matrix quick links - prioritywholesale.net fannie mae requirements and that all loans submitted to...

TRANSCRIPT

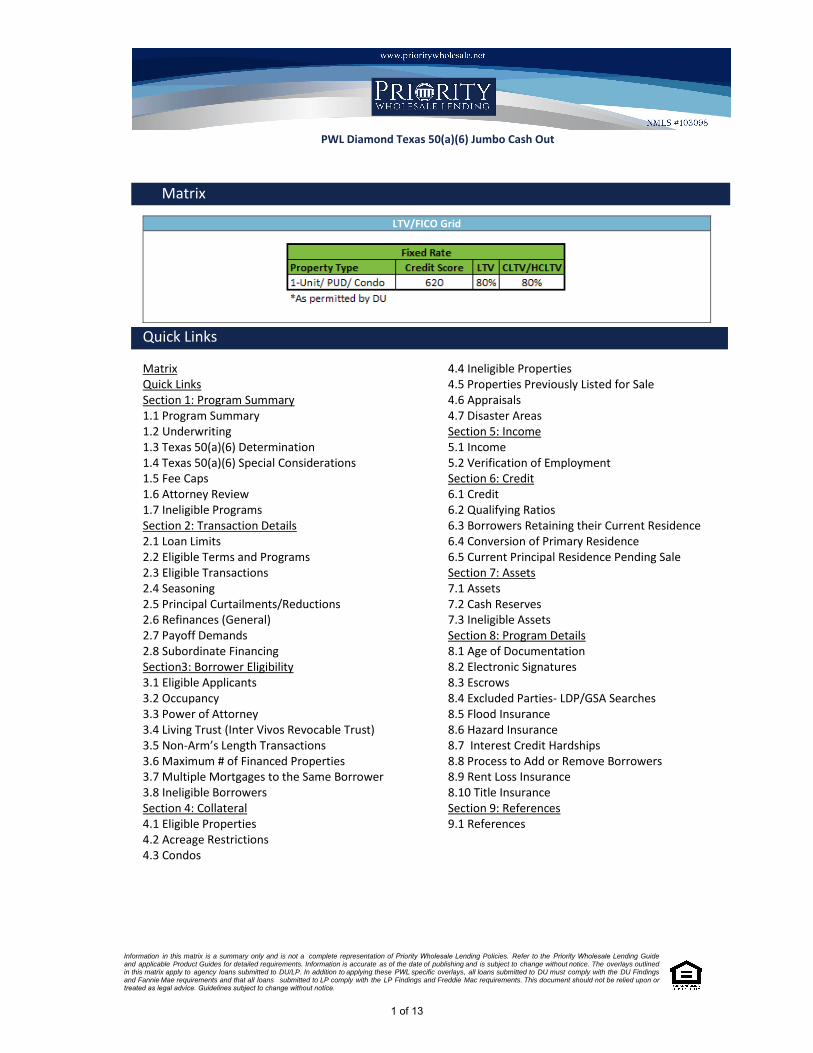

LTV/FICO Grid

Quick Links

Matrix Quick Links Section 1: Program Summary 1.1 Program Summary 1.2 Underwriting 1.3 Texas 50(a)(6) Determination 1.4 Texas 50(a)(6) Special Considerations 1.5 Fee Caps 1.6 Attorney Review 1.7 Ineligible Programs Section 2: Transaction Details 2.1 Loan Limits 2.2 Eligible Terms and Programs 2.3 Eligible Transactions 2.4 Seasoning 2.5 Principal Curtailments/Reductions 2.6 Refinances (General) 2.7 Payoff Demands 2.8 Subordinate Financing Section3: Borrower Eligibility 3.1 Eligible Applicants 3.2 Occupancy 3.3 Power of Attorney 3.4 Living Trust (Inter Vivos Revocable Trust) 3.5 Non-Arm’s Length Transactions 3.6 Maximum # of Financed Properties 3.7 Multiple Mortgages to the Same Borrower 3.8 Ineligible Borrowers Section 4: Collateral 4.1 Eligible Properties 4.2 Acreage Restrictions 4.3 Condos

4.4 Ineligible Properties 4.5 Properties Previously Listed for Sale 4.6 Appraisals 4.7 Disaster Areas Section 5: Income 5.1 Income 5.2 Verification of Employment Section 6: Credit 6.1 Credit 6.2 Qualifying Ratios 6.3 Borrowers Retaining their Current Residence 6.4 Conversion of Primary Residence 6.5 Current Principal Residence Pending Sale Section 7: Assets 7.1 Assets 7.2 Cash Reserves 7.3 Ineligible Assets Section 8: Program Details 8.1 Age of Documentation 8.2 Electronic Signatures 8.3 Escrows 8.4 Excluded Parties- LDP/GSA Searches 8.5 Flood Insurance 8.6 Hazard Insurance 8.7 Interest Credit Hardships 8.8 Process to Add or Remove Borrowers 8.9 Rent Loss Insurance 8.10 Title Insurance Section 9: References 9.1 References

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

Matrix

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

1 of 13

1.1 Program Summary

Program Summary This Program Guide serves as a comprehensive summary of Priority Wholesale Lending's Conventional Underwriting Overlays. Refer to Fannie Mae’s SellingGuide for any information not specified in the Program Summary.

