macroeconomics: fluctuations and...

TRANSCRIPT

Macroeconomics: Fluctuations and Growth

Francesco Franco1

1

Nova School of Business and Economics

Fluctuations and Growth, 2011

Francesco Franco Macroeconomics: Fluctuations and Growth 1/45

Players in the Money Supply Process

1 Central bank2 Banks (depository institutions; financial intermediaries)3 Depositors (individuals and institutions)4 Borrowers (individuals and institutions)

The CB use of• reserve requirements• open market operations• discount loans

influences the other players’ actions leading to changes in themonetary aggregates

Francesco Franco Macroeconomics: Fluctuations and Growth 2/45

CB Balance Sheet

• Monetary Liabilities• Currency in circulation: in the hands of the public• Reserves: bank deposits at the Fed and vault cash

• Assets• Government securities: holdings by the CB that a�ect money

supply and earn interest• Discount loans: provide reserves to banks and earn the

discount rate

Francesco Franco Macroeconomics: Fluctuations and Growth 3/45

CB Balance Sheet

The CB controls the Monetary Base (aka high-powered money:H):

H = CU + R

CU: Currency in circulation R: Total reserves in the bankingsystem, namely RR + ERThe Fed has more control over the monetary base than overreserves:

1 Open market operations2 Discount loans

Francesco Franco Macroeconomics: Fluctuations and Growth 4/45

Open Market Purchase from a Bank

• Net result is that reserves have increased by $100• No change in currency• Monetary base and reserves have risen by $100

Francesco Franco Macroeconomics: Fluctuations and Growth 5/45

Open Market Purchase from a Nonbank

Case I: Person selling bonds to the Fed deposits the Fed’scheck in the bank

• Identical result as the purchase from a bank• No change in currency• Monetary base and reserves have risen by $100

Francesco Franco Macroeconomics: Fluctuations and Growth 6/45

Open Market Purchase from a Nonbank

Case II: The person selling the bonds cashes the Fed’scheck

• Reserves are unchanged• Currency in circulation increases by the amount of the open

market purchase• Monetary base increases by the amount of the open market

purchase

Francesco Franco Macroeconomics: Fluctuations and Growth 7/45

Random Shifts from Deposits into Currency

Net e�ect on monetary liabilities is zero. Reserves are changed byrandom fluctuations. Monetary base is a more stable variable.

Francesco Franco Macroeconomics: Fluctuations and Growth 8/45

Discount Loans to Banks

• Monetary liabilities of the Fed have increased by $100• Monetary base also increases by this amount

Francesco Franco Macroeconomics: Fluctuations and Growth 9/45

Other Factors A�ecting the Monetary Base

• Interventions in the foreign exchange market• Buying or selling foreign exchange• Similar to a open market operation• Usually sterilized, i.e. counteracted by operations that o�set

the change in the monetary base.

Francesco Franco Macroeconomics: Fluctuations and Growth 10/45

From H to M1

• By using its instruments, the CB controls the monetarybase/reserves

• How does this translate to control of broader monetaryaggregates?

• Mostly dependent on Deposit creation by banks

Francesco Franco Macroeconomics: Fluctuations and Growth 11/45

Deposit Creation: The Banking System

Excess reserves increase; banks loan out the excess reserves;creates a checking account; borrower makes purchases; the moneysupply has increased

Francesco Franco Macroeconomics: Fluctuations and Growth 12/45

Multiple Deposit Creation

• Assuming that banks do not hold excess reserves, i.e.

Required Reserves RR = Total Reserves TR

RR = ◊ ◊ D

◊ = is the required reserve ratioD= checkable deposits

• Dividing both sides by ◊:

D =RR◊

Francesco Franco Macroeconomics: Fluctuations and Growth 13/45

Multiple Deposit Creation

• Looking at changes:

�D =1◊�RR

• ◊ is the Simple deposit multiplier• Deposit creation continues until all excess reserves are

eliminated in the banking system• Note that whether the banks chooses to use its excess

reserves to make loans or buy securities does not matter

Francesco Franco Macroeconomics: Fluctuations and Growth 14/45

Summary

• A given level of reserves in the banking system determines thelevel of checkable deposits

• By controlling reserves, the CB controls the level of checkabledeposits

• By controlling checkable deposits, the Fed controls the moneysupply (M1)

• Critique of the Simple Model:• Holding cash stops the process• Banks may not use all of their excess reserves to buy securities

or make loans

Francesco Franco Macroeconomics: Fluctuations and Growth 15/45

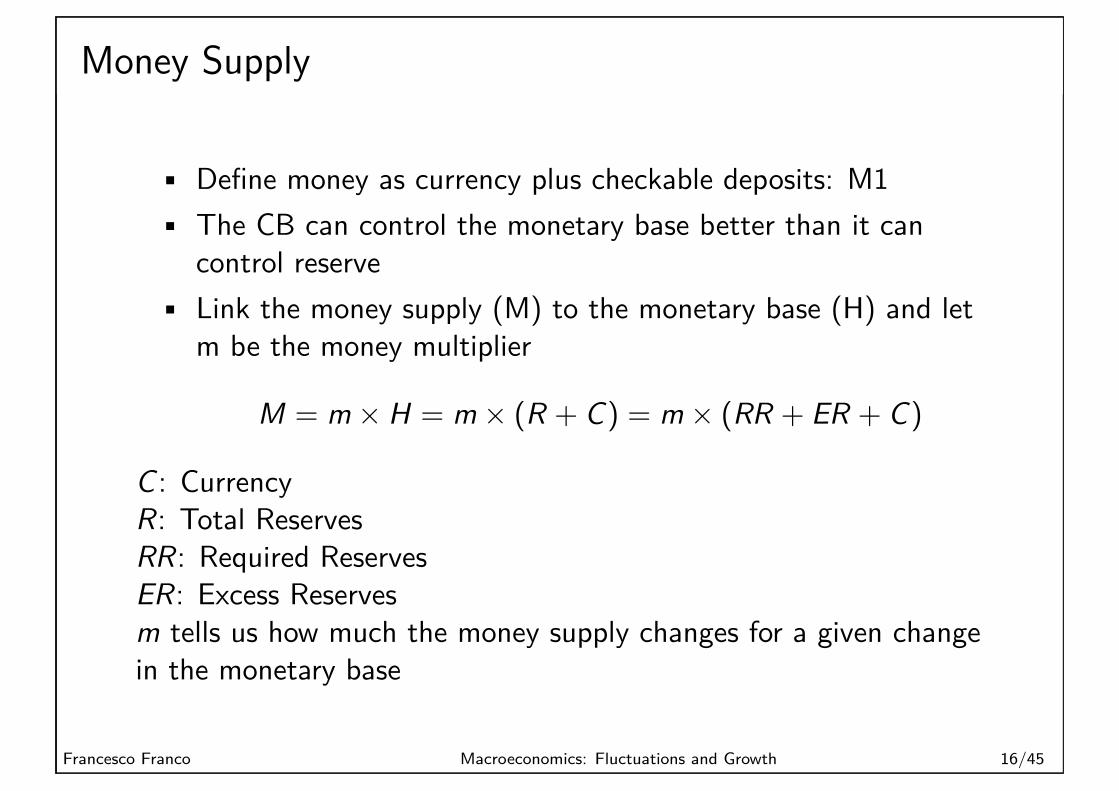

Money Supply

• Define money as currency plus checkable deposits: M1• The CB can control the monetary base better than it can

control reserve• Link the money supply (M) to the monetary base (H) and let

m be the money multiplier

M = m ◊ H = m ◊ (R + C) = m ◊ (RR + ER + C)

