m ay 2 0 2 0 • s t rat e g y merchandising strategies for

TRANSCRIPT

M A Y 2 0 2 0 • S T R A T E G Y

Merchandising Strategies for the New Normal

Written by Nur Atiqah Kamarudin, Senior Business Intelligence Analyst

Introduction | Compact Seasonality | Full Price Opportunity |

Dynamic Pricing | Relevant SKU Styles | Deliver What Consumers

Want | Use Data Analytics | Conclusion

IntroductionKey Insights• Shift in Comfort Dressing: Current lifestyles have created a

renewed a surge in athleisure, as consumers prioritised comfort.

• Opportunity in Full Price Sell-Out: We’ve identified high-growthcategories and subcategories, which provide opportunity for brandsto experiment with pricing and maximise full price sell-out.

• Accelerating Demand-Driven Supply Chain: Seasonless collectionsand tight assortments will allow brands to create agile, demand-driven supply chain.

We can’t understate the impact the coronavirus pandemic has had onthe fashion industry. As retailers continue to face inventory issues,changing consumer preference has highlighted the industry’s deep-rooted problem – seasonality. Some brands have taken measures to cutback on assortments, while others decided to push deliveries to nextyear.

This report aims to uncover the merchandising strategies adopted byfast fashion retailers in the UK and how they can move ahead toleverage on potential opportunities in embracing the new normal.

More than 200,000 data points were screened from January to May2020 against the same period in 2019 across womenswear categorieson Asos, Boohoo, Zara and H&M.

Instagram @zara

M A Y 2 0 2 0 • S T R A T E G Y

All data used in this report comes from products retailing online as trackedby Omnilytics, unless otherwise mentioned.

Compact SeasonalityWith production cycles and deliveries in disarray, many designers andretailers are wanting to reset the traditional fashion calendar, bringingit in line with the weather seasons. Saint Laurent, the first major labelto skip Paris Fashion Week and move off schedule for the rest of 2020,will likely inspire others to follow suit.

With excess inventory and rampant discounting at an all-time high,retailers are in a better position to keep their assortments tight.Consumers, currently less interested in fleeting trends, are more likelyto shop essentials and seasonless items.

Shift in Comfort DressingDespite low consumer sentiment, key apparel categories still observedpositive YoY increase in sell-outs. The already-successful Activewearcategory benefitted from the growth in at-home workouts, with astrong 43% growth in sell-out YoY.

As lockdown measures started to ease in the UK, comfort dressingremained at the fore. Intimates, mostly dominated by Sleepwear, saw awhopping 41% increase in sell-out YoY. The bottoms category also sawa clear shift from formal styles to casual and relaxed silhouettes,indicating longevity post-pandemic.

With consumers prioritising comfort, loungewear – a trend closelyaligns with athleisure – is at its peak. The style was uptrending acrossmost core categories. Hoodies & Sweatshirts, Joggers, Jumpers &Sweaters and Sleepwear Tops & Bottoms were the main subcategoriesthat made up this new core offering (Chart 2).

M A Y 2 0 2 0 • S T R A T E G Y C H A R T 1 : C H A N G E I N S E L L - O U T Y O Y B Y C A T E G O R I E S

C H A R T 2 : D E M A N D F O R L O U N G E W E A R B Y S U B C A T E G O R I E S

Key Apparel Categories

-50% -30% -10% 10% 30% 50%

Jeans

Dresses

Skirts

Tops

Outerwear

Intimates

Pants & Leggings

Activewear

Shorts

3

4

The main Activewear, Outerwear and Pants & Leggings subcategoriesreported above average sell-outs at full price.

Activewear performed best in both total sell-out and sell-out at fullprice, signifying the renewed popularity of the category. Drillingfurther into Activewear, we can see that Tops & T-Shirts was the mostpopular subcategory, which was made up mostly of Tank and JerseyTops.