1.2 Underwriting

Underwriting

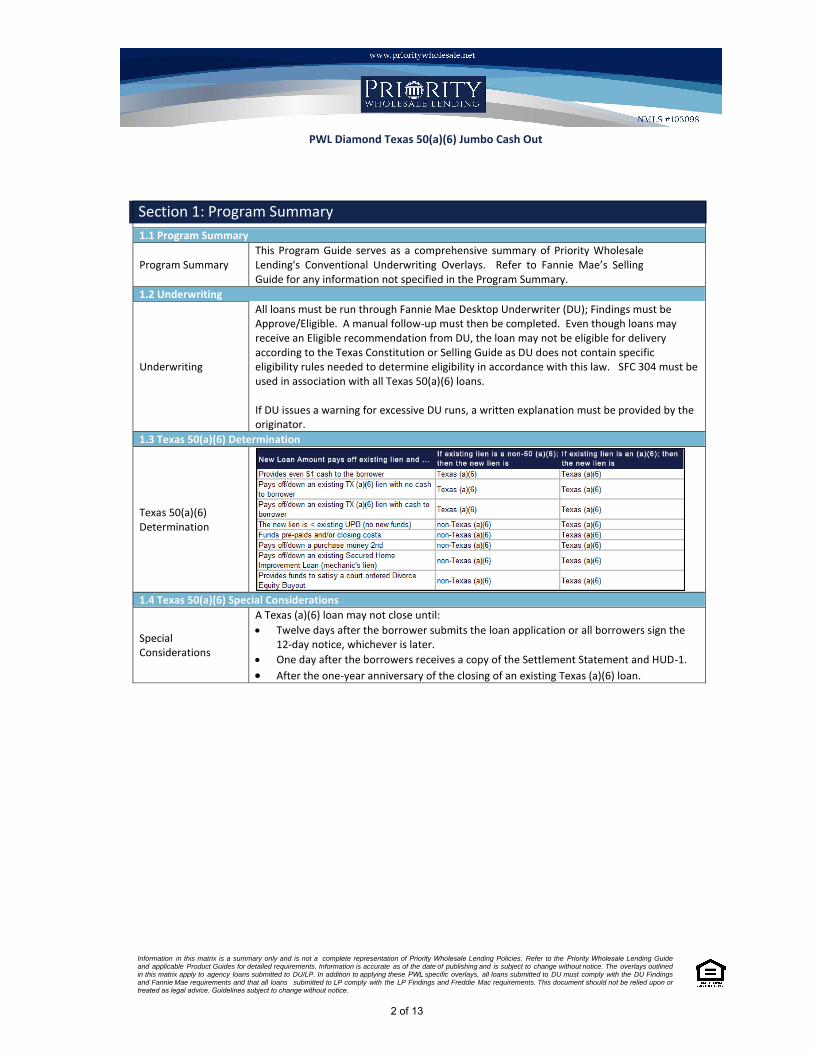

All loans must be run through Fannie Mae Desktop Underwriter (DU); Findings must be Approve/Eligible. A manual follow-up must then be completed. Even though loans may receive an Eligible recommendation from DU, the loan may not be eligible for delivery according to the Texas Constitution or Selling Guide as DU does not contain specific eligibility rules needed to determine eligibility in accordance with this law. SFC 304 must be used in association with all Texas 50(a)(6) loans.

If DU issues a warning for excessive DU runs, a written explanation must be provided by the originator.

1.3 Texas 50(a)(6) Determination

Texas 50(a)(6) Determination

1.4 Texas 50(a)(6) Special Considerations

Special Considerations

A Texas (a)(6) loan may not close until:

Twelve days after the borrower submits the loan application or all borrowers sign the12-day notice, whichever is later.

One day after the borrowers receives a copy of the Settlement Statement and HUD-1.

After the one-year anniversary of the closing of an existing Texas (a)(6) loan.

Section 1: Program Summary

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

2 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

1.5 Fee Caps

Fee Caps

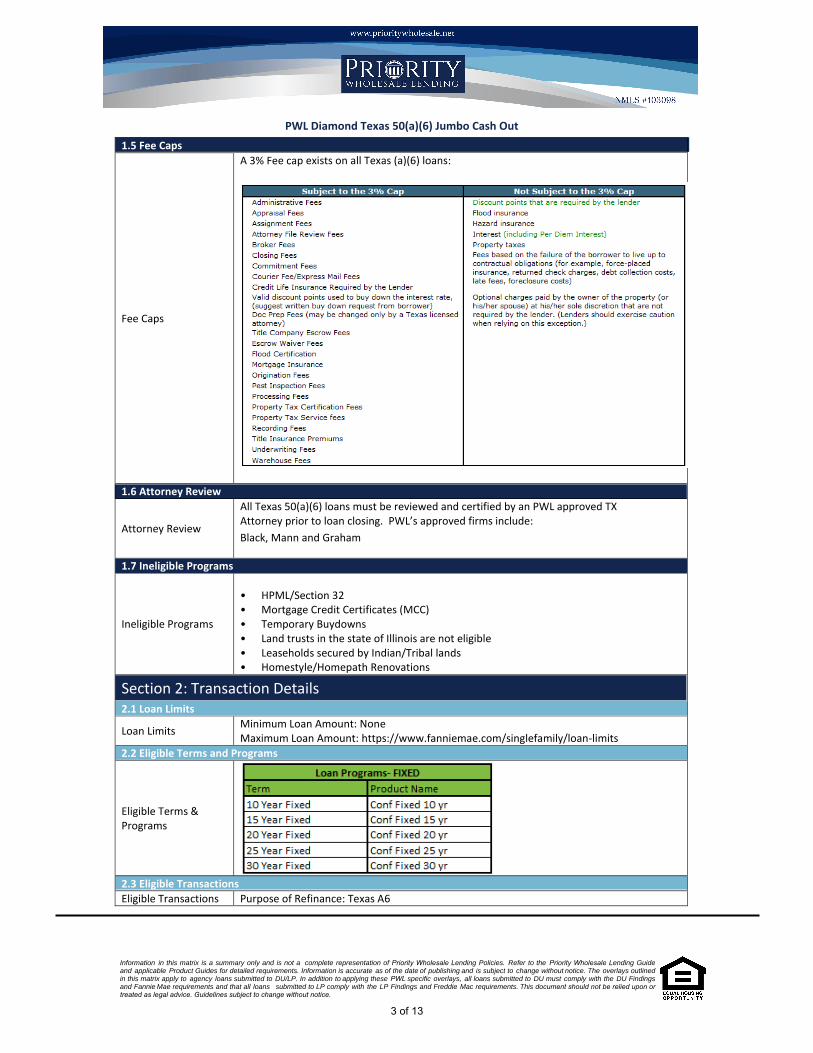

A 3% Fee cap exists on all Texas (a)(6) loans:

1.6 Attorney Review

Attorney Review

All Texas 50(a)(6) loans must be reviewed and certified by an PWL approved TXAttorney prior to loan closing. PWL’s approved firms include:

Black, Mann and Graham

Ineligible Programs

• HPML/Section 32• Mortgage Credit Certificates (MCC)• Temporary Buydowns• Land trusts in the state of Illinois are not eligible• Leaseholds secured by Indian/Tribal lands• Homestyle/Homepath Renovations

Section 2: Transaction Details 2.1 Loan Limits

Loan LimitsMinimum Loan Amount: None Maximum Loan Amount: https://www.fanniemae.com/singlefamily/loan-limits

2.2 Eligible Terms and Programs

Eligible Terms & Programs

2.3 Eligible Transactions Eligible Transactions Purpose of Refinance: Texas A6

1.7 Ineligible Programs

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

3 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

2.4 Seasoning

Seasoning

If an existing Texas 50(a)(6) first or second mortgage will be paid off, the lender must verify that 12 months have passed since the closing date of the existing TX 50(a)(6) loan being paid off before the new lien is secured. TX only permits one equity loan at a time and only one within a 12 month period.

