march 24, 2018 milwaukee, wisconsin -...

TRANSCRIPT

2018 Spring National Meeting

© 2018 National Association of Insurance Commissioners

Title Insurance (C) Task Force

March 24, 2018 Milwaukee, Wisconsin

© 2018 National Association of Insurance Commissioners 1

Date: 3/15/18

2018 Spring National Meeting Milwaukee, Wisconsin

TITLE INSURANCE (C) TASK FORCE Saturday, March 24, 2018

2:00 – 3:00 p.m. Wisconsin Center—Room 103 A-C—1st Floor

ROLL CALL

Larry Deiter, Chair South Dakota Chlora Lindley-Myers Missouri David Altmaier, Vice Chair Florida Matthew Rosendale Montana Lori K. Wing-Heier Alaska Mark O. Rabauliman N. Mariana IslandsPeter Fuimaono American Samoa Bruce R. Ramge NebraskaMichael Conway Colorado Barbara D. Richardson NevadaStephen C. Taylor District of Columbia John G. Franchini New MexicoRalph T. Hudgens Georgia Mike Causey North CarolinaGordon I. Ito Hawaii Jillian Froment OhioDean L. Cameron Idaho John D. Doak OklahomaKen Selzer Kansas Raymond G. Farmer South CarolinaJames J. Donelon Louisiana Todd E. Kiser UtahAl Redmer Jr. Maryland Michael S. Pieciak VermontPatrick M. McPharlin Michigan Scott A. White VirginiaJessica Looman Minnesota

NAIC Support Staff: Jennifer Gardner/Aaron Brandenburg

AGENDA

1. Consider Adoption of its 2017 Fall National Meeting Minutes—Director Larry Deiter (SD) Attachment One

2. Hear a Presentation from Tridster and Demotech Regarding Partnership for Consumer Attachment Two Shopping Tool—Joseph Petrelli (Demotech)

3. Discuss Potential Update to the NAIC Survey of State Insurance Laws Regarding Title Attachment Three Data and Title Matters—Director Larry Deiter (SD)

4. Hear an Update Regarding Title Insurance Webinar—Jennifer Gardner (NAIC)

5. Discuss Any Other Matters Brought Before the Task Force—Director Larry Deiter (SD)

6. Adjournment

W:\National Meetings\2018\Spring\Agenda\TitleTF.dotx

© 2018 National Association of Insurance Commissioners

Attachment One Fall National Meeting Minutes

© 2017 National Association of Insurance Commissioners 1

Draft: 12/7/17

Title Insurance (C) Task Force Honolulu, Hawaii December 2, 2017

The Title Insurance (C) Task Force met in Honolulu, HI, and via conference call Dec. 2, 2017. The following Task Force members participated: Larry Deiter, Chair (SD); David Altmaier, Vice Chair, represented by Matthew Guy, Anoush Brangaccio and Jeffrey Joseph (FL); Lori K. Wing-Heier represented by Michael Ricker (AK); Dave Jones represented by Ken Allen and Emma Hirschhorn (CA); Marguerite Salazar represented by Michael Conway (CO); Stephen C. Taylor (DC); Ralph T. Hudgens represented by Margaret Witten (GA); Gordon I. Ito represented by Paul Yuen (HI); Stephen W. Robertson represented by Claire Szpara (IN); James J. Donelon represented by Warren Byrd (LA); Nancy G. Atkins represented by Tony Butler (KY); Al Redmer Jr. represented by Erica Bailey (MD); Patrick M. McPharlin represented by Jean Boven (MI); Jessica Looman represented by Martin Fleischhacker (MN); Chlora Lindley-Myers represented by Carrie Couch and Leslie Nehring (MO); Bruce R. Ramge represented by Matt Holman (NE); John G. Franchini (NM); Kent Sullivan represented by J’ne Byckovski and Marianne Baker (TX); Todd E. Kiser represented by Suzette Green-Wright (UT); Jacqueline K. Cunningham represented by Mike Beavers (VA); Michael Pieciak represented by Christina Rouleau (VT); and Mike Kreidler represented by Eric Slavich (WA). Also participating was: Ted Hamby (NC).

1. Adopted its Oct. 16 Meeting Minutes

The Task Force met Oct. 16 and took the following action: 1) adopted its Summer National Meeting minutes; and 2) adopted its 2018 proposed charges. Mr. Byrd made a motion, seconded by Mr. Conway, to adopt the Task Force’s Oct. 16 minutes (Attachment One). The motion passed unanimously.

2. Adopted a Report from the Title Insurance Financial Reporting (C) Working Group

Mr. Brandenburg said the Title Insurance Financial Reporting (C) Working met Sept. 7 to review a proposal to include known claims reserve (KCR) within Exhibit A of the Statement of Actuarial Opinion (SAO). After taking comments from interested parties and state insurance regulators, the Working Group decided not to move forward with the proposal for appointed actuaries to include KCR in the SAO. NAIC staff developed and distributed aggregate industry reports using exhibits from the title insurance annual financial statement for Working Group members to review and provide feedback.

Mr. Byrd made a motion, seconded by Ms. Green-Wright, to adopt the report of the Title Insurance Financial Reporting (C) Working Group (Attachment Two). The motion passed unanimously.

3. Heard a Presentation from States Title Regarding the Use of Predictive Analytics in Underwriting for Title Insurance

Adrienne Harris (States Title) said most loans are sold to government-sponsored enterprises (GSEs), which require a lenders policy. There are approximately 10 million policies written per year, and the market is approximately $14 billion in premiums written. The market is 100% larger with the inclusion of closing and settlement fees. Four underwriters— Fidelity, First American, Old Republic and Stewart—make up approximately 50% of the market. Title insurance historically has very low claims, the majority of which are related to fraud. The loss ratio is approximately 5%. Eighty-nine percent of the premiums written are attributable to operating expenses. The net income for the largest title insurance underwriters is approximately 6%.

States Title expects to launch a new lenders policy product for refinance agreements and home equity lines of credit (HELOC) beginning the week of Dec. 4. Ms. Harris said States Title has secured agreements to launch with two lenders. She said the company is working with the Federal Housing Administration (FHA) and GSEs to ensure that the products they develop meet lender requirements. The company expects to launch products for property purchases at a later date.

Ms. Harris said in a refinance transaction, lenders typically suggest the title underwriter to the borrower, and the borrower purchases the policy on behalf of the lender. Typically, title underwriters search property databases, public records and other proprietary sources for liens, encumbrances and other information pertinent to the property. This information becomes the title report. The title insurer and loan processor negotiate the records to become part of the policy and defects cured before the loan is closed. States Title estimates that this negotiation takes approximately five to 10 business days and constitutes about 15% of the operating expenses charged as part of the premium. Lenders estimate that the negotiation and curative measures consume a majority of the margin they expect to make on the loan. Lenders acknowledge that the appraisal takes longer to obtain, but securing the title requires more negotiation and time on the part of the lender.

© 2017 National Association of Insurance Commissioners 2

States Title will replace the title search with a predictive analytics algorithm. The algorithm uses the property address to predict the likelihood of a title claim. Using this method, a comprehensive title commitment can be delivered in five to 10 seconds instead of five to 10 business days. States Title will provide comprehensive coverage with no exclusions, and they expect to have a higher loss ratio than traditional title insurers. Ms. Harris said the company estimates their loss ratio to be approximately 9%. Due to the company’s low operating expenses and marginally higher loss ratio, Ms. Harris said the company expects to pass on significant savings to consumers.

Ms. Harris said States Title is a member of the American Land Title Association (ALTA), and the company intends to write business on standard ALTA policy forms. States Title is in the process of securing an underwriter license in multiple states, including California, and has Certificates of Authority (COA) allowing it to transact business in Arizona and Illinois. Ms. Harris said the company is a full title insurance operation with a joint venture (JV) partner. The JV partner will be available to perform traditional search and curative services, as well as provide closing, settlement and escrow account management.

The company is backed by reinsurance from SCOR Global. SCOR has agreed to cover 100% of losses incurred by States Title for its first three years of operations. The algorithm is designed to be scaled to the risk appetite of States Title and the reinsurer. Transactions deemed too high risk for States Title or SCOR Global will be sent to the JV partner to underwrite in the traditional manner, curing potential defects in advance of the loan closing.

Mr. Deiter asked how States Title has worked with the GSEs to ensure that the products developed meet GSE loan requirements. Ms. Harris said Max Simkoff, founder of States Title, began working with Fannie Mae approximately one year ago. The GSEs have three basic requirements. First, States Title had to certify that the mortgagor would always be in the first lien position. Second, States Title proved the validity and success rate of the algorithm by testing its ability to predict foreclosure rates using existing transactions. Finally, as a startup, States Title does not have a credit rating, so the company has to qualify for a waiver. The waiver is an agreement between the GSEs and the lender. To qualify, States Title performed financial stability stress testing using A.M. Best’s rating methodology. Additionally, the company secured a 100% reinsurance agreement with SCOR Global to accommodate the solvency requirement. Ms. Harris said the company anticipates the lenders with whom the company has agreed to do business will sign the waiver with the GSEs early the week of Dec. 4.

Mr. Franchini asked how States Title’s business model differs from the traditional model using title plants and vast quantities of data. Ms. Harris said States Title will not exclude anything from the policy other than outstanding mortgages and current property taxes. She said the company uses different data sources than a traditional title insurer. A traditional insurer uses county records to search for mechanic’s liens. States Title uses an algorithm to search hundreds of data points. It uses permitted construction filings instead of county records to determine the likelihood of a mechanic’s lien based on the type and length of time required to complete construction. The property is given a risk score based on data States Title believes to be much more predictive of claims.

Mr. Byrd asked for an estimate of the premium savings States Title expects to afford its customers. Ms. Harris said States Title has filed rates in the bottom 10% of the current market in the states it is licensed to operate. As the company acquires more loss history, it expects to drop 10% to 15% below the bottom of the current market. The state insurance regulators with whom States Title has worked requested that they not undercut the market too much without the loss history to support it. Mr. Byrd said current title policies often have exclusions for outstanding mechanic’s liens. Ms. Harris said because the algorithm is not looking explicitly for mechanic’s liens but instead projecting the propensity for a property to encounter a mechanic’s lien, the policy would not contain any such exclusion.

Ms. Byckovski asked for an explanation of the variables included in the algorithm. Ms. Harris said there are approximately 190 variables included in the algorithm, which is constantly changing and uses machine learning. She said the majority of the data used by the algorithm is census data in addition to proprietary data and some traditional data points used by most title insurers. She said data regarding the borrower is excluded from the data currently but they have considered using FICO information in the future. Approximately 12 variables have been identified as highly predictive of title risk; an example is the expected appreciation rate of the neighborhood. States Title has been working with state insurance regulators to explain the model and the data science behind the algorithm. Mr. Deiter said the availability of public data may be harder to find in certain regions. Ms. Harris said the algorithm accounts for this variability in the access of property data in some regions by using more data sources than a traditional insurance underwriter.

Mr. Franchini welcomed States Title to work with New Mexico regarding the legislation required to make their business model possible in the state.

© 2017 National Association of Insurance Commissioners 3

Mr. Yuen asked how States Title expects to handle claims. Ms. Harris said States Title will pay out claims expeditiously and seek recovery and subrogation after the policyholder has been paid. The current reinsurance arrangement will cover all claims incurred during the first three years of operation, and the company intends to seek a quota share agreement thereafter. The company, based in San Francisco, has in-house claims counsel, as well as a third-party administrator to assist with claims handling.

