march 8, 2012 massbio state of the industry biotechnology 2012: the new normal?

TRANSCRIPT

J ohnst on Bl akel y& Company

J ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& Company

J ohnst on Bl akel y

& Company, LLCJ ohnst on Bl akel y

& Company

J ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& Company

J ohnst on Bl akel y

& Company, LLC

March 8, 2012

MassBio State of the Industry

Biotechnology 2012: The New Normal?

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

2

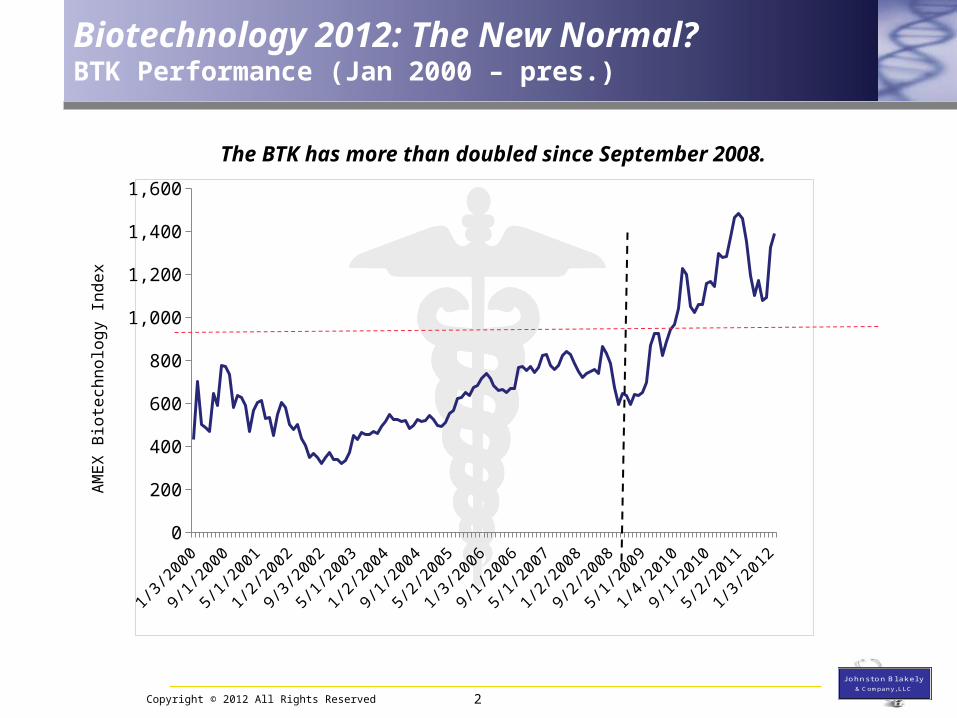

Biotechnology 2012: The New Normal?BTK Performance (Jan 2000 – pres.)

1-Ja

n-00

1-Ju

l-00

1-Ja

n-01

1-Ju

l-01

1-Ja

n-02

1-Ju

l-02

1-Ja

n-03

1-Ju

l-03

1-Ja

n-04

1-Ju

l-04

1-Ja

n-05

1-Ju

l-05

1-Ja

n-06

1-Ju

l-06

1-Ja

n-07

1-Ju

l-07

1-Ja

n-08

1-Ju

l-08

1-Ja

n-09

1-Ju

l-09

1-Ja

n-10

1-Ju

l-10

1-Ja

n-11

1-Ju

l-11

1-Ja

n-12

0

200

400

600

800

1,000

1,200

1,400

1,600

AM

EX

Bio

tech

nolo

gy I

ndex

The BTK has more than doubled since September 2008.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

1-Ja

n-01

1-Ju

l-01

1-Ja

n-02

1-Ju

l-02

1-Ja

n-03

1-Ju

l-03

1-Ja

n-04

1-Ju

l-04

1-Ja

n-05

1-Ju

l-05

1-Ja

n-06

1-Ju

l-06

1-Ja

n-07

1-Ju

l-07

1-Ja

n-08

1-Ju

l-08

1-Ja

n-09

1-Ju

l-09

1-Ja

n-10

1-Ju

l-10

1-Ja

n-11

1-Ju

l-11

1-Ja

n-12

0

200

400

600

800

1,000

1,200

1,400

Nas

daq

Bio

tech

nolo

gy I

ndex

Biotechnology 2012: The New Normal?NBI Performance (Jan 2001 – pres.)

The NBI is at its all-time high.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

1/1/20

08

3/1/20

08

5/1/20

08

7/1/20

08

9/1/20

08

11/1/

2008

1/1/20

09

3/1/20

09

5/1/20

09

7/1/20

09

9/1/20

09

11/1/

2009

1/1/20

10

3/1/20

10

5/1/20

10

7/1/20

10

9/1/20

10

11/1/

2010

1/1/20

11

3/1/20

11

5/1/20

11

7/1/20

11

9/1/20

11

11/1/

2011

1/1/20

1240.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0% NBINasdaqS&P 500

Performance (1/1/11 – pres.)

28.6%

8.0%

4.4%

Biotechnology 2012: The New Normal?Index Performance (Jan 2008 – pres.)

Over the past 12+ months, the biotech sector has outperformed both the technology sector and the broader market.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

Biotechnology 2012: The New Normal?Recent Headlines

“Ambit Withdraws IPO, Cites Market Conditions”

“Biotech IPO Forecast for 2012 Expected to Remain Chilly”

“Biotech funding hits four-year high as startups suffer”

“Prospect Venture Dumps Latest Fund, Won’t Make New Biotech Bets”

- Bloomberg (Jan 2012)

- Xconomy (June 2011)

- GEN (Jan 2012)

- Fierce Biotech (Oct 2011)

Despite the sector’s performance, indications of troubled times abound.

Biotechnology 2012: The New Normal?

