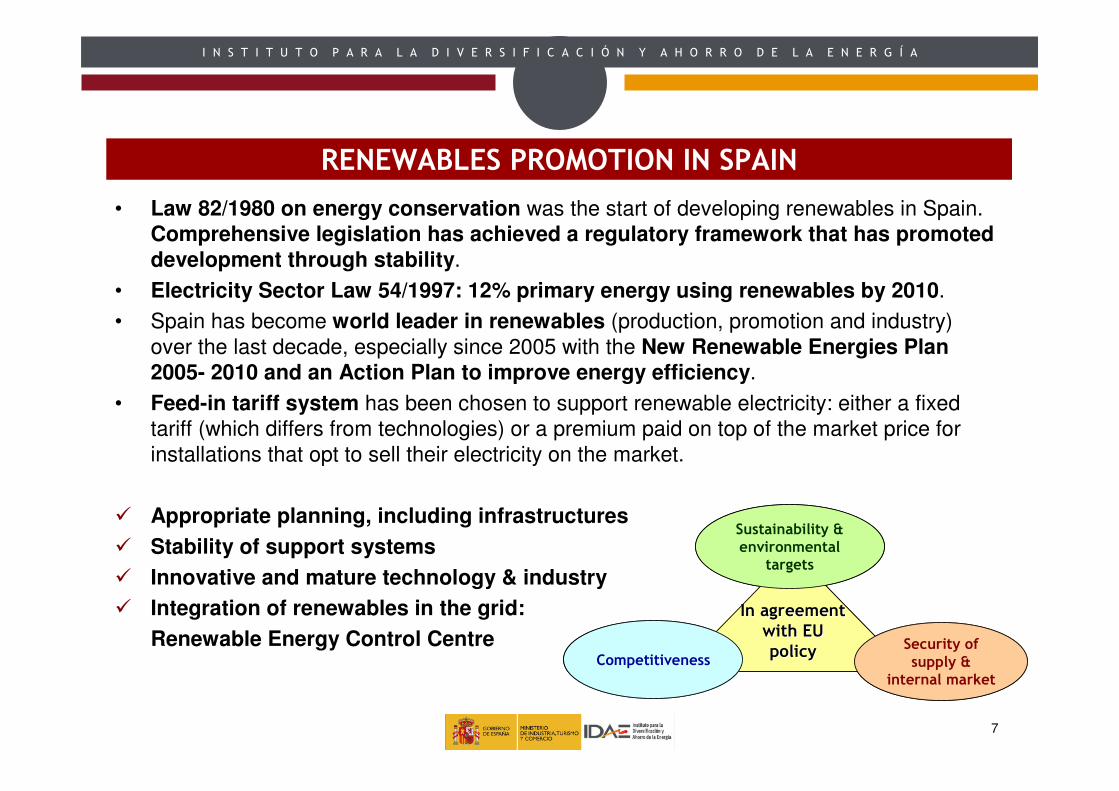

RENEWABLES PROMOTION IN SPAIN

• Law 82/1980 on energy conservation was the start of developing renewables in Spain.

Comprehensive legislation has achieved a regulatory framework that has promoted

development through stability.

• Electricity Sector Law 54/1997: 12% primary energy using renewables by 2010.

• Spain has become world leader in renewables (production, promotion and industry)

over the last decade, especially since 2005 with the New Renewable Energies Plan

2005- 2010 and an Action Plan to improve energy efficiency.

• Feed-in tariff system has been chosen to support renewable electricity: either a fixed

tariff (which differs from technologies) or a premium paid on top of the market price for

installations that opt to sell their electricity on the market.

� Appropriate planning, including infrastructures

� Stability of support systems

� Innovative and mature technology & industry

� Integration of renewables in the grid:

