lululemon deck

TRANSCRIPT

1

LululemonNASDAQ: LULUJason A. Moser

2

Retail’s brutal holiday season resulted in weak top line growth & heavy discounting.

The move to ecommerce continues to quickly shape the changing retail space.

Lululemon isn’t immune, however new leadership, expanded product lines and direct-to-consumer offer a powerful brand on sale today.

The idea

3

What does Lululemon do?

It sells clothes. Plain and simple.OK seriously, known primarily for its

women’s yoga gear, Lululemon is also expanding its product line:“We also

continue to broaden our product range to increasingly appeal to male athletes

and athletic female youth.”

4

How do they do it?

254 company-owned stores (2/14/2014) North America, Australia and New Zealand Wholesale via studios, health centers, etc. Direct-to-consumer = e-commerce sales

5

Margins, margins everywhere

6

Past growth

CAGR 38%

7

What’s the market opportunity?

Long-term target 350-375 stores in North America; Next three years focused on new US stores; Europe and Asia both show evidence of demand

which will boost the overall opportunity; Store count and breakdown today:

Country Stores

United States 171

Canada 54

Australia 25

New Zealand 4

Total 254

8

Lululemon also owns 12 ivivva athletica stores which specialize in dance-inspired apparel for female youth.

Also referred to as a “tween brand”; this concept will grow.

What’s ivivva?

9

Direct-to-consumer

Direct to consumer introduced in 2009. Defined as Lulu’s e-commerce website. Has grown from 4% to now 17% of net sales.

10

Who do they compete with?

Anyone and everyone in the retail clothing industry, fashion, sports or otherwise.

