market. market is an area where buyers and sellers come in contact with each other to determine a...

TRANSCRIPT

Market

Market

Market is an area where buyers and sellers come in contact with each other to determine a single price of a product in a whole of area at a time.

Kinds of Market

Market can be classified according to

• Time

• Space

• Commodities

• Competition

According to Time

• Day to day market

• Short period market

• Long period market

According to Space

• Local Market

• Regional Market

• National market

• International market

According to Commodities

• General Market

• Specialized Market

• Capital Market

• Stock Exchange Market

• Factor Market

• Money Market

• Foreign Exchange Market

According to Competition

• Perfect Competition

• Monopolistic Competition

• Oligopoly

• Monopoly

• Duopoly

• Monophony

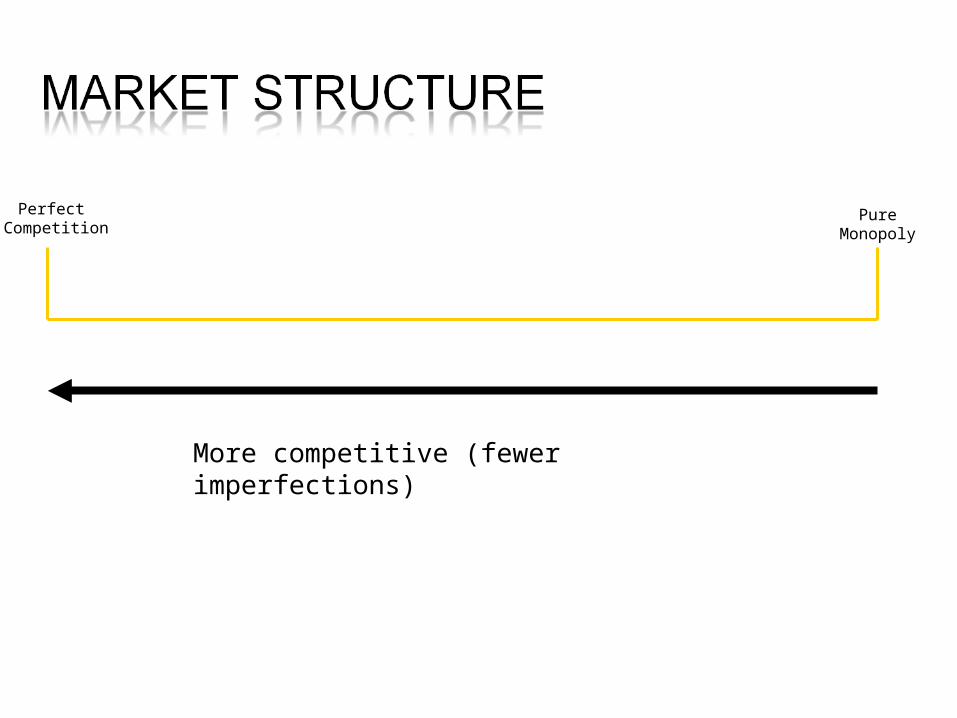

• Market structure – identifies how a market is made up in terms of:– The number of firms in the industry– The nature of the product produced– The degree of monopoly power each firm has– The degree to which the firm can influence price– Profit levels– Firms’ behaviour – pricing strategies, non-price competition,

output levels – The extent of barriers to entry– The impact on efficiency

More competitive (fewer imperfections)

Perfect Competition

Pure Monopoly

Market Structure

Less competitive (greater degree of imperfection)

Perfect Competition

Pure Monopoly

Market StructurePerfect

Competition

Pure Monopoly

Monopolistic Competition Oligopoly Duopoly Monopoly

The further right on the scale, the greater the degree of monopoly power exercised by the firm.

Importance:

• Degree of competition affects the consumer – will it benefit the consumer or not?

• Impacts on the performance and behaviour of the company/companies involved

• Characteristics of each model:– Number and size of firms that make up

the industry– Control over price or output– Freedom of entry and exit from the industry– Nature of the product – degree of homogeneity

(similarity) of the products in the industry (extent to which products can be regarded as substitutes for each other)

– Diagrammatic representation – the shape of the demand curve, etc.