Renewable Energy Control Centre

In agreement In agreement

with EU with EU

policypolicy

Sustainability & environmental

targets

Security of supply &

internal market

Competitiveness

In agreement In agreement

with EU with EU

policypolicy

Sustainability & environmental

targets

Security of supply &

internal market

Competitiveness

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

8

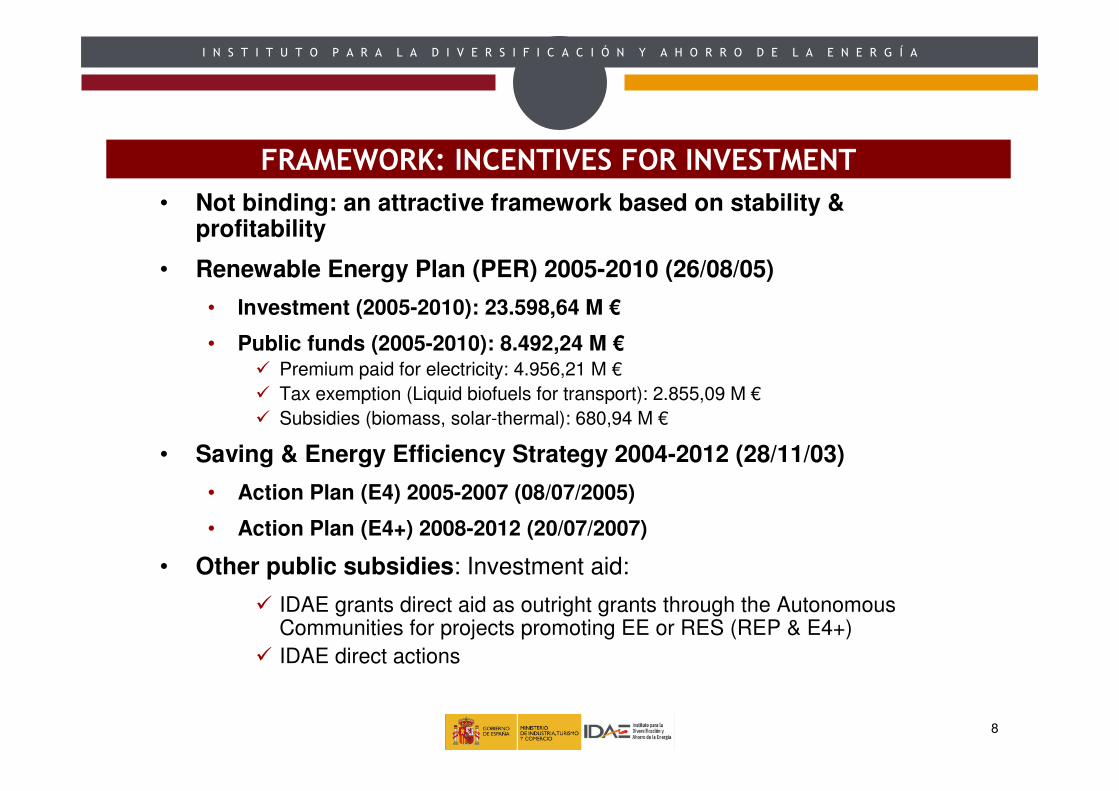

FRAMEWORK: INCENTIVES FOR INVESTMENT

• Not binding: an attractive framework based on stability & profitability

• Renewable Energy Plan (PER) 2005-2010 (26/08/05)

• Investment (2005-2010): 23.598,64 M €

• Public funds (2005-2010): 8.492,24 M €� Premium paid for electricity: 4.956,21 M €

� Tax exemption (Liquid biofuels for transport): 2.855,09 M €

� Subsidies (biomass, solar-thermal): 680,94 M €

• Saving & Energy Efficiency Strategy 2004-2012 (28/11/03)

• Action Plan (E4) 2005-2007 (08/07/2005)

• Action Plan (E4+) 2008-2012 (20/07/2007)

• Other public subsidies: Investment aid:

� IDAE grants direct aid as outright grants through the AutonomousCommunities for projects promoting EE or RES (REP & E4+)

� IDAE direct actions

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

9

RES ELECTRICITYAccumulated power (MW)

Installed annual Power (MW)

41.981 MW

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

45.000

19901991199219931994199519961997199819992000200120022003200420052006200720082009

0

890

1.780

2.670

3.560

4.450

5.340

6.230

7.120

8.010

REP23.420 MW

Installed annual power (MWth)

Accumulated power (MWth)

20.000

20.500

21.000

21.500

22.000

22.500

23.000

23.500

24.000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 20090

150

300

450

600

750

900

1.050

1.200

REP

RES THERMAL

• Spain in UE (installed capacity)

• 1st in thermoelectric; 2nd in wind and PV; 3rd in mini-hydro

• Employment: 109.368

• RES grid integration: overcoming planning

hurdles, sharing costs, accessing equipment…

• Renewable Energy Source Control Centre (CECRE), worldwide pioneering initiative to monitor and control RES

• In 2009: 2.700 MWe & 400 MWt

• Significant increases: wind, CSP and

biofuels

• Constant increase: achieving 2010

targets.

• New REP in 2011

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

10

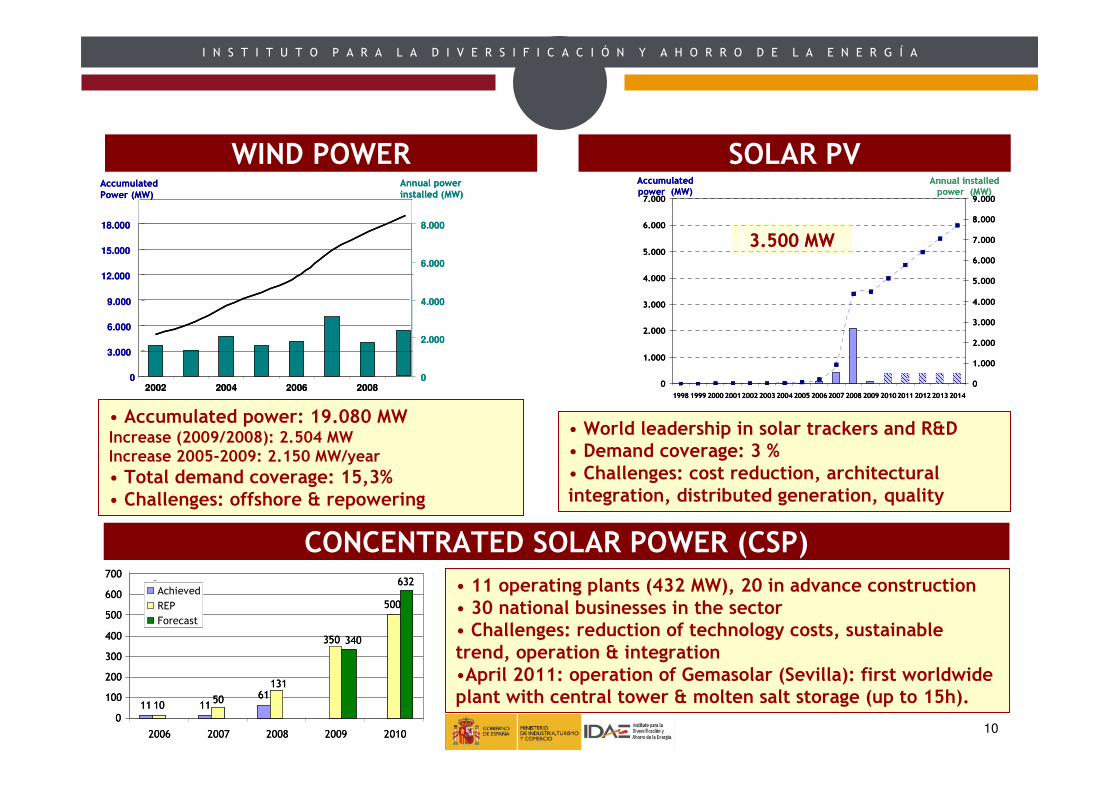

WIND POWER

• Accumulated power: 19.080 MWIncrease (2009/2008): 2.504 MWIncrease 2005-2009: 2.150 MW/year