Pharma Industry Perspectives

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

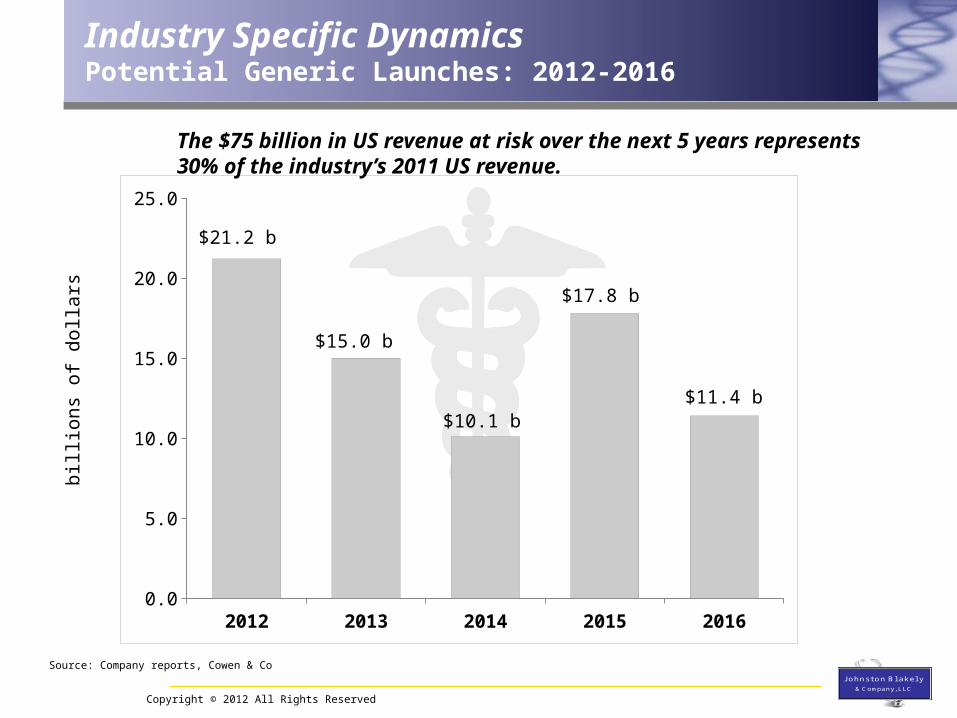

Industry Specific DynamicsPotential Generic Launches: 2012-2016

2012 2013 2014 2015 20160.0

5.0

10.0

15.0

20.0

25.0

bill

ions

of

doll

ars

$21.2 b

Source: Company reports, Cowen & Co

$10.1 b

$15.0 b

$17.8 b

$11.4 b

The $75 billion in US revenue at risk over the next 5 years represents 30% of the industry’s 2011 US revenue.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

1999 2000 2001 2002 2003 2004 2004 2006 2007 2008 2009 20100.0

10.0

20.0

30.0

40.0

50.0$

tota

l R&

D e

xpen

ditu

re s

(b$

)

$3,000

$2,500

$2.000

$1,500

$1.000

$500

$0

R&

D cost per N

ME

($mm

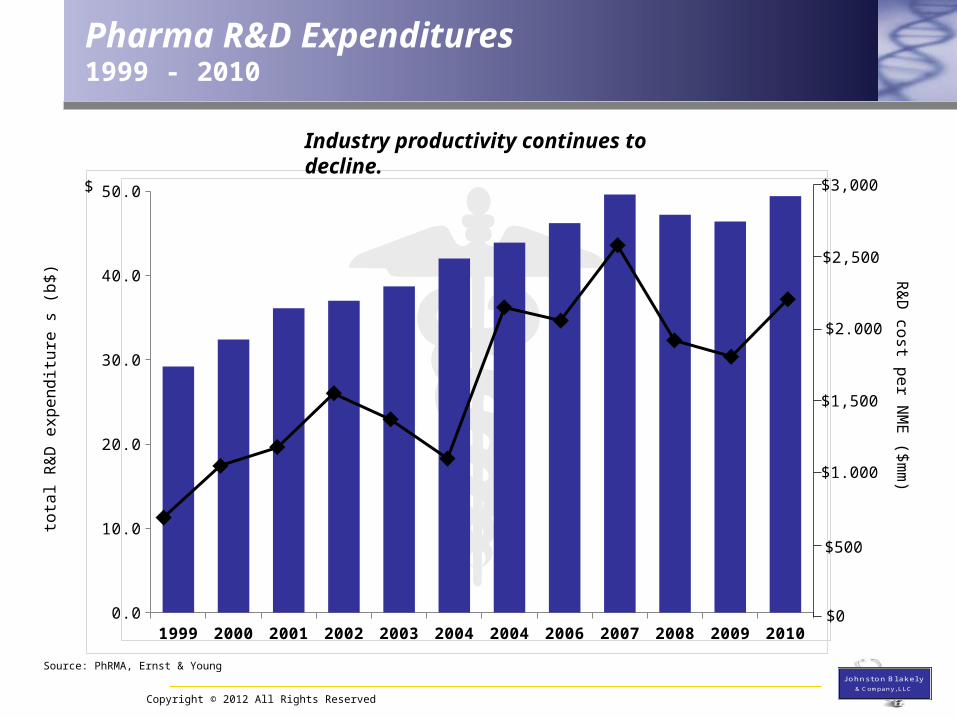

)Pharma R&D Expenditures1999 - 2010

Industry productivity continues to decline.

Source: PhRMA, Ernst & Young

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

1989 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010E

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Pre/non clinical %: 51.0% 44.0% 39.0% 32.0% 25.9% 25.7% 27.2%

Pe

rce

nt

of

tota

l R&

D e

xpen

ditu

res

Pharma R&D Expenditures1989 – 2010E (by function)

• Pre/non clinical

• Ph I – III clinicals

• Post-approval studies

• Regulatory/ other

Source: PhRMA,Note: Pre/non-clinical category includes process development, QC and formulation related expenditures.

32.5% 31.9% 27.3% 27.0%

$29.2 B $32.4 B $36.1 B $37.0 B $38.7 B $42.0 B $43.8 B $46.2 B $49.6 B $47.2 B $46.4 B $49.4 B

25.2% 24.3%

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110.0%

20.0%

40.0%

60.0%

80.0%

100.0%

Per

cent

of a

nnua

l new

dru

g ap

prov

al

21 3949 40 43 38 33 31 41 45

Bio/Specialty Pharma:Large Pharma:

66.7%33.3%

74.4%25.6%

40.8%59.2%

42.5%57.5%

51.2%48.8%

57.9%42.1%

39.4%60.6%

48.4%51.6%

70.7%29.3%

84.4%15.6%

Source: PhRMA, BIO, FDALarge Pharma Bio/specialty pharma

35 4335

80.0%20.0%

76.7%23.3%

60.0%40.0%

31 36

74.2%25.8%

58.3%41.7%

Pharmaceutical InnovationRelative New Therapeutic Contributions (1997 – 2011)