2.5 Principal Curtailments/Reductions Principal Curtailments/Reductions Permitted in instances where there is excess lender credit only

2.6 Refinances (General)

Refinances (General) Continuity of Obligation as defined in FNMA B2-1.2-04 must be met

A Net Tangible Benefit Worksheet must be completed on ALL refinance transactions

2.7 Payoff Demands

Payoff Demands

Payoff demands are required to ensure the current lien is paid in full prior to closing. The expiration date of the payoff demand must be reviewed. A loan may not move to closing if the payoff will expire prior to funding. If the payoff demand contains an expiration date, the underwriter must verify the date is after the funding date.

If the payoff demand does not contain an expiration date, the underwriter must verify a per diem amount is listed. The per diem should be applied to the payoff amount to cover proceeds through the funding date; it can be used for an unlimited number of days; unless otherwise specified in the payoff letter.

A payoff is considered expired when:

The document instructs the associate to void after a specified date; or

The interest accrued amount on the statement signals the borrower will be past-duewhen the new loan funds;o The borrower must make a mortgage payment prior to closing to avoid a late

payment on the credit; ando The borrower must provide evidence the payment has been made and the

updated payoff demand must reflect that a payment has been made.

2.8 Subordinate Financing

Subordinate Financing

New subordinate financing is not permitted on a first lien TX (a)(6).

Existing subordinate liens on the real estate that are not paid off with the new 50(a)(6) loan are permitted provided that: the subordinated 2nd mortgages cannot already be a 50(a)(6) loan (verification is required-the title company must obtain a copy of the security instrument) and the subordinated 2nd mortgage must meet the 80% CLTV requirement. HELOCs are not eligible for subordinate financing.

A copy of the subordinating Note, Mortgage/Deed and Subordination Agreement is also required.

Section3: Borrower Eligibility 3.1 Eligible Applicants

Eligible Applicants

All borrowers must have valid and verifiable Social Security Numbers, as well as a valid driver’s license, state-issued ID or passport. Other forms of taxpayer identification are not allowed.

Borrowers must be either U.S. Citizens or be lawful permanent or non-permanent residents of the United States. A non-U.S. citizen, who is lawfully residing in the U.S. as a permanent or a nonpermanent resident alien, is eligible for a mortgage on the same terms as a U.S. citizen.

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

4 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

There can be no more than 4 borrowers per loan.

A married borrower cannot create a lien against the property unless his/her spouse consents to the lien by signing all applicable program and closing disclosures and documents.

3.2 Occupancy

Occupancy Eligible occupancy types include:

1 unit Primary Residences serving are the borrower’s TX Homestead

3.3 Power of Attorney Power of Attorney Not permitted

3.4 Living Trust (Inter Vivos Revocable Trust)

Living Trust (Inter Vivos Revocable Trust)

A living trust is an eligible mortgage borrower if it meets the following requirements as well as State requirements. All trusts must be approved by PWL legal prior to Loan Approval.

To determine whether or not the Trust meets all the criteria required by State and investor standards, one of the following will be required:

A copy of the trust document must be included in the file

Trust must meet “qualifying trust” under Texas law for purposes of owning residentialproperty that qualifies for the homestead exemption

3.5 Non-Arm’s Length Transactions Non-Arm’s Length Transactions

Not permitted

3.6 Maximum # of Financed Properties

Maximum # of Financed Properties

Borrowers financing their Primary Residence may have up to 10 properties (financed orfree & clear). Borrowers with greater than 4 financed properties must have a minimum12 month history of landlord experience (the agencies may require additionalexperience).

These limitations apply to the borrower’s ownership in one-to four unit properties ormortgage obligations on such properties and are cumulative for all borrowers. Thislimitation includes properties financed abroad.

3.7 Multiple Mortgages to the Same Borrower Multiple Mortgages to the Same Borrower

• PWL will finance no more than 4 properties for any oneborrower

• PWL limits its maximum exposure to one borrower at $1.5M• Maximum of 2 financed units in a single condo project or PUD 3.8 Ineligible Borrowers

Ineligible Borrower (Ineligible Applicants)

Non-Occupant Co-Borrowers

Co-Signers/Co-Guarantors

Limited Partnerships, Corporations and LLC’s

Non-Revocable Trusts or Guardianships

Foreign Nationals

Borrowers with Diplomatic Immunity

Individuals Employed by PWL Third PartyOriginators

Individuals on the LPD/GSA exclusionary listsSection 4: Collateral 4.1 Eligible Properties

Eligible Properties

Attached/Detached SFRs (1 Unit)

Attached/Detached PUDs (1 Unit)

Low/Mid/High-Rise Condos and site Condos

Modular Homes (these are not considered to be manufactured and are eligible underthe guidelines for 1-unit properties)

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

5 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

Mixed Use Properties: For mixed use properties, originators may follow FNMA guidelines with the exception that the square footage of commercial part of the property cannot exceed 25% of the total square footage

Deed Restricted Properties: All deed restricted properties must be reviewed and approved by legal prior to loan approval and must adhere to FNMA requirements (B5-5.2) and Texas State Law

4.2 Acreage Restrictions

Acreage Restrictions Urban Homesteads – maximum 10 acres per Article XVI, Section 50(a)(6) of the Texas

Constitution (no exceptions)