11

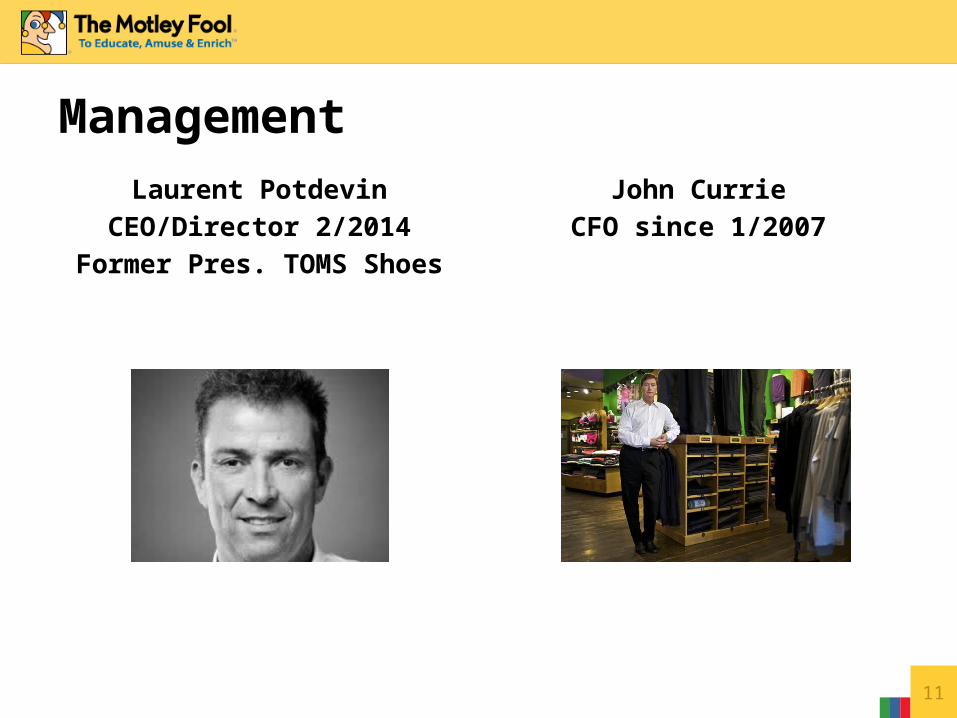

ManagementLaurent Potdevin

CEO/Director 2/2014Former Pres. TOMS Shoes

John CurrieCFO since 1/2007

12

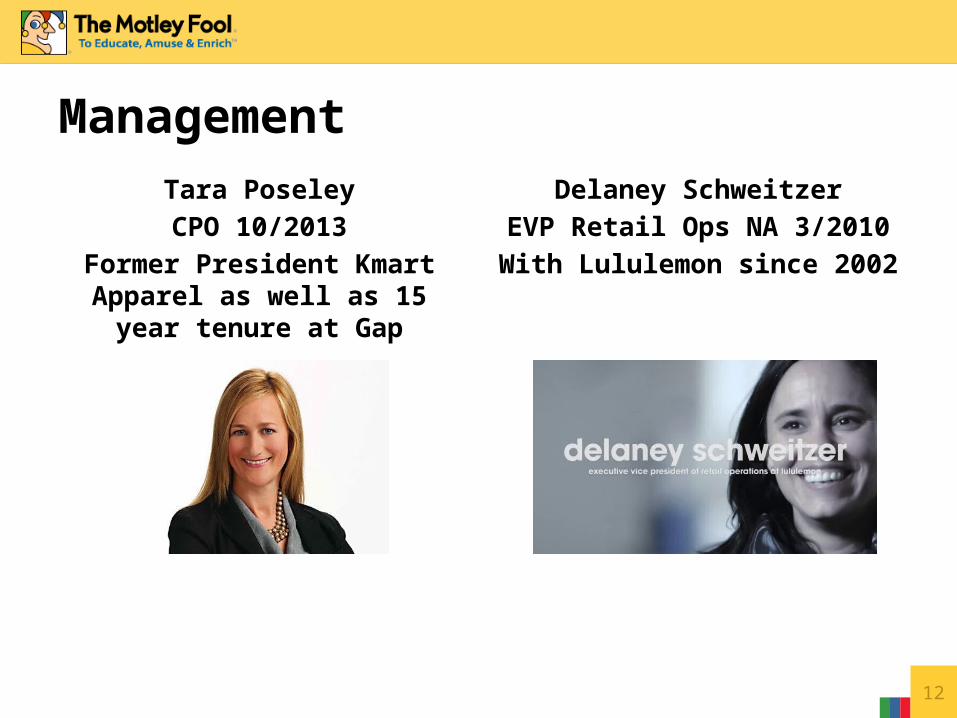

ManagementTara PoseleyCPO 10/2013

Former President Kmart Apparel as well as 15 year tenure at Gap

Delaney SchweitzerEVP Retail Ops NA 3/2010

With Lululemon since 2002

13

Understanding future worthIt’s worth looking at the past. What kind of multiples has

Lululemon garnered throughout the years?

14

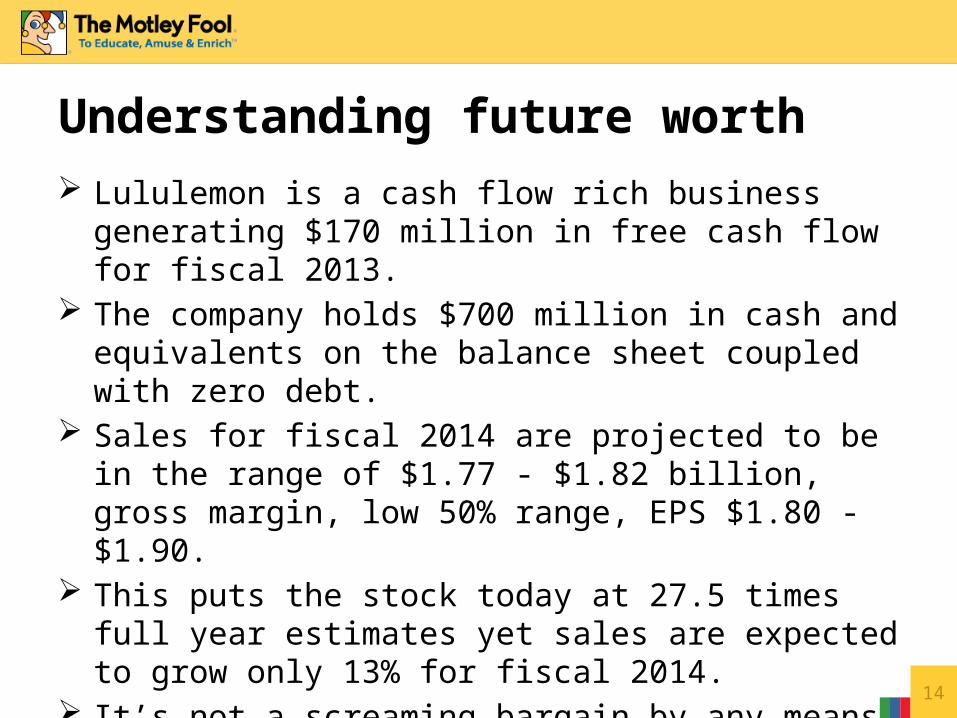

Lululemon is a cash flow rich business generating $170 million in free cash flow for fiscal 2013.

The company holds $700 million in cash and equivalents on the balance sheet coupled with zero debt.

Sales for fiscal 2014 are projected to be in the range of $1.77 - $1.82 billion, gross margin, low 50% range, EPS $1.80 - $1.90.

This puts the stock today at 27.5 times full year estimates yet sales are expected to grow only 13% for fiscal 2014.

It’s not a screaming bargain by any means, but it’s starting to look much more attractive now than a year ago.

Understanding future worth

15

Understanding future worthLululemon typically carries one of the higher SPSF metrics in the retail industry with only Tiffany and top-dog Apple ahead of it.

16

What are management’s long-term margin goals?Gross margin – 55%Operating margin – 25%Net margin – 20%

Sales growth of 30%+ is done. Next five years will be 15%. Sales for fiscal 2018 of $3.2 billion, net income $640 million. Multiple scenarios:

20 - $12.8 billion market cap;25 - $16 billion market cap;30 - $19.2 billion market capToday’s market cap = $7.5 billion

Understanding future worth

17

Retail is known for its lack of competitive advantages. Depending on the brand and leadership here.