Mr. Birnbaum asked if the cost of the policy will vary by location or value of the property. Ms. Harris said the cost of the policy will vary by the value of the property, just as it does with traditional title insurance. Mr. Birnbaum asked how the company intends to eliminate the bias of higher foreclosure rates for low income individuals and minority communities that became prevalent after the period of predatory lending leading up to the financial crisis. Ms. Harris stated that the company does not use borrower data and they have worked with the Consumer Financial Protection Bureau (CFPB) as well as the Federal Housing Administration (FHA) to test their algorithms. The company will write policies for all loans, even those with higher risk. Low risks will be underwritten using the algorithm, and high-risk transactions will be underwritten using traditional title insurance methods, including curative services. Mr. Birnbaum asked how the company intends to gain business. Ms. Harris said the company will work with lenders to sell their approach and customer service model but will not engage in illegal inducements or affiliated business arrangements.

4. Heard an Update Regarding Title Insurance Education Course Materials

Ms. Boven said in April 2016, the Task Force discussed the need for a title insurance education course. Michael Draminski (MI), Krystle Ledvina Garcia (NE) and Otis Phillips (NM) drafted course materials designed to be a training guide for state insurance regulators new to title insurance regulation. She said the plan is to offer the course through the NAIC Education & Training Department in regulator-to-regulator session in the spring of 2018. The course may be offered again in open session at a later date. Questions or comments may be sent to NAIC staff no later than Dec. 29.

5. Heard an Update on Federal Activities

Mr. Brandenburg said the TRID (TILA-RESPA Integrated Disclosure) Improvement Act (H.R. 3978) was introduced by U.S. Rep. French Hill (R-AR) on Oct. 5 and passed by the House Financial Services Committee by a vote of 53 to 5 on Nov.15. The bill would amend the federal Real Estate Settlement Procedures Act of 1974 (RESPA) to require the CFPB to allow for the calculation of the discounted rate that title insurance companies may provide to consumers when they purchase a lenders and owners title insurance policy simultaneously.

Mr. Brandenburg said the NAIC supports the Business of Insurance Regulatory Reform Act (H.R. 3746), which was introduced in the U.S. House of Representatives on Sept. 12 by U.S. Rep. Sean Duffy (R-WI) and U.S. Rep. Gwen Moore (D-WI). U.S. Sen. Tim Scott (R-SC) has offered to introduce the Senate companion bill. The bill would clarify the authority of the CFPB with respect to persons regulated by a state insurance regulator.

Having no further business, the Title Insurance (C) Task Force adjourned.

W:\National Meetings\2017\Fall\TF\Title\_Final Minutes\TitleTF12-2 minutes.docx

© 2018 National Association of Insurance Commissioners

Attachment Two Demotech and Tridster

Presentation

March 24, 2018

1

Consumer education is important to improve title insurance buyingdecisions. Consumers deserve to know that their insurer can honor ameritorious claim.

2

3

1986 – MBA

Research

1992 – Began rating

Title insurers

1996 – Conferenc

e of Consultin

g Actuaries

1999 – Commerce

Clearing House

publication

1994 – Fannie Mae

promulgated Title

underwriter requirements

2001 – Manage Ohio

Title Insurance Rating Bureau

Reviewed State

of Iowa reserving

procedures

Began consulting for

NC Title Insurance

Bureau

2002 - Assisted Iowa with

implementation of closing protection coverage program

2003 – Acquired

Performance of Title

Insurance Companies

2004 – Reviewed Iowa Title insurance L&LAE reserves

Manage

Louisiana Title Insurance

Bureau

2014 – Agreed to

administer Indiana Title

Demotech’s review and analysis process is the most comprehensive in the Titlesector.

Demotech performs quarterly financial reviews on each Title underwriter,including a review of reinsurance treaties. This means that all underwriters arescrutinized every three months.

4

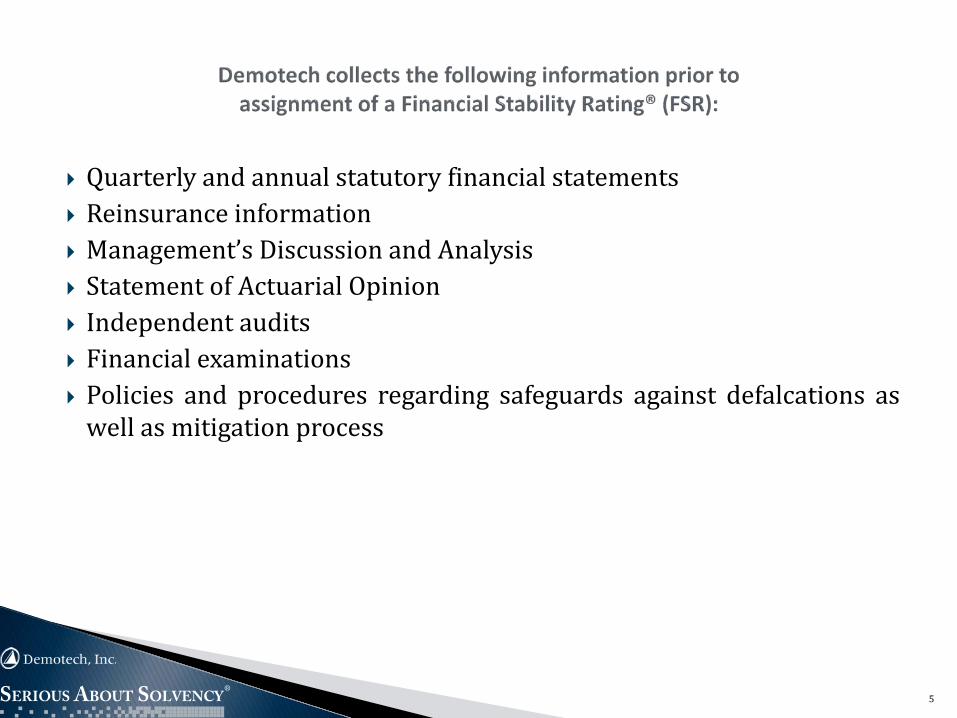

Quarterly and annual statutory financial statements Reinsurance information Management’s Discussion and Analysis Statement of Actuarial Opinion Independent audits Financial examinations Policies and procedures regarding safeguards against defalcations as

well as mitigation process

5

Policies and procedures regarding agent appointments Business plans Pro forma financial statements (when applicable) Investment guidelines Proposed underwriting guidelines Biographical information on principals and key employees (when

applicable) Proposed marketing and sales materials (when applicable).

6

“For three years, I led the State of Nebraska Department of Insurance as its Commissioner. No federal agency is tasked with reviewing solvency oversight of title insurance companies. This responsibility resides with state insurance regulators. As a state regulator, my responsibilities included national financial and solvency oversight of title underwriters domesticated in Nebraska although they do business nationally. I came to know Demotech for this reason. I was charged with national solvency and financial regulation for the title underwriters, or insurers, under the now defunct, LandAmerica Financial Group, including Lawyers Title Insurance Corporation and Commonwealth Land Title Insurance Company. Nebraska also provides the financial oversight of those underwriters within Fidelity National Title group. In carrying out my duties, I became familiar with the practices of rating organizations for the title insurance industry. In 2008, I benefited particularly from the assistance of Demotech when LandAmerica Financial Group, as a publicly traded insurance holding company, sought to respond to the housing market crisis by raiding its subsidiary title underwriters’ funds for support. To protect the policyholders under LandAmerica’s bankruptcy, I seized the title underwriters and sold them to Fidelity National Title. During this process, I learned that Demotech’s superior grasp of the intricacies of the title insurance industry exceeded that of other rating organizations. Without their quick assistance based upon a deep knowledge of the industry, I doubt my efforts would have been successful without their insights and assistance.”

7

2014 – What We’ve Got Here is a Failure toCommunicate (update to 2006 whitepaper)

2012 – Escrow Theft: Today’s Challenge inTitle Insurance

2008 – Demotech, Inc.’s Perspective ofCommonwealth Land Title InsuranceCompany and Lawyers Title InsuranceCorporation

2006 – What We’ve Got Here is a Failure toCommunicate, How Traditional FinancialReporting Contributes to Misunderstandingof Title Insurance Loss Activity

2005 – A Primer on the Basics of the Use ofTitle Insurance in the United States (updateto 2000 whitepaper)

2003 – Defalcations: Today’s Challenge inTitle Insurance and our Thoughts onAddressing this Challenge

2000 – A Primer on the Basics of the Use ofTitle Insurance in the United States

Title Insurance: A Guide to Regulation,Coverage and Claims Process in Ontario

1992 – FirstRate/Title: The First Word inTitle Ratings

8

Publications Authored by Joseph Petrelli and Demotech

9

Tridster, the leading price comparison provider for title insurance and settlement services, recently joined forces with Demotech to provide consumers with Demotech’s Financial Stability Ratings® (FSRs) as consumers comparison shop title insurance and settlement costs. Demotech believes that consumers benefit when they are able to compare the costs of insurance and services as well as the financial stability of the insurer providing the insurance. Demotech receives no compensation, directly or indirectly, for providing this information. As the only entity to review and rate all Title underwriters, in addition to hundreds of regional and specialty P&C insurers, Demotech is pleased to complement Tridster’s efforts to help consumers make smart buying decisions.

10

Tridster

Copyright © by Tridster LLC 2018

Presented to the NAIC Tit le Insurance Task Force

March 24, 2018

Helping Consumers Shop For Tit le Insurance

Thank you to the NAIC Tit le Insurance Task Force for providing us with the opportunity to part icipate in this important and t imely forum.

Contents:

● About Tridster● Consumers are going online to shop for t it le insurance in increasing numbers● Consumers are asking good quest ions online● Piecing it all together can be overwhelming● Tridster delivers t it le insurance information to consumers in a convenient and intuit ive format● Founded by an experienced team● Backed by an industry leader in financial technology development● Thank you

2

● Founded in June 2016

● Tridster is a financial technology startup

● Focused on providing real estate consumers with t it le insurance and sett lement services information

● We officially launched our online price comparison service in the Spring of 2017

● We believe that there is significant consumer demand for online t it le insurance and sett lement services information

About Tridster

3

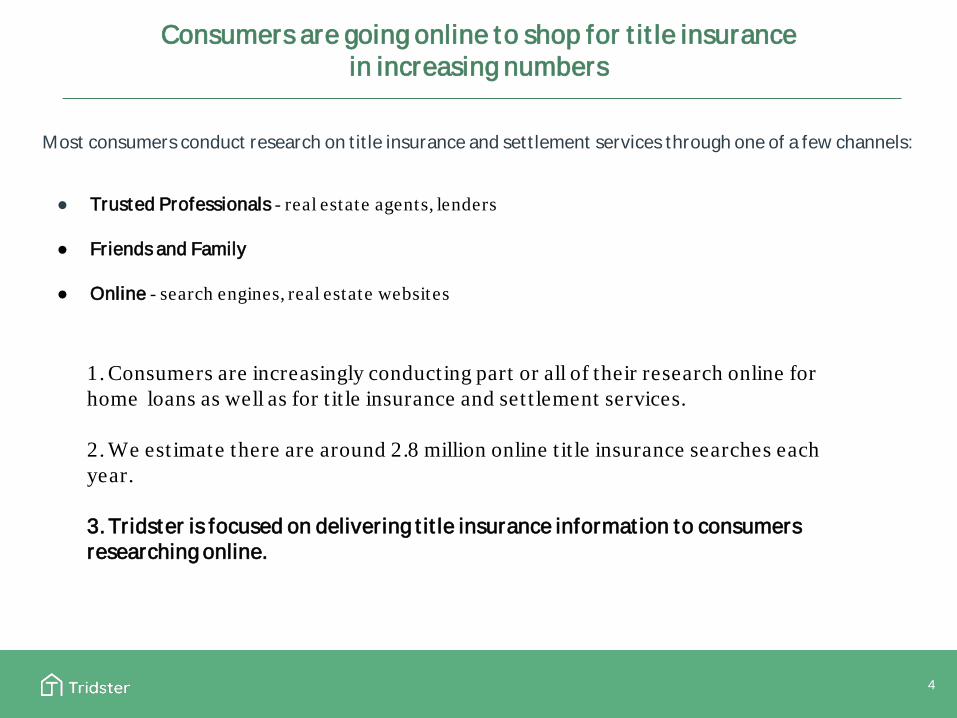

Most consumers conduct research on t it le insurance and sett lement services through one of a few channels:

● Trusted Professionals - real estate agents, lenders

● Friends and Family

● Online - search engines, real estate websites

Consumers are going online to shop for t it le insurance in increasing numbers

1. Consumers are increasingly conducting part or all of their research online for home loans as well as for t it le insurance and set t lement services.