Rural Homesteads- maximum 25 acres

4.3 Condos

Condos

Condominiums must be either: 1) Fannie Mae approved: https://www.efanniemae.com/sf/refmaterials/approvedprojects/or2) DU/DO Findings must provide for a limited review, CPM Expedited or Full Lender Review(which is required for new construction projects)• On CPM approved condos, PWL will allow up to 10% lender exposure. A Condo ProjectManager certification is valid for 90 days; after 90 days an updated Dec Page andQuestionnaire must be provided.• Limited review not permitted on new projects, investment properties or LTV >80%.• PWL will allow financing on 100% of the units of a PERS fully-approved condo with thefollowing limitation: Loans that are sold to FNMA/FHLMC and held within our servicingportfolio cannot exceed 25% of the project. All loans within a project must be registeredwith the Condo Review Department• FNMA Special Designation- FNMA approved condos with unexpired special designationcodes will be permitted for primary residences. Project must be eligible and reviewed witheither a limited or full review based on the AUS findings; FNMA Special Designation is noteligible with LP Findings• Leasehold not permitted

Short-Term Rentals: A Short Term Rental (generally a rental period less than 30 days) doesn’t disqualify a project from approval as long as the home owner’s association has absolutely no involvement in the facilitation of renting of units on a short term basis.

Typically, units that are being advertised for nightly or weekly rentals through any of the following sources are acceptable:

Rental Agency

Vacation Club

Third Party Management Company

VRBO

Individual Unit Owners

Ineligible projects: Hotel or motel conversions (or conversion of other similar transient properties)

Projects that are managed & operated as a hotel or motel, even though the units areindividually owned

Projects that included the word “hotel” or ‘motel”

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

6 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

Projects that include registration services, registration desks and offer rentals of anyunits on a daily basis

Timeshares or segmented ownership

Projects where units are advertised for short term rentals or registration can becompleted on the HOA website

The project is also ineligible if the Homeowner Association’s budget shows income from non-incidental business operations such as:

Restaurants / Bars

Spas

Leasing Pool Passes

Dock / Marina

Valet Parking / Garage Fees

Maid Services (daily cleaning)

Room Service

Beach Shuttles

Established projects where the budget shows less than 5% of the overall income from non-incidental business operations may be eligible for a loan level exception from FNMA. The condo review team will submit the project through CVAS for an exception review. The cost for each review is $200 regardless of the outcome and the process takes approx. 48-72 hours to complete.

The appraisal report, condo questionnaire or sales contract may identify characteristics that would make the project ineligible. These items do not definitively determine the condo is a condo hotel; however it provides evidence that would require additional research. These characteristics are red flags and warrant further investigation but are not limited to:

Central telephone system

Room Service

Units that don’t contain full-sized kitchen appliances

Daily Cleaning Services

Advertising of rental rates

Registration Services

Restrictions on interior decorating

Franchise Agreement

Central Key System

Location of the project in a resort area

The occupancy of the project (The project may have few or even no owner occupants)

Projects converted from a hotel or motel

4.4 Ineligible Properties

Ineligible Properties

• 2-4 Unit Properties• Co-ops• Condotels• Non-Warrantable Condos• Manufactured/Mobile homes• Geodesic Domes, Berms, Earth homes• Hobby Farms• Bed and Breakfast Properties• Live/Work Units not meeting the standards of a Mixed Use Property• Properties with manufactured on site being used as storage• Properties with excessive acreage

Diamond Texas 50(a)(6) Jumbo Cash Out

7 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

• Properties where farm or agricultural income from the subject property is claimed onborrowers tax returns

• Properties/Land held in a life estate• Properties encumbered with private transfer fee covenants• Properties which are subject to a right of redemption• Properties appraised with a property condition of C5

4.5 Properties Previously Listed for Sale

Properties Previously Listed for Sale

Rate/Term Refi – listing must have been cancelled or expired prior to the application

date, and the borrower must confirm their intent to occupy the subject for Owner

Occupied

Cashout refi – Properties listed for sale in the six months preceding the disbursement

date of the new mortgage loan are limited to 70% LTV/CLTV/HCLTV ratios (or less if

mandated by the specific product, occupancy, or property type)

In all instances, careful consideration should be given to the listing price and appraised

value to be sure the value is supported.

Note: The definition of properties listed for sale includes non-owner occupied properties where the current tenants have a lease-to-own provision in their lease; these transactions are ineligible.

4.6 Appraisals

Appraisals

All appraisals must be ordered and processed in compliance with Appraiser IndependenceRequirements (AIR) through a PWL approved Appraisal Management Company. • A full 1004/appraisal is required on all Texas 50(a)(6) transactions• Appraisal must be completed by a Certified appraiser from an PWL approved

AMC• Copy of the appraiser’s licensee must be included in all funded loan files• The re-use of an appraisal is not permitted 4.7 Disaster Areas

Disaster Areas

Refer to the list of affected counties published by FEMA at the following link: http://www.fema.gov/news/disaster_totals_annual.fema

PWL will require recertification from the appraiser on all loans located in the affectedCounties prior to closing. If the county is indicated as being in a declared disaster area, thepolicy must be adhered to The Disasters are referenced with both an incident start date and an incident ending

date. The property is considered potentially impacted for 120 days from the incidentEND date;

If a full appraisal was obtained on the property prior to the declared disaster, theinspection must verify the property is sound and habitable and in the same conditionas when it was appraised. Any of the following options are acceptable to satisfy thisrequirement:o A 1004D Final Inspection or Appraisal Update signed by the original appraisero FNMA 2075 – Desktop Underwriter Property Inspection Reporto DAIR – Disaster Area Inspection Report

Full appraisals obtained after the declaration need to indicate the property has notbeen impacted by the disaster;

The PWL branches will request the appropriate appraisal or inspection through the normal channels; TPO clients will be required to furnish Priority Wholesale Lendingwith the proper recertification prior to loan approval.