• Total demand coverage: 15,3%• Challenges: offshore & repowering

Annual power installed (MW)

0

3.000

6.000

9.000

12.000

15.000

18.000

2002 2004 2006 2008

Accumulated

Power (MW)

0

2.000

4.000

6.000

8.000

Annual power installed (MW)

0

3.000

6.000

9.000

12.000

15.000

18.000

2002 2004 2006 2008

Accumulated

Power (MW)

0

2.000

4.000

6.000

8.000

Annual installed power (MW)

Accumulated power (MW)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

19981999200020012002200320042005200620072008200920102011201220132014

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

3.500 MW

Annual installed power (MW)

Accumulated power (MW)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

19981999200020012002200320042005200620072008200920102011201220132014

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

9.000

3.500 MW

SOLAR PV

• World leadership in solar trackers and R&D• Demand coverage: 3 % • Challenges: cost reduction, architectural integration, distributed generation, quality

11 1161

1050

131

350

500

340

632

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010

MW

Achieved

REP

Forecast

11 1161

1050

131

350

500

340

632

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010

MW

Achieved

REP

Forecast

CONCENTRATED SOLAR POWER (CSP)

• 11 operating plants (432 MW), 20 in advance construction • 30 national businesses in the sector • Challenges: reduction of technology costs, sustainable trend, operation & integration•April 2011: operation of Gemasolar (Sevilla): first worldwide plant with central tower & molten salt storage (up to 15h).

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

11

1.953.963 m2

Annual surfaceinstalled (m2)

Accumulatedsurface (m2)

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

)

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

1.000.000

1.953.963 m2

Annual surfaceinstalled (m2)

Accumulatedsurface (m2)

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

)

0

100.000

200.000

300.000

400.000

500.000

600.000

700.000

800.000

900.000

1.000.000

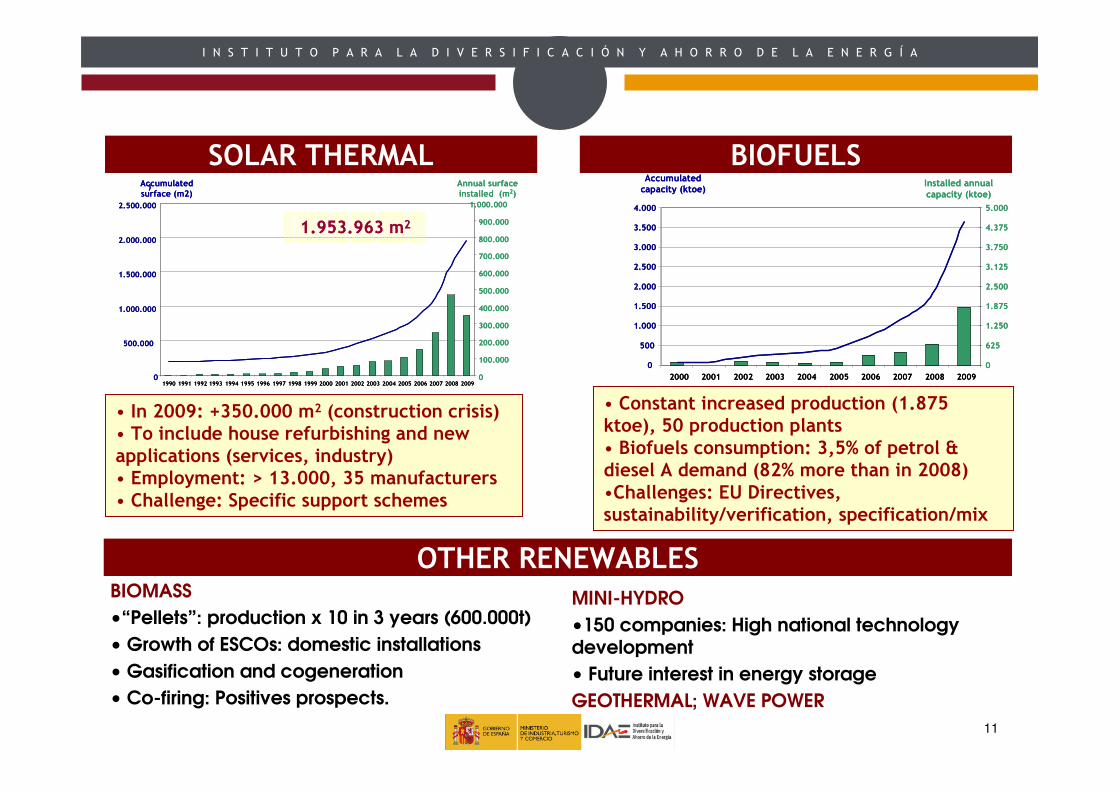

SOLAR THERMAL

• In 2009: +350.000 m2 (construction crisis) • To include house refurbishing and new applications (services, industry)• Employment: > 13.000, 35 manufacturers• Challenge: Specific support schemes

Accumulatedcapacity (ktoe)

Installed annualcapacity (ktoe)

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0

625

1.250

1.875

2.500

3.125

3.750

4.375

5.000

Accumulatedcapacity (ktoe)

Installed annualcapacity (ktoe)

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0

625

1.250

1.875

2.500

3.125

3.750

4.375

5.000

• Constant increased production (1.875 ktoe), 50 production plants• Biofuels consumption: 3,5% of petrol & diesel A demand (82% more than in 2008)•Challenges: EU Directives, sustainability/verification, specification/mix

BIOFUELS

OTHER RENEWABLESBIOMASS

•“Pellets”: production x 10 in 3 years (600.000t)

• Growth of ESCOs: domestic installations

• Gasification and cogeneration

• Co-firing: Positives prospects.