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

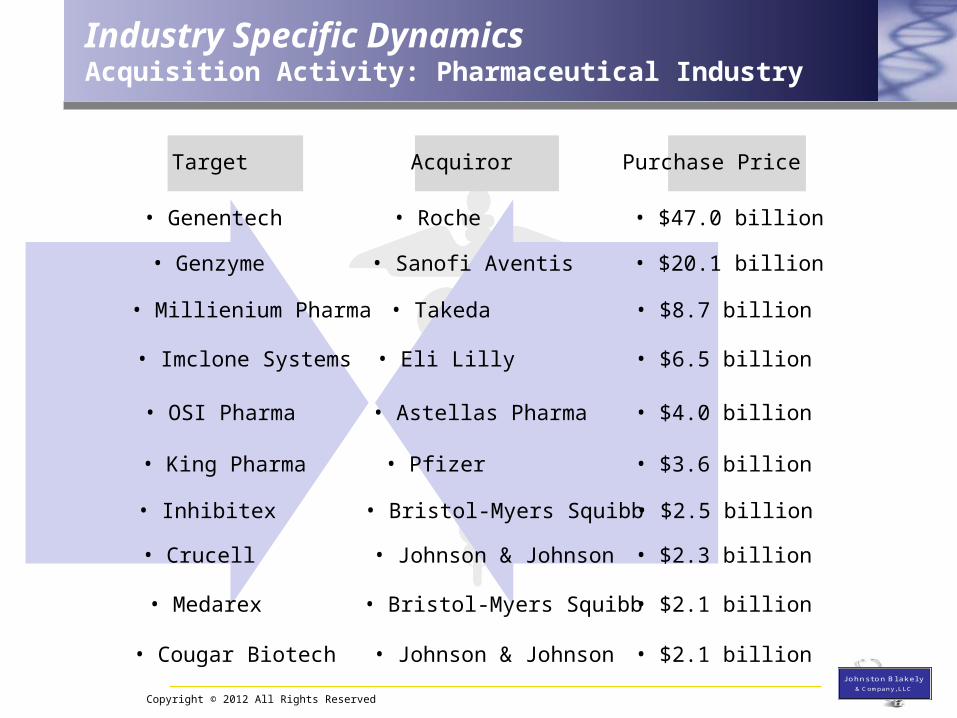

Target Acquiror Purchase Price

• Genentech • Roche • $47.0 billion

• Genzyme • Sanofi Aventis • $20.1 billion

• Millienium Pharma • Takeda • $8.7 billion

• OSI Pharma • Astellas Pharma • $4.0 billion

• King Pharma • Pfizer • $3.6 billion

• Crucell • Johnson & Johnson • $2.3 billion

• Medarex • Bristol-Myers Squibb • $2.1 billion

• Imclone Systems • Eli Lilly • $6.5 billion

• Cougar Biotech • Johnson & Johnson • $2.1 billion

Industry Specific DynamicsAcquisition Activity: Pharmaceutical Industry

• Inhibitex • Bristol-Myers Squibb • $2.5 billion

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

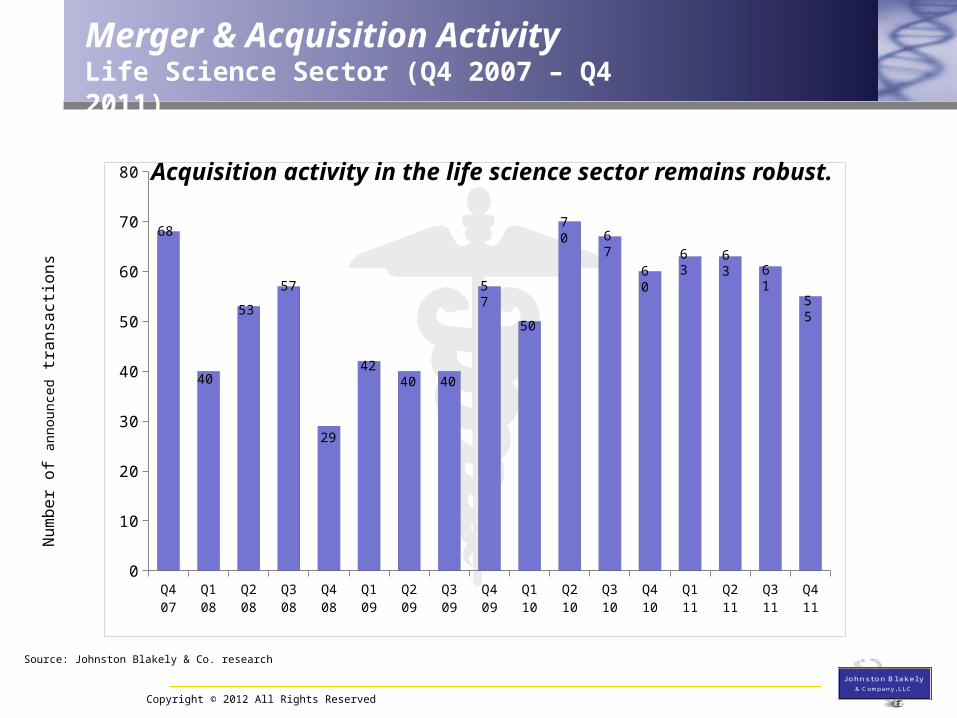

Q4 07 Q1 08 Q2 08 Q3 08 Q4 08 Q1 09 Q2 09 Q3 09 Q4 09 Q1 10 Q2 10 Q3 10 Q4 10 Q1 11 Q2 11 Q3 11 Q4 110

10

20

30

40

50

60

70

80

Num

ber

of a

nnou

nced

tran

sact

ions

Source: Johnston Blakely & Co. research

68

40

53

57

4240 40

57

50

70

29

Merger & Acquisition ActivityLife Science Sector (Q4 2007 – Q4 2011)

67

6063 63

61

55

Acquisition activity in the life science sector remains robust.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