Section 5: Income

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

8 of 13

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

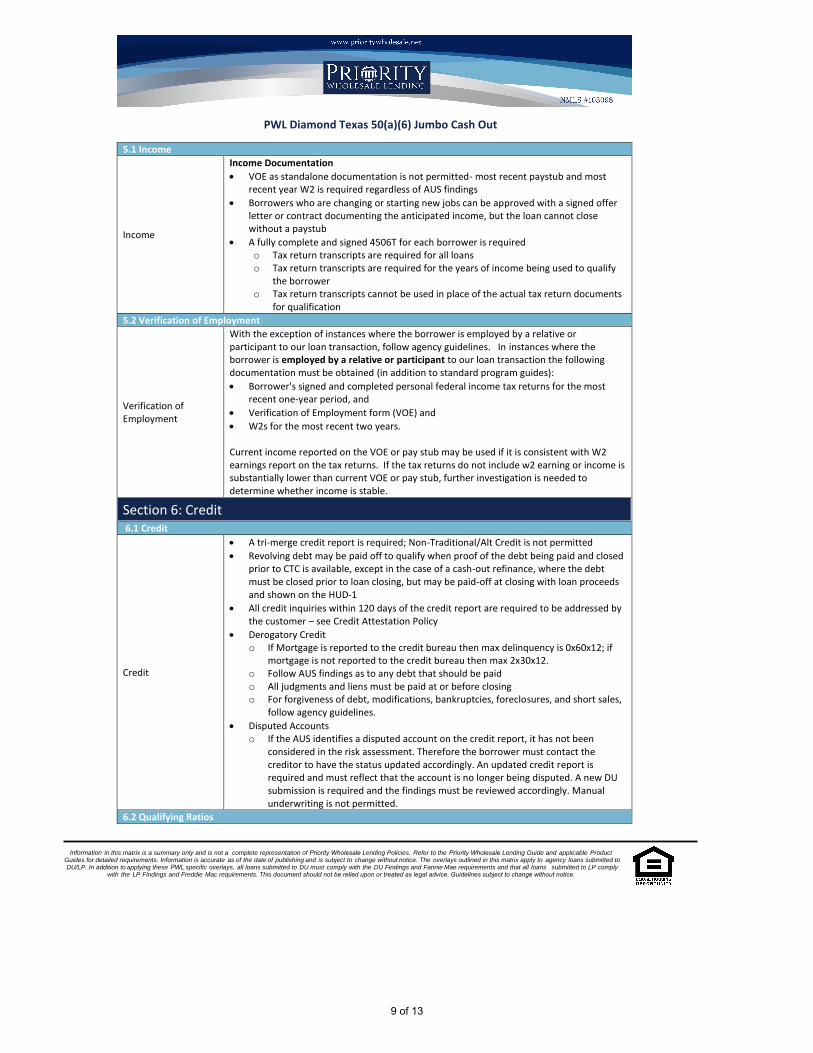

5.1 Income

Income

Income Documentation VOE as standalone documentation is not permitted- most recent paystub and most

recent year W2 is required regardless of AUS findings

Borrowers who are changing or starting new jobs can be approved with a signed offerletter or contract documenting the anticipated income, but the loan cannot closewithout a paystub

A fully complete and signed 4506T for each borrower is requiredo Tax return transcripts are required for all loanso Tax return transcripts are required for the years of income being used to qualify

the borrowero Tax return transcripts cannot be used in place of the actual tax return documents

for qualification

5.2 Verification of Employment

Verification of Employment

With the exception of instances where the borrower is employed by a relative or participant to our loan transaction, follow agency guidelines. In instances where the borrower is employed by a relative or participant to our loan transaction the followingdocumentation must be obtained (in addition to standard program guides):

Borrower's signed and completed personal federal income tax returns for the mostrecent one-year period, and

Verification of Employment form (VOE) and

W2s for the most recent two years.

Current income reported on the VOE or pay stub may be used if it is consistent with W2 earnings report on the tax returns. If the tax returns do not include w2 earning or income is substantially lower than current VOE or pay stub, further investigation is needed to determine whether income is stable.

Section 6: Credit 6.1 Credit

Credit

A tri-merge credit report is required; Non-Traditional/Alt Credit is not permitted

Revolving debt may be paid off to qualify when proof of the debt being paid and closedprior to CTC is available, except in the case of a cash-out refinance, where the debtmust be closed prior to loan closing, but may be paid-off at closing with loan proceedsand shown on the HUD-1

All credit inquiries within 120 days of the credit report are required to be addressed bythe customer – see Credit Attestation Policy

Derogatory Credito If Mortgage is reported to the credit bureau then max delinquency is 0x60x12; if

mortgage is not reported to the credit bureau then max 2x30x12.o Follow AUS findings as to any debt that should be paido All judgments and liens must be paid at or before closingo For forgiveness of debt, modifications, bankruptcies, foreclosures, and short sales,

follow agency guidelines.

Disputed Accountso If the AUS identifies a disputed account on the credit report, it has not been

considered in the risk assessment. Therefore the borrower must contact thecreditor to have the status updated accordingly. An updated credit report isrequired and must reflect that the account is no longer being disputed. A new DUsubmission is required and the findings must be reviewed accordingly. Manualunderwriting is not permitted.