MINI-HYDRO

•150 companies: High national technology development

• Future interest in energy storage

GEOTHERMAL; WAVE POWER

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

12

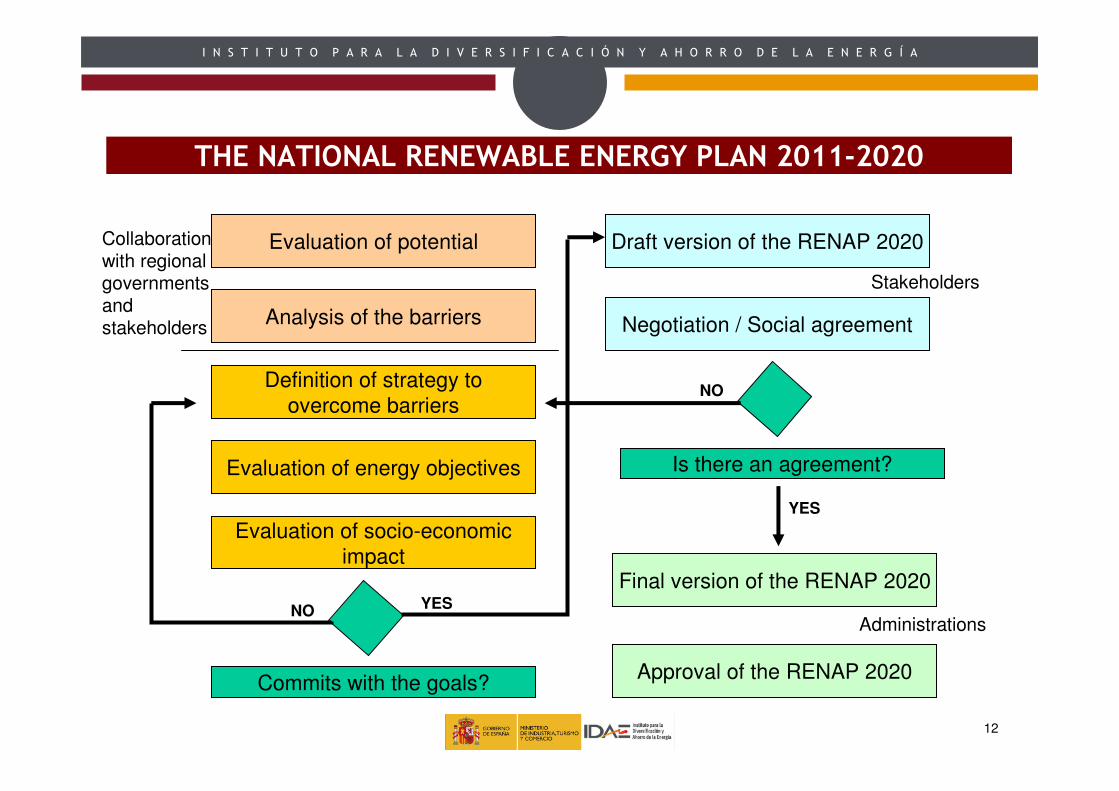

THE NATIONAL RENEWABLE ENERGY PLAN 2011-2020

Evaluation of potential

Analysis of the barriers

Definition of strategy to

overcome barriers

Evaluation of energy objectives

Evaluation of socio-economic

impact

Commits with the goals?

NO

Collaboration with regional governments and stakeholders

Draft version of the RENAP 2020

Negotiation / Social agreement

Is there an agreement?

NO

Approval of the RENAP 2020

Final version of the RENAP 2020YES

YES

Stakeholders

Administrations

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

13

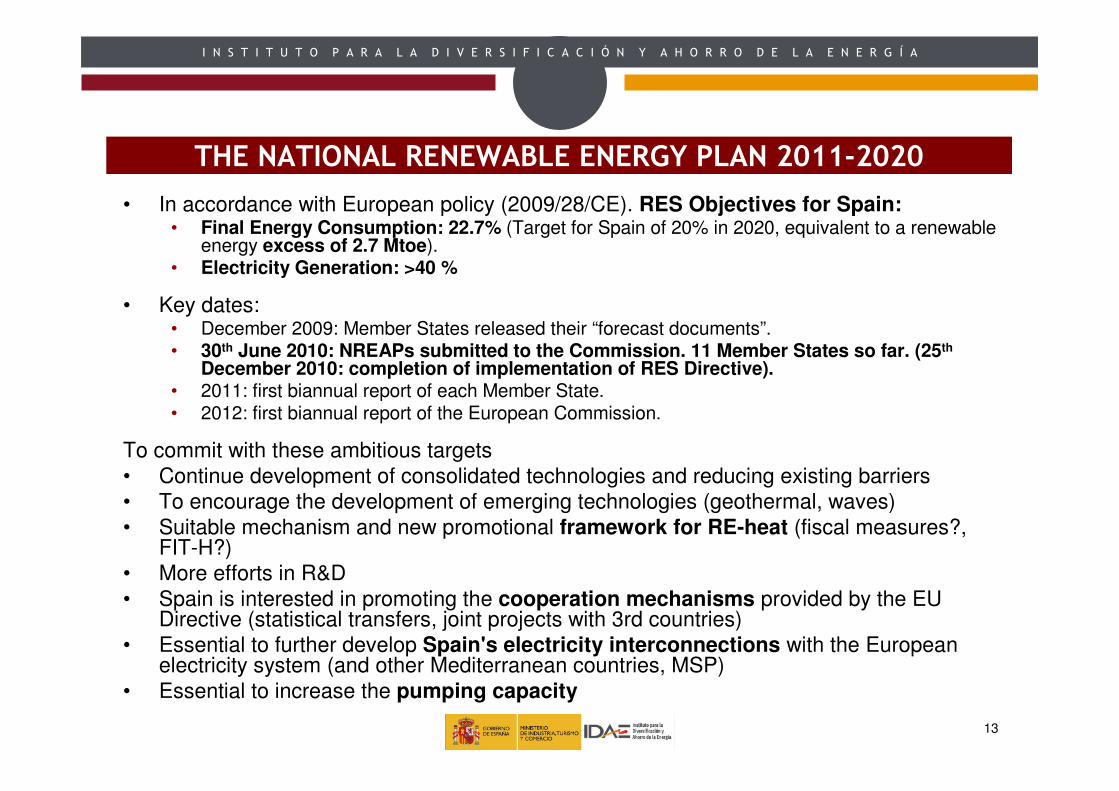

THE NATIONAL RENEWABLE ENERGY PLAN 2011-2020

• In accordance with European policy (2009/28/CE). RES Objectives for Spain: • Final Energy Consumption: 22.7% (Target for Spain of 20% in 2020, equivalent to a renewable

energy excess of 2.7 Mtoe).• Electricity Generation: >40 %

• Key dates:• December 2009: Member States released their “forecast documents”.• 30th June 2010: NREAPs submitted to the Commission. 11 Member States so far. (25th