Pharmaceutical InnovationEscalating Risk Profiles

Clinical Risk

Regulatory RiskReimbursement

Risk• outcomes-based pricing• comparative effectiveness

• significant drop in post Vioxx approvals

• increasing approval times

ReimbursementDevelopment Costs

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

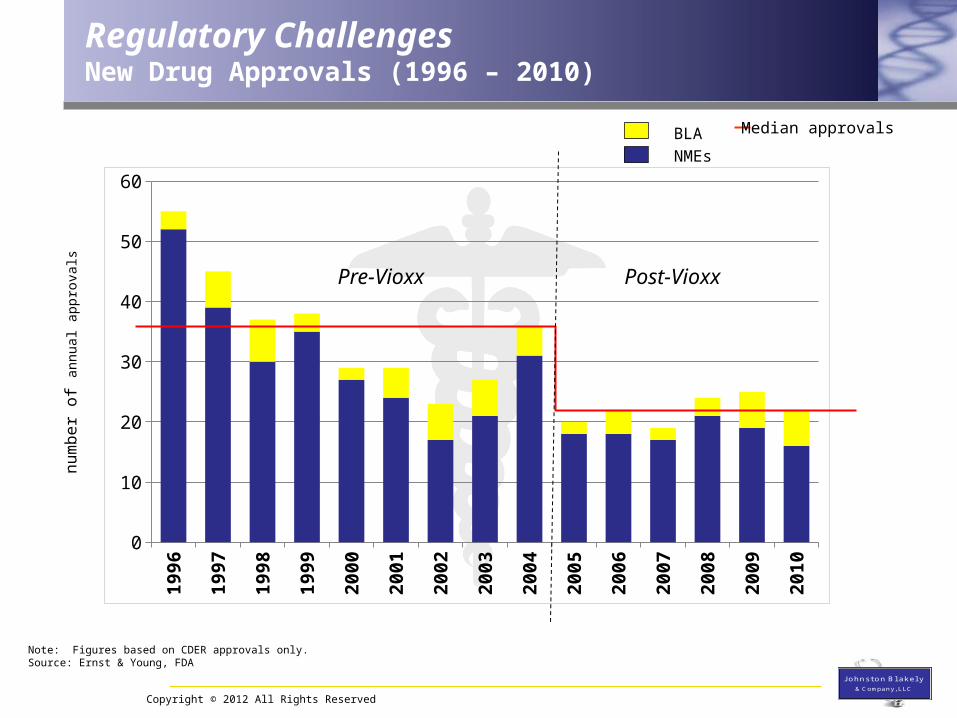

Regulatory ChallengesNew Drug Approvals (1996 – 2010)

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

0

10

20

30

40

50

60NMEs

BLA Median approvals

Post-VioxxPre-Vioxx

Note: Figures based on CDER approvals only.Source: Ernst & Young, FDA

num

ber

of a

nnua

l app

rova

ls

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

Reimbursement ChallengesCase Study: Dendreon

1-Ju

n-11

13-Ju

n-11

25-Ju

n-11

7-Ju

l-11

19-Ju

l-11

31-Ju

l-11

12-A

ug-1

1

24-A

ug-1

1

5-Sep

-11

17-S

ep-1

1

29-S

ep-1

1

11-O

ct-11

23-O

ct-11

4-Nov

-11

16-N

ov-1

1

28-N

ov-1

1

10-D

ec-1

1

22-D

ec-1

1

3-Ja

n-12

15-Ja

n-12

27-Ja

n-12

8-Feb

-12

20-F

eb-1

2

3-M

ar-12

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$35.00

$40.00

$45.00

pric

e pe

r sh

are

• Provenge sales guidance withdrawn• reimbursement concerns• inability to identify eligible patients

Biotechnology 2012: The New Normal?

Capital Markets Perspectives

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

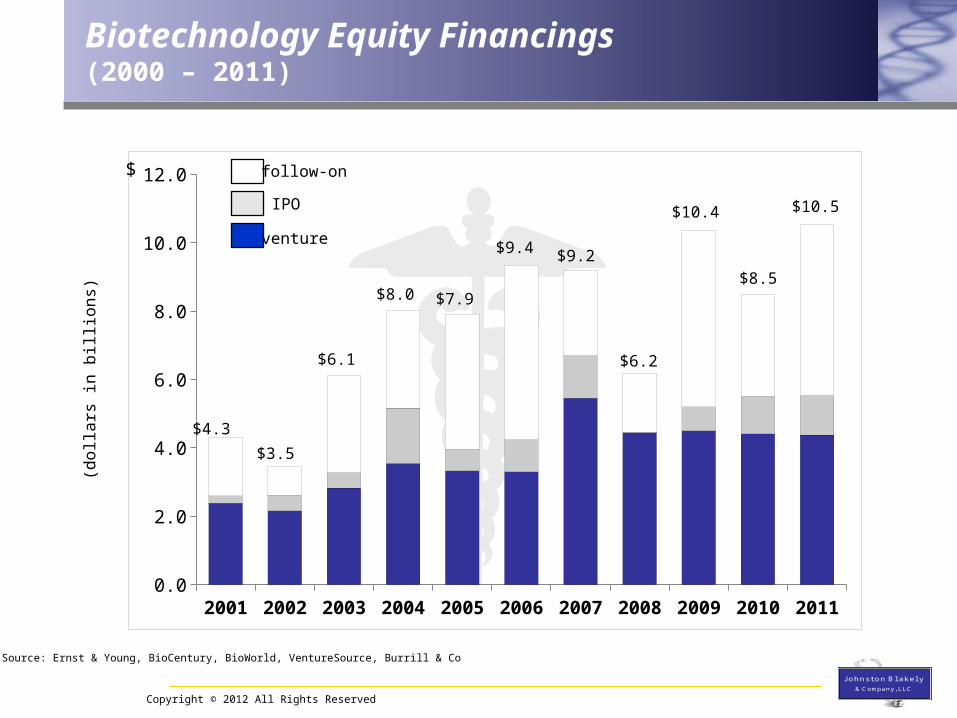

Biotechnology Equity Financings(2000 – 2011)

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110.0

2.0

4.0

6.0

8.0

10.0

12.0$

(dol

lars

in b

illi

ons)

venture

follow-on

IPO

$4.3

$3.5

$6.1

$8.0 $7.9

$9.4 $9.2

$6.2

$10.4

$8.5

Source: Ernst & Young, BioCentury, BioWorld, VentureSource, Burrill & Co

$10.5

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

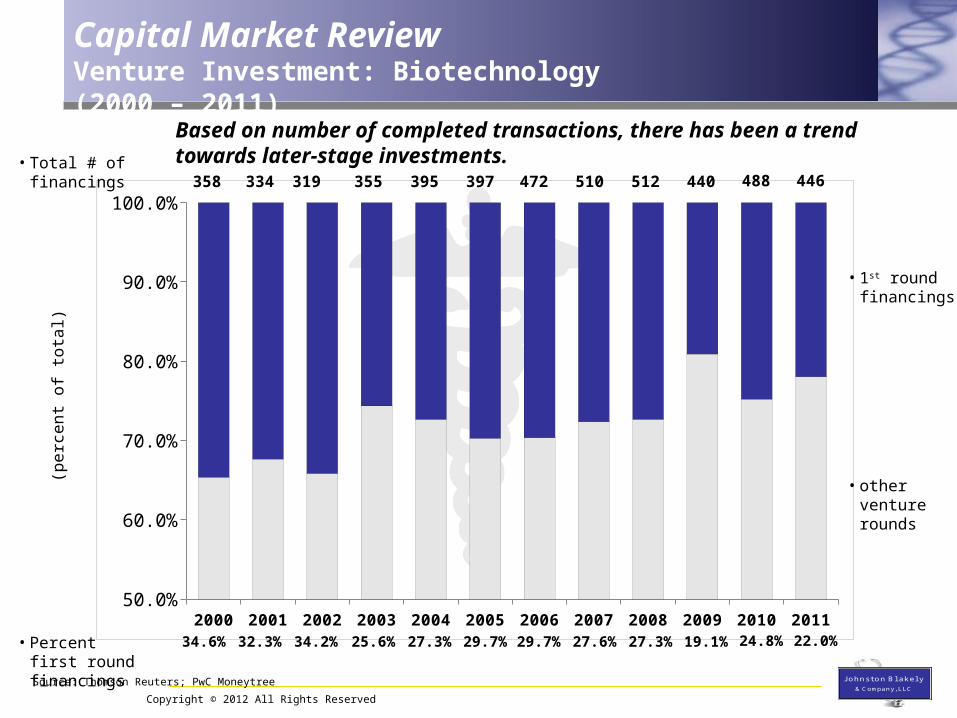

Capital Market ReviewVenture Investment: Biotechnology (2000 – 2011)