In Outerwear, Hoodies & Sweatshirts garnered above average sell-outat full price, while Jumpers & Sweaters fell short by 0.5 percentagepoint. Casual silhouettes proved to be in high demand as Joggers andLeggings managed to record above average sell-outs, compared tomore formal bottoms subcategories.

Consumers’ increased willingness to pay for these products signals ahuge opportunity for retailers to continue driving these subcategoriesat full price. It’s wise to look out for opportunities like this on coreitems, prolonging the product lifecycle.

Retailers Championing Full Price Sell-OutZara was driving full price sell-out for casual outerwear at 65%. Theretailer leant into the popularity of the category, as it increased itsofferings this year by 40% compared to last.

With activewear on the rise and loungewear being the new essential,Asos was in a better position as it had the widest offering on thesecategories with nearly 10,000 SKUs. The retailer also led with aboveaverage sell-out at full price, signifying its strong position in thesecategories.

Full Price OpportunityC H A R T 3 : C A T E G O R Y P E R F O R M A N C E B Y A L L R E T A I L E R SM A Y 2 0 2 0 • S T R A T E G Y

5

Breaking down the median price by key subcategories revealed Zara’sdynamic pricing during the Covid-19 crisis. The retailer chose toincrease pricing for categories with high growth, capitalising ondemand.

Zara launched new Hoodies & Sweatshirts and Cardigans during theCovid-19 period with an average of 6% and 9% increase in pricesrespectively, compared to last year. Despite the higher price, theretailer managed to achieve an overall improvement in total sell-out atfull price of 65%. Sell-out in April also increased following the rise inmedian price in Outerwear subcategories (Chart 5).

Similarly, the subcategories within Pants & Leggings also experiencedincreased sell-out. The success of the pricing strategy was led by therelevant offering, as you’ll see next.

Dynamic Pricing C H A R T 4 : C H A N G E I N M E D I A N P R I C E F O R Z A R A

Categories Subcategories 2019 (GBP) 2020 (GBP)

