mb0041 accounts assingment final

DESCRIPTION

MB0041 SMU MBA SEM-1TRANSCRIPT

FINANCIAL ACCOUNTS

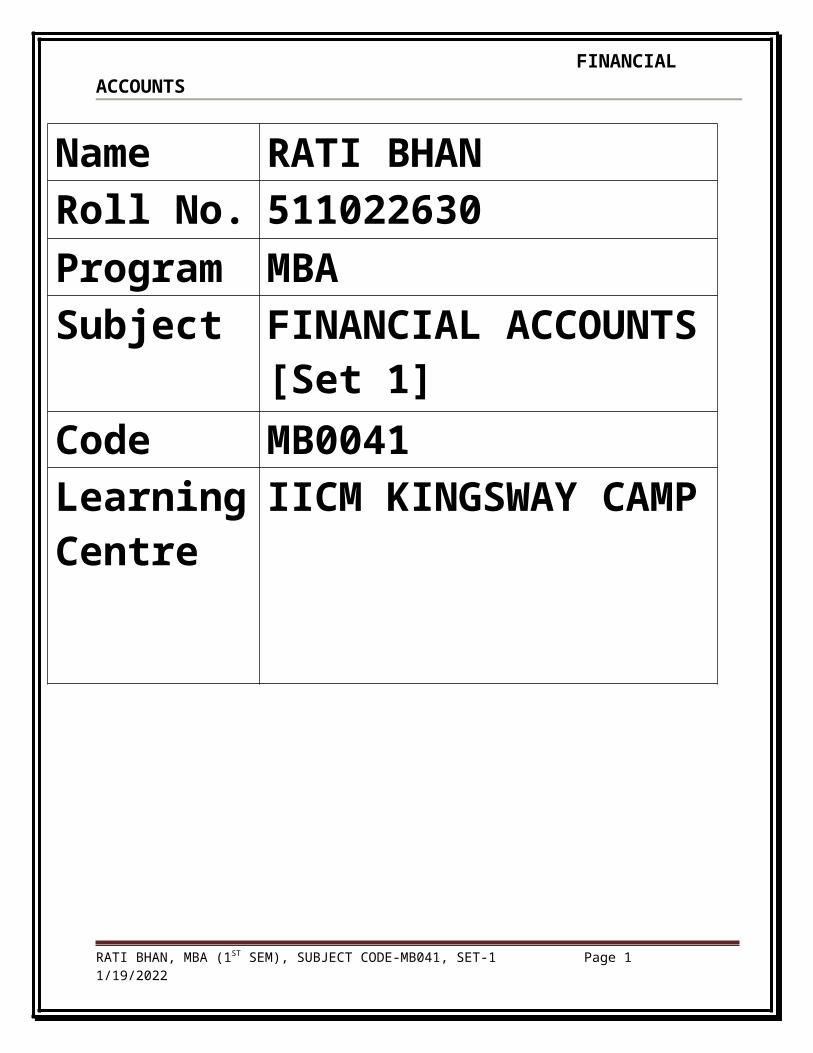

Name RATI BHAN

Roll No. 511022630

Program MBA

Subject FINANCIAL ACCOUNTS [Set 1]

Code MB0041

Learning Centre

IICM KINGSWAY CAMP

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 1 4/11/2023

FINANCIAL ACCOUNTS

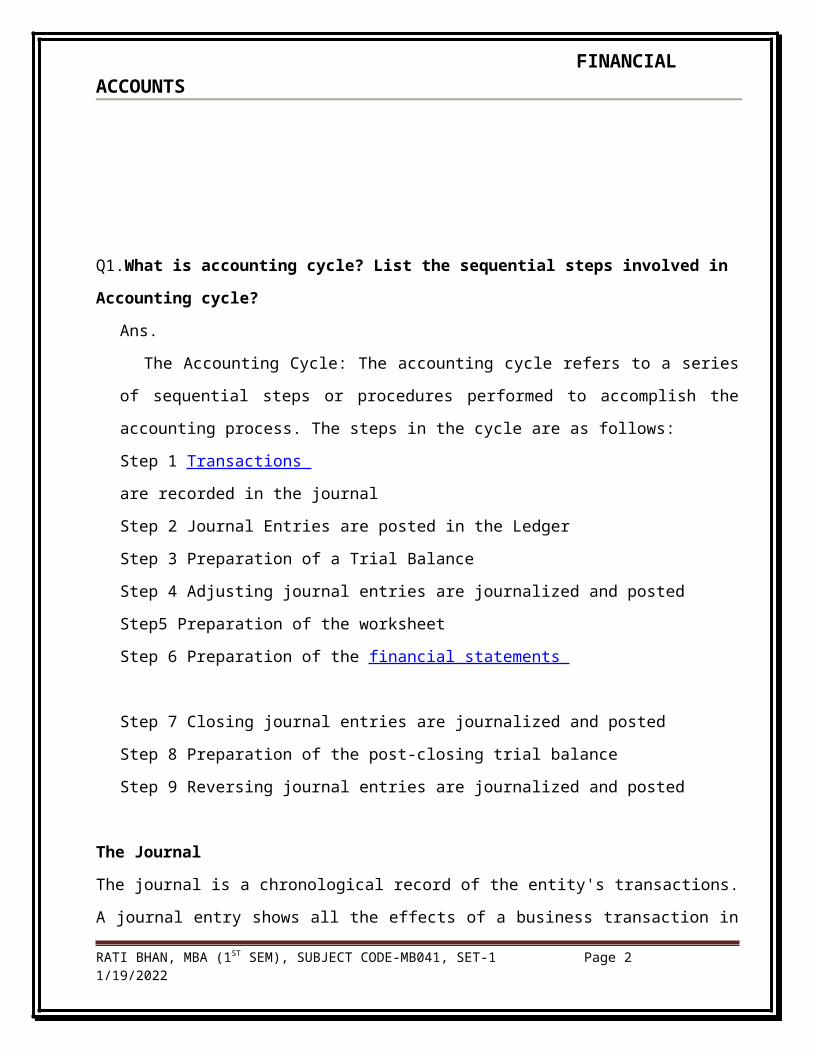

Q1.What is accounting cycle? List the sequential steps involved in Accounting cycle?

Ans.

The Accounting Cycle: The accounting cycle refers to a series of sequential steps or

procedures performed to accomplish the accounting process. The steps in the cycle are as

follows:

Step 1 Transactions

are recorded in the journal

Step 2 Journal Entries are posted in the Ledger

Step 3 Preparation of a Trial Balance

Step 4 Adjusting journal entries are journalized and posted

Step5 Preparation of the worksheet

Step 6 Preparation of the financial statements

Step 7 Closing journal entries are journalized and posted

Step 8 Preparation of the post-closing trial balance

Step 9 Reversing journal entries are journalized and posted

The Journal

The journal is a chronological record of the entity's transactions. A journal entry shows all the

effects of a business transaction in terms of debits and credits. Each transaction is initially

recorded in a journal rather than directly in the ledger. A journal is called the book of original

entry. Of only two accounts are affected- one account is debited and the oilier account is

credited- it is called a Simple Journal entry. When three or more accounts are required in a

journal entry, the entry is referred to as a Compound entry.