2. We est imate there are around 2.8 million online t it le insurance searches each year.

3. Tridster is focused on delivering t it le insurance informat ion to consumers researching online.

4

Consumers are asking good quest ions online

General Product Understanding ● What is t it le insurance? ● How do I shop for this product?

Providers ● Who sells this product? ● What dist inguishes one provider from another and are they reliable?

Pricing ● How much does this product cost? ● Is there a difference in cost between different providers?

5

● Real estate blogs ● Tit le insurance underwriter websites ● Tit le insurance agency websites ● State insurance department websites ● Companies that rate t it le underwriters (such as Demotech)

Piecing it all together can be overwhelming

Title insurance is an unfamiliar product for many if not most consumers.

In a real estate t ransact ion, consumers usually have very limited t ime to research t it le insurance; as a result , many do not shop for it .

Answers to consumer quest ions are dispersed across many online resources - it can take a significant amount of t ime to locate informat ion across all of them:

6

Tridster delivers t it le insurance informat ion to consumers in a convenient and intuit ive format

7

A simple, online comparison plat form

Tridster provides consumers with a view of t it le products and services available in their market Comparat ive pricing

Product and pricing details in an easy to understand, comparat ive format Financial rat ings

Tit le insurer Financial Stability Rat ings® from trusted, 3rd-party rat ing firm Demotech

8

State-specific educat ional materials

Helpful market context and informative resources on t it le insurance Regulatory Resources

An organized set of links to important state-specific regulatory resources for consumers

Tridster delivers t it le insurance informat ion to consumers in a convenient and intuit ive format

Founded by an experienced team

9

Our founding team is made up of seasoned entrepreneurs and professionals with experience building and running consumer credit , technology, data analyt ics, and capital markets businesses.

Jordan Cohen Co-Founder Mortgage Capital Markets Brown University

William DeVar CEO Product/Biz Dev/Member of founding team at Better Mortgage, Partner at 1/0 Capital University of Virginia

Steve Berg Co-Founder MD at LPS, Inc., President of McDash Analyt ics (exited to FIS) The Pennsylvania State University

William Buell Co-Founder Real Estate Investment Banking University of Texas

Backed by an indust ry leader in financial technology development

10

a leading investor in cutt ing-edge consumer finance companies, including

In summary

Consumers are going online in increasing numbers to gather information about t it le insurance. While there is a tremendous amount of information available online, it is dispersed across many different locat ions on the internet, making effect ive shopping a difficult and t ime-consuming exercise for most.

Tridster is working to gather and organize information around t it le insurance markets, providers, products, and costs in order to make it possible for more consumers to quickly get the information they need in one place for their home purchase or refinance t it le insurance transact ion.

11

Thank you again to the NAIC Tit le Insurance Task Force for giving us the opportunity to part icipate.

Quest ions

William DeVar - CEO [email protected]

+1 (434) 465-8448

12

Links to selected Tridster Resources

● Tridster website

○ Tridster Homepage ○ Example of state FAQ page

● Tridster research

○ How much consumers can save in PA

Appendix

13

© 2018 National Association of Insurance Commissioners

Attachment Three NAIC Survey of State Insurance Laws Regarding Title Data and Title Matters

NAIC Title Insurance (C) Task Force

Survey of State Insurance Laws Regarding Title Data

and Title Matters November 2015

The Title Insurance (C) Task Force conducted a survey of each jurisdiction’s laws and regulations regarding title insurance. The Task Force agreed at the 2015 Spring National Meeting to update the Survey of State Insurance Laws Regarding Title Data and Title Matters. The survey’s intent is to be a tool for regulators and interested parties to gain insight into the regulation of title insurance. The survey was enhanced by the Task Force members and sent out for completion in June 2015. Respondents were the insurance department or other jurisdictional agency responsible for title agents or title insurance as appropriate in each jurisdiction. The information in this document contains the results of the survey. The initial responses were provided in SurveyMonkey. Great care was taken in assembling and compiling the responses that appear in the summarized tables that follow. Each jurisdiction will be given an opportunity to review the data for accuracy. Requests for revisions can be sent to Jennifer Gardner at [email protected]. DISCLAIMER THE DATA REFLECTED IN THIS REPORT WAS VOLUNTARILY SUBMITTED BY STATE INSURANCE DEPARTMENTS. THE NAIC DOES NOT GUARANTEE THE TRUTH, ACCURACY, QUALITY OR COMPLETENESS OF THE DATA AND IS NOT RESPONSIBLE FOR ERRORS, OMISSIONS OR RESULTS OF FURTHER USE OF THE DATA. THE DATA SUBMITTED MAY REFLECT ONLY THE OPINIONS OF INDIVIDUAL RESPONDENTS TO AN INFORMAL SURVEY. THE SURVEY RESULTS DO NOT CONSTITUTE A BINDING LEGAL OR REGULATORY OPINION.

© 2015 National Association of Insurance Commissioners 1

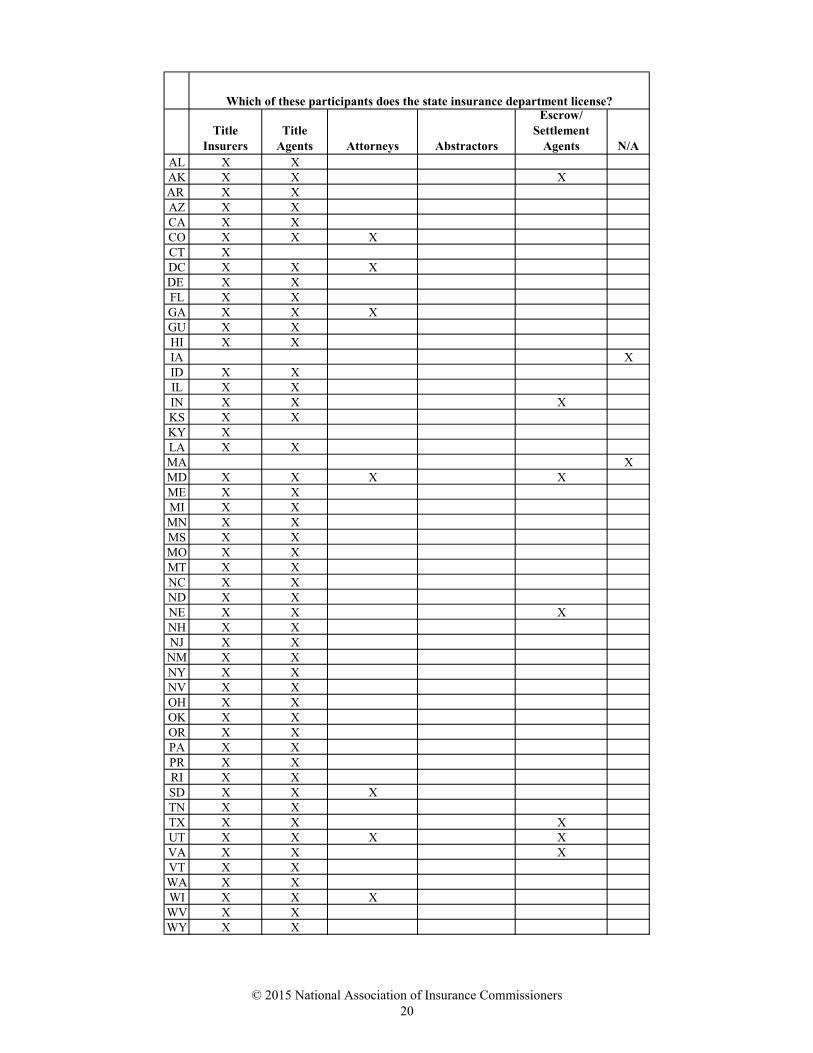

Title Insurers

Title Agents Attorneys Abstractors

Escrow/ Settlement

Agents N/A Other (please specify)AL X XAK X XAR X XAZ X XCA X X XCO X X XCT XDC X XDE X X XFL X Title insurers and title agencies, not individual agents. A title agency may

employ several title agents. We are not authorized to collect data individually from title agents.

GA X XGU X XHI XIA XID X XIL X Illinois does not require title insurers to report specific data.IN X X X XKS X XKY XLA X XMA XMD X X X XME X XMI X XMN X X X XMS XMO X XMT XNC X NC Title Insurance Rating BureauND XNE X X XNH X XNJ X

NM X XNY X XNV X XOH X X Title Marketing RepresentativesOK X XOR XPA X XPR X XRI X XSD X X X XTN XTX X X XUT X X X XVA X XVT X X XWA X XWI X XWV XWY X X

From which of these title participants is the state insurance department authorized to require data reporting? (Check all that apply)

© 2015 National Association of Insurance Commissioners 2

Title Agents Attorneys Abstractors

Escrow/ Settlement

Agents N/A Other (please specify)AL XAK X XAR XAZ XCA X XCO X X XCT XDC XDE X XFL XGA X X X XGU X XHI XIA XID X

IL X Illinois does not require title insurers to report specific data.

IN X XKS XKY X noneLA XMA XMD X X XME X

MI X“or all persons considered to have material information

regarding the insurer’s property, assets, business, or affairs.” (MCL 500.222, in pertinent part)

MN XMS XMO XMT If there is a complaintNC NC Title Insurance Rating BureauND XNE XNHNJ XNM XNY XNV XOH X Title Marketing RepresentativesOK XOR XPA Refer to our response to Question 4.PR XRI XSD XTN X XTX X XUT X We do not require Title insurers to obtain this information.VA XVT UnsureWA XWI XWV Title producers only.WY X

From which of these title participants is the state insurance department authorized to require title insurers to obtain the participant's data and report it to the state?