C : CurrencyR: Total ReservesRR: Required ReservesER: Excess Reservesm tells us how much the money supply changes for a given changein the monetary base

Francesco Franco Macroeconomics: Fluctuations and Growth 16/45

Money Supply

• RR = ◊ ◊ D, where ◊ < 1 is the required reserve ratio

H = RR + ER + C = ◊ ◊ D + ER + C

This reveals the amount of monetary base is needed tosupport the existing amounts of checkable deposits, excessreserves and currency

• An increase in H that goes into currency C is not multiplied,whereas an increase that goes into supporting deposits D ismultiplied

• An additional dollar of H that goes into excess reserves ERdoes not support any additional deposits or currency

Francesco Franco Macroeconomics: Fluctuations and Growth 17/45

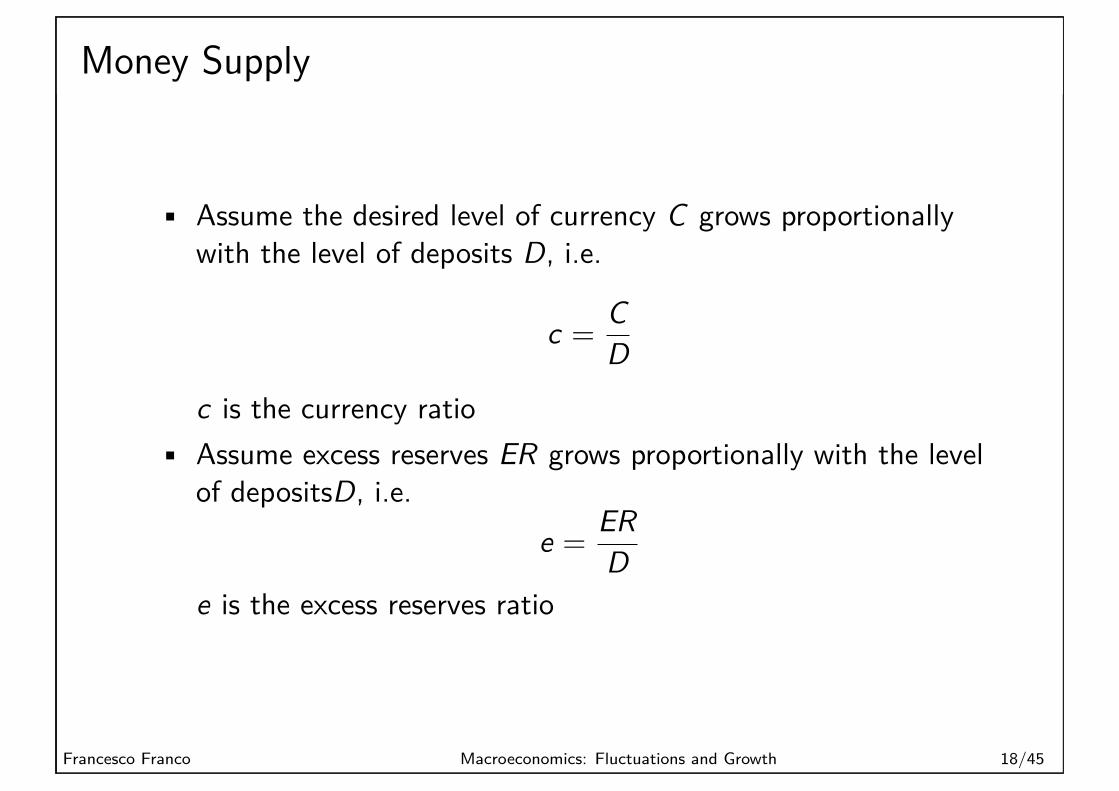

Money Supply

• Assume the desired level of currency C grows proportionallywith the level of deposits D, i.e.

c =CD

c is the currency ratio• Assume excess reserves ER grows proportionally with the level

of depositsD, i.e.e =

ERD

e is the excess reserves ratio

Francesco Franco Macroeconomics: Fluctuations and Growth 18/45

Money multiplier

H = R + C = RR + ER + C

RR = ◊ ◊ D, where r is the required reserve ratioER = e ◊ DC = c ◊ D

H = RR + ER + C = (◊ + e + c)◊ D

Francesco Franco Macroeconomics: Fluctuations and Growth 19/45

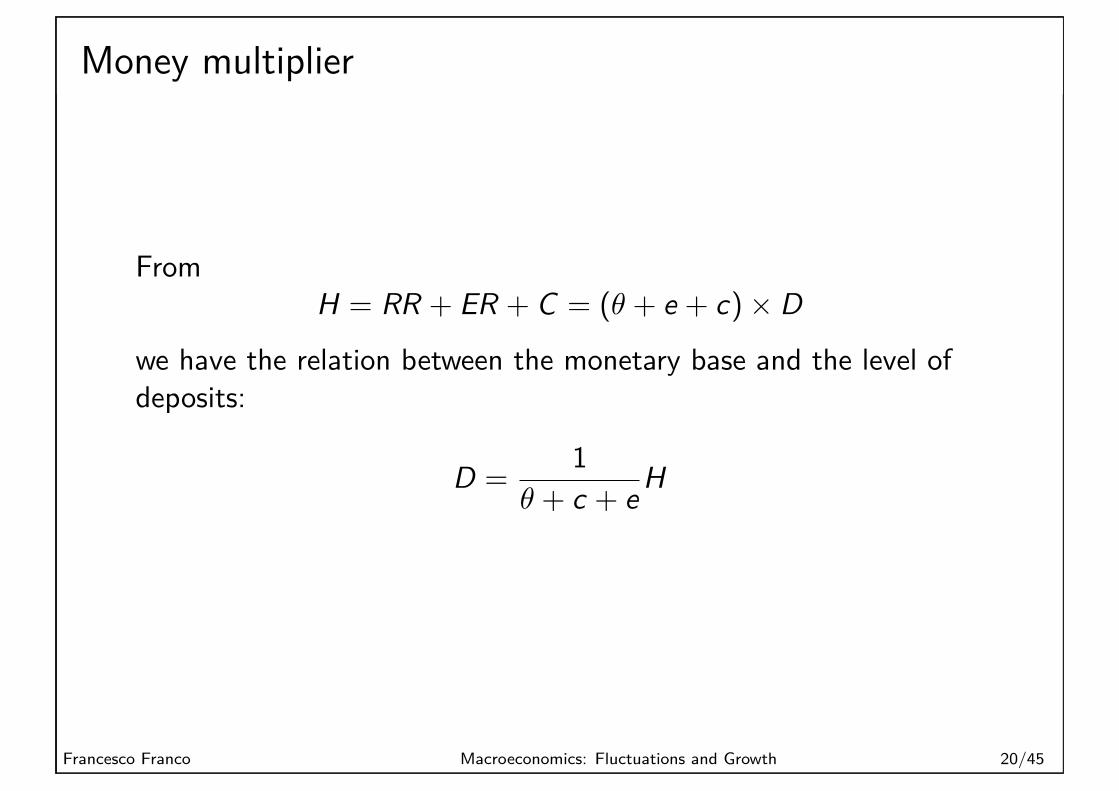

Money multiplier

FromH = RR + ER + C = (◊ + e + c)◊ D

we have the relation between the monetary base and the level ofdeposits:

