lucent leveraging china’s supply chain capabilities idate 19 th november 2003 carlos nieva

Post on 18-Dec-2015

216 views

TRANSCRIPT

Lucent Leveraging China’sLucent Leveraging China’s

Supply Chain CapabilitiesSupply Chain Capabilities

IDATE 19IDATE 19thth November 2003 November 2003

Carlos Nieva Carlos Nieva

2Lucent Technologies – Proprietary (Restricted)

Agenda for today ...

The Opportunity

Lucent Supply Chain Strategy

Strategic Sourcing process

Experience in leveraging China’s SC

Key Takeaways

3Lucent Technologies – Proprietary (Restricted)

Danger and Opportunity

The Opportunity . . .

China’s economy is big & growingFour to six million new cell phone subscribers are signing up every month

Projected to be the biggest Telecomm market by 2005

China’s cost structure is affecting the competitive capabilities of all multinational corporations

A powerful combination of: disciplined, low-cost labor force; large amount of technical personnel

0

0,5

1

1,5

2

Graduated Technicians andEngineers

2002

2003

4Lucent Technologies – Proprietary (Restricted)

Supply Chain Strategy

Lucent’s strategy is to design, deliver and execute world class supply chainsto optimally serve customers in any region

Lucent’s strategy is to design, deliver and execute world class supply chainsto optimally serve customers in any region

We have executed on our low cost manufacturing strategy, by moving Productionto low cost manufacturing areas, thereby drastically improving our margins

We have executed on our low cost manufacturing strategy, by moving Productionto low cost manufacturing areas, thereby drastically improving our margins

TL9000 is the quality Management standard for the design,development, production, delivery & installation processes

TL9000 is the quality Management standard for the design,development, production, delivery & installation processes

We take a cross functional approach to sourcing strategy,evaluating netpresent value for a number of scenarios,while considering qualitative factors

We take a cross functional approach to sourcing strategy,evaluating netpresent value for a number of scenarios,while considering qualitative factors

We are adopting a strategy that compliment low cost manufacturingwhile ensuring a local (regional) presence to win business

We are adopting a strategy that compliment low cost manufacturingwhile ensuring a local (regional) presence to win business

5Lucent Technologies – Proprietary (Restricted)

Labor Cost

Duty Rates

TransportCost

Transport Time

IncomeTax Rates

InventoryInvestment

Delivery Time

OrderFill-rate

Existing

Facilities

BESTSUPPLYCHAIN

DESIGN

Quantitative Factors• Labor rate• Materials Cost s• Transportation cost• Corporate tax rate• Duty rate• VAT• Lead Times (Transportation, Mfg, Supply)• Variability of Supply and Demand• Required Provisioning Interval• Required On-Time Deliver %• Cost of Capital• New Investment Costs

Qualitative Factors• Labor productivity• Availability of skilled labor• Distribution infrastructure• Intellectual Property protection• Technology resources• Economic stability• Proximity to Customer• Proximity to R&D• Quality and Reliability of Supply

How Does One ApproachSupply Chain Design?

6Lucent Technologies – Proprietary (Restricted)