© 2015 National Association of Insurance Commissioners 3

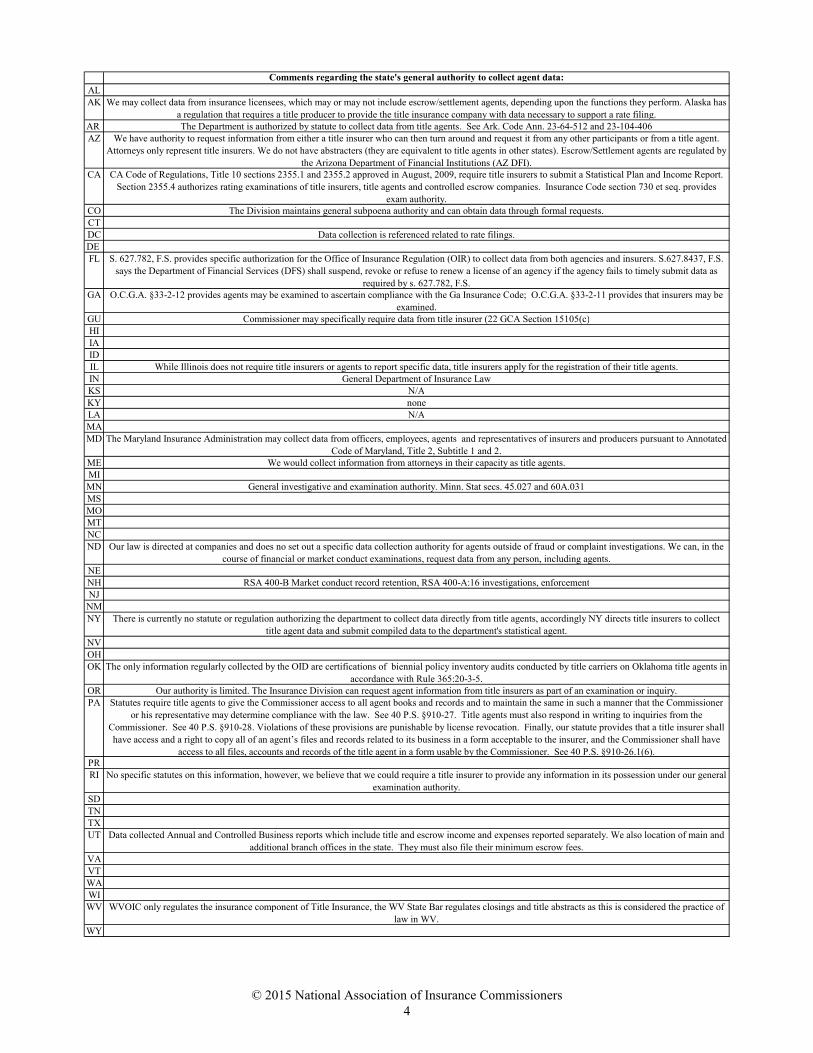

Comments regarding the state's general authority to collect agent data:ALAK We may collect data from insurance licensees, which may or may not include escrow/settlement agents, depending upon the functions they perform. Alaska has

a regulation that requires a title producer to provide the title insurance company with data necessary to support a rate filing.AR The Department is authorized by statute to collect data from title agents. See Ark. Code Ann. 23-64-512 and 23-104-406AZ We have authority to request information from either a title insurer who can then turn around and request it from any other participants or from a title agent.

Attorneys only represent title insurers. We do not have abstracters (they are equivalent to title agents in other states). Escrow/Settlement agents are regulated by the Arizona Department of Financial Institutions (AZ DFI).

CA CA Code of Regulations, Title 10 sections 2355.1 and 2355.2 approved in August, 2009, require title insurers to submit a Statistical Plan and Income Report. Section 2355.4 authorizes rating examinations of title insurers, title agents and controlled escrow companies. Insurance Code section 730 et seq. provides

exam authority.CO The Division maintains general subpoena authority and can obtain data through formal requests.CTDC Data collection is referenced related to rate filings.DE FL S. 627.782, F.S. provides specific authorization for the Office of Insurance Regulation (OIR) to collect data from both agencies and insurers. S.627.8437, F.S.

says the Department of Financial Services (DFS) shall suspend, revoke or refuse to renew a license of an agency if the agency fails to timely submit data as required by s. 627.782, F.S.

GA O.C.G.A. §33-2-12 provides agents may be examined to ascertain compliance with the Ga Insurance Code; O.C.G.A. §33-2-11 provides that insurers may be examined.

GU Commissioner may specifically require data from title insurer (22 GCA Section 15105(c)HIIAIDIL While Illinois does not require title insurers or agents to report specific data, title insurers apply for the registration of their title agents.IN General Department of Insurance LawKS N/AKY noneLA N/AMAMD The Maryland Insurance Administration may collect data from officers, employees, agents and representatives of insurers and producers pursuant to Annotated

Code of Maryland, Title 2, Subtitle 1 and 2.ME We would collect information from attorneys in their capacity as title agents.MIMN General investigative and examination authority. Minn. Stat secs. 45.027 and 60A.031MSMOMTNCND Our law is directed at companies and does no set out a specific data collection authority for agents outside of fraud or complaint investigations. We can, in the

course of financial or market conduct examinations, request data from any person, including agents.NENH RSA 400-B Market conduct record retention, RSA 400-A:16 investigations, enforcementNJNMNY There is currently no statute or regulation authorizing the department to collect data directly from title agents, accordingly NY directs title insurers to collect

title agent data and submit compiled data to the department's statistical agent.NVOHOK The only information regularly collected by the OID are certifications of biennial policy inventory audits conducted by title carriers on Oklahoma title agents in

accordance with Rule 365:20-3-5.OR Our authority is limited. The Insurance Division can request agent information from title insurers as part of an examination or inquiry.PA Statutes require title agents to give the Commissioner access to all agent books and records and to maintain the same in such a manner that the Commissioner

or his representative may determine compliance with the law. See 40 P.S. §910-27. Title agents must also respond in writing to inquiries from the Commissioner. See 40 P.S. §910-28. Violations of these provisions are punishable by license revocation. Finally, our statute provides that a title insurer shall have access and a right to copy all of an agent’s files and records related to its business in a form acceptable to the insurer, and the Commissioner shall have

access to all files, accounts and records of the title agent in a form usable by the Commissioner. See 40 P.S. §910-26.1(6).PRRI No specific statutes on this information, however, we believe that we could require a title insurer to provide any information in its possession under our general

examination authority.SDTNTXUT Data collected Annual and Controlled Business reports which include title and escrow income and expenses reported separately. We also location of main and

additional branch offices in the state. They must also file their minimum escrow fees.VAVTWAWIWV WVOIC only regulates the insurance component of Title Insurance, the WV State Bar regulates closings and title abstracts as this is considered the practice of

law in WV.WY

© 2015 National Association of Insurance Commissioners 4

Does the state insurance department currently collect

data from title agents?

Does the state insurance department aggregate or

compile data collected from title agents?

How would data reported to the state insurance department by title agents,

attorneys, abstractors and escrow/settlement agents be handled?

AL No N/A Open to public disclosureAK No No Kept confidentialAR Yes, on an ad hoc basis No It depends on the type of data collectedAZ Yes, on an ad hoc basis Yes Open to public disclosureCA Yes, on an ad hoc basis Yes Kept confidentialCO Yes, on an ad hoc basis No It depends on the type of data collectedCT No N/A N/ADC No N/A It depends on the type of data collectedDE No N/A N/AFL Yes, on a regular basis Yes Kept confidentialGA Yes, on an ad hoc basis No Kept confidentialGU No No It depends on the type of data collectedHI No N/A N/AIA No N/A N/AID Yes, on an ad hoc basis No It depends on the type of data collectedIL No No N/AIN Yes, on an ad hoc basis No Kept confidentialKS No N/A N/AKY No No N/ALA No N/A It depends on the type of data collectedMA No N/A N/AMD Yes, on a regular basis Yes Kept confidential

ME Yes, on an ad hoc basis No Kept confidentialMI Yes, on an ad hoc basis No It depends on the type of data collectedMN Yes, on an ad hoc basis No It depends on the type of data collectedMS N/A It depends on the type of data collectedMO Yes, on a regular basis No Kept confidentialMT No No N/ANC No N/A N/AND No N/A N/ANE No N/A Kept confidentialNH Yes, on an ad hoc basis No It depends on the type of data collectedNJ No N/A Open to public disclosure

NM Yes, on a regular basis Yes Open to public disclosureNY No N/A N/ANV No No Kept confidentialOH Yes, on a regular basis Yes It depends on the type of data collectedOK Yes, on a regular basis No It depends on the type of data collectedOR No N/A Kept confidentialPA Yes, on an ad hoc basis Yes It depends on the type of data collectedPR Yes, on a regular basis No N/ARI No No It depends on the type of data collectedSD Yes, on a regular basis Yes Kept confidentialTN No N/A N/ATX Yes, on a regular basis Yes Open to public disclosureUT Yes, on a regular basis No It depends on the type of data collectedVA No N/A Kept confidentialVT No No N/AWA Yes, on a regular basis Yes Kept confidential

WI No N/A Open to public disclosureWV No No N/A

WY No No It depends on the type of data collected

© 2015 National Association of Insurance Commissioners 5

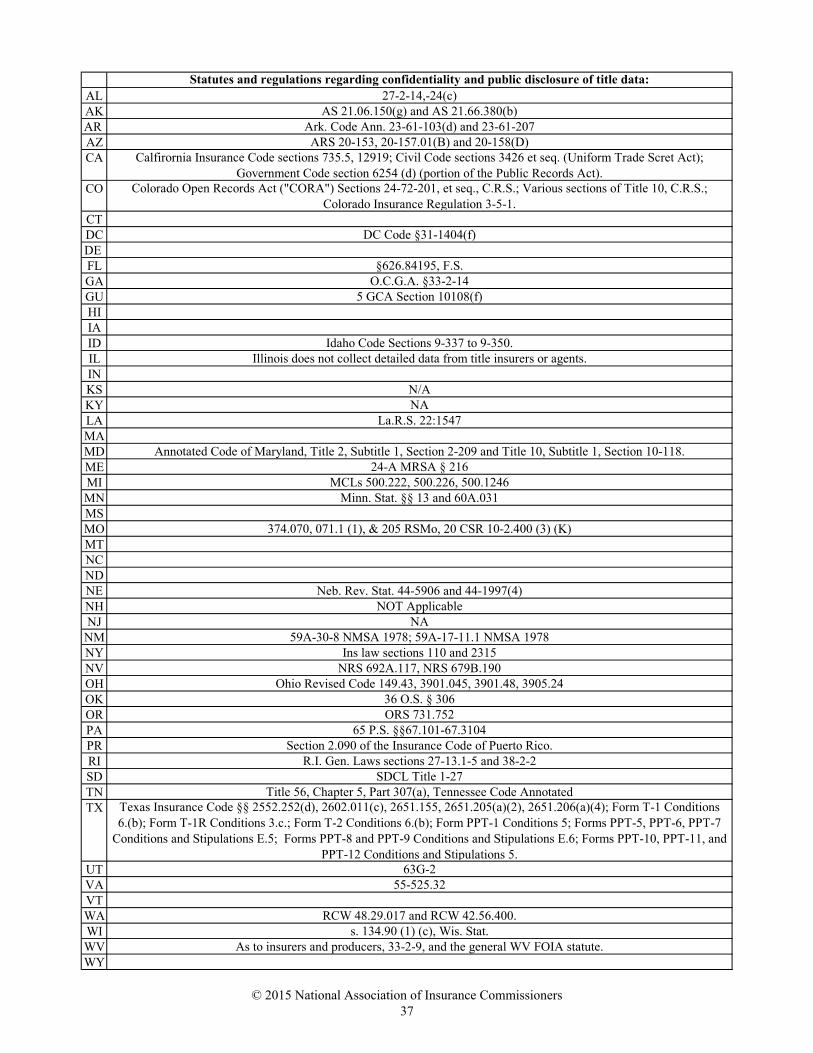

By what legal protection is the data reported kept confidential? What kind of data is collected and how is it used?

AL N/AAK confidentiality of examination materials (not specific to

market regulation)We have collected data regarding profit and loss.

AR Arkansas law protects information that is part of an

examination or active and open investigation.

The Department receives and reviews the annual statutory audits performed by title insurers. It may collect other data, such as closing files and policy records,

during an investigtion.AZ

N/ADuring a Market Conduct Exam, we collect underwriting, claims handling and

operational data which includes procedures and policyholder data.

CA

Statutory authority, both regulatory and non regulatory, and general state law as applicable.

Data collected may include a review of the books, records, accounts, rates, charges, fees, rating plans, rating systems, underwriting rules, policy forms; loss or expense experience and the data, statistics, or information collected or used

in determining or establishing the rates, charges, fees, rating plans, rating systems, underwriting rules or policy forms; statistical plan and financial data

reports. Purpose is to aid in the administration of rate reglatory laws.

COAll of the above apply depending upon the

circumstances (including n/a because there are times the Division cannot keep reported data confidential).

CTDC Proprietary Information None at this time.DE N/A N/AFL

S. 626.84195 designates the information submitted in a data call by an agency or an insurer as proprietary

information if so requested by the agency or insurer.