D =1

◊ + c + e H

Francesco Franco Macroeconomics: Fluctuations and Growth 20/45

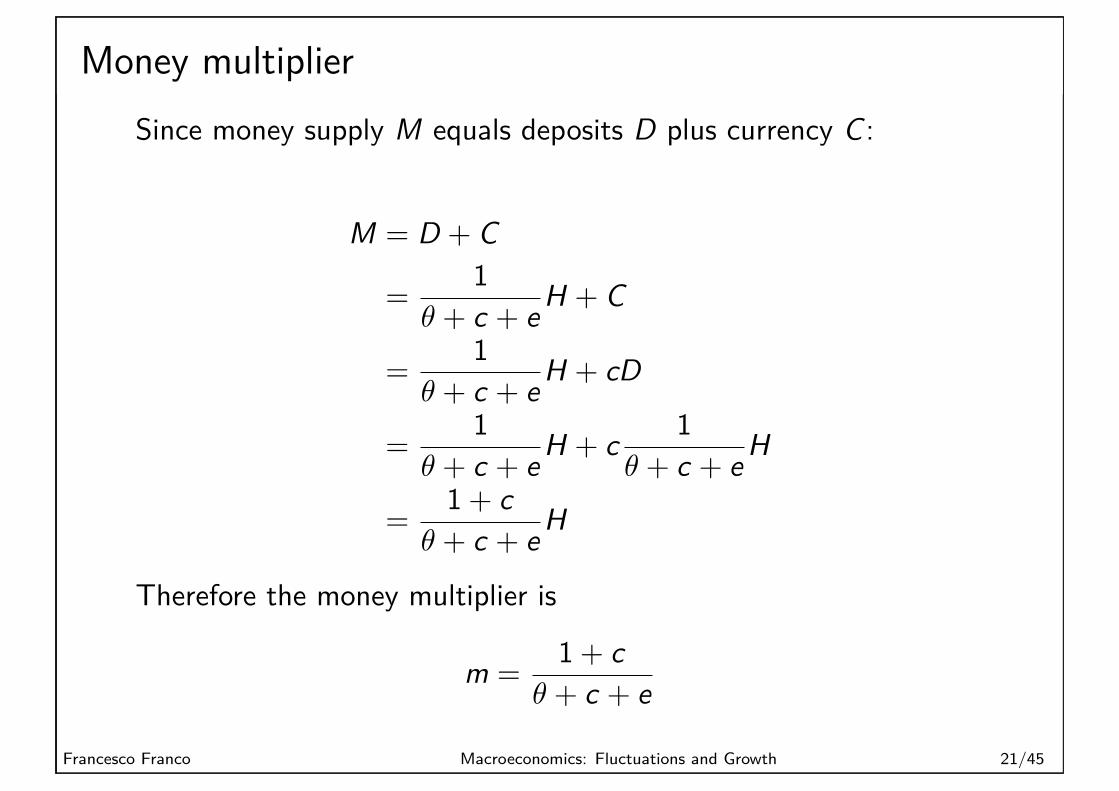

Money multiplierSince money supply M equals deposits D plus currency C :

M = D + C

=1

◊ + c + e H + C

=1

◊ + c + e H + cD

=1

◊ + c + e H + c 1◊ + c + e H

=1 + c◊ + c + e H

Therefore the money multiplier is

m =1 + c◊ + c + e

Francesco Franco Macroeconomics: Fluctuations and Growth 21/45

Money multiplier

◊= required reserve ratio = 0.10C= currency in circulation = $400BD= checkable deposits = $800BER= excess reserves = $0.8BM= money supply (M1) = C + D = $1200Bc= 0.5e= 0.001m¥ 2.5Compare with the simple deposit multiplier 1/r = 10

Francesco Franco Macroeconomics: Fluctuations and Growth 22/45

Money multiplier

m =1 + c◊ + c + e

• Changes in the required reserve ratio r The money multiplierand the money supply are negatively related to ◊

• Changes in the currency ratio c The money multiplier and themoney supply are negatively related to c

• Changes in the excess reserves ratio e The money multiplierand the money supply are negatively related to the excessreserves ratio e

Francesco Franco Macroeconomics: Fluctuations and Growth 23/45

Money multiplier

Moreover,• The excess reserves ratio e is negatively related to the market

interest rate i.e.i øæ e ¿æ m ø

Reserves do not pay any interest, so R is the opportunity costof holding reserves

• The excess reserves ratio e is positively related to expecteddeposit outflows i.e.

D outflows øæ e øæ m ¿

Reserves provide insurance against losses due to depositoutflows

Francesco Franco Macroeconomics: Fluctuations and Growth 24/45

Money multiplier

• Open market operations are controlled by the CB• The CB cannot determine the amount of borrowing by banks

from the CB• Split the monetary base into two components

MBn = MB≠BR therefore

M = m(MBn + BR)

• The money supply is positively related to both thenon-borrowed monetary base MBn and to the level ofborrowed reserves, BR, from the Fed

• In practice, the Fed generally sets the discount rate abovemarket interest rates such that BR is very small