6.2 Qualifying Ratios

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply

with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

9 of 13

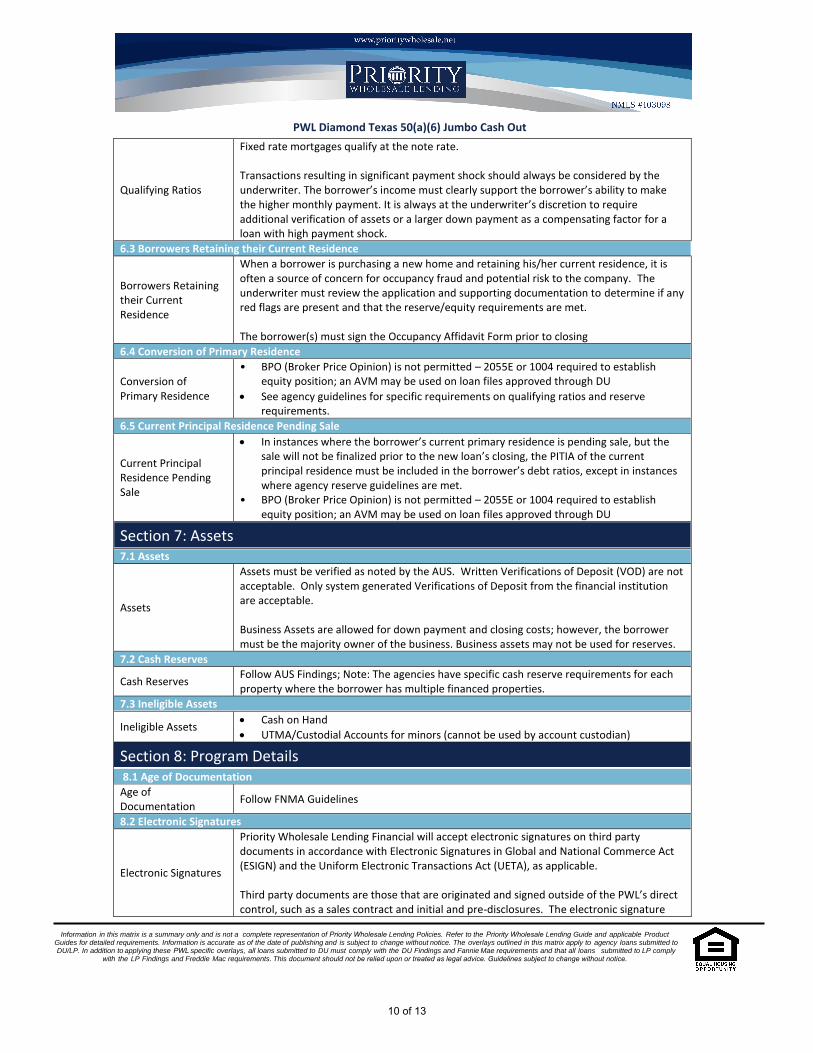

Qualifying Ratios

Fixed rate mortgages qualify at the note rate.

Transactions resulting in significant payment shock should always be considered by the underwriter. The borrower’s income must clearly support the borrower’s ability to make the higher monthly payment. It is always at the underwriter’s discretion to require additional verification of assets or a larger down payment as a compensating factor for a loan with high payment shock.

6.3 Borrowers Retaining their Current Residence

Borrowers Retaining their Current Residence

When a borrower is purchasing a new home and retaining his/her current residence, it is often a source of concern for occupancy fraud and potential risk to the company. The underwriter must review the application and supporting documentation to determine if any red flags are present and that the reserve/equity requirements are met.

The borrower(s) must sign the Occupancy Affidavit Form prior to closing

6.4 Conversion of Primary Residence

Conversion of Primary Residence

• BPO (Broker Price Opinion) is not permitted – 2055E or 1004 required to establishequity position; an AVM may be used on loan files approved through DU

See agency guidelines for specific requirements on qualifying ratios and reserverequirements.

6.5 Current Principal Residence Pending Sale

Current Principal Residence Pending Sale

In instances where the borrower’s current primary residence is pending sale, but thesale will not be finalized prior to the new loan’s closing, the PITIA of the currentprincipal residence must be included in the borrower’s debt ratios, except in instanceswhere agency reserve guidelines are met.

• BPO (Broker Price Opinion) is not permitted – 2055E or 1004 required to establishequity position; an AVM may be used on loan files approved through DU

Section 7: Assets 7.1 Assets

Assets

Assets must be verified as noted by the AUS. Written Verifications of Deposit (VOD) are not acceptable. Only system generated Verifications of Deposit from the financial institution are acceptable.

Business Assets are allowed for down payment and closing costs; however, the borrower must be the majority owner of the business. Business assets may not be used for reserves.

7.2 Cash Reserves

Cash Reserves Follow AUS Findings; Note: The agencies have specific cash reserve requirements for each property where the borrower has multiple financed properties.

7.3 Ineligible Assets

Ineligible Assets Cash on Hand

UTMA/Custodial Accounts for minors (cannot be used by account custodian)

Section 8: Program Details 8.1 Age of Documentation Age of Documentation

Follow FNMA Guidelines

8.2 Electronic Signatures

Electronic Signatures

Priority Wholesale Lending Financial will accept electronic signatures on third party documents in accordance with Electronic Signatures in Global and National Commerce Act (ESIGN) and the Uniform Electronic Transactions Act (UETA), as applicable.

Third party documents are those that are originated and signed outside of the PWL’s directcontrol, such as a sales contract and initial and pre-disclosures. The electronic signature

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply

with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

10 of 13

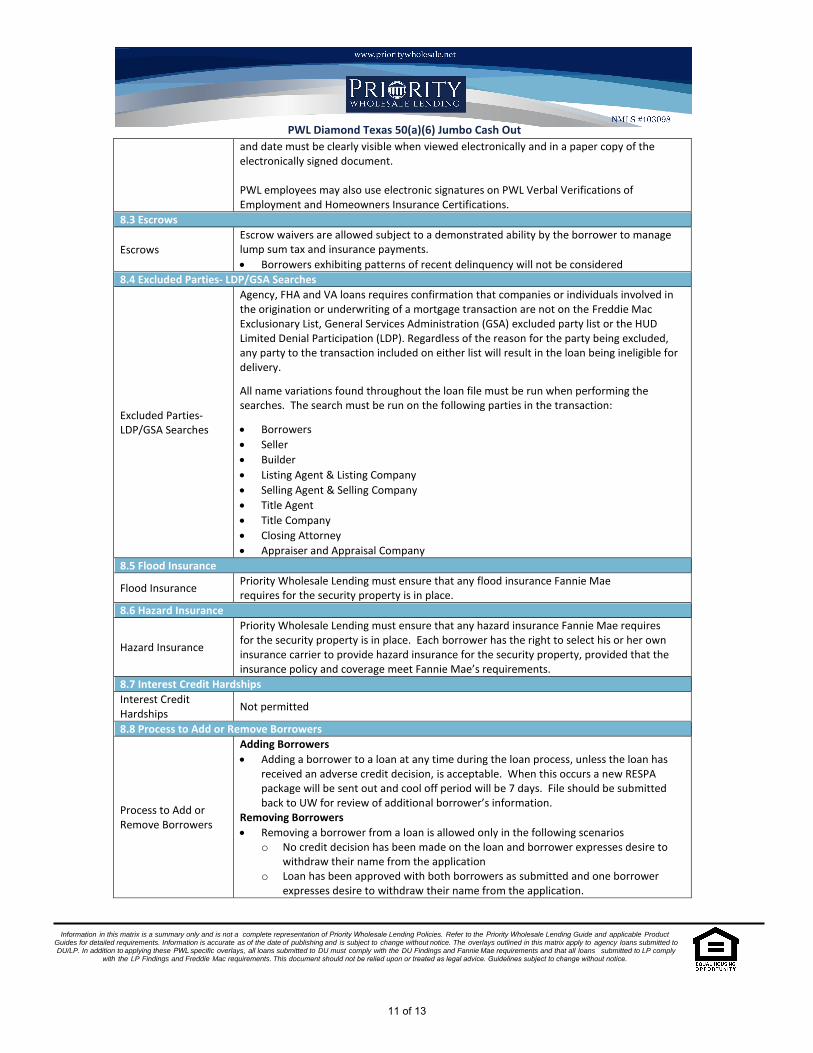

and date must be clearly visible when viewed electronically and in a paper copy of the electronically signed document.