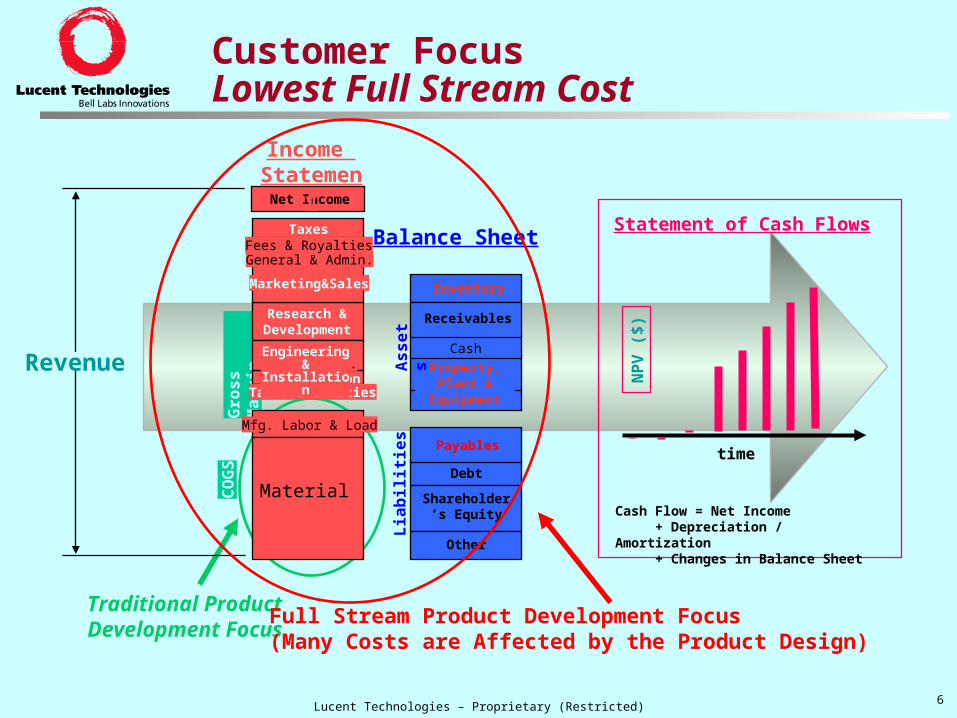

Customer FocusLowest Full Stream Cost

Balance Sheet

Debt

Shareholder’s Equity

Payables

Other

Property, Plant & Equipment

Inventory

As

se

ts

Lia

bil

itie

s

Other

Cash

Receivables

Traditional Product Development Focus

Revenue

CO

GS

Gro

ss

Ma

rgin

Net Income

Research & Development

Marketing&Sales

General & Admin.

Taxes

Distribution

Mfg. Labor & Load

Tariffs & Duties

Material

Engineering & Installation .

Fees & Royalties

Income Statement

Full Stream Product Development Focus(Many Costs are Affected by the Product Design)

Statement of Cash Flows

Cash Flow = Net Income+ Depreciation / Amortization+ Changes in Balance Sheet

NP

V (

$)

time

7Lucent Technologies – Proprietary (Restricted)

SG&A, R&DReturn on Invested Capital

Suppliers (In-country)

Suppliers (USA)

Suppliers(Asia)

e.g. 50%

e.g.: 50%

e.g. 30%

e.g. 70%

RawMat’ls.

UniqueMat’ls.

Cct.Pk.Buffer

FinishedGoodsCircuit-Pack

Assy. & Test

COUNTRY X

Customers

Model Outputs:• Lowest Full Stream Cost • Highest relative total profits & NPV• Optimal Balance Sheets• Optimal inventory investment• Best production mode• Best Expected Interval

Model Inputs:• Operational Performances & Constraints• Product COGS Structure• Transportation Costs & Times• Variability of all Intervals • Labor Rates• Tax Rates• Duty Rates

Raw Material Supply Sources (Defined in the Model)

Required Inventory Stores (Calculated by the Model)

Manufacturing Location (Defined by the Scenarios)

Market being Serviced(Defined for each Set of Scenarios)

What is the Profitability of Each Possible Supply Chain into Each Market?

SystemAssy. & Test

COUNTRY Y

Supplier(In-country)

e.g. 25%

e.g. 75%

OtherSuppliers

RawMat’ls.

Supply Chain AnalysisQuantitative Evaluation of Supply Chain Alternatives

8Lucent Technologies – Proprietary (Restricted)

Current State(EOY F2003)

Initial State(early FY2002)

Circuit-Pack assembly & test to EMS partners 90% of all CP production to low-cost regions 24 fewer facilities yet 50+ available LU System Integration for complex technologies Significant product transfers while maintaining

sequential customer delivery improvements

NAR

CALA

EMEA

PRC

A/P

NAR

CALA

EMEA PRC

A/P

Leveraging Low Cost Regions forManufacturing in becoming theLow Cost Provider to our Customers

9Lucent Technologies – Proprietary (Restricted)

2004 EMS Volume by Region

NAR

Europe

APAC

Brazil

2004 LU Revenue Outlook by Region

NAR

EMEA

APAC

CALA

Note: Revenue does not include Services

2004 Outlook2004 OutlookRevenue vs. EMS VolumesRevenue vs. EMS Volumes

Less regional correlation between Revenue and EMS SpendAdditional volumes in cost-competitive regions increase margin

11% increase in EMEA Revenue is spread across many products

90% of circuit board manufacturing has been moved to low costregions

10Lucent Technologies – Proprietary (Restricted)

Much of our production has moved to Asia, particularly China

Competitive cost structure

A well-established electronic component supply chain network in

a relatively-compressed geographic area (e.g., Suzhou/Shanghai

industry park and Dongguan in Guangzhou)

Well-educated work force including operators / workers,

engineering, and management staff

Efficient government policy for quick turn-around of logistics

(Customs Clearance) and well-connected infrastructure.