December 2010: completion of implementation of RES Directive).• 2011: first biannual report of each Member State.• 2012: first biannual report of the European Commission.

To commit with these ambitious targets

• Continue development of consolidated technologies and reducing existing barriers

• To encourage the development of emerging technologies (geothermal, waves)

• Suitable mechanism and new promotional framework for RE-heat (fiscal measures?, FIT-H?)

• More efforts in R&D

• Spain is interested in promoting the cooperation mechanisms provided by the EU Directive (statistical transfers, joint projects with 3rd countries)

• Essential to further develop Spain's electricity interconnections with the European electricity system (and other Mediterranean countries, MSP)

• Essential to increase the pumping capacity

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

14

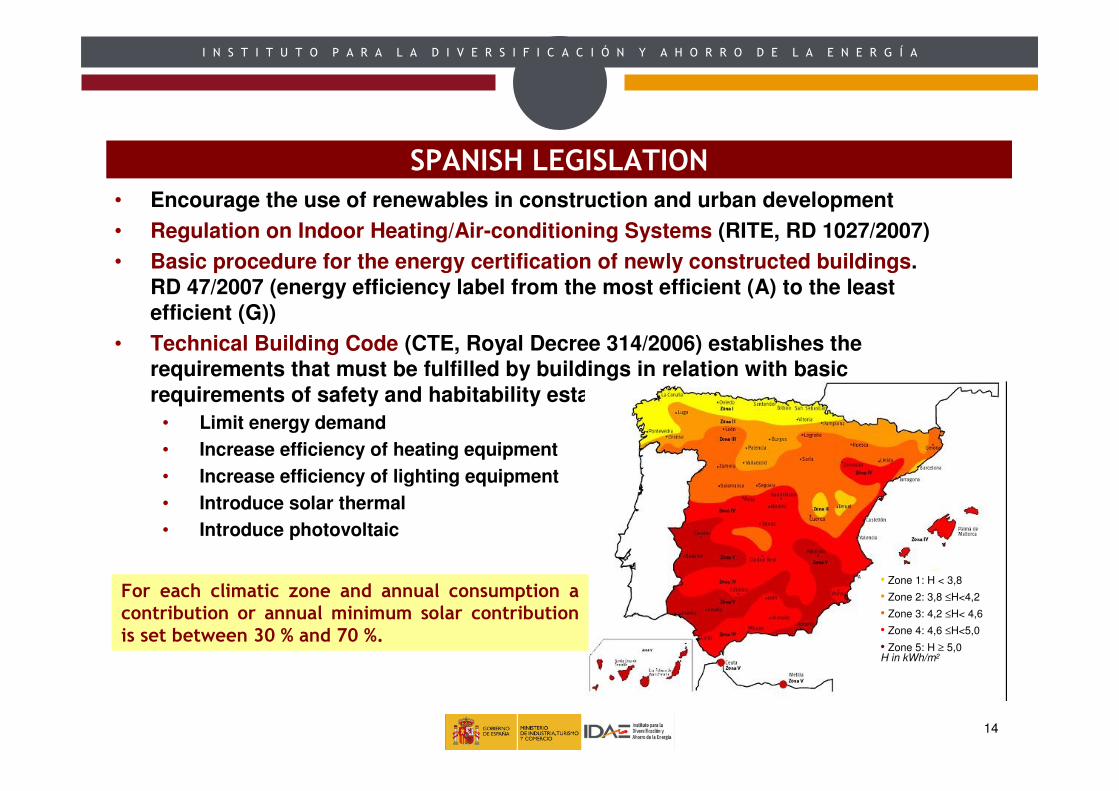

SPANISH LEGISLATION

• Encourage the use of renewables in construction and urban development

• Regulation on Indoor Heating/Air-conditioning Systems (RITE, RD 1027/2007)

• Basic procedure for the energy certification of newly constructed buildings.

RD 47/2007 (energy efficiency label from the most efficient (A) to the least

efficient (G))

• Technical Building Code (CTE, Royal Decree 314/2006) establishes the

requirements that must be fulfilled by buildings in relation with basic

requirements of safety and habitability established in the Law of Buildings.

• Limit energy demand

• Increase efficiency of heating equipment

• Increase efficiency of lighting equipment

• Introduce solar thermal

• Introduce photovoltaic

• Zone 1: H < 3,8

• Zone 2: 3,8 ≤H<4,2

• Zone 3: 4,2 ≤H< 4,6

• Zone 4: 4,6 ≤H<5,0

• Zone 5: H ≥ 5,0 H in kWh/m2

For each climatic zone and annual consumption a contribution or annual minimum solar contribution is set between 30 % and 70 %.