Revenues; expenses; premiums and losses by limit of liability; amount of time spent on primary title services, searches and closings. It is used to analyze title insurance premium rates, title insurance search costs, and the condition of the

title insurance industry in Florida.GA

Market Regulation Lawson an ad hoc basis, the GID may collect federal statements, disclosures,

policies, CPLs, agent/agency contracts, affiliated agency agreements, premium data, and other items and documents to verify compliance with Ga law.

GU Applications filed with the Banking and Insurance Commissioner falling within the exemption from

Sunshine law. ( 5 GCA Section 10108(f).

No data is collected, except loss and expense data is required when title company apply for rate increase.

HI N/AIA N/AID

Pursuant to Idaho Public Records Laws.Complaint information; title and escrow rates; any data needed to complete

examinatrion/audit regulations.IL N/A Illinois does not require title insurers to report specific data.IN Market Regulation LawsKS N/A N/AKY N/A not applicableLA Legal protection for confidential or proprietary data

would be set forth in the provisions of the Louisiana Public Records Act (La. R.S. 44.1 et seq.).

N/A

MA N/AMD

Market Regulation Laws

When advisable to determine compliance with Maryland's insurance laws, the Commissioner may examine the accounts, records, documents and transactions that related to the insurance affairs or proposed insurance affairs of an insurer

or insurance producer and others pursuant to Annotated Code of Maryland, Title 2, Subtitle 2, Section 2-206 through 2-209.

MEMarket Regulation Laws

We have not collected data from title agents. We have the authority to do so, however, and would collect data for whatever purpose was necessary to enforce

the Maine insurance laws.MI Market Regulation Laws Ad Hoc, as needed; use variesMN Market Regulation Laws Transactional, documents, etc.MS Market Regulation LawsMO

Proprietary InformationMO DIFP collects an annual underwriter on site review of report of agents title

and closing practices and ownership/affiliated business information.MT Market Regulation LawsNC N/A

© 2015 National Association of Insurance Commissioners 6

By what legal protection is the data reported kept confidential? What kind of data is collected and how is it used?

ND N/ANE

Market Regulation Laws Data is collected to investigate consumer complaints and conduct examinations.

NH Market Regulation LawsNJ N/ANM

N/ANew Mexico collects detailed revenue, expenses, and policy issuance

information from title insurers, title agents to promulgate ratesNY N/A title agent data on revenue and expenses is collected by title insurers.NV Market Regulation LawsOH

Data collected as a result of an annual review is public information. Information can only be kept confidential if

it falls into an exception of the public records statute.

Ohio collects data related to the annual review of escrow accounts, IOTA accounts, affiliated business arrangements, errors and omissions insurance and surety bail bond coverage.The data is used to determine compliance with Ohio

title insurance laws. OK N/AOR Market Regulation LawsPA Generally, information submitted to the Department is

considered public unless it is exempt from public disclosure under Pennsylvania’s Right-to-Know Law or other applicable statute. See 65 P.S. §§67.101-67.3104.

The person or entity submitting the information must typically assert a claim that the information submitted is exempt from disclosure under one of the exceptions to

public disclosure such as that for trade secrets or confidential proprietary financial information.

The Department does not regularly collect data from the title industry. In 1984 and 1993 we conducted studies of agent commissions. In 2010 we conducted a study of the expense component of title insurance rates. In order to perform the

2010 study, we required title agent information from title insurers in 2009.

PRN/A

Annual volume of business placed by isurers and the commission earned. The data is used ofr statistical and public inspection purposes.

RIIf requested in an examination it would fall under the

exclusion from public access in our examination statute. If requested in another manner it would fall under our

general access to public records statute and depend upon the information requested.

n/a

SDProprietary Information Premiums remitted for premium tax purposses and determination of liability.

TN N/ATX

N/A Revenues, expenses, policies, claims. Used for setting rates and other purposes.

UT Proprietary through Government Records Access and Management Act(GRAMA).

Income, Expense, Fees, number of offices, banking institution, fidelity bond, qualifying title individual.

VAMarket Regulation Laws

Financial information and insurance information is collected on escrow/settlement agents

VT N/A We do not collect anything but routine license/renewal data from AgentsWA

N/APolicy & order count, premium, income, and expense date to be used to support

the filing of title insurance rates.WI N/AWV A combination of laws or statutes. FOIA, Insuracne

confidentilay statutes, etc...N/A

WY N/A

© 2015 National Association of Insurance Commissioners 7

Risk Transfer

Policy Production/

IssuanceTitle Search or Abstract

Examination of Title

Clearing Title Defects

Escrow & Closing

AL X XAK X X X X XAR X X X X XAZ X XCA X X X X X XCO X X X X X XCTDC X X XDE X XFL X X X X XGA X XGU X X XHI XIAID X X X X X XIL X X X X X XIN X X X XKSKY X XLA X XMAMD X X X X XME X XMI X X X X XMN X XMSMO X X X X XMT X X XNC XND X XNE X X X X X XNH XNJ X X XNM X X X X X XNY XNV X X X X X XOH X XOK X XOR X X X XPA X XPR X XRI XSD XTN X X X XTX X X X XUT X X X X XVA X XVT X XWA X X X X XWI X X X X XWV X XWY X

Which processes does the state insurance department regulate if a title insurance policy is issued?

© 2015 National Association of Insurance Commissioners 8

Title Search or Abstract Examination of Title Clearing Title Defects Escrow & Closing

ALAK X X XAR AZCA X X X XCO X X X XCTDCDE FLGAGUHIIAIDIL X X X XINKSKYLAMAMD X X X XMEMIMNMSMOMTNCNDNENHNJ

NMNYNV X X X XOH XOKORPAPR XRISDTNTXUT X X XVA XVTWA XWI X X XWVWY

Which processes does the state insurance department regulate if NO title insurance policy is issued? (Some states only regulate the transaction if title insurance is involved maintaining that ancillary services such as title search, escrow & closing, etc. are not insurance products and are

therefore only regulated if title insurance is included in the transaction.)

© 2015 National Association of Insurance Commissioners 9

Risk Transfer

Policy Production/

IssuanceTitle Search or

AbstractExamination of

TitleClearing Title

DefectsEscrow &

ClosingAL XAK X X X X XAR AZ XCA X X X X X XCO X X X X X XCTDC X XDE XFL X X X XGA X XGU X X X XHI XIAID X X X X X XILIN X XKS X X X X X XKY X XLA X XMAMD XME X XMI X X X XMN X XMSMO XMTNC XND X XNE X X X X XNH XNJ X X X XNM X X X X XNY XNV X X X X X XOH X XOKOR X X X X XPA X X X X X XPR XRI XSD X XTN X X X XTX X X X X X XUT X X X X XVA X XVT X XWA X X X X XWI X XWV X XWY X

For which processes does the state insurance department regulate the pricing if a title insurance policy is issued?

© 2015 National Association of Insurance Commissioners 10

Risk Transfer

Policy Production/

IssuanceTitle Search or

AbstractExamination of

TitleClearing

Title DefectsEscrow &

ClosingAL XAK X X X X XAR XAZ X X X X XCA X X X X XCO X X X X X XCTDC X XDE XFL X X X XGA X XGU X X X XHI XIAID X X X X XILIN X XKS X X X X X XKY X XLA X XMAMD X X X X X XME X XMI X X X XMN X XMSMO XMT X X X X XNC X X X X X XND X XNE X X X X XNH XNJ X X X X X XNM X X X X XNY X X X X X XNV X X X X XOH X XOKOR X X X X XPA X X X X X XPR X X X X XRI XSD X X X X XTN X X X XTX X X X X X XUT X X X XVA X XVT X X X XWA X X X X XWI X X X X XWV X XWY X

Which processes are included in the title rates?

© 2015 National Association of Insurance Commissioners 11

Are rates required to be filed with the state insurance department?

How does the state insurance department regulate title insurance rates?

Does the state insurance department require title agents to file their fees for processes which are not included in title

rate?AL Yes Prior-Approval No AK Yes Prior-Approval N/AAR No Rates Are Not Regulated No AZ Yes File and Use N/ACA Yes File and Use YesCO Yes File and Use YesCT Yes Prior-Approval No DC Yes Prior-Approval No DE Yes File and Use No FL Florida's OIR promulgates rates by administrative rule. Promulgated Rates No GA No agents must charge the book rates (i.e., rates fixed

by the insurer.)N/A

GU Yes Prior-Approval No HI No Rates Are Not Regulated No IA N/AID Yes Rates are filed 30 days prior to use to allow for

comments.Yes

IL No Illinois does not regulate rates. No IN Yes Prior-Approval No KS Yes File and Use YesKY Yes File and Use No LA Yes Prior-Approval N/AMA No Rates Are Not Regulated No MD Yes File, Approval and Use. No ME Yes File and Use No MI Yes File and Use No MN Yes File and Use No MS No Rates Are Not Regulated N/AMO Yes File & use if not disapproved within 30 days NoMT Yes File and Use No NC Yes Subject to review by Actuarial Services Division No

ND Prior approval for initial filing. Use & File for changes.

Yes

NE Yes Prior-Approval No NH Yes File and Use No NJ Yes Prior-Approval N/ANM A biennial hearing is held and rates are set by the

Superintendent of InsurancePromulgated Rates No

NY Yes Prior-Approval No NV Yes Prior-Approval YesOH Yes Prior-Approval No OK No Rates Are Not Regulated No OR Prior-Approval YesPA Yes Title rate filings are typically File & Use (see 40

P.S. §910-37(d)) unless they are consent-to-rate filings, for which Use and File applies (see 40 P.S.

§910-37(g)). The Department typically issues affirmative approvals of filings that are not consent-

to-rate filings.

No

PR Yes Prior-Approval No RI Yes File and Use YesSD Yes Prior-Approval No TN Yes Prior-Approval No TX Rates are promulgated Promulgated Rates No UT Yes File and Use YesVA No Not required to be filed No VT Yes Use and File No WA Yes Currently is file and use, but will change to prior

approval on July 1, 2016.No

WI Yes Use and File No WV Yes Seperate personal and commercial. personal file

with 60 day deemer if not approved or disapproved. Commercial if file and use.

N/A

WY Yes Prior-Approval No

© 2015 National Association of Insurance Commissioners 12

What is the statutory standard for title rate adequacy?AL Rates Not Excessive, Inadequate or Unfairly DiscriminatoryAK Rates Not Excessive, Inadequate or Unfairly DiscriminatoryAR N/A The Department does not regulate rates.AZ Rates Not Excessive, Inadequate or Unfairly DiscriminatoryCA Rates Not Excessive, Inadequate or Unfairly DiscriminatoryCO Rates Not Excessive, Inadequate or Unfairly DiscriminatoryCT Rates Not Excessive, Inadequate or Unfairly DiscriminatoryDC No Particular StandardDE Rates Not Excessive, Inadequate or Unfairly DiscriminatoryFL (2) In adopting premium rates, the commission (The commission refers to Florida's Financial Services Commission. It is the agency head of OIR

and is made up of the Governor and the Cabinet.) must give due consideration to the following: (a) The title insurers’ loss experience and prospective loss experience under closing protection letters and policy liabilities. (b) A reasonable margin for underwriting profit and

contingencies, including contingent liability under s. 627.7865, sufficient to allow title insurers, agents, and agencies to earn a rate of return on their capital that will attract and retain adequate capital investment in the title insurance business and maintain an efficient title insurance delivery system.

(c) Past expenses and prospective expenses for administration and handling of risks. (d) Liability for defalcation. (e) Other relevant factors.