Outerwear

Hoodies & Sweatshirts 22.13 23.40

Jumpers & Sweaters 29.35 27.03

Cardigans 32.02 35.01

Pants & Leggings

Joggers 22.90 23.88

Leggings 16.85 19.92

Wide Leg Pants 34.36 27.57

ShortsBermuda Shorts 22.86 27.96

Denim Shorts 20.17 19.64

M A Y 2 0 2 0 • S T R A T E G Y

Cheaper than 2019 More expensive than 2019

C H A R T 5 : O U T E R W E A R S U B C A T E G O R I E S S E L L - O U T M O V E M E N T F O R Z A R A

6

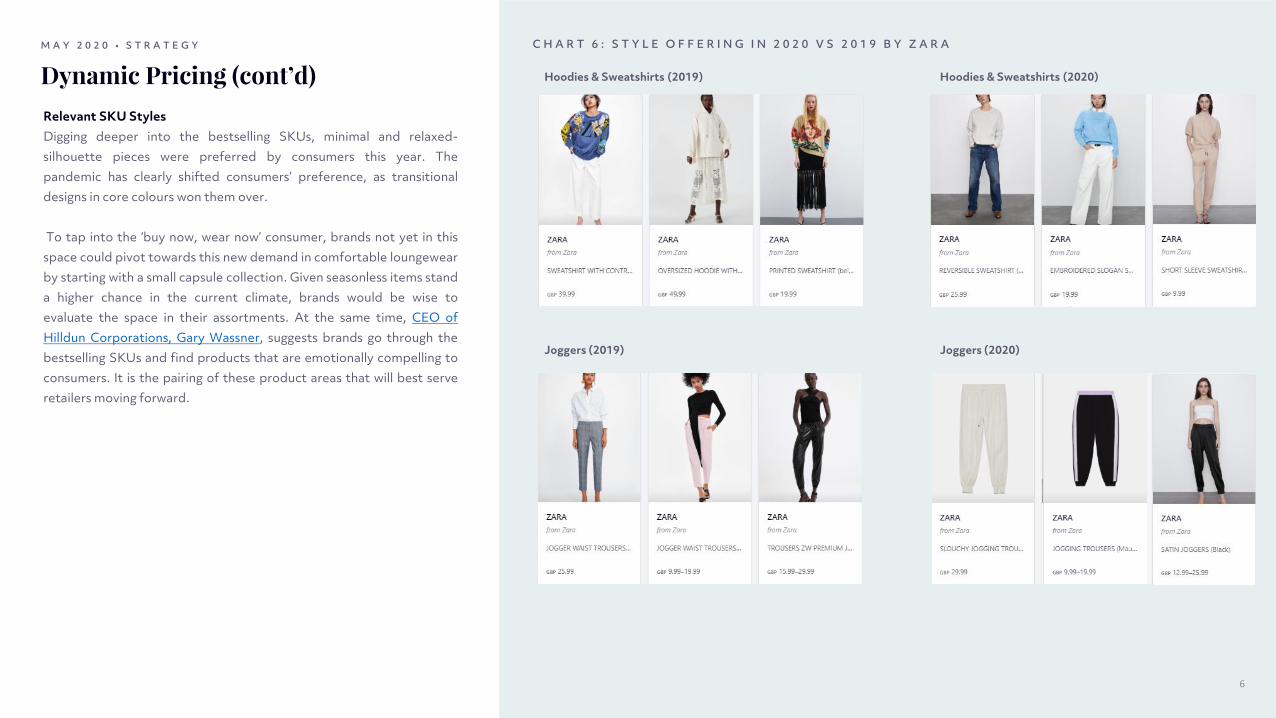

Relevant SKU StylesDigging deeper into the bestselling SKUs, minimal and relaxed-silhouette pieces were preferred by consumers this year. Thepandemic has clearly shifted consumers’ preference, as transitionaldesigns in core colours won them over.

To tap into the ‘buy now, wear now’ consumer, brands not yet in thisspace could pivot towards this new demand in comfortable loungewearby starting with a small capsule collection. Given seasonless items standa higher chance in the current climate, brands would be wise toevaluate the space in their assortments. At the same time, CEO ofHilldun Corporations, Gary Wassner, suggests brands go through thebestselling SKUs and find products that are emotionally compelling toconsumers. It is the pairing of these product areas that will best serveretailers moving forward.

Dynamic Pricing (cont’d)M A Y 2 0 2 0 • S T R A T E G Y

Hoodies & Sweatshirts (2019)

C H A R T 6 : S T Y L E O F F E R I N G I N 2 0 2 0 V S 2 0 1 9 B Y Z A R A

Joggers (2019)

Hoodies & Sweatshirts (2020)

Joggers (2020)

Agility is the critical tool in being able to respond to the shiftingconsumer demands of the moment. Nimble communications are agreat way to achieve this.

As consumers sought comfort dressing, Asos, Boohoo, and H&Mpromoted loungewear throughout the period. Tactical promotions andnew style edits surrounding the theme were prominent on their landingpages and email newsletters. With summer approaching and WFHbeing the new norm, the interest towards this trend is expected tocontinue, but in lightweight, breathable fabrics.

Besides investing in seasonless product, delivering personalised itemsthat resonate well with consumers will also keep them enticed. As seenfrom the collaborations at H&M with designers such as GiambattistaValli and Maison Martin Margiela, the campaigns managed to createhype and in turn generate full-priced sales for the brand.

Brands can also tap into a new category by paying close attention tomarket demand, as seen from the surge in face masks following thecurrent pandemic. Face masks were one of the best-selling accessoriesin the UK and observed a steady rise in the market (Chart 7). Aslockdown restrictions ease and more consumers venture into public,we expect to see further increase in demand and sales for this item.

Deliver What Consumers WantM A Y 2 0 2 0 • S T R A T E G Y

C H A R T 7 : I N C R E A S E I N D E M A N D F O R F A C E M A S K S

Retailer’s Marketing Activities on Loungewear

7

8

Demand-Driven Supply ChainAs the Covid-19 crisis accelerates the transformation towards ademand-driven supply chain, brands need to rely on data analyticsmore than ever.