Francesco Franco Macroeconomics: Fluctuations and Growth 25/45

Reserve market

Figure: Equilibrium in the market of reserves

Francesco Franco Macroeconomics: Fluctuations and Growth 26/45

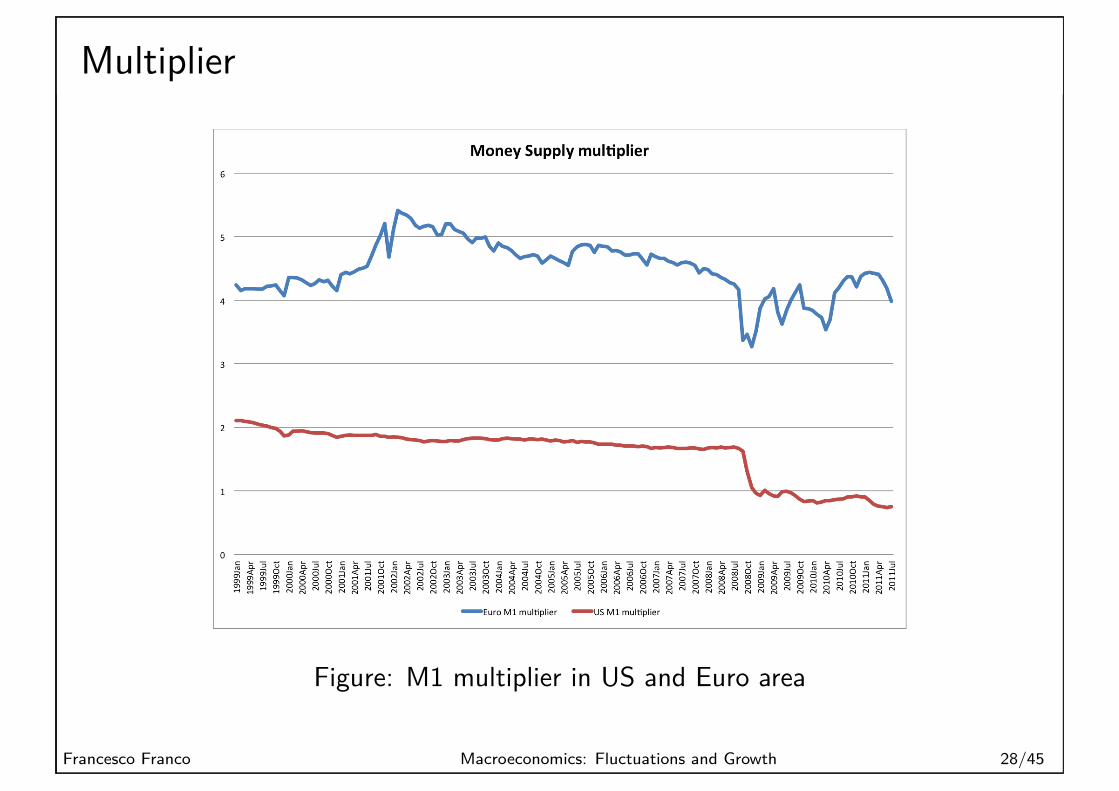

Multiplier

Figure: Currency in US and Euro areaFrancesco Franco Macroeconomics: Fluctuations and Growth 27/45

Multiplier

Figure: M1 multiplier in US and Euro area

Francesco Franco Macroeconomics: Fluctuations and Growth 28/45

Credit

• Money, the bank liability, is given a special role in thedetermination of aggregate demand

• Bank loans are lumped together with other debt instrumentsin a "bond market," which is then conveniently suppressed byWalras’ Law

Francesco Franco Macroeconomics: Fluctuations and Growth 29/45

Credit

• Importance of intermediaries in the provision of credit and thespecial nature of bank loans

• abandon the perfect substitutability assumption: 3 Assets,Money, Bonds and Loans

Francesco Franco Macroeconomics: Fluctuations and Growth 30/45

CreditImperfect subsitutes

• assume that both borrowers and lenders choose betweenbonds and loans according to the interest rates on the twocredit instruments

• Denote the interest rate on loans by fl, the loan demand is:

⇤d = ⇤(fl, i ,Y )

Francesco Franco Macroeconomics: Fluctuations and Growth 31/45

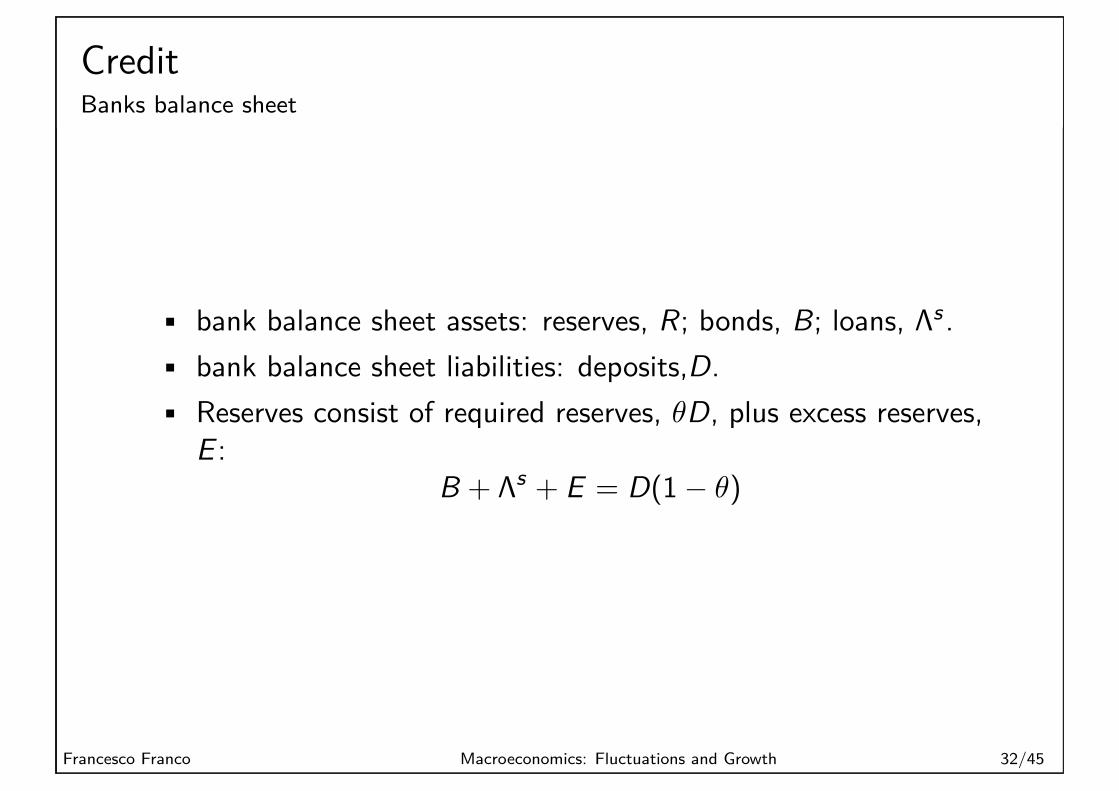

CreditBanks balance sheet

• bank balance sheet assets: reserves, R; bonds, B; loans, ⇤s .• bank balance sheet liabilities: deposits,D.• Reserves consist of required reserves, ◊D, plus excess reserves,

E :B + ⇤s + E = D(1≠ ◊)

Francesco Franco Macroeconomics: Fluctuations and Growth 32/45

CreditPortfolio choice

Assume the desired protfolio depends on the rate of returns, wehave

⇤s = ⁄(fl, i)D(1≠ ◊)

and similar equations for B and E . The clearing condition for theloan market is

⇤(fl, i ,Y ) = ⁄(fl, i)D(1≠ ◊)

Francesco Franco Macroeconomics: Fluctuations and Growth 33/45

Credit

Suppose bank excess reserves are

E = ‘(i)D(1≠ ◊)

and currency is zero

R = ‘(i)D(1≠ ◊) + ◊D

Francesco Franco Macroeconomics: Fluctuations and Growth 34/45

CreditDeposits

Now deposit demand is our usual money demand and equilibriumrequires

D(i ,Y ) = m(i)R

where the money multiplier is m(i) = [‘(i)(1≠ ◊) + ◊]≠1 .Now D(i ,Y ) and ⇤(i , fl,Y ) define the non bank Bond demandgiven total wealth is constant.