GA Unfair Trade Practices Act governs. GU Rates Not Excessive, Inadequate or Unfairly DiscriminatoryHI No Particular StandardIAID Rates Not Excessive, Inadequate or Unfairly DiscriminatoryIL Illinois does not regulate rates.IN Rates Not Excessive, Inadequate or Unfairly DiscriminatoryKS No Particular StandardKY Rates Not Excessive, Inadequate or Unfairly DiscriminatoryLA Rates Not Excessive, Inadequate or Unfairly DiscriminatoryMA No Particular StandardMD Rates Not Excessive, Inadequate or Unfairly DiscriminatoryME Rates Not Excessive, Inadequate or Unfairly DiscriminatoryMI Rates Not Excessive, Inadequate or Unfairly DiscriminatoryMN Rates Not Excessive, Inadequate or Unfairly DiscriminatoryMS No Particular StandardMO Rates Not Excessive, Inadequate or Unfairly DiscriminatoryMT Rates Not Excessive, Inadequate or Unfairly DiscriminatoryNC Rates Not Excessive, Inadequate or Unfairly DiscriminatoryND Rates Not Excessive, Inadequate or Unfairly DiscriminatoryNE No Particular StandardNH Rates Not Excessive, Inadequate or Unfairly DiscriminatoryNJ Rates Not Excessive, Inadequate or Unfairly Discriminatory

NM Rates Not Excessive, Inadequate or Unfairly DiscriminatoryNY Rates Not Excessive, Inadequate or Unfairly DiscriminatoryNV Rates Not Excessive, Inadequate or Unfairly DiscriminatoryOH Rates Not Excessive, Inadequate or Unfairly DiscriminatoryOK No Particular StandardOR Rates have to be supported with historical data or other information when filed. Investment income also has to be considered.PA Rates Not Excessive, Inadequate or Unfairly DiscriminatoryPR Rates Not Excessive, Inadequate or Unfairly DiscriminatoryRI Rates Not Excessive, Inadequate or Unfairly DiscriminatorySD Rates Not Excessive, Inadequate or Unfairly DiscriminatoryTN Rates Not Excessive, Inadequate or Unfairly DiscriminatoryTX Rates Not Excessive, Inadequate or Unfairly DiscriminatoryUT Rates Not Excessive, Inadequate or Unfairly DiscriminatoryVA Rates Not Excessive, Inadequate or Unfairly DiscriminatoryVT Rates Not Excessive, Inadequate or Unfairly DiscriminatoryWA Rates Not Excessive, Inadequate or Unfairly DiscriminatoryWI Rates Not Excessive, Inadequate or Unfairly DiscriminatoryWV No Particular StandardWY Rates Not Excessive, Inadequate or Unfairly Discriminatory

© 2015 National Association of Insurance Commissioners 13

Is the state insurance department authorized to regulate the percentage of premium that title agents retain?

Is there a statutory standard for determining that percentage?

AL No N/AAK Yes NoAR No N/AAZ No N/ACA Yes NoCO No N/ACT

YesYes, CT General Statutes Section 38a-415: agents may retain no more than 60% of the

premium. DC Yes NoDE No N/AFL

Yes

Yes, S. 627.782 says that the tile insurer must retain no less than 30 percent, which means

that the agent can retain no more than 70 percent.

GA No N/AGU No NoHI No NoIA N/A N/AID No NoIL No N/AIN No N/AKS No N/AKY No N/ALA No NoMA N/A N/AMD No N/AME No N/AMI No N/AMN No N/AMS N/A N/AMO No N/AMT No NoNC No N/AND Yes NoNE No N/ANH No N/ANJ No N/ANM Yes NoNY No N/ANV No N/AOH No N/AOK No NoOR No N/APA No N/APR Yes NoRI No NoSD No N/ATN No N/ATX Yes NoUT No N/AVA No N/AVT Yes NoWA No N/AWI No N/AWV Yes NoWY No N/A

© 2015 National Association of Insurance Commissioners 14

Risk Transfer

Policy Production/

IssuanceTitle Search or

AbstractExamination of

TitleClearing

Title DefectsEscrow &

Closing N/AAL X X X XAK X X X X X XAR XAZ X X X X X XCA X X X X X XCO X X X X X XCTDC X X X X X XDE X XFL X X X X X XGA X X X XGU X X X XHI X X X X XIA XID X XIL X X X X X XIN X X X X X XKS X X X X X XKY X X X X XLA X XMA XMD X X X X X XME X X X X X XMI X X X X X XMN X X X X X XMS XMO X X X X X XMT X XNC X X XND X X X X X XNE X X X X X XNH X XNJ X X X X X XNM X XNY X X X X X XNV X X X X X XOH X X X X X XOK X XOR X X X X XPA X X X X X XPR XRI X X X X X XSD XTN X X X XTX X XUT X X X X XVA X X X X X XVT X XWA X X X X X XWI X X X X XWV X XWY X

Which processes are, or can be, performed by title insurers?

© 2015 National Association of Insurance Commissioners 15

Risk TransferPolicy Production/

IssuanceTitle Search or Abstract

Examination of Title

Clearing Title Defects

Escrow & Closing N/A

AL X X XAK X X X X X XAR X X X X X XAZ X X X XCA X X X XCO X X X X XCTDC X X X XDE X X XFL X X X X XGA XGU X X X X XHIIA XID X X X X XIL X X X XIN X X X X XKSKY XLA X XMA XMD X X X X XME X X X XMI X X X X X XMN X X X X XMS XMO X X X X XMT X X X XNC XND XNE X X X X X XNH X X X X XNJ X X X X X

NM X X X X XNY X X X X XNV X X X X XOH X X X X XOK X X X XOR X X X X XPA X X X X XPR XRI XSD X X X X XTN X X XTX X X X X XUT X X X X XVA X X X XVT XWA X X X X X XWI X X X XWV XWY X X X

Which processes are, or can be, performed by title agents?

© 2015 National Association of Insurance Commissioners 16

Risk Transfer

Policy Production/

IssuanceTitle Search or

AbstractExamination of

TitleClearing Title

DefectsEscrow &

Closing N/AALAK X X X XAR XAZ XCA XCO X X X X XCTDC X X X XDE X X X X XFL X X X X XGA X X X XGU X X XHIIA XIDIL XIN X X X XKS X X X X XKY XLA X X X XMA XMD X X X X XME X X X X XMI X XMN X X X XMS XMO XMT XNC X X X X XND XNE XNH X X X X XNJ X XNMNY X XNV XOH XOK X X X XOR XPA X X X XPR X X X XRI X X X XSD X XTN X X X X XTX X X X XUT X X X X XVA X X X XVT X X X X XWA X XWI X X X X XWV X X X XWY X X X X

Which processes are, or can be, performed by attorneys?

© 2015 National Association of Insurance Commissioners 17

Risk Transfer

Policy Production/

IssuanceTitle Search or

AbstractExamination of

TitleClearing

Title DefectsEscrow &

Closing N/AAL X X X XAK X X X XAR XAZ XCA XCO XCTDC XDE XFL XGA XGU X XHIIA XIDIL XIN X XKS X XKY XLA XMA XMD XME XMI XMN X XMS XMO XMT XNC XND XNE X XNH X XNJ X

NMNY X XNV XOH XOKOR XPA XPR XRI XSD X X X XTN XTX XUT X X XVA XVT XWA XWI XWV XWY X X

Which processes are, or can be, performed by abstractors?

© 2015 National Association of Insurance Commissioners 18

Risk Transfer

Policy Production/

IssuanceTitle Search or

AbstractExamination of

TitleClearing Title

DefectsEscrow &

Closing N/AAL X XAK X X X XAR XAZ X XCA XCO XCTDC XDE XFL XGA XGU X X XHIIA XID XIL X X X XIN X X X XKS XKY XLA XMA XMD X X X X XME XMI XMN XMS XMO N/AMT N/ANC X X XND XNE XNH XNJ X

NM XNY XNV XOH XOKOR X XPA XPR XRI XSD XTN XTX XUT X XVA X X X XVT XWA X XWI XWV XWY X

Which processes are, or can be, performed by escrow/settlement agents?

© 2015 National Association of Insurance Commissioners 19

Title Insurers

Title Agents Attorneys Abstractors

Escrow/ Settlement

Agents N/AAL X XAK X X XAR X XAZ X XCA X XCO X X XCT XDC X X XDE X XFL X XGA X X XGU X XHI X XIA XID X XIL X XIN X X XKS X XKY XLA X XMA XMD X X X XME X XMI X XMN X XMS X XMO X XMT X XNC X XND X XNE X X XNH X XNJ X XNM X XNY X XNV X XOH X XOK X XOR X XPA X XPR X XRI X XSD X X XTN X XTX X X XUT X X X XVA X X XVT X XWA X XWI X X XWV X XWY X X

Which of these participants does the state insurance department license?

© 2015 National Association of Insurance Commissioners 20

Title AgenciesIndividual Title

Agents N/AAL X N/A N/AAK X X No, don't allow N/AAR X X No, don't allow NoAZ X No, don't allow N/ACA X No, don't allow NoCO X X No, don't allow NoCT X Yes, requiredDC X X No, allowed but not required NoDE X Yes, required N/AFL X X No, allowed but not required YesGA X XGU X X No, don't allow NoHI X X N/AIA X N/A N/AID X X No, don't allow NoIL X X No, don't allow NoIN X X No, don't allow NoKS X X No, don't allow N/AKY X N/A N/ALA X X No, don't allow NoMA X No, allowed but not required N/AMD X X No, don't allow NoME X X No, allowed but not required NoMI X X No, don't allow NoMN X X No, allowed but not required NoMS X No, allowed but not required YesMO X X No, don't allow NoMT No, allowed but not required YesNC X Yes, required YesND X X No, allowed but not required NoNE X X No, don't allow NoNH X X No, allowed but not required YesNJ X X N/A N/A

NM X X No, don't allow NoNY X X No, don't allow NoNV X X No, don't allow NoOH X X No, don't allow NoOK X X No, allowed but not required YesOR X X No, don't allow N/APA X X No, allowed but not required YesPR X X No, don't allow NoRI X No, allowed but not required NoSD X X No, don't allow N/ATN X No, allowed but not required YesTX X X N/A YesUT X X No, allowed but not required NoVA X X No, don't allow NoVT X No, allowed but not required NoWA X No, don't allow NoWI X No, allowed but not required YesWV X N/A N/AWY X X No, don't allow No

From which of the following does the state insurance department require a title agent license? Does the state insurance

department require the use of attorneys in lieu of title agents?

Are attorneys, not licensed as title agents, allowed by state law to

perform any duties of title agents?