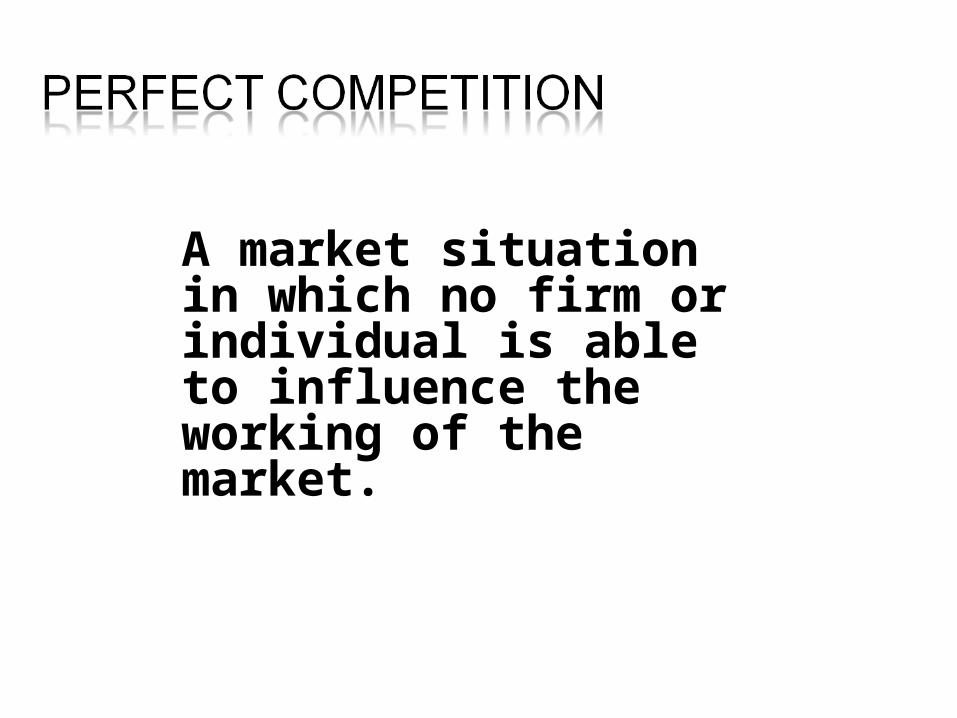

A market situation in which no firm or individual is able to influence the working of the market.

• Characteristics:

– Large number of firms– Products are homogenous (identical) – consumer has no reason

to express a preference for any firm– Freedom of entry and exit into and out of the industry– Firms are price takers – have no control over the price they

charge for their product– Each producer supplies a very small proportion of total industry

output– Consumers and producers have perfect knowledge about the

market

• PC imply that no firm can influence the price at which it sells output. They are price-takers.

• A Price –Taker is a firm that cannot influence the price of a good or service.

• Firms are price takers because it produces a tiny proportion of the total output of a particular good and buyers are well informed about the prices of other firms.

Price is usually constant in perfect competition and only the quantity changes.

Competitive firms always need to maximize its economic profit and therefore firms makes 4 key decisions: 2 in short run and 2 in long run.

Short run decisions – is a time frame in which each firm has a given plant and the number of firms in the industry is fixed.

1. whether to produce or to shutdown.2. if the decision is to produce, what quantity to

produce.

Long Run is a time frame in which each firm can change the size of its plant and decide whether to leave the industry or let other firms enter into the industry.

In LR, firms plant size can change, number of firms can change and even the constraints faced by firms can also change. For example the demand for goods can permanently fall or technological advancement can change the industries cost. In LR:

1. Firms need to decide to increase or decrease its plant size or

2. stay in the industry or leave it.