Francesco Franco Macroeconomics: Fluctuations and Growth 35/45

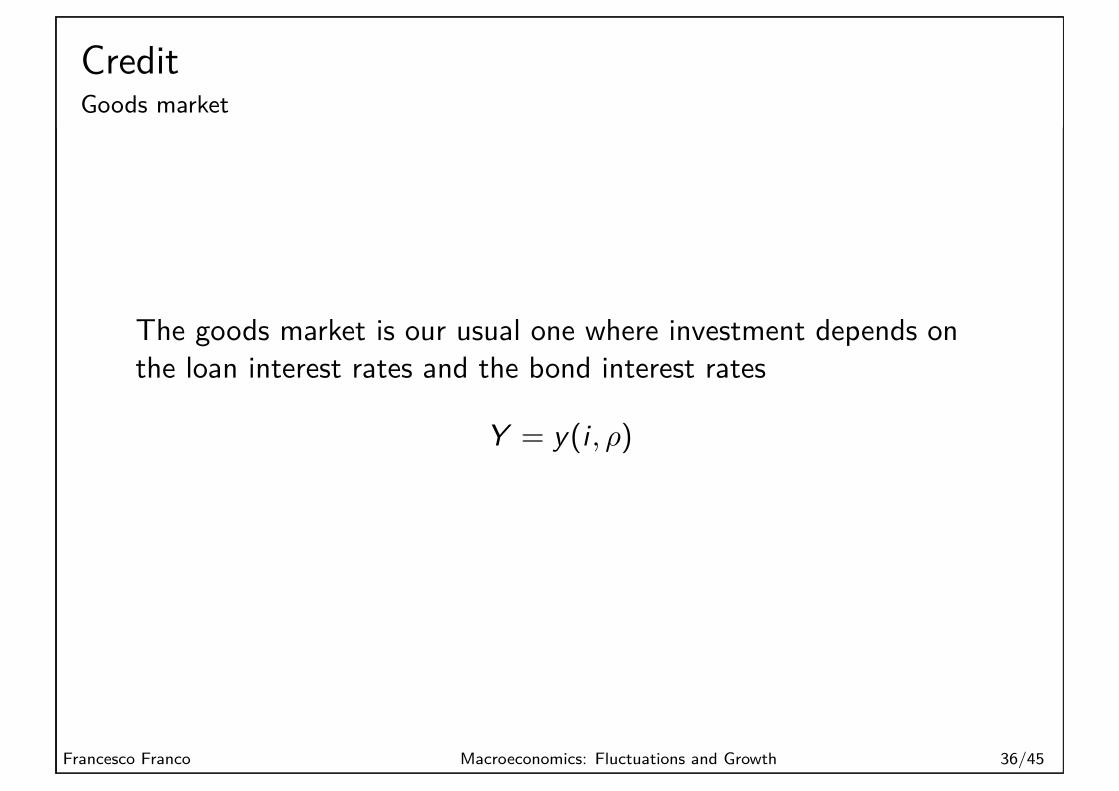

CreditGoods market

The goods market is our usual one where investment depends onthe loan interest rates and the bond interest rates

Y = y(i , fl)

Francesco Franco Macroeconomics: Fluctuations and Growth 36/45

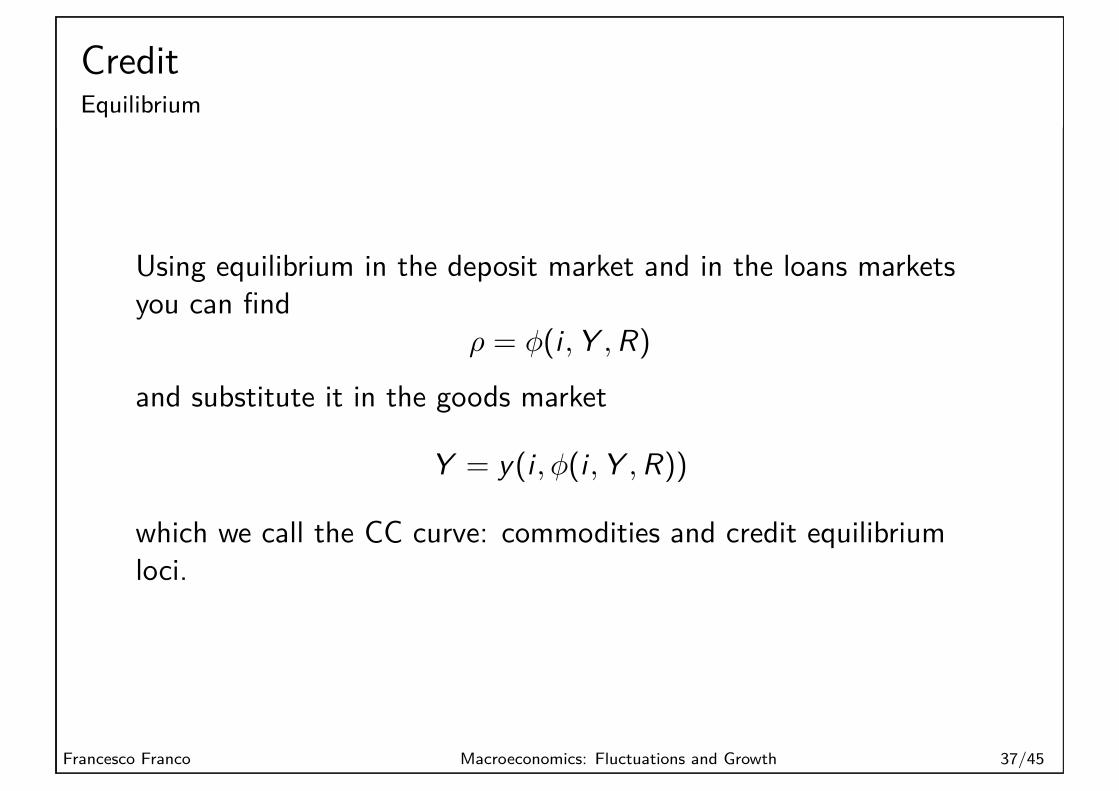

CreditEquilibrium

Using equilibrium in the deposit market and in the loans marketsyou can find

fl = „(i ,Y ,R)

and substitute it in the goods market

Y = y(i ,„(i ,Y ,R))

which we call the CC curve: commodities and credit equilibriumloci.