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

15

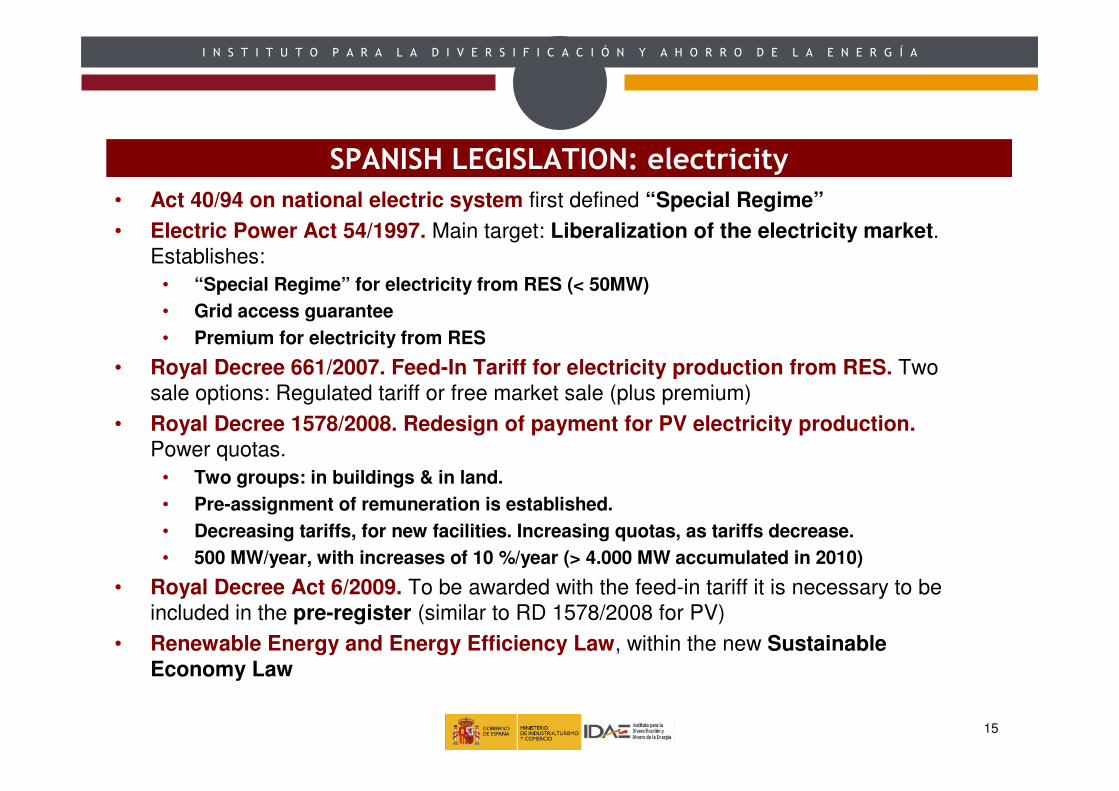

SPANISH LEGISLATION: electricity

• Act 40/94 on national electric system first defined “Special Regime”

• Electric Power Act 54/1997. Main target: Liberalization of the electricity market.

Establishes:

• “Special Regime” for electricity from RES (< 50MW)

• Grid access guarantee

• Premium for electricity from RES

• Royal Decree 661/2007. Feed-In Tariff for electricity production from RES. Two

sale options: Regulated tariff or free market sale (plus premium)

• Royal Decree 1578/2008. Redesign of payment for PV electricity production.

Power quotas.

• Two groups: in buildings & in land.

• Pre-assignment of remuneration is established.

• Decreasing tariffs, for new facilities. Increasing quotas, as tariffs decrease.

• 500 MW/year, with increases of 10 %/year (> 4.000 MW accumulated in 2010)

• Royal Decree Act 6/2009. To be awarded with the feed-in tariff it is necessary to be

included in the pre-register (similar to RD 1578/2008 for PV)

• Renewable Energy and Energy Efficiency Law, within the new Sustainable

Economy Law

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

16

http://www.renovablesmadeinspain.es/

RENEWABLES MADE IN SPAIN

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

17

ENERGY EFFICIENCY IN SPAINENERGY EFFICIENCY IN SPAIN

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

18

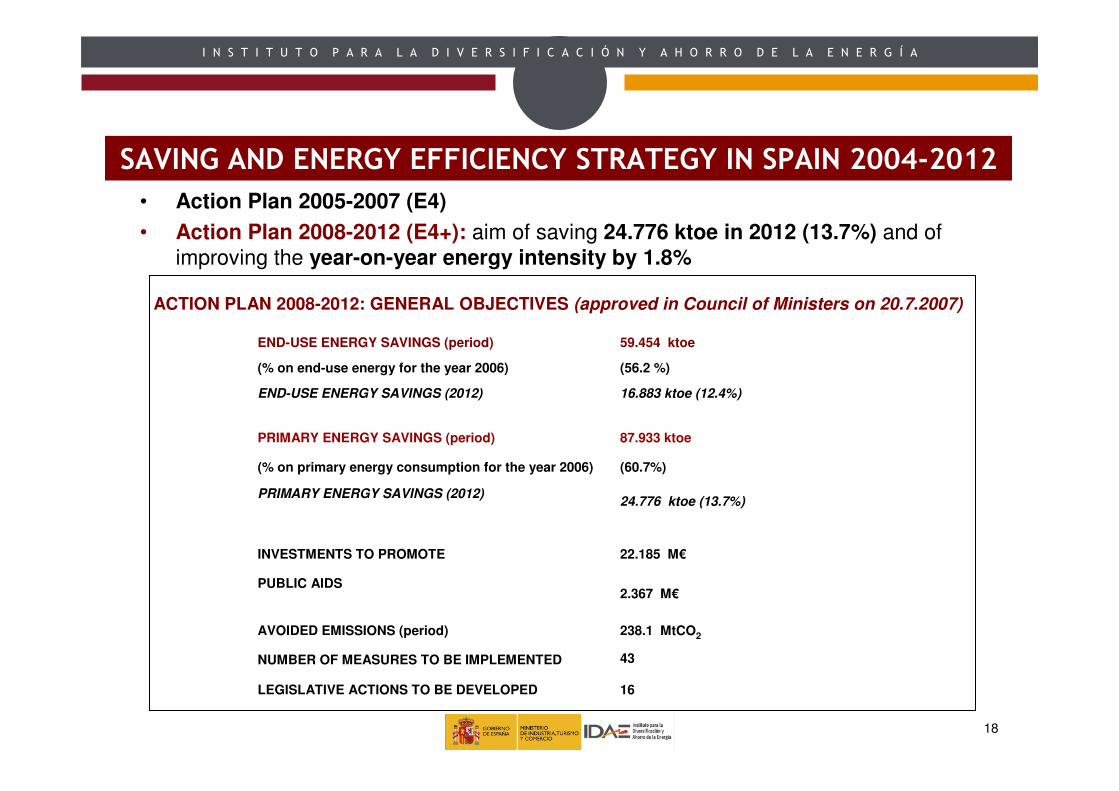

SAVING AND ENERGY EFFICIENCY STRATEGY IN SPAIN 2004-2012

• Action Plan 2005-2007 (E4)