The Ledger

A grouping of the entity's accounts is referred to as the ledger. Although some firms may use

various ledgers to accumulate certain detailed information, all firms have a general ledger. A

general ledger is the reference book of the accounting system and is used to classify and

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 2 4/11/2023

FINANCIAL ACCOUNTS

summarize transactions, and to prepare data for the basic financial statements.

The Trial Balance

The Trial Balance is a list of all accounts with their respective debit or credit balances. It is

prepared to verily the equality of debits and credits in the ledger at the end of each accounting

period or at any time the postings are updated.

Q2.A. Bring out the difference between Indian GAAP and US GAAP norms?

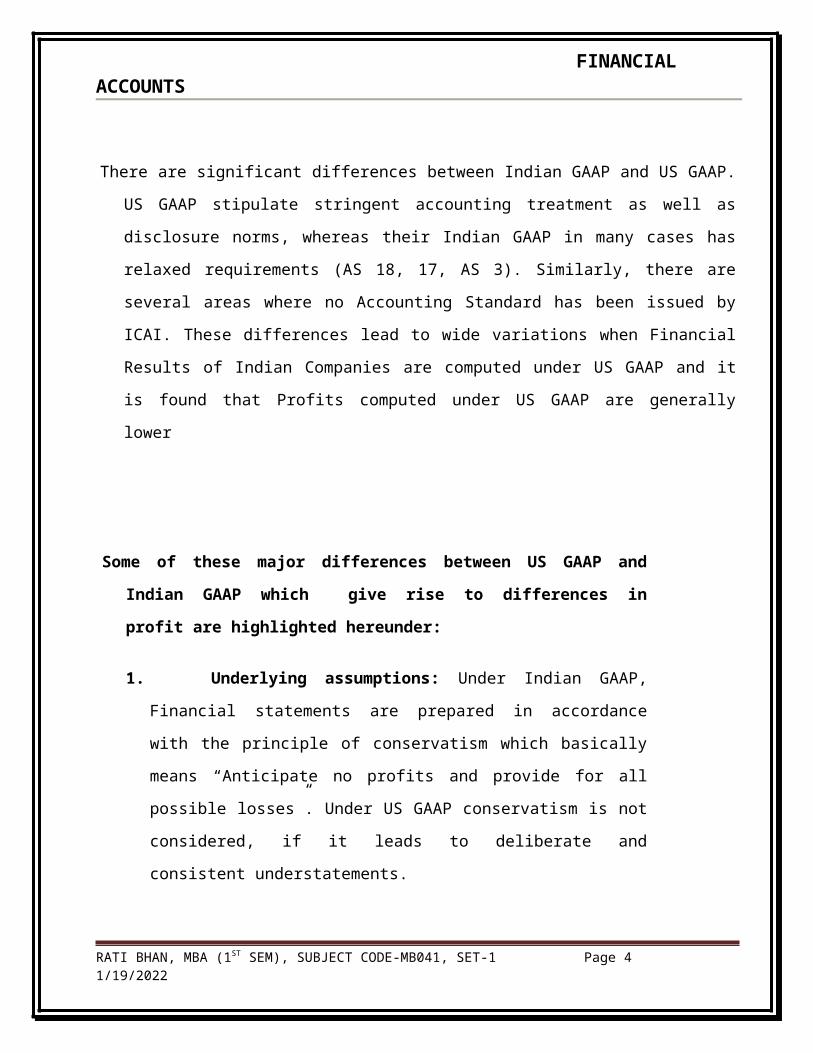

There are significant differences between Indian GAAP and US GAAP. US GAAP stipulate

stringent accounting treatment as well as disclosure norms, whereas their Indian GAAP in

many cases has relaxed requirements (AS 18, 17, AS 3). Similarly, there are several areas

where no Accounting Standard has been issued by ICAI. These differences lead to wide

variations when Financial Results of Indian Companies are computed under US GAAP and

it is found that Profits computed under US GAAP are generally lower

Some of these major differences between US GAAP and Indian GAAP which

give rise to differences in profit are highlighted hereunder:

1. Underlying assumptions: Under Indian GAAP, Financial statements

are prepared in accordance with the principle of conservatism which

basically means “Anticipate no profits and provide for all possible

losses”. Under US GAAP conservatism is not considered, if it leads to

deliberate and consistent understatements.

2. Prudence vs. rules: The Institute of Chartered Accountants of India

(ICAI) has been structuring Accounting Standards based on the

International Accounting Standards (IAS), which employ concepts and

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 3 4/11/2023

FINANCIAL ACCOUNTS

`prudence' as the principle in contrast to the US GAAP, which are “rule

oriented", detailed and complex. It is quite easy for the US accountants to

handle issues that fall within the rules, while the International

Accounting Standards provide a general framework of accounting

standards, which emphasise "substance over form" for accounting. These

rules are less descriptive and their application is based on prudence. US

GAAP has thus issued several Industry specific GAAP, like SFAS 51 (Cable

TV), SFAS 50 (Record and Music Industry) , SFAS 53 ( Motion Picture

Industry) etc.

3. Format/ Presentation of financial statements: Under Indian GAAP,

financial statements are prepared in accordance with the presentation

requirements of Schedule VI to the Companies Act, 1956. On the other

hand, financial statements prepared as per US GAAP are not required to

be prepared under any specific format as long as they comply with the

disclosure requirements of US GAAP. Financial statements to be filed

with SEC include

4. Consolidation of subsidiary companies: Under Indian GAAP (AS 21),

Consolidation of Accounts of subsidiary companies is not mandatory. AS

21 is mandatory if an enterprise presents consolidated financial

statements. In other words, the accounting standard does not mandate

an enterprise to present consolidated financial statements but, if the

enterprise presents consolidated financial statements for complying

with the requirements of any statute or otherwise, it should prepare and

present consolidated financial statements in accordance with AS

21.Thus, the financial income of any company taken in isolation neither

reveals the quantum of business between the group companies nor does

it reveal the true picture of the Group . Savvy promoters hive off their

loss making divisions into separate subsidiaries, so that financial

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 4 4/11/2023

FINANCIAL ACCOUNTS

statement of their Flagship Company looks attractive .Under US GAAP

(SFAS 94), Consolidation of results of Subsidiary Companies is and

should be further segregated as Current or Non mandatory, hence

eliminating material, inter company transaction and giving a true

picture of the operations and Profitability of the various majority owned

Business of the Group.

5. Cash flow statement: Under Indian GAAP (AS 3) , inclusion of Cash

Flow statement in financial statements is mandatory only for companies

whose share are listed on recognized stock exchanges and Certain

enterprises whose turnover for the accounting period exceeds Rs. 50

crore. Thus , unlisted companies escape the burden of providing cash

flow statements as part of their financial statements. On the other hand,

US GAAP (SFAS 95) mandates furnishing of cash flow statements for 3

years – current year and 2 immediate preceding years irrespective of

whether the company is listed or not .