According to Sarah Johnson, who is the former Head of Merchandisingat Asos and Founder of Flourish Retail, it is crucial for brands toreforecast sales according to the current climate. With historical datanow redundant, brands should be guided by current market insights togenerate a base forecast when reforecasting, before layering onstrategic plans.

As consumer preferences change and the retail landscape getsincreasingly competitive, brands should rely on data-backed analyticsespecially in a demand-driven supply chain model, where being agile iskey. Brands will then be able to reposition themselves better byputting out more relevant products consistently, and in turn reducingthe risk of markdowns and excess inventory.

They should also continue to pay attention to social media. TheCOVID-19 outbreak, which has led to the birth of several hashtags inthe fashion circle, including #WFHFits, can be used to monitor the shiftin consumer demand. The popularity of loungewear and relaxed,comfortable silhouettes were evident across influencers’ andcelebrities’ profiles.

The change in the post-pandemic environment has also forced brandsto continually reassess their strategies, which places a higherimportance on real-time market insights.

Use Data AnalyticsM A Y 2 0 2 0 • S T R A T E G Y C H A R T 8 : T R E N D P E R F O R M A N C E F O R A C T I V E W E A R

Stay At Home Outfits on Social Media

Instagram @wfhfitsInstagram @emilydidonatoInstagram @kyliejenner

Instagram @hm

Next Steps for BrandsIdentify Consumers’ Wants: At a time when consumers aresteering the demand wheel, it is imperative for brands to meettheir needs with increased speed and efficiency. Withseasonless items taking centre stage and loungewear being thenew essential, brands that do not react to this shift quickly willlose out in market share.

Strike a Balance Between Products and Dynamic Pricing:Zara’s ability to apply dynamic pricing on the relevant SKUstyles has proven to be a fundamental strategy to enticeconsumers through Covid-19. The retailer saw animprovement in total sell-outs as it took advantage of the highgrowth categories and subcategories by increasing prices.Brands wanting to employ this strategy need to ensure theright price is in line with the value offered to consumers.

Increase Agility with a Focused Range Plan: As seasonalitybecomes increasingly meaningless, there is opportunity forbrands to accelerate towards a demand-driven supply chain.However, speed is of the essence in this model. To increaseagility, brands can start with reduced assortment width andtargeted, focused range planning while shaving trend-leditems. Brands such as Tanya Taylor have employed thisstrategy, by cutting back on its pre-fall collection by 30% andfocusing more on transitional design. In order to succeed,brands need to start acknowledging this change by acting andplanning now, supported by data and analytics.

Conclusion

Reroute and Reassort Existing Stock: In order to mitigatelosses and protect margin, retailers can consider movingexisting stock. In identifying products that can lendthemselves to future seasons, there will be more time togenerate full price sales, rather than resorting to aggressivediscounting, which will erode brand equity. 3.1 Philip Lim hasdecided to shift its Pre-Fall products to Pre-Spring in order toavoid deep discounting and minimise possible ordercancellations. Meanwhile, products that are still sitting in thewarehouse can be integrated into the assortment regardlessof seasonality, as advised by Gary Wassner.