Note: Dollar amounts adjusted to reflect 2011 dollarSource: Thomson Reuters; PwC Moneyytree

(dol

lars

in m

illi

ons)

$5.2b

$4.1b$4.0b

$4.4b$4.3b

$5.0b $5.0b

$6.2b

$3.9b $3.9b

$4.7b$4.8b $4.6 billion

Measured in constant dollar terms, venture investment in biotechnology has remained relatively consistent for more than a decade.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

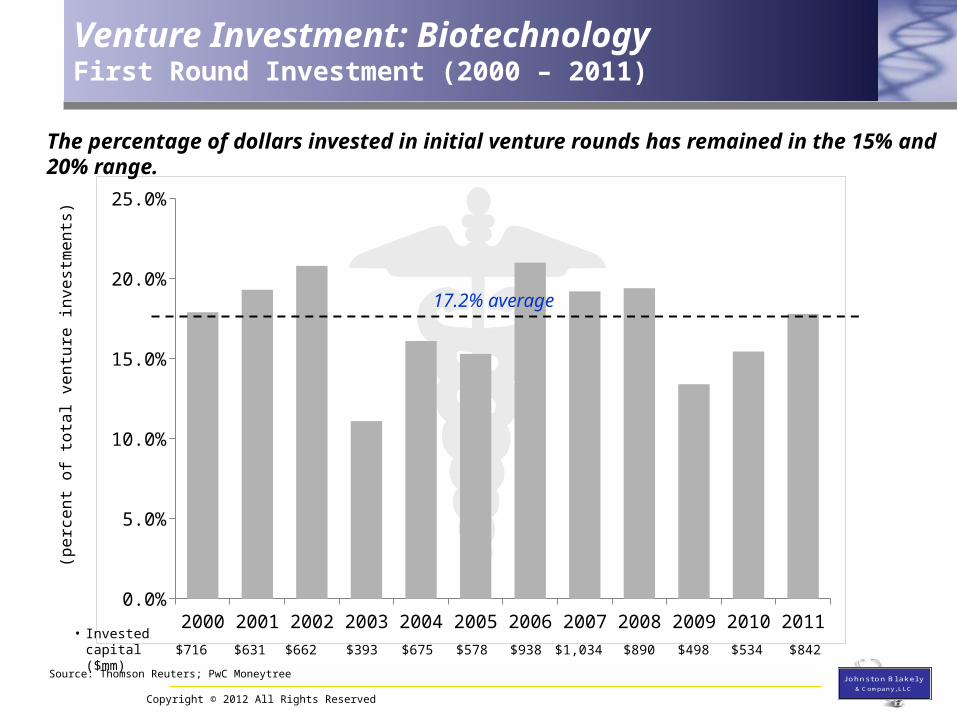

Venture Investment: BiotechnologyFirst Round Investment (2000 – 2011)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110.0%

5.0%

10.0%

15.0%

20.0%

25.0%

17.2% average

(per

cent

of

tota

l ven

ture

inve

stm

ents

)

$716 $631 $662 $393 $675 $578 $938 $1,034 $890 $498 $534 $842

Source: Thomson Reuters; PwC Moneytree

The percentage of dollars invested in initial venture rounds has remained in the 15% and 20% range.

• Invested capital ($mm)

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

Capital Market ReviewVenture Investment: Biotechnology (2000 – 2011)

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 201150.0%

60.0%

70.0%

80.0%

90.0%

100.0%

(per

cent

of

tota

l)

512 440358 334 319 355 395 397 472 510 446488

• Percent first round financings

27.3% 19.1%34.6% 32.3% 34.2% 25.6% 27.3% 29.7% 29.7% 27.6% 22.0%24.8%

• Total # of financings

Source: Thomson Reuters; PwC Moneytree

Based on number of completed transactions, there has been a trend towards later-stage investments.

• 1st round financings

• other venture rounds

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

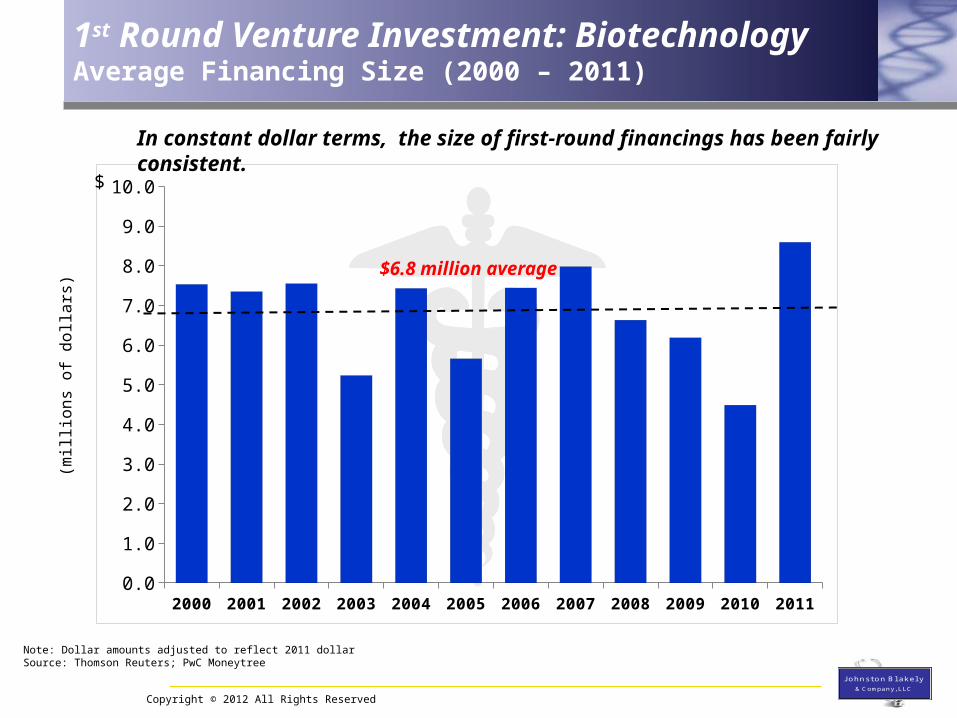

1st Round Venture Investment: BiotechnologyAverage Financing Size (2000 – 2011)