(i) optimal allocation of resources

(ii) competition encourages efficiency

(iii) consumers charged a lower price

(iv) responsive to consumer wishes: Change in demand, leads extra supply

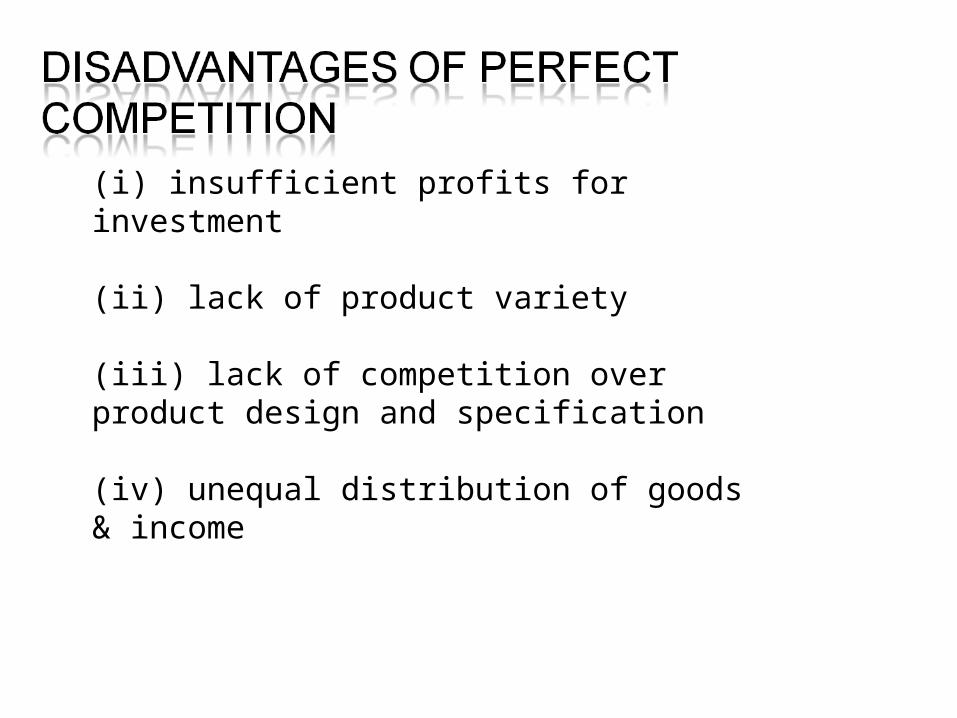

(i) insufficient profits for investment

(ii) lack of product variety

(iii) lack of competition over product design and specification

(iv) unequal distribution of goods & income

• Where the conditions of perfect competition do not hold, ‘imperfect competition’ will exist

• Varying degrees of imperfection give rise to varying market structures

• Monopolistic competition is one of these – not to be confused with monopoly!

• Characteristics:– Large number of firms in the industry– May have some element of control over price due to

the fact that they are able to differentiate their product in some way from their rivals – products are therefore close, but not perfect, substitutes

– Entry and exit from the industry is relatively easy – few barriers to entry and exit

– Consumer and producer knowledge imperfect

• No one firm can influence what other firms can do because all firms are small.

• Products are differentiated - a slight difference from the products of competing firms.

• Demand curve is downward sloping due to Product differentiation. Increase in price will usually lead to decrease in demand and switch to substitute good.

Profit is maximized by choosing its price.LR – economic profit cannot be made

because of firms free entry and exit.Economic profit – new firms enter, price

decreases and eliminated profit.Economic losses – firms leave the industry,

price increases and profits and thus eliminates loss.

LR- firms neither enter or leave, zero economic profit.

• Restaurants• Plumbers/electricians/local builders• Private schools• Health clubs• Hairdressers• Estate agents

• In each case there are many firms in the industry

• Each can try to differentiate its product in some way

• Entry and exit to the industry is relatively free• Consumers and producers do not have perfect

knowledge of the market

• There are no significant barriers to entry; therefore markets are relatively contestable.

• Differentiation creates diversity, choice and utility. For example, a typical food street in any town will have a number of different restaurants from which to choose.