6. Investments: Under Indian GAAP (AS 13), Investments are classified

as Current and Long term. These are to be further classified Government

or Trust securities ,Shares, debentures or bonds Investment properties

Others-specifying nature. Investments classified as current investments

are to be carried in the financial statements at the lower of cost and fair

value determined either on an individual investment basis or by category

of investment, but not on an overall (or global) basis. Investments

classified as long term investments are carried in the financial

statements at cost. However, provision for diminution is to be made to

recognise a decline, other than temporary, in the value of the

investments, such reduction being determined and made for each

investment individually. Under US GAAP ( SFAS 115) , Investments are

required to be segregated in 3 categories i.e. held to Maturity Security

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 5 4/11/2023

FINANCIAL ACCOUNTS

( Primarily Debt Security) , Trading Security and Available for sales

Security current on Individual basis. Debt securities that the enterprise

has the positive intent and ability to hold to maturity are classified as

held-to-maturity securities and reported at amortized cost. Debt and

equity securities that are bought and held principally for the purpose of

selling them in the near term are classified as trading securities and

reported at fair value, with unrealised gains and losses included in

earnings. All Other securities are classified as available-for-sale securities

and reported at fair value, with unrealised gains and losses excluded

from earnings and reported in a separate component of shareholders'

equity

7. Depreciation: Under the Indian GAAP, depreciation is provided based

on rates prescribed by the Companies Act, 1956. Higher depreciation

provision based on estimated useful life of the assets is permitted, but

must be disclosed in Notes to Accounts.( Guidance note no 49) .

Depreciation cannot be provided at a rate lower than prescribed in any

circumstance. Similarly , there is no compulsion to provide depreciation

at a higher rate, even if the actual wear and tear of the equipments is

higher than the rates provided in Companies Act. Thus , an Indian

Company can get away with providing with lesser depreciation , if the

same is in compliance to Companies Act 1956. Contrary to this, under the

US GAAP , depreciation has to be provided over the estimated useful life

of the asset, thus making the Accounting more realistic and providing

sufficient funds for replacement when the asset becomes obsolete and

fully worn out.

8. Foreign currency transactions: Under Indian GAAP(AS11) Forex

transactions ( Monetary items ) are recorded at the rate prevalent on the

transaction date .Year end foreign currency assets and liabilities ( Non

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 6 4/11/2023

FINANCIAL ACCOUNTS

Monetary Items) are re-stated at the closing exchange rates. Exchange

rate differences arising on payments or realizations and restatements at

closing exchange rates are treated as Profit /loss in the income

statement. Exchange fluctuations on liabilities incurred for fixed assets

can be capitalized. Under US GAAP (SFAS 52), Gains and losses on foreign

currency transactions are generally included in determining net income

for the period in which exchange rates change unless the transaction

hedges a foreign currency commitment or a net investment in a foreign

entity . Capitalization of exchange fluctuation arising from foreign

liabilities incurred for acquiring fixed assets does not exist. Translation

adjustments are not included in determining net income for the period

but are disclosed and accumulated in a separate component of

consolidated equity until sale or until complete or substantially complete

liquidation of the net investment in the foreign entity takes place . US

GAAP also permits use of Average monthly Exchange rate for Translation

of Revenue, expenses and Cash flow items, whereas under Indian GAAP,

the closing exchange rate for the Transaction date is to be taken for

translation purposes.

9. Expenditure during Construction Period: As per the Indian GAAP

(Guidance note on ‘Treatment of expenditure during construction

period' ) , all incidental expenditure on Construction of Assets during

Project stage are accumulated and allocated to the cost of asset on

completion of the project. Contrary to this, under the US GAAP (SFAS 7) ,

such expenditure are divided into two heads – direct and indirect.

While, Direct expenditure is accumulated and allocated to the cost of

asset, indirect expenditure are charged to revenue.

10. Research and Development expenditure: Indian GAAP ( AS 8)

requires research and development expenditure to be charged to profit

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 7 4/11/2023

FINANCIAL ACCOUNTS

and loss account, except equipment and machinery which are capitalized

and depreciated. Under US GAAP ( SFAS 2) , all R&D costs are expenses

except intangible assets purchased from others and Tangible assets that

have alternative future uses which are capitalised and depreciated or

amortised as R&D Expense. Under US GAAP, R&D expenditure incurred

on software development are expensed until technical feasibility is

established ( SOP 81.1) . R&D Cost and software development cost

incurred under contractual arrangement are treated as cost of revenue.

11. Revaluation reserve : Under Indian GAAP, if an enterprise needs to

revalue its asset due to increase in cost of replacement and provide

higher charge to provide for such increased cost of replacement, then the

Asset can be revalued upward and the unrealised gain on such

revaluation can be credited to Revaluation Reserve ( Guidance note no

57). The incremental depreciation arising out of higher book value may

be adjusted against the Revaluation Reserve by transfer to P&L Account.

However for window dressing some promoters misutilise this facility to

hoodwink the shareholders on many occasions. US GAAP does not allow

revaluing upward property, plant and equipment or investment.

12. Long term Debts: Under US GAAP , the current portion of long term

debt is classified as current liability, whereas under the Indian GAAP,

there is no such requirement and hence the interest accrued on such

long term debt in not taken as current liability.

13. Extraordinary items, prior period items and changes in accounting

policies: Under Indian GAAP( AS 5) , extraordinary items, prior period

items and changes in accounting policies are disclosed without netting

off for tax effects . Under US GAAP (SFAS 16) adjustments for tax effects

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 8 4/11/2023

FINANCIAL ACCOUNTS

are required to be made while reporting the Prior period Items.

14. Goodwill: Under the Indian GAAP goodwill is capitalized and charged to

earnings over 5 to 10 years period. Under US GAAP ( SFAS 142) , Goodwill and

intangible assets that have indefinite useful lives are not amortized ,but they

are tested at least annually for impairment using a two-step process that begins

with an estimation of the fair value of a reporting unit. The first step is a screen

for potential impairment, and the second step measures the amount of

impairment, if any. However, if certain criteria are met, the requirement to test

goodwill for impairment annually can be satisfied without a remeasurement of

the fair value of a reporting unit.

15. Capital issue expenses: Under the US GAAP, capital issue expenses are

required to be written off when incurred against proceeds of capitals, whereas

under Indian GAAP , capital issue expense can be amortized or written off

against reserves.

16. Proposed dividend: Under Indian GAAP , dividends declared are accounted

for in the year to which they relate. For example, if dividend for the FY 1999-

2000 is declared in Sep 2000 , then the corresponding charge is made in 2000-

2001 as below the line item . Contrary to this , under US GAAP dividends are

reduced from the reserves in the year they are declared by the Board. Hence in

this case under US GAAP , it will be charged Profit and loss account of 2000-

2001 above the line.

17. Investments in Associated companies: Under the Indian GAAP( AS 23) ,

investment in associate companies is initially recorded at Cost using the Equity

method whereby the investment is initially recorded at cost, identifying any

goodwill/capital reserve arising at the time of acquisition. The carrying amount

of the investment is adjusted thereafter for the post acquisition change in the

investor’s share of net assets of the investee. The consolidated statement of

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 9 4/11/2023

FINANCIAL ACCOUNTS

profit and loss reflects the investor’s share of the results of operations of the

investee.are carried at cost . Under US GAAP ( SFAS 115) Investments in

Associates are accounted under equity method in Group accounts but would be

held at cost in the Investor’s own account.