© 2015 National Association of Insurance Commissioners 21

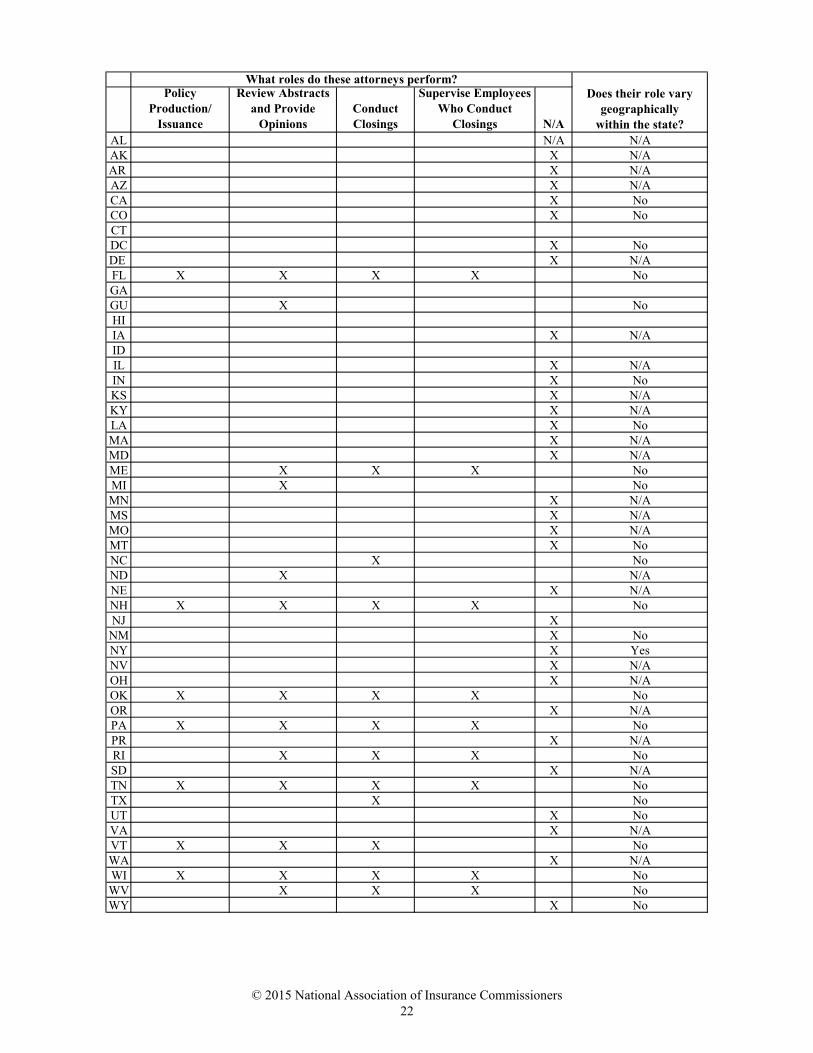

Policy Production/

Issuance

Review Abstracts and Provide

OpinionsConduct Closings

Supervise Employees Who Conduct

Closings N/AAL N/A N/AAK X N/AAR X N/AAZ X N/ACA X NoCO X NoCTDC X NoDE X N/AFL X X X X NoGAGU X NoHIIA X N/AIDIL X N/AIN X NoKS X N/AKY X N/ALA X NoMA X N/AMD X N/AME X X X NoMI X NoMN X N/AMS X N/AMO X N/AMT X NoNC X NoND X N/ANE X N/ANH X X X X NoNJ XNM X NoNY X YesNV X N/AOH X N/AOK X X X X NoOR X N/APA X X X X NoPR X N/ARI X X X NoSD X N/ATN X X X X NoTX X NoUT X NoVA X N/AVT X X X NoWA X N/AWI X X X X NoWV X X X NoWY X No

What roles do these attorneys perform?Does their role vary

geographically within the state?

© 2015 National Association of Insurance Commissioners 22

Title Agents Attorneys Abstractors Escrow/ Settlement AgentsAL Alabama State BarAK Alaska Bar AssociationAR Arkansas

Insurance Department

Arkansas Supreme CourtArkansas Abstractors

BoardNone

AZ AZ DFICA CA Division of Business OversightCO completely unlicensed completely unlicensedCT The State Bar AssociationDC No license (other than

business license)No license (other than business license)

DE DE Bar Assoc.FL

Florida BarMust hold title agent

license, or be an attorney

Escrow agents may be licensed title agents, or insurers; lenders (Office of Financial Regulation); real estate brokers (Dept. of Bus. & Prof. Reg.) or attorneys (FL Bar) under

Florida Statutes.GA State Bar, in addition to

GID (if necessary; see OCGA 33-23-1(b)(1) and

33-23-4(b))GU

Guam Bar AssociationGeneral Licensing and

Registration BranchGeneral Licensing and Registration Branch

HI Hawaii State Bar Association

Division of Financial Institutions

IAID Idaho Department of FinanceIL Not regulatedINKS

Kansas Supreme CourtKansas Board of

Technical ProfessionsKY not licensed

by DOIKentucky Bar Association not licensed by DOI not licensed by DOI

LA Louisiana State Supreme Court

Louisiana Office of Financial Institutions

MA Board of Bar OverseersMDME Maine Supreme Judicial

CourtBureau of Consumer Credit Protection

MI N/A Michigan State Bar Not Licensed Not LicensedMN Lawyers Professional

Responsibility BoardDepartment of

CommerceDepartment of Commerce

MS Mississippi State BarMOMT Supreme CourtNC NC DOI State Bar N/A N/ANDNE

Department of Insurance

Nebraska State Bar Association

Nebraska Board of Abstractors

Must be licensed or regulated by one of the following entities: Department of Insurance, Supreme Court, State Real Estate Commission, Department of Banking and Finance, Federal Deposit Insurance Corporation, Federal Office of Thrift Supervision, Federal

Farm Credit Administration, or National Credit Union Administration.NH NH Bar AssociationNJ NJ Supreme Court to

practice lawCompletely unlicensed

NMNY State BarNV Division of Mortgage LendingOH Ohio Supreme Court Completely UnlicensedOK

Oklahoma Bar Assoc.Oklahoma Abstractors

BoardN/A

OR Oregon State Bar Oregon Real Estate AgencyPA N/A (Licensed

by Insurance Department)

PA Supreme Court Completely Unlicensed Completely Unlicensed

PRRI Insurance

DepartmentRhode Island Supreme

Courtnot licensed not licensed

SD South Dakota Abstracters

Board of Examiners

South Dakota Abstracters Board of Examiners

South Dakota Abstracters Board of

Examiners

TNTennessee Bar Association Unlicensed Unlicensed

TX State Bar of TexasUT Utah State Bar Assoc. and

the Insurance Dept.Registered thru Div. of Financial Institutions unrelated to title insurance.

VAVTWA Those entities not licensed as title insurers/agents are licensed by the Department of

Financial Institutions.WI Completely unlicensedWV WV OIC WV State BarWY Wyoming State Bar Completely unlicensed Completely unlicensed

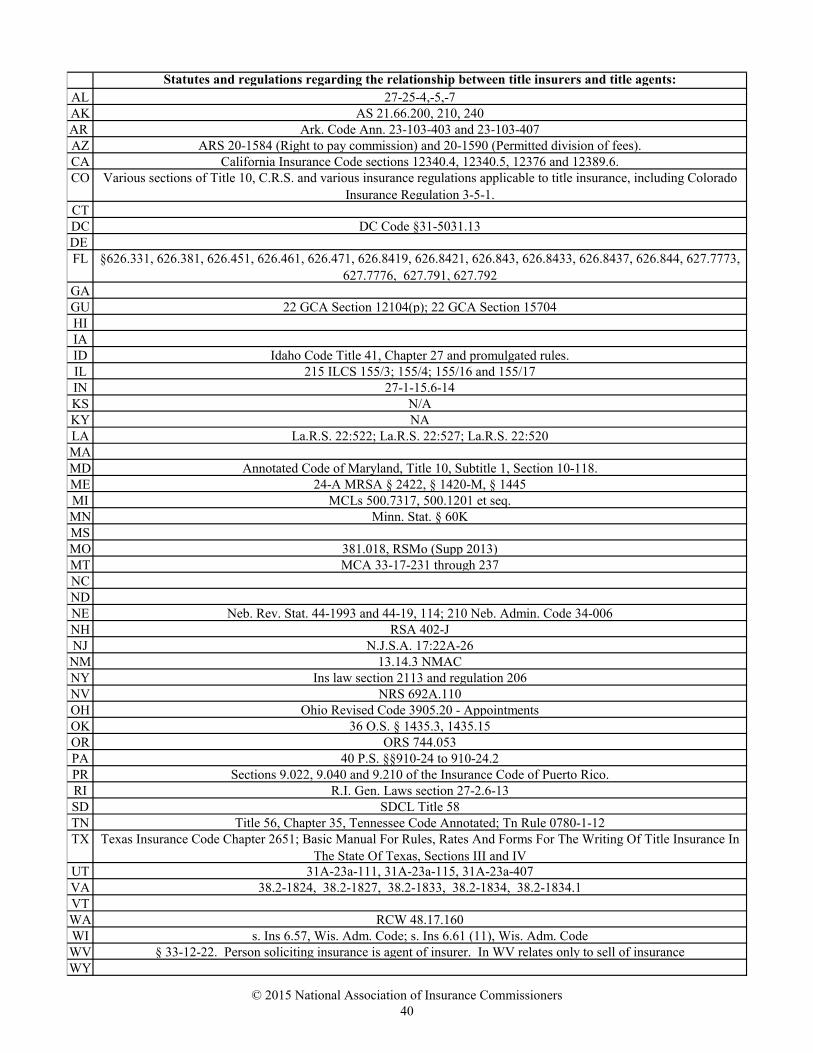

If title participants are not licensed by state insurance departments, by whom are they licensed?

© 2015 National Association of Insurance Commissioners 23

Are title insurers required to appoint the title agents they use?

Is the state insurance department authorized to review

contracts between title insurers and title agents?

Is the state insurance department required to keep the details of these contracts confidential?

AL Yes Yes, but the department rarely reviews these contracts

No

AK Yes Yes, but the department rarely reviews these contracts

Yes

AR Yes Yes, but the department rarely reviews these contracts

If the contract is part of an investigatory file, the files contents are subject to disclosure under the Freedom of Information Act once

the file is closed.AZ Yes N/A N/ACA Yes Yes, and the department sometimes

reviews these contractsNo

CO No Yes, and the department sometimes reviews these contracts

In certain, limited circumstances the details of the contracts may be required to be kept confidential.

CT N/A NoDC Yes Yes, but the department rarely reviews

these contractsYes

DE Yes N/A N/AFL Yes Yes, and the department sometimes

reviews these contractsIf requested by either party, which is usually the case.

GA Yes Yes Insurers are not required to file contracts in the ordinary course of business. If the GID obtains a contract in the course of an

examination, it is kept confidential.GU Yes Yes, but the department rarely reviews

these contractsNo

HI Yes NoIA N/A N/A N/AID Yes Yes, and the department sometimes

reviews these contractsYes

IL Yes No N/AIN Yes Yes, and the department sometimes

reviews these contractsYes

KS Yes No N/AKY No No N/ALA Yes No N/AMA N/A N/A N/AMD Yes Yes, and the department sometimes

reviews these contractsYes

ME Yes Yes, but the department rarely reviews these contracts

Yes

MI Yes Yes, and the department sometimes reviews these contracts

Yes

MN Yes Yes, but the department rarely reviews these contracts

Depends upon how they were obtained

MS Yes N/A N/AMO Underwriters must have

a written contract with the agents issuing the

insurers' policies.

Yes, and the department sometimes reviews these contracts

Confidentiality may depend on how the contract was obtained and whether the parties to it asserted it was a trade secret.

MT Yes No N/ANC Yes No N/AND Yes No N/ANE Yes Yes, and the department sometimes

reviews these contractsYes

© 2015 National Association of Insurance Commissioners 24

Are title insurers required to appoint the title agents they use?

Is the state insurance department authorized to review

contracts between title insurers and title agents?

Is the state insurance department required to keep the details of these contracts confidential?

NH Yes Yes, but the department rarely reviews these contracts

Depends upon authority to gather information in first instance.

NJ Yes Yes, but the department rarely reviews these contracts

No

NM Yes Yes, and the department sometimes reviews these contracts

No

NY Yes Yes, but the department rarely reviews these contracts

No

NV Yes Yes, and the department sometimes reviews these contracts

No

OH Yes Yes, and the department sometimes reviews these contracts

It depends on the authority under which the information was obtained (i.e. Market Conduct, Enforcement, etc.)

OK Yes Yes, but the department rarely reviews these contracts

No

OR Yes This type of review would arise if there were other concerns about the activity, a

particular agent or questionable practice.

Yes

PA Yes While the Department has authority to obtain a copy of such agreements, there

are no statutory standards for the “review” of such agreements.

Maybe, depending on why/how the agreement was obtained by the Department. For example, materials that are investigatory or

obtained in a Market Conduct examination are privileged and are generally required to be protected. Also, materials otherwise

submitted to the Department that are claimed to be trade secret or confidential proprietary financial information must also be treated as such, unless a determination is made in the context of a public records request that such claims are not, in fact, valid (which the

party that submitted the materials may then appeal).