M A Y 2 0 2 0 • S T R A T E G Y

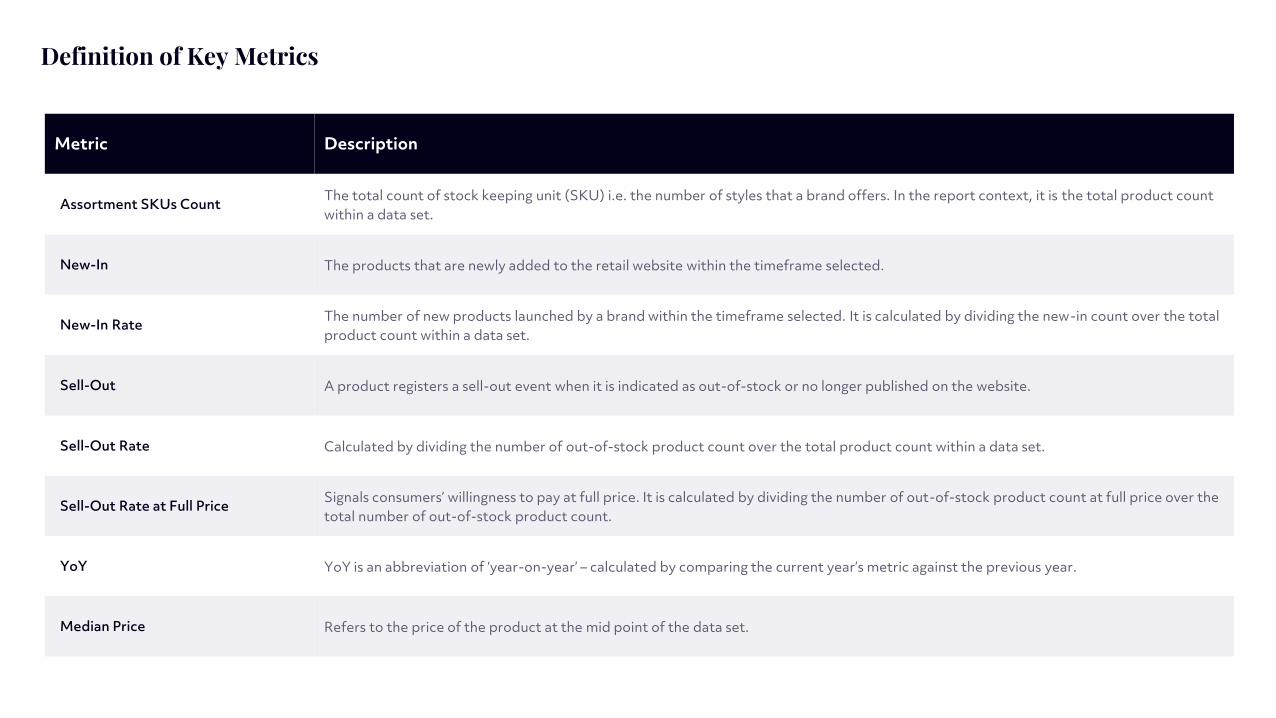

Metric Description

Assortment SKUs Count The total count of stock keeping unit (SKU) i.e. the number of styles that a brand offers. In the report context, it is the total product count within a data set.

New-In The products that are newly added to the retail website within the timeframe selected.

New-In Rate The number of new products launched by a brand within the timeframe selected. It is calculated by dividing the new-in count over the total product count within a data set.

Sell-Out A product registers a sell-out event when it is indicated as out-of-stock or no longer published on the website.

Sell-Out Rate Calculated by dividing the number of out-of-stock product count over the total product count within a data set.

Sell-Out Rate at Full Price Signals consumers’ willingness to pay at full price. It is calculated by dividing the number of out-of-stock product count at full price over the total number of out-of-stock product count.

YoY YoY is an abbreviation of ‘year-on-year’ – calculated by comparing the current year’s metric against the previous year.

Median Price Refers to the price of the product at the mid point of the data set.

Definition of Key Metrics

Get in touchOmnilytics is a fashion analytics company that helps brands and retailers – born to make data accessible and

insights actionable so that businesses can make decisions with confidence and speed. At the core of what

Omnilytics does is the belief that information is power; pairing deep industry expertise and ground-breaking

technical innovation to bolster businesses’ agility with data-driven insights.

Find out more

www.omnilytics.co

M A Y 2 0 2 0 • S T R A T E G Y

Smart Retail Markdown During COVID-19

Similar Industry Reports

See more Industry Reports

M A R C H 2 1 , 2 0 2 0 • C O V I D - 1 9

Fashion Retail & theCOVID-19 Crisis