PWL employees may also use electronic signatures on PWL Verbal Verifications of Employment and Homeowners Insurance Certifications.

8.3 Escrows

Escrows

Escrow waivers are allowed subject to a demonstrated ability by the borrower to manage lump sum tax and insurance payments.

Borrowers exhibiting patterns of recent delinquency will not be considered

8.4 Excluded Parties- LDP/GSA Searches

Excluded Parties- LDP/GSA Searches

Agency, FHA and VA loans requires confirmation that companies or individuals involved in the origination or underwriting of a mortgage transaction are not on the Freddie Mac Exclusionary List, General Services Administration (GSA) excluded party list or the HUD Limited Denial Participation (LDP). Regardless of the reason for the party being excluded, any party to the transaction included on either list will result in the loan being ineligible for delivery.

All name variations found throughout the loan file must be run when performing the searches. The search must be run on the following parties in the transaction:

Borrowers

Seller

Builder

Listing Agent & Listing Company

Selling Agent & Selling Company

Title Agent

Title Company

Closing Attorney

Appraiser and Appraisal Company

8.5 Flood Insurance

Flood Insurance Priority Wholesale Lending must ensure that any flood insurance Fannie Maerequires for the security property is in place.

8.6 Hazard Insurance

Hazard Insurance

Priority Wholesale Lending must ensure that any hazard insurance Fannie Mae requiresfor the security property is in place. Each borrower has the right to select his or her own insurance carrier to provide hazard insurance for the security property, provided that the insurance policy and coverage meet Fannie Mae’s requirements.

8.7 Interest Credit Hardships Interest Credit Hardships

Not permitted

8.8 Process to Add or Remove Borrowers

Process to Add or Remove Borrowers

Adding Borrowers Adding a borrower to a loan at any time during the loan process, unless the loan has

received an adverse credit decision, is acceptable. When this occurs a new RESPApackage will be sent out and cool off period will be 7 days. File should be submittedback to UW for review of additional borrower’s information.

Removing Borrowers Removing a borrower from a loan is allowed only in the following scenarios

o No credit decision has been made on the loan and borrower expresses desire towithdraw their name from the application

o Loan has been approved with both borrowers as submitted and one borrowerexpresses desire to withdraw their name from the application.

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply

with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

11 of 13

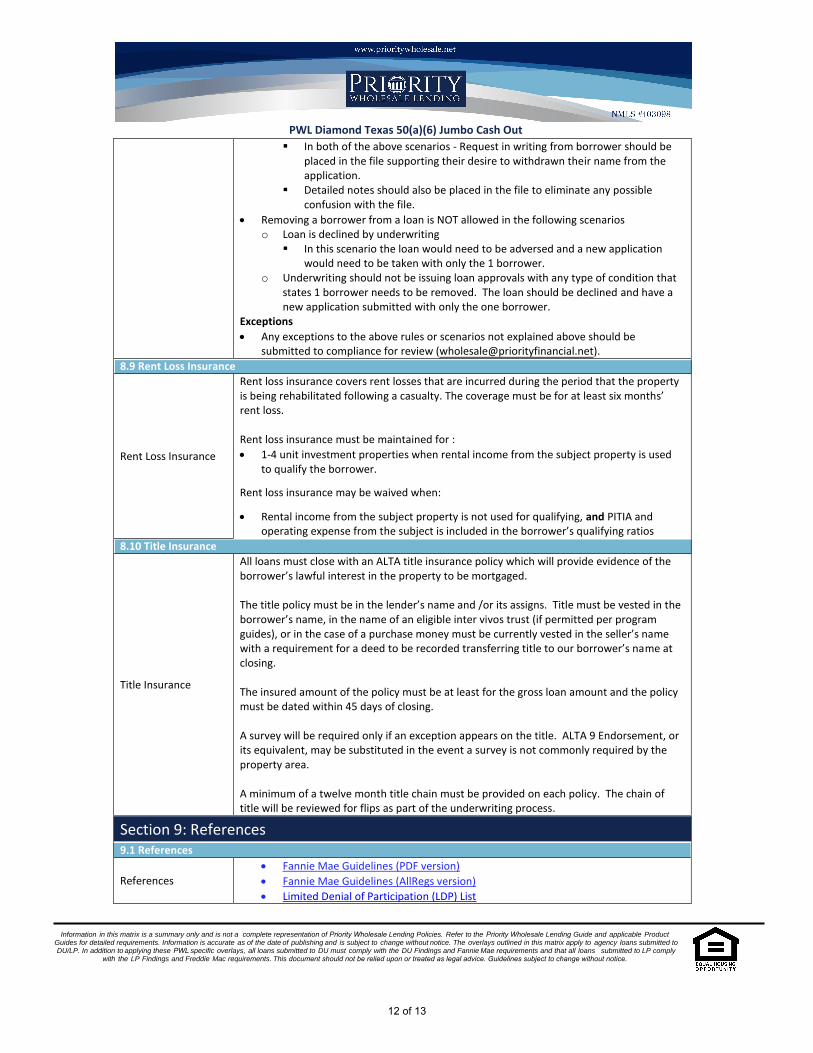

In both of the above scenarios - Request in writing from borrower should beplaced in the file supporting their desire to withdrawn their name from theapplication.

Detailed notes should also be placed in the file to eliminate any possibleconfusion with the file.

Removing a borrower from a loan is NOT allowed in the following scenarioso Loan is declined by underwriting

In this scenario the loan would need to be adversed and a new applicationwould need to be taken with only the 1 borrower.

o Underwriting should not be issuing loan approvals with any type of condition thatstates 1 borrower needs to be removed. The loan should be declined and have anew application submitted with only the one borrower.