• Action Plan 2008-2012 (E4+): aim of saving 24.776 ktoe in 2012 (13.7%) and of

improving the year-on-year energy intensity by 1.8%

43NUMBER OF MEASURES TO BE IMPLEMENTED

238.1 MtCO2AVOIDED EMISSIONS (period)

16LEGISLATIVE ACTIONS TO BE DEVELOPED

2.367 M€PUBLIC AIDS

22.185 M€INVESTMENTS TO PROMOTE

24.776 ktoe (13.7%)PRIMARY ENERGY SAVINGS (2012)

(60.7%)(% on primary energy consumption for the year 2006)

87.933 ktoePRIMARY ENERGY SAVINGS (period)

16.883 ktoe (12.4%)END-USE ENERGY SAVINGS (2012)

(56.2 %)(% on end-use energy for the year 2006)

59.454 ktoeEND-USE ENERGY SAVINGS (period)

ACTION PLAN 2008-2012: GENERAL OBJECTIVES (approved in Council of Ministers on 20.7.2007)

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

19

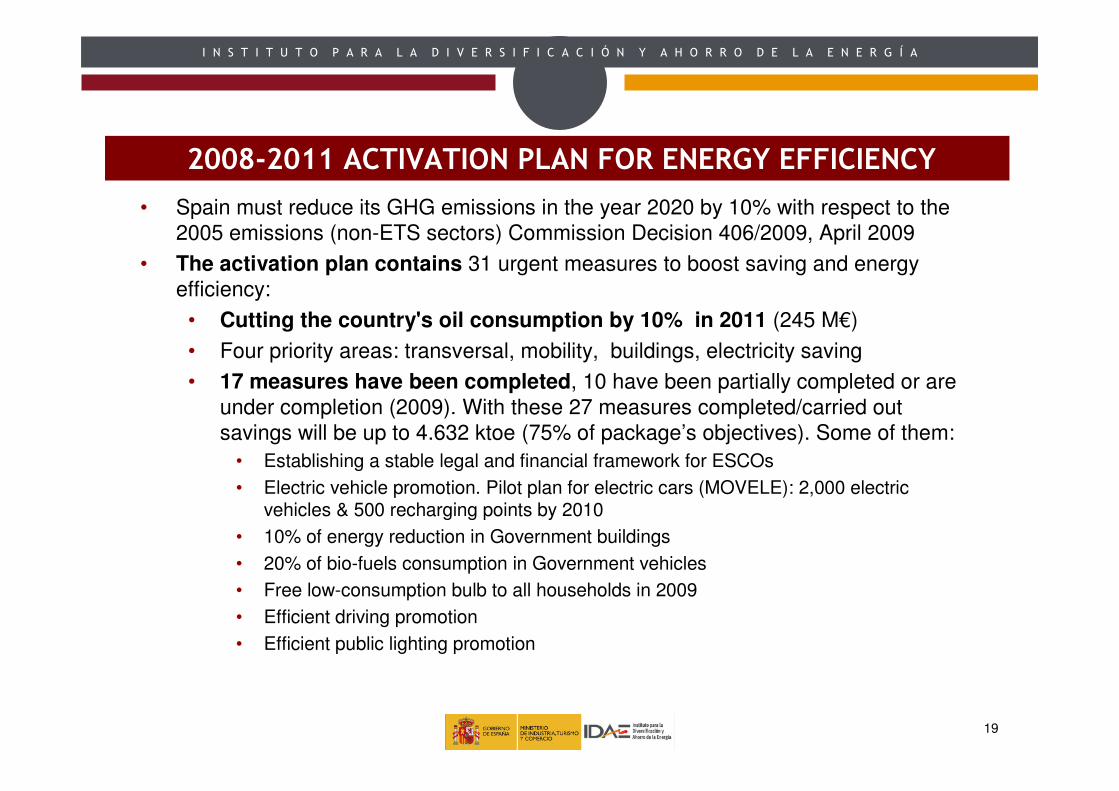

2008-2011 ACTIVATION PLAN FOR ENERGY EFFICIENCY

• Spain must reduce its GHG emissions in the year 2020 by 10% with respect to the

2005 emissions (non-ETS sectors) Commission Decision 406/2009, April 2009

• The activation plan contains 31 urgent measures to boost saving and energy

efficiency:

• Cutting the country's oil consumption by 10% in 2011 (245 M€)

• Four priority areas: transversal, mobility, buildings, electricity saving

• 17 measures have been completed, 10 have been partially completed or are

under completion (2009). With these 27 measures completed/carried out

savings will be up to 4.632 ktoe (75% of package’s objectives). Some of them:

• Establishing a stable legal and financial framework for ESCOs

• Electric vehicle promotion. Pilot plan for electric cars (MOVELE): 2,000 electric vehicles & 500 recharging points by 2010

• 10% of energy reduction in Government buildings

• 20% of bio-fuels consumption in Government vehicles

• Free low-consumption bulb to all households in 2009

• Efficient driving promotion

• Efficient public lighting promotion

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

20

SECTORIAL APPLICATION OF PUBLIC RESOURCES

PUBLIC SERVICES

3.8%

ENERGY TRANSFORM.