18. Preoperative expenses: Under Indian GAAP, (Guidance Note 34 - Treatment

of Expenditure during Construction Period), direct Revenue expenditure during

construction period like Preliminary Expenses, Project related expenditure are

allowed to be Capitalised. Further , Indirect revenue expenditure incidental and

related to Construction are also permitted to be capitalised. Other Indirect

revenue expenditure not related to construction, but since they are incurred

during Construction period are treated as deferred revenue expenditure and

classified as Miscellaneous Expenditure in Balance Sheet and written off over a

period of 3 to 5 years. Under US GAAP ( SFAS 7) , the concept of preoperative

expenses itself doesn’t exist. SOP 98.5 also madates that all Start up Costs should

be expensed. The enterprise has to prepare its balance sheet and Profit and Loss

Account as if it were a normal running organization. Expenses have to be

charged to revenue and Assets are Capitalised as a normal organization. The

additional disclosure include reporting of cash flow, cumulative revenues and

Expenses since inception. Upon commencement of normal operations, notes to

Statement should disclose that the Company was but is no longer is a

Development stage enterprise. Thus , due to above accounting anomaly,

Accounts prepared under Indian GAAP , contain higher charges to depreciation

which are to be adjusted suitably under US GAAP adjustments for indirect

preoperative expenses and foreign currencies.

19. Employee benefits: Under Indian GAAP, provision for leave encashment is

accounted based n actuarial valuation. Compensation to employees who opt for

voluntary retirement scheme can be amortized over 60 months. Under US

GAAP, provision for leave encashment is accounted on actual basis.

Compensation towards voluntary retirement scheme is to be charged in the year

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 10 4/11/2023

FINANCIAL ACCOUNTS

in which the employees accept the offer.

20. Loss on extinguishment of debt: Under Indian GAAP, debt extinguishment

premiums are adjusted against Securities Premium Account. Under US GAAP,

premiums for early extinguishment of debt are expensed as incurred.

2.B. What is Matching Principle? Why should a business concern follow this principle?

Ans. The Matching principle is a culmination of accrual accounting and the revenue

recognition principle. They both determine the accounting period, in which revenues and

expenses are recognized. According to the principle, expenses are recognized when

obligations are (1) incurred (usually when goods are transferred or services rendered, e.g.

sold), and (2) offset against recognized revenues, which were generated from those expenses

(related on the cause-and-effect basis), no matter when cash is paid out. In cash accounting—

in contrast—expenses are recognized when cash is paid out, no matter when obligations are

incurred through transfer of goods or rendition of services: e.g., sale.

If no cause-and-effect relationship exists (e.g., a sale is impossible), costs are recognized as

expenses in the accounting period they expired: i.e., when have been used up or consumed

(e.g., of spoiled, dated, or substandard goods, or not demanded services). Prepaid expenses are

not recognized as expenses, but as assets until one of the qualifying conditions is met resulting

in a recognition as expenses. Lastly, if no connection with revenues can be established, costs

are recognized immediately as expenses (e.g., general administrative and research and

development costs).

Prepaid expenses, such as employee wages or subcontractor fees paid out or promised, are

not recognized as expenses (cost of goods sold), but as assets (deferred expenses), until the

actual products are sold.

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 11 4/11/2023

FINANCIAL ACCOUNTS

The matching principle allows better evaluation of actual profitability and performance

(shows how much was spent to earn revenue), and reduces noise from timing mismatch

between when costs are incurred and when revenue is realized.

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 12 4/11/2023

FINANCIAL ACCOUNTS

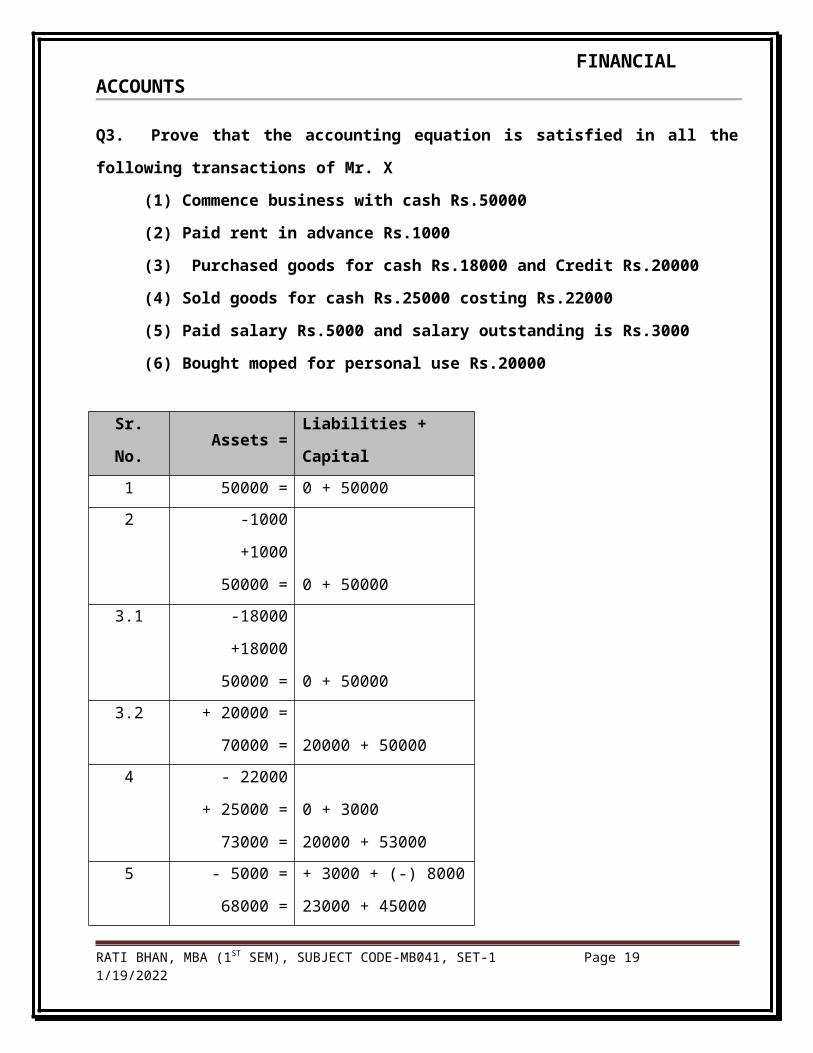

Q3. Prove that the accounting equation is satisfied in all the following transactions of