Francesco Franco Macroeconomics: Fluctuations and Growth 37/45

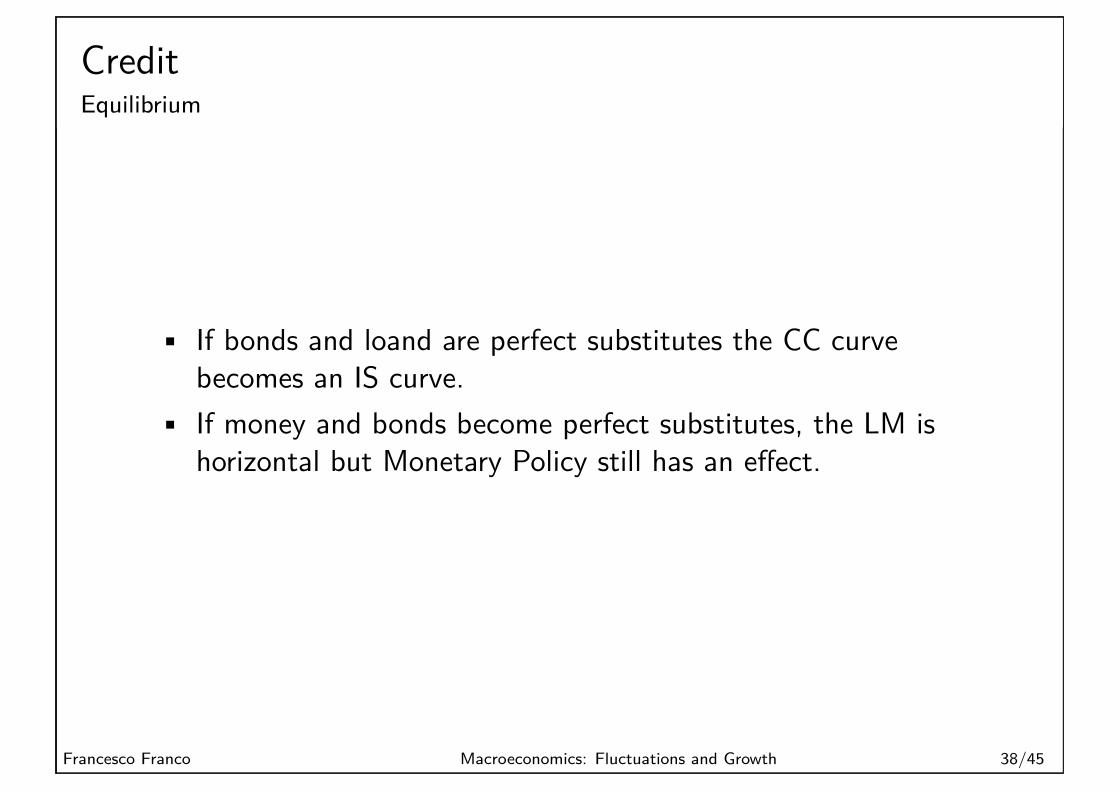

CreditEquilibrium

• If bonds and loand are perfect substitutes the CC curvebecomes an IS curve.

• If money and bonds become perfect substitutes, the LM ishorizontal but Monetary Policy still has an e�ect.

Francesco Franco Macroeconomics: Fluctuations and Growth 38/45

CreditEquilibrium

• An upward shift in the credit supply ⁄(.) shifts the CC curveupward, increase i and Y but decreases fl.

• Bernanke’s (1983) explanation for the length of the GreatDepression can be thought of as a downward shock to creditsupply stemming from the increased riskiness of loans andbanks’ concern for liquidity in the face of possible runs.

Francesco Franco Macroeconomics: Fluctuations and Growth 39/45

CreditTargets vs Indicators

• Target and indicator issues of monetary policy: the so- calledmonetary indicator problem arises if the central bank sees itsimpact on aggregate demand only with a lag but sees itsimpacts on financial-sector variables like interest rates, money,and credit more promptly.

Francesco Franco Macroeconomics: Fluctuations and Growth 40/45

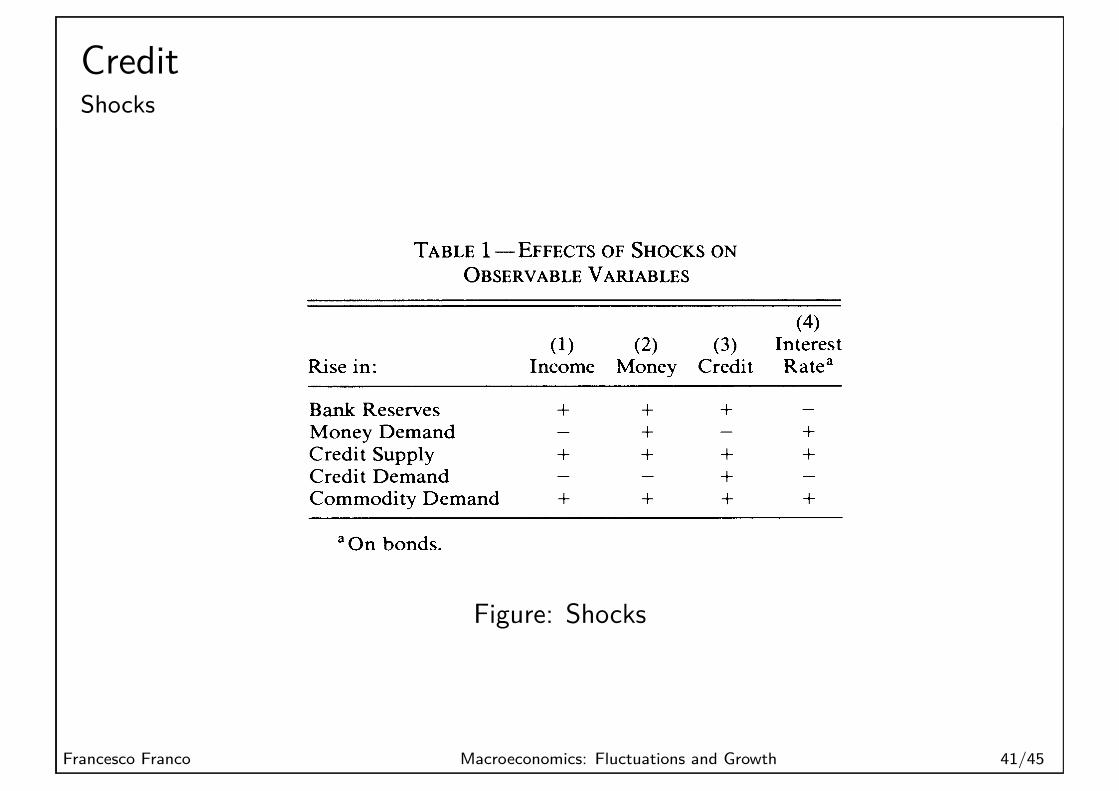

CreditShocks

438 A EA PAPERS AND PROCEEDINGS MA Y 1988

TABLE 1-EFFECTS OF SHOCKS ON OBSERVABLE VARIABLES

(4) (1) (2) (3) Interest

Rise in: Income Money Credit Ratea

Bank Reserves + + + Money Demand - + - + Credit Supply + + + + Credit Demand - - + Commodity Demand + + + +

aOn bonds.

to shocks to the supply of credit or to the money multiplier.

But suppose the demand for money in- creases (line 2), which sends a contractionary impulse to GNP. Since this shock raises M, a monetarist central bank would contract reserves in an effort to stabilize money, which would destabilize GNP. This, of course, is the familiar Achilles heel of monetarism. Notice, however, that this same shock would make credit contract. So a central bank try- ing to stabilize credit would expand reserves. In this case, a credit-based policy is superior to a money-based policy.

The opposite is true, however, when there are credit-demand shocks. Line 4 tells us that a contractionary (for GNP) credit- demand shock lowers the money supply but raises credit. Hence a monetarist central bank would turn expansionary, as it should, while a creditist central bank would turn contrac- tionary, which it should not.

We therefore reach a conclusion similar to that reached in discussing indicators: If money-demand shocks are more important than credit-demand shocks, then a policy of targeting credit is probably better than a policy of targeting money.

V. Empirical Evidence

The foregoing discussion suggests that the case for credit turns on whether credit de- mand is, or is becoming, relatively more stable than money demand. We conclude with some evidence that this is true, at least since 1979.6

TABLE 2-SIMPLE CORRELATIONS OF GROWTH RATES OF GNP WITH GROWTH RATES OF

FINANCIAL AGGREGATES, 1973-85a, b

Period With Money With Credit

1953:1-1973:4 .51,37 .17,11 1974:1-1979:3 .50,.54 .50,.51 1979:4-1985:4 .11,34 .38,.47

aGrowth rates are first differences of natural loga- rithms.

bCorrelations in nominal terms come first; correla- tions in real terms come second.