The access to the market for the OEM’s (who are EMS’s

customers) – EMS’s follow their customers into the market.

What attracts EMS Partners to set up a manufacturing location in China:

11Lucent Technologies – Proprietary (Restricted)

What are the challenges of having a manufacturing footprint in China?

Financial Infrastructure:Tax structures are complex

EMS Partners are challenged to understand how to take advantage of low tax manufacturing areas – e.g. VAT implications vary from province to province and the type of operation (manufacturing vs. repair)

Legal entity structure makes it difficult to optimally manage money (spreading of currency risk)

e.g. Jabil/LTOS JV structure

Currency instability

if the Yuan inflates compared with the US Dollar, China may no longer be low cost compared with other sourcing options

Language and Cultural Barriers

Communication is challenging

high tech companies focus hiring process on English speaking natives, with skill and knowledge level being secondary)

Time difference makes communication challenging, especially when communication is required across 3 continents

e.g EMS GM is in the US, NPI in Germany, Manufacturing in China

General nervousness in the area of data management

a tendency to react to every piece of new information (e.g. change in forecast), rather than taking the time to sit back and see what the impact of this new piece of information really is in the big picture

12Lucent Technologies – Proprietary (Restricted)

What are the challenges of having a manufacturing footprint in China?

Language and Cultural Barriers: Communication is challenging

High tech companies focus hiring process on English speaking natives, with skill and knowledge level being secondary

Time difference makes communication challenging, especiallywhen communication is required across 3 continents

e.g EMS GM is in the US, NPI in Germany, Manufacturing in China

General nervousness in the area of data management

A tendency to react to every piece of new information (e.g. change in forecast), rather than taking the time to sit backand see what the impact of this new piece of information reallyis in the big picture

13Lucent Technologies – Proprietary (Restricted)

What are the challenges of having a manufacturing footprint in China?

Supply Chain Efficiency:Implementing LEP (Leading Edge Procurement)programs is challenging

They are used to the simple PO arrangements, andhave little to no experience with LEP arrangements- e.g. mismatch between the contracts with our EMS Partners,

and the expectations to manage liabilities

Buffering of extra inventory is required to account forextra transit time and custom delays

e.g. import into Shanghai took 60 days to clearcustoms, once we knew the right people, it only took 20 days

Customer financing is not easily obtained throughChina’s Export Credit Agency

14Lucent Technologies – Proprietary (Restricted)