Mr. X

(1) Commence business with cash Rs.50000

(2) Paid rent in advance Rs.1000

(3) Purchased goods for cash Rs.18000 and Credit Rs.20000

(4) Sold goods for cash Rs.25000 costing Rs.22000

(5) Paid salary Rs.5000 and salary outstanding is Rs.3000

(6) Bought moped for personal use Rs.20000

Sr. No. Assets = Liabilities + Capital

1 50000 = 0 + 50000

2 -1000

+1000

50000 = 0 + 50000

3.1 -18000

+18000

50000 = 0 + 50000

3.2 + 20000 =

70000 = 20000 + 50000

4 - 22000

+ 25000 =

73000 =

0 + 3000

20000 + 53000

5 - 5000 =

68000 =

+ 3000 + (-) 8000

23000 + 45000

6 - 20000 =

48000 =

0 + (-) 20000

23000 + 25000

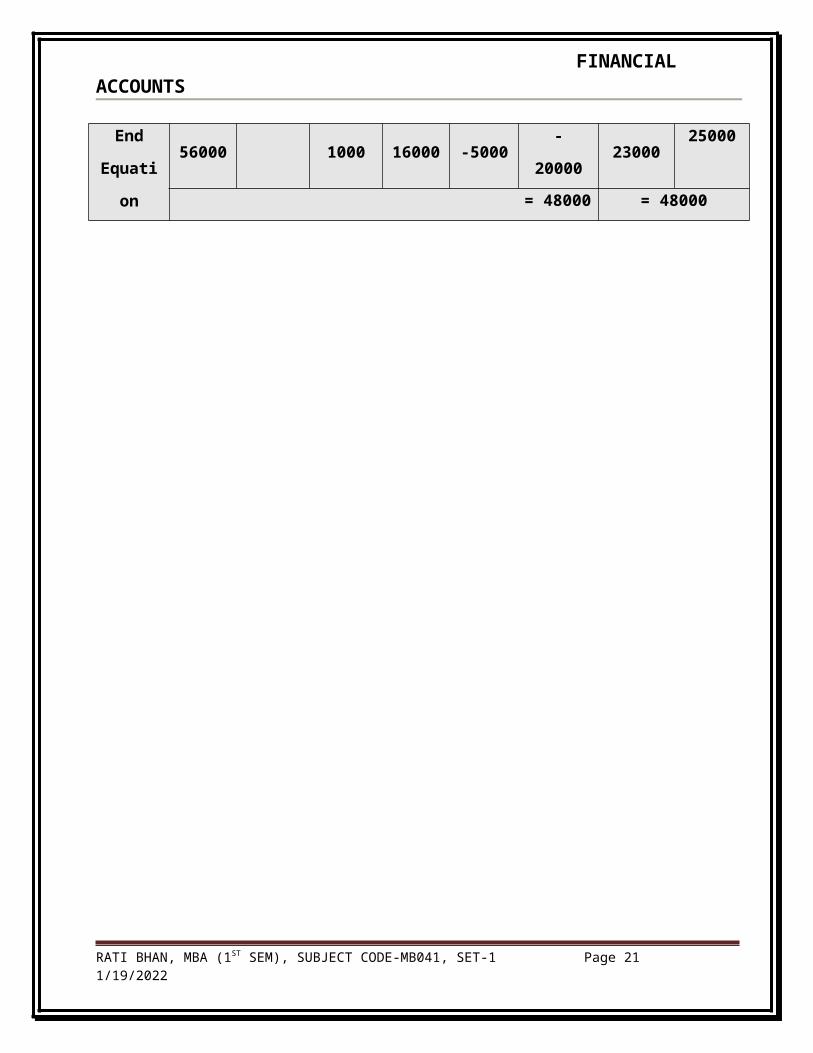

End

Equation48000 = 48000

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 13 4/11/2023

FINANCIAL ACCOUNTS

Sr.No.Asset =

Liabilities +

Capital

Cash Debtors Rent Goods Salary Personal Creditor Capital

1 50000 50000

2 -1000 +1000

3.1 -18000 +18000

3.2 20000 20000

4 +25000 -22000 +3000

5 -5000 3000 -8000

6 - 20000 -20000

End

Equation

56000 1000 16000 -5000 - 20000 23000 25000

= 48000 = 48000

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 14 4/11/2023

FINANCIAL ACCOUNTS

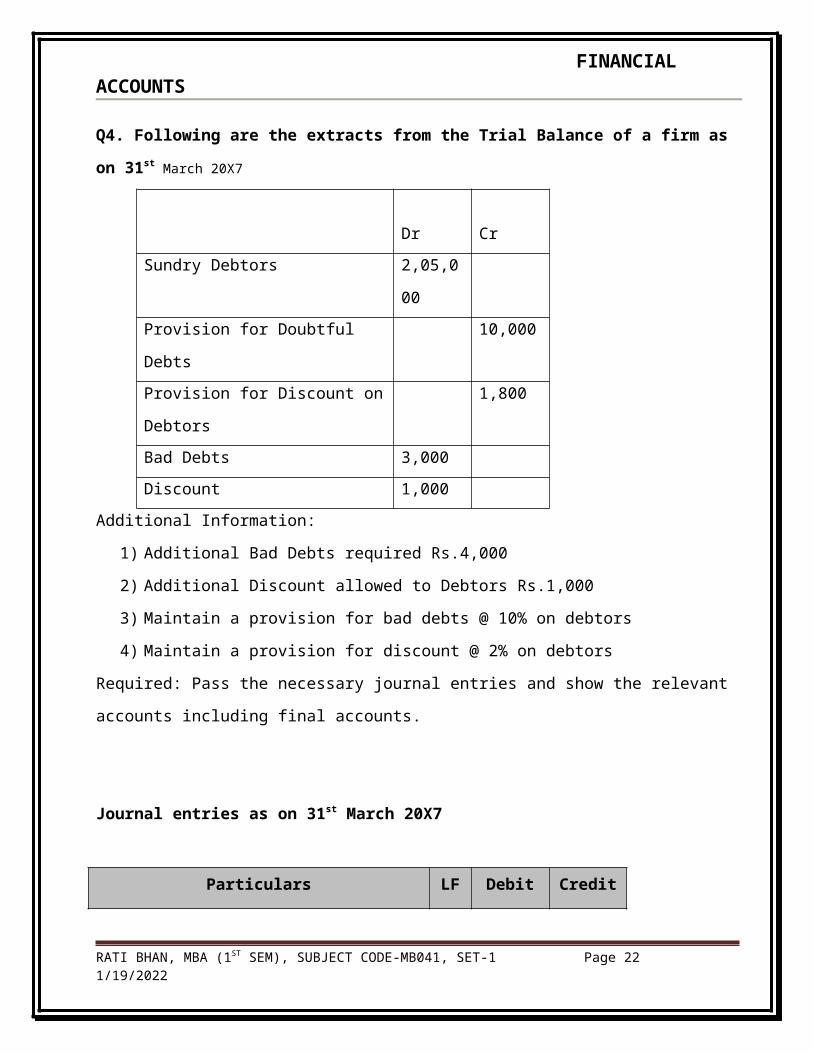

Q4. Following are the extracts from the Trial Balance of a firm as on 31st March 20X7

Dr Cr

Sundry Debtors 2,05,000

Provision for Doubtful Debts 10,000

Provision for Discount on Debtors 1,800

Bad Debts 3,000

Discount 1,000

Additional Information:

1) Additional Bad Debts required Rs.4,000

2) Additional Discount allowed to Debtors Rs.1,000

3) Maintain a provision for bad debts @ 10% on debtors

4) Maintain a provision for discount @ 2% on debtors

Required: Pass the necessary journal entries and show the relevant accounts including final

accounts.

Journal entries as on 31st March 20X7

Particulars LF Debit

(Rs.)

Credit

(Rs.)