• The market is more efficient than monopoly but less efficient than perfect competition

• However, they may be dynamically efficient, innovative in terms of new production processes or new products.

• For example, retailers often constantly have to develop new ways to attract and retain local custom.

• competing firms are inefficient and the prices of the products usually exceed the benefits or value provided by the products or services.

• Government lacks the control because market is huge and a large number of buyers and sellers exist.

• emphasize on the advertisements and promotional strategies which induces the customers to spend more because of the brand names.

• no regulatory control over the prices therefore, consumers suffer in a monopolistic competition.

• only a few firms in a market and entry is difficult for other firms.

• Key feature – profitability of any one firms actions depend on how the other firms respond to those actions.

• Strategic behavior – when firms are aware of other firms expected responses , they take those expected responses into account when making choices.

• Decide on how much to produce, what price to charge, and how much to spend on advertising.

• Features of an oligopolistic market structure:• Profit maximization conditions: An oligopoly maximizes profits by

producing where marginal revenue equals marginal costs.

• Ability to set price: Oligopolies are price setters rather than price takers.

• Entry and exit: Barriers to entry are high. The most important barriers are economies of scale, patents, access to expensive and complex technology etc.

• Number of firms: "Few" – a "handful" of sellers. There are so few firms that the actions of one firm can influence the actions of the other firms.

• Long run profits: Oligopolies can retain long run abnormal profits. High barriers of entry prevent sideline firms from entering market to capture excess profits.

• Product differentiation: Product may be homogeneous (steel) or differentiated (automobiles).

• Perfect knowledge: Oligopolies have perfect knowledge of their own cost and demand functions. Buyers have only imperfect knowledge as to price, cost and product quality.

• Interdependence: The distinctive feature of an oligopoly is interdependence. Oligopolies are typically composed of a few large firms. Each firm is so large that its actions affect market conditions. Therefore the competing firms will be aware of a firm's market actions and will respond appropriately.

• Is an industry that produces a good or service for which no close substitute exists.

• There is only one supplier/seller – protected from competitions by barriers to entry of new firms.

2 key features:

1. No close substitutes – firms produces a product for which there is no close substitute. E.g. water supply.

2. barriers to entry – legal or natural constraints that protect a firm from potential competitors.

• One seller of a good or service.• High degree of control over the price at

which the product is sold. Price –maker or has market power.

• Barriers to entry by other firms. - Capital cost can be seen as a strong barrier in the case of big firms.

• Economies of scale – larger output with least cost of production

1. Legal barriers – occurs when a law, license or patent restricts competition by preventing entry. E.g. public franchise – exclusive right given to a firm to supply good or service.

• Government license – controls entry into particular occupations, professions, and industries.

• Patent – exclusive right given to the inventor of the product or service.

2. Natural Barriers to entry- where one firm can supply the entire market at a lower price than two or more firms can.

• Monopoly uses two strategies – 1. Single price Monopoly - firm that must sell

each unit of output for the same price to all the consumers.

2. Price discrimination- is the practice of selling different units of the same good or service for different prices. e.g. hairdresser, restaurant.

• Firms in Monopoly can also make positive economic profits and this will not cause other firms to enter like in PC due to barriers to entry.

• Monopolists always produces output where both MR=MC and are positive.

• The demand is elastic. They do not produce in the inelastic range.

• Price discrimination is an attempt by the monopoly to convert consumer surplus into economic profit.

• A monopoly can price discriminate if it

a.Can identify and separate different buyer types.

b.Sells a product that cannot be resold.

c. Price discrimination usually increases economic profit and decreases consumer surplus

• Monopolist will have better resources to spend on research and development and will be able to bring new techniques and products to strengthen its position

• reacts to demand changes in a more effective manner than other forms.

• They charge higher prices as there is no other competitor in the market

• Monopolist has the power to restrict market supply

• because there is no competition monopolist have little incentive to introduce new products and techniques.

• Monopolies also restrict entries of new firms and drive them out of business

• there is lack of choice for consumers in the market.

Slides prepared by Bized