Table 2 shows the simple correlations be- tween GNP growth and growth of the two financial aggregates during three periods. Money was obviously much more highly cor- related with income than was credit during the period of stable money demand, 1953-73. But the two financial aggregates were on a more equal footing during 1974:1-1979:3. Further changes came during the period of unstable money demand, 1979:4-1985:4; money-GNP correlations dropped sharply while money-credit correlations fell only slightly, giving a clear edge to credit.7

More direct evidence on the relative magnitudes of money-demand and credit- demand shocks was obtained by comparing the residuals from estimated structural mon- ey-demand and credit-demand functions like D(*) and L(*) in our model. We used the logarithmic partial adjustment model, with adjustment in nominal terms, which we are not eager to defend but which was designed to fit money demand. Hence, our procedure seems clearly biased toward finding rela- tively larger credit shocks than money shocks.

Unsurprisingly, estimates for the entire 1953-85 period rejected parameter stability across a 1973:4-1974:1 break, so we con- centrated on the latter period.8 Much to our

6 In what follows, " money" is MI, "credit" is an aggregate invented by one of us: the sum of intermedi- ated borrowing by households and businesses (derived

from Flow-of-Funds data). For details and analysis of the latter, see Blinder (1985).

7Similar findings emerged when we controlled for many variables via a vector-autoregression and looked at correlations between VAR residuals.

8Estimation was by instrumental variables. Instru- ments were current, once, and twice lagged logs of real government purchases, real exports, bank reserves, and a supply shock variable which is a weighted average of the relative prices of energy and agricultural products.

Figure: Shocks

Francesco Franco Macroeconomics: Fluctuations and Growth 41/45

CreditEvidence

438 A EA PAPERS AND PROCEEDINGS MA Y 1988

TABLE 1-EFFECTS OF SHOCKS ON OBSERVABLE VARIABLES

(4) (1) (2) (3) Interest

Rise in: Income Money Credit Ratea

Bank Reserves + + + Money Demand - + - + Credit Supply + + + + Credit Demand - - + Commodity Demand + + + +

aOn bonds.

to shocks to the supply of credit or to the money multiplier.

But suppose the demand for money in- creases (line 2), which sends a contractionary impulse to GNP. Since this shock raises M, a monetarist central bank would contract reserves in an effort to stabilize money, which would destabilize GNP. This, of course, is the familiar Achilles heel of monetarism. Notice, however, that this same shock would make credit contract. So a central bank try- ing to stabilize credit would expand reserves. In this case, a credit-based policy is superior to a money-based policy.

The opposite is true, however, when there are credit-demand shocks. Line 4 tells us that a contractionary (for GNP) credit- demand shock lowers the money supply but raises credit. Hence a monetarist central bank would turn expansionary, as it should, while a creditist central bank would turn contrac- tionary, which it should not.

We therefore reach a conclusion similar to that reached in discussing indicators: If money-demand shocks are more important than credit-demand shocks, then a policy of targeting credit is probably better than a policy of targeting money.

V. Empirical Evidence

The foregoing discussion suggests that the case for credit turns on whether credit de- mand is, or is becoming, relatively more stable than money demand. We conclude with some evidence that this is true, at least since 1979.6

TABLE 2-SIMPLE CORRELATIONS OF GROWTH RATES OF GNP WITH GROWTH RATES OF

FINANCIAL AGGREGATES, 1973-85a, b

Period With Money With Credit

1953:1-1973:4 .51,37 .17,11 1974:1-1979:3 .50,.54 .50,.51 1979:4-1985:4 .11,34 .38,.47

aGrowth rates are first differences of natural loga- rithms.

bCorrelations in nominal terms come first; correla- tions in real terms come second.

Table 2 shows the simple correlations be- tween GNP growth and growth of the two financial aggregates during three periods. Money was obviously much more highly cor- related with income than was credit during the period of stable money demand, 1953-73. But the two financial aggregates were on a more equal footing during 1974:1-1979:3. Further changes came during the period of unstable money demand, 1979:4-1985:4; money-GNP correlations dropped sharply while money-credit correlations fell only slightly, giving a clear edge to credit.7

More direct evidence on the relative magnitudes of money-demand and credit- demand shocks was obtained by comparing the residuals from estimated structural mon- ey-demand and credit-demand functions like D(*) and L(*) in our model. We used the logarithmic partial adjustment model, with adjustment in nominal terms, which we are not eager to defend but which was designed to fit money demand. Hence, our procedure seems clearly biased toward finding rela- tively larger credit shocks than money shocks.

Unsurprisingly, estimates for the entire 1953-85 period rejected parameter stability across a 1973:4-1974:1 break, so we con- centrated on the latter period.8 Much to our

6 In what follows, " money" is MI, "credit" is an aggregate invented by one of us: the sum of intermedi- ated borrowing by households and businesses (derived

from Flow-of-Funds data). For details and analysis of the latter, see Blinder (1985).

7Similar findings emerged when we controlled for many variables via a vector-autoregression and looked at correlations between VAR residuals.

8Estimation was by instrumental variables. Instru- ments were current, once, and twice lagged logs of real government purchases, real exports, bank reserves, and a supply shock variable which is a weighted average of the relative prices of energy and agricultural products.