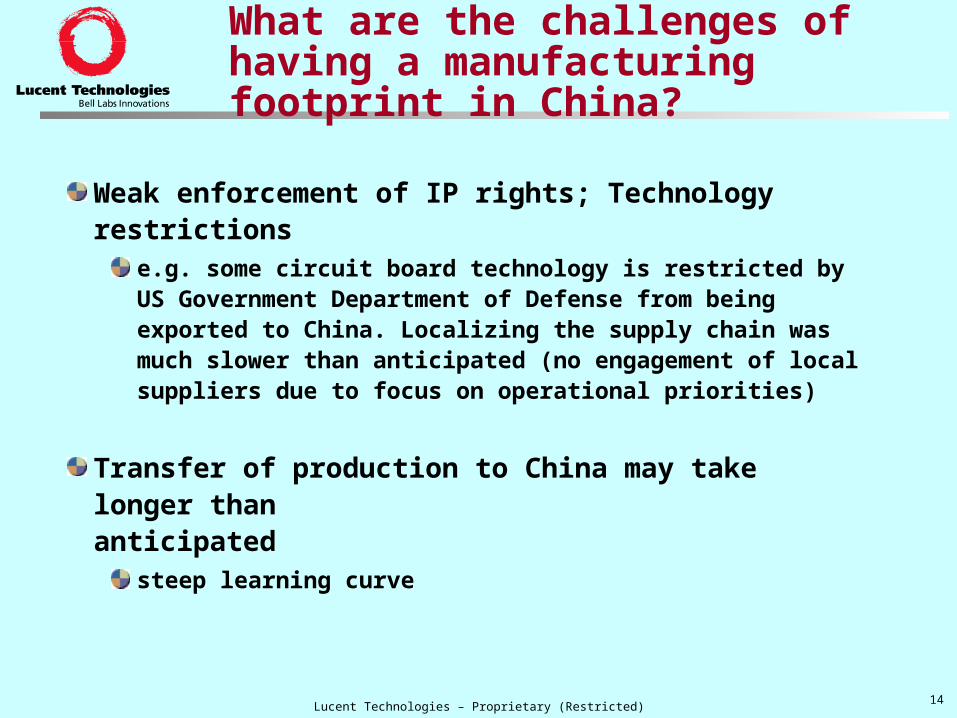

What are the challenges of having a manufacturing footprint in China?

Weak enforcement of IP rights; Technology restrictions

e.g. some circuit board technology is restricted byUS Government Department of Defense from beingexported to China. Localizing the supply chain wasmuch slower than anticipated (no engagement of localsuppliers due to focus on operational priorities)

Transfer of production to China may take longer thananticipated

steep learning curve

15Lucent Technologies – Proprietary (Restricted)

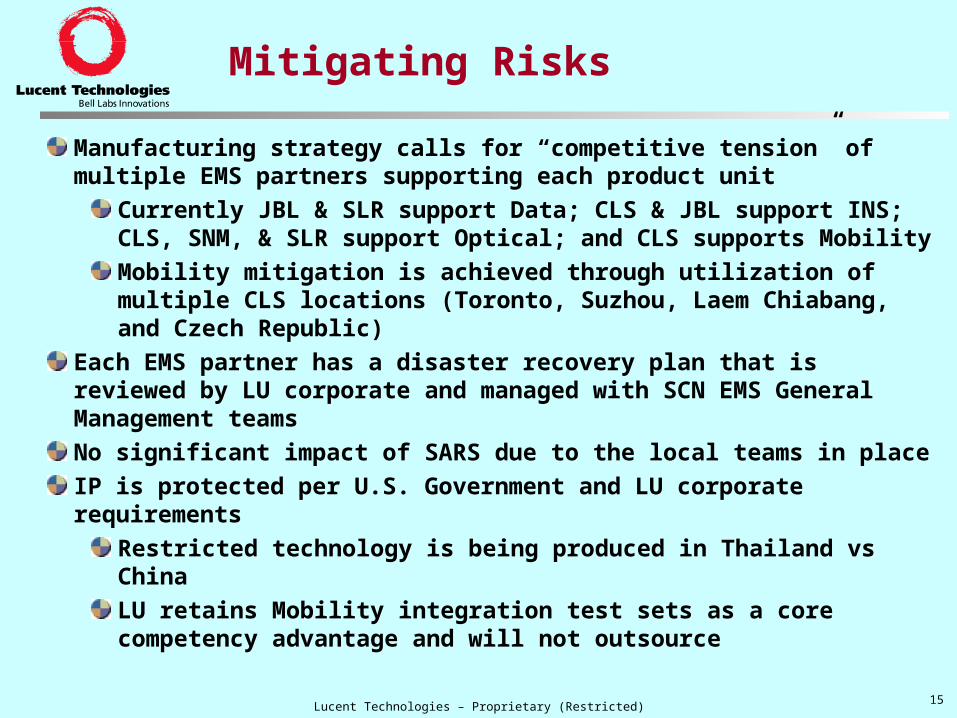

Mitigating Risks

Manufacturing strategy calls for “competitive tension” of multiple EMS partners supporting each product unit

Currently JBL & SLR support Data; CLS & JBL support INS; CLS, SNM, & SLR support Optical; and CLS supports Mobility

Mobility mitigation is achieved through utilization of multiple CLS locations (Toronto, Suzhou, Laem Chiabang, and Czech Republic)

Each EMS partner has a disaster recovery plan that is reviewed by LU corporate and managed with SCN EMS General Management teams

No significant impact of SARS due to the local teams in place

IP is protected per U.S. Government and LU corporate requirements

Restricted technology is being produced in Thailand vs China

LU retains Mobility integration test sets as a core competency advantage and will not outsource

16Lucent Technologies – Proprietary (Restricted)

Takeaways ...