PR Yes Yes, and the department sometimes reviews these contracts

No

RI Yes Issue is not addressed in statute, however, we would take the position

that we are entitled to review contracts (although we have not done so to date).

N/A

SD Yes No N/ATN Yes No N/ATX Yes Yes, and the department sometimes

reviews these contractsNo

UT Yes No N/AVA Yes Yes, but the department rarely reviews

these contractsYes

VT Yes Yes, but the department rarely reviews these contracts

Other (please specify)

WA Yes Yes, but the department rarely reviews these contracts

No

WI Yes Yes, but the department rarely reviews these contracts

No

WV Yes Yes, but the department rarely reviews these contracts

If the information contained therein falls with an exemption form disclosure under FOIA, then it is confidential. Depends on the content of the contract, whether part of an examination, or trade

secret in nature.

WY Yes No N/A

© 2015 National Association of Insurance Commissioners 25

Are title insurers liable for losses resulting from defalcation by title

agents?

Are title insurers liable for losses resulting from defalcation by escrow/settlement

agents?

If title insurers are liable for losses resulting from defalcations, by what is

that liability imposed?AL Yes N/AAK Yes Yes Common LawAR

YesIf a compliant Closing Protection Letter was

issued, the insurer is liable for the loss.Common Law

AZ N/A N/A N/ACA Yes Yes Common LawCO Yes Yes StatuteCTDC If a closing protection letter is

issued.If a closing protection letter is issued. Contract

DE N/A N/A N/AFL

YesOnly when the defalcation is of a title agent or

agency appointed to represent the insurer.Statute

GA Yes, if covered under a closing protection letter. See O.C.G.A. §33-

7-8.1.Yes, if covered under a CPL. CPL/Contract

GU Yes Yes ContractHIIA N/A N/A N/AID Yes No ContractIL Yes Yes ContractIN Yes Yes Common LawKSKY Questionable as there is no express

insurance law and title agents are not licensed.

No Common Law

LA No No N/AMA N/A N/A N/AMD Yes Yes StatuteME Yes Yes ContractMI Only losses covered by the title

policies and/or closing protection letters when issued.

No N/A

MN Yes Yes StatuteMS N/A N/A N/AMO It depends on the facts, including

whether a closing protection letter was issued.

It depends on the facts, including whether a closing protection letter was issued.

Common Law

MT depends on the contract N/A ContractNC Based on contractual relationship N/A ContractNDNE Yes Yes StatuteNH Yes No StatuteNJ Yes Yes Common LawNM No NoNY Yes Yes Common LawNV While NRS 692A.110 states that a

title insurer is responsible for and shall supervise the acts of each title agent and escrow officer it employs or appoints, it is unclear whether it

can be held liable for defalcations in the absence of a closing protection

letter.

N/A

The liability may be imposed by statute or by contract. While NRS 692A.110 states that a

title insurer is responsible for and shall supervise the acts of each title agent and

escrow officer it employs or appoints, it is unclear whether it can be held liable for defalcations in the absence of a closing

protection letter.

© 2015 National Association of Insurance Commissioners 26

Are title insurers liable for losses resulting from defalcation by title

agents?

Are title insurers liable for losses resulting from defalcation by escrow/settlement

agents?

If title insurers are liable for losses resulting from defalcations, by what is

that liability imposed?OH Title insurers are liable for losses

resulting from defalcations by title agents if closing protection coverage

was purchased by the person or entity claiming the loss.

Only if title insurance is issued and the closing/escrow agent is acting on behalf of the

title agent. Contract

OK Yes Yes Common LawOR Yes Yes ContractPA Yes Yes ContractPR Yes No N/ARI

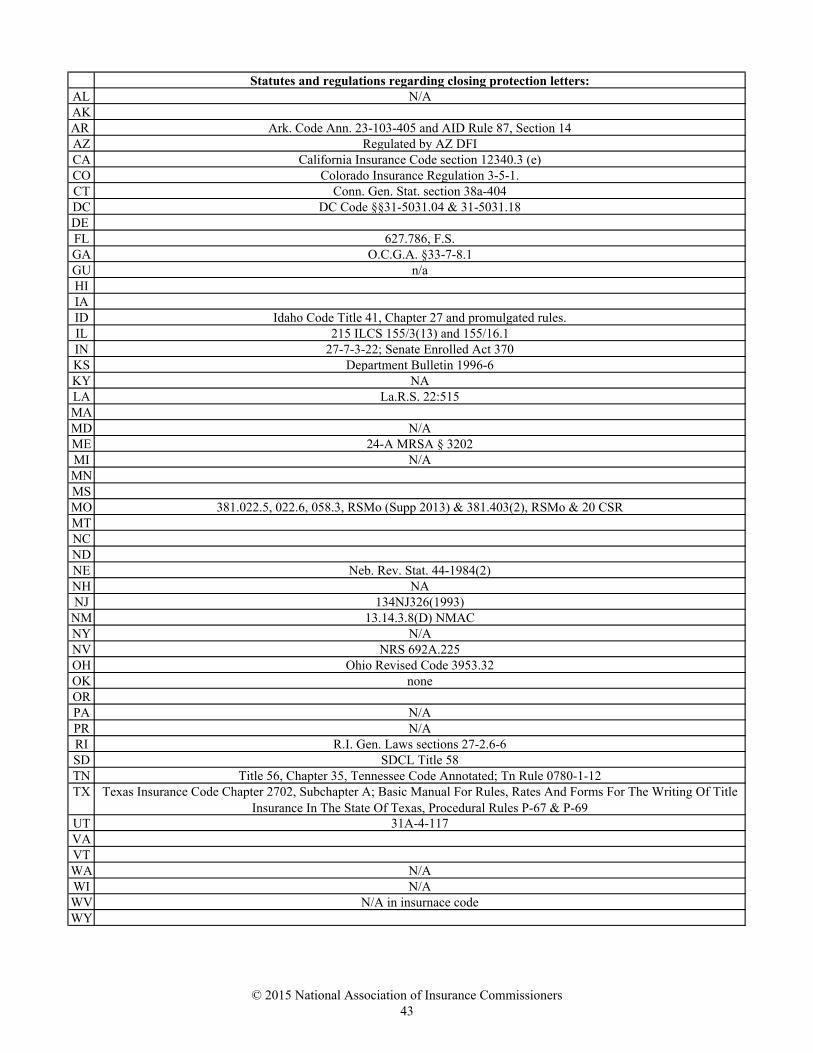

Closing protection letters are required for residential properties.

Closing protection letters are required for residential properties.

Statute

SD N/A N/A N/ATN Statute makes no mention of

defalcation. Common law or contractual remedies.

Statute makes no mention of defalcation. Common law or contractual remedies.

N/A

TX Sometimes, for example, under an insured closing letter

Sometimes, for example, under an insured closing letter

Contract

UT Yes Yes StatuteVA Yes It depends on the type of theft StatuteVT Yes unsure Other (please specify)WA No No N/AWI No No N/AWV

Yes with a caveat. The WVOIC only regulates the sale of insurance. Thus only premium falls with in the Insurance regulation. Other funds fall with the pnumbra of the WV

State Bar escrow account regulations. Closings and title

searches are considered the practice of law in WV.

See question 35 answer.It would be combination of the above,

Statue, Common law and contract.

WY Yes No

© 2015 National Association of Insurance Commissioners 27

Is a title search required before a title policy is

issued?

Are title insurers required to maintain a

title plant?

Is it acceptable for the title plant's records to be

electronic?

Is it acceptable for searches to be conducted from publicly

available recorders' websites?

Is it acceptable for title plants to offer their records via a secured web portal?

AL Yes NoAK Yes Yes Yes NoAR Yes No Yes Yes YesAZ Yes Yes N/A N/A N/ACA No No Yes Yes YesCO Yes No N/A N/A N/ACT Yes NoDC No No Yes Yes YesDE N/A N/A N/A N/A N/AFL Yes No Yes Yes YesGA Yes No N/A N/A N/AGU Yes No No No YesHI N/AIA N/A N/A N/A N/AID Yes Yes Yes No YesIL No No N/A Yes YesIN Yes No N/A No N/AKS Yes No N/A N/A N/AKY No No N/A N/A N/ALA Yes No N/A Yes N/AMA N/A N/A N/A N/A N/AMD Yes No N/A N/A N/AME No No N/A N/A N/AMI No No Yes Yes YesMN No No N/A N/A N/AMS N/A N/A N/A N/A N/AMO Yes No Yes Yes YesMT Yes No Yes Yes YesNC Yes No N/A N/A N/AND Yes Yes Yes N/A N/ANE No No N/A N/A N/ANH No No N/A Yes N/ANJ Yes No

NM Yes Yes Yes No YesNY No No N/A Yes N/ANV Yes No Yes Yes YesOH Yes No N/A N/A N/AOK Yes No N/A N/A N/AOR Yes Yes Yes No YesPA Yes No Yes N/A N/APR Yes No N/A Yes YesRI No No Yes Yes YesSD Yes Yes N/A No NoTN Yes No Yes N/A N/ATX Yes No Yes No YesUT Yes No N/A Yes N/AVA Yes No N/A N/A N/AVT N/A N/A N/A N/A N/AWA No Yes Yes No NoWI No No N/A N/A N/AWV Yes No Yes Yes YesWY Yes No

© 2015 National Association of Insurance Commissioners 28

Buyer Seller Lender N/AAL Voluntary and Typically Used X Yes No Charge

AK Voluntary and Not Typically Used

AR Voluntary and Typically Used X X X Yes By a Separate Charge to Consumer

AZ N/A X N/A N/A

CA N/A X Yes N/A

CO Voluntary and Typically Used X X X Yes N/A

CT X Yes By a Separate Charge to Consumer

DC Voluntary and Not Typically Used X X X Yes By a Separate Charge to Consumer

DE Voluntary and Not Typically Used X X N/A Included in the Rate

FL Voluntary and Typically Used X X Yes Included in the Rate

GA Voluntary and Typically Used X Yes By a Separate Charge to Consumer

GU Voluntary and Typically Used X X Yes Included in the Rate

HI N/A

IA N/A X N/A N/A

ID Voluntary and Typically Used X Yes By a Separate Charge to Lender

IL Voluntary and Typically Used X X X Yes By a Separate Charge to Consumer

IN Required X X X Yes By a Separate Charge to Consumer

KS Voluntary and Typically Used X X Yes By a Separate Charge to Lender

KY Voluntary and Typically Used X X X Yes By a Separate Charge to Lender

LA Voluntary and Typically Used X X X Yes Included in the Rate

MA N/A X N/A N/A

MD Voluntary and Typically Used X Yes By a Separate Charge to Consumer

ME Voluntary and Typically Used X X Yes N/A

MI Voluntary and Typically Used X Yes No Charge

MN Voluntary and Typically Used X Yes No Charge

MS N/A X N/A N/A

MO Voluntary and Typically Used X X X Yes By a Separate Charge to Consumer

MT N/A X Yes N/A

NC Voluntary and Typically Used X Yes By a Separate Charge to Consumer

ND Voluntary and Typically Used X N/A N/A

NE Required X X Yes By a Separate Charge to Consumer

NH N/A X Yes No Charge

NJ Voluntary and Typically Used X Yes By a Separate Charge to Consumer

NM Voluntary and Typically Used X X X Yes No Charge

NY Prohibited and Not Issued X N/A N/A

NV Voluntary and Typically Used X X X Yes By a Separate Charge to Consumer

OH Required X X X Yes By a Separate Charge to Consumer

OK N/A X N/A N/A

OR Voluntary and Not Typically Used X N/A N/A

PA Voluntary and Typically Used X Yes By a Separate Charge to Consumer