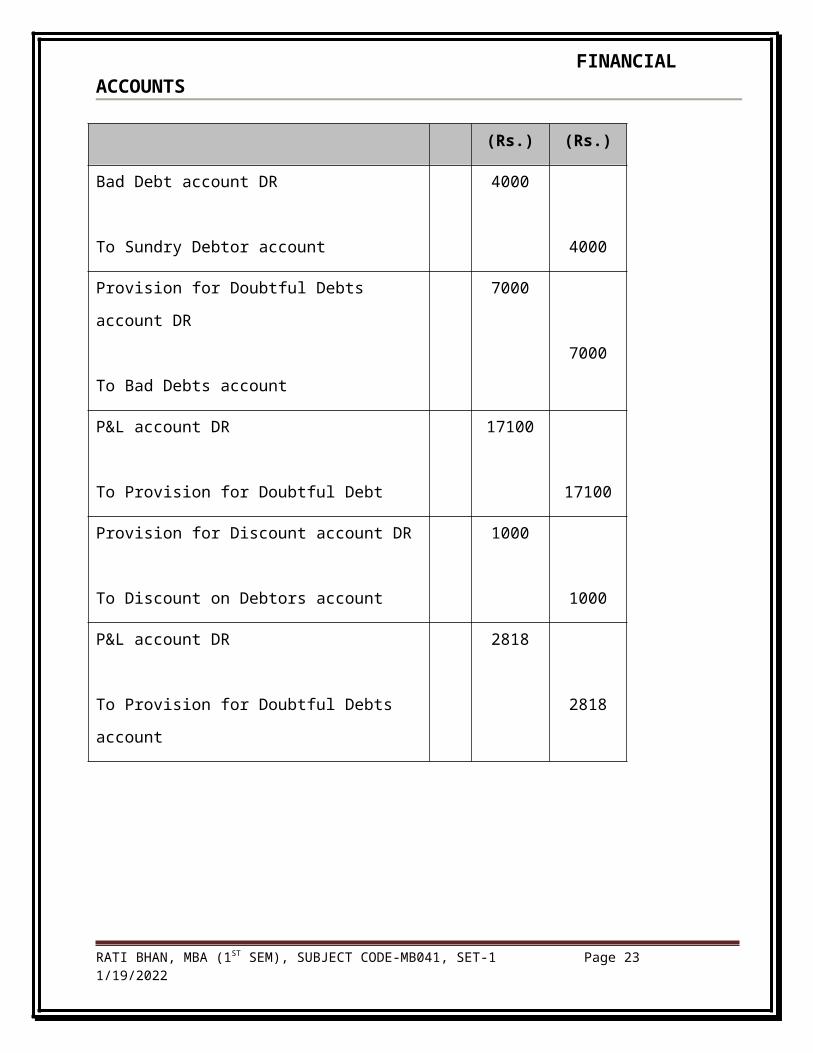

Bad Debt account DR

To Sundry Debtor account

4000

4000

Provision for Doubtful Debts account DR

To Bad Debts account

7000

7000

P&L account DR

To Provision for Doubtful Debt

17100

17100

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 15 4/11/2023

FINANCIAL ACCOUNTS

Provision for Discount account DR

To Discount on Debtors account

1000

1000

P&L account DR

To Provision for Doubtful Debts account

2818

2818

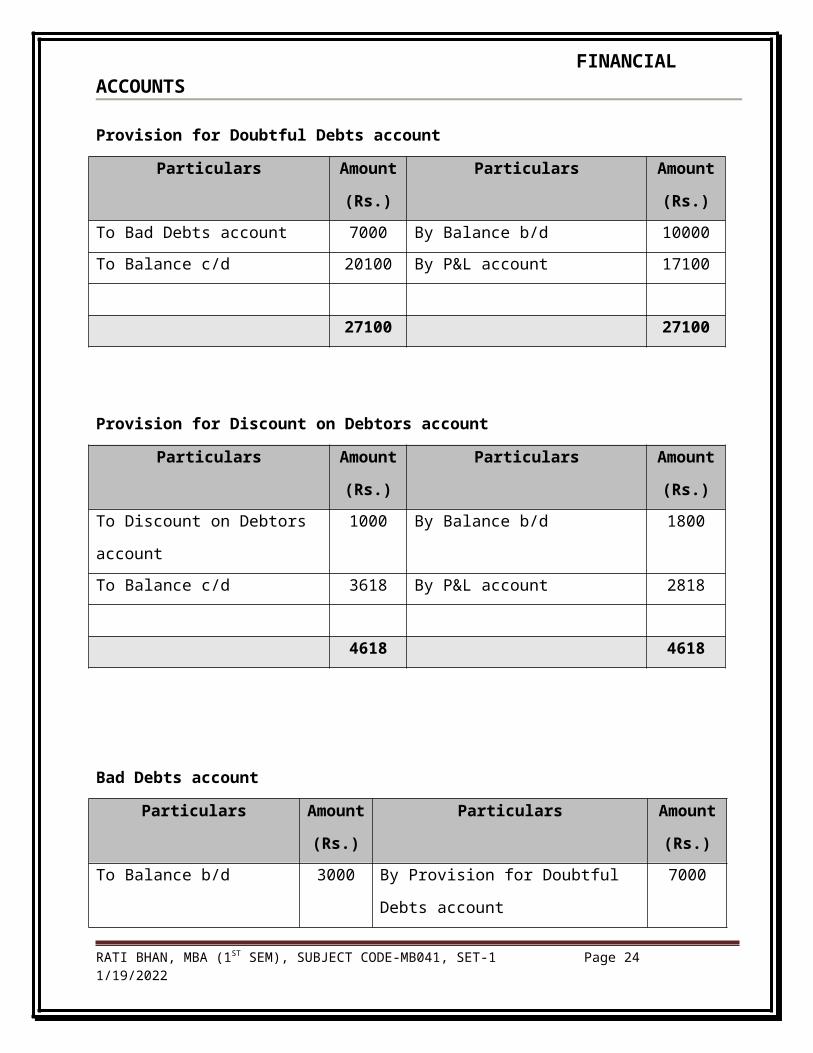

Provision for Doubtful Debts account

Particulars Amount

(Rs.)

Particulars Amount

(Rs.)

To Bad Debts account 7000 By Balance b/d 10000

To Balance c/d 20100 By P&L account 17100

27100 27100

Provision for Discount on Debtors account

Particulars Amount

(Rs.)

Particulars Amount

(Rs.)

To Discount on Debtors account 1000 By Balance b/d 1800

To Balance c/d 3618 By P&L account 2818

4618 4618

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 16 4/11/2023

FINANCIAL ACCOUNTS

Bad Debts account

Particulars Amount

(Rs.)

Particulars Amount

(Rs.)