To win the Chinese market you have to “show your face” there China represents a true cost competitive advantage for high tech

business

Unit cost is just a piece of the equation. You need to factor in full stream costs and associated complexities when sourcing from China

While there is an abundance of information available on the “to do’s” of moving manufacturing to China, there are few critical lessons learned:

Cultural and language barriers are real… hire the right people and team up with the right partners

The financial and legal structure is complex, complex, complex

Supply Chain Management expertise is still evolving, take a ‘back to basics’ approach

Technological barriers are low, but expect product transfers to take longer than planned

17Lucent Technologies – Proprietary (Restricted)

18Lucent Technologies – Proprietary (Restricted)

Goals in Creating the Most Competitive Supply ChainGoals in Creating the Most Competitive Supply Chain

Maximize Customer Satisfaction (On-Time Delivery, Promised Interval)

Maximize Agility and Flexibility

Achieve Lowest Full Stream Cost

Manage Cash and Investments

Minimize Investment Risk and Supply Chain Liabilities

(Stranded Capital, Inventory, Other) – “built-in” Flexibility

Build the supply chain of a “Competitor from Hell” and attempt to construct a supply chain and product design

to meet/exceed it

Supply Chain Design - Goal

19Lucent Technologies – Proprietary (Restricted)

“The Goods” “The Bads” Volume production consolidation to cost comp. facilities

Greater than 50% of spend in cost competitive regions

EMS presence in all four regions

System integrations centers transitioning to VMO model

Increasing direct fulfillment activities…more variable cost structure

Utilize low volume facilities where cost of move > benefit

Too many EMS facilities given level of business

Complexities of a globally distributed supply chain

Multiple handoffs

Higher fixed cost structure through existing SICs

NORTH AMERICA• 14 EMS Facilities (10 Prod, 6 NPI)• 4 EMS Partners• 4 Lucent Production Facilities

ASIA PACIFIC / CHINA• 6 EMS Facilities (6 Prod, 2 NPI)• 4 EMS Partners• 3 Lucent Production Facilities

EMEA• 6 EMS Facilities (5 Prod, 3 NPI)• 4 EMS Partners• 3 Lucent Production Facilities

CALA• 2 EMS Facilities (2 Prod, 0 NPI)• 2 EMS Providers• 1 Lucent Production Facilities

Global Supply Chain FY2003:The World Today

20Lucent Technologies – Proprietary (Restricted)

2003 EMS Volume by Region

NAR

Europe

APAC

Brazil

2003 LU Revenue by Region

NAR

EMEA

APAC

CALA

2003 Revenues vs.2003 Revenues vs.EMS VolumesEMS Volumes

EMS volumes essentially mirror Lucent revenue projections

Previous product transfers have allowed LU to achieve significant margin improvements

PCBA transitions are heavily weighted to more cost competitive regions, while FAT is more evenly distributed

21Lucent Technologies – Proprietary (Restricted)