Note: Dollar amounts adjusted to reflect 2011 dollarSource: Thomson Reuters; PwC Moneytree

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 20110.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0$

$6.8 million average

(mil

lion

s of

dol

lars

)

In constant dollar terms, the size of first-round financings has been fairly consistent.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

Venture Investment: BiotechnologyNet Cash Flows (2005 – 2011)

Series1

-$5,000

-$4,000

-$3,000

-$2,000

-$1,000

$0

$1,000

$2,000

(dol

lars

in m

illi

ons)

2005 2006 2007 2008 2009 2010 2011

Ven

ture

Exi

tsV

entu

re I

nve

stm

ents

$0.3b $1.1b

($3.8b) ($4.5b) ($5.8b) ($3.7b)($4.6b)

More recently, venture realizations have outpaced dollars invested.

Note: Venture exit totals include dollars from IPO and disclosed M&A activity.Source: Thomson Reuters; NVCA

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

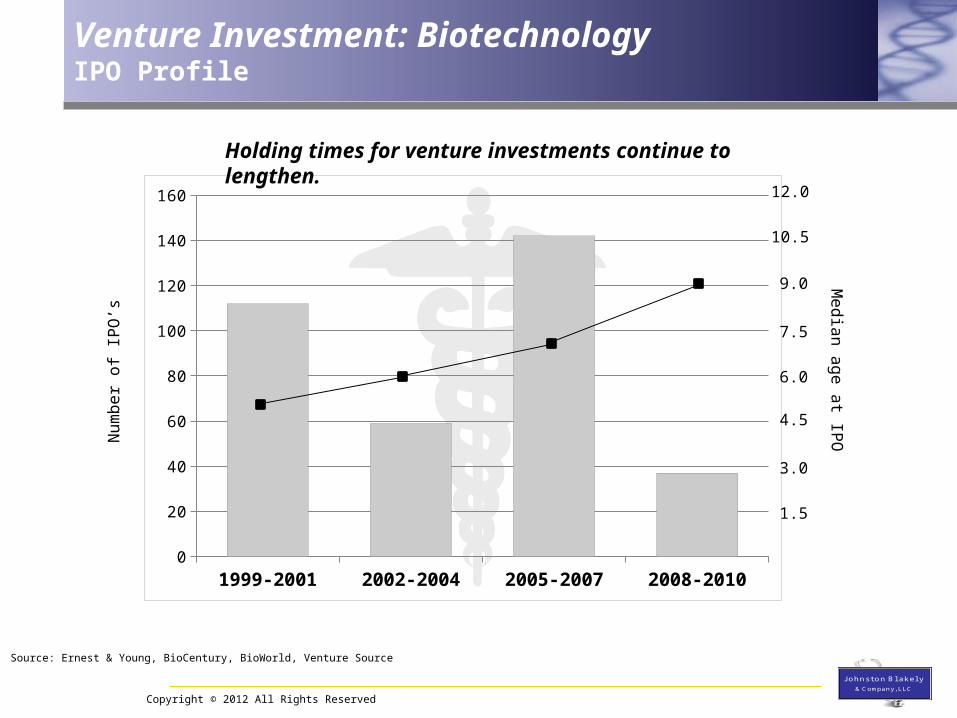

Venture Investment: BiotechnologyIPO Profile

1999-2001 2002-2004 2005-2007 2008-20100

20

40

60

80

100

120

140

160

1.5

3.0

4.5

6.0

7.5

9.0

10.5

12.0

Num

ber

of I

PO

’sM

edian age at IPO

Source: Ernest & Young, BioCentury, BioWorld, Venture Source

Holding times for venture investments continue to lengthen.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

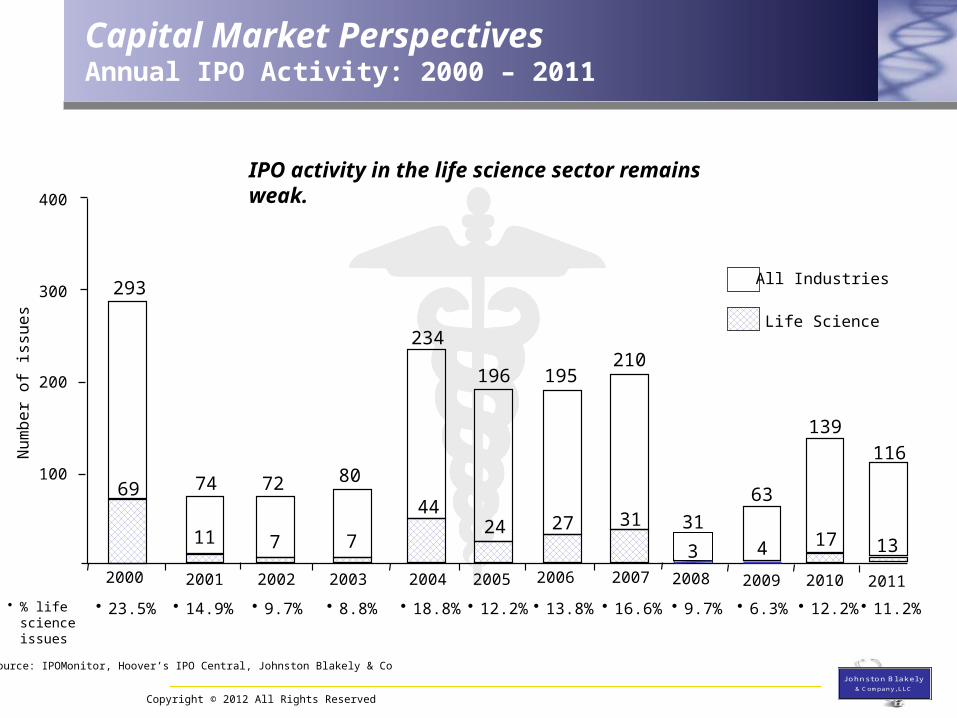

Nu

mb

er

of

issu

es

• % life science issues

• 23.5% • 14.9% • 9.7% • 8.8%

All Industries

Life Science

Capital Market PerspectivesAnnual IPO Activity: 2000 – 2011

293

74 72 8069

11 7 7

234

44

• 18.8%

Source: IPOMonitor, Hoover’s IPO Central, Johnston Blakely & Co

100

200

300

400

2000 2001 2002 2003 2004

196

• 12.2%

2005

24

195

27

• 13.8%

2006

210

• 16.6%

2007

31 31

2008

3

• 9.7% • 6.3% • 12.2%

139

17

2010

4

2009

63

2011

116

13

• 11.2%

IPO activity in the life science sector remains weak.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