New CEO Potdevin is an unknown, though I’m optimistic. Sourcing for Luon (30% of total fabric from one supplier); Founder Chip Wilson holds a bit more than 29% of the

company’s outstanding shares. While growth in direct-to-consumer is a net positive, it does

present additional tech and distribution challenges. ivivva is an additional lever for growth; failure on this front

would hurt.

Risks

18

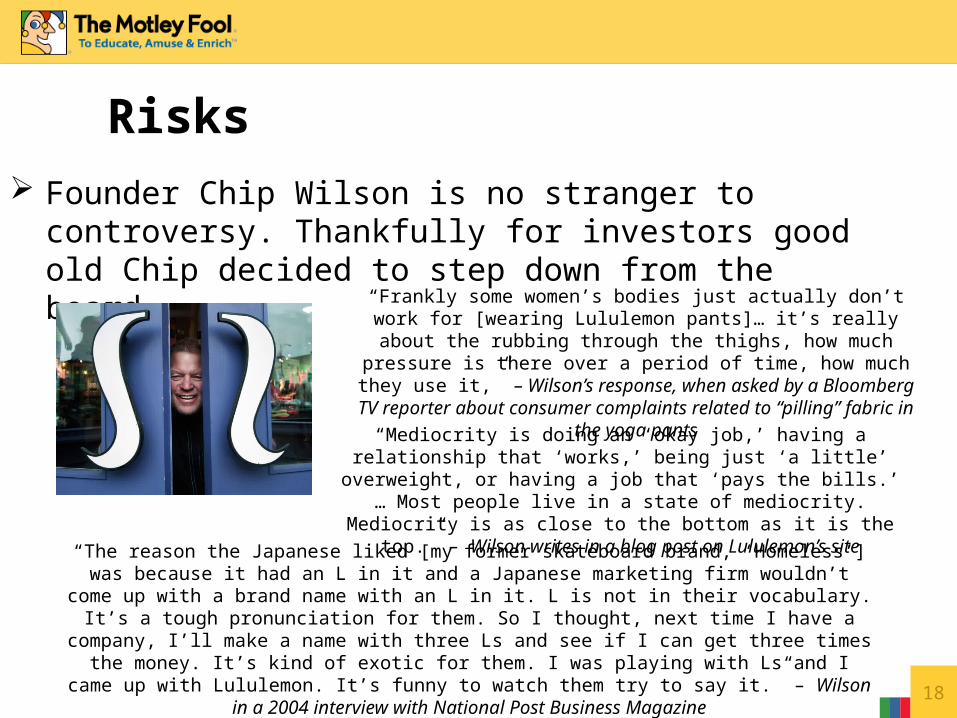

Founder Chip Wilson is no stranger to controversy. Thankfully for investors good old Chip decided to step down from the board.

Risks

“Frankly some women’s bodies just actually don’t work for [wearing Lululemon pants]… it’s really about the rubbing through the thighs, how much pressure is there over a period of time, how much they use it,” –

Wilson’s response, when asked by a Bloomberg TV reporter about consumer complaints related to “pilling” fabric in the yoga pants

“Mediocrity is doing an ‘okay job,’ having a relationship that ‘works,’ being just ‘a little’ overweight, or having a job that ‘pays the bills.’ … Most people live in a state of mediocrity. Mediocrity is as close to the bottom as it is the

top.” – Wilson writes in a blog post on Lululemon’s site

“The reason the Japanese liked [my former skateboard brand, ‘Homeless’] was because it had an L in it and a Japanese marketing firm wouldn’t come up with a brand name with an L in it. L is not in their vocabulary. It’s a tough pronunciation for them. So I thought, next time I have a company, I’ll make a name with three Ls and see if I can get three times the money. It’s kind of exotic for them. I was playing with Ls and I came up with Lululemon. It’s funny to watch them try to say it.” – Wilson in a 2004 interview with National Post

Business Magazine

19

Management’s annual cash incentive bonuses are tied to: operating income (50%), company revenue (10%), gross margin (30%) and inventory turns (10%). I like this.

Are the multiple scenarios in “Understanding future worth” reasonable? If the growth is still in fact there then yes. Under Armour ($12.2 billion market cap) still trades for 75 times earnings and Nike ($65 billion market cap) is 25 times earnings. Both have admittedly larger market opportunities.

Very encouraged by the website, focus on free-shipping homes in on exactly what consumers want. More than 13% of all clothing sales now occur online.

Are margin targets reasonable? Yes, particularly if Europe and Asia succeed.

Questions/ideas to ponder

20

Lululemon was fast out of the gate but the past couple of years have shown chinks in the armor.

Leadership changes are not always bad and can sometimes be very good. I am optimistic in this case given the low bar Wilson set and Potdevin’s experience.

Lululemon shares are down over 17% year to date bringing the stock to a more reasonable valuation considering what I see as an overall positive picture over the coming five years.

I’m calling a buy-around of $50 for Lululemon shares today to outperform the S&P 500 over the next 3-5 years.

Bottom line takeaway for investors