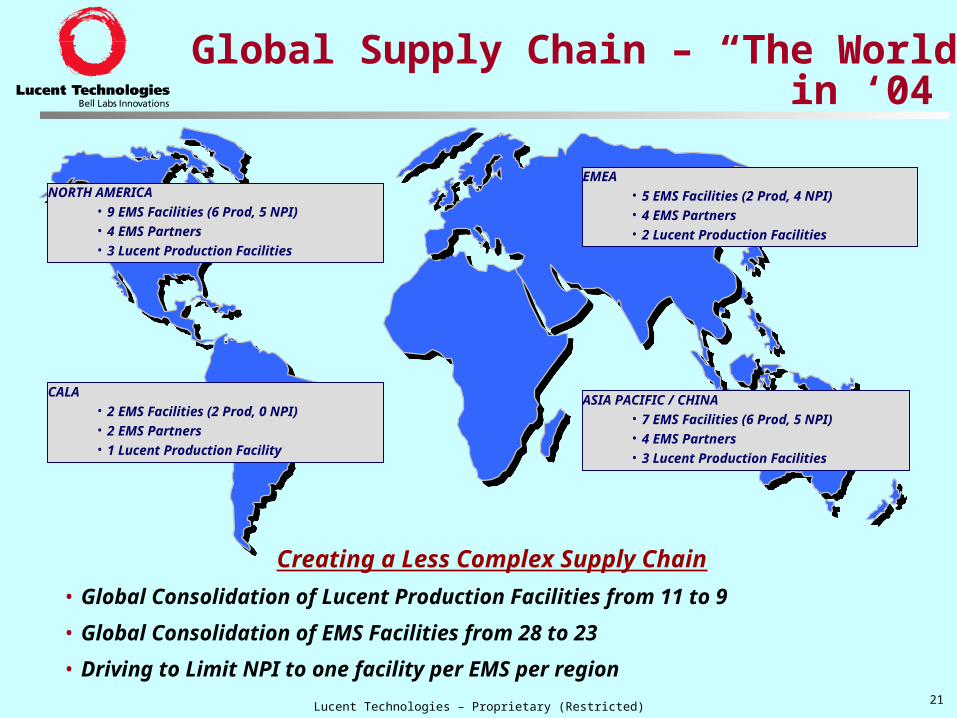

NORTH AMERICA• 9 EMS Facilities (6 Prod, 5 NPI) • 4 EMS Partners• 3 Lucent Production Facilities

ASIA PACIFIC / CHINA• 7 EMS Facilities (6 Prod, 5 NPI)• 4 EMS Partners• 3 Lucent Production Facilities

EMEA• 5 EMS Facilities (2 Prod, 4 NPI)• 4 EMS Partners• 2 Lucent Production Facilities

CALA• 2 EMS Facilities (2 Prod, 0 NPI)• 2 EMS Partners• 1 Lucent Production Facility

Creating a Less Complex Supply Chain

• Global Consolidation of Lucent Production Facilities from 11 to 9

• Global Consolidation of EMS Facilities from 28 to 23

• Driving to Limit NPI to one facility per EMS per region

Global Supply Chain – “The World in ‘04”

22Lucent Technologies – Proprietary (Restricted)

Strategic Initiatives in Place - Product Sourcing

Product Sourcing Process

Identify Product Sourcing

Opportunities

Engage Stakeholders

Review Decision with Sourcing

Council(If Needed)

Communicate Decision

Verify Implementation

Bal

ance

d S

core

card

Team: Reviews analysis. Finalizes and documents decision based on completed analysis

PTL/PM/SCDO/EMS: Initiates sourcing requests for new, existing and EOL products

SCDO: Engages key stakeholders (PUs, SCN, …) and holds Collaborative Roundtable kickoff meeting

SCDO: If applicable, reviews and applies product family sourcing strategy. Otherwise, identify options, gather data and perform analysis

PTL: Provides updates and communicates completion of implementation of decision to SCDO

SCDO: Prepares and distributes sourcing decision to all stakeholders (PU, SCN, CFO, …)

SCDO: Plans and facilitatesreview of decision with Sourcing Council (if needed)

Analyze Options

Reach Consensus on

Sourcing Decision

23Lucent Technologies – Proprietary (Restricted)

Final Supply Chain Design

Principle Trading Company

Distributor

Customers

CPA&TC-Items FA&T

ASICCriticalUnique

CPABuffer

Supplier(In-country)

Supplier(USA)

RawMat'ls

Supplier(In-country)

Supplier

FinishedGoods

Supplier(Asia)

A-ItemsB-Items

(Non-Critical Components)

Supplier

Lucent Owned & Managed

Contract Mfg. Owned & Managed

Supplier Owned & Managed

CustomersDistributors

& VARs

Ireland Ireland

CPA&T

(USA)

FA&T

(USA)

New Product Introduction(where necessary)

($)

Transitional

24Lucent Technologies – Proprietary (Restricted)

Lucent’s strategy in Europe

Establish a low cost, flexible supply chain supporting EU content, Whole

order delivery, Complex Large Projects & Superior Performance in

Business Metrics & Results

Leverage Lucent Supply Chain partners that are investing in the Central

Europe Area.

Utilize Poland and the Czech Republic as a main manufacturing

campuses in the EMEA Supply chain

Establish a regional footprint that is complementary to our low cost

strategy in China/Asia Pacific