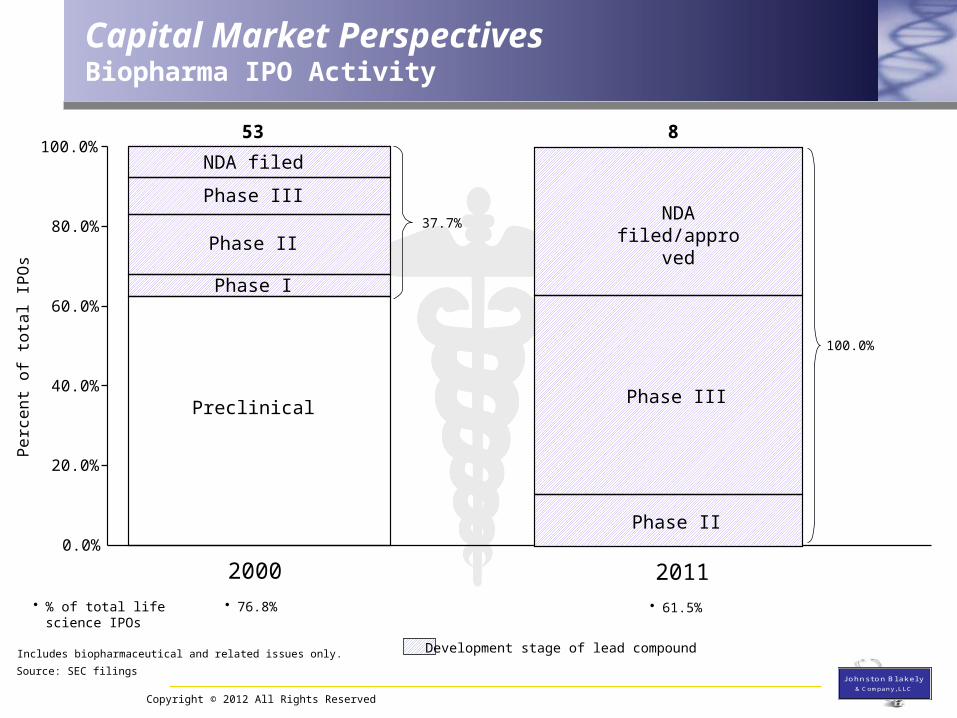

Capital Market PerspectivesBiopharma IPO Activity

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

2000

53

Preclinical

Phase I

Phase II

Phase III

NDA filed

37.7%

Pe

rce

nt

of

tota

l IP

Os

Source: SEC filings

Note: Includes biopharmaceutical and related issues only. Development stage of lead compound

• % of total life science IPOs

• 76.8%

100.0%

2011

Phase II

Phase III

• 61.5%

8

NDA filed/approved

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

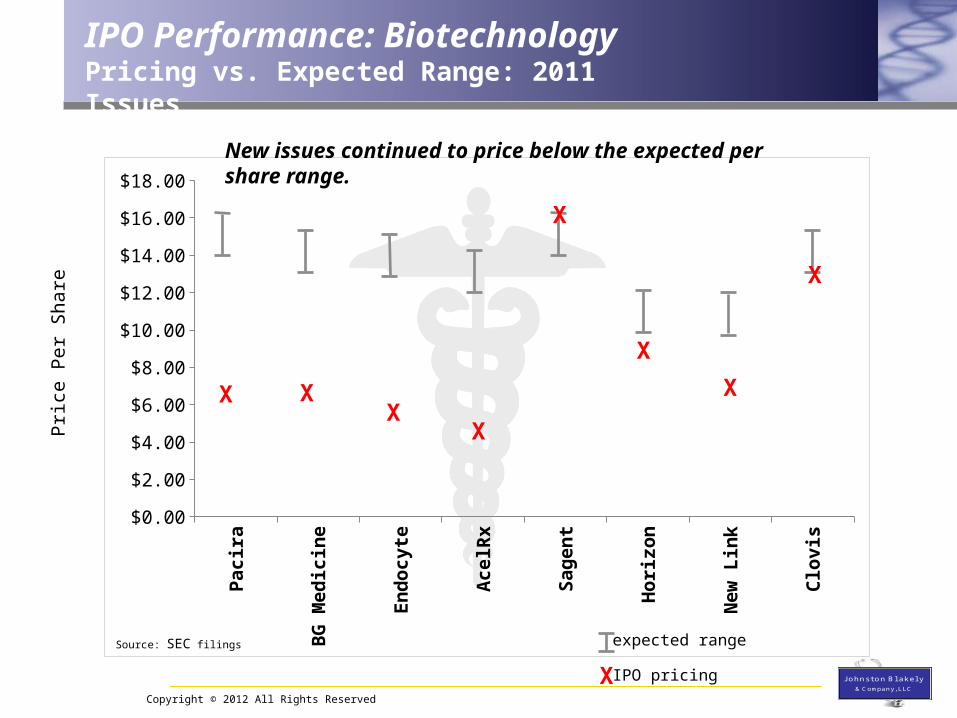

IPO Performance: BiotechnologyPricing vs. Expected Range: 2011 Issues

Pac

ira

BG

Med

icin

e

En

doc

yte

Ace

lRx

Sag

ent

Hor

izon

New

Lin

k

Clo

vis$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

XX

X

X

X

X

X

X

Source: SEC filings

Pri

ce P

er S

hare

X

expected range

IPO pricing

New issues continued to price below the expected per share range.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