To Balance b/d 3000 By Provision for Doubtful Debts

account

7000

To Sundry debtors 4000

7000 7000

Calculation of Provision required

Debtors as per Trial Balance 205000

Less additional Bad Debt - 4000

201000

10% on 201000 20100

Opening balance in Provision account 10000

Less Bad Debts w/o - 7000

3000

Provision needed 20100

Therefore Provision required to be made 20100 – 3000 = 17100

Calculation of Provision for Discount

Debtors as per Trial Balance 205000

Less additional Bad Debts - 4000

201000

Less additional Provision- 20100

180900

2% of 180900 3618

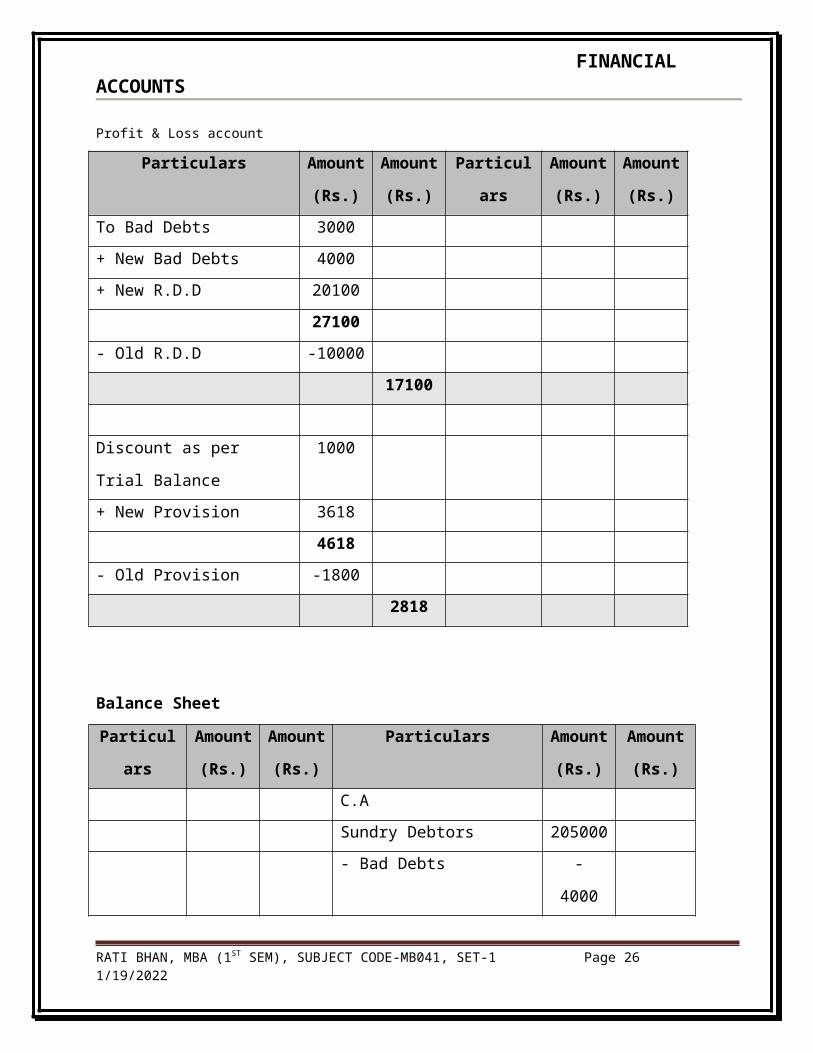

Profit & Loss account

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 17 4/11/2023

FINANCIAL ACCOUNTS

Particulars Amount

(Rs.)

Amount

(Rs.)

Particulars Amount

(Rs.)

Amount

(Rs.)

To Bad Debts 3000

+ New Bad Debts 4000

+ New R.D.D 20100

27100

- Old R.D.D -10000

17100

Discount as per Trial

Balance

1000

+ New Provision 3618

4618

- Old Provision -1800

2818

Balance Sheet

Particulars Amount

(Rs.)

Amount

(Rs.)

Particulars Amount

(Rs.)

Amount

(Rs.)

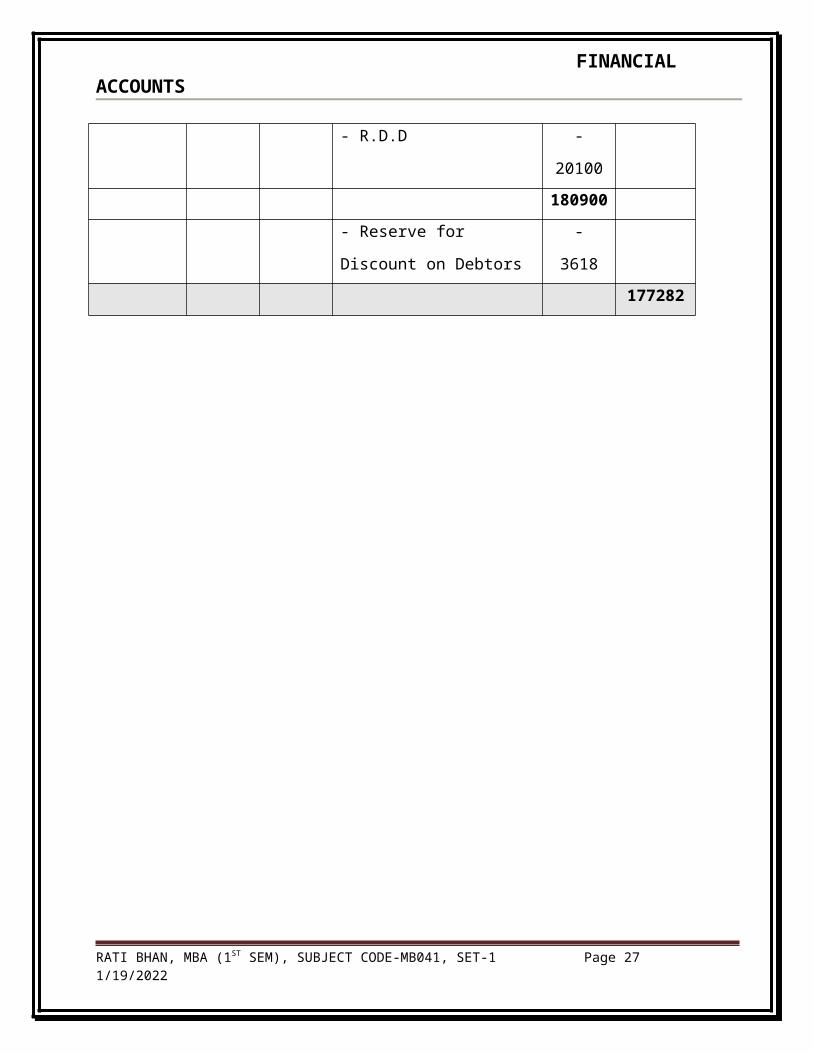

C.A

Sundry Debtors 205000

- Bad Debts - 4000

- R.D.D - 20100

180900

- Reserve for Discount on

Debtors

- 3618

177282

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 18 4/11/2023

FINANCIAL ACCOUNTS

Q.5. A. Bring out the difference between trade discount and cash discount.

Cash

DiscountTrade Discount

Is a reduction granted by

supplier from the invoice price in

consideration of immediate or

prompt payment

Is a reduction granted by supplier from the list

price of goods or services on business

consideration re: buying in bulk for goods and

longer period when in terms of services

As an incentive in credit

management

to encourage prompt payment

Allowed to promote the sales

Not shown in the supplier bill or

invoiceShown by way of deduction in the invoice itself

Cash discount account is opened

in the ledger

Trade discount account is not opened in the

ledger

Allowed on payment of money Allowed on purchase of goods

It may vary with the time period

within which payment is

received

It may vary with the quantity of goods

purchased or amount of purchases made

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 19 4/11/2023

FINANCIAL ACCOUNTS

Q5.B. Explain the term (1) asset (2) liability with the help of examples.