Figure: Evidence

Francesco Franco Macroeconomics: Fluctuations and Growth 42/45

CreditEvidence

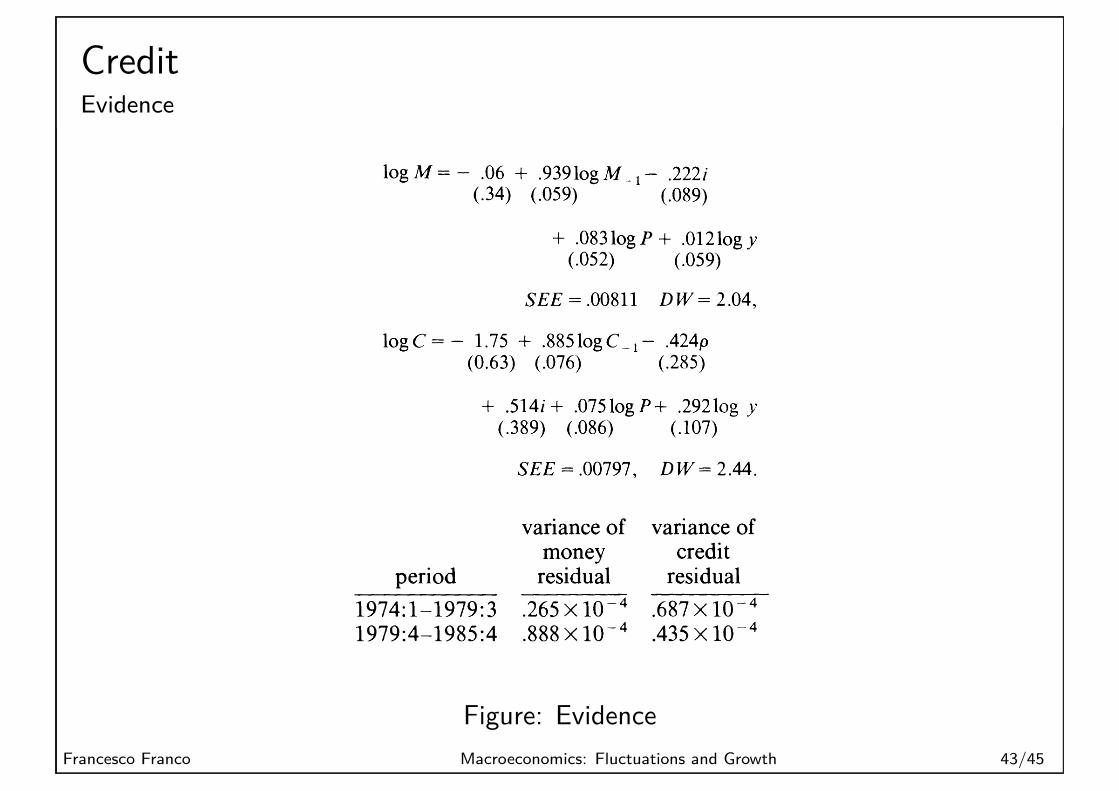

VOL. 78 NO. 2 IS IT MONEY OR CREDIT, OR BOTH, OR NEITHER? 439

amazement, we estimated moderately sensi- ble money and credit demand equations for the 1974:1-1985:4 period on the first try (standard errors are in parentheses):

log M=- .06 + .939 logM1- .222i (.34) (.059) (.089)

+ .083logP+ .012logy (.052) (.059)

SEE = .00811 D W = 2.04,

logC=- 1.75 + .885logC1 - .424p (0.63) (.076) (.285)

+ .514i+ .075logP+ .292log y (.389) (.086) (.107)

SEE =.00797, DW= 2.44.

Here y is real GNP, P is the GNP deflator, p is the bank prime rate, and i is the three- month Treasury bill rate. Although the inter- est rate coefficients in the credit equation are individually insignificant, they are jointly significant, have the correct signs, and are almost equal in absolute value-suggesting a specification in which the spread between p and i determines credit demand. Notice that the residual variances in the two equations are about equal.

Since the sample was too short to test reliably for parameter stability, we examined the residuals from the two equations over two subperiods with these results:

variance of variance of money credit

period residual residual 1974:1-1979:3 .265 x 10-4 .687 x 10-4 1979:4-1985:4 .888 x 10-4 .435 X 10-4

The differences are striking. By this crude

measure, the variance of money-demand shocks was much smaller than that of credit-demand shocks during the first sub- period but much larger during the second.

The evidence thus supports the idea that money-demand shocks became much more important relative to credit-demand shocks in the 1980's. But that does not mean we should start ignoring money and focusing on credit. After all, it is perfectly conceivable that the relative sizes of money-demand and credit-demand shocks will revert once again to what they were earlier. Rather, the mes- sage of this paper is that a more symmetric treatment of money and credit is feasible and appears warranted.

REFERENCES

Bernanke, Ben S., "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression," American Eco- nomic Review, June 1983, 73, 257-76.

Blinder, Alan S., "Credit Rationing and Effec- tive Supply Failures," Economic Journal, June 1987, 97, 327-52.

, "The Stylized Facts About Credit Aggregates," mimeo., Princeton Univer- sity, June 1985.

Brunner, Karl and Meltzer, Alan H., "Mon- ey, Debt, and Economic Activity," Journal of Political Economy, September/October 1972, 80, 951-77.

Patinkin, Don, Money, Interest, and Prices, New York: Harper and Row, 1956.

Poole, William, " Optimal Choice of Monetary Policy Instruments in a Simple Stochastic Macro Model," Quarterly Journal of Eco- nomics, May 1970, 2, 197-216.

Tobin, James, "A General Equilibrium Ap- proach to Monetary Theory," Journal of Money, Credit and Banking, November 1970, 2, 461-72.

VOL. 78 NO. 2 IS IT MONEY OR CREDIT, OR BOTH, OR NEITHER? 439

amazement, we estimated moderately sensi- ble money and credit demand equations for the 1974:1-1985:4 period on the first try (standard errors are in parentheses):

log M=- .06 + .939 logM1- .222i (.34) (.059) (.089)

+ .083logP+ .012logy (.052) (.059)

SEE = .00811 D W = 2.04,

logC=- 1.75 + .885logC1 - .424p (0.63) (.076) (.285)

+ .514i+ .075logP+ .292log y (.389) (.086) (.107)

SEE =.00797, DW= 2.44.

Here y is real GNP, P is the GNP deflator, p is the bank prime rate, and i is the three- month Treasury bill rate. Although the inter- est rate coefficients in the credit equation are individually insignificant, they are jointly significant, have the correct signs, and are almost equal in absolute value-suggesting a specification in which the spread between p and i determines credit demand. Notice that the residual variances in the two equations are about equal.

Since the sample was too short to test reliably for parameter stability, we examined the residuals from the two equations over two subperiods with these results:

variance of variance of money credit

period residual residual 1974:1-1979:3 .265 x 10-4 .687 x 10-4 1979:4-1985:4 .888 x 10-4 .435 X 10-4

The differences are striking. By this crude

measure, the variance of money-demand shocks was much smaller than that of credit-demand shocks during the first sub- period but much larger during the second.

The evidence thus supports the idea that money-demand shocks became much more important relative to credit-demand shocks in the 1980's. But that does not mean we should start ignoring money and focusing on credit. After all, it is perfectly conceivable that the relative sizes of money-demand and credit-demand shocks will revert once again to what they were earlier. Rather, the mes- sage of this paper is that a more symmetric treatment of money and credit is feasible and appears warranted.

REFERENCES

Bernanke, Ben S., "Nonmonetary Effects of the Financial Crisis in the Propagation of the Great Depression," American Eco- nomic Review, June 1983, 73, 257-76.

Blinder, Alan S., "Credit Rationing and Effec- tive Supply Failures," Economic Journal, June 1987, 97, 327-52.

, "The Stylized Facts About Credit Aggregates," mimeo., Princeton Univer- sity, June 1985.

Brunner, Karl and Meltzer, Alan H., "Mon- ey, Debt, and Economic Activity," Journal of Political Economy, September/October 1972, 80, 951-77.

Patinkin, Don, Money, Interest, and Prices, New York: Harper and Row, 1956.

Poole, William, " Optimal Choice of Monetary Policy Instruments in a Simple Stochastic Macro Model," Quarterly Journal of Eco- nomics, May 1970, 2, 197-216.

Tobin, James, "A General Equilibrium Ap- proach to Monetary Theory," Journal of Money, Credit and Banking, November 1970, 2, 461-72.

Figure: EvidenceFrancesco Franco Macroeconomics: Fluctuations and Growth 43/45

Summary

• Adding intermediaries and financial assets strenghten theimplications of the model.

• Monetary Policy has a role even with horizontal LM.

Francesco Franco Macroeconomics: Fluctuations and Growth 44/45

Readings I

Ben S. Bernanke and Alan Blinder.MCredit, Money, and Aggregate Demand.American Economic Review, Vol. 78, No. 2, May 1988.Olivier Blanchard, Alessia Aminghini and Francesco GiavazziMacroeconomics, a European Perspective.Prentice Hall, 2010, chapters 2-3.

Francesco Franco Macroeconomics: Fluctuations and Growth 45/45