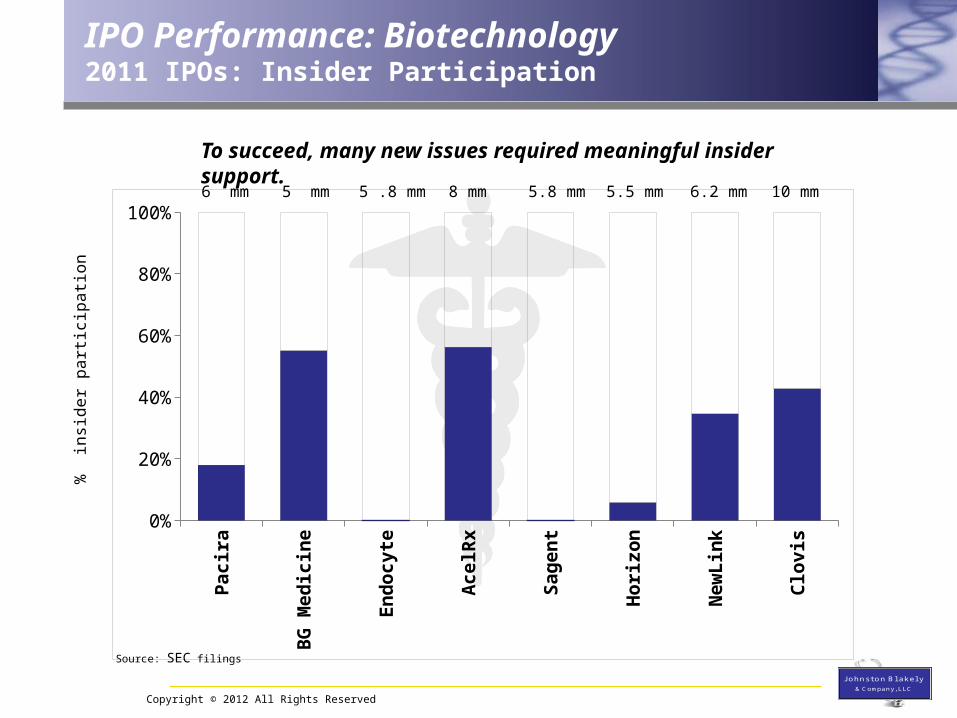

IPO Performance: Biotechnology2011 IPOs: Insider Participation

Pac

ira

BG

Med

icin

e

En

doc

yte

Ace

lRx

Sag

ent

Hor

izon

New

Lin

k

Clo

vis0%

20%

40%

60%

80%

100%

% i

nsid

er p

arti

cipa

tion

6 mm 5 mm 5 .8 mm 8 mm 5.8 mm 5.5 mm 6.2 mm 10 mm

Source: SEC filings

To succeed, many new issues required meaningful insider support.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

IPO Performance: Biotechnology2010 – 2011 Issues

CL

VS

PC

RX

SGN

T

TZ

YM

NL

NK

BG

MD

EC

YT

HZ

NP

AE

GR

AN

AC

AV

EO

IRW

D

TSR

X

AN

TH

ZG

NX

GN

OM

AL

IM

PA

CB

TN

GN

CR

MD

-100.0%

-75.0%

-50.0%

-25.0%

0.0%

25.0%

50.0%

75.0%

100.0%

Per

Shar

e Pe

rfor

man

ce P

ost I

PO

Class of 2011 Class of 2010

• Aggregate return 17.4 % (19.0 %)

Note: Aggregate return represents collective return from one share of each new issue.

Biotechnology 2012: The New Normal?

The New Normal?

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

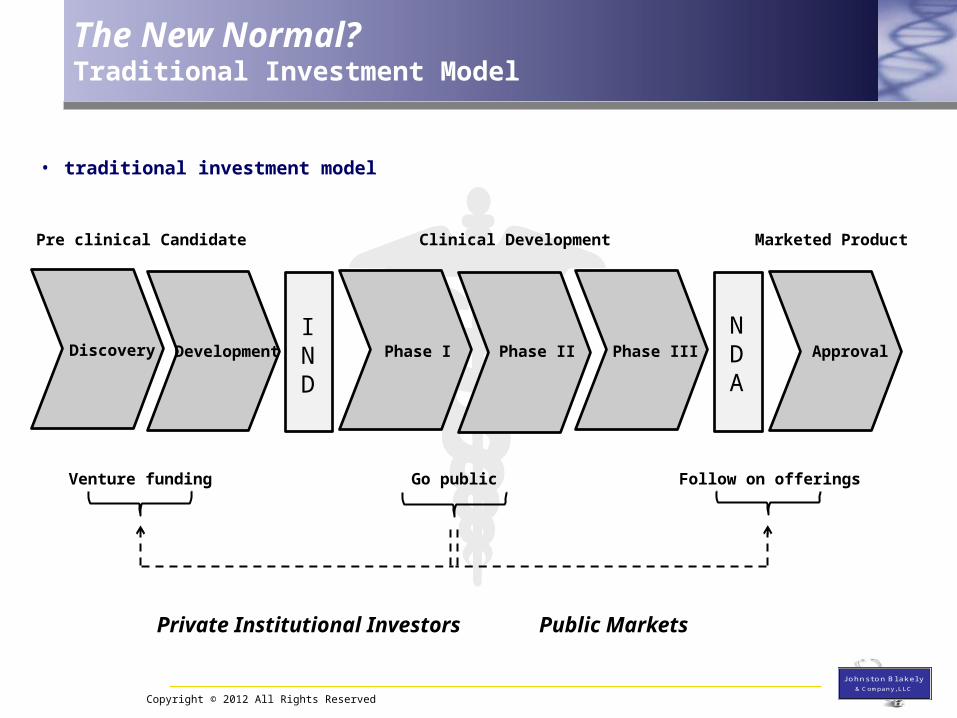

The New Normal?Traditional Investment Model

IND

NDA

Discovery Development Phase I Phase II Phase III Approval

Pre clinical Candidate Clinical Development Marketed Product

Go publicVenture funding

• traditional investment model

Follow on offerings

Private Institutional Investors Public Markets

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

The New Normal?Sector Influences

Transitioning from revolutionary advances to evolutionary advances− sign of continuing maturation of the industry

− M&A activity blurs of sector boundaries

Less public market enthusiasm for hope/hype.− increasing attention on products and profits

Primary interest of big pharma is ability to leverage downstream capabilities.

− biopharma sector continued to be viewed as outsourced R&D function.

− resource allocation (of necessity) skewed towards later stage candidates.

Venture investors required to adjust their investment horizon – and their exit strategy - accordingly.

Copyright © 2012 All Rights Reserved

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company

J ohnst on Bl akel y& Company, LLC

The New Normal?Shifting Investment Dynamics

IND

NDA

Discovery Development Phase I Phase II Phase III Approval

Pre clinical Candidate Clinical Development Market

Go publicVenture funding

• traditional investment model

Acquisition/ go publicVenture funding

• current investment model

Follow on offerings

Private Institutional Investors Public Markets

Private Institutional InvestorsThe Financial Abyss?

J ohnst on Bl akel y& Company

J ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& Company

J ohnst on Bl akel y

& Company, LLCJ ohnst on Bl akel y

& Company

J ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& CompanyJ ohnst on Bl akel y

& Company

J ohnst on Bl akel y

& Company, LLC

March 8, 2012

MassBio State of the Industry

Biotechnology 2012: The New Normal?

Benjamin Conway

978-526-4014617-834-8482