1.2% COMMUNICATION

1.7%

AGRICULTURE4.0%

TRANSPORT

17.3%

INDUSTRY

15.6%

BUILDINGS

34.0%

HOME & OFF, AUT. EQUIPMENT

22.5%

PUBLIC SERVICES

3.8%

ENERGY TRANSFORM.

1.2% COMMUNICATION

1.7%

AGRICULTURE4.0%

TRANSPORT

17.3%

INDUSTRY

15.6%

BUILDINGS

34.0%

HOME & OFF, AUT. EQUIPMENT

22.5%

ORIGIN OF PUBLIC FUNDS

ELECTRICITYSECTOR

58.3%

GAS SECTOR

12.0%STATE BUDGET

10.1%

ERDF NATIONAL

TRANCHE

2.7%

REG GOV. (OWN RESOURCES

AND ERDF

REGIONAL TRANCHE)

16.9%

ELECTRICITYSECTOR

58.3%

GAS SECTOR

12.0%STATE BUDGET

10.1%

ERDF NATIONAL

TRANCHE

2.7%

REG GOV. (OWN RESOURCES

AND ERDF

REGIONAL TRANCHE)

16.9%

ELECTRICITYSECTOR

58.3%

GAS SECTOR

12.0%STATE BUDGET

10.1%

ERDF NATIONAL

TRANCHE

2.7%

REG GOV. (OWN RESOURCES

AND ERDF

REGIONAL TRANCHE)

16.9%

National Budget = 35.0 M€

TARIFF (electricity) = 275.9 M€

TARIFF (gas) = 57.0 M€

TOTAL ANNUAL BUDGET= 367.9 M€

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

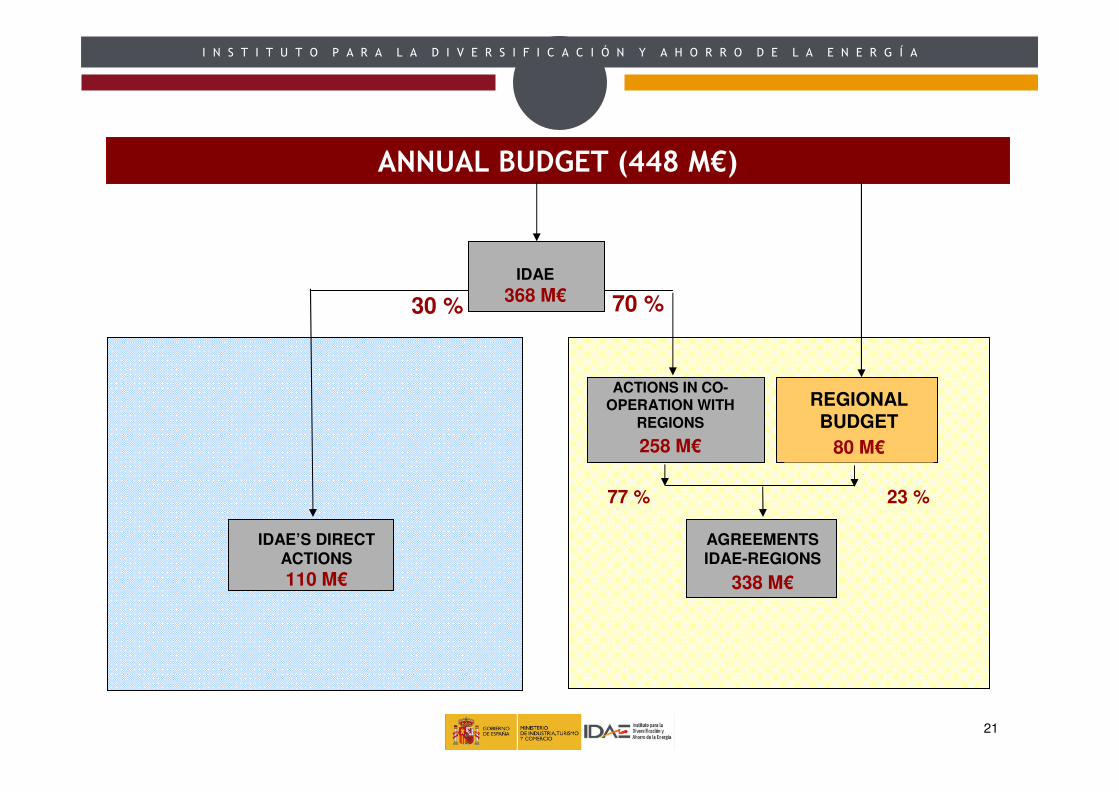

21

IDAE’S DIRECT ACTIONS

110 M€

ACTIONS IN CO-OPERATION WITH

REGIONS

258 M€

ANNUAL BUDGET (448 M€)

REGIONAL BUDGET

80 M€

IDAE

368 M€30 % 70 %

77 % 23 %

AGREEMENTS IDAE-REGIONS

338 M€

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

22

2010 PERSPECTIVES IN ENERGY EFFICIENCY

• Improving energy efficiency ≈ 1.5%

• Strategy to promote electric vehicle: 250.000 electric vehicles in 2014.

• Public support: 590 M€

• Development of the Activation plan for energy Saving and efficiency in public

buildings: IDAE has drawn up a standard contract for integrated energy and

maintenance services for publicly owned buildings (ESCOs)

• Promotion of ESCOs in regions and cities

• Continuity of Saving and Energy Efficiency Strategy in Spain and its Action Plans

• Review of the Technical Building Code: boost for building rehabilitation

• New Directive on energy efficiency in buildings

• Sustainable Economy Act:

• Renewable energy law

• Energy efficiency in buildings: housing rehabilitation versus energy rehabilitation

• Sustainable transport

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

23

I N S T I T U T O P A R A L A D I V E R S I F I C A C I Ó N Y A H O R R O D E L A E N E R G Í A

24

Thanks for your [email protected]

www.idae.es