Exceptions Any exceptions to the above rules or scenarios not explained above should be

submitted to compliance for review ([email protected]).

8.9 Rent Loss Insurance

Rent Loss Insurance

Rent loss insurance covers rent losses that are incurred during the period that the property is being rehabilitated following a casualty. The coverage must be for at least six months’ rent loss.

Rent loss insurance must be maintained for :

1-4 unit investment properties when rental income from the subject property is usedto qualify the borrower.

Rent loss insurance may be waived when:

Rental income from the subject property is not used for qualifying, and PITIA andoperating expense from the subject is included in the borrower’s qualifying ratios

8.10 Title Insurance

Title Insurance

All loans must close with an ALTA title insurance policy which will provide evidence of the borrower’s lawful interest in the property to be mortgaged.

The title policy must be in the lender’s name and /or its assigns. Title must be vested in the borrower’s name, in the name of an eligible inter vivos trust (if permitted per program guides), or in the case of a purchase money must be currently vested in the seller’s name with a requirement for a deed to be recorded transferring title to our borrower’s name at closing.

The insured amount of the policy must be at least for the gross loan amount and the policy must be dated within 45 days of closing.

A survey will be required only if an exception appears on the title. ALTA 9 Endorsement, or its equivalent, may be substituted in the event a survey is not commonly required by the property area.

A minimum of a twelve month title chain must be provided on each policy. The chain of title will be reviewed for flips as part of the underwriting process.

Section 9: References 9.1 References

References

Fannie Mae Guidelines (PDF version)

Fannie Mae Guidelines (AllRegs version)

Limited Denial of Participation (LDP) List

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply

with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

12 of 13

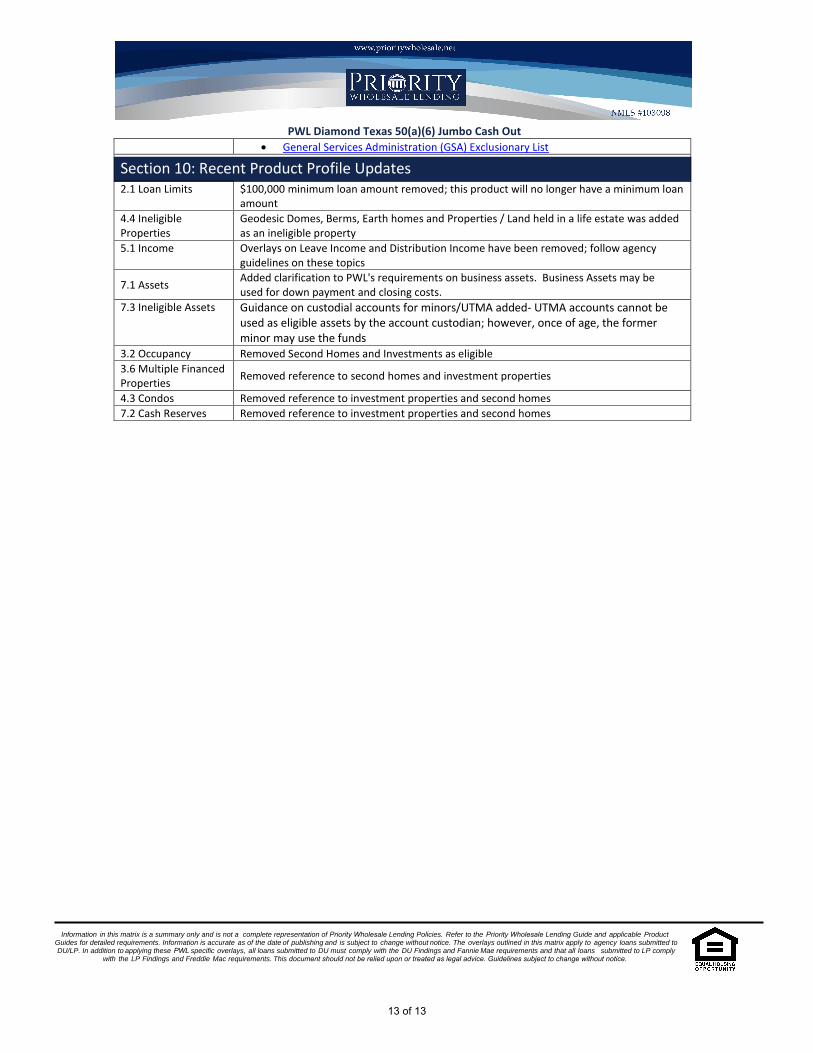

General Services Administration (GSA) Exclusionary List

Section 10: Recent Product Profile Updates 2.1 Loan Limits $100,000 minimum loan amount removed; this product will no longer have a minimum loan

amount

4.4 Ineligible Properties

Geodesic Domes, Berms, Earth homes and Properties / Land held in a life estate was added as an ineligible property

5.1 Income Overlays on Leave Income and Distribution Income have been removed; follow agency guidelines on these topics

7.1 Assets Added clarification to PWL's requirements on business assets. Business Assets may beused for down payment and closing costs.

7.3 Ineligible Assets Guidance on custodial accounts for minors/UTMA added- UTMA accounts cannot be used as eligible assets by the account custodian; however, once of age, the former minor may use the funds

3.2 Occupancy Removed Second Homes and Investments as eligible

3.6 Multiple Financed Properties

Removed reference to second homes and investment properties

4.3 Condos Removed reference to investment properties and second homes

7.2 Cash Reserves Removed reference to investment properties and second homes

Information in this matrix is a summary only and is not a complete representation of Priority Wholesale Lending Policies. Refer to the Priority Wholesale Lending Guide and applicable Product Guides for detailed requirements. Information is accurate as of the date of publishing and is subject to change without notice. The overlays outlined in this matrix apply to agency loans submitted to DU/LP. In addition to applying these PWL specific overlays, all loans submitted to DU must comply with the DU Findings and Fannie Mae requirements and that all loans submitted to LP comply

with the LP Findings and Freddie Mac requirements. This document should not be relied upon or treated as legal advice. Guidelines subject to change without notice.

PWL Diamond Texas 50(a)(6) Jumbo Cash Out

13 of 13