Ans. In financial accounting, assets are economic resources. Anything tangible or intangible

that is capable of being owned or controlled to produce value and that is held to have positive

economic value is considered an asset. Simplistically stated, assets represent ownership of

value that can be converted into cash (although cash itself is also considered an asset).[1] The

balance sheet of a firm records the monetary value of the assets owned by the firm. It is money

and other valuables belonging to an individual or business. Two major asset classes are

tangible assets and intangible assets. Tangible assets contain various subclasses, including

current assets and fixed assets.[4] Current assets include inventory, while fixed assets include

such items as buildings and equipment.[5] Intangible assets are nonphysical resources and

rights that have a value to the firm because they give the firm some kind of advantage in the

market place. Examples of intangible assets are goodwill, copyrights, trademarks, patents and

computer programs,[5] and financial assets, including such items as accounts receivable, bonds

and stocks.

In financial accounting, a liability is defined as an obligation of an entity arising from past

transactions or events, the settlement of which may result in the transfer or use of assets,

provision of services or other yielding of economic benefits in the future.

All type of borrowing from persons or banks for improving a business or person

income which is payable during short or long time.

They embody a duty or responsibility to others that entails settlement by future

transfer or use of assets, provision of services or other yielding of economic benefits, at

a specified or determinable date, on occurrence of a specified event, or on demand;

The duty or responsibility obligates the entity leaving it little or no discretion to avoid

it; and,

The transaction or event obligating the entity has already occurred.

Liabilities in financial accounting need not be legally enforceable; but can be based on

equitable obligations or constructive obligations. An equitable obligation is a duty based on

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 20 4/11/2023

FINANCIAL ACCOUNTS

ethical or moral considerations. A constructive obligation is an obligation that can be inferred

from a set of facts in a particular situation as opposed to a contractually based obligation.

The accounting equation relates assets, liabilities, and owner's equity:

Assets = Liabilities + Owner's Equity

Probably the most accepted accounting definition of liability is the one used by the International Accounting Standards Board (IASB). The following is a quotation from IFRS Framework:

A liability is a present obligation of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits

Regulations as to the recognition of liabilities are different all over the world, but are roughly similar to those of the IASB.

Examples of types of liabilities include: money owing on a loan, money owing on a mortgage, or an IOU.

Liabilities are debts and obligations of the business they represent creditors claim on business assets. Example of Liabilities All kinds of payable 1) Notes payable - an written promise. 2) Accounts Payable - an oral promise. 3) Interests Payable. 4) Sales Payable

Classification of accounting liabilities

Liabilities are reported on a balance sheet and are usually divided into two categories:

Current liabilities — these liabilities are reasonably expected to be liquidated within a year. They usually include payables such as wages, accounts, taxes, and accounts payables, unearned revenue when adjusting entries, portions of long-term bonds to be paid this year, short-term obligations (e.g. from purchase of equipment), and others.

Long-term liabilities — these liabilities are reasonably expected not to be liquidated within a year. They usually include issued long-term bonds, notes payables, long-term leases, pension obligations, and long-term product warranties.

Bank account example

Money deposited with a bank becomes a liability of the bank, because the bank has an obligation to pay the depositor the money deposited; usually on demand. The money

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 21 4/11/2023

FINANCIAL ACCOUNTS

deposited is an asset for the depositor; but this asset will not be recorded by the bank because it is not the bank's asset.

A debit increases an asset; and a credit decreases an asset. A debit decreases a liability; and credit increases a liability.

When a bank receives a deposit it credits a liability account called "deposits" and credits the depositor's bank account for the same amount (the bank's "deposits" account is the sum of all of the amounts credited to all of its customer's individual bank accounts). A deposit received by a bank is credited because the bank's liability to its customer, the depositor, increases. When a bank informs its depositor that it has debited the depositor's bank account, it means that the depositor's bank account has been decreased by the amount debited.

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 22 4/11/2023

FINANCIAL ACCOUNTS

6. A fresh MBA student joined as trainee was asked to prepare Trial balance. He was

unable to submit a correct trial balance. You, as a senior accountant find out the errors

and rectify them. After redrafting the trial balance prepare trading and Profit and loss

account.

Particulars Debit Credit

Capital 7,670

Cash in Hand 30

Purchases 8,990

Sales 11,060

Cash at bank 885

Fixtures and Fittings 225

Freehold premises 1,500

Lighting and Heating 65

Bills Receivable 825

Return Inwards 30

Salaries 1,075

Creditors 1890

Debtors 5,700

Stock at 1st April 2007 3,000

Printing 225

Bills Payable 1,875

Rates, taxes and insurance 190

Discount received 445

Discount allowed 200

21,175 21,705

Adjustments:

1) Stock on hand on 31st March 2008 was valued at Rs.1800

2) Depreciate fixtures and fittings by Rs.25

3) Rs.35 was due and unpaid in respect of salaries

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 23 4/11/2023

FINANCIAL ACCOUNTS

4) Rates and insurance had been paid in advance to the extent of Rs.40

Trading Account for the year ended 31-03-2008

ParticularsAmount

(Rs.)

Amount

(Rs.)Particulars

Amount

(Rs.)

Amount

(Rs.)

To Opening stock 3000 By Sales 11060

To Purchase 8990 Less Sales Returns 30 11030

To G/P closed 840 By closing stock 1800

12830 12830

P&L Account for the year ended 31-03-2008

ParticularsAmount

(Rs.)

Amount

(Rs.)Particulars

Amount

(Rs.)

Amount

(Rs.)

To Lighting and heating 65 By G/P balanced 840

To Salaries 1075 By Discount received 445

Add outstanding 35 By N/L closed 490

To Printing 225

To Rates taxes &

insurance 190 1775

- Less prepaid - 40

To Discount Allowed 200

To depreciation fixture &

fittings 25

1775

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 24 4/11/2023

FINANCIAL ACCOUNTS

Balance Sheet as on 31-03-2008

ParticularsAmount

(Rs.)

Amount

(Rs.)Particulars

Amount

(Rs.)

Amount

(Rs.)

Capital 7670 Freehold premises 1500

- Less Net Loss - 490 7180 Fixtures & Fittings 225

- Less Depreciation -25 200

Creditor 1890 1700

Bills Payable 1875

Outstanding salaries 35 Stock 1800

Debtors 5700

Bills Receivable 825

Cash at Bank 885

Cash in hand 30

Prepaid Rates 40

10980 10980

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 25 4/11/2023

FINANCIAL ACCOUNTS

Redrafted Trial Balance

Particulars Debit Credit

Capital 7,670

Cash in Hand 30

Purchases 8,990

Sales 11,060

Cash at bank 885

Fixtures and Fittings 225

Freehold premises 1.500

Lighting and Heating 65

Bills Receivable 825

Return Inwards 30

Salaries 1.075

Creditors 1890

Debtors 5,700

Stock at 1st April 2007 3,000

Printing 225

Bills Payable 1875

Rates, taxes and insurance 190

Discount received 445

Discount allowed 200

22940 22940

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 26 4/11/2023

FINANCIAL ACCOUNTS

RATI BHAN, MBA (1ST SEM), SUBJECT CODE-MB041, SET-1 Page